Credit contagion and credit risk

Abstract

We study a simple, solvable model that allows us to investigate effects of credit contagion on the default probability of individual firms, in both portfolios of firms and on an economy wide scale. While the effect of interactions may be small in typical (most probable) scenarios they are magnified, due to feedback, by situations of economic stress, which in turn leads to fatter tails in loss distributions of large loan portfolios.

pacs:

02.50.-r, 05.40.-a, 89.65.Gh, 89.75.Da1 Introduction

Modelling credit risk in a coherent yet applicable manner is an important yet challenging problem. The difficulties arise from the combination of a large, and co-dependent set of risk parameters such as default rates, recovery rates, or exposures, which are correlated and non-stationary in time. An additional issue is that of credit contagion [1, 2, 4], which examines the role of counter-party risk in credit risk modelling. If a firm is in economic distress, or defaults, this will implications for any firm which is economically influenced by this given firm, for example, a service provider to it, purchaser of its goods or a bank with a credit line to the firm. The direct correlations between firms caused by credit contagion lead to further complications in modelling the overall, either portfolio or economy wide, level of risk. Jarrow and Yu [1] introduced a framework of primary and secondary firms, the former would default depending on some background stochastic process while the latter were affected by a stochastic process and the performance of the primary firms. They argued that this was a reasonable level of detail for their purposes and it also simplifies matters as there are no feedback loops in the system. Secondary firms depend only on primary firms whose performance is independent of the secondary firms. Another approach for modelling credit contagion dynamics was provided by Giesecke and Weber [2] who used the well known voter process [3], from the theory of interacting particle systems, to model interactions between firms. They assumed a regular structure for their firms (a regular hyper-cubic lattice) and focussed on the equilibrium properties of their model. Davis and Lo [4] considered a model in which defaults occur either directly, or through infection by another defaulted firm, with probabilities for direct default or infection taken uniform throughout the system. Defaults occurring due to both, endogenous or exogenous causes were not considered in their set-up.

There are a variety of techniques for modelling the correlations between firms’ default behaviour, which is a major complication in credit risk modelling. The binomial expansion technique assumes independence between firms so that the number of defaults in a portfolio is described by a binomial distribution. In order to capture the effects of correlations a binomial distribution with an “effective” number of firms is assumed which is smaller than the actual number in the portfolio, but the weight given to each firm scaled so as to keep the mean number of defaults constant, while the variance of the overall number of defaults is increased. The relationship between the true number of firms and the effective reduced number is a modelling choice that depends on the diversity of the firms in terms of sectors, geographic locations or any other identifiable trait that would lead to strong correlations in default behaviour. JP Morgans’ CreditMetrics approach [5] and Credit Suisse First Financial Products CreditRisk+ [6] (see [7] for a detailed comparison between the two) uses the correlations in equity values as a surrogate for the correlations in credit quality. The structural modelling approach goes back a long way to work by Merton [8] which directly models the dynamics of a firm’s assets, with default being triggered by the asset value hitting some predetermined value (which henceforth we take without loss of generality to be zero). Correlations between firms are due to correlations in the dynamics of different firms’ assets. This approach is very general, as it is relatively transparent to identify different driving forces of asset levels and straightforward to include them in the model (though the resulting model itself will be non-trivial). However, it suffers from the fact that the asset level is not an observable quantity [9]. On the other hand, the reduced form approach gives default rates for a given firm without modelling the underlying default process. Correlations are then directly introduced between the default rates. There was some discussion in the literature about whether the reduced form model could describe the true level of default correlations seen empirically but Yu [10] seems to have answered this question in the affirmative if a suitable structure between the default rates is taken into account.

The approach we take here is a discrete time Markov process (at the microeconomic level) where the probability of a default of a given firm in a particular time step depends materially on the state of its economic partners at the start of that time step, as well as on macro-economic influences. Using techniques developed in the statistical mechanics of disordered systems, and recently applied to this specific model in [11], we are able to solve our model exactly, and given our assumptions that we describe shortly, this solution takes a particularly simple form despite the fact that in principle we have feedback correlations, non-equilibrium dynamics and in principle non-Markovian behaviour at the macroscopic (economy/portfolio wide) level. We note that it is possible to frame our model in either the structural approach or the reduced form approach, depending on requirements and taste, although the interpretation of the variables in the two approaches will of course be different. We find that the correlations introduced through credit contagion lead to large increases in default rates in times of economic stress, above and beyond those introduced by simple macro-economic dependencies. This has strong implications for portfolio risk management.

2 The microeconomic framework

We will analyse an economy of firms in the large limit. Generally, we focus on the characteristic changes in the economy due to interactions between firms, which will be described in a probabilistic manner.

As mentioned in the introduction we take a discrete time approach. For clarity we restrict our discussion to a one year time frame split into twelve steps; this is not essential, but parameters may need rescaling depending on the set-up. We use a binary indicator variable to denote whether firm is solvent at time () or has defaulted (). The default process is a function of an underlying stochastic process for each firm in terms of a “wealth” variable , where we assume default if the wealth drops below zero. We shall assume that recovery from default over the time horizon of a year is not possible, so that the defaulted state is absorbing. As a function of the wealth, therefore, the indicator variables evolve according to

| (1) |

where is the Heavyside function.

A dynamic model for the indicator variables is obtained from (1) by specifying the underlying stochastic process for the wealth variables . We shall take it to be of the form

| (2) |

Here denotes an initial wealth of firm at the beginning of the risk horizon, and quantifies the material impact on the wealth of firm that would be caused by a default of firm . This may or may not be a reduction in wealth, depending on whether has a cooperative () or a competitive () economic relation with .

We shall assume that the fluctuating contributions to (2) are zero-mean Gaussians. There is still some degree of flexibility concerning the decomposition of the into contributions that are intrinsic to the firm and extrinsic contributions. The latter describe the influence of economy-wide fluctuations or fluctuations pertaining to different economic sectors, depending on the level of detail required. We restrict ourselves to a minimal model containing a single macro-economic factor (assumed to be constant over a risk horizon of a year), and individual fluctuations for each firm,

| (3) |

where sets the scale of the individual fluctuations, and the are taken to be independent Gaussians; finally, the parameters quantify the correlations of the created via the coupling to economy-wide fluctuations , also taken to be .

Up to this point the wealth dynamics does not contain an endogenous drift. If predictions are required over longer time periods then it may also be pertinent to introduce such a drift, e.g. by using a time-dependent for example, , where denotes an intrinsic growth rate of the average wealth of firm (with for a firm making profits and for a firm making losses). However, for the current purposes of examining default rates over the medium term and especially focussing on the behaviour on the tails, this adjustment does not lead to significant changes in our overall conclusion.

The model, as formulated above, clearly takes a structural point of view on the problem of credit contagion. However, we note that the dynamics (1) of the indicator variables is clearly independent of the scale of the wealth variables . By appropriately rescaling the initial wealths and the impact parameters we can thus assume a unit-scale for the noise variables (3). Interestingly, this simple rescaling, which leaves the dynamics of the system unaffected, amounts to changing to a reduced-form interpretation of the dynamics.

To see this, note from (2) that the event is equivalent to . With , we see that this occurs with probability where is the cumulative normal distribution. From a reduced form point of view this is just the intensity of default of firm at time step (in a given economic environment specified by the set of firms defaulted at time ). This allows us to re-interpret the (rescaled) initial wealth and impact variables and in terms of the bare default probabilities [11, 12, 13]. I.e., if company has an expected default probability of in a given time unit (e.g. one month in the present set-up) as predicted from tables from ratings agencies, then . Similarly, the expected default probability of firm , given that only firm has defaulted leads to the value .

In determining the model parameters by the method suggested above we are splitting our default probability into terms that come from credit contagion and other terms such as the bare default probability that come from historical data. It could fairly be argued that the historical data already incorporate the credit contagion terms and thus we are double counting. As we will see later in numerical simulations, the credit contagion terms make very little difference to average behaviour and thus making estimates based on average historical data is still a reasonable approach.

In choosing the variable we follow the prescription given by BASEL II [14] which sets

| (4) |

where gives the probability of default of firm over one year, ignoring credit contagion effects. With as the monthly default probability, we have .

We still have to specify the form for the economic interactions. We adopt here a probabilistic approach, so take them to be random quantities of the form

| (5) |

Here, the detail the network (presence or absence) of interactions between different firms and we choose these to be randomly fixed according to

| (6) |

We assume that the average connectivity of each firm is large in the limit of a large economy; this will allow the influence of partner firms to be described by the central limit theorem and the law of large numbers. Concerning the values of the (non-zero) impact parameters, we parametrise them as shown, with assumed to be zero-mean, unit-variance random variables, with finite moments, and independent in pairs,

| (7) |

The parameters and determine mean and variance of the interaction strengths; the scaling of mean and variance with and respectively in (5) is necessary to allow a meaningful large limit to be taken. Taking would encode the fact that on average firms have a synergy with their economic partners.

At first sight, specifying the appears to introduce a vast number of parameters into our model, but in fact only the first two moments of the distribution of interaction strengths are sufficient to determine the macroscopic behaviour of the system, and so the model space is not too large.

Let us now turn to the capital required to be held against credit risk. In the BASEL II document [14] the capital requirement for a unit-size loan given to firm is

| (8) |

The first factor, the loss given default of firm , is related to the average fraction of a loan that can be recovered despite default. The last factor, , is related to the maturity (long dated loans are inherently riskier). Adjustments related to liquidity (low liquidity loans are risker) and concentration (fewer, larger loans give a greater variance in returns for given expected return) are occasionally also included in this factor — concentration-adjustments, in fact, are a means to account for reduced granularity in a credit portfolio resulting from the possibility of credit contagion.

The factor inside square brackets in (8) is entirely related to the loss-frequency distribution. The first term is the value of the loss frequency not exceeded with probability under fluctuating macro-economic conditions, with describing the dependence of the firm’s loss-frequency on the macro-economic factor. The second term is the average loss frequency. The value of the confidence level is in principle arbitrary, but is related to the target rating of the bank. The risk weighted asset is then found by further multiplying by terms such as the exposure at default (i.e. size of the loan). Thus the capital required for firm can be viewed as the loss at the 99.9th percentile level of stress, in excess of the expected loss, multiplied by a conversion factor. From this structure it is clear that a key ingredient for the capital adequacy requirements is a good model of credit risk that works well into the tail of the loss frequency distribution.

Returning to our description of default dynamics, let us first focus on the case of independent firms, with , and consider a single epoch for our model with fluctuating forces given by (3) at given macro-economic condition . The probability of a default of firm with average unconditional monthly default probability occurring during the epoch in our model is given by

| (9) |

Since the probability of default is increasing with , we can find the probability of default not exceeded at e.g. the 99.9 percent confidence level; it is given by setting in the above equation (recall is distributed as a zero-mean, unit-variance Gaussian random number). As above, the excess capital required is the loss at the 99.9th percent level minus the expected loss (multiplied by a risk factor). However, when we consider the case of an interacting economy with non-zero , we find that in fact

| (10) |

where

| (11) |

is the fraction of firms within the economy that have defaulted up to time ; we also expressed the expected monthly default rate in terms of a ‘rescaled initial wealth’ , .

Thus we find that our formulation is very similar to that used in BASEL II. However, we directly take account of the correlations in defaults caused by credit contagion. This introduces two extra parameters into the model but it does markedly change the behaviour in the tails of the loss frequency distribution, and thereby in the tails of the loss distribution itself. Correlation between firms is essentially a dynamic phenomenon — if there is no dynamics, there is no way for one’s firms’ performance to influence the viability of any other firm. Thus rather than considering firms to be independent over a single epoch which lasts the entire period of any loan, we split the overall time (e.g. one year) into smaller units (e.g. one month) and let the firms evolve over these smaller time units with the default probability adjusted (since the default event in 12 monthly epochs is compounded 12 times as opposed to a single epoch). A firm may default at any point, but will then influence its partner firms for the remainder of the time horizon. The complexity of the theory is merely linear in time, thus it is not a great computational burden to choose this approach.

Following the approach described in [11] it is possible to solve the model in a stochastic manner. Credit contagion within this model is encoded at each time by a single number, the fraction of firms that have defaulted thus far, which evolves according to

| (12) |

where denotes the time-dependent monthly default rate of firms with , as influenced by interactions with the economy (see Eq (16) of [11]), and the larger angled brackets with subscript denote an average over the bare monthly probabilities of default for the ensemble of firms, or equivalently over the distribution of their rescaled initial wealth parameters . In (12) the Basel II recommendation which links correlations to macro-economic factors with (unconditional) default probabilities, , via (4) is formally taken into account.

Note that credit contagion affects the dynamics of defaults only via two parameters, and , which characterise the mean and variance of the impact parameter distribution. Note also that the parameter which quantifies forward-backward correlation of mutual impacts according to (7) does not appear in the final formulation, nor are there any memory-effects in the dynamics, as would normally be expected for systems of this type. The reason for this simplifying feature is in the fact that the defaulted state is taken to be absorbing over the risk horizon of one year.

3 Results

We now turn to presenting a few key results of our analysis. Our results concerning default dynamics and loss distributions are obtained for an economy in which the parameters determining unconditional monthly default probabilities according to , are normally distributed with mean , and variance so that typical monthly bare default probabilities are in the range. The couplings to the macro-economic factor are chosen to depend on the expected default probabilities according to the Basel II prescription (4).

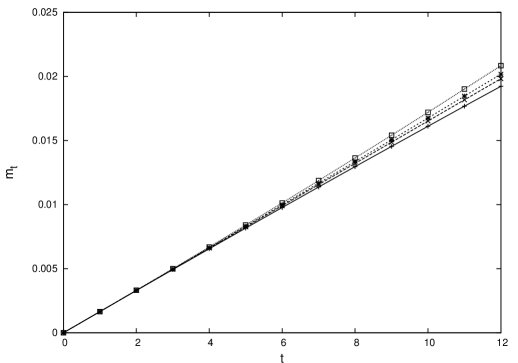

In Fig. 1 we we show that renormalisation (with respect to credit contagion) makes little difference to the typical default dynamics. The evolution of the fraction of defaulted firms in interacting economies differs hardly from that of the non-interacting economy with .

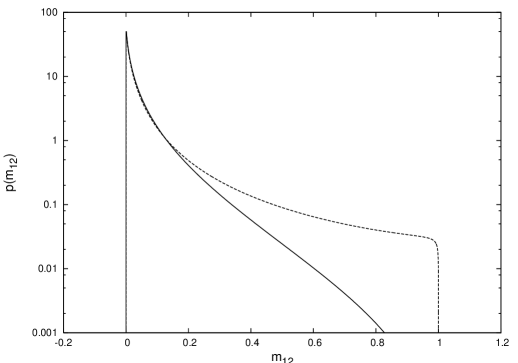

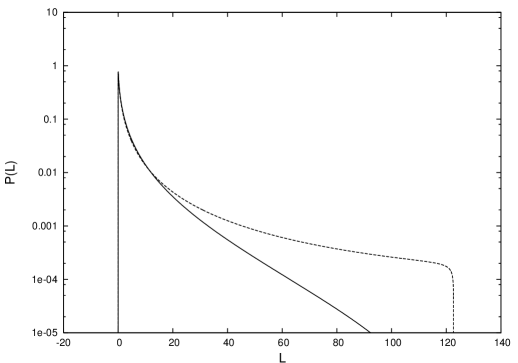

In marked contrast to this, the tails of loss-frequency and loss distributions are strongly affected by the presence of interactions in the system, as shown in Figs. 2 and 3. We note that the tails of the loss-frequency distribution and the loss distribution are more pronounced than in our previous study [11]. This solely due to the fact that in the present paper we followed the Basel II suggestion that relates the coupling of a company to macro-economic factors with its default probability via (4).

In computing the economy-wide losses per node for given macro-economic condition ,

| (13) |

we assume that the are randomly sampled from the loss distribution for node , taken to be independent of the stochastic evolution, but correlated with the bare monthly default probability. In the large limit this gives

| (14) |

by the law of large numbers, where is the mean of the loss distribution for a node with default probability . As an example we consider an economy where average losses are inversely proportional to the unconditional default probabilities ,

| (15) |

with a parameter preventing divergence as . In this way, the contribution to the total losses will be approximately uniform over the bands of different default probabilities. The distribution of the economy-wide losses per node is driven by the distribution of the macro-economic factor, and is computed analytically as shown in [11]. A typical result is shown in Fig. 3, for which we chose the scale and the regularizer . Once more economic interactions are seen to strongly affect the tail of the loss distribution at large losses, which is due to the possibility of avalanches of loss events in times of extreme economic stress.

Note that we have been dealing here with “synthetic” parameter distributions for averages of loss distributions, as well as bare monthly failure probabilities. These could be replaced by realistic ones without affecting the general set-up. We have not looked specifically at finite size effects here. In [11] it was shown that they are fairly small.

4 Conclusion

In this paper we have looked to incorporate the risk due to credit contagion into the internal ratings based approach discussed in BASEL II. While the mathematical subtleties are discussed in full detail elsewhere [11], essentially the large number of neighbours assumed for firms means that the law of large numbers and central limit theorems apply to the interactions, meaning that our theory requires only two more parameters than the BASEL II approach. In terms of risk, one of the striking results is that while the effect of interactions is relatively weak in typical economic scenarios, it is pronounced in times of large economic stress, which leads to a significant fattening of the tails of the portfolio loss distribution. This has implications on the fitting of loss distributions to historical data, where care must be taken not only to fit the average behaviour but also to take care with the more extreme events.

This touches the issue of model calibration discussed in greater detail in [13]. We note that our model requires bare default probabilities and conditional default probabilities as inputs. Historical data, however only contain interaction-renormalised default probabilities, and thus the problem arises of how to disentangle the two effects. Concerning typical behaviour, Fig. 1 shows that the effect of interactions is fairly small, and interaction-renormalised default probabilities can, to a first approximation within this model, be taken as substitutes for the bare ones. Concerning conditional default probabilities, these would have to be obtained from refined rating procedures; see [13]. Interestingly, however, only the low order statistics of these are needed to describe the collective dynamics of the system. Their effect manifests itself only in situations of economic stress, generating fat tails in portfolio loss distributions.

The model we have proposed is relatively simple in two important respects. Firstly, we do not take into account credit quality migration but have just two states for our firms, solvent or defaulted. The model could be extended to allow for more states for each firm, although the full complexity of non-Markovian dynamics would resurface in an attempt to take credit quality migration along these lines into account. Secondly, the firms and their environment are rather homogeneous, which in practical situations is of course an approximation. This approximation has been made for convenience rather than out of necessity; the techniques described in [11] can be adapted so as to treat situations with more heterogeneity in local environments. We intend to work on some of these possible model generalisations in the future.

One advantage of our simple model is that it is exactly solvable and the solution itself is not overly involved theoretically or computationally, and we only need to introduce two extra parameters to quantify the effect of economic interactions — compared to the BASEL II approach, which ignores credit contagion altogether.

Acknowledgements

We thank Peter Neu for useful discussions and helpful remarks. This paper has been prepared by the authors as a commentary on the topic as at September 2006 and is not a definitive analysis of the subject matter covered. It does not constitute advice or guidance in this area and should not be relied upon as such. The paper has not been prepared by J.H. in his capacity as an employee of Hymans Robertson LLP and the views expressed do not represent those of Hymans Robertson LLP. Neither the authors nor Hymans Robertson LLP accept liability for any errors or omissions

References

References

- [1] R Jarrow and F Yu, 2001 J. Finance 56 1765-1799

- [2] K Giesecke and S Weber, 2006 J. Econ. Dyn. Control Credit contagion and aggregate losses (submitted)

- [3] T M Liggett, 1999 Stochastic Interacting Systems: Contact, Voter and Exclusion Processes Springer-Verlag: Berlin

- [4] M Davis and V Lo, 2001 Quant. Finance 1 382-387

- [5] J.P. Morgan Global Research, 1997 CreditMetricsTM: The Benchmark for Understanding Credit Risk Technical Document (New York) (www.creditmetrics.com)

- [6] Credit Suisse First Boston, 1997 Credit Risk+: A Credit Risk Management Framework Technical Document (New York) (www.csfb.com/creditrisk)

- [7] M B Gordy, 2000 J. Bank. Finance 24 119-149

- [8] R Merton, 1974 J. Finance 29 449-470

- [9] T K Siu, W K Ching, E S Fung and M K Ng, 2005 Quantitative Finance 5 543-556

- [10] F Yu 2005, Math. Finance submitted

- [11] J P L Hatchett and R Kühn 2006 J. Phys. A: Math. Gen 39 2231-2251

- [12] R Kühn and P Neu, 2003 Physica A 322 650-666

- [13] P Neu and R Kühn, 2004 Physica A 342 639-655

- [14] Basel Committee on Banking Supervision 2005 International Convergence of Capital Measurement and Capital Standards: A Revised Framework (Basel) (http://www.bis.org) Section III: Credit Risk - The Internal Ratings Based-Approach