Mixtures of compound Poisson processes as models of tick-by-tick financial data

Abstract

A model for the phenomenological description of tick-by-tick share prices in a stock exchange is introduced. It is based on mixtures of compound Poisson processes. Preliminary results based on Monte Carlo simulation show that this model can reproduce various stylized facts.

keywords:

Waiting-time; Duration; random walk; statistical finance;PACS: 05.40.-a, 89.65.Gh, 02.50.Cw, 05.60.-k, 47.55.Mh

Corresponding author: Enrico Scalas (scalas@unipmn.it),

url: www.econophysics.org

1 Introduction

Continuous time random walks (CTRWs) were introduced in Physics by Montroll and Weiss as a model for single-particle (tracer) diffusion [1]. An instance of CTRW, the normal compound Poisson process, had already been used in the probabilistic theory of insurance ruin since the beginning of the XXth Century [2, 3].

The seminal paper of Montroll and Weiss has been followed by many studies focusing on anomalous relaxation and anomalous diffusion. This is the subject of two recent reviews by Metzler and Klafter [4, 5].

The present author has recently reviewed the applications of CTRWs to Finance and Economics [6]. These applications were triggered by a series of papers on finance and fractional calculus [7, 8, 9], but the reader is referred to ref. [10] for an early application of the normal compound Poisson process to financial data.

The recent research of the present author has focused on the behaviour of waiting times (also known as durations) between trades and order in financial markets [8, 11, 12, 13]. It turned out that interorder and intertrade waiting times are not exponentially distributed. Therefore, the jump process of tick-by-tick prices is non-Markovian [8].

In an article within this issue [14], Bianco and Grigolini apply a new method to verify whether the intertrade waiting time process is a genuine renewal process [15, 16, 17]. This was assumed by the CTRW hypothesis in [7]. They find that intertrade waiting times follow a renewal process.

Here, inspired by the work of Edelman and Gillespie [18, 19], a phenomenological model for intraday tick-by-tick financial data is presented. It is able to reproduce some important stylized facts. The paper is organized as follows. Section 2 contains an outline of the theory of CTRWs. Section 3 contains a description of the model as well as a discussion on results from Monte Carlo simulations.

2 Outline of theory

2.1 Basic definitions

CTRWs are point processes with reward. The point process is characterized by a sequence of independent identically distributed (i.i.d.) positive random variables , which can be interpreted as waiting times between two consecutive events:

| (1) |

The rewards are i.i.d. not necessarily positive random variables: . In the usual physical intepretation, they represent the jumps of a random walker, and they can be -dimensional vectors. In this paper, only the 1-dimensional case is studied for a continuous random variable, but the extension of many results to the -dimensional case and to a lattice is straightforward. The position of the walker at time is (with and ):

| (2) |

CTRWs are rather good and general phenomenological models for diffusion, including anomalous diffusion, provided that the time of residence of the walker is much greater than the time it takes to make a jump. In fact, in this formalism, jumps are instantaneous.

The financial interpretation of the random variables is straightforward. If trades take place in a continuous double auction, both price variations and waiting times (also called durations) between two consecutive trades are random variables. If is the price of an asset at time defined according to the previous tick interpolation procedure, where is the time instant at which the last trade took place, then the price process can be considered as a pure jump stochastic process in continuous time. In finance, it is better to work with returns rather that prices. If is the price at time , then the variable is called the log-return or, better, the log-price. This variable is analogous to the position of the walker in the physical interpretation. In the financial intepretation the jump random variables are tick-by-tick log returns and they coincide with the difference between two consecutive log prices, whereas the waiting times or durations denote the elapsed time between two consecutive trades.

In general, jumps and waiting times are not independent from each other. In any case, a CTRW is characterized by the joint probability density of jumps and waiting times; is the probability of a jump to be in the interval and of a waiting time to be in the interval . The following integral equation gives the probability density, , for the walker being in position at time , conditioned on the fact that it was in position at time :

| (3) |

where is the so-called survival function. is related to the marginal waiting-time probability density . The two marginal densities and are:

| (4) |

and the survival function is defined as:

| (5) |

The integral equation, eq. (3) is linear and it can be solved in the Laplace-Fourier domain. The Laplace transform, of a (generalized) function is defined as:

| (6) |

whereas the Fourier transform of a (generalized) function is defined as:

| (7) |

A generalized function is a distribution (like Dirac’s ) in the sense of S. L. Sobolev and L. Schwartz [20].

One gets:

| (8) |

or, in terms of the density :

| (9) |

as, from eq. (5), one has:

| (10) |

In order to obtain , it is then necessary to invert its Laplace-Fourier transform . Analytic solutions are quite important, as they provide a benchmark for testing numerical inversion methods. In the next section, an explicit analytic solution for a class of continuous-time random walks with anomalous relaxation behaviour will be presented. It will be necessary to restrict oneself to the uncoupled case, in which jumps and waiting-times are not correlated.

2.2 The normal compound Poisson process

In this section, the solution of eq. (3) will be derived in the uncoupled case where the joint probability density of jumps and durations can be factorized in term of its marginals. After the derivation of a genearal formula for , this will be specialized to the case of the normal compound Poisson process (NCPP).

If jump sizes do not depend on waiting times, the joint probability density for jumps and waiting times can be written as follows:

| (11) |

with the normalization conditions and .

In this case the integral master equation for becomes:

| (12) |

This equation has a well known general explicit solution in terms of , the probability of jumps occurring up to time , and of the -fold convolution of the jump density, :

| (13) |

Indeed, is given by:

| (14) |

where is the -fold convolution of the waiting-time density:

| (15) |

The -fold convolutions defined above are probability density functions for the sum of variables.

The Laplace transform of , , reads:

| (16) |

By taking the Fourier-Laplace transform of eq. (12), one gets:

| (17) |

But, recalling that and , if and , eq. (17) becomes:

| (18) |

this gives, inverting the Fourier and the Laplace transforms and taking into account eqs. (13) and (14):

| (19) |

Eq. (19) can also be used as the starting point to derive eq. (12) via the transforms of Fourier and Laplace, as it describes a jump process subordinated to a renewal process.

A remarkable analytic solution is available when the waiting-time probability density function has the following exponential form:

| (20) |

Then, the survival probability is and the probability of jumps occurring up to time is given by the Poisson distribution:

| (21) |

This is the only Markovian case, and equation (19) becomes:

| (22) |

If follows the normal distribution , then the n-fold convolution is given by: .

Given a series of empirical tick-by-tick log returns, , as well as durations, , one can directly evaluate the three parameters : the activity of the Poisson process, : the average of log-returns, and : the standard deviation of log-returns by means of suitable estimators [10].

However, the normal compound Poisson process is not able to reproduce the following stylized facts on high frequency data:

-

1.

The empirical distribution of log-returns is leptokurtic, whereas the NCPP assumes a mesokurtic (actually normal) distribution.

- 2.

-

3.

The autocorrelation of absolute log-returns decays slowly [11], whereas the NCPP assumes i.i.d. log-returns.

- 4.

-

5.

Volatility and activity vary during the trading day [24], whereas the NCPP assumes they are constant.

3 Mixtures of normal compound Poisson processes

3.1 Definition

It is possible to overcome the above shortcomings by using a suitable mixture of NCPPs. During a trading day, the volatility and the activity are higher at the opening of the market, then they decrease at midday and they increase again at market closure [24]. If the trading day can be divided into intervals of constant activity , then the waiting-time distribution is a mixture of exponential distributions and its probability density can be written as:

| (23) |

where is a set of suitable weights. The activity seasonality can be mimicked by values of that decrease towards midday and then increase again towards market closure. In order to reproduce the correlation between volatility and activity, one can assume that:

| (24) |

where is a suitable constant. Future work will be devoted to an analytical study of this model as well as to further empirical investigations on model validation. Below, the results of a simulation performed with the model are presented, and the performance of the model with respect to the stylized facts is discussed.

3.2 Results

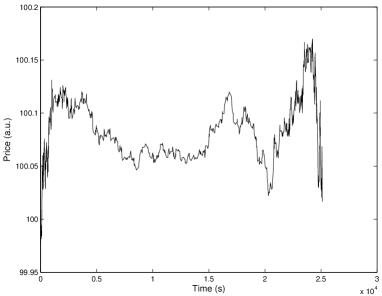

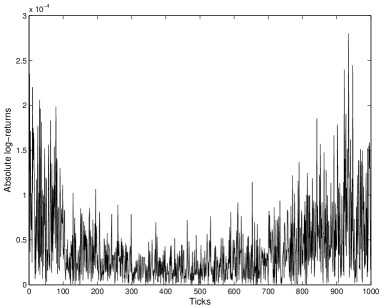

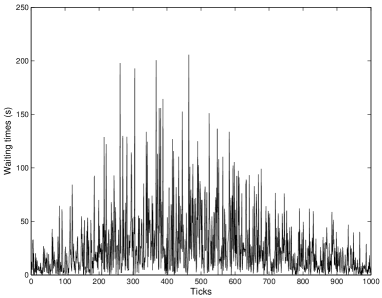

A Monte Carlo simulation of the model described in the previous subsection has been performed by considering a trading day divided into ten intervals of constant activity with = , s-1. For each value of , 100 exponentially distributed waiting times have extracted as well as 100 normally distributed log-returns with zero average and . Therefore, there are 1000 values of waiting times and log returns in a trading day, representing a rather liquid share. The opening price is set to 100 arbitrary units (a.u.). In Fig. 1, a sample path is plotted for the price as a function of trading time. Fig. 2 and Fig. 3 represent the tick-by-tick time series of log-returns and waiting times respectively. For this particular simulation, the effect of variable activity and volatility can be detected by direct eye inspection.

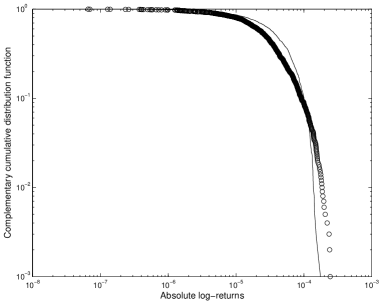

In order to show that this model is able to reproduce the stylized facts described above, another set of figures is presented in the following. In Fig. 4 the empirical complementary cumulative distribution function is plotted for absolute tick-by-tick log returns. For comparison, the Gaussian fit with the same standard deviation of the 1000 log-returns is given by a solid line. This distribution has fat tails, is leptokurtic and the kurtosis is equal to 6.

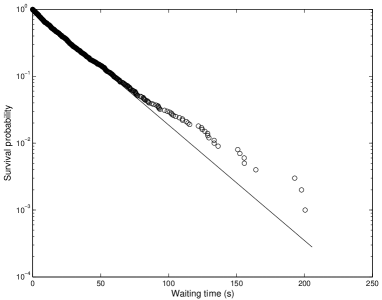

The empirical complementary cumulative distribution function for intertrade durations is given in Fig. 5. The solid line is the single exponential fit to the simulated data. There is excess standard deviation: the standard deviation of waiting times is 29 s, whereas the average waiting time is 25 s.

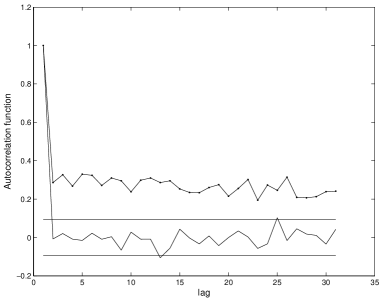

Fig. 6 shows the slow decay of the autocorrelation of absolute log-returns related to volatility clustering, whereas signed log-returns are zero already at the second lag.

In conclusion, the model based on mixtures of normal compound Poisson processes incorporates variable daily activity, as well as the dependence between durations and tick-by-tick log-returns via eq. (24). It is then able to replicate the following stylized facts:

-

•

The empirical distribution of log-returns is leptokurtic;

-

•

the empirical distribution of durations is non-exponential with excess standard deviation;

-

•

The autocorrelation of absolute log-returns decays slowly.

Work is currently in progress to empirically validate the model [25].

ACKNOWLEDGEMENTS

The authors acknowledges an interesting discussion with Peter Buchen and Tom Gillespie. He is indebted to Rudolf Gorenflo and Francesco Mainardi with whom he developed the application of continuous time random walks to finance. This work has been supported by the Italian MIUR grant ”Dinamica di altissima frequenza nei mercati finanziari”.

References

- [1] E.W. Montroll and G.H. Weiss, Random walks on lattices, II, J. Math. Phys. 6, 167–181 (1965).

- [2] F. Lundberg, Approximerad Framställning av Sannolikehetsfunktionen. AAterförsäkering av Kollektivrisker, (Almqvist & Wiksell, Uppsala, 1903).

- [3] H. Cramér, On the Mathematical Theory of Risk, (Skandia Jubilee Volume, Stockholm 1930).

- [4] R. Metzler and J. Klafter, The random walk’s guide to anomalous diffusion: a fractional dynamics approach, Phys. Rep. 339, 1-77, 2000.

- [5] R. Metzler and Y. Klafter, The restaurant at the end of the random walk: recent developments in the description of anomalous transport by fractional dynamics, J.Phys. A: Math. Gen. 37, R161-R208, (2004).

- [6] E. Scalas The application of continuous-time random walks in finance and economics, Physica A, 225-239, (2006).

- [7] E. Scalas, R. Gorenflo, and F. Mainardi, Fractional calculus and continuous-time finance, Physica A 284, 376–384 (2000).

- [8] F. Mainardi, M. Raberto, R. Gorenflo, and E. Scalas, Fractional calculus and continuous-time finance II: the waiting-time distribution, Physica A 287, 468–481, (2000).

- [9] R. Gorenflo, F. Mainardi, E. Scalas, and M. Raberto Fractional calculus and continuous-time finance III: the diffusion limit, in M. Kohlmann and S. Tang (Editors): Trends in Mathematics - Mathematical Finance, pp. 171–180 (Birkhäuser, Basel, 2001).

- [10] S.J. Press, A compound events model for security prices, Journal of Business 40, 317–335 (1967).

- [11] M. Raberto, E. Scalas, and F. Mainardi, Waiting-times and returns in high-frequency financial data: an empirical study, Physica A 314, 749–755 (2002).

- [12] E. Scalas, R. Gorenflo, H. Luckock, F. Mainardi, M. Mantelli, and M. Raberto, Anomalous waiting times in high-frequency financial data, Quantitative Finance 4, 695–702 (2004).

- [13] E. Scalas, T. Kaizoji, M. Kirchler, J. Huber, and A. Tedeschi, Waiting times between orders and trades in double-auction markets Physica A, in press.

- [14] S. Bianco and P. Grigolini, Aging in financial markets, this issue (2006).

- [15] D. Cox, Renewal Theory, (Methuen, London, 1967). (First edition in 1962).

- [16] P. Allegrini, F. Barbi, P. Grigolini, and P. Paradisi, Dishomogeneous Poisson processes vs. homogeneous non-Poisson processes, preprint (2006).

- [17] P. Allegrini, F. Barbi, P. Grigolini, and P. Paradisi, Renewal, Modulation and Superstatistics, Phys. Rev. E, in press.

- [18] T.R. Gillespie, The stochastically subordinated Poisson normal process for modelling financial assets, Ph.D Thesis, School of Mathematics and Statistcs, The University of Sydney, (1999).

- [19] D. Edelman and T. Gillespie, The stochastically subordinated Poisson normal process for modelling financial assets, Annals of Operations Research, 100, 133–164, (2000).

- [20] I. M Gelfand and G. E. Shilov, Generalized Functions, vol. 1, (Academic Press, New York and London 1964). (Translated from the 1958 Russian Edition).

- [21] R. Engle and J. Russel Forecasting the frequency of changes in quoted foreign exchange prices with the autoregressive conditional duration model, Journal of Empirical Finance 4, 187–212 (1997).

- [22] R. Engle and J. Russel, Autoregressive conditional duration: A new model for irregularly spaced transaction data, Econometrica 66, 1127–1162 (1998).

- [23] M.M. Meerschaert and E. Scalas, Coupled continuous time random walks in finance, Physica A, in press.

- [24] W. Bertram, An empirical investigation of Australian Stock Exchange data, Physica A 341, 533–546.

- [25] E. Scalas, T. Aste, T. Di Matteo, M. Nicodemi, A. Tedeschi, in preparation.