Analysis of price diffusion in financial markets using PUCK model

Takayuki Mizunoa, Hideki Takayasub, and Misako TakayasuaaDepartment of Computational Intelligence & Systems Science,

Interdisciplinary Graduate School of Science & Engineering,

Tokyo Institute of Technology, 4259-G3-52 Nagatsuta-cho, Midori-ku, Yokohama 226-8502, Japan

bSony Computer Science Laboratories Inc., 3-14-13 Higashigotanda, Shinagawa-ku, Tokyo 141-0022, Japan

Abstract

Based on the new type of random walk process called the Potentials of

Unbalanced Complex Kinetics (PUCK) model, we theoretically show that the

price diffusion in large scales is amplified times, where

is the coefficient of quadratic term of the potential. In short time

scales the price diffusion depends on the size of the super moving

average. Both numerical simulations and real data analysis of Yen-Dollar

rates are consistent with theoretical analysis.

pacs:

89.65.Gh, 05.40.Fb, 05.45.Tp

††preprint: APS/123-QED

I Introduction

Crashes and uncontrollable hikes can often occur in financial markets. Such

changes of the prices confuse the market and damage the economy because they

start abruptly in many cases. Therefore, techniques to measure the

probabilistic risk of sudden change in the prices have been studied using

tick-by-tick data [1]. Recently, it was empirically found that change of

prices can be approximated by the Fokker-Planck equation and the new type of

random walk in a potential field [2,3,4,5]. The potential field is

approximated by a quadratic function with its center given by the moving

average of past market prices. This random walk model is called the

Potentials of Unbalanced Complex Kinetics (PUCK) model in which the

potential slowly changes in the market [3,4]. In this paper, we focus on the

diffusion properties of this random walk process and calculate the diffusion

coefficient which is helpful for estimating the market risk.

We first review an empirical derivation of the PUCK model. We next show

that the statistically steady condition of price fluctuations depends on the

potential field, and clarify relationships between the price diffusion and

the potential field. We finally demonstrate that the price diffusion in

short time scales depends on the size of moving average, however, large

scale diffusion properties are independent of the moving average. In the

paper, we used all the Bid record (about 20 million ticks) of the exchange

rates for Yen/Dollar that were traded by the term from 1989 to 2002 to find

the firm statistical laws.

II Empirical derivation of PUCK model

Prices in financial markets always have violent fluctuation in a short time

scale. We first eliminate the uncorrelated noise from the

price in order to reduce the statistical error. We next investigate

the dynamics of the price.

We can perform this noise elimination process by introducing an optimum

moving average :

(1)

(2)

where is a price, is an uncorrelated noise and

gives the weight factors where the time is measured by ticks. The weight

factors are calculated by using Yule-Walker equation [6,7,8]. In a case of

Yen-Dollar rate, the weight factor follows an exponential function

whose characteristic decay time is about 30 seconds [6].

We investigate a behavior of the optimum moving average

obtained by eliminating the uncorrelated noise from the price

. We introduce a super moving average defined

by

(3)

In financial markets, it is found that the following relationship between

and holds for a certain range of

[2],

(4)

where the mean of noise is zero. The Eq.(4) means that the price

change can be approximated by a random walk in a quadratic potential field

whose center is given by the moving average of past prices. It is known that

the potential coefficient has a long autocorrelation [3,4].

III Statistically steady condition of price fluctuations in the PUCK

model

We focus on Eq.(4) with the case of a constant because the coefficient

is known to change slowly in financial markets. Eq.(4) is transformed

as follows,

(5)

This is a type of AR process for price difference when is a constant. We

can estimate the conditions of to make the AR process being

statistically steady. Eq.(5) is transformed by the following determinant,

(6)

where

(7)

If , the time

series of is in a weakly steady

state because becomes independent of the initial value of .

This condition is fulfilled when the absolute values of all eigenvalues of

are less than 1. For example, when the time series of is statistically steady if the potential

coefficient satisfies . When the eigenvalues

of are given by

(8)

Solving the steady state condition we find that the potential coefficient

should be in the range of for . Numerically

calculating the eigenvalues for as shown in Fig.1 we find

that the time series of is

statistically stationary if the potential coefficient is in the following

range,

(9)

Outside the condition of Eq.(9), the range of price fluctuations increases

indefinitely depending on the time .

IV Diffusion of prices in market potential field

As the potential coefficient has a long autocorrelation, we can

calculate the future price diffusion using Eq.(4). This prediction is

crucial in order to evaluate the risks of market. We clarify statistical

laws of price diffusion described by Eq.(4) using both simulations and

theoretical analysis.

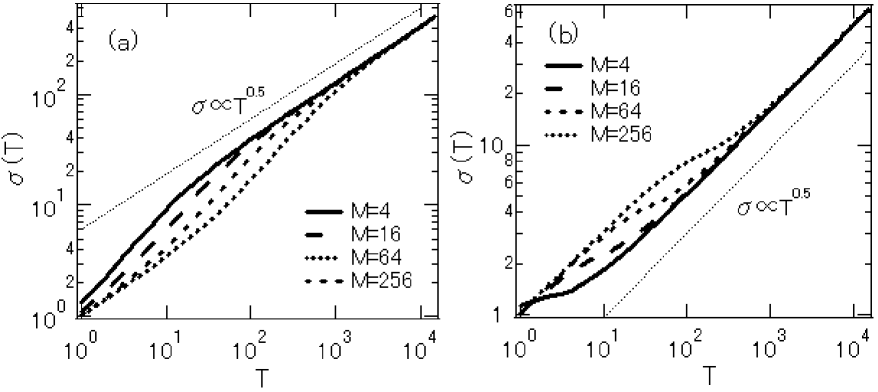

By simulating Eq.(4) for the case of is a constant, we investigate

the standard deviation on a time scale defined by

(10)

In Fig.2 we plot for , , , when and . Here, is the Gaussian random number whose standard

deviation is 1. The time scale where the Hurst exponent converges 0.5

depends on . For example, the time scale is about when ,

while the time scale is around when

We can estimate the standard deviation in the long time

scale limit. The variance of change of optimum moving average price

is given by

(11)

By introducing a rough approximation

(12)

we have the following simple formulation after some calculation,

(13)

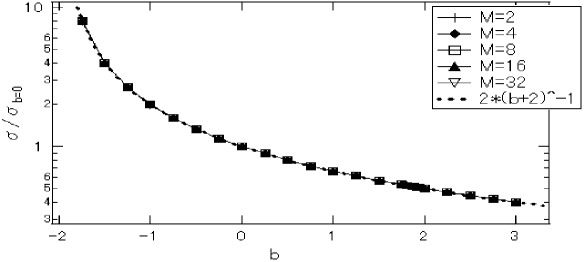

where , and is the standard deviation when . In this long time scales,

the standard deviation of the price is amplified times by

the potential field. In Fig.3 we show relationships between the potential

coefficient and the ratio of standard deviation when by

simulating Eq.(4) for , 4, 8, 16, 32. We can confirm that the price

diffusion of numerical simulations follows Eq.(13) independent of in the

long time scale. From Eq.(13) we can theoretically find that in the long

time scales the price diffusion is independent of , independent of ,

.

V Diffusion of Yen-Dollar rates

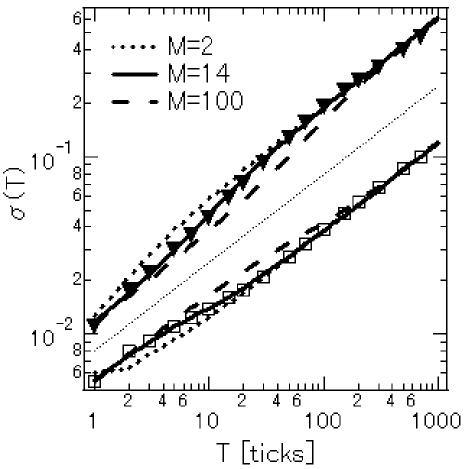

From dataset of real market prices, we can estimate the value of , and

presume the best value of by comparing the price diffusion of numerical

simulations to real price diffusion. Fig.4 shows the diffusions of

Yen-Dollar rates from 3:35 to 8:35 and from 9:25 to 23:25 in 11/9/2001, the

day of terrorism. The rates were stable till 8:35 and it became quite

unstable after 9:25. The rates until 8:35 follow a slow diffusion in short

time scales, namely, the market has an attractive potential . As

shown in Fig.4, we can recreate the rate diffusion in all time scales by

simulating Eq.(4) with and ticks. We next focus on the

unstable rates after 9:25 that follow a fast diffusion in short time scales.

When and ticks, the price diffusion of numerical

simulation is also consistent with the rate diffusion. The price diffusion

depends on in the short time scales, although the price diffusion is

independents of in the long time scales. Therefore, if ticks,

there are gaps between the price diffusion of numerical simulations and the

rate diffusion in the short time scales as shown in Fig.4. In other real

markets, we can also estimate the best value of from such

characteristics of price diffusion.

VI Discussion

We can approximate the change of market prices by the random walk in a

potential field. The potential field is well approximated by a quadratic

function with its center given by the moving average of past prices. The

random walk process is called the PUCK model. By analyzing the model, we

clarified that the statistically steady condition of price fluctuations

depends on the potential coefficient , and we also theoretically proved

that the price diffusion in the long time scales is amplified times, independent of the size of super moving average. In short

time scales the price diffusion depends on . We can estimate the best

value of in real financial markets by observing this dependence. We

recreated the diffusion of Yen-Dollar rates in all time scales by the PUCK

model. The potential coefficient is helpful to measure the probabilistic

risk of sudden change in the prices. We may be able to build better

financial options that offset the risk by applying the price diffusion of

the PUCK model.

Acknowledgements.

This work is partly supported by Research Fellowships of the Japan Society

for the Promotion of Science for Young Scientists (T.M.). The authors

appreciate H. Moriya of Oxford Financial Education Co Ltd. for providing the

tick data.

References

(1)[1] J. P. Bouchaud and M. Potters, Theory of financial risks, Cambridge

university press, 2000.

(2)[2] M. Takayasu,T. Mizuno, T. Ohnishi, and H. Takayasu, Temporal

Characteristics of Moving Average of Foreign Exchange Markets, in Practical

Fruits of Econophysics (Springer Verlag, Tokyo. 2006) 29-32.

(3)[3] M. Takayasu, T. Mizuno and H. Takayasu, Potentials of Unbalanced Complex

Kinetics Observed in Market Time Series, physics/0509020.

(4)[4] M. Takayasu, T. Mizuno and H. Takayasu, Potential Force Observed in

Market Dynamics, Physica A, to appear.

(5)[5] R. Friedrich, How to Quantify Deterministic and Random Influences on the

Statistics of the Foreign Exchange Market, PRL 84, 5224-5227, 2000.

(6)[6] T. Ohnishi, T. Mizuno, K. Aihara, M. Takayasu, H. Takayasu, Statistical

properties of the moving average price in dollar-yen exchange rates, Physica

A 344, pp.207-210, 2004.

(7)[7] T. Mizuno, M. Takayasu, and H. Takayasu, Modeling a foreign exchange

rate using moving average of Yen-Dollar market data, in Practical Fruits of

Econophysics (Springer Verlag, Tokyo. 2006) 57-61.

(8)[8] T. Ohnishi, T. Mizuno, K. Aihara, M. Takayasu, H. Takayasu, Systematic

tuning of optimal weighted-moving-average of yen-dollar market data, in

Practical Fruits of Econophysics (Springer Verlag, Tokyo. 2006) 62-66.

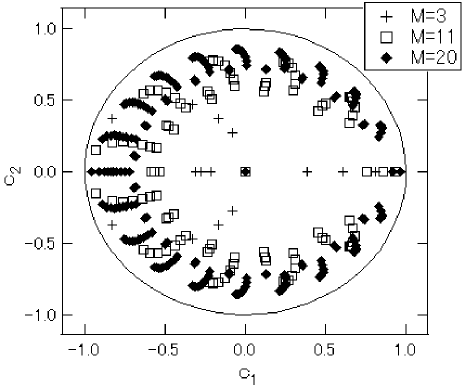

Figure 1: The eigenvalues of matrix . The and are

real and imaginary parts of . The pluses are for

when . The squares show for when . The diamonds express for when .

The circle indicates .

Figure 2: Standard deviation of price changes in the time scale

. The heavy lines show price diffusions of numerical simulation for (top), 16(second), 64(third), 256(bottom). Here, in (a)

and in (b). The standard deviation of is 1. The guideline

indicates .

Figure 3: Relationship between potential coefficient and standard deviation

ratio / when

the time scale . Theory (dashed line) and numerical simulations

for (plus), 4(diamond), 8(square), 16(black triangle), 32(white

triangle).[4]

Figure 4: Diffusion of Yen-Dollar rates. The squares and triangles show the

diffusion from 3:35 to 8:35 and from 9:25 to 23:25 in 11/9/2001. The top 3

lines are the numerical simulation of Eq.(4) for , 14, 100 ticks when

. The standard deviation of is 0.0115 yen/dollar. The

bottom 3 lines show the numerical simulation for , 14, 100 ticks when

. The standard deviation of is 0.0054 yen/dollar. The straight

line expresses the normal diffusion with the slope 0.5.