Market memory and fat tail consequences in option pricing on the expOU stochastic volatility model

Abstract

The expOU stochastic volatility model is capable of reproducing fairly well most important statistical properties of financial markets daily data. Among them, the presence of multiple time scales in the volatility autocorrelation is perhaps the most relevant which makes appear fat tails in the return distributions. This paper wants to go further on with the expOU model we have studied in Ref. masoliver by exploring an aspect of practical interest. Having as a benchmark the parameters estimated from the Dow Jones daily data, we want to compute the price for the European option. This is actually done by Monte Carlo, running a large number of simulations. Our main interest is to “see” the effects of a long-range market memory from our expOU model in its subsequent European call option. We pay attention to the effects of the existence of a broad range of time scales in the volatility. We find that a richer set of time scales brings to a higher price of the option. This appears in clear contrast to the presence of memory in the price itself which makes the price of the option cheaper.

Keywords: stochastic volatility, option pricing, long memory

pacs:

89.65.Gh, 02.50.Ey, 05.40.Jc, 05.45.TpI Introduction

The model, suggested by Bachelier in 1900 as an ordinary random walk and redefined in its final version by Osborne in 1959 osborne , presupposes a constant “volatility” , that is to say, a constant diffusion coefficient . However, and especially after the 1987 crash, there seems to be empirical evidence, embodied in the so-called “stylized facts”, that the assumption of constant volatility does not properly account for important features of markets cont ; plerou ; bouchaud . It is not a deterministic function of time either (as might be inferred by the evidence of non stationarity in financial time series) but a random variable. In its more general form one therefore may assume that the volatility is a given function of a random process , i.e., .

At late eighties different stochastic volatity (SV) models [Brownian motion with random diffusion coefficient] were presented for giving a better price to the options somewhat ignoring their ability to reproduce the real price time series fouquebook . More recently SV models have been suggested by some physicists as good candidates to account for the so-called stylized facts of speculative markets dragulescu ; perello ; perello1 ; perello2 ; silva ; duarte . In the context of mathematical finance, we mainly have three models: the Ornstein-Uhlenbeck (OU) perello2 , the Heston dragulescu and the exponential Ornstein-Uhlenbeck model fouque . We have recently tried to decide which model works better perello ; perello1 . Very recently we have studied the exponential Ornstein-Uhlenbeck stochastic volatility model fouque and observed that the model shows a multiscale behavior in the volatility autocorrelation masoliver . It also exhibits a leverage correlation and a probability profile for the stationary volatility which are consistent with market observations. All these features seem to make the model more complete than other stochastic volatility models also based on a two-dimensional diffusion. It is worth to mention that there has been some more sophisiticated models based on a three-dimensional diffusion process that reproduce the intrincate set of memories in market dynamics vicente ; perello3 . Indeed, coming from multifractality framework, there are recent nice papers bacry with promising features to provide even a better description that the one by the common stochastic volatility models sornette .

II The volatility model

Let us briefly summarize the main definitions and the properties of the exponential Ornstein-Uhlenbeck stochastic volatility model masoliver . The model consists in a two-dimensional diffusion process given by the following pair of Itô stochastic differential equations (SDEs):

| (1) | |||||

| (2) |

where dots represent time derivative. The variable is the undrifted log-price or zero-mean return defined as , where is a the asset price. The parameters , , and appearing in Eq. (2) are positive and nonrandom quantities. The two noise sources of the process are correlated Wiener processes, i.e., are zero-mean Gaussian white noise processes with cross correlations given by

| (3) |

where , . In terms of the proces the volatility is given by

| (4) |

It is worth to mention that multifractals models also considers a random variable which describes the logarithm of the volatility bacry ; sornette .

Among the most important results of the expOU, we must stress the following three masoliver . First of all the stationary volatility pdf which is a log-normal distribution being quite consistent with empirical data bouchaud

| (5) |

where . Notice that the stationary distribution broadens the tails as we increase the value of . Secondly, we have the leverage effect bouchaud

| (6) |

where is the Heaviside step function. One can show that

| (7) |

while leverage is negligible for large times. These approximations hold only if we take . Thirdly, and perhaps the most important, the volatility autocorrelation

| (8) |

which expanded in the right way allow us to observe a cascade of exponentials

| (9) |

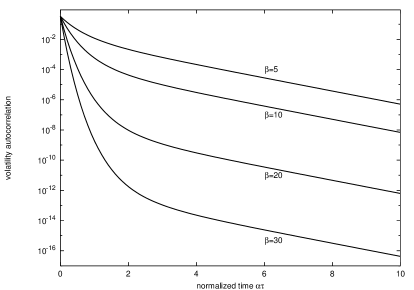

This expression indicates that there are infinite time scales between the limiting behaviours

| (10) |

As one can observe the characteristic time scale for the long time might be associated to while short time scale in leverage is related to (see Fig. 1). The distance between the smallest time scale and the largest is given by . The bigger , the larger is the distance and the richer is the cascade of multiple time scales of the process. Even more, as we enlarge the distance between smaller time scale and larger time scale, we also get a broader lognormal distribution (cf. Eq. (5)) for the volatility and a fatter distribution fo the returns.

III Option pricing

Having in mind latter expressions and main messages concerning , we can start looking at the inferrences of the volatility long range memory in the option price. An European option is a financial instrument giving to its owner the right but not the obligation to buy (European call) or to sell (European put) a share at a fixed future date, the maturity time , and at a certain price called exercise or striking price . In fact, this is the most simple of a large variety of derivatives contracts. In a certain sense, options are a security for the investor thus avoiding the unpredictable consequences of operating with risky speculative stocks.

The payoff of the European call contract at maturity date is

To compute the price of the call we can use the average (on an equivalent martingale measure) over a large set of simulated paths which can be written mathematically as follows

| (11) |

To do so we assume the process defined in the pair of Eqs. (1)-(2) but with a drift equal to the risk free interest ratio and with a market price of risk for the volatility component set to be 0. That is: keeping the current measure for the dynamics of the volatility. There are many subtleties behind the evaluation of the volatility market price of risk and we address the reader to the book by Fouque et al. fouquebook to get a deeper knowledge on this issue.

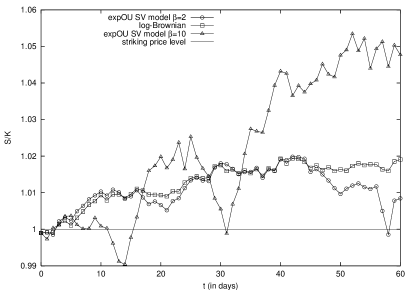

We thus simulate the random path assuming one day timesteps. Figure 2 shows the different paths observed for the SV model and the log-Brownian one using as a volatility o diffusion coefficient (cf. Eq.( 4)). Repeating the paths 1,000,000 times over the same time window, we can get an approximate idea of the correction to the classic Black-Scholes price formula. We recall that Black-Scholes assumes a log-Brownian motion for the underlying whose price is well-known and has the analytical solution:

| (12) |

where is the probability integral

| (13) |

and its arguments are

| (14) |

In contrast with some contributions from mathematical finance, we are not inserting the parameters values blindly nor providing a large collection of parameters where it is quite hard to intuit the meaning and the effects of each parameters. We take the parameters set in Ref. masoliver for the Dow Jones daily index as a benchmark. The parameters derived gives an opposite approach to the one already performed by Fouque etal. fouque for the expOU. They are focused in analytical asymptotic results with the cases where but the problem is that with this restriction one does not have the desired cascade of time scales in the volatility autocorrelation.

We recall that is the volatility level assuming no auxilary diffusion process for the volatility, gives the asymetry between positive and negative return change and the appropriate sign for the leverage effect. And finally, short range memory time scale is measured by which appears to be of the order of few weeks (10-20 days). We will now focus on the effect of the largest time scale memory which is considered to be of the order of years. We have shown in Ref. masoliver that a good approximate solution for reproduce the memories of the market is performed taking , and . The comparison between shortest and largest time scale is provided with and at least for the Dow Jones daily data this is around 3.8.

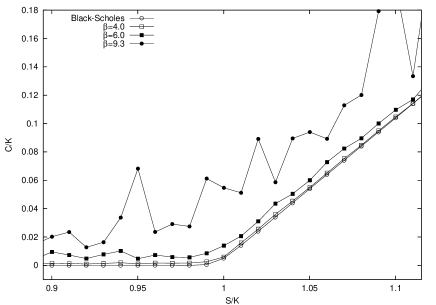

In Figure 3 we plot the call price for several values of averaging over the initial volatility with the lognormal distribution (5). We take maturity date at 20 days and we represent the option assuming that the risk free interest ratio to 5% per year. Even for such a small time horizon (much smaller than the volatility memory), we get important price differences. And in any case the longer the memory is the more expensive is the option. This can also be quantified by the relative price between new option price and the Black-Scholes one, that is:

| (15) |

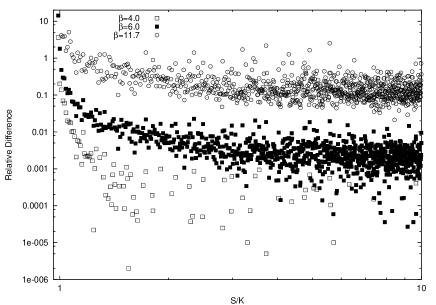

The results are plotted in Fig. 4. One observe that the price difference becomes more important with a monotonic increase in terms of . These differences may become relatively very important for small moneyness . And the decay of the relative difference for larger distances with respect to the striking price is becoming slowler with a higher value of . We have tested the results with different maturity dates and with different values for , and with similar conclusions.

In a previous paper option , we also have been studying the effects of the memory in the option price. In that case, however, we had memory in the price itself breaking the efficient market hypothesos. We had observed that the call became cheaper with this kind of memory even if this of only one day. The presence of memory in the volatility has opposite consequences. This paper has aimed to insist in the fact that the memory persistence in volatility affects the price making this to be higher.

Acknowledgements.

I wish to warmly thank Jaume Masoliver for useful discussions on the expOU modeling. This work has been supported in part by Dirección General de Investigación under contract No. BFM2003-04574 and by Generalitat de Catalunya under contract No. 2000 SGR-00023.References

- (1) E-mail: josep.perello@ub.edu

- (2) J. Masoliver, J. Perelló, Quantitative Finance in press.

- (3) M.F.M. Osborne, Operations Research 7 (1959) 145–173.

- (4) R. Cont, Quantitative Finance 1 (2001) 223.

- (5) V. Plerou, P. Gopikrishnan, L. N. Amaral, M. Meyer and E. Stanley, Phys. Rev. E 60 (1999) 6519-6528.

- (6) J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing: From Statistical Physics to Risk Management (Cambridge University Press, Cambridge, 2003)

- (7) J.-P. Fouque, G. Papanicolaou, and K. R. Sircar, Derivatives in Financial Markets with Stochastic Volatility (Cambridge University Press, Cambridge, 2000).

- (8) J.-P. Fouque, G. Papanicolaou and K. R. Sircar, International Journal of Theoretical and Applied Finance 3 (2000) 101–142.

- (9) A. Dragulescu and V. Yakovenko, Quantitative Finance 2 (2002) 443–453.

- (10) J. Perelló and J. Masoliver, Physical Review E 67 (2003) 037102.

- (11) J. Perelló, J. Masoliver and N. Anento, Physica A 344 (2004) 134–137.

- (12) J. Masoliver and J. Perelló, International Journal of Theoretical and Applied Finance 5 (2002) 541–562.

- (13) C. Silva, R. Prange and V. Yakovenko, Physica A 344 (2004) 227–235.

- (14) S.M. Duarte Queiros, Europhysics Letters 71 (2005) 339.

- (15) J. Perelló, J. Masoliver and J.-P. Bouchaud, Applied Mathematical Finance 11 (2004) 27–50.

- (16) R. Vicente, C. de Toledo, V. Leite, N. Caticha, Physica A 361 (2006) 272–288.

- (17) J.-P. Fouque, G. Papanicolau, R. Sircar and K. Solna, SIAM J. Multiscale Modeling and Simulation 2 (2003) 22–42.

- (18) See for instance: Muzy, J.-F., E. Bacry, Phys. Rev. E 66 (2002) 056121.

- (19) A. Saichev, D. Sornette, Phys Review E in press. cond-mat/0602660

- (20) J. Perelló, J. Masoliver, Physica A 3̱30 (2003) 622-652