Dynamical change of Pareto index in Japanese land prices

Abstract

We investigate the dynamical behavior in the large scale region of non-equilibrium systems, by employing data on the assessed value of land in 1983 – 2006 Japan. In the system we find the detailed quasi-balance, which has the symmetry: ( and are two successive land prices). By using the detailed quasi-balance and Gibrat’s law, we derive Pareto’s law with varying Pareto index annually. The parameter corresponds with the ratio of Pareto indices , and the relation is confirmed in the empirical data nicely.

PACS code : 04.60.Nc

Keywords : Econophysics; Pareto law; Gibrat law; Detailed quasi-balance

1 Introduction

In the large scale region of wealth, income, profits, assets, sales, the number of employees and etc (), the cumulative probability distribution obeys a power-law:

| (1) |

This power-law and the exponent are called Pareto’s law and Pareto index, respectively [1].

Recently, Fujiwara et al. [2] have explained Pareto’s law (and the reflection law) by using the law of detailed balance and Gibrat’s law [3], which are also observed in empirical data. The detailed balance is time-reversal symmetry observed in a relatively stable economy:

| (2) |

Here and are two successive incomes, profits, assets, sales, etc. and is a joint probability distribution function (pdf). On the other hand, Gibrat’s law is valid in the large scale region where the conditional probability distribution of growth rate is independent of the initial value :

| (3) |

Here growth rate is defined as the ratio and is defined by using the pdf and the joint pdf as . In the proof, Fujiwara et al. assume no model and only use these two underlying laws in empirical data. In Ref. [4], it is reported that the Pareto index is also induced from the reflection law.

These findings are important for the progress of econophysics. Above derivations are, however, valid only in the economic equilibrium where the detailed balance (2) holds. In order to discuss the transition, the dynamics should be established by investigating long-term economic data in which dynamical transitions are observed. Unfortunately, it is difficult to obtain personal income or company size data for a long period.

In this study, we investigate the dynamical behavior in the large scale region of non-equilibrium systems, by employing data on the assessed value of land in 1983 – 2006 Japan. Because the distribution of Japanese land prices has similar features with one of personal income and company size [5], and the long-term database is readily available [6].

In the non-equilibrium system we find the detailed quasi-balance, which has the symmetry: . By using the detailed quasi-balance and Gibrat’s law, we derive Pareto’s law with varying Pareto index annually. The parameter corresponds with the ratio of Pareto indices , and the relation is confirmed in the empirical data nicely [7].

2 Detailed quasi-balance

In Japan, land is a very important asset and land prices change annually in a 24-period (1983 – 2006). This period contains bubble term (1986 – 1991) caused by the abnormal rise of land prices. The economy correlates with land prices. We employ the database of the assessed value of land, which indicates the standard land prices, covering the 24-year period from 1983 to 2006.222 In Ref. [7], the number of data points of land prices increased gradually, because the database only contained data points which existed in the 2005 evaluation. In this study, the database contains all data points which existed in every year evaluation. The results, however, do not change seriously.

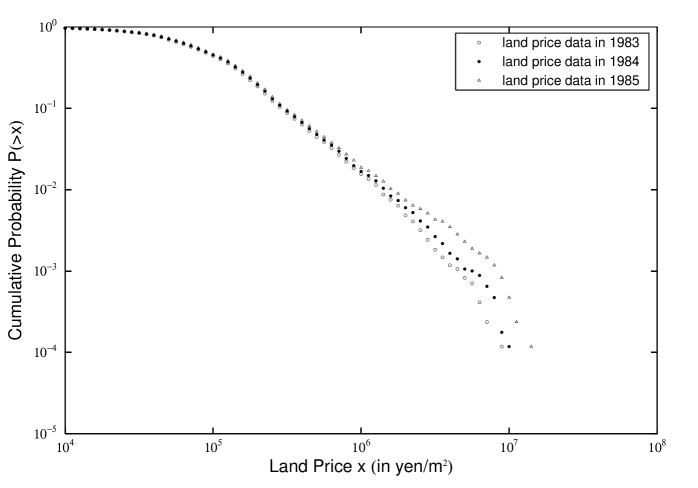

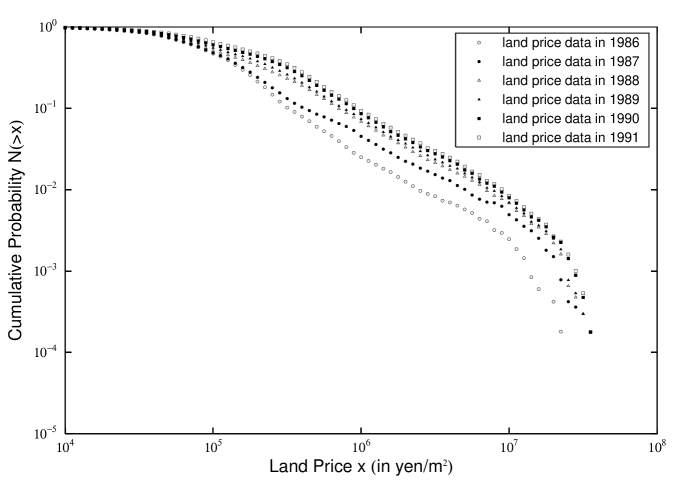

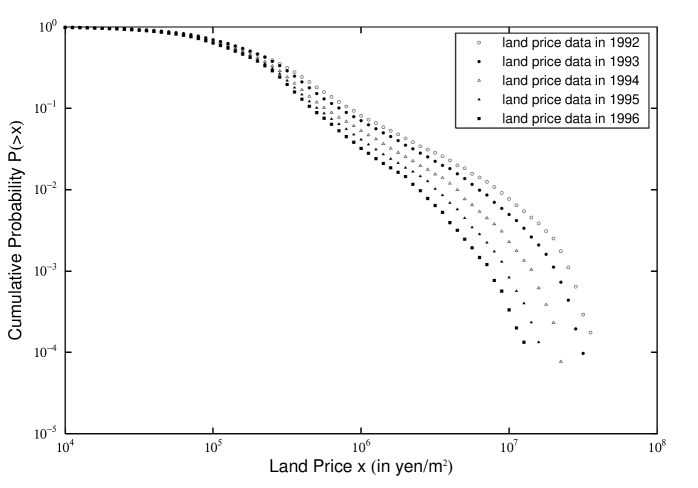

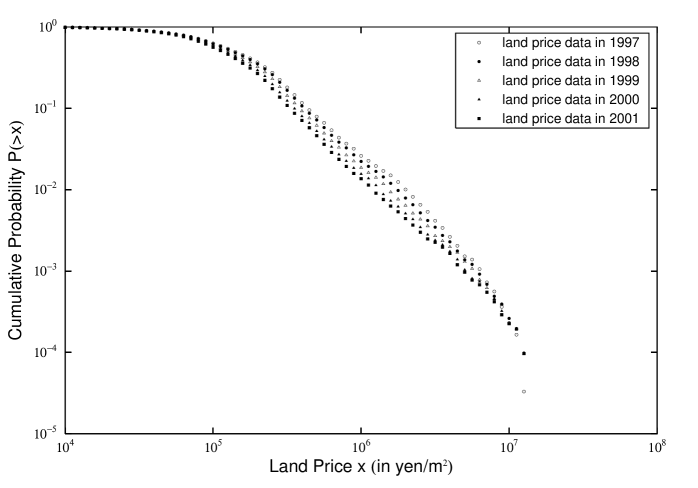

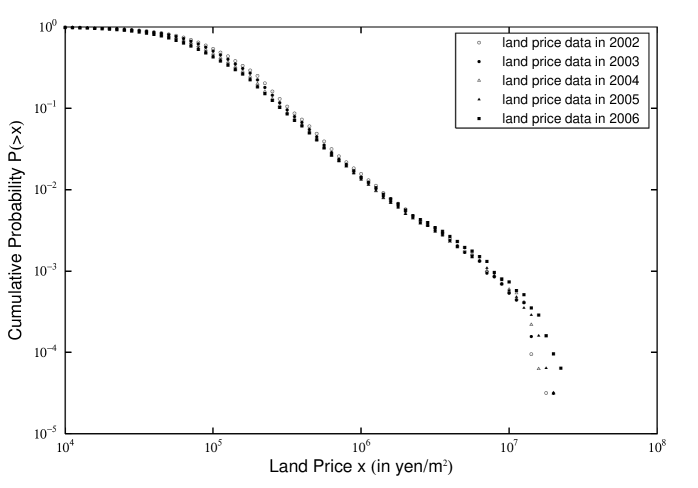

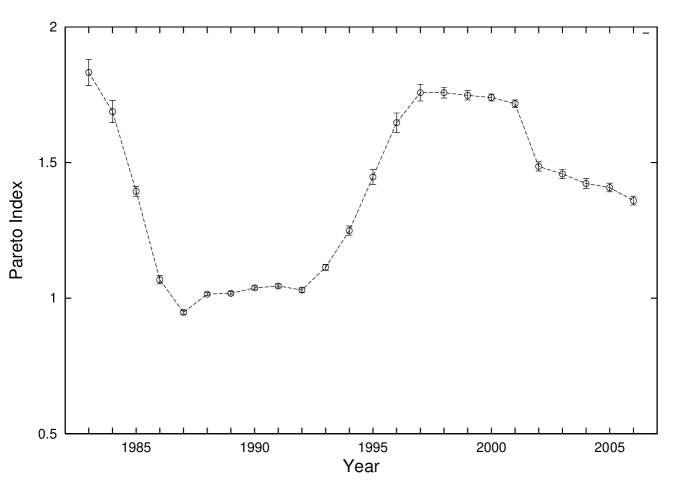

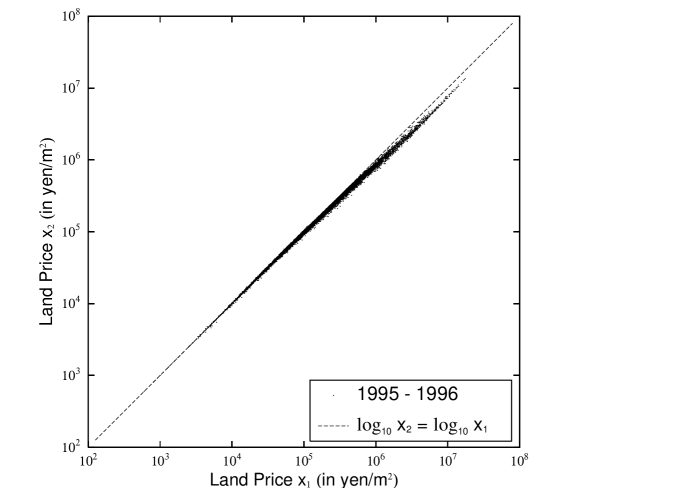

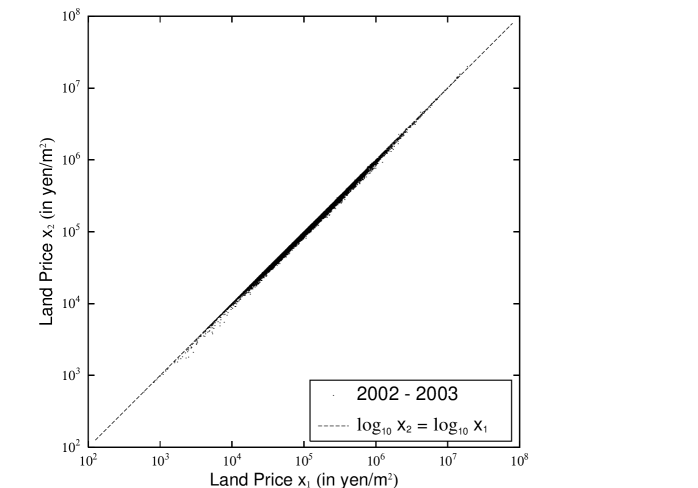

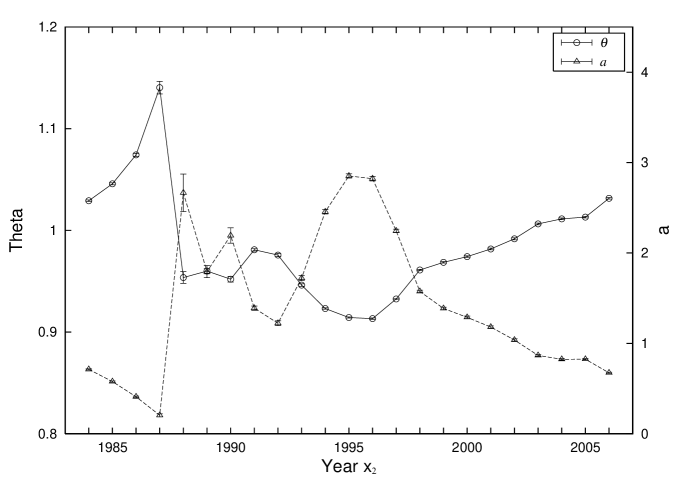

The cumulative probability distributions of land prices are shown in Fig. 1 – 5. From Fig. 1 – 5, the power-law is confirmed in the large scale region. For each year, we estimate Pareto index in the range of land prices from to where Pareto’s law holds approximately. Annual change of Pareto index from 1983 to 2006 is represented in Fig. 6. In this period, Pareto index has changed annually. This means that the system is not in equilibrium and the detailed balance (2) does not hold. Actually, the breakdown in the large scale region is observed in the scatter plot of all pieces of land assessed in the database (Fig. 7 for instance). There is no symmetry in Fig. 7 obviously. On the other hand, the detailed balance ( symmetry) in the large scale region is observed approximately in Fig. 8 for instance.

From Fig. 7 – 8, we make a simple assumption that the symmetry of the joint pdf is represented as a regression line fitted by least-square method as follows

| (4) |

In this form, the detailed balance (2) has the special symmetry, . For each scatter plot, we measure , in the same range where Pareto index is estimated and the result is shown in Fig. 9.

From this symmetry (), we extend the detailed balance (2) to

| (5) |

We call this law the detailed quasi-balance.

3 Pareto’s law with varying Pareto index

In this section, we derive Pareto’s law with varying Pareto index by using the detailed quasi-balance (5). In the proof, we assume Gibrat’s law (3) in the large scale region, because the number of data points is insufficient to observe Gibrat’s law.

Due to the relation of under the change of variables from to , these two joint pdfs are related to each other

| (6) |

where we use a modified ratio . From this relation, the detailed quasi-balance (5) is rewritten in terms of as follows:

| (7) |

Substituting the joint pdf for the conditional probability , the detailed quasi-balance is expressed as

| (8) | |||||

| (9) |

By expanding Eq. (9) around , the following differential equation is obtained

| (10) |

The solution is given by

| (11) |

Here we consider two cumulative probability distributions and , which lead

| (12) | |||||

| (13) |

From Eq. (11), (12) and (13), the relation between , and is expressed as

| (14) |

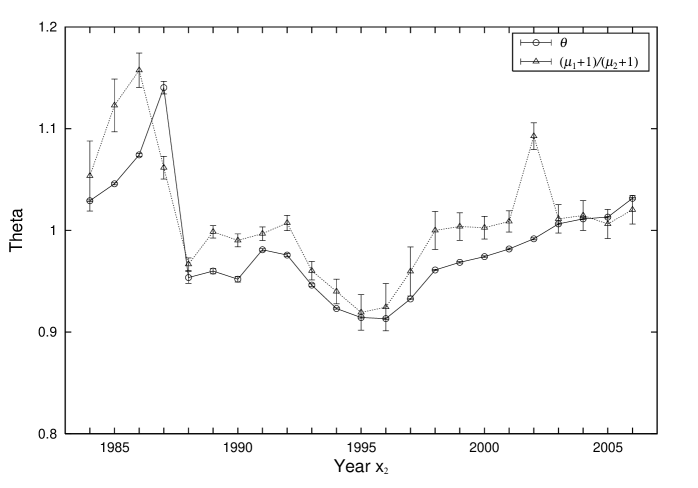

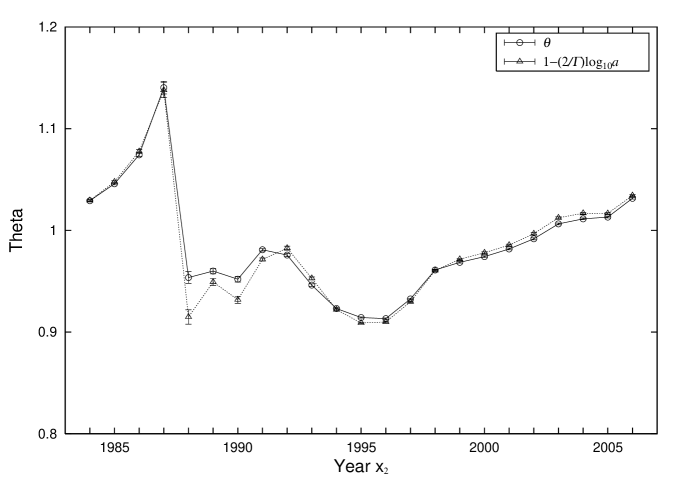

This is an equation between detailed quasi-balance and Pareto’s law in the non-equilibrium dynamical system. We confirm that the empirical data satisfy this correlation in Fig. 10.

4 Conclusion

In this study, we have investigated the dynamical behavior of non-equilibrium system in the large scale region by employing data on the assessed value of land in 1983 – 2006 Japan. We have identified the detailed quasi-balance (5) in the database, and have derived Pareto’s law with varying Pareto index by assuming Gibrat’s law (3). As a result, we have obtained a relation between the change of Pareto index and the parameter in the detailed quasi-balance. The relation (14) has been confirmed in the empirical data nicely.

What does the other parameter mean? Because we demand detailed quasi-balance in the system, the area above the regression line (4) equals the area below it. The two parameters and are, therefore, related to each other. The relation is expressed as

| (15) |

Here is sufficient large number compared with the upper bound () where and are estimated. This is the reason why the two parameters and vary in opposite direction in Fig. 9. The relation (15) is confirmed directly in Fig. 11 where we set to be 10. Consequently, the detailed quasi-balance has one parameter in principle.

We should comment on several separations between and in Fig. 10. An abrupt jump of Pareto index between 1984 and 1986 (2001 and 2002) is observed in Fig. 6. This means that the system changes vigorously in this period, where the symmetry is not represented as the regression line (4). Nevertheless, the dynamical equation (14) is valid in almost all the other quasistatic periods.

For the next step, we should investigate the dynamical behavior in the middle scale region. In Ref. [8], it is reported that Pareto index changes annually whereas the distributions in the middle region are stationary in time by analyzing income data for 1983 – 2001 USA. This phenomenon is explained by the Fokker-Planck equation [9] under two assumptions with respect to the change of income. The middle scale distributions of land prices, however, are not stationary. The distributions do not collapse onto a single curve by the normalization of the average land price. This difference is thought to be caused by the difference between the trend of increasing (decreasing) income and the trend of increasing (decreasing) land price. In order to study the dynamical behavior in the middle scale region, we must identify each peculiar feature of middle scale distributions in the database [10].

Acknowledgments

The author is grateful to Professor V.M. Yakovenko for useful discussions about his work, and to Professor T. Kaizoji for useful comments.

References

- [1] V. Pareto, Cours d’Economique Politique, Macmillan, London, 1897.

-

[2]

Y. Fujiwara, W. Souma, H. Aoyama, T. Kaizoji and M. Aoki,

Physica A321 (2003) 598;

H. Aoyama, W. Souma and Y. Fujiwara, Physica A324 (2003) 352;

Y. Fujiwara, C.D. Guilmi, H. Aoyama, M. Gallegati and W. Souma, Physica A335 (2004) 197;

Y. Fujiwara, H. Aoyama, C.D. Guilmi, W. Souma and M. Gallegati, Physica A344 (2004) 112;

H. Aoyama, Y. Fujiwara and W. Souma, Physica A344 (2004) 117. - [3] R. Gibrat, Les inegalites economiques, Paris, Sirey, 1932.

- [4] A. Ishikawa, Physica A363 (2006) 367.

- [5] T. Kaizoji, Physica A326 (2003) 256.

- [6] The Ministry of Land, Infrastructure and Transport Government of Japan’s World-Wide Web site, http://nlftp.mlit.go.jp/ksj/.

- [7] A. Ishikawa, Annual change of Pareto index dynamically deduced from the law of detailed quasi-balance, physics/0511220.

- [8] A.C. Silva and V.M. Yakovenko, Europhys. Lett. 69 (2005) 304.

- [9] E.M. Lifshitz and L.P. Pitaevskii, Physical Kinetics (Pergamon Press, Oxford, 1981).

- [10] A. Ishikawa, Physica A367 (2006) 425.