Wealth redistribution with finite resources

Abstract

We present a simplified model for the exploitation of finite resources by interacting agents, where each agent receives a random fraction of the available resources. An extremal dynamics ensures that the poorest agent has a chance to change its economic welfare. After a long transient, the system self-organizes into a critical state that maximizes the average performance of each participant. Our model exhibits a new kind of wealth condensation, where very few extremely rich agents are stable in time and the rest stays in the middle class.

pacs:

87.23.Ge, 89.65.Gh, 89.75.Da, 45.70.Ht, 05.65.+bExtended systems showing critical behavior do not need any fine-tuning of a parameter to be in a critical state. In an attempt to explain this behavior, Bak, Tang and Wiesenfeld introduced the concept of self–organized criticality (SOC) BTW87 . In the critical state, there are long-range interactions, by which each part of the system feels the influence of all the others. More precisely, this means that many of the relevant observables in the system follow a power–law or Pareto–Lévy distribution with a non-trivial exponent.

Economics is, by far, one of the more complex extended systems. Economic development has always been considered the driving (or relevant) force in determining the relationships inside a society. Similar to what happens in paleontology Raup86-EG72-GE77-EG88 , it follows a punctuated pattern: Wars, famines, revolutions (and counter-revolutions) are the most evident (and extreme) illustrations of these bursts of historical activity. It is then natural, if nothing else by the force of mere analogy, to look for evidences of critical behavior in economic systems.

In this paper we will concentrate on one particular aspect of economic processes. In recent years a great deal of effort has been devoted to the analysis of economic data. From stock–exchange fluctuations LM99-MS95-Mantegna91 , models of production BCSW93 , size distribution of companies Stanley_ea96 , to the appearance of money Donan2000 , and the effects of controls on the market CVV01 , it has finally been shown that market economy exhibits properties characteristic of a critical system Mandelbrot97-MS97-MS99 .

Here we aim at modeling the competition among different agents (countries, enterprises, etc.) acting in an environment with constant resources. For this reason, we call the present model TWC-model (Total Wealth Conserved model). This restriction has several motivations. On the one hand, it can be argued that our planet is finite and consequently the resources in it are finite. Even though there are resources that are actually renewable, we assume that those are renewed at the expense of others, thus making the totality of available resources constant. On the other hand any study of wealth increase requires understanding the behavior of the reference (conservative) system.

We will model our economy as a one-dimensional lattice, every site of which represents an agent. Agents with closer ties to each other (geographical or otherwise) will be neighbors on the lattice. For simplicity sake we assume periodic boundary conditions. Each agent will be characterized by some wealth-parameter that represents its welfare. The exact choice of this parameter is not straightforward. For instance, if we are thinking of countries in the world economy the GDP, GNP or some function of macroeconomic indicators could be a reasonable choice. In the case of companies, equity, share price or some combination of them with outstanding debt are reasonable candidates. We choose an initial configuration where the wealth is distributed randomly among agents, the wealth of each agent being between 0 and 1.

In the marketplace, all agents strive to improve their situation. In particular the poorest agent is the one feeling the strongest pressure to move up the ladder. Thus, we model this process by an extremal dynamics. At each time step, the poorest country, i.e. the one with the minimum wealth, will take some action to improve its economic state. That is, it will change its production methods, borrow money, increase the percentage of sown fields or take some other measure aiming at increasing its wealth. Since the outcome of any such measure is uncertain, we model this outcome as a random change in the wealth parameter of this country. Moreover, whatever wealth is gained (lost) by the poorest agent will be at the expense of its neighbors and we assume it to be equally divided among its two nearest neighbors. We would like to remark that, apart from conservation, we do not impose any limit on the wealth evolution, so negative values are possible, corresponding to agents having debt rather than wealth. Since a site with negative wealth will most probably be the minimum in the near future, we expect such a site to linger only a few steps in red. In this simplified version of the model, default is not taken into account, that is, any company may stay for ever in debt, albeit with a very low probability.

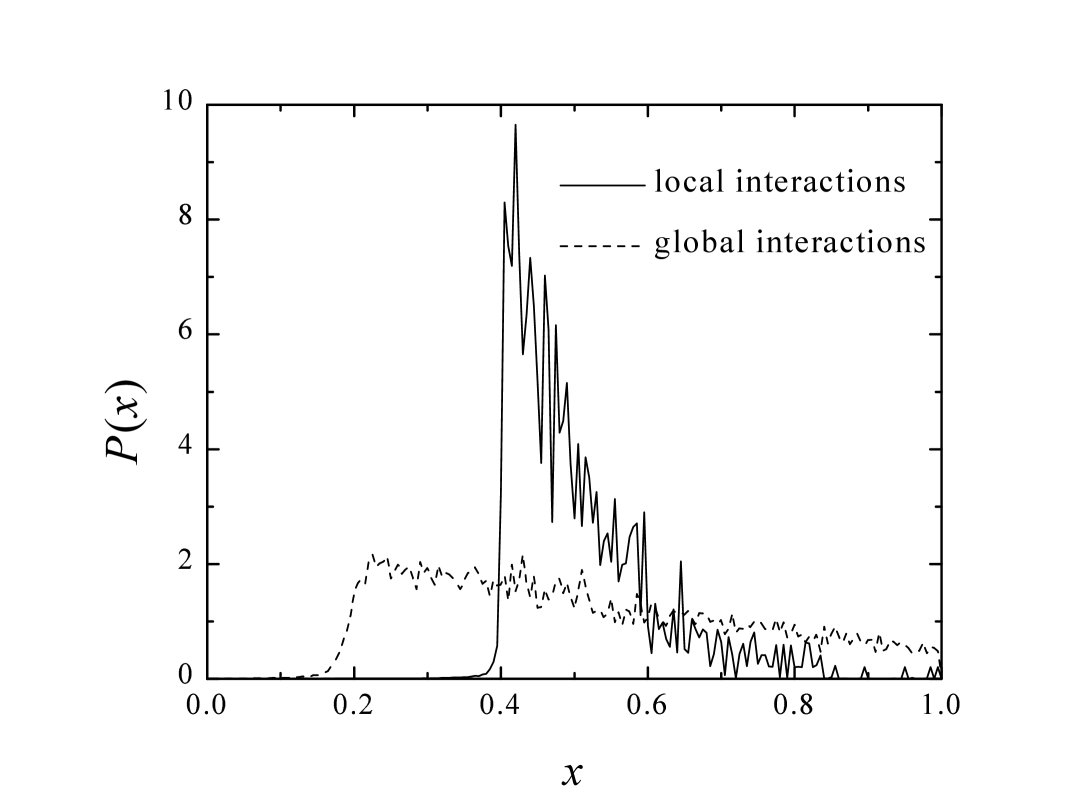

After a relatively long transient the system arrives at a stationary wealth distribution; one typical image of the wealth’s landscape is shown in Fig. 1.

As in other extremal dynamics models the system self-organizes into a state in which almost all agents are beyond a certain threshold, . Above threshold, the distribution of agents is exponential, i.e. there are exponentially few rich agents while the mass of them remain in what we call a middle class. Wealth redistribution is then evident.

Turning our attention back to Fig. 1, we show also the globally coupled (mean field) solution, corresponding to a random choice of sites from which wealth is taken or given to. This mean field solution exhibits a lower threshold and, more strikingly, an almost linear behavior beyond threshold. This departs from standard extremal dynamics models where both distributions are rather uniform. Furthermore, the distribution of avalanches follows a power law with the same exponent as the Bak-Sneppen universality class.

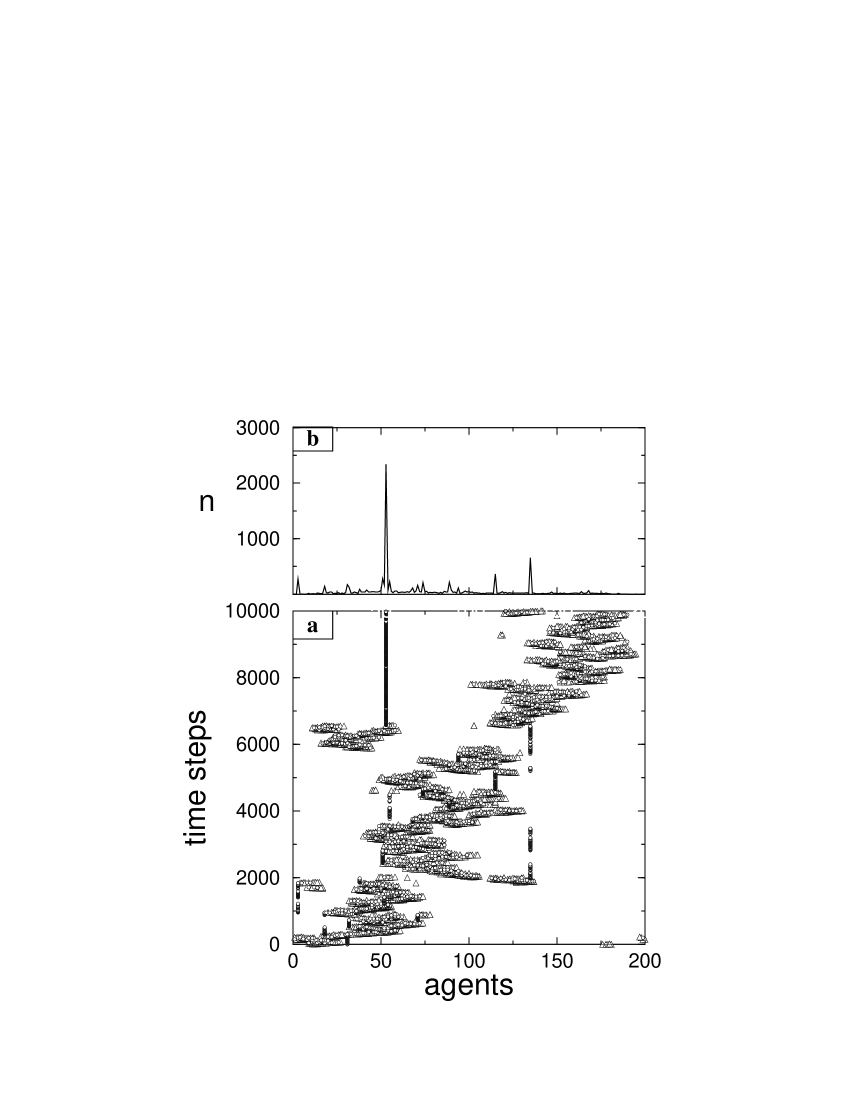

In Fig. 2a we show the temporal evolution, in the SOC state, of the position of the systems minimum and maximum wealth. We can see that, while the site of minimum wealth is changing continuously, generating avalanches of wealth redistribution among neighbors, the richest site is stable over long periods of time. Indeed, when affected by an avalanche it can recover its status after a short time. These brief interruptions, usually produced by short-lived avalanches, are reflected as gaps in the maxima lines.

In Fig. 2b we present the statistics of the number of time-steps a site spends as absolute maximum. Clearly only a few agents have spent most of the time as maxima, while the rest lurks somewhere in the middle class. We have also observed that not only the absolute maximum is stable, but also a privileged group, whose wealth is around the same value of the maximum, remains in its prosperous position for quite a while. The composition and hierarchy of this privileged group is barely affected by the avalanches that produce the abovementioned gaps.

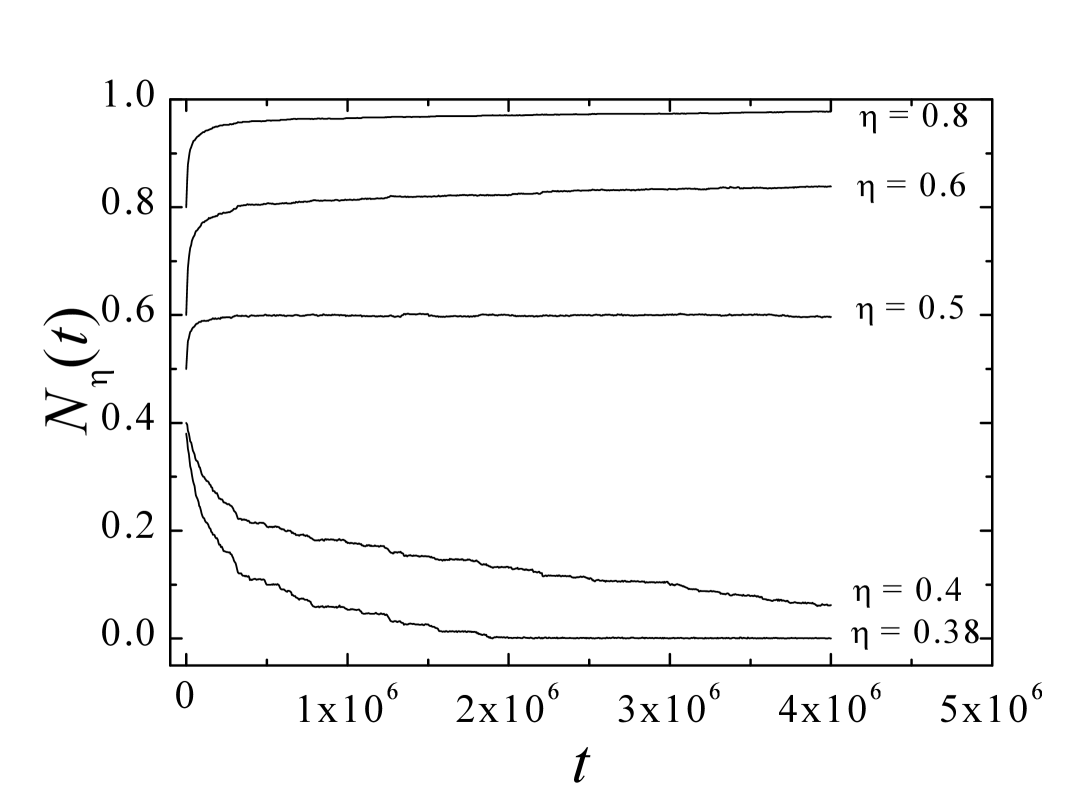

So far we have focused our attention on the final state of the economy, that is, on the wealth distribution in the self-organized state. Let us now devote some time to discuss the transient. In particular, we are interested in understanding the process of wealth accumulation. In Fig. 3 we show the time evolution of , the fraction of the agents whose wealth , for different values of . Slowly but steadily, for values of these fractions decrease, thus showing the speed of wealth redistribution in the system. As expected, the higher the value of , the slower the progress. As can be clearly seen in the picture, all fractions with converge to zero, while for the fraction grows quickly to its asymptotic value. When the value of is near 1, the fraction quickly converges to 1, reflecting the existence of small privileged groups. We have also observed that the probability of one agent becoming wealthier in a time step decreases as time goes by, to finally converge to a finite value, . Both effects are a consequence of the fact that the total wealth to be distributed is finite.

From these results several conclusions may be drawn. First and foremost, resource conservation leads to an exponential wealth distribution, where the very few extremely rich agents are stable in time and the rest is just above threshold. This is tantamount to saying that the invisible hand Adam of redistribution works only among the middle class. Neither trade nor cost of debt, returns or tax on wealth is explicitly included in this model. This reinforces the role played by geography. As can be seen in Fig. 1, the a-geographic mean field solution generates a completely different wealth distribution. Indeed, this globally coupled solution can be compared with the results obtained in Refs. BM2000 ; Burda2001 for stochastic multiplicative market models, and reinforces the conclusions presented in Ref. HS2001 concerning wealth condensation with a finite number of agents. Secondly, the economic progress in society is steady, even if slow.

At this point it is instructive to compare these results with Pareto’s law pareto , which suggests that individual wealth follows a power law distribution. Our model exhibits exponential distribution in the local limit and a particular power law distribution (with an exponent close to one) in the mean field limit. As explained above, the later case corresponds to global interactions, and in this case there is also a higher number of poorer agents, because the threshold is much lower than in the local interaction case. In brief, power laws seem to be a consequence of globalization in the market and favor a wide spectrum of wealth distribution, i.e. increase inequalities. In a sense, our local model corresponds to a kind of feudal world, where local barons maintain their dominance for long periods of time.

Summarizing, the model presented here provides a simple description of wealth redistribution in the early stages of human economic history, and indicates some of the possible driving forces beyond the market expansions that influenced this redistribution process. We believe these conclusions may be of interest in view of the present debate over the goods and evils of globalization.

J.R.I. and S.P. acknowledge support from Conselho Nacional de Desenvolvimento Científico e Tecnológico (CNPq, Brazil); J.R.I also acknowledges the hospitality and support of Université Paris-Sud, Orsay, France, and Facultad de Ciencias, Universidad de Cantabria, Santander, Spain. We acknowledge partial support from SETCYP (Argentina) and CAPES (Brazil) through the Argentine-Brazilian Cooperation Agreement BR 18/00, and G.A. thanks the hospitality of the Instituto de Física, Universidade Federal do Rio Grande do Sul, Porto Alegre, Brazil.

References

- (1) P. Bak, C. Tang, and K. Wiesenfeld, Phys. Rev. Lett. 59, 381 (1987); Phys. Rev. A 38, 364 (1988); P. Bak and K. Sneppen, Phys. Rev. Lett. 71, 4083 (1993).

- (2) M. D. Raup, Science 231, 1528 (1986); N. Eldredge and S. J. Gould, in Models in Paleobiology, (Freeman, Cooper & Co., San Francisco, 1972); N. Eldredge and S. J. Gould, Nature 332, 211 (1988).

- (3) T. Lux and M. Marchesi, Nature 397, 498 (1999); R. N. Mantegna and H. E. Stanley, Nature 376, 46 (1995).

- (4) P. Bak, K. Chen, J. A. Scheinkman, and M. Woodford, Ricerche Economiche 47, 3 (1993).

- (5) M. H. R. Stanley, L. A. N. Amaral, S. V. Buldyrev, S. Havlin, H. Leschhorn, P. Maass, M. A. Salinger, and H. E. Stanley, “Scaling behaviour in the growth of companies” Nature 379, 804 (1996).

- (6) R. Donangelo and K. Sneppen, Physica A 276, 272 (2000)

- (7) G. Cuniberti, A. Valleriani, and J. L. Vega, Quantitative Finance 1, 332 (2001).

- (8) B. B. Mandelbrot, Fractal and Scaling in Finance, (Springer, New York, 1997); R. N. Mantegna and H. E. Stanley, J. Stat. Phys. 89, 469 (1997).

- (9) J.P.Bouchaud and M. Mézard, Physica A 282, 536 (2000).

- (10) Z. Burda, D. Johnston, J. Jurkiewicz, M. Kaminski, M.A. Nowak, G. Papp and I. Zahed, cond-mat/0101068 (2001).

- (11) Z.F. Huang and S. Solomon, Physica A 294, 503 (2001).

- (12) A. Smith, An Inquiry into the Nature and Causes of the Wealth of Nations, (Random House, New York, 1937) (First Edition 1776).

- (13) V. Pareto, Cours d’économie politique, reprinted as a volume Oeuvres complètes (Droz, Geneva 1896-1965).