Stochastic volatility and leverage effect

Abstract

We prove that a wide class of correlated stochastic volatility models exactly measure an empirical fact in which past returns are anticorrelated with future volatilities: the so-called “leverage effect”. This quantitative measure allows us to fully estimate all parameters involved and it will entail a deeper study on correlated stochastic volatility models with practical applications on option pricing and risk management.

pacs:

89.65.Gh, 02.50.Ey, 05.40.Jc, 05.45.TpThe multiplicative diffusion process known as the geometric Brownian motion (GBM) has been widely accepted as one of the most universal models for speculative markets. The model, started out by Bachelier in 1900 as an ordinary random walk and redefined in its final version by Osborne in 1959 cootner , presupposes a constant “volatility” which is equivalent to a constant diffusion coefficient . However, and especially after the 1987 crash, there seems to be ample empirical evidence, given by the so-called “stylized facts”, that the assumption of constant volatility does not properly account for important features of markets. Some relevant examples of stylized facts are the “leverage” and “smile” effects and the skewness and “fat tails” in probability distributions cont .

One of the main ideas that has come out to explain those features is that the market dynamics has intrinsically changed in the sense that volatility is no longer constant. It is not a function of time either (as might be inferred by the evidence of nonstationarity in financial time series lo ) but a random variable. In its most general form one therefore assumes that the volatility is a function of a random process , i.e., . We could make an analogy from physics saying that speculative prices evolve in a “random medium” determined by a random diffusion coefficient. Most of the stochastic volatility (SV) models presented up to date suppose that is itself a diffusion process that may or may not be correlated with price and different models differ from each other basically in the form of the function ghysels ; fouquebook .

As mentioned above, the hypothesis of stochastic volatility (SV) has been suggested to explain significant peculiarities observed in real markets. Thus, the smile effect, related to the implicit volatility in option prices, has been thoroughly studied both qualitatively and quantitatively smile ; heston . Other features such as leverage and long tails are less studied and some works on SV only address to them from a qualitative point of view fouque while others measure them by giving numerical coefficients, based on ARCH-GARCH models, for kurtosis and skewness englepat . However, the time evolution and structure of the leverage and tails have never been investigated. Our main objective here is to prove that the leverage effect can be quantitatively explained by a wide class of correlated SV models. This will allow us to overturn the main objection against SV models: the impossibility of fitting all parameters appearing in these models fouquebook ; fouque which, in turn, opens the door to simulations of real markets with far reaching practical consequences on option pricing and risk management.

We recall that the leverage effect has its origin in the observation that volatility seems to be negatively correlated with stock returns which, in continuous time finance and in terms of speculative prices , are defined by . The first explanation to this empirical fact was given by Black black and Christie christie in the sense that negative returns increase financial leverage which extend the risk of the company and therefore its volatility. Hence the name of “leverage effect”. Nevertheless, the cause of this effect is still unclear since another explanation is just the contrary, that is, an increase of volatility makes the stock riskier which produces a fall of demand and the price drops ghysels .

In a very recent paper, Bouchaud et al. bouchaud have performed a complete empirical study of the leverage effect for both individual stocks and indices using daily data. The volatility-return (negative) correlation is clearly shown to have a definite direction in time – a very confusing fact in the literature – since correlations are shown to be between future volatilities and past returns. Bouchaud et al. conclusively prove from data that the negative correlation decays exponentially in time, faster for indices than for individual stocks bouchaud .

In this letter, we present a theoretical study on these correlations and show that a wide class of SV models completely explain the leverage effect, both qualitatively and quantitatively, in complete agreement with experimental observations. The starting point is the GBM model:

| (1) |

where is the drift and is a random volatility and is a diffusion process:

| (2) |

In these equations are Wiener processes, i.e., where are zero-mean Gaussian white noises with cross-correlation given by

| (3) |

. As is common in finance, Eqs. (1)-(2) are interpreted in the sense of Ito and for the rest of the paper we will follow Ito convention perello1 .

Bouchaud et al. bouchaud , quantify the leverage effect by means of a leverage correlation function defined by

| (4) |

where

| (5) |

is the zero-mean return and is a convenient normalization coefficient. Bouchaud et al. have analyzed a large amount of daily relative changes for either market indices and stock share prices and find that bouchaud

| (6) |

. Hence, there is a negative correlation with an exponential time decay between future volatility and past returns changes but no correlation is found between past volatility and future price changes. In this way, they provide a sort of causality to the leverage effect which, to our knowledge, has never been previously mentioned in the literature ghysels ; fouquebook .

Let us sketch how correlated SV models are able to exactly reproduce this result. We first combine Eqs. (1) and (5) to produce . Note that when Ito’s rules tell us that is uncorrelated with the rest of terms then, recalling that , we have if . On the other hand, when , is uncorrelated with the rest and, since , we conclude that

| (7) |

where is the Heaviside step function and . Note that we have proved the existence of correlations between future volatilities and past returns but not vice-versa. Note also that this have been proved independently of the underlying volatility process (which needs not to be a diffusion process) and of the specific form of in terms of .

Suppose now that is a diffusion process given by Eq. (2). As is well known any pair of correlated Wiener process, such as and , satisfy the identity , where is a Wiener process independent of (therefore, is independent of ). Substituting this identity into Eq. (7) we get in terms of the average . This average can be calculated by means of Novikov’s theorem novikov with the result pm

| (8) |

where and is the functional derivative of with respect to novikov .

There is a wide consensus on volatility being “mean reverting”. This means that there exists a normal level of volatility footnote to which volatility will eventually return englepat . For a general SV model such as (1)-(2), the presence of mean-reversion implies restrictions on the form of the drift coefficient . In order to include this experimental fact in the model, the simplest choice is to assume that is a linear function. That is,

| (9) |

where . The formal solution to this equation in the stationary state reads

from which we get pm

Substituting this expression into Eq. (8) yields

| (10) |

where

| (11) |

and

| (12) |

In consequence, any SV model of the form given by Eqs. (1) and (9) and whose function does not increase faster than as , satisfies an exponentially decaying leverage as expressed by Eq. (6). Moreover, if is an increasing function of with definite sign and is positive definite (or is decreasing and is negative) we see from Eq. (10) that the correlation coefficient must be negative and driving noises and are anticorrelated. Eqs. (10)-(12) constitute the main result of the paper.

The exact form of will depend on the expression of which in turn will depend on the SV model chosen. Within diffusion theory, as is the case of Eq. (9), there are basically three different SV models fouquebook : 1) The Ornstein-Uhlenbeck (OU) model where and (a positive constant) stein , 2) the exponential Ornstein-Uhlenbeck (expOU) model where and fouque and 3) the Cox-Ingersoll-Ross (CIR) model where and heston . For all these models the leverage function has the form given by Eq. (10). In the OU model and in the CIR model (the latter with zero mean-reversion, i.e., ) the leverage function is respectively given by pm

| (13) |

| (14) |

while for the expOU model we have

| (15) |

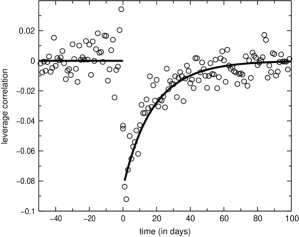

In Fig. 1 we show the leverage effect for the Dow-Jones daily index (1900-2000) and plot the leverage function for the OU model.

Any market model, besides being able to reproduce the market dynamics, must provide a systematic way of evaluating its parameters. Almost all current SV models have four parameters to estimate: , , , and . To our knowledge, all works on SV models presented up till now are able to evaluate only two of them. Thus, for instance, Fouque et al. fouque estimate and from the empirical second and fourth moment of daily data but they can’t give a clear estimation of and . This constitutes the main criticism to SV models, say, their inability to estimate all parameters involved. This situation changes completely when one measures leverage. Indeed, and are obtained, as usual, from the empirical second and fourth moment. Next, by adjusting to leverage empirical data we estimate . Moreover, comparing the theoretical and empirical leverage at , , we finally obtain . Following this procedure, for the Dow-Jones daily index and using the OU model, we have estimated , , , and .

As an illustration we have simulated, using Eqs. (1) and (9), the OU resulting process with the parameters estimated above. We follow the random dynamics of the daily changes of the zero-mean return and compare it with the empirical Dow-Jones time series during one trading year. We have also simulated the geometric Brownian motion assuming a constant volatility whose value is directly estimated from Dow-Jones one-century data. We present these results in Fig. 2 and observe that GBM cannot describe either the largest or the smallest fluctuations of daily returns. We nonetheless see in the figure that the SV model chosen describes periods of high volatility together with periods of very low volatility, resulting in a more similar trajectory to the Dow-Jones index than that of the GBM. This is quite remarkable, because we have simulated last year trajectory using all past data (one century) of the Dow-Jones index thus showing the stability of parameters.

These results may encourage to deepen in the study of statistical properties of SV models showing leverage. Several models have been presented in the literature without being able to discern which is the more realistic one. Now, thanks to leverage correlation, it is possible to estimate all parameters involved in SV models. This will allow us to confront in detail different models with the empirical statistical properties of markets. Finally, a better knowledge of SV models has non trivial consequences on option pricing (since classical Black-Scholes method is still suitable in SV models smile ; heston ) and, more generally, on risk management.

Acknowledgements.

This work has been supported in part by Dirección General de Investigación under contract No. BFM2000-0795, by Generalitat de Catalunya under contract No. 2000 SGR-00023. We thank Marian Bogunya for useful suggestions and careful reading of the manuscript.References

- (1) Corresponding author, email address: jaume@ffn.ub.es

- (2) P. H. Cootner ed., The Random Character of Stock Market Prices (MIT Press, Cambridge, MA, 1964).

- (3) R. Cont, Quantitative Finance 1, 223 (2001).

- (4) J. Y. Campbell, A. W. Lo, and A. C. MacKinlay, The Econometrics of Financial Markets (Princeton University Press, Princeton, 1997).

- (5) E. Ghysels, A. C. Harvey, and E. Renault, in G. S. Mandala, and C. R. Rao eds. Statistical Methods in Finance. Handbook of Statistics Vol. 14 (North-Holland, Amsterdam, 1996).

- (6) J-P. Fouque, G. Papanicolaou, and K. R. Sircar, Derivatives in Financial Markets with Stochastic Volatility (Cambridge University Press, Cambridge, 2000).

- (7) J. C. Hull and A. White, J. Finance 42, 281 (1987); L. Scott, J. Financial and Quantitative Analysis 22, 419 (1987); J. Wiggins, J. Financial Economics 19, 351 (1987).

- (8) S. L. Heston, Rev. Financial Studies 6, 327 (1993).

- (9) J-P. Fouque, G. Papanicolaou, and K. R. Sircar, Int. J. Theoretical and Applied Finance 3, 101 (2000).

- (10) R. Engle and A. Patton, Quantitative Finance 1, 237 (2001).

- (11) F. Black, in Proceedings of the 1976 American Statistical association, Business and Economical Statistics Section (American Statistical Association, Alexandria, VA, 1976).

- (12) A. A. Christie, J. Financ. Econom. 10, 407 (1982).

- (13) J-P. Bouchaud, A. Matacz, and M. Potters, Phys. Rev Lett. 87, 228701 (2001).

- (14) J. Perelló, J. M. Porrà, M. Montero, and J. Masoliver, Physica A 278, 260 (2000).

- (15) E. A. Novikov, Soviet Phys. JETP 20, 1290 (1965).

- (16) J. Perelló and J. Masoliver, in preparation (2002).

- (17) The normal level of volatility is usually defined by (see englepat ).

- (18) E. M. Stein, and J. C. Stein, Rev. Financial Studies 4, 727 (1991).