[table]capposition=top

On Finite Time Span Estimators of Parameters for Ornstein-Uhlenbeck Processes

Abstract

We study the bias and the mean-squared error of the maximum likelihood estimators (MLE) of parameters associated with a two-parameter mean-reverting process for a finite time . Using the likelihood ratio process, we derive the expressions for MLEs, then compute the bias and the MSE via the change of measure and Ito’s formula. We apply the derived expressions to the general Ornstein-Uhlenbeck process, where the bias and the MSE are numerically computed through a joint moment-generating function of key functionals of the O–U process. A numerical study is provided to illustrate the behaviour of bias and the MSE for the MLE of the mean-reverting speed parameter.

1 Introduction

We focus on the univariate two-parameter mean-reverting process , which is defined through the following stochastic differential equation (SDE),

| (1) |

The two parameters and are to be estimated from the following sets of observations in open intervals and , respectively. The standard Brownian motion is defined on a probability space , with being a filtration generated by . and are measurable processes with respect to , where is the family of sigma-algebras generated by .

The stochastic process driven by SDE in (1) appears frequently in mathematical finance. For example, if and , then becomes an Ornstein-Uhlenbeck process, which was introduced in finance in [41]. The work was extended to more general type of SDE in [7], known as the CKLS (Chan-Karolyi-Longstaff-Sanders) process, with and , which is defined as

| (2) |

Note that from (2), if and , then this leads to a CIR (Cox-Ingersoll-Ross) process in [9]. These stochastic processes were widely used for modelling the term structure of interest rates, and for volatility estimation in a finite time span; see [35] and [21].

Several studies were made based on the SDE in (1). Theoretical results on the existence of strong and weak solutions were studied in the monographs in [23] and [24], and statistical inferences for stochastic models described by SDE driven by Brownian motion have been presented in the monographs by [1], [36], [17], [23], [4], [18], [39] and [13]. The asymptotic properties of the estimators for discretised SDE-driven process in (1) under various discretisation schemes can be found in [14], while the asymptotic properties of sequential estimators for discretised O-U process have been studied in [20], [22], and [32]. In continuous time, the asymptotic properties of the maximum likelihood estimators (MLEs) for the CKLS process in (2) were studied in [38], [14], [6], [31], [16], [26]. In addition, the computation and asymptotic properties of the pseudo moment estimators were studied in [27], while a least squares approach has been studied in [12] for a fractional Ornstein-Uhlenbeck processes, later extended to non-ergodic O–U processes in [3], [10] and [11].

In this paper, we study the bias and the mean-squared error (MSE) of the maximum likelihood estimators of , which are defined as

with the assumption that the sample size is fixed.

Studies on bias of estimators in autoregressive processes began from the classical study of the estimation of the correlation coefficient. The analytical calculation of the bias in the correlation estimator was first explored in [25] and [15] in a stationary AR(1) model. In particular, [15] highlighted the limitations of asymptotic expansions when is near unity, due to the skewness in the distribution of the estimator and the slow decay of higher-order terms. These concerns suggest that alternative approaches may be necessary to improve the accuracy of bias corrections. For a Gaussian stationary AR(1) process, the overview of asymptotics of least squares estimators for three parameters, including the bias corrections for the slope parameter was provided in [33]. These studies have triggered further developments for bias analysis of various types of estimators, including the maximum likelihood estimators (see [37], [8]). In the case of continuous time, the asymptotic expansions for the bias and MSE of the maximum likelihood estimators analytically for the SDE in (1), in particular for O–U and CIR processes, have been studied in [40]. The computational challenges arising from the dependence of the mean reversion parameter estimator on the initial value and discretisation frequency, as well as its slow convergence for small parameter values, have been examined in [2].

We will derive an integral transform using the change of measure and Ito’s formula to compute and for fixed under the assumptions made in (1). This approach allows us to derive expansions for cases as or at , where is a constant. When referring to the study in [32], the first-order asymptotic approximations for and could be misleading for moderate values of or small values of . The bias of the MLE can be used in the bias correction to reduce the mean-squared error of the MLE.

This paper is organised as follows. In Section 2, we formulate some general results studied in [32] that are valid within the framework of the mean-reverting process in (1). These results provides the basis for studying the fixed sample properties of the MLE for the Ornstein-Uhlenbeck (O-U) process. In Section 3, we study the properties of MLEs to provide the analytical formulae and numerical illustrations for the bias and the MSE of the MLEs, and its modification using the moment generating functions (MGFs). The derivations of these MGFs are included in the Appendix. In Section 4, we provide a numerical study to illustrate the behaviour of bias and MSE for a finite sample size . Section 5 concludes this paper.

2 Maximum Likelihood Estimators

In this section, we derive the expressions of the MLEs for the two parameters and , and discuss their properties.

2.1 Notations and Assumptions

We assume be the probability measure generated by the process in (1), with representing the expectation with respect to . In addition, assume that for any and , where and are open intervals in , the following conditions hold:

| (3) | |||

| (4) |

While these conditions hold, the measures are equivalent, and this indicates that for any parameters and ,

| (5) |

where is an indicator function of an event , and is a likelihood ratio process, also known as Radon-Nikodym derivative.

Under assumptions from [23], we have

| (6) |

To simplify (6), we introduce the following notations.

| (7) | ||||

| (8) | ||||

| (9) |

To align with (1),

where is the quadratic characteristic of the local martingale with respect to the measure and the filtration . Hence, the likelihood ratio process can be written in the following form:

| (10) |

2.2 Maximum Likelihood Estimators

(A) When is known, we first need to solve the following equation:

| (11) |

and hence, the maximum likelihood estimator of is

| (12) |

Note, that using (1), we may obtain the following useful representation:

| (13) |

(B) When is known, with , we need to solve the following equation:

| (14) |

and hence, the maximum likelihood estimator of is

| (15) |

For simpler representation, we denote

| (16) | ||||

| (17) | ||||

| (18) |

where is the quadratic characteristic of the local martingale with respect to the measure , and the filtration . Using these notations, we can rewrite in the following form:

| (19) |

(C) When both and are unknown, the MLEs can be found by solving the system of two equations with respect to and ,

| (20) |

The following relations between the MLEs and are obtained:

| (21) | ||||

| (22) |

Now, note that in the SDE in (1), we have

| (23) |

Hence, as , if

| (24) |

where the conditions in (24) hold when is ergodic, e.g. in the case of CKLS model in (2), then we obtain a strongly consistent estimator ,

| (25) |

Using , we may obtain the modified MLE of :

| (26) |

This MLE is connected to the previous MLE in (13) via the following relation:

| (27) |

If is a strongly consistent estimator, then as , it can be expected that

This will be shown in Section 3, that in the case of an ergodic O–U process, the estimators and are asymptotically efficient.

2.3 Properties of MLEs

Using the model in (1), we define Theorems 1 and 2 on general properties of MLEs, and in (13) and (19), assuming one of the parameters is known. These theorems are reformulations of Theorem 1 from the study in [32] in the case of model (1).

Theorem 1. Assume .

-

a)

For , let

Then,

-

b)

Let and for some . Then,

-

c)

Let for some . Then,

-

d)

Let for some . Then,

-

e)

Let and for some . Then, for any -measurable integrable estimator ,

(28) which is the Cramer-Rao lower bound for .

-

f)

If there exists a constant , such that , then, for ,

Theorem 2. Assume is fixed, and .

-

a)

For , let

Then,

-

b)

Let and for some . Then,

-

c)

Let for some . Then,

-

d)

Let for some . Then,

-

e)

Let and for some . Then, for any -measurable estimator ,

Remarks

-

1.

The Cramer-Rao lower bound in Theorem 1(e) was considered in [24] under more general assumptions.

-

2.

For a case when the explicit formula for the Laplace transform , is known, then the negative moments can be obtained using the following formula:

where is a gamma function, defined as

3 The O-U Process and Results

For this section, we consider a special case of the (1), when the process is defined by the SDE with and ,

| (29) |

which is an O-U process. We further study the properties of the MLEs described in Section 2, along with a brief numerical result based on this special case.

3.1 General Properties of O-U Process

To simplify notations in our work, we consider the case . However, the results for general can be obtained by simple rescaling. As , when , the process is strongly ergodic, and

A very well-known explicit solution for the SDE in (29) is given by

and this indicates that is a Gaussian process with the following moments:

From (29), the integrated O-U process is defined as

| (30) |

and the moments of the process and are

3.2 Properties of the MLE and

For the case in the process in (29), by definitions in (16), (17), we obtain

and hence, the MLE in (13) is represented as:

| (31) |

This indicates that the bias and the mean-squared errors are

| (32) | ||||

| (33) |

As , we can easily obtain the result from (31), that . In addition, by Theorem 2(e) in Section 2.3 , the Cramer-Rao lower bound for any estimator was

and since and , it can be shown that the MLE is the most efficient estimator among all other unbiased estimators.

Now, with the estimator from (25), for the case of the O-U process, the estimator is expressed as

Note that this estimator follows a normal distribution, and does not need the knowledge of . However, considering this estimator in terms of the integrated O-U process in (30) and its moments,

| (34) |

and hence, the mean and the variance are

| (35) | ||||

| (36) | ||||

| (37) |

Thus, the estimator is asymptotically efficient amongst all other unbiased estimators. Also, since and as , the estimator is a strongly consistent estimator of .

3.3 Properties of the MLE

For the case of O-U process in (29) with , two integrals and from (8) and (7) are expressed as

| (38) | ||||

| (39) |

where is expressed after applying the Ito’s formula. Using (38) and (39) and (13), the MLE is

| (40) |

Now, the distribution of in the case of the O-U process can be defined through the cumulative distribution function,

which leads to looking into the distribution of , such that

The moment generating function (MGF) of the random variable can be found through the joint moment-generating function of the random variables . The explicit formula for the joint MGF is given by

| (41) |

with .

By finding the MGF of the random variable through , one can numerically find through a proper inversion formula, such as the Gaver-Stehfest algorithm in [19]. Other methods include considering the analytical continuation of to the region of complex values of the parameter , and use techniques for numerical inversion of Fourier transform.

By Theorem 1 in Section 2.3, it is required to use the Laplace transform of to find the bias and the mean-squared error of . The Laplace transform is defined below.

Proposition 1. Let be an O–U process with , , . Then for ,

| (42) | |||

where . The above result was presented in [29] with , including non-ergodic case as well, and the result has been used in [28] and [30] for finding asymptotic expansions of bias and MSE of for two cases: and , see details in [32].

Note that in the case when and , we have , and through the former formulas presented, a version of the Cameron-Martin formula in [5] can be obtained, which is expressed as:

| (43) |

Now, using , all moments of can be calculated. Since

| (44) |

and using Theorem 1 in Section 2.3, the bias and the MSE can be obtained.

| (45) | ||||

| (46) |

These calculations can be easily performed using mathematical computation programs such as Wolfram Mathematica. Alternatively, in general, the moments of can be calculated through the use of the distribution of , which involves additional integrations, see [39] for example.

is a strongly consistent estimator. The non-asymptotic result of the MSE is obtained through the Cramer-Rao lower bound for any estimator in (28), where

which can be obtained directly from (29), or by finding .

For the case when ,

which leads to the following result:

Using Theorem 1(c) in Section 2.3, the bias is

| (47) |

and also, since

using Theorem 1(d) in Section 2.3, the MSE is

| (48) |

The asymptotic expansions for bias and MSE of in (47) and (48) for cases when or are of interest in the discipline of econometrics, see [34] for example. Using (42), it can be seen that for ,

| (49) | ||||

| (50) |

where and . Similar arguments can be applied to obtain the second order asymptotic expansions for and for the case when , where is a constant.

3.4 Properties of the MLE

Using (13), the modified MLE estimator is expressed as

| (51) |

To calculate the bias and the mean-squared error of numerically, the joint MGF of random vector is used, i.e.)

| (52) |

For this MGF, we again adopt the tools from Wolfram Mathematica, as it is reasonably fast for calculating the bias and the MSE of , see Appendix. The following formula can be used for calculating moments of :

| (53) |

Through the formula in (53), assuming , we have

and similar formulas can be used to calculate and higher moments of . Now, from (27), since and

we get the following relation:

| (54) |

and through (54), it can be seen that is a strongly consistent estimator, since

and in the ergodic case, we get

It can also be shown that as ,

and hence, is asymptotically the most efficient estimator among other unbiased estimators.

4 Numerical Results

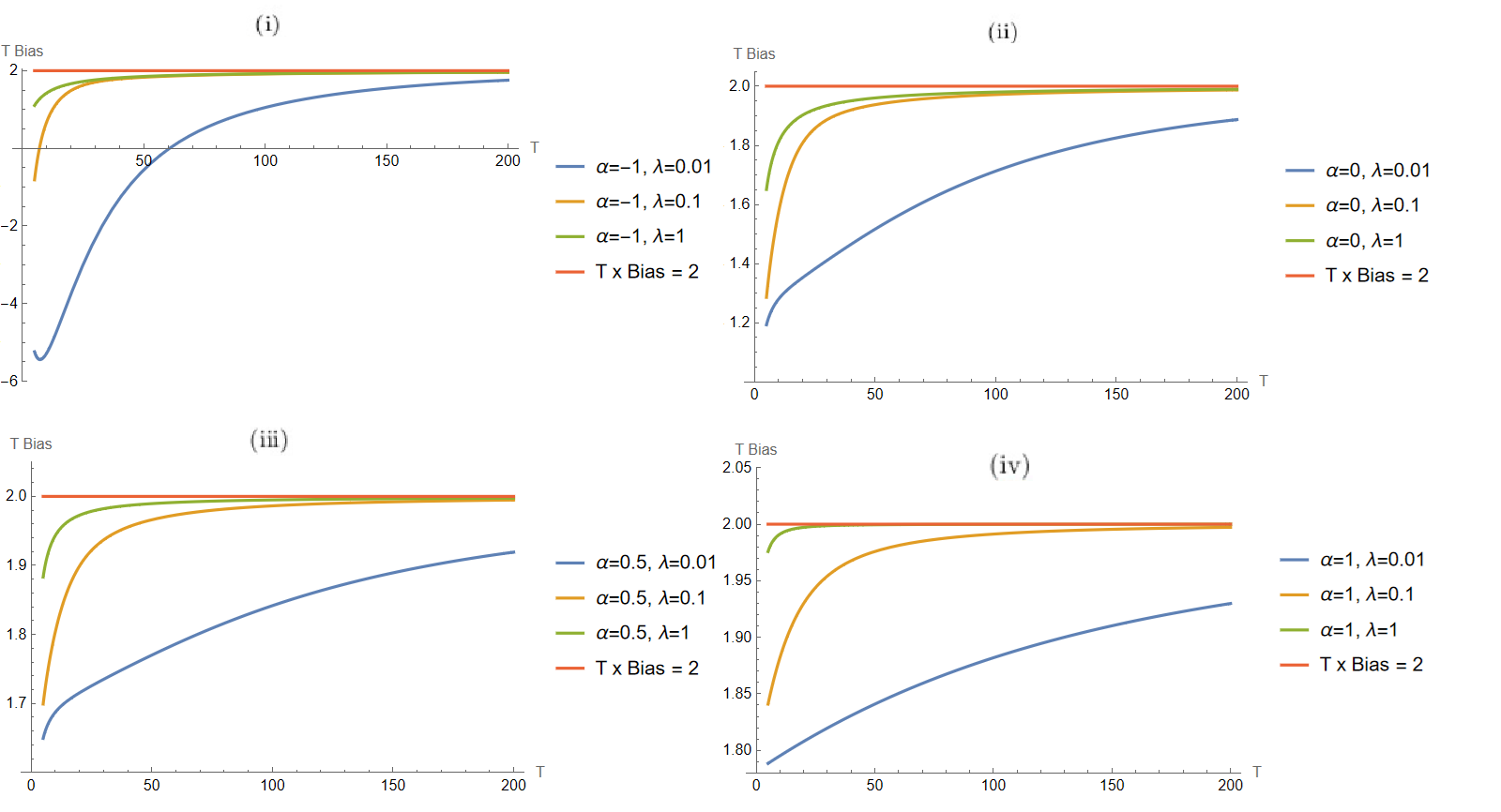

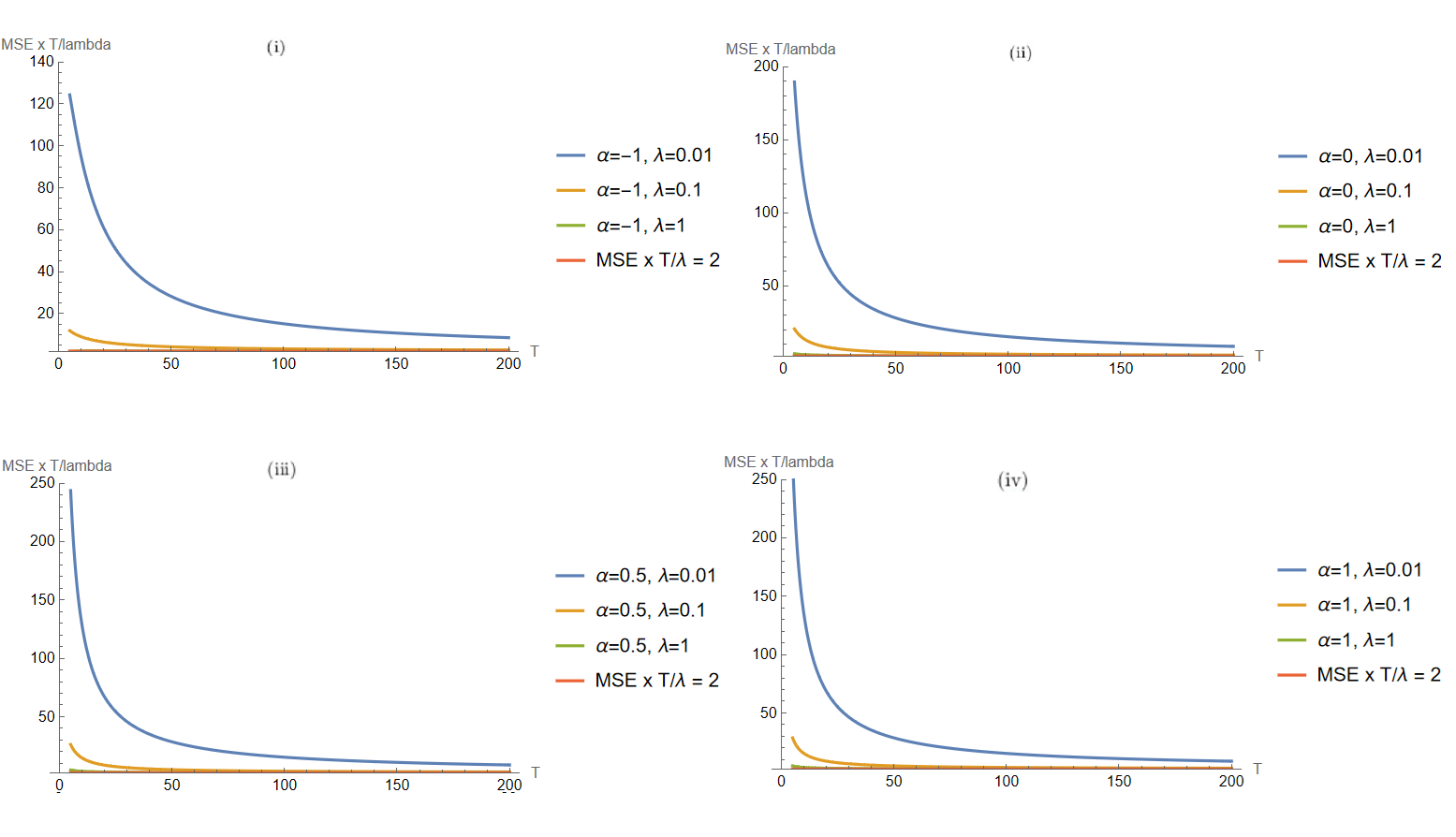

In this section, we provide some graphical illustrations for the bias and the mean-squared error of in (45) and (46). For ergodic cases, using the facts in (47) and (48), we present two following functions:

so that as , two functions approach to 2. We assume that and .

By Wolfram Mathematica, (45) and (46) are used to approximate the bias and the mean-squared error numerically. Figures 1 and 2 depict bias and MSE in terms of two functions and across varying sample sizes , and Table 1 in the Appendix provides a comparison of bias and MSE. Across all values of and , the bias tends to decrease as increases, indicating better estimation with larger sample sizes. At smaller values of , particularly at , the MLE is underestimating , while for all other combinations, we see positive bias. The gap between bias values across different and positive shrinks, indicating that increasing reduces the dependence on . The bias decreases at a faster rate as both and increase.

Looking into the MSEs, across all parameter settings, MSE decreases as increases, reflecting that larger sample sizes leads to more precise estimates. Larger values tend to have higher MSE, particularly for small , indicating that it leads to higher estimation error if the speed of mean-reversion is faster. At large , the impact of both and on MSE is reduced, suggesting that sample size is the dominant factor in estimation accuracy.

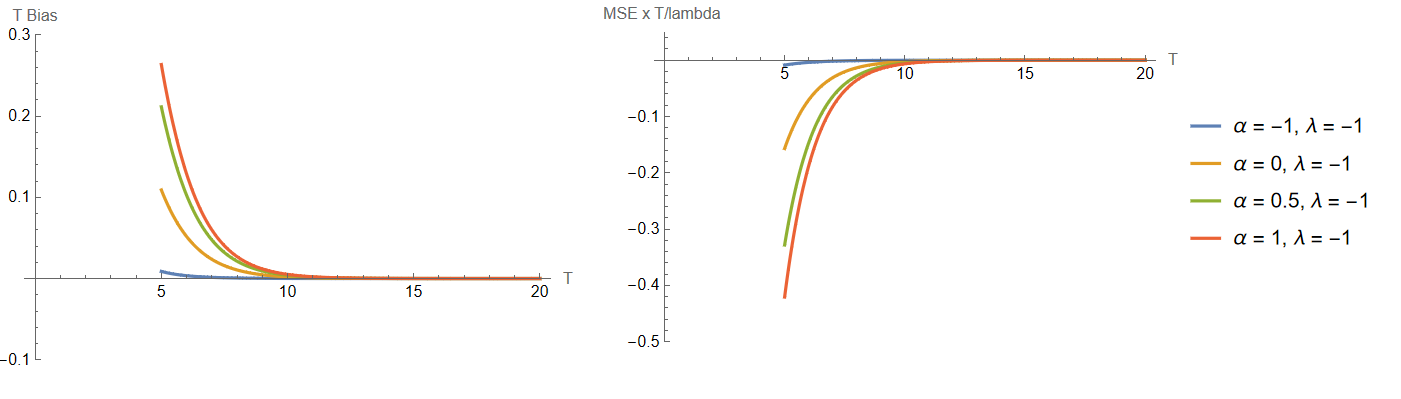

In contrast, the non-ergodic case displays qualitatively different behaviour. When , we see that both and converge to zero, indicating a different scaling regime for the estimation error. Although the estimator no longer exhibits consistency in the classical ergodic sense, both scaled quantities decay rapidly as increases. As shown in Figure 3, the resulting curves are nearly indistinguishable for across different values of , suggesting that the long-run mean has limited influence in this unstable regime.

5 Conclusion

This paper examined the theoretical properties of maximum likelihood estimators (MLEs) for a univariate, two-parameter mean-reverting process. Using the likelihood ratio process, we derived the expressions for MLEs of the parameters in cases when , , or both parameters were unknown, and formulated the general expressions for the bias and mean-squared errors (MSEs) of parameters.

From the general setting in (1), we simplified our model to follow an Ornstein-Uhlenbeck (O-U) process, with a constant volatility . We derived the MLE of , the parameter representing the long-term mean, along with its bias and the MSE. For , the parameter representing the speed of mean-reversion, the bias and the MSE were derived based on the joint moment generating function in (41), and examined their asymptotic properties as the sample size increases.

In our numerical experiment, for an Ornstein-Uhlenbeck process with , we provided graphical illustrations to demonstrate the dependency of bias and the MSE on the sample size and parameter values. Our findings indicate that as sample size increases, both bias and mean-squared error (MSE) consistently decrease across all parameter settings. While small values of and led to a negative bias, and larger led to higher MSE under small , these effects diminish with larger samples. Figures 1 and 2 have shown that the bias and the MSE of approaches to and , respectively, which verified the theoretical derivation in Section 3.3. In contrast, under the non-ergodic setting , the estimation error showed a different scaling behaviour, with bias and MSE converging to zero even at smaller sample sizes. Furthermore, as illustrated in Figure 3, the estimation results show minimal variation across different values of , indicating that the influence of the long-term mean becomes negligible in this unstable regime.

For further research, one could explore extending the current estimation framework and develop a discretised approximation method for mean-reverting diffusion processes under both ergodic and non-ergodic conditions. This includes incorporating fractional Ornstein-Uhlenbeck processes that allow for long-range dependence through fractional Brownian motion. Examining the effects of discretisation on the bias and MSE of parameter estimators in these general settings could enhance the understanding of inference under relaxed assumptions, which may contribute to the development of robust estimation procedures for models exhibiting structural complexities encountered in empirical applications.

References

- Arató [1982] Arató, M., 1982. Linear stochastic systems with constant coefficients: a statistical approach. Springer.

- Bao et al. [2017] Bao, Y., Ullah, A., Wang, Y., 2017. Distribution of the mean reversion estimator in the Ornstein–Uhlenbeck process. Econometric Reviews 36, 1039–1056.

- Belfadli et al. [2011] Belfadli, R., Es-Sebaiy, K., Ouknine, Y., 2011. Parameter estimation for fractional Ornstein–Uhlenbeck processes: Non-ergodic case. Frontiers in Science and Engineering 1, 1–16. An International Journal Edited by Hassan II Academy of Science and Technology.

- Bishwal [2007] Bishwal, J.P., 2007. Parameter estimation in stochastic differential equations. Springer.

- Cameron and Martin [1945] Cameron, R., Martin, W., 1945. Transformations of Wiener integrals under a general class of linear transformations. Transactions of the American Mathematical Society 58, 184–219.

- Çetin et al. [2013] Çetin, U., Novikov, A., Shiryaev, A., 2013. Bayesian sequential estimation of a drift of fractional brownian motion. Sequential Analysis 32, 288–296.

- Chan et al. [1992] Chan, K.C., Karolyi, G.A., Longstaff, F.A., Sanders, A.B., 1992. An empirical comparison of alternative models of the short-term interest rate. The Journal of Finance 47, 1209–1227.

- Cordeiro and Klein [1994] Cordeiro, G.M., Klein, R., 1994. Bias correction in ARMA models. Statistics & Probability Letters 19, 169–176.

- Cox et al. [2005] Cox, J.C., Ingersoll Jr, J.E., Ross, S.A., 2005. A theory of the term structure of interest rates, in: Theory of valuation. World Scientific, pp. 129–164.

- El Machkouri et al. [2016] El Machkouri, M., Es-Sebaiy, K., Ouknine, Y., 2016. Least squares estimator for non-ergodic Ornstein–Uhlenbeck processes driven by Gaussian processes. Journal of the Korean Statistical Society 45, 329–341.

- El Onsy et al. [2017] El Onsy, B., Es-Sebaiy, K., Tudor, C.A., 2017. Statistical analysis of the non-ergodic fractional Ornstein–Uhlenbeck process of the second kind. Communications on Stochastic Analysis 11, 1.

- Hu and Nualart [2010] Hu, Y., Nualart, D., 2010. Parameter estimation for fractional Ornstein–Uhlenbeck processes. Statistics & probability letters 80, 1030–1038.

- Iacus and Yoshida [2018] Iacus, S.M., Yoshida, N., 2018. Simulation and inference for stochastic processes with YUIMA. A comprehensive R framework for SDEs and other stochastic processes. Use R .

- Kelly et al. [2004] Kelly, L., Platen, E., Sørensen, M., 2004. Estimation for discretely observed diffusions using transform functions. Journal of Applied Probability 41, 99–118.

- Kendall [1954] Kendall, M.G., 1954. Note on bias in the estimation of autocorrelation. Biometrika 41, 403–404.

- Kohatsu-Higa et al. [2014] Kohatsu-Higa, A., Vayatis, N., Yasuda, K., 2014. Strong Consistency of the Bayesian Estimator for the Ornstein–Uhlenbeck Process. Inspired by Finance: The Musiela Festschrift , 411–437.

- Küchler and Sørensen [1997] Küchler, U., Sørensen, M., 1997. Exponential families of stochastic processes. volume 3. Springer Science & Business Media.

- Kutoyants [2013] Kutoyants, Y.A., 2013. Statistical inference for ergodic diffusion processes. Springer Science & Business Media.

- Kuznetsov [2013] Kuznetsov, A., 2013. On the Convergence of the Gaver–Stehfest Algorithm. SIAM Journal on Numerical Analysis 51, 2984–2998.

- Lai and Siegmund [1983] Lai, T., Siegmund, D., 1983. Fixed accuracy estimation of an autoregressive parameter. The Annals of Statistics , 478–485.

- Laurent and Shi [2020] Laurent, S., Shi, S., 2020. Volatility estimation and jump detection for drift–diffusion processes. Journal of Econometrics 217, 259–290.

- Le Breton and Pham [1989] Le Breton, A., Pham, D.T., 1989. On the bias of the least squares estimator for the first order autoregressive process. Annals of the Institute of Statistical Mathematics 41, 555–563.

- Liptser and Shiryaev [2001a] Liptser, R.S., Shiryaev, A.N., 2001a. Statistics of random processes I: General theory, Stochastic Modelling and Applied Probability, Applications of Mathematics (New York), 5, Second, revised and expanded edition. Springer-Verlag, Berlin.

- Liptser and Shiryaev [2001b] Liptser, R.S., Shiryaev, A.N., 2001b. Statistics of random processes II: Applications, Stochastic Modelling and Applied Probability, Applications of Mathematics (New York), 6, Second, revised and expanded edition. Springer-Verlag, Berlin.

- Marriott and Pope [1954] Marriott, F., Pope, J., 1954. Bias in the estimation of autocorrelations. Biometrika 41, 390–402.

- Mishura et al. [2022] Mishura, Y., Ralchenko, K., Dehtiar, O., 2022. Parameter estimation in CKLS model by continuous observations. Statistics & Probability Letters 184, 109391.

- Mota and Esqu´ıvel [2018] Mota, P., Esquível, M.L., 2018. Pseudo Maximum Likelihood and Moments Estimators for Some Ergodic Diffusions. Recent Studies on Risk Analysis and Statistical Modeling , 335–343.

- Novikov [1971] Novikov, A., 1971. The sequential parameter estimation in the process of diffusion type. Probabability Theory and its Applications 16, 394–396.

- Novikov [1972a] Novikov, A., 1972a. On the estimation of parameters of diffusion processes. Studia Sci. Math. Hungarica 7, 201–209.

- Novikov [1972b] Novikov, A., 1972b. Sequential estimation of the parameters of diffusion processes. Mathematical Notes of the Academy of Sciences of the USSR 12, 812–818.

- Novikov and Shiryaev [2014] Novikov, A., Shiryaev, A., 2014. Discussion on “Sequential Estimation for Time Series Models” by TN Sriram and Ross Iaci. Sequential Analysis 33, 182–185.

- Novikov et al. [2024] Novikov, A., Shiryaev, A., Kordzakhia, N., 2024. On parameter estimation of diffusion processes: sequential and fixed sample size estimation revisited. Theory of Probability and its Applications 68.

- Orcutt and Winokur Jr [1969] Orcutt, G.H., Winokur Jr, H.S., 1969. First order autoregression: inference, estimation, and prediction. Econometrica: Journal of the Econometric Society , 1–14.

- Perron [1991] Perron, P., 1991. A continuous time approximation to the unstable first-order autoregressive process: The case without an intercept. Econometrica: Journal of the Econometric Society , 211–236.

- Phillips and Yu [2009] Phillips, P.C., Yu, J., 2009. A two-stage realized volatility approach to estimation of diffusion processes with discrete data. Journal of Econometrics 150, 139–150.

- Prakasa Rao [1987] Prakasa Rao, B.L.S., 1987. Asymptotic theory of statistical inference. John Wiley & Sons, Inc.

- Quenouille [1956] Quenouille, M.H., 1956. Notes on bias in estimation. Biometrika 43, 353–360.

- Sørensen [1986] Sørensen, M., 1986. On sequential maximum likelihood estimation for exponential families of stochastic processes. International Statistical Review/Revue Internationale de Statistique , 191–210.

- Tanaka [2017] Tanaka, K., 2017. Time series analysis: nonstationary and noninvertible distribution theory. volume 4. John Wiley & Sons.

- Tang and Chen [2009] Tang, C.Y., Chen, S.X., 2009. Parameter estimation and bias correction for diffusion processes. Journal of Econometrics 149, 65–81.

- Vasicek [1977] Vasicek, O., 1977. An equilibrium characterization of the term structure. Journal of Financial Economics 5, 177–188.

Appendix A Derivation of Moment Generating Function

Theorem 3. Let . Then,

| (55) | ||||

Proof.

The logarithm of the likelihood ratio process in (6) is

By expanding (i), we get

| (i) | |||

Now, by the change of measure argument, since we have

Hence, the MGF can be written as

Now, since and are arbitrary, we choose these two values, such that random variables and become zeros. That is, we have

This indicates that

This simplifies the MGF to

| (56) |

where .

We set and , and find the joint MGF of ,

| (57) |

By expanding and simplifying the exponents,

Hence the integral is

which is the expression in (55), and this completes the proof. ∎

Appendix B Derivation of Moment Generating Function

The MGF in (53) for calculation of the bias and mean-squared error of the modified MLE was given by:

where

Firstly, we consider an auxiliary function,

where . is a two-dimensional Gaussian random vector, where

and is the range, such that .

The MGF function is evaluated using Wolfram Mathematica, with the following expressions. First defining the bivariate-normal distribution,

we find the MGF using the following command:

Now, setting , along with and

Proof.

Theorem 3 can be modified in this case, and hence,

where , as previously defined. ∎

Appendix C Summary of Numerical Results as a Table

| 0.01 | 50 | -0.011 | 0.030 | 0.035 | 0.037 |

| (0.006) | (0.006) | (0.006) | (0.006) | ||

| 75 | 0.007 | 0.022 | 0.024 | 0.025 | |

| (0.003) | (0.003) | (0.003) | (0.003) | ||

| 100 | 0.011 | 0.017 | 0.018 | 0.019 | |

| (0.002) | (0.002) | (0.002) | (0.002) | ||

| 125 | 0.011 | 0.014 | 0.015 | 0.015 | |

| (0.001) | (0.001) | (0.001) | (0.001) | ||

| 150 | 0.010 | 0.012 | 0.013 | 0.013 | |

| (0.001) | (0.001) | (0.001) | (0.001) | ||

| 175 | 0.010 | 0.011 | 0.011 | 0.011 | |

| (0.001) | (0.001) | (0.001) | (0.001) | ||

| 200 | 0.009 | 0.009 | 0.010 | 0.010 | |

| (0.0004) | (0.0004) | (0.0004) | (0.0004) | ||

| 0.1 | 50 | 0.037 | 0.039 | 0.039 | 0.040 |

| (0.008) | (0.009) | (0.009) | (0.009) | ||

| 75 | 0.025 | 0.026 | 0.026 | 0.026 | |

| (0.005) | (0.005) | (0.005) | (0.005) | ||

| 100 | 0.019 | 0.020 | 0.020 | 0.020 | |

| (0.003) | (0.003) | (0.003) | (0.003) | ||

| 125 | 0.015 | 0.016 | 0.016 | 0.016 | |

| (0.002) | (0.002) | (0.002) | (0.002) | ||

| 150 | 0.013 | 0.013 | 0.013 | 0.013 | |

| (0.002) | (0.002) | (0.002) | (0.002) | ||

| 175 | 0.011 | 0.011 | 0.011 | 0.011 | |

| (0.02) | (0.02) | (0.02) | (0.02) | ||

| 200 | 0.010 | 0.010 | 0.010 | 0.010 | |

| (0.001) | (0.001) | (0.001) | (0.001) | ||

| 1 | 50 | 0.037 | 0.039 | 0.040 | 0.040 |

| (0.042) | (0.044) | (0.045) | (0.045) | ||

| 75 | 0.025 | 0.026 | 0.027 | 0.027 | |

| (0.027) | (0.029) | (0.029) | (0.029) | ||

| 100 | 0.019 | 0.020 | 0.020 | 0.020 | |

| (0.020) | (0.021) | (0.021) | (0.021) | ||

| 125 | 0.016 | 0.016 | 0.016 | 0.016 | |

| (0.016) | (0.017) | (0.017) | (0.017) | ||

| 150 | 0.013 | 0.013 | 0.013 | 0.013 | |

| (0.014) | (0.014) | (0.014) | (0.014) | ||

| 175 | 0.011 | 0.011 | 0.011 | 0.011 | |

| (0.012) | (0.012) | (0.012) | (0.012) | ||

| 200 | 0.010 | 0.010 | 0.010 | 0.010 | |

| (0.010) | (0.010) | (0.010) | (0.010) |