Dynamic Basis Function Generation for Network Revenue Management

Abstract

This paper introduces an algorithm that dynamically generates basis functions to approximate the value function in Network Revenue Management. Unlike existing algorithms sampling the parameters of new basis functions, this Nonlinear Incremental Algorithm (NLIAlg) iteratively refines the value function approximation by optimizing these parameters. For larger instances, the Two-Phase Incremental Algorithm (2PIAlg) modifies NLIAlg to leverage the efficiency of LP solvers. It reduces the size of a large-dimensional nonlinear problem and transforms it into an LP by fixing the basis function parameters, which are then optimized in a second phase using the flow imbalance ideas from Adelman and Klabjan (2012). This marks the first application of these techniques in a stochastic setting. The algorithms can operate in two modes: (1) Standalone mode, to construct a value function approximation from scratch, and (2) Add-on mode, to refine an existing approximation. Our numerical experiments indicate that while NLIAlg and 2PIAlg in standalone mode are only feasible for small-scale problems, the heuristic version of 2PIAlg (H-2PIAlg) in add-on mode, using the Affine Approximation and exponential ridge basis functions, can handle extremely large instances that may cause benchmark network revenue management methods to run out of memory. In these scenarios, H-2PIAlg delivers substantially better policies and upper bounds than the Affine Approximation. Furthermore, H-2PIAlg achieves higher average revenues in policy simulations compared to network revenue management benchmarks in instances with limited capacity.

Keywords: Approximate Dynamic Programming, Basis Generation, Revenue Management, Row Generation

1 Introduction

Dynamic programming (Bellman, 1966) is an optimization tool that is typically used to find the optimal policy for a controlled stochastic process. Usually, it involves assigning a value to each state of the process through the so-called value function. Under certain conditions, both the value function and the optimal policy can be retrieved by solving a linear program (LP) with one variable for each state in the state space and one constraint for each feasible state-action pair. In applications with high-dimensional state spaces, solving this LP may become computationally intractable for two reasons. First, there might be too many variables. Second, the number of constraints may become impractically large. This challenge calls for an extension of traditional dynamic programming methods, leading to the emergence of Approximate Dynamic Programming (ADP).

To address dimensionality challenges via ADP, value function approximations seek to capture the underlying structure of the optimal value function without explicitly enumerating values for each state. Frequently, a linear combination of basis functions is chosen to approximate the true value function. This technique effectively reduces the number of parameters to be estimated (representing variables in the LP) by focusing on characterizing the basis functions and their weights within the proposed approximation.

The estimation of these new parameters can be addressed by plugging the value function approximation into the LP formulation (De Farias and Van Roy, 2003); we call this problem the approximate LP. However, a lingering issue remains: the number of constraints may be too large for any solver to handle. This challenge is often addressed by using row generation, an iterative optimization technique employed in mathematical programming. The algorithm starts with a relaxed version of the approximate LP, called the master program, that only considers a subset of the constraints. In the context of value function approximation, this means that constraints are imposed only for a subset of feasible state-action pairs. At each step, new rows (i.e., constraints corresponding to some state-action pairs) are generated by fixing the parameters of the approximation and finding state-action pairs that induce violated constraints. These newly generated rows are then added to the master program, with the objective of progressively refining the estimate of the approximation parameters over time. Once the row generation algorithm concludes, it provides a value function approximation.

While this procedure has been widely employed in ADP (see, for instance, Adelman (2007); Tong and Topaloglu (2013)), the set and number of basis functions in the value function approximation are typically predefined. Both are crucial for the quality and tractability of the approximation. For instance, a larger number of basis functions may provide a better approximation due to increased degrees of freedom, but it also introduces more parameters, potentially leading to dimensionality issues. Thus, selecting the appropriate values for requires balancing the quality of the approximation with the tractability of the problem.

The purpose of this paper is to propose an algorithm that iteratively adds basis functions from a given set by solving an optimization problem. This algorithm allows the user to either stop the algorithm based on her satisfaction with the current approximation or to further improve it at an additional computational cost. In particular, the suggested Nonlinear Incremental Algorithm (NLIAlg) iteratively follows these two steps: (I) estimating the weights and parameters of the current basis functions using a row generation algorithm, and (II) increasing until the improved approximation meets a user-specified criterion. For large instances, we propose to estimate the parameters of the approximation in two different phases within Step (I). We first transform the master problem into an LP by fixing the parameters that define the basis functions, which would otherwise make the problem nonlinear. In Phase (i), we follow the flow imbalance ideas introduced in Adelman and Klabjan (2012) to estimate those parameters. Given these fixed parameters, the other parameters are then optimized in Phase (ii). This constitutes the Two-Phase Algorithm (2PIAlg).

The proposed approaches can be used to either (1) find a suitable value function approximation from scratch in a standalone mode (when initialized with an empty set of initial basis functions), or (2) enhance a given value function approximation in an add-on mode. Despite the computational improvement of the two-phase-estimation approach, our numerical results highlight that the standalone mode is practical only for toy problems. This is why for problems of realistic size, we will use the add-on mode with an heuristic version of 2PIAlg.

Summarizing, the main contributions of this paper are the following.

-

(a)

We develop the first algorithm in the NRM context that iteratively refines the approximation by sequentially optimizing and adding new basis functions. These algorithms endow the user with control over the approximation process. Unlike traditional methods where number and shape of the basis functions are predefined, our approach allows users to either stop the algorithm if the current approximation meets their criteria or continue refining it further by increasing the number of basis functions . This flexibility balances quality and computational cost, addressing the critical issue of the selection of .

-

(b)

We extend for the first time the flow-balance gap ideas of Adelman and Klabjan (2012) to a stochastic context. Originally developed for deterministic settings, we adapt this approach to the NRM problem. While Pakiman et al. (2020) and Bhat et al. (2023) apply sampling-based approaches to generate basis functions, our method leverages mathematical programming to construct basis functions that maximize flow imbalances in the NRM problem. Under certain conditions we prove that if the family of basis functions has enough fidelity to perfectly fit the optimal value function, and there is still a gap between the optimal objectives of the LP and the ALP problem, then one can find a new basis function that improves the current solution.

-

(c)

We carry out a performance analysis against strong NRM benchmarks. Our computational study compares the heuristic version of 2PIAlg (H-2PIAlg) in add-on mode against well-established methods in the NRM literature, namely AA, SPLA, and NSEP, using two sets of benchmark instances. Our numerical results demonstrate that H-2PIAlg significantly outperforms the policies and upper bounds provided by AA. Additionally, it achieves superior policies and upper bounds compared to SPLA and NSEP in scenarios where capacity is scarce, although these improvements come at a greater computational cost. However, thanks to its iterative nature, H-2PIAlg is able to provide solutions for instances where SPLA and NSEP run out of memory.

The structure of the paper is as follows. Section 2 reviews the relevant literature. In Section 3, we introduce the dynamic programming formulation for the NRM problem and present the ideas behind our iterative approximation approach. We also introduce the concept of flow imbalance and discuss how it can be implemented. Section 4 details the NLIAlg, explaining how row generation is employed to implement the approximation and discussing criteria for deciding when to stop adding new basis functions. Section 5 explains how to modify NLIAlg to yield the more tractable 2PIAlg. In Section 5.1, we discuss heuristic modifications for the algorithms, while in Section 6 we explore the choice of basis functions. Finally, Section 7 presents our numerical analysis, and Section 8 concludes with remarks and potential extensions. All proofs can be found in the Appendix.

2 Literature Survey

In this section, we point at overviews on NRM and ADP before we summarize particular classes of basis functions suggested when using approximate linear programming in Section 2.1. In Section 2.2, we then provide an overview of the related literature applying different methods within approximate linear programming. Given the vast literature in this area, we focus on papers applying such methods for NRM problems and highlight the novelty of our contributions.

Chapter 3 of Talluri et al. (2004) provides an introduction to NRM problems, formulating the decision problem as a Markov decision process with states representing the remaining number of seats on all legs. In this context, the curse of dimensionality emerges due to exponential growth of the state space in the number of legs, prompting the application of ADP.

As mentioned above, ADP provides an array of methods to approximate Markov decision processes in the face of the curse of dimensionality. A summary of simulation-based approaches is given in Powell (2011). On the other hand, approximate linear programming approximates the value function of a Markov decision process as a linear combination of basis functions and integrates this approximation into the linear programming formulation (Schweitzer and Seidmann, 1985; De Farias and Van Roy, 2003; Adelman, 2007).

2.1 Basis Functions in Approximate Linear Programming

In the context of NRM, Adelman (2007) was the first to suggest an additively separable value function approximation within the linear programming formulation of the corresponding Markov decision process. By approximating the value function with an affine function with time-dependent slopes, Adelman (2007) demonstrated the efficiency of column generation in solving the approximated LP.

This affine approximation implies two major assumptions: (i) the different resources are separable, i.e., the marginal value of one unit of resource is independent of the number of units available for resources ; and (ii) the marginal value of one unit of resource is constant and hence independent of the number of units available for this resource.

To remove Assumption (ii), different basis functions have been suggested. In the general separable framework, the values of the value function in different states can be directly viewed as variables. This broader approximation is often referred to as the Separable Piecewise Linear Approximation (SPLA). Farias and Van Roy (2007) use constraint sampling to analyze this case, Vossen and Zhang (2015b) develop a reduction and Kunnumkal and Talluri (2016) prove the equivalence between this approximation and the Lagrangian relaxation introduced by Topaloglu (2009).

Assumption (i), separability, is pervasive in the literature. However, in the context of NRM non-separable approximations have been explored by Zhang (2011), who combines the solutions of decomposed single-leg revenue management problems using a minimum-operator, leading to a non-separable approximation. Additionally, Laumer and Barz (2023) propose basis functions explicitly dependent on more than one resource, suggesting reductions for non-separable approximations.

In a different setting, Guestrin et al. (2003) consider non-separable basis functions depending on a small number of variables each. Lin et al. (2020) advocate for constraint-violation learning for non-separable approximations for inventory control and energy storage. In contrast to sampling-based approaches such as Pakiman et al. (2020) and Bhat et al. (2023), we generate basis functions analytically using row generation. Nevertheless, both works share with ours the use of basis functions with universal approximability.

Regarding our chosen approximation structure, the ideas presented in Klabjan and Adelman (2007) align closely with our work. They suggest using ridge functions to capture interactions between different components of the state variable. However, unlike our work, they apply this approximation in a deterministic setting without improving a given approximation.

2.2 Solution Methods for Approximate Linear Programming

For any choice of basis functions, the use of a linear combination of them within the linear programming formulation typically yields a linear problem with few variables and many constraints. The resulting problem can then be solved by row or column generation (Trick and Zin, 1997; Adelman, 2004, 2007; Zhang and Adelman, 2009; Kunnumkal and Talluri, 2016). Sometimes, the resulting problem can also be reduced analytically to allow for a computationally more efficient solution; see, e.g. Farias and Van Roy (2007), Tong and Topaloglu (2013), Vossen and Zhang (2015b), Kunnumkal and Talluri (2019) and Laumer and Barz (2023). Although unconventional in traditional NRM, alternative approaches to solving the approximated LP include constraint sampling (De Farias and Van Roy, 2004) and constraint violation learning (Lin et al., 2020).

In this paper, we suggest a row generation method that iteratively adds basis functions to a given approximation (which can also be an empty set of basis functions). Methodologically, our algorithm mirrors early ideas from Adelman (2007), but for a non-linear setting and deciding on the number of basis functions to be added.

3 Iterative Approximation Refinement in ADP for NRM

We begin by presenting the dynamic programming formulation of the NRM problem in Section 3.1. Section 3.2 introduces the nonlinear approximation we propose. Estimating the parameters for this approximation involves solving a large-dimensional nonlinear program, which we outline in Section 3.3. In this section, we also discuss how the approximation can be iteratively refined by increasing the number of basis functions. Finally, in Section 3.4, we present the dual formulation of the linearized counterpart of such a large-dimensional program, which allows us to introduce the flow-balance constraints.

3.1 The NRM Problem

We consider a finite discrete-time horizon with time units to sell products . At each time , at most one customer arrives and requests a particular product with probability . No customer arrives with probability . The sale of product at time generates revenue and reduces the number of units of available resources by . The values of are summarized in the consumption matrix . At the beginning of the horizon, i.e. when , the seller has units of resource , that are referred to as the capacities of the resources and are denoted jointly as . The remaining capacity of resource at any given point in time is denoted by with . We assume that at the end of the selling period, i.e. when , remaining units of resources are worthless.

At every period , the seller must determine whether a customer request for product is accepted () or rejected () with . Given a customer request for product , this binary variable allows us to write the revenue obtained as and the remaining resources as , where denotes the -th column of matrix . At every state we assume that we cannot sell more resources than we have, thus our set of feasible actions is

The set of feasible remaining resources is given by

We denote the hypercube convex hull of by . Furthermore, we denote the set of feasible state-action pairs at time by

The objective is to maximize the total expected revenue that can be gained given initial capacity over the selling horizon . In this paper, we do not consider cancellations. Then, the maximum expected revenue that can be obtained over the selling horizon given remaining resources can be computed using the optimality equations

| (1) |

and for all . Instead of tackling the above optimality equations directly, we formulate the following LP

| (LP) | ||||

As pointed out in Proposition 1 of Adelman (2007), for every any feasible solution to (LP) gives an upper bound of the optimal value function solving (1). According to complementary slackness, an optimal solution to (LP) fits the optimal value function exactly for states with non-zero visit probability. In particular, the optimal solution to (LP) evaluated at period 1 and at full capacity, , coincides with the optimal value function evaluated at that state; i.e., .

However, this NRM problem is hardly tackled directly because it suffers from the well-known curse of dimensionality. Indeed, Problem (LP) has as many constraints as feasible state-action pairs and functions may lie on a highly dimensional space. As a consequence, this problem can only be solved exactly for very small instances. To solve larger instances, typically the value function is approximated and a row generation algorithm for (LP) is implemented or equivalent reductions are developed.

3.2 The Value Function Approximation

We denote any given approximation of the value function by , and suggest an extension that accommodates non-separable terms and nonlinearities. More specifically, for any given we approximate the value function by the Nonlinear (and potentially non-separable) Approximation (NLA)

| (NLA) |

with offset , number of additional basis functions , weights for and nonlinear, nonseparable functions in with parameters . Even though the same basis functions are used in every period , the weights are time-dependent, allowing for very differently shaped approximations over time. While the value function may not be jointly concave, numerical approximations of the value functions (NLA) often exhibit a concave structure. To predominantly obtain non-negative weights with convex basis functions, we subtract the weighted sum of basis functions in (NLA).

The quality of the optimal approximation in the form (NLA) depends on the selection of the baseline approximation , the class of basis functions , and the number of basis functions . When for all , (NLA) generates a new approximation that does not fit the residuals of any baseline approximation (standalone mode). Nonetheless, the fundamental concept behind (NLA) lies in its capacity to improve a given approximation (add-on mode).

By substituting the exact value function with (NLA) on the right-hand side of (1), the proposed value function approximation yields the following policy for a given

| (2) |

In the subsequent sections, we will refer to this policy as the policy based on (NLA). To evaluate this policy, we first choose a class of basis functions and a baseline approximation . If the current policy is not satisfactory, we can increase to improve the current approximation. An iterative refinement of (NLA) can be performed as follows:

-

Step (I):

Estimate for a given number of basis functions

-

Step (II):

Decide if should be increased. If yes, increase and return to Step (I).

The resulting value function approximation can then be used in (2).

3.3 The Approximate LP

To implement Step (I), we leverage the nonlinear problem that arises from plugging (NLA) into the linear programming formulation (LP) for a fixed

| (AP) | ||||

The solution of (AP) provides the parameters for Step (I). As mentioned in Adelman (2007), the approximate program (AP) finds the lowest upper bound on of the form (NLA). This means that choosing basis functions that are dense on the space where the value function lies may yield an approximation with the potential to fit arbitrarily close. Since an optimal solution to (LP) also fits the optimal value function exactly for states with non-zero visit probability, (AP) may also fit the optimal value function exactly at such states under a strong approximation. In sum, the ability of the proposed approximation (NLA) to fit the value function seems to be crucially dependent on the choice of the basis functions . In addition, the shape of in also affects the computational burden of solving (AP). More specifically, nonlinear basis functions in lead to a nonlinear problem (AP). We provide guidance on the choice of basis functions in Section 6.

A straightforward implementation of Step (II) is to add variables and to the nonlinear problem (AP) in every iteration. By increasing the degrees of freedom with every set of newly added variables, this approach might have the potential to refine the current approximation with increasing .

3.4 Using Flow-Balance Constraints to Refine the Value Function Approximation

Since Problem (AP) might be nonlinear in , , it might be difficult to solve even for a moderate number of basis functions. However, for fixed values , , (AP) is a finite-dimensional LP with variables and . We call this resulting problem linearized (AP), and strong duality holds with the following dual formulation:

| (D) | ||||

| s.t. | ||||

| (D.FB) |

In the problem above, denotes the dual variables for the constraints . The so-called Flow-Balance constraint (D.FB) is associated with primal variables . It is the only constraint that includes the parameters of the basis function. In any feasible solution to this dual, (D.FB) will be satisfied for the values . If (D.FB) does not hold for some , adding a basis function with these parameters could change the solution and refine the approximation. If there are no values within our selected set of basis functions violating (D.FB), the current approximation cannot be further improved using any additional from this selected set of basis functions .

This idea to improve value function approximations via flow-balance conditions was originally suggested by Adelman and Klabjan (2012) in a deterministic context with flow-balance equations similar to (D.FB). For deterministic MDPs and piecewise linear basis functions, Klabjan and Adelman (2007) can even prove the convergence of such an algorithm. To mathematically formulate this idea in the context of NRM, we subtract the right-hand side of (D.FB) on both sides of (D.FB) for all and view the resulting left-hand side as functions in . For given , the result quantifies the flow-imbalance of (D.FB) given :

Adding another basis function with parameters and new variables in the primal generates a new flow-balance constraint in the dual. Adding a basis function with parameters that result in no flow imbalance for all , hence will not alter the solution of the dual linear master problem. In contrast, adding a basis function violating constraint (D.FB) will improve the bound given by (NLA) under certain conditions.

Proposition 1

The following theorem demonstrates that if a finite set of basis functions can perfectly represent the optimal value function, and there remains a gap between the current approximation and the true optimal objective, then at least one of these basis functions must violate flow balance.

Theorem 1

Assume there exists a finite number of basis functions, , and parameters , , and , for , such that the optimal value function can be expressed as

Consider a given collection , with . Let be an optimal primal-dual solution pair to the corresponding approximation problem, such that , where the approximate value function is given by

Define as the flow-balance functions parametrized by . Then, there must exist some and such that

4 The Nonlinear Incremental Algorithm (NLIAlg)

We begin in Section 4.1 discussing how we can use row generation in Step (I) to solve Problem (AP) for a fixed number of basis functions. Based on the quality of the current approximation, Section 4.2 then discusses whether the number of basis functions should be increased in Step (II).

In a nutshell, NLIAlg involves the following two steps:

-

Step (I):

Estimate for a given solving (AP) via row generation.

-

Step (II):

Decide if should be increased. If yes, increase and return to Step (I).

4.1 Solving (AP) for Given via Row Generation

Due to the extensive number of constraints in Problem (AP), solving it directly for realistically sized problems is impractical. Instead of addressing (AP) with constraints for all and , we employ row generation. That is, we minimize (AP) only for a subset of constraints for all . Additional constraints are added sequentially until a predefined stopping criterion is met.

Constraints for period are generated by identifying a state-action pair that violates a constraint in (AP). We refer to the optimization problem that emerges when seeking these state-action pairs as subproblem . For fixed , and for , subproblem minimizes the difference between the left-hand side and the right-hand side of the constraints for that time,

| (3) |

If, for a given , the objective value of the optimal solution to (3) is positive, the current solution fulfills all constraints for time , not just the ones that were explicitly considered in the master problem. If the objective value is negative, the optimal solution of the subproblem , with , is added to the subset of the constraints considered in the master problem. The subproblem corresponding to the last time period is

| (4) |

and treated accordingly. Given a stopping criterion (e.g., stopping if the objective value of all subproblems is greater than or equal to 0) we can hence solve (AP) using Row Generation. This algorithm iteratively solves the master problem for given sets of constraints , solves the subproblems for all and expands the sets until the stopping criterion is met. The pseudocode for the Row Generation Algorithm can be found in the Appendix.

4.2 Determining Whether to Increase the Number of Basis Functions

While there are a few exceptions (see, for instance, Pakiman et al. (2020)), the literature frequently overlooks the question of finding the appropriate number of basis functions to approximate the value function. Leveraging our adaptable approximation design, can simply be increased until a sufficiently good approximation is reached according to a user-specified stopping criterion . Every time is increased, a new set of variables and for all and is added to the master problem. A more detailed pseudocode of this procedure is given in the Appendix.

To assess whether the quality of the approximation is sufficient, the stopping criterion could consider the difference between average revenue obtained from a simulation of the current policy (2) and the approximated objective value (AP), which provide a lower and upper bound on , respectively. If that difference is smaller than some predefined value, the algorithm is terminated.

5 A Two-Phase Approach to Reduce the Dimensionality of Nonlinear (AP)

A successful implementation of NLIAlg hinges on the tractability of both the master problem and the subproblems. The master problem is a large-dimensional nonlinear program with many constraints, whose tractability is deeply influenced by the shape of the basis functions in . In this section, we leverage LP solvers’ efficiency by fixing for in (AP). This transforms the master problem into an LP, regardless of the shape of in . In addition, it reduces the dimensionality of (AP). We then integrate the flow-balance idea discussed in Section 3.4 to optimize the parameter values of the new basis function . Thus the estimation estimation of the parameters in (NLA) is computed in two phases:

-

Step (I)

Use the following two phases to find a solution to (AP):

-

Phase (i)

Estimate by maximizing flow imbalances.

-

Phase (ii)

Estimate for a given number of basis functions solving linearized (AP) via row generation for fixed .

-

Phase (i)

-

Step (II):

Decide if should be increased. If yes, increase and go to Step (I).

Although the subproblems remain nonlinear integer optimization programs, their dimensionality is smaller and more manageable with appropriate choices of basis functions and baseline approximation. Section 6 provides more details on this choice.

Based on the rationale discussed in Section 3.4 we expect that adding a basis function with parameters maximizing will result in a closer fit to the real value function. Instead of maximizing the flow imbalance for a specific time period, we suggest finding parameters that maximize the overall weighted flow imbalance across the entire time horizon:

| (5) |

Because flow imbalances early on propagate to future periods, intuition suggests that they should be prioritized for closure. This is why we emphasize the importance of the first periods to provide a good value function approximation. Once the flow-imbalances in early periods are removed, the focus moves towards later periods. A more detailed pseudocode of 2PIAlg is given in the Appendix.

5.1 The Heuristic Two-Phase Algorithm (H-2PIAlg)

In this section we propose a Heuristic Two-Phase Incremental Algorithm (H-2PIAlg), which includes modifications to the algorithm that intend to improve tractability. First, we propose heuristic approaches to generating rows and basis functions. To generate a new basis function we do not need to find the optimal solution of the flow imbalance problem (5). Parameters yielding an objective value larger than zero still cut off flow imbalances. Therefore, H-2PIAlg uses local solvers and enforces time limits on (5).

Similarly, solutions yielding negative objective values in (3) or (4) constitute violated constraints in (AP), and their inclusion in the master problem is likely to bring improvement. As a consequence, H-2PIAlg also uses local solvers and imposes time limits when solving these subproblems. In addition, instead of solving one subproblem for each time period , H-2PIAlg reuses state-action pairs found for a given in other time periods if this state-action pair leads to a negative objective value in the corresponding subproblem. This might potentially avoid solving subproblems at each iteration of the row generation algorithm.

Second, we explain how to exploit the monotonicity of the NRM value function. In NRM, the optimal value function is non-negative and decreases over time for a given ; i.e., for all . Additionally, it is increasing in each component when the resources for all other legs and time are held fixed; i.e., for all , where . If we required (NLA) to fullfil these properties, these would translate into the following constraints

| (6) | |||

| (7) | |||

| (8) |

where and . Constraints (6)-(7) are redundant as they are given by constraints with in (AP). However, adding constraints (8) additionally enforces monotonicity in , thus we may consider our master problem to be (AP) with feasible region restricted by constraints of type (8). We call these problems with additional constraints tightened (AP). Abusing notation, we refer to this kind of tightened problem as (AP)+(8). Nonetheless, considering all the monotonicity constraints for all and would significantly increase the dimension of this problem, and our numerical experience showed that they do not improve much the current approximation when enough basis functions and rows have already been generated so there is already enough information about the structure of the value function. Hence H-2PIAlg generates monotonicity constraints (8) only for . We denote by for all the subsets of generated constraint indices.

To generate monotonicity constraints, the right-hand side of (8) is minimized for a particular and . This subproblem is a nonlinear integer problem, solved with local solvers and imposing time limits. H-2PIAlg also uses solutions obtained by solving subproblem and to generate rows at other periods of time and other legs. A pseudocode can be found in the Appendix. The master program of this modified Row Generation algorithm is (AP)+(8), thus when finding a new basis function with H-2PIAlg one needs to maximize flow imbalances taking into account dual variables associated with monotonicity constraints (8). The dual formulation of the tightened LP giving rise to adjusted flow-imbalance functions . These formulations can be found in the Appendix.

6 Choosing the Set of Basis Functions

In this section, we explore the selection of basis functions. Section 6.1 outlines the properties we consider desirable for . Section 6.2 introduces piecewise linear and exponential ridge basis functions and provides a numerical comparison.

6.1 Desirable Properties for Basis Functions

Although the algorithms introduced so far can be used for any choice of , in this paper we recommend using basis functions that

-

(a)

Have the potential to fit the value function arbitrarily closely,

-

(b)

Are smooth and/or tractable to solve in and , and

-

(c)

Exhibit structural properties akin to the real optimal value function and/or good interpolation properties.

The rationale behind (a) is to support our goal of providing an accurate approximation of the value function. Specifically, our goal is to select functions that ensure that parameters of our approximation can lead to a small difference between the value function and the approximation for large . To state this objective more precisely, we want the following: , and such that . To achieve this, it suffices to choose basis functions from a set of functions that is fundamental in the space of continuous functions , i.e., with a linear span that is dense in . Intuitively, this should ensure a desirable behavior of our two-phase heuristic (see Proposition 1).

Property (b) aligns with previous discussions about how the choice of impacts both the speed of row generation and the overall quality of the approximation. The subproblems solved to generate rows are integer programs in and . As the number of basis functions increases, the complexity of these subproblems also increases, potentially slowing down the algorithm. Therefore, it is essential to have basis functions that can be easily modeled and solved in . Similarly, the choice of baseline approximation should provide a good starting point while having a manageable shape in . Finally, H-2PIAlg must solve a low-dimensional continuous problem to generate a that violates the flow-balance constraints. Thus, having basis functions that are also easy to model and solve in is crucial.

Imposing (c) can reduce the number of basis functions needed by the algorithm. Intuitively, the more state values a single basis function can closely fit, the fewer basis functions will be required to meet the user’s accuracy threshold. Additionally, imposing (c) is beneficial if structural properties of the real value function are known. In our NRM problem, in particular, the real value function is known to be monotonically increasing and asymptotically concave in (Talluri and Van Ryzin, 1998). By selecting convex and decreasing in , we could easily impose the approximation to be concave and increasing by requiring for all and . This may allow our approximation to capture the true structure of the value function, potentially providing well-behaved policies even for a small value of .

6.2 Piece-Wise Linear Hat versus Exponential Ridge Basis functions

A function is called a ridge function if it has the form , where is a function in and is a fixed vector (Sun and Cheney, 1992). Ridge functions form a fundamental set in (see Theorem 4 in Sun and Cheney (1992)) and hence naturally fulfill (a). The following result shows that as long as is a convex function, the ridge function is convex, ensuring Property (c).

Proposition 2

Let be a ridge function with direction and convex. Then, is convex.

To ensure stable estimation and robust numerical performance, it is often advantageous to constrain or penalize . Theorem 5 in Sun and Cheney (1992) confirms that we can add this type of constraints while still preserving Property (a). In the Appendix, we show that norm-constrained convex ridge basis functions give rise to DC optimization problems.

Inspired by Adelman and Klabjan (2012), one might consider using continuous piecewise linear hat functions in approximation (NLA), but they fail to meet Conditions (b) and (c). Specifically, hat functions are nondifferentiable and encoded via MINLP, potentially making efficient row generation less tractable. As noted in Adelman and Klabjan (2012), the flow-balance problem (5) is a hard nonlinear integer problem, complicating the generation of new basis functions. Furthermore, Klabjan and Adelman (2007) discuss the challenges of enforcing convexity over the entire domain when using these functions. Lastly, since each hat function is composed of two linear segments, they may be able fit a very limited number of points closely. Given the stochastic nature of the NRM problem, one would expect to need almost as many functions as there are states in the state space.

The set of exponential ridge functions is another set of fundamental functions. The corresponding basis functions

| (9) |

are differentiable, monotone decreasing, and convex. If all weights in (NLA) are chosen positive, the value function approximation will hence be monotone increasing and concave. Furthermore, basis functions of the form (9) are smooth, easy to code and solve. The flexibility of these functions may also allow to closely fit a larger number of points at once, possibly reducing the number of basis functions needed. Summarizing, exponential ridge basis functions fulfill Conditions (a), (b) and (c).

For numerical purposes, we restrict ourselves to norm-constrained exponential ridge-basis functions with

| (10) |

where is the capacity of leg . The following proposition shows that adding the norm constraint (10) allows us to bound the basis function away from zero and away from large values. This might avoid numerical issues in practice, further ensuring Property (b).

Proposition 3

If is constrained by (10), then

Instead of solving (AP), the Row Generation Algorithm can also be used to solve (AP)+(10) by adding (10) to the master problem. In addition, the resulting minimum objective value of the tightened problem (AP)+(10) provides an upper bound on .

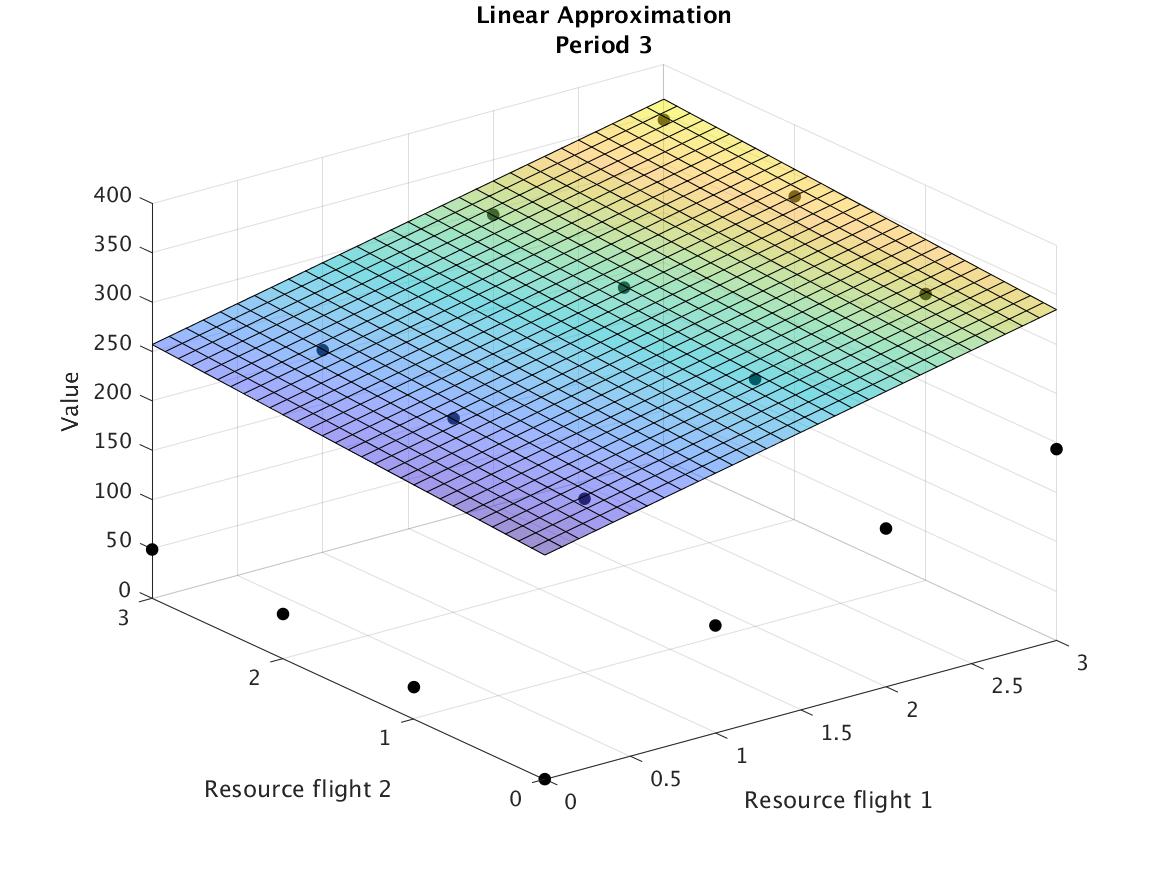

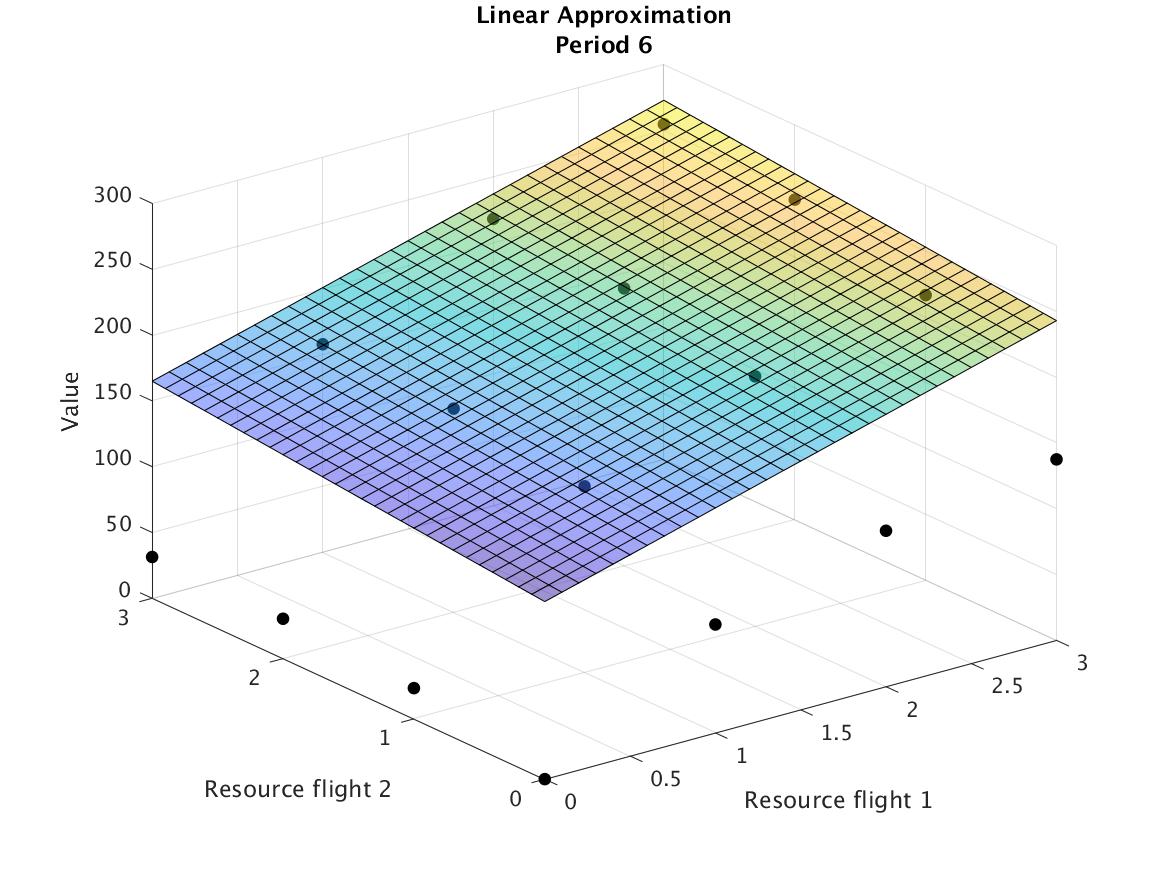

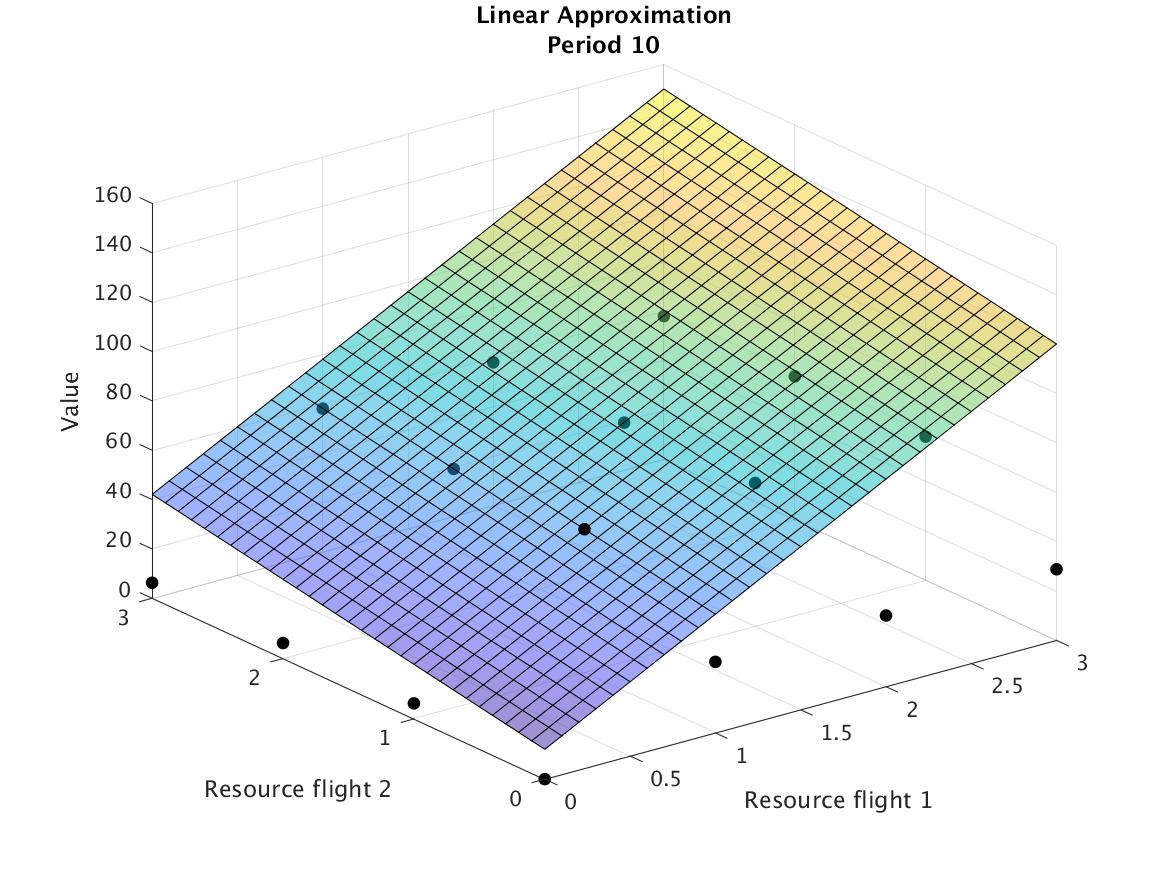

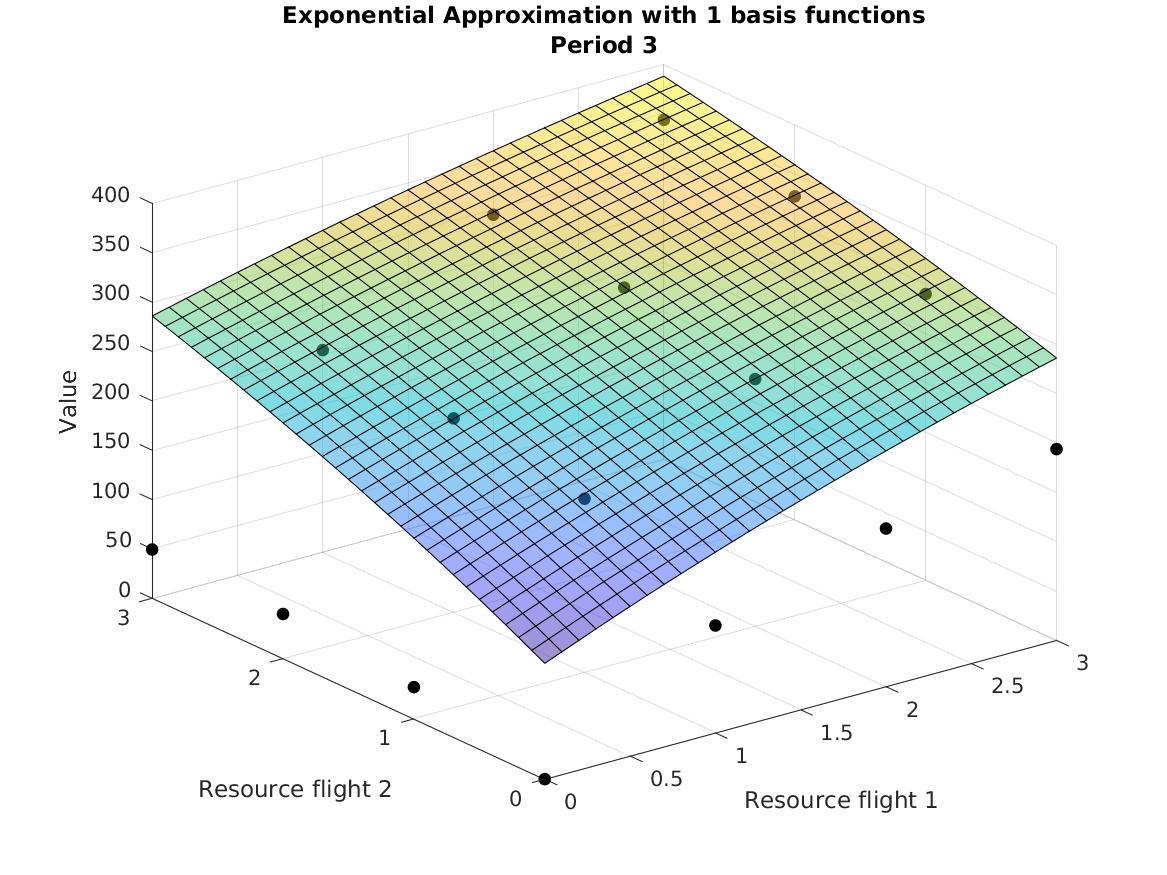

To numerically compare the performance of H-2PIAlg with hat and exponential ridge basis functions, we use a toy example We consider the standalone version of the algorithm; i.e., . Although NLIAlg provides similar results, it is less tractable, so its results are relegated to the Appendix. We consider a small network with two flights, Flight 1 connecting cities and and Flight 2 connecting and . Customers can travel from to by taking both flights. Hence, there are three itineraries each offered at a low and high fare, generating six products in total. There are 10 periods of time and the demand process is assumed to be stationary, i.e. for all . Fares and arrival probabilities for all products are specified in the Appendix.

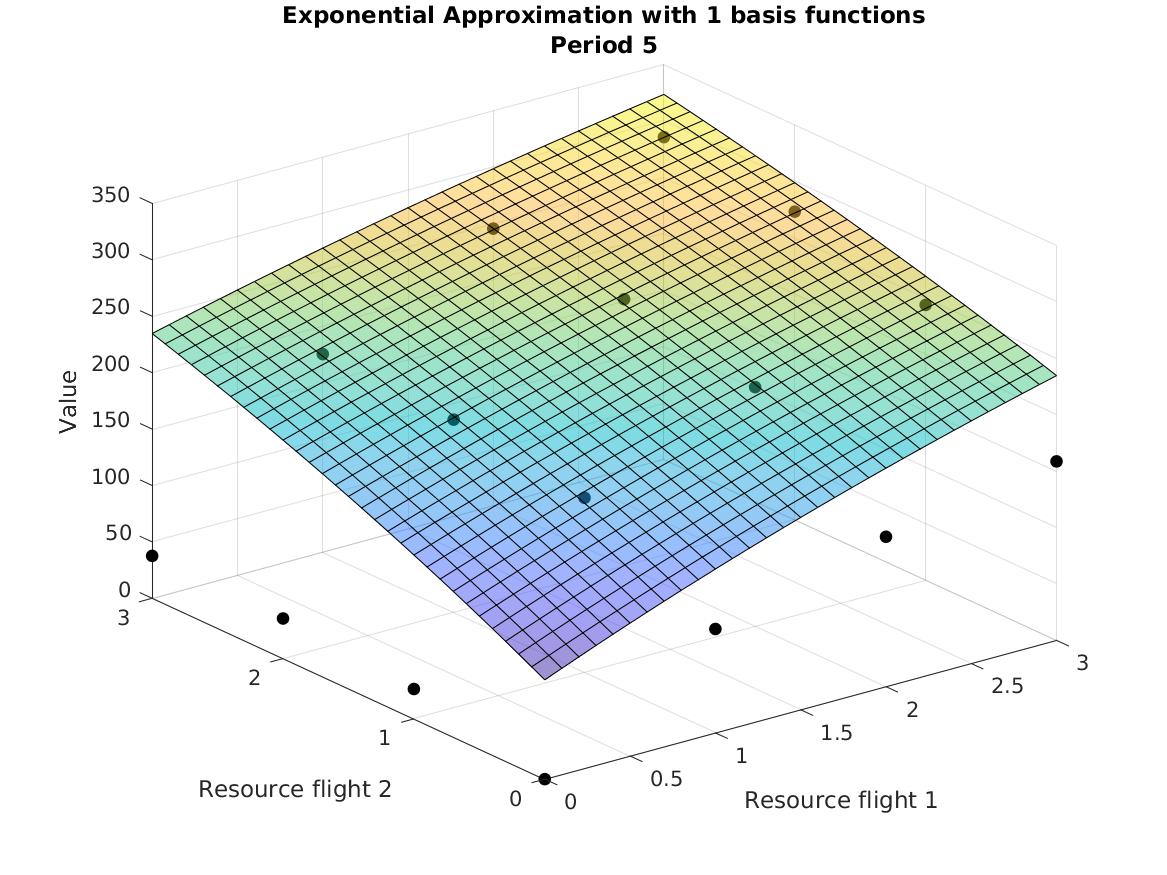

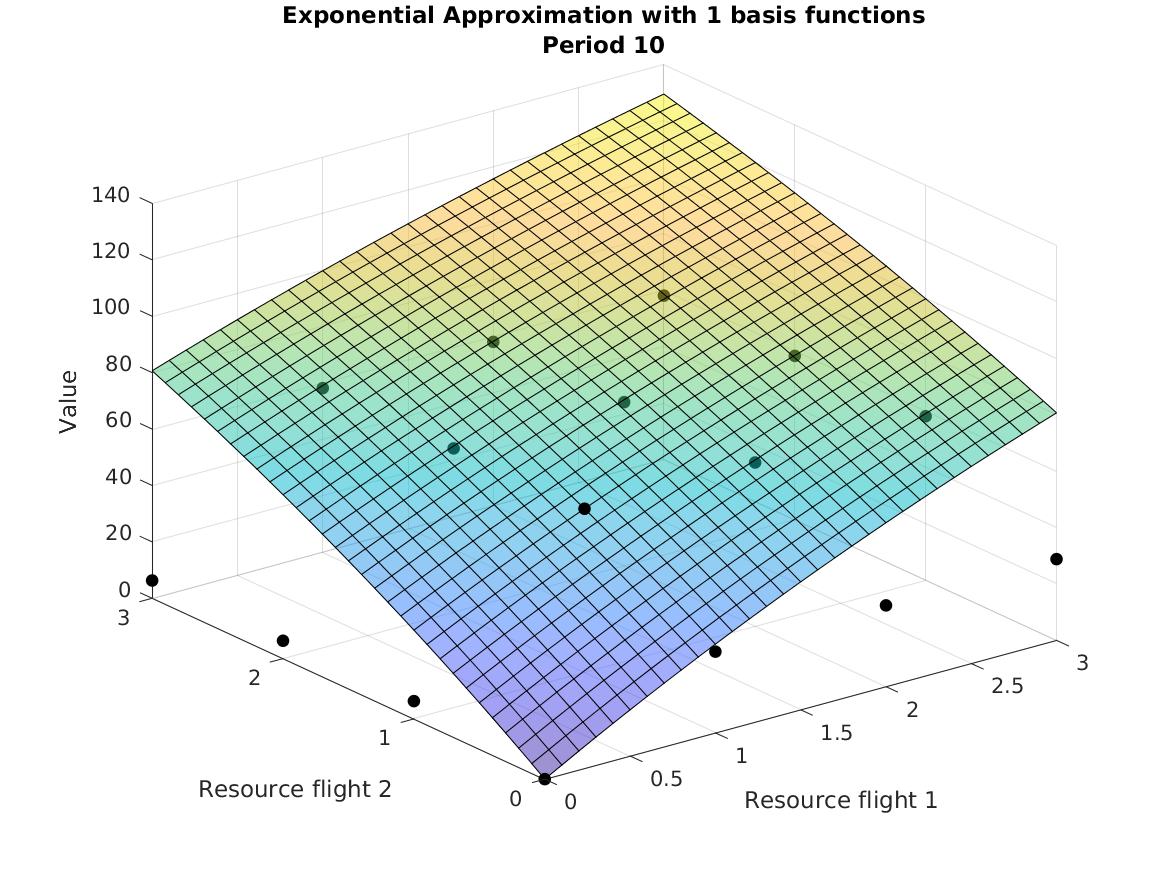

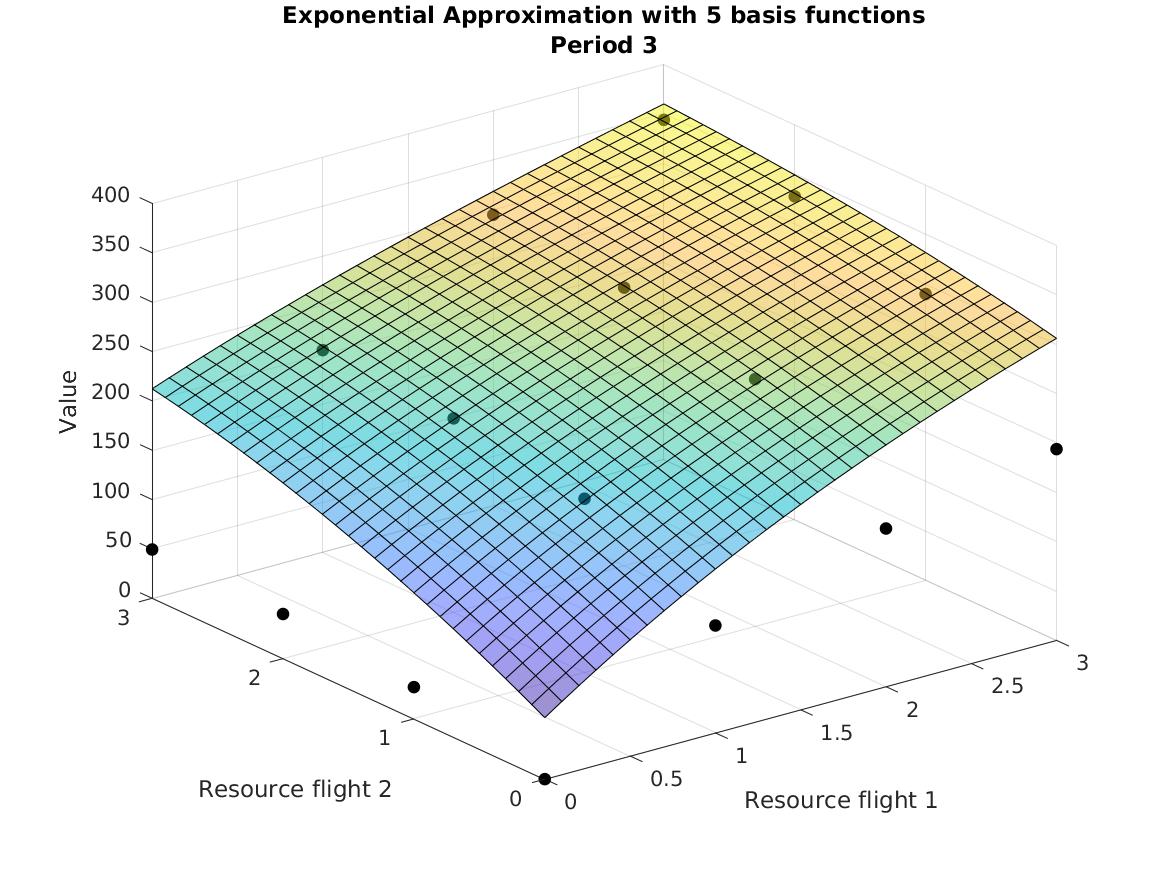

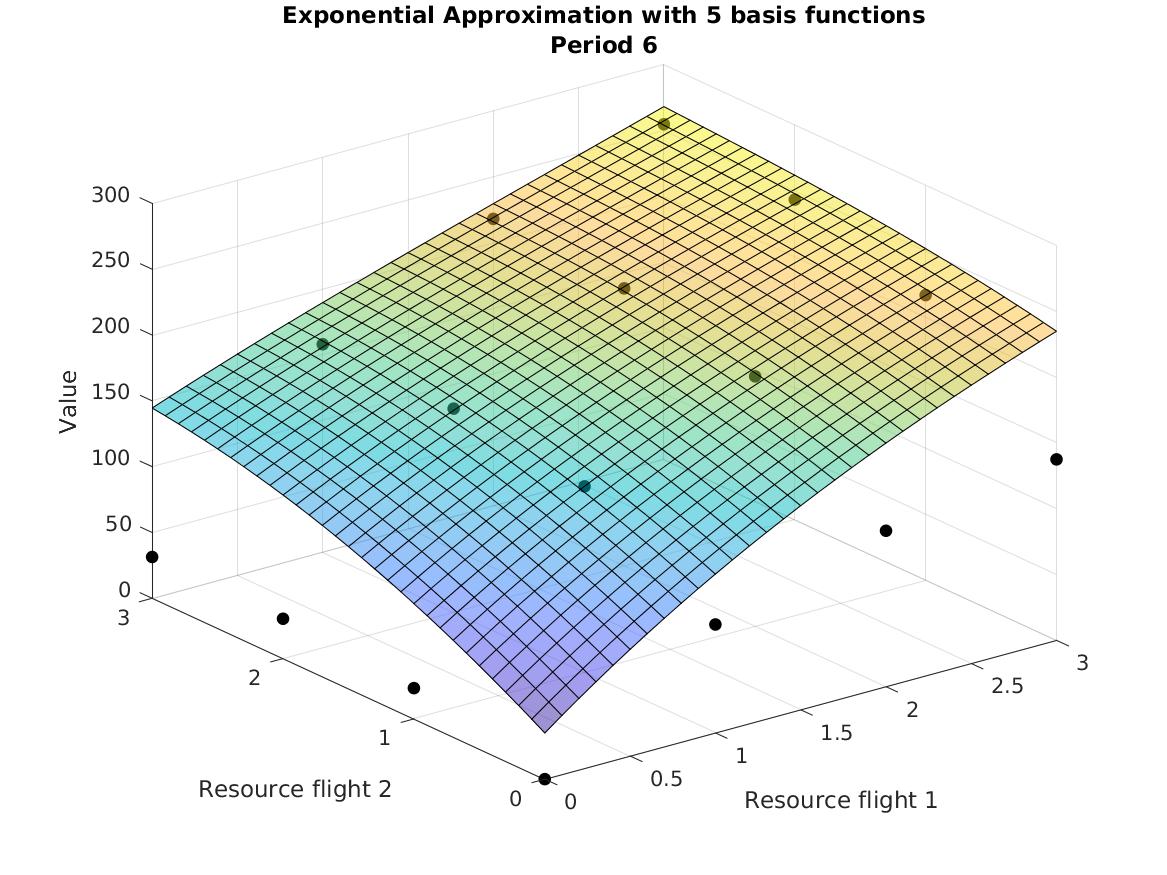

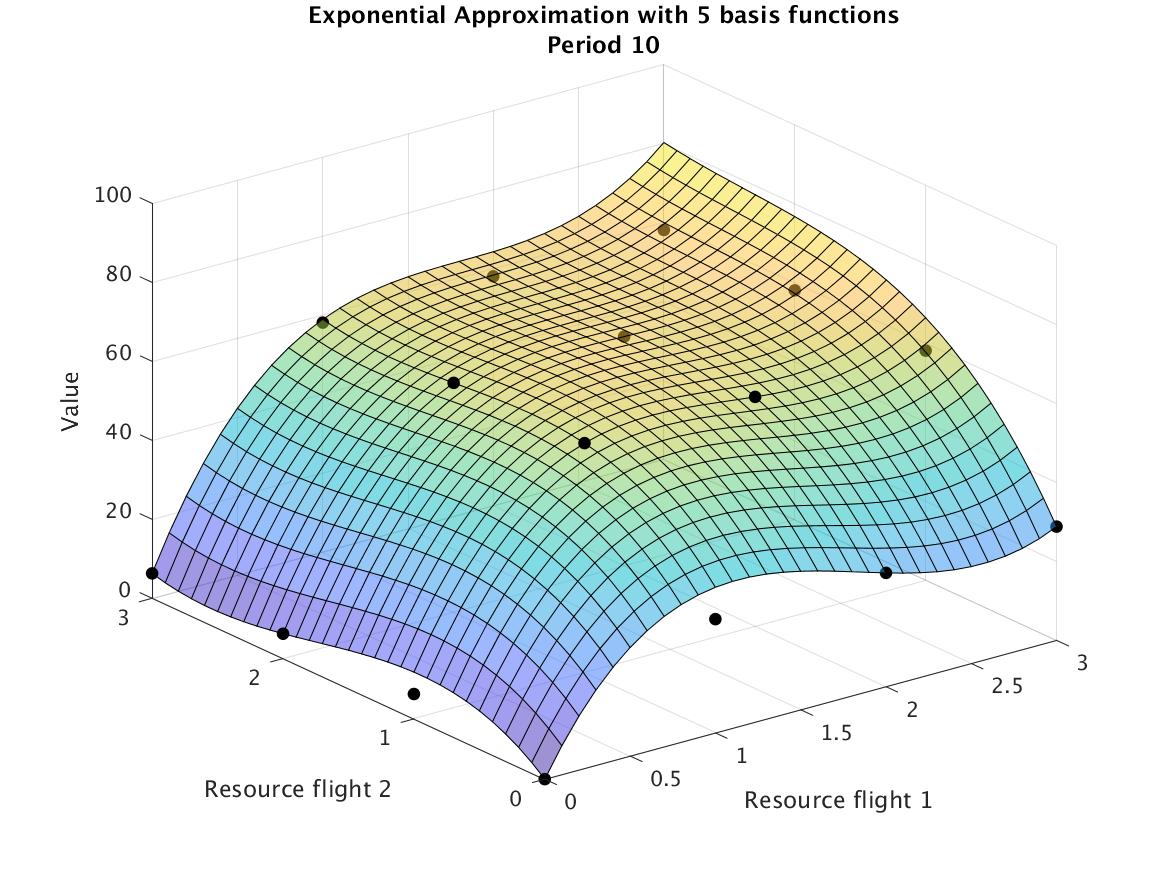

After generating 60 time-dependent hat basis functions (6 per period of time), H-2PIAlg struggled to generate new rows. H-2PIAlg ran for more than 12 hours without converging, whereas the algorithm converged in 28 seconds after generating only 10 exponential ridge basis functions. More specifically, H-2PIAlg achieved an average revenue of 397.2 when simulating policy (2), which is very close to the optimal value function , computed using value iteration. As a result, we selected exponential ridge basis functions for subsequent numerical experiments. More details on the performance of H-2PIAlg on this toy example can be found in the Appendix. There we also provide graphical illustration showing that the more exponential ridge basis functions H-2PIAlg adds, the better the approximated value function fits the optimal value function.

7 Computational study

The objective of this section is to assess the performance of H-2PIAlg against strong benchmark methods in NRM. Section 7.1 details the computational specifications for H-2PIAlg, while Section 7.2 describes the methods we compare. Section 7.3 provides an overview of the datasets used in our experiments, and Section 7.4 examines the performance of H-2PIAlg.

7.1 Computational Specifications for H-2PIAlg

To implement H-2PIAlg we need to specify the following six inputs:

1. The baseline approximation :

When choosing the baseline approximation, recall that H-2PIAlg has two modes: the standalone mode and the add-on mode. To run the add-on mode, we first have to specify a baseline approximation and determine its parameters. We choose the Affine Approximation

| (AA) |

as proposed in Adelman (2007). This baseline approximation adds little computational burden (see Tong and Topaloglu (2013)). In addition, this choice of is linear in , so this basis function fulfills Property (b) (see Section 6), allowing an efficient generation of rows. Additionally, it provides a reasonable approximation of the real value function, addressing Property (c). Since the standalone version is not tractable for larger instances, we only report the results for the add-on mode here. Appendix D.3 compares the convergence of the standalone and add-on modes for smaller hub-and-spoke problem instances.

2. The class of basis functions :

As discussed in Section 6, we select from the set of exponential ridge basis functions. This choice allows H-2PIAlg to exploit nonlinearities and resource interactions.

3. The initial value of :

To fulfill constraint (10), we let for all .

4.The initial subset of constraints :

The initial subsets of constraints are , for all .

5. The stopping criterion for the Row Generation Algorithm:

Our stopping criterion is based on a bound for the optimality gap. To specify this, let denote the optimal objective value of linearized (AP). Similarly, let denote the minimum objective value of the tightened problem (AP)+(8) considering the reduced set of constraints . Let be the minus the objective value of (3) or (4) when evaluated at their global optima. Using Proposition 3 in Adelman (2007), we obtain the bound . For a given value of , stopping the Row Generation Algorithm when ensures that the estimate is less than larger than the true value .

We have defined as minus the (globally) optimal solutions of subproblems (3) and (4). If only locally optimal reduced costs are available, an alternative stopping criterion is to stop generating additional rows when . Since , we expect an algorithm with stopping criterion based on to run for shorter times. However, note that is not an upper bound for .

If the stopping criterion should be based on an upper bound , the dual bounds given by Knitro when solving subproblem can be used. Since H-2PIAlg might not solve all the subproblems for each period of time when generating rows (see Section 5.1), one would have to enforce the solution of subproblems for all time periods. However, such a stopping criterion would make H-2PIAlg intractable for large instances. Therefore, we calculate the upper bound only after the algorithm terminates according to a stopping criterion based on .

6. The stopping criterion for adding new basis functions:

Recall that every solution of the master problem with the reduced set of constraints provides a policy as specified in (2). For given values and , we simulate instances of this policy until the relative standard error of the average policy revenue is smaller than a given value ; i.e., until . We then stop generating additional basis functions and terminate the incremental algorithms if this average policy revenue is within from ; i.e., we stop adding basis functions if . Since , this criterion provides an optimality gap guarantee on the policy. In practice the user may decide not to wait until is fulfilled, but to stop earlier if a reasonably-good improvement (either in terms of estimated bound or simulated policy) is achieved. In our numerical experiments, we terminate the H-2PIAlg when either is met or when a CPU time of 168h is reached. More computational details can be found in Appendix C

7.2 Methods Under Comparison

The numerical experiments compare four methods. The Affine Approximation (AA) is used to evaluate the extent to which the proposed algorithm enhances the quality of an initial approximation. The Separable Piecewise Linear Approximation (SPLA) serves as a strong benchmark, as it is known for producing small optimality gaps. It can be computed via a linear program (Vossen and Zhang, 2015b). The Non-Separable Approximation (NSEP)111To run NSEP, we used the codes available in the Github repository https://github.com/slaume/Reductions-of-Non-Separable-ALPs-for-NRM. We chose what seemed the “best” performer in the hub-and-spoke instances of Laumer and Barz (2023). That is to say, in the Github code we set task = 2, i.e., we determined the partition for which the network measure is largest, which can then be used for NSEP4(I/q,q,gl.). As recommended by the authors, we then saved the partition set Icaln and reset the rest of the environment before running the code with task=1. lets us evaluate how much H-2PIAlg can improve upon an approximation with nonlinearities and resource interactions. Finally, H-2PIAlg with the specifications discussed in Section 7.1.

7.3 Instances, Code, and Hardware

We consider two types of network instances: the experimental setup specified in Adelman (2007) and the bus networks considered in Laumer and Barz (2023). The Hub-and-Spoke (H&S) instances of Adelman (2007) include up to 20 non-hub locations and 2 fares, resulting in up to single-leg itineraries and up to two-leg itineraries. Time horizons of up to 1,000 periods are considered. The capacities, specified in Section B of the Online Appendix, are chosen so that the load factor is roughly 1.6.

In the bus line examples provided in Laumer and Barz (2023), there are three types of instances: the Simple Bus Line (SBL), which consists of consecutive legs; the Consecutive Bus Lines (CBL), which combines multiple simple networks; and the Realistic Bus Line (RBL), a real-world example from a large European bus company. More details can be found in Laumer and Barz (2023), and the data for these instances are available on Github.

All experiments were conducted on the Mercury high-performance computing cluster at The University of Chicago Booth School of Business, with 50 GB of memory and 1 core utilized. The code is available in GitHub.

7.4 Numerical Results and Discussion

In this section, we compare the performance of the methods outlined in Section 7.2 in terms of Upper Bounds (UBs), Lower Bounds (LBs) corresponding to the average revenue when simulating policy (2), and computational times. For H-2PIAlg, we simulate the policy and calculate its average revenue for each . Although there is a tendency towards improvement with the increment of , the policy does not necessarily improve monotonically in . As a consequence, we report the highest average revenue found in that process. In other words, it might be the case that H-2PIAlg stopped at , and there was a such that , where is the average reward of the simulated policy for basis functions. So the LB corresponds to the best policy found, which is . Table 1 display UBs and LBs for the H&S and bus instances. More details about CPU times and the number of basis functions added by H-2PIAlg can be found in Section C of the Appendix.

| Upper bound (UB) | Policy (LB) | |||||||||

| SPLA | NSEP | AA | H-2PIAlg | SPLA | NSEP | AA | H-2PIAlg | |||

| Hub-and-Spoke instances (H&S) | ||||||||||

| 2 | ||||||||||

| ∗ | ||||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| 3 | ||||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| 5 | ||||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | † | † | |||||||

| 10 | † | † | ||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | † | † | |||||||

| 20 | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | |||||||||

| † | † | † | † | |||||||

| † | † | † | † | |||||||

| Bus instances | ||||||||||

| Simple (SBL) | ||||||||||

| Consecutive (CBL) | ||||||||||

| Realistic (RBL) | † | † | ||||||||

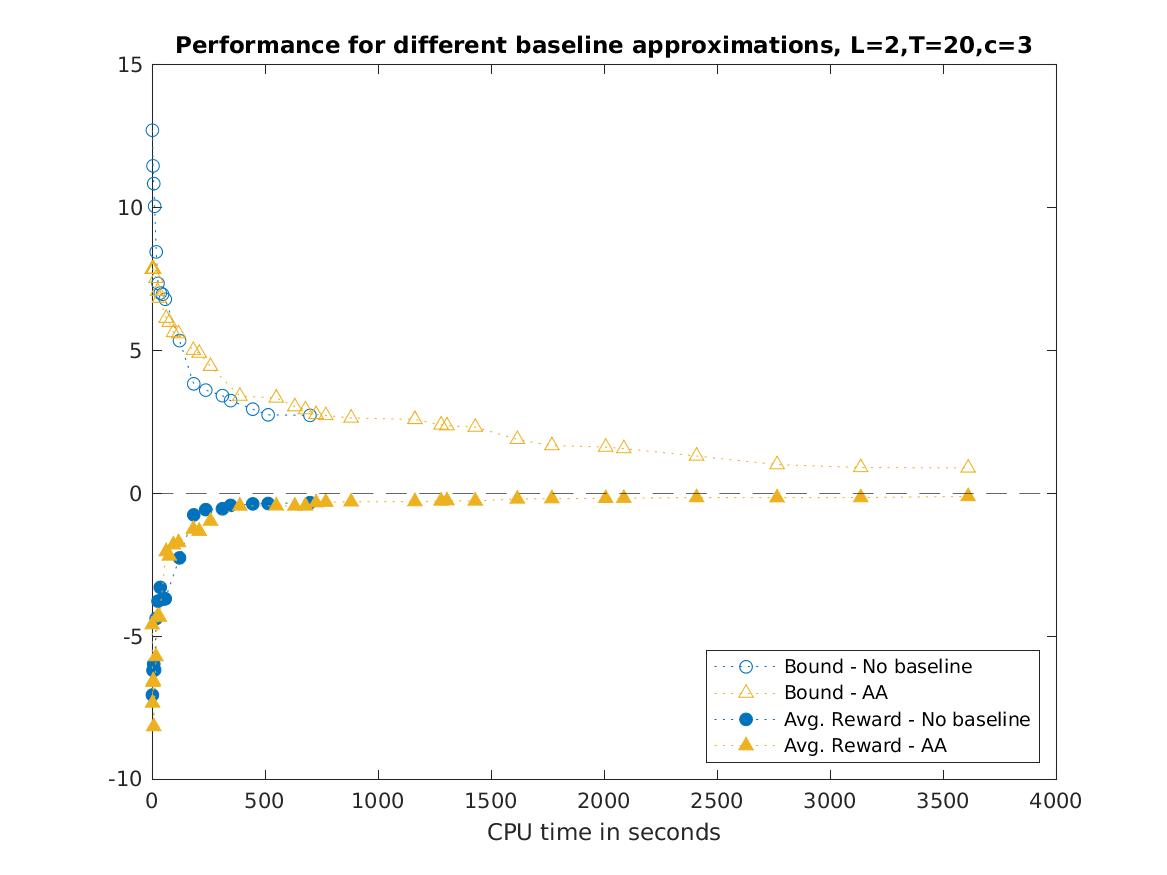

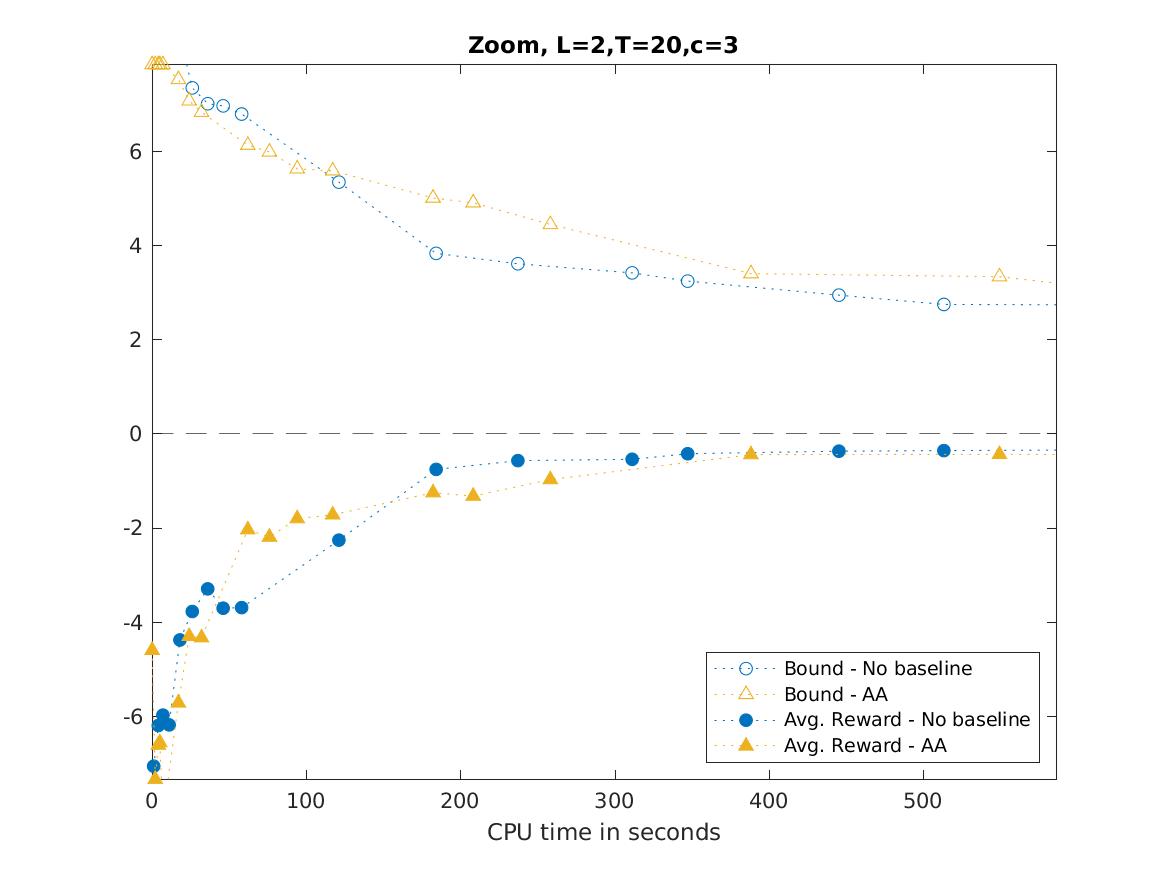

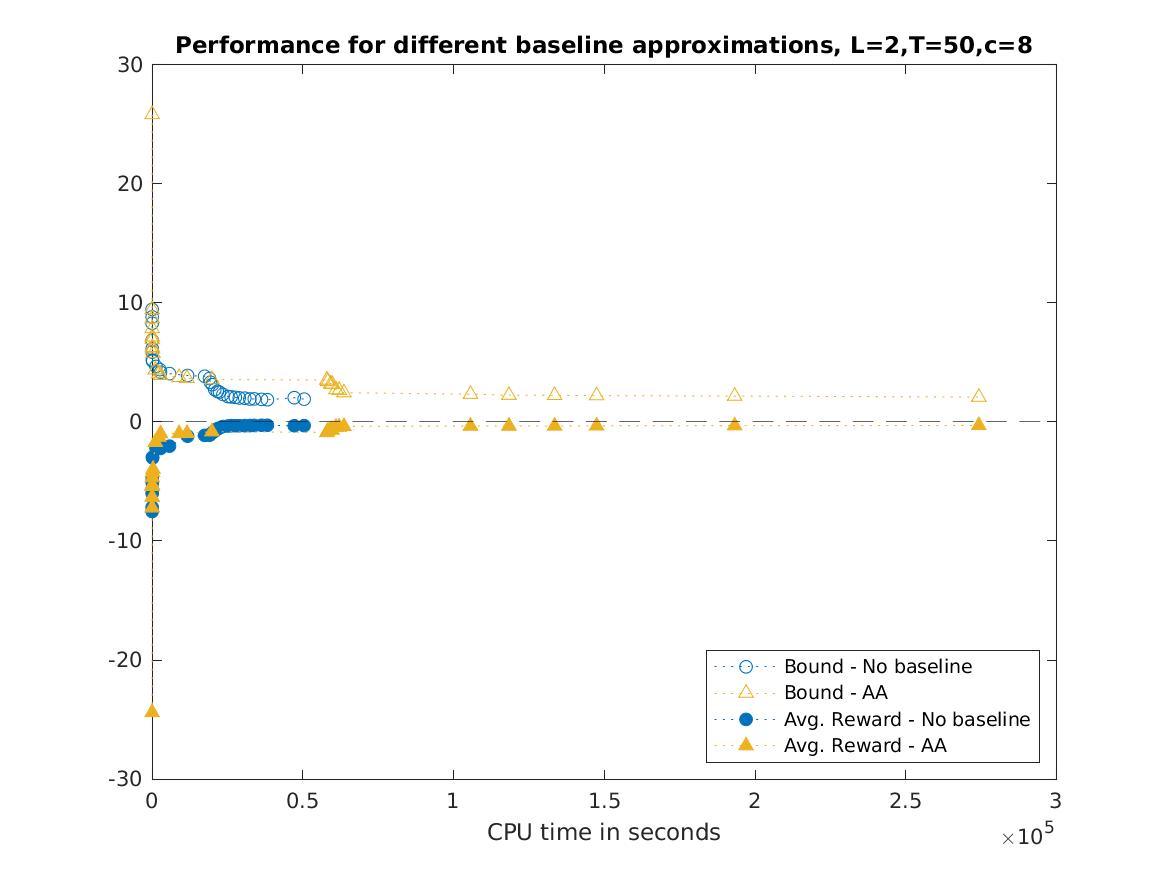

AA provides a tractable baseline approximation, with the smallest instances being solved in mere seconds and the largest instance taking less than 12 hours. We observe relative optimality gaps (UB vs. LB) below 20% for the smallest instances (H&S with , , and Bus instances). For the remaining cases, the gap exceeds 54%. For each , the worst performance is observed for moderate time horizons (), and performance generally deteriorates as increases. In particular, H&S scenarios with and exhibit the worst performance, with gaps exceeding 125% and thus leaving more room for improvement. In fact, although H-2PIAlg outperforms AA by improving both UBs and LBs across all instances, these latter H&S instances show the largest UB improvement, exceeding 28%. Interestingly, the most significant LB improvements occur in H&S instances with and large time horizons, yielding up to 37% more average revenue. More generally, for H&S instances with , UB and LB improvements remain above 10% and 15%, respectively. These improvements, however, come at a computational cost, with CPU times approaching the time limit set in the cluster.

Despite SPLA being a strong NRM benchmark, it fails to solve the largest instances in our numerical experiments due to memory limitations; those instances are marked with . For instances that do solve, computational times remain reasonable, always below 7253 seconds, and optimality gaps are often relatively small, particularly for H&S instances with larger time horizons. However, the larger the and the smaller the , the larger the gaps, exceeding 10% in some cases. H-2PIAlg capitalizes on this room for improvement to enhance SPLA’s UB and LB by up to 4% and 0.54%, respectively, for instances with short time horizons (SBL, CBL and H&S instances with ). These improvements come at a computational cost, ranging from 1.8h to 156h. For other instances, no improvement is observed. In fact, for the largest instances that SPLA solves (e.g., , ), SPLA produces a UB more than 9% better than H-2PIAlg. NSEP also fails to handle larger instances, marked with in Table 1. Among the small instances it could solve, NSEP outperformed SPLA, providing UBs and LBs that are nearly tight and close to optimal, with the largest gap being 3.4%. Despite this, for the smallest instances (, SBL, and CBL), H-2PIAlg generated better policies, achieving up to a 0.22% improvement in average revenue. While H-2PIAlg generally requires additional computational effort (e.g., 153 hours more for CBL), its runtime can also be shorter (e.g., 3.4 hours less for , ). However, the key advantage of H-2PIAlg over NSEP and SPLA lies in scalability: H-2PIAlg remains computationally feasible for larger instances, providing reasonable UB and LB values where the benchmarks cannot.

Discussion:

Summarizing, we find that H-2PIAlg is particularly competitive under two conditions: (1) in large problem instances, when SPLA and NSEP run out of memory, and (2) when capacity is very scarce. The reason behind (1) is its smaller complexity space. For instance, SPLA has variables and constraints, with . For the largest instance, this yields variables and constraints. In contrast, H-2PIAlg has a more manageable complexity. Instead of solving one large problem, namely (AP), our algorithm solves smaller problems (linear master program, the flow-balance problem (5), and subproblems (3) and (4)) multiple times. The linear master program consists of variables and constraints, where is iteratively increased through row generation. The number of basis functions, , is relatively small compared to and is incremented by one each time (5) is solved. This problem involves continuous variables and a single linear constraint. The nonlinear subproblems for row generation feature integer variables, binary variables, and linear constraints. Each iteration of the algorithm requires a exponential number of floating-point operations to solve the subproblems in the worst case. Although the dimension of the subproblems remain invariant across iterations, the shape of their objective functions become increasingly complex with , thereby increasing solution times. However, in our numerical experience we observe that the solution times are mainly driven by the LPs, whose sizes increase with . By progressively adding basis functions, H-2PIAlg incrementally increases the complexity of the problem and provides an approximation at every stage. If the problem becomes too complex to solve in later steps, solutions from earlier, simpler stages remain valid. As a result, this algorithm requires longer computational times compared to other approaches but allows to approximate significantly larger instances.

The reason for (2) is that the value function is more challenging to approximate in these scenarios, where non-separability and non-linearities play a significant role. Since the exponential ridge basis functions are able to exploit nonlinearities and interactions across all resources, H-2PIAlg adds multiple basis functions so that (NLA) is able to capture these intricate aspects of the value function. In fact, the shorter the time horizon, the larger the produced by H-2PIAlg (see Table 7 of the Appendix). This observation aligns with the findings in Laumer and Barz (2023), which indicate that the benefits of non-separability and non-linearity diminish as capacity increases. As also noted in Laumer and Barz (2023), NSEP is particularly effective at exploiting non-separability and non-linearity to improve upper bounds. However, because NSEP only models these within a small subnetwork and relies on affine approximations for all other resources, policies generated by NSEP do not show significant improvement compared to AA. Since H-2PIAlg allows for non-separability and non-linearity across all resources, its ability to enhance policies and obtain higher average revenues is superior.

8 Concluding Remarks and Extensions

In this paper we proposed a Nonlinear Incremental Algorithm (NLIAlg), which dynamically generates and optimizes basis functions for approximating value functions in NRM. The algorithm progresses through two main steps: (I) Estimate the weights and parameters of the approximation (NLA) with fixed number of basis functions using a row generation algorithm, and (II) Increase until the approximation is deemed satisfactory according to user-specified criteria. This approach allows for iterative improvements, balancing dimensionality and accuracy. In addition, NLIALg stands out as the first algorithm to optimize new basis functions rather than sampling them (see Bhat et al. (2023) and Pakiman et al. (2020)).

To address large instances, the Two-Phase Incremental Algorithm (2PIAlg) estimates the parameters in two phases within Step (I). In Phase (i), the parameters of the basis functions are estimated following the flow imbalance ideas introduced by Adelman and Klabjan (2012). In Phase (ii), the remaining parameters of the approximation are estimated by solving the master problem with fixed basis function parameters, which simplifies the problem into an LP. This constitutes the first application of the flow-balance methodology in a stochastic setting.

Both NLIAlg and 2PIAlg can be used either in (1) Standalone mode to find a suitable value function approximation from scratch, or in (2) Add-on mode, to enhance a given value function approximation. Our numerical results show that NLIAlg and 2PIAlg in standalone mode are practical only for toy problems. However, the heuristic version of 2PIAlg (H-2PIAlg) on add-on mode with the Affine Approximation (AA) and exponential ridge basis functions (9) can solve instances so large that the benchmark NRM methods SPLA (Vossen and Zhang, 2015a) and NSEP (Laumer and Barz, 2023) run out of memory. In addition, in these instances H-2PIAlg provides significantly better policies and upper bounds than AA. Moreover, H-2PIAlg is able to improve the policies of SPLA, NSEP and AA for those instances where capacity is scarce.

A potential future direction is exploring hybrid policies that combine the strengths of SPLA and our proposed method. For instance, using SPLA early in the booking period and switching to our approach later could yield significant benefits. Optimizing this transition point through methods such as line search or advanced policy search approaches could be a valuable extension of this work. Moreover, adapting our methodology to other stochastic dynamic programming problems beyond NRM is a promising avenue for future research. Finally, investigating the theoretical convergence of our approach in a broader Markov decision process context would also be an interesting line of research.

Appendices

Appendix A Additional theoretical results and proofs

A.1 Norm-Constrained Convex Ridge Basis Functions Give Rise to DC Optimization problems

Basis functions that are convex or concave in and give rise to optimization problems in our algorithms whose objective and constraints are difference-of-convex (DC) functions222 We call a function a DC function if it can be expressed as the difference of two convex functions, i.e., if , where are convex functions. Moreover, we say an optimization problem is a DC program if are DC functions. . Under such a choice of basis functions, running NLIAlg implies solving a large DC master problem and low-dimensional integer DC problems for row generation. 2PIAlg entails solving a large linear master program, low-dimensional integer DC problems for row generation, and low-dimensional continuous DC problems for basis function generation. For convenience, the following proposition gathers these statements and characterizes the structure of the value function approximation.

Proposition 4

Let be convex (resp. concave) in and , and let the baseline approximation be concave on . Then:

Proof.

Proposition 4: Proposition 2.1 in Horst and Thoai (1999) claims that any finite linear combination and product of DC functions is also DC. According to this statement, (i) and (ii) are fulfilled. In addition, Proposition 2.1 in Horst and Thoai (1999) also claims that the absolute value of a DC function is still DC, rendering (5) a DC program. ∎

A.2 Supporting Lemma for Theorem 1

The following lemma that is essential for proving Theorem 1.

Lemma 1

For any value function approximation and any dual variables the following decomposition applies

| (11) |

where

and .

A.3 Proofs of all results in the manuscript

Proof.

Proposition 1: Let denote the dual problem with basis functions. Let be the dual problem where a violated flow-balance constraint has been added; i.e. and the following violated constraint for has been added. Then, (D.FB) reads:

| (12) |

Let and be the optimal solutions to and , respectively. The solution leads to and hence violates (12). Thus, is not a feasible solution for . In contrast, is feasible to . Because is the unique and optimal solution to ,

Because the feasible region of does not contain , the optimal objective value of is (strictly) smaller than that of . Strong duality then implies that linearized (AP) with the new variables and new basis function reduces the previous upper bound. ∎

Proof.

On the other hand, because and for all , we have that

where the last equality holds due to . Since by assumption, we cannot have for all , . In fact, we need

∎

Proof.

Proposition 3:

For given , a lower bound of the basis function (9) can be found by solving

Since the objective function is monotone decreasing in , we can write this problem as

This objective function is monotone increasing in every with and monotone decreasing in given . Hence, the optimal value of the previous problem is upper bounded by the optimal objective of the following program

Appendix B Additional details on the algorithms

B.1 Flow-imbalances including monotonicity constraints

We use dual variables for the constraints defined in , and for the monotonicity constraints . Then the dual formulation of the approximate LP including monotonicity constraints is

| (Dμ) | ||||

| s.t. | ||||

| (D.FBμ) |

This yields the flow-imbalance functions

B.2 Pseudocodes

Appendix C Computational details

At the end of each row generation cycle, we simulate the policy given by (2) to determine if our estimate of is close enough to the simulated average policy revenue and the algorithm is stopped, or if we should generate another basis function. To obtain the average policy revenue for a given value function approximation we

-

0.

let ;

-

1.

simulate the policy given by (2) for one instance, i.e. one departure date, and save the total revenue obtained as ;

-

2.

compute the average policy revenue as well as the standard error of . ;

-

3.

If , the simulation is stopped, otherwise and go to 1.

In our numerical experiments, we used .

For the stopping criteria, we used and . For the H-2PIAlg, Knitro was used to solve the linear master program, the nonlinear integer subproblems, and the nonconvex continuous flow-balance maximization problem. To further improve computational performance, we chose time limits of 5 seconds to solve the subproblems. For the NLIAlg, the global solver Baron was used to solve any DC problem.

Finally, Table 2 summarizes the capacities of the hub-and-spoke instances generated for each number of non-hub locations and time periods .

| 2 | 3 | 5 | 10 | 20 | |

| 20 | 3 | 2 | 2 | 1 | 1 |

| 50 | 8 | 6 | 4 | 2 | 1 |

| 100 | 17 | 12 | 8 | 5 | 2 |

| 200 | 33 | 25 | 17 | 9 | 5 |

| 500 | 83 | 62 | 41 | 23 | 12 |

| 1000 | 165 | 124 | 83 | 45 | 24 |

Appendix D Additional Numerical Results

D.1 Comparing the performance of H-2PIAlg with hat versus exponential ridge basis functions

Piece-wise linear hat functions, also known as hat functions or B-splines of degree 1, could take the following form in our our NRM setting

| (15) |

where not only the -dimensional parameter vector but also the -dimensional vector need to be estimated via maximizing flow imbalances. To generate a new basis function with of the form (15), H-2PIAlg needs to solve a MINLP with approximately constraints in the worst-case scenario, where is the number of rows generated for period . When is large, as it will be for moderately to large instances, the use of hat functions impractical. In contrast, generating exponential basis functions entails solving a continuous problem with variables and one constraint. We considered modifying (15) by parametrizing basis functions over time, specifically generating basis functions with parameters and breakpoints for . While this increases the dimensionality of our approximation, it allows for the decomposition of the flow-imbalance maximization problem.

The toy example discussed in Section 6.2 uses the fares and arrival probabilities specified in Table 3. Results reported in Section 6.2 were computed using Knitro. To further assess the tractability of piecewise linear basis functions, we attempted to use Gurobi instead of Knitro for row generation in H-2PIAlg with hat basis functions. We chose Gurobi because it can convert the subproblem, which involves products of bounded continuous variables and binary variables, into an LP. However, after generating 90 basis functions (9 per period of time), Gurobi also struggled to produce new rows.

| low fare | high fare | |||||

| AB | BC | AC | AB | BC | AC | |

| 20 | 30 | 42 | 100 | 150 | 210 | |

| 0.3 | 0.1125 | 0.1875 | 0.1 | 0.0375 | 0.0625 | |

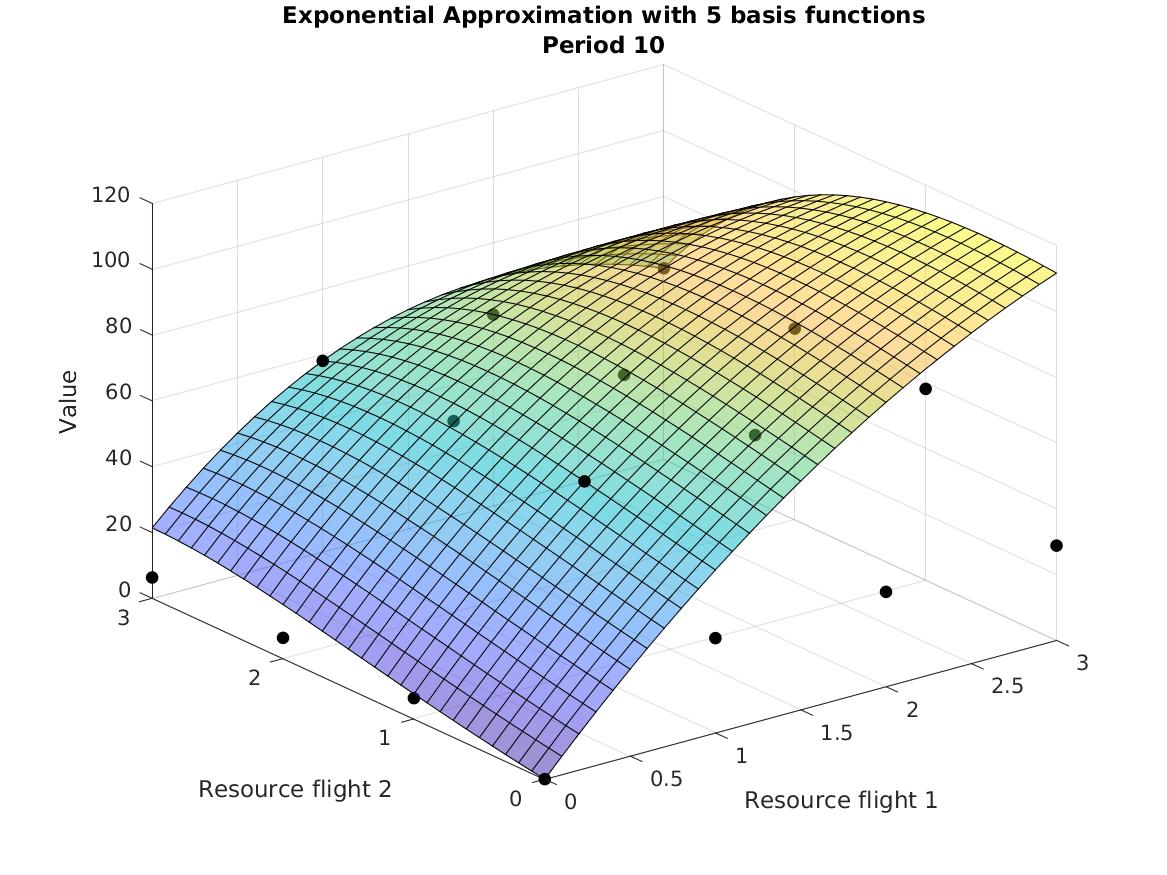

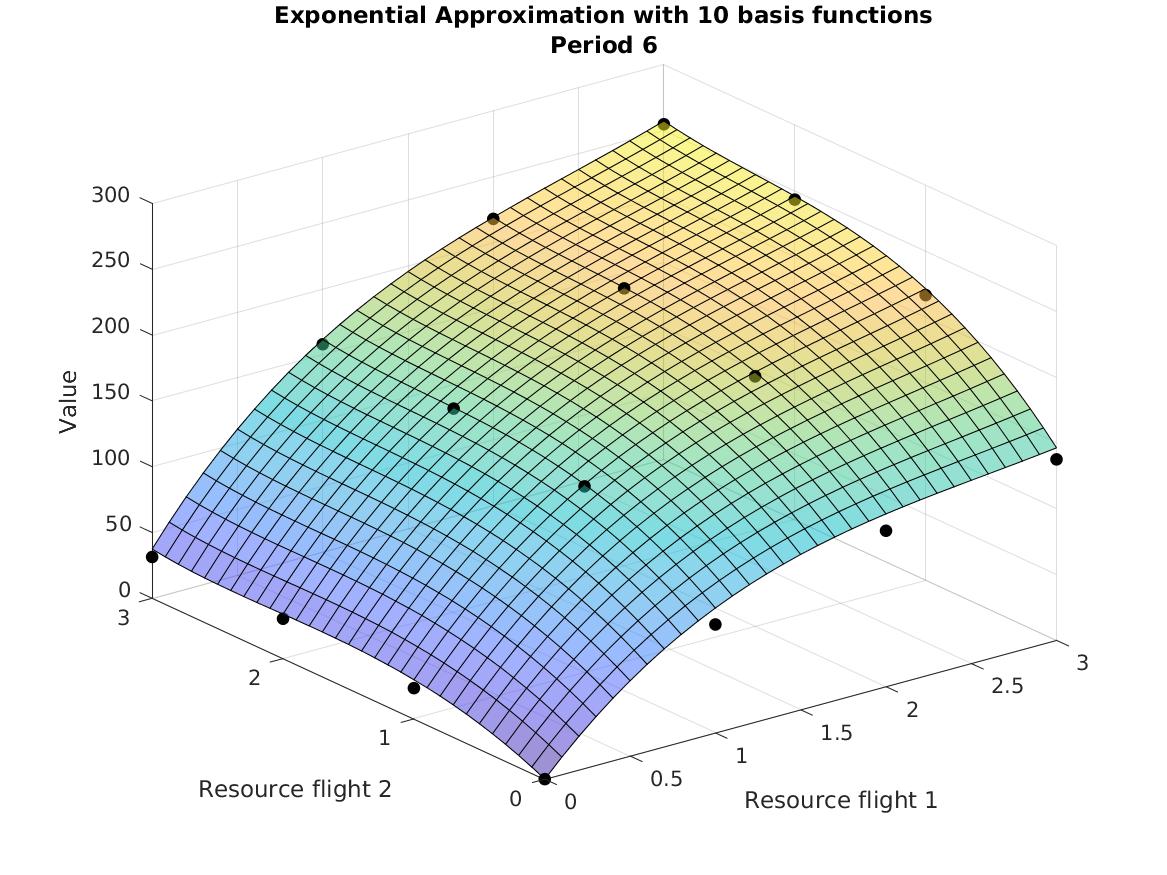

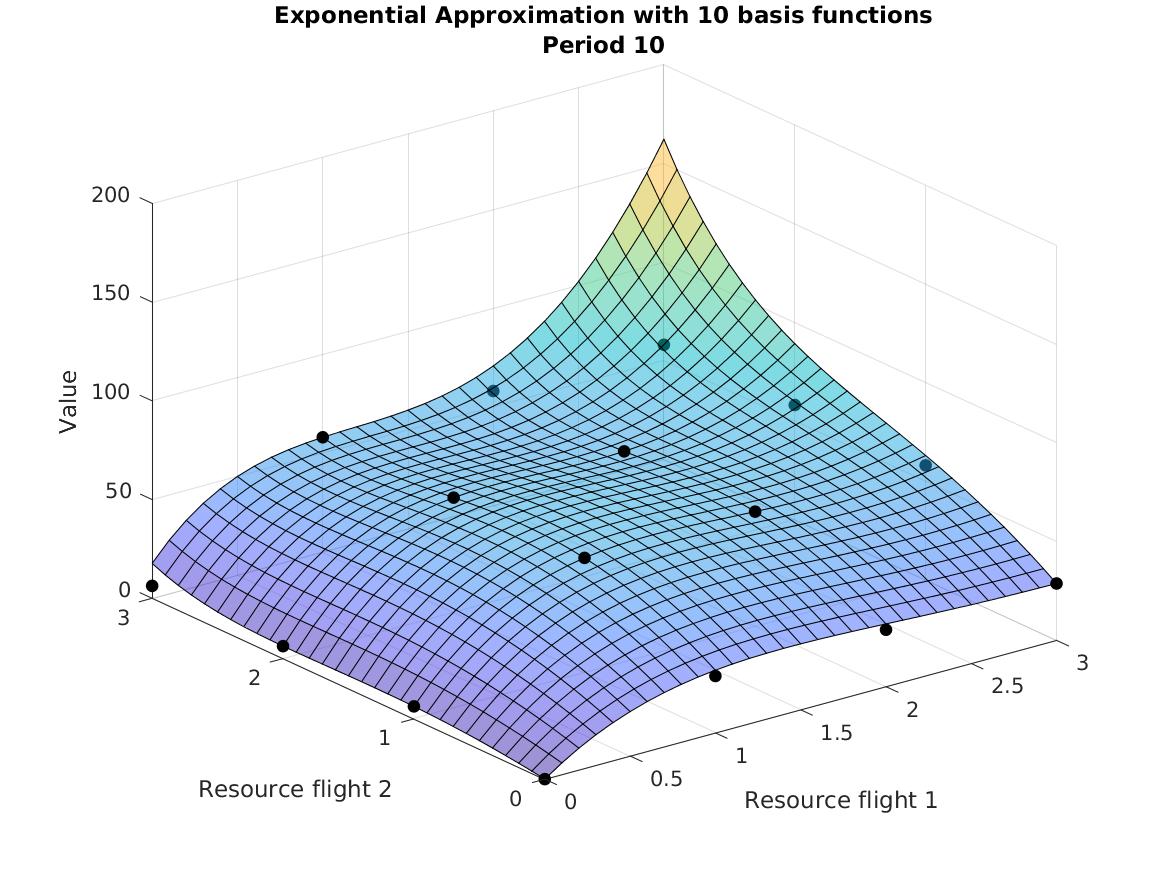

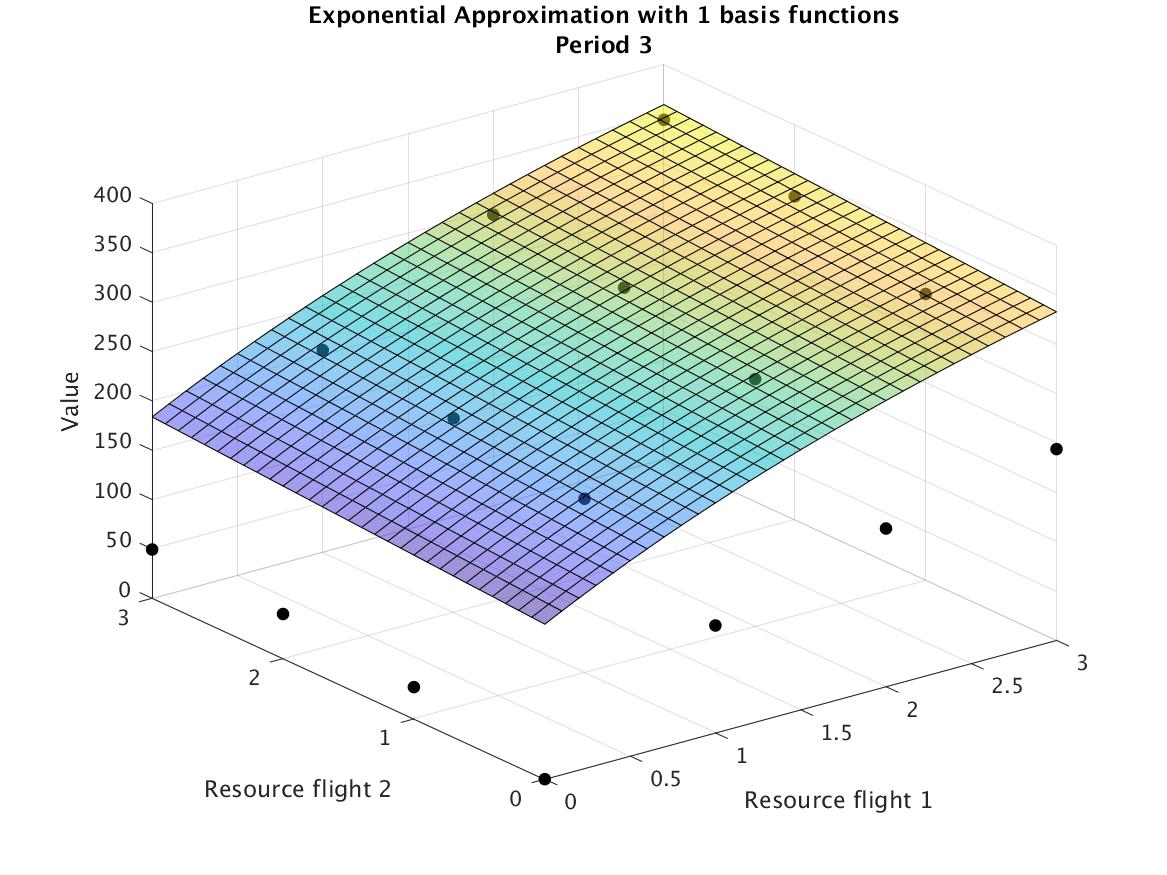

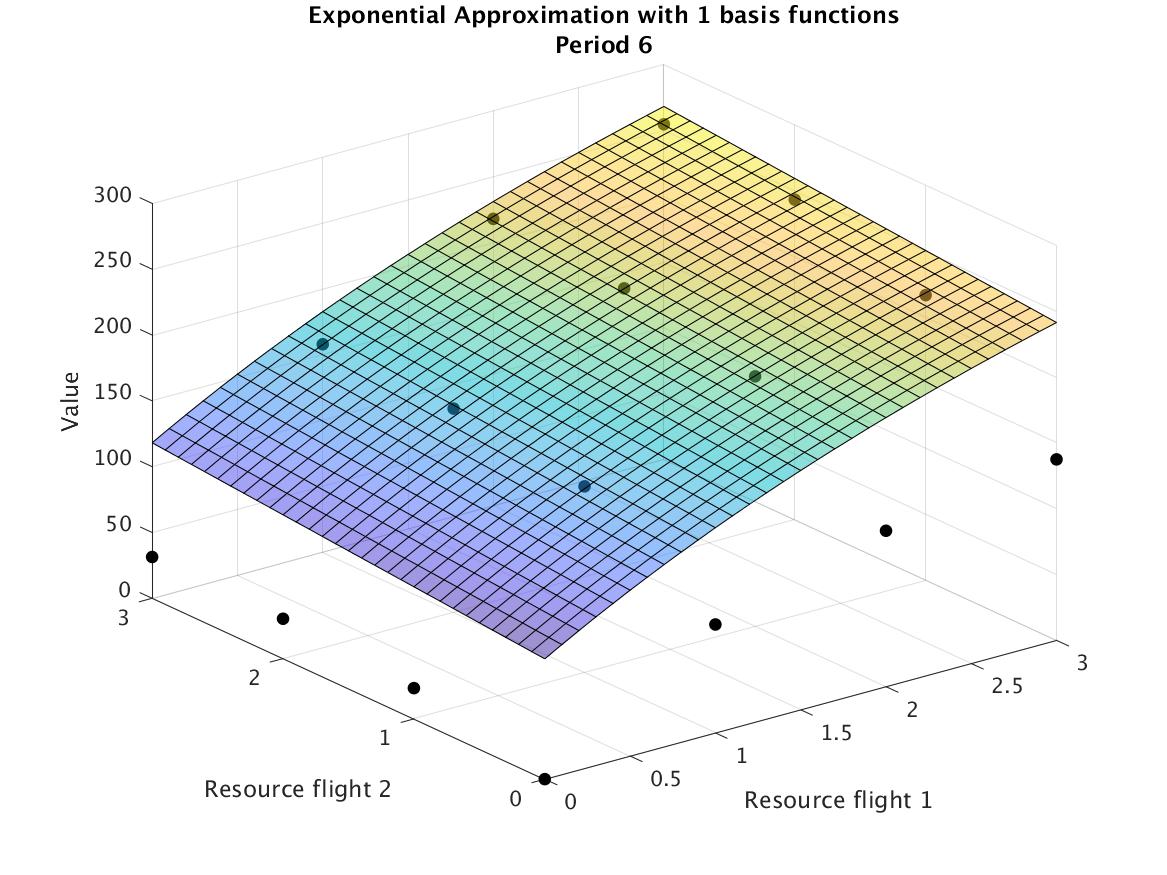

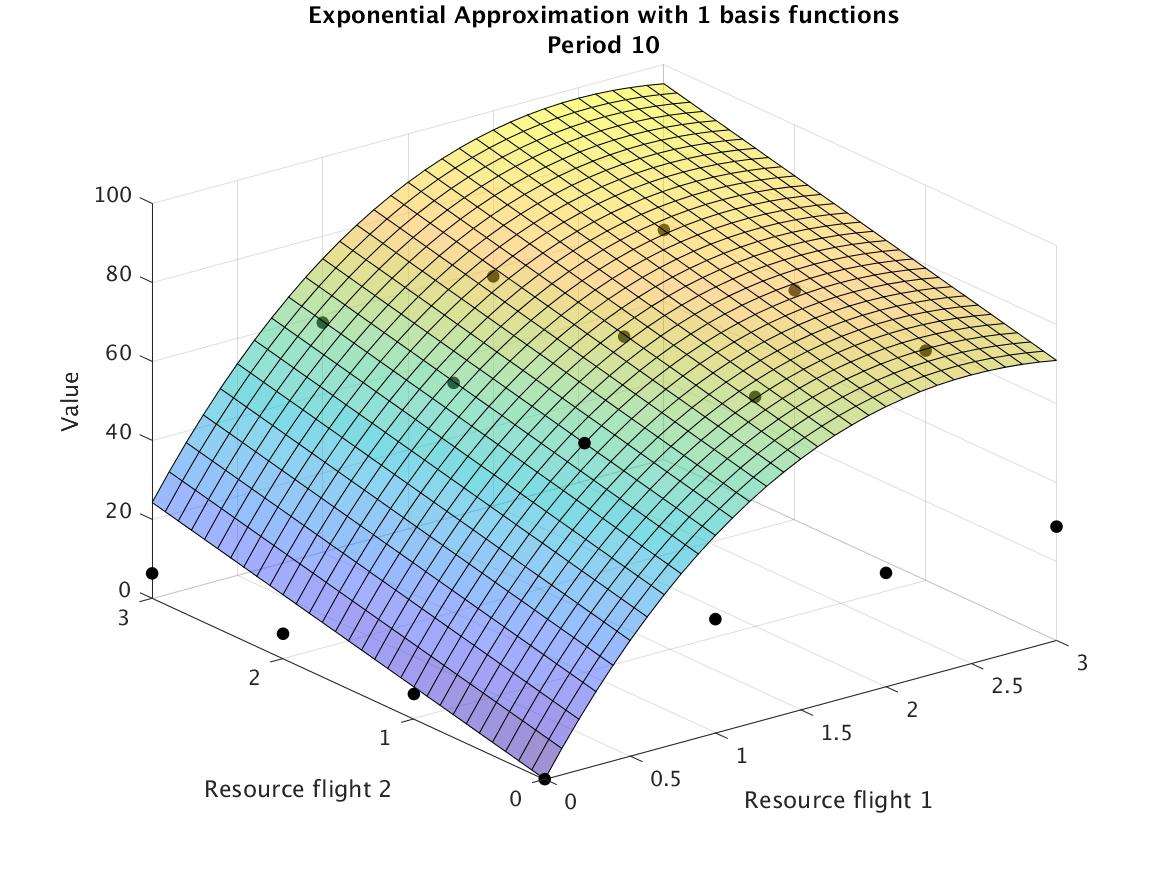

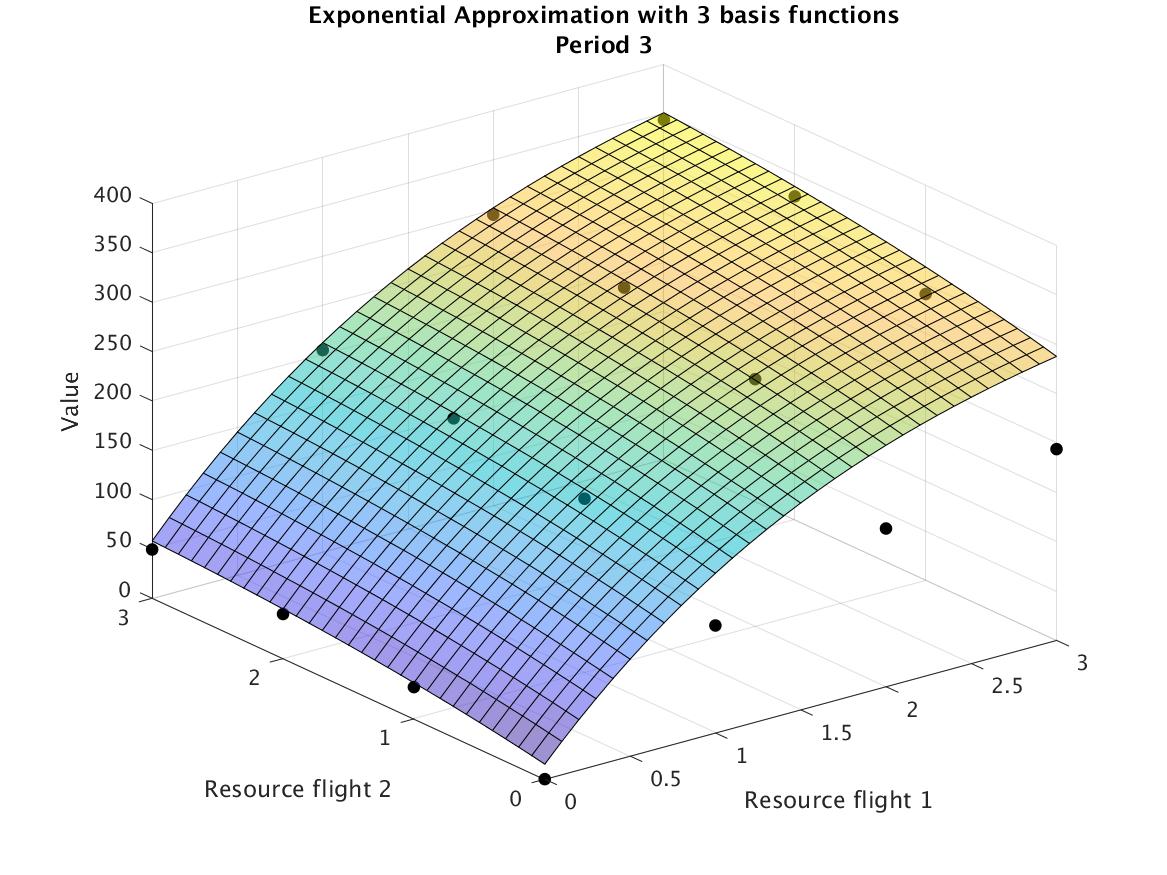

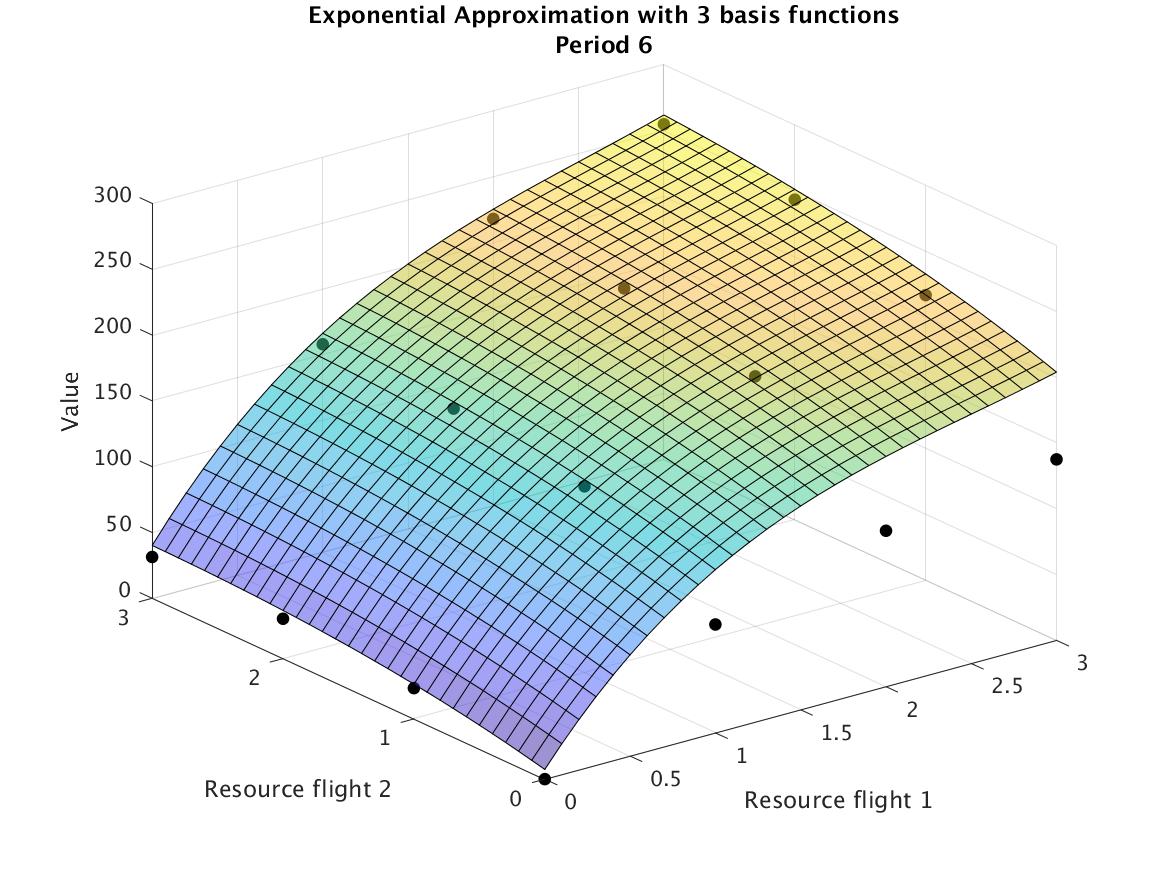

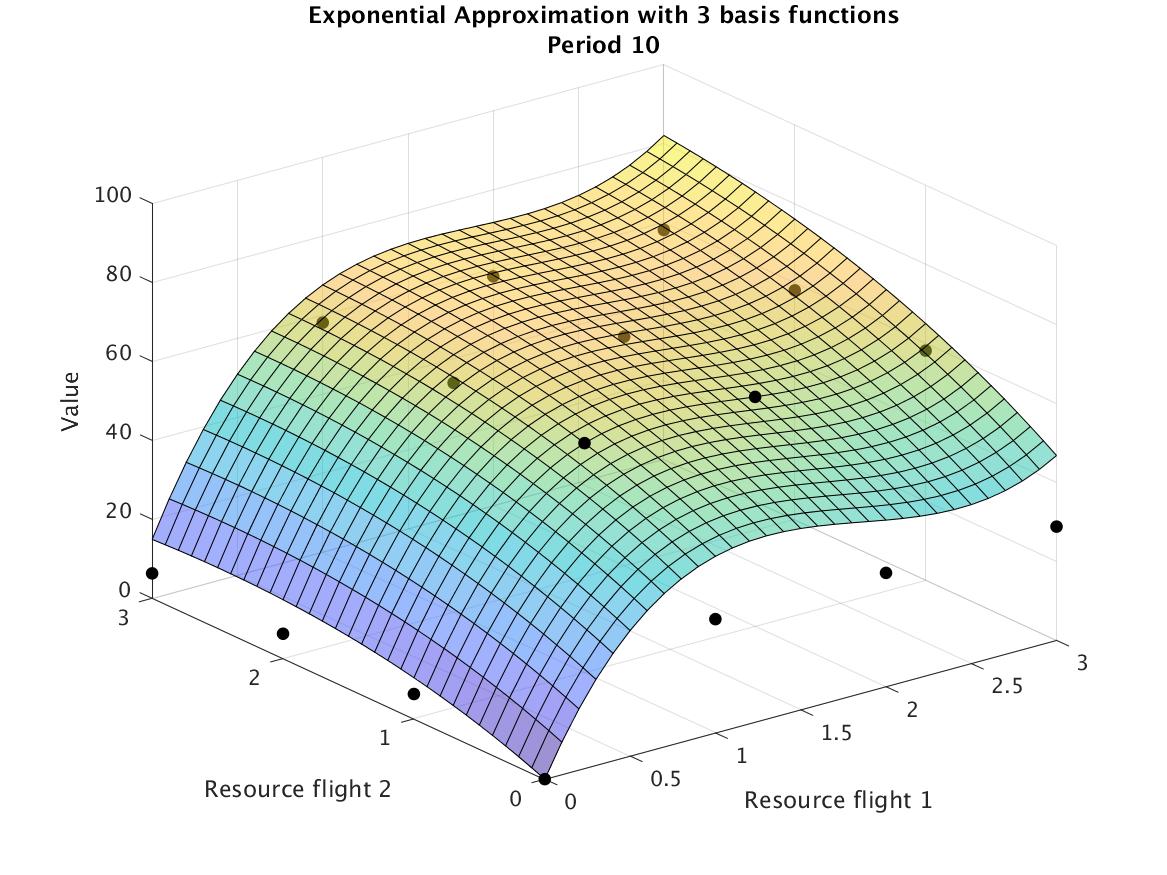

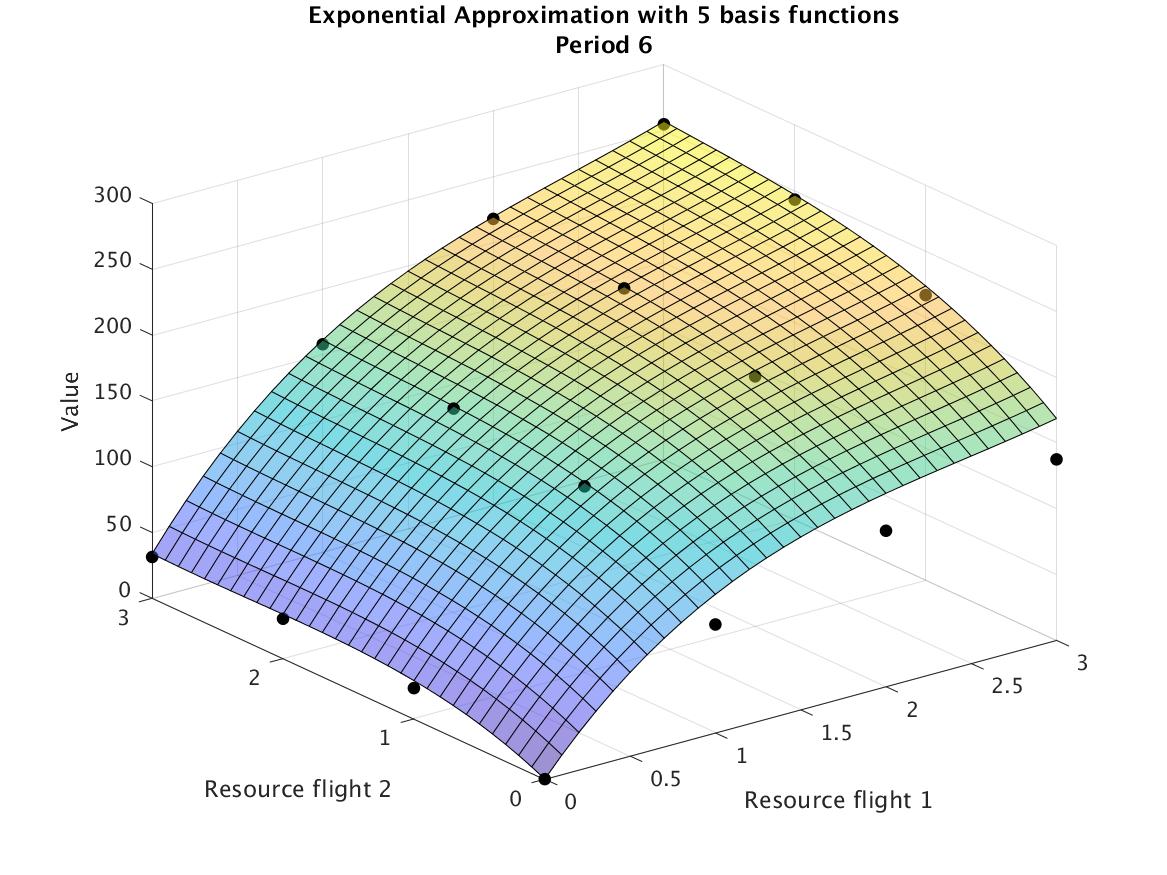

Table 4 provides the upper bounds, average revenues obtained by simulating policy (2), and CPU times in seconds for H-2PIAlg using exponential ridge basis functions. Figure 1 visualizes the different iterations of the H-2PIAlg in this small example. The black dots represent the true values , computed using value iteration, for some periods . The surface corresponds to the approximated function after basis functions have been added. Plots in the first row show the results of the affine approximation for comparison. The following lines show the corresponding pictures of the H-2PIAlg for and 8. We can observe that the more basis functions the H-2PIAlg adds, the more the surface resembles the true value function, fitting the optimal value function at the discrete points representing feasible states.

| H-2PIAlg | |||

| Time | |||

| 1 | 448.5 | 324.2 | 0 |

| 2 | 430.4 | 386.2 | 1 |

| 3 | 420.5 | 387.1 | 4 |

| 4 | 419.6 | 387.1 | 6 |

| 5 | 418.1 | 385.3 | 8 |

| 6 | 412.4 | 393.7 | 11 |

| 7 | 411.5 | 394.5 | 13 |

| 8 | 404.1 | 395.7 | 21 |

| 9 | 401.8 | 395.0 | 25 |

| 10 | 399.5 | 397.2 | 28 |

|

|

|

|

|

|

|

|

|

|

|

|

D.2 Results from NLIAlg

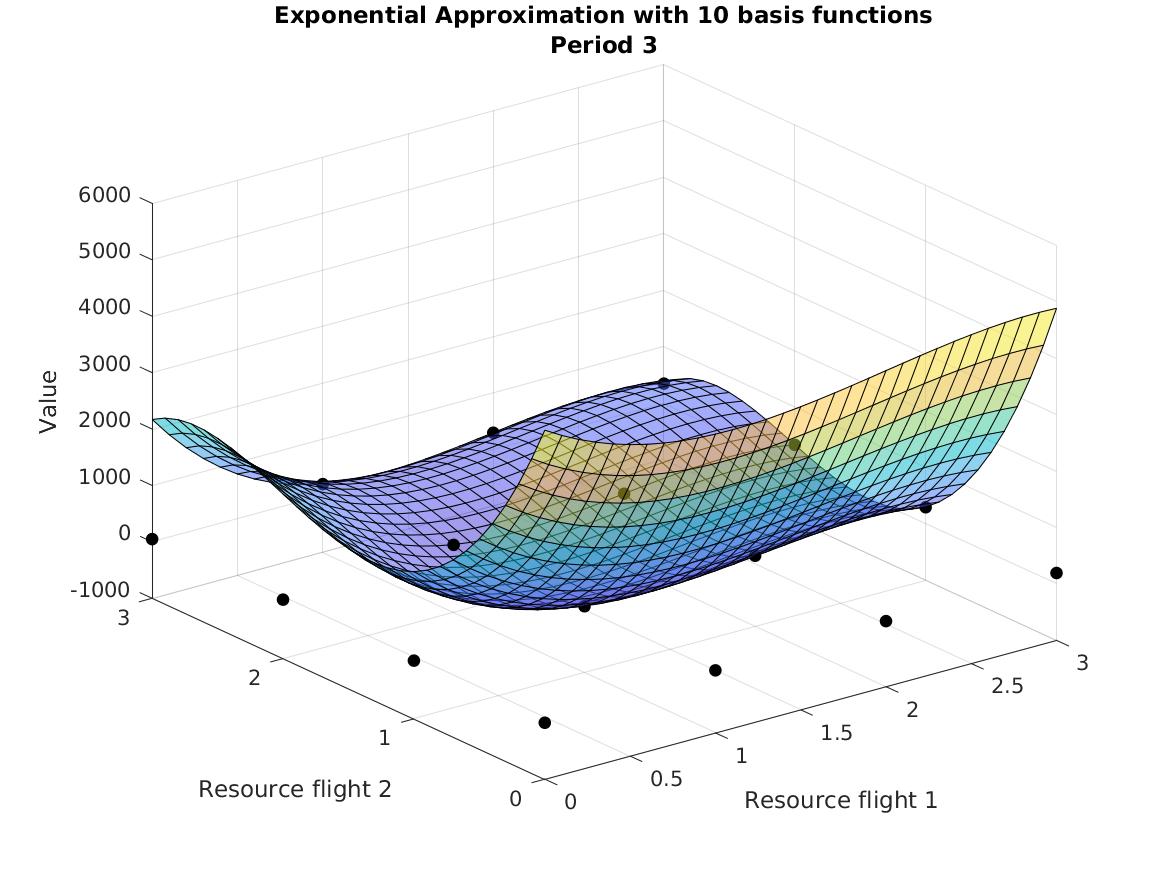

Table 5 displays the upper bound, simulated average reward and CPU time in seconds for the approximation provided by NLIAlg as the number of basis functions increases.

| NLIAlg | |||

| Time | |||

| 1 | 418.7 | 385.1 | 1813 |

| 2 | 410.9 | 388.9 | 3022 |

| 3 | 405.7 | 394.2 | 3627 |

| 4 | 401.4 | 396.6 | 4846 |

| 5 | 400.4 | 397.1 | 5157 |

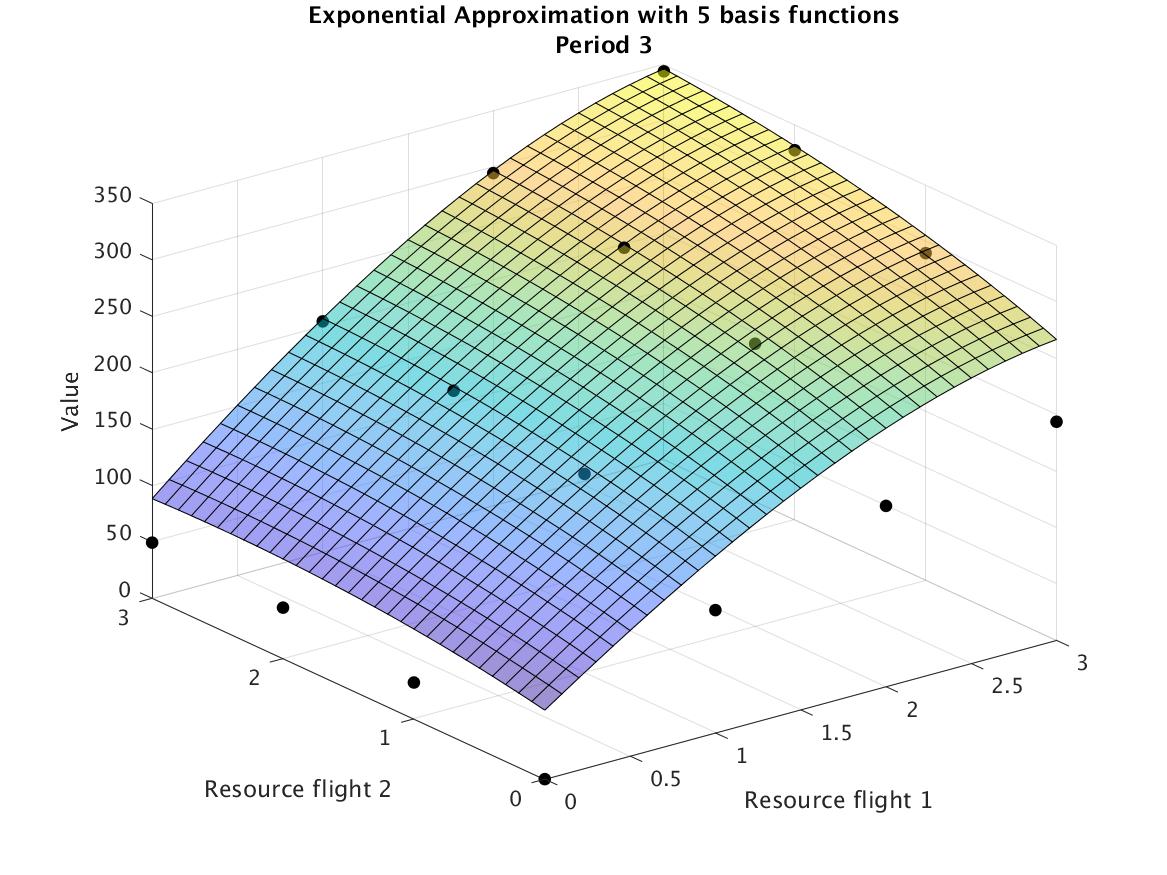

Figure 2 shows the fitting of the value function estimated via the NLIAlg in the toy example introduced in Section 6.2. The black dots represent the true values , computed using value iteration. The surface corresponds to the approximated function after basis functions have been added. The first, second and third rows of the figure show the fitting of the NLIAlg for and 5.

|

|

|

|

|

|

|

|

|

To further assess the tractability of NLIAlg, Table 6 compares the NLIAlg against the H-2PIAlg for the smaller hub&spoke instance in the paper. In this case, not only the NLIAlg takes longer than the H-2PIAlg, but the complexity of the DC master problem seems to make it difficult for the global solver to find a good solution within a reasonable time limit, affecting the convergence and the stability of the algorithm. This supports our decision to focus on the H-2PIAlg.

| NLIAlg | H-2PIAlg | |||||

| Time | Time | |||||

| 524.3 | 746.2 | 1223 | 873.9 | 773.5 | 35 | |

| 823.6 | 773.6 | 6347 | 864.1 | 786.2 | 70 | |

| 807.8 | 794.6 | 7873 | 860.9 | 792.4 | 106 | |

| 786.6 | 785.2 | 8495 | 858.6 | 794.0 | 144 | |

| 853.1 | 796.2 | 188 | ||||

| 852.7 | 795.8 | 227 | ||||

| 850.5 | 798.7 | 274 | ||||

| 849.4 | 799.6 | 319 | ||||

| 845.6 | 800.1 | 369 | ||||

| 840.8 | 802.8 | 426 | ||||

| 840.6 | 805.5 | 482 | ||||

| 836.1 | 806.0 | 545 | ||||

| 828.8 | 808.6 | 645 | ||||

| 824.1 | 809.1 | 721 | ||||

| 821.1 | 809.2 | 857 | ||||

| 821.0 | 809.4 | 1140 | ||||

| 819.8 | 809.4 | 1514 | ||||

| 819.6 | 809.6 | 1838 | ||||

D.3 Standalone versus Add-on Mode.

In this section we compare the two different modes of H-2PIAlg, namely

-

(1)

Standalone mode: find a suitable value function approximation from scratch; i.e. ,

-

(2)

Add-on mode: enhance a given value function approximation; i.e., .

For the add-on mode we choose the Affine Approximation (AA) because it exhibits Property (b); i.e., it is very tractable to generate rows since is linear in . In addition, it provides a reasonable approximation of the real value function.

We use the smallest instances of the experimental setup specified in Adelman (2007): 2 non-hub locations and 2 fares, low and high, resulting in single-leg itineraries and two-leg itineraries. The initial capacity is the same for each flight, i.e. for all . The values of and are chosen such that the load factor, i.e. the ratio of demand to supply, is approximately . Both fares and arrival probabilities are randomly generated. For these small problems with and , we can determine the true value function via value iteration, which takes 1,293 CPU seconds and 295,510 CPU seconds for the small and the large instances, respectively.

|

|

|

|

Figure 3 shows both the estimated upper bound and the simulated average revenue generated by the value function approximation of the H-2PIAlg when increasing , which translates in increasing CPU times. We report all bounds and average revenues as the relative difference with respect to the true value . More specifically, the normalization performed is

| (16) |

where represents the estimated upper bound or the average revenue of an approximation .

Since H-2PIAlg adds new basis functions to the baseline approximations, it is not surprising that they provide tighter estimates of upper bounds even for . Average simulated revenues of the improved approximations, i.e., for , are larger than the revenues obtained by the policies based on the baseline approximations with . The more basis functions are added (i.e., the larger the ), the lower the values of the objective function and the higher the simulated average revenues . Interestingly, the initial approximation does not seem to strongly affect the convergence of H-2PIAlg. In other words, for different initial approximations the H-2PIAlg converges to the same revenue . A similar value is also achieved regardless of the choice of .

D.4 CPU times and number of basis functions generated

| CPU times | H-2PIAlg Analysis | ||||||||

| SPLA | NSEP | AA | H-2PIAlg | H-2PIAlg+AA | Gap | K | |||

| Hub-and-Spoke instances (H&S) | |||||||||

| 2 | |||||||||

| † | |||||||||

| † | |||||||||

| † | |||||||||

| 3 | |||||||||

| † | |||||||||

| † | |||||||||

| † | |||||||||

| 5 | |||||||||

| † | |||||||||

| † | |||||||||

| † | † | ||||||||

| 10 | † | ||||||||

| † | |||||||||

| † | |||||||||

| † | |||||||||

| † | |||||||||

| † | † | ||||||||

| 20 | † | ||||||||

| † | |||||||||

| † | |||||||||

| † | |||||||||

| † | † | ||||||||

| † | † | ||||||||

| Bus instances | |||||||||

| Simple (SBL) | |||||||||

| Consecutive (CBL) | |||||||||

| Realistic (RBL) | † | ||||||||

References

- (1)

- Adelman (2004) Adelman, Daniel, 2004, A price-directed approach to stochastic inventory/routing, Operations Research 52, 499–514.

- Adelman (2007) Adelman, Daniel, 2007, Dynamic bid prices in revenue management, Operations Research 55, 647–661.

- Adelman and Klabjan (2012) Adelman, Daniel, and Diego Klabjan, 2012, Computing near-optimal policies in generalized joint replenishment, INFORMS Journal on Computing 24, 148–164.

- Bellman (1966) Bellman, Richard, 1966, Dynamic programming, Science 153, 34–37.

- Bhat et al. (2023) Bhat, Nikhil, Vivek Farias, Ciamac C Moallemi, and Andrew T Zheng, 2023, Nonparametric approximate dynamic programming via the kernel method, Stochastic Systems 13, 321–342.

- De Farias and Van Roy (2003) De Farias, Daniela Pucci, and Benjamin Van Roy, 2003, The linear programming approach to approximate dynamic programming, Operations research 51, 850–865.

- De Farias and Van Roy (2004) De Farias, Daniela Pucci, and Benjamin Van Roy, 2004, On constraint sampling in the linear programming approach to approximate dynamic programming, Mathematics of operations research 29, 462–478.

- Farias and Van Roy (2007) Farias, Vivek F, and Benjamin Van Roy, 2007, An approximate dynamic programming approach to network revenue management, Technical report, Working paper.

- Guestrin et al. (2003) Guestrin, Carlos, Daphne Koller, Ronald Parr, and Shobha Venkataraman, 2003, Efficient solution algorithms for factored mdps, Journal of Artificial Intelligence Research 19, 399–468.

- Horst and Thoai (1999) Horst, Reiner, and Nguyen V Thoai, 1999, DC programming: overview, Journal of Optimization Theory and Applications 103, 1–43.

- Klabjan and Adelman (2007) Klabjan, Diego, and Daniel Adelman, 2007, An infinite-dimensional linear programming algorithm for deterministic semi-markov decision processes on borel spaces, Mathematics of Operations Research 32, 528–550.

- Kunnumkal and Talluri (2016) Kunnumkal, Sumit, and Kalyan Talluri, 2016, On a piecewise-linear approximation for network revenue management, Mathematics of Operations Research 41, 72–91.

- Kunnumkal and Talluri (2019) Kunnumkal, Sumit, and Kalyan Talluri, 2019, Choice network revenue management based on new tractable approximations, Transportation Science 53, 1591–1608.

- Laumer and Barz (2023) Laumer, Simon, and Christiane Barz, 2023, Reductions of non-separable approximate linear programs for network revenue management, European Journal of Operational Research 309, 252–270.

- Lin et al. (2020) Lin, Qihang, Selvaprabu Nadarajah, and Negar Soheili, 2020, Revisiting approximate linear programming: Constraint-violation learning with applications to inventory control and energy storage, Management Science 66, 1544–1562.

- Pakiman et al. (2020) Pakiman, Parshan, Selvaprabu Nadarajah, Negar Soheili, and Qihang Lin, 2020, Self-guided approximate linear programs, Technical report, Working paper.

- Powell (2011) Powell, Warren B, 2011, Approximate Dynamic Programming: Solving the curses of dimensionality, volume 703 (John Wiley & Sons).

- Schweitzer and Seidmann (1985) Schweitzer, Paul J, and Abraham Seidmann, 1985, Generalized polynomial approximations in markovian decision processes, Journal of mathematical analysis and applications 110, 568–582.

- Sun and Cheney (1992) Sun, Xingping, and Elliott Ward Cheney, 1992, The fundamentality of sets of ridge functions, aequationes mathematicae 44, 226–235.

- Talluri and Van Ryzin (1998) Talluri, Kalyan, and Garrett Van Ryzin, 1998, An analysis of bid-price controls for network revenue management, Management science 44, 1577–1593.

- Talluri et al. (2004) Talluri, Kalyan T, Garrett Van Ryzin, and Garrett Van Ryzin, 2004, The theory and practice of revenue management, volume 1 (Springer).

- Tong and Topaloglu (2013) Tong, Chaoxu, and Huseyin Topaloglu, 2013, On the approximate linear programming approach for network revenue management problems, INFORMS Journal on Computing 26, 121–134.

- Topaloglu (2009) Topaloglu, Huseyin, 2009, Using lagrangian relaxation to compute capacity-dependent bid prices in network revenue management, Operations Research 57, 637–649.

- Trick and Zin (1997) Trick, Michael A, and Stanley E Zin, 1997, Spline approximations to value functions: linear programming approach, Macroeconomic Dynamics 1, 255–277.

- Vossen and Zhang (2015a) Vossen, Thomas WM, and Dan Zhang, 2015a, A dynamic disaggregation approach to approximate linear programs for network revenue management, Production and Operations Management 24, 469–487.

- Vossen and Zhang (2015b) Vossen, Thomas WM, and Dan Zhang, 2015b, Reductions of approximate linear programs for network revenue management, Operations Research 63, 1352–1371.

- Zhang (2011) Zhang, Dan, 2011, An improved dynamic programming decomposition approach for network revenue management, Manufacturing & Service Operations Management 13, 35–52.

- Zhang and Adelman (2009) Zhang, Dan, and Daniel Adelman, 2009, An approximate dynamic programming approach to network revenue management with customer choice, Transportation Science 43, 381–394.