On Distributional Discrepancy for Experimental Design with General Assignment Probabilities

Anup B. Rao Peng Zhang

Adobe Research Rutgers University

anuprao@adobe.com pz149@rutgers.edu

Abstract

We investigate experimental design for randomized controlled trials (RCTs) with both equal and unequal treatment-control assignment probabilities. Our work makes progress on the connection between the distributional discrepancy minimization (DDM) problem introduced by Harshaw et al., (2024) and the design of RCTs. We make two main contributions: First, we prove that approximating the optimal solution of the DDM problem within even a certain constant error is NP-hard. Second, we introduce a new Multiplicative Weights Update (MWU) algorithm for the DDM problem, which improves the Gram-Schmidt walk algorithm used by Harshaw et al., (2024) when assignment probabilities are unequal. Building on the framework of Harshaw et al., (2024) and our MWU algorithm, we then develop the MWU design, which reduces the worst-case mean-squared error in estimating the average treatment effect. Finally, we present a comprehensive simulation study comparing our design with commonly used designs.

1 Introduction

Randomized Controlled Trials (RCTs) are the “gold standard” for estimating the causal effects of a new treatment (Hernán and Robins,, 2010; Morgan and Winship,, 2014; Imbens and Rubin,, 2015). In an RCT, experimental units are randomly assigned into one of two groups: a treatment group, which receives the new treatment, and a control group, which receives the standard treatment. The outcomes of these groups will be compared to estimate the causal effects of the new treatment. Ideally, the two groups are “similar”, so the only difference is the treatment they receive. The design of an RCT refers to the distribution of the random assignment. It involves a trade-off between balancing observed covariates and being robust to unobserved confounders and model misspecification. This trade-off was first introduced by Efron, (1971) and has been central in commonly used designs, such as randomized blocking, pairwise matching, and rerandomization.

A recent breakthrough by Harshaw et al., (2024) introduced the Distributional Discrepancy Minimization (DDM) problem, offering a precise mathematical framework for balancing covariates while preserving robustness. This approach achieved a nearly optimal trade-off between balance and robustness, leading to more accurate causal effect estimates. Their framework has since inspired further advancements in RCT design (Arbour et al.,, 2022; Chatterjee et al.,, 2023).

However, the GSW design proposed in Harshaw et al., (2024) has a notable limitation. As we show in Section 3, the GSW design does not provide nearly optimal guarantees when the probabilities of treatment and control assignments are unequal (i.e., not ). We address this gap in this paper.

Unequal assignment probabilities are important in RCTs to reduce costs, address ethical concerns, and manage differences in response variances between groups (Torgerson and Campbell,, 1997; Dumville et al.,, 2006; Wong and Zhu,, 2008; Ryeznik and Sverdlov,, 2018; Sverdlov and Ryeznik,, 2019; Azriel et al.,, 2022). However, few studies have focused on balancing covariates in this context. For example, the authors of Azriel et al., (2022) state, “We are not aware of work that discusses unequal-allocation design vis-a-vis the consideration of minimizing observed [covariate] imbalance in the non-sequential setting where all ’s [covariates] are known a prior.” Our results expand on this understanding for unequal assignment probabilities.

1.1 Our Contributions

This paper builds on the framework of Harshaw et al., (2024) and makes significant progress in solving the DDM problem for unequal assignment probabilities, further leading to new contributions in the design of RCTs.

First, we prove that achieving instance-optimality or even nearly instance-optimality for the DDM problem is NP-hard. Assuming PNP, no polynomial-time algorithm can guarantee that, for every instance, it returns an assignment that approximates the optimal assignment within even a certain constant error.

Second, we present a new Multiplicative Weights Update (MWU) algorithm that finds improved solutions for the DDM problem for the full spectrum of assignment probabilities. Theoretically, we show that our algorithm improves the GSW algorithm when assignment probabilities are unequal and matches its performance when probabilities are equal, both up to constant factors. Empirically, we demonstrate that our algorithm consistently produces solutions to the DDM problem with the lowest objective values across all assignment probabilities, outperforming the GSW algorithm and other commonly used designs on both synthetic and real-world datasets. While the MWU framework has been widely used in optimization and machine learning, its application to the DDM problem and the design of RCTs is new.

Third, we propose the MWU design building on the framework of Harshaw et al., (2024) and our MWU algorithm. Our design enhances the GSW design on the trade-off between covariate balance and robustness when assignment probabilities are unequal, and further reduces the mean-squared error (MSE) in estimating the average treatment effect (ATE). In addition, our simulation results show that our design achieves lower MSE in estimating the ATE when outcomes depend linearly or nearly linearly on covariates, compared with both the GSW design and other commonly used designs.

1.2 Related Work

Distributional discrepancy minimization and the design of RCTs.

Our work builds upon the rigorous framework of analyzing the balance-robustness trade-off provided in Harshaw et al., (2024). A tighter asymptotic analysis of the GSW design introduced in that paper was given in Chatterjee et al., (2023) and was adapted to online design in Arbour et al., (2022). The GSW design was shown to have an optimal trade-off between balance and robustness when treatment-control assignment probabilities are equal. While the design can adapt to unequal probabilities, it can be sub-optimal, as discussed in Section 3.2.

Balance-robustness trade-off and other commonly used designs.

There are various designs that span the spectrum between covariate balance and robustness. On one end of the spectrum is the Bernoulli design and the Complete Randomization. They uniformly sample an assignment from all assignments that satisfy marginal probability conditions or group-size conditions regardless of covariates. They have the strongest robustness (Kallus,, 2018; Azriel et al.,, 2022; Harshaw et al.,, 2024), but can cause covariate imbalance by chance. On the other end is the optimal designs, first suggested by Student, (1938) and then expanded by Bertsimas et al., (2015), Kasy, (2016), Deaton and Cartwright, (2018), Kallus, (2018), and Bhat et al., (2020). They define a measure of covariate balance and find the best possible assignment that minimizes covariate imbalance using tools from numerical or combinatorial optimization. The best assignment is usually deterministic and thus lacks robustness.

Various designs lie in between these two extremes, trading off some robustness to ensure covariates balance is considered important. Pairwise matching designs pair units based on covariates and then randomized within each pair (Greevy et al.,, 2004; Imai et al.,, 2009; Bai et al.,, 2022). Randomized block designs group units into blocks based on covariates and then randomize within each block (Fisher,, 1935; Higgins et al.,, 2016; Azriel et al.,, 2022). Rerandomization repeatedly generates random assignments uniformly from all feasible assignments until one meets a pre-specified covariate balance criterion, at which point it is accepted (Morgan and Rubin,, 2012; Li et al.,, 2018; Li and Ding,, 2020).

Pairwise matching cannot be used for unequal assignment probabilities since it assigns exactly one unit from each matched pair to treatment and one to control. Randomized block design and rerandomization can adapt unequal assignment probabilities. However, they do not perform well when the number of covariates is large (Branson and Shao,, 2021; Zhang et al.,, 2024; Davezies et al.,, 2024), and they do not provide a formal analysis of the balance-robustness trade-off (Harshaw et al.,, 2024).

Discrepancy theory.

The distributional discrepancy minimization problem introduced in Harshaw et al., (2024) is closely related to discrepancy theory, a subfield of discrete mathematics and theoretical computer science (Matousek,, 1999; Chazelle,, 2001; Chen et al.,, 2014). Besides Harshaw et al., (2024), algorithms in discrepancy theory have also played a role in inspiring RCT design, either directly or indirectly (Krieger et al.,, 2019; Turner et al.,, 2020). Our work continues this line of research by further connecting algorithmic discrepancy theory with the design of RCTs. Finally, recent advancements in algorithmic discrepancy theory potentially suggest new improvements in the design of RCTs (for example, Bansal, (2010), Lovett and Meka, (2015), Rothvoss, (2014), Eldan and Singh, (2018), Levy et al., (2017), Bansal et al., (2018), Alweiss et al., (2021), Bansal et al., (2022), Pesenti and Vladu, (2023), Kulkarni et al., (2023) and the references therein).

Roadmap.

We introduce notations in Section 2. We outline the problem setting and formally define the DDM problem in Section 3. We then formally state our contributions in Section 4, and present our MWU algorithm in Section 5. Finally, we provide a comprehensive empirical study in Section 6. Due to space constraints, all proofs are deferred to our Supplementary Material.

2 Notations

In this paper, we use bold letters for vectors and matrices and regular letters for scalars. For , we let . For a vector , let be its Euclidean norm. For a matrix , let be its operator norm induced by Euclidean norm, defined as . We let be the trace of . In addition, we define the norm as the maximum Euclidean norm among ’s columns. For two vectors or two matrices , we let and denote their inner products respectively, where and are the transposes of and respectively. We let be the all-one vector, and be the identity matrix. For a random vector drawn from distribution , let denote the covariance matrix of , defined as the expected value of the outer product of with itself. When the context is clear, we drop the subscript from the covariance matrix and expectation.

3 Problem setup

In this section, we present the assumptions of RCTs, covariate balance and robustness, and the Distributional Discrepancy Minimization (DDM) problem introduced by Harshaw et al., (2024).

We follow the Neyman-Rubin potential outcome framework (Rubin,, 2005) for an RCT with a population of units and two treatment groups: treatment and control. Each unit has two potential outcomes: under treatment and under control. If unit is assigned to the treatment group, we observe the outcome ; otherwise, we observe the outcome .

The experimenter needs to randomly assign each unit to either the treatment or control group, with respective pre-specified marginal probabilities and . Let represent the random assignment of the units, where indicates that unit is assigned to the treatment group, and indicates assignment to the control group. In this paper, we restrict ourselves to feasible designs/assignments in which, for each , and .

We assume that the potential outcomes of each unit are deterministic and the only source of randomness comes from the random assignment of the units. This model is known as the randomization model or Neyman model (Fisher,, 1935; Kempthorne,, 1955; Rosenberger and Lachin,, 2015).

We want to estimate the average treatment effect (ATE):

| (1) |

We will use the Horvitz-Thompson (HT) estimator:

| (2) |

The HT estimator is unbiased for a feasible assignment, meaning that . We want to minimize the mean-squared error (MSE) of , defined as

| (3) |

where and each is a weighted sum of the two potential outcomes for . The vector is called the potential outcome vector.

Since is fixed but unknown, we want to find a feasible design that minimizes the worst-case MSE among all (up to scaling). This ensures that our estimation is robust even with an adversary that provides the worst possible . The worst-case MSE has been studied by Efron, (1971), Kallus, (2018), Kapelner et al., (2021), Harshaw et al., (2024), and others.

3.1 The Distributional Discrepancy Minimization Problem

We assume that each unit has covariates – pre-treatment variables observed before the trial, denoted by . We also define . We can normalize the covariate vectors so that for every (for example, by dividing each with ).

We can write the potential outcome vector where and is orthogonal to the columns of . Both and are assumed to be fixed but unknown. Using this decomposition of , we can write the MSE as

Also see Kapelner et al., (2021) and Harshaw et al., (2024). In the above equation, measures covariate balance, and captures robustness against unobserved variables or model misspecification.

We build on the framework of Harshaw et al., (2024) to simultaneously balance covariates and maintain robustness. The GSW design in Harshaw et al., (2024) has a design parameter , chosen by the experimenter, to govern the trade-off between covariate balance and robustness. One constructs an augmented covariate matrix : if , let

| (4) |

if , simply let (only robustness) and if , let (only covariate balance). A smaller emphasizes more on covariate balance. The authors reduced finding feasible that minimizes the worst-case MSE to the following problem.

Problem 3.1 (The Distributional Discrepancy Minimization (DDM) problem).

Given with and , find a random vector sampled from

| (5) |

In addition, we want to develop a computationally efficient algorithm that returns such a .

The GSW design finds a feasible such that for any satisfying the conditions in Problem 3.1. It implies that, for any design parameter , and ; for , , and for , .

3.2 Sub-Optimality of the GSW Design for Unequal Probabilities

The GSW design’s guarantee is optimal when (i.e., equal treatment-control assignment probabilities). However, this guarantee can be far from optimal when (i.e., unequal probabilities).

The following example demonstrates the sub-optimality of the GSW bound. Consider and . If we use the Bernoulli design, assigning each unit to treatment with a probability of and to control with , then is a diagonal matrix with diagonal entries equal to , resulting in . In addition, . These values are significantly smaller than the upper bound of provided by the GSW design, regardless of the choice of . While one might argue that the GSW upper bound is overly conservative in some examples, we provide a numerical example in Supplementary Section 1 showing that for some instance of the DDM problem. To the best of our knowledge, we are the first to establish improved bounds for the DDM problem with unequal assignment probabilities.

4 Our Results

4.1 Hardness Results

We establish a strong NP-hard result showing that, assuming PNP, we cannot approximate the optimum of the DDM problem, described in Problem 3.1, within even a certain constant additive error.

Theorem 4.1.

There exists a universal constant such that the following holds: For any and , there exists such that, assuming PNP, NO polynomial-time algorithm can, for any , return a feasible random whose distribution satisfies .

The parameters in Theorem 4.1 can depend on the dimensions of . When are both constants and , the theorem means there is a constant gap between any achievable in polynomial time and the optimal . When is a fixed constant different from and approaches , the assignment probabilities (i.e., entries of ) approach , and the gap between achievable in polynomial time and goes to . For the equal probabilities case, that is, , we establish a similar NP-hard result. We defer the theorem statement and proofs to Supplementary Section 2.

4.2 An Efficient MWU Design

We develop a computationally efficient algorithm for the DDM problem that achieves the best performance of the GSW and Bernoulli designs for unequal assignment probabilities. Let and denote the feasible distributions under the GSW and Bernoulli designs, respectively. For the function defined in the DDM problem, we have:

where is a diagonal matrix with diagonals for .

Theorem 4.2.

Given a matrix with and a vector , for any , we can find a random drawn from a feasible distribution such that

| (6) |

and the runtime is polynomial in . The algorithm that achieves the above guarantees is presented in Algorithm 1 MWU.

Consider being a constant that does not depend on and . When (i.e., unequal treatment-control assignment probabilities), the upper bound in Equation (6) is better than the best achievable by the Bernoulli and the GSW designs, up to constant. For the example given in Section 3.2, Theorem 4.2 obtains the Bernoulli upper bound, which is better than the GSW bound. When (i.e., equal probabilities), Theorem 4.2 guarantees that our algorithm is no worse than the GSW design, up to a constant factor.

Our theoretical upper bound in Equation (6) may be conservative; therefore, we conduct empirical experiments to compare our algorithm with the GSW algorithm, the Bernoulli design, and other commonly used designs. Our simulation results demonstrate that has the lowest values across all assignment probabilities in both synthetic and real-world datasets.

Estimating the ATE.

Building on the framework of Harshaw et al., (2024) and our MWU algorithm, we propose the MWU design. In this design, the experimenter selects a design parameter and an accuracy parameter . The design then constructs an augmented matrix as specified in Equation (4) and runs the MWU algorithm (Algorithm 1) on with parameter to solve the DDM problem, returning a feasible assignment .

We obtain similar results on the balance-robustness trade-off, the expectation, variance, and convergence rate of the error of estimating the ATE under the MWU design, substituting the GSW upper bound with the MWU upper bound. A smaller upper bound immediately improves the estimation accuracy. Our proofs are similar to those from Harshaw et al., (2024), and we include them in Supplementary Section 4 for completeness.

Proposition 4.3 (Balance-robustness trade-off).

Proposition 4.4.

The HT estimator for the ATE under the MWU design is unbiased, that is, .

Proposition 4.5.

Assume the conditions in Proposition 4.3 hold. Let , where for each , be the potential outcome vector. Then, under the MWU design, the variance

Proposition 4.6.

Let and be fixed constants. Assume that (1) the design parameter , (2) every assignment probability , and (3) . Then, under the MWU design, in probability. Furthermore, the convergence rate satisfies .

In Section 6, we perform detailed empirical studies to compare the MWU design with the GSW and other commonly used designs, showing that our design decreases the variance of estimating the ATE when outcomes and covariates are nearly linearly correlated.

5 Our Algorithm

In this section, we describe Algorithm 1 MWU for the DDM problem that achieves Theorem 4.2. The algorithm is based on the matrix Multiplicative Weights Update method (MWU), which is commonly used in machine learning, optimization, and game theory (Arora et al.,, 2012).

A key idea of Algorithm 1 is to transform the problem of minimizing into a sequence of simpler tasks that minimize “projections” of the covariance matrix onto positive definite (PD) matrices. Let denote the set of all symmetric PD matrices of dimensions . The objective of the DDM problem can be rephrased as minimizing:

Algorithm 1 reduces this minimax problem into a sequence of subproblems with fixed . We represent a distribution using its support set and the probabilities associated with the vectors in , which we will iteratively build. During this process, we update the weight matrix , which indicates the directions that need improvement in . At each iteration, we find a feasible random vector that minimizes . We then add to the set and adjust based on the new set . After enough iterations, the algorithm produces a feasible distribution supported on with a small value of .

Theorem 5.1.

Suppose we can access an oracle which takes a matrix with , a positive definite matrix , and a vector as input and returns a random feasible vector whose distribution satisfies

| (7) |

Then, for any , Algorithm 1 MWU() returns a feasible random vector whose distribution satisfies

| (8) |

In addition, the number of calls to and the algorithm’s runtime are polynomial in .

Algorithm 1 can incorporate additional constraints on random assignments. Given an oracle that produces a random assignment satisfying Equation (7) and the constraints, we can run Algorithm 1 with to obtain a random assignment that satisfies Equation (8) and the constraints.

5.1 The MWU Oracle

We describe a polynomial-time algorithm for the oracle that satisfies the condition in Theorem 5.1. Our algorithm is presented in Algorithm 2 Oracle(). Without loss of generality, we make the following assumptions on : (1) the trace of is ; (2) is a diagonal matrix (otherwise, we take the eigendecomposition of and apply a linear transform to and ).

Algorithm 2 Oracle is inspired by algorithmic discrepancy theory, particularly the random walks over from Bansal et al., (2019). It starts at , the expected value of a feasible assignment. At each step , it randomly moves from to a new position , which ensures that (that is, form a martingale). Once the walk reaches a face of the cube , it remains on that face in all future steps. After enough steps, the walk reaches a corner of the cube at and returns . We have . The main challenge is how to properly choose given at each step .

At each step , we update using the formula where is a unit vector and is a random step size. Below, we explain how to choose and . We maintain a set of “alive” variables at the start of step , as defined in line 6 of Algorithm 2. Only alive variables can be changed.

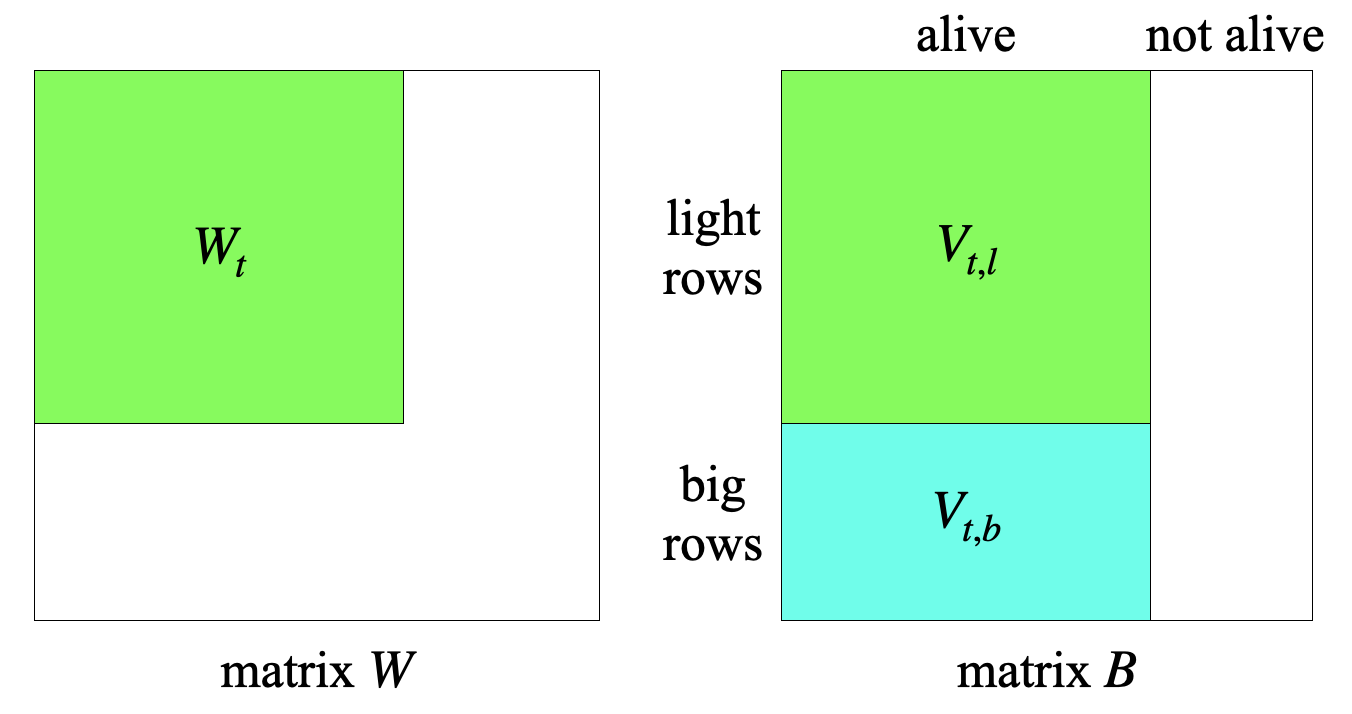

Let be the submatrix of restricted to columns indexed in . We classify the rows of into “big” rows and “light” rows as follows: Let111For a matrix , let denote the submatrix of restricted to rows in and columns in ; let denote the submatrix restricted to rows in , and the submatrix restricted to columns in .

be a set of rows with large norms, and let . We choose (when restricted to alive entries) to be orthogonal to the big rows and have small projections (in absolute value) onto the light rows.

To formalize these concepts, we introduce the following notations (illustrated in Figure 1):

| (9) | ||||

We choose such that

| (10) | ||||

Next, we select the step size as a zero-mean random variable that pushes at least one of the alive variables to (thus not alive next step).

Theorem 5.2.

We run Algorithm 1 MWU(). Oracle is given in Algorithm 2 with the same error parameter , and parameter is given in Theorem 5.2. Combining Theorems 5.1 and 5.2 results in Theorem 4.2. The covariance matrix in Algorithm 1 might be unknown. In this case, we replace it with its empirical mean, and we discuss more details in Supplementary Section 3.1. All proofs are in Supplementary Section 3.

6 Experiments

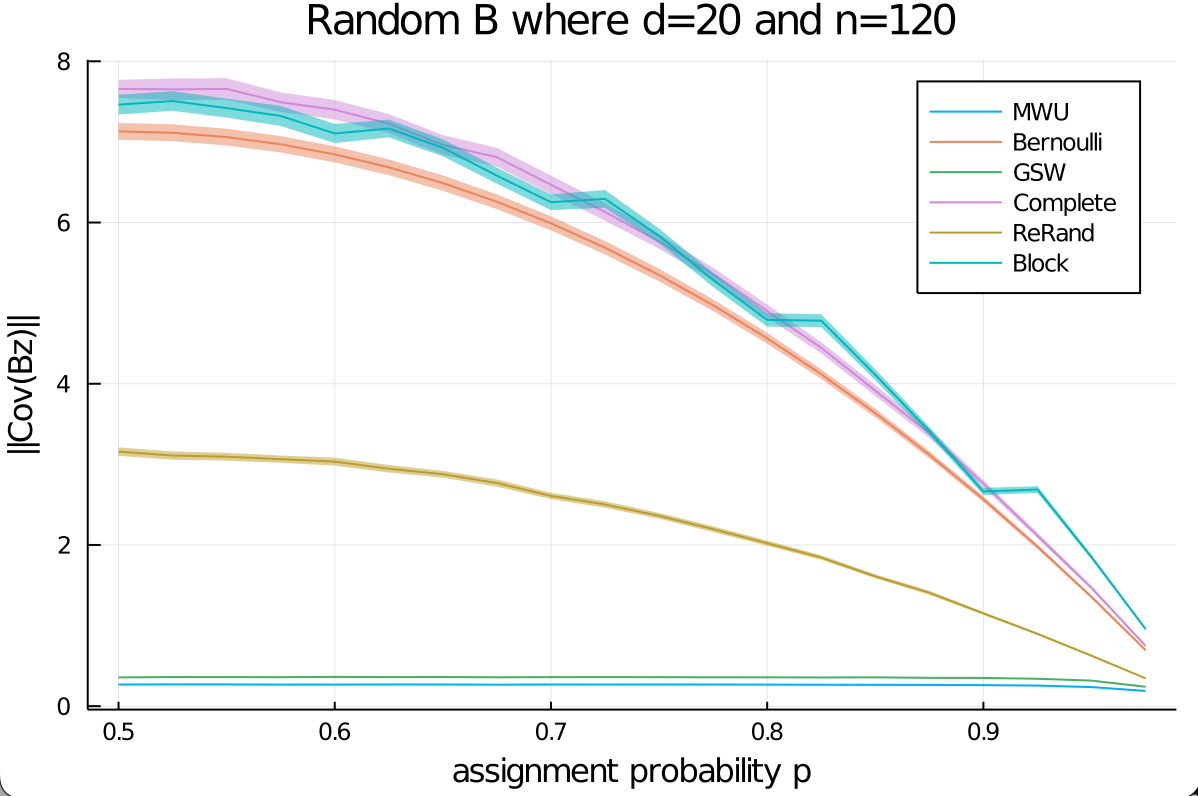

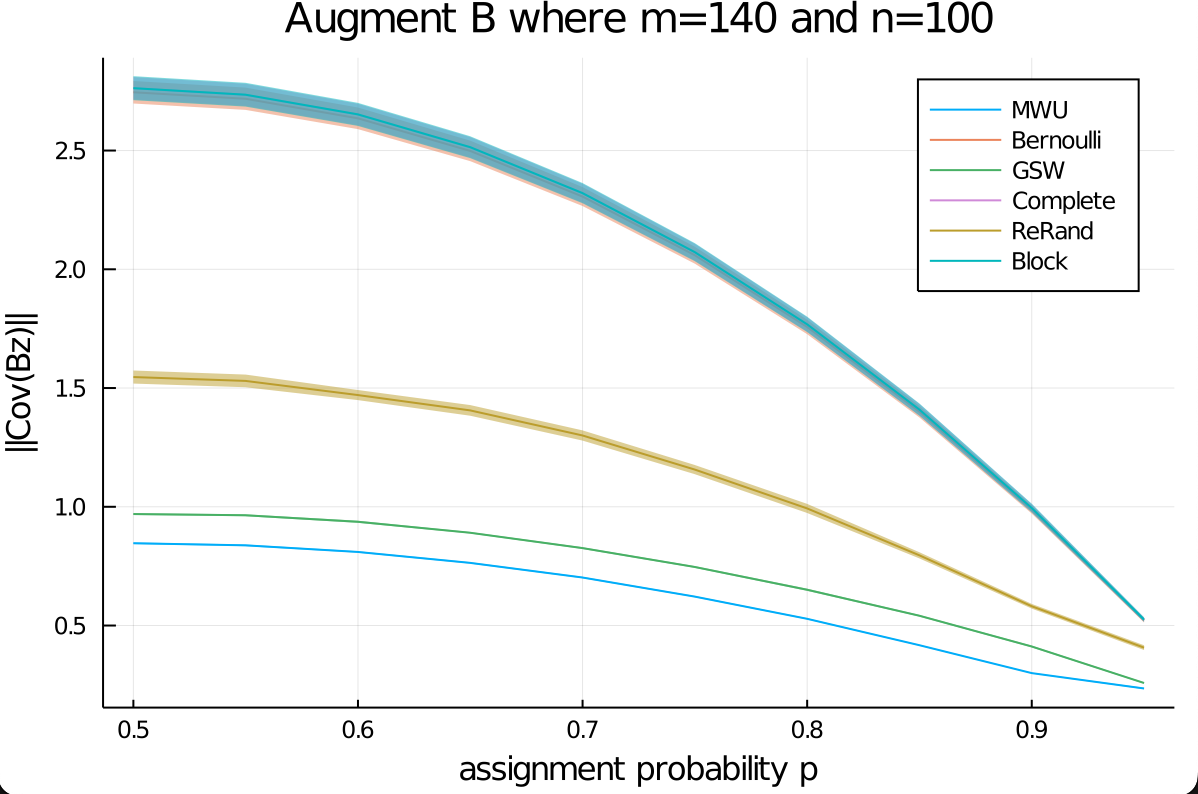

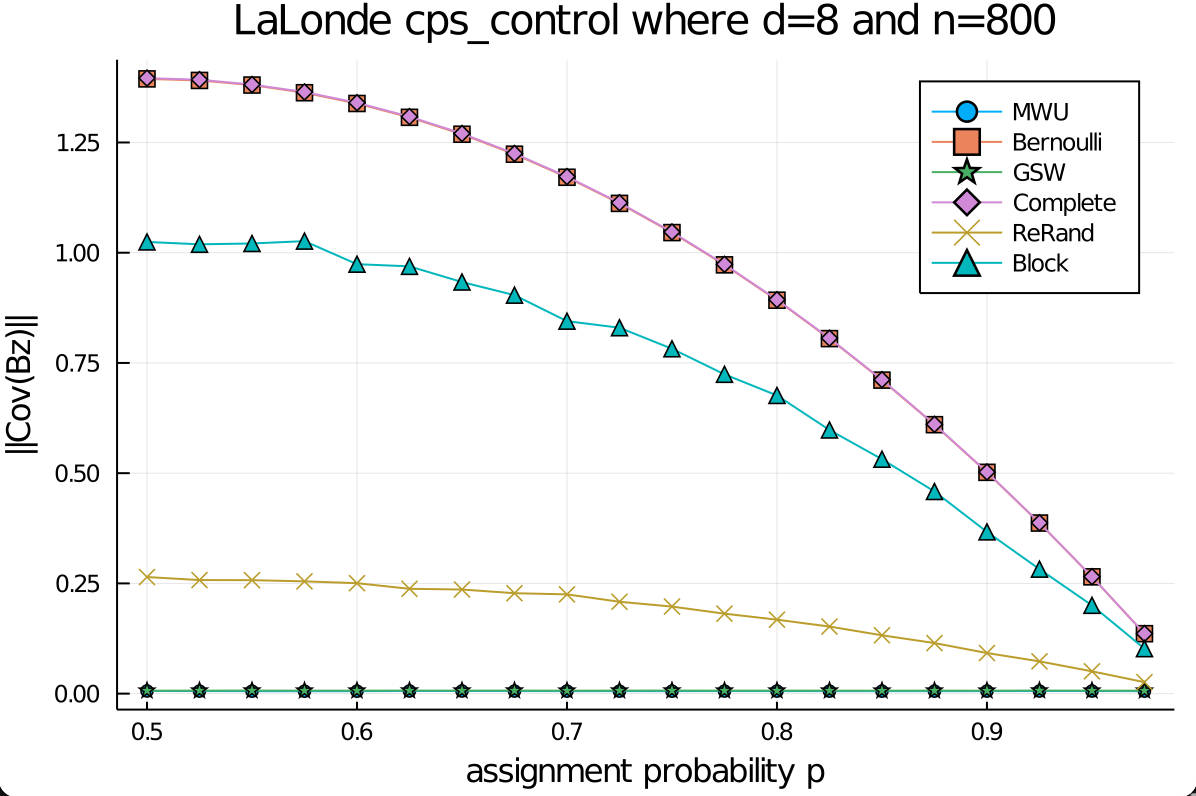

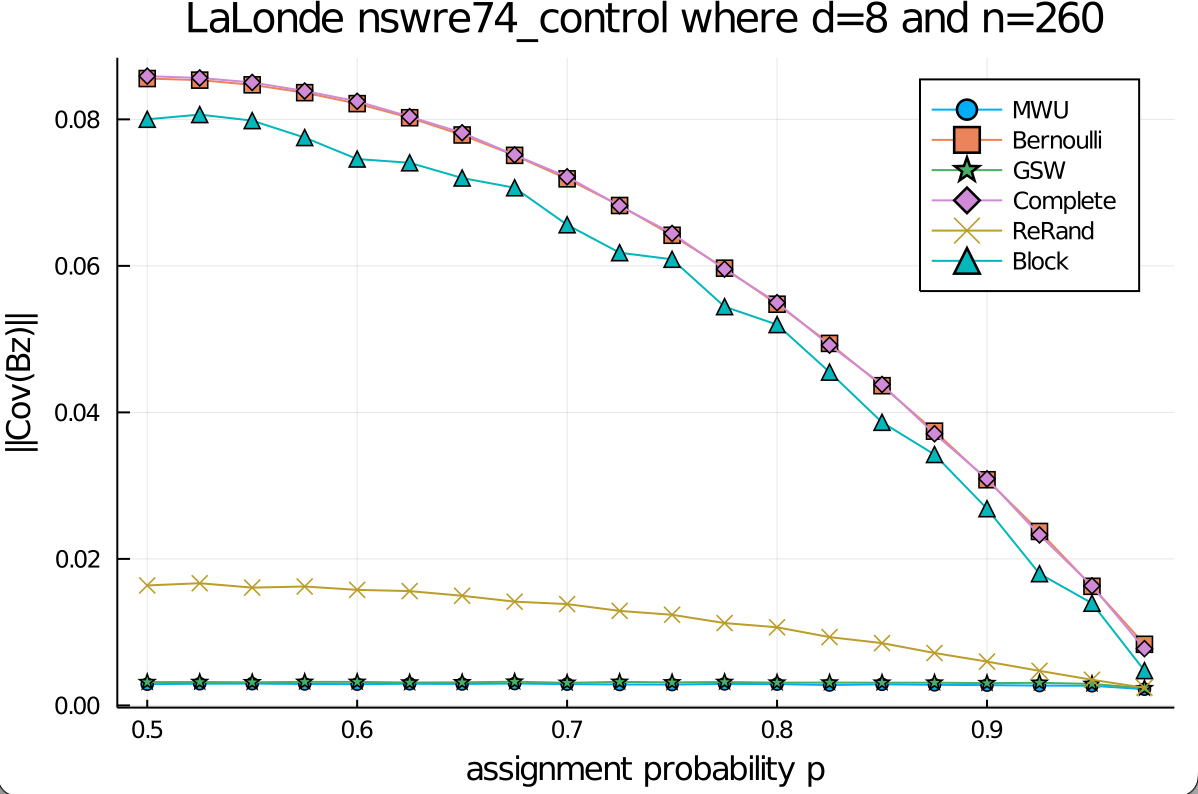

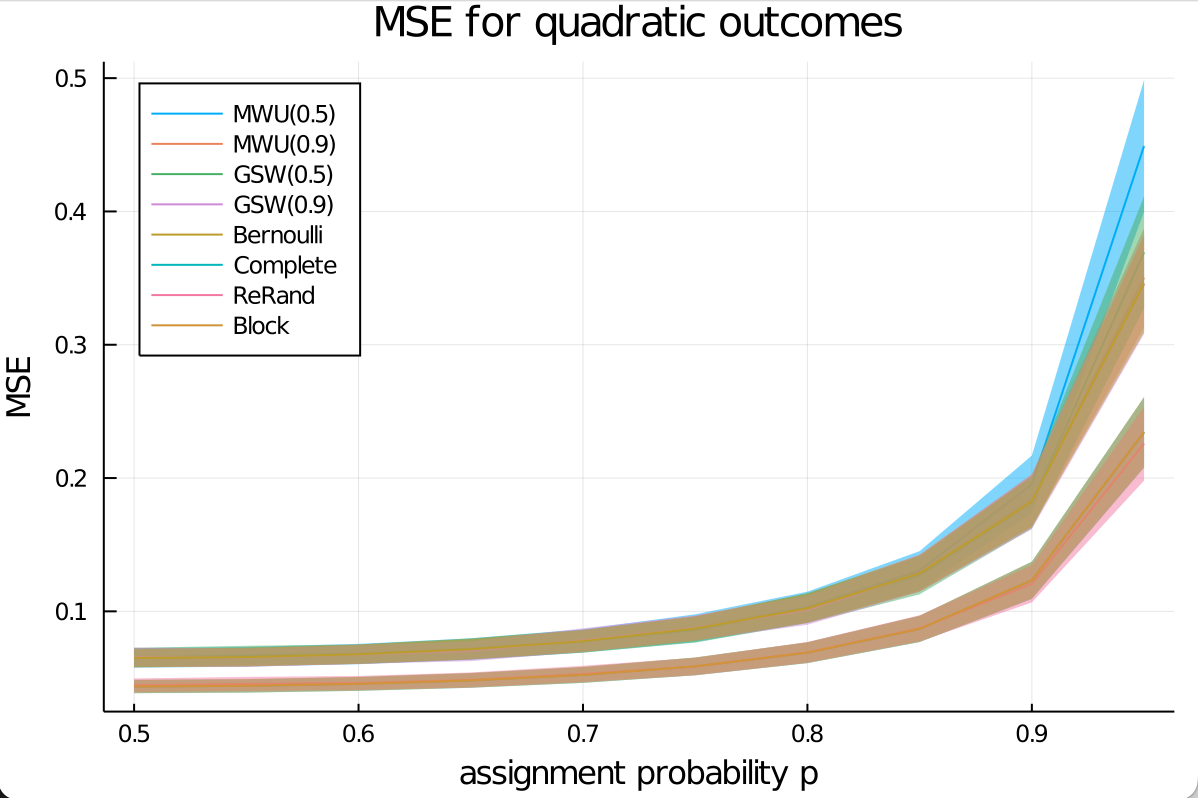

In this section, we compare our design with several designs222Pairwise matching does not naturally generalize to unequal treatment-control assignments, as it pairs units and assigns one to treatment and the other to control.: the GSW design, Bernoulli design, Complete Randomization, Randomized Block Design, and Rerandomization. Details of the design implementations are provided in Supplementary Section 5.1. We experiment with different treatment-control assignment probabilities by setting , where ranges from to . Due to the symmetry between the treatment and control groups, we only plot from to . The designs are evaluated based on two metrics: (1) , the objective of the DDM problem described in Problem 3.1, and (2) the mean squared error (MSE) in estimating the ATE.

6.1 The DDM Objective

We begin by examining different algorithms/designs for solving the DDM problem, where the goal is to minimize . We consider two types of : (1) randomly generated entries and (2) covariate data from the Lalonde dataset (LaLonde,, 1986).

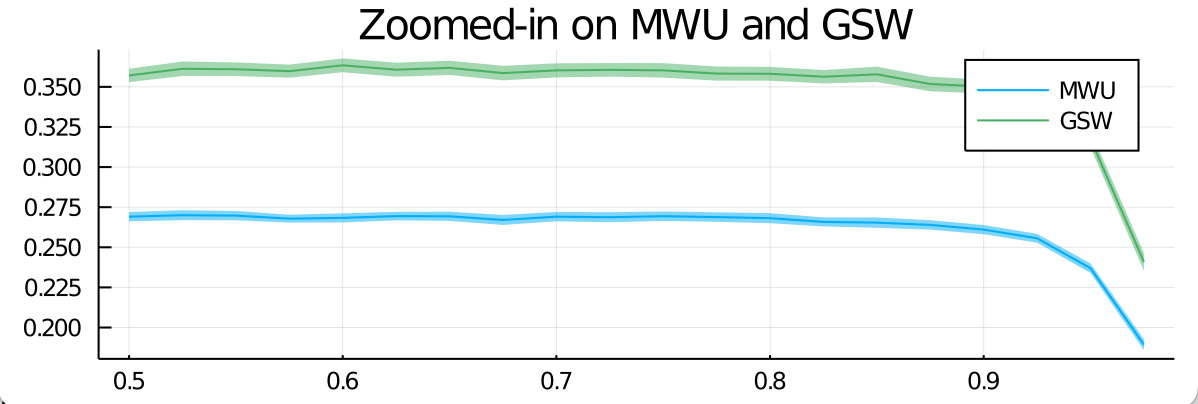

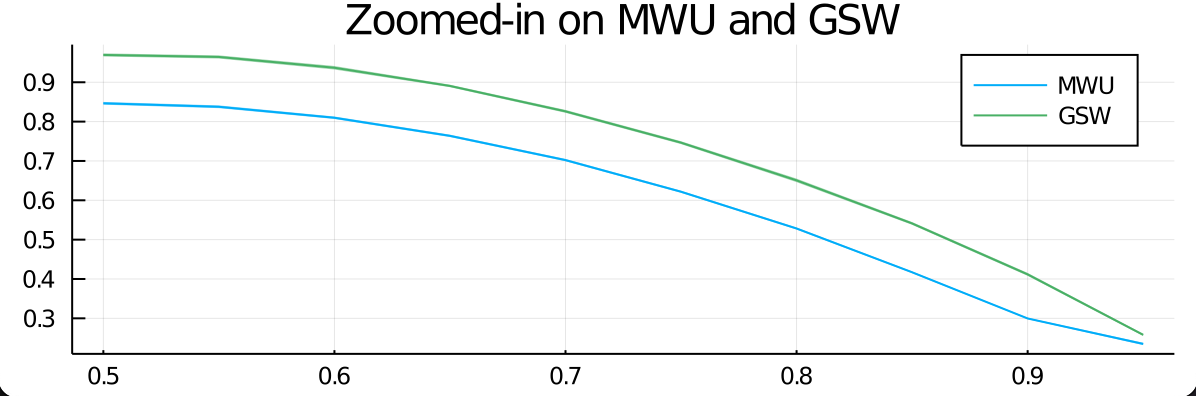

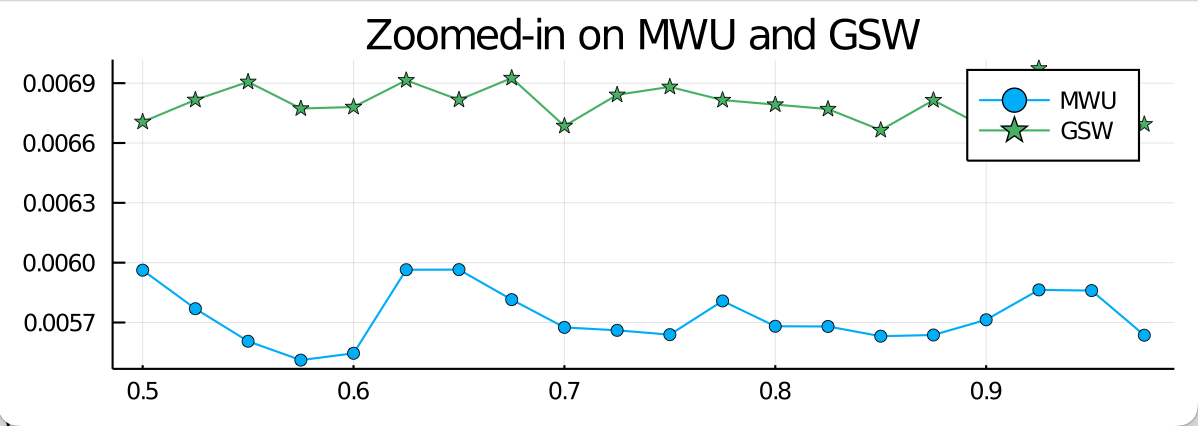

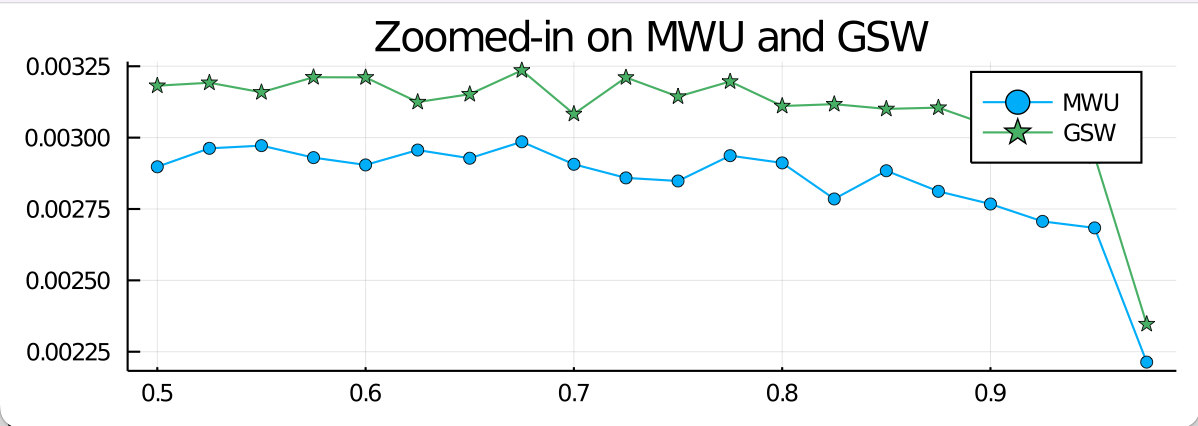

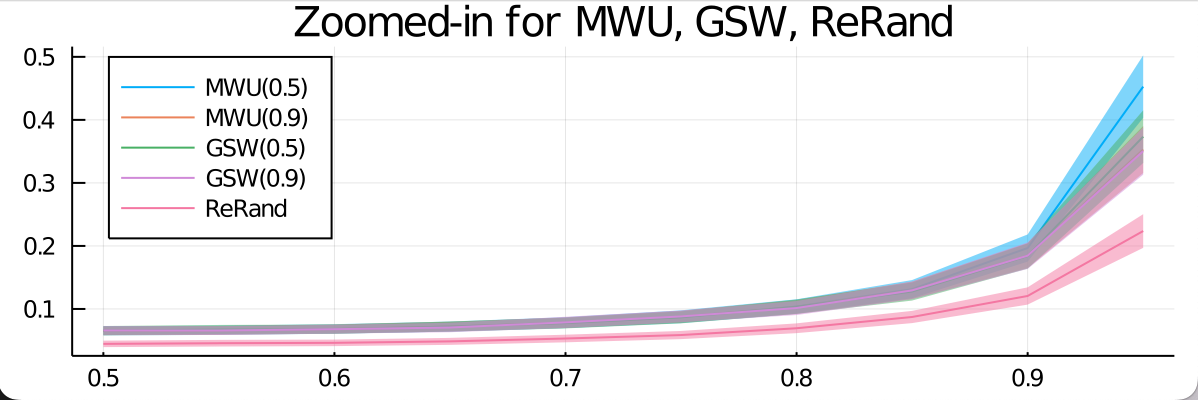

Random . We consider two types of matrices for : (1) a matrix where all entries are i.i.d. random variables uniformly sampled from ; (2) an augmented matrix as defined in Equation (4). For the first type, we set the dimensions of to be . For the second type, we set the dimensions of the covariate matrix in Equation (4) to be , with ’s entries being i.i.d. random variables uniformly sampled from ; we set parameter for constructing . For each type of , we generate independent samples of and plot the resulting confidence intervals in Figure 2 (where the randomness comes only from the random samples of ). Among the six designs, the Bernoulli, Complete Randomization, and Randomized block designs perform the worst; Rerandomization is better; the MWU and GSW designs have the best results. We zoom in on the MWU and GSW designs, and we observe that MWU yields even better values of than GSW.

LaLonde dataset. We evaluate the six designs using the LaLonde dataset from LaLonde, (1986) and Dehejia and Wahba, (1999, 2002) 333The dataset is available at users.nber.org/~rdehejia/data/.nswdata2.html. We use the data from files cps_controls.txt and nswre74_control.txt. . The dataset estimates the impact of the National Support Work Demonstration (NSW) job training program on trainee earnings. The dataset has different experimental and control data. We test on two of them: CPS control data and NSW control data. Both the two datasets have eight covariates: four binary covariates and four numeric covariates. For the CPS dataset, we randomly choose units (aka, ); for the NSW dataset, we use all the units. We normalize each covariate to have a sample mean of and a sample standard deviation of . We take to be this standardized covariate matrix. We then add an independent Gaussian noise to each covariate to make full row rank. Finally, we scale all the entries of to ensure the new matrix satisfies . Our experiment results are shown in Figure 2.

6.2 Mean-Squared Error (MSE)

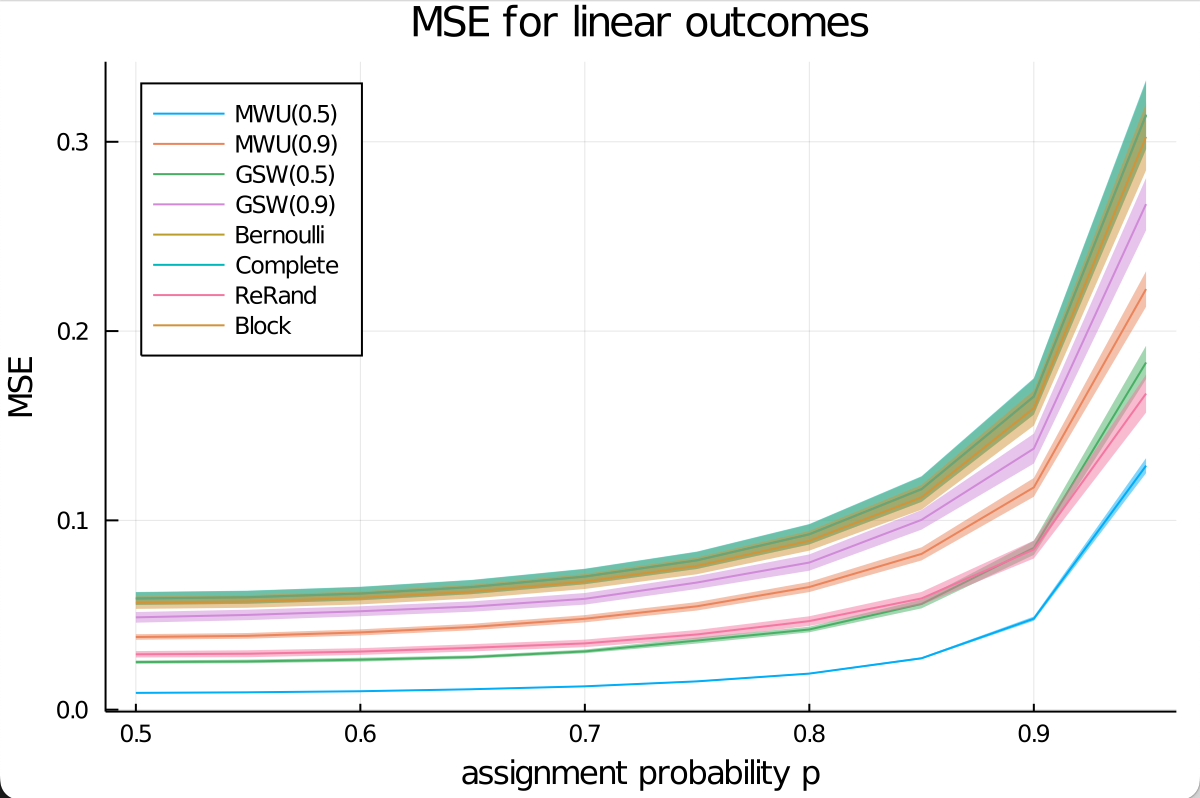

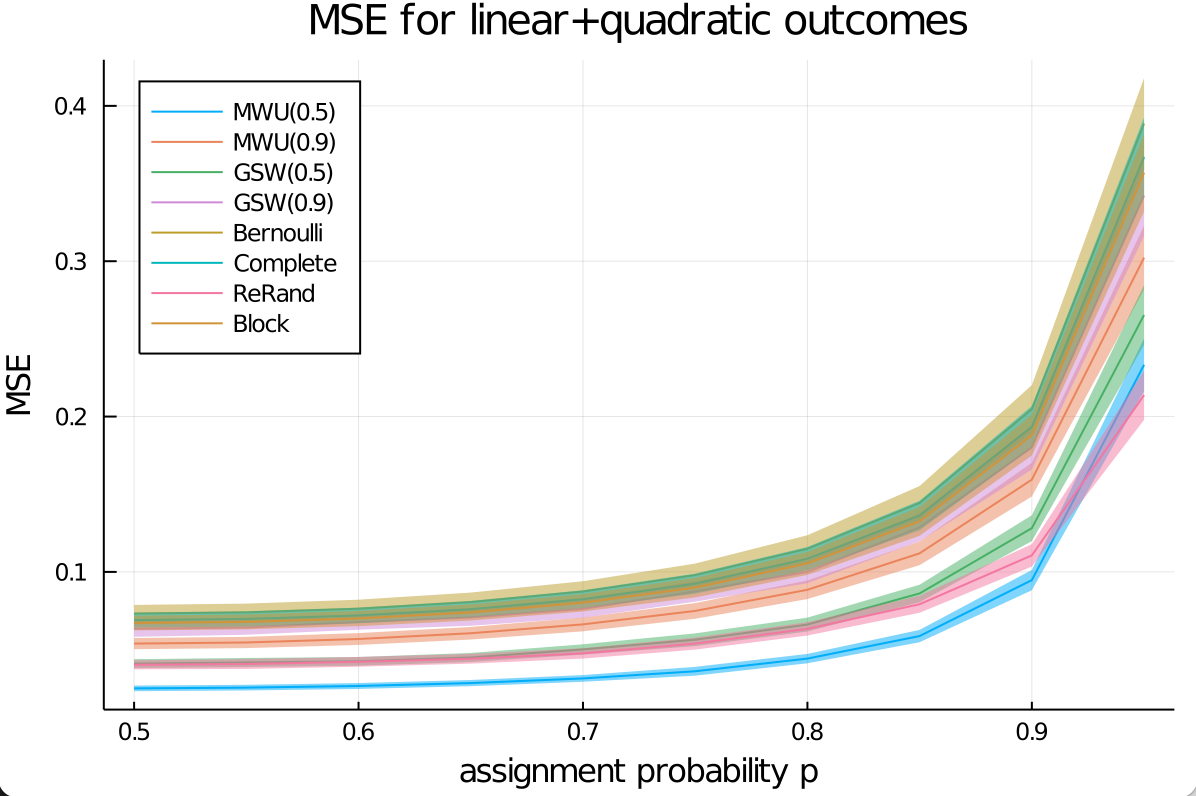

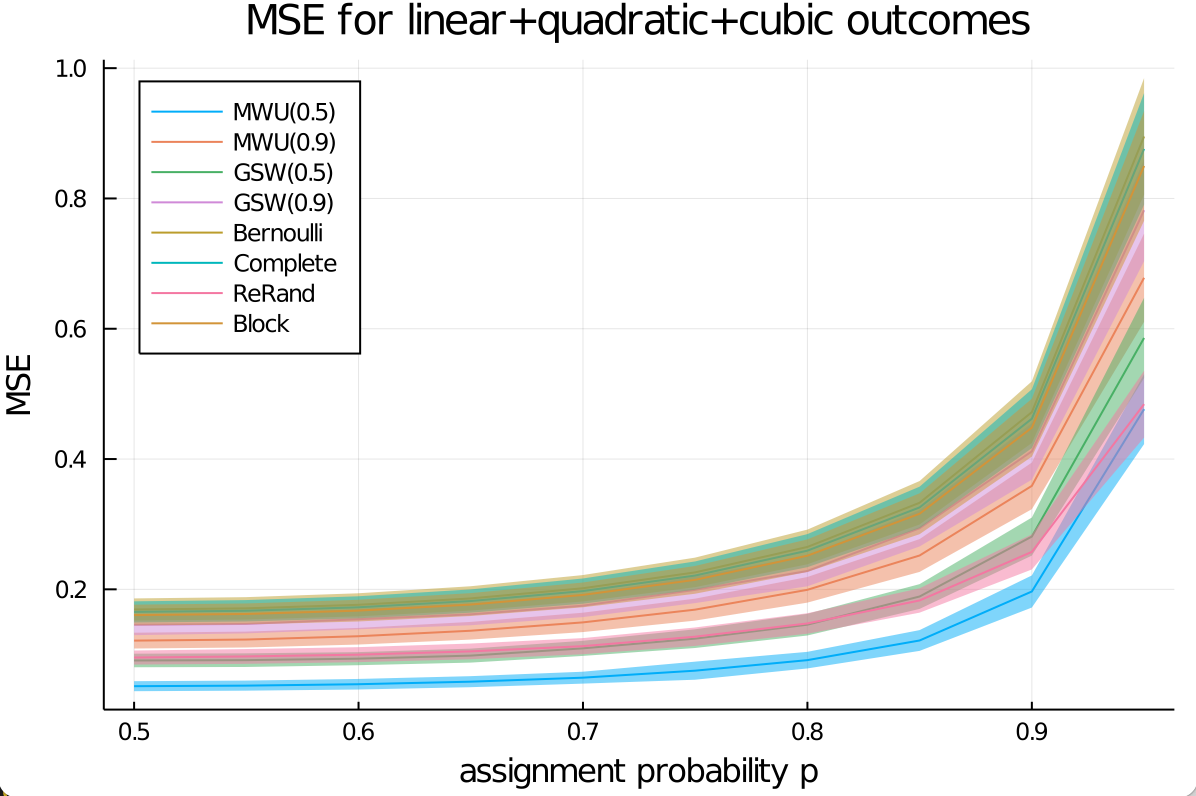

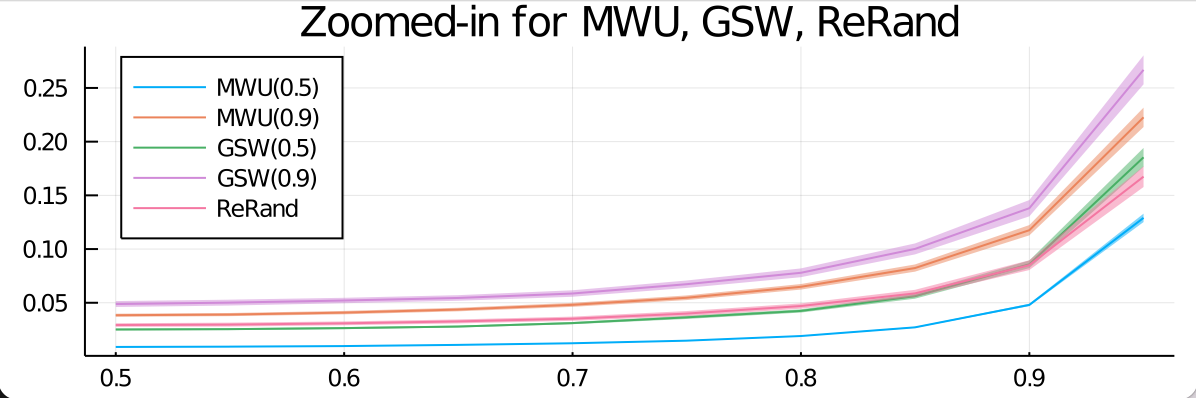

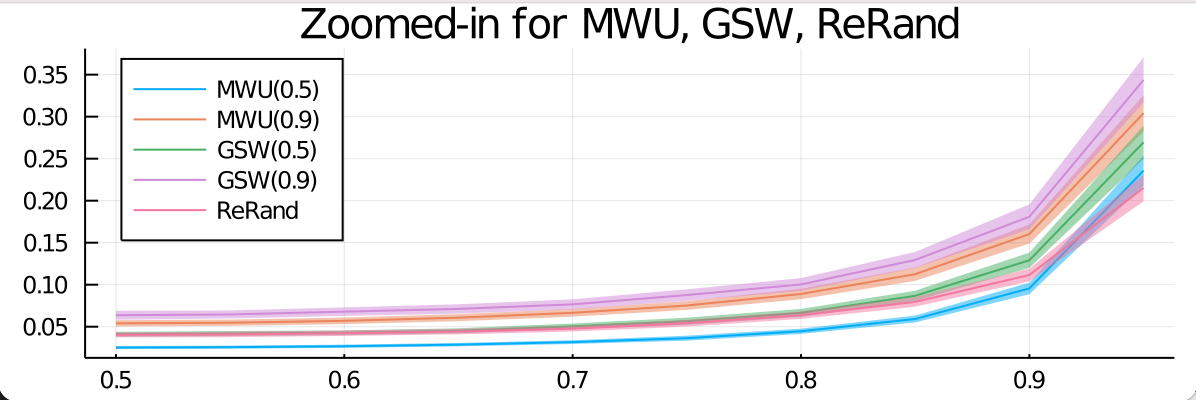

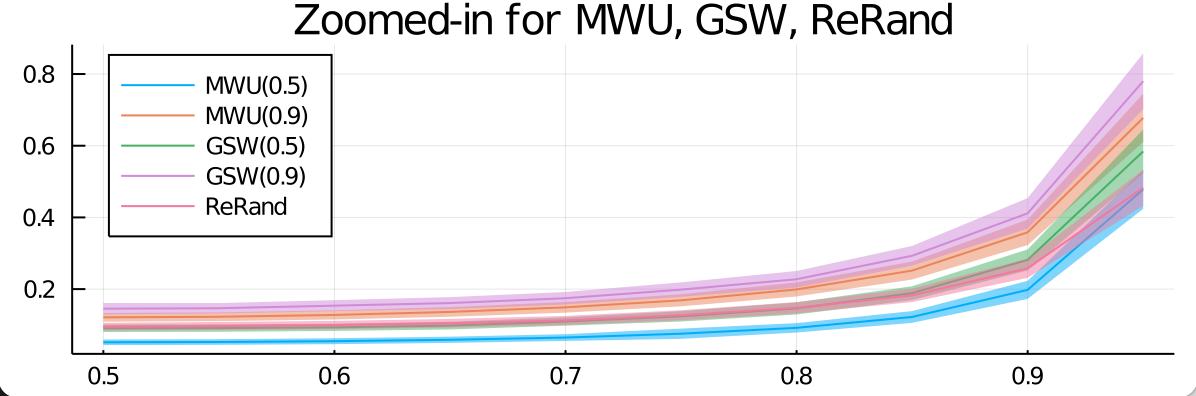

We then evaluate all six designs by measuring the MSE for estimating the average treatment effect, as described in Section 3. We test the MWU and GSW designs using the design parameter , following the recommendation from Harshaw et al., (2024), who suggests choosing to ensure robustness.

We set and , and generate the covariate ’s whose entries are i.i.d. random variables uniformly sampled from . We choose potential outcomes and , where is a function that depends only on the first twenty covariates of unit , and is Gaussian noise. We consider to take various forms, representing different relations between covariates and outcomes: linear, a mix of linear and quadratic, a mix of linear and quadratic and cubic, and pure quadratic terms. Details of the data-generating process are in Supplementary Section 5.2. The results are presented in Figure 3.

The MWU design with a parameter of (referred to as MWU()) achieves the lowest MSE when the relationship between outcomes and covariates is linear (first plot in Figure 3) or nearly linear (second and third plots). Specifically, the best MSE from other designs is at least times that of MWU() on average, and at least times for . When the outcome-covariate relationship is pure quadratic (fourth plot), Rerandomization has the lowest MSE, but MWU() performs comparably, with an MSE that is no more than times that of Rerandomization.

7 Concluding Remarks

We present a new MWU algorithm for the distributional discrepancy minimization problem introduced by Harshaw et al., (2024). Our algorithm outperforms the GSW design for unequal assignment probabilities, which have important applications in experimental design. Building on the framework of Harshaw et al., (2024), our approach reduces the mean-squared error in estimating the ATE compared to commonly used designs, strengthening the connection between distributional discrepancy and experimental design.

One limitation of our design is that we assume the relationship between covariates and outcomes is nearly linear, the same as Harshaw et al., (2024). This limitation could be addressed by incorporating higher-order covariate terms and their interactions or using kernel methods. We leave this as a direction for future work.

Our algorithm is slower than the GSW design and other designs, but its runtime remains polynomial in input size, which is acceptable for many small randomized experiments in fields like medicine, agriculture, and education. The higher computational cost of planning could be outweighed by the increase in estimation accuracy.

Acknowledgments

The authors acknowledge the Office of Advanced Research Computing (OARC) at Rutgers, The State University of New Jersey, for providing access to the Amarel cluster and associated research computing resources that have contributed to the results reported here. URL: https://it.rutgers.edu/oarc.

References

- Alweiss et al., (2021) Alweiss, R., Liu, Y. P., and Sawhney, M. (2021). Discrepancy minimization via a self-balancing walk. In Proceedings of the 53rd Annual ACM SIGACT Symposium on Theory of Computing, pages 14–20.

- Arbour et al., (2022) Arbour, D., Dimmery, D., Mai, T., and Rao, A. (2022). Online balanced experimental design. In International Conference on Machine Learning, pages 844–864. PMLR.

- Arora et al., (2012) Arora, S., Hazan, E., and Kale, S. (2012). The multiplicative weights update method: a meta-algorithm and applications. Theory of computing, 8(1):121–164.

- Azriel et al., (2022) Azriel, D., Krieger, A. M., and Kapelner, A. (2022). The optimality of blocking designs in equally and unequally allocated randomized experiments with general response. arXiv preprint arXiv:2212.01887.

- Bai et al., (2022) Bai, Y., Romano, J. P., and Shaikh, A. M. (2022). Inference in experiments with matched pairs. Journal of the American Statistical Association, 117(540):1726–1737.

- Bansal, (2010) Bansal, N. (2010). Constructive algorithms for discrepancy minimization. In 2010 IEEE 51st Annual Symposium on Foundations of Computer Science, pages 3–10. IEEE.

- Bansal et al., (2019) Bansal, N., Dadush, D., and Garg, S. (2019). An algorithm for komlós conjecture matching banaszczyk’s bound. SIAM Journal on Computing, 48(2):534–553.

- Bansal et al., (2018) Bansal, N., Dadush, D., Garg, S., and Lovett, S. (2018). The gram-schmidt walk: a cure for the banaszczyk blues. In Proceedings of the 50th Annual ACM SIGACT Symposium on Theory of Computing, pages 587–597.

- Bansal et al., (2022) Bansal, N., Laddha, A., and Vempala, S. (2022). A unified approach to discrepancy minimization. In Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques (APPROX/RANDOM 2022). Schloss Dagstuhl-Leibniz-Zentrum für Informatik.

- Bertsimas et al., (2015) Bertsimas, D., Johnson, M., and Kallus, N. (2015). The power of optimization over randomization in designing experiments involving small samples. Operations Research, 63(4):868–876.

- Bhat et al., (2020) Bhat, N., Farias, V. F., Moallemi, C. C., and Sinha, D. (2020). Near-optimal ab testing. Management Science, 66(10):4477–4495.

- Branson and Shao, (2021) Branson, Z. and Shao, S. (2021). Ridge rerandomization: An experimental design strategy in the presence of covariate collinearity. Journal of Statistical Planning and Inference, 211:287–314.

- Charikar et al., (2005) Charikar, M., Guruswami, V., and Wirth, A. (2005). Clustering with qualitative information. Journal of Computer and System Sciences, 71(3):360–383.

- Charikar et al., (2011) Charikar, M., Newman, A., and Nikolov, A. (2011). Tight hardness results for minimizing discrepancy. In Proceedings of the twenty-second annual ACM-SIAM symposium on Discrete Algorithms, pages 1607–1614. SIAM.

- Chatterjee et al., (2023) Chatterjee, S., Dey, P. S., and Goswami, S. (2023). Central limit theorem for gram-schmidt random walk design. arXiv preprint arXiv:2305.12512.

- Chazelle, (2001) Chazelle, B. (2001). The discrepancy method: randomness and complexity. Cambridge University Press.

- Chen et al., (2014) Chen, W., Srivastav, A., Travaglini, G., et al. (2014). A panorama of discrepancy theory, volume 2107. Springer.

- Davezies et al., (2024) Davezies, L., Hollard, G., and Merino, P. V. (2024). Revisiting randomization with the cube method. arXiv preprint arXiv:2407.13613.

- Deaton and Cartwright, (2018) Deaton, A. and Cartwright, N. (2018). Understanding and misunderstanding randomized controlled trials. Social science & medicine, 210:2–21.

- Dehejia and Wahba, (1999) Dehejia, R. H. and Wahba, S. (1999). Causal effects in nonexperimental studies: Reevaluating the evaluation of training programs. Journal of the American statistical Association, 94(448):1053–1062.

- Dehejia and Wahba, (2002) Dehejia, R. H. and Wahba, S. (2002). Propensity score-matching methods for nonexperimental causal studies. Review of Economics and statistics, 84(1):151–161.

- Dumville et al., (2006) Dumville, J., Hahn, S., Miles, J., and Torgerson, D. (2006). The use of unequal randomisation ratios in clinical trials: a review. Contemporary clinical trials, 27(1):1–12.

- Efron, (1971) Efron, B. (1971). Forcing a sequential experiment to be balanced. Biometrika, 58(3):403–417.

- Eldan and Singh, (2018) Eldan, R. and Singh, M. (2018). Efficient algorithms for discrepancy minimization in convex sets. Random Structures & Algorithms, 53(2):289–307.

- Fisher, (1935) Fisher, R. A. (1935). The design of experiments. London: Oliver & Boyd.

- Golden, (1965) Golden, S. (1965). Lower bounds for the helmholtz function. Physical Review, 137(4B):B1127.

- Greevy et al., (2004) Greevy, R., Lu, B., Silber, J. H., and Rosenbaum, P. (2004). Optimal multivariate matching before randomization. Biostatistics, 5(2):263–275.

- Guruswami, (2004) Guruswami, V. (2004). Inapproximability results for set splitting and satisfiability problems with no mixed clauses. Algorithmica, 38(3):451–469.

- Harshaw et al., (2024) Harshaw, C., Sävje, F., Spielman, D. A., and Zhang, P. (2024). Balancing covariates in randomized experiments with the gram–schmidt walk design. Journal of the American Statistical Association, pages 1–13.

- Hernán and Robins, (2010) Hernán, M. A. and Robins, J. M. (2010). Causal inference.

- Higgins et al., (2016) Higgins, M. J., Sävje, F., and Sekhon, J. S. (2016). Improving massive experiments with threshold blocking. Proceedings of the National Academy of Sciences, 113(27):7369–7376.

- Imai et al., (2009) Imai, K., King, G., and Nall, C. (2009). The essential role of pair matching in cluster-randomized experiments, with application to the mexican universal health insurance evaluation.

- Imbens and Rubin, (2015) Imbens, G. W. and Rubin, D. B. (2015). Causal inference in statistics, social, and biomedical sciences. Cambridge University Press.

- Kallus, (2018) Kallus, N. (2018). Optimal a priori balance in the design of controlled experiments. Journal of the Royal Statistical Society Series B: Statistical Methodology, 80(1):85–112.

- Kapelner et al., (2021) Kapelner, A., Krieger, A. M., Sklar, M., Shalit, U., and Azriel, D. (2021). Harmonizing optimized designs with classic randomization in experiments. The American Statistician, 75(2):195–206.

- Kasy, (2016) Kasy, M. (2016). Why experimenters might not always want to randomize, and what they could do instead. Political Analysis, 24(3):324–338.

- Kempthorne, (1955) Kempthorne, O. (1955). The randomization theory of experimental inference. Journal of the American Statistical Association, 50(271):946–967.

- Krieger et al., (2019) Krieger, A. M., Azriel, D., and Kapelner, A. (2019). Nearly random designs with greatly improved balance. Biometrika, 106(3):695–701.

- Kulkarni et al., (2023) Kulkarni, J., Reis, V., and Rothvoss, T. (2023). Optimal online discrepancy minimization. arXiv preprint arXiv:2308.01406.

- LaLonde, (1986) LaLonde, R. J. (1986). Evaluating the econometric evaluations of training programs with experimental data. The American economic review, pages 604–620.

- Levy et al., (2017) Levy, A., Ramadas, H., and Rothvoss, T. (2017). Deterministic discrepancy minimization via the multiplicative weight update method. In International Conference on Integer Programming and Combinatorial Optimization, pages 380–391. Springer.

- Li and Ding, (2020) Li, X. and Ding, P. (2020). Rerandomization and regression adjustment. Journal of the Royal Statistical Society Series B: Statistical Methodology, 82(1):241–268.

- Li et al., (2018) Li, X., Ding, P., and Rubin, D. B. (2018). Asymptotic theory of rerandomization in treatment–control experiments. Proceedings of the National Academy of Sciences, 115(37):9157–9162.

- Lovett and Meka, (2015) Lovett, S. and Meka, R. (2015). Constructive discrepancy minimization by walking on the edges. SIAM Journal on Computing, 44(5):1573–1582.

- Matousek, (1999) Matousek, J. (1999). Geometric discrepancy: An illustrated guide, volume 18. Springer Science & Business Media.

- Morgan and Rubin, (2012) Morgan, K. L. and Rubin, D. B. (2012). Rerandomization to improve covariate balance in experiments. The Annals of Statistics.

- Morgan and Winship, (2014) Morgan, S. L. and Winship, C. (2014). Counterfactuals and Causal Inference: Methods and Principles for Social Research. Analytical Methods for Social Research. Cambridge University Press, 2 edition.

- Pesenti and Vladu, (2023) Pesenti, L. and Vladu, A. (2023). Discrepancy minimization via regularization. In Proceedings of the 2023 Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 1734–1758. SIAM.

- Rosenberger and Lachin, (2015) Rosenberger, W. F. and Lachin, J. M. (2015). Randomization in clinical trials: theory and practice. John Wiley & Sons.

- Rothvoss, (2014) Rothvoss, T. (2014). Constructive discrepancy minimization for convex sets. In Proceedings of the 2014 IEEE 55th Annual Symposium on Foundations of Computer Science, pages 140–145. IEEE Computer Society.

- Rubin, (2005) Rubin, D. B. (2005). Causal inference using potential outcomes: Design, modeling, decisions. Journal of the American Statistical Association, 100(469):322–331.

- Ryeznik and Sverdlov, (2018) Ryeznik, Y. and Sverdlov, O. (2018). A comparative study of restricted randomization procedures for multiarm trials with equal or unequal treatment allocation ratios. Statistics in Medicine, 37(21):3056–3077.

- Spielman and Zhang, (2022) Spielman, D. A. and Zhang, P. (2022). Hardness results for weaver’s discrepancy problem. In Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques (APPROX/RANDOM 2022). Schloss Dagstuhl-Leibniz-Zentrum für Informatik.

- Student, (1938) Student (1938). Comparison between balanced and random arrangements of field plots. Biometrika, pages 363–378.

- Sverdlov and Ryeznik, (2019) Sverdlov, O. and Ryeznik, Y. (2019). Implementing unequal randomization in clinical trials with heterogeneous treatment costs. Statistics in Medicine, 38(16):2905–2927.

- Thompson, (1965) Thompson, C. J. (1965). Inequality with applications in statistical mechanics. Journal of Mathematical Physics, 6(11):1812–1813.

- Torgerson and Campbell, (1997) Torgerson, D. and Campbell, M. (1997). Unequal randomisation can improve the economic efficiency of clinical trials. Journal of Health Services Research & Policy, 2(2):81–85.

- Tropp, (2015) Tropp, J. A. (2015). An introduction to matrix concentration inequalities. Foundations and Trends® in Machine Learning, 8(1-2):1–230.

- Turner et al., (2020) Turner, P., Meka, R., and Rigollet, P. (2020). Balancing gaussian vectors in high dimension. In Conference on Learning Theory, pages 3455–3486. PMLR.

- Wong and Zhu, (2008) Wong, W. K. and Zhu, W. (2008). Optimum treatment allocation rules under a variance heterogeneity model. Statistics in Medicine, 27(22):4581–4595.

- Zhang et al., (2024) Zhang, H., Yin, G., and Rubin, D. B. (2024). Pca rerandomization. Canadian Journal of Statistics, 52(1):5–25.

- Zhang, (2022) Zhang, P. (2022). Hardness results for minimizing the covariance of randomly signed sum of vectors. arXiv preprint arXiv:2211.14658.

Supplementary Materials

1 A Numerical Instance where Bernoulli Performs Better than GSW

We present a numerical example showing that the Bernoulli design has a smaller objective value than the GSW design for the distributional discrepancy minimization (DDM) problem:

The Bernoulli design has , while the GSW design’s is . Building on this -by- matrix, we can construct a family of matrices in larger dimensions. In general, the Bernoulli design may perform better than the GSW when entries of are near or and the operator norm of is small but greater than .

2 Missing NP-hardness Proofs for the DDM Problem

In this section, we prove two strong NP-hardness results for the Distributional Discrepancy Minimization (DDM) problem described in Problem 3.1. One result is for equal assignment probabilities (Theorem 2.1), and the other is for unequal probabilities (Theorem 2.2). We can obtain Theorem 4.1 as a Corollary of Theorem 2.2. The results and proofs are originally presented in an unpublished manuscript by the second author (Zhang,, 2022).

Theorem 2.1.

There exists a universal constant such that given a matrix with , it is NP-hard to distinguish whether or .

Theorem 2.2 (Restatement of Theorem 4.1).

There exists a universal constant such that the following holds. For any positive integer and parameters , there exists such that it is NP-hard to distinguish between the following two cases for a given matrix with : (1) or (2) .

Our proofs are based on reductions from the - Set-Splitting problem, which was introduced and shown to be NP-hard in a strong sense in Guruswami, (2004). In an instance of the - Set-Splitting problem, we are given a universe and a family of sets in which each consists of distinct elements from . We denote such an instance . Our goal is to find an assignment of the elements in to , denoted by , to maximize the number of sets in in which the values of its elements sum up to . We say an assignment --splits (or simply, splits) a set if ; we say unsplits otherwise, in which case . We say a - Set-Splitting instance is satisfiable if there exists an assignment that splits all the sets in . For any , we say an instance is -unsatisfiable if any assignment must unsplit at least fraction of the sets in . A - Set-Splitting instance is called a - Set-Splitting instance if each element in appears in at most sets in . In such an instance, we have .

Theorem 2.3 (Spielman and Zhang, (2022)).

There exists a constant such that it is NP-hard to distinguish satisfiable instances of the - Set-Splitting problem from -unsatisfiable instances.

Our proofs are inspired by the methods from Charikar et al., (2011) and Spielman and Zhang, (2022). However, the problems and proofs in these two papers are very different from ours.

2.1 Proof of Theorem 2.1

We locally abuse our notations to let the columns of be in this subsection.

Given a - Set-Splitting instance where and , we will construct a matrix where each column has Euclidean norm and are parameters to be determined later. Our construction will map a satisfiable - Set-Splitting instance to an such that and a -unsatisfiable instance to an such that .

For each element , let consist of the indices of the sets that contain . For each element that appears in exactly set in (that is, ), we create new sets and new elements. For each element that appears in sets in , we create new sets and new elements. Let be the set consisting of the indices of the newly created sets for element . The sets ’s are disjoint. Suppose there are elements in that appear in exactly set in and elements that appear in sets. We set

Consider each element , there are cases depending on how many sets in containing :

-

1.

Element appears in sets in : We define such that for and otherwise.

-

2.

Element appears in set in : Suppose . We define such that for and otherwise. We define two more vectors: (1) such that and for all other ’s, and (2) such that and and for all other ’s.

-

3.

Element appears in sets in : Suppose . We define such that for and otherwise. We define three more vectors (1) such that and for all other ’s, (2) such that and for all other ’s, and (3) such that and for all other ’s.

We let be the vectors ’s constructed above. We can check that all have Euclidean norm .

By our construction, the first entries of every vector all have a zero value. For any assignment for the - Set-Splitting instance and , the number equals the sum of the elements in set .

Claim 2.4.

For any , there exists a vector such that the following holds: Let . Then, for every , and for every .

Proof.

For each , we set . Since the first entries of for are all zero, our satisfies the first condition in the statement for where . We will choose the signs of the rest of the entries of to satisfy the second condition.

Since all the ’s are disjoint, for each element appearing in less than sets in , we only need to check the entries of with indices in . Let be an element that appears in set in . The subvectors of restricted to the coordinates in are:

We choose the signs in for to be and , respectively, which guarantees the signed sum of the is when restricted to . Since any other vector has for the coordinates in , we have for . Now, let be an element that appears in set in . The subvectors of restricted to the coordinates in are:

We choose the signs in for to be , respectively. This guarantees for . Thus, the constructed satisfies the conditions. ∎

Proof of Theorem 2.1.

Suppose the given - Set-Splitting instance is satisfiable, meaning there exists an assignment such that for every . We construct a vector as in Claim 2.4 that satisfies . We define a random vector such that with probability and with probability . Thus, and . This implies .

Next, suppose the given - Set-Splitting instance is -unsatisfiable, meaning that for any assignment , at least fraction of the entries of are in . Then, for any , at least fraction of the entries of are in . Then, for any random with , let ,

The last inequality holds since . That is, . If we can distinguish whether or , then we can distinguish whether a - Set-Splitting instance is satisfiable or -unsatisfiable, which is NP-hard by Theorem 2.3. ∎

2.2 Proof of Theorem 2.2

In this section, we prove Theorem 2.2.

Given a - Set-Splitting instance where and , we will construct a matrix and a probability vector . Let be the incidence matrix of the - Set-Splitting instance , where if element and otherwise. Since each set in has distinct elements, each row of has a sum of value . We define a larger matrix:

where is the identity matrix and is the orthogonal projection matrix onto the subspace of that is orthogonal to the all-one vector. Let

Observe that all columns of have Euclidean norm . Let

We will show that satisfies the conditions in Theorem 2.2.

Next, we construct the assignment probability vector . Let

For a positive integer , we let be the all-one vector in dimensions. We define

and

The following claim provides a simple formula for for with expectation .

Claim 2.5.

If satisfies , then .

Proof.

Note that

It suffices to show that . By our construction of ,

Since and , we have . ∎

2.2.1 Satisfiable - Set-Splitting Instance

Lemma 2.6.

Suppose the - Set-Splitting instance satisfiable. Then, , that is, there exists a random such that and .

We construct a random as follows. Let be an assignment that splits all the sets in . Then, . Let

and let

We construct the following random : let with probability (w.p.) , w.p. , w.p. , w.p. , and w.p. . We can check that is well-defined:

2.2.2 Unsatisfiable - Set-Splitting Instance

Lemma 2.7.

Suppose the - Set-Splitting instance is -unsatisfiable, that is, for any , at least fraction of the entries of are in . Then, , that is, for any random satisfying , we must have .

Let be a random vectors satisfying . We let , , and ; that is, contains the first entries of , contains the next entries, and contains the last entries. Then,

It suffices to show that . The following claim decomposes into three terms.

Claim 2.8.

For any satisfying ,

Proof.

We will show that at least one of the three terms in Claim 2.8 is sufficiently large. We first look at the last two terms and . Define

Claim 2.9.

Let . If , then .

Proof.

Note that

Take expectation:

where the last equality holds since . ∎

Claim 2.10.

If for each , then .

The idea is to show that under the assumption of Claim 2.10, with probability , a large fraction of the entries of are . Assuming this event holds,

where the last equality holds since the - Set-Splitting instance is -unsatisfiable. Thus, Claim 2.10 holds.

We will need the following properties about for .

Claim 2.11.

Let be a random variable. Then, for any , .

Proof.

Note that

By rearranging the inequality above, we can show that the claim statement holds. ∎

Claim 2.12.

Let be a random variable. Then, for any ,

Proof.

We introduce some notations:

Let (respectively, ) be the indicator for (respectively, ). Then,

In addition,

Combining the above two inequalities obtains the first inequality in the claim statement.

To lower bound , we note that

In addition,

Combining the above two inequalities obtains the second inequality in the claim statement. ∎

Now, we are ready to prove Claim 2.10.

Proof of Claim 2.10.

We choose . By our choice of ,

| (11) |

Let be the event that both happen. Let be the complement of . Then,

| (by a union bound) | ||||

| (by Claim 2.12) | ||||

| (by Equation (11) and Claim 2.11) | ||||

| (by our setting of and assumption on ) | ||||

| (since ) | ||||

| (since ) |

Assuming event happens, at least

fraction of the entries of are , and at least

fraction of the entries of are . Thus, at least fraction of the entries of are . Among these -valued entries of , at least fraction of the entries of are in . In this case,

Therefore,

| (since ) |

∎

3 Missing Proofs in Section 5

3.1 Proofs for Theorem 5.1

We start with presenting a proof that assumes the matrices , which appear in lines 3 and 4 of Algorithm 1, have explicit forms (that is, given , an oracle can return an explicit form of ). This assumption simplifies our proof: Under it, all covariance matrices , weight matrices , probabilities , and the number of while-iterations are deterministic. Later, in Section 3.1.1, we explain how to drop this assumption by estimating the covariance matrices using their empirical means.

Let returned by Algorithm 1. Let be the last while-iteration, that is, . For , let .

By our assumption of the oracle that for , we have the following lemma.

Lemma 3.1.

Assuming all have known forms in Algorithm 1, we have .

Proof.

Let . Under the assumption, probabilities and iterations are deterministic. By our assumption on the oracle , we have for each . Thus,

∎

It remains to provide an upper bound for . We will need the following facts on matrix exponential and matrix trace. For two symmetric matrices , is the Loewner order meaning that is positive semidefinite.

Theorem 3.2 (Golden–Thompson inequality (Golden,, 1965; Thompson,, 1965)).

Let be two symmetric matrices. Then, .

Lemma 3.3.

Let be symmetric positive semidefinite matrices such that . Then, .

Proof.

Let be the square root of matrix , that is, is symmetric positive semidefinite and . Since , we have

∎

Claim 3.4.

Let where each column has unit norm, and let . Then,

Proof.

∎

Proof of Theorem 5.1 assuming known forms for in Algorithm 1.

By line 7 of Algorithm 1, we have

Let . For each , we define a potential function where is defined in line 4. Then,

| (by the Golden-Thompson inequality (Theorem 3.2)) | ||||

| (since for and Lemma 3.3) | ||||

| (12) | ||||

| (by the assumption of oracle ) | ||||

Recursively applying the above inequality, we have

| (since ) |

By the definition of and ,

Take the logarithm on both sides,

Diving on both sides,

where the second inequality follows the termination criteria in line 2. Thus, .

3.1.1 Unknown Covariance Matrices

When covariance matrices in Algorithm 1 do not have explicit forms, we can estimate them by their empirical means. Specifically, we replace each by defined as follows: We pre-specify a parameter . For , independently sample . Let

where .

Let be the output of Algorithm 1 using ’s. Let be the last iteration, that is, . In addition, let be the expectation conditioned on the first iterations.

Lemma 3.5.

Assuming that we estimate each in Algorithm 1 using its empirical mean of independent samples, we have .

Proof.

Let be a fixed upper bound of . For , we let and . For each , conditioning on the first iterations, and are independent, and thus by the assumption of the oracle,

Then,

∎

For each , let be the covariance matrix where . Suppose the algorithm produces a sequence and a sequence (which are no longer deterministic since they depend on random matrices ). We can express the covariance matrix as follows:

| (13) |

For notation brevity, we will drop the subscript or when the context is clear.

We claim that if is chosen sufficiently large, given , our estimate is sufficiently close to the true value of . We will need the following theorem on approximating a covariance matrix by an empirical estimator.

Theorem 3.6 (Covariance estimator (Ref: Section 1.6.3. of Tropp, (2015))).

Let be a random vector with and . Let be the covariance matrix of . Let be independent copies of , and let

Then,

Proof of Theorem 5.1 assuming no known forms for in Algorithm 1.

We first bound the runtime of the algorithm. Let

| (14) |

We choose

| (15) |

which is polynomial in . Similar to the proof of Theorem 5.1 assuming known in Section 3.1, we can bound the number of iterations . So, the algorithm has a polynomial runtime.

Next, we upper bound .

Given any fixed and , we apply Theorem 3.6 with . Then, and (by Claim 3.4). Let be the probability conditioned on . Then,

Let be the event there exists such that conditioning on , . We note . Then,

We condition on event , the complement of event . For each , we define a potential function , and we reload the notation . By Equation (12) (replacing with for ), we have

Since and we assume , we have

Plugging into the equation on and :

Following the rest of the proof of Theorem 5.1 in Section 3.1 where we replace with and replace with , we have

Thus,

where the last inequality is by our setting of in Equation (14).

Remark on runtime.

Our choice of in Equation (15) guarantees the stated covariance norm bound in the worst case. In practice, a much smaller such as might be sufficient. Our algorithm is slower than the GSW design in Harshaw et al., (2024). However, our algorithm’s runtime remains polynomial in the size of the inputs, which is acceptable for a broad spectrum of randomized experiments. In the fields of medicine, agriculture, and education, many experiments have no more than hundreds of covariates and units; running our algorithm takes a reasonable amount of time (depending on the parameters). The additional time required for planning/designing a randomized experiment may be negligible in comparison to the potentially years-long duration of the experiment’s implementation. In such cases, the increased computational cost of planning is far outweighed by the gains in estimation accuracy.

3.2 Proofs for Theorem 5.2

Our choice of the update vector in Equation (10) for Algorithm 2 and our analysis of the norm of covariance draws inspiration from Bansal et al., (2019). However, both our Algorithm 2 and its analysis differ from those in Bansal et al., (2019). The algorithm in Bansal et al., (2019) chooses each through a semidefinite program, but our algorithm finds from a linear subspace of . This simpler approach makes it possible to use Algorithm 2 in (slightly) larger-scale applications where the input matrix has (slightly) larger dimensions. In addition, while the analysis of the algorithm in Bansal et al., (2019) only implies , the relation between and is unclear.

Let . Let be the last while-iteration, that is, . Our choice of guarantees for each , which leads to the following lemma.

Lemma 3.7.

.

Proof.

By our choice of , for each , . Thus,

∎

We upper bound . We need the following property about the update vector .

Let . Let be the vector in Equation (10).

Claim 3.8.

.

Proof.

We show that there exists a linear subspace of dimension at least such that

| (16) |

By the definition of ,

Since is positive semidefinite, if its th diagonal is zero, then its th row and th column are all zero. Let be the square root of and be the pseudo-inverse of . Then,

Let be the eigenvalues of . Then,

Rearranging the above inequality:

We let be the linear subspace spanned by the eigenvectors associated with . Then, satisfies Equation (16).

In addition, the rank of the subspace that is orthogonal to is at least

Thus, there exists that is orthogonal to and satisfies . Therefore, . ∎

For each , let

| (17) |

Note that and .

Claim 3.9.

.

Proof.

By definition of and the fact that ,

By our update of , for each ,

| (since ) |

For each where at least one of not in ,

Thus,

| (since ) | ||||

| (by Claim 3.8) |

∎

Below, we bound in terms of .

Lemma 3.10.

.

Proof.

Without loss of generality, assume (otherwise, we can do a linear transform). Let be the columns of . Then,

Let . For each , let .

| (18) | ||||

| (since ) | ||||

| (by Claim 3.9) |

Sum up the above equation over ,

| (since ) | ||||

∎

Finally, we bound in terms of .

Lemma 3.11.

.

Proof.

Proof of Theorem 5.2.

Lemma 3.7, 3.10, and 3.11 guarantees the expectation and covariance requirement on . Since each while-iteration in Algorithm 2 turns at least one non entry of to and the algorithm only updates non entries, the total number of iterations is at most . Each iteration runs in polynomial time, thus the total runtime is polynomial. ∎

4 Statistical Characterizations of the MWU Design

In this section, we characterize the expected value, variance, consistency, and convergence rate of estimation error for the average treatment effect under the MWU design. We prove Propositions 4.3, 4.4, 4.5, and 4.6. The proofs follow those in Harshaw et al., (2024). We include them for completeness.

Proof of Proposition 4.3.

Proof of Proposition 4.4.

The statement follows that returned by the MWU design is a feasible assignment and the definition of the HT estimator. ∎

Proof of Proposition 4.5.

5 Additional Experiment Details

We include the details of design implementations and experiment setups for the experiments in Section 6.

5.1 Designs

5.1.1 The MWU Design

We provide implementation details for our MWU design. Algorithm 1 has two parameters: and . The parameter controls the approximation quality of the assignment returned by the oracle in Algorithm 2 and the assignment by Algorithm 1 itself. The parameter serves as an upper bound for the assignments generated by the oracle and, along with , determines the number of iterations in the while loop at line 2 of Algorithm 1. Given that the theoretical upper bound in Theorem 5.2 for Algorithm 2 might be overly conservative, we simplify the parameter choices by omitting and introducing a new parameter, , to explicitly specify the number of while-iterations. This modification does not change the algorithm’s main ideas. If a suitable is available, one can estimate an upper bound for the while-iterations and assign this value to .

As explained in Supplementary Section 3.1.1, the matrices in lines 3 and 4 of Algorithm 1 typically do not have explicit forms. However, we can approximate these matrices by calculating their empirical mean using independent samples of . Therefore, we include as an additional parameter in the implementation of Algorithm 1.

In our experiments, we set , , and .

5.1.2 Other Benchmark Designs

We provide the details for some compared benchmark designs. Our implemented randomized block design follows the one in Azriel et al., (2022): we only use the first two covariates to block units. Suppose we set each block to have size . We first sort the units by the first covariate. Then within blocks of size , we sort and block the units by the second covariate. We implement Rerandomization with (exact) acceptance probability and Mahalanobis distance.

5.2 Data Generating Process

We detail the outcome data-generating process in Section 6.2. Recall that, for units, we generate each covariate vector with i.i.d. entries uniform from . We choose outcomes and , where . For each , let

the sum of the first twenty entries of . We choose function from the following four categories:

-

1.

linear:

-

2.

quadratic:

-

3.

a mix of linear and quadratic:

-

4.

a mix of linear, quadratic and cubic: