Factor risk measures

Abstract

This paper introduces and studies factor risk measures. While risk measures only rely on the distribution of a loss random variable, in many cases risk needs to be measured relative to some major factors. In this paper, we introduce a double-argument mapping as a risk measure to assess the risk relative to a vector of factors, called factor risk measure. The factor risk measure only depends on the joint distribution of the risk and the factors. A set of natural axioms are discussed, and particularly distortion, quantile, linear and coherent factor risk measures are introduced and characterized. Moreover, we introduce a large set of concrete factor risk measures and many of them are new to the literature, which are interpreted in the context of regulatory capital requirement. Finally, the distortion factor risk measures are applied in the risk-sharing problem and some numerical examples are presented to show the difference between the Value-at-Risk and the quantile factor risk measures.

Keywords: Distortion factor risk measures, quantile factor risk measure, linear factor risk measure, coherent factor risk measure, , risk sharing

1 Introduction

Risk measures have been widely used in banking and insurance for various purposes such as regulation, optimization and risk pricing. Since the seminal paper of Artzner et al. (1999), risk measures are commonly defined as functionals on a set of random variables representing profit/loss of the portfolios. The commonly used risk measures are law-invariant, only depending on the distribution of the risk. Two popular law-invariant risk measures in regulation are the Value-at-Risk () and the Expected Shortfall (); one can refer to McNeil et al. (2015) and Föllmer and Schied (2016) for more discussions on the risk measures.

From the regulatory prospective, a regulator is more concerned with the risk in stress scenario; see e.g., Acharya et al. (2012) for more detailed discussion. In the credit rating practice, a structured finance security is rated by the risk behavior on each economic scenario; see e.g., Standard and Poor’s (2019), Moody’s (2023) and Guo et al. (2024). However, the distribution of the risk alone is not able to capture the behavior of the risk under different scenarios. Different scenarios can be represented by some random variables. Those random variables can be viewed as factors. The nature of the risk is more comprehensively described by the risk together with some factors than the risk alone. Hence, different problems in insurance and finance consider risk management relative to a set of specific risk factors. For instance, in the systematic risk, the market risk works as the factor; in pricing, the economic factors indexes are considered as the factors; in the systemic risk, the common shock is the variable relative to which we do the risk management; in the catastrophic risk, specific natural indexes such as the temperature in frost events, or Richter index in earthquake constitute the major factors for the losses.

All the above facts motivate us to study risk functionals with double arguments: one is the risk and the second is a vector of random variables representing the factors. We call them factor risk measures. Recently, in Wang and Ziegel (2021), different scenarios are captured by a set of probability measures, which is very different but also closely related to the setup in this paper. One can also refer to Kou and Peng (2016) for the similar consideration. More details will be discussed in Sections 2 and 3.

Since the financial crisis in 2008, systemic risk have been considered more seriously as part of the risk management process. Co-risk measures are among the most studied systemic risk measures. This type of risk measures conditions the risk measurement on the occurrence of a systemic risk such as conditional Value-at-Risk (CoVaR) of Adrian and Brunnermeier (2016), the conditional Expected Shortfall (CoES) of Mainik and Schaanning (2014), and the marginal Expected Shortfall (MES) of Acharya et al. (2017). Recently, Dhaene et al. (2022) have integrated all the above risk measures in one, and call them conditional distortion risk measure. The Co-risk measures actually rely on the conditional distribution of the risk on the event of systemic risk, which is determined by the joint distribution of the risk and the systemic risk. This is intrinsically different from the classical law-invariant risk measures in Föllmer and Schied (2016). In this paper, we will follow the same idea as Co-risk measures to consider the factor risk measures solely depending on the joint distribution of the risk and the factors. We call it law-invariant factor risk measure.

Compared with the risk measures in the literatures, the novelty of this paper stems from the new type of law-invariance. The law-invariance considered in this paper is closely related to the scenario-based law-invariance discussed in Wang and Ziegel (2021) and the conditional law-invariance studied in Dela Vega and Elliott (2021) and de Castro et al. (2024). Their relation is discussed in Proposition 1 in Section 2. The law-invariance is crucial in our characterization as it relates the risk and the factors and allows us to evaluate the risk relative to the factors. Hence, the main theme of this study is to assess the risk relative to a set of major factors. This will be clear from our discussions and examples later in the paper.

Under this new law-invariance, we study factor risk measures satisfying monotonicity and comonotonic-additivity which are called the distortion factor risk measures in Section 3. The classical distortion risk measures have been widely applied in decision theory (Yaari (1987)), insurance and option pricing (Wang (1996) and Wang (2000)), performance evaluation (Cherny and Madan (2009)) and quantitative risk management (McNeil et al. (2015) and Föllmer and Schied (2016)). Hence, its generalization to the case with factors is important from both theoretical and practical perspective. In our characterization in Theorem 1, the distortion factor risk measure can be represented by a Choquet integral defined by a distortion functional on a set of Borel measurable functions, which extends the classical distortion risk measures given by a Choquet integral with a distortion function on the real line. Moreover, we find a necessary and sufficient condition on the distortion functionals such that the distortion factor risk measure is coherent. Finally, we show some concrete examples of distortion factor risk measures such as , the distortion of conditional and the expectation of conditional . Most of those factor risk measures are new and they offer new angles to evaluate the risk affected by some factors. To some extend, our characterization results in Section 3 extend the results in Wang and Ziegel (2021). It is also worth mentioning that our characterization with the aid of the distortion functionals on a set of Borel measurable functions is very different from Gong et al. (2022), where the axioms are state-wise and the expressions are state-wise based.

Quantiles are one of the important tools in decision theory (Rostek (2010) and de Castro and Galvao (2019)), statistics (Koenker and Hallock (2001)), finance (Basak and Shapiro (2001)), risk management (Embrechts et al. (2018)) and many other fields. Its characterization has been considered using different axioms such as elicitability in Kou and Peng (2016), tail-relevance in Liu and Wang (2021), and ordinality in Chambers (2009) and Fadina et al. (2023). In Section 4, we study factor risk measures satisfying law-invariance, monotonicity and ordinality, called quantile factor risk measures. We find the expressions of the quantile factor risk measures including as a special case. The expressions in Theorem 2 have the same spirit as the definition of quantiles, offering a natural extension of quantiles to the cases with factors. Some concrete examples are given such as the of conditional and the esssup of conditional . Those quantile factor risk measures are interpreted in the context of the regulatory capital requirement and they have the potential to be applied in practice because of the simple form.

In Section 5, we characterize linear factor risk measures, which can be expressed as the weighted average of the conditional expectation. It includes as a special case and has the same form as Moody’s rating measure for credit rating (Moody’s (2023)). Coherent risk measures and its extensions become popular in the quantitative risk management since the seminal papers of Artzner et al. (1999), Föllmer and Schied (2002) and Frittelli and Rosazza Gianin (2005); see also Föllmer and Schied (2016) for a comprehensive overview of coherent risk measures. The coherent factor risk measures are studied in Section 6. It is nontrivial to obtain its expression as it relies on an extension of the Hardy-Littewood inequality. Some simple examples are also shown such as the of conditional and the esssup of conditional .

Finally, in Section 7, we put our focus on the applications of the distortion factor risk measures to the comonotonic risk sharing problem and on the numerical comparison of and the quantile factor risk measures in risk evaluation. Some notation and definitions are displayed in Section 2 and all the proofs of the results in this paper are postponed to Appendix.

2 Preliminaries

Consider an atomless probability space , where is the set of the states, is a sigma field on and is a probability measure. Let be a random variable, from the set consisting of loss variables. We suppose . Let be the set of factor random variables consisting of random vectors with . Typically, we suppose is law-invariant, i.e., implies if , where represents quality in distribution. As usual, denotes the cumulative distribution function (CDF) of and denotes the left quantile of , given by

with the convention . Moreover, two regulatory risk measures Value-at-Risk () and Expected shortfall () are defined as follows: For ,

For ,

Another important class of risk measure is called distortion risk measure. For , the distortion risk measure with the distortion function is given by

where denotes the set of all non-decreasing functions satisfying and . We refer to McNeil et al. (2015) and Föllmer and Schied (2016) for more discussions on these risk measures.

Before we introduce the conditional and , we need the following nation. For and , by Theorem 33.3 of Billingsley (1995), there exists such that

-

(i)

For each , is a probability measure on ;

-

(ii)

For each , is a version of .

The conditional quantile is defined by for and . Moreover, the conditional expected shortfall (ES) is defined by for , for .

In Adrian and Brunnermeier (2016) and Mainik and Schaanning (2014), the and are defined as below: For and ,

and

For , the MES is given by in Acharya et al. (2017). Our characterization of factor risk measures in Sections 3-5 cover those Co-risk measures as special cases.

We next introduce the factor risk measure. Our approach following the same idea as in the literature is to introduce axioms that are perceived to be the most appealing ones to insurance and finance applications, and then explore the implications. The axioms that are being presented are motivated from three major strands, a group stemming from the distortion risk measures, a group from the quantiles, and a group stemming from coherent risk measures.

Let us consider a risk whose risk measurement is our main objective and a vector of factors , , that has a great influence in the risk measurement of variable . These factors can have different interpretations, for instance, they can be macro-economic factors, they can be the systemic or systematic risk variable or just some random factors that may add to the uncertainty of the model.

Definition 1.

A factor risk measure is a double-argument functional to measure the risk of given , denoted by . The first variable is called the risk variable and the second variable is called the factor variable.

We next introduce the axioms that are not only appealing in the application of insurance and finance but also play crucial role in our characterization results later. We say are comonotonic if there exist a random variable and two non-decreasing functions and satisfying such that and .

-

1.

Monotonicity (M). For any two random variables , and any factor , we have .

-

2.

Comonotonic additivity (CA). For any factor and two comonotone random variables and , we have

-

3.

Normalization (N). For all .

-

4.

Law-invariance (LI). If , then .

-

5.

Ordinality (OR). For all continuous and strictly increasing functions , and , we have

As one can realize axioms M, CA and N, are mainly stemmed from the theory of distortion risk measures as it is shown in Schmeidler (1986). Axiom LI is very different from the corresponding concept in the literature, showing that the factor risk measure solely depends on the joint distribution of the risk and the factors. OR is a property introduced in Chambers (2007, 2009) to the axiomatize quantiles. In the decision-theoretic setup, it means that any continuous and strictly increasing transform on the prospects does not change the preference order; see e.g., Fadina et al. (2023).

We next introduce the coherent factor risk measures. For a mapping , we say is cash-invariant if for all and ; is positively homogeneous if for all and ; is subadditive if for . We say is monetary if is monotone and cash-invariant; is coherent if is monetary, positively homogeneous and subadditive. We refers to the monograph Föllmer and Schied (2016) for more details on the coherent risk measures.

Here, it is worth emphasizing that the novelty of this paper comes from LI. The law-invariance discussed in this paper is closely related to the -based law-invariance introduced in Wang and Ziegel (2021). For a collection of probability measures , we say is -based if for , under for all implies . The mapping considered in this paper is a double-argument mapping. However, if we fix the second argument, it boils down to a single-argument mapping. We obtain the following conclusion on the law-invariance defined in this paper and the -based law-invariance in Wang and Ziegel (2021).

Proposition 1.

Fix . A mapping is law-invariant if and only if it is -based, where ; If is discrete, then can be chosen as .

In Dela Vega and Elliott (2021) and de Castro et al. (2024), the mapping is studied based on conditional law-invariance, where is a set of random variable. The conditional law-invariance has the similar meaning to the LI in this paper if we fix the second argument.

In the rest of the paper, for simplicity and consistency, we set . Some of the results can be easily extended to more general sets.

3 Distortion factor risk measures

In this section, we shall study the risk measures satisfying M and CA. Let us first introduce some notation which plays a crucial role in the characterization results in this paper.

Let be the set of all Borel measurable functions , and is a functional satisfying and for . We say is monotone if for , , i.e., , implies ; is law-invariant if whenever for . Note that for and , is a Borel measurable function in and is not unique. We denote by .

Theorem 1.

A mapping satisfies conditions M, CA, N and LI if and only if there exists a law-invariant family of monotone functionals such that

| (1) |

It is noteworthy that provides a natural extension of distortion functions to a conditional one, and therefore can be used to introduce the factor risk measures interpreted as the risk measure based on the conditional distribution functions.

For a family of monotone functionals , we denote (1) by and call it the distortion factor risk measure with distortion functionals and factor . Clearly, satisfies M, CA and N, which can be seen from the proof of Theorem 1 in Appendix 9.2. Note that the law-invariance of is a sufficient condition but not a necessary condition to ensure the law-invariance of . A sufficient and necessary condition is weak law-invariance of : For satisfying , we have .

Proposition 2.

For a distortion factor risk measure with a family of monotone functionals , it is law-invariant if and only if is weakly law-invariant.

Note that the law-invariance of implies the weak law-invariance of . However, the converse conclusion is not true in general. One can see a counterexample in Example 7 in Appendix 9.7.

We say that is indicator lower semicontinuous (IC) if for , , implies that for all ,

The following result shows that if additionally satisfies IC, then the corresponding is continuous from below: For , (pointwise) implies . This result will be used to characterize the linear factor risk measure later in Section 5.

Proposition 3.

A mapping satisfies conditions M, CA, IC, N and LI if and only if there exists a law-invariant family of monotone and continuous from below functionals such that (1) holds.

If only contains random variables taking finite values, then Theorem 1 has a simpler version. We say is an increasing function if for , whenever , i.e., for all ; we say is law-invariant if whenever for .

Corollary 1.

Suppose all take different values. A mapping satisfies conditions M, CA, N and LI if and only if there exists a law-invariant family of monotone functions such that

Note that the result in Corollary 1 corresponds to Theorem 3.4 of Wang and Ziegel (2021) with mutually singular probability measures. More precisely, Theorem 3.4 of Wang and Ziegel (2021) states that for and , a mapping is monetary, commonotonic additive and -based if and only if there is a function such that is standard and

Here the mapping is standard means that it is increasing with set inclusion and .

For a fixed , one can see from Proposition 1 that in Theorem 1, we are in fact dealing with -based risk measures, where contains infinite many distinct probability measures. From this perspective, our result in Theorem 1 extends Theorem 3.4 of Wang and Ziegel (2021). The main technical challenge of the extension of the statement in Wang and Ziegel (2021) is that one cannot easily define a function on similarly as in our paper. Note also that Corollary 1 has the same form as the rating measure of credit rating criteria in Theorem 7 of Guo et al. (2024).

One natural question is what conditions are needed to guarantee that is coherent. Inspired by Proposition 3.5 in Wang and Ziegel (2021) and Theorem 3.12.2 of Müller and Stoyan (2002), we introduce the following condition. Condition A: For satisfying and , we have for all .

Proposition 4.

Suppose is given by (1) with a law-invariant family of monotone functionals . Then is a coherent factor risk measure if and only if satisfies condition A.

Distortion factor risk measure is very fruitful as it contains many interesting factor risk measures. We next display some examples with conditional and as the building blocks.

Example 1.

-

(i)

For with , if for all , then

-

(ii)

For , if for all , then

-

(iii)

For with , if for all , then

-

(iv)

For , if for all , then

For (i)-(iv), they can be interpreted as follows. For each scenario , the capital requirement is computed using at level , where the level varies as the scenario changes. Then, represents the average capital requirement across all scenarios and represents the distorted average capital requirement across all scenarios.

Next, we see some examples related to conditional .

Example 2.

-

(i)

For with , let for all , then

-

(ii)

For , let for all , then

-

(iii)

For , and with , where represents the collection of all Borel subsets of , let for all , then

which extends Co.

-

(iv)

For with , let for all , then

where for . Clearly, .

One can easily check that the functionals of the distortion factor risk measures defined in (i), (ii) and (iv) of Example 2 satisfy condition A. By Proposition 4, they are all coherent factor risk measures. Moreover, is the average value of under different scenarios. In terms of capital requirement, it can be interpreted as: For each scenario , the requirement is calculated using at level , where the level varies for different scenarios. The overall capital requirement is summarized as an expected value across all scenarios.

4 Quantile factor risk measure

Next, we consider the characterization of -type risk measures in terms of conditional distribution of on the factors . We shall offer expressions with two different parametric systems. We start with the following notation.

We say is increasing if and , and whenever for some . Let be a probability measure on . The notation means there exists such that . We say a family of subsets of , , is law-invariant if implies for .

Let represent the collection of all with and such that , where . Let represent a set of functions for . We say is increasing if and , and whenever for some . The law-invariance of is adapted as: For , implies . Let for .

Theorem 2.

A mapping satisfies conditions M, OR and LI if and only if one of the following statements holds:

-

(i)

There exists a law-invariant family of increasing sets such that

(2) -

(ii)

There exists a law-invariant family of increasing sets such that

(3)

For a family of increasing sets , we denote defined by (2) by and we call it quantile factor risk measure with level set and factor . Note that the classical left quantile can be expressed as and the classical right quantile can be expressed as . Clearly, if is a constant, then boils down to the classical quantiles. Hence, can be viewed as an extension of the classical quantiles.

Moreover, satisfies monotonicity and ordinality, which can be seen from the proof of Theorem 2 in Appendix 9.3. Similarly for the distortion factor risk measure, the law-invariance of is a sufficient but not a necessary condition to guarantee the law-invariance of . A sufficient and necessary condition is the weak law-invariance of : For satisfying , we have either or .

Proposition 5.

For a quantile factor risk measure with a family of increasing sets , it is law-invariant if and only if is weakly law-invariant.

If , then in (ii) of Theorem 2 is independent of : . Hence (3) becomes

If we restrict as discrete random vectors, (i) of Theorem 2 admits a simplified expression. Let be the set of all discrete random vectors . For , we denote We say is an increasing set if , and if for some . The law-invariance of : For satisfying , we have .

Corollary 2.

A mapping satisfies conditions M, OR and LI if and only if there exists a law-invariant family of increasing sets such that

| (4) |

If is a set of constants, then Theorem 2 boils down to the result in Chambers (2009) and Fadina et al. (2023), which offers the characterization of the classical quantiles. Hence, Theorem 2 defines a more general quantiles summarizing the quantiles under different scenarios into a single value.

Example 3.

For , it can be interpreted in the context of regulatory capital requirement as below. For each scenario , the capital requirement is calculated using at level , where the level varies with respect to different scenarios. The overall capital requirement is summarized by another to cover the capital requirement for different scenarios. For , guarantees the capital requirement is satisfied for all scenarios.

The following two examples are closely related to .

Example 4.

For , (3) can be simplified as follows.

-

(i)

If , then

-

(ii)

If and , then

-

(iii)

If additionally for (ii), then

Example 5.

For , and , expression (4) can be reduced to the following expressions.

-

(i)

If , then

-

(ii)

If and , then

5 Linear factor risk measures

In this section, we consider linear factor risk measures, which includes MES as a special case. We say a family of probability measures on , , is law-invariant if whenever for ; we say is additive (AD) if for all .

Theorem 3.

A mapping satisfies conditions M, AD, IC, N and LI if and only if there exists a law-invariant family of probability measures on such that , and

| (5) |

Note that if , then (5) boils down to the law of iterated expectation. Hence Theorem 3 can be viewed as an extension of the law of iterated expectation. Moreover, as is the so-called conditional expectation, (5) can be demonstrated as the weighted average of the conditional expectation. It will be more clear for the discrete random vector . Let us see some examples as below.

- (i)

- (ii)

6 Coherent factor risk measure

In this section, we aim to find the expression of coherent factor risk measures. We start with an extension of the Hardy-Littewood inequality, which is inspired by Proposition 4.6 in Dela Vega and Elliott (2021) and Lemma 3.3 of de Castro et al.(2024). This extension is crucial to characterize the coherent factor risk measure and it is also of interest independently. For and , let . In this section, we suppose that for any , there exists that is independent of .

Lemma 1.

For , and , we have

Let us next introduce some notation and properties. We denote by the set of all probability measures on that are absolutely continuous with respect to . We say a family of subsets of , , is law-invariant if for , implies . For a mapping , we say is continuous from above if whenever .

In what follows, we characterize the coherent factor risk measure.

Theorem 4.

A mapping is coherent, continuous from above and law-invariant if and only if there exists a law-invariant family of sets of probability measures such that

| (6) |

For the case of discrete taking only finite values, Theorem 4 boils down to Theorem 3.8 of Wang and Ziegel (2021). This can be seen from the following result.

Corollary 3.

Alternatively, we can construct coherent factor risk measures as follows. Using Proposition 11.9 of Föllmer and Schied (2016), we immediately arrive at the following result.

Proposition 6.

Let be a law-invariant coherent risk measure. Then the mapping with is a law-invariant coherent factor risk measure.

Example 6.

For , and are two families of law-invariant coherent factor risk measures.

7 Risk management applications

In this section, we consider the application of our main results to risk sharing problem and the evaluation of the risk with factors.

7.1 Risk sharing

In this subsection, we consider the risk sharing problem among multiple agents with the preference represented by the distortion factor risk measures. Risk sharing problem with risk measures has been widely studied in the literature. We refer to Barrieu and El Karoui (2005) and Filipović and Svindland (2008) for risk sharing with convex risk measures, and Embrechts et al. (2018) and Liu et al. (2022) for risk sharing problem with quantile-based risk measures. Our interest here is the comonotonic risk sharing problem, which is widely applied in optimal insurance and reinsurance contract design; see e.g., Arrow (1963), Albrecher et al. (2017) and Cai and Chi (2020) and the references therein.

For , we denote all the comonotonic allocations by

The risk sharing problem is defined as

We say an allocation is an optimal allocation if .

Proposition 7.

For continuous from below distortion functionals , we have

where . Moreover, the optimal allocations are with , where are non-negative measurable functions satisfying if , and .

Using Proposition 7 and the expressions in Examples 1-2, we immediately arrive at the following results.

Corollary 4.

-

(i)

For left-continuous and , let . Then we have

-

(ii)

For , let . Then we have

-

(iii)

For , let . Then we have

7.2 Evaluation of risk using

In this subsection, we evaluate the risk using a factor risk measure and then compare it with . A standard approach in economics is that we regress , over and use the model. Hence, let us consider the following model:

where is an independent idyosyncratic risk with standard normal distribution, and . By implementing this into our risk measure, we have

where is the CDF of the standard normal random variable. For non-factor risk measure, we consider

For each scenario , represents the confidence level of the capital requirement and represents the overall emphasis we want to put on the systematic risk. From the capital requirement point of view or , are standard choices, however, for we can have a wide range from to . Let us check the percentage change of compared to , i.e.,

Note that the numerator can be interpreted as the risk contribution of the -centralized factors i.e., .

7.2.1 Data

Here we describe the data set we use in this chapter. The data are on a monthly basis: a set of 642 months, from February 1952 to August 2012. We use almost the same data as in van den Goorbergh et al. (2003). The data consists of seven different securities, which work as the factors in our risk evaluation:

-

1.

Risk Free, three-month T-bill rate (as a proxy), denoted by (RF);

-

2.

Market , Market Risk minus Risk Free, denoted by (RM-RF);

-

3.

Size, Small Minus Big, denoted by (SMB);

-

4.

Book-to-market value, High Minus Low, denoted by (HML);

-

5.

Momentum, Up Minus Down, denoted by (UMD);

-

6.

Term factor, the difference between a long-term government bond return and the three-month T-bill rate, denoted by (TERM);

-

7.

Default factor, the difference between the return on a portfolio of long-term corporate bonds and a long-term government bond return, denoted by (DEF).

Items 1,2,3,4,5 are taken from the Fama and French Library. Items 2,3,4 are the usual three Fama and French factors in Fama and French (1992) and item 5 is used in Carhart (1997). The first five factors explain the premiums on stocks. Factors 6 and 7 are known as bond-market factors. The TERM factor is the difference between long-term government bond, provided by BGFRS111Board of Governors of the Federal Reserve System, and the short-term government or Treasury Bonds (T-Bill) which is the same as risk free. As for DEF, we took the Moody’s Aaa rated corporation bonds, provided by BGFRS.

In FRED222Federal Reserve Economic Data, it has a set of six macro-economic risk variables. We consider the following two risk variables as the risk that will be evaluated later:

-

1.

Real Interest rate, the monthly return on a three-month T-bill, denoted by (RI);

-

2.

Dividend yield, the monthly dividend yield on the S&P 500, denoted by (DIV).

7.2.2 Numerical results

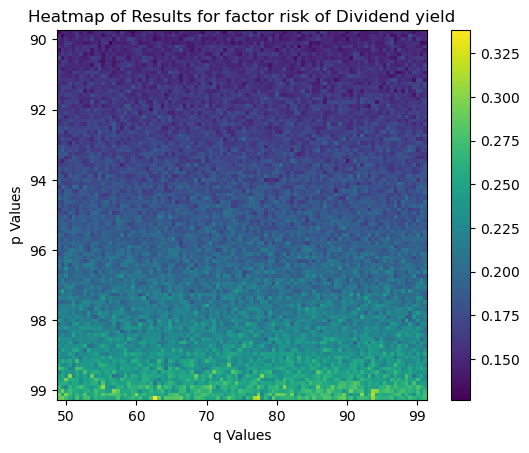

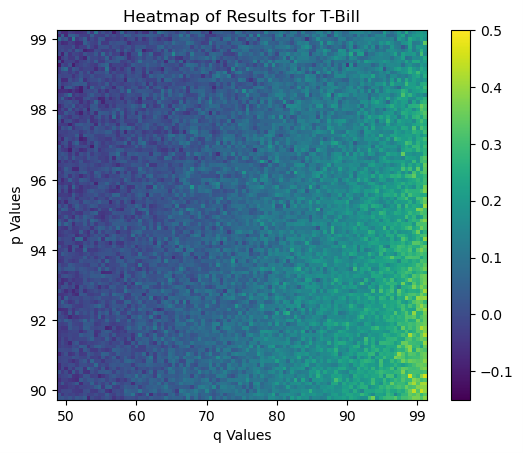

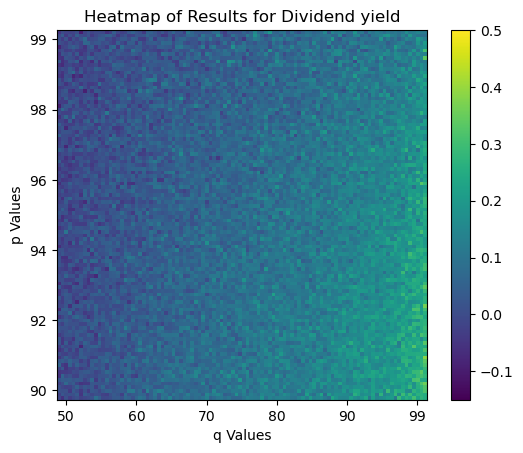

In the following, we set the range of as and the range of as and consider economic risk. We present the heatmaps of the value of in Figure 1 and the heatmaps of Diff to show the difference between and in percentage in Figure 2. The regression model is obtained in Table 1.

| coef | std err | t | Pt | [0.025 | 0.975] | ||

|---|---|---|---|---|---|---|---|

| T-bill | const | 0.1413 | 0.061 | 2.322 | 0.021 | 0.022 | 0.261 |

| RF | -0.2686 | 0.124 | -2.161 | 0.031 | -0.513 | -0.025 | |

| RM-RF | -0.0155 | 0.004 | -4.021 | 0.000 | -0.023 | -0.008 | |

| SMB | -0.0051 | 0.006 | -0.916 | 0.360 | -0.016 | 0.006 | |

| HML | -0.0207 | 0.006 | -3.433 | 0.001 | -0.033 | -0.009 | |

| UMD | -2.031e-05 | 0.004 | -0.005 | 0.996 | -0.008 | 0.008 | |

| TERM | 0.0303 | 0.013 | 2.265 | 0.024 | 0.004 | 0.057 | |

| DEF | 0.1532 | 0.033 | 4.694 | 0.000 | 0.089 | 0.217 | |

| Dividend yield | const | 0.0325 | 0.017 | 1.891 | 0.059 | -0.001 | 0.066 |

| RF | -0.1273 | 0.035 | -3.631 | 0.000 | -0.196 | -0.058 | |

| RM-RF | 0.0022 | 0.001 | 2.060 | 0.040 | 0.000 | 0.004 | |

| SMB | -0.0002 | 0.002 | -0.124 | 0.901 | -0.003 | 0.003 | |

| HML | -0.0005 | 0.002 | -0.299 | 0.765 | -0.004 | 0.003 | |

| UMD | 0.0025 | 0.001 | 2.293 | 0.022 | 0.000 | 0.005 | |

| TERM | 0.0119 | 0.004 | 3.159 | 0.002 | 0.005 | 0.019 | |

| DEF | 0.0369 | 0.009 | 4.005 | 0.000 | 0.019 | 0.055 |

In Figure 1, we present the values of of T-Bill and Dividend for different values of and .

In Figure 2, we present the Diff(T-Bill) and Diff(Dividend) for different values of and .

As it is clear that for larger values of , Diff(T-Bill) and Diff(Dividend) are more positive, which indicates for larger the value of the factor risk measure is larger. For smaller , Diff(T-Bill) and Diff(Dividend) become more negative, which indicates the value of the factor risk measure is smaller than for smaller . We can expect that there is a such that . This means that can satisfy the capital requirement for of different scenarios. We can also see that is more flexible than as it has one additional parameter to adjust the values.

While the values of Diff for T-bill ranges in , Diff for Dividend yield ranges in . This shows that the contribution of the factors to the risk causes larger percentage change for T-bill compared with Dividend yield.

8 Concluding remarks

In this paper we motivated and introduced factor risk measures, to evaluate the risk with regards to a factor vector. The main contribution of this paper is to characterize the distortion, quantile, linear and coherent factor risk measures by deriving the explicit expressions for the factor risk measures satisfying some desirable properties. We have introduced many concrete examples of factor risk measures such as , , , , , and . Those factor risk measures have potential to be applied in quantitative risk management and other fields, and need further investigation. We have shown how distortion factor risk measures can be naturally applied in risk-sharing and how quantile factor risk measures are applied in risk evaluation.

References

- Acharya et al. (2012) Acharya, V., Engle, R. and Richardson, M. (2012). Capital shortfall: a new approach to ranking and regulating systemic risks, American Economic Reveiw, 102, 59–64.

- Acharya et al. (2017) Acharya, V., Pedersen, L., Philippon, T. and Richardson, M. (2017). Measuring Systemic Risk, The Review of Financail Studies, 30(1), 2–47.

- Adrian and Brunnermeier (2016) Adrian, T. and Brunnermeier, M. K. (2016). Covar. American Economic Review, 106(7), 1705–1741.

- Arrow (1963) Arrow, K. J. (1963). Uncertainty and the Welfare Economics of Medical Care. American Economic Review, 53, 941–973.

- Albrecher et al. (2017) Albrecher, H., Beirlant, J. and Teugels, J.L. (2017). Reinsurance: Actuarial and Statistical Aspects. John & Wiley Sons.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J.-M. and Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9(3), 203–228.

- Barrieu and El Karoui (2005) Barrieu, P. and El Karoui, N. (2005). Inf-convolution of risk measures and optimal risk transfer. Finance and Stochastics, 9, 269–298.

- Basak and Shapiro (2001) Basak, S. and Shapiro, A. (2001). Value-at-Risk based risk management: Optimal policies and asset prices. Review of Financial Studies, 14(2), 371–405.

- Billingsley (1995) Billingsley, P. (1995). Probability and Measure. Third edition. John Wiley & Sons, Inc., New York.

- Cai and Chi (2020) Cai, J. and Chi, Y. (2020). Optimal reinsurance designs based on risk measures: a review. Statistical Theory and Related Fields, 4(1), 1–13.

- Carhart (1997) Carhart, M. M. (1997). On persistence in mutual fund performance. The Journal of Finance, 52(1), 57–82.

- Chambers (2007) Chambers, C. P. (2007). Ordinal aggregation and quantiles. Journal of Economic Theory, 137(1), 416–431.

- Chambers (2009) Chambers, C. P. (2009). An axiomatization of quantiles on the domain of distribution functions. Mathematical Finance, 19(2), 335–342.

- Cherny and Madan (2009) Cherny, A. S. and Madan, D. (2009). New measures for performance evaluation. Review of Financial Studies, 22(7), 2571–2606.

- de Castro and Galvao (2019) de Castro, L. and Galvao, A. F. (2019). Dynamic quantile models of rational behavior. Econometrica, 87, 1893–1939.

- de Castro et al. (2024) de Castro, L.I., Costa, B.N., Galvao, A.F. and Zubelli, J.(2024). Convex and Conditionally Law-Invariant Risk Measures. Available at http://dx.doi.org/10.2139/ssrn.4678487.

- Dela Vega and Elliott (2021) Dela Vega, E.J.C. and Elliott, R.J.(2021). Conditional coherent risk measures and regime-switching conic pricing. Probability, Uncertainty and Quantitative Risk, 6(4), 267–300.

- Dhaene et al. (2022) Dhaene, J., Laeven, R. J. and Zhang, Y. (2022). Systemic risk: Conditional distortion risk measures. Insurance: Mathematics and Economics, 102, 126–145.

- Embrechts et al. (2018) Embrechts, P., Liu, H. and Wang, R. (2018). Quantile-based risk sharing. Operations Research, 66(4), 936–949.

- Embrechts et al. (2019) Embrechts, P., Liu, H., Mao, T. and Wang, R. (2020). Quantile-based risk sharing with heterogeneous beliefs. Mathematical Programming Series B, 181(2), 319–347.

- Fadina et al. (2023) Fadina, T., Liu, P. and Wang, R. (2023). One axiom to rule them all: A minimalist axiomatization of quantiles. SIAM Journal on Financial Mathematics, 14(2), 644–662.

- Fama and French (1992) Fama, E. F. and French, K. R. (1992). The cross-section of expected stock returns. The Journal of Finance, 47(2), 427–465.

- Filipović and Svindland (2008) Filipović, D. and Svindland, G. (2008). Optimal capital and risk allocations for law- and cash-invariant convex functions. Finance and Stochastics, 12, 423–439.

- Föllmer and Schied (2002) Föllmer, H. and Schied, A. (2002). Convex measures of risk and trading constraints. Finance and Stochastics, 6(4) 429–447.

- Föllmer and Schied (2016) Föllmer, H. and Schied, A. (2016). Stochastic Finance. An Introduction in Discrete Time. Walter de Gruyter, Berlin, Fourth Edition.

- Frittelli and Rosazza Gianin (2005) Frittelli, M. and Rosazza Gianin, E. (2005). Law-invariant convex risk measures. Advances in Mathematical Economics, 7, 33–46.

- Gong et al. (2022) Gong, S., Hu, Y. and Wei, L. (2022). Distortion risk measures in random environments: construction and axiomatic characterization. arXiv:2211.00520.

- Guo et al. (2024) Guo, N., Kou, S., Wang, B. and Wang, R. (2024). A theory of credit rating criteria. Management Science, forthcoming.

- Jouini et al. (2008) Jouini, E., Schachermayer, W. and Touzi, N. (2008). Optimal risk sharing for law invariant monetary utility functions. Mathematical Finance, 18(2), 269–292.

- Koenker and Hallock (2001) Koenker, R. and Hallock, K. F. (2001). Quantile regression. Journal of Economic Perspectives, 15(4), 143–156.

- Kou and Peng (2016) Kou, S. and Peng, X. (2016). On the measurement of economic tail risk. Operations Research, 64(5), 1056–1072.

- Kusuoka (2001) Kusuoka, S. (2001). On law invariant coherent risk measures. Advances in Mathematical Economics, 3, 83–95.

- Liu and Wang (2021) Liu, F. and Wang, R. (2021). A theory for measures of tail risk. Mathematics of Operations Research, 46(3), 1109–1128.

- Liu et al. (2022) Liu, F., Mao, T., Wang, R. and Wei, L. (2022). Inf-convolution, optimal allocations, and model uncertainty for tail risk measures. Mathematics of Operations Research, 47(3), 2494–2519.

- Mainik and Schaanning (2014) Mainik, G. and Schaanning, E. (2014). On dependence consistency of covar and some other systemic risk measures. Statistics & Risk Modeling, 31(1), 49–77.

- McNeil et al. (2015) McNeil, A. J., Frey, R. and Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools. Revised Edition. Princeton, NJ: Princeton University Press.

- Moody’s (2023) Moody’s. (2023). Rating Methodology: Corporate synthetic CDOs. Available on https://ratings.moodys.com/rmc-documents/409859 (accessed January 2024).

- Müller and Stoyan (2002) Müller, A. and Stoyan, D. (2002). Comparison Methods for Stochastic Models and Risks. Wiley, England.

- Rostek (2010) Rostek, M. (2010). Quantile maximization in decision theory. Review of Economic Studies, 77, 339–371.

- Rüschendorf (2013) Rüschendorf, L. (2013). Mathematical Risk Analysis. Dependence, Risk Bounds, Optimal Allocations and Portfolios. Springer, Heidelberg.

- Schmeidler (1986) Schmeidler, D. (1986). Integral representation without additivity. Proceedings of the Americian Mathematical Society, 97(2), 255–261.

- Standard and Poor’s (2019) Standard and Poor’s (2019). Global methodology and assumptions for CLOs and corporate CDOs. Available on https://disclosure.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/11020014.

- van den Goorbergh et al. (2003) van den Goorbergh, R. W. J., de Roon, F. A. and Werker, B. J. M. (2003). Economic hedging portfolios. Discussion Paper 2003–102, Tilburg University, Center for Economic Research.

- Wang and Ziegel (2021) Wang, R. and Ziegel, J.F. (2021). Scenario-based risk evaluation. Finance and Stochastics, 25(4), 725–756.

- Wang (1996) Wang, S. (1996). Premium calculation by transforming the layer premium density. ASTIN Bulletin, 26(1), 71–92.

- Wang (2000) Wang, S. (2000). A class of distortion operators for pricing financial and insurance risks. Journal of Risk and Insurance, 67, 15–36.

- Yaari (1987) Yaari, M. E. (1987). The dual theory of choice under risk. Econometrica, 55(1), 95–115.

9 Appendix

9.1 Proof of results in Section 2

9.2 Proof of results in Section 3

Let us first show a new version of the characterization of Choquet integral in Schmeidler (1986), which plays an important role in the proofs of Theorems 1- 2 and Proposition 5 later. We say is a capacity if is monotone: for , and . We say is comonotonic monotone (CM) if for any two comonotonic random variables satisfying , and any factor , we have .

Proposition 8.

For a mapping , it satisfies CM and CA if and only if admits the following expression:

| (7) |

where is a capacity. Moreover, additionally satisfies LI if and only if whenever . As a by-product, we have that CM and CA is equivalent to M and CA.

Proof of Proposition 8. Note that the "if" part is obvious. We next fix a to show the "only if" part. By CA, we have for and . For , there exist two sequence and as . For , by CM, we have

Letting , we obtain . One can similarly show that for and for and . Note that and are comonotonic. Hence for ,

By Proposition 1 of Schmeidler (1986), we have for taking only finite number of values

where . Note that implies that , and and are comonotonic. Hence . Moreover, . We next show that the above expression holds for all . Let , where represents the floor function. Note that and are comonotonic and . Hence . This implies

We establish the first claim. For the second claim, note that LI of and imply whenever . Now we show the converse conclusion. For , let and . Then and . We can write and , where , and , and . Without loss of generality, we suppose . Applying (7) and noting that , we have

Moreover, it follows from (7) that and . Hence, we obtain by letting . We establish the second claim. ∎

Proof of Theorem 1. We first show the "if" part. If , then for any , we have . It follows from the monotonicity of that

for all , leading to . Hence, M of is verified. For two comonotonic random variables and , there exist increasing and Lipschitz continuous functions and satisfying such that and . It follows that

where with the convention that . Analogously, we have

Hence , meaning that satisfies CA. Direct computation shows

which implies

Hence N of is satisfied. Finally, we show LI of . For and satisfying , we have for any , . It follows from the law-invariance of that . Hence by (1), we have . The LI of is verified.

We next show the "only if" part. In light of Proposition 8, M, CA, N and LI imply that has the following representation:

| (8) |

where is a capacity with satisfying whenever . For , define . Direct computation gives and . Moreover, it follows from the definition that implies . Hence is monotone over .

Next, we show that for all . By the definition, we have . For any satisfying , we have a.s.. Note that there exist and such that and is independent of . Then and , where is the quantile function of . Note that a.s., and both of them are indicator functions. We denote and . Then we have a.s. and a.s.. By LI, we have and . By M, we have , which implies . Hence for all . Replacing by in (8), we obtain (1). Note that there exist and such that and is independent of . Hence, for any , there exists such that . By LI of , we have

This implies that can be chosen as . Hence, we can choose a law-invariant family of such that (1) holds. ∎

Proof of Proposition 2. We first show the "if" part. For and satisfying , we have for any , . It follows from the weak law-invariance of that . Hence by (1), we have .

Next, we focus on the "only if" part. The LI of implies that for satisfying , we have , which implies . Hence is weakly law-invariant. ∎

Proof of Proposition 3. We first show the "if" part. By Theorem 1, satisfies M, CA, N and LI. We next show that satisfies IC. For , we have a.s. as . We choose such that a.s.. Let and . Then and a.s. and a.s.. Direct computation shows

By (1), we have and . Using the fact that and the continuity from below of , we have , implying IC of .

Next, we focus on the "only if" part. By Theorem 1, we have (1) holds for a law-invariant family of monotone functionals . It suffices to show the continuity from below for . For , suppose . Note that there exist and such that and is independent of . Using the law-invariance of , we have and . Hence, we only need to show . Let . Then we have a.s.. The fact that implies a.s.. It follows from (1) that and . Hence, by M and IC of and the fact , we have . ∎

Proof of Corollary 1. Note that the proof of the "if" part is similar to the proof of Theorem 1. Hence, it is omitted. We next show the "only if" part. By Theorem 1, there exists a law-invariant family of monotone functionals such that

For , define , where for , and takes values . If , then the values will be arranged in the same order. Clearly, is a law-invariant family of monotone functions. Moreover, by the definition, for all . This implies the desired expression in Corollary 1. ∎

Proof of Proposition 4. By Theorem 1, a mapping defined by (1) with a law-invariant family of monotone functionals satisfies M, CA and N. Hence, in light of Theorem 4.94 in Follmer and Schied (2015), is coherent if and only if holds for all and . We first focus on the "if" part. We could find such that , , and hold almost surely. One can easily check that and almost surely. We can choose a version of such that and . Hence, by (1) and Condition A, we have

This implies is a coherent risk measure.

We next focus on the "only if" part. As is coherent, we have holds for all and . It follows from (1) that

| (9) |

holds for all and . We choose a such that there exists that is independent of . For such that and , we set , , and . It follows that and almost surely for and and . By (9.2), we have . In light of the law-invariance of , this conclusion holds for all . ∎

9.3 Proof of results in Section 4

Proof of Theorem 2. (i) We first show the "if part". By (2), we have that M follows from the monotonicity of . For any strictly increasing and continuous function , we have

where with the convention that . Hence OR is satisfied. Moreover, the LI of is implied by the expression (2) and the law-invariance of .

We next show the "only if" part. In light of Corollary 1 of Chambers (2007), and by M and OR, we have

| (10) |

where is a capacity taking values from . By Proposition 8, we have satisfies CA. Hence it follows from Theorem 1 that there exists a law-invariant family of monotone functionals such that (1) holds. For any strictly increasing and continuous function with and , we have . Hence we have , implying or for all . Using (1), we have or . We let

By monotonicity of , we have for all . It follows from (1) that

where Note that , and if for some . Hence , and if for some , which implies is an increasing set. Next, we show can be chosen to be law-invariant. We fix such that there exists that is independent of . Let . For any , there exists such that . By LI of and the above conclusion, we have

Hence, can be chosen as .

(ii) The proof of "if" part is similar to that of case (i). Next, we only show the "only if" part. Let be the conditional probability measure for . Define by . In light of Corollary 1 of Chambers (2007), and by M and OR, we have (10) holds. We denote the set of all by and let

It follows from (10) that for any . Define such that for and otherwise . Note that is law-invariant. Hence for , if , then , which implies .

Next we show that if and only if . It is obvious that implies . For the converse direction, note that implies there exists such that and . Hence we have for all and with . Define two measures and on by and . Note that is a semiring and for . It follows from Theorem 11.3 of Billingsley (1995) that

holds for or . Hence in light of the fact for all , we have for all . This implies a.s.. Moreover, there exist and such that and is independent of . Then and , where is the quantile function of . Note that a.s., and both of them are indicator functions. We let and . Then we have , and . By LI, we have and . It follows from M and LI that Consequently, for . Note that is decreasing with respect to . It follows from (10) that

| (11) |

where Note that , and if for some . Hence , and if for some , which implies is an increasing set. Similarly as in (i), we can show that can be chosen to be law-invariant. ∎

Proof of Proposition 5. We first show the "if" part. If , then we have and

| (15) |

a.s. under . Direct computation gives if , and if . Hence, we have . Moreover, by the proof of Theorem 2, satisfies CM and CA. Hence, in light of the second statement of Proposition 8, we obtain LI of .

Next, we consider the "only if" part. For , using (2), we have and . Direct computation shows if and otherwise ; if and otherwise . Hence, the weak law-invariance of is implied by the fact that . ∎

9.4 Proof of results in Section 5.

Proof of Theorem 3. We first show the "if" part. First, we show (5) is well-defined. Let such that a.s. and a.s., which imply . As , we have . Consequently, , implying (5) is well-defined.

Next we show the properties of (5). Clearly, satisfies M, AD and N. For , we have and . Moreover, it follows from the law-invariance of that . Note that implies . Hence, , implying the law-invariance of . For , we have a.s.. It follows from the monotone convergence theorem that . Hence the IC is satisfied.

Next, we show the "only if" part. It follows from Proposition 3 that (1) holds with a law-invariant family of monotone and continuous from below functionals . By (1), we have for all . For any , there exists and such that and is independent of . By the law-invariance of , we have . For satisfying , define and . Then the additivity of implies , which is equivalent to . Hence, we have holds for all satisfying and . Moreover, by the additivity and monotonicity of , we have for and .

Define for all . The finite-additivity of is implied by the additivity of and infinite-additivity of is implied by the continuity from below of . Hence, is a probability measure. Note that for , if , then , which implies . The law-invariance of implies the law-invariance of . Let . Then one can easily check that . Letting , we have . It follows from the continuity from below for that . Moreover, the monotone convergence theorem implies . Consequently, we have for all .

9.5 Proof of results in 6

Proof of Lemma 1. In light of Lemma 3.3 of de Castro et al. (2024), we have

where is defined e.g., in Definition A.38 of Föllmer and Schied (2016). This implies

We next show the inverse inequality by following the same idea as in the proof of Lemma 3.3 of de Castro et al.(2024). If is a continuous function with respect to on with , then for , a.s.. Hence, a.s.. Let . It follows that a.s. for all . Hence, implying . By definition, a.s.. Moreover, direct computation shows

Hence, we have a.s.. Using the above conclusion, we obtain

Hence,

Without loss of generality, we suppose in the following proof. For , there exists a sequence of discrete random variables such that and . Let be independent of . It follows that a.s.. One can easily check that is continuous over on some with . Using the above conclusion, there exists such that

Consequently,

Letting , we obtain

which is the desired inverse inequality.

Note that

Hence, using the above conclusion, we have

∎

Proof of Theorem 4. It follows from Corollary 4.38 of Föllmer and Schied (2016) that is coherent and continuous from above if and only if

for some . Next, we only need to show that is additionally law-invariant if and only if (6) holds. The "if" part is obvious. In light of (6) and the law-invariance of , implies . Hence, is law-invariant. We next show the "only if" part. Using the law-invariance of , we have

By Lemma 1, we have

Suppose such that . Then for , there exists such that . Hence,

if . Hence, can be chosen to be law-invariant. ∎

9.6 Proof of results in Section 7

Proof of Proposition 7. Fix such that and are comonotonic. Let for . Clearly, is an increasing function with and . Since is continuous from below, then is left-continuous. For , there exist increasing and Lipschitz continuous functions such that and . Direct computation gives for all . Hence, we have

The above inequality becomes equality if when , and . We establish the claim. ∎

9.7 A counterexample

Example 7.

Let be the probability space, where is the set of all Borel subsets of and is the Lebesgue measure. Moreover, let and . Let . For , define for all , where . Moreover, let with . One can easily check that for , is monotone. For , there exists such that and a.s.. Hence, if or . Now we consider the case and . If , then , implying . Suppose and . Then , which implies there exists such that over with . It follows that for all and . Using the fact that for , we have for all and . Choosing , we have . Thus we have . However, for , , leading to a contradiction. Hence, if , then , implying . Consequently, we conclude that is weakly law-invariant. Note that if and . Hence, is not law-invariant.