The CATT SATT on the MATT: semiparametric inference for sample treatment effects on the treated

Abstract

We study variants of the average treatment effect on the treated with population parameters replaced by their sample counterparts. For each estimand, we derive the limiting distribution with respect to a semiparametric efficient estimator of the population effect and provide guidance on variance estimation. Included in our analysis is the well-known sample average treatment effect on the treated, for which we obtain some unexpected results. Unlike the ordinary sample average treatment effect, we find that the asymptotic variance for the sample average treatment effect on the treated is point-identified and consistently estimable, but it potentially exceeds that of the population estimand. To address this shortcoming, we propose a modification that yields a new estimand—the mixed average treatment effect on the treated—which is always estimated more precisely than both the population and sample effects. We also introduce a second new estimand that arises from an alternative interpretation of the treatment effect on the treated with which all individuals are weighted by the propensity score.

1 Introduction

In observational studies with no unmeasured confounding, causal effects are identified as structured combinations of marginal and conditional population parameters. If some—or even all—of these distributional components were replaced by their sample counterparts, we might expect the modified estimand to be inferable with greater precision, having stripped away layers of uncertainty in the population distribution (Imbens, 2024). This increase in precision could be pivotal in settings with low statistical power, e.g., treatment effects that are small relative to the standard deviation of the outcomes (Athey et al., 2023).

For the average treatment effect, a complete characterization of such sample variants was provided by Imbens (2004). Any asymptotically efficient estimator of the population estimand is also consistent and asymptotically normal for the sample average treatment effect but always with a smaller or equal asymptotic variance. This asymptotic variance is not point-identified, however, because it depends on the covariance between the two potential outcomes, requiring the use of a conservative variance estimator. An intermediate estimand—introduced by Abadie and Imbens (2002)—averages the conditional treatment effect over the observed covariates rather than the population marginal covariate distribution. It is estimated with a precision bounded above and below by those of the sample and population estimands respectively.

Our contribution is to develop a similar characterization for the average treatment effect on the treated. It transpires that this theory is much richer for two reasons. First, the problem is asymmetric in the two treatment arms, which has surprising consequences for the commonly used sample average treatment effect on the treated (Robins, 1988; Imbens, 2004; Hartman et al., 2015; Dorie et al., 2019). Despite involving both potential outcomes together, we show that its asymptotic variance is point-identified and consistently estimable. To the best of our knowledge, this provides the first asymptotically exact confidence interval procedure for the sample average treatment effect on the treated in observational studies, complementing a related finding by Sekhon and Shem-Tov (2021) for randomized clinical trials. Yet we also find that the asymptotic variance can exceed that of the population effect, rendering it arguably unsuitable as a sample variant. We introduce an attractive alternative estimand—the mixed average treatment effect on the treated—that avoids this problem.

Second, the average treatment effect on the treated has a dual interpretation. The literal intepretation restricts attention to the individuals on treatment (e.g. Abadie and Imbens, 2002; Imbens, 2004), whereas estimands arising from the figurative interpretation incorporate the entire population or sample, weighted by the propensity score. The asymptotic variances for these figurative estimands account for the variability in the treatment assignment, thus protecting against the possibility of an unrepresentative treated subsample. Included in this subfamily is another new estimand—the sample weighted average treatment effect on the treated—that shares structural similarities with the sample average treatment effect.

2 Set-up and point estimation

Suppose that the variables are independent and identically distributed replicates of drawn from an unknown distribution . The real-valued or binary potential outcomes and correspond to treatment and control respectively, and is a binary variable that indicates the realized treatment assignment. We work in an observational setting: is a vector of covariates deemed sufficiently rich to adjust for confounding, and we require the propensity score to be bounded away from 0 and 1.

Assumption 1.

(i) (Strong ignorability) Suppose . (ii) (Positivity) There exists a number such that with -probability 1.

The data observed by the statistician are , where . Under Assumption 1, the population average treatment effect on the treated is identified by , where . It should be understood that Assumption 1 holds for the remainder of the paper without further statement.

We introduce some convenient notation. For any measurable function , let . In particular, , where is the empirical measure. Furthermore, let denote the Hilbert space of all real-valued measurable functions with equipped with the inner product and norm .

The analysis in this paper is based on an asymptotically efficient estimator of . For concreteness, we state the construction of an estimator using an estimating equation approach similar to Kennedy et al. (2015) and provide sufficient conditions on the estimation of the nuisance parameters. The efficient influence function for with unknown (Hahn, 1998) is

Our estimator

| (1) |

is defined by solving the empirical average of after replacing and with user-specified estimators and .

Assumption 2.

(i) Both and are square-integrable (ii) the sequences of estimators and each take values in fixed -Donsker classes (iii) (iv) there exist fixed positive constants such that and with -probability 1.

Remark 1.

The Donsker condition in Assumption 2(ii)—like the subsequent empirical process conditions in the paper—can be dropped if the construction of is modified with sample-splitting and cross-fitting (e.g. Chernozhukov et al., 2018; Hines et al., 2022). Assumption 2(iii) is a rate double robustness condition (Rotnitzky et al., 2021) that requires the combined convergence rate of to exceed .

Proposition 1.

We deduce that converges weakly to the normal distribution . The variance of can be estimated by , where is the sample variance of after replacing with .

Proposition 2.

Under Assumption 2, converges to in -probability.

Remark 2.

In the subsequent sections, we will apply to estimate different estimands. In each case, we obtain a weak convergence result of the form ; we abuse terminology slightly by saying that the estimand has asymptotic variance . The following definition gives us a concise way of comparing precisions.

Definition 1.

For two estimands and with respective asymptotic variances and , we say that is less conservative than if for all distributions . We denote this by ; it is clear that the relation is reflexive and transitive.

Our theory is underpinned by orthogonal decompositions of efficient influence functions. We can write , where

Each component is the least favourable submodel score (e.g. Chapter 8 of van der Laan and Rose, 2011) corresponding to different factors of the observed data distribution: , the conditional distribution of given ; , the conditional distribution of given ; and , the marginal distribution of . By mutual orthogonality, the variance of decomposes into . We can interpret each variance component as the uncertainty in induced by the corresponding factor of .

3 Estimands and inference

3.1 The literal and figurative interpretations

A complexity in defining sample variants of arises from its dual interpretation. From the literal perspective, we restrict our attention to the subpopulation currently on treatment; that is, quantifies the average effect of withholding treatment on the treated. This suggests defining a subfamily of literal estimands that take the form of a simple average across the treated in the sample, such as the sample average treatment effect on the treated

The alternative interpretation follows from writing as

| (2) |

indicating that is also the -weighted average of the treatment effects across the whole population, putting more weight on individuals with a higher propensity of receiving treatment, and vice-versa. We call this the figurative interpretation of the treatment effect on the treated, and figurative estimands are accordingly defined as propensity-score-weighted averages across the sample.

When we average across the infinite superpopulation, the causal effect defined by both interpretations coincide. Restricting to the sample, however, we obtain estimands with significantly different inferential properties. In the next subsections, we will study the limiting distributions of the estimator defined in (1) for estimands in both subfamilies. Literal estimands condition on the sampling variability from the treatment assignment mechanism, so we do not need to account for the uncertainty in the unknown propensity score. Consequently, their asymptotic variances do not include the corresponding variance component . This might be the appropriate option if, for example, we deem the treated in the sample to be typical of what we expect to see in the population. Figurative estimands are more conservative in this respect because they account for the variability in the treatment assignment, which provides protection against the risk of unrepresentative treated subsamples. We will also see that the two subfamilies behave differently when we consider estimands that involve the potential outcomes.

3.2 Figurative estimands

Our first figurative estimand is the average covariate-conditional treatment effect on the treated (Yiu et al., 2023)

| (3) |

which is defined by replacing the marginal distribution of in the middle expression of (2) with its empirical counterpart . Since this estimand conditions on the observed covariates, we would expect to have by removing the component from the asymptotic variance. This is confirmed by comparing Proposition 3 below with Proposition 1.

In contrast to the population effect, variance estimation for requires estimating . Fortunately, the assumptions on the estimator are relatively mild; a Glivenko-Cantelli condition, rather than a Donsker condition, is sufficient, and a rate of -convergence is unnecessary.

Assumption 3.

(i) The sequence of estimators takes values in a fixed -Glivenko-Cantelli class (ii) (iii) there exists a fixed positive constant such that with -probability 1.

Proposition 3.

The next estimand is based on the last expression in (2). Starting from the previous estimand , the conditional expectations are replaced by the potential outcomes .

Definition 2.

The sample weighted average treatment effect on the treated is defined as

Theorem 1.

Inspecting the asymptotic variance in Theorem 1, we see that is even less conservative than , so we have . The difference is zero if and only if with -probability 1. Unfortunately, the conditional variance of is not point-identified because we only observe one potential outcome per individual. If Assumption 3 holds, then provides a simple asymptotically conservative variance estimator. This is analogous to the approach advocated by Imbens (2004) for the sample average treatment effect. However, a sharper estimator is available if we are willing to undertake conditional variance estimation.

For each , let . These conditional variances are identified by

An application of the Cauchy-Schwarz inequality yields , from which we deduce the lower bound . To estimate the lower bound, we require estimators that satisfy the following conditions.

Assumption 4.

For each , suppose: (i) the sequence of estimators takes values in a fixed uniformly bounded -Glivenko-Cantelli class; (ii) .

Consequently, we can use as an asymptotically conservative variance estimator for . This is asymptotically sharper than just using unless with -probability 1. The sharpest possible bound follows from applying the Fréchet-Hoeffding upper bound to the conditional covariance. Estimating this is more involved, however, because it generally involves quantile regression for the potential outcome distributions. An exception is the case of binary outcomes, for which the sharpest bound takes a simple form and can be consistently estimated under Assumptions 2 and 3. Details are provided in the Appendix.

Providing an intuitive explanation for why is less conservative than appears to be difficult. It is perhaps tempting to state that is conditioning on more of the variability in the data by substituting the potential outcomes for their conditional expectations . But this is fallacious because we never observe both potential outcomes together; this point is demonstrated by the results in the next subsection.

3.3 Literal estimands

The conditional average treatment effect on the treated

was introduced by Abadie and Imbens (2002). It can be obtained by replacing the population joint distribution of in with the empirical joint distribution . If we compare this to the covariate-conditional effect in (3), which only replaces the marginal distribution of , we would expect to be less conservative, given that we have further removed the uncertainty regarding the conditional distribution of given . This is confirmed by the following result.

Proposition 5.

Recall that the population effect is identified by , where . The remaining two estimands replace with the sample average , which is completely determined by the observed data. Thus, our analysis now revolves around the functional ; its efficient influence function has the orthogonal decomposition

We return to the sample treatment effect on the treated discussed earlier. Perhaps surprisingly, despite involving both potential outcomes together, the asymptotic variance of is point-identified and can be consistently estimated.

Theorem 2.

Suppose Assumption 2 holds. Then

in weak convergence and

is a consistent estimator of the asymptotic variance.

Remarkably, it can be deduced from Theorem 2 that the asymptotic variance of potentially exceeds that of the population effect , as illustrated by the following example.

Example 1.

Suppose the treatment effect is homogeneous; that is, is constant. Then , and it follows that . It is straightforward to show that the asymptotic variance of is , which is strictly less than the asymptotic variance of if and only if .

Remark 3.

A similar argument yields as a general sufficient condition for the asymptotic variance of to be upper-bounded by that of .

The above phenomenon highlights that the inference for requires accounting for a source of uncertainty that is absent when inferring , namely, the variance of that is unexplained by when . Besides the undesirable possibility of obtaining a wider confidence interval for the sample effect, this is problematic if we wish to interpret as a distillation of the information contained in the observed data about ; see Imbens (2004) for a related discussion. To resolve this issue, we introduce a new estimand that replaces the awkward term in with .

Definition 3.

The mixed average treatment effect on the treated is defined as

Proposition 6.

Suppose Assumption 2 holds, and let be the sample variance of after replacing with . Then in weak convergence, and converges to in -probability. Moreover, we have , so .

Combined with our earlier results in Propositions 3 and 5, we deduce that is less conservative than both and . This makes an attractive alternative to that retains a similar literal interpretation. An advantage over and the figurative estimands is that estimation of is not required.

figurative estimands; literal estimands; means that .

| Estimand | Asymptotic variance |

|---|---|

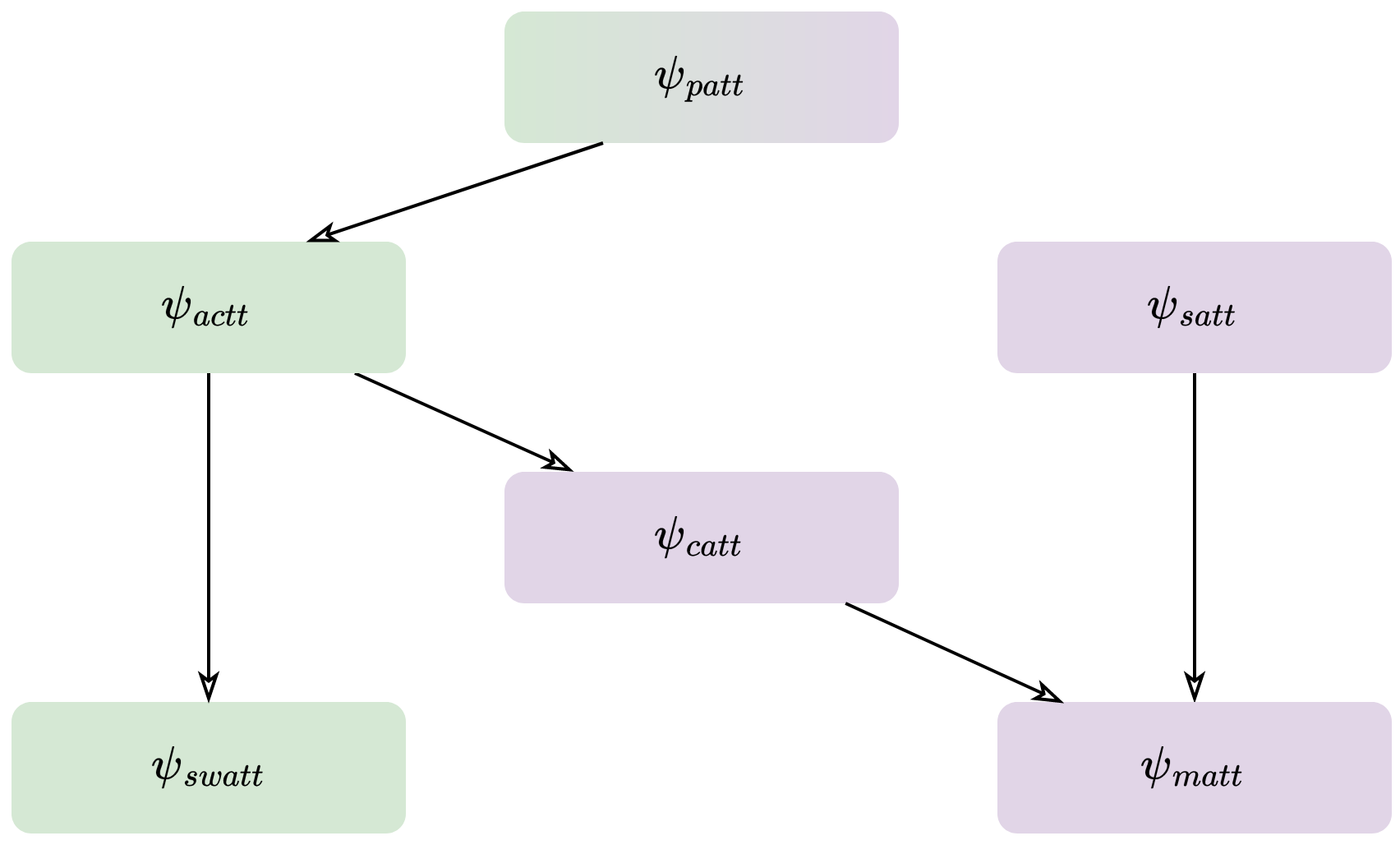

Figure 1 and Table 1 summarize our results, describing the partial ordering on our estimands defined by the relation . As discussed in Section 3.1, is the unique estimand that enjoys both the literal and figurative interpretations. There exist further estimands that belong in neither class, but we have deemed them to be less practically relevant. Details can be found in the Appendix, which also includes examples to justify why the diagram contains no directed paths between and any of . We emphasize again that our results are relative to an asymptotically efficient estimator for . For future work, it would be of interest to either verify that is efficient for the sample variants, or to show that there exist more efficient estimators.

Acknowledgements

The author receives funding from Novo Nordisk and thanks Edwin Fong for helpful suggestions that improved the paper.

References

- Abadie and Imbens [2002] A. Abadie and G. Imbens. Simple and bias-corrected matching estimators for average treatment effects. Technical Report T0283, NBER, 2002.

- Athey et al. [2023] S. Athey, P. Bickel, A. Chen, G. Imbens, and M. Pollmann. Semi-parametric estimation of treatment effects in randomised experiments. Journal of the Royal Statistical Society, Series B, 85:1615–1638, 2023.

- Chernozhukov et al. [2018] V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey, and J. Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21:C1–C68, 2018.

- Dorie et al. [2019] V. Dorie, J. Hill, U. Shalit, M. Scott, and D. Cervone. Automated versus do-it-yourself methods for causal inference: lessons learned from a data analysis competition. Statistical Science, 34:43–68, 2019.

- Hahn [1998] J. Hahn. On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, 66:315–331, 1998.

- Hartman et al. [2015] E. Hartman, R. Grieve, R. Ramsahai, and J. Sekhon. From sample average treatment effect to population average treatment effect on the treated: combining experimental with observational studies to estimate population treatment effects. Journal of the Royal Statistical Society, Series C, 178:757–778, 2015.

- Hines et al. [2022] O. Hines, O. Dukes, K. Diaz-Ordaz, and S. Vansteelandt. Demystifying statistical learning based on efficient influence functions. The American Statistician, 76:292–304, 2022.

- Hirano et al. [2003] K. Hirano, G. Imbens, and G. Ridder. Efficient estimation of average treatment effects using the estimated propensity score. Econometrica, 71:1161–1189, 2003.

- Imbens [2004] G. Imbens. Nonparametric estimation of average treatment effects under exogeneity: a review. Review of Economics and Statistics, 86:4–29, 2004.

- Imbens [2024] G. Imbens. Causal inference in the social sciences. Annual Review of Statistics and Its Application, 11:18.1–18.30, 2024.

- Kennedy et al. [2015] E. Kennedy, A. Sjölander, and D. Small. Semiparametric causal inference in matched cohort studies. Biometrika, 102:739–746, 2015.

- Robins [1988] J. Robins. Confidence intervals for causal parameters. Statistics in Medicine, 7:773–785, 1988.

- Rotnitzky et al. [2021] A. Rotnitzky, E. Smucler, and J. Robins. Characterization of parameters with a mixed bias property. Biometrika, 108:231–238, 2021.

- Sekhon and Shem-Tov [2021] J. Sekhon and Y. Shem-Tov. Inference on a new class of sample average treatment effects. Journal of the American Statistical Association, 116(534):798–804, 2021.

- van der Laan and Rose [2011] M. van der Laan and S. Rose. Targeted Learning. Springer-Verlag, New York, 2011.

- van der Vaart [1998] A. van der Vaart. Asymptotic Statistics. Cambridge University Press, Cambridge, 1998.

- van der Vaart and Wellner [2023] A. van der Vaart and J. Wellner. Weak Convergence and Empirical Processes (2nd edition). Springer, New York, 2023.

- Yiu et al. [2023] A. Yiu, E. Fong, C. Holmes, and J. Rousseau. Semiparametric posterior corrections. arXiv, page 2306.06059, 2023.

Appendix A Proofs of results in the main text

A.1 Proof of Proposition 1

By assumption, there exist fixed constants such that

with -probability 1. Without loss of generality, we can redefine as so that it can be used to bound both and for the sake of convenience.

We start by showing that , i.e. the semiparametric efficiency bound for is finite:

where the boundedness on the final line follows from the assumed square-integrability of and .

We will use to denote the empirical process. It is helpful to define

Then by the definition of , we have

Consider the decomposition

where we have used the fact that . We will show that terms and are both .

For term ,

so

which is by the assumptions of -convergence of and . Using Assumption 2 and repeated applications of Lemma 4, the sequence takes values in a fixed -Donsker class. Then we can apply Lemma 19.24 of van der Vaart [1998] to obtain as required.

For term , we have

where the inequality on the penultimate line is due to Cauchy-Schwarz and the assumed bounding on .

Thus, we have shown that

Since , we also have , and the central limit theorem yields . So Lemma 1 implies that

A.2 Proof of Proposition 2

Let

which differs from in the proof of Proposition 1 only in replacing with . Since takes values in a fixed bounded set, we deduce from Lemma 4 and the proof of Proposition 1 that also takes values in a fixed -Donsker class, which is, moreover, a -Glivenko-Cantelli class. Furthermore, Lemma 3 implies that takes values in a -Glivenko-Cantelli class. Thus,

We will show that , which suffices to establish by Lemma 2. As mentioned above, we have . Hence, Minkowski’s inequality yields

The first term on the right-hand side of the inequality was already shown to be in the proof of Proposition 1. And the second term is upper-bounded by , which is by Proposition 1. A similar argument yields .

A.3 Proof of Proposition 3

Using Proposition 1, we can start with , so

Thus, it suffices to show that since the remaining term converges weakly to the desired normal distribution. Some simple manipulations yield

Since , the central limit theorem implies that is . By the weak law of large numbers,

in -probability. Combining these with Slutsky’s lemma and using the figurative representation of , we deduce that the term in curly brackets is . Using Slutsky’s lemma again, we have that converges weakly to zero. Since zero is a constant, we also have convergence in -probability.

Now we proceed to variance estimation. Define

It is clear that the above expressions sum to as defined in the proof of Proposition 2. The functions , and are defined similarly, replacing the estimators of the parameters with their true values. Assumptions 2 and 3, along with repeated applications of Lemma 3, imply that each of takes values in a fixed -Glivenko-Cantelli class. This is also the case for and by Lemma 3 again. Thus,

We wish to establish . But we have already established that in the proof of Proposition 2, so by Minkowski’s inequality, it is sufficient to show that , which is comparatively simple. We have

For the first term in the upper-bound,

For the second term, first consider

with -probability 1 by Assumptions 2 and 3. Hence,

Now, Lemma 2 implies that and . Finally, we have

A.4 Proof of Theorem 1

Using Proposition 1, we can start with . Then we have

Consider the numerator in the second term on the right. First, the expectation with respect to is

The first equality is due to the tower property with conditioning on . The second equality uses the tower property in reverse combined with the ignorability in Assumption 1. Next, the variance is also finite:

by the assumed square-integrability of and . So the central limit theorem implies that and we deduce from Lemma 1 that

Putting everything together yields

Let . Write

so

The second term on the right, expressed by the inner product, is equal to zero by applying the tower property conditioning on and the fact that by strong ignorability. A similar argument yields . We deduce that

and by applying the tower property conditioning on .

A.5 Proof of Proposition 4

A.6 Proof of Proposition 5

Using Proposition 1, we can start with , so

Thus, it suffices to show that since the remaining term converges weakly to the desired normal distribution. We can write

Since has mean zero and finite variance, the central limit theorem implies that . Then we apply Lemma 1 to deduce the result.

For the variance estimation, we use the same notation as the proof of Proposition 3. Arguing similarly to the proof of Proposition 3, we want to establish

and it is sufficient to show that . Then

Putting the ingredients together with Lemma 1 yields

A.7 Proof of Theorem 2

Using Proposition 1, we can start with , so

It is clear that because with -probability 1. Therefore, converges weakly to . Then we apply Lemma 1 and Slutsky’s lemma to obtain the required limiting normal distribution.

For the variance estimation, we begin by showing that we can consistently estimate . Consider

Thus,

By applying similar arguments to the proof of Proposition 2, we obtain

in -probability.

Next we show that is identified. By the tower property and ignorability, we have

Then

Now we want to prove that

We will do this by leveraging the earlier computations. Consider

Then we have

The first term on the right is by using the -convergence established earlier in the proof along with Lemma 2. The second term on the right is by the assumed convergence of and the Cauchy-Schwarz inequality. Moreover,

takes values in a fixed -Glivenko-Cantelli class by applying Lemma 3 and Assumption 3. Then by similar arguments to the proof of Proposition 2,

in -probability. Combining this with the earlier convergence result for completes the proof.

A.8 Proof of Proposition 6

We can relate to by

So we deduce from the proof of Theorem 2 that

Then the central limit theorem and Lemma 1 yield the required normal weak limit. The consistency of the variance estimator also follows from the proof of Theorem 2.

For the last statement of the proposition, write

The two terms on the right are orthogonal because -almost surely. Thus,

Appendix B Auxiliary lemmas

Lemma 1.

Suppose Assumption 3 holds. Then

Proof.

Lemma 2.

Suppose that is a sequence of random functions taking values in such that for some . Then

Proof.

For the first objective, we have

where the inequality on the penultimate line used the Minkowski and Cauchy-Schwarz inequalities. For the second objective, we have

by Cauchy-Schwarz again. ∎

The remaining lemmas are well-known empirical process results that we state here for convenient reference.

Lemma 3 (Theorem 2.10.5 of van der Vaart and Wellner [2023]).

Let be -Glivenko-Cantelli classes with integrable envelopes. If is continuous, then is -Glivenko-Cantelli provided that it has an integrable envelope function.

Lemma 4 (Examples 2.10.9, 2.10.10 and 2.10.11 of van der Vaart and Wellner [2023]).

Suppose and are -Donsker classes.

-

(i)

If , then the set of pairwise sums is a -Donsker class.

-

(ii)

If and are uniformly bounded, then the set of pairwise products is a -Donsker class.

-

(iii)

If and for some for every , then is a -Donsker class.

Appendix C The sharpest bound for the asymptotic variance of the sample weighted effect

Recall that the asymptotic variance of is equal to

as shown in Theorem 1. We mentioned that one could simply estimate , the asymptotic variance of , to use as a simple asymptotically conservative variance estimator. This has the benefit of not requiring any additional estimation of nuisance parameters. Alternatively, we showed using Cauchy-Schwarz that

which gives us a sharper bound on the asymptotic variance but requires conditional variance estimation to operationalize.

The sharpest possible bound on the asymptotic variance of is obtained through the Fréchet-Hoeffding upper bound. For each , let be the distribution function of given . These are identified by

Then the Fréchet-Hoeffding upper bound for the conditional covariance is

which is attained if and are comonotonic given ; that is, for . Consequently,

This suggests that we should estimate to obtain the sharpest possible asymptotic variance estimate for . However, this generally appears to require simultaneous quantile regression to obtain plug-in estimates and across all and all values of . We defer the development of this methodology to future work. An exception is the case of binary outcomes, where the sharpest bound takes a particularly simple form.

Proposition 7.

Proof.

The conditional covariance between and can be written as

The first term on the right is bounded above by

This upper bound can always be attained if the only restriction on the joint conditional distribution is the pair . Hence,

Plugging this into the expectation completes the proof of the first part.

Using similar arguments to the proofs of previous propositions, the assumptions imply that takes values in a fixed -Glivenko-Cantelli class, so

Moreover, the argument in the proof of Proposition 4 can be used to show

after replacing with . Using Lemma 2, we have

Combining the above yields the result. ∎

Consequently, we can use as the asymptotically sharp variance estimator for .

Appendix D Additional comparisons and estimands

D.1 Comparisons between the sample weighted effect and the literal estimands

In Figure 1 of the main text, it is indicated that there is no ordering between and any of . We justify this assertion with the following examples.

Example 2 (Asymptotic variance of asymptotic variance of ).

For arbitrary , set to be an arbitrary constant, so -almost surely. Also let have any distribution such that on a set of positive -probability and set . Then

and

Compare this with the asymptotic variance of :

A sufficient condition for the asymptotic variance of to be strictly smaller is:

with -probability 1. This is equivalent to with -probability 1.

Example 3 (Asymptotic variance of asymptotic variances of and ).

Suppose are such that , i.e. the CATE function is not -almost surely constant. Also let , so the asymptotic variance of is while the asymptotic variance of is just . Then

Thus, the asymptotic variance of is strictly smaller than that of .

If we further let and , then the asymptotic variance of is also just , and we deduce from the above that has strictly smaller asymptotic variance as well.

D.2 Additional estimands

Recall from the main text that the population effect can be written as

where . Sample variants could be created by replacing the first term by any of

and the second term by any of

This includes all of the sample variants studied in the main text; the remaining combinations appear to lack practical motivations or utilities.

We highlight two additional estimands that provide some interesting context. It is perhaps appealing to consider

since the problem now reduces to estimating . As expected, we have

using a similar analysis to before. But it is in fact possible for to exceed , as illustrated by the following example.

Example 4.

Set to be an arbitrary constant, so that with -probability 1. Then

So if and only if , e.g. if , then it is sufficient to have . Essentially, scenarios like the above can occur because may be less variable than on its own.

Finally, it is natural to investigate the sample variant that can be estimated most precisely. This can be deduced by looking directly at the form of . Define

Proposition 8.

Under Assumption 2, in weak convergence.