globalization_mechanism \BODY \NewEnvironglobalization_strategy \BODY \NewEnvironstep_computation \BODY

Binary Quantum Control Optimization with Uncertain Hamiltonians

Abstract

Optimizing the controls of quantum systems plays a crucial role in advancing quantum technologies. The time-varying noises in quantum systems and the widespread use of inhomogeneous quantum ensembles raise the need for high-quality quantum controls under uncertainties. In this paper, we consider a stochastic discrete optimization formulation of a binary optimal quantum control problem involving Hamiltonians with predictable uncertainties. We propose a sample-based reformulation that optimizes both risk-neutral and risk-averse measurements of control policies, and solve these with two gradient-based algorithms using sum-up-rounding approaches. Furthermore, we discuss the differentiability of the objective function and prove upper bounds of the gaps between the optimal solutions to binary control problems and their continuous relaxations. We conduct numerical studies on various sized problem instances based of two applications of quantum pulse optimization; we evaluate different strategies to mitigate the impact of uncertainties in quantum systems. We demonstrate that the controls of our stochastic optimization model achieve significantly higher quality and robustness compared to the controls of a deterministic model.

1 Introduction

Quantum control [1, 2, 3] focuses on designing efficient and accurate controls that manipulate quantum systems toward desired quantum states and operations. Applications of quantum control include nuclear magnetic resonance experiments [4, 5, 6, 7] and quantum chemistry [8, 9]. With the development of quantum technologies, quantum control plays an important role in quantum information [10, 11, 12, 13, 14, 15, 16] and the high-level design of quantum algorithms [17, 18, 19, 20, 21, 22, 23].

Various methods have been developed to solve quantum optimal control problems. Khaneja et al. [5] develop the gradient ascent pulse engineering (GRAPE) algorithm, which estimates controls by piecewise constant functions. Larocca and Wisniacki [24] improve the computational efficiency of the GRAPE algorithm using a Krylov subspace approach. Another popular method is the chopped random basis algorithm, which describes the control space using basis functions [25, 26, 27]. Other studies solve these optimal control problems using gradient-free methods, including evolution algorithms [28] and reinforcement learning approaches [29, 30, 31, 32, 33]. For binary control problems, Vogt and Petersson [34] propose a trust-region method for the optimal control of a single-flux quantum system. Fei et al. [19] develop a solution framework for general quantum systems and further improve it using a switching time approach [20].

The aforementioned papers study only deterministic quantum optimal control problems, which have fixed Hamiltonians, Hermitian operators that generate the time evolution of the system and whose eigenvalues correspond to energy levels of the system. These Hamiltonians are specified by the experimental setup with the control coming from how long we use each Hamiltonian and in what order for time evolving the state of the system. However, the imprecise estimation of the Hamiltonian controllers and time-varying noises in quantum systems has recently raised the need for robust quantum control [35, 36, 37, 38, 39]. Moreover, designing a robust uniform control is an important topic in inhomogeneous quantum ensembles, involving a large number of quantum systems with variations in system parameters [40, 41, 42, 43, 44]. Fourier decomposition methods can be applied to design a uniform control for inhomogeneous quantum fields [41, 42]. Barr et al. [45] extend quantum noise spectroscopy to design optimized amplitude control waveforms that suppress low-frequency dephasing noise and detuning errors. Ruths and Li [46] propose a multidimensional pseudospectral method with uncertainty sampling for optimal control of quantum ensembles. Chen et al. [40] apply a sample approximation algorithm, and Wu et al. [47] extend it to a batch-based sampling algorithm that minimizes the expected error between final and target operations. To hedge against risk, other studies focus on optimizing the worst-case performance under uncertainties. Wesenberg [48] solves a robust quantum optimal control problem using a general minmax algorithm based on a series of constrained quasi-Newton sequential quadratic programs. Kosut et al. [49] develop a sample-based sequential convex programming scheme to obtain an optimal control for the worst-case robust optimization problem.

Here we seek to make three major contributions to the literature. First, we develop a stochastic optimization model and a sample-based reformulation for the general quantum optimal control problem under uncertain Hamiltonians; this model balances risk-neutral and risk-averse objectives. Second, we apply multiple gradient-based methods and rounding techniques to solve the reformulated mixed-integer stochastic programming model. We provide the derivative of the objective function as well as derive bounds for the gap between solutions before and after rounding. Third, we analyze the performance of our approaches under various variance settings and demonstrate the benefits of considering uncertainties when conducting binary controls of various quantum systems.

The manuscript is organized as follows. Section 2 presents a general mixed-integer stochastic optimization model and its reformulation based on finite samples of the uncertain Hamiltonians. In Section 3 we derive the reformulation of the original stochastic optimization model and propose our gradient-based algorithm to solve the continuous relaxation. We apply rounding techniques to obtain binary controls and analyze the gap between binary and continuous control solutions. Section 4 introduces two specific quantum control instances and discusses the results of our numerical tests and simulation. Section 5 summarizes our study and states future research directions.

2 Modeling Uncertain Hamiltonians

For completeness, Section 2.1 first introduces the model for deterministic binary quantum optimal control presented in Fei et al. [20]. In Section 2.2, we extend this model to a general stochastic optimization model and we propose a sample-based reformulation. Section 2.3 describes how the objective function can be modified to account for various risk measures.

2.1 Deterministic Optimal Control Model

Consider a quantum system with qubits, and let the control process be conducted on the time interval , where is defined as the evolution time. Let be the intrinsic Hamiltonian, a Hamiltonian over which we do not have control and which is always applied in the time evolution of the system. Let be the number of control Hamiltonians given by . Let be the initial and target unitary operators of the quantum system, respectively. We define as the number of time steps and divide the time horizon into time intervals . (In this work we use a uniform time discretization where each time interval has an equal length , but our work can be extended to discretization with nonuniform time interval length.) For each controller and each time step , we define discretized control variables as . For each time step , we define the discretized time-dependent Hamiltonians as and unitary operators as .

We define the general deterministic binary quantum control model as follows.

| (1a) | ||||

| (1b) | ||||

| (1c) | ||||

| (1d) | ||||

| (1e) | ||||

| (1f) | ||||

The objective function is a general function to measure the difference between the final and desired quantum systems and can take different forms depending on specific problem instances. (In the numerical simulations of this manuscript, we employ two widely used objective functions in the quantum control field, but our methods described later are general and can be used for general differentiable functions .)

In quantum mechanics, the quantum state is defined as the description of the physical properties of a quantum system. We use and to represent a quantum state vector and its conjugate transpose, respectively. This notation is standard Dirac notation in quantum mechanics; and the state of a quantum system, , can be represented numerically as a dimensional, complex vector, normalized to one. We also use as a modifier to denote the conjugate transpose of a complex matrix. We define a parameter as the constant Hamiltonian that determines the energy structure of the quantum system.

One function we will use later evaluates the difference between the energy of the quantum system with final operator and the minimum energy corresponding to , given by

| (2) |

where represents the initial state of the quantum system and the constant minimum energy represents the minimum eigenvalue of , with an assumption that .

Another function we consider is the infidelity function

| (3) |

which measures the difference between and the target operator . Both objective functions (2) and (3) are bounded between .

Constraints (1b) compute time-dependent Hamiltonians for as linear combinations of the intrinsic Hamiltonian and the control Hamiltonians weighted by control variables . The constraints, (1c), describe the time evolution process for computing unitary operators, , by solving the Schrödinger equation. Constraint (1d) is the initial condition of the unitary operators. Constraint (1e) ensures that at each time step, the summation of all the control values should be one, which is Special Ordered Set of Type 1 (SOS1) property in optimal control theory [50]. Combining the SOS1 property with binary constraints for control variables (1f), we ensure that only one controller is active at any time.

2.2 Stochastic Optimal Control Model

In practice, the intrinsic and control Hamiltonians are affected by time-dependent noise due to various reasons such as decoherence, hardware limitations, and environmental noise [51, 52, 53]. On the other hand, multiple applications, such as inhomogeneous quantum ensembles, require applying a uniform control to manipulate quantum systems with different Hamiltonian values. These properties and applications lead to quantum control studies that take the uncertainty of Hamiltonians into consideration. In this manuscript we assume that the uncertainty parameters have a known distribution, and we define a measure space , where is the sample space and represents the probability distribution function. We denote the uncertainty parameters as , where represents the uncertainty of the intrinsic Hamiltonian () and th control Hamiltonian () in the time interval . We use finite samples to approximate the distribution, and we define the set as a finite set of uncertainty realizations, , according to the distribution such that , for each , is associated with probability with . The time-dependent Hamiltonians and unitary operators are the functions of uncertain parameters . For each sample , at each time step , we denote the corresponding time-dependent Hamiltonian and unitary operator as and , respectively. We define as a risk measure function based on the uncertainty sample set . The generic stochastic optimization model variant of Model (1) is given by

| (4a) | ||||

| s.t. | (4b) | |||

| (4c) | ||||

| (4d) | ||||

| (4e) | ||||

The objective (4a) uses the risk measure to evaluate the risk of having deviations from the desired cost of controlling quantum operators under uncertainty, which we detail in Section 2.3. (In Section 4 for the numerical results, we introduce specific quantum control objective functions for different examples.) Constraints (4b) compute the time-dependent Hamiltonians given samples . Constraints (4c)–(4d) are the copies of constraints (1c)–(1d) for scenarios .

2.3 Risk Measures and Objective Functions

The risk measure in (4a) in the stochastic optimization model can take different forms depending on the decision-maker’s risk attitudes and uncertainty levels. One of the most widely used measures is the expectation of a random variable, which measures the average performance, also known as the risk-neutral measure [54]. For any stochastic function on the measure space , the expectation is defined as . With a sample set , the approximation expectation formulation for the stochastic function is .

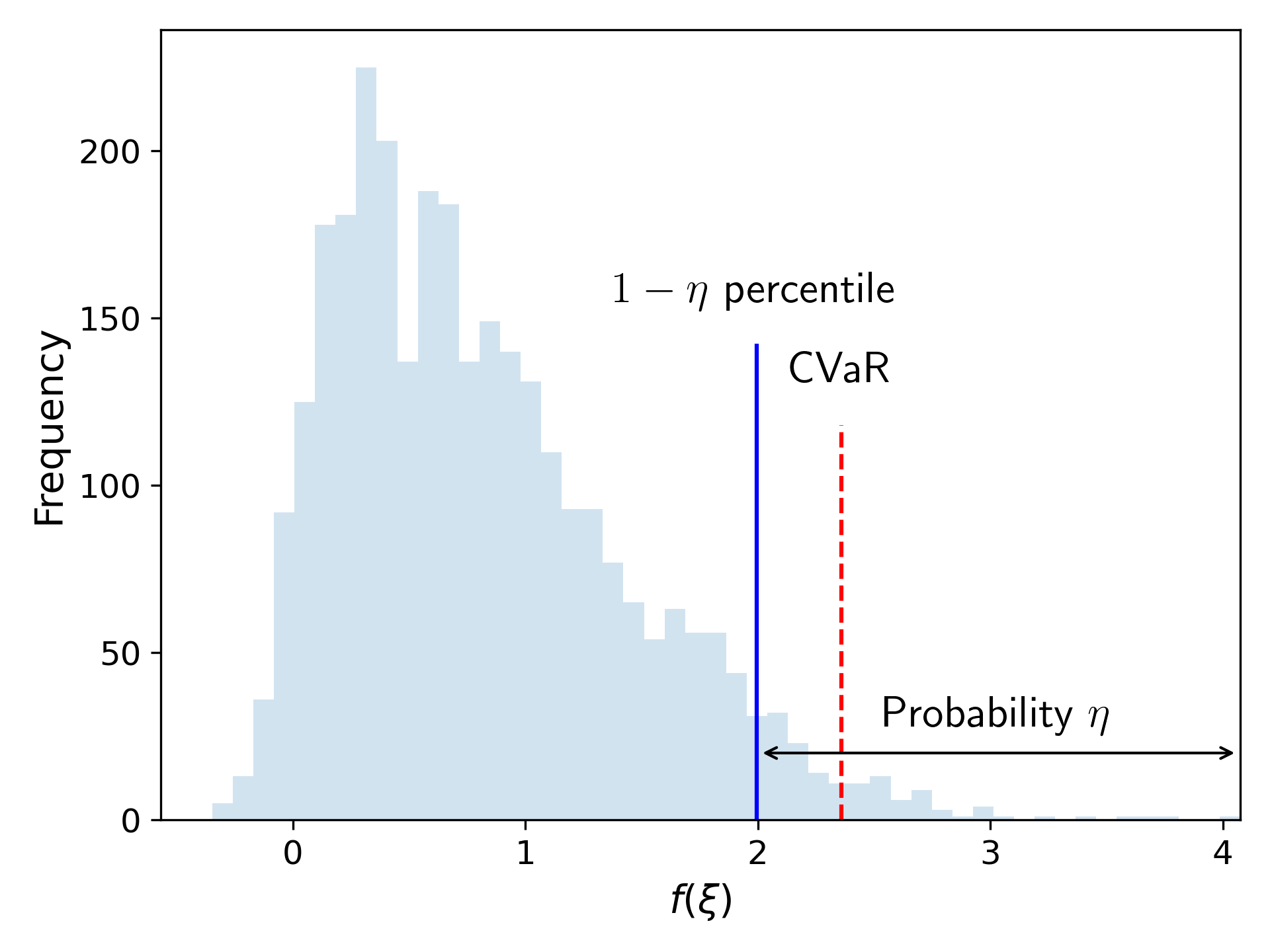

However, a particular realization of can be significantly different from its expectation. In some quantum control applications, avoiding extremely poor performance of the given systems is important and necessary. Here we consider a risk-averse measure, to control the risk in the solutions given by the stochastic optimization model 4 [55, 56, 57, 58]. We consider the Conditional Value-at-Risk (CVaR) [56] because it is a coherent risk measure with nice properties such as convexity. For any stochastic function , the CVaR with risk level is defined as the expected value of subject to the constraint that the value of is no less than the lower percentile [55]. Figure 1 illustrates CVaR for , where the blue line at 2 represents the 95th percentile of and the red dashed line represents the CVaR value as the average of all values of that are larger than 2.

We also introduce the equivalent formulation for the CVaR function [56]:

| (5) |

The CVaR of has the following sample-based approximation form:

| (6) |

One can consider a linear combination of expectation and CVaR function as the specific objective function in 4 to balance between risk-neutral and risk-averse attitudes. With a sample set , the risk measure (4a) can be formulated:

where is a weight parameter and is a risk level parameter. When , the problem is equivalent to minimizing the CVaR function to obtain a risk-averse control. When , the goal is to optimize the expected performance of the control.

3 Gradient-Based Algorithm

We now present our algorithm for solving the stochastic optimization model, which consists of two parts, first solving a continuous relaxation and then rounding the continuous solution. In Section 3.1 we first convert the stochastic optimization model with sample approximation 4 to an unconstrained optimization model. We then discuss the derivative for the objective function and introduce two gradient-based algorithms to solve the continuous relaxation of the model. In Section 3.2 we apply a sum-up rounding algorithm to obtain binary solutions with an optimality guarantee.

3.1 Solution Methods for Continuous Relaxation

To start, we follow constraints (4b)–(4d) and convert the final operator into an implicit function of control variables :

| (7) |

We use to denote the objective function of given uncertainty realization by substituting into the objective function (1a); that is, . We penalize the SOS1 property (1e) by a squared penalty function in the form of

| (8) |

By relaxing the binary constraints (1f), the stochastic optimization model 4 is converted to an unconstrained optimization problem over a bounded feasible region as

| (9) |

where is the penalty weight parameter for the SOS1 property. The function in the second term leads to the objective possibly being nondifferentiable with respect to the variables and ; we therefore discuss the closed-form expression and then the derivative of the objective function in the following theorems. For simplicity, we denote the second term without weight by :

| (10) |

We derive a closed-form expression of as follows.

Theorem 1.

For a given control variable , define as the scenario number with the largest original objective value such that

| (11) |

Then the closed-form expression of at point is given by

| (12) |

Proof.

To prove the closed-form expression, it is equivalent to prove that given any feasible control variable , is an optimal solution for the minimization problem . When , we have

| (13) |

The equalities directly follow from the definition of . The first inequality holds because of the definition of such that . The last inequality holds because all the terms in the summation have . Similarly, we can show that when , we have

| (14) |

The only difference is that for the last inequality it holds because all the terms in the summation have . ∎

Remark 1.

Remark 2.

For a special case where we sample the scenario with equal probability, that is, , an optimal solution is the largest original objective function value among all the scenarios .

Using the closed-form expression in (12), we convert the original problem to minimizing an unconstrained continuous relaxation with uncertainty sample set . For simplicity, in the remaining discussion we define the summation of terms coming from the original objective function as

| (15) |

where is defined in (12).

Taking the penalty function into consideration, the unconstrained continuous relaxation is

| (16) |

which is a relaxation of our original stochastic optimization model 4 with relaxed binary constraints and penalized SOS1 property (4e). The differentiability of the term depends on the objective values of all the scenarios. For a given control variable point , we present the following theorem about the derivative.

Theorem 2.

For any given control variable point , if , then the closed form is differentiable at point , with the derivative formulation as

| (17) |

Proof.

Because the functions and are differentiable for each scenario , the function is differentiable and thus continuous. Because the objective function is continuous, given a control variable point , for any , there exists a distance for each scenario such that for any , we have . Choosing , from the assumption that , , we have . Define . Then, for any such that , . We prove this claim by the following statements that

| (18) | |||

| (19) |

For both formulas, the first and last inequalities follow from the continuity of , and the other inequalities follow from the definition of . Now we show that is still the scenario number with the largest original objective value such that , which means that . Furthermore, we show that . Therefore, the derivative of at point is

| (20) |

∎

When the conditions in Theorem 2 hold, with the derivative of , we compute the derivative of the objective function in 16 by the chain rule as

| (21) |

where the gradient of the original objective functions for every scenario depends on specific quantum problems and can be computed by the popular GRAPE algorithm [5]. We apply two optimization methods, L-BFGS-B [60] and Adam [61], with our derived gradient for in (21) to solve the continuous relaxation of the stochastic optimization model. In numerical studies we empirically show that L-BFGS-B is better for quantum problems aiming to minimize the energy of a quantum state, while Adam performs better on problems minimizing the infidelity compared with a target quantum operator.

L-BFGS-B algorithm

L-BFGS-B is a widely used quasi-Newton method for optimizing unconstrained models with deterministic objective functions. We first generate samples for the uncertain parameters , then apply L-BFGS-B to solve 16. Specifically, during each iteration of L-BFGS-B, we compute the derivative using (21) and the search direction, then conduct a line search to update control variables, following the details in Byrd et al. [60], Zhu et al. [62].

Adam method

Adam is a popular first-order gradient-based optimization method for optimizing unconstrained models with stochastic objective functions [61]. We modify Adam to solve our problem with a bounded feasible region by adding a projection step. The details of the algorithm are presented in Algorithm 1 (where represents elementwise multiplication between two vectors). Specifically, during each iteration we first generate samples of the uncertain parameters to formulate the corresponding continuous relaxation 16 (see Algorithm 1). Then we compute the derivative by Equation 21 (see Algorithm 1), update the control variables, and project the updated variables to the feasible region (see Algorithms 1–1).

3.2 Sum-Up Rounding Technique

With continuous solutions , we apply the sum-up rounding (SUR) technique to obtain binary solutions . The SUR technique is proposed by the work of Sager et al. [50] and is widely used in integer control optimization problems. To the best of our knowledge, most work using SUR rounds either a continuous-time control function [63, 64] or controls of the continuous relaxation with the same time discretization [65, 66, 19, 20].

In our problem, the time of solving the continuous relaxation is the major part of the overall computational time and significantly increases when the number of time steps and scenarios is high. Therefore, we solve the continuous relaxation using fewer time steps and round the solutions using more time steps to achieve a balance between computational time and the difference between continuous and binary solutions. For simplicity, we assume here that , where is a predetermined integer constant. We present the rounding algorithm procedure in Algorithm 2.

Remark 3.

Algorithm 2 can be extended to a more general case when the SOS1 property is not required for controls by only changing Algorithms 2–2. We set where and other controller values as .

In the rest of this section we discuss how the difference between continuous and binary controls varies with time steps . In the remaining discussion we use to represent all the discretized controls and to represent all the control functions on a continuous time horizon (i.e., ). We first propose two assumptions for the original problem, which are satisfied in most quantum control problems.

Assumption 1.

We assume that the original objective function for each quantum system is continuous, non-negative, and upper-bounded.

Assumption 2.

We assume that the stochastic optimization model 4 is feasible.

We define piecewise constant control functions and as equivalent formulations to discretized controls and :

| (22a) | |||

| (22b) | |||

In the following theorem we discuss the cumulative difference between continuous and binary control functions:

Theorem 3.

With Assumptions 1–2, let be the upper bound of . Then the cumulative difference between continuous and binary controls at any time satisfies

| (23) |

where is defined in (8). Furthermore, we have the following convergence results for the objective values defined in (15) of continuous and binary solutions:

| (24) |

Proof.

For any time interval length , let be the index of the time step in the SUR algorithm that falls in. Then the integral can be written as follows based on the definition of piecewise constant functions:

| (25) |

The remaining proof of the upper bound in (23) directly follows the proof of Theorem 4 and Corollary 1 in Fei et al. [19] with details being omitted here. For any control value , we have

| (26) |

Hence, the original risk measure function defined in (15) is upper bounded by . Because is the optimal solution of penalized continuous relaxation, for a feasible solution of model 4 we have

| (27) |

where the last equality follows by the fact that is a feasible solution of the model with the SOS1 property, so . Therefore, we have , and the convergence of objective values directly follows Corollary 8 in Sager et al. [50]. ∎

Theorem 3 proves that and the cumulative difference is upper bounded by . In the following propositions we show that with additional assumptions the upper bound can be tightened. We first introduce the infinite-dimension formulation (i.e., ) for the original objective function of a single scenario :

| (28) |

Note that we use for the objective value of the discretized control and for the objective value of the continuous-time control.

The operator is the value of at time , and is the solution for the following differential equation with given control functions :

| (29) |

where are time-dependent uncertain parameters. We use the infinite-dimension objective function in (28) to replace in the stochastic objective function defined in (12) and (15). We define as the scenario number with the largest original objective value such that (see the discretized version in Theorem 1). For simplicity, we use to replace in the following formulation of the infinite-dimension stochastic objective function :

| (30) |

With the definition of infinite-dimension stochastic objective function in (15), we define the infinite-dimension formulation with the SOS1 property for the stochastic optimization model 4 as

| (31a) | ||||

| (31b) | ||||

| (31c) | ||||

The objective function (31a) is the stochastic objective function defined in (3.2). Constraint (31b) enforces that the control function holds the SOS1 property for . Constraint (31c) indicates that the control function value is binary for [67]. Every feasible solution of the discretized model 4 can be considered as a piecewise constant control function and thus is a feasible solution for the infinite-dimension formulation 31. For this model we impose the following assumption and derive an upper bound for the cumulative difference based on it.

Assumption 3.

We assume that there exists an optimal solution for the continuous relaxation of the infinite-dimension model with the SOS1 property 31, represented by such that the original objective value .

Proposition 1.

Recall that is the weight parameter of the SOS1 penalty function, with Assumptions 1–3. Then we have the following bound for the cumulative difference:

| (32) |

where is a constant determined by control Hamiltonians and evolution time .

Proof.

We only need to prove that there exists a constant such that . We define as the optimal solution for the continuous relaxation of the discretized model with the SOS1 property 4. From the optimality of we have

| (33) |

where the inequality follows the fact that holds the SOS1 property, so the penalty term . Combining with the Assumption 1 that , we have

| (34) |

We then consider the difference in objective values between the optimal infinite-dimension relaxation solution (defined in Assumption 3) and the optimal discretized relaxation solution . We first construct a piecewise constant control function satisfying the inequality as

| (35) |

It is obvious that during each time interval we have

| (36) |

For any time , let be the index of time interval that falls in. Then we have

| (37) |

In the time subinterval , the two integrals hold:

| (38a) | |||

| (38b) | |||

From the definition of in (35), we know that

| (39) |

Therefore, for any ,

| (40) |

We notice that the values of control functions and are both bounded by . Hence, the difference of integral is upper bounded by . From Theorem 2 in Sager and Zeile [64] we have

| (41) |

where is a constant determined by control Hamiltonians and evolution time. Combining with the continuity of the objective function , we have

| (42) |

where is a constant determined by objective function . From the definition of the piecewise constant control function , we can construct an equivalent discretized solution , where is the index of time interval that falls in. Because is the optimal solution of the discretized formulation, it holds that

| (43) |

With Assumption 3 that and the upper bound for in (34), we prove that

| (44) |

where . ∎

Furthermore, we prove in Proposition 2, with an additional Assumption 4 for the infinite dimension model 31 that the second term of the cumulative difference is upper bounded by , where .

Assumption 4.

We assume that there exists a constant time interval length such that for any time discretization with , the optimal solution for the continuous relaxation of infinite dimension model with the SOS1 property 31 is continuous in each time subinterval.

Proposition 2.

With Assumptions 1–4, for any we have the following bound for the cumulative difference:

| (45) |

where .

Proof.

We consider the upper bound for the cumulative difference between and in (3.2). Because we assume that the optimal solution is continuous in each subinterval in Assumption 4, the right-hand side is upper bounded by . The other parts of the proof are the same as the proof of Proposition 1. ∎

The upper bound in Proposition 2 indicates that the first term dominates the second term, and therefore increasing the multiplier factor for time steps in the SUR algorithm () significantly reduces the cumulative difference between binary and continuous controls if Assumptions 1–4 hold.

For a fixed number of time steps , the optimal value of the continuous relaxation () provides a lower bound for the binary model with the same time steps but not necessarily for the binary model with time steps . We provide a counterexample in the following remark.

Remark 4.

We provide an example showing that the objective value of the continuous relaxation optimal solution is larger than the objective value of the binary solution obtained by SUR with rounding time steps . We consider a quantum control problem with zero noises as follows. The objective function is defined as

| (46) |

where is

| (47) |

We set intrinsic and control Hamiltonians as

| (48) |

The initial operator is a 4-dimensional identity matrix. The evolution time . The number of time steps for continuous relaxation and the number of time steps for SUR . We consider only one scenario and uncertainty for all and . The time-dependent Hamiltonians are computed by (4b), and the time-dependent operators are computed by (4c). By solving the model, we show that .

4 Numerical Studies

We now apply the algorithms discussed in Section 3 to solve two quantum control problems with uncertain Hamiltonians: an energy minimization problem and a circuit compilation problem. In Section 4.1 we introduce our simulation setup for quantum systems with uncertain Hamiltonians. In Section 4.2 we introduce the settings of the energy minimization problem and present the numerical results. In Section 4.3 we introduce the circuit compilation problem and describe the numerical results. All numerical simulations were conducted on a macOS computer with 8 cores, 16 GB RAM, and a 3.20 GHz processor. The implementation was in Python with version 3.8. Our full code and results are available on our GitHub repository [68].

4.1 Uncertainty Design

Our proposed stochastic optimization model focues on quantum systems where the control Hamiltonians are inexact. In realistic experiments, the control uncertainty of Hamiltonians varies among each simulation and each time step and has different distribution parameters for different Hamiltonians. The variances of the uncertain parameters are larger across simulations and smaller within each time step during a single simulation. Specifically, we assume that for each controller and each time step , the uncertain parameter follows a normal distribution , where is a random variable following a normal distribution , with constant variance determined by the Hamiltonians.

For each scenario , we generate the corresponding samples as follows. We first sample a parameter from a normal distribution with mean value 0 and variance for each Hamiltonian , representing the mean value of uncertainties for Hamiltonian across all time steps for scenario , defined as an offset. We then sample for each Hamiltonian , for all and time step from a normal distribution with mean value and variance .

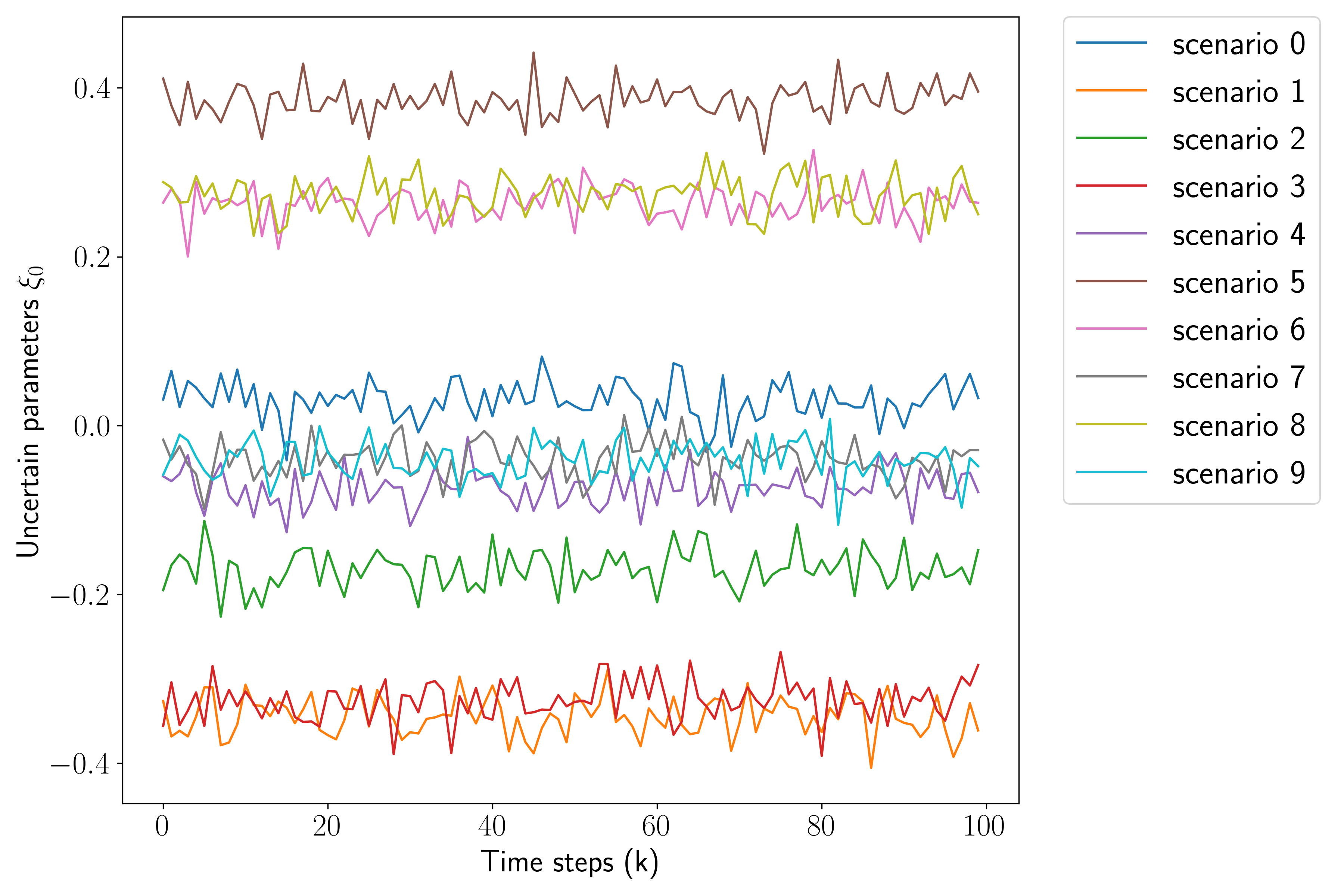

We show the values of sampled scenarios of in Figure 2. The different intercepts of lines reflect the variances of each simulation described by , and the fluctuation of each line indicates the variances among time steps for each simulation, described by .

4.2 Energy Minimization Problem

We apply L-BFGS-B to solve the stochastic optimization model of an energy minimization quantum control problem. Consider a spin system with qubits, no intrinsic Hamiltonian, and two control Hamiltonians . We define the initial state as the ground state of , which is the eigenvector of with minimum eigenvalue. The goal is to minimize the energy corresponding to of the final state . Denote the theoretical minimum value of obtained energy as , which is the minimum eigenvalue of . The specific deterministic formulation is given by

| (49a) | ||||

| (49b) | ||||

| (49c) | ||||

| (49d) | ||||

| (49e) | ||||

where are Pauli matrices of qubit for . The matrix is the adjacency matrix of a randomly generated graph with nodes. Specifically, is a symmetric matrix with zero diagonals and other elements randomly generated uniformly from the range for . When , is a symmetric matrix with zero diagonals and other elements as .

We assume that for control Hamiltonians . We set the CVaR risk-level parameter , the number of qubits , the evolution time , the number of time steps for solving the continuous relaxation , and the number of time steps for rounding . We conduct out-of-sample tests for all controls under the same distribution as in-sample tests across groups, each with scenarios. We present the results of various numbers given by different scenario numbers, weight choices, and variance settings in Sections 4.2.1–4.2.3, respectively, and then discuss the CPU time of solving the problem with different sizes in Section 4.2.4.

4.2.1 Results of Scenarios

We set the weight parameter , variance for both controllers and solve the stochastic optimization model with in-sample scenarios . Table 1 presents mean values, CVaR function values defined in (6), and weighted summation values of the mean and CVaR with weight . The “In-sample objective” columns represent the results among in-sample scenarios generated to solve the model. The “Out-of-sample objective” columns represent the results across independently generated samples for evaluating different control solutions. The columns under “Gap” represent the gaps between in-sample and out-of-sample tests for all the function values.

| In-sample objective | Out-of-sample objective | Gap | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Mean | CVaR | Total | Mean | CVaR | Total | Mean | CVaR | Total | |

| 1 | 0.038 | 0.038 | 0.038 | 0.107 | 0.357 | 0.232 | 64.16% | 89.27% | 83.48% |

| 20 | 0.100 | 0.206 | 0.153 | 0.141 | 0.410 | 0.276 | 29.07% | 49.82% | 44.50% |

| 100 | 0.105 | 0.290 | 0.198 | 0.104 | 0.326 | 0.215 | 0.84% | 10.96% | 8.10% |

| 300 | 0.102 | 0.286 | 0.194 | 0.108 | 0.309 | 0.208 | 5.67% | 7.29% | 6.87% |

| 500 | 0.100 | 0.300 | 0.200 | 0.099 | 0.318 | 0.208 | 0.90% | 5.64% | 4.08% |

We show that generally the gap of all the objective values decreases when the number of scenarios increases and the gap of the CVaR function value is higher than the mean value.

4.2.2 Results of Weight Parameter

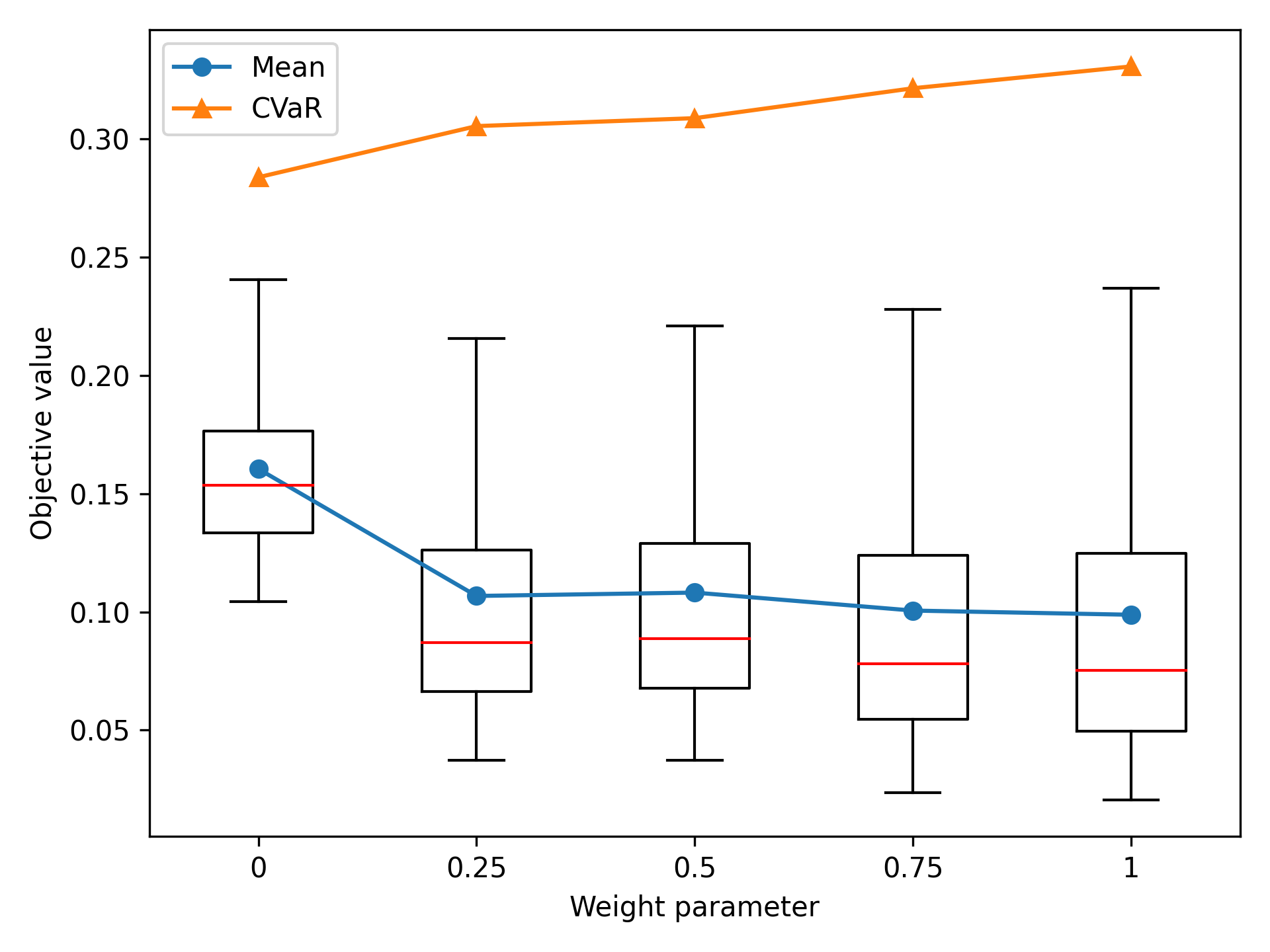

For the remaining tests we fix the in-sample size as and keep the out-of-sample size as 5,000 scenarios. We set the variance for and solve the stochastic optimization model with different weight parameters . When , the model optimizes only the CVaR function; in comparison, when , the model optimizes only the expected value of the random objective. Figure 3 presents how the values of mean and CVaR in out-of-sample tests vary depending on the weight parameter. The blue line marked by dots represents the mean, and the orange line marked by triangles represents the CVaR. Furthermore, we present box plots describing the objective values of 5,000 out-of-sample test scenarios for each weight parameter . The red lines, the box edges, and the caps represent the medians, the first to the third quartiles, and the whiskers based on the interquartile range, respectively (see Wickham and Stryjewski [69] for details).

We see that when increases, the out-of-sample mean values decrease while the CVaR function values increase because the objective function assigns more weight to the expectation. Moreover, the box plots illustrate that decreasing results in a reduced deviation, showing the advantages of incorporating risk aversion into the objective function.

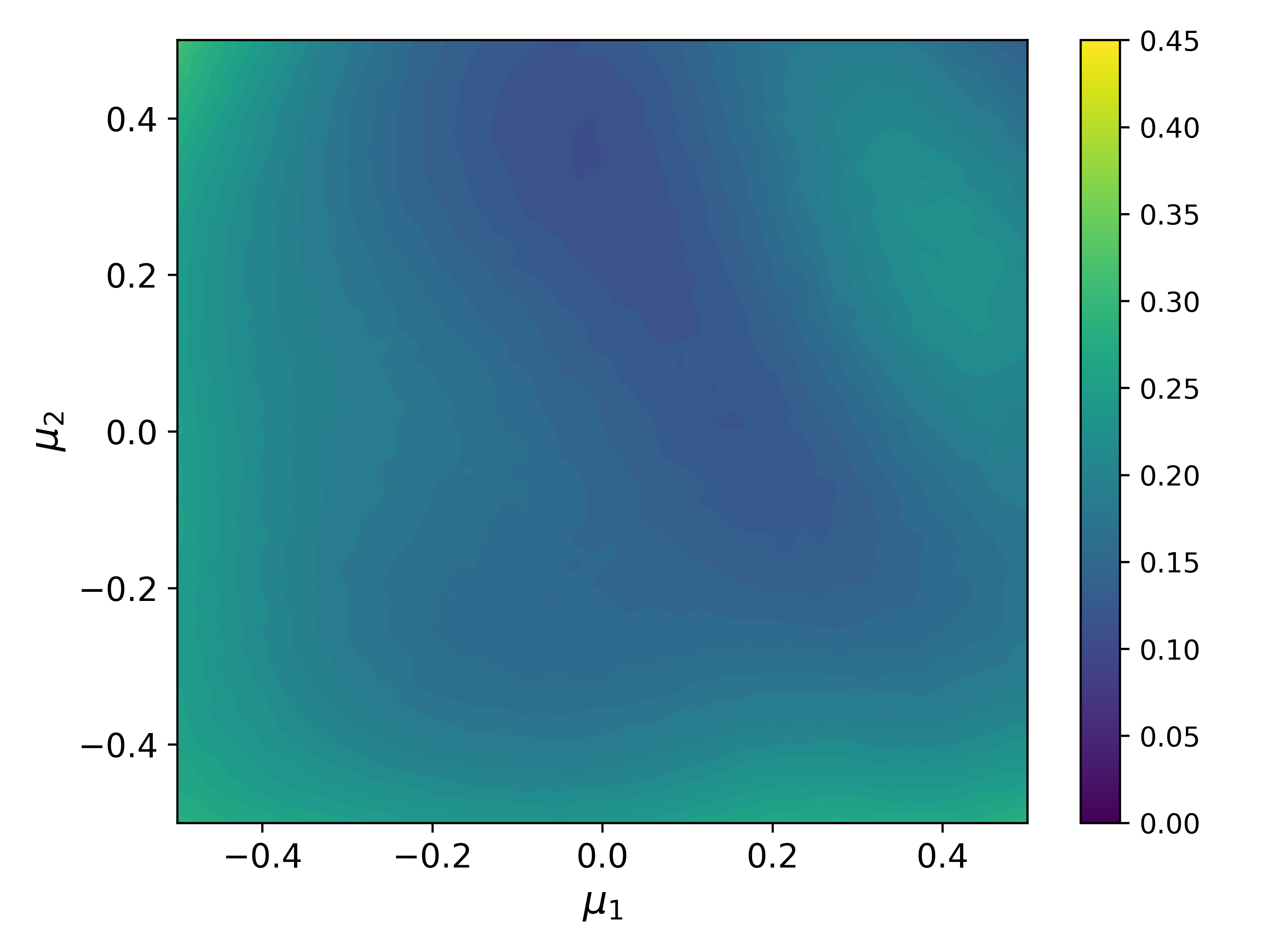

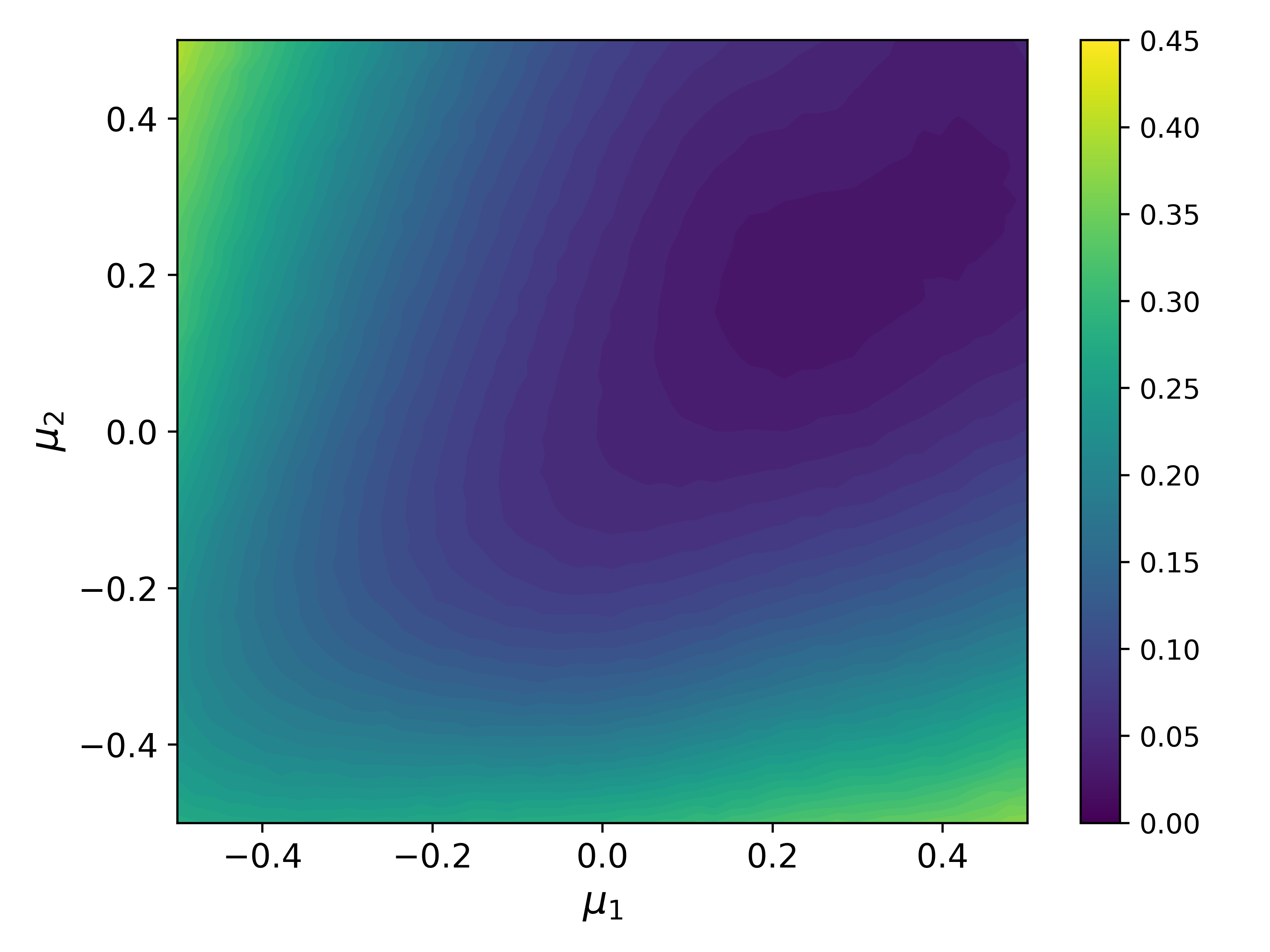

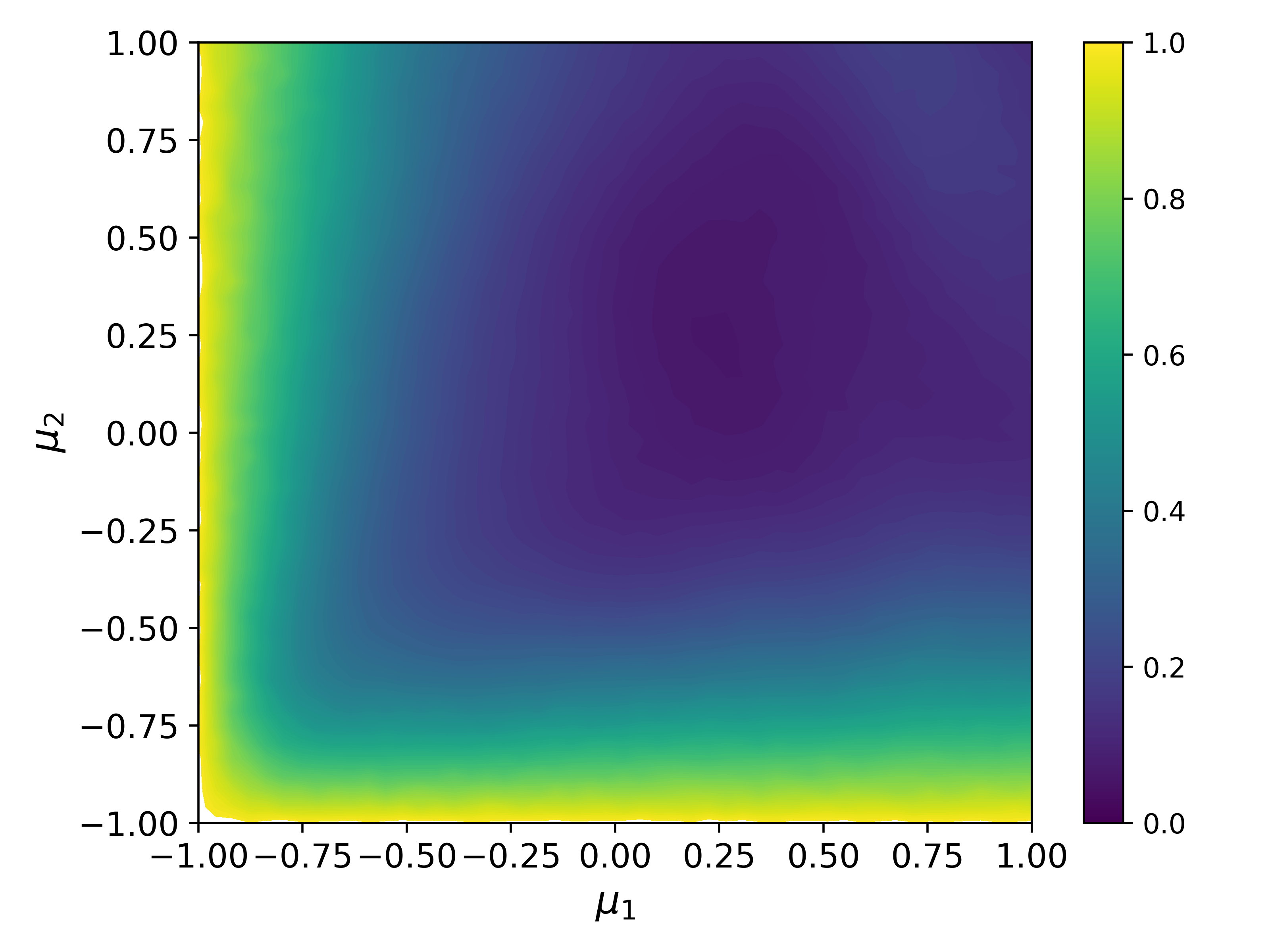

In our out-of-sample tests we find that with the same offset for , the standard deviations of the out-of-sample objective value with different are always smaller than . Therefore, we focus on comparing the objective values with various offsets in our following discussion. Using a derived control from a given weight parameter and offsets , we generate scenarios for following the normal distribution and compute the objective value . The average objective value is considered as the performance of control under a specific simulation uncertainty offset . In Figure 4 we select the risk-averse case () and the risk-neutral case () to present the figures of average objective value among 20 scenarios for offsets .

We see that the control of the risk-neutral case attains a lower objective value when the uncertainty offsets are small, leading to better average performance. On the other hand, the control of the risk-neutral case has a significantly higher objective value when the uncertainty offsets are large, as shown in the upper-left and lower-right corners of Figure 4b, while the control of the risk-averse case is more robust among all scenarios.

4.2.3 Results of Variance

Again, we fix the number of scenarios and solve the stochastic optimization model with weight for different choices of variances as . We evaluate the derived control solution using three metrics: the mean value, the CVaR function value, and the success rate in distinguishing states in the energy minimization problem. In this instance, a control successfully distinguishes the first excited state from the minimum energy state if its objective value is smaller than the energy difference ratio of these two states, which is one of our control design goals. The third metric is thus the percentage of scenarios in the out-of-sample tests that achieve this distinction, defined as the distinguished percentage (DP).

To more straightforwardly compare the performance of the stochastic optimization models with the deterministic model, we compute the percentage of change in metrics as , where and represent the evaluation metric value of the deterministic model and stochastic optimization model, respectively. Our goal is to achieve a lower quantum system energy and a higher success rate in distinguishing states. Therefore, for mean and CVaR, a negative percentage of change means a lower energy consumption and better performance compared with the deterministic model; in contrast, for the DP, a positive percentage of change means a higher success rate of the distinction and better performance compared with the deterministic model. We present the percentage of change in Table 2 and bold the best results of each variance setting. Columns with “,” “,” and “” represent the results of the model optimizing the expectation, optimizing the CVaR function, and optimizing the weighted summation function, respectively.

For the mean value we show that the results with are always better performing (in our tests) compared with the deterministic model, while the results with have worse performance because the stochastic model focuses only on the tail distribution. The balanced model with performs worse with low variance but better with high variance. For the CVaR function value we show that models with all the weights have better results and the model with is the best, demonstrating an improvement in robustness when considering parameter uncertainty. For the DP we show that the models with and are both better than the deterministic model for all the variance settings, showing the benefits of our stochastic optimization model. The model with performs worse with high variance because it optimizes for scenarios with a high error and sacrifices the performance in other scenarios.

Mean CVaR DP 0.01 0.01 3.43% 5.29% 1.15% 4.10% 5.24% 1.92% 0.00% 0.00% 0.00% 0.01 0.05 5.30% 38.85% 0.22% 4.90% 17.55% 14.95% 0.25% 1.44% 1.03% 0.01 0.1 8.85% 80.32% 4.43% 7.21% 26.08% 17.66% 1.68% 9.27% 4.20% 0.05 0.01 8.65% 25.35% 4.28% 9.30% 29.15% 16.33% 0.95% 2.57% 1.53% 0.05 0.05 9.06% 47.67% 0.44% 7.50% 20.61% 13.62% 2.04% 3.08% 2.89% 0.05 0.1 11.45% 64.49% 7.61% 7.29% 19.86% 12.18% 3.71% 24.40% 4.20% 0.1 0.01 11.66% 38.76% 2.02% 8.96% 31.38% 18.00% 3.87% 7.97% 6.00% 0.1 0.05 12.12% 33.77% 5.13% 7.87% 23.16% 12.37% 5.20% 0.74% 6.38% 0.1 0.1 14.26% 55.23% 5.45% 6.87% 17.99% 10.52% 6.79% 72.22% 7.08%

Furthermore, we observe that with a fixed uncertainty offset variance for one controller, increasing the variance of the other controller leads to higher mean values, higher CVaR function values, and lower DP, because the uncertainty in the quantum system increases. Increasing the uncertainty offset variance of the first controller has a larger negative impact on objective values compared with increasing the uncertainty variance of , which means this quantum control system is more sensitive to the uncertainty of controller .

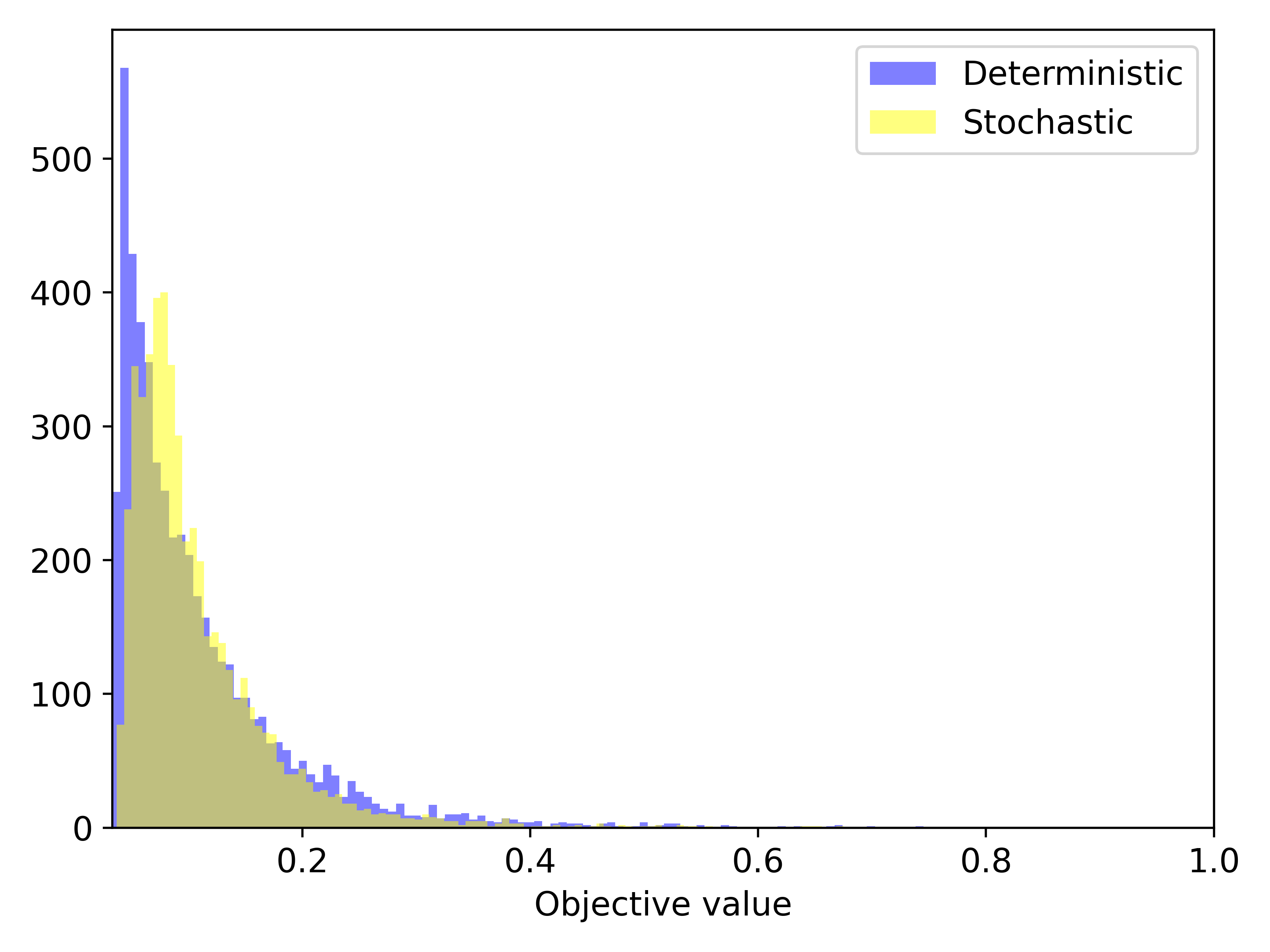

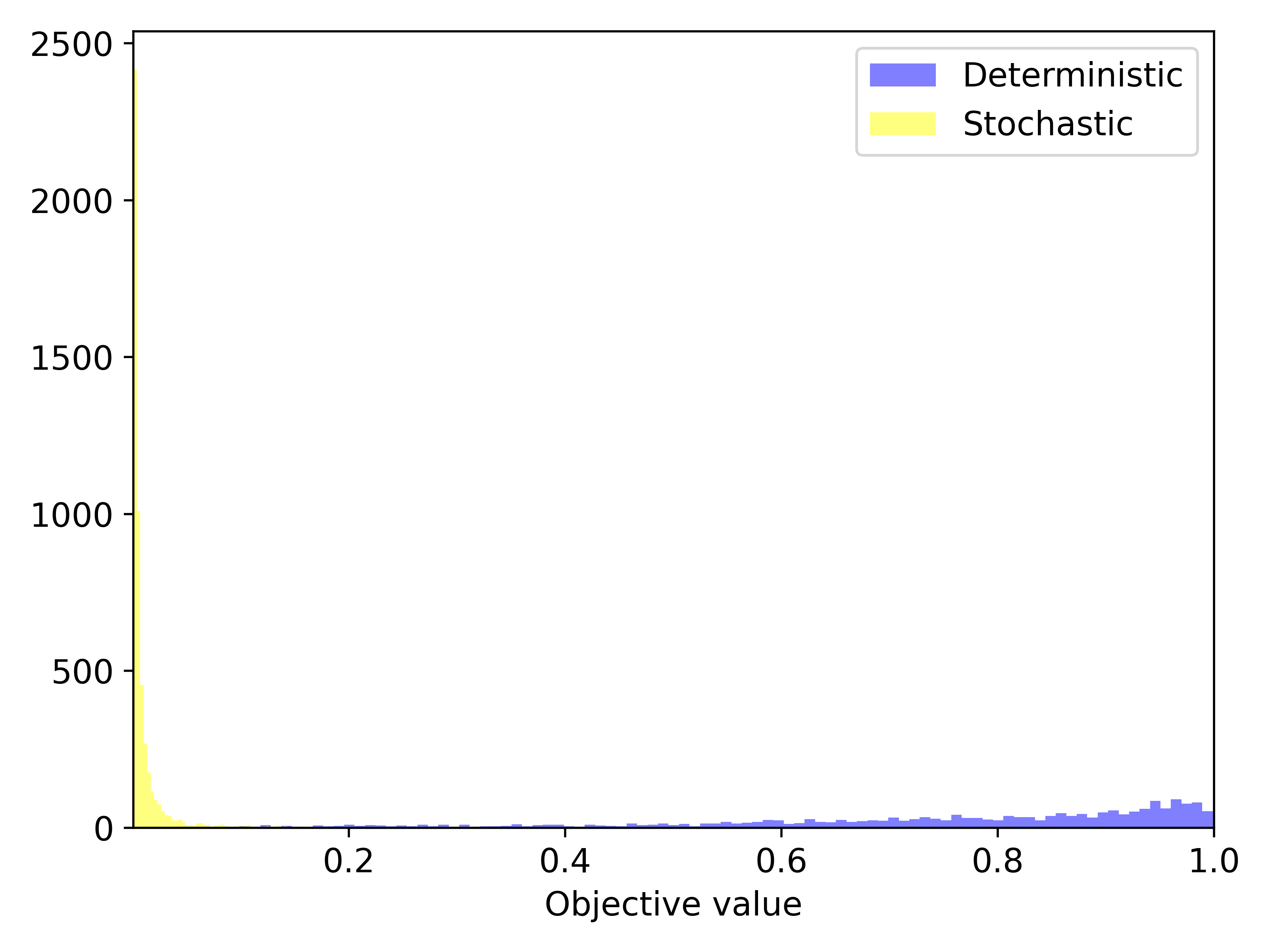

We show the histogram of out-of-sample tests for both deterministic and stochastic optimization models and the zoomed-in tail distribution with a variance of in Figure 5. The blue and yellow histograms represent the results of the deterministic and the stochastic optimization models, respectively. The figures show that our stochastic optimization model obtains a lighter tail distribution.

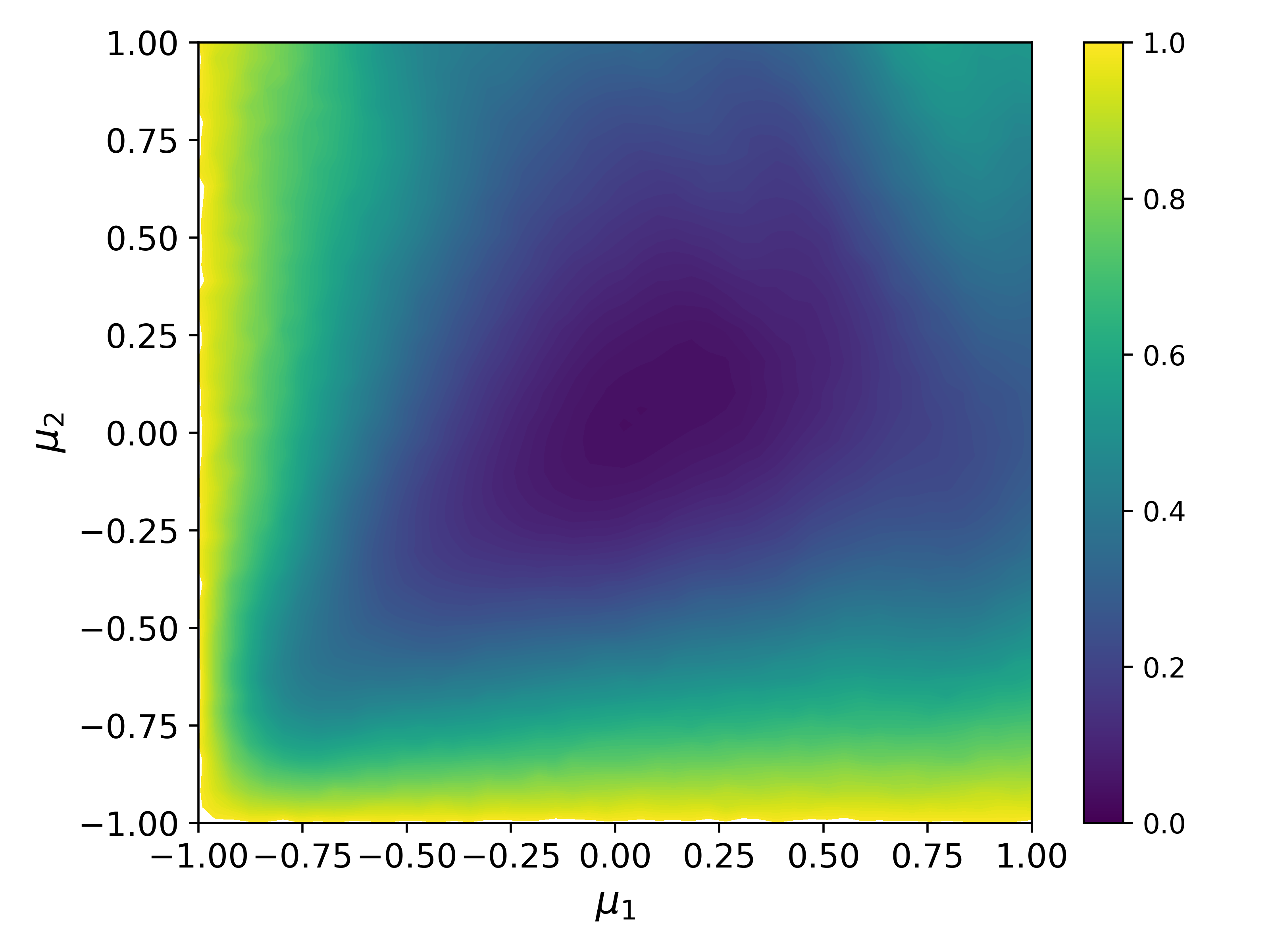

Similar to Figure 4, for each obtained control and for every combination of offsets value , we generate different scenarios for with a normal distribution and compute the average objective value . The average objective value represents the performance of control under a specific simulation uncertainty offset . In Figure 6 we present the average objective values for different offset values for obtained from the deterministic and stochastic optimization models with both offset variances set as . We show that although both controls have high objective value when goes to , the control of the stochastic optimization model is more robust, especially for and .

With a given risk level parameter , we solve the in-sample stochastic optimization model with weight and obtain the percentile value among all the scenarios. To evaluate the performance of our model on controlling the risk, we present the percentage of scenarios in the out-of-sample tests with an objective value smaller than the percentile of the in-sample objective value distribution in Table 3. We show that for all the variance settings, the difference between the percentage and the ideal value is mostly smaller than 1%. We have the closest percentage when the risk level is . When the risk control is too strict or too relaxed, the percentage in out-of-sample tests is usually smaller than , and the difference increases when variances increase.

| 0.05 | 0.05 | 98.68% | 95.76% | 89.82% |

|---|---|---|---|---|

| 0.05 | 0.1 | 98.54% | 95.68% | 90.34% |

| 0.1 | 0.05 | 98.62% | 95.46% | 87.74% |

| 0.1 | 0.1 | 98.26% | 95.50% | 88.42% |

4.2.4 Results of CPU Time

We fix the offset variances , and the weight parameter and solve the stochastic optimization model with different numbers of qubits , different numbers of time steps , and different numbers of scenarios . We present the CPU time and the number of iterations for L-BFGS-B in Table 4.

| CPU time (s) | Iteration | |||

|---|---|---|---|---|

| 2 | 20 | 300 | 32.90 | 15 |

| 2 | 50 | 300 | 99.74 | 27 |

| 6 | 50 | 300 | 2814.33 | 26 |

| 6 | 50 | 200 | 971.06 | 14 |

| 6 | 50 | 100 | 401.20 | 19 |

| 6 | 50 | 20 | 121.18 | 15 |

| 6 | 50 | 1 | 21.66 | 34 |

We show that the number of qubits has the most important impact on the CPU time because the dimension of Hamiltonian matrices grows exponentially with . This issue can be potentially resolved in the future by using quantum computers to conduct time evolution. An increasing number of scenarios leads to an increase in CPU time, which can be reduced by parallel computing on multiple CPU cores of classical computers or multiple quantum computers. The CPU time also increases with the increase in the number of time steps . Moreover, we notice that the number of iterations is robust regardless of the problem size.

4.3 Circuit Compilation Problem

Quantum circuit compilation aims to represent a circuit by specific controllers and constraints, to build a foundation for general quantum algorithms. In this section, we apply the modified Adam method (Algorithm 1) to study a compilation problem for the quantum circuit that has the ground state energy of molecules generated by the unitary coupled-cluster single-double method [70, 71]. We consider a gmon qubit quantum system with qubits, which is a superconducting qubit architecture combining high-coherence qubits and tunable qubit couplings [72]. Each qubit has a flux-drive controller and a charge-drive controller, and they are connected with their nearest neighbors according to a rectangular-grid topology. The set of connected qubits is denoted by with size . Each connected qubit group in has a corresponding Hamiltonian controller. The initial operator is a -dimensional identity matrix, and the target operator is the matrix formulation of the circuit for a certain molecule. The specific formulation of the deterministic model is

| (50a) | ||||

| (50b) | ||||

| (50e) | ||||

| (50f) | ||||

| (50g) | ||||

| (50h) | ||||

where are Pauli matrices for qubits and the subscript in constraints (50e) represents the matrix operation acting on the th qubit. The constants correspond to specific quantum machines and are set as .

We assume that the variance of uncertainty among time steps for all the control Hamiltonians. All the single-qubit control Hamiltonians have the same uncertainty offset variance, represented by ; and all two-qubit control Hamiltonians have the same uncertainty offset variance, represented by . In Sections 4.3.1–4.3.2 we discuss the performance of the stochastic optimization model on an instance of the molecule H2 (dihydrogen). The system includes qubits, single-qubit controllers, and a two-qubit controller. We set the evolution time , number of time steps , and number of rounding time steps ; the risk level . We generate 10 groups, each with 500 scenarios sampled from the same distribution under in-sample tests, to conduct out-of-sample tests for evaluating the obtained controls. In Section 4.3.3 we present the CPU time of solving the circuit compilation problem with different molecules and problem sizes.

4.3.1 Results of Scenarios

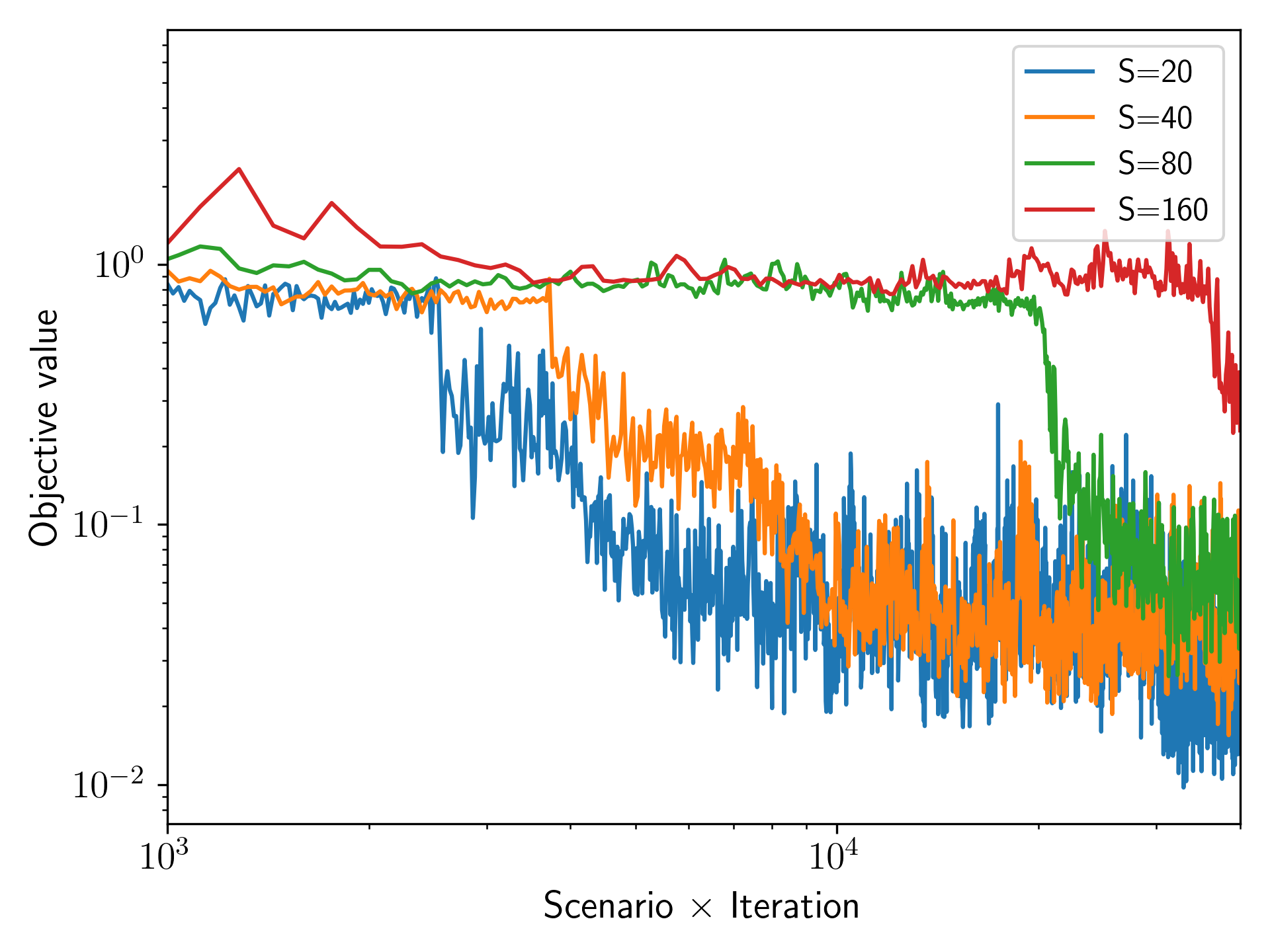

In this section we set the weight parameter and offset variances . We test our algorithm with a different number of scenarios , and with adjusted learning rates of and . To compare the performance under the same computational costs, which is represented by the product of the number of scenarios and iterations (), we set the number of iterations to and accordingly. In Figure 7 we show how the objective value varies with the computational costs during the algorithm procedure by a log-log scale. We show that with a larger number of scenarios, the objective value is more stable because the method learns more about the distribution at each iteration. However, the convergence is slower because the algorithm runs for fewer iterations.

We present the out-of-sample test results for the controls obtained by a different number of scenarios, including the mean value, the CVaR function value, and the total objective value as weighted summation with in Table 5. We show that the control with achieves the lowest objective value primarily because of its higher number of iterations within the same computational cost.

| Scenario | Mean | CVaR | Total |

|---|---|---|---|

| 20 | 8.19 | 3.21 | 2.02 |

| 40 | 1.21 | 4.30 | 2.76 |

| 80 | 1.35 | 6.76 | 4.06 |

| 160 | 2.38 | 9.51 | 5.94 |

4.3.2 Results of Variance

We compare the performance of the deterministic and the stochastic optimization model with sample size , weight parameter under different offset variances . In Table 6 we present the mean value and the CVaR function value of the deterministic model (represented by “Deter”) and the stochastic program (represented by “SP”) for different variances of the uncertainty offsets.

| Mean | CVaR | ||||

|---|---|---|---|---|---|

| Deter | SP | Deter | SP | ||

| 0.01 | 0.01 | 0.639 | 8.19 | 0.986 | 3.21 |

| 0.01 | 0.05 | 0.639 | 8.74 | 0.988 | 4.32 |

| 0.05 | 0.01 | 0.748 | 5.44 | 0.990 | 0.353 |

| 0.05 | 0.05 | 0.748 | 9.84 | 0.990 | 0.419 |

Comparing the results of different variances, we show that the uncertainty in single-qubit controllers significantly affects the objective values more than the two-qubit controllers do, mainly because single-qubit controllers are expected to have more impact on unitary operators and they are the majority of controllers in the quantum system. For example, the instance of H2 includes 4 single-qubit controllers but only 1 two-qubit controller. Moreover, increasing variance leads to a larger increase in the CVaR function value, indicating a larger negative impact on scenarios with large deviations.

We demonstrate that the control of the deterministic model performs badly even under a small variance, with all the mean values larger than 0.6 and all the CVaR function values larger than 0.9. On the other hand, the control of our stochastic optimization model performs dramatically better on the mean values and CVaR function values for all the settings, illustrating the advantages of our model considering the uncertainty in quantum control systems.

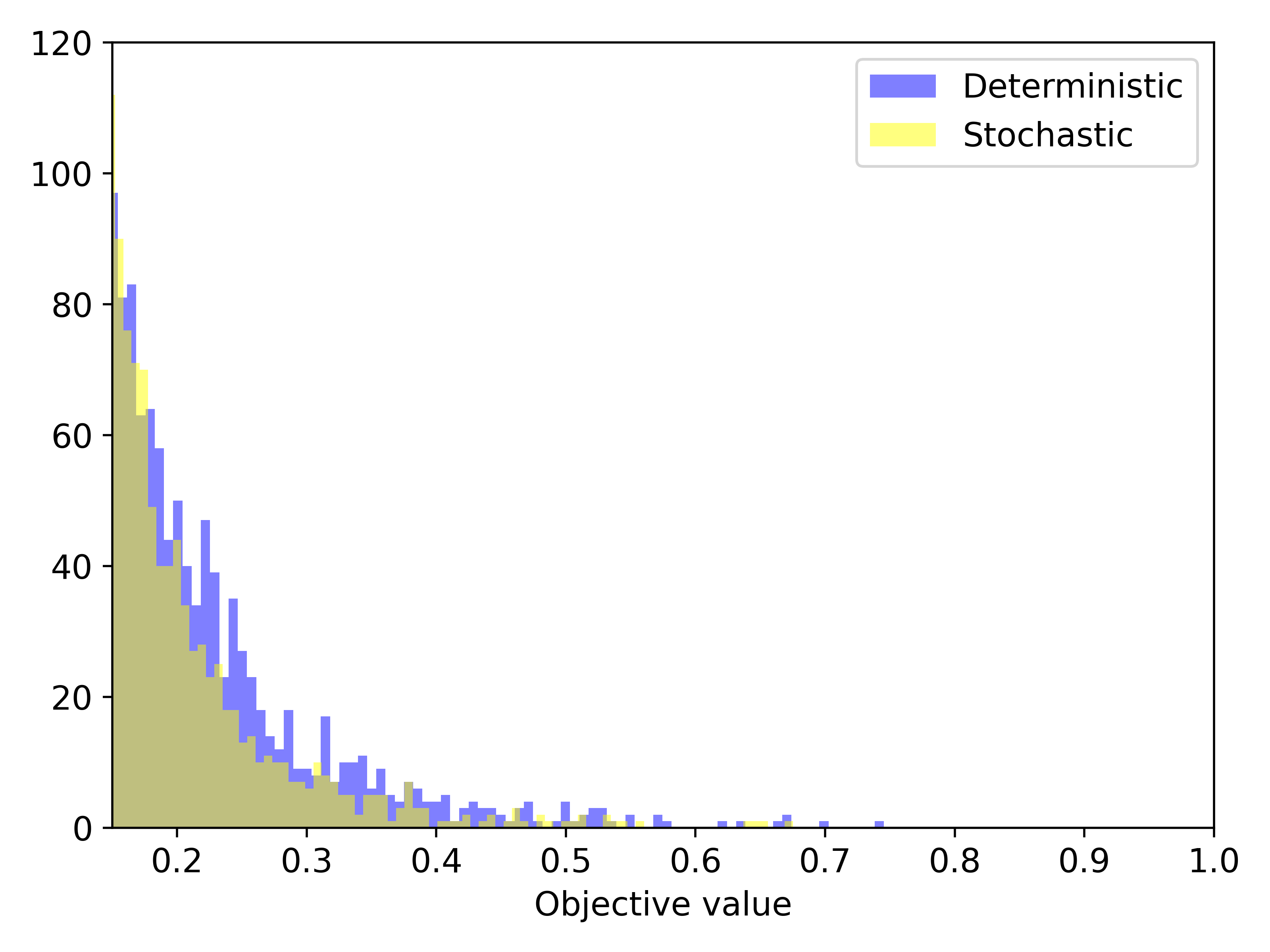

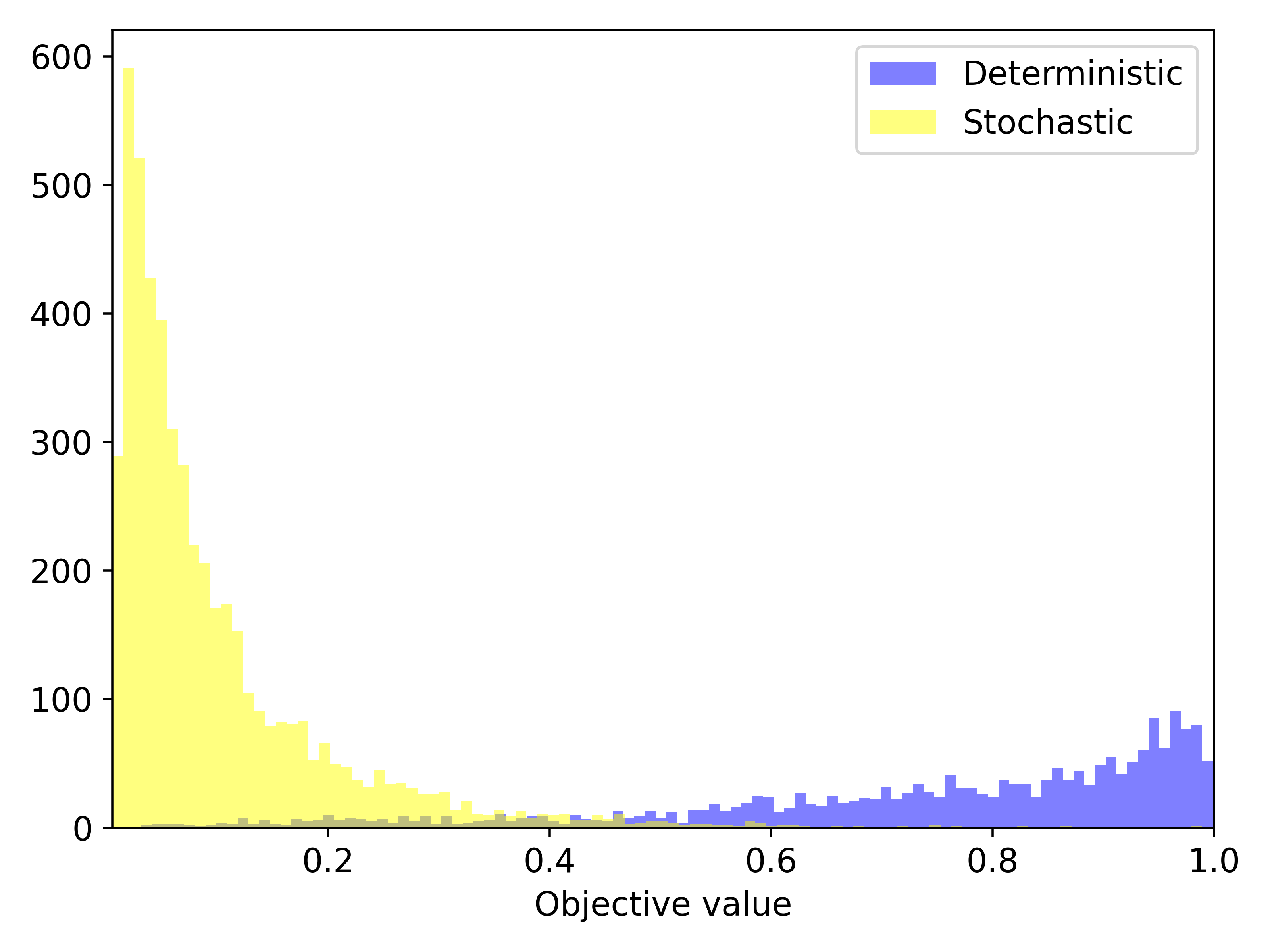

In Figure 8 we present the histogram of out-of-sample tests for both deterministic and stochastic optimization models with variances for all the controllers as 0.01 and 0.05. The blue and yellow histograms represent the results of the deterministic and the stochastic optimization model, respectively. We show that with the increase of variance, both models have heavier tail distribution, but the stochastic optimization model always has a much lighter tail distribution compared with the deterministic model.

4.3.3 Results of CPU Time

We set the iteration number for the modified Adam at 2000, weight parameter , and offset variances . We solve the stochastic optimization model for molecules H2 and LiH, with time steps and scenario numbers . In Table 7 we present the CPU time of the algorithm for different problem sizes and molecules, with the respective number of qubits and controllers .

| Molecule | CPU time (s) | ||||

|---|---|---|---|---|---|

| 2 | 5 | 50 | 20 | 1383.62 | |

| H2 | 2 | 5 | 50 | 40 | 2713.80 |

| 2 | 5 | 100 | 20 | 2888.77 | |

| 4 | 12 | 50 | 20 | 4168.16 | |

| LiH | 4 | 12 | 50 | 40 | 7918.20 |

| 4 | 12 | 100 | 20 | 8482.01 |

We show that with the same number of time steps and scenarios, changing molecules leads to a significant CPU time increase, mainly because the dimension of Hamiltonian matrices increases exponentially with and the number of controllers also increases. The CPU time increases with time steps and scenario numbers approximately linearly. In practice, the CPU time can be potentially reduced by conducting time evolution on quantum computers and parallel computing among different scenarios on large amounts of CPU cores.

5 Conclusion

In this paper we built a stochastic mixed-integer program with the sample-based reformulation for the quantum optimal control problem with uncertain Hamiltonians. We introduced an objective function aiming to balance risk-neutral and risk-averse measurements, which are evaluated by expectation and CVaR function, respectively. We derived a closed-form expression and discussed the derivative for the objective function. We modified and applied two gradient-based methods to solve the continuous relaxation and obtained binary solutions by the sum-up rounding technique with a discussion of the rounding errors.

We conducted numerical simulations on multiple quantum control instances. Based on the results, we recommend L-BFGS-B for quantum control problems minimizing system energy and the modified Adam for problems minimizing infidelity. The results show that our stochastic optimization model outperforms the deterministic model in terms of both average and robust performance for different variance levels.

With all the simulations completed on classical computers, we find that the number of qubits in quantum systems has a significant impact on the computational time. Conducting time-evolution processes on quantum computers to reduce computational time is an interesting direction for future research. Furthermore, model-free optimization methods, including reinforcement learning, provide chances to capture more complex uncertainties in quantum systems.

Acknowledgements

This work was supported by the U.S. Department of Energy, Office of Science, Office of Advanced Scientific Computing Research, Accelerated Research for Quantum Computing program under Contract No. DE-AC02-06CH11357. X. F. and S. S. received partial support from U.S. National Science Foundation (NSF) grant CMMI-2041745 and the Department of Energy (DOE) grant #DE-SC0018018. L. T. B. is a KBR employee working under the Prime Contract No. 80ARC020D0010 with the NASA Ames Research Center and is grateful for support from the DARPA Quantum Benchmarking program under IAA 8839, Annex 130.

The United States Government retains and the publisher, by accepting the article for publication, acknowledges that the United States Government retains a non-exclusive, paid-up, irrevocable, worldwide license to reproduce, prepare derivative works, distribute copies to the public, and perform publicly and display publicly, or allow others to do so, for United States Government purposes. All other rights are reserved by the copyright owner.

References

- Glaser et al. [2015] Steffen J. Glaser, Ugo Boscain, Tommaso Calarco, Christiane P. Koch, Walter Köckenberger, Ronnie Kosloff, Ilya Kuprov, Burkhard Luy, Sophie Schirmer, Thomas Schulte-Herbrüggen, Dominique Sugny, and Frank K. Wilhelm. Training Schrödinger’s cat: quantum optimal control. The European Physical Journal D, 69, 2015. doi:10.1140/epjd/e2015-60464-1. URL https://doi.org/10.1140/epjd/e2015-60464-1.

- Werschnik and Gross [2007] J Werschnik and E K U Gross. Quantum optimal control theory. Journal of Physics B: Atomic, Molecular and Optical Physics, 40(18):R175, sep 2007. doi:10.1088/0953-4075/40/18/R01. URL https://dx.doi.org/10.1088/0953-4075/40/18/R01.

- d’Alessandro [2021] Domenico d’Alessandro. Introduction to Quantum Control and Dynamics. Chapman and Hall/CRC, 2021. doi:10.1201/9781003051268. URL https://doi.org/10.1201/9781003051268.

- Kehlet et al. [2004] Cindie T Kehlet, Astrid C Sivertsen, Morten Bjerring, Timo O Reiss, Navin Khaneja, Steffen J Glaser, and Niels Chr Nielsen. Improving solid-state NMR dipolar recoupling by optimal control. Journal of the American Chemical Society, 126(33):10202–10203, 2004. doi:10.1021/ja048786e. URL https://doi.org/10.1021/ja048786e.

- Khaneja et al. [2005] Navin Khaneja, Timo Reiss, Cindie Kehlet, Thomas Schulte-Herbrüggen, and Steffen J Glaser. Optimal control of coupled spin dynamics: Design of NMR pulse sequences by gradient ascent algorithms. Journal of Magnetic Resonance, 172(2):296–305, 2005. doi:10.1016/j.jmr.2004.11.004. URL http://dx.doi.org/10.1016/j.jmr.2004.11.004.

- Maximov et al. [2008] Ivan I Maximov, Zdenĕk Tošner, and Niels Chr Nielsen. Optimal control design of NMR and dynamic nuclear polarization experiments using monotonically convergent algorithms. The Journal of Chemical Physics, 128(18):05B609, 2008. doi:10.1063/1.2903458. URL http://dx.doi.org/10.1063/1.2903458.

- Skinner et al. [2003] Thomas E Skinner, Timo O Reiss, Burkhard Luy, Navin Khaneja, and Steffen J Glaser. Application of optimal control theory to the design of broadband excitation pulses for high-resolution NMR. Journal of Magnetic Resonance, 163(1):8–15, 2003. doi:10.1016/s1090-7807(03)00153-8. URL http://dx.doi.org/10.1016/s1090-7807(03)00153-8.

- Kosloff et al. [1989] R. Kosloff, S.A. Rice, P. Gaspard, S. Tersigni, and D.J. Tannor. Wavepacket dancing: Achieving chemical selectivity by shaping light pulses. Chemical Physics, 139(1):201–220, 1989. doi:10.1016/0301-0104(89)90012-8. URL https://www.sciencedirect.com/science/article/pii/0301010489900128.

- Peirce et al. [1988] Anthony P. Peirce, Mohammed A. Dahleh, and Herschel Rabitz. Optimal control of quantum-mechanical systems: Existence, numerical approximation, and applications. Physical Review A, 37:4950–4964, Jun 1988. doi:10.1103/PhysRevA.37.4950. URL https://link.aps.org/doi/10.1103/PhysRevA.37.4950.

- Pawela and Sadowski [2016] Łukasz Pawela and Przemysław Sadowski. Various methods of optimizing control pulses for quantum systems with decoherence. Quantum Information Processing, 15(5):1937–1953, 2016. doi:10.1007/s11128-016-1242-y. URL http://dx.doi.org/10.1007/s11128-016-1242-y.

- Motzoi et al. [2009] F. Motzoi, J. M. Gambetta, P. Rebentrost, and F. K. Wilhelm. Simple pulses for elimination of leakage in weakly nonlinear qubits. Physical Review Letters, 103(11), 2009. doi:10.1103/physrevlett.103.110501. URL https://link.aps.org/doi/10.1103/PhysRevLett.103.110501.

- Gokhale et al. [2019] Pranav Gokhale, Yongshan Ding, Thomas Propson, Christopher Winkler, Nelson Leung, Yunong Shi, David I Schuster, Henry Hoffmann, and Frederic T Chong. Partial compilation of variational algorithms for noisy intermediate-scale quantum machines. In Proceedings of the 52nd Annual IEEE/ACM International Symposium on Microarchitecture, pages 266–278, 2019. doi:10.1145/3352460.3358313. URL http://dx.doi.org/10.1145/3352460.3358313.

- Leung et al. [2017] Nelson Leung, Mohamed Abdelhafez, Jens Koch, and David Schuster. Speedup for quantum optimal control from automatic differentiation based on graphics processing units. Physical Review A, 95(4):042318, 2017. doi:10.1103/PhysRevA.95.042318. URL http://dx.doi.org/10.1103/PhysRevA.95.042318.

- Palao and Kosloff [2002] José P. Palao and Ronnie Kosloff. Quantum computing by an optimal control algorithm for unitary transformations. Physical Review Letters, 89:188301, 2002. doi:10.1103/physrevlett.89.188301. URL http://dx.doi.org/10.1103/physrevlett.89.188301.

- Palao and Kosloff [2003] José P. Palao and Ronnie Kosloff. Optimal control theory for unitary transformations. Physical Review A, 68:062308, 2003. doi:10.1103/PhysRevA.68.062308. URL http://dx.doi.org/10.1103/PhysRevA.68.062308.

- Rebentrost and Wilhelm [2009] Patrick Rebentrost and Frank K Wilhelm. Optimal control of a leaking qubit. Physical Review B, 79(6):060507, 2009. doi:10.1103/PhysRevB.79.060507. URL http://dx.doi.org/10.1103/PhysRevB.79.060507.

- Brady et al. [2021a] Lucas T. Brady, Christopher L. Baldwin, Aniruddha Bapat, Yaroslav Kharkov, and Alexey V. Gorshkov. Optimal protocols in quantum annealing and quantum approximate optimization algorithm problems. Physical Review Letters, 126(7), feb 2021a. doi:10.1103/physrevlett.126.070505. URL https://doi.org/10.1103%2Fphysrevlett.126.070505.

- Brady et al. [2021b] Lucas T. Brady, Lucas Kocia, Przemyslaw Bienias, Yaroslav Kharkov Aniruddha Bapat, and Alexey V. Gorshkov. Behavior of analog quantum algorithms. https://arXiv.org/abs/2107.01218, 2021b.

- Fei et al. [2023a] Xinyu Fei, Lucas T. Brady, Jeffrey Larson, Sven Leyffer, and Siqian Shen. Binary control pulse optimization for quantum systems. Quantum, 7:892, January 2023a. doi:10.22331/q-2023-01-04-892. URL https://doi.org/10.22331/q-2023-01-04-892.

- Fei et al. [2023b] Xinyu Fei, Lucas T Brady, Jeffrey Larson, Sven Leyffer, and Siqian Shen. Switching time optimization for binary quantum optimal control. https://doi.org/10.48550/arXiv.2308.03132, 2023b.

- Bapat and Jordan [2018] Aniruddha Bapat and Stephen Jordan. Bang-bang control as a design principle for classical and quantum optimization algorithms. https://arXiv.org/abs/1812.02746, 2018.

- Mbeng et al. [2019] Glen Bigan Mbeng, Rosario Fazio, and Giuseppe Santoro. Quantum annealing: A journey through digitalization, control, and hybrid quantum variational schemes, 2019. URL https://arXiv.org/abs/1906.08948.

- Venuti et al. [2021] Lorenzo Campos Venuti, Domenico D’Alessandro, and Daniel A. Lidar. Optimal control for quantum optimization of closed and open systems. Physical Review Applied, 16(5), nov 2021. doi:10.1103/PhysRevApplied.16.054023. URL https://doi.org/10.1103%2FPhysRevApplied.16.054023.

- Larocca and Wisniacki [2021] Martín Larocca and Diego Wisniacki. Krylov-subspace approach for the efficient control of quantum many-body dynamics. Physical Review A, 103(2), Feb 2021. doi:10.1103/PhysRevA.103.023107. URL http://dx.doi.org/10.1103/PhysRevA.103.023107.

- Doria et al. [2011] Patrick Doria, Tommaso Calarco, and Simone Montangero. Optimal control technique for many-body quantum dynamics. Physical Review Letters, 106:190501, May 2011. doi:10.1103/PhysRevLett.106.190501. URL https://link.aps.org/doi/10.1103/PhysRevLett.106.190501.

- Caneva et al. [2011] Tommaso Caneva, Tommaso Calarco, and Simone Montangero. Chopped random-basis quantum optimization. Physical Review A, 84(2):022326, 2011. doi:10.1103/PhysRevA.84.022326. URL http://dx.doi.org/10.1103/PhysRevA.84.022326.

- Sørensen et al. [2018] JJWH Sørensen, MO Aranburu, Till Heinzel, and JF Sherson. Quantum optimal control in a chopped basis: Applications in control of Bose-Einstein condensates. Physical Review A, 98(2):022119, 2018. doi:10.1103/PhysRevA.98.022119. URL http://dx.doi.org/10.1103/PhysRevA.98.022119.

- Zahedinejad et al. [2014] Ehsan Zahedinejad, Sophie Schirmer, and Barry C Sanders. Evolutionary algorithms for hard quantum control. Physical Review A, 90(3):032310, 2014. doi:10.1103/PhysRevA.90.032310. URL http://dx.doi.org/10.1103/PhysRevA.90.032310.

- Bukov et al. [2018] Marin Bukov, Alexandre GR Day, Dries Sels, Phillip Weinberg, Anatoli Polkovnikov, and Pankaj Mehta. Reinforcement learning in different phases of quantum control. Physical Review X, 8(3):031086, 2018. doi:10.1103/physrevx.8.031086. URL http://dx.doi.org/10.1103/physrevx.8.031086.

- Niu et al. [2019] Murphy Yuezhen Niu, Sergio Boixo, Vadim N Smelyanskiy, and Hartmut Neven. Universal quantum control through deep reinforcement learning. npj Quantum Information, 5(1):1–8, 2019. doi:10.1038/s41534-019-0141-3. URL http://dx.doi.org/10.1038/s41534-019-0141-3.

- Sivak et al. [2022] VV Sivak, A Eickbusch, H Liu, B Royer, I Tsioutsios, and MH Devoret. Model-free quantum control with reinforcement learning. Physical Review X, 12(1):011059, 2022. doi:10.1103/PhysRevX.12.011059. URL https://link.aps.org/doi/10.1103/PhysRevX.12.011059.

- Chen et al. [2013] Chunlin Chen, Daoyi Dong, Han-Xiong Li, Jian Chu, and Tzyh-Jong Tarn. Fidelity-based probabilistic Q-learning for control of quantum systems. IEEE Transactions on Neural Networks and Learning Systems, 25(5):920–933, 2013. doi:10.1109/tnnls.2013.2283574. URL http://dx.doi.org/10.1109/tnnls.2013.2283574.

- Zhang et al. [2019] Xiao-Ming Zhang, Zezhu Wei, Raza Asad, Xu-Chen Yang, and Xin Wang. When does reinforcement learning stand out in quantum control? A comparative study on state preparation. npj Quantum Information, 5(1):85, 2019. doi:10.1038/s41534-019-0201-8. URL http://dx.doi.org/10.1038/s41534-019-0201-8.

- Vogt and Petersson [2022] Ryan H Vogt and N Anders Petersson. Binary optimal control of single-flux-quantum pulse sequences. SIAM Journal on Control and Optimization, 60(6):3217–3236, November 2022. doi:10.1137/21m142808x. URL http://dx.doi.org/10.1137/21m142808x.

- Dahleh et al. [1990] M Dahleh, AP Peirce, and H Rabitz. Optimal control of uncertain quantum systems. Physical Review A, 42(3):1065, 1990. doi:10.1103/PhysRevA.42.1065. URL https://link.aps.org/doi/10.1103/PhysRevA.42.1065.

- Grace et al. [2012] Matthew D Grace, Jason M Dominy, Wayne M Witzel, and Malcolm S Carroll. Optimized pulses for the control of uncertain qubits. Physical Review A, 85(5):052313, 2012. doi:10.1103/PhysRevA.85.052313. URL http://dx.doi.org/10.1103/PhysRevA.85.052313.

- Propson et al. [2022] Thomas Propson, Brian E Jackson, Jens Koch, Zachary Manchester, and David I Schuster. Robust quantum optimal control with trajectory optimization. Physical Review Applied, 17(1):014036, 2022. doi:10.1103/PhysRevApplied.17.014036. URL http://dx.doi.org/10.1103/PhysRevApplied.17.014036.

- Green et al. [2013] Todd J Green, Jarrah Sastrawan, Hermann Uys, and Michael J Biercuk. Arbitrary quantum control of qubits in the presence of universal noise. New Journal of Physics, 15(9):095004, 2013. doi:10.1088/1367-2630/15/9/095004. URL http://dx.doi.org/10.1088/1367-2630/15/9/095004.

- Kosut et al. [2022] Robert L Kosut, Gaurav Bhole, and Herschel Rabitz. Robust quantum control: Analysis & synthesis via averaging. https://arXiv.org/abs/2208.14193, 2022.

- Chen et al. [2014a] Chunlin Chen, Daoyi Dong, Ruixing Long, Ian R Petersen, and Herschel A Rabitz. Sampling-based learning control of inhomogeneous quantum ensembles. Physical Review A, 89(2):023402, 2014a. doi:10.1103/PhysRevA.89.023402. URL http://dx.doi.org/10.1103/PhysRevA.89.023402.

- Li and Khaneja [2006] Jr-Shin Li and Navin Khaneja. Control of inhomogeneous quantum ensembles. Physical Review A, 73:030302, Mar 2006. doi:10.1103/PhysRevA.73.030302. URL https://link.aps.org/doi/10.1103/PhysRevA.73.030302.

- Pryor and Khaneja [2006] Brent Pryor and Navin Khaneja. Fourier decompositions and pulse sequence design algorithms for nuclear magnetic resonance in inhomogeneous fields. The Journal of Chemical Physics, 125(19):194111, 2006. doi:10.1063/1.2390715. URL http://dx.doi.org/10.1063/1.2390715.

- Owrutsky and Khaneja [2012] Philip Owrutsky and Navin Khaneja. Control of inhomogeneous ensembles on the bloch sphere. Physical Review A, 86:022315, Aug 2012. doi:10.1103/PhysRevA.86.022315. URL https://link.aps.org/doi/10.1103/PhysRevA.86.022315.

- Mischuck et al. [2012] Brian E. Mischuck, Seth T. Merkel, and Ivan H. Deutsch. Control of inhomogeneous atomic ensembles of hyperfine qudits. Physical Review A, 85:022302, Feb 2012. doi:10.1103/PhysRevA.85.022302. URL https://link.aps.org/doi/10.1103/PhysRevA.85.022302.

- Barr et al. [2022] Robert Barr, Yasuo Oda, Gregory Quiroz, B David Clader, and Leigh M Norris. Qubit control noise spectroscopy with optimal suppression of dephasing. Physical Review A, 106(2):022425, 2022. doi:10.1103/PhysRevA.106.022425. URL http://dx.doi.org/10.1103/PhysRevA.106.022425.

- Ruths and Li [2011] Justin Ruths and Jr-Shin Li. A multidimensional pseudospectral method for optimal control of quantum ensembles. The Journal of Chemical Physics, 134(4):044128, 2011. doi:10.1063/1.3541253. URL http://dx.doi.org/10.1063/1.3541253.

- Wu et al. [2019] Re-Bing Wu, Haijin Ding, Daoyi Dong, and Xiaoting Wang. Learning robust and high-precision quantum controls. Physical Review A, 99(4):042327, 2019. doi:10.1103/PhysRevA.99.042327. URL http://dx.doi.org/10.1103/PhysRevA.99.042327.

- Wesenberg [2004] Janus H. Wesenberg. Designing robust gate implementations for quantum-information processing. Physical Review A, 69:042323, Apr 2004. doi:10.1103/PhysRevA.69.042323. URL https://link.aps.org/doi/10.1103/PhysRevA.69.042323.

- Kosut et al. [2013] Robert L Kosut, Matthew D Grace, and Constantin Brif. Robust control of quantum gates via sequential convex programming. Physical Review A, 88(5):052326, 2013. doi:10.1103/PhysRevA.88.052326. URL http://dx.doi.org/10.1103/PhysRevA.88.052326.

- Sager et al. [2012] Sebastian Sager, Hans Georg Bock, and Moritz Diehl. The integer approximation error in mixed-integer optimal control. Mathematical Programming, 133(1):1–23, 2012. doi:10.1007/s10107-010-0405-3. URL http://dx.doi.org/10.1007/s10107-010-0405-3.

- Lidar and Brun [2013] Daniel A Lidar and Todd A Brun. Quantum Error Correction. Cambridge University Press, September 2013. doi:10.1017/cbo9781139034807. URL http://dx.doi.org/10.1017/cbo9781139034807.

- Breuer and Petruccione [2007] Heinz-Peter Breuer and Francesco Petruccione. The Theory of Open Quantum Systems. Oxford University PressOxford, January 2007. doi:10.1093/acprof:oso/9780199213900.001.0001. URL http://dx.doi.org/10.1093/acprof:oso/9780199213900.001.0001.

- Bruzewicz et al. [2019] Colin D. Bruzewicz, John Chiaverini, Robert McConnell, and Jeremy M. Sage. Trapped-ion quantum computing: Progress and challenges. Applied Physics Reviews, 6(2), May 2019. ISSN 1931-9401. doi:10.1063/1.5088164. URL http://dx.doi.org/10.1063/1.5088164.

- Shapiro et al. [2014] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczyński. Lectures on Stochastic Programming: Modeling and Theory. Society for Industrial & Applied Mathematics, 2014. doi:10.1137/1.9781611973433. URL https://epubs.siam.org/doi/book/10.1137/1.9781611973433.

- Sarykalin et al. [2008] Sergey Sarykalin, Gaia Serraino, and Stan Uryasev. Value-at-Risk vs. Conditional Value-at-Risk in Risk Management and Optimization, pages 270–294. INFORMS, 2008. doi:10.1287/educ.1080.0052. URL http://dx.doi.org/10.1287/educ.1080.0052.

- Rockafellar and Uryasev [2000] R Tyrrell Rockafellar and Stanislav Uryasev. Optimization of conditional value-at-risk. Journal of Risk, 2:21–42, 2000. doi:10.21314/JOR.2000.038. URL https://www.risk.net/journal-risk/2161159/optimization-conditional-value-risk.

- Rockafellar and Uryasev [2002] R Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26(7):1443–1471, 2002. doi:10.1016/s0378-4266(02)00271-6. URL http://dx.doi.org/10.1016/s0378-4266(02)00271-6.

- Pflug [2000] Georg Ch Pflug. Some Remarks on the Value-at-Risk and the Conditional Value-at-Risk, pages 272–281. Springer, 2000. doi:10.1007/978-1-4757-3150-7_15. URL http://dx.doi.org/10.1007/978-1-4757-3150-7_15.

- Pang and Leyffer [2004] Jong-shi Pang and Sven Leyffer. On the global minimization of the value-at-risk. Optimization Methods and Software, 19(5):611–631, 2004. doi:10.1080/10556780410001704911. URL http://dx.doi.org/10.1080/10556780410001704911.

- Byrd et al. [1995] Richard H Byrd, Peihuang Lu, Jorge Nocedal, and Ciyou Zhu. A limited memory algorithm for bound constrained optimization. SIAM Journal on Scientific Computing, 16(5):1190–1208, 1995. doi:10.1137/0916069. URL https://doi.org/10.1137/0916069.

- Kingma and Ba [2014] Diederik P Kingma and Jimmy Ba. Adam: A method for stochastic optimization. https://arXiv.org/abs/1412.6980, 2014.

- Zhu et al. [1997] Ciyou Zhu, Richard H Byrd, Peihuang Lu, and Jorge Nocedal. Algorithm 778: L-BFGS-B: Fortran subroutines for large-scale bound-constrained optimization. ACM Transactions on Mathematical Software, 23(4):550–560, 1997. doi:10.1145/279232.279236. URL https://doi.org/10.1145/279232.279236.

- Sager et al. [2011] Sebastian Sager, Michael Jung, and Christian Kirches. Combinatorial integral approximation. Mathematical Methods of Operations Research, 73(3):363–380, 2011. doi:10.1007/s00186-011-0355-4. URL http://dx.doi.org/10.1007/s00186-011-0355-4.

- Sager and Zeile [2021] Sebastian Sager and Clemens Zeile. On mixed-integer optimal control with constrained total variation of the integer control. Computational Optimization and Applications, 78(2):575–623, 2021. doi:10.1007/s10589-020-00244-5. URL https://doi.org/10.1007/s10589-020-00244-5.

- Leyffer et al. [2021] Sven Leyffer, Paul Manns, and Malte Winckler. Convergence of sum-up rounding schemes for cloaking problems governed by the Helmholtz equation. Computational Optimization and Applications, 79(1):193–221, 2021. doi:10.1007/s10589-020-00262-3. URL http://dx.doi.org/10.1007/s10589-020-00262-3.

- Manns and Kirches [2020] Paul Manns and Christian Kirches. Multidimensional sum-up rounding for elliptic control systems. SIAM Journal on Numerical Analysis, 58(6):3427–3447, 2020. doi:10.1137/19M1260682. URL http://dx.doi.org/10.1137/19m1260682.

- Wikipedia [2023] Wikipedia. https://en.wikipedia.org/wiki/Almost_everywhere, 2023. [Online; accessed 13-January-2024].

- Fei et al. [2023c] Xinyu Fei, Lucas T. Brady, Jeffrey Larson, Sven Leyffer, and Siqian Shen. Code and results: Quantum control optimization with uncertain Hamiltonians. https://github.com/xinyufei/Stochastic-quantum-control, 2023c.

- Wickham and Stryjewski [2011] Hadley Wickham and Lisa Stryjewski. 40 years of boxplots. The American Statistician, 2011. URL https://api.semanticscholar.org/CorpusID:36975036.

- Bartlett and Musiał [2007] Rodney J Bartlett and Monika Musiał. Coupled-cluster theory in quantum chemistry. Reviews of Modern Physics, 79(1):291, 2007. doi:10.1103/RevModPhys.79.291. URL https://link.aps.org/doi/10.1103/RevModPhys.79.291.

- Romero et al. [2018] Jonathan Romero, Ryan Babbush, Jarrod R McClean, Cornelius Hempel, Peter J Love, and Alán Aspuru-Guzik. Strategies for quantum computing molecular energies using the unitary coupled cluster ansatz. Quantum Science and Technology, 4(1):014008, 2018. doi:10.1088/2058-9565/aad3e4. URL http://dx.doi.org/10.1088/2058-9565/aad3e4.

- Chen et al. [2014b] Yu Chen, C. Neill, P. Roushan, N. Leung, M. Fang, R. Barends, J. Kelly, B. Campbell, Z. Chen, B. Chiaro, A. Dunsworth, E. Jeffrey, A. Megrant, J. Y. Mutus, P. J. J. O’Malley, C. M. Quintana, D. Sank, A. Vainsencher, J. Wenner, T. C. White, Michael R. Geller, A. N. Cleland, and John M. Martinis. Qubit architecture with high coherence and fast tunable coupling. Physical Review Letters, 113(22):220502, 2014b. doi:10.1103/PhysRevLett.113.220502. URL https://link.aps.org/doi/10.1103/PhysRevLett.113.220502.