Limiting Spectra of inhomogeneous random graphs

Abstract.

We consider sparse inhomogeneous Erdős-Rényi random graph ensembles where edges are connected independently with probability . We assume that where is a sequence of deterministic weights, is a bounded function and . We characterise the limiting moments in terms of graph homomorphisms and also classify the contributing partitions. We present an analytic way to determine the Stieltjes transform of the limiting measure. The convergence of the empirical distribution function follows from the theory of local weak convergence in many examples but we do not rely on this theory and exploit combinatorial and analytic techniques to derive some interesting properties of the limit. We extend the methods of Khorunzhy et al. (2004) and show that a fixed point equation determines the limiting measure. The limiting measure crucially depends on and it is known that in the homogeneous case, if , the measure converges weakly to the semicircular law (Jung and Lee (2018)). We extend this result of interpolating between the sparse and dense regimes to the inhomogeneous setting and show that as , the measure converges weakly to a measure which is known as the operator-valued semicircular law.

Key words and phrases:

generalized random graphs, inhomogeneous random graph, empirical spectral distribution, spectrum, free probability2000 Mathematics Subject Classification:

05C80, 60B20, 60B10, 46L541. Introduction

Homogeneous Erdős-Rényi Random Graphs (ERRG) serve as the basis for many mathematical theories in random graphs. Real-world networks are highly inhomogeneous and have a far more complex structure. Various attempts have been made to generalize this to other kinds of random graph models. One of the successful extensions is the inhomogeneous Erdős-Rényi random graph model introduced by Bollobás et al. (2007). This graph has vertices labeled by , and edges are present independently with probability given by , where is a nice symmetric kernel on a state space , and are certain attributes associated with vertex belonging to . If is bounded, the graph is a sparse random graph. To introduce the non-sparse regime, in this article, we consider a small variant of the above inhomogeneous random graph. The vertex set remains the same, but the connection probabilities are given by

| (1.1) |

where is a tuning parameter, is a sequence of deterministic weights, and is a symmetric, bounded function on . The weights can signify a property of vertex . They can also be generally random, but we do not consider this case. Note that when , the average degree is unbounded, and when , the average degree is bounded. We call the former case dense and the latter case sparse. In the sparse case, the properties of the connected components were studied in Bollobás et al. (2007). They studied the properties of the connected components and their relationship with the branching process. It was shown that the largest component of the graph has a size of order if the operator norm of the kernel operator corresponding to is strictly greater than (see also (van der Hofstad, 2023, Theorem 3.9)). In the subcritical case, the sizes of the largest connected components can exhibit different behaviour compared to the ERRG. The study of the largest connected components in various inhomogeneous random graphs has attracted a lot of attention (see, for example, Bhamidi et al. (2010), Broutin et al. (2021), Bet et al. (2023), van der Hofstad (2013), Devroye and Fraiman (2014)). In this article, we are interested in the empirical distribution of the eigenvalues of the adjacency matrix of the graph and how the transition occurs from the sparse to the dense case in terms of the limiting spectral distribution. There hasn’t been much literature in this area, even though various specific graphs have been studied. For example, the largest eigenvalue of the sparse Chung-Lu random graph was studied in Chung et al. (2003), and this was extended to an inhomogeneous setting by Benaych-Georges et al. (2020, 2019). The bulk of the spectrum of sparse graphs is mainly studied through local weak convergence. Here, we present a unifying approach to understanding both the sparse and the dense cases, allowing us to interpolate between the two regimes.

In the case of homogeneous ERRG, it is known that in the dense case, the empirical distribution converges to the semicircle law after an appropriate scaling (Tran et al. (2013)). In the sparse case, it converges to a measure that depends on the parameter . The behaviour is much more complicated in the sparse case. Various interesting properties were predicted by Bauer and Golinelli (2001). The existence of the limiting distribution was proved by Khorunzhy et al. (2004), who also showed some interesting properties of the moments and the limiting Stieltjes transform. The local geometric behaviour of sparse random graphs can be well studied using the theory of local weak convergence (LWC), which builds on the works Aldous and Lyons (2007) and Benjamini and Schramm (2001). It roughly describes how a graph looks like in the limit around a uniformly chosen vertex. For a detailed review of LWC and various other applications, see van der Hofstad (2023). In a remarkable work by Bordenave and Lelarge (2010), it was proved that if a graph with vertices converges locally weakly to a Galton-Watson tree, then the Stieltjes transform of the empirical spectral distribution converges in to the Stieltjes transform of the spectral measure of the tree, and it satisfies a recursive distributional equation. The example of homogeneous ERRG was treated in (Bordenave and Lelarge, 2010, Example 2). The limiting measure of sparse ERRG depends on and is still very non-explicit. It was proved by Bordenave et al. (2017), Arras and Bordenave (2021) that the measure has an absolutely continuous component if and only if . The size of the atom at the origin was shown by Bordenave et al. (2011), and the nature of the atomic part of the measure was studied in the same article. The study of so-called extended states at origin was initiated in Coste and Salez (2021), and it was shown that for , there were no extended states, and for , it has extended states. All these results were conjectured in Bauer and Golinelli (2001). Most of these results on local limits show that properties are generally true for unimodular Galton Watson trees.

In the simulations of Bauer and Golinelli (2001), it is clear that when is slightly larger than 1, the limiting measure already starts taking the shape of the semicircular law. It was shown in Jung and Lee (2018) that indeed, if , then the limiting measure converges to the semicircular law. The main motivation of this work comes from the work of (Jung and Lee, 2018, Theorem 1), and we extend the results from ERRG to inhomogeneous models. We explicitly derive the moments of the limiting measure for the inhomogeneous setting, extending the works of Khorunzhy et al. (2004), albeit with a much simpler proof. The moments of the limiting measure depend on certain kinds of graph homomorphism counts, which also appeared in the works of Zhu (2020). Although the theory of local weak convergence is very useful, we do not know if it can be used to derive the moments of the limiting measure. We also study the Stieltjes transform of the limiting measure, following the idea of Khorunzhy et al. (2004), and attempt an expansion of it for large enough. This has also gained attention in the physics literature, see references in Akara-pipattana and Evnin (2023). We show that when , the limiting moments closely resemble those of the inhomogeneous ERRG, as derived in Chakrabarty et al. (2021) and also implied by the work of Zhu (2020). In Chakrabarty et al. (2021), they considered inhomogeneous ERRG to have weights , and . This result can be extended to general deterministic weights without significant effort, and we state this general result in Section 2. The limiting measure is well-known in the free probability literature and appears as a universal object in many inhomogeneous systems, referred to as the operator-valued semicircle law (Speicher, 2011, Theorem 22.7.2). The Stieltjes transform satisfies a recursive analytic equation. We derive the Stieltjes transform in the sparse setting using a fixed-point equation. The fixed point is simpler in the case of homogeneous ERRG, but in the inhomogeneous case, it becomes more complex. We explicitly characterise this fixed-point equation. We believe that in the future, this will aid in determining the rate of convergence of the empirical spectral distribution, which can be precisely quantified in terms of and . The rates of convergence in the free central limit theorem were recently explored in Banna and Mai (2023), but these results are not directly applicable to our setting. We leave this as an open problem. Obtaining an explicit rate of convergence will provide an exact explanation of why the limiting measure in the sparse setting is very close to the non-sparse setting for relatively small .

Brief summary of the results. The two main results of this work aim to characterise the limiting spectral measure of inhomogeneous Erdős-Rényi random graphs. Our first result, Theorem 2.7, gives a characterisation of the moments of this measure, where the moment for any is described in terms of homomorphism densities of the inhomogeneity function and special classes of partitions of the tuple . We can recover the moments of the dense regime asymptotically (as ) using this result. The second result Theorem 2.9 provides an analytic characterisation of the measure. In particular, we provide an analytic characterisation of a functional of the resolvent of the adjacency matrix in terms of a fixed point equation. As a consequence, in Corollaries 2.10 and 2.11, we obtain the Stieltjes transform of the sparse and dense limiting measures. The form of the limiting Stieltjes transform can be seen as an alternative description of the form obtained through local weak convergence (whenever it applies).

Outline. We begin Section 2 by describing the model and stating the results of the dense regime. We state the assumptions on the sparse setting more explicitly and proceed by stating our main results for this setting. We then describe a relationship with local weak convergence and also give some examples of popular random graph models. We show that the sparse Chung-Lu type model falls into our setting, and while the Norros-Riettu model and the Generalised Random Graph models do not directly fall into our setting, we show that asymptotically the three models have the same spectral distribution, which has a free-multiplicative part that can be seen from our main results.

In Section 3, we prove our first main result which takes a combinatorial approach, and we set up all the necessary tools used in proving the result. We identify the moments of the limiting spectral measure in terms of partitions of a tuple and graph-homomorphism densities. We provide a characterisation of the partitions and explicit expressions for the moments that are given by homomorphism densities defined based on these partitions. We further identify a leading order of the moments and a polynomial in , which was also seen for the homogeneous setting in Jung and Lee (2018).

In Section 4, we prove our second main result which in contrast has an analytic flavour. We set up the relevant analytic structures, and instead of working directly with the Stieltjes Transform, we work with a functional of the resolvent of the adjacency matrix, which was introduced in Khorunzhy et al. (2004). We borrow both fundamental and advanced tools from analysis to provide an exact analytic characterisation of the limiting spectral measure. We conclude with the Appendix as Section 5 where we state the key analytic tools we use in Section 4.

2. Setting and Main results

2.1. Model

We consider the inhomogeneous Erdős-Rényi random graph (IER) on the vertex set where edges are independently added with probability . As mentioned before we will assume that has a special form as

where is a tuning parameter such that , is a sequence of deterministic non-negative weights and is bounded and continuous. We will use to denote the law of this random graph and we will drop the subscript for notational convenience, and will be the expectation with respect to . We will always assume that is large enough and hence is small enough to make since is bounded.

Let denote the adjacency matrix of the graph , that is, the -th entry is if shares an edge with , and otherwise. So is a symmetric matrix, where any entry is distributed as Bernoulli random variable with parameter as in (1.1) and is an independent collection. Instead of studying the adjacency matrix we will study the scaled adjacency matrix. In particular, we do a CLT type scaling by the variance of the entries, that is, we study the matrix

| (2.1) |

The empirical measure which puts mass on each eigenvalue of an random matrix is called the Empirical Spectral Distribution of , and is denoted by

| (2.2) |

We are interested in studying the following object:

where are the eigenvalues of .

We are interested in the weak convergence (in probability) of the above measure and the limiting measure is called the Limiting Spectral Distribution (LSD). The limiting measure depends on the following two geometric regimes in random graphs and its properties differ in the two cases:

-

•

Dense Regime: and . The connectivity regime with falls in this regime.

-

•

Sparse Regime : and .

Dense Regime:

In literature, the dense regime is characterised by but we will not use the features of dense graphs in this article and hence by abuse of terminology we say that a graph is dense when it is not sparse. Let us now recall briefly what happens in the dense regime. The following result was proved in Chakrabarty et al. (2021) and also can be obtained from Zhu (2020).

Theorem 2.1 ( ESD in the dense case).

Consider the inhomogeneous ER graph with as in (1.1) with and . Suppose the deterministic weights satisfy the following assumption:

Let be an uniform random variable on and let . We assume that there exists a with law such that

Then there exists a measure which is compactly supported such that

Many interesting properties of this limiting measure are known. To define the moments we need a quantity which is similar to the homomorphism density of graphons. Define

| (2.3) |

where is a simple graph on vertices with the edge set , is the -fold product measure of , and . If we restrict the range of to and take as the Lebesgue measure on , then this quantity is the standard graph homomorphism density (see Lovász and Szegedy (2006)).

The rooted planar tree is a planar graph with no cycles, with one distinguished vertex as a root, and with a choice of ordering at each vertex. The ordering defines a way to explore the tree starting at the root. One of the algorithms used for traversing the rooted planar trees is depth-first search. An enumeration of the vertices of a tree is said to have depth-first search order if it is the output of the depth-first search.

We now recall the definition of a Stieltjes transform of a measure on . For , where is the upper half complex plane, the Stieltjes Transform of a measure is given by

The following proposition gives the properties of the measure which appear in Theorem 2.1.

Proposition 2.2.

-

(a)

[Moments] The measure is the unique probability measure identified by the following moments:

(2.4) where is the rooted planar tree with vertices and is the Catalan number.

-

(b)

[Stieltjes transform] There exists an unique analytic function defined on such that

and satisfies the integral equation

(2.5)

Example 2.3 (Rank 1).

One special case which arises in many examples of random graphs, and will be discussed later is when has a multiplicative structure, that is, , where is a bounded continuous function. In this case, the measure

where is the standard semicircle law and is the law of and is the free multiplicative convolution of the two measures. When is identically equal to then , the standard semicircle law. We refer to Chakrabarty et al. (2021, Theorem 1.3) for details.

Sparse regime.

The seminal work of Bordenave and Lelarge (2010) characterises the limiting spectral distribution for locally tree-like graphs. In particular, if one takes to be the scaled adjacency matrix as given in (2.1), they show that if the sequence of random graphs have a weak limit , and for any uniformly chosen root , its degree sequence is uniformly integrable, then there exists a unique probability measure on such that weakly in probability. Furthermore, it is shown that when , the measure represents the expected spectral measure associated with the root of a Galton-Watson tree with an offspring distribution of and weights . This result comes from the theory of local weak convergence, also known as Benjamini-Schramm convergence (see van der Hofstad (2023), Benjamini and Schramm (2001)), which is a powerful tool to study spectral measures associated with many sparse random graph models.

In particular, consider the space of holomorphic functions , equipped with the topology induced by uniform convergence on compact sets. Then, this is a complete separable metrizable compact space. The resolvent of the adjacency operator is given as

for each . The map is in , and the Stieltjes transform of is given by , where denotes the normalised trace operator. Let denote the set of rooted isomorphism classes of rooted connected locally finite graphs. Assume that the random graph sequence has the random local limit , and further that is a Galton Watson Tree with degree distribution , that is, a rooted random tree obtained from a Galton-Watson process with root having offspring distribution and all children having a distribution (which may or may not be the same as ).

Let denote the Stieltjes transform of the empirical measure . It was shown in Bordenave and Lelarge (2010, Theorem 2) that there exists a unique probability measure on , such that for each

where has distribution and are iid with law and independent of . Moreover

where is such that:

| (2.6) |

where are i.i.d. copies with law , and is a random variable independent of having distribution .

In Bordenave and Lelarge (2010, Example 2), we see that the sparse Erdős-Rényi random graph with falls in their setup, and in particular, is distributed as . For a general , Bordenave and Lelarge (2010, Theorem 1) still guarantees the existence of , since the graphs we will consider will have a local weak limit known as the multitype branching process (see (van der Hofstad, 2023, Chapter 3) for more details). As is bounded, we get that the degree sequence will still remain uniformly integrable. As mentioned before we will not follow this well-known route of local weak convergence. Instead, we show the above convergence through albeit classical methods. We now introduce the conditions under which we will work. We will have the following sparsity assumption on and a regularity assumption on the function and the weights:

-

A.1

Connectivity function: Let be a bounded, continuous function, with ,

-

A.2

Sparsity assumption : ,

-

A.3

Assumption on weights: Let be an uniform random variable on and let . We assume that there exists a with law such that

We make some preliminary remarks about the assumptions. Since is bounded, we can easily see that is integrable. In the sparse setting, in most important examples, the graph is locally tree-like and this can be seen from the theory of local weak convergence.

Note that the limit recovers the dense regime. By this choice, we can see that as N becomes very large, and . Thus, our matrix of interest is a scaled adjacency matrix now defined as follows:

| (2.7) |

2.2. Main Results

In this subsection, we state the main results of this article. As mentioned before in the introduction, we would like to understand first the limiting empirical distribution of the sparse inhomogeneous Erdős Rényi (IER) Random Graph and also study the behaviour of the measure when the sparsity parameter increases. Recall that the adjacency matrix is defined in (2.7) and the empirical spectral distribution is denoted by (see (2.2)). In what follows, we will see that

| (2.8) |

and where is as in Theorem 2.1. For the homogeneous case, where , we get the final limit as the classical Wigner’s semicircular law, that is, . These iterated limits were studied in Jung and Lee (2018). An interesting open question is how close is to . Although we do not manage to give an explicit estimate, through the moment method we show that it is very close and the structure of the moments of is hidden inside the structure of moments of . This will be our first result. To describe the moments we need to introduce some notation.

Method of moments: Combinatorial Approach

We first define the Special Symmetric Partitions which was introduced in Bose et al. (2022). Let denote the set of partitions of and be the set of pair partitions where each block has size . Let be the set of non-crossing partitions of and be the set of non-crossing pair partitions of . Note that and these are known as the Catalan numbers and represent the even moments of the semicircle distribution.

Partition terminology.

Let be a partition of a tuple . Let consist of disjoint blocks , for some . We arrange the blocks in the ascending order of their smallest element. For any block , a sub-block is defined to be a subset of consecutive integers in the block. Two elements and in a block are said to be successive if for all between and , .

Definition 2.1 (Special Symmetric Partition).

A partition of a tuple is said to be a Special Symmetric partition if it satisfies the following:

-

•

All blocks of are of even size.

-

•

Let be any arbitrary block, and let be two successive elements in with . Then, either of the following is true:

-

1.

, or

-

2.

between and there are sub-blocks of even size.

In other words, there exist elements , , , with and , such that are even.

-

1.

We denote the class of Special Symmetric partitions as . Note that for odd, . For example, take . Note here that between and in the first block, there are no elements from the other blocks, and between and , there is the sub-block that is of even size.

In Bose et al. (2022) a more elaborate definition was given and this is useful in computations. Later, it was shown by (Pernici, 2021, Section 3) that the definition in Bose et al. (2022) is equivalent to the above one. In Pernici (2021), the set is denoted by , a special subclass of -divisible partitions.

Remark 2.2.

We note down some important properties of :

-

1.

If is even, then

-

2.

for . When , there are partitions that are either crossing or non-paired. For example, for , is a Special Symmetric partition. In particular, crossings start appearing when there are at least two or more blocks in a partition having 4 or more elements.

- 3.

Any partition can be realized as a permutation of , that is, a mapping from . Let denote the set of permutations on elements. Let be the shift by modulo . We will be interested in the compositions of the two permutations and , denoted by , and this will be seen below as a partition.

Definition 2.3 (Graph associated to a partition).

For a fixed , let denote the cyclic permutation . For a partition , we define as a rooted, labelled graph associated with any partition of , constructed as follows.

-

•

Initially consider the vertex set and perform a closed walk on as and with each step of the walk, add an edge.

-

•

Evaluate , which will be of the form for some where are disjoint blocks. Then, collapse vertices in to a single vertex if they belong to the same block in , and collapse the corresponding edges. Thus, .

-

•

Finally root and label the graph as follows.

-

–

Root: We always assume that the first element of the closed walk (in this case ‘1’) is in , and we fix the block as the root.

-

–

Label: Each vertex gets labelled with the elements belonging to the corresponding block in .

-

–

Remark 2.4.

While is a partition and is a permutation, we do a composition in the permutation sense. We read the partition as a permutation, compose it with the permutation , and finally read as a partition. As an example, consider and . To compute , we read as , and compute . We finally read as .

Example 2.5.

Consider for example partitions of and reading the partitions as permutations and evaluating their composition with gives us:

-

(1)

-

(2)

-

(3)

-

(1)

,

-

(2)

,

-

(3)

.

The corresponding graphs and are as follows:

One can see that structurally the three graphs are the same. However, if we root them on , then the first two graphs are different from the third. Further, if we label the vertices as shown, all three graphs become distinct.

Example 2.6.

Here, we illustrate the type of graph structures that can occur for . Consider , and the following three partitions.

-

(1)

.

-

(2)

.

-

(3)

.

-

(1)

,

-

(2)

,

-

(3)

.

Then, but . Moreover, is non-crossing whereas has 2 crossings. The corresponding graphs are as below.

The following result is the first main result of the article. This is an extension of the results obtained recently in Bose et al. (2022) and the homogeneous case obtained in Jung and Lee (2018).

Theorem 2.7 (Identification of moments).

(a) Let be the adjacency matrix of the sparse IER random graph as defined in (2.7) satisfying assumptions A.1–A.3. Then there exists a deterministic measure such that

Moreover, is uniquely determined by its moments, which are given as follows:

| (2.9) |

where is the set of all Special Symmetric partitions of as defined in Definition 2.1, is the graph associated to a partition as defined in Definition 2.3, and is the homomorphism density as in (2.3).

Remark 2.8.

Note that limiting second moment is given by where and . Hence is the graph with vertices and edge. Therefore

Stieltjes transform: Analytic approach.

It is well-known that can be characterised by its Stieltjes transform, which, in turn, can be characterised by a random recursive equation. Local weak convergence is a powerful tool for studying the Stieltjes transform of spectral measures associated with sparse random graphs. However, it becomes challenging to provide accurate estimates on the Stieltjes transform to study local laws and extreme values. Therefore, we present an alternative approach to studying the Stieltjes transform of the spectral measure of IER graphs. The ideas used here originate from the works of Khorunzhy et al. (2004).

We denote the upper half complex plane by

For an analytic approach to the problem, we analyse the resolvent of this matrix, defined as

The Stieltjes transform of the empirical spectral distribution of is given by

where denotes the normalized trace. To get more refined estimates we need an additional assumption on the connectivity function:

-

A.4

is symmetric and bounded by a constant . Moreover, is Lipschitz in one coordinate, that is, for all ,

where is the Lipschitz constant for .

To state the result we will need a Banach space of analytic functions. Consider the space defined by

| (2.10) |

and take the norm

Then, is a Banach space. We defer the proof of this in Proposition 5.1 in the appendix.

Consider the function given by

| (2.11) |

where , the diagonal element of the resolvent of . It turns out that

and hence one can derive a form of the limiting Stieltjes transform.

Theorem 2.9 (Analytic functional of the resolvent).

Let be the adjacency of the IER random graph as defined in (2.7) and satisfying assumptions (A.2)–(A.4). Further, consider as defined in (2.11). Define the function as

| (2.12) |

Then, for there exists a function such that for each and uniformly in we have

| (2.13) |

and

Here, is a unique analytic solution (in the space ) for the fixed point equation:

| (2.14) |

where is the Bessel function of the first order of the first kind defined as

| (2.15) |

Observe that there is a slight difference in the right-hand sides of (2.13) and (2.14) but in the case both are the same. The next corollary describes the convergence of the Stieltjes transform.

Corollary 2.10 (Identification of the Stieltjes Transform).

Under the assumptions of the above theorem, we have that any ,

where is as in Theorem 2.7. The satisfies the following equation:

| (2.16) |

To recover the dense regime, we study the asymptotic as in the next corollary.

Corollary 2.11 (Stieltjes Transform as ).

For , we have that

| (2.17) |

for each , where satisfies an integral equation given by

| (2.18) |

where satisfies the dependent fixed point equation (2.5).

Remark 2.12 ( and the Stieltjes Transform in the homogeneous setting).

In the case when , we recover the homogeneous setting. We know satisfies the fixed point equation (2.14). If we substitute in (2.14) we get

We see that the right-hand side has no dependency on the parameter , and so, we have a unique analytical functional that satisfies the fixed point equation

| (2.19) |

This matches the result of Khorunzhy et al. (2004).

2.3. Examples

We now list out a few examples of the model that can be approached by our methods.

Example 1: Homogeneous Erdős-Rényi Random Graph.

When we have , the model reduces to the standard homogeneous Erdős-Rényi graph with edge probability . As discussed, in this case the moments of can be computed. In particular, we have for all . Hence we have

Since the (even) moments of the semicircle law are given by the Catalan numbers, it is immediate that

Hence Theorem 2.7(b) is true in this special case. It is known that has an absolutely continuous spectrum when (see Bordenave et al. (2017), Arras and Bordenave (2021)). In this case, the Stieltjes transform is given by

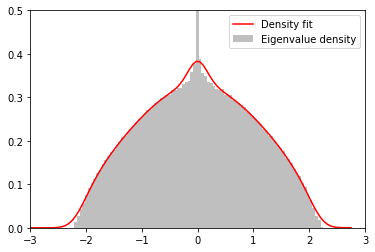

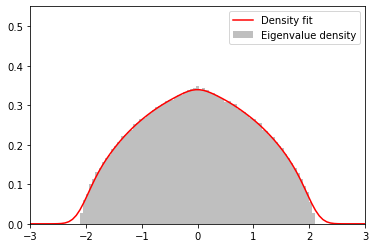

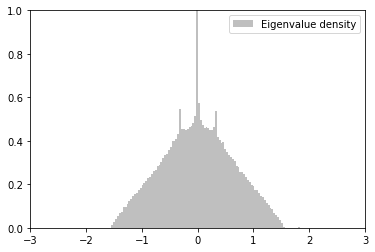

and satisfies the equation (2.19). What is interesting and cannot be immediately derived from our results is the rate of convergence of the measure to as becomes large. In the simulation below we consider the and the simulation already suggests the appearance of semicircle law. We believe the representation above of the Stieltjes transform as in Corollary 2.10 can be used to prove the rate of convergence as done in the classical Wigner case in Bai (2008).

Example 2: Chung-Lu Random Graph:

Let be a graphical sequence and denote by and , the total and the maximum degree, respectively. Let be defined on as

and

We can choose an appropriate degree sequence such that and . The connection probabilities will be given by

Let be a uniformly chosen vertex and be the degree of this vertex. We assume that

where has law which is compactly supported. Then the conditions of Theorem 2.7 are satisfied. Hence there exists a limiting spectral distribution which we call and the even moments can identified in the following way.

Let be the set of Special Symmetric partitions with blocks. Then,

where denotes the size of the blocks of a partition . For , its Kreweras complement is the maximal non-crossing partition of , such that is a non-crossing partition of . For example,

Note that this slightly differs from the standard notation of Kreweras complement in Nica and Speicher (2006) but for pairings, the and coincide. It follows easily that when , can be replaced by . The benefit of this representation is the following. It follows from (Nica and Speicher, 2006, Page 228) that

where is the free multiplicative convolution of the measures and semicircle law . Hence the moments of can be written as

This also shows that

and consequently, is of the form .

Remark 2.1.

We want to add a remark about heavy-tailed degrees. Our conditions are not satisfied when the degree sequence follows a power-law distribution. In that case, the need to be scaled differently, and the limiting will not have a compact support. For further discussion on inhomogeneous random graphs with heavy tails, we refer to (van der Hofstad, 2017, Chapter 6).

Example 3: Generalized random graph:

Again let be as above. Let and . Then,

Although the above example does not directly fall in our set-up (due to lack of ), one can still derive the limiting spectral distribution using the Chung-Lu model. We will use the following two facts. The first is (Bai, 2008, Corollary A.41), and is also a corollary of the Hoffman-Wielandt inequality.

Fact 2.2.

If denotes the Lévy distance between two probability measures, then for symmetric matrices and ,

The following is a fact about the coupling of two Bernoulli random variables with parameters and (see van der Hofstad (2023, Theorem 2.9))

Fact 2.3.

There exits a coupling between and such that

Using the above coupling, we can construct a sequence of independent Bernoulli random variables and with parameters and , respectively. Let and be the adjacency matrix of Chung-Lu and Generalized random graph models respectively, with the above coupled Bernoulli random variables. Suppose the sequence satisfies the assumptions described in Example 2 and let and and . Then,

since can be trivially bounded by 1. Using for any , we have

Therefore

If we consider , then the empirical distribution functions are close. Now using Markov inequality and the fact that converges weakly in probability to it follows that

Example 4: Norros-Riettu.

Let be a given sequence and . Take . Then,

Again the form of the above connection probability does not fall directly in our set-up but we can show that Norros-Riettu model is close to the generalized random graph models. Let where is the adjacency of the Norros-Riettu model. Without loss of generality, we assume that we can couple Bernoulli random variable and with parameters and using Fact 2.3. Just as in the previous example, it follows using Fact 2.2 that

We bound trivially by a constant and hence we get that

Now,

for some constant . Therefore, for some new constant ,

| (2.20) |

where . Since has compact support, we have that and . So is bounded for large and hence the right hand side of (2.20) goes to . This shows that

Example 5: Inhomogeneous Random Graphs:

Let and be any continuous function. Then,

This is a case which falls directly into our set-up if we assume and the measure is the Lebesgue measure. The other examples considered in this section are mostly of the rank-1 type but through this example, one can achieve limiting measures which are of wide variety.

We note that in van der Hofstad (2023), inhomogeneous random graphs are introduced in a much more abstract setting, following the works of Bollobás et al. (2007). The connectivity function is generally continuous and also satisfies reducibility properties. The above examples also fall under the setup described there.

3. Method of Moments: Proof of Theorem 2.7

In this section, we will prove the main result Theorem 2.7 using the method of moments.

We begin with a small observation. Recall from Assumption A.3 that if is an uniformly chosen vertex and and we assume . This means that has a distribution function given by

and if we denote by the distribution of then for any continuity point of we have

Also for any bounded continuous function , we have . Let be i.i.d. Uniform random variables on . Let for . Then

where are independent copies of the limiting variable . Hence for any bounded continuous in -variables we have

| (3.1) |

In our model, we can allow self-loops as we are not imposing that but the presence of self-loops does not affect the . The following lemma shows that we can remove the self-loops.

Lemma 3.1 (Diagonal contribution).

Let be the matrix with zero on the diagonal, and let denote the Lévy distance. Then,

In particular, if converges weakly in probability to , then so will and visa-versa.

Proof.

Let denote the diagonal of . Then, . Using Fact 2.2 we have

Hence we have

for some constant , which comes from the fact that is bounded. The result follows using Markov’s inequality. ∎

We are now ready to begin with the proofs of the main results.

3.1. Expected Moments

We split up the proof into three parts. To ease the notation we abbreviate the empirical spectral distribution and its expectation as

| (3.2) |

Note that is now a deterministic measure, for which we compute the moments as

where denotes the normalized trace. Using the trace formula it follows that

| (3.3) |

where are entries of the adjacency matrix . We compute the expected moments and demonstrate that they are finite. Subsequently, we establish a concentration result to show that the moments of the empirical measure converge to in probability. Next, we prove that the sequence satisfies Carleman’s condition, thereby uniquely determining the limiting measure.

Let be the set of Special Symmetric partitions, and be the cyclic permutation. For the following computations, one has to read the partition as a permutation, with elements of a block in the partition set in an ascending manner in the permutation. That is, if , then the corresponding permutation is .

Lemma 3.1 (Expected moments).

Let be the of and . Let be decomposed into blocks of the form

where be the number of blocks. Define as

| (3.4) |

Then,

| (3.5) |

Example 3.2.

For , take . Then, . We see that tuples of the form and belong in .

Proof of Lemma 3.1.

Recall from (3.3) that

where . The term is associated with the closed walk . Let the set of distinct vertices and edges along a closed walk correspond to a -tuple be denoted by and , respectively. An edge that connects vertices and , will be denoted by . Without loss of generality, we assume that in we assign the positions where the first of distinct indices appear in .

For example, for the 4-tuple , we have . So, . Since

we can rewrite (3.3) as

| (3.6) |

Let be a partition of and , where . Recall the definition of as in (3.4) and also the graph corresponding to as in Definition 2.3. Note that for a fixed , and . Moreover, if , then and . Using this formulation, we can rewrite our summation in (3.6) once again as

Since , we can multiply and divide by to get

Note that since is bounded, then the product is bounded. For a fixed and a partition of , . One can also see that . We thus focus only on . For this to contribute, a tuple must yield a tree structure in , this will give us , which would imply . In particular, all tuples such that is a coloured rooted tree as defined in Definition 2.3 contribute to the summation.

For other graphs with , the leading error would be of the order . The leading order error is given when is a -cycle and hence the error is of the order of . Thus our sum reduces to

Thus rewriting the expression with we get,

| (3.7) |

Remark 3.3.

We would like to remark here that if there exists an edge , such that it is traversed only once in the closed walk, then the graph cannot be a tree. Consider, without loss of generality, that this edge is , with and , as in figure 4, where . Here and are the remaining components of the graph .

Thus, since the closed walk has to return back to , it has to do so via since the edge cannot be traversed again. Clearly, this will form a cycle in the graph. Thus, every edge must be traversed at least twice.

It is well-known (see Nica and Speicher (2006)) that for if and only if , but in the above setting we shall see that other partitions will also contribute as . In particular, we need to sum over only those that give rise to a tree structure. We show in a series of characterizations that the resulting partitions are .

Characterising partitions

Property 1.

[Block characterisation] For with , if has a tree structure, then all elements of a block , , have either all odd elements or all even elements.

Proof of Property 1.

For simplicity, we show that the first block has this property. Assume that has all odd elements except one special element . We assume that element ‘1’ belongs to .

Recall from the definition of that we first perform a closed walk on as , and then collapse elements of the same block of into a single vertex. Thus, if (or ) belong to , then, we get a self-loop since and collapse to the same vertex and the edge (or ) forms a loop, which does not give a tree structure. Hence (respectively ) is not in .

Now, suppose for some . Then, there exists a path from to of length , since if , the closed walk would imply that , which contradicts our claim. Now, if , the next edge from the closed walk will be from to , leading to a cycle in the graph. Thus, violating property 1 yields a graph that is not a tree.

∎

Property 2.

[Initial characterisation of ] If then in any block of , no two consecutive elements can either be both odd or both even.

Proof of Property 2.

Suppose and belong in the same block of with no elements between them, and , either both even or odd. Then in , and belong in the same block, which contradicts Property 1. ∎

Property 3.

[Diagonal terms] If is a contributing partition, then for any in , each element of must be pairwise distinct, that is, .

Proof of Property 3.

Suppose not, and assume for some . Then, in , ‘a’ and ‘a+1’ belong to the same block. This contradicts Property 1. ∎

We now use the above properties for further characterisation of the partitions.

Lemma 3.4.

Every block in must be of even size.

Proof of Lemma 3.4.

We prove this by contradiction. Consider an odd-sized block with . Assume that is odd. By Property 2, must be even, and by continuing the argument, we have that at every even position, the element is even, and at odd positions, it is odd. Since is odd, and is on the position, which is an odd position, must be odd. Then, in , the element will map to the element which is even, which contradicts Property 1. A similar argument holds when is taken to be even. This proves the result. ∎

Corollary 3.5 (Vanishing odd moments).

The odd moments vanish as .

Proof of Corollary 3.5.

Recall that partitions whose graphs do not yield a tree structure contribute to the error term with leading order . For odd, every must have at least one block of odd size. Therefore, Lemma 3.4 is violated, and consequently, the odd moments asymptotically. ∎

Proposition 3.6.

Let such that is a rooted labelled tree. Then must satisfy the following properties.

-

•

All blocks of the partition must be of even size.

-

•

Between any two successive elements of a block, there lie sub-blocks of even sizes.

Proof of Proposition 3.6.

The first condition is already proved using Lemma 3.4. For the second condition, begin by considering a block that is of the form

with , and there doesn’t exist any element such that and . The sub-block here of interest is . We claim that this sub-block has an odd number of elements, or equivalently, is an even number. We can also assume, without loss of generality, that is an odd number. As a consequence of Property 2, must be even. If we now evaluate using the above information, we have that contains the following three (and possibly more) blocks.

Thus, the graph associated with will be as shown in figure 5, where , , and are the remaining components of the graph.

We now focus on the closed walk that occurs on the tuple . Since this is a closed walk, it does not matter if instead of beginning at , we begin at an arbitrary element and perform . So, we pick as the starting point and consequently, without loss of generality, we assume the walk begins at .

The walk will immediately proceed to move back and forth between and due to the path , and will eventually end at .

Now, the walk will jump from into the component . On the other hand, when the walk eventually enters , it will move at least once to , due to the path . So, to preserve the tree structure, the walk must first come back to and then proceed to via . Thus, there is an element such that and , where and . Therefore, in , maps to . This implies that and belong to the same block in , and thus, . This contradicts our construction, and therefore, the walk must form a cycle from or to either , or . ∎

Recall the definition of Special Symmetric Partitions as provided in Definition 2.1, where the two properties outlined in Proposition 3.6 are the main characteristics. As a result, we have demonstrated (3.5), leading us to the conclusion of the proof of Lemma 3.1. ∎

We would now like to take limits in (3.5) and finally get the expression for the moments. The following lemma is an easy consequence of Lemma 3.1 and the fact that .

Now, going back to equation (3.7) and taking limits gives us

| (3.9) |

Now, the sum over can be further split up as the sum over and the remaining partitions. Moreover, for , we have . In particular, for , , and when is the full partition , . So, we can write

| (3.10) |

3.2. Concentration and uniqueness.

We now show a concentration result to obtain convergence in probability.

Lemma 3.1 (Concentration of trace).

For all , we have that

Proof.

We shall proceed to compute the variance

Let and denote the tuples

and denote by the expectation

Similarly, we have

For the tuple , we can define a closed walk as in the proof of Lemma 3.1 to get a graph . In the same spirit, one can define , with the closed walk now performed as

where the jump from 1 to is without an edge. Then, we can define

With this notation set up, one can see that

| (3.11) |

We remark here that the construction of the graph is similar to how we did in Lemma 3.1, with the essential difference being the closed walk structure over two separate tuples.

Suppose that . Then by independence, (3.11) becomes 0. Thus, we must have . Moreover, due to remark 3.3, each term must appear at least twice in , that is, each edge in is traversed at least twice. This implies that the maximum number of edges our graph can have is .

Next, note that the only way the graph will be disconnected is when the closed walk over the two tuples yields two disjoint graphs, and thus we once again obtain .

Thus, our computation boils down to the case where is a connected graph, with each edge appearing at least twice, and . Note that one can have to be connected and still have , for example when and are collapsed into the same vertex. This gives us that . Using gives us that

This completes the proof. ∎

An immediate consequence using Chebychev’s inequality is that the moments concentrate around their mean as . In other words, for all ,

where are as in (2.9). To conclude Theorem 2.7, we now further analyse the sequence , and show that it is unique for the measure . A measure is said to be uniquely determined by its moment sequence if the following holds (Carleman’s condition):

| (3.12) |

Lemma 3.2 (Uniqueness of moments).

For bounded away from 0, that is, , the moments uniquely determine the limiting spectral measure.

Proof.

Let denote the moment. Since is bounded, we have

Let be defined as

Then,

where the last inequality follows since and is bounded by . Thus,

So, we have the series to be lower bounded by , where

Thus,

Since , we see that the series diverges, and consequently,

∎

4. Analytic approach: Proof of Theorem 2.9

4.1. Resolvent and Stieltjes Transform

We fix a throughout this argument, with . Recall that resolvent is given by

The Stieltjes transform of the empirical spectral distribution of is given by

| (4.1) |

where denotes the normalized trace.

Lemma 4.1 (Resolvent Properties).

For any , the following properties are well-known for the resolvent of an matrix .

-

(i)

Analytic: is an analytic function on .

-

(ii)

Bounded : , where denotes the operator norm.

-

(iii)

Normal : .

-

(iv)

Diagonals are bounded:

-

(v)

Trace bounded: . In particular,

For the first three properties see (Bordenave, 2019, Chapter 3). Note that the property (iv) follows from (iii) by the following argument:

The last property (v) follows from (iv). We now state the Ward’s identity, for which we refer the reader to Erdős and Yau (2017, Lemma 8.3).

Lemma 4.2 (Ward’s identity).

Let be a Hermitian matrix and be the resolvent. Let . Then for any fixed , we have

Since we have already shown in the previous section weakly in probability and hence it follows that for any

Due to the involved structure of the moments, it is not immediately evident what the limiting Stieltjes transform looks like.

Recall the notation of expected empirical spectral distribution of from (3.2). Let denote the Stieltjes transform of . Notice that . It is known that if a measure converges weakly in probability to a measure , then the corresponding Stieltjes transforms converge. In particular, we have the following lemma.

Lemma 4.3.

(Anderson et al., 2010, Theorem 2.4.4) A sequence of measures converge weakly in probability to a measure if and only if converges in probability to for each .

Thus, we compute an expression for the expected Stieltjes transform , and using convergence in probability from Theorem 2.7, we can claim that the Stieltjes transform converges in probability to the same expression. For ease of notation we shall denote by for .

The following identity can be found in Abramowitz and Stegun (1964). For any complex number , we have for all ,

| (4.2) |

where is the first-order Bessel function of the first kind given by (2.15). Note that for all , (see (Abramowitz and Stegun, 1964, Chapter 9)). We know that resolvent maps the upper half complex plane to the upper half complex plane. Thus, we begin by fixing , the diagonal entry of the resolvent matrix, as our complex variable in . So we can get

| (4.3) |

If we look at then the relation between the Stieltjes transform and the above equation becomes apparent. It turns out that

| (4.4) |

To understand the Stieltjes transform we will first try to understand the behaviour of (4.3). We will adapt the approach of Khorunzhy et al. (2004). For ease of notation, for what follows, will denote the norm as defined in (2.10), unless stated otherwise.

Proposition 4.4.

Let denote the diagonal entry of the resolvent . Let

| (4.5) |

and for any define the function as follows

| (4.6) |

Then, for any ,

| (4.7) |

where .

We begin by stating two results we use in this proof. Note that we conveniently drop the dependence on for , since we fix throughout and hence just use the notation .

Fact 4.5 (Exponential Inequalities).

The following holds true for any real numbers and complex numbers .

| (4.8) |

| (4.9) |

Proof of Proposition 4.4.

For the resolvent of a matrix with zero diagonal, we have the relation

for any diagonal element of the resolvent , where are the entries of the resolvent of in , which is the adjacency matrix with deleted row and column. Plugging into (4.2) yields

| (4.10) |

Adding and subtracting the appropriate exponential to (4.10) yields

| (4.11) |

where is an error term given by

It is easy to see that for with and , we have . Thus,

| (4.12) | ||||

where in the last step, we use inequality (4.8) and the bound for . Note that in the last sum in (4.12), the entries and are independent of one another, and of . Thus, since is bounded by a constant , taking expectation on the summation gives us

| (4.13) |

since are distributed as Bernoulli random variables with parameter , and are scaled by a factor . Using (4.13) and taking expectation in (4.12) gives us

where in the last step we do a change of variable to show the integral is finite. So, if we now take an expectation in (4.11), we get

| (4.14) |

where . Note that the expectation could be pulled inside the integral in (4.11) using Fubini’s Theorem since the integral is bounded above by a constant. To evaluate the expectation inside (4.14), we use a conditioning argument as follows. We have

| (4.15) |

where is an error given by

Since , doing a Taylor expansion for the exponential term in gives us

| (4.16) |

We can write

| (4.17) |

where is an expression involving all the other terms of the product in (4.15). To get the order of , we take a supremum over in (4.15) and compute the binomial expansion of the form modulo the leading term . In particular, since , and again using (4.16), we have

which for some constant and large enough further simplifies to

where the last equality is due to the sum being a geometric series. Thus,

| (4.18) |

which is a faster error than so we can later absorb it into the existing error of (4.14). Thus, using (4.18), we can rewrite (4.17) as

| (4.19) |

where

| (4.20) |

Note that is a bounded function and is bounded above by . To get the error down from the exponent, we again use inequality (4.9).

To conclude the proof of the proposition, we need to return back to an expression involving terms of the form of the original resolvent. To do so, we do an interpolation argument. Let and define with the resolvent , whose entries we denote by , that also implicitly depends on but we drop that for convenience of notation. Also, define

We remark using property (i) from Lemma 4.1 that is also bounded above by for all values of , since the complex exponential is bounded by 1 for any and . In particular, we have that for all .

Our target function is . By the fundamental theorem of calculus,

Now, and thus, .

Note that , where is given by

Thus,

| (4.21) |

since the complex exponential is trivially bounded by 1 as . Then, using Cauchy-Schwarz and Lemma 4.2 in (4.21), we have

Bounding by (property (iv) of Lemma 4.1) and taking expectation, we get

| (4.22) |

Now, again using Cauchy-Schwarz and Lemma 4.2, we have for some constant that

| (4.23) |

Thus, using (4.23) and Jensen’s inequality on the function in (4.22), we get

Since is bounded, we have for some new constant that

Using the fact that is bounded by for all , we get

Since this is an error of the same order as , we can absorb it into the existing error . Finally, using (4.19) and the interpolation argument allows us to write (4.14) as

which proves the proposition. ∎

Now, consider the expression (4.7) from the Proposition 4.4. If we multiply throughout by and then sum over , and finally scale by , we get

| (4.24) | ||||

Consider the space of Lipschitz functions defined as

Now, under the bounded Lipshitz metric given by

we have

where for a uniformly chosen vertex . So, taking to be Lipschitz in one coordinate (and since we already have that is bounded), the first term in the RHS of (4.24) becomes

| (4.25) |

where .

Recall from (2.12) that we have

Then, one simply gets

| (4.26) |

Thus, using (4.25) and (4.26) in (4.7) gives us

| (4.27) | ||||

where

Finally, for a fixed , define

Then, we have the following lemma.

Lemma 4.6.

is Lipschitz.

Proof.

Consider as defined. Then,

| (4.28) |

Recall that a function is Lipschitz if and only if it has a bounded derivative. Thus, if is Lipschitz in , the first term in (4.28) uniformly bounded in . Moreover, this makes the second term in (4.28) bounded as well since

| (4.29) |

is bounded. To justify interchanging the derivative and the integral in (4.29), we have to utilise Theorem 5.2 for which we need to verify the following conditions.

-

•

is integrable for each and the map is continuous for each .

-

•

For each , the derivative exists.

-

•

For each , there is a integrable function and a neighbourhood containing , such that for all , .

The first and second are trivial to check, and by Lipschitz property, since , we have , which is integrable on since is a probability measure.

Finally, for notational convenience, let be denote

Once again, we need to verify the three conditions as above so as to apply Theorem 5.2. Note that is integrable with respect to . Moreover,

where one can compute

which again is bounded. Thus, exists, and is bounded above by , which is integrable with respect to . This verifies the three conditions and allows us to pull the derivative inside the third term in (4.28), and also makes that term bounded. Thus, is Lipschitz. ∎

Since is Lipschitz, we can exploit the weak convergence of under the Lipschitz metric in (4.27) to give us

| (4.30) |

Recall the Banach space as defined in (2.10), and consider . In this space, consider the map

| (4.31) |

Note that also implicitly depends on but we drop that for notational purposes since we fix throughout.

Take such that . Then, using the norm we defined in (2.10) and inequality 4.9, from (4.31) we get

where is the constant upper bound to the integral of the form

which is finite. Taking sufficiently large, we get that is a contraction in an open ball of radius , and thus, by the Banach Fixed Point Theorem, there exists a unique such that for .

We are now ready to prove a concentration result. Recall the function defined in (2.11) as

If we now define a new function that acts identically on the first coordinate as

then one can see that , and so , and consequently, a concentration result for would imply concentration for .

Proposition 4.7 (Concentration and convergence).

For any and , and uniformly over in , we have . Further, we have

Proof of Proposition 4.7.

Let denote the error

Let and consider the covariance

Using (4.11) for the first term and Proposition 4.4 for the second term, we get

| (4.32) | ||||

where and are the RHS of equations (4.11) and (4.7) respectively, and differ by the error in expectation. In the first double integral of (4.32), one can do the interpolation argument term-wise, and obtain the error by making a difference with the second double integral in (4.32), where is the constant upper bound to for any . Thus, we have that

| (4.33) |

Using inequality 4.9 on gives us

since and . We can now bound this by using the definition of to get

| (4.34) |

Since is deterministic, we can pull it out of the expectation and take it common, giving us

We can conclude using triangle inequality that

| (4.35) |

For sufficiently large, taking the norm, we get

| (4.36) |

However, is a bounded analytic function in . Using the identity theorem from complex analysis , which states that if two holomorphic functions agree in an open set of the domain then they must agree everywhere on the domain, we have that since on an open set of the upper-half complex plane, it must approach 0 everywhere on the upper-half plane. Since the error in (4.35) can be absorbed in , using 4.9 gives us

| (4.37) |

where the error vanishes in the norm as

Now, consider the function and the error

By definition of , one can see that expanding will yield an expression similar to (4.34) modulo , and so, using (4.33) again, we get that

By taking the norm and again using identity theorem, we get that vanishes in and thus

| (4.38) |

A quick inspection of (4.34) shows that in fact we also have the concentration for , since the RHS is precisely the upper bound on

and so,

| (4.39) |

Finally, comparing (4.37) with the contraction mapping (4.31), we have the following:

So, with large enough and being a contraction on of radius , we have

and consequently,

Thus, since ,

As a quick remark, notice that

| (4.40) |

since is bounded.

Now, since is an analytic function on , we have is an analytic function. Again from the identity theorem of complex analysis, since and are analytic and agree on an open set of , they agree everywhere in the complex domain , and thus the convergence holds for any . Note that for a fixed , although both the functionals and live in , the domain of is since has the domain . Now, for each , fixing in the compact set gives us that for each and uniformly over ,

| (4.41) |

∎

We can now prove Theorem 2.9.

Proof of Theorem 2.9.

Equation (4.38) proves the concentration statement of Theorem 2.9. Recall that we had shown that

and so,

| (4.42) |

Next, we see that the function

is Lipschitz by using an argument similar to Lemma 4.6. Thus, we get

Since from Proposition 4.7 we have concentration for , using inequality (4.9) we have that

Finally, taking the limit gives us

| (4.43) |

completing the proof of Theorem 2.9. ∎

4.2. Deriving the expression for the Stieltjes Transform

Since we took to be in , we can take a derivative with respect to and evaluate it at . Recall from equation (4.42) that we have

Note that by definition, is a bounded function, and thus by DCT, limit operations can be interchanged with expectation. We would like to take a derivative with respect to and evaluate at to extract out from the LHS of (4.42). On the other hand, we would first like to take for the RHS to remove the error term. To interchange these operations, we have the following result.

Proposition 4.1.

Both the limits and exist and are equal.

Proof.

We fix a . Now, exists due to the RHS of (4.42), which we denote by . If we define and as

Then,

We would like to claim

Thus, we want to interchange the order of limits. Note that

uniformly in , and

for each , where the limit can be taken inside the expectation using dominated convergence. Thus, using Rudin (1976, Theorem 7.11), we have that the limits and exist and are equal. ∎

We are now ready to prove Corollary 2.10.

Proof of Corollary 2.10.

We now do precisely as we stated before Proposition 4.1. We evaluate the derivative at and then take on the LHS of (4.42), and we do the reverse for the RHS of (4.42). Note that since in probability, and also as for all . Thus, we then obtain using Proposition 4.1

| (4.44) | ||||

We now wish to evaluate the derivative on the RHS of (4.44). Let denote

| (4.45) |

Observe that

| (4.46) |

for by a change of variables. If we expand the Bessel function as defined in (2.15) in equation (4.45) and take the absolute value, we observe using (4.46) and using (from (4.40)), that we can use Fubini’s Theorem to interchange the integral with the summand. Thus, we have

Denote by the integral

Therefore,

| (4.47) |

where denotes

Note that for any , we have that is finite since

Since and by (4.47) it follows that

| (4.48) |

Therefore we would like to evaluate . Note that , as is bounded by 1. Note that the series

converges, and consequently by the dominated convergence theorem, we have

Thus by (4.48) we have

Therefore we get

To conclude the argument, we use Lemma 4.3 with Theorem 2.7 to state that converges in probability to for each . ∎

We conclude with the proof of Corollary 2.11

Proof of Corollary 2.11.

From Corollary 2.10, we have

Recall that

| (4.49) |

is the unique analytical solution of the fixed point equation as in (4.31). Expanding the Bessel function in (4.49) using (2.15) gives

| (4.50) |

We would like to interchange the summand and integral with respect to in (4.50). Using the for some and , we have that

Thus, by Fubini’s Theorem, we can interchange the summand with the integral with respect to , giving us

| (4.51) |

Now, denote by the function

| (4.52) |

Then, by Corollary 2.10, we can see that . From (4.51) we get that

and so, we can write

| (4.53) |

where

| (4.54) |

Substituting for in (4.53) and multiplying throughout by , we have

We begin by claiming the following:

Claim 4.2.

For any , we have

| (4.55) |

Then, one can see that

and so for each

Thus, from (4.53), for any we have

| (4.56) |

What remains now is to justify Claim 4.2, and taking the limit inside the integral in (4.56).

First we consider the homogeneous case when . Recall from Remark 2.12, that due to the lack of dependency of one coordinate, we denote Then,

and from (4.56) we have . Moreover, from Corollary 2.10, we have

Since , from (4.40) we have that and . Then, , justifying Claim 4.2. Thus, the expression inside the integral is uniformly bounded by . Using dominated convergence, we can pull the limit inside the integral to obtain

which is precisely the Stieltjes transform of the semicircular law.

In the case of general , recall from (4.41) that for any and ,

Now, for any , by trivially bounding the complex exponential by 1 for any , we have that

Thus, by triangle inequality, we have that

Thus, we have that

| (4.57) |

Taking on both sides in (4.2) yields that

Using this, we conclude that

| (4.58) |

for any and , proving Claim 4.2. Now, to evaluate , we take the limit inside the integral in the RHS of (2.16) using DCT, which we can use from (4.58). This gives us

and so, using (4.56), we get

| (4.59) |

Recall from (4.52) that

Again using (4.58), we have that the integral is bounded in absolute value, and so, using DCT allows us to define

where . Moreover, since is bounded by a constant, and is a probability measure, we use DCT once again to take the limit inside . Thus, we obtain

The proof follows by observing that satisfies the analytic equation defined in (2.5). ∎

![[Uncaptioned image]](/html/2312.02805/assets/EUlogo.jpeg)

The work of L.A., R.S.H. and N.M. is supported in part by the Netherlands Organisation for Scientific Research (NWO) through the Gravitation NETWORKS grant 024.002.003. The work of N.M. is further supported by the European Union’s Horizon 2020 research and innovation programme under the Marie Skłodowska-Curie grant agreement no. 945045.

References

- Abramowitz and Stegun (1964) M. Abramowitz and I. A. Stegun. Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. Dover, New York, ninth dover printing, tenth gpo printing edition, 1964.

- Akara-pipattana and Evnin (2023) P. Akara-pipattana and O. Evnin. Random matrices with row constraints and eigenvalue distributions of graph laplacians. Journal of Physics A: Mathematical and Theoretical, 2023. URL http://iopscience.iop.org/article/10.1088/1751-8121/acdcd3.

- Aldous and Lyons (2007) D. Aldous and R. Lyons. Processes on unimodular random networks. Electron. J. Probab., 12:no. 54, 1454–1508, 2007. ISSN 1083-6489. doi: 10.1214/EJP.v12-463. URL https://doi.org/10.1214/EJP.v12-463.

- Anderson et al. (2010) G. W. Anderson, A. Guionnet, and O. Zeitouni. An introduction to random matrices, volume 118. Cambridge university press, 2010.

- Arras and Bordenave (2021) A. Arras and C. Bordenave. Existence of absolutely continuous spectrum for Galton-Watson random trees. arXiv preprint arXiv:2105.10177, 2021.

- Bai (2008) Z. D. Bai. Methodologies in spectral analysis of large dimensional random matrices, a review. In Advances In Statistics, pages 174–240. World Scientific, 2008.

- Banna and Mai (2023) M. Banna and T. Mai. Berry-Esseen bounds for the multivariate -free CLT and operator-valued matrices. Trans. Amer. Math. Soc., 376(6):3761–3818, 2023. ISSN 0002-9947. doi: 10.1090/tran/8717. URL https://doi.org/10.1090/tran/8717.

- Bauer and Golinelli (2001) M. Bauer and O. Golinelli. Random incidence matrices: moments of the spectral density. J. Statist. Phys., 103(1-2):301–337, 2001. ISSN 0022-4715. doi: 10.1023/A:1004879905284. URL https://doi.org/10.1023/A:1004879905284.

- Benaych-Georges et al. (2019) F. Benaych-Georges, C. Bordenave, and A. Knowles. Largest eigenvalues of sparse inhomogeneous erdős–rényi graphs. The Annals of Probability, 47(3):1653–1676, 2019.

- Benaych-Georges et al. (2020) F. Benaych-Georges, C. Bordenave, and A. Knowles. Spectral radii of sparse random matrices. Ann. Inst. Henri Poincaré Probab. Stat., 56(3):2141–2161, 2020. ISSN 0246-0203,1778-7017. doi: 10.1214/19-AIHP1033. URL https://doi.org/10.1214/19-AIHP1033.

- Benjamini and Schramm (2001) I. Benjamini and O. Schramm. Recurrence of distributional limits of finite planar graphs. Electron. J. Probab., 6:no. 23, 13, 2001. ISSN 1083-6489. doi: 10.1214/EJP.v6-96. URL https://doi.org/10.1214/EJP.v6-96.

- Bet et al. (2023) G. Bet, K. Bogerd, and V. Jacquier. First-order asymptotics for the structure of the inhomogeneous random graph. arXiv preprint arXiv:2306.06396, 2023.

- Bhamidi et al. (2010) S. Bhamidi, R. Van Der Hofstad, and J. S. van Leeuwaarden. Scaling limits for critical inhomogeneous random graphs with finite third moments. Electronic Journal of Probability, 15:1682–1702, 2010.

- Billingsley (2012) P. Billingsley. Probability and measure. Wiley Series in Probability and Statistics. John Wiley & Sons, Inc., Hoboken, NJ, anniversary edition, 2012. ISBN 978-1-118-12237-2. With a foreword by Steve Lalley and a brief biography of Billingsley by Steve Koppes.

- Bollobás et al. (2007) B. Bollobás, S. Janson, and O. Riordan. The phase transition in inhomogeneous random graphs. Random Structures & Algorithms, 31(1):3–122, 2007.

- Bordenave (2019) C. Bordenave. Lecture notes on random matrix theory. IMPA, 2019.

- Bordenave and Lelarge (2010) C. Bordenave and M. Lelarge. Resolvent of large random graphs. Random Structures Algorithms, 37(3):332–352, 2010. ISSN 1042-9832. doi: 10.1002/rsa.20313. URL https://doi.org/10.1002/rsa.20313.

- Bordenave et al. (2011) C. Bordenave, M. Lelarge, and J. Salez. The rank of diluted random graphs. Ann. Probab., 39(3):1097–1121, 2011. ISSN 0091-1798. doi: 10.1214/10-AOP567. URL https://doi.org/10.1214/10-AOP567.

- Bordenave et al. (2017) C. Bordenave, A. Sen, and B. Virág. Mean quantum percolation. J. Eur. Math. Soc. (JEMS), 19(12):3679–3707, 2017. ISSN 1435-9855. doi: 10.4171/JEMS/750. URL https://doi.org/10.4171/JEMS/750.

- Bose et al. (2022) A. Bose, K. Saha, A. Sen, and P. Sen. Random matrices with independent entries: beyond non-crossing partitions. Random Matrices Theory Appl., 11(2):Paper No. 2250021, 42, 2022. ISSN 2010-3263,2010-3271. doi: 10.1142/S2010326322500216. URL https://doi.org/10.1142/S2010326322500216.

- Broutin et al. (2021) N. Broutin, T. Duquesne, and M. Wang. Limits of multiplicative inhomogeneous random graphs and lévy trees: Limit theorems. Probability Theory and Related Fields, 181:865–973, 2021.

- Chakrabarty et al. (2021) A. Chakrabarty, R. S. Hazra, F. den Hollander, and M. Sfragara. Spectra of adjacency and Laplacian matrices of inhomogeneous Erdős-Rényi random graphs. Random Matrices Theory Appl., 10(1):Paper No. 2150009, 34, 2021. ISSN 2010-3263. doi: 10.1142/S201032632150009X. URL https://doi.org/10.1142/S201032632150009X.

- Chung et al. (2003) F. Chung, L. Lu, and V. Vu. Eigenvalues of random power law graphs. Annals of Combinatorics, 7(1):21–33, 2003.

- Coste and Salez (2021) S. Coste and J. Salez. Emergence of extended states at zero in the spectrum of sparse random graphs. Ann. Probab., 49(4):2012–2030, 2021. ISSN 0091-1798. doi: 10.1214/20-aop1499. URL https://doi.org/10.1214/20-aop1499.

- Devroye and Fraiman (2014) L. Devroye and N. Fraiman. Connectivity of inhomogeneous random graphs. Random Structures & Algorithms, 45(3):408–420, 2014.

- Erdős and Yau (2017) L. Erdős and H.-T. Yau. A dynamical approach to random matrix theory, volume 28 of Courant Lecture Notes in Mathematics. Courant Institute of Mathematical Sciences, New York; American Mathematical Society, Providence, RI, 2017. ISBN 978-1-4704-3648-3.

- Jung and Lee (2018) P. Jung and J. Lee. Delocalization and limiting spectral distribution of Erdős-Rényi graphs with constant expected degree. Electron. Commun. Probab., 23:Paper No. 92, 13, 2018. doi: 10.1214/18-ECP198. URL https://doi.org/10.1214/18-ECP198.

- Khorunzhy et al. (2004) O. Khorunzhy, M. Shcherbina, and V. Vengerovsky. Eigenvalue distribution of large weighted random graphs. J. Math. Phys., 45(4):1648–1672, 2004. ISSN 0022-2488. doi: 10.1063/1.1667610. URL https://doi.org/10.1063/1.1667610.

- Lovász and Szegedy (2006) L. Lovász and B. Szegedy. Limits of dense graph sequences. Journal of Combinatorial Theory, Series B, 96(6):933–957, 2006.

- Nica and Speicher (2006) A. Nica and R. Speicher. Lectures on the combinatorics of free probability, volume 13. Cambridge University Press, 2006.

- Pernici (2021) M. Pernici. Noncrossing partition flow and random matrix models. arXiv preprint arXiv:2106.02655, 2021.

- Rudin (1976) W. Rudin. Principles of mathematical analysis. McGraw-Hill Book Co., New York-Auckland-Düsseldorf,,, third edition, 1976.

- Speicher (2011) R. Speicher. Free probability theory. In The Oxford handbook of random matrix theory, pages 452–470. Oxford Univ. Press, Oxford, 2011.

- Tran et al. (2013) L. V. Tran, V. H. Vu, and K. Wang. Sparse random graphs: Eigenvalues and eigenvectors. Random Structures & Algorithms, 42(1):110–134, 2013.

- van der Hofstad (2013) R. van der Hofstad. Critical behavior in inhomogeneous random graphs. Random Structures & Algorithms, 42(4):480–508, 2013.

- van der Hofstad (2017) R. van der Hofstad. Random graphs and complex networks. Vol. 1, volume [43] of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge, 2017. ISBN 978-1-107-17287-6. doi: 10.1017/9781316779422. URL https://doi.org/10.1017/9781316779422.

- van der Hofstad (2023) R. van der Hofstad. Random graphs and complex networks- vol. ii. Available on http://www. win. tue. nl/rhofstad/NotesRGCN.pdf, 11:60, 2023.

- Zhu (2020) Y. Zhu. A graphon approach to limiting spectral distributions of Wigner-type matrices. Random Structures & Algorithms, 56(1):251–279, 2020.

5. Appendix

Proposition 5.1 (Banach Space).

Let and consider the space defined by

and consider the norm

Then, is a Banach space.

Proof of Proposition 5.1.

For ease of notation, throughout this argument, . Clearly is a norm, and thus, is a normed vector space.

Let be a Cauchy sequence in . Thus, for all , there is an such that for all ,

Let be the Lebesgue measure on . Define

Then, . Let and . Then, , and

So, for all , we have an such that for all and ,

Let . Then, we have for all and

In other words, for all , denoting gives us that is a Cauchy sequence in the metric space . Since is a complete metric space, for all , there exists a limit , that is, for all , there exists a such that

For with , . This is a well-defined limit. Note that since lives in , lives in , and we thus conclude that

Passing the limit through , we have

For all , define

One can see that . Use triangle inequality to conclude ∎

For the next theorem, we refer the reader to Billingsley (2012, Theorem 16.8).

Theorem 5.2 (Interchanging derivative and integral).

Consider the measure space and an open set . Let be such that for each , is integrable, and moreover for a.e. , is continuous. Consider the function defined by

Suppose that for each the partial derivative of with respect to exists. Then, if for every , there is a nonnegative integrable function and a neighbourhood containing such that for all , , then, is continuously differentiable and