Bootstrap Prediction Inference of Non-linear Autoregressive Models

Abstract

The non-linear autoregressive (NLAR) model plays an important role in modeling and predicting time series. One-step ahead prediction is straightforward using the NLAR model, but the multi-step ahead prediction is cumbersome. For instance, iterating the one-step ahead predictor is a convenient strategy for linear autoregressive (LAR) models, but it is suboptimal under NLAR. In this paper, we first propose a simulation and/or bootstrap algorithm to construct optimal point predictors under an or loss criterion. In addition, we construct bootstrap prediction intervals in the multi-step ahead prediction problem; in particular, we develop an asymptotically valid quantile prediction interval as well as a pertinent prediction interval for future values. In order to correct the undercoverage of prediction intervals with finite samples, we further employ predictive—as opposed to fitted—residuals in the bootstrap process. Simulation studies are also given to substantiate the finite sample performance of our methods.

1 Introduction

In the domain of time series analysis, accurate forecasting based on observed data is an important topic. Such single- or multi-step ahead predictions play an important role in forecasting crop yields, stock prices, traffic volume, etc. For Linear Autoregressive (LAR) models with finite order and independent, identically distributed (i.i.d.) innovations, it is easy to construct the optimal (with respect to risk) multi-step ahead predictor by iterating the one-step ahead predictor.

Actually, the optimal prediction of linear time series models does not dependent on the distribution of innovations beyond its first two moments (Guo et al.,, 1999). The only things that matter are the historical observations and the parameters of the model. When the parameters are unknown, practitioners can apply the Box-Jenkins method of identifying, fitting, checking and predicting LAR models systematically (Box et al.,, 2015). However, the LAR model may not be enough to analyze complicated data in the real world. As pointed out by the work of De Gooijer and Kumar, (1992) and Tjøstheim, (1994), there are various occasions when prior knowledge indicates the data-generating process is in a non-linear form; see the review of Politis, (2009) for example. Furthermore, there are several ways to test the hypothesis of linearity of the data at hand; see the work of Berg et al., (2012) for traditional and bootstrap/subsampling approaches.

The analysis of Non-linear Autoregressive (NLAR) models can be traced back to the work of Jones and Cox, (1978). Putting aside the issue of identifying and estimating an NLAR model, a major application of NLAR models is forecasting future values. Although the one-step ahead optimal (with respect to risk) prediction of (causal) NLAR models is usually easy to obtain, the optimal (no matter in or loss) multi-step ahead prediction can not be obtained by the iterative procedure we employ for LAR models, even when the NLAR model parameters are known. To resolve this issue, Pemberton, (1987) proposed a numerical integration approach to get the exact solution. However, his approach assumes that the distribution of innovation is known, which is usually not realistic in the real world. Besides, this numerical approach can be very computationally heavy for long-horizon predictions. Instead, some suboptimal ideas were proposed, such as estimating a model by minimizing multi-step ahead mean squared errors and then making predictions directly; see the work of Zhang et al., (1998) and Lee and Billings, (2003) for a discussion.

The work of Guo et al., (1999) further shed some light on the multi-step ahead prediction of NLAR models. Taking advantage of the true innovation distribution or the empirical residual distribution, they propose an analytic predictor which asymptotically converges to the optimal predictor. Nevertheless, their analyses are limited to the optimal point prediction and are lacking details when the model is unknown. In several applied areas, e.g. econometrics, climate modeling, water resources management, etc., data might not possess a finite 2nd moment in which case optimizing loss is vacuous. For example, financial returns typically do not possess a finite 4th moment; hence, to predict their volatility (which is a 2nd moment), we can not rely on optimal prediction. For all such cases—but also of independent interest—prediction that is optimal with respect to loss should receive more attention in practice; see detailed discussions from Ch. 10 of Politis, (2015).

Unfortunately, the aforementioned numerical integration and analytic methods for NLAR prediction can not be extended to optimal prediction directly. In addition, even for linear autoregressions, the multi-step ahead optimal predictor is elusive since iterating the one-step ahead predictor does not work in the loss setup. Furthermore, we should also be concerned about the accuracy of our point predictions. In analogy to the construction of Confidence Intervals (CI) in estimation problems, we may attempt to measure the accuracy of point predictions by constructing Prediction Intervals (PI); see the formal definition of such measures in Section 2.

In the paper at hand, we provide an algorithm to make prediction inferences for a general class of NLAR models. Then, we focus on analyzing a popular type of NLAR model with a specific structural form that contains the separate parametric mean and volatility/variance functions. When the model and innovation distribution are known, we can deploy Monte Carlo (MC) simulation to achieve consistent forecasting. When the model is unknown—which is typically the case—we need to fit the model to get estimated parameters and innovation distribution111Throughout, we assume that the order of the parametric non-linear time series model is known; when we say the model is unknown, we mean that the corresponding parameter values of this model are unknown.. Performing MC simulation using the fitted model and estimated innovation distribution effectively becomes a bootstrap method.

Although the one-step ahead bootstrap optimal predictors and PI for NLAR models were constructed in Politis, (2015); Pan and Politis, (2016), the methodology for multi-step ahead prediction inference was left open. The challenge for this task is that we must handle the effects of future innovations on predictions appropriately since they play a crucial role due to the non-linearity. In short, our idea is to derive the expression of the multi-step ahead future value by the true/estimated model first and then attempt to approximate this cumbersome expression through simulation/bootstrap so that we can capture the (conditional) distribution of future values.

The bootstrap idea was introduced by Efron, (1979) to carry out statistical inference for independent data. After that, many variants of bootstrap were developed to handle time series data which possess an inherent dependence structure; see the book Kreiss and Paparoditis, (2023) for discussions. For estimation purposes, the core idea of the bootstrap is to mimic the underlying stochastic structure in order to generate artificial samples in the bootstrap world; on each of those re-samples, the statistic of interest can be recomputed, thus manifesting the variability of the statistic across samples.

However, for the task of time series prediction, we should notice that all future predictions are conditional on the latest observed data where is the order of the NLAR model. Thus, to construct a reasonable predictor in the bootstrap world, we need to make sure predictors of the bootstrap series are also conditional on the exact same data; this is the idea of the forward bootstrap proposed by Politis, (2015) and Pan and Politis, (2016). Using the forward bootstrap approach, with consistent estimations on the NLAR model and innovation distribution, we can simulate many future values in the bootstrap world. Then, the empirical distribution of a future value in the bootstrap world can be used to approximate the distribution of the future value in the real world. A so-called Quantile PI (QPI) can also be built by directly using the relevant quantile values of this empirical distribution; this method is similar to the density forecast of future value—see Chen et al., (2004) and Manzan and Zerom, (2008) who applied non-parametric approaches to do density forecast. Although asymptotically valid, the QPI is typically characterized by finite-sample undercoverage because it does not take the variability of the model estimation into account; see Wang and Politis, (2021) made a related discussion.

To account for the variability in model estimation, Politis, (2015) introduced the notion of a so-called Pertinent PI (PPI) that has a better empirical Coverage Rate (CVR) in finite-sample cases; see more explanations in Section 2. To implement the PPI, we need to impose more requirements on the bootstrap series, i.e., we require that the estimated model in the bootstrap is also consistent to the true one. To check the consistency, the bootstrap series should possess some mixing or weak dependence properties. As developed in the work of Franke et al., 2002b , it is possible to get a self-ergodic bootstrap series that also approximates the true series by a non-parametric autoregressive residual bootstrap (AR bootstrap) approach. Nevertheless, as far as we know, there is no literature about performing AR bootstrap in a non-linear parametric approach to do predictions. For the non-parametric approach within the forward bootstrap frame, only Pan and Politis, (2016) took the local constant technique to estimate the model and then make one-step ahead predictions. After that, although some studies devoted to improving the bootstrap prediction performance or combining the bootstrap idea with the prediction of the state-of-the-art technique—neural network, see the work of Trucíos et al., (2017) and Eğrioğlu and Fildes, (2020) for example, there is a lack of research in direct non-parametric forward-bootstrap prediction for both theoretical and practical aspects. Beyond applying the local constant technique, we can consider other non-parametric estimation methods, such as local liner/polynomial methods. Since the bootstrap can not capture the bias-type term of the non-parametric estimator exactly, these considerations may be gainful in the prediction process because the inherent estimation bias term of local liner/polynomial estimation is simplified and tends to be smaller than applying local constant estimation. We leave the discussion and development of non-parametric forward-bootstrap prediction in future work. For this paper, we focus on the forward-bootstrap prediction of parametric non-linear models.

We should also notice that the earliest method which is similar to ours is the work of Paparoditis and Politis, (1998) where the maximum likelihood estimator was applied to approximate a parametric AR model with ARCH residuals, and then they adopted the local bootstrap proposed by Paparoditis and Politis, (2002) to generate the bootstrap series. After re-estimating parameters based on the bootstrap series, the prediction in the real world is approximated by its analog in the bootstrap world. Paparoditis and Politis, (1998) argued that such bootstrap predictions can capture the variability due to parameter estimations, thus resulting in a pertinent prediction interval. However, they do not consider multi-step ahead prediction. Finally, Chen and Politis, (2019) applied the bootstrap technique to find approximations of the optimal predictors and build corresponding PIs for the so-called NoVaS transformation and compare to ARCH and GARCH models; they also consider multi-step ahead prediction albeit without formal proof of consistency. The last two works mentioned are both limited to a specific type of model. Instead, the paper at hand rigorously explores one-step ahead and multi-step ahead prediction inference under general parametric non-linear NLAR models.

The variability of parameter estimation in finite-sample cases can be captured by relying on the PPI with the AR bootstrap. Nevertheless, we may still find bootstrap-based PPIs undercovering for small sample sizes. To further boost the empirical CVR of our bootstrap-based PPIs, we may use predictive (instead of fitted) residuals analogously to the successful construction of PI for regression and autoregression with predictive residuals in work of Politis, (2013) and Pan and Politis, (2016). In brief, the -th time predictive residual is computed using the delete- dataset; the formal definition of predictive residuals is presented in Section 4. Although the performance of PIs with fitted and predictive residuals are asymptotically the same, the CVR of PIs can typically be improved by the use of predictive residuals when the sample size is small.

The paper is organized as follows. In Section 2, an algorithm to offer prediction inference of general NLAR models will be provided. In Section 3, based on the aforementioned algorithms, we show how to handle a specific form of NLAR model when we have knowledge of its innovation distribution, mean and variance functions. In Section 4, under standard assumptions, we show the consistency of optimal point prediction; furthermore, we show that asymptotically valid PI and PPI can be constructed when the parametric model and innovation distribution are unknown. In Section 5, some simulation results will be presented. Conclusions are given in Section 6. The proofs of theorems from Sections 3 and 4 are given in Appendix.

2 Prediction of general NLAR models

In this paper, we assume that we observe number of real-valued data from a general ergodic NLAR model which satisfies the recursion shown below:

| (1) |

here is assumed to be i.i.d. with mean zero, and represents vector . Throughout this paper, we will assume represents a random variable and represents the observation corresponding to . Thus, represents the observation of which is . can be any continuous (possibly non-linear) function that makes the variance and mean of finite.

Remark 2.1.

In section 4 of Tong, (1990), Eq. 1 is analyzed as a stochastic difference equation. Assuming that Eq. 1 can be decomposable to , they give the conditions under which Eq. 1 is ergodic. We will also discuss similar conditions in Section 3. Here, we are interested in providing a methodological algorithm to predict the general NLAR model Eq. 1.

The problem is how can we make multi-step ahead prediction inferences with such a complicated model. As known to us, for a stochastic process , the optimal predictor of , , given the (infinite) past is:

| (2) |

when it exists. As pointed out by Pemberton, (1987), this result does not require the stochastic process to be stationary. In our case, since we assume the order of the NLAR model is finite. Eq. 2 can be simplified to:

| (3) |

Similarly, the optimal predictor of given past history is the conditional median:

| (4) |

where is the conditional quantile function of .

We will call Eq. 3 and Eq. 4 the exactly optimal point predictors based on or loss. However, it is hard to compute them directly. Subsequently, we will propose the simulation or bootstrap-based method to find an approximation of the exactly optimal prediction. Moreover, we also consider the PI of future values; an asymptotically valid PI of with CVR given past history can be defined as:

| (5) |

where and are lower and higher PI bounds, respectively. Implicitly, the probability should be understood as the conditional probability given the latest observations. We typically construct a PI that is centered at some meaningful point predictor . An asymptotically valid centered PI with CVR given past history can then be defined as:

| (6) |

where and denote the lower and quantiles with respect to the conditional distribution of the so-called predictive root: .

2.1 Simulation-based prediction

Consider an idealized situation where the model and the distribution of innovations are known. In this case, we propose to approximate the -step ahead prediction by simulating innovations from and plugging them into the NLAR model. To describe the idea, focus on the 2-step ahead prediction, and note that the distribution of the future value (conditional on the observed ) is identical to the distribution of

where and are i.i.d..

Going to the -step ahead prediction, the distribution of the future value (conditional on the observed ) is identical to the distribution of the quantity

| (7) |

where are i.i.d..

Of course, in order to obtain the or optimal point predictor, we would need to approximate the mean or median of the quantity (7). We can do this by Monte Carlo (MC) simulation; the simulation will be based on replicates of the quantity (7); these are denoted . To generate , we need to generate values i.i.d. from ; the latter are denoted . Since we need to generate for , all in all, we need to generate values i.i.d. from ; this sums up the computational cost of the MC simulation.

The or optimal predictor of can be approximated by the mean or median, respectively, of ; the approximation will become more and more accurate as tends to infinity. Moreover, we can also find the approximation of the optimal predictor of by taking the mean or median of where is a continuous function of interest. Finally, the empirical distribution of the values can also be used to approximate the distribution of the future value (conditional on the observed ), leading to the construction of asymptotically valid PIs; the details will be given shortly.

2.2 Bootstrap-based prediction

In the more realistic scenario, both and are unknown but can be estimated from the data at hand; denote their estimators by and respectively, and assume they are consistent. Typically, in order to construct the estimator , the practitioner must be able to approximate the unobserved errors by ; in standard situations, have the interpretation of residuals from fitting the model Eq. 1 to the data.

Remark 2.2.

In order to decompose the estimation from the prediction problem, the estimated quantities , and could be based just on the data instead of the full sample . This trick may help with theoretical analysis but is not important in practical applications.

Conducting a simulation as described in the previous subsection using and in place of the unknown and turns the MC simulation into a bootstrap procedure. The bootstrap version of the quantity (7) is now given by

| (8) |

where are i.i.d.; is an estimator to the true model. Next, we can take a similar approach as the simulation-based method previously described to approximate the optimal predictor of . We summarize this procedure in Algorithm 1.

| Step 1 | Fit the data with the general autoregressive model of Eq. 1, and construct the estimator . Furthermore, compute all fitted residuals . Then, center all residuals by subtracting their sample mean for . Denote the empirical distribution of centered residuals. |

| Step 2 | Generate as i.i.d. from , and plug them into Eq. 8 to obtain pseudo-values . |

| Step 3 | The or optimal predictor of can be approximated by which is the mean or median of , respectively. |

If and are consistent to and , respectively. Then, can be made to be arbitrarily close to the true optimal predictor by taking large enough. Furthermore, based on Algorithm 1, the conditional distribution of is approximated by the empirical distribution of . It is then straightforward to construct a bootstrap QPI that is asymptotically valid. However, such a QPI will suffer from finite-sample undercoverage since the variability of estimating the model is not taken into account. We will prefer constructing a PPI instead that possesses a stronger property than the asymptotic validity. In other words, the PPI can asymptotically capture the variability stemming from the error in the estimation of the model—see Politis, (2015) and Pan and Politis, (2016) for an in-depth discussion.

We present the method to build the PPI for in Algorithm 2. In short, we employ the distribution of the bootstrap predictive root to estimate the conditional distribution of the predictive root in the real world. Then, we can use the bootstrap quantiles associated with the bootstrap predictive root as bounds for the true root ; solving for yields the desired PI. The fact that this PI is actually pertinent can be justified under additional conditions; see Definition 2.4 of Pan and Politis, (2016) for a formal discussion.

| Step 1 | Same as Step 1 of Algorithm 1. |

| Step 2 | Apply Step 2-3 of Algorithm 1 to construct , the optimal point predictor of (based on or loss). |

| Step 3 | (a) Resample the residuals and as i.i.d. from to create pseudo-errors. |

| (b) Let where is generated as a discrete random variable uniformly on the values . Then, use the fitted general autoregressive model of Step 1 and the generated in Step 3 (a) to get bootstrap pseudo-series in a recursive manner, i.e., for . | |

| (c) Based on the bootstrap series , re-estimate the general model to obtain . | |

| (d) Guided by the idea of forward bootstrap, re-define the last values of the bootstrap data to match the original data, i.e., re-define for . | |

| (e) Use , the bootstrap data , and the pseudo-errors to generate recursively the future bootstrap data , i.e., for . | |

| (f) With bootstrap data and the re-estimated model , utilize Algorithm 1 to compute the bootstrap predictor denoted by , with the same loss criterion as in Step 2. | |

| (g) Construct the bootstrap predictive root: . | |

| Step 4 | Repeat Step 3 times. The bootstrap root replicates are collected in the form of an empirical distribution whose -quantile is denoted . The equal-tailed prediction interval for centered at is then approximated by |

Remark 2.3.

Step 3 part (f) of Algorithm 2 in the bootstrap world is an analogy with Step 2 in the real world. For Step 3 part (f), we actually make the bootstrap prediction again in the bootstrap world. The reason behind this step is that the effects of innovation can not be reduced in future predictions even if the mean of the innovation is 0, which is different from the situation for the linear time series. This double-bootstrap step is worthy and necessary if we want to get a PI that is asymptotically centered at the mean or median of the future value.

As discussed in Section 1, to improve the finite-sample CVR of PIs we may use predictive (instead of fitted) residuals in the bootstrap procedure. We will give details in the following section where we focus on a specific NLAR of interest. We should clarify that the success of Algorithms 1 and 2 and subsequent algorithms heavily depend on the estimation accuracy of . If the estimator is asymptotically consistent to the true model. Besides, with uniform convergence between empirical residual and true innovation distributions, the consistency of bootstrap predictions to the exactly optimal point predictors is possible. With further conditions, the PPI is also achievable. In other words, if we can find such desirable estimations, these above prediction inferences will be valid.

3 Prediction inference for a specific NLAR of interest

Here and in all that follows, we are exclusively interested in analyzing the NLAR model of the specific form:

| (9) |

where are i.i.d. innovations. Eq. 9 is a special case of Eq. 1 that decomposes the NLAR function to —that represents the conditional mean— plus the so-called variance function multiplying the innovations . Under Eq. 9, the innovations are more explicitly defined and thus easily estimable as residuals after model fitting. If , then we have an NLAR with homoscedastic errors. For simplifying the notation, we assume that mean and variance functions have the same order . We first impose some standard assumptions and suppose they are met throughout this paper:

-

A1

and are continuous functions from to , and is positive and bounded. Moreover, for quantifying the boundness of in probability to serve the proof, we assume that there are with for all , where is the starting point of the time series.

-

A2

are with distribution , satisfying and . However, if (homoscedastic errors case), then is not restricted to equal one, but needs to be finite.

-

A3

For all , is independent of .

3.1 Sufficient conditions for geometric ergodicity

To conduct statistical inference for non-linear time series data in the following sections, we need to find a tool to quantify the degree of asymptotic independence of time series. Popular choices are various mixing conditions. For simplifying proofs and relying on existing results, in this paper, we focus on time series with geometrically ergodic property which is equivalent to -mixing condition with at least exponentially fast mixing rate; see Bradley, (2005) made a detailed introduction of different mixing conditions and ergodicity. Thus, the first question we face is how we can make sure the geometric ergodicity of model Eq. 9 is satisfied.

Checking geometric ergodicity for a LAR model is simple; it is well known that the LAR model is stationary and geometrically ergodic as long as the corresponding characteristic polynomial does not have zero roots inside or on the unit circle. However, this check criterion depends on the linearity assumption, and can not be extended to serve for NLAR model directly (An and Huang,, 1996). Thus, practitioners rely on Markov chain techniques to explore conditions under which the NLAR model is geometrically ergodic. The motivation is that the NLAR model can be described as a Markov chain in a general state space; the extensive discussions and literature related to Markov chains can guide the development of criteria to check the ergodicity of NLAR models.

One of the earliest criteria developed to guarantee the ergodicity of a Markov chain is Doeblin’s condition given by Doob, (1953). Later, Tweedie, (1975) proposed a more generalized condition, the so-called Drift criterion. This criterion gives a sufficient condition for an aperiodic and irreducible Markov chain to be geometrically ergodic. For completeness, we present this criterion using the version applied by An and Huang, (1996):

Lemma 3.1 (Drift criterion).

Let be an aperiodic and irreducible Markov chain. Suppose that there exists a small set , a non-negative measurable function , positive constants , and such that:

| (10) |

The function is called the test function in the literature. For the formal definition of a ‘small set’; see Tjøstheim, (1990) or Tong, (1990). We will soon see that the small set can be taken as a compact set in some situations.

Thus, to ensure the ergodicity of an NLAR model, people can check if is aperiodic and irreducible and 3.1 holds. Along with this idea, An and Huang, (1996) give several kinds of sufficient conditions for Eq. 9 with (homoscedastic errors case) to be geometrically ergodic. Note that the test function and the specific small set will change according to which condition is based. Then, Min and Hongzhi, (1999) extend these results to the region of NLAR models with heteroscedastic errors. Based on this body of work, if we assume:

-

A4

The probability density function of innovation is continuous and everywhere positive.

-

A5

The conditional mean and volatility functions satisfy the inequalities:

(11) where , and is the Euclidean norm.

we can obtain a useful Lemma:

Lemma 3.2.

Let satisfy the model Eq. 9. Suppose A4 and A5 are fulfilled. Then is aperiodic and irreducible with respect to which is the Lebesgue measure. Moreover, the -non-null compact sets are small sets.

Remark 3.1.

The proof of 3.2 can be found in Min and Hongzhi, (1999). The original proof only requires the density function to be lower semi-continuous. In this paper, since the estimation of the innovation distribution and the optimal predictor will be discussed, we require a stronger condition for the density function. Besides, we should notice that we can check the classical properties defined by the Markov chain to verify the aperiodicity and irreducibility. Nevertheless, it is more natural to apply 3.2 for analyzing NLAR models. For example, when we consider a homoscedastic NLAR model with , the drift criterion and the boundedness of the conditional mean function on a suitable compact set can be satisfied by a simple condition: , for all and some ; this is exactly Assumption 3 (i) of Franke et al., 2002b . In their work, they mention that the everywhere-positive assumption (A4) on the density function is unnecessarily restrictive. Thus, they replace it with their Assumption 3 (iii). However, for simplifying the proofs of our paper, we still require the everywhere-positive property. Furthermore, we will apply a convolutional technique to acquire an everywhere-positive “innovation distribution” in the bootstrap world to satisfy this strong assumption.

The condition which ensures the Drift criterion is satisfied for a homoscedastic NLAR models can be drawn from An and Huang, (1996). If we assume:

-

A6

There exists a positive number and a constant C such that the conditional mean function satisfies:

(12)

then we can get the below lemma:

Lemma 3.3 (Theorem 3.2 of An and Huang, (1996)).

Let satisfy the homoscedastic version of the model Eq. 9. If A4 and A6 are fulfilled, then this NLAR model is geometrically ergodic.

Similarly, we can obtain the condition for heteroscedastic NLAR models to be geometrically ergodic by imposing an additional assumption on the variance function:

-

A7

The conditional variance function satisfies:

(13)

Then the Lemma holds:

Lemma 3.4 (Theorem 3.5 of Min and Hongzhi, (1999)).

Let satisfy the model Eq. 9. Suppose the conditional variance function satisfies A5 and A7. In addition, A6 holds true for the conditional mean function, and A4 holds true for the probability density function. Then, this heteroscedastic NLAR model is geometrically ergodic.

3.2 Prediction inference for NLAR models with known form

Through 3.1 to 3.4, we have seen sufficient conditions to guarantee the geometric ergodicity of NLAR models. Before considering the case when the NLAR model and innovation distribution are unknown, we first show how can we conclude prediction inference for NLAR models of known form. Although this case is usually unrealistic, it serves as a useful illustration before we investigate NLAR model cases. To simplify notation, we only consider the homoscedastic NLAR model in the main text, the analogous algorithms and theorems serve for NLAR models with heteroscedastic errors can be shown similarly; see more discussions in the Appendix.

According to the discussion in Section 2, we can deploy the Monte Carlo simulation to approximate the exactly optimal point prediction or PI conditional on the past history. The procedure is summarized in Algorithm 3.

| Step 1 | Note that the homoscedastic Eq. 9 can be written as ; this can be iterated to find an expression for . For example, . We can write as: (14) where we used the notation to specify that depends on and . |

| Step 2 | Simulate i.i.d. from . |

| Step 3 | Plug the from Step 2 and into Eq. 14 to obtain a pseudo-value of given by . |

| Step 4 | Repeat Steps 2 and 3 times to get pseudo values . The and optimal predictor can be approximated by and , respectively. Furthermore, a QPI can be built by taking corresponding quantiles of the empirical distribution of . |

Remark 3.2.

The procedure implied by Algorithm 3 can be easily extended to NLAR models with heteroscedastic errors. The only difference is that we compute iteratively for

We first show that the mean of pseudo values derived from Algorithm 3 can be consistent to the exactly optimal predictor. This is formalized in 3.1.

Theorem 3.1.

Under assumptions A1-A6, the point predictor of homoscedastic Eq. 9 as converges to the exactly optimal predictor almost sure as tends to infinity. Here, ; are i.i.d. with common distribution for all .

Next, inspired by the proof of Guo et al., (1999), we can show the median of pseudo values in Algorithm 3 is also consistent to the exactly optimal predictor. We can also build a PI that is asymptotically valid with any arbitrary CVR. To achieve this goal, we need additional one mild assumption:

-

A8

The mean function is uniformly continuous.

This will lead to 3.2:

Theorem 3.2.

Under assumptions A1-A6, if we take the point predictor as , it is consistent to the exactly optimal predictor when converges to infinity. Here, and have the same definitions with 3.1. We can further show that the QPI is asymptotically valid with any arbitrary CVR.

4 Prediction inference for parametric NLAR models of unknown form

In practice, it is not realistic to assume that we know the NLAR model Eq. 9 and the corresponding innovation distribution. Therefore, it is necessary to research if the aforementioned algorithms stand meaningful when the NLAR model is unknown. In this section, we will consider the case that the NLAR model has a known parametric specification but the parameter values are unknown. After estimating the model by Least Square (LS) technique, we show that the prediction inference can also be built with standard assumptions.

4.1 Consistent point prediction and QPI

In this subsection, we assume that the NLAR model Eq. 9 has the parametric specification

| (15) |

where the functional form of and is known but the real-valued parameters and are unknown.

For carrying out prediction inference, we need to estimate and first; denote the estimators. The consistency of parameter estimation is crucial for getting a consistent prediction. Thus, we suppose that we have a consistent parameter estimation and other mild conditions:

-

A9

The parameter estimator and are consistent to and respectively.

-

A10

For all in the support of , the non-linear functions and are both Lipschitz continuous with respect to their 2nd argument.

-

A11

The probability density of innovation satisfies and for finite .

Based on these assumptions, we will show how to get consistent point predictors and asymptotically valid QPI. The assumption A9 can be satisfied by applying the non-linear LS (NLS) estimation method. The reason for choosing this method and the procedure of estimation will be discussed in Section 4.4. First, we want to show the Cumulative Distribution Function (CDF) of innovations can be approximated by the empirical CDF of residuals. Their relationship can be summarized in 4.1.

Lemma 4.1.

Under A1–A7, A9–A11, the CDF of innovation can be approximated by the empirical CDF of residuals in a way:

| (16) |

where ; is the indicator function, and we define the residual for .

With 4.1, we can build a QPI or find approximations of optimal and predictors. Of course, for this case, we need to apply the bootstrap technique. In short, being similar to the Algorithm 1, we summarize the approach to obtain prediction inference for unknown parametric NLAR models Eq. 15 in Algorithm 4. For simplifying notation, we focus on the case with homoscedastic errors.

| Step 1 | Fit the homoscedastic Eq. 15 model based on to obtain parameter estimator that satisfies A9. Furthermore, compute and record all centered residuals for and construct their empirical distribution . |

| Step 2 | Similarly to Eq. 14, we see that depends on , on , and on . We can denote this as X_T+h = G(X_T,…,X_T-p+1; ϵ_T+1 ,…, ϵ_T+h ; θ_1). Hence, we can generate a pseudo-value of as: (17) where are drawn i.i.d. from . |

| Step 3 | Repeat Step 2 times to get . Then, and optimal predictors can be approximated by and , respectively. Furthermore, a QPI can be built by taking corresponding quantiles. |

The analogous algorithm for NLAR model Eq. 15 with heteroscedastic errors is easy to be built. The asymptotic validity of QPI and consistency of optimal or point prediction are guaranteed by 4.1 under the additional assumption of mean and volatility functions given below:

-

A12

For all parameter values in their respective domains, the non-linear functions and are continuous w.r.t their first argument.

Theorem 4.1.

Under A1-A7, A9–A12, let satisfy Eq. 15. For we have:

| (18) |

where ; this is computed as iteratively for ; ; is an appropriate sequence converges to infinity as converges to infinity; is the distribution of h-step ahead future value in the bootstrap world, i.e., conditional on all observed data.

As we discussed in the Section 1, instead of adopting the fitted (traditional) residuals in Algorithm 4, we can apply the predictive residuals to compute QPI. To acquire such predictive residuals which are denoted hereafter, we need to estimate models based on delete-, i.e., the available data for the scatter plot of vs. excludes the single point at . Evaluate and collect the estimation residual at this point and repeat it for , we obtain all predictive residuals . The corresponding prediction procedure with predictive residuals is written in Algorithm 5.

| Step 1 | Fit the homoscedastic Eq. 15 model based on to get parameter estimation which satisfies A9. Furthermore, for , re-estimate the model based on delete- dataset to get estimation . Compute all predictive residual . Center all predictive residuals by manipulation for and record the result as the empirical predictive residual distribution . |

| Steps 2-3 | Change the residual distribution to , the rest is the same as Algorithm 4. |

Remark 4.1.

When tends to infinity, the effects of leaving out one data pair is negligible. Hence, for large , the predictive residual is approximately the same as the fitted residual . Therefore, 4.1 and 4.1 are still true with predictive residuals. Similarly, for NLAR models with heteroscedastic errors, we can define the predictive residual , where is the parameter estimation of the variance function with the delete- dataset. In Section 5, we will show the positive effects brought by applying predictive residuals on the empirical CVR of QPI.

4.2 Pertinent PIs

As shown in 4.1, it is straightforward to build a QPI for . However, this type of prediction interval can not capture the variability arising from the model estimation. Thus, we propose a new bootstrap procedure based on the general Algorithm 2 and summarize it in Algorithm 6.

| Step 1 | Fit the homoscedastic Eq. 15 model based on to get parameter estimation which satisfies A9. Furthermore, compute and record for to get . |

| Step 2 | Find the prediction based on Algorithm 4. |

| Step 3 | (a) Resample (with replacement) the residuals from to create pseudo-errors and . |

| (b) Let where is generated as a discrete random variable uniformly on the values . Then, use the fitted homoscedastic NLAR model of Step 1 and the generated in Step 3 (a) to create bootstrap pseudo-data in a recursive manner, i.e., compute for . | |

| (c) Based on the bootstrap data , re-estimate the homoscedastic NLAR model to get . | |

| (d) Guided by the idea of forward bootstrap, re-define the last values of the bootstrap data to match the original, i.e., re-define for . | |

| (e) With parameter estimation , the bootstrap data , and the pseudo-errors to generate recursively the future bootstrap data . | |

| (f) With bootstrap data and parameter estimation , utilize Algorithm 4 to compute the bootstrap predictor which is denoted by . For generating innovations, we still use . | |

| (g) Determine the bootstrap root: . | |

| Step 4 | Repeat Step 3 times; the bootstrap root replicates are collected in the form of an empirical distribution whose -quantile is denoted . The equal-tailed prediction interval for centered at is then estimated by |

Analogously to the development of QPI with predictive residuals, we also propose the variant of Algorithm 6 with predictive residuals to improve the CVR in finite sample cases; this is given in Algorithm 7. Algorithm 6 and Algorithm 7 focus on a homoscedastic NLAR satisfying Eq. 15; corresponding algorithms for an NLAR with heteroscedastic error can be built similarly.

| Step 1 | Fit the homoscedastic Eq. 15 model to get parameter estimation which satisfies A9. Furthermore, for , re-estimate the model based on delete- dataset to compute the estimate . Compute the predictive residual . Then, take for as the empirical predictive residual distribution . |

| Step 2 | Find the prediction based on Algorithm 5. |

| Steps 3-4 | Chang the residual distribution to and change the application of Algorithm 4 to Algorithm 5; the rest is the same as Algorithm 6. |

Remark 4.2.

To build the PPI for Eq. 15 with heteroscedastic error, we need to make predictions and generate bootstrap series including variance function; see 3.2. In addition, since we assume the innovation has variance 1 if , we also need to normalize the variance of fitted/predictive residuals to 1 in Algorithm 6 and Algorithm 7, i.e, take to get and take to get for . This additional manipulation for Eq. 15 with heteroscedastic error simplifies the theoretical proof. Moreover, from a practical issue, the length of PPI will decrease with this additional step.

4.3 Asymptotic validity of the PPIs

The idea that underlies Algorithm 6 and Algorithm 7 is approximating the distribution of predictive root by its bootstrap version . From a theoretical view, as we have clarified in 4.1, the difference between applying fitted residuals and predictive residuals lies in the available dataset. The difference in parameter estimations based on fitted residuals and predictive residuals asymptotically converges to zero in probability under standard assumptions. In other words, the difference between fitted residuals and predictive residuals also converges to zero in probability. Thus, in what follows, we just analyze the asymptotic performance of a PPI with fitted residuals since it is the same as the asymptotic performance of a PPI with predictive residuals. However, the latter invariably has a larger finite-sample CVR.

For , if we insist on doing the prediction in the bootstrap world parallelly with the procedure in the real world, we need to use the residual distribution , which is obtained from re-estimating the model in the bootstrap world. However, in the bootstrap world, the underlying “true innovation” distribution is the and we can expect that converges to , so we apply to compute directly. All in all, we want to compare two predictive roots and . If we can show

| (19) |

then we can utilize the distribution of to consistently estimate the distribution of ; as a result, the PPI has asymptotic validity within .

4.4 The consistency of to

In this paper, we adopt the NLS technique to perform parameter estimation; the reason is that NLS is based entirely on the scatter plot of vs. so that predictive residuals can be easily defined. First, we consider a homoscedastic version of Eq. 15. The heteroscedastic version will be handled by a two-step estimation approach later. To simplify notation in the proofs, we consider an NLAR model with order one, and we attempt to minimize a quadratic empirical loss function as given below:

| (20) |

where is the domain of possible values of . With correctly specified model, the true parameter satisfies that:

| (21) |

The consistency of the non-linear least squares estimator to can be guaranteed with below additional assumptions:

-

A13

is bounded, closed and with finite dimension.

-

A14

uniquely minimizes over .

If we can not correctly specify the model, we call the optimal parameter in the sense of minimizing . We can still build the consistency relationship between and if we assume A14. As we have clarified at the beginning of Section 1, we focus on the case where we can correctly specify the model. The model misspecification case can be analyzed similarly.

Lemma 4.2.

Under assumptions A1-A7 and A10, A13-A14, if satisfies a homoscedastic Eq. 15, the non-linear least squares estimation converges to the true parameter in probability, i.e., for any ,

| (22) |

To handle the heteroscedastic Eq. 15, we still estimate by minimizing the empirical risk Eq. 20. The corresponding true risk with respect to is:

| (23) |

which implies that the minimizer of risk Eq. 23 is equal to the true . Thus, the minimizer of empirical risk will still converge to the true parameter in probability. After securing this consistent estimation of , we proceed to estimate the by minimizing the below empirical risk:

| (24) |

The corresponding true risk should be:

| (25) |

which implies . Under the additional assumptions:

-

A15

is bounded, closed and with finite dimension.

-

A16

uniquely minimizes over ,

we can derive the lemma below to ensure the consistency of to :

Lemma 4.3.

Under assumptions A1-A7 and A10, A13-A16, if satisfies a heteroscedastic Eq. 15, the NLS estimators and converge respectively to the true parameters and in probability.

In fact, under the consistency of parameter estimations, we can impose more conditions on the mean and variance functions to develop estimation inference of and , i.e., building confidence interval for and , respectively. If we can further approximate the confidence interval by bootstrap, the PPIs derived from Algorithms 6 and 7 are indeed pertinent. We first discuss the consistency property of ; then the discussions of estimation inference on and are put in Section 4.6.

4.5 The consistency of to in the bootstrap world

From the last subsection, we have seen the non-linear least squares can return a satisfied estimation but this is still not enough for us to derive the asymptotic validity of the PPI. As we discussed in Section 4.3, the necessary component is the consistency between and . We first investigate the relationship between and . Once this relationship is determined, the consistency between and is trivial. In the work of Franke and Neumann, (2000), a similar problem is considered for the regression case. In short, this consistency can be proved by showing that analogous converges uniformly to . In our case, has the form as below:

| (26) |

Here, is the bootstrap series, which mimics the property of the true series. It can be created based on Algorithm 6 or Algorithm 7 with fitted or predictive residuals, respectively. And satisfies that:

| (27) |

As discussed in Section 4.4, it is necessary that we have the additional condition: the bootstrap series is also geometrically ergodic. Then, with close enough empirical residual distribution and true innovation distribution, we may show the uniform convergence of and . Then, the consistency of to is easily found.

The first problem we face is that the probability density of the fitted residual is not continuous and positive everywhere which means the basic assumption A4 needed to show the ergodicity of the bootstrap series is not met. In a similar situation, Franke et al., 2002b apply the kernel technique to build a probability density of . Here, we take a convolution approach to make the density function of empirical residual continuous and positive everywhere, i.e., we define another random variable which is the sum of empirical fitted residual and an independent normal random variable with mean 0 and suitable variance , i.e., let:

| (28) |

where , where converges to 0 as with a suitable rate. Then, we create bootstrap residuals by drawing i.i.d. from , the CDF of , in order to build a bootstrap series as we did in Algorithm 6. Subsequently, we re-estimate the parameter of NLAR based on the bootstrap series . Since the convergence in mean squares implies the convergence in probability, we can easily see that 4.1 still stands true for . Thus, if we replace by in Algorithm 4 and Algorithm 6, all claims will still be true.

Remark 4.3.

Here, we take a convolution approach to create residuals that possess a continuous probability density function. We should notice that this approach is equivalent to the kernel density estimator taken by Franke et al., 2002a ; Franke et al., 2002b with a Gaussian kernel. More specifically, the variance plays the same role as the bandwidth in the Gaussian kernel. Thus, if we take for some constant , we can show that the probability density of , converges uniformly to ,i.e., , see the proof of Lemma 4 from Franke et al., 2002b for a reference. In addition, this convolution technique can also be applied to predictive residuals. As we have discussed in Section 4.3, the predictive residual is equivalent to the fitted residual asymptotically.

Although we will use and the corresponding density function to develop subsequent theorems, in practice we still apply since effects stemming from are negligible when we sample innovations from the empirical residual distribution. For simplifying notations, we keep using and , though their representation may change according to the context. Similarly with the deduction of 4.2, we can get:

| (29) |

for some constant . Focusing on analyzing , we can partition the parameter space into different balls, i.e., make a -covering of . Let the -covering number of be which means for every , s.t. for . Define , we can consider:

| (30) |

Consider the second term of the r.h.s. of the above inequality. From Lipschitz continuous assumption of with respect to , we can get:

| (31) |

Similarly, we can find the . For the first term of the r.h.s of Eq. 30, if we can show the bootstrap series is also ergodic when the parameter is fixed, then we actually have , such a similar result is also implied by Theorem 5 of Franke et al., 2002b , here stands for the conditional expectation in the bootstrap world. Therefore, for getting the uniform convergence of to in probability, it is enough to show:

| (32) |

For notational simplicity, we consider an NLAR(1) model; then, the l.h.s. of Eq. 32 equals:

| (33) |

where stands for the marginal stationary density function of the bootstrap series. As we can see, the uniform convergence of Eq. 30 in probability depends on the ergodic property of the bootstrap series and the closeness of and which is the true stationary density function of the real series. In other words, the ergodic property of bootstrap series is not enough to get our desired result. Actually, such ergodic property alone is of little use since the main goal of performing bootstrap is to mimic features of the true process, i.e., we require the stationary distribution of the bootstrap series and real series should be close enough to show Eq. 32. Here, we develop a theorem to illustrate the required conditions.

Theorem 4.2.

Suppose that the data generating process obeys Eq. 15 and the bootstrap time series are generated according to Algorithm 6 or Algorithm 7. Under A1-A7, A9-A12, we have:

| (34) |

Then, we can show that Eq. 30 converges to zero in probability, and that converges to in probability. In addition, applying the two-stage estimation strategy taken in Section 4.4, the consistency between and can also be shown. Thus, is consistent to , meeting the requirement of proving Eq. 19. For showing the asymptotic validity of PPI with predictive residuals, we can apply the same strategy to make predictive residuals have a smooth probability density function as we did in Eq. 28. Then, the consistency between the parameter estimation in the bootstrap world and the true parameter can also be shown as proof of applying fitted residuals. Although the PPI with fitted residuals and predictive residuals are the same asymptotically, the performance of PPI with predictive residuals is better in finite sample cases. Examples can be found in the next section.

All in all, the prediction intervals defined in Algorithms 6 and 7 are asymptotically valid, since we can get consistent parameter estimations in the bootstrap world. 4.1 below summarizes this result:

Corollary 4.1.

Under assumptions A1-A7, A9-A12, is consistent to with both fitted and predictive residuals, which substantiates Eq. 19. Thus, the conditional distribution of can be asymptotically approximated by the conditional distribution of which guarantees the validity of PI derived by Algorithm 6 or Algorithm 7 with both homoscedastic or heteroscedastic errors asymptotically.

4.6 The estimation inference of and

From the above sections, the asymptotic validity of PPI is checked. However, with a more complicated prediction procedure in Algorithms 6 and 7, we expect to get a stronger PI, i.e, pertinent PI. The crucial part behind the pertinence is that we can approximate the distribution of by the distribution of . In other words, the estimation variability can be captured by the bootstrap-based PI. To derive the estimation inference, we need stronger assumptions than A10 on the mean and variance function. We assume:

-

A17

For all in the support of , and are twice differentiable w.r.t. parameters in some neighborhood of true parameters.

-

A18

If we write as , we need is non-singular; If we write as , we need is non-singular.

-

A19

The first order condition of minimizing the empirical risk function satisfies that and . Similarly, we assume we can achieve such accuracy for optimization in the bootstrap world.

A19 implies that the first-order conditions for minimizing criterion functions hold approximately since it may be hard to find exactly or . Then, we first develop the estimation inference of and in the 4.3.

Theorem 4.3.

Under A1-A7, A13-A19, with consistent parameter estimations and , we have:

| (35) |

where ; ; ; is the gradient operator w.r.t. . Similarly, we can analyze the distribution of parameter estimation :

| (36) |

where ; ; ; ; ; here is the gradient operator w.r.t. .

Remark 4.4.

From here, we can see the distribution of depends on the time series structure. If we do not assume that we can specify the correct model format, the covariance matrix of the parameter’s asymptotic distribution will depend on the whole structure of the time series. This is the reason why we need the forward bootstrap to generate time series and do estimation in the bootstrap world, otherwise, we can not approximate the covariance term well.

In the bootstrap world, we can perform a similar parameter estimation procedure as we did in Section 4.5. As we have seen in the proof of 4.2, for , where and , under the consistency of parameter estimation in the real world, the bootstrap series is also ergodic in the sense of -mixing. Thus, we can have below consistency results in the bootstrap world:

| (37) |

where is between and ; is between and ; hence and also converge to and in probability, respectively. It is easily to find and for . To simplify the result about , we need the variance of to be one to remove the second term. This is guaranteed since we normalize the variance of the residuals to 1 when we perform the bootstrap prediction algorithms for models with heteroscedastic errors. Another advantage of this manipulation comes from analyzing . With this additional manipulation, is 0, which implies that the asymptotic distribution of has mean 0. By the CLT for a triangular array of strongly mixing series given in Politis et al., (1997), we can further show:

| (38) |

The required assumptions can be checked in the same way shown in Theorem 5 of Franke et al., 2002b . All in all, we can develop estimation inference for parameter estimation in the bootstrap world, i.e, 4.2 as below:

Corollary 4.2.

If we restrict on observed data , where as , under assumptions of 4.3, we can further build the estimation inference of parameter estimations in the bootstrap world, i.e, we have:

| (39) |

4.3 and 4.2 together guarantee the pertinence of PPI returned by Algorithms 6 and 7 with high probability. The notable advantage of this type of PI will be illustrated in Section 5.

5 Simulations

In this section, we deploy simulations to check the performance of our bootstrap point predictions and the asymptotic validity of corresponding PIs in platform for finite sample size. We first consider a simple case: NLAR model with order one and homoscedastic errors. We present the model as below:

| (40) |

where satisfies A2. We can easily check that the model Eq. 40 satisfies the condition to make sure the time series is geometrically ergodic. Assuming that we have observed series , we want to predict the value of . As pointed out before, the exactly optimal predictor is the conditional mean of :

| (41) |

where represents the analytic formula of which can be obtained by computing for iteratively. When we know the NLAR model and the innovation distribution, Eq. 41 can be computed by multiple-integration directly. However, it is very time-consuming or even impossible to perform such computation for a long prediction horizon. Thus, throughout this section, we assume that the forecasting result returned by the simulation approach of Algorithm 3 represents the exactly optimal or prediction. We take the simulation repeating number to get a satisfying approximation. For a fair comparison, we also do times bootstrap with Algorithm 4 or Algorithm 5 to get the bootstrap prediction when the model and innovation are unknown. Starting from a simple example, we consider and . For the prediction horizon, we consider for the moment. To generate the data of Eq. 40, we take , then generate a series with size . Here, is a large enough burn-in number to remove the effects of the initial distribution of .

Remark 5.1.

In the model of Eq. 40, we include the constant parameter in order to safely ensure that the innovation distribution has mean zero; this is important for the consistency of NLS.

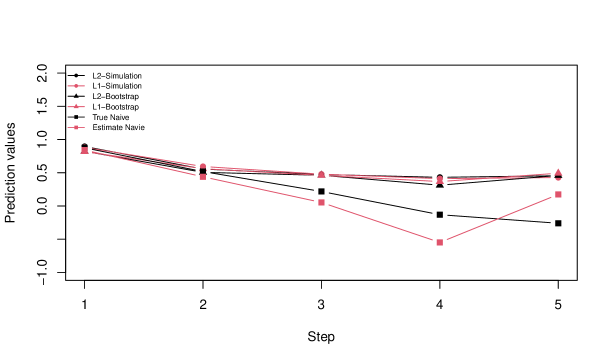

To see the crucial difference between the prediction of LAR and NLAR models, we apply two naive prediction methods which predict of Eq. 40 by computing or repeatedly for . In total, we compare four methods to do prediction. We call them (1) Simulation, with a known model and innovation; (2) Bootstrap, with an unknown model and innovation; (3) True Naive Prediction—naive prediction with the known model; (4) Estimated Naive Prediction—naive prediction with the estimated model. We call (3) and (4) naive since the variability in model estimation is not captured by these two methods. Compared to bootstrap-based methods (2) and (4), the simulation and true naive prediction methods are “oracles” since we assume that model and innovation information are known to us. Setting the burn-in number and , we present one simulation experiment result in Fig. 1 showing the -step ahead optimal prediction value vs. the step .

For the optimal prediction of , all four methods return almost the same value as expected. This is in our expectation since the innovation is assumed to have 0 mean. In addition, the normal distribution is symmetric. Thus, two naive predictions, and optimal predictions from simulation and bootstrap approaches coincide. For prediction horizon beyond 1-step, we can still see the approximations of and optimal predictors based on bootstrap are very close to the oracle and optimal predictors return by the simulation method. On the other hand, true and estimated naive prediction methods give significantly different and even opposite results. We should notice that the only difference between these two naive prediction methods is using true parameters or estimated parameters. Under the consistent relationship between true parameters and estimated parameters which is indicated by the closeness of simulation and bootstrap approaches, the importance of including innovation in prediction gets emphasized. Otherwise, the multi-step ahead prediction of the NLAR model will be spoiled by the error accumulation issue.

Obviously, we can not get a conclusion based on only one experiment. For comparing the relationship between simulation and bootstrap methods, we repeat the above experiment times. Then, we approximate the Mean Squared Difference (MSD) between oracle (simulation-based) and bootstrap-based predictions according to the below equation:

| (42) |

where and are -th step ahead oracle and bootstrap predictions in the -th replication, respectively. We summarize all MSD different prediction steps in Table 1. For all prediction horizons, the MSD is very small, which supports the conclusion that the bootstrap-based optimal prediction is consistent to the simulation-based optimal prediction.

| Prediction Horizon | 1 | 2 | 3 | 4 | 5 |

| -Bootstrap | |||||

| -Bootstrap |

In addition to comparing oracle and bootstrap-based predictions, we are also interested in the Mean Squared Prediction Error (MSPE) of all predictions. MSPE of predictions is approximated based on the below formula.

| (43) |

where represents -th step ahead predictions implied by four approaches and stands for the true future value in the -th replication. All MSPE are recorded in Table 2.

| Prediction Horizon | 1 | 2 | 3 | 4 | 5 |

| -Simulation | 0.9595 | 1.2357 | 1.2101 | 1.1905 | 1.2153 |

| -Simulation | 0.9594 | 1.2360 | 1.2107 | 1.1901 | 1.2156 |

| -Bootstrap | 0.9639 | 1.2390 | 1.2144 | 1.1958 | 1.2181 |

| -Bootstrap | 0.9640 | 1.2406 | 1.2158 | 1.1960 | 1.2193 |

| True Naive | 0.9596 | 1.3748 | 1.4894 | 1.5581 | 1.6309 |

| Estimated naive | 0.9641 | 1.3826 | 1.4910 | 1.5518 | 1.6084 |

We can find the MSPE of simulation- and bootstrap-based or optimal predictions are also very close to each other, respectively. Since the bootstrap optimal prediction is obtained with an estimated model and innovation distribution, it is not surprising that the MSPE is slightly larger than the simulation-based (oracle) optimal prediction, no matter if or is the loss criterion. In our expectation, the MSPE of simulation- and bootstrap-based prediction are all smaller than the MSPE of two naive predictions. Again, the importance of including the innovation effect in NLAR prediction is highlighted.

Rather than applying the standard normal innovation distribution, we also research the MSPE of different methods with a skewed innovation distribution. Take , here, we subtract 3 from for getting a mean-zero innovation distribution. Repeating the above procedure, we summarize the MSPE of all prediction approaches in Table 3.

| Prediction Horizon | 1 | 2 | 3 | 4 | 5 |

| -Simulation | 5.7351 | 6.1817 | 6.3648 | 6.8767 | 6.3593 |

| -Simulation | 6.1200 | 6.4845 | 6.6904 | 7.2933 | 6.7039 |

| -Bootstrap | 5.7885 | 6.1704 | 6.3679 | 6.8900 | 6.3749 |

| -Bootstrap | 6.1695 | 6.4643 | 6.6953 | 7.2931 | 6.7036 |

| True Naive | 5.7398 | 6.5561 | 6.8901 | 7.7830 | 7.4002 |

| Estimated naive | 5.7798 | 6.5294 | 6.8703 | 7.7172 | 7.2002 |

From there, the relative performance of different prediction methods is consistent to results implied by Table 2. Simulation-based methods are the best as expected; bootstrap-based methods give just slightly higher MSPE compared to the simulation-based method. Both computationally heavy methods outperform the naive methods.

Another notable phenomenon indicated by Table 3 is that the MSPE of optimal prediction is always less than its corresponding optimal prediction. This is reasonable since the optimal prediction is determined based on loss which coincides with the mean squared errors. However, for the simulation result in Table 2, this phenomenon is not remarkable since the innovation distribution is symmetric.

As we have clarified in 5.1, the constant parameter in Eq. 40 is important and can cover cases in which the mean of the innovation distribution is not zero. We present the MSPE of all prediction methods with in Table 4. Here, we can see the MSPE of bootstrap-based methods is still very close to the corresponding MSPE of simulation-based methods. The interesting finding is that the estimated naive approach also gives great MSPE values. The reason behind this phenomenon is that the estimated parameter value already includes the mean effects of the innovation distribution. On the other hand, the true naive estimation approach returns terrible MSPE, since the effects of innovation distribution are discarded.

| Prediction Horizon | 1 | 2 | 3 | 4 | 5 |

| -Simulation | 6.329292 | 6.066646 | 6.040300 | 6.358251 | 5.988886 |

| -Simulation | 6.831067 | 6.445046 | 6.413609 | 6.754066 | 6.352465 |

| -Bootstrap | 6.346281 | 6.099135 | 6.075808 | 6.378988 | 6.014661 |

| -Bootstrap | 6.836730 | 6.469492 | 6.440389 | 6.775695 | 6.366932 |

| True Naive | 15.818671 | 20.260416 | 23.381642 | 26.636934 | 29.088646 |

| Estimated naive | 6.335469 | 6.097773 | 6.080526 | 6.381737 | 6.021346 |

Beyond analyzing the performance of point prediction, we are also interested in measuring prediction accuracy by building PIs. As discussed before, we can build two types of bootstrap-based prediction intervals, (1) Quantile PI; (2) Pertinent PI. The advantage of pertinent PI is that it can be centered in the optimal or predictors. Moreover, it includes the estimation error of parameters into consideration, which means a superior empirical CVR, especially in short data size situations. For deriving pertinent PI, we take in Algorithm 6. We repeat experiment times and set significance level . Then, we compute empirical CVR of bootstrap-based QPI and PPI for step ahead predictions with the below formula:

| (44) |

where and represent -th step ahead prediction intervals and the true future value in the -th replication, respectively. Recall that the PPI can be centered at or optimal point predictor, thus we have three types of PIs based on bootstrap. Moreover, we can build PIs with fitted or predictive residuals. Besides, if all model information is known to us, we can use Algorithm 3 to get oracle QPI based on simulations. Thus, we totally have seven different PIs in hand. We denote them by (1) QPI-f, QPI with fitted residuals; (2) QPI-p, QPI with predictive residuals; (3) -PPI-f, PPI centered at optimal predictor with fitted residuals; (4) -PPI-p, PPI centered at optimal predictor with predictive residuals; (5) -PPI-f, PPI centered at optimal predictor with fitted residuals; (6) -PPI-p, PPI centered at optimal predictor with predictive residuals; (7) SPI, which is QPI based on simulations. In addition, since building a valid PI is more challenging work, we totally consider seven different models to check the feasibility of our methods:

-

•

Model 1: + .

-

•

Model 2: + .

-

•

Model 3: .

-

•

Model 4: .

-

•

Model 5: .

-

•

Model 6: .

-

•

Model 7: ,

where and is the indicator function which equals to 0 when and 1 otherwise. Models 1-2 are two different threshold models in the form , where are different non-overlapping intervals. The ergodicity can be guaranteed if , which is satisfied by Models 1-2. In addition, for Model 3 with heteroscedastic errors, A5 and A7 are also met so that the ergodicity is achieved. Model 4 is according to Eq. 40. The Models 5 is according to the form for positive . It is also in NLAR form and ergodic by checking the first condition of An and Huang, (1996), but they are simpler compared to Model 4. For Models 6 and 7, they have a general form: for . The ergodicity of this model is guaranteed by checking A6. All simulation results of CVR are summarized in Tables 5, 6, 7, 8, 9, 10 and 11. Besides the analyses of CVR, we are also concerned about the average length of PIs of different methods. In practice, a wide PI is less useful even though it has great coverage probability. We define the average length (LEN) of PIs as below:

| (45) |

where and are higher and lower bounds of the -th step ahead PI in the -th replication, respectively. Accordingly, we present LEN of different PIs along with CVR in Tables 5, 6, 7, 8, 9, 10 and 11.

Remark 5.2.

We should clarify that the CVR computed by Eq. 44 is the unconditional coverage rate of since it is an average of the conditional coverage of for all replications. Also, when the sample size is small, we may get parameter estimations that make the time series close to be unstationary, especially for estimating different regions of a threshold model where the sample size further decreases. This will destroy our prediction process when multi-step ahead predictions are required. Thus, we redo the simulation once we find such abnormal larger or small predictions.

From these simulations, the first thing we can notice is that all CVR for SPI are great and close to the oracle coverage level even for short data, which implies the simulation-based approach works well once we know the true model and innovation distribution. For , we can find all PPIs work well and are even competitive compared to the SPI. On the other hand, the QPI with fitted residuals is the worst one, especially for complicated Models 6 and 7. By applying predictive residuals, the CVR gets improved for QPI. For , no matter with fitted or predictive residuals, PPIs dominate QPIs. Generally speaking, PI with predictive residuals works better than the corresponding one with fitted residuals. The naive QPI with fitted residuals is still the worst method among all choices. For , the gap between applying fitted residuals and predictive residuals gets amplified. All PIs with predictive residuals work better than the corresponding ones with fitted residuals. Moreover, the gap between QPI and PPI also gets amplified. The simple QPI with fitted residuals only returns around 85 and 89 CVR for 5-step ahead predictions of Model 6 and Model 2, respectively. On the other hand, the PPI with predictive residuals achieves more than 90 and 93 CVR, respectively. For the LEN of different PIs, we can find that LENs of SPIs are barely changed for a specific model with various sample sizes. This is in our expectation since SPI is oracle and we can approximate the true quantile region of future value by simulation even with 50 sample points. Also, compared to the LEN of PPI and QPI, SPI tends to have smaller LEN, but possesses more accurate CVR due to the oracle property again. For PPI, although its LEN tends to be slightly larger than the LEN of SPI and QPI, it is the best bootstrap-type PI according to the CVR. Based on these simulation results, we summarize some important conclusions below:

-

•

If we know the parameters of the model and innovation distribution, SPI can work well and give accurate CVR even for short data, but it is usually unrealistic in practice.

-

•

If we do not have model information and the data is short, PPI with predictive residuals is the best method, which can give competitive performance compared to SPI for simple models. However, the QPI can not cover future values well and its CVR is severely lower than oracle level.

-

•

If we do not have model information and the data in hand is large enough, both QPI and PPI work well.

-

•

Since in practice we can not judge whether the data in hand is large enough for the problem at hand, using the PPI (with predictive residuals) is recommendable.

Remark 5.3.

To perform bootstrap-based prediction, we ran simulations in a parallel fashion using 30 Xeon(R) E5-2630 CPUs. Besides, we should notice that the constant parameter inside the function of Model 6 is the hardest one to be estimated, since the low change rate of the partial derivative. This may be the reason for the relatively poor performance of bootstrap-based prediction methods on Model 6.

| Model 1: | + | |||||||||

| CVR for each step | LEN for each step | |||||||||

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | |

| QPI-f | 0.9456 | 0.9472 | 0.9478 | 0.9496 | 0.9484 | 3.89 | 4.60 | 4.87 | 5.01 | 5.07 |

| QPI-p | 0.9470 | 0.9468 | 0.9478 | 0.9502 | 0.9500 | 3.91 | 4.62 | 4.90 | 5.03 | 5.09 |

| -PPI-f | 0.9474 | 0.9454 | 0.9486 | 0.9500 | 0.9514 | 3.90 | 4.61 | 4.89 | 5.03 | 5.09 |

| -PPI-p | 0.9474 | 0.9480 | 0.9480 | 0.9510 | 0.9526 | 3.92 | 4.63 | 4.92 | 5.05 | 5.12 |

| -PPI-f | 0.9468 | 0.9456 | 0.9494 | 0.9494 | 0.9520 | 3.90 | 4.61 | 4.89 | 5.03 | 5.09 |

| -PPI-p | 0.9464 | 0.9468 | 0.9484 | 0.9512 | 0.9530 | 3.92 | 4.63 | 4.92 | 5.05 | 5.12 |

| SPI | 0.9484 | 0.9474 | 0.9500 | 0.9502 | 0.9546 | 3.90 | 4.62 | 4.91 | 5.04 | 5.10 |

| QPI-f | 0.9388 | 0.9408 | 0.9362 | 0.9328 | 0.9330 | 3.86 | 4.52 | 4.78 | 4.91 | 4.97 |

| QPI-p | 0.9438 | 0.9446 | 0.9394 | 0.9366 | 0.9352 | 3.94 | 4.61 | 4.88 | 5.00 | 5.07 |

| -PPI-f | 0.9416 | 0.9424 | 0.9382 | 0.9350 | 0.9358 | 3.91 | 4.58 | 4.85 | 4.98 | 5.05 |

| -PPI-p | 0.9478 | 0.9478 | 0.9442 | 0.9396 | 0.9402 | 3.99 | 4.67 | 4.94 | 5.08 | 5.15 |

| -PPI-f | 0.9428 | 0.9430 | 0.9376 | 0.9346 | 0.9358 | 3.91 | 4.58 | 4.85 | 4.97 | 5.04 |

| -PPI-p | 0.9476 | 0.9482 | 0.9442 | 0.9402 | 0.9404 | 3.99 | 4.67 | 4.94 | 5.07 | 5.14 |

| SPI | 0.9502 | 0.9482 | 0.9464 | 0.9468 | 0.9460 | 3.90 | 4.61 | 4.89 | 5.03 | 5.09 |

| QPI-f | 0.9168 | 0.9248 | 0.9204 | 0.9106 | 0.9218 | 3.74 | 4.44 | 4.69 | 4.81 | 4.87 |

| QPI-p | 0.9296 | 0.9360 | 0.9334 | 0.9238 | 0.9324 | 3.91 | 4.63 | 4.90 | 5.02 | 5.09 |

| -PPI-f | 0.9306 | 0.9318 | 0.9268 | 0.9176 | 0.9306 | 3.91 | 4.57 | 4.83 | 4.96 | 5.04 |

| -PPI-p | 0.9402 | 0.9438 | 0.9392 | 0.9292 | 0.9390 | 4.07 | 4.76 | 5.04 | 5.18 | 5.26 |

| -PPI-f | 0.9302 | 0.9314 | 0.9264 | 0.9170 | 0.9300 | 3.91 | 4.56 | 4.82 | 4.95 | 5.02 |

| -PPI-p | 0.9390 | 0.9438 | 0.9366 | 0.9290 | 0.9364 | 4.08 | 4.75 | 5.03 | 5.16 | 5.24 |

| SPI | 0.9486 | 0.9492 | 0.9508 | 0.9452 | 0.9464 | 3.90 | 4.61 | 4.90 | 5.03 | 5.09 |

| Model 2: | + | |||||||||

| CVR for each step | LEN for each step | |||||||||

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | |

| QPI-f | 0.9420 | 0.9506 | 0.9468 | 0.9444 | 0.9372 | 3.88 | 4.68 | 5.11 | 5.40 | 5.58 |

| QPI-p | 0.9462 | 0.9512 | 0.9502 | 0.9474 | 0.9428 | 3.92 | 4.72 | 5.16 | 5.45 | 5.64 |

| -PPI-f | 0.9446 | 0.9510 | 0.9486 | 0.9470 | 0.9408 | 3.90 | 4.71 | 5.15 | 5.44 | 5.63 |

| -PPI-p | 0.9466 | 0.9542 | 0.9516 | 0.9494 | 0.9434 | 3.94 | 4.75 | 5.20 | 5.49 | 5.69 |

| -PPI-f | 0.9448 | 0.9518 | 0.9478 | 0.9468 | 0.9402 | 3.90 | 4.71 | 5.15 | 5.44 | 5.62 |

| -PPI-p | 0.9470 | 0.9544 | 0.9500 | 0.9486 | 0.9436 | 3.94 | 4.75 | 5.20 | 5.49 | 5.68 |

| SPI | 0.9446 | 0.9534 | 0.9508 | 0.9510 | 0.9454 | 3.90 | 4.71 | 5.16 | 5.46 | 5.65 |

| QPI-f | 0.9270 | 0.9304 | 0.9294 | 0.9272 | 0.9250 | 3.81 | 4.57 | 4.98 | 5.23 | 5.40 |

| QPI-p | 0.9370 | 0.9412 | 0.9368 | 0.9372 | 0.9372 | 3.98 | 4.76 | 5.19 | 5.46 | 5.63 |

| -PPI-f | 0.9358 | 0.9352 | 0.9338 | 0.9314 | 0.9298 | 3.95 | 4.71 | 5.13 | 5.40 | 5.59 |

| -PPI-p | 0.9454 | 0.9454 | 0.9444 | 0.9430 | 0.9418 | 4.10 | 4.90 | 5.34 | 5.63 | 5.83 |

| -PPI-f | 0.9364 | 0.9360 | 0.9336 | 0.9310 | 0.9304 | 3.95 | 4.71 | 5.13 | 5.39 | 5.58 |

| -PPI-p | 0.9450 | 0.9456 | 0.9432 | 0.9422 | 0.9412 | 4.11 | 4.90 | 5.33 | 5.62 | 5.81 |

| SPI | 0.9446 | 0.9472 | 0.9498 | 0.9474 | 0.9478 | 3.90 | 4.71 | 5.16 | 5.46 | 5.65 |

| QPI-f | 0.8980 | 0.9054 | 0.9018 | 0.8950 | 0.8926 | 3.66 | 4.47 | 4.87 | 5.14 | 5.38 |

| QPI-p | 0.9260 | 0.9314 | 0.9272 | 0.9218 | 0.9212 | 4.05 | 4.97 | 5.42 | 5.74 | 5.99 |

| -PPI-f | 0.9340 | 0.9268 | 0.9214 | 0.9164 | 0.9152 | 4.22 | 5.10 | 5.86 | 6.89 | 8.97 |

| -PPI-p | 0.9522 | 0.9478 | 0.9404 | 0.9400 | 0.9376 | 4.60 | 5.57 | 6.36 | 7.33 | 9.03 |

| -PPI-f | 0.9338 | 0.9268 | 0.9194 | 0.9144 | 0.9130 | 4.23 | 5.09 | 5.82 | 6.79 | 8.71 |

| -PPI-p | 0.9522 | 0.9482 | 0.9384 | 0.9378 | 0.9356 | 4.61 | 5.55 | 6.30 | 7.20 | 8.71 |

| SPI | 0.9494 | 0.9448 | 0.9464 | 0.9458 | 0.9462 | 3.90 | 4.71 | 5.16 | 5.46 | 5.65 |

| Model 3: | ||||||||||

| CVR for each step | LEN for each step | |||||||||

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | |

| QPI-f | 0.9478 | 0.9442 | 0.9526 | 0.9444 | 0.9418 | 1.47 | 1.74 | 1.82 | 1.84 | 1.85 |

| QPI-p | 0.9474 | 0.9486 | 0.9504 | 0.9444 | 0.9432 | 1.47 | 1.74 | 1.82 | 1.84 | 1.85 |

| -PPI-f | 0.9520 | 0.9488 | 0.9542 | 0.9436 | 0.9434 | 1.59 | 2.22 | 2.24 | 2.30 | 2.29 |

| -PPI-p | 0.9510 | 0.9486 | 0.9522 | 0.9454 | 0.9446 | 1.64 | 2.37 | 2.37 | 2.44 | 2.42 |

| -PPI-f | 0.9514 | 0.9480 | 0.9540 | 0.9448 | 0.9440 | 1.63 | 1.88 | 2.10 | 2.17 | 2.18 |

| -PPI-p | 0.9480 | 0.9514 | 0.9530 | 0.9474 | 0.9448 | 1.68 | 1.92 | 2.19 | 2.27 | 2.28 |

| SPI | 0.9500 | 0.9500 | 0.9516 | 0.9444 | 0.9442 | 1.47 | 1.74 | 1.82 | 1.84 | 1.85 |

| QPI-f | 0.9344 | 0.9388 | 0.9420 | 0.9390 | 0.9372 | 1.47 | 1.73 | 1.81 | 1.84 | 1.85 |

| QPI-p | 0.9318 | 0.9348 | 0.9404 | 0.9392 | 0.9378 | 1.47 | 1.73 | 1.82 | 1.84 | 1.86 |

| -PPI-f | 0.9406 | 0.9418 | 0.9452 | 0.9418 | 0.9434 | 1.55 | 2.08 | 2.11 | 2.13 | 2.11 |

| -PPI-p | 0.9424 | 0.9422 | 0.9452 | 0.9410 | 0.9452 | 1.64 | 2.40 | 2.38 | 2.40 | 2.36 |

| -PPI-f | 0.9400 | 0.9426 | 0.9464 | 0.9430 | 0.9440 | 1.60 | 1.91 | 2.01 | 2.02 | 2.03 |

| -PPI-p | 0.9398 | 0.9440 | 0.9466 | 0.9412 | 0.9454 | 1.72 | 2.04 | 2.16 | 2.17 | 2.18 |

| SPI | 0.9482 | 0.9474 | 0.9506 | 0.9518 | 0.9456 | 1.47 | 1.74 | 1.82 | 1.84 | 1.85 |

| QPI-f | 0.9060 | 0.9268 | 0.9266 | 0.9222 | 0.9302 | 1.43 | 1.71 | 1.80 | 1.83 | 1.84 |

| QPI-p | 0.9030 | 0.9286 | 0.9262 | 0.9206 | 0.9312 | 1.44 | 1.73 | 1.82 | 1.85 | 1.87 |

| -PPI-f | 0.9300 | 0.9394 | 0.9350 | 0.9338 | 0.9408 | 1.55 | 3.37 | 3.34 | 3.23 | 3.11 |

| -PPI-p | 0.9302 | 0.9414 | 0.9358 | 0.9372 | 0.9398 | 1.64 | 3.85 | 3.74 | 3.60 | 3.44 |

| -PPI-f | 0.9302 | 0.9410 | 0.9358 | 0.9356 | 0.9412 | 1.61 | 2.39 | 2.58 | 2.54 | 2.50 |

| -PPI-p | 0.9308 | 0.9422 | 0.9364 | 0.9384 | 0.9412 | 1.79 | 2.79 | 2.81 | 2.74 | 2.68 |

| SPI | 0.9486 | 0.9520 | 0.9486 | 0.9444 | 0.9518 | 1.47 | 1.74 | 1.81 | 1.84 | 1.85 |

| Model 4: | ||||||||||

| CVR for each step | LEN for each step | |||||||||

| 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 | |

| QPI-f | 0.9498 | 0.9446 | 0.9482 | 0.9444 | 0.9444 | 3.89 | 4.30 | 4.33 | 4.33 | 4.33 |