Entropy Bounds for Invariant Measure Perturbations in Stochastic Systems with Uncertain Noise

Abstract

This paper is concerned with stochastic systems whose state is a diffusion process governed by an Ito stochastic differential equation (SDE). In the framework of a nominal white-noise model, the SDE is driven by a standard Wiener process. For a scenario of statistical uncertainty, where the driving noise acquires a state-dependent drift and thus deviates from its idealised model, we consider the perturbation of the invariant probability density function (PDF) as a steady-state solution of the Fokker-Planck-Kolmogorov equation. We discuss an upper bound on a logarithmic Dirichlet form for the ratio of the invariant PDF to its nominal counterpart in terms of the Kullback-Leibler relative entropy rate of the actual noise distribution with respect the Wiener measure. This bound is shown to be achievable, provided the PDF ratio is preserved by the nominal steady-state probability flux. The logarithmic Dirichlet form bound is used in order to obtain an upper bound on the relative entropy of the perturbed invariant PDF in terms of quadratic-exponential moments of the noise drift in the uniform ellipticity case. These results are illustrated for perturbations of Gaussian invariant measures in linear stochastic systems involving linear noise drifts.

keywords:

stochastic system; diffusion process; uncertain noise; Fokker-Planck-Kolmogorov equation; invariant measure; logarithmic Dirichlet form; relative entropy.1 Introduction

Continuous-time physical systems subject to external random noise (and artificial dynamical systems such as stochastic optimization algorithms with intentionally introduced randomness) are often described by Ito SDEs for the evolution of a finite-dimensional state vector driven by a standard Wiener process or more complicated Ito processes [39]. The dynamics of the noise itself are usually modelled by a shaping filter, also in the form of an SDE, which can be incorporated in the system, so that the resulting augmented system is driven by a standard Wiener process. The statistical structure of the system state then corresponds to a diffusion process whose PDF (provided it exists and is sufficiently smooth) evolves in time according to the Fokker-Planck-Kolmogorov equation (FPKE) [10, 43, 45] which is a linear second-order partial differential equation of parabolic type.

In the presence of dissipative effects (strong enough to make the system stable), the FPKE usually has a unique normalised steady-state solution describing the invariant measure for the Markovian dynamics of the system state. However, unmodelled dynamics can lead to deviations of the actual probability law of the driving noise from its nominal white-noise model which assumes the noise to be a standard Wiener process. Interpreted as a statistical uncertainty, such deviation from the Wiener measure arises, for example, when the external noise acquires a state-dependent drift through a “parasitic” feedback coming from the interaction of the system with its environment. The latter is exemplified by acoustic resonance, electromagnetic interference in circuitry, or fluid-structure coupling in turbulent flows. The presence of an unknown state-dependent drift in the noise (making it statistically uncertain and “coloured”) modifies the drift term of the SDE which governs the system dynamics, and this, in turn, changes the invariant measure of the system.

Assuming that the FPKE for the perturbed system also has a unique steady-state solution, the present paper investigates the influence of the noise drift on the resulting perturbation in the invariant PDF of the system state variables. This perturbation is formulated using the ratio of the invariant PDF for the perturbed system to the nominal invariant PDF (which the system would have in the nominal white-noise case). We discuss an entropy identity for the noise drift (as a function of the system state) and the logarithmic PDF ratio and derive from it an upper bound for a diffusion-weighted logarithmic Dirichlet form in terms of the second moment of the noise drift over the invariant PDF. Up to a factor of , this moment (which quantifies the “size” of the noise drift) coincides with the rate of the Kullback-Leibler relative entropy [18] of the probability law of the noise with respect to the Wiener measure.

Entropy and information theoretic quantification of statistical uncertainty is employed in a number of approaches to stochastic robust control, including the anisotropy-based theory [49] (see also [56] and references therein), minimax LQG control [42, 48] (with its links [21, 41] to risk-sensitive control), and other control settings with entropy functionals [16, 46]. Entropy theoretic criteria also underlie the Schrödinger bridge, which is a state PDF transition problem with relative entropy minimisation, considered both for classical [3, 6, 19, 35] and quantum [4] systems using the formalism of stochastic mechanics [37] (see also [15, 17, 40, 50, 51] and references therein).

Accordingly, the upper bound on the logarithmic Dirichlet form quantifies the influence of the statistical uncertainty in the noise on the deviation of the invariant PDF of the system from its nominal counterpart. We show that this bound is tight in the sense that it is achievable at a particular noise drift, provided the PDF ratio is preserved along the divergenceless probability flux [43] associated with the nominal invariant measure of the system. The logarithmic Dirichlet form bound is combined with the logarithmic Sobolev inequality [2, 25, 26, 32] in order to obtain upper bounds on the Fisher [44] and Kullback-Leibler relative entropies of the invariant PDF of the perturbed system state with respect to its nominal counterpart in the case when the diffusion matrix satisfies the uniform ellipticity condition [22] and the nominal invariant PDF has strong logarithmic concavity. These results are illustrated for perturbations of Gaussian invariant measures in linear stochastic systems (governed by SDEs with a linear drift and constant diffusion) caused by linear noise drifts.

We mention that regularity of solutions of stationary FPKEs was previously studied, for example, in [7, 8, 9, 10, 11, 12, 34]. In particular, their behaviour under drift perturbations for the Ornstein-Uhlenbeck process is considered in [12], and differentiability of the invariant measure over a parameter of the drift vector and diffusion matrix is discussed in [11]. Also, Lemma 2 of the present paper can be derived by using appropriate modifications of [7, Theorem 3.1], [8, Theorem 1.1], [9, Theorem 2.4] on logarithmic Dirichlet forms. However, our results are directly oriented to specific drift perturbations considered in this work under conditions of classical smoothness and vector field decay at infinity. Also, we employ a variational formula from [20, Eq. (1.15)] (similarly to the way it is used in minimax LQG control) in order to obtain entropy bounds for the invariant PDF perturbation in terms of nominal quadratic-exponential moments of the noise drift. Such moments (with integrals or sums of quadratic forms over time) are typical for classical [5, 29, 55] and quantum [13, 52, 53, 54] risk-sensitive control. Furthermore, since the entropy inequalities use, as a gain coefficient, the reciprocal to the product of the uniform ellipticity and logarithmic concavity constants, we investigate the asymptotic behaviour of the entropy bound for small values of the coefficient and provide a lower bound for this coefficient in terms of the mean divergence of the drift in the nominal system dynamics.

The paper is organised as follows. Section 2 describes the class of stochastic systems with statistically uncertain noise under consideration. Section 3 specifies the actual and nominal invariant PDFs along with FPKEs for such a system. Section 4 establishes the logarithmic Dirichlet form bound for the PDF ratio. Section 5 discusses the achievability of the upper bound along with the noise drift which saturates it. Section 6 obtains upper bounds on the Fisher and Kullback-Leibler relative entropies for the PDF perturbation in the uniform ellipticity case. Section 7 illustrates the results for linear stochastic systems with linear noise drifts and Gaussian PDFs. Section 8 provides a numerical example on perturbed Langevin dynamics. Section 9 makes concluding remarks.

2 Uncertain Stochastic Systems

We consider a stochastic system whose state is an -valued diffusion process governed by an Ito SDE

| (1) |

where the drift vector and the dispersion matrix are specified by given maps and in the appropriate spaces of (respectively, once and twice) continuously differentiable functions. The SDE (1) is driven by an external random noise which is an -valued Ito process on an underlying probability space with a filtration (of -algebras of events for any ) satisfying the usual conditions [30], with the initial system state being -measurable. The stochastic differential of is assumed to be in the form

| (2) |

(with zero initial condition , without loss of generality), where the drift vector is described by a map , and is an -valued standard Wiener process with respect to the filtration (and hence, independent of ). In what follows, is assumed to be the natural filtration of the pair , so that for any , the -algebra is generated by and the past history of the process over the time interval :

| (3) |

The presence of an unknown drift in (2) makes a statistically uncertain “coloured” noise, which (in contrast to ) is, in general, correlated with . As a consequence, for any fixed but otherwise arbitrary time horizon , the probability distribution of the random element (as an -measurable map from to ) can differ from the Wiener measure on the measurable space . Here, is the Banach space of continuous functions vanishing at the origin and endowed with the uniform norm, and is the Borel -algebra generated by open subsets of . The Wiener measure plays the role of an idealised white-noise model for , which would hold if the SDE (2) were driftless, leading to and the nominal system dynamics

| (4) |

The above described statistical uncertainty (where deviates from ) results from a feedback loop (due to interaction of the system with its environment) depicted schematically in Fig. 1, which refers to the integral form of the SDEs (1), (2).

In order to guarantee the existence and uniqueness of a solution for the SDE

| (5) |

obtained by substituting (2) into (1), and also for its nominal counterpart (4), it is assumed (see, for example, [39, Theorem 5.2.1]) that the initial state has finite second moments (, where is expectation), and the maps , , , are Lipschitz (and hence, have at most linear growth at infinity). Under Novikov’s condition [38]

| (6) |

where is the usual Euclidean norm, and is the nominal expectation (which considers in (1) a standard Wiener process independent of ), the Kullback-Leibler relative entropy of the distribution of (conditioned on ) with respect to the Wiener measure admits the representation

| (7) |

Recall [18] that the relative entropy of a probability measure on a measurable space with respect to a reference probability measure on the same space is defined as (under absolute continuity , with the logarithm of the Radon-Nikodym derivative being averaged over as the actual probability measure). This definition is combined in (7) with Girsanov’s theorem [24], whereby the corresponding log-likelihood ratio takes the form

| (8) |

so that (7) results from averaging (8) in accordance with the actual noise and system dynamics (2), (5), including the fact that is a standard Wiener process independent of . The noise relative entropy in (7) quantifies the deviation of the probability law of from that of (that is, the Wiener measure) over the time interval and thus vanishes in the nominal case when .

3 Actual and Nominal Invariant Measures

Under the parabolic Hörmander condition [27, 45], the value of the diffusion process in (5) at any time is an absolutely continuously distributed random vector with a smooth PDF (with respect to the Lebesgue measure in ) satisfying the FPKE

| (9) |

where is a linear differential operator acting on a function as

| (10) |

and the map , with values in the set of positive semi-definite matrices in the subspace of real symmetric matrices of order , describes the diffusion matrix:

| (11) |

Here, repeated application of the divergence operator to a function yields the maps and , where is the partial derivative over the th Cartesian coordinate in . In accordance with the divergence theorem, in (10) is the formal adjoint [45] of the infinitesimal generator for the diffusion process , acting on a function with the gradient vector and the Hessian matrix as

| (12) |

where is the Frobenius inner product [28] of real matrices. Using the notation for functions with an integrable point-wise product , a sufficient condition for the adjointness relation to hold is provided by the property that the pair is -decaying as specified below.

Definition 1.

For given maps and , the pair of functions is said to be -decaying if the following vector field (as an -valued function of ) satisfies

| (13) |

The decay condition in (13) (which is weaker than the requirement that or has compact support) is a joint property of , , , at infinity. Its meaning is clarified by integrating both sides of the identity (similar to those in Green’s formulas) over a ball of radius and applying the divergence theorem along with the fact that the decay rate of the vector field in (13) makes its flux through the sphere asymptotically vanish: , where is the oriented surface area element (with the outward normal). For any function with nonzero values, . In the case of , this transformation follows from the representation

| (14) |

We assume that the FPKE (9) has a unique steady-state solution (with the normalization ):

| (15) |

The invariant PDF is, in general, different from another invariant PDF which the system would have in the nominal case of in (2). The nominal invariant PDF , which is also assumed to exist and be unique in subject to the normalization , satisfies

| (16) |

where

| (17) | ||||

| (18) |

are the nominal versions of (10), (12), respectively, with .

4 Logarithmic Dirichlet Form Bound

In what follows, we will discuss an entropy identity in order to obtain an upper bound for the discrepancy between the invariant PDF of the perturbed system and its nominal counterpart . The bound will be formulated in terms of a steady-state second moment of the noise drift map over . To this end, we will use the PDF ratio

| (19) |

which is well-defined on the set , provided vanishes whenever does, thus making the invariant measure of the system absolutely continuous with respect to the nominal invariant measure. For simplicity, both PDFs and are assumed to be positive everywhere, and hence, the property is inherited from them. Also, we will use a function associated by

| (20) |

with the dispersion matrix map and the PDF ratio (19). In view of the factorisation (11) of the diffusion matrix,

| (21) |

where is a weighted Euclidean (semi-) norm of a real vector , specified by a real positive (semi-) definite symmetric matrix . If everywhere in , then the ratio (19) reduces to , and the function in (20) (and its point-wise norm (21)) is the identical zero.

Lemma 2.

Suppose the generator in (12), evaluated at the logarithmic PDF ratio from (19), the noise drift map in (2) and the function in (20) have the following finite moments

| (22) |

over the invariant PDF of the perturbed system (5) in (15). Also, suppose the pair is -decaying, while is -decaying in the sense of Definition 1. Then

| (23) |

In application to the generator in (12) and the PDF ratio in (19), the Fleming logarithmic transformation [23] (see also [4, Eq. (81) on p. 201]) leads to

| (24) |

Here, use is also made of (21) and an auxiliary differential operator , which acts on a function as

| (25) |

in accordance with (5), (12), (18). Application of (25) to yields

| (26) |

where the last equality uses (20). By combining (24) with (26), it follows that

| (27) |

In view of (22) and the Cauchy-Bunyakovsky-Schwarz inequality

| (28) |

the right-hand side of (27) has a finite expectation over the PDF , and hence, so also does its left-hand side:

| (29) |

Now, since the pair is assumed to be -decaying, then

| (30) |

where the rightmost equality follows from (15). Due to the PDF change identity from (19), the left-hand side of (29) can be represented in terms of the nominal expectation :

| (31) |

where the last two equalities use (16) and the condition that the pair is -decaying. The relation (23) is now obtained by substitution of (30), (31) into (29).

Note that the identity (23) is of entropy theoretic nature. More precisely, suppose the system (5) is initialised at its invariant PDF from (15). Then its state vector retains this PDF at any time . In particular, assuming that , the following quantity remains constant:

| (32) |

which, in view of (19), is the relative entropy of the invariant PDF with respect to its nominal counterpart (we slightly abuse notation by referring to the densities instead of the distributions). On the other hand, from the Ito lemma [30] combined with (5), (12), (20) along with the first and third conditions in (22), it follows that is an Ito process with the stochastic differential

| (33) |

Here,

| (34) |

is a square integrable martingale [39] (with zero mean and variance for any by the Ito isometry) with respect to the natural filtration of the pair given by (3). Therefore, in view of (33), the equalities (30) represent the fact that the time derivative of the relative entropy (32) vanishes: , which is not affected by the martingale (34).

The following theorem is a direct corollary of Lemma 2.

Theorem 3.

By combining (23) with (28), it follows that

| (36) |

and hence, , which establishes (35). An alternative (yet equivalent) argument employs the determinant of a positive semi-definite Gram matrix as

| (37) |

Recalling (21), note that the nonnegative quantity on the left-hand side of (35) is a diffusion-weighted Dirichlet form [22] for the logarithmic PDF ratio.

In view of (7) (assuming that the sufficient condition (6) is satisfied), the inequality (35) can also be represented as

| (38) |

where the limit is the relative entropy rate of the input noise and coincides with for any time horizon if the initial system state has the invariant PDF . This limit quantifies the ease of detecting the drift in the noise based on the strong law of large numbers which manifests itself in sufficiently long samples of the log-likelihood ratio (8) (see, for example, [33]). The latter consideration motivates the following definition.

5 Upper Bound Achievability

The inequality (35) is tight in the sense that it becomes an equality (as do the inequalities in (28), (36), (37)) if the noise drift map in (2) is related to the PDF ratio through (20) by

| (40) |

However, this relation is not necessarily compatible with being an invariant PDF satisfying (15) and its nominal counterpart in (16). A condition for such compatibility is provided by the following theorem in terms of an auxiliary vector field (a steady-state probability flux [43]) in given by

| (41) |

Theorem 5.

By using the identity from (19), it follows that

| (43) | ||||

| (44) |

Therefore, substitution of (43), (44) into (17) leads to

| (45) |

where use is made of (16) along with the vector field from (41). Now, if the relation (40) is satisfied, then in view of (11), and hence, the adjoint of the operator in (25) acts on the invariant PDF as

| (46) |

By taking the sum of the right-hand sides of (45) and (46), it follows that in the case of the noise drift map (40),

| (47) |

A comparison of (47) with (15) leads to (42), which is equivalent to in (41) being tangent to the level hypersurfaces of the PDF ratio , or the property that is a first integral of motion for the incompressible flow in generated by .

6 Entropy Bounds on PDF perturbation

The inequality (35) is particularly useful when the diffusion matrix map in (11) satisfies the uniform ellipticity condition [22]

| (48) |

(with the smallest eigenvalue of a real symmetric matrix), and hence, with necessity, the dispersion matrix is of full row rank for all , so that . In this case, (21) admits a lower bound which leads to the inequality

| (49) |

whose left-hand side is the Fisher relative entropy (originating from the Fisher information for the shift parameter; see, for example, [44, Eq. (1.4)]). By the probabilistic version [2] of the logarithmic Sobolev inequalities [25, 26, 32], the Kullback-Leibler relative entropy in (32) satisfies

| (50) |

provided the function is strongly concave in the sense that its Hessian matrix is uniformly negative definite:

| (51) |

where is the largest eigenvalue. In contrast to in (48), the quantity in (51) depends not only on the diffusion part of the nominal SDE (4) for the system, but also on the drift map (we will address this dependence in Lemma 8). A combination of (49) with (50) and (35) of Theorem 3 leads to

| (52) |

where

| (53) |

is an auxiliary quantity which has the physical dimension of time. In particular, for -stealthy noise drift maps (as specified by the relative entropy threshold in (39) and motivated by (38) under the sufficient condition (6)), the inequality (52) yields

| (54) |

The last inequality describes the influence of such deviations of the actual noise in (2) from its nominal white-noise model on the discrepancy between the corresponding PDFs and , so that, up to a factor of , the quantity from (53) plays the role of a gain coefficient for this influence.

While the condition (39) and the corresponding bound (54) are formulated in terms of over the invariant PDF , it is also possible to develop (52) in an alternative direction, which (instead of (39)) employs moments of over the nominal invariant PDF and takes into account the deviation of from in computing the right-hand side of (52). More precisely, it follows from (52) that

| (55) |

where is a nondecreasing function defined as

| (56) |

that is, the largest mean square of over those PDFs whose deviation from is bounded in terms of the relative entropy constraint. In particular, . The maximal solution of (55) provides the upper bound

| (57) |

Now, the function in (56) can be computed through the variational formula of [20, Proposition 1.4.2 on pp. 33, 34] as

| (58) |

where the ratio is set to its limit values or by continuity at if or , respectively. Here, use is made of the cumulant-generating function (CGF) for associated by

| (59) |

with a quadratic-exponential moment of the noise drift map over the PDF :

| (60) |

that is, the nominal moment-generating function for . Here, plays the role of a risk-sensitivity parameter and, similarly to , has the physical dimension of time. With , we assume that is finite at least for some , so that

| (61) |

and hence, (accordingly, ) for any . Note that if the system state is initialised at the PDF and obeys the nominal SDE (4), then (61) secures the fulfillment of the Novikov condition (6) for any :

where Jensen’s inequality is combined with the convexity of the exponential function, and (60) is used. Except for the trivial case of being an identical constant (we exclude it from consideration), the CGF in (59) is strictly increasing and strictly convex, with positive first and second derivatives , , which, together with implies that for any , the infimum in (58) is achieved at a unique point . Here, is the inverse of a strictly increasing differentiable function defined as the Bregman divergence [14] for at the points , (with ):

| (62) |

so that, due to the representation (58), the function in (56) takes the form

| (63) |

Since the strictly increasing function , associated with (62) and used in (63), maps onto the interval , then the set on the right-hand side of (57) is the image

| (64) |

of another set

| (65) |

By the structure (62) of the function , the inequality in (65) is equivalent to

| (66) |

whose left-hand side satisfies and is strictly increasing over since

| (67) |

where in accordance with the strict convexity of mentioned above. Hence, if

| (68) |

then the maximal solution of the inequality (66), which is related to the set (65) by , is found uniquely from

| (69) |

and satisfies

| (70) |

Therefore, due to (64), the upper bound (57) acquires the following form (its proof is provided by the above discussion).

Theorem 6.

Suppose the uniform ellipticity (48) for the diffusion matrix and the strong logarithmic concavity (51) for the nominal invariant PDF are satisfied. Also, suppose the function for the noise drift map in (2) is not identically constant and satisfies (61). Then the relative entropy in (32) admits the upper bound

| (71) |

in terms of the gain coefficient from (53) and the unique solution of (69), where the function is associated by (66) with the nominal CGF of from (59).

The inequality (71) is also applicable to other measures of deviation of from , which are bounded in terms of the Kullback-Leibler relative entropy. For example, a combination of Pinsker’s inequality [47, Lemma 2.5 on p. 88] with (71) leads to an upper bound for the -distance:

| (72) |

The relations (68)–(71) (and their corollary (72)) can be reformulated in a “small-gain” fashion: for any fixed but otherwise arbitrary , the following implication holds:

| (73) |

In turn, the entropy bound (73) can be applied not only to other distance measures for the PDFs as in (72), but also to obtaining guaranteed upper bounds on a cost functional in the form of a generalised moment of the system variables specified by a function : , which, similarly to (56), (58)–(60), employs the variational formula together with the nominal CGF for .

In practical calculations, the solution of the equation (69) for computing as a function of , or the inversion of for finding the critical value of versus in (73), can be avoided by parameterising this curve in the -plane as

| (74) |

For small values of , the upper bound in (71) behaves asymptotically as , which corresponds to neglecting the discrepancy between and on the right-hand side of (52). The next term in the asymptotic expansion of , as , which takes into account the deviation of from , is provided below.

Theorem 7.

By the implicit function theorem, the solution of (69) is a strictly increasing differentiable function of , with in view of (67), (70) and since from (66) for any . This monotonicity implies the existence of a limit . From the convergence , as , which is uniform over for any , it follows that due to (69), and hence, :

| (77) |

By (59)–(62), the functions , satisfy the asymptotic relations

| (78) | ||||

| (79) |

Here, the property is used along with the first two cumulants of over the nominal invariant PDF :

| (80) |

where the second cumulant is the nominal variance of given by (76). Due to (77), a combination of (78), (79) with the equality on the right-hand side of (71) leads to the asymptotic equivalence , and hence,

| (81) |

Therefore, , and substitution of (81) into (79) yields

| (82) |

The relation (75) for the right-hand side of (71) now follows from (82) in view of (80).

Since the entropy bounds (54), (71) involve the coefficient from (53), and the asymptotic relation (75) pertains to its small values, of relevance is the following lower bound for in terms of the drift part of the nominal system dynamics (4).

Lemma 8.

Similarly to (30), (31) in the proof of Lemma 2, from the first condition in (83), the assumption that is -decaying and from (16), it follows that

| (85) |

The second condition in (83) and the assumption that is -decaying (that is, , as , in accordance with (13) with , , , ) imply that

| (86) |

At the same time, (18) yields , whose averaging over , in combination with (85), (86), leads to

| (87) |

By the monotonicity of the Frobenius inner product on the cone , the inequalities (48), (51) imply that

| (88) |

where the last equality uses (53). A combination of (87) with (88) leads to , which establishes (84).

The averaging in (84) is redundant if the map is affine, when is identically constant, as is the case for linear stochastic systems.

7 Illustration for Linear-Gaussian Dynamics

Consider a class of linear stochastic systems described by (1) with a linear drift vector and a constant dispersion matrix:

| (89) |

where , are given matrices, so that the corresponding diffusion matrix in (11) is also constant:

| (90) |

Assuming that is Hurwitz, the unperturbed system (4), governed by the SDE

| (91) |

(with the standard Wiener process ), has a unique nominal invariant Gaussian measure with zero mean and covariance matrix

| (92) |

Here,

| (93) |

(with the complex conjugate transpose) is the nominal spectral density of the stationary Gaussian process , and

| (94) |

is the transfer function from the incremented input to . The matrix in (92) is the infinite-horizon controllability Gramian [31] of the pair satisfying the algebraic Lyapunov equation (ALE)

| (95) |

in view of (90). If is controllable, then , and the nominal invariant measure is absolutely continuous with the PDF

| (96) |

In the presence of a linear drift in the actual noise dynamics (2), given by

| (97) |

with a constant matrix (specifying the parasitic coupling of the noise to the system through the feedback loop in Fig. 1), the nominal SDE (91) is replaced with

| (98) |

in accordance with (5). Assuming that is also Hurwitz, the system state has a zero-mean Gaussian invariant measure whose covariance matrix satisfies the ALE

| (99) |

Since the pair inherits controllability from , then is also positive definite, giving rise to the invariant PDF

| (100) |

The deviation of the invariant covariance matrix from its nominal counterpart depends on the matrix and vanishes when . The following theorem, which specifies Lemma 2 and Theorem 3 in the case of linear-Gaussian dynamics, provides an identity and an upper bound for the difference

| (101) |

of the corresponding precision matrices in terms of the Frobenius norm for real matrices. Their applicability is secured by the fact that the corresponding vector fields in (13) (see also (14)) are organised as a product of a Gaussian PDF and a polynomial (with an exponentially fast decay at infinity) and since the integrability conditions (22) hold for a similar reason.

Theorem 9.

In the linear-Gaussian setting under consideration, substitution of (89), (96), (100) into (19) leads to

| (104) |

with the matrix from (101), so that the map in (20) is also linear:

| (105) |

Hence, the identity (102) is obtained by computing the expectations of quadratic forms in (23) over the invariant Gaussian distribution as

| (106) |

where (90), (97), (105) are used along with the symmetry of the matrix in (101). In a similar fashion, the averaging in (35) yields

| (107) |

which establishes the norm bound (103) (whose derivation from (102) by matrix manipulations without the probabilistic reasoning behind (23), (35), (106), (107) would be less intuitive).

We will now apply Theorem 5 to achievability of an equality in (103). Since, in the linear-Gaussian case, the diffusion matrix in (90) is constant, then , and hence, the vector field in (41) takes the form

| (108) |

Here, use is also made of (89), (96) together with an auxiliary matrix

| (109) |

which is defined in terms of a real antisymmetric matrix

| (110) |

whose antisymmetry follows from the nominal ALE (95) as . Note that the matrix in (109) is Hamiltonian in the sense of the symplectic structure specified by (provided the matrix in (110) is nonsingular, in which case, the state dimension is, with necessity, even). It now follows from (104), (108), (19) that

with from (101), and hence, (42) is equivalent to the fulfillment of for all , which holds if and only if the matrix

| (111) |

of this quadratic form is antisymmetric. In turn, the latter condition reduces to the antisymmetry of the matrix (since in (111) is antisymmetric):

| (112) |

Therefore, by comparing (40) with (105) and using Theorem 5, it follows that the inequality (103) becomes an equality if in (97), provided the condition (112) is satisfied.

We will now apply the entropy bounds of Section 6 to the linear-Gaussian setting. The uniform ellipticity (48) is equivalent to positive definiteness of the diffusion matrix in (90):

| (113) |

(that is, , and in (89) is of full row rank). This implies the controllability of the pair , which (together with being Hurwitz) makes the nominal invariant covariance matrix positive definite. Since the Hessian matrix for the Gaussian PDF in (96) is also constant, the condition (51) is satisfied:

| (114) |

The quadratic-exponential moment (60) of the linear map from (97) is calculated (in a standard fashion) as

(where denotes the identity matrix of order ), and hence, the nominal CGF for in (59) acquires the form

| (115) |

for any

| (116) |

in accordance with (61). Here, is the operator norm (the largest singular value), and is the Schatten -norm [28, p. 441] of a real matrix (with the Frobenius norm being its particular case: ). Under the condition (116), the matrix is positive definite, and the derivative of (115) is given by

| (117) |

(in view of the identity for a differentiable nonsingular matrix-valued function of a scalar parameter) and is strictly positive whenever . By (115), (117), the corresponding function (62) takes the form

| (118) |

which can be used for computing the upper bound (71) in the elliptic linear-Gaussian case. The coefficients of the Taylor series in (115) provide the cumulants (80) for the asymptotic relation (75):

| (119) |

The following lemma (which specifies Lemma 8 for the linear case) provides an inequality for the influence of the drift part of the nominal SDE (91) on the coefficient from (53), which is used in the entropy bounds (54), (71).

Lemma 10.

Although (120) is a corollary of (84) due to the linearity of the map in (89), whereby , we will also provide an alternative proof using the Hamiltonian structure of the matrix in (109). From the latter property, or directly from the orthogonality of the subspaces of real symmetric and real antisymmetric matrices in the sense of the Frobenius inner product , it follows that (which is closely related to the Liouville theorem [1] on the phase-space volume preservation by Hamiltonian flows). Hence, (109) implies that

| (121) |

where, similarly to (88), the monotonicity of on is combined with , from (113), (114), and (53) is used. The inequality (121) leads to (120) (note that follows directly from being Hurwitz).

From the lower bound (120), it follows that in order for the inequality (68) to be satisfied with given by (116), the matrix in (97) has to be small enough in the sense that

| (122) |

Also, the fulfillment of the sufficient condition (6) for (7) at any , with the system being in the nominal invariant measure according to (91), is secured by another constraint on the matrix :

| (123) |

where the transfer function is given by (94), and is the -norm. The condition (123) originates from the limit relation [5, 36]

| (124) |

where is the spectral density (93), so that is the spectral density of the stationary Gaussian process (computed for the case when is a stationary Gaussian process governed by the nominal SDE (91)). However, (123) can only affect the link between and the noise relative entropy rate on the right-hand side of (38), whereas the inequality (35) and all its corollaries remain valid regardless of this link.

8 Perturbed Langevin Dynamics Example

For a comparison of the upper bound (71) with the exact value

| (125) |

of the Kullback-Leibler relative entropy for the invariant Gaussian PDFs (96), (100) (see, for example, [51, Lemma 9.1] and references therein), consider a linear stochastic system whose nominal dynamics (91) are specified by

| (126) |

where , and is a real positive definite symmetric matrix of order . The resulting form of the SDE (91) is

| (127) |

and describes the Langevin dynamics [57] for the velocity of a particle of unit mass in with a damping matrix , or, alternatively, a noisy gradient descent for minimising over . In accordance with (90), (126) yields

| (128) |

and, by (95), the nominal invariant covariance matrix in (92) is given by

| (129) |

The corresponding Gaussian PDF in (96) is a Boltzmann equilibrium PDF , , where plays the role of an absolute temperature parameter. Therefore, the ellipticity and logarithmic concavity constants , in (113), (114) and the coefficient in (53) are

| (130) |

In the presence of a linear noise drift (97), specified by a matrix , the perturbed SDE (98) takes the form

| (131) |

replacing (127). Similarly to Gershgorin’s circle argument [28], if the matrix satisfies

| (132) |

(in particular, whenever is small enough in the sense that ), then the matrix in (131) is Hurwitz. Also note that, in view of (126), (128), (129), the matrix (109) vanishes: , whereby the condition (112) is satisfied for any , and an equality in (103) is indeed achieved at a symmetric matrix . For a numerical example with dimensions , we used (126) with and the following matrix:

(its smallest eigenvalue is ), so that in (130). The perturbed system (131) was considered with

which satisfies the strict inequality in (122) with , (123) with (thus making (124) valid in this example), and (132). The invariant covariance matrix , found by solving (99) with , , from (126), (128), is given by

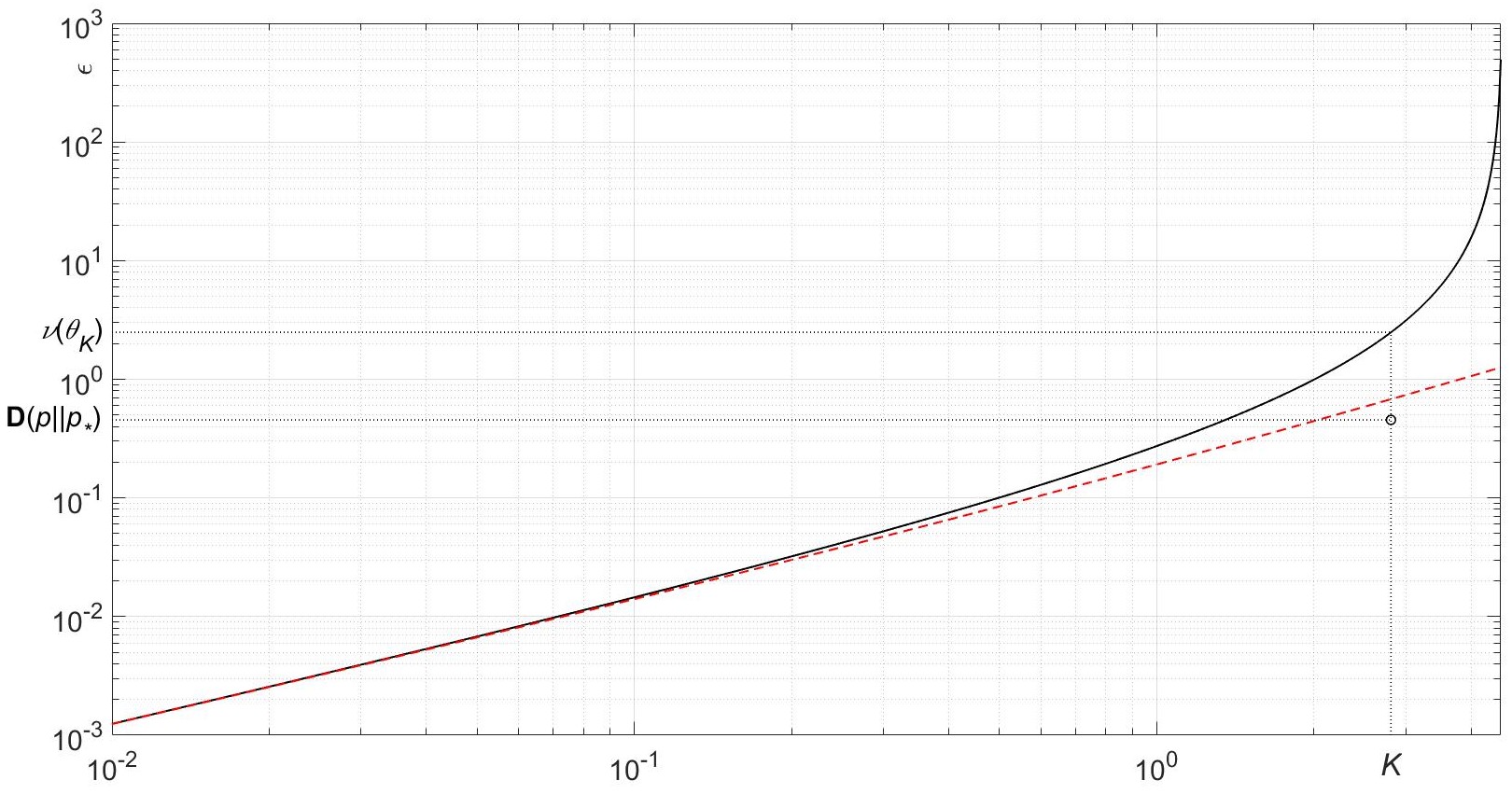

which, together with (129), yields the following exact value (125) for the relative entropy: . Its upper bound was computed according to (71) of Theorem 6 using (117), (118) and the parameterisation (74) of (73) in the -plane shown in Fig. 2.

9 Conclusion

We have considered a class of stochastic systems governed by SDEs whose driving noise deviates from the standard Wiener process due to a state-dependent drift. An upper bound on a diffusion-weighted Dirichlet form for the logarithmic PDF ratio (corresponding to the actual invariant measure of the perturbed system and its nominal counterpart in the white-noise case) has been obtained in terms of the Kullback-Leibler relative entropy rate of the input noise. This bound has been shown to be achievable (and the noise drift which saturates this inequality provided) under the preservation of the PDF ratio by the divergenceless steady-state probability flux associated with the nominal FPKE. Together with the logarithmic Sobolev inequality, the Dirichlet form bound has been used for obtaining (and studying the asymptotic behaviour of) an upper bound on the relative entropy of the perturbed invariant PDF in terms of quadratic-exponential moments of the noise drift in the case of a uniformly elliptic diffusion matrix and a strongly logarithmically concave nominal invariant PDF. These results have been illustrated for perturbations of Gaussian invariant measures in linear stochastic systems with linear noise drifts, including a perturbed Langevin dynamics example.

Support from the Australian Research Council grants DP210101938, DP200102945 is gratefully acknowledged.

References

- [1] V.I.Arnold, Mathematical Methods of Classical Mechanics, 2nd Ed., Springer, New York, 1989.

- [2] D.Bakry, and M.Emery, Diffusions hypercontractives, in “Seminaire de Probabilitts XIX,”, Lecture Notes in Mathematics, vol. 1123, Springer-Verlag, New York/Berlin, 1985, pp. 175–206.

- [3] A.Beghi, Continuous-time Gauss-Markov processes with fixed reciprocal dynamics, J. Math. Sys. Estim. Contr., vol. 4, no. 4, 1994, pp. 1–24.

- [4] A.Beghi, A.Ferrante, and M.Pavon, How to steer a quantum system over a Schrödinger bridge, Quant. Inform. Process., vol. 1, no. 3, 2002, pp. 183–206.

- [5] A.Bensoussan, and J.H. van Schuppen, Optimal control of partially observable stochastic systems with an exponential-of-integral performance index, SIAM J. Control Optim., vol. 23, no. 4, 1985, pp. 599–613.

- [6] A.Blaquiére, Controllability of a Fokker-Planck equation, the Schrödinger system, and a related stochastic optimal control (revised version), J. Dynam. Contr., vol. 2, no. 3, 1992, pp. 235–253.

- [7] V.I.Bogachev, and M.Rockner, Regularity of invariant measures on finite and infinite dimensional spaces and applications, J. Funct. Anal., vol. 133, no. 1, 1995, 168–223.

- [8] V.I.Bogachev, N.V.Krylov, and M.Röckner, Regularity of invariant measures: the case of non-constant diffusion part, J. Funct. Anal., vol. 138, 1996, 223–242.

- [9] V.I.Bogachev, N.V.Krylov, and M.Röckner, Elliptic equations for measures: regularity and global bounds of densities, J. Math. Pures Appl., vol. 85, 2006, pp. 743–757.

- [10] V.I.Bogachev, N.V.Krylov, M.Röckner, and S.V.Shaposhnikov, Fokker–Planck–Kolmogorov Equations, American Mathematical Society, Providence, Rhode Island, 2015.

- [11] V.I.Bogachev, S.V.Shaposhnikov, and A.Yu.Veretennikov, Differentiability of solutions of stationary Fokker-Planck-Kolmogorov equations with respect to a parameter, Discrete and Continuous Dynamical Systems Series A, vol. 36, no. 7, 2016, pp. 3519–3543.

-

[12]

V.I.Bogachev, E.D.Kosov, and A.V.Shaposhnikov,

Regulari-

ty of solutions to Kolmogorov equations with perturbed drifts, Potential Anal., vol. 58, 2023, pp. 681–702 (published 21 September 2021). - [13] A.Boukas, Stochastic control of operator-valued processes in boson Fock space, Russian J. Math. Phys., vol. 4, 1996, pp. 139–150.

- [14] L.M.Bregman, The relaxation method of finding the common points of convex sets and its application to the solution of problems in convex programming, USSR Comput. Math. Math. Phys., vol. 7, no. 3, 1967, pp. 200–217.

- [15] P.Cattiaux, and C.Léonard, Minimization of the Kullback information of diffusion processes, Ann. Inst. H. Poincare, vol. 30, no. 1, 1994, 83–132.

- [16] C.D.Charalambous and F.Rezaei, Stochastic uncertain systems subject to relative entropy constraints: induced norms and monotonicity properties of minimax games, IEEE Trans. Autom. Contr., vol. 52, no. 4, 2007, pp. 647–663.

- [17] Y.Chen, T.T.Georgiou, and M.Pavon, On the relation between optimal transport and Schrödinger bridges: a stochastic control viewpoint, J. Optim. Theory Appl., vol. 169, 2016, pp. 671–691.

- [18] T.M.Cover, and J.A.Thomas, Elements of Information Theory, Wiley, Hoboken, New Jersey, 2006.

- [19] P.Dai Pra, A stochastic control approach to reciprocal diffusion processes, Appl. Math. Optim., vol. 23, no. 1, 1991, pp. 313–329.

- [20] P.Dupuis, and R.S.Ellis, A Weak Convergence Approach to the Theory of Large Deviations, Wiley, 1997.

- [21] P.Dupuis, M.R.James, and I.R.Petersen, Robust properties of risk-sensitive control, Math. Contr. Sign. Sys., vol. 13, 2000, pp. 318–332.

- [22] L.C.Evans, Partial Differential Equations, American Mathematical Society, Providence, Rhode Island, 2008.

- [23] W.H.Fleming, Logarithmic transformations and stochastic control, Lecture Notes in Control and Information Sciences, vol. 42, 1982, pp. 131–141.

- [24] I.V.Girsanov, On transforming a certain class of stochastic processes by absolutely continuous substitution of measures, Theor. Probab. Appl., vol. 5, no. 3, 1960, pp. 285–301.

- [25] L.Gross, Logarithmic Sobolev inequalities, American Journal of Mathematics, vol. 97, no. 4, 1975, pp. 1061–1083.

- [26] L.Gross, Logarithmic Sobolev inequalities and contractivity properties of semigroups, In: G.Dell’Antonio, and U.Mosco (Eds), Dirichlet Forms, Lecture Notes in Mathematics, vol. 1563, Springer, Berlin, Heidelberg, 1993, pp. 54–88.

- [27] L.Hörmander, Hypoelliptic second order differential equations, Acta Math., vol. 119, 1967, pp. 147–171.

- [28] R.A.Horn, and C.R.Johnson, Matrix Analysis, Cambridge University Press, New York, 2007.

- [29] D.H.Jacobson, Optimal stochastic linear systems with exponential performance criteria and their relation to deterministic differential games, IEEE Trans. Autom. Control, vol. 18, 1973, pp. 124–31.

- [30] I.Karatzas, and S.E.Shreve, Brownian Motion and Stochastic Calculus, 2nd Ed., Springer, New York, 1991.

- [31] H.Kwakernaak, and R.Sivan, Linear Optimal Control Systems, Wiley, New York, 1972.

- [32] M.Ledoux, On an integral criterion for hypercontractivity of diffusion semigroups and extremal functions, J. Funct. Anal., vol. 105, 1992, 444–465.

- [33] R.S.Liptser, and A.N.Shiryaev, Statistics of Random Processes II: Applications, Springer, Berlin, 2001.

- [34] G.Metafune, D.Pallara, and A.Rhandi, Global properties of invariant measures, J. Funct. Anal., vol. 223, 2005, pp. 396–424.

- [35] T.Mikami, Variational processes from the weak forward equation, Commun. Math. Phys., vol. 135, 1990, pp. 19–40.

- [36] D.Mustafa, and K.Glover, Minimum Entropy Control, Springer-Verlag, Berlin, 1990.

- [37] E.Nelson, Dynamical Theories of Brownian Motion, 2nd Ed., Princeton University Press, 2001.

- [38] A.A.Novikov, On an identity for stochastic integrals, Theor. Probab. Appl., vol. 17, no. 4, 1973, pp. 717–720.

- [39] B.Øksendal, Stochastic Differential Equations, 5th Ed., Springer-Verlag, Berlin, 2000.

- [40] M.Pavon, and A.Ferrante, On the geometry of maximum entropy problems, SIAM Rev., vol. 55, no. 3, 2013, pp. 415–439.

- [41] I.R.Petersen, V.A.Ugrinovskii, and A.V.Savkin, Robust Control Design Using Methods, Springer, London, 2000.

- [42] I.R.Petersen, Minimax LQG control, Int. J. Appl. Math. Comput. Sci., vol. 16, 2006, pp. 309–323.

- [43] H.Risken, The Fokker-Planck Equation: Methods of Solution and Applications, 2nd Ed., Springer, Berlin, 1996.

- [44] A.J.Stam, Some inequalities satisfied by the quantities of information of Fisher and Shannon, Information and Control, vol. 2, no. 2, 1959, 101–112.

- [45] D.W.Stroock, Partial Differential Equations for Probabilists, Cambridge University Press, Cambridge, 2008.

- [46] T.Tanaka, P.M.Esfahani, and S.K.Mitter, LQG control with minimum directed information: semidefinite programming approach, IEEE Trans. Automat. Contr., vol. 63, no. 1, 2018, pp. 37–52.

- [47] A.B.Tsybakov, Introduction to Nonparametric Estimation, Springer, New York, 2009.

- [48] V.A.Ugrinovskii and I.R.Petersen, Minimax LQG control of stochastic partially observed uncertain systems, SIAM J. Contr. Optim., vol. 40, no. 4, 2001, pp. 1189–1226.

- [49] I.G.Vladimirov, A.P.Kurdjukov, and A.V.Semyonov, Anisotropy of signals and entropy of linear time-invariant systems, Doklady Mathematics, vol. 342, no. 5, 1995, pp. 583–585 (Russian) (English translation in vol. 51, no. 3, pp. 388–390).

- [50] I.G.Vladimirov, and I.R.Petersen, Minimum relative entropy state transitions in linear stochastic systems: the continuous time case, In: Proc. 19th International Symposium on Mathematical Theory of Networks and Systems (MTNS), 5-9 July 2010, Budapest, Hungary, pp. 51–58.

- [51] I.G.Vladimirov, and I.R.Petersen, State distributions and minimum relative entropy noise sequences in uncertain stochastic systems: the discrete time case, SIAM J. Contr. Optim., vol. 53, no. 3, 2015, pp. 1107–1153.

- [52] I.G.Vladimirov, I.R.Petersen, and M.R.James, Multi-point Gaussian states, quadratic-exponential cost functionals, and large deviations estimates for linear quantum stochastic systems, Appl. Math. Optim., vol. 83, no. 1, 2021, pp. 83–137 (published online 24 July 2018).

- [53] I.G.Vladimirov, I.R.Petersen, and M.R.James, Quadratic-exponential functionals of Gaussian quantum processes, Infinite-dimensional Analysis, Quantum Probability and Related Topics, vol. 24, no. 4, 2021, pp. 2150024.

- [54] I.G.Vladimirov, Probabilistic bounds with quadratic-exponential moments for quantum stochastic systems, IFAC World Congress, 9-14 July 2023, Yokohama, Japan, accepted (preprint: arXiv:2211.12161 [quant-ph], 22 November 2022).

- [55] P.Whittle, Risk-sensitive linear/quadratic/Gaussian control, Adv. Appl. Probab., vol. 13, 1981, pp. 764–77.

- [56] A.V.Yurchenkov, A.Yu.Kustov, and V.N.Timin, The sensor network estimation with dropouts: anisotropy-based approach, Automatica, vol. 151, 2023, pp. 110924.

- [57] R.Zwanzig, Nonequilibrium Statistical Mechanics, Oxford University Press, New York, 2001.