Price Optimization Combining Conjoint Data and Purchase History: A Causal Modeling Approach

Abstract

Pricing decisions of companies require an understanding of the causal effect of a price change on the demand. When real-life pricing experiments are infeasible, data-driven decision-making must be based on alternative data sources such as purchase history (sales data) and conjoint studies where a group of customers is asked to make imaginary purchases in an artificial setup. We present an approach for price optimization that combines population statistics, purchase history and conjoint data in a systematic way. We build on the recent advances in causal inference to identify and quantify the effect of price on the purchase probability at the customer level. The identification task is a transportability problem whose solution requires a parametric assumption on the differences between the conjoint study and real purchases. The causal effect is estimated using Bayesian methods that take into account the uncertainty of the data sources. The pricing decision is made by comparing the estimated posterior distributions of gross profit for different prices. The approach is demonstrated with simulated data resembling the features of real-world data.

Keywords: Pricing, Bayesian model, Causal inference, Data-fusion, Demand estimation

1 Introduction

Pricing decisions are vital for any business seeking profitability. In price optimization (Phillips, 2021), a company has to estimate the impact of a price change on the behavior of both current customers and potential new customers. This estimation task is essentially a problem of causal inference (Pearl, 2009) where the goal is to quantify the causal effect of price on the demand (Guelman and Guillén, 2014).

Price elasticity of demand is a traditional approach for measuring the effect of price change in demand (Bijmolt et al., 2005). However, elasticity is only the derivative of demand at one price point and may not correctly describe the change of demand for large price changes. A more general approach is to consider the price-response function (Phillips, 2021) that specifies the expected demand as a function of price. When customer-level data are available, the purchase probabilities of each customer can be modeled as a function of price and customer characteristics.

Historical data on sales and prices are readily available for most companies. If the product is a subscription-based digital service, purchases can be identified on the customer level and additional personal data on demographics and usage habits can be often collected via registration forms and browser cookies. Historical sales data alone are usually insufficient for price optimization. The price may have remained the same for a relatively long time and there may be confounders that have affected both the changes in pricing and the changes in sales (Tian and Feinberg, 2020).

In a pricing experiment, also known as an A/B test (Kohavi and Longbotham, 2017), customers are randomized into two or more groups and a different price is offered for each group. Ideally, a pricing experiment is the most reliable way to estimate the causal effect of price on the purchase. However, some challenges may render real-life pricing experiments impractical. For instance, browser cookies may not have a one-to-one correspondence with customers, which complicates the technical implementation of randomization in digital channels. In addition to the lack of full controllability, offering different prices may cause confusion among customers, affect their behavior, and even have negative effects on the brand.

A conjoint study (see e.g., Rao et al., 2014) is an experimental setting, where a customer is asked to choose among different variations of a product with modifications to the features, such as price. A conjoint study as a well-designed randomized experiment can bring valuable information about the customers’ sensitivity to prices and enables testing of many different prices at once. However, the behavior of the participants in the artificial setup may differ from their behavior in a real purchase situation (see e.g., Natter and Feurstein, 2002).

Combining data collected under various potentially heterogeneous conditions is known as the data-fusion problem (Bareinboim and Pearl, 2016). Such heterogeneity can be a result of for example inherent differences between the populations or the sampling methods used. Data-fusion is often not straightforward, as in the case of combining data from pricing experiments and conjoint studies due to the difference in participant behavior. This scenario is an example of a transportability problem where the goal is to use data from several source populations to make inferences about a target population of interest.

In this paper, we propose an approach for combining different data sources to estimate the causal effect of pricing on a purchase in the absence of real-life pricing experiments. We consider a subscription-based service, such as video or music streaming, an audiobook service, or a digital newspaper. The proposed work is motivated by a real business case that we carried out together with a company that offers subscription-based digital services. As publishing the results based on the real data would be against the business interest of the company, we use simulated data that aim to capture the most important features of real data.

The proposed approach consists of four steps: 1) The causal relations of the purchase process are described in the form of a directed acyclic graph (DAG). 2) The causal effect of price on purchases is identified from both observational and experimental data sources presented in a symbolic form. 3) A hierarchical Bayesian model is fitted to estimate the causal effect according to the obtained identifying functionals. 4) The posterior distribution of the optimal price is found by maximizing the expected gross profit defined as a function of the price and the purchase probabilities estimated in step 3.

The rest of the paper is organized as follows. We begin by describing the subscription-based business model, the data sources and the transportability problem in Section 2. The details of the simulation are described in Section 3. The optimization procedure and its results are presented in Section 4 and compared with the approach where only sales data is used for estimation and optimization. We conclude the paper with an evaluation of our method and discuss further research possibilities in Section 5. Table 1 in Appendix summarizes the notation of this paper. Code and data to reproduce the results and figures are available at https://github.com/lvalkone/Proptim.

2 Causal model for a subscription-based service

2.1 Problem definition and causal diagram

We consider a company that offers a subscription-based service for consumers. The subscription is automatically renewed monthly unless the customer cancels it. The total revenue of the company is the product of the price and the number of subscriptions, and the total profit is the difference of the revenue and the costs which can be divided into variable costs and fixed costs. The total profit is maximized when the gross profit, defined as the difference of the revenue and the variable costs, is maximized.

In addition to the price, the purchase behavior of a customer depends on background variables such as age, gender, and location. It is also clear that the probability of retention (an existing customer continues to subscribe) is higher than the probability of acquisition (a new customer subscribes) (Reinartz et al., 2005). In our model, we assume that each customer has a latent personal reference price (see e.g., Winer, 1986; Mazumdar et al., 2005; Cao et al., 2019) that they implicitly or explicitly compare with the actual price. When the price of the product is changed, the subscription probability will change as well, and the impact will be different for new and existing subscriptions because the distribution of reference prices differs between these groups due to selection. Estimating the demand after the price change is essential for the optimization of the profit.

Figure 1 shows the DAG that represents the causal relations of the variables of interest in our scenario. At the time , the purchase is affected directly by the price of the service . We also assume that the purchase is affected by a latent variable that represents the customer’s reference price. The larger the difference between the reference price and the product price is, the more likely the customer is willing to buy. The reference price is also affected by background variables (age, gender, location) denoted commonly by cluster (Tikka et al., 2021a), which for simplicity of the exposition are assumed to be constant in time. Accumulated subscription history is assumed to have a positive effect on repurchasing, and thus we also assume that is affected by the number of consequent subscription periods .

The DAG also contains transportability nodes that describe differences between populations in the underlying causal model (Bareinboim et al., 2013). The transportability node describes that the distribution of the background variables may differ between subscribers and non-subscribers. The transportability node (presented separately for time points and ) describes that the purchase probability of a customer may be different between a conjoint scenario and a real purchase scenario.

2.2 Data sources

The company gathers data on the customers, purchases , and the purchase history . The customers register for the service and provide information on their age (), gender (), and location (), commonly denoted by . We denote the distributions related to the subscriber population () as and to the non-subscriber population () as .

The company conducts a conjoint study (Rao et al., 2014) to increase its understanding on the expected consequences of a price change. This allows the company to test a variety of prices without interfering with the actual business. The conjoint is targeted at both current and earlier subscribers as well those who have never subscribed.

In a symbolic form, the purchase history data is denoted by . The conjoint data contains both subscribers and non-subscribers and thus provides information from two domains via two distributions: and , respectively. The purchase history and the conjoint data cannot be combined in a straightforward manner because the behavior of customers is expected to differ between the real purchase situation and the artificial purchase situation in the conjoint study. Formally, we can show that our causal effects of interest, i.e., the effect of price on the purchase in the context of a real purchase scenario for subscribers and non-subscribers, respectively, cannot be identified from the conjoint data alone, because the transportability node directly affects the purchase decision . Therefore, the conjoint data cannot be used without further assumptions. We assume here that the difference in the purchase probability between the conjoint scenario and the real purchase scenario can be parametrized via a level shift in the reference price:

| (1) |

where unknown parameter models the conjoint effect.

Population level data on the background variables are needed when potential new customers are included in the analysis. These data are available in an aggregated form from official statistics and they provide information on the distribution . Data on background variables of the subscribers is available from the price history data as . We assume that the reference price is a latent variable and that the parametric form of its distribution is known. Given the background variables, the distribution of the reference price is same across domains, i.e., , which we simply denote by .

2.3 Identifying the causal effect and formulating the model

Our goal is to identify the causal effect of price on the purchase probability for non-subscribers and subscribers, i.e., and from the available data sources in the DAG of Figure 1. Due to the challenging nature of the task, we apply the do-search algorithm (Tikka et al., 2021b) to identify the effects. Do-search accepts arbitrary data sources (in a symbolic form) as input and provides the identifying functional when the effect in question is identifiable. The DAG of Figure 1 and the data sources , , , , and are given as input to the algorithm. We note that the conjoint data also provides information on and due to our assumption in (1). Do-search returns the following identifying functionals for our causal effects of interest:

We need to model the conditional distribution of the latent reference price . As the reference price is assumed to vary between individuals, we fit a log-normal model for each individual . Our model for the reference price is then

where refers to the th category of the th predictor, and is an individual normally distributed random effect. The purchase choice is modeled via a Bernoulli distribution using logit-link as

where parameter describes the impact of the difference between the reference price (adjusted by the conjoint effect when ) and the price , parameter is the effect of consecutive subscription periods, and parameter describes the impact of the difference between customers who are just starting their subscription and those who are simply continuing their earlier subscription.

3 Data simulation

We simulate our data based on the structure of the DAG in Figure 1. The simulations are implemented in the R environment (R Core Team, 2021) with the R6Causal package (Karvanen, 2021). The statistics related to the choice of parameters are described in Table 2 of the Appendix.

We use real data from Statistics Finland (Statistics Finland, 2021) as a basis for the population demographics, covering a joint distribution of age, gender, and location. The variables are categorized for our study such that the age covers four groups: 18–30, 31–45, 46–60, and 61–75. The two other variables consist of dichotomous classifications as male and female in gender, and urban and rural in location. According to the data above, the company’s target market is here limited to Finland and individuals who are between 18–75 years old. The market size as the population of our study in 2020 is thus . Other variables of the DAG are simulated according to the flowchart presented in Figure 2. The chosen parameters defining the functional forms of the causal relationships used in the simulation are presented in Table 2 of the Appendix.

At the time , the company launches the product to the market, and every time point , a share of the population signs into the service of which a subset makes a subscription. We simulate the subscription history of two years (). The company launches the product for 16 euros. The price is then raised by 0.50 euros two times during the two years: after 6 months and after 18 months, i.e. at the times , and .

The customer choice (purchase or not) is modeled by a Bernoulli distribution with purchase probability . Probability depends on the difference between the product price and the customer’s reference price which is affected by background variables (see the DAG in Figure 1). Besides this, the number of earlier subscription periods directly affects the choice.

Using the sales data alone for finding the optimal price is unreliable since it contains information on the effect of the price for only three points: 16, 16.5, and 17 euros. Thus, after two years in the market, the company implements a conjoint study to explore the price sensitivity of customers. The participants of conjoint studies include current and earlier customers as well as those who have never subscribed.

In the conjoint study setting, 10 separate tasks of product alternatives are shown to a customer who is asked to choose whether to purchase the option offered. A modification of the product comprises varying prices ranging between 12 and 22 euros by 0.50 euros. With this price range, 10 out of 21 possible tasks are randomly sampled without replication for a participant to be shown. The conjoint effect of Equation 1 is set to a moderate value of 0.75 euros.

4 Optimizing the price

4.1 Estimating the model

We estimate the joint Bayesian (see e.g., Gelman et al., 2014) model for the reference prices and purchases using Markov chain Monte Carlo with the R package NIMBLE (de Valpine et al., 2017). Prior distributions for the regression coefficients are defined as distributions. Individual random effects are assumed to be distributed as , and for the standard deviation we set a prior using the shape-scale parameterization.

4.2 Maximizing the expected gross profit

Next, we describe how to optimize the price of the product by using the Bayesian model defined in Section 2.3. We aim to maximize the expected gross profit at the time , defined as

| (2) |

where is the price of the product, and are the purchase probabilities of earlier and current customers correspondingly. is the number of potential customers making a purchase decision at time , whereas is the number of current customers i.e. those who made a purchase at time and are now making a decision to continue or cancel the subscription. The cost structure related to gross profit includes the variable costs, which are denoted as .

As we optimize the expected gross profit by the price at the following time point , we can formalize the optimization problem as

We assume that every month a constant number of potential customers make a purchase choice. On the other hand, the number of current customers can be calculated directly from the historical sales data, which is for . In addition, we assume that the variable costs are constant over time, such that .

In Equation (2), the pricing affects both current and potential customers. Therefore, we divide the upcoming customer base data into two sets: The data set includes the customers that either canceled the subscription at or have never purchased. This data set of customers can be obtained by random sampling from the population with a size of . The data set consists of those customers who purchased at , so they are automatically about to choose at time . This customer base in can be obtained directly from the historical sales data.

We simulate 1 000 000 samples from the posterior distributions of the model parameters with 500 000 burn-in period and 500 thinning interval, resulting in the final sample size of 1000. We denote the model parameters commonly as . To study the effect of pricing by inspecting the posterior predictive distributions, we repeat the following for a set of different prices: For a given posterior sample, we calculate the reference prices and and purchase probabilities and for all and . As all of the customers in do not have an estimated individual level , we generate the value from -distribution. The expected purchase probability for decisions and for th posterior samples are then estimated as

| (3) | ||||

| (4) |

The estimates from (3) and (4) are then input into (2), and finally, the mean and 95% quantiles are calculated over the posterior samples to obtain the estimated expected gross profits and their credible intervals.

4.3 Optimization results

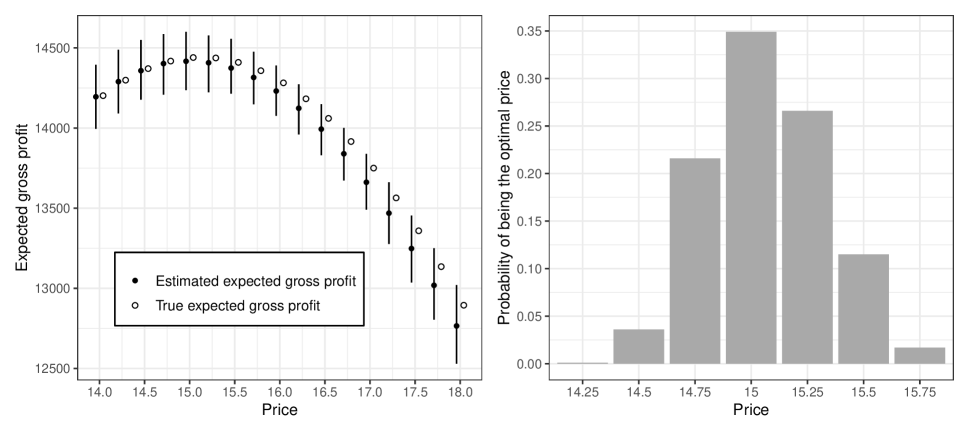

Figure 3 considers the price optimization in the case of combining the purchase history and conjoint data. The left panel in Figure 3 shows the estimated expected gross profits and their 95% credible intervals against the different price interventions (from 14 to 18 euros by increments of 0.25 euros), and the true expected gross profits, which can be calculated from (2), where and are obtained from the purchase history simulation for . By calculating which price yields the highest expected gross profit in each posterior sample, we can also obtain a probability distribution of the prices that maximize the expected gross profit, which is presented in the right panel in Figure 3. The price with the highest probability, i.e., the optimal price, can be found at with the expected gross profit of euros and (14 236, 14 600) 95% credible interval.

We attempted to estimate the model and optimize the price without the conjoint data. As expected, we encountered severe convergence issues. This may indicate that the model is not identifiable from the purchase history data alone, when the number of different prices is small.

5 Discussion

We proposed an approach for optimizing the price of a subscription-based service when real-life pricing experiments are unavailable. We described the customers’ behavior in the form of a causal graph and identified the causal effect of the price by combining population statistics, purchase history and conjoint data. The causal effect was estimated by Bayesian methods and as a result we obtained a posterior distribution for the optimal price that maximizes the expected gross profit.

The strengths of the proposed approach are related to the use of causal inference to guide the fusion of data sources. Instead of mixing the historical observational data with experimental data from the conjoint studies in an ad hoc fashion, we illustrated how such data sources can be combined in a theoretically sound fashion using causal inference. While we relied on simulated data due to the confidentiality of the real data, the causal graph used in the simulation and subsequent analysis was designed to closely emulate the assumed causal relations of the motivating real scenario.

We demonstrated that combining data sources is often necessary for price optimization. In our scenario, we were unable to estimate the model when the conjoint data were not available due to identifiability issues. Purchase history alone was insufficient for price optimization as the variation in the historical prices was low.

The proposed approach requires a good understanding of the causal mechanisms of customer behavior. These mechanisms can be communicated in the form of a graph as illustrated in Figure 1. The most critical assumptions are those related to unobserved confounders because the causal effect of price on the purchase may not be identifiable in the presence of unobserved confounders.

Another important assumption is the stability of market conditions and customer behavior in time. Without this assumption, we could not use past data to make decisions about the future. In practice, this assumption means that the data used for the analysis must be recent, not decades old.

For the clarity of the presentation, the presented scenario included some simplifying assumptions that could be extended in real use cases. For instance, the number of background variables could be higher and customer-level data on the service usage could be available. In some cases, it may be necessary to model the seasonal variation in the demand and the number of upcoming customers. The design of the conjoint study could also be more refined than the described setting. If a real-life pricing experiment is available, it should naturally be included as one of the data sources. The proposed approach can be easily adapted to these more complicated settings.

A possible direction for future research includes extension to multiple products. In the case of a subscription-based business model, there could be alternative subscription plans with different coverage, quality, and price. The model would be expanded to incorporate product-specific reference prices that are correlated on the customer level. Along similar lines, we could take into account the price changes implemented by the competitors. As the competitors are expected to react to price changes by the company in focus, dynamical modeling, and game theoretic considerations come into play.

Our work is one of the first applications of causality-driven data-fusion in the business context. We anticipate that the proposed methodology can be applied to various other causal inference and price optimization problems.

Declaration of interests

ST and JK have applied the proposed method in consulting.

References

- Bareinboim et al. (2013) Bareinboim, E., Lee, S., Honavar, V., and Pearl, J. (2013). Transportability from multiple environments with limited experiments. In Burges, C., Bottou, L., Welling, M., Ghahramani, Z., and Weinberger, K., editors, Advances in Neural Information Processing Systems, volume 26. Curran Associates, Inc.

- Bareinboim and Pearl (2016) Bareinboim, E. and Pearl, J. (2016). Causal inference and the data-fusion problem. Proceedings of the National Academy of Sciences, 113(27):7345–7352.

- Bijmolt et al. (2005) Bijmolt, T. H., Van Heerde, H. J., and Pieters, R. G. (2005). New empirical generalizations on the determinants of price elasticity. Journal of Marketing Research, 42(2):141–156.

- Cao et al. (2019) Cao, P., Zhao, N., and Wu, J. (2019). Dynamic pricing with Bayesian demand learning and reference price effect. European Journal of Operational Research, 279(2):540–556.

- de Valpine et al. (2017) de Valpine, P., Turek, D., Paciorek, C., Anderson-Bergman, C., Temple Lang, D., and Bodik, R. (2017). Programming with models: Writing statistical algorithms for general model structures with NIMBLE. Journal of Computational and Graphical Statistics, 26:403–413.

- Gelman et al. (2014) Gelman, A., Carlin, J. B., Stern, H. S., Dunson, D. B., Vehtari, A., and Rubin, D. B. (2014). Bayesian Data Analysis. CRC Press, Boca Raton, 3rd edition.

- Guelman and Guillén (2014) Guelman, L. and Guillén, M. (2014). A causal inference approach to measure price elasticity in automobile insurance. Expert Systems with Applications, 41(2):387–396.

- Karvanen (2021) Karvanen, J. (2021). R6Causal: R6 Class for Structural Causal Models. R package version 0.6.0.

- Kohavi and Longbotham (2017) Kohavi, R. and Longbotham, R. (2017). Online controlled experiments and A/B testing. Encyclopedia of Machine Learning and Data Mining, 7(8):922–929.

- Mazumdar et al. (2005) Mazumdar, T., Raj, S. P., and Sinha, I. (2005). Reference price research: Review and propositions. Journal of Marketing, 69(4):84–102.

- Natter and Feurstein (2002) Natter, M. and Feurstein, M. (2002). Real world performance of choice-based conjoint models. European Journal of Operational Research, 137(2):448–458.

- Pearl (2009) Pearl, J. (2009). Causality: Models, Reasoning, and Inference. Cambridge University Press, 2nd edition.

- Phillips (2021) Phillips, R. L. (2021). Pricing and Revenue Optimization. Stanford University Press.

- R Core Team (2021) R Core Team (2021). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Rao et al. (2014) Rao, V. R. et al. (2014). Applied Conjoint Analysis. Springer.

- Reinartz et al. (2005) Reinartz, W., Thomas, J. S., and Kumar, V. (2005). Balancing acquisition and retention resources to maximize customer profitability. Journal of Marketing, 69(1):63–79.

- Statistics Finland (2021) Statistics Finland (2021). Population 31.12. by Information, Urban-rural classification, Age, Area, Year and Sex. https://pxdata.stat.fi/PxWeb/pxweb/en/StatFin/. The material was downloaded from Statistics Finland’s interface service on 2021-09-27 with the licence CC BY 4.0.

- Tian and Feinberg (2020) Tian, L. and Feinberg, F. M. (2020). Optimizing price menus for duration discounts: A subscription selectivity field experiment. Marketing Science, 39(6):1181–1198.

- Tikka et al. (2021a) Tikka, S., Helske, J., and Karvanen, J. (2021a). Clustering and structural robustness in causal diagrams. arXiv preprint arXiv:2111.04513.

- Tikka et al. (2021b) Tikka, S., Hyttinen, A., and Karvanen, J. (2021b). Causal effect identification from multiple incomplete data sources: A general search-based approach. Journal of Statistical Software, 99(5):1–40.

- Winer (1986) Winer, R. S. (1986). A reference price model of brand choice for frequently purchased products. Journal of Consumer Research, 13(2):250–256.

Appendix

| DAG | |

|---|---|

| Time | |

| Age , Gender , and Location of a customer | |

| Customer’s reference price related to the product | |

| Transportability node concerning between real purchase and conjoint scenario | |

| Number of consecutive subscription periods of a customer until time | |

| Price of the product at time | |

| Customer’s choice at time | |

| Transportability node of differences between among subscribers and non-subscribers | |

| Data | |

| Population | |

| Customers at time having | |

| Customers at time having | |

| i.e. Current customer data | |

| Conjoint data of earlier subscribers | |

| Conjoint data of current subscribers | |

| Conjoint data of customers who have never subscribed | |

| Model | |

| Constant and regression coefficients of related to | |

| Individual random effect in reference price of th customer | |

| Standard deviation parameter of random effect | |

| Purchase probability of th customer | |

| Regression coefficients of (), , and I() respectively | |

| Conjoint effect on | |

| Common notation for all unknown parameters above | |

| Optimization | |

| Average purchase probability of th customer having | |

| Average purchase probability of th customer having | |

| Choice of th customer in data | |

| Choice of th customer in data | |

| Number of potential customers making a choice at time | |

| Number of current customers making a choice at time | |

| Expected gross profit of the product | |

| Variable costs of the product |

| Parameter | True values | Posterior mean | Posterior SD |

|---|---|---|---|

| 2.8000 | 2.7952 | 0.0070 | |

| 0.0000 | 0.0000 | 0.0000 | |

| -0.0150 | -0.0068 | 0.0050 | |

| -0.0300 | -0.0267 | 0.0053 | |

| -0.4500 | -0.0353 | 0.0052 | |

| 0.0000 | 0.0000 | 0.0000 | |

| 0.0100 | 0.0072 | 0.0037 | |

| 0.0000 | 0.0000 | 0.0000 | |

| -0.0200 | -0.0180 | 0.0042 | |

| 0.1000 | 0.1031 | 0.0074 | |

| 0.3500 | 0.3568 | 0.0111 | |

| 0.4500 | 0.4298 | 0.0547 | |

| -0.3000 | -0.3083 | 0.0395 | |

| 0.7500 | 0.6787 | 0.1098 |