A lower confidence sequence for the changing mean of non-negative right heavy-tailed observations with bounded mean

Abstract

A confidence sequence (CS) is an anytime-valid sequential inference primitive which produces an adapted sequence of sets for a predictable parameter sequence with a time-uniform coverage guarantee. This work constructs a non-parametric non-asymptotic lower CS for the running average conditional expectation whose slack converges to zero given non-negative right heavy-tailed observations with bounded mean. Specifically, when the variance is finite the approach dominates the empirical Bernstein supermartingale of Howard et al. [5]; with infinite variance, can adapt to a known or unknown -th moment bound; and can be efficiently approximated using a sublinear number of sufficient statistics. In certain cases this lower CS can be converted into a closed-interval CS whose width converges to zero, e.g., any bounded realization, or post contextual-bandit inference with bounded rewards and unbounded importance weights. A reference implementation and example simulations demonstrate the technique.

1 Introduction

Recently the A/B testing and contextual bandit communities have embraced anytime-valid strategies to facilitate composition of arbitrary decision logic into online experimental procedures.[6, 8] A confidence sequence (CS) is an anytime-valid sequential inference primitive which, for any , produces an adapted sequence of sets for a predictable parameter sequence of interest with the guarantee : non-parametric non-asymptotic variants have broad utility.

This work is a robust lower CS for the average conditional expectation of an adapted sequence of non-negative right heavy-tailed observations. The basic approach assumes a non-negative scalar observation with bounded mean and produces a lower CS for the running mean, i.e., a CS of the form . A lower CS has immediate utility for pessimistic decision scenarios such as gated deployment, i.e., requiring changes to production environments to certify improvement with high probability.[8] Furthermore, even with unbounded observations, this lower CS can sometimes be converted into a closed-interval CS, e.g., post contextual-bandit inference with bounded rewards and unbounded importance weights.[15] Bounded observations always permit constructing a CS: this is sensible despite all moments being finite, as the proposed approach is both theoretically and empirically superior to the empirical Bernstein supermartingale of Howard et al. [5].

Contributions

In Section 3, we introduce a novel test supermartingale for the running mean. We prove the following: the supermartingale dominates the empirical Bernstein supermartingale of Howard et al. [5]; does not require finite variance to converge, but can instead adapt to a known or unknown -th moment bound; and can be efficiently approximated using a sublinear number of sufficient statistics. The result is the imminently practical doubly-discrete robust mixture of Theorem 4. We provide simulations in Section 4; code to reproduce all results is available at https://github.com/microsoft/csrobust.

2 Related Work

Anytime-valid sequential inference is an active research area with a rich history dating back to Wald [12]. Here we only discuss aspects relevant to the current work, and we refer the interested reader to the excellent overview contained in Waudby-Smith and Ramdas [14].

Waudby-Smith and Ramdas [14] derive time-uniform confidence sequences for a fixed parameter and bounded observations. Their constructions can produce a lower CS when observations are unbounded above with bounded mean. Unfortunately their techniques are only applicable to a fixed parameter: when the parameter is changing, their techniques cover a data-dependent weighted mixture, providing limited utility. The fixed parameter case is not restricted to stationary processes, e.g., sampling without replacement is governed by a fixed parameter despite the data distributions predictably changing. Nonetheless, the fixed parameter restriction limits the applicability, e.g., when the conditional mean is changing over time.

Wang and Ramdas [13] improve upon Waudby-Smith and Ramdas [14] by leveraging Catoni-style influence functions, including an infinite variance result for a known -th moment bound. Adapting to an unknown bound is provably impossible in their setting due to Bahadur and Savage [1], whereas our more restrictive assumption of bounded mean allows us to adapt. The approach shares the limitations of Waudby-Smith and Ramdas [14] with respect to a changing parameter.

Howard et al. [5] describes multiple non-asymptotic boundaries for the running average conditional expectation. In particular they propose the empirical Bernstein boundary, which has zero asymptotic slack for lower-bounded right heavy-tailed observations with bounded mean and finite variance, e.g., log-normally distributed. However, all of their one-sided discrete time boundaries require finite variance for asymptotically zero slack.

3 Derivations

The following novel construction is a test martingale qua Shafer et al. [10].

Definition 1 (Heavy NSM).

Let be a filtered probability space, and let be an adapted non-negative -valued random process with bounded mean . Let be a predictable -valued random process, and let be a constant bet. Then

| (1) |

Statistical Considerations

Empirical Bernstein Dominance

Definition 1 is essentially the empirical Bernstein supermartingale of Howard et al. [5, Section A.8] without the slack from the Fan et al. [3] inequality. Consequently it is straightforward to show dominance.

Definition 2 (Empirical Bernstein Supermartingale).

| (2) |

where .

Thus Eq. 1 inherits the asymptotic guarantee of the mixed empirical Bernstein martingale.

Definition 3 (Mixture boundary).

For any probability distribution on and ,

is a time-uniform crossing boundary with probability at most for .

Proposition Howard 2 (Howard et al. [5]).

If is absolutely continuous wrt Lebesque measure in a neighborhood around zero, the mixture boundary is upper bounded by as , where , and .

Computationally this is less felicitous as closed-form conjugate mixtures are not available for Eq. 1. We revisit computational issues later in this section.

Heavy Tailed Results

When the conditional second moment is not bounded, Howard 2 provides no guarantee because the variance process grows superlinearly. However, unlike the empirical Bernstein process, Definition 1 can induce confidence sequences that shrink to zero asymptotically even if the conditional second moment is unbounded, and can adapt to an unknown -th moment bound. This is essentially because the function asymptotically grows more slowly than for any .

Lemma 1 (-growth).

For any and where is the principal branch of the Lambert W function,

where for , where uniquely solves

and defines .

Proof.

See Appendix A. ∎

For example when , . Combining the -growth lemma with a modified version of Laplace’s method yields Theorem 2.

Theorem 2 (-asymptotics).

For the mixture boundary of Definition 3, for any , any , and any absolutely continous with Lebseque measure in a neighborhood of zero with and , the mixture boundary is at most

where

with as in Lemma 1.

Proof.

See Appendix A. ∎

Theorem 2 gives a rate of : for comparison the -moment law of the iterated logarithm is .[11] Thus, like the finite variance case, the mixture method achieves the LIL rate to within a logarithmic factor. Note the quantity appearing in Theorem 2 is for analysis only and need not be explicitly computed; rather Definition 3 is used. However Theorem 2 cannot directly adapt to an unknown moment bound, as it requires a specification of the moment being bounded in order to construct the mixture distribution with the appropriate integrable singularity at the origin. Given Lemma 1 it is reasonable to seek adaptation to an unknown moment bound111Note the impossibility result of Bahadur and Savage [1] does not apply because the mean is bounded. which we achieve via a discrete mixture over Theorem 2.

Corollary 1 (-adaptive).

Corollary 1 is conservative: it ignores the contribution to the mixture wealth from all but one component. Nonetheless, choosing with for Corollary 1 yields a degradation in the boundary while adapting to a which is at most closer to 1 than .

Computational Considerations

Computationally, Eq. 1 is less convenient than Eq. 2 in several respects:

- 1.

-

2.

The mixture boundary of Definition 3 must be computed numerically for Eq. 1, whereas Eq. 2 has a closed-form conjugate mixture.

We mitigate the first issue by exploiting strong convexity of the variance process, and we mitigate the second issue by using discrete mixtures with early termination.

Approximate Sufficient Statistics

Define and write Eq. 1 as

If we can upper bound , we can lower bound and therefore upper bound any resulting boundary. We use the following upper bound,

| (3) |

where for ,

with setting the resolution of our exponential grid of sufficient statistics.

Theorem 3 (-approximation).

For all , , and ,

Furthermore can be computed in space and time.

Proof.

See Appendix B. ∎

Discrete Mixture

Given , the mixture boundary of Definition 3 for a single can be computed using numerical quadrature. In practice this is wasteful because a generic quadrature routine will spend compute on refinements that do not change the decision boundary. By contrast the discrete mixtures of Howard et al. [5] can be early terminated. Combining this with the discrete mixture of Corollary 1 and lower-bounding the inner sum leads to the doubly-discrete robust mixture.

Theorem 4 (DDRM).

For fixed , , , and ,

where is the Riemann zeta function and is the Jonquière polylogarithm, is a time-uniform crossing boundary with probability at most for .

Proof.

See Appendix B. ∎

Note Theorem 4 only asserts coverage, and not the other properties of Corollary 1. Hopefully, approximating Corollary 1 preserves the beneficial properties. In practice we terminate the sum of Theorem 4 dynamically, either because the wealth is above the threshold, or because we can upper bound the wealth below the threshold.

4 Simulations

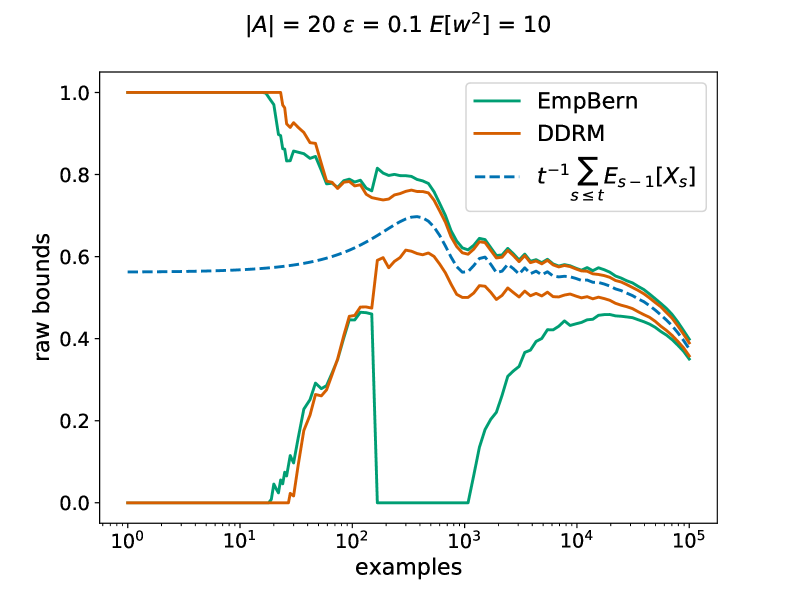

For demonstration we simulate contextual bandit off-policy estimation.222Code to reproduce all results available at https://github.com/microsoft/csrobust. Using the framework of Waudby-Smith et al. [15] we transform a lower CS on a non-negative random variable with mean upper bounded by 1 into a lower and upper CS for a contextual bandit problem with bounded rewards. Specifically, the raw observations are tuples of importance-weighted rewards where a.s. , , and a.s. ; the lower CS is obtained via ; and the upper CS is obtained from one minus the lower CS on . The importance weight and reward distributions can be predictably adversarially chosen, corresponding to any combination of changing environment (e.g., reward per action is changing), changing logging policy (e.g., the logging policy is from an online contextual bandit learning algorithm), and changing policy being evaluated (e.g., the evaluated policy is from an offline contextual bandit learning algorithm). We simulate an empirical Bernstein CS with gamma conjugate prior and ; and the DDRM of Theorem 4 with , , , , and .

Fig. 2 simulates off-policy estimation in an environment where rewards exhibit diurnal seasonality and a negative long-term trend, and the logging policy is -greedy over a discrete action set. The number of actions (20) and amount of exploration (0.1) are typical production settings. The policy being evaluated frequently agrees with the logging policy and hence has importance-weight variance much lower than the worst case of 190, which is typical of policies produced by off-policy learning algorithms. The occurrence of the largest importance weight at circa 100 examples causes a visible downward adjustment in the lower CS for empirical Bernstein, but DDRM is unaffected. Thus, even when the variance is finite and the range is bounded, DDRM exhibits beneficial robustness to outliers. If the lower CS is used for gated deployment of policy improvements as in Karampatziakis et al. [8], this increased robustness implies improvements can be reliably deployed more rapidly. Computationally, for this simulation on the author’s laptop, empirical Bernstein can compute a CS over points in circa 0.3ms, whereas DDRM takes circa 20ms: slower but acceptable.

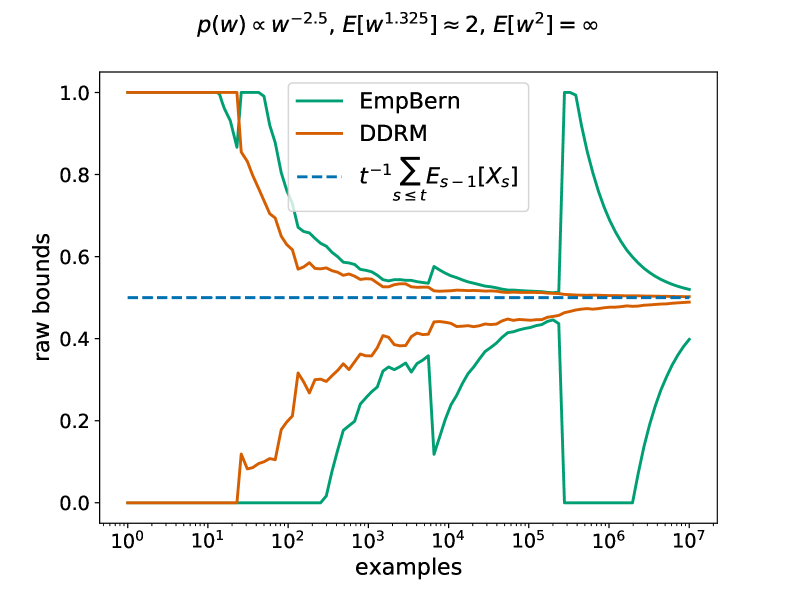

Fig. 2 simulates off-policy estimation in a constant environment and Pareto-distributed importance weights with infinite variance. This simulation is inspired by off-policy estimation in continuous action spaces. The empirical Bernstein confidence sequence has no asymptotic width guarantees as the variance process increases superlinearly. A large realization at circa examples illustrates the issue, as the empirical Bernstein CS is completely reset: if we continue running the simulation forever in infinite precision arithmetic, an infinite number of these complete resets will occur. By contrast, the DDRM is able to adapt to the (unknown) finite lower moment and converge.

5 Discussion

This paper advocates Theorem 4 as an always-preferable drop-in replacement for the empirical Bernstein conjugate mixture of Howard et al. [5]. Statistically, the underlying martingale and associated mixtures are superior; computationally, approximations mitigate the increased cost.

The structure of Definition 1 is intriguing: it contains a betting martingale term, but instead of betting that a fixed parameter is close to the actuals, it bets that the predictions are close to the actuals. This centers the martingale at the summed conditional mean plus the prediction error: in contrast, betting martingales are either centered at a weighted sum of the conditional means (if a fixed parameter is used), or define feasible sets on the Cartesian product of the parameter space (if a different parameter is used per timestep).

By testing if the running mean of an identification statistic is zero, Corollary 1 can be modified to extend the framework of Casgrain et al. [2] to in-hindsight elicitation, i.e., elicitable hypotheses of the running average conditional distribution . For example, expectiles of the average historical distribution are in-hindsight elicitable, but the identification statistic can exhibit infinite variance, e.g., a Pareto distributed observation. If the mean is bounded, Corollary 1 can adapt to an unknown moment bound of the identification statistic. We will elaborate this in future work.

References

- Bahadur and Savage [1956] Raghu R Bahadur and Leonard J Savage. The nonexistence of certain statistical procedures in nonparametric problems. The Annals of Mathematical Statistics, 27(4):1115–1122, 1956.

- Casgrain et al. [2022] Philippe Casgrain, Martin Larsson, and Johanna Ziegel. Anytime-valid sequential testing for elicitable functionals via supermartingales. arXiv preprint arXiv:2204.05680, 2022.

- Fan et al. [2015] Xiequan Fan, Ion Grama, and Quansheng Liu. Exponential inequalities for martingales with applications. Electronic Journal of Probability, 20:1–22, 2015.

- Fulks [1951] W Fulks. A generalization of laplace’s method. Proceedings of the American Mathematical Society, 2(4):613–622, 1951.

- Howard et al. [2021] Steven R Howard, Aaditya Ramdas, Jon McAuliffe, and Jasjeet Sekhon. Time-uniform, nonparametric, nonasymptotic confidence sequences. The Annals of Statistics, 49(2):1055–1080, 2021.

- Johari et al. [2022] Ramesh Johari, Pete Koomen, Leonid Pekelis, and David Walsh. Always valid inference: Continuous monitoring of a/b tests. Operations Research, 70(3):1806–1821, 2022.

- Kaminski and Paris [1997] D Kaminski and RB Paris. Asymptotics via iterated mellin–barnes integrals: application to the generalised faxén integral. Methods and Applications of Analysis, 4(3):311–325, 1997.

- Karampatziakis et al. [2021] Nikos Karampatziakis, Paul Mineiro, and Aaditya Ramdas. Off-policy confidence sequences. In International Conference on Machine Learning, pages 5301–5310. PMLR, 2021.

- Olver [1997] Frank Olver. Asymptotics and special functions. AK Peters/CRC Press, 1997.

- Shafer et al. [2011] Glenn Shafer, Alexander Shen, Nikolai Vereshchagin, and Vladimir Vovk. Test martingales, bayes factors and p-values. Statistical Science, 26(1):84–101, 2011.

- Shao [1997] Qi-Man Shao. Self-normalized large deviations. The Annals of Probability, 25(1):285–328, 1997.

- Wald [1945] A Wald. Sequential tests of statistical hypotheses. Annals of Mathematical Statistics, 1945.

- Wang and Ramdas [2022] Hongjian Wang and Aaditya Ramdas. Catoni-style confidence sequences for heavy-tailed mean estimation. arXiv preprint arXiv:2202.01250, 2022.

- Waudby-Smith and Ramdas [2020] Ian Waudby-Smith and Aaditya Ramdas. Estimating means of bounded random variables by betting. arXiv preprint arXiv:2010.09686, 2020.

- Waudby-Smith et al. [2022] Ian Waudby-Smith, Lili Wu, Aaditya Ramdas, Nikos Karampatziakis, and Paul Mineiro. Anytime-valid off-policy inference for contextual bandits, 2022. URL https://arxiv.org/abs/2210.10768.

Appendix A Heavy Tailed Results

Proof of Lemma 1

See 1

Proof.

The lemma is trivially true for via Fan et al. [3]. For , consider

This last expression is positive whenever

Noting is strictly decreasing for , this implies is strictly increasing whenever . Further noting , , and the continuity of ensures the uniqueness of .

To establish a globally decreasing function, we augment the denominator with for and equate them at the boundary. Redefine as,

then for and ,

Here is the principal branch of the Lambert W function and . To establish , we expand for ,

∎

Proof of Theorem 2

See 2

Proof.

Our object of interest is the boundary

where ,

and is assumed absolutely continuous with Lebesque measure, and with in a neighborhood of zero , with . From Lemma 1 we can upper bound the variance, and hence upper bound the boundary, via

where will be evaluated at

and we have further upper bounded the boundary by restricting to the absolutely continuous neighborhood. Our proof steps are as follows:

- 1.

- 2.

-

3.

Invert the boundary: the sandwich lemmas, combined with continuity of the integral wrt and the intermediate value theorem, allows us to assert an exact boundary.

Inverting the boundary, as ,

Supporting propositions follow. ∎

First we restate Theorem 4.1 of Olver [9].

Theorem Olver 4.1 (Olver [9] pg. 332).

Let

and assume that

-

1.

In the interval , is continuous and positive, and the real or complex functions and are continuous.

-

2.

As ,

where

Then

where and

is the Faxén integral.

Lemma 2.

First we restate Theorem 2.1 of Olver [9].

Theorem Olver 2.1 (Olver [9] pg. 326).

Let and be fixed positive numbers, and

-

1.

is continuous and positive in with

with and .

-

2.

For all , and are continuous for . Moreover,

where , , , , , , , and are independent of and , and

Then

where .

Furthermore if is real and non-positive then the conditions relax to .

Lemma 3.

Proof.

Consider the expected value of the inverse wealth,

For any , to apply Olver 2.1 to , establish the following correspondences:

where holds. This results in

Thus for sufficiently large , . From Jensen’s inequality,

∎

Customized Fulks [4]

Ideally we could reuse Theorem 4 of Fulks [4] directly, but this was not possible. Instead we follow the same line of argument, changing one critical step to accommodate our scenario.

Theorem 5 (Customization of Fulks [4] Theorem 4).

For and , let

where is absolutely continuous with Lebesque measure, with and . For , with and , we have

where

Proof.

First we change the integration variable,

where and . Note . Next we define the value as333Contrasting with Fulks [4], we exactly compute here, which allows us to proceed.

Since we have . We also have

since . Choose large enough such that . We start by assuming is constant and relax this assumption later. Consider the centered integrand,

For the exponent is strictly concave. Noting

we take , allowing us to crudely bound via the exponent being non-positive. For we Taylor expand around ,

where is between and , and . For we have the sandwich

where , so we substitute to get

The limit of integration diverges and we get

noting . For we have the sandwich

noting , so we substitute to get

The limit of integration diverges and we get

Combining yields

To show for our actual it suffices to bound

where . From the strong concavity result above, we choose to ensure . Meanwhile for we have upper bounded by .

∎

Appendix B Computational Considerations

Proof of Theorem 3

See 3

Proof.

For ,

There is a single sufficient statistic for , .

For ,

There is a single sufficient statistic for , .

For : we have . is strongly convex in this region with strong convexity parameter , therefore

For each , there are three sufficient statistics to accumulate:

from which for any we can compute

The statement about computational cost follows from upper bounding the number of non-zero sufficient statistics. ∎

Proof of Theorem 4

See 4

Proof.

We start by replacing in the -specific construction from Theorem 2. Then we apply the mixture strategy from Howard et al. [5]: for some we discretize the mixture distribution

Embedding the previous into the robust construction of Corollary 1 yields

For some the choice yields

∎