Inference for Change Points in High-Dimensional Time Series via a Two-Way MOSUM

Abstract

We propose an inference method for detecting multiple change points in high-dimensional time series, targeting dense or spatially clustered signals. Our method aggregates moving sum (MOSUM) statistics cross-sectionally by an -norm and maximizes them over time. We further introduce a novel Two-Way MOSUM, which utilizes spatial-temporal moving regions to search for breaks, with the added advantage of enhancing testing power when breaks occur in only a few groups. The limiting distribution of an -aggregated statistic is established for testing break existence by extending a high-dimensional Gaussian approximation theorem to spatial-temporal non-stationary processes. Simulation studies exhibit promising performance of our test in detecting non-sparse weak signals. Two applications, analyzing equity returns and COVID-19 cases in the United States, showcase the real-world relevance of our proposed algorithms.

Keywords: multiple change-point detection, inference for break existence, Two-Way MOSUM, Gaussian approximation, temporal and spatial dependence, nonlinear time series

1 Introduction

Change-point analysis is a fundamental problem in various fields of applications: in economics, the break effects of policy are of particular interest ([12]); in biology, high-amplitude co-fluctuations are utilized in cortical activity to represent dynamics of brain functional connectivity ([24, 23]); in network analysis, change-point detection can be employed for the anomaly of network traffic data caused by attacks ([36]), etc. The above list of scenarios spans a wide range of data structures, including high-dimensional data with temporal and cross-sectional dependence, which pose substantial challenges to change-point analysis. The paper aims to address this issue by providing theory on multiple break inference for high-dimensional time series allowing both temporal and spatial dependence.

There is a sizable literature on high-dimensional change-point detection. Various studies consider data aggregation, and many of them consider -based methods. See, for example, [49, 29, 13, 62]. Most aforementioned studies focus on sparse signals, while an -based approach favors non-sparse weak signals, and this is also the focus of this study. In the meanwhile, the -type aggregation is quite common in the literature. [4] evaluates the performance of a least square estimation and establishes a distribution theory for single change-point estimator in panel data without cross-sectional dependence; [65] develops a recursive algorithm based on sums of chi-squared statistics across samples with independent and identically distributed (i.i.d.) Gaussian noises, which could be viewed as an extension of the circular binary segmentation algorithm by [44]. In addition, [26, 10, 27, 5, 38] study -based cumulative sum (CUSUM) statistics to estimate and make inference for change points in linear regression or panel models. Although their methods primarily concentrate on scenarios with a single break per time series, their approaches bear similarities to ours, with the key difference being our utilization of a moving sum (MOSUM) variant. More recently, [22] proposes a linear and a scan CUSUM statistic with the minimax bound established for the change-point estimator of i.i.d. Gaussian data; [14] introduces a coordinate-wise likelihood ratio test for online change-point detection for independent Gaussian data and present the response delay rate. In addition to aggregation, there are other well-known techniques for high-dimensional change-point analysis, including the U-statistics as demonstrated by [53, 54, 62], threshold-based approaches proposed by [18, 17], and a projection-based method developed by [56]. In this paper, we consider a maximized -type test statistic to adapt to different datasets containing signals of distinct temporal-spatial properties and errors with complex dependency structures.

Besides the challenge of change-point test brought by high-dimensionality, studies on multiple change-point detection have a long-standing tradition. In general, two broad classes of methods have been developed: model selection and hypothesis testing. Model selection approaches aim to treat change-point signals as parameters and derive estimators for them, such as the PELT algorithm ([32]) and the fused LASSO penalty ([51, 37, 35]). [19] proposes a localised application of the Schwarz criterion for multiscale change points. [34, 60, 52] consider change-point analysis for linear regression models featuring varying parameters, encompassing a broad range of nonlinear time series. As for testing, a traditional approach is binary segmentation developed by [48]. Its variants are considered in [6, 44]. Moreover, [25] introduces a wild binary segmentation and [18] proposes a sparsified binary segmentation algorithm. [63] reviews diverse minimax rates in change-point analysis literature.

In the context of testing, MOSUM is a notably popular technique for both univariate and multivariate time series, such as [28] on i.i.d. data, [58, 21] on temporal dependent data, and [33] on multivariate time-continuous stochastic processes. MOSUM is attractive due to the simplicity of implementation and an overall control of significance level which avoids issues in multiple testing. However, for high-dimensional time series, when a MOSUM statistic aggregates all the series by an -norm, the testing power would suffer if breaks only occur in a portion of them. Hence, in this paper, we propose a novel spatial-temporal moving sum algorithm called Two-Way MOSUM. This method utilizes moving spatial-temporal regions to search for temporal breaks and locate spatial neighborhoods where temporal breaks occur. Such moving regions can be viewed as a generalized concept of the moving windows in previous MOSUM, which can aggregate signals adaptive to cross-sectional group structures to enhance testing power. We emphasize that overlapping groups are allowed in our method, and therefore the prior knowledge of groups is not a requirement for effective detection of breaks, since one can always search for all possible grouping scenarios. Nevertheless, prior grouping information is available in numerous data applications, which can boost the testing power by decreasing the number of searching windows. See, for example, in neuroscience, regions of interest (ROI) in human brains can be assigned to networks by different functions and the ROIs from the same network will undergo simultaneous functional change points ([7]); in finance, stock prices of industries are often grouped by market capitalization and a few number of sectors may experience market shocks at the same time ([45]). Note that all the theoretical comparison of testing power in this paper is only among MOSUM-based statistics.

Although both aggregation and MOSUM statistics have been well investigated respectively, it is quite challenging to rigorously develop an inference theory for -based MOSUM statistics to detect the existence of breaks for the high-dimensional data. To be more specific, when we take the maximum of statistics obtained from all the rolling windows over time, these aggregated statistics are temporally dependent even though the underlying errors may be independent. Most of the previous works concerning -based statistics only provide inference for the break estimators by assuming the existence of a break, such as an -type break location estimator and its inference introduced by [4] for single change-point estimation with cross-sectionally independent errors. To the best of our knowledge, this study is the first to establish the limiting distribution of an -type test statistic to facilitate the inference for change-point detection, which allows both spatial and temporal dependence.

To summarize, we contribute to the literature in both theory and algorithms. On the theory front, we propose an -type MOSUM test statistic for multiple break detection in high-dimensional time series, allowing both temporal and spatial dependence. The Gaussian approximation (GA) result under the null is provided as a theoretical foundation to backup our detection of breaks (cf. Theorems 1 & 4). Correspondingly, we introduce an innovative Two-Way MOSUM statistic to account for spatially-clustered signals (cf. Theorem 3). Consistency results of estimators for number of breaks, temporal and spatial break locations, as well as break sizes are all established (cf. Theorem 2 & Proposition 1).

Roadmap. The rest of this article is organized as follows. Section 2 is devoted to the test specification and asymptotic properties with cross-sectional independence assumed. Section 3 serves as an extension to the cases where breaks might exist only in a subset of component series (clustered signals). We follow with Section 4 as a generalization to nonlinear time series with spatial space in , allowing both temporal and cross-sectional dependence. In Section 5, we deliver two empirical applications on testing structural breaks for the stock return and COVID-19 data. The simulation studies and proofs are deferred to Appendix.

Notation. For a vector and , we denote and . For and a random vector , we say if , and denote . For two positive number sequences and , we say or (resp. ) if there exists such that (resp. ) for all large , and say or if as . Let and to be two sequences of random variables. Write if for , there exists such that for all large , and say if in probability as .

2 Testing and Estimating High-Dimensional Change Points

In this section, we propose a test statistic based on an aggregated MOSUM and investigate its theoretical properties to test the presence of structural breaks. To formulate our model, let be observed -dimensional random vectors satisfying

| (1) |

where is a sequence of -dimensional stationary errors with zero-mean and is a -dimensional vector of unknown trend functions. Our main interest is to detect the potential change points occurring on the trend function

| (2) |

where is the number of structural breaks which is unknown and could go to infinity as increases; are the time stamps of the breaks with and the minimum gap , where is allowed to tend to 0 as ; represents the benchmark level when no break occurs and is the jump vector at the time stamp with size .

It should be noted that not all entries of need to be nonzero, which allows for cases where only a subset of time series experience a jump at the time stamp . In such situations, it is preferable to aggregate only the series with breaks rather than all of them, as it can improve the testing power. A more detailed discussion of this scenario is given in Section 3 where the Two-Way MOSUM method is introduced. In this section, for readability, we focus solely on the improved MOSUM that aggregates all time series. For brevity, we assume the time series to be linear and cross-sectionally independent throughout Sections 2 and 3, which will be relaxed to nonlinear and cross-sectionally dependent cases in Section 4.

2.1 -Based Test Statistics

This subsection is devoted to test the null hypothesis:

which denotes the case with no breaks, against the alternative : there exists , such that . Note that the number of breaks is allowed to go to infinity under some condition on the separation of breaks. We refer to a detailed discussion below Definition 1 in Section 2.3.

The primary reason for testing the presence of structural breaks is to prevent model misspecification. If we apply a change-point algorithm to a data generating process without any actual breaks, we may obtain false break estimates, leading to erroneous conclusions. Therefore, it is necessary to test for the existence of breaks before conducting further analysis. However, previous studies on change points in high-dimensional time series mostly focus on inference for break location estimators, such as Theorem 2.2 in [27], which assumes the existence of breaks. Although there are some available literature on change-point testing for high-dimensional time series (see [29, 13, 55]), there is no existing theory of -based statistics for testing break existence, which can be necessary and highly beneficial in identifying dense signals.

We define a jump vector at the time point as when no break occurs at the time stamp , and when for some . Intuitively, we can test the existence of breaks by evaluating the jump estimate , where

| (3) |

are the local averages on the left and the right hand sides of the time point , respectively, and is a bandwidth parameter satisfying and . Without loss of generality, we assume that is an integer. We shall reject the null if is too large. To this end, we shall develop an asymptotic distributional theory which appears to be highly nontrivial.

Throughout Sections 2 and 3, we assume that there is no dependence between component processes , , and we later relax this restriction to allow for weak cross-sectional dependence in Section 4. To make all components in comparable, we need to specify the error process and obtain the long-run variances for standardization. In particular, we model as a vector moving average (VMA) process in Sections 2 and 3, which embraces many important time series models such as a vector autoregressive moving averages (VARMA) model, and we discuss a more general in Section 4 using functional dependence measure, which allows nonlinear forms. Let

| (4) |

where are i.i.d. random vectors with zero mean and an identity covariance matrix with , for some constant . The coefficient matrices , , take values in such that is a proper random vector. Define . Then the long-run covariance matrix of and the diagonal matrix of the long-run standard deviations are

| (5) |

respectively, where , for some constant , is the long-run variance of the -th component series. Note that in Sections 2 and 3, we assume , and all , , are diagonal matrices, which indicates the independence between the component processes . We relax this assumption to weak cross-sectional dependence for a general in Section 4, and also provide the results for the same linear in (4) as a special case in Appendix B.4.

Following the previous intuition, we test the existence of breaks by evaluating the gap vectors . Namely, we standardize by the long-run standard deviations of each time series, that is, for ,

| (6) |

To conduct the change-point detection with , we take the aggregation of each in the cross-sectional dimension, i.e. , to capture dense signals. Note that by model (1), the random vector involves both the signal part and the error part . We define

| (7) |

and is the -th coordinate of . Since no break exists under the null hypothesis, i.e. , it follows that is a centered statistic under the null. The detailed evaluation of is deferred to Remark 5. Finally, we move the windows in the temporal direction to find the maximum and formulate our -based test statistic as follows:

| (8) |

We consider as a feasible test statistic by assuming that the long-run standard deviation is known. The estimated long-run variances via a robust M-estimation method proposed by [13] are utilized in Section 5 for applications, and the details are deferred to Appendix A.1.

It is worth noticing that when breaks are sparse in the cross-sectional components, an -type statistic, i.e., , could be more powerful ([13]) than an -based one. However, in the presence of weak dense signals, the test would have power loss ([11]) while the -type statistic can boost the power due to the aggregation of weak signals; see Remark 1 for a simple comparison. The current study targets change-point detection with non-sparse or spatially clustered signals. An -based test statistic is therefore being proposed.

Remark 1 (Comparison of and statistics).

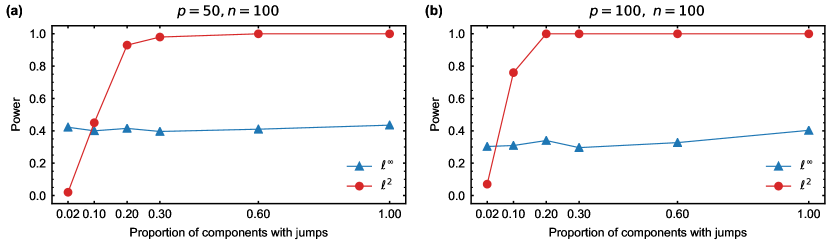

Here we present a simulation study to intuitively show that an -based test statistic is generally more powerful in detecting weak dense signals compared to an one, while in the case of sparse signals, an type statistic appears better. Specifically, we perform a single change-point detection using test statistics and respectively, and compare their testing powers with varied proportions of cross-sectional dimensions containing jumps. The errors are generated from MA() models defined in (4) with and the sample size . We consider and the window size . We set the coefficient matrix in (4) to be , where are uniformly ranging from to . For each time series with a break, the jump size is . All the reported powers in Figure 1 are averaged over replicates. Intuitively, our test statistic incorporates the term , which aggregates dense signals in a linear fashion with respect to the number of components , while the standard deviation of weakly dependent random noises is aggregated on the order of . As a result, an -type statistic is better suited for identifying dense signals, while its performance for sparse signals may be inferior since aggregating sparse signals will only add noise without any significant signal. After introducing Theorem 1, we shall provide a theoretical power comparison (cf. Remark 4).

2.2 Asymptotic Properties of Test Statistics

To conduct the test, it is essential to understand the asymptotic behavior of the test statistic . However, deriving the limiting distribution of under the null is highly challenging. This is because, even if the underlying errors are i.i.d., the standardized jump estimator defined in (6) is still dependent over due to the overlapped observations among different moving windows. In this section, we provide an intuition for the theoretical proofs of our first main theorem, which extends the high-dimensional GA for dependent data.

First, recall that the random vector can be decomposed into the expectation and the deviation part . We have for any under the null hypothesis. Let

| (9) |

where is defined in (7). By (6), we can write the test statistic under the null into

| (10) |

When the errors are cross-sectionally independent, are also independent. Therefore, as goes to infinity, we can apply the high-dimensional GA theorem to (10) to derive the asymptotic distribution of . In this way, the temporal dependence caused by the overlapped moving windows can be properly dealt with. We generalize this result in Section 4 with cross-sectionally dependence allowed between .

We introduce the centered Gaussian random vector with covariance matrix , and denote the -th element in by . Here with expression

| (11) |

where the function is defined as

| (12) |

Note that has bounded second derivatives except for the point . The matrix is asymptotically equal to the covariance matrix of . The detailed evaluation of in (12) is deferred to Lemma 14 in Appendix C. The regime with corresponds to correlations of statistics within length of , while is concerning statistics which are further apart () and still have weaker correlations. Finally, suggests that statistics beyond are uncorrelated.

By the GA theorem, we shall expect the asymptotic distribution of under the null to be approximated by the maximum coordinate of a centered Gaussian vector , that is,

| (13) |

This result allows us to find the critical value of our proposed test statistic by Monte-Carlo replicates. We refer to a simulation study in Appendix A.2.

2.3 Gaussian Approximation

In this section, we provide a theory which implies the critical value of the proposed change-point test. We first consider the simplest setting where the errors are assumed to be cross-sectionally independent, and a MOSUM statistic aggregating all the series is adopted. The novel Two-Way MOSUM follows in Section 3. A generalized case with cross-sectionally dependent errors is investigated in Section 4.

We begin with two necessary assumptions as follows.

Assumption 1 (Finite moment).

Assume that the innovations defined in (4) are i.i.d. with for some .

Assumption 2 (Temporal dependence).

There exist constants , such that

for all , where is the -th row of .

Assumption 3 (Cross-sectional independence).

Assume that for all , the coefficient matrices defined in (4) are diagonal matrices.

Assumption 1 puts tail assumptions on the moment of the noise sequences in our moving average model (4). Assumption 2 is a very general and mild temporal dependence condition, which requires the polynomial decay rate of the temporal dependence. It also ensures that the long-run variance is finite. Many interesting processes fulfill this assumption. We refer to a specific example in Appendix B.1. Note that we introduce Assumption 3 for the simplicity to show the GA and it shall be relaxed to allow weak cross-sectional dependence in Section 4.

Provided all the aforementioned conditions, we state our first main theorem as follows.

Theorem 1 (GA with cross-sectional independence).

The symbol and in this theorem and the rest of the paper is in the asymptotic regime . It is worth noting that the convergence rate of the GA in Theorem 1 depends on the number of cross-sectional components , and a larger is no longer a curse when utilizing an -type test statistic. The intuition behind this is that when applying the GA, we effectively treat our cross-sectional components as equivalent to the ” observations” in [15]. As such, a larger provides more information that can be used to detect change points, which can in turn reduce the approximation error.

Compared to the finite moment condition (E.2) in [15] which assumes that , we require since in our test statistic is quadratic with regard to the random noise . As for the GA rate in Proposition 2.1 in [15], our and correspond to their rate with replaced by and . It shall be noted that our additional term is due to an additional step to compare non-centered Gaussian variables (cf. Lemma 4 in Appendix C).

Remark 2 (Allowed dimension relative to ).

Remark 3 (Comment on the convergence rate in Theorem 1).

We standardize defined in (9) and denote it by , i.e. . [16] derives a nearly optimal bound in the case when the smallest eigenvalue of the covariance matrix of is bounded below from zero. However, this sharp approximation rate cannot be achieved in our case. To see this, we consider the simple case where the errors are i.i.d.. Then, for any integer , the -th element of the covariance matrix takes the form of in (11). It shall be noted that is a -banded matrix and it is symmetric. Since has bounded second derivative except for one point, for any four coordinates at the positions , , and in , , , we can bound them in the following way,

| (17) |

Inspired by (17), we define a vector . When , the upper bound of the smallest eigenvalue of tends to , that is

| (18) |

Therefore, [16] is not applicable to our case and we instead extend the GA in [15] to achieve the rate in Theorem 1, which does not require the covariance matrix of to be non-degenerate.

Theorem 1 implies that, for any level , we can choose the threshold value to be the quantile of the Gaussian limiting distribution indicated by Theorem 1:

| (19) |

We shall reject the null hypothesis if the test statistic exceeds the threshold value , i.e. . Under the alternative hypothesis, we show that when the break size is sufficiently large, we can achieve the testing power asymptotically tending to (cf. Corollary 1). Recall the trend function defined in (2). We denote the break location by , , and introduce the following assumption for the identification of breaks.

Definition 1 (Temporal separation).

Define the minimum gap between breaks as , for some , and we allow as diverges.

Definition 1 concerns the separation of temporal break locations to ensure the consistency of break estimation, and it implies that cannot be larger than . When , can grow to infinity, which is in line with Assumption (1b) in [60], where they allow the minimum spacing to be a function of and to vanish as diverges. In addition, we require the bandwidth parameter in (3) to satisfy as . Otherwise, if more than one break exists within a window of temporal width , the adopted MOSUM statistics might fail to distinguish the break time points in the same window. For any time point satisfying , we define the weighted break vectors as

| (20) |

and let . Under the alternative hypothesis, there exists at least one break, that is . We evaluate our testing power in the following corollary.

The symbols and hold here and throughout the rest of the paper in the asymptotic regime that . Corollary 1 provides a condition for the test power tending to . It allows for cases with nontrivial alternatives. Namely, in some component series, the break sizes could be small and tend to , as long as the aggregated size of the break is sufficiently large. It is generally challenging to make an exact comparison between different break statistics with different assumptions for complicated panel data. Nevertheless, we can observe that our detection lower bound is quite sharp in the situation where many weak signals with similar magnitude are present. For example, suppose the jump size of each component series is and then we only require . Compared with Table 1 in [19] which summarizes the procedures under different settings, is smaller than all entries in the table since we have in the denominator resulting from the -aggregation.

Remark 4 (Detailed power comparison of and statistics).

This remark is a complement to Remark 1. Now we clarify these differences by a detailed power comparison in those two cases. First, we consider sparse signals. Suppose that there is only one time series with a single break and the break size is , and we use the MOSUM with bandwidth for detection. Then to ensure the power tending to , only requires (see, for example, [13]), while needs a stronger condition by Corollary 1 that . Secondly, we check dense signals. Suppose all series jump with the same size . Then, for , we still need , while only requires .

2.4 Estimation of Change Points

Based on the theoretical underpinnings of the test in prior subsections, we can now present our detection algorithm (cf. Algorithm 1). To begin with, we explicate our strategy for detecting and estimating change points. Furthermore, we showcase the consistency for the estimators pertaining to the number, time stamps, and sizes of breaks. A simulation study can be found in Appendix A.3.

We consider the size of the break at time point normalized by the long-run standard deviation , that is . Define the minimum of normalized break sizes over time as

| (21) |

which can be viewed as the minimum strength of signals in the setting of Corollary 1.

Remark 5 (Comments on the centering term ).

To implement Algorithm 1, we need to provide the centering term defined in (7). Due to the weak temporal dependence of , one can show that

| (22) |

In practice, we can simply take the centering term to be . This still ensures the consistency results in Theorem 2 when the window size is slightly larger than the dimension , since the approximation error of using is of , which is smaller than the order of .

Remark 6 (Selection of bandwidth ).

Technically, the larger the bandwidth is, the more data points could be used. Thus, a larger would reduce the magnitude of noise, and then the signals shall be easier to detect. However, we also need to restrict , since the identification condition below Definition 1 requires us to have fewer than one break within each window. Therefore, we suggest starting with a small bandwidth, for example to ensure that . One could continue to increase the bandwidth until the estimated number of breaks decreases. We refer to Appendix A for a simulation study including the influences of different bandwidth parameters, as well as a discussion in Remark 12 for the potential extension of our method to a multi-scale MOSUM.

Now we outline the consistency results of estimators for break numbers, break time stamps and break sizes. We shall impose a minimum requirement of break sizes to guarantee that all of the breaks can be precisely captured and estimated.

Assumption 4 (Signal).

Assume .

We highlight that Assumption 4 imposes a moderate condition on the signals, which relates the break separation to the break signal strength , and does not require series to jump simultaneously. A comprehensive discussion on the advantage of our setting can be found following the consistency results presented below.

Theorem 2 (Temporal consistency).

The results in Theorem 2 are in an asymptotic context as . To see the advantage of our method, let us consider the simple case with a jump size for each component series. To achieve the consistency results in (ii), we only require by Assumption 4 and by the condition . Notably, as discussed following Corollary 1, our detection lower bound is weaker compared to those reported in Table 1 by [19]. In (iii), since contains both the signal part and the error part , we center under the null by subtracting . This guarantees that the break sizes can be estimated consistently. We have in the consistency rates in (ii) and (iii) since we take the maximum overall moving windows. It is also worth noticing that, for single change-point detection, [4] achieves by assuming that is a constant. Under this condition, by our Theorem 2 (ii), we can achieve the same consistency rate up to a logarithm factor. Indeed, does not need to be a constant for consistent estimators (of a single or finitely many breaks) with an order of ; see for instance [27]. Intuitively, a larger makes the estimation problem easier, and in the same example mentioned earlier, where the break size for each series is denoted as , one can see that our can diverge as grows, leading to improved consistency rates for .

3 Testing and Estimation via a Two-Way MOSUM

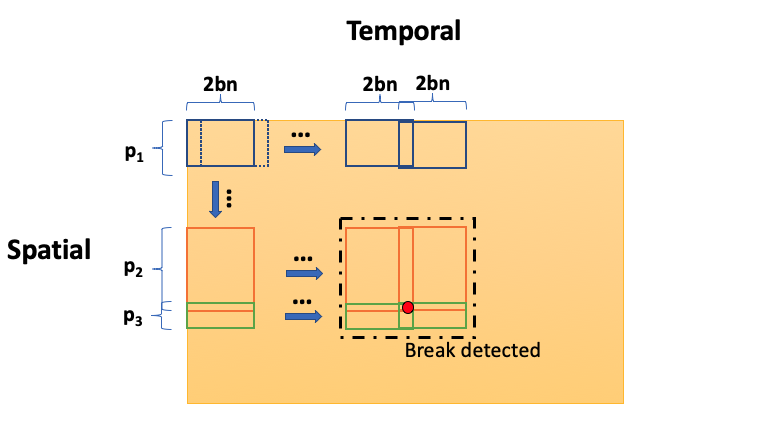

The previous section focuses on change-point statistics for data generating processes with dense breaks across all component series. In this section, we propose a novel Two-Way MOSUM to address cases where change points may exist in only a subset of time series. In such case, aggregating all component series using the -norm dilutes the testing power due to the overwhelming aggregated noises compared to signals. To handle this issue, we construct temporal-spatial windows (cf. Definition 4) to aggregate series within spatial neighborhoods and maximize over neighborhoods and time. Our method allows for the estimation of both the temporal break stamp and the spatial neighborhood that contains the breaks. We extend the Two-Way MOSUM to nonlinear processes and a general spatial space in Section 4.

3.1 Two-Way MOSUM

As [59] suggested, in certain applications, data streams could represent observations from multiple sensors, where breaks only occur in some but not all of them. However, testing procedures aggregating all sensors include noise from unaffected sensors in detection statistics, leading to poor performance. To address this problem, we introduce cross-sectional neighborhoods comprised of spatially adjacent series, and propose the Two-Way MOSUM to account for spatial group structure and detect existence of breaks. This statistic improves test performance for signals dense within clusters but sparse among them. We emphasize that Two-Way MOSUM can work even in the absence of a-prior clustering information. See the discussion below Definition 4 for detailed reasoning after introducing the temporal-spatial moving window.

To define the relative spatial locations of component series, we consider a spatial space for all series. In particular, we start with a simple case in this section by assuming a linear ordering in the coordinates, i.e., . Then in Section 4, we extend it to a more general space with for a general , where the spatial location of each series shall be determined by a -dimensional vector. We define the linear spatial neighborhood and the corresponding neighborhood-norm as follows.

Definition 2 (Linear spatial neighborhood).

Let be the set of coordinates in a spatial neighborhood, , where is the total number of spatial neighborhoods. We denote the size of each by . In particular, we define

| (23) |

Definition 3 (Linear nbd-norm).

For a -dimensional vector with a linear ordering in coordinates, we define the linear neighborhood-norm (nbd-norm) as , .

It shall be noted that the spatial neighborhoods defined in Definition 2 can be overlapped, which means that each component series can belong to multiple different spatial neighborhoods. Therefore, these spatial neighborhoods actually can be viewed as an analogue of the temporal moving windows, but moving in the spatial direction and allowing different window sizes (i.e. neighborhood sizes). All are only the indices of different spatial groups and do not necessarily reflect the spatial order of these groups. The size of each neighborhood could tend to infinity as .

We highlight that the spatial moving windows can be adapted to different data scenarios. Apart from an identification condition, we do not need more knowledge (e.g. clustered breaks) on the spatial structure of the signals. It is worth noting that similar definitions of neighborhoods are considered in the literature, see for example, [3, 1, 2]. These setups exclusively focus on the topological structure of neighborhood with simple Gaussian or i.i.d. assumptions. Comparably, we are more flexible in modeling spatial temporal dependency of the data. In fact, our spatial windows can be extended to more complicated shapes depending on the demand of applications as long as Assumption 5 is satisfied. Many real-life data streams, such as those in geographical or economic contexts, provide prior knowledge about which spatial groups are likely to include breaks, as demonstrated in the geostatistics data examples in Chapter 4 of [20]. Our definition of the temporal-spatial window (cf. Definition 4) does not require this prior knowledge, but if it is available, it can be utilized for the more relevant detection and estimation procedures.

Our goal is to model the breaks occurring on the vector of unknown trend functions. When there potentially exists a group structure, we formulate the trend function in (1) as

| (24) |

where is an unknown integer represents the number of localized breaks which could go to infinity as or increases; are the time stamps of the breaks with and , for some constant , where is allowed to tend to zero as ; is the jump vector at the time stamp with if , where is the index of the spatial location of the -th break. We define the break size as . In the rest of this paper, we use to denote the temporal-spatial location of the -th break.

To test the existence of spatially localized breaks, it suffices to test the null hypothesis

which denotes the case with no breaks, against the alternative that at least one break exists, that is, : there exists , such that . This enables us to identify both the time stamps and the spatial neighborhoods with significant breaks. Our Two-Way MOSUM statistic aims to adopt more flexible moving windows to efficiently capture both temporal and spatial information of breaks. To achieve this goal, we shall derive a localized test statistic which first aggregates the time series within each spatial neighborhood by an -norm and then take the maximum over all the neighborhoods and time points. Accordingly, we define temporal-spatial windows as follows:

Definition 4 (Temporal-spatial window).

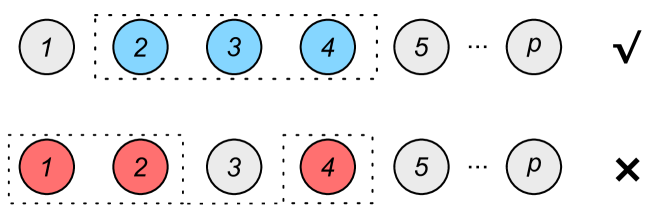

For , , define an index set . Then, define the temporal-spatial moving window as .

Note that the index set can be regarded as a vertical line, which is the center of the temporal-spatial moving window . Specifically, spans the neighborhood in the spatial direction and centered at the time point with radius in the temporal direction. In the rest of this paper, we shall depict the index set as a vertical line at time and neighborhood . We refer to Figure 10 in Appendix B.3 for a more straightforward illustration of this Two-Way moving window. It is worth emphasizing that even without prior knowledge of clusters, the number of potential windows is relatively small, because only the adjacent series can be assigned to the same group, which leads to the number of potential windows at most . See a more detailed explanation in Appendix B.3 and consider Figure 9 as an example. In general, for any time series, there are only at most possible windows in a space, . This fact does not diminish the validity of our results obtained through GA (cf. Theorem 3). Consequently, while prior knowledge about the clusters is beneficial for boosting power, it is not a prerequisite.

Definition 5 (Influenced set).

We define the set of vertical lines influenced by the break located at as

| (25) |

Assumption 5 (Neighborhood size).

Assume that holds for some constant , where and are defined in Definition 2.

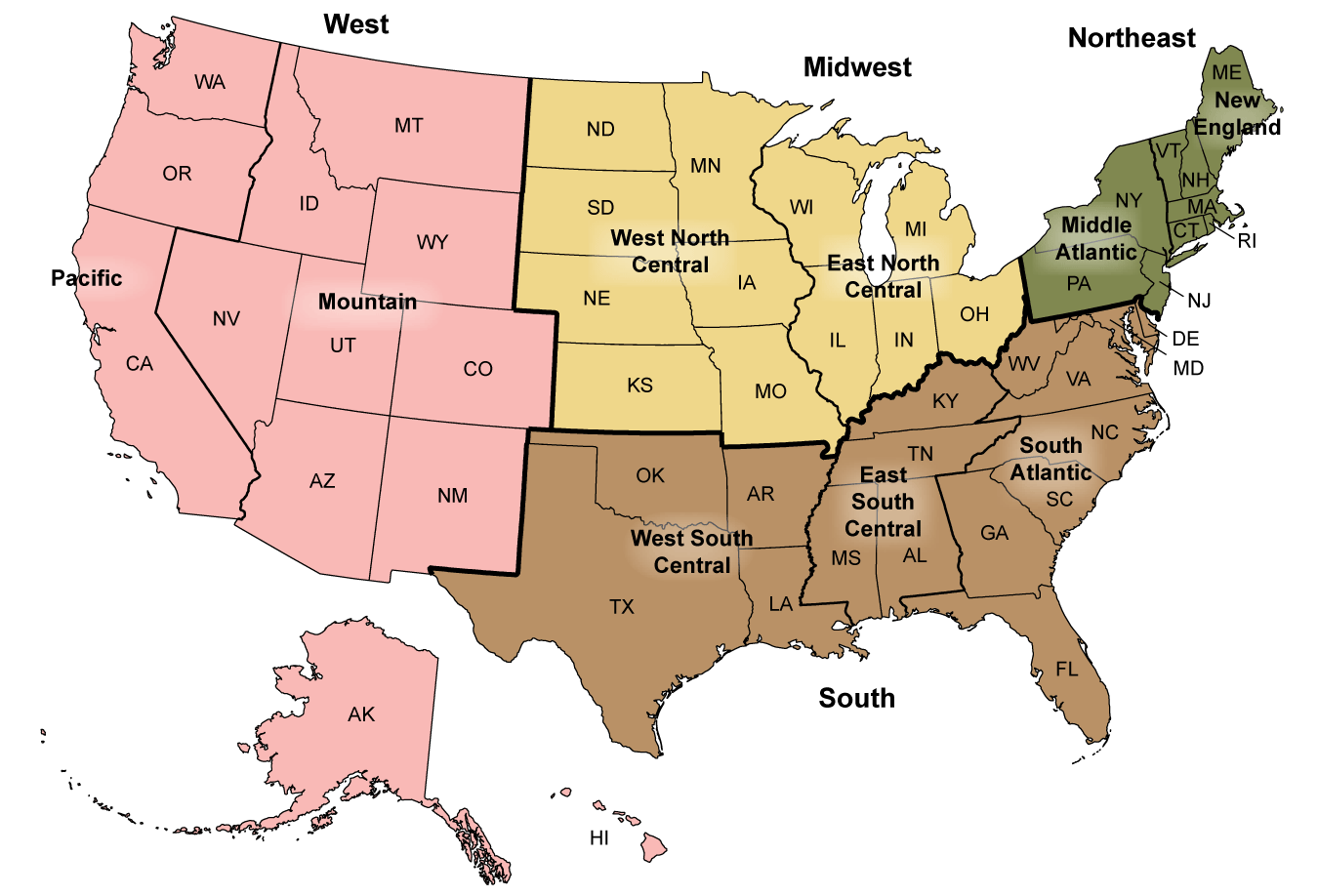

Assumption 5 requires that the sizes of all spatial neighborhoods do not differ too much, which still allows the flexibility of different neighborhood sizes but in a reasonable range. This assumption embraces many interesting cases in practice. For example, according to the geographical locations, the Centers for Disease Control and Prevention (CDC) divides the states in the United States (US) into four regions with similar spatial sizes, which is also taken into consideration in our application (cf. Section 5); based on the patterns of synchronous activity and communication between different brain regions, [61] identifies and segregates the brain into seven distinct functional networks with similar scales.

Similar to (7), we define the centering term of the statistics as

| (26) |

Following the intuitions that we could adopt temporal-spatial moving windows to account for spatially clustered jumps, we formulate our Two-Way MOSUM test statistic as follows:

| (27) |

where the nbd-norm is introduced in Definition 3. Recall (9) for . Let

| (28) |

Then, under the null hypothesis, we can rewrite into

| (29) |

When the time series are cross-sectionally independent, are independent, . Hence, by applying the GA to (29), we can properly address the dependence resulting from the overlapped temporal-spatial windows. We also note that cluster-based statistics can be seen as a special case of Two-Way MOSUM as in (29) when the prior knowledge of clusters is given, which can also be seen as an extension of the statistic introduced by [29] where one essentially gets back to his idea by taking each component as its own cluster.

We introduce the centered Gaussian vector

| (30) |

with the covariance matrix

| (31) |

Recall the covariance matrix for the Gaussian vector in (11). By (28) and (29), we similarly define

| (32) |

We aim to provide the GA theorem under the null with a Two-Way MOSUM applied (cf. Theorem 3). This result shall enable us to find the critical value of our proposed Two-Way MOSUM test statistic. We denote each element in by , where

| (33) |

By the GA, the distribution of shall approximate the one of our test statistic under the null with large , that is

| (34) |

Remark 7 (Comparison of MOSUM and -clustered Two-Way MOSUM).

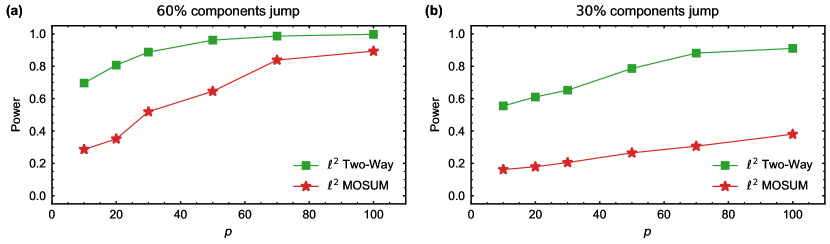

When the breaks only occur in a portion of time series, aggregation of all dimensions would cause power loss. This situation is frequently encountered when a spatial group structure exists and only a few groups have breaks. Our proposed Two-Way MOSUM can account for this situation by taking the -norm within each spatial group. To explicitly show the differences, we present a simulated example with two different proportions of jumps and compare the testing powers in Figure 2. We simulate observations of , , , , and . The number of spatial groups is and each group size is . Specifically, we let , and . In Figure 2(a), two groups and contain breaks at the same time . In Figure 2(b), breaks only exist in one group at . The errors in both two figures are generated from MA() models defined in (4) with and jump sizes are for each dimension. We let the window size . All the reported powers in Figure 2 are averaged over samples. We defer a more detailed power comparison to Remark 9.

3.2 Gaussian Approximation for Two-Way MOSUM

Given the updated statistics for spatially clustered signals, we further formalize our GA theory in this setting. Theoretically, it shall be noted that when signals are dense within the clusters and sparse among clusters, our Two-Way MOSUM improves the one adopted in Section 2.

Theorem 3 (GA for Two-Way MOSUM).

One shall note that the GA results in Theorem 1 is a special case of Theorem 3. Specifically, when and , which indicates that there does not exist any group structure and all time series belong to the same group, condition (15) can be implied by (36), and the same convergence rate of GA can be achieved. We extend the above theorem to nonlinear processes with general spatial temporal dependency in Theorem 4.

Remark 8 (Allowed neighborhood number and size).

In Theorem 3, we can allow the minimum neighborhood size to be of a polynomial order of the sample size , and its order depends on the moment parameter defined in Assumption 1. In particular, let , for some . Then, if , expression (37) holds. The larger the moment parameter is, the larger minimum group size we can allow. In addition, one shall note that the allowed number of neighborhoods can be as large as , while a bigger keeps more detailed local structure at the expense of time to inspect more windows.

Next, we consider the alternative hypothesis that there exists at least a break. Since the temporal-spatial moving windows can be overlapped, for the identification of breaks, we pose the following assumption on the separation of break locations.

Assumption 6 (Temporal-spatial separation).

For any two breaks located at and , , assume that there does NOT exist any moving window , , , such that and , where is defined in Definition 5.

Assumption 6 can be viewed as an analogue of the condition below Definition 1 when we apply a Two-Way MOSUM. To see this, consider the trend function in (2). For any two breaks located at and , guarantees that there is no moving window intersects both and , where (resp. ) is the sliding window (resp. influenced set) spanning all components. This adheres to the separation requirement in Assumption 6.

To achieve consistent estimation of the temporal and spatial break locations, for any given significance level , we can choose the threshold value to be the quantile of the Gaussian limiting distribution indicated by Theorem 3, that is

| (38) |

Hence, we shall reject the null hypothesis if . To evaluate the power of our localized test, consider the alternative hypothesis that there exists at least a break, i.e., . We provide the power limit of our localized change-point detection in the following corollary.

Corollary 2 (Power of a Two-Way MOSUM).

Remark 9 (Detailed power comparison of MOSUM and -clustered Two-Way MOSUM).

This comment is complementary to Remark 7. Here we compare the testing power of the MOSUM aggregating all time series and the Two-Way MOSUM. Specifically, we consider a case where time series belong to groups and breaks only occur to one group. Suppose that all the series in this group jump with the same size , and we use the (Two-Way) MOSUM with bandwidth for detection. Then, to ensure the power tending to , by Corollary 2, only requires , while needs a stronger condition by Corollary 1 that .

3.3 Estimation of Change Points with Spatial Localization

Providing the GA for the Two-Way MOSUM statistics, we gather the detailed steps of a change-point estimation procedure in Algorithm 2. Specifically, we extend Algorithm 1 to the cases with cross-sectional localization via Two-Way MOSUM, and we shall expect to obtain spatial locations of change points besides the temporal ones. One follow-up theorem shows the consistency properties of some break statistics in this setup.

We denote the minimum break size over time and spatial neighborhoods by

| (39) |

and assume that this minimum break size is lower bounded as follows:

Assumption 7 (Signal).

.

Let us consider the simple example that within any spatial neighborhood , , the jump size of each time series is the same, denoted by . Then, Assumption 7 means , which is a weaker requirement of the signal strength for each series with breaks similar to Assumption 4.

To implement Algorithm 2, by the definition of in (26) and the similar arguments in Remark 5, one can take , which still ensures the consistency. Also, similar to Algorithm 1, the selection of bandwidth parameter can follow the suggestions in Remark 6, and the long-run variance can be estimated by a robust M-estimation method. The consistency results of the estimated number and temporal-spatial locations of breaks as well as the break sizes are all provided.

Proposition 1 (Temporal-spatial consistency).

Let . Suppose that Assumptions 1–3, 5–7 and condition (36) hold. If , and , then we have the following results.

-

(i)

(Number of breaks). .

-

(ii)

(Time stamps of breaks). , where and . If in addition, , then

-

(iii)

(Spatial locations of breaks). If there exists a constant such that , for all and , then

where and .

-

(iv)

(Break sizes). . This also implies that

Proposition 1 (i) indicates the consistency of the estimator for the number of significant breaks; (ii) and (iii) show that we can consistently recover both the spatial break neighborhood and the temporal break stamp ; (iv) suggests that the sizes of break vector can also be estimated consistently. Note that in Proposition 1 (ii), indicates the temporal precision, and the spatial precision is represented by in (iii). Both results are normalized by their window widths respectively and the two consistency rates are of the same order.

Remark 10 (Comparison of consistency rates with Theorem 2).

We see that the temporal consistency rate of in Proposition 1 (ii) is similar to that in Theorem 2 except for an additional term in the log factor. For the break size, the convergence rate of similarly admits an additional term in the log factor compared to in Theorem 2. Both two terms result from the maximization over all spatial neighborhoods in the estimators.

4 Nonlinear Time Series with Cross-Sectional Dependence

In this section, we present three generalizations. Firstly, we expand the linear series given in (4) to accommodate a nonlinear scenario (see Eq. (49)) for a broader range of time series models. Secondly, we move beyond the linear ordering in coordinates by introducing a more comprehensive space in the spatial dimension, denoted as (where is a fixed integer). Lastly, we generalize the GA from earlier sections by allowing weak cross-sectional dependence in the underlying error process. We will begin with the definition of the new spatial space and the nonlinear model, proceed with the conditions for both temporal and cross-sectional dependence structures, and ultimately, present our primary theoretical findings and the rationale behind the proof strategy.

4.1 Multi-Dimensional Spatial Space

To detect breaks in , we shall first provide a generalized notion of spatial window accordingly. In particular, denote , , as spatial neighborhoods, which is a generalization of in the previous section. Without loss of generality, we focus on hyper rectangles,

| (40) |

where is some interval on whose end points and can depend on . Different are allowed to be overlapped and can go to infinity as . We define and let , which implies

| (41) |

Suppose that the total number of locations in denoted as is , which can go to infinity as increases. We consider the time series model

| (42) |

Our main objective is to identify possible change points in the trend functions

| (43) |

where and are defined similarly to those in (2); represents the benchmark level when no break occurs, and denotes the jump at time point and location in the neighborhood , the -th spatial neighborhood containing breaks.

We then introduce definitions to characterize the mass and volume of the spatial neighborhood . By working with the spatial location , we can bypass the linear ordering presented in Section 3. This notion of spatial location is similar to the general definition of spatial change-points in a -dimensional spatial lattice used in studies such as [64] and [39].

Definition 6 (Spatial neighborhood).

(i) (Mass). Define the mass of the spatial neighborhood by the number of series in , i.e. , where is the number of elements in a Borel set. Denoted by and the sizes of the smallest and biggest spatial neighborhoods, respectively, i.e.,

which satisfy , for some constant . (ii) (Volume). Define the volume of the spatial neighborhood as , where is the Lebesgue measure of a Borel set.

Following [40], we introduce the following density assumption on the spatial space that makes it possible to extend the asymptotic properties in regular space in to ones in irregular space.

Assumption 8 (Density of spatial space ).

Let , , be the spatial locations in on which is observed, . Assume that each can be written as Here, is a sequence of i.i.d. random vectors with a density function with a compact support in . We assume that as , for all . Also, for all , for some constants .

Here we only require the density function to be uniformly bounded from both sides, which is a weaker condition compared to Assumption 1 in [40], where they aim to perform Fourier analysis for irregularly spaced data on and more restrict assumptions such as the existence of higher-order derivatives of are therefore desired. Differently, our goal is to perform block approximation in the spatial direction to deal with the cross-sectional dependence (cf. Remark 14), which in fact only requires that, for any hyper-rectangle satisfying , there exist constants such that One can view this condition as a special case of Assumption 8. Also, when it breaks down to a simple space with linear ordering, the linear spatial neighborhood defined in Definition 2 can be represented by and we have , , that is for all with . Concerning the shape of spatial neighborhoods, we pose the following assumption to eliminate the degenerate case which holds little relevance in the context of spatial statistics.

Assumption 9 (Neighborhood shape).

There exists a constant , such that for each neighborhood , .

4.2 Generalized Two-Way MOSUM

We now introduce a generalized Two-Way MOSUM, designed to accommodate the multi-dimensional spatial space constructed in the previous section. Let , . We denote the long-run covariance matrix of and the corresponding diagonal matrix by

| (44) |

respectively, where representing the long-run variance of the component . To test for the existence of breaks, we denote , and evaluate a jump statistic defined by

| (45) |

Note that comprises the signal part and the noise part . Under the null hypothesis, where no break exists and , we define the centering term of the -aggregation of within the neighborhood as

| (46) |

Subsequently, we propose the following test statistic

| (47) |

Under the null hypothesis , since , we can rewrite into

| (48) |

It shall be noted that when , the test statistic reduces to in Section 3.

4.3 Dependence Structure

Although it is quite convenient to assume that the errors are cross-sectionally i.i.d., it is unrealistic to ignore the spatial dependence. The assumption on cross-sectional independence in previous sections can be relaxed accordingly to allow for a weak spatial dependence case. In this section, we extend the GA in Section 3 to the cases where the underlying errors are allowed to be cross-sectionally weakly dependent. This will allow us to evaluate the critical values of the test statistics accordingly.

Suppose that the stationary noise process in (1) is of the form:

| (49) |

Here , , , are i.i.d. random variables, and is an -valued measurable function such that is well-defined. We assume throughout the paper that and , for some . Next, we introduce the functional dependence measures to characterize the temporal and spatial dependence structure of . Let be an i.i.d. copy of . Specifically, we consider the temporal and temporal-spatial coupled versions of defined respectively by

where for any and ,

Following [57], we generalize the functional dependence measures as follows

| (50) |

Note that represents the change measure of dependence by perturbing solely in the temporal direction, while denotes the counterpart which perturbs in both the temporal and spatial directions.

To account for the temporal and cross-sectional dependence structure of , we shall impose the following assumptions on and . The assumptions essentially require the algebraic decay of dependence both in the temporal and the spatial directions and are controlling the tail behavior of the noise terms.

Assumption 10 (Finite moment).

Assume , for .

Assumption 11 (Temporal dependence).

There exist some constants and , such that, for all , for .

Assumption 12 (Weak cross-sectional dependence).

Assume that there exist some constants and , such that, for all ,

| (51) |

It shall be noted that we can also switch the temporal and spatial aggregation in the above assumption. Specifically, (51) also implies

| (52) |

To see this, for any , we denote the partial sum . Let , and . By the triangle inequality, . Since , we let and achieve the desired result. Furthermore, (52) also indicates the decay of cross-sectional long-run correlation as depicted in Lemma 1.

Lemma 1 (Decay of long-run correlation).

Assume that condition (52) holds. Then, for any , the long-run correlation between and , denoted by , decays at a polynomial rate as increases, that is

| (53) |

4.4 Gaussian Approximation with Weak Cross-Sectional Dependence

This subsection is devoted to the GA in the high-dimensional setting under the above-mentioned general framework. In the case when is fixed, we provide an invariance principle in Appendix B.2. When grows to infinity as increases, to derive the limiting distribution of the test statistic under the null, we introduce the centered Gaussian random vector

| (54) |

with the covariance matrix

| (55) |

Let , and equals to

| (56) |

We defer the detailed evaluation of (56) to Lemma 15. Note that, if for all , and , , which denotes the case with no spatial dependence, then (56) is the same as (32). Recall defined in (33). We denote each element in by , where . Similar to the cross-sectionally independent case, we can approximate the limiting distribution of under the null by the one of . We refer to Remark 14 in Appendix C for the proof strategies based on the block approximation.

Theorem 4 (GA with weak cross-sectional dependence).

Remark 11 (Comparison with Theorem 3).

Moving on to the alternative hypothesis, we can set the detection threshold as the critical value of determined by the Gaussian limiting distribution presented in Theorem 4. Specifically, we set as , for significant level . We reject the null hypothesis if . For any time point that satisfies , we define the weighted break as . Under the alternative, where there exists and such that , we refer to Corollary 4 in Appendix B.5 for the power limit of our test. Further algorithm for detecting and identifying breaks can be developed accordingly.

5 Application

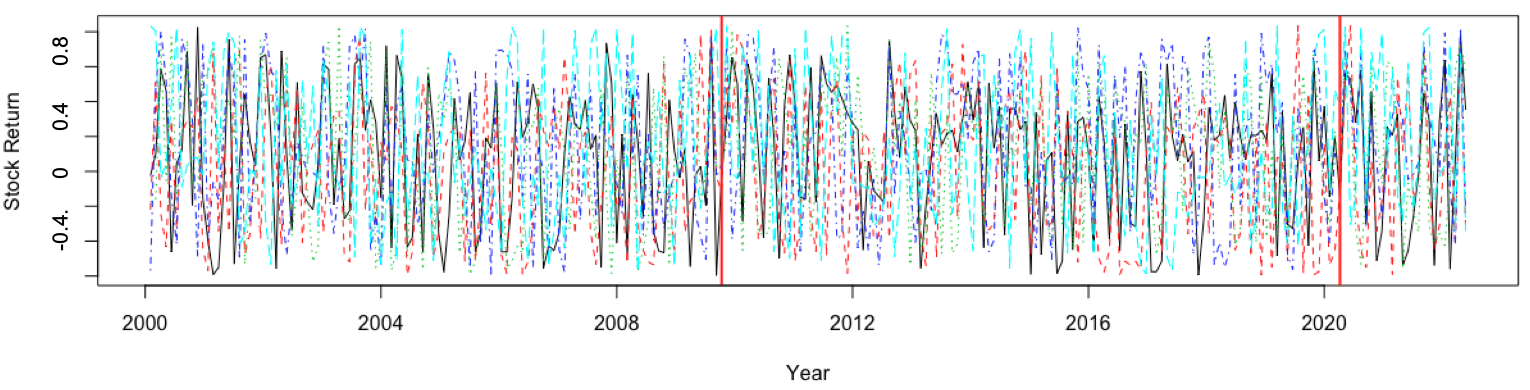

This section is devoted to the real-data analysis to illustrate our proposed method for multiple change-point detection. We apply Algorithm 1 to a stock-return dataset and use Algorithms 1 and 2 to a COVID-19 dataset. Due to the space limit, we defer the results of the stock-return data to Appendix A.4.

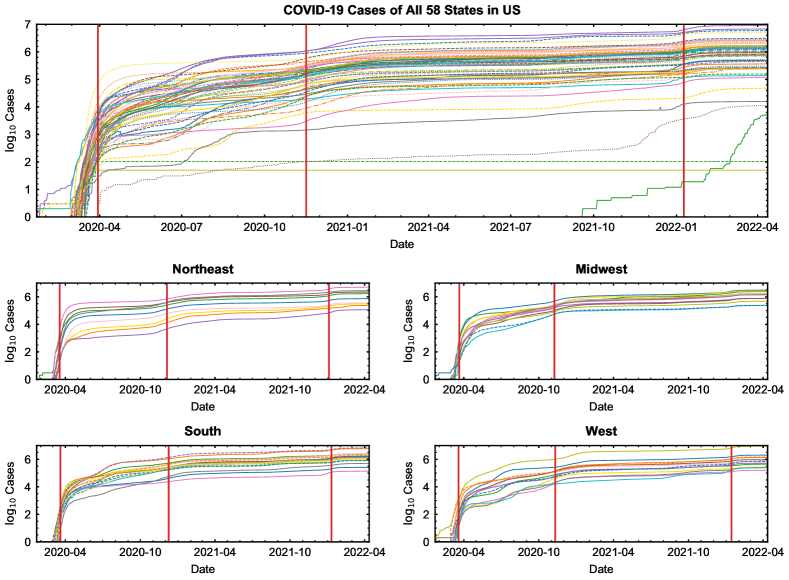

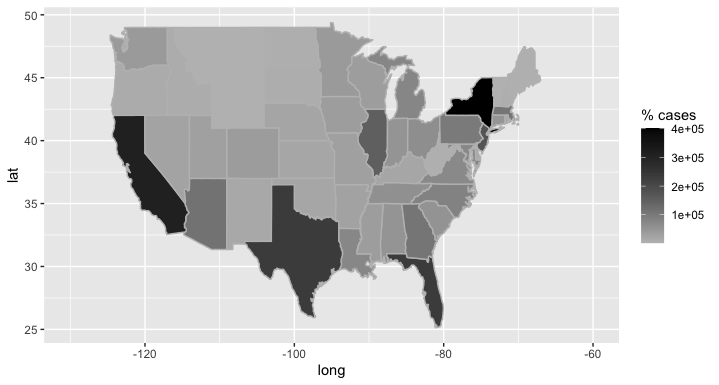

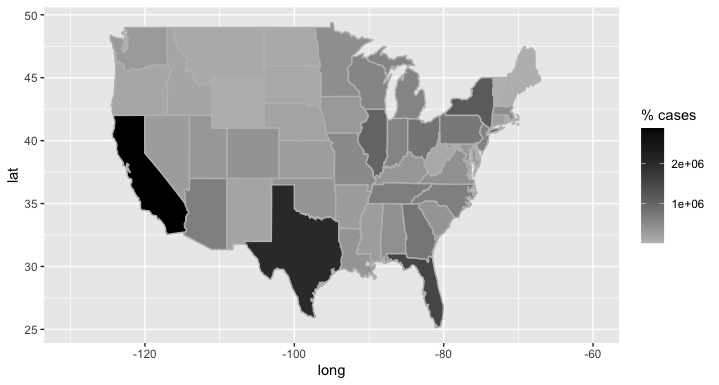

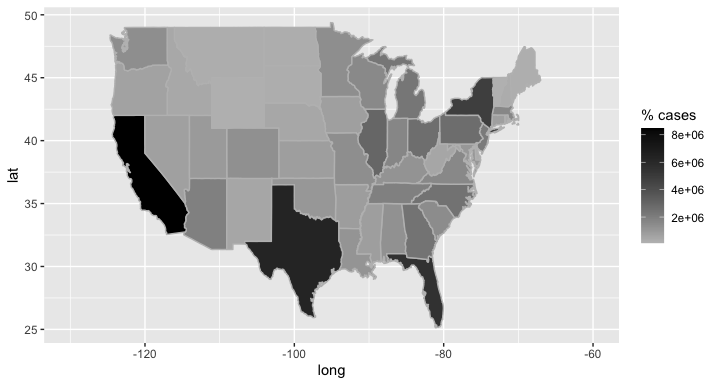

Analyzing 812 days of daily COVID-19 case numbers in the US, we identified three significant breaks (Figure 3 top): March 2020 (first outbreak), October 2020 (Delta variant), and December 2021 (Omicron variant). Further, we consider four geographic regions of the US as per the guidelines of the CDC: Northeast, Midwest, South, and West. A map of these four regions is available in Figure 8 in Appendix A.5. By our algorithm, each region exhibited different break time stamps, with the Northeast and West experiencing early outbreaks due to major international airports. The Midwest was the first to encounter the Delta variant, while the Northeast initially faced the Omicron variant. Our detection algorithm effectively captured these variations (Figure 3 bottom), demonstrating the efficacy of our proposed testing procedures in identifying breaks over time and across diverse locations. For more detailed information, please refer to Appendix A.5.

References

- [1] Louigi Addario-Berry, Nicolas Broutin, Luc Devroye and Gábor Lugosi “On combinatorial testing problems” In The Annals of Statistics 38, 2010, pp. 3063–3092

- [2] Ery Arias-Castro, Emmanuel J Candes and Arnaud Durand “Detection of an anomalous cluster in a network” In The Annals of Statistics 39 JSTOR, 2011, pp. 278–304

- [3] Ery Arias-Castro, Emmanuel J. Candès, Hannes Helgason and Ofer Zeitouni “Searching for a trail of evidence in a maze” In The Annals of Statistics 36, 2008, pp. 1726–1757

- [4] Jushan Bai “Common breaks in means and variances for panel data” In Journal of Econometrics 157.1, Nonlinear and Nonparametric Methods in Econometrics, 2010, pp. 78–92

- [5] Jushan Bai, Xu Han and Yutang Shi “Estimation and inference of change points in high-dimensional factor models” In Journal of Econometrics 219.1 Elsevier, 2020, pp. 66–100

- [6] Jushan Bai and Pierre Perron “Estimating and testing linear models with multiple structural changes” In Econometrica 66.1, 1998, pp. 47–78

- [7] Ian Barnett and Jukka-Pekka Onnela “Change point detection in correlation networks” In Scientific Reports 6.1, 2016, pp. 18893

- [8] Donald L. Burkholder “Sharp inequalities for martingales and stochastic integrals” In Colloque Paul Lévy sur les processus stochastiques, Astérisque 157-158 Société mathématique de France, 1988, pp. 75–94

- [9] Olivier Catoni “Challenging the empirical mean and empirical variance: A deviation study” In Annales de l’Institut Henri Poincaré, Probabilités et Statistiques 48.4, 2012, pp. 1148–1185

- [10] Julian Chan, Lajos Horváth and Marie Hušková “Darling–Erdős limit results for change-point detection in panel data” In Journal of Statistical Planning and Inference 143.5, 2013, pp. 955–970

- [11] Cathy Yi-Hsuan Chen, Yarema Okhrin and Tengyao Wang “Monitoring network changes in social media” In To appear in Journal of Business & Economic Statistics, 2022

- [12] LiKai Chen, Weining Wang and Wei Biao Wu “Dynamic semiparametric factor model with structural breaks” In Journal of Business & Economic Statistics 39, 2021, pp. 757–771

- [13] Likai Chen, Weining Wang and Wei Biao Wu “Inference of breakpoints in high-dimensional time series” In Journal of the American Statistical Association 117.540, 2022, pp. 1951–1963

- [14] Yudong Chen, Tengyao Wang and Richard J. Samworth “High-dimensional, multiscale online changepoint detection” In arXiv preprint arXiv:2003.03668, 2020

- [15] Victor Chernozhukov, Denis Chetverikov and Kengo Kato “Central limit theorems and bootstrap in high dimensions” In The Annals of Probability 45.4, 2017, pp. 2309–2352

- [16] Victor Chernozhukov, Denis Chetverikov and Yuta Koike “Nearly optimal central limit theorem and bootstrap approximations in high dimensions” In arXiv preprint arXiv: 2012.09513, 2021

- [17] Haeran Cho “Change-point detection in panel data via double CUSUM statistic” In Electronic Journal of Statistics 10.2, 2016, pp. 2000–2038

- [18] Haeran Cho and Piotr Fryzlewicz “Multiple-change-point detection for high dimensional time series via sparsified binary segmentation” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 77.2 Wiley Online Library, 2015, pp. 475–507

- [19] Haeran Cho and Claudia Kirch “Two-stage data segmentation permitting multiscale change points, heavy tails and dependence” In Annals of the Institute of Statistical Mathematics 74.4 Springer, 2022, pp. 653–684

- [20] Noel Cressie “Statistics for spatial data” John Wiley & Sons, 2015

- [21] Birte Eichinger and Claudia Kirch “A MOSUM procedure for the estimation of multiple random change points” In Bernoulli 24.1, 2018, pp. 526–564

- [22] Farida Enikeeva and Zaid Harchaoui “High-dimensional change-point detection under sparse alternatives” In The Annals of Statistics 47.4 Institute of Mathematical Statistics, 2019, pp. 2051–2079

- [23] Farnaz Zamani Esfahlani, Youngheun Jo, Joshua Faskowitz, Lisa Byrge, Daniel P. Kennedy, Olaf Sporns and Richard F. Betzel “High-amplitude cofluctuations in cortical activity drive functional connectivity” In Proceedings of the National Academy of Sciences 117.45, 2020, pp. 28393–28401

- [24] Joshua Faskowitz, Farnaz Zamani Esfahlani, Youngheun Jo, Olaf Sporns and Richard F. Betzel “Edge-centric functional network representations of human cerebral cortex reveal overlapping system-level architecture” In Nature Neuroscience 23.12, 2020, pp. 1644–1654

- [25] Piotr Fryzlewicz “Wild binary segmentation for multiple change-point detection” In The Annals of Statistics 42.6 Institute of Mathematical Statistics, 2014, pp. 2243–2281

- [26] Lajos Horváth and Marie Hušková “Change-point detection in panel data” In Journal of Time Series Analysis 33.4, 2012, pp. 631–648

- [27] Lajos Horváth, Marie Hušková, Gregory Rice and Jia Wang “Asymptotic properties of the CUSUM estimator for the time of change in linear panel data models” In Econometric Theory 33.2, 2017, pp. 366–412

- [28] Marie Hušková and Aleš Slabý “Permutation tests for multiple changes” In Kybernetika 37.5, 2001, pp. 605–622

- [29] Moritz Jirak “Uniform change point tests in high dimension” In The Annals of Statistics 43.6 Institute of Mathematical Statistics, 2015, pp. 2451–2483

- [30] Robert M. Jong “Central limit theorems for dependent heterogeneous random variables” In Econometric Theory 13.3, 1997, pp. 353–367

- [31] Sayar Karmakar and Wei Biao Wu “Optimal Gaussian Approximation for Multiple Time Series” In Statistica Sinica 30.3, 2020, pp. 1399–1417

- [32] Rebecca Killick, Paul Fearnhead and I.A. Eckley “Optimal detection of changepoints with a linear computational cost” In Journal of the American Statistical Association 107, 2012, pp. 1590–1598

- [33] Claudia Kirch and Philipp Klein “Moving sum data segmentation for stochastics processes based on invariance” In arXiv preprint arXiv:2101.04651, 2021

- [34] Arun K Kuchibhotla, Lawrence D Brown, Andreas Buja, Edward I George and Linda Zhao “Uniform-in-submodel bounds for linear regression in a model-free framework” In To appear in Econometric Theory Cambridge University Press, 2021

- [35] Sokbae Lee, Myung Hwan Seo and Youngki Shin “The lasso for high dimensional regression with a possible change point” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 78.1, 2016, pp. 193–210

- [36] Céline Lévy-Leduc and François Roueff “Detection and localization of change-points in high-dimensional network traffic data” In Annals of Applied Statistics 3.2, 2009, pp. 637–662

- [37] Degui Li, Junhui Qian and Liangjun Su “Panel data models with interactive fixed effects and multiple structural breaks” In Journal of the American Statistical Association 111.516, 2016, pp. 1804–1819

- [38] Bin Liu, Zhengling Qi, Xinsheng Zhang and Yufeng Liu “Change Point Detection for High-dimensional Linear Models: A General Tail-adaptive Approach” In arXiv preprint arXiv:2207.11532, 2022

- [39] Oscar Hernan Madrid Padilla, Yi Yu and Alessandro Rinaldo “Lattice partition recovery with dyadic CART” In Advances in Neural Information Processing Systems 34, 2021, pp. 26143–26155

- [40] Yasumasa Matsuda and Yoshihiro Yajima “Fourier analysis of irregularly spaced data on Rd” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 71.1, 2009, pp. 191–217

- [41] Michael Messer, Marietta Kirchner, Julia Schiemann, Jochen Roeper, Ralph Neininger and Gaby Schneider “A multiple filter test for the detection of rate changes in renewal processes with varying variance” In The Annals of Applied Statistics 8.4, 2014, pp. 2027–2067

- [42] S.. Nagaev “Large Deviations of Sums of Independent Random Variables” In The Annals of Probability 7.5, 1979, pp. 745–789

- [43] Fedor Nazarov “On the maximal perimeter of a convex set in with respect to a Gaussian measure” Springer, Berlin, 2003, pp. 169–187

- [44] Adam B. Olshen, E.. Venkatraman, Robert Lucito and Michael Wigler “Circular binary segmentation for the analysis of array-based DNA copy number data” In Biostatistics 5.4, 2004, pp. 557–572

- [45] J.-P. Onnela, A. Chakraborti, K. Kaski, J. Kertész and A. Kanto “Dynamics of market correlations: Taxonomy and portfolio analysis” In Physical Review E 68.5, 2003, pp. 056110

- [46] Carl Edward Rasmussen and Christopher K.. Williams “Gaussian processes for machine learning”, Adaptive computation and machine learning Cambridge, Mass: MIT Press, 2006

- [47] Emmanuel Rio “Moment inequalities for sums of dependent random variables under projective conditions” In J Theor Probab 22.1, 2009, pp. 146–163

- [48] A.. Scott and M. Knott “A cluster analysis method for grouping means in the analysis of variance” In Biometrics 30.3, 1974, pp. 507–512

- [49] Xiaofeng Shao “A self-normalized approach to confidence interval construction in time series” In Journal of the Royal Statistical Society. Series B (Statistical Methodology) 72.3, 2010, pp. 343–366

- [50] Michael L Stein “Interpolation of spatial data: some theory for kriging” Springer Science & Business Media, 1999

- [51] Robert Tibshirani and Pei Wang “Spatial smoothing and hot spot detection for CGH data using the fused lasso” In Biostatistics 9.1, 2008, pp. 18–29

- [52] Daren Wang and Zifeng Zhao “Optimal change-point testing for high-dimensional linear models with temporal dependence” In arXiv preprint arXiv:2205.03880, 2022

- [53] Runmin Wang and X. Shao “Hypothesis testing for high-dimensional time series via self-normalization” In The Annals of Statistics 48.5 Institute of Mathematical Statistics, 2020, pp. 2728–2758

- [54] Runmin Wang and Xiaofeng Shao “Dating the break in high-dimensional data” In arXiv preprint arXiv:2002.04115, 2020

- [55] Runmin Wang, Changbo Zhu, Stanislav Volgushev and Xiaofeng Shao “Inference for change points in high-dimensional data via selfnormalization” In The Annals of Statistics 50.2 Institute of Mathematical Statistics, 2022, pp. 781–806

- [56] Tengyao Wang and Richard J. Samworth “High dimensional change point estimation via sparse projection” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 80.1, 2018, pp. 57–83

- [57] Wei Biao Wu “Nonlinear system theory: Another look at dependence” In Proceedings of the National Academy of Sciences 102.40, 2005, pp. 14150–14154

- [58] Wei Biao Wu and Zhibiao Zhao “Inference of trends in time series” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 69.3, 2007, pp. 391–410

- [59] Yao Xie and David Siegmund “Sequential multi-sensor change-point detection” In The Annals of Statistics 41.2, 2013, pp. 670–692

- [60] Haotian Xu, Daren Wang, Zifeng Zhao and Yi Yu “Change point inference in high-dimensional regression models under temporal dependence” In arXiv preprint arXiv:2207.12453, 2022

- [61] B.. Yeo, Fenna M. Krienen, Jorge Sepulcre, Mert R. Sabuncu, Danial Lashkari, Marisa Hollinshead, Joshua L. Roffman, Jordan W. Smoller, Lilla Zöllei, Jonathan R. Polimeni, Bruce Fischl, Hesheng Liu and Randy L. Buckner “The organization of the human cerebral cortex estimated by intrinsic functional connectivity” In Journal of Neurophysiology 106.3, 2011, pp. 1125–1165

- [62] Mengjia Yu and Xiaohui Chen “Finite sample change point inference and identification for high-dimensional mean vectors” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 83.2, 2021, pp. 247–270

- [63] Yi Yu “A review on minimax rates in change point detection and localisation” In arXiv preprint arXiv:2011.01857, 2020

- [64] Yi Yu, Oscar Madrid and Alessandro Rinaldo “Optimal partition recovery in general graphs” In International Conference on Artificial Intelligence and Statistics, 2022, pp. 4339–4358 PMLR

- [65] Nancy R. Zhang, David O. Siegmund, Hanlee Ji and Jun Z. Li “Detecting simultaneous changepoints in multiple sequences” In Biometrika 97.3, 2010, pp. 631–645

Appendix A Simulation and Application

A.1 Estimation of Long-Run Covariance Matrices

Recall that in previous sections, we assumed that the long-run covariance matrix is known, which, however, is hardly realistic in practice. Therefore, we utilize a robust M-estimation introduced by [9] and extended by [13] for the long-run covariance matrix to ensure our Gaussian approximation theory can still work even when the long-run covariance matrix is not given. Note that the classical covariance matrix estimation procedure is not directly applicable in our setting due to possible breaks.

First, we group observations into blocks with each block having same size . We denote the index set of the observations in the -th block by and define the average of the observations in the block as

Under the classic setting without change points, we can estimate the long-run covariance matrix by

where the difference between is aimed to cancel out the trends, since our trend function is piece-wise constant. But when there exist break points which cannot be canceled out by simply taking the difference, this estimator would fail as it is contaminated by the breaks. Hence, we consider a robust version of M-estimator ([13]) that fits well to our interest to estimate the long-run covariance matrix.

To this end, we let , and for , we define

| (58) |

Now, we introduce the M-estimation zero function of the long-run covariance matrix to be, for some ,

| (59) |

where and

| (60) |

As indicated by [9], the function is bounded by , and it is also Lipschitz continuous with the Lipschitz constant bounded by 1. Additionally, the non-decreasing influence function has neat envelopes in the form that

| (61) |

To obtain a consistent estimator of the long-run covariance matrix , we solve the equation for each , and use the root to be the estimator of the element with indices in the long-run covariance matrix. We denote this estimator by . Since the equation may have more than one solution, in which case any of them can be used to define . Finally, we collect the estimates of all the elements and combine them into the long-run covariance matrix,

| (62) |

In particular, we define and set in expression (59) to be . Here we present the consistency result of the estimated long-run covariance matrix.

Theorem 5 (Consistency of the estimated long-run covariance matrix).

Suppose that conditions in Theorem 1 hold and the number of breaks . We take . Then

where , for matrix .

Proof of Theorem 5.

The proof strategies essentially follow Proposition 2.4 in [9] and Theorem 5 in [13]. The main difference is that we relax the assumption which restricts the number of breaks to be finite in [13]. In other words, we allow . First, we consider the set

| (63) |

One can see that . Let . For the block estimators without change points, we define the corresponding M-estimation zero function as

| (64) |

For , we define the block-mean and block-variance respectively by

| (65) |

For , we define the envelope bound functions

| (66) |

By applying the result of Step 1 in Theorem 5 [13], we can bound the expected influence functions without change points in the following way:

| (67) |

Further, following Step 2 in Theorem 5 [13], we can show that the estimated influence function is concentrated around its mean , that is, for some constant and , we have the tail probability

| (68) |

where and the constant in are independent of and . Next, we shall bound the difference between the estimator and the true long-run covariance . Since is defined on the blocks without change points, we can similarly follow Step 3 in Theorem 5 in [13]. The only difference is that in our setting, we have assumed that the trend function is piece-wise constant while they assumed a smooth trend. Therefore, we can obtain that

| (69) |

Lastly, we consider the blocks with change points. Since and , for any , it follows that

| (70) |

This, together with expressions (67) and (A.1) with , yields, with probability tending to 1, for all , and ,

| (71) |

where

| (72) |

It shall be noted that to ensure the existence of real roots for , we need to have

| (73) |

Suppose that expression (73) holds, and we denote the smaller real root by , then we have

| (74) |

We take . Since is lower bounded for any , it follows from expression (69) that

| (75) |

We can obtain a similar bound for the larger real root . Then, when expression (71) is satisfied, we can bound the long-run estimator by . We let . Then, with probability tending to 1, we have

| (76) |

uniformly over , where . Also note that there exist some constants such that for any with probability tending to 1, which completes the proof. ∎

A.2 Simulation Under the Null

First, we show the Gaussian approximation results under the null. Three different models are considered to generate the errors , which are (i) i.i.d., (ii) AR(1), and (iii) MA(). Specifically, we consider the AR(1) model , where uniformly range from 0.6 to 0.9, and follow two different types of distributions, which are and . For each component series , we assume that it takes the form

Throughout all the simulation study in this paper, we let which is larger than the number of observations . Furthermore, we denote and generate by computing , where uniformly range from 0.5 to 0.9. We set to be 2 which determines the decay speed of the temporal dependence.

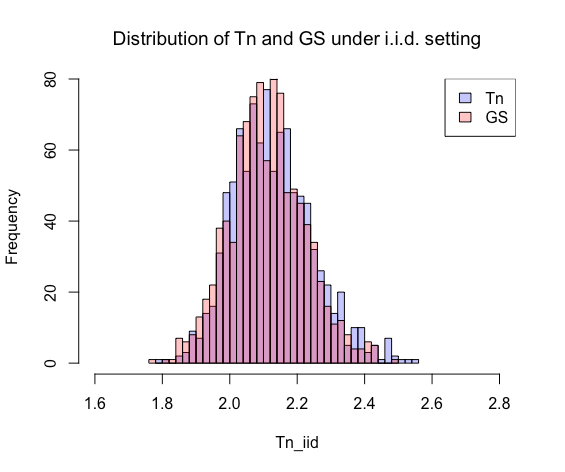

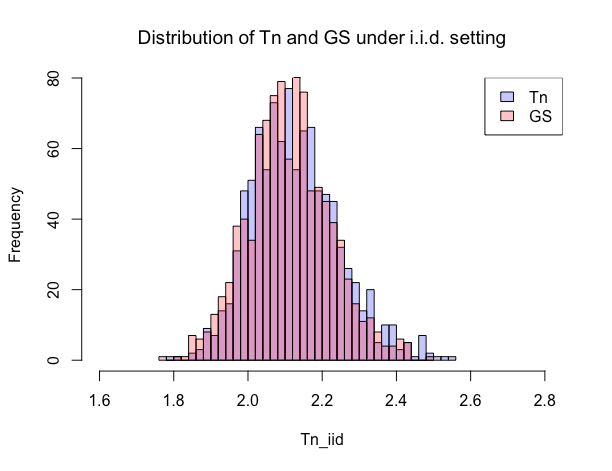

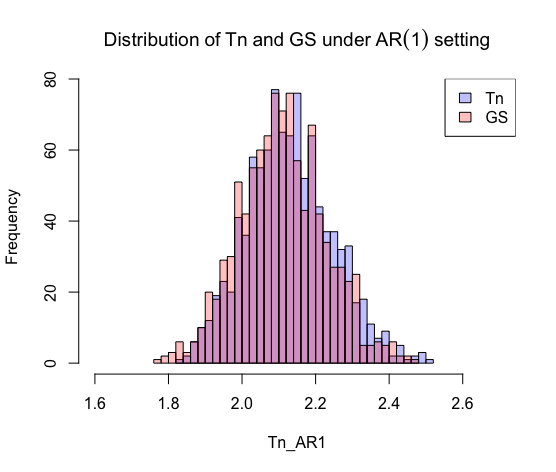

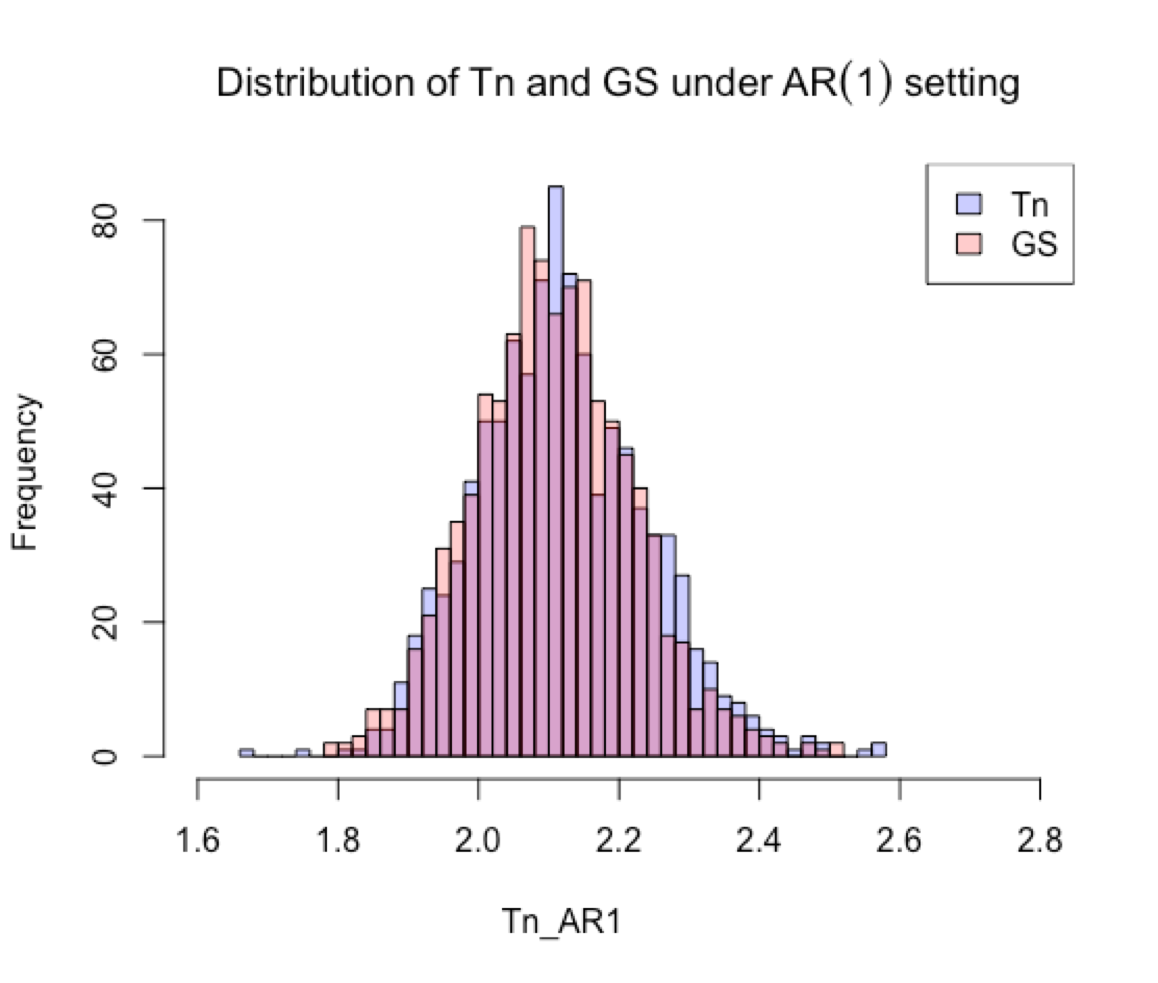

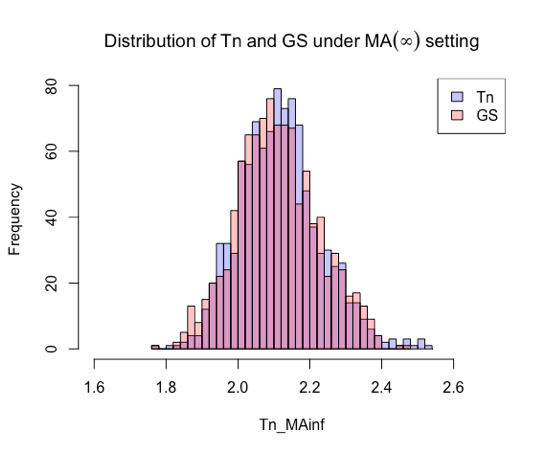

First, we intuitively present the distributions of our test statistic and the corresponding Gaussian counterparts based on 1000 Monte-Carlo replicates, respectively. Note that in practice, when a dataset is given, one only needs to calculate the test statistics once, and calculate the threshold value by generating Gaussian counterparts via 1000 Monte-Carlo replicates and computing the critical value. For each new data scenario, we need to simulate a new critical value as the detection threshold. Here, we generate the distributions of (i.e. ”Tn” in Figure 4) and Gaussian counterparts (i.e. ”GS” in Figure 4). We let the sample size , and window size . As shown in Figure 4, for all three different models and two different types of tails, the null distribution of the test statistic (purple) coincides with the one of its Gaussian counterparts (orange). The pink area is the overlapped part of two distributions. The histograms show that the two distributions are in general similar to the large overlapped areas, which supports the the Gaussian approximation theorem for our test statistics.

Further, we report the empirical sizes for the distributions of the test statistics based on quantiles of the Gaussian counterparts. We again consider the three different models and two different types of tails that we used for Figure 4. Let the sample size and the window size . We consider three different numbers of components, that is , 200 and 400. As shown in Table 1, the empirical sizes are close to 0.05 under different scenarios. These results, again, demonstrate the validity of our proposed Gaussian approximation theorem.

| i.i.d. | 0.0501 | 0.0503 | i.i.d. | 0.0498 | 0.0494 | i.i.d. | 0.0502 | 0.0507 |

| AR(1) | 0.0507 | 0.0495 | AR(1) | 0.0505 | 0.0506 | AR(1) | 0.0493 | 0.0510 |

| MA() | 0.0489 | 0.0483 | MA() | 0.0486 | 0.0477 | MA() | 0.0481 | 0.0471 |

A.3 Simulation with Change Points

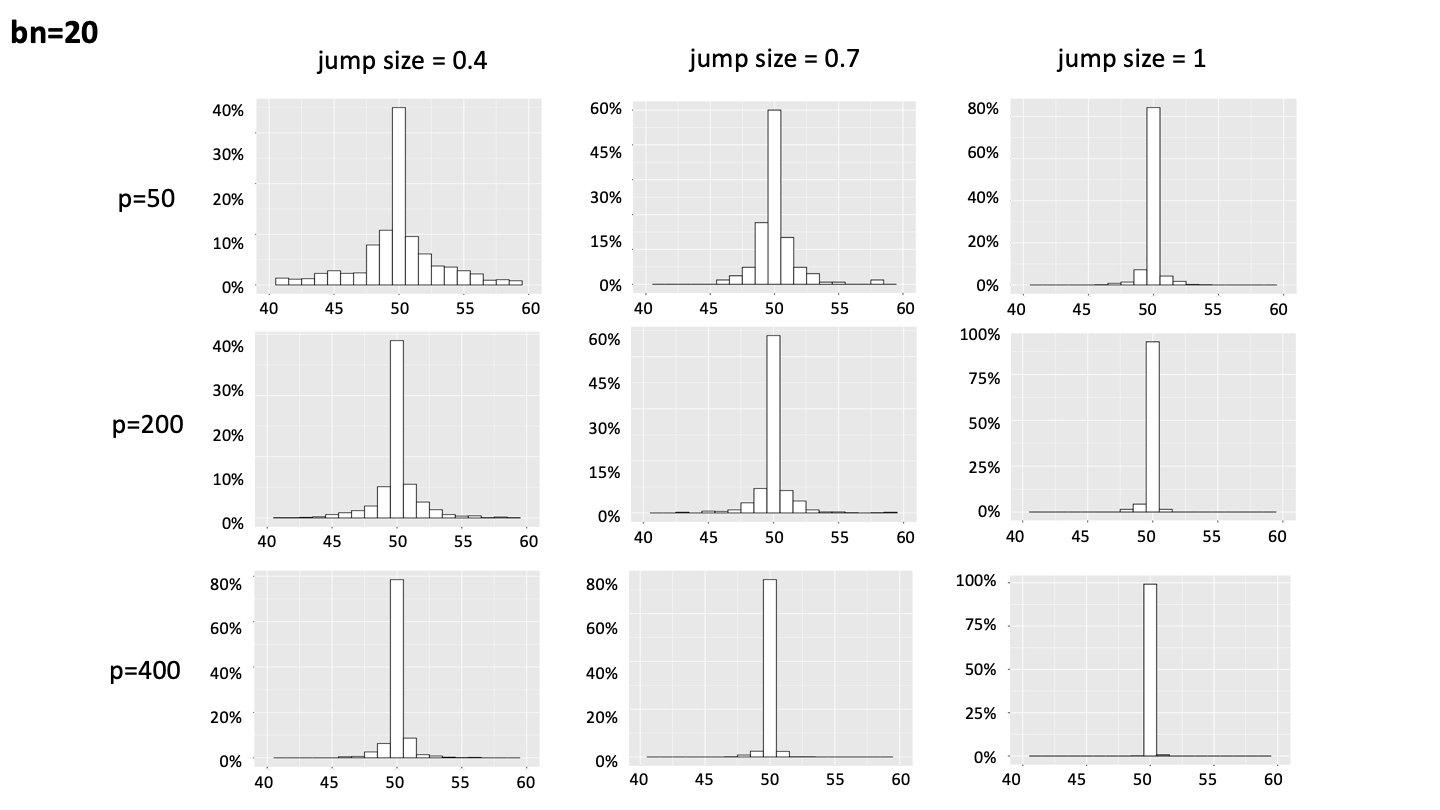

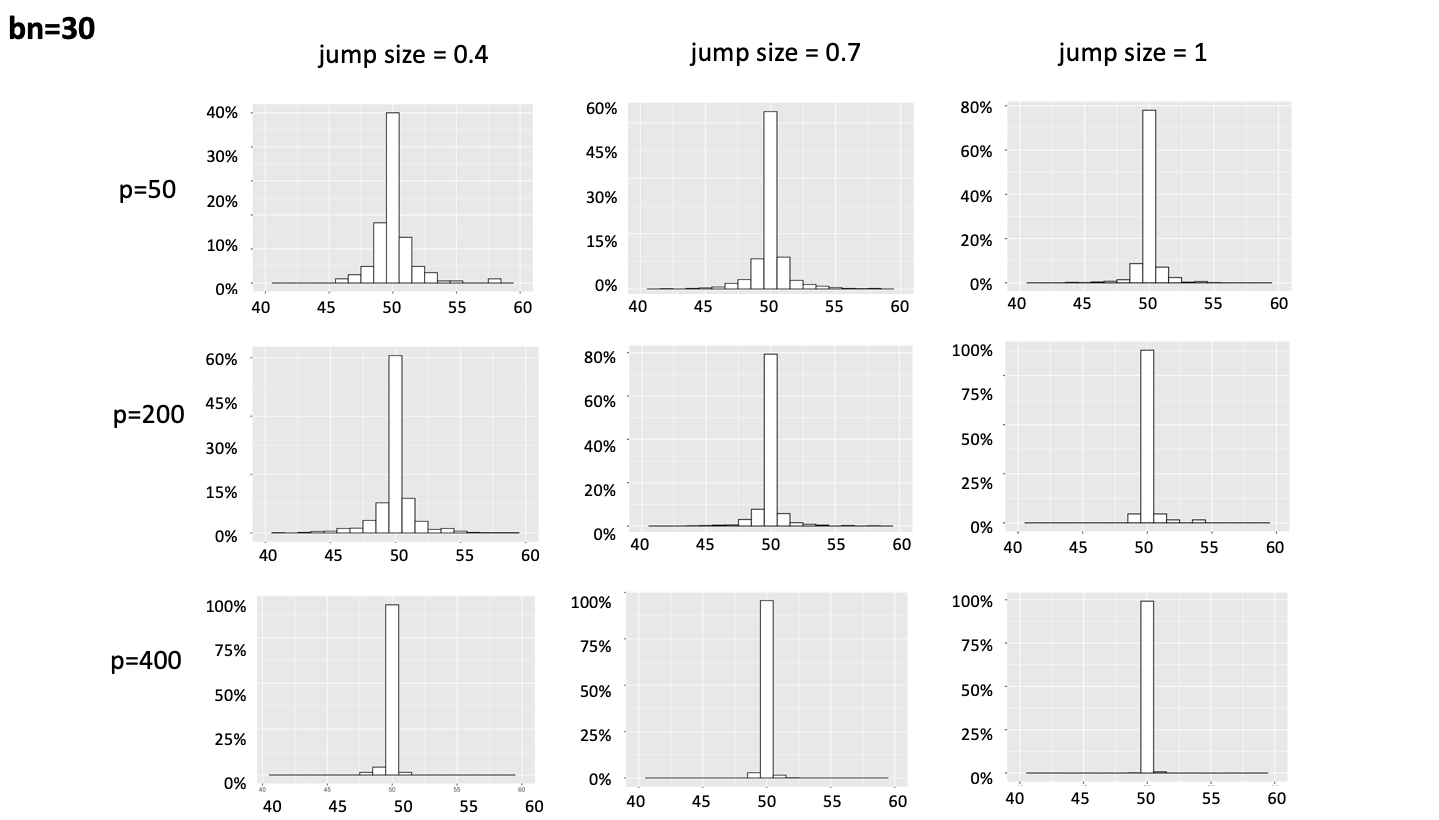

Now we present the simulation study of our proposed change-point detection method. We shall start with the single change-point case to show the precision of break-time estimation. Figure 5 illustrates the estimation of a single break located at the time point which is the center of the x-axis in each histogram. The number of observations is . We consider three different numbers of components , and (where is larger than the sample size , and this case can be considered as a high-dimensional setting), two different window sizes or , three jump sizes 1, 0.6 and 0.3, and the decay rate of the dependence of the time series is . All the errors are MA() with tails. Throughout this section we consider simulation samples.

To demonstrate the robustness of Algorithm 1, we set the number of breaks and break-time stamps , , for all cases, Moreover, we consider two window sizes and 30, and three two different jump sizes 1, 0.7 and 0.4. Note that for a simpler setting, in each sample, the jump sizes of all dimensions are set to be the same. Two different decay rates of the moving average model are shown, and 1.5. We report the averaged difference between the estimated number of change points and the true number of breaks (AN) in Table 2. The averaged distances between the estimated and true break temporal locations (AT) under different scenarios are shown in Table 3. The algorithm produces accurate break estimation in terms of all measures in different cases. For example, the estimation precision improves with increasing and jump sizes. It is worth noting that our proposed algorithm is computationally efficient as one only needs to estimate breaks once. Also, we do not need a second step aggregation after estimating the break statistics.

| jump size = 2, | jump size = 1, | ||||||

|---|---|---|---|---|---|---|---|

| 0.059 | 0.034 | 0.006 | 0.388 | 0.302 | 0.254 | ||

| 0.021 | 0.013 | 0 | 0.259 | 0.187 | 0.099 | ||

| jump size = 0.7, | jump size = 0.4, | ||||||

| 0.844 | 0.759 | 0.530 | 0.998 | 0.806 | 0.629 | ||

| 0.734 | 0.683 | 0.348 | 0.887 | 0.723 | 0.451 | ||

| jump size = 2, | jump size = 1, | ||||||

|---|---|---|---|---|---|---|---|