Vulnerability-CoVaR: Investigating the Crypto-market

Abstract

This paper proposes an important extension to Conditional Value-at-Risk (CoVaR), the popular systemic risk measure, and investigates its properties on the cryptocurrency market. The proposed Vulnerability-CoVaR (VCoVaR) is defined as the Value-at-Risk (VaR) of a financial system or institution, given that at least one other institution is equal or below its VaR. The VCoVaR relaxes normality assumptions and is estimated via copula. While important theoretical findings of the measure are detailed, the empirical study analyzes how different distressing events of the cryptocurrencies impact the risk level of each other. The results show that Litecoin displays the largest impact on Bitcoin and that each cryptocurrency is significantly affected if an event of joint distress among the remaining market participants occurs. The VCoVaR is shown to capture domino effects better than other CoVaR extensions.

Keywords: copula, Conditional Value-at-Risk, cryptocurrency, systemic risk

1 Introduction

Various developments and crises over the last two decades, such as the financial crisis of 2009, have demonstrated how volatile, fragile, and interconnected the financial system and its institutions can be. This gives rise to systemic risk, which can be described as ‘the risk of the financial system as a whole’ (Cao 2014, p. 2). The regulatory methodology focuses highly on protecting the financial system against systemic risk events by identifying globally systemically important financial institutions based on cross-jurisdictional activities, size, interconnectedness, substitutability, and complexity. These higher risk institutions are subject to higher loss absorbency requirements, which are imposed next to general liquidity and risk-based capital requirements (Basel Committee on Banking Supervision 2013). However, the question of correctly quantifying systemic risk via appropriate measures remains a crucial task and has developed into a highly researched area. Classical univariate risk measures such as the VaR or the Expected Shortfall are constructed to quantify the risk of an isolated institution or asset class. Consequently, these univariate measures are unable to quantify the impact of an institution’s distress on another institution or the whole financial system. As a result, alternative multivariate measures which overcome these limitations and are able to quantify the impact of the risk of a financial institution on other institutions in a system need to be defined.

The last decade has seen a rise of a completely new, highly volatile, and risky financial product known as Cryptocurrency (CC). The CC has recently received increased attention in academia (Vidal-Tomás 2021; Petukhina et al. 2021). However, the economics of those financial assets are yet not well understood, and the risks hidden in this system require thorough investigation. The potential threats from CC have recently also been recognized by regulating authorities, see Basel Committee on Banking Supervision (2019). The following systemic risk discussion focuses solely on CC as financial assets, but the methods are general and are applicable to other inter-connected financial asset classes.

Bisias et al. (2012) and Benoit et al. (2017) provide extensive surveys of current methodologies to quantify systemic risk. Among these several methods, the most widely-applied market-based measure is the Conditional Value-at-Risk (CoVaR) by Adrian and Brunnermeier (2016), which expands the approach of the VaR to a conditional setting. The can be defined as a quantile of the conditional return distribution of CC (or a system) given that the CC is under distress, which means that if the usually stable Litecoin (LTC) becomes risky, will this risk be transferred to Bitcoin (BTC)? Based on that concept, Adrian and Brunnermeier (2016) define a measure called Delta-CoVaR by taking the difference between with being exactly at its VaR and with being in its median state, therefore highlighting the strength of the effect. A list of further systemic risk measures has been developed and analyzed by Girardi and Ergün (2013), Mainik and Schaanning (2014), Acharya et al. (2017), and Brownlees and Engle (2017). Zhou (2010) considers, among other measures, the Vulnerability Index (VI) that represents the probability that the CC of interest violates its VaR under the condition of at least one other CC violating its VaR. Several studies have expanded the CoVaR measure to a multiple case by incorporating more than one variable in the conditional event. Cao (2014) introduces the Multi-CoVaR (MCoVaR) with the condition of several CCs being simultaneously in distress. Bernardi et al. (2019) propose the System-CoVaR (SCoVaR), in which the conditional variables are aggregated via their sum. Further extensions are detailed in Bernardi et al. (2018), Di Bernardino et al. (2015), Bernardi et al. (2017), and Bonaccolto et al. (2021).

The main goal of this paper is to formalise a flexible approach that allows to capture a variety of distress events without having to specify a pre-specified distressing situation of the given system, e.g., distress of a specific element or group of elements. Therefore, complementary to SCoVaR and MCoVaR, this empirical study proposes the Vulnerability-CoVaR (VCoVaR), which translates the idea of the VI to the conditional quantile setting. The VCoVaR is defined as the VaR of a CC (or the CC system) given there exists at least one other CC being below or equal to its VaR. Copula-based estimation strategies and characteristics for CoVaR and all investigated CoVaR extensions (SCoVaR, MCoVaR, VCoVaR) are detailed and validated in a thorough simulation study. CoVaR, MCoVaR, and VCoVaR are found to be equal in certain dependence scenarios. Simulation-based analysis of the measures depending on the dependence structure and intensity reveal the desirable property of the VCoVaR of being a monotonically decreasing function of the dependence parameter for a selected list of Archimedean copulae (AC). As an important by-product of this research, a semi-automated univariate model selection procedure based on the minimization of an information criterion while fulfilling the requirements on the respective time series residuals is proposed, see Appendix B.

The paper is structured as follows: Section 2 illustrates why the VCoVaR is particularly appropriate for the CC market and further motivates the use of copula for estimation. Section 3 formally defines the measures and derives the copula-based estimation. Section 4 investigates the properties of the risk measures. Section 5 includes the simulation study, while Section 6 contains the application study of CCs. Section 7 concludes. The R code to reproduce the results from this paper will be published in a GitHub repository as soon as the paper is accepted.

2 Systemic Risk in the Cryptocurrency Market

The literature identifies two highly relevant characteristic properties of the CC market: the existence of significant spillover effects and the occurrence of herding behaviour among CC market participants. The latter relates to the phenomenon that investors tend to imitate each others transaction behaviour instead of following their own information and belief basis (Hwang and Salmon 2004). The existence of spillover effects is displayed in Borri (2019), who applies the CoVaR of Adrian and Brunnermeier (2016) based on quantile regression to discover that CCs are highly exposed to tail-risk from other CCs. Ji et al. (2019) use the methodology of Diebold and Yilmaz (2015) to quantify return and volatility spillovers in the CC market. Pursuing a similar methodological approach, Li et al. (2020) find that risk spillovers are stronger in the direction from CCs with small market capitalization to those with larger capitalization. Xu et al. (2021) run the TENET approach originally developed in Härdle et al. (2016) to conclude that the market of CCs is coined by significant effects of spillover risk and that the connectedness in the market increased steadily over the course of time. Further spillover analysis of the crypto-market can be found in Koutmos (2018), Luu Duc Huynh (2019), and Katsiampa et al. (2019), while the empirical findings are greatly summarized in the survey of Kyriazis (2019). Along with spillover effects, CCs also show a strong behaviour of tail dependence, see Tiwari et al. (2020) and Xu et al. (2021), which can be modelled using the copula method.

Regarding the existence of herding behaviour, a relevant contribution is Bouri et al. (2019), who identify using the approach of Stavroyiannis and Babalos (2017) significant herding effects whose intensity varies over time. Vidal-Tomás et al. (2019) give evidence for herding effects during downward market situations, based on the methodology of Chang et al. (2000) and Chiang and Zheng (2010). They notice that the behaviour of the main CCs is crucial for the investment decisions of traders. Ballis and Drakos (2020) and Kallinterakis and Wang (2019) also follow the method of Chang et al. (2000) and confirm the presence of herding effects, although detecting stronger effects during upward market situations. Finally, Kyriazis (2020) contains a survey about the empirical findings.

These two properties - spillover effects and herding behaviour - of the CC market suggest that distress of a CC leads to subsequent distresses of other CCs, and consequently, a domino effect might take place, increasing the likelihood of a systemic risk event. Additionally, there is evidence that the CC market can be primarily influenced by one dominant CC, for example BTC, as stated in Smales (2020).

The VCoVaR is especially appropriate for the CC market because the measure is tailored for quantifying tail-dependence and domino effects. For example, in the case of extreme losses of Bitcoin (BTC) under the condition that at least one of Ethereum (ETH), Litecoin (LTC), Monero (XMR), and Ripple (XRP) is under distress, with the VCoVaR we capture all situations of such distress spreading processes in the system. It is not necessary to define which CC initially was under distress or how far the domino effect is already developed. The notion of at least one includes all possible scenarios and is hence more appropriate in capturing domino effects than the existing alternatives CoVaR, MCoVaR, and SCoVaR, which focus only on one pre-specified distress situation. The use of copulae allows to model both tail dependencies and contagion risk, with the latter being especially pronounced in this market with one dominant CC. Consequently, the VCoVaR provides a flexible tool to depict the impact of such systemic risk scenarios due to its natural consideration of the special characteristics of the CC market.

3 Conditional Multivariate Risk Measures

3.1 Definitions

Before formally introducing the conditional measures, the univariate VaR measure is reviewed. Let be the return of CC at time . The at probability level is implicitly defined as:

| (1) |

If , one can alternatively write , with being the generalized inverse of , defined as .

Let be the return of CC (or the CC system) at time . The original Adrian and Brunnermeier (2016) with probability level for given equals its is defined as:

| (2) |

The is the quantile of the conditional return distribution. Frequently applied probability levels in practice are or . We consider general cases with for all measures. Girardi and Ergün (2013) modify (2) by adding inequality to the condition:

| (3) |

It is argued that this definition is reasonable as it considers more extreme distressing events of CC and gives the opportunity to apply standard backtesting procedures, e.g., Kupiec (1995). Mainik and Schaanning (2014) showed for selected bivariate distributions that the CoVaR in (2) is not a monotonically increasing function of the dependence coefficient between , while the one in (3) is monotonically increasing. Note that this translates into monotonically decreasing functions in our case, as Mainik and Schaanning (2014) considered loss variables. This characteristic is referred to as dependence consistency. More precisely, Theorem 3.6 in Mainik and Schaanning (2014) guarantees the measure in (3) is dependence consistent if follows a bivariate elliptical distribution or an elliptical copula. Similar properties have been found for the Gumbel copula.

However, the relationships in the CC world are unlikely to be fully captured with a bivariate distribution. It is necessary to find alternatives, including several variables for the conditional event, to capture more complex scenarios in which CCs are in distress. In the following, let be the vector of returns of CCs, with indices collected in the vector at time where is not part of these CCs. The first considered extension, the SCoVaR, aggregates the variables in the conditional event by taking their sum and was introduced in Bernardi et al. (2019). Building on this idea, the SCoVaR in this paper is implicitly defined as follows:

Definition 3.1 (System-CoVaR).

Given the return of cryptocurrency/system and the returns of cryptocurrencies , the SCoVaR is defined as:

| (4) |

Bernardi et al. (2019) impose the additional restriction that every variable in the conditional event is below or equal its individual VaR, what leads to a different form of (4), namely:

Building on their formulation, the authors find a generalization of the Expected Shortfall measure, which is used to pursue a game theoretic approach of risk allocation. However, this paper separates these naturally different restrictions into the SCoVaR as in Definition 3.1 and the MCoVaR, which is introduced in the following.

The MCoVaR is the second extension and was introduced in Cao (2014). This measure covers cases when all are simultaneously equal or below their level. Thus, using probability levels and , it is defined as:

Definition 3.2 (Multi-CoVaR).

Given the return of cryptocurrency/system and the returns of cryptocurrencies , the MCoVaR is defined as:

| (5) |

Although it is possible to consider different -levels for each to balance individual effects, for simplicity, it is assumed that all measures impose a common -level for the conditional variables. Cao (2014) defines a measure of systemic risk contribution by taking the difference of the MCoVaR as in (5) and the MCoVaR when the are at a normal state. As for the SCoVaR, the aim of this paper is also to study the properties and estimation of the MCoVaR given in (5).

Along these lines, we propose the VCoVaR, which is to the best of our knowledge not existent in the current literature, although allowing for a new perspective on systemic risk. It translates the idea of the VI of Zhou (2010) into a conditional quantile setting. The VI was originally defined on loss distributions and measures the probability of violating its VaR given there exists at least one other CC violating its VaR. Transferring this approach, the VCoVaR is implicitly defined as follows:

Definition 3.3 (Vulnerability-CoVaR).

Given the return of cryptocurrency/system and the returns of cryptocurrencies , the VCoVaR is defined as:

| (6) |

This approach allows to cover a variety of distress events and naturally generalizes the CoVaR of (3) and the MCoVaR of (5). It is straightforward to see that the conditional event of the MCoVaR is a subset of the conditional events of the VCoVaR. In a setting of positive dependencies, the distressing event of the MCoVaR relates to the worst case covered in the VCoVaR, namely all are below or equal to their VaR. On the other side, the VCoVaR is able to cover situations that are less negative than the bivariate CoVaR. Having, e.g., the return of three CCs LTC, XMR, and XRP as conditional variables, the VCoVaR captures situations in which XMR violates its VaR while LTC and XRP do not. This crypto market situation can be assessed more positive than the one of the bivariate CoVaR with XMR in the conditional event as additional positive information about LTC and XRP exist.

3.2 Estimation of Systemic Risk Measures

3.2.1 CoVaR Estimation

The original CoVaR of Adrian and Brunnermeier (2016) given in (2) was estimated using a quantile regression approach (Koenker and Bassett Jr 1978). Girardi and Ergün (2013) point out that - although the resulting estimate is time-variant - the impact of on is constant, which is unlikely to be the case in practice. In contrast, they propose to estimate their CoVaR modification based on the bivariate distribution of , thus rewrite (3) as:

which reduces to:

| (7) |

as per definition , see (1). On this basis, the following three-step procedure was proposed for the estimation:

-

Step 1:

Fit a suitable univariate time-series process (selected, e.g., through our newly proposed procedure, see Section 6.1.2) to and estimate .

-

Step 2:

Estimate the bivariate conditional heteroscedasticity model (e.g. the DCC-GARCH model of Engle 2002) to obtain an estimate of the time dependent bivariate density with observations , of , with .

-

Step 3:

Solve for the equation:

(8)

This procedure might be computationally demanding as it involves numerical evaluation of a double integral. Overcoming this issue, we base our estimation on copulae. Copulae are multivariate distribution functions with margins being , see Joe (2014). Copulae give the opportunity to specify the dependence structure of random variables in a flexible way, allowing to go beyond the commonly applied multivariate Gaussian and -distribution. This is also handy because CC returns are even less normal than fiat stocks, see, e.g. Szczygielski et al. (2020) for an extensive investigation of proper CC return distributions.

To estimate the CoVaR as given in (7), Reboredo and Ugolini (2015) express the bivariate distribution function of as:

using the Sklar (1959) theorem. and denote the marginal distributions of and , respectively. refers to the copula function with parameter . The is estimated by solving:

| (9) |

which uses . Note that in the case of AC (9) can be solved analytically for , see Karimalis and Nomikos (2018). Another crucial advantage is that it is not necessary to estimate the VaR of the conditional variable beforehand (Reboredo and Ugolini 2015). To compute (9), it is sufficient to estimate the copula and the marginal distribution of . This estimation strategy is transferred to the SCoVaR of (4). Although it involves information of conditional variables, it can be estimated using (9) while replacing with for estimating the copula between and .

3.2.2 MCoVaR Estimation

Set , where holds componentwise. Furthermore, set and . To estimate the MCoVaR, (5) can be rewritten as:

| (10) |

Similar to the procedure of Girardi and Ergün (2013), Cao (2014) computes the individual VaR for each CC and assumes a parametric form of the -dimensional distribution for all involved variables. On this basis, the denominator of (10) can be computed, leading to an expression with a multiple integral with variables and the MCoVaR as the only unknown. This is solved numerically, and Cao (2014) assumes a multivariate -distribution driving the overall dependency in the application.

Furthermore, (10) is given in terms of copulae by:

leading to:

| (11) |

where . denotes the -dimensional copula of with the parameter . refers to the -dimensional copula of with parameter . This expression can be solved, as the MCoVaR is the only unknown term. Consequently, it is sufficient to have an appropriate estimate of the copulae and the marginal distribution . One can assume different structures for the copulae enabling different interpretations of the gained MCoVaR, which will be detailed in Section 4.2. In practice, is estimated from the data, and the copula is gained through marginalization, setting , from the grounding property (Nelsen 2006). Notice that (11) yields an analytic solution for specific copula families. Let be a generator function for an AC with parameter and the corresponding inverse. Let be some copula under the assumption, that with is the proper copula function. Simplification of (11) yields:

| (12) |

Special cases are where is an AC or a Hierarchical Archimedean copula (HAC), see Okhrin et al. (2013). In the former case, (12) transforms to:

where the dependence intensity is expressed via the AC parameter . Furthermore, from (11) follows that for , as (11) reduces to (9).

3.2.3 VCoVaR Estimation

In the following, the copula-based representation of the VCoVaR of (6) is derived. Set of length .

Lemma 3.1.

The VCoVaR defined in (6) is equivalent to:

| (13) |

where denotes the -dimensional survival copula associated with and parameter and denotes the -dimensional survival copula of , characterized by a parameter .

Proofs of all lemmata are provided in Appendix A. The VCoVaR is estimated by solving (13). The estimation approach includes survival functions, which can - analogously to the case of distribution functions - be decomposed using survival copulae, see Georges et al. (2001). A crucial characteristic is that the survival copula of a pair of random variables is the 180 degrees rotated version of its copula, similar holds for any dimension. In consequence, there exists a direct relationship between and . This allows estimation of the involved survival copulae in practice as follows: first, estimate the copula from the data and rotate it to find . Second, extract through marginalization, setting . The essential point is again the sufficiency of having an estimate of the (survival) copulae and the marginal distribution . Additionally, the considered risk measures in (9), (11), and (13) are continuous transformations of these estimators. Therefore all asymptotic distributional properties of the risk measures are directly determined by application of the delta method, see Oehlert (1992).

The following Lemma shows the equivalence between the copula-based representations of CoVaR and VCoVaR if only one conditional variable is considered.

4 Properties of Systemic Risk Measures

4.1 Independence and Perfect Dependence

Let us establish a connection between the CoVaR measures introduced previously if all variables are independent or perfectly positive dependent. The case of perfect negative dependence is not considered, as countermonotonicity in higher dimensions is problematic.

This observation is reasonable, as in the case of independence, the conditional probabilities of (3), (5) and (6) equal the respective unconditional probability, which results in the VaR at level . Transferred to the market of CCs, in the case of independence, an extreme event for a crypto return under condition is completely irrelevant for the crypto return .

Lemma 4.2.

All conditional measures equal the VaR at level in the given scenario, being directly influenced by the VaR level of the conditional variables, which means that in the case of perfect positive dependence, it is sufficient to consider one conditional crypto return, as additional CCs would not generate any additional information.

4.2 General Positive Dependencies

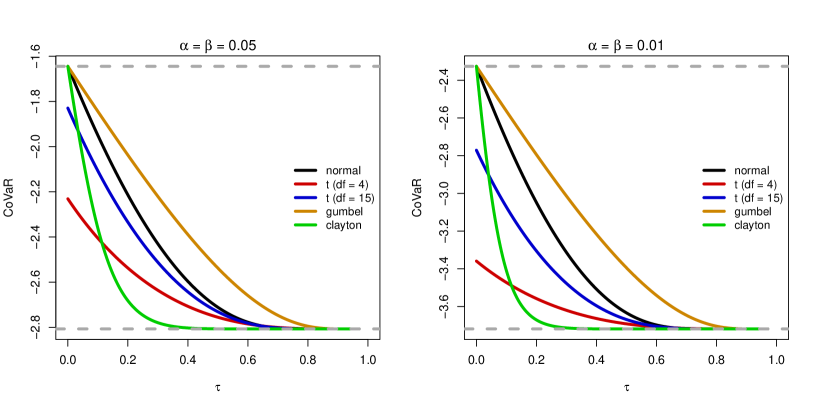

We want to gain further understanding of the measures based on (9), (11), and (13). Two major objectives are pursued. First, to detect the general behaviour of the measures as the function of the dependence parameter for a given copula. Second, to investigate differences between different copula families. This is realized by solving (9), (11), and (13) for a range of copula parameters. The marginal distribution is set to be standard normal.

For the bivariate CoVaR of (9), the Gaussian, , Clayton, and Gumbel copulae are chosen, while we consider two approaches to analyze the MCoVaR of (11) and the VCoVaR of (13). Generally, we set . First, the copula is assumed to be Clayton or Gumbel, thus belonging to the AC family. We excluded the Gaussian and -copula as they require more correlation parameters in higher dimensions, and we want to start the analysis by varying one dependence parameter at a time. The copula of is attained by marginalization: . As a consequence, the measure depends only on one parameter for the Clayton and Gumbel copula and can be visualized comparable to the bivariate CoVaR case. This allows interpreting how the measure changes if the dependence of as a whole changes. Second, the copula of is assumed to be a HAC. The idea of a HAC is to nest AC in a hierarchical structure to allow for a more flexible specification of the dependence structure, as the property of AC of having one parameter materializes in practice often as a limitation. The following structure is imposed: The bivariate copula describes the dependency inside the conditional variables, while describes the dependency between the target variable and the conditional variables. Notice that for the VCoVaR each copula is rotated, as the measure is based on survival copulae.

For comparability, each copula parameter is converted into Kendall’s (Joe 2014). As in Section 4.1, only positive dependencies with Kendall’s are considered, although does not range over the whole domain in some cases as numerical issues at the limits appeared. Note that results in negative pair-dependencies, which is controversial in dimensions . The computations in the following are realized using the R-packages copula (Kojadinovic and Yan 2010) and HAC (Okhrin and Ristig 2014).

4.2.1 CoVaR Properties

Starting with the bivariate CoVaR, Figure 1 shows the measure depending on the selected copula and Kendall’s . The probability levels and are considered. In general, the CoVaR decreases monotonically for all copulae if Kendall’s increases. This is consistent with the findings of Mainik and Schaanning (2014). For example, this implies the stronger LTC depends on XRP, the stronger a distressing event of XRP will impact LTC. Furthermore, the results of Section 4.1 are special cases for those copulae where independence () and perfect positive dependence () are attained. Given the standard normal distribution for the margins, these are and , respectively, for . The CoVaR converges for all copulae towards these theoretical limits, except for the -copula if . This is reasonable as restricts the correlation of the -copula to be 0, but does not affect the degrees of freedom . However, the -copula converges towards the Gaussian one if (Eling and Toplek 2009). This is reflected in Figure 1, as with increasing the curve of the -copula comes closer to the one of the Gaussian copula. The curve of the Clayton copula decreases very fast, while the curves of the Gumbel and Gaussian copulae decrease slowly. Thus, the Clayton copula leads to more conservative estimates of the CoVaR and should produce in an application fewer exceedances than the other copulae.

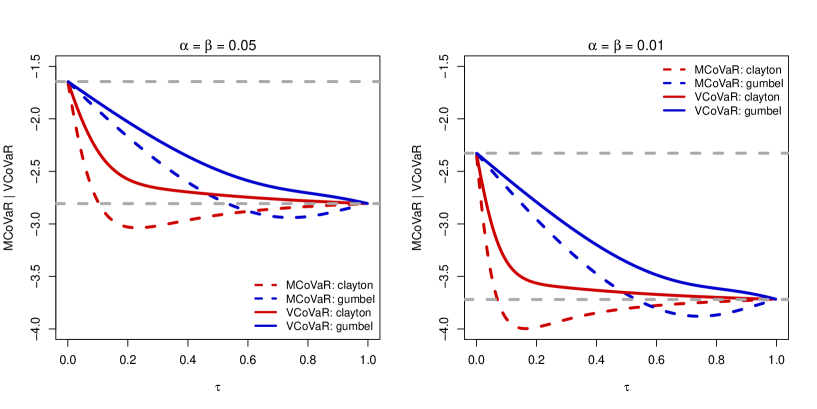

4.2.2 MCoVaR and VCoVaR Properties

Figure 2 shows the results of the first approach with three-dimensional AC. The figure also contains the theoretical limits of Section 4.1, and both the MCoVaR and the VCoVaR converge towards them if or . This is the case for both considered probability levels. However, the MCoVaR is not a monotonically decreasing function of Kendall’s . For the Clayton copula, the MCoVaR achieves its minimum for , while for the Gumbel copula it is around . Thus, the MCoVaR measure of (11) does not reflect the behaviour of the bivariate CoVaR for the given copula specification. Nevertheless, it is reasonable to detect lower values of the MCoVaR in comparison to the CoVaR, as the conditioning event describes a worse market situation. In contrast to the MCoVaR, the VCoVaR is a monotonically decreasing function of Kendall’s . Thus the measure decreases if the dependency of as a whole intensifies. Furthermore, the curve of the Clayton copula again decreases faster than the one of the Gumbel copula. Transferring this to practice, we can expect the Clayton copula to lead to more conservative estimates for the VCoVaR in the empirical part.

|

|

| (a) Multi-CoVaR | (b) Vulnerability-CoVaR |

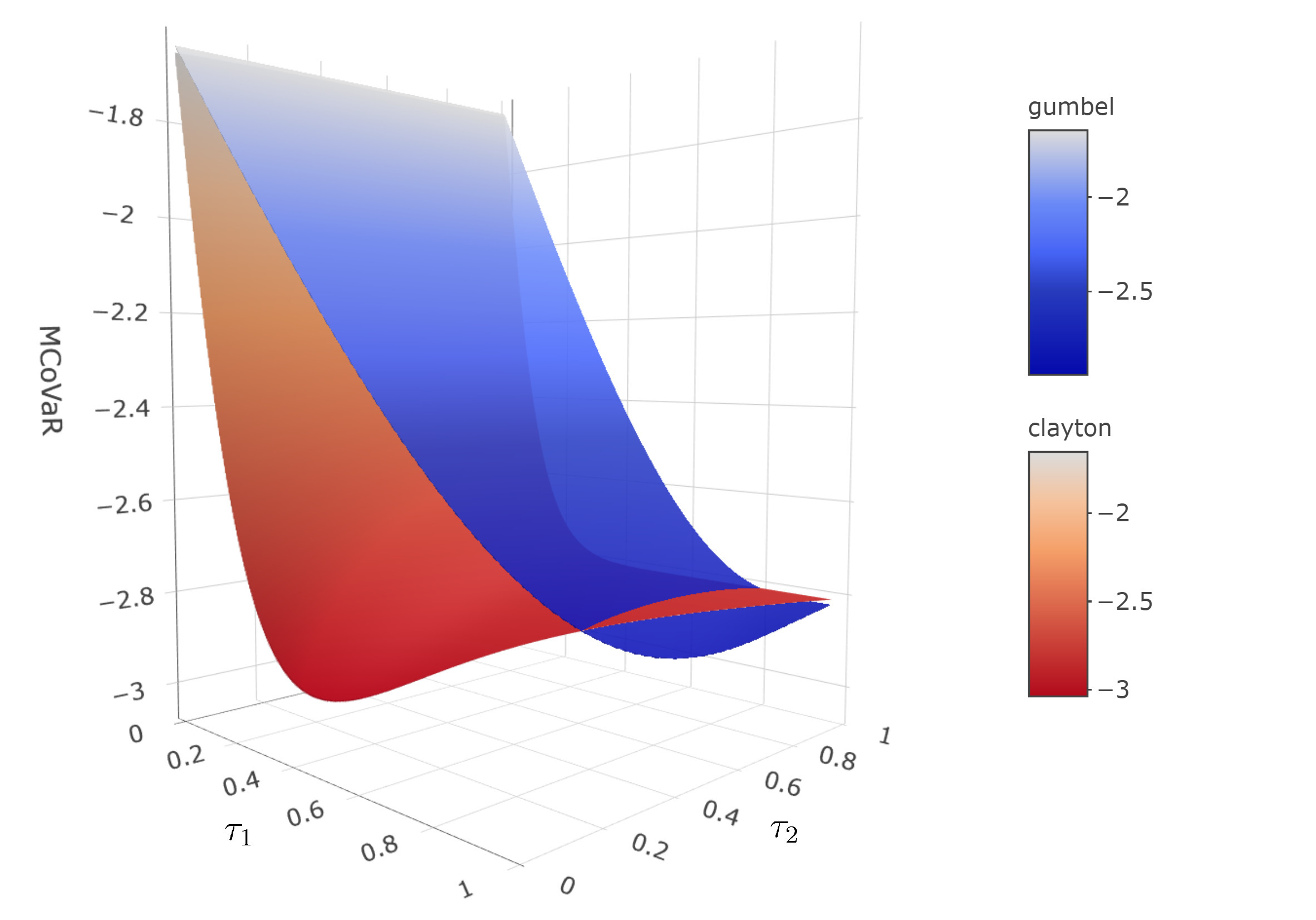

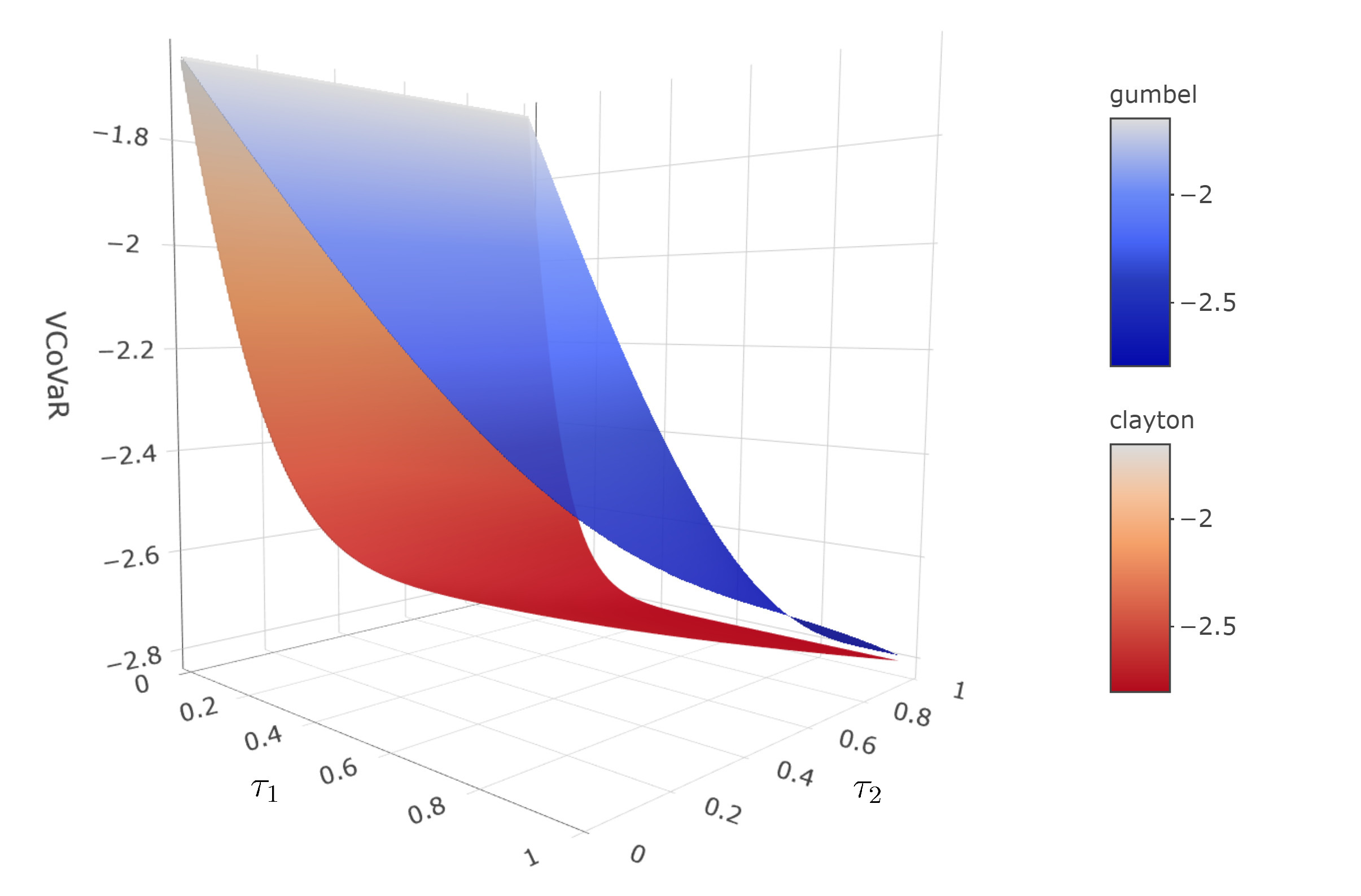

The second approach using the HAC allows decomposing these characteristics even further. Figure 3 shows the surfaces for Clayton and Gumbel generators if a HAC is assumed. Regarding notation, the figure contains and , referring to and , respectively. Note that a HAC is required to fulfil the sufficient nesting condition in order to be a proper copula (Okhrin et al. 2013). This condition corresponds to for considered copulae, the area in the surface plots violating this condition remains empty. The edges of the surfaces at in Figure 3 equal the corresponding curves in Figure 2, as the HAC is the equivalent with the AC of the first approach.

The MCoVaR decreases for both copulae if the dependency between the target variable and the conditional variables, represented through , intensifies. For example, if BTC is the variable of interest and XRP and XMR are under condition, the impact of joint distresses of XRP and XMR on BTC increases if BTC has a larger dependency with XRP and XMR. This observation is reasonable and justifies the application of the MCoVaR. However, this mainly reflects the dependence consistency of the bivariate CoVaR. Given a fixed , the value can be calculated with set to , as seen from (11). In consequence, the analysis with varying becomes analogous to a bivariate CoVaR analysis with an -level adjusted by the dependency between and . If on the other side is fixed and increases, the MCoVaR is much less affected and tends to increase. Regarding our example with BTC, XMR, and XRP, this could potentially be interpreted as follows: if the conditional CCs XMR and XRP only have a weak dependence, the conditional event in (5) will be unlikely. If such a joint event still happens, the market situation will be devastating and the MCoVaR needs to be very small. If in the other case, XRP and XMR depend highly on each other, distress of XRP suggests distress of XMR and vice versa. The fulfilment of the condition is a consequence of the dependency between XRP and XMR and not of the situation of the overall market. Thus, the values of the MCoVaR are slightly higher. However, the overall impact of on the MCoVaR is of primary importance and determines the general behaviour of the measure. Differentiating between the two considered copulae shows the Clayton copula decreases faster in , although there is an overlapping of the two surfaces in Figure 3(a) for high .

The VCoVaR using the HAC structure in Figure 3(b) decreases if increases. This observation confirms that the VCoVaR as calculated in (13), is a reasonable extension of the bivariate CoVaR measure. In contrast to the MCoVaR, the VCoVaR decreases if the dependency between the conditional variables, expressed through , increases. This could be explained via different conditional events. Consider the example of BTC with XRP and XMR under condition again. If the dependency between XRP and XMR increases, the probability that the conditional event of the VCoVaR in (6) yields a bad scenario, namely both CCs are in distress, increases. Consequently, the VCoVaR needs to decrease to capture these potentially worse situations. However, the impact of on the VCoVaR is less pronounced than the one of . Finally, the Clayton copula produces again smaller VCoVaR values than the Gumbel copula.

5 Simulation Study

A simulation study is performed to test whether (9), (11), and (13) can reliably calculate the respective measure if the true copula is known, and no temporal dependency is present. The study is performed as follows: Step 1: Assume for the CoVaR or for the M- and VCoVaR follow a certain copula with dependence parameter . Step 2: Sample iid observations from the copula with margins being and estimate the assumed copula via maximum likelihood (ML). Step 3: Compute the respective conditional measure through (9), (11), and (13), and the VaR of the conditional variables as the empirical -quantile. Step 4: Compute the violation rate of the respective measure using the sample equivalents of from the definitions in (3), (5), and (6), respectively. Step 5: Repeat Steps 2 to 4 for times and calculate the average violation rate.

| Measure | ||||||

| Clayton | Gumbel | Clayton | Gumbel | Clayton | Gumbel | |

| CoVaR | 0.0489 | 0.0493 | 0.0499 | 0.0507 | 0.0506 | 0.0506 |

| MCoVaR | 0.0491 | 0.0516 | 0.0501 | 0.0501 | 0.0490 | 0.0480 |

| VCoVaR | 0.0503 | 0.0505 | 0.0507 | 0.0495 | 0.0496 | 0.0502 |

| CoVaR | 0.0102 | 0.0082 | 0.0102 | 0.0089 | 0.0093 | 0.0085 |

| MCoVaR | 0.0080 | 0.0062 | 0.0082 | 0.0112 | 0.0101 | 0.0117 |

| VCoVaR | 0.0110 | 0.0099 | 0.0115 | 0.0113 | 0.0091 | 0.0089 |

The Gumbel and Clayton copulae are analyzed with Kendall’s . The sample equivalents of in Step 4 are calculated by considering only the simulated observations which fulfill the conditional event. Of those observations, the number of violations of the respective CoVaR measure is computed. The equivalent of is then the ratio between the latter and the number of observations fulfilling the conditional event, which were considered in the first stage. This is equivalent to the procedure of Mainik and Schaanning (2014), in which the bivariate CoVaR was analyzed. Table 1 shows that for both selected probability levels, both copulae, and all values of Kendall’s , the violation rates are close to nominal level . Concluding this simulation study, the copula-based (9), (11), and (13) are able to reliably compute the respective measure if the correct copula is assumed for the data-generating process.

6 Empirical Study

6.1 In-sample Estimation

6.1.1 Proceeding and Data Investigation

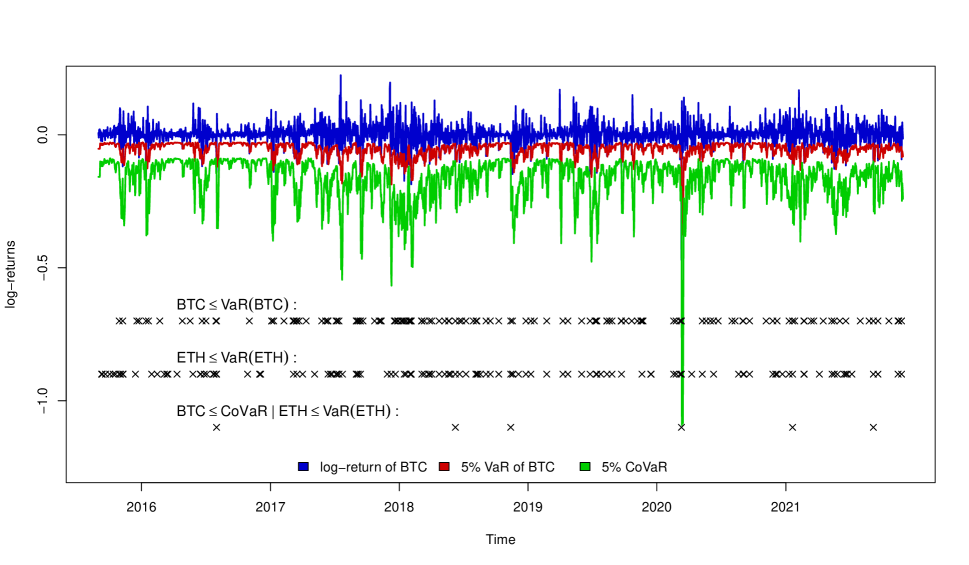

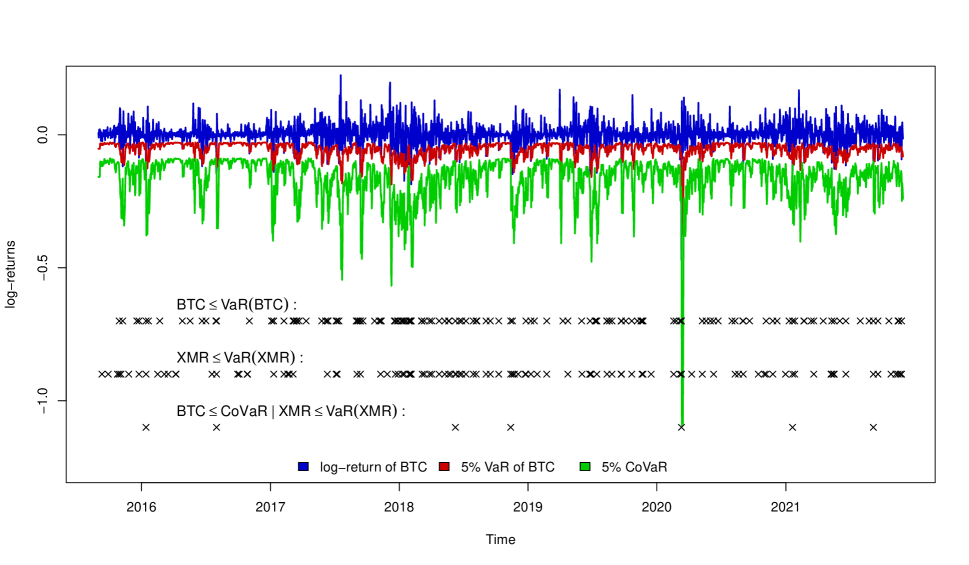

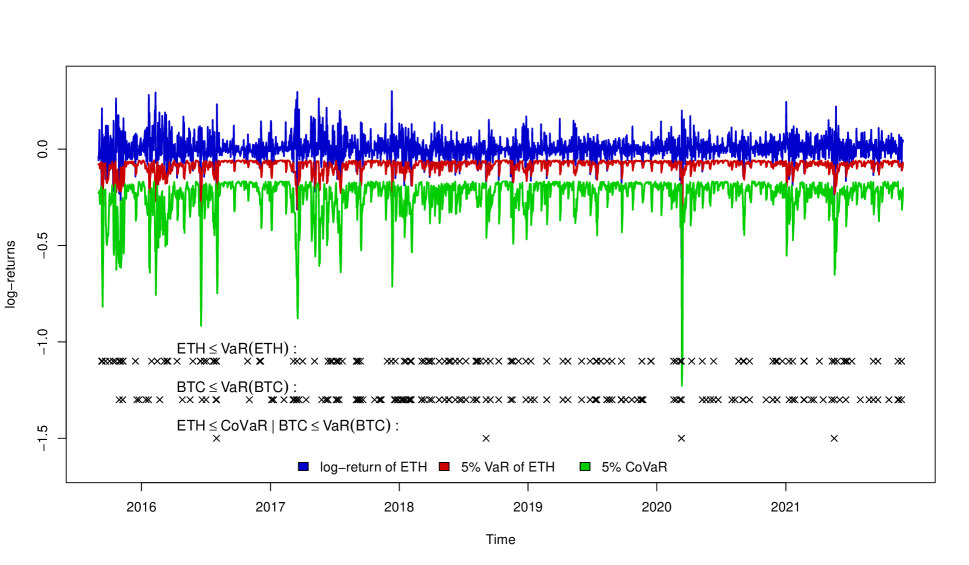

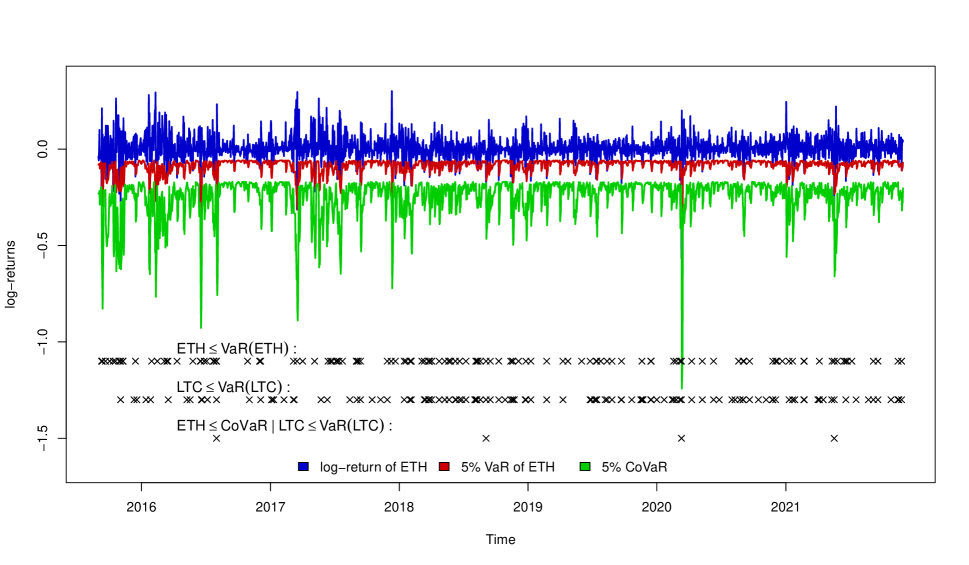

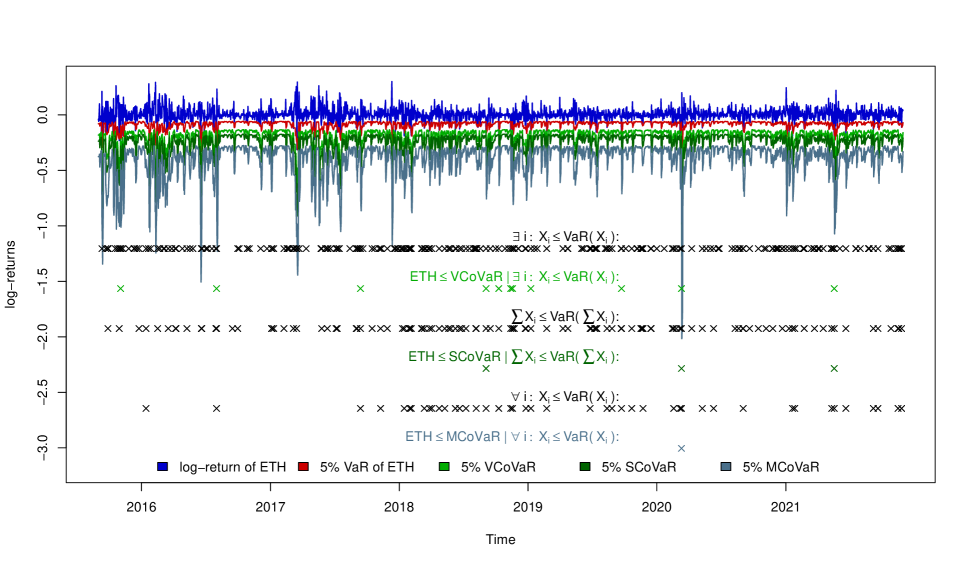

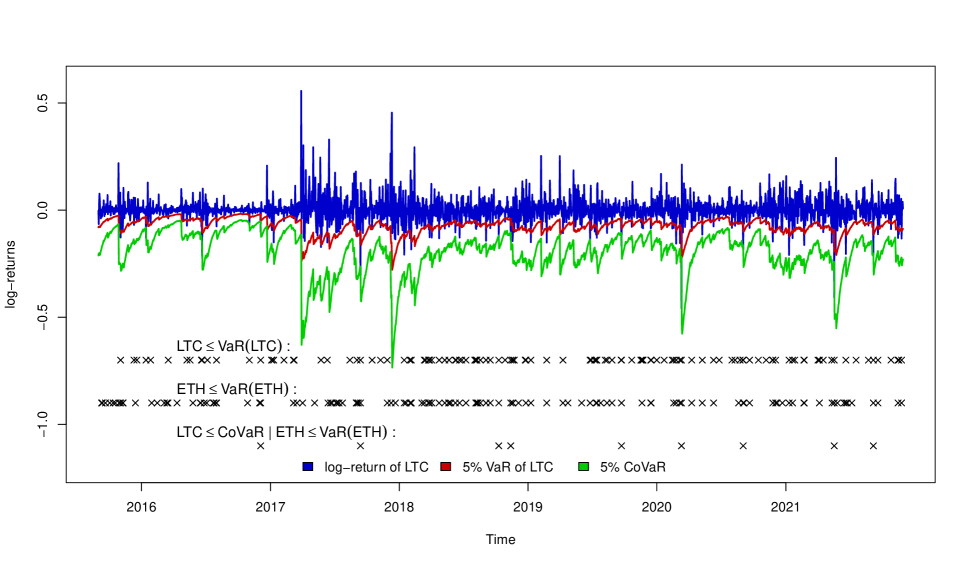

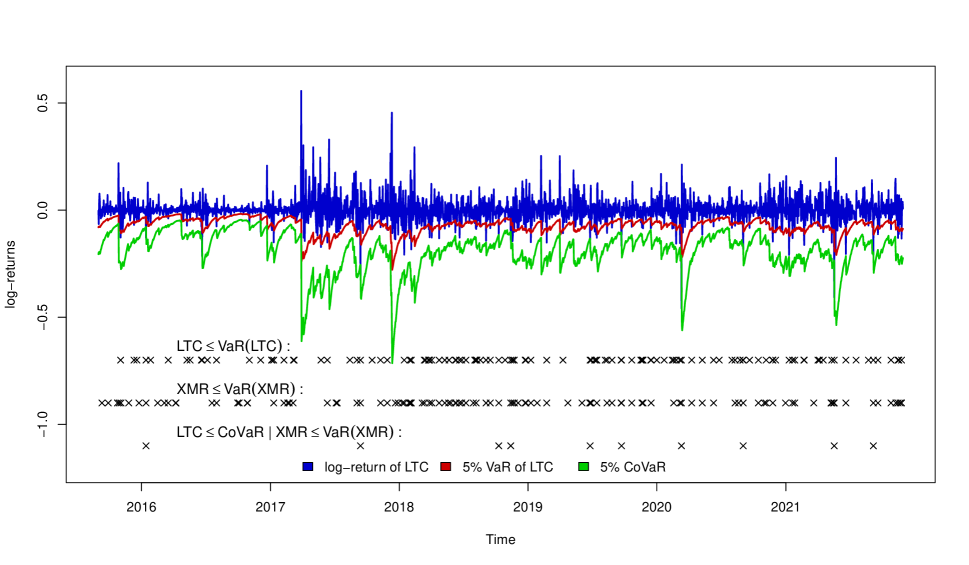

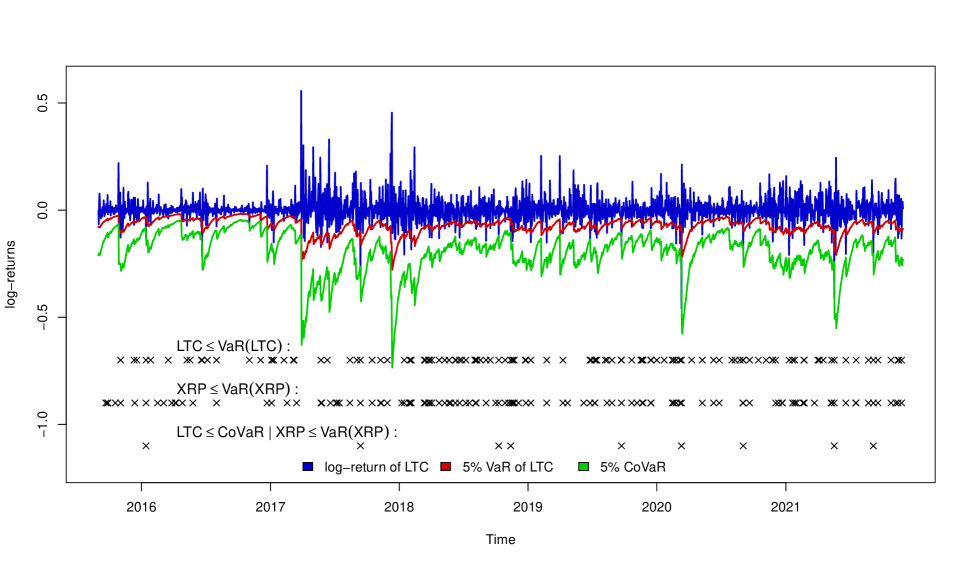

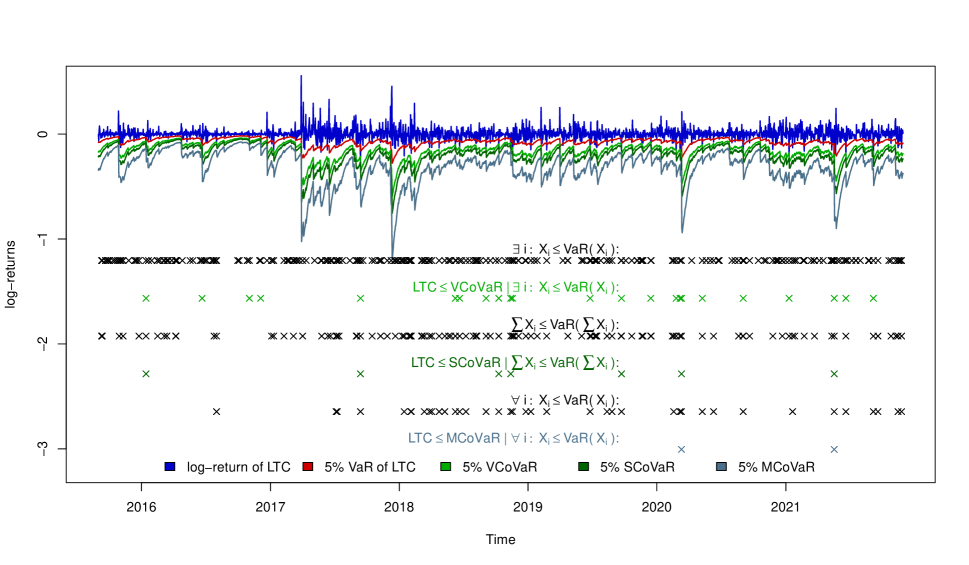

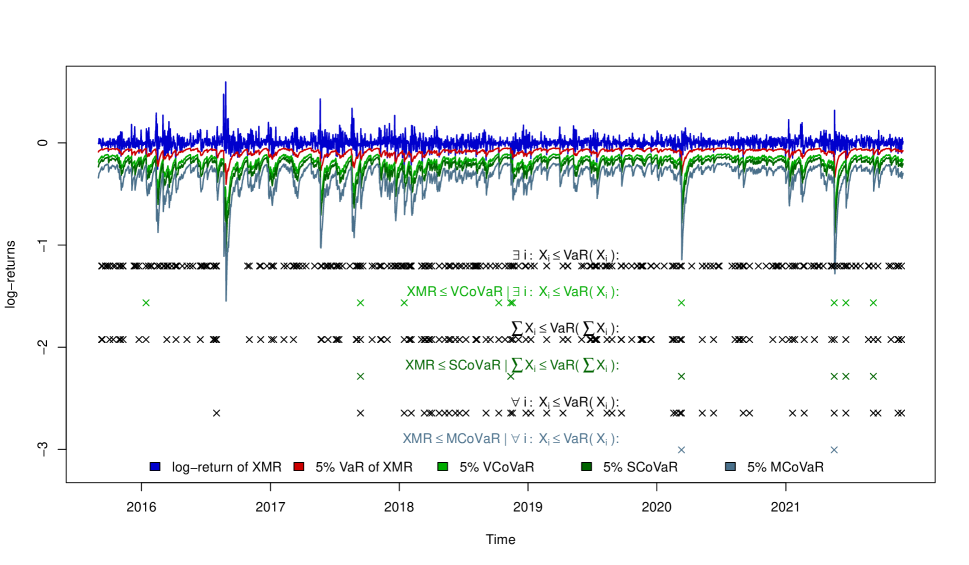

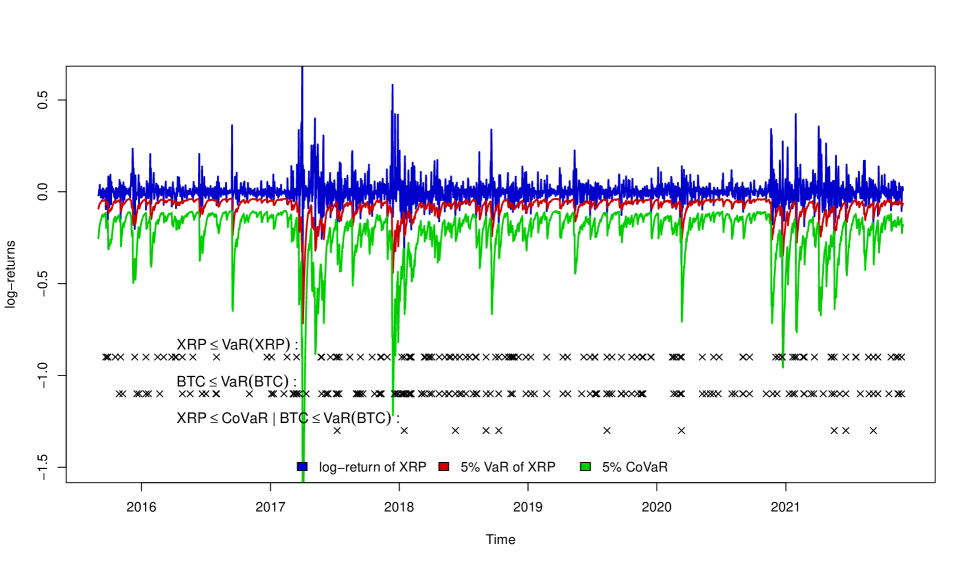

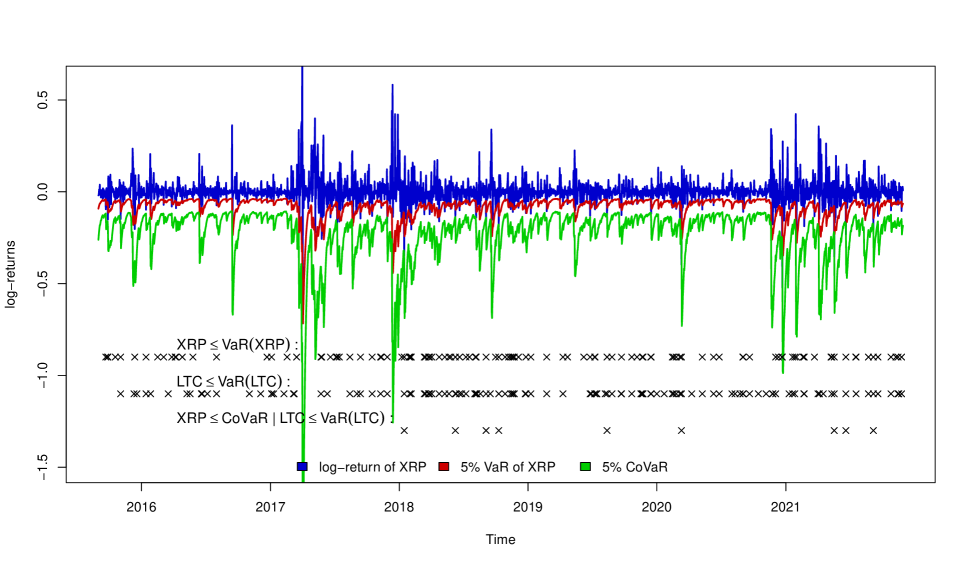

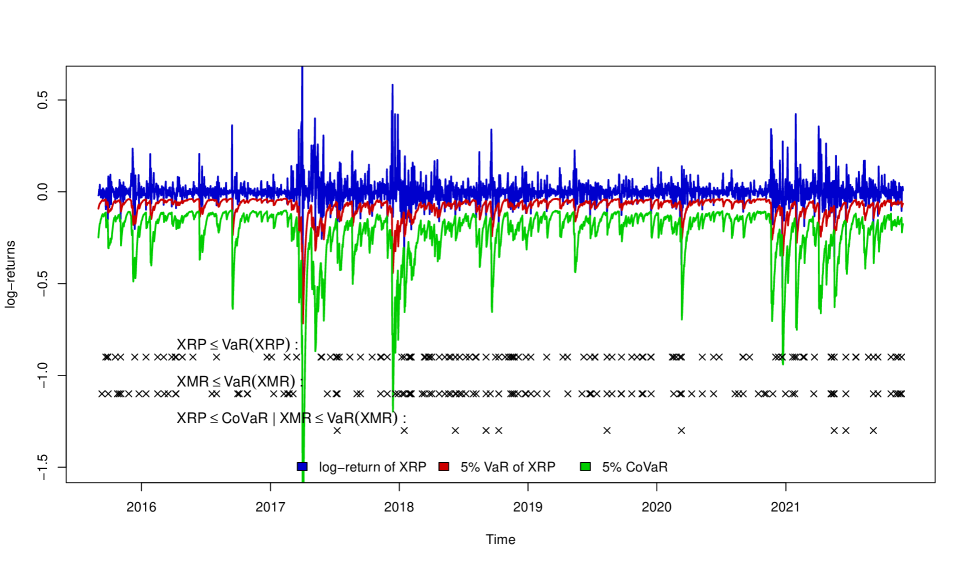

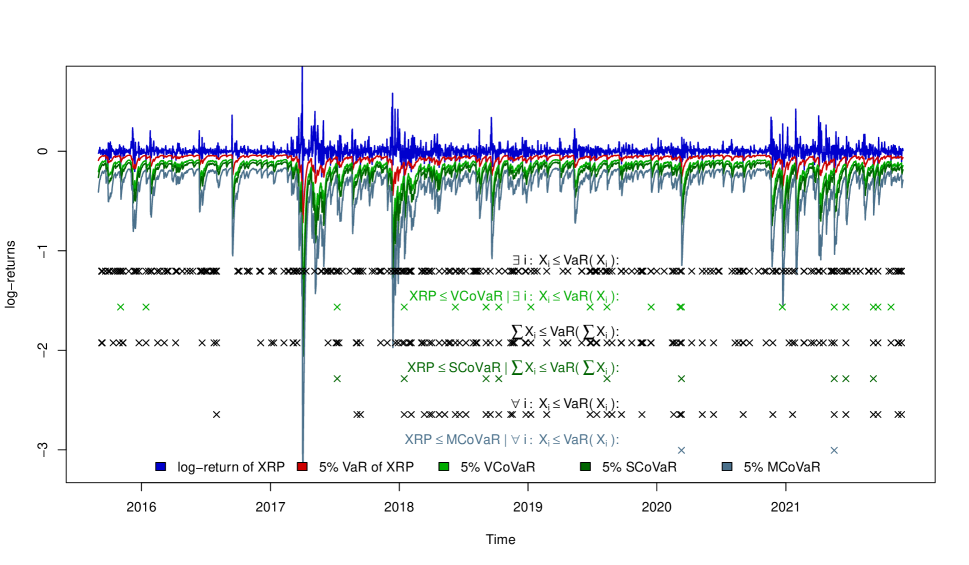

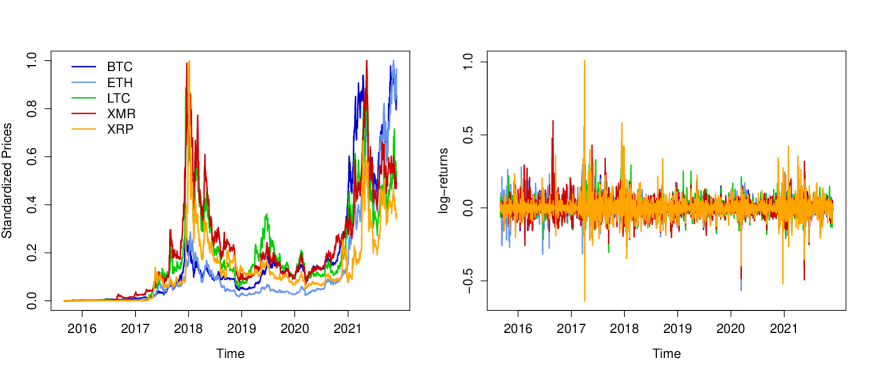

The study uses five CCs BTC, ETH, LTC, XMR, and XRP. These five CCs constitute 64.54% (https://coinmarketcap.com/, accessed: 07/12/2021) of the overall CC market capitalization and offer relatively long time series compared to other CCs, thus providing a sufficient database. The data contains daily closing prices in USD stemming from the Community Network Data kindly provided by CoinMetrics (https://coinmetrics.io/, accessed: 01/12/2021). The sample includes observations from 01/09/2015 to 30/11/2021 as CCs are traded every day, including weekends. For the analysis, the prices are transformed in log-returns. We calculate: (1) The bivariate CoVaR for all possible combinations of the five CC; (2) The SCoVaR, MCoVaR, and VCoVaR of each CC if the remaining four CCs are treated as conditional variables. We fix: . Figure 4 shows the prices (scaled to [0,1]) and the log-returns. Descriptive statistics, tests, and estimates of Kendall’s for the log-returns are given in Appendix B.

To estimate the different measures of (3), (4), (5), and (6), the following empirical procedure is used: Step 1: Estimate the respective marginal model for each time series separately. Step 2: Perform the parametric probability integral transformation on residuals to obtain iid data. Step 3: Estimate the copula based on the resulting pseudo-sample observations. Step 4: Solve (9), (11), or (13), respectively.

6.1.2 Univariate Models

Empirical results from the literature indicate that CC returns exhibit characteristics as volatility clustering, fat tails, and leverage effects, see Zhang et al. (2018) and Phillip et al. (2018). To account for these dynamics and building on the stationarity assumption, the margins are assumed to follow an autoregressive moving-average (ARMA) model for the conditional mean and a GJR-GARCH model (Glosten et al. 1993) for the conditional variance . For example, when denotes the log-return of a CC at time , the full ARMA(, )-GJR-GARCH(P,Q) model can be outlined as follows (Ghalanos 2020):

| (14) |

with iid and being an indicator function. This results in the ability of the GJR-GARCH specification to model positive and negative shocks, represented by , differently and accounts for the leverage effect (Ghalanos 2020). For , the skew- distribution with skewness and shape of Fernández and Steel (1998) is selected, as the time series exhibited a strong indication of non-normality and skewness. For parameter constraints and additional remarks on the model, see Glosten et al. (1993). In the context of this application, the ARMA-GJR-GARCH model acts as a filter for temporal dependencies inside the time series and the empirical counterparts of are extracted for further modeling. These standardized residuals should be as serially independent as possible. In addition, it might be unnecessary to specify the model as presented above, and a more parsimonious version would be sufficient to capture the dynamics of the data. Considering these facts, we use a semi-automated process which selects the best fitting model according to an information criterion while fulfilling necessary requirements on the residuals, for details see Appendix B.

Building on the selected univariate models, the VaR for each time series at level can be calculated parametrically as described in a forecasting context in Kuester et al. (2006):

| (15) |

where are the estimates from the fitted univariate model. The generated in-sample VaR estimates are necessary for evaluation and comparison with the conditional measures. To validate the VaR estimates, Table 2 shows the realized equivalents of in (1) and the absolute number of observations, in which the respective log-return was equal or below the VaR estimate. The rates are close to in all cases, indicating the accuracy of the models.

| BTC | ETH | LTC | XMR | XRP | Sys:BTC | Sys:ETH | Sys:LTC | Sys:XMR | Sys:XRP | |

| Rate in | 6.00 | 5.43 | 5.35 | 4.78 | 5.04 | 4.69 | 4.86 | 4.73 | 5.17 | 5.04 |

| Number | 137 | 124 | 122 | 109 | 115 | 107 | 111 | 108 | 118 | 115 |

-

•

NOTE: Sys:BTC denotes the sum of the log-returns of ETH, LTC, XMR, and XRP. For the selected we should observe 114.1 violations.

6.1.3 Copula Models

With the univariate models being estimated, the standardized residuals are parametrically transformed to , denoted with for BTC, ETH, LTC, XMR, and XRP. Based on these pseudo-observations, the copulae are estimated. The following time-invariant copula models are chosen for the application: Gaussian, , Clayton, and Gumbel. Time-invariance relates to having the same copula parameter at every point of time . In this case, the measures in (9), (11), and (13) become time-variant only through the dynamic nature of the univariate model of BTC, while the dependencies are assumed to be constant. However, it might be beneficial to investigate time-variant copulae to capture the potential dynamics of the dependencies, which is why we incorporate the dynamic model of Patton (2006) and the DCC-copula approach of Jin (2010). Detailed descriptions of these models alongside resulting parameter estimates of all copulae can be found in Appendix B.

6.1.4 Estimates of the Systemic Risk Measures

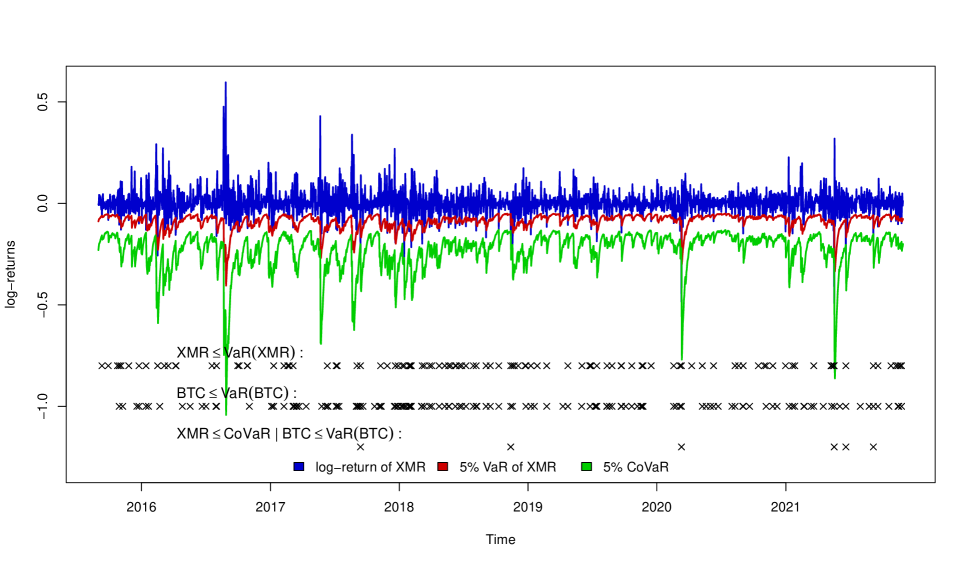

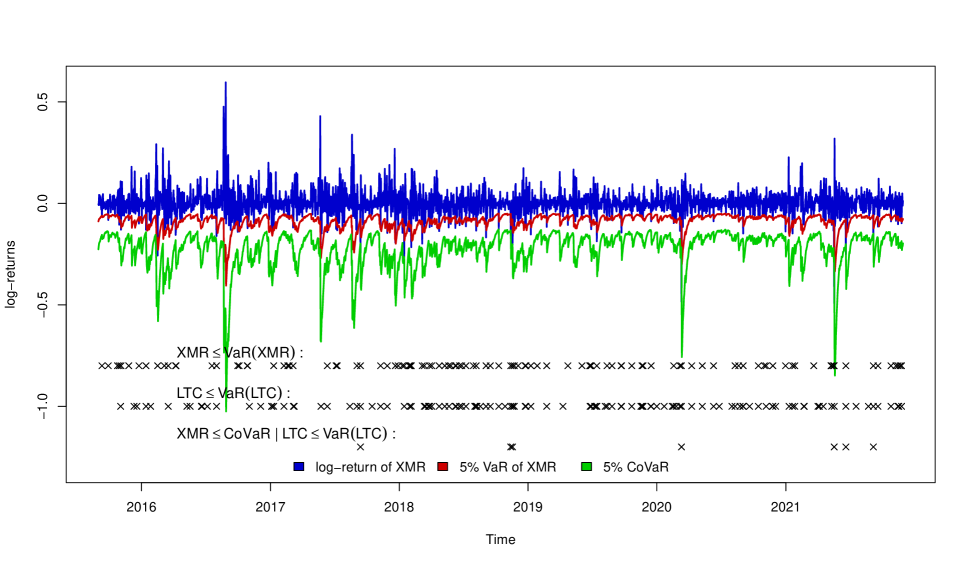

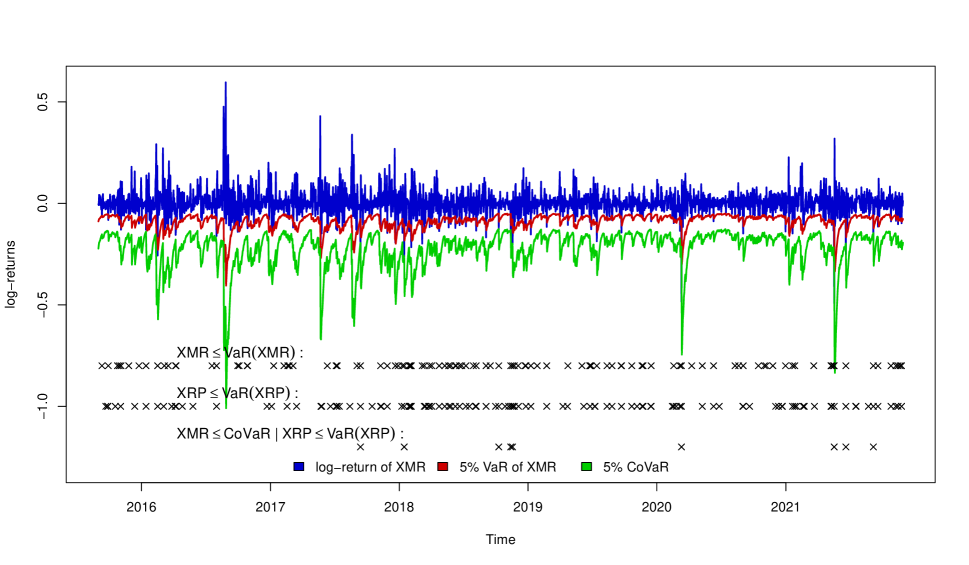

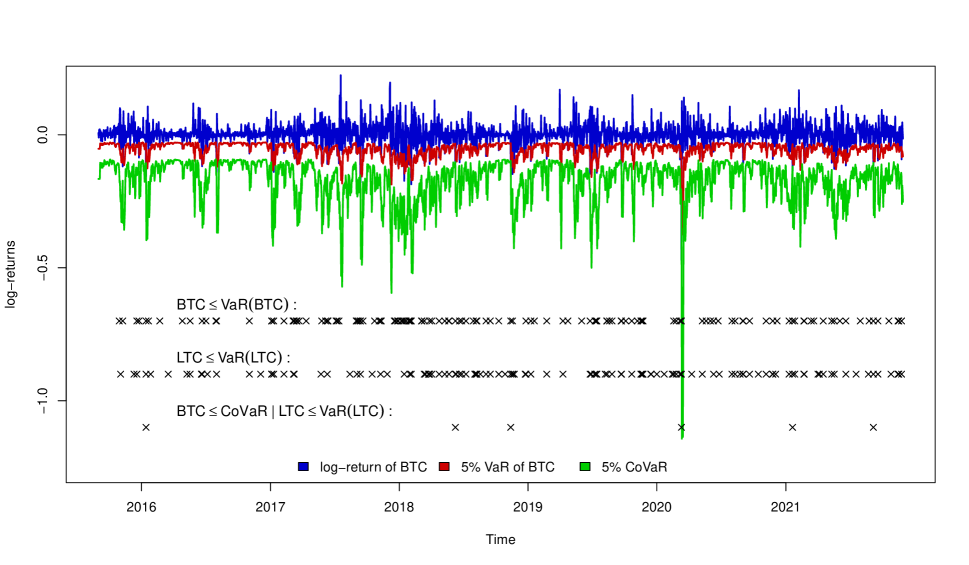

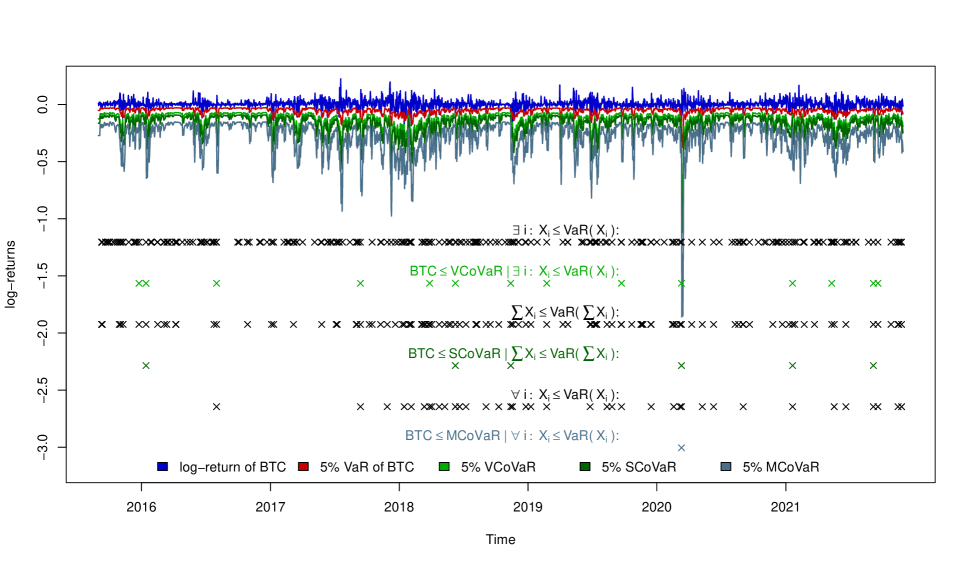

Building on the estimated marginal distributions and copulae, (9), (11), and (13) are solved for the systemic risk measures. Table 3 shows descriptive statistics alongside violation rates, which are the sample equivalents of and computed similar to Section 5. Figures 5 and 6 illustrate selected measures when the log-return of BTC is . Appendix B contains further plots.

| Measure | Mean (-copula) | Sd (-copula) | Violation rates for copula | |||||

| Gaussian | Clayton | Gumbel | Patton- | DCC- | ||||

| BTC-VaR | -0.0545 | 0.0271 | - | - | - | - | - | - |

| BTC-ETH | -0.1641 | 0.0791 | 0.0645 | 0.0484 | 0.0403 | 0.1774 | 0.0645 | 0.0645 |

| BTC-LTC | -0.1720 | 0.0829 | 0.0574 | 0.0492 | 0.0492 | 0.1066 | 0.0492 | 0.0574 |

| BTC-XMR | -0.1642 | 0.0792 | 0.0917 | 0.0642 | 0.0550 | 0.2477 | 0.0734 | 0.0826 |

| BTC-XRP | -0.1609 | 0.0776 | 0.1130 | 0.0609 | 0.0522 | 0.2435 | 0.0696 | 0.0957 |

| BTC-SCoVaR | -0.1694 | 0.0816 | 0.0654 | 0.0561 | 0.0561 | 0.1776 | 0.0654 | 0.0654 |

| BTC-MCoVaR | -0.2819 | 0.1352 | 0.0263 | 0.0263 | 0.0263 | 0.1316 | - | 0.0263 |

| BTC-VCoVaR | -0.1309 | 0.0633 | 0.1070 | 0.0576 | 0.0412 | 0.1358 | - | 0.0741 |

| ETH-VaR | -0.0860 | 0.0350 | - | - | - | - | - | - |

| ETH-BTC | -0.2442 | 0.0972 | 0.0657 | 0.0292 | 0.0219 | 0.1387 | 0.0511 | 0.0365 |

| ETH-LTC | -0.2472 | 0.0984 | 0.0738 | 0.0328 | 0.0246 | 0.1475 | 0.0410 | 0.0410 |

| ETH-XMR | -0.2455 | 0.0977 | 0.0826 | 0.0367 | 0.0275 | 0.1560 | 0.0459 | 0.0459 |

| ETH-XRP | -0.2458 | 0.0979 | 0.0870 | 0.0348 | 0.0261 | 0.1652 | 0.0609 | 0.0609 |

| ETH-SCoVaR | -0.2533 | 0.1008 | 0.0541 | 0.0270 | 0.0270 | 0.1171 | 0.0270 | 0.0360 |

| ETH-MCoVaR | -0.4026 | 0.1596 | 0.0227 | 0.0227 | 0.0227 | 0.0682 | - | 0.0227 |

| ETH-VCoVaR | -0.1950 | 0.0779 | 0.0753 | 0.0460 | 0.0418 | 0.1004 | - | 0.0711 |

| LTC-VaR | -0.0726 | 0.0359 | - | - | - | - | - | - |

| LTC-BTC | -0.1974 | 0.0976 | 0.0876 | 0.0657 | 0.0511 | 0.1533 | 0.0730 | 0.0730 |

| LTC-ETH | -0.1916 | 0.0948 | 0.1290 | 0.0726 | 0.0484 | 0.1774 | 0.0806 | 0.0645 |

| LTC-XMR | -0.1863 | 0.0921 | 0.1468 | 0.0917 | 0.0550 | 0.2202 | 0.0917 | 0.1009 |

| LTC-XRP | -0.1916 | 0.0947 | 0.1304 | 0.0783 | 0.0522 | 0.1826 | 0.0783 | 0.0870 |

| LTC-SCoVaR | -0.1968 | 0.0973 | 0.0926 | 0.0648 | 0.0556 | 0.1852 | 0.0741 | 0.0741 |

| LTC-MCoVaR | -0.3122 | 0.1544 | 0.0256 | 0.0513 | 0.0513 | 0.1282 | - | 0.0256 |

| LTC-VCoVaR | -0.1551 | 0.0767 | 0.1000 | 0.0885 | 0.0731 | 0.1231 | - | 0.0885 |

| XMR-VaR | -0.0876 | 0.0361 | - | - | - | - | - | - |

| XMR-BTC | -0.2276 | 0.0925 | 0.0730 | 0.0438 | 0.0438 | 0.1387 | 0.0584 | 0.0657 |

| XMR-ETH | -0.2286 | 0.0929 | 0.0726 | 0.0484 | 0.0484 | 0.1290 | 0.0565 | 0.0565 |

| XMR-LTC | -0.2239 | 0.0910 | 0.0820 | 0.0574 | 0.0492 | 0.1557 | 0.0656 | 0.0656 |

| XMR-XRP | -0.2204 | 0.0896 | 0.0870 | 0.0783 | 0.0522 | 0.1826 | 0.0783 | 0.0870 |

| XMR-SCoVaR | -0.2324 | 0.0944 | 0.0763 | 0.0508 | 0.0508 | 0.1186 | 0.0593 | 0.0678 |

| XMR-MCoVaR | -0.3388 | 0.1373 | 0.0488 | 0.0488 | 0.0488 | 0.1463 | - | 0.0488 |

| XMR-VCoVaR | -0.1861 | 0.0757 | 0.0675 | 0.0397 | 0.0397 | 0.0833 | - | 0.0476 |

| XRP-VaR | -0.0817 | 0.0552 | - | - | - | - | - | - |

| XRP-BTC | -0.2250 | 0.1522 | 0.1095 | 0.0730 | 0.0365 | 0.1971 | 0.0730 | 0.0657 |

| XRP-ETH | -0.2308 | 0.1561 | 0.1129 | 0.0887 | 0.0484 | 0.1935 | 0.0887 | 0.0887 |

| XRP-LTC | -0.2321 | 0.1570 | 0.0984 | 0.0738 | 0.0328 | 0.1885 | 0.0902 | 0.0820 |

| XRP-XMR | -0.2211 | 0.1495 | 0.1560 | 0.0917 | 0.0459 | 0.2661 | 0.1193 | 0.1009 |

| XRP-SCoVaR | -0.2345 | 0.1586 | 0.1043 | 0.0783 | 0.0435 | 0.1652 | 0.0870 | 0.0783 |

| XRP-MCoVaR | -0.3644 | 0.2463 | 0.0488 | 0.0488 | 0.0244 | 0.0976 | - | 0.0488 |

| XRP-VCoVaR | -0.1821 | 0.1231 | 0.1004 | 0.0763 | 0.0562 | 0.1285 | - | 0.0763 |

-

•

NOTE: The copula with the closest rate to for each row is marked bold. BTC-LTC denotes the CoVaR of BTC with LTC under condition. Mean and sd of each measure (except VaR) are given for the static -copula case.

This leads to the following findings:

-

1.

On average, all conditional measures are below the respective univariate VaR, reflecting the positive dependencies in the crypto-market. Moreover, the figures show that the conditional measures are driven by similar dynamics as the VaR, which is a consequence of the chosen static -copula and the inverse margin operation (15).

-

2.

According to average bivariate CoVaR, BTC and LTC primarily affect each other. Consequently, Figure 5 displays the CoVaR of BTC drastically below its VaR. This finding agrees with Luu Duc Huynh (2019) and Xu et al. (2021), who noticed BTC as a risk recipient of other CCs. Investors might keep that in mind when driving towards BTC. ETH responds similarly to isolated distressing events of BTC, LTC, XMR, and XRP. However, a notable impact has LTC on XRP since it leads to the lowest average CoVaR estimates for this CC.

-

3.

Generally, the average SCoVaR estimate for each CC is below the bivariate CoVaR estimates. The only exception being the pair BTC and LTC. This implies that knowing LTC is in distress appears to be worse for BTC than knowing the summation of ETH, LTC, XMR, and XRP is in a critical state.

-

4.

The MCoVaR yields the lowest average estimates for each CC, illustrating how strongly a joint distressing event of other major CCs can impact a particular currency. In addition, the MCoVaR has the highest variance among all considered measures.

-

5.

Finally, the VCoVaR is estimated below the VaR, but larger than all conditional measures. This means that knowing that at least one out of the other four CC is in distress appears less critical than knowing that exactly one is in distress without information on the other three. This reflects the nature of the conditional event and can be interpreted in two ways. First, from a methodological point of view, the conditional event of the VCoVaR includes more scenarios than all other considered measures. Consequently, more observations will fulfil it, see Figure 6. To achieve a violation rate at level for this amount of observations, the VCoVaR estimate has to lie closer to the log-return of BTC than the other conditional measures. Second, from an economic point of view, the cases of the conditional event of the VCoVaR when one CC is in distress have the additional information that the other CCs are not in distress, which the bivariate CoVaR does not include. For example, knowing LTC is in distress is worse than knowing LTC is in distress and ETH, XMR, and XRP are not. This information advantage is decisive, as it gives positive information about the market. This was discussed theoretically in Section 3.1 and perfectly materializes in this application. Furthermore, the VCoVaR exhibits the lowest variance among all other conditional measures.

-

6.

All measure can be reliably estimated via copulae. However, the selected dependence model is crucial for the estimation quality. In general, the best copulae are the -copula and the Clayton one. The time-variant Patton (2006) and DCC models can reliably be used as well, but offer only in distinct cases advantages over the static and Clayton models. The worst performance yields the Gumbel copula since it cannot the model the lower tail dependence adequately. These observations are in line with the results of the simulations in Section 4.2. However, the violation rates should be treated carefully due to the evaluation approach, which only considers the observations fulfilling the respective conditional event.

6.2 Out-of-sample Estimation

To validate the estimation performance in an out-of-sample setting, we analyze the CCs based on a moving window approach. As in Section 6.1 holds: , and we calculate the same systemic risk measures. The window size covers observations, and a one-day-ahead forecasting strategy is pursued. The univariate model is always assumed to be a GJR-GARCH(1,1) model with and skew- innovations. The CoVaR, SCoVaR, MCoVaR, and VCoVaR forecasts for are evaluated based on calculating the realized equivalents of in (3), (4), (5), and (6) while using the forecasted VaR and the log-return of . This is motivated by Girardi and Ergün (2013), although this work focuses directly on violation rates instead of tests like Kupiec (1995). To perform the one-day-ahead VaR forecasting, (15) is calculated using the forecasts of the conditional mean and conditional variance. The procedure for the conditional measures for each window is as follows: Step 1: Fit a GJR-GARCH(1,1) model to each time series and transform the resulting standardized residuals parametrically to . Step 2: Based on these pseudo-observations, estimate the respective copula via ML. Step 3: Forecast the measure by solving (9), (11), and (13) using the one-day-ahead forecast of the univariate model (14) of the variable:

| Measure | Violation rates for copula | |||

| Gaussian | Clayton | Gumbel | ||

| BTC-ETH | 0.1237 | 0.0825 | 0.0928 | 0.1959 |

| BTC-LTC | 0.0583 | 0.0485 | 0.0485 | 0.1165 |

| BTC-XMR | 0.1023 | 0.0568 | 0.0568 | 0.1932 |

| BTC-XRP | 0.1466 | 0.0862 | 0.0345 | 0.2328 |

| BTC-SCoVaR | 0.1099 | 0.0549 | 0.0549 | 0.1758 |

| BTC-MCoVaR | 0.0513 | 0.0513 | 0.0513 | 0.1026 |

| BTC-VCoVaR | 0.0909 | 0.0642 | 0.0481 | 0.1390 |

| ETH-BTC | 0.1078 | 0.0784 | 0.0686 | 0.1667 |

| ETH-LTC | 0.0583 | 0.0583 | 0.0485 | 0.1068 |

| ETH-XMR | 0.1023 | 0.0795 | 0.0455 | 0.1705 |

| ETH-XRP | 0.0948 | 0.0690 | 0.0431 | 0.1552 |

| ETH-SCoVaR | 0.0968 | 0.0753 | 0.0430 | 0.1290 |

| ETH-MCoVaR | 0.0233 | 0.0233 | 0.0233 | 0.0698 |

| ETH-VCoVaR | 0.0952 | 0.0635 | 0.0423 | 0.1270 |

| LTC-BTC | 0.0588 | 0.0490 | 0.0392 | 0.1176 |

| LTC-ETH | 0.0722 | 0.0515 | 0.0515 | 0.1031 |

| LTC-XMR | 0.1023 | 0.0682 | 0.0568 | 0.1477 |

| LTC-XRP | 0.0776 | 0.0431 | 0.0345 | 0.1121 |

| LTC-SCoVaR | 0.0814 | 0.0581 | 0.0465 | 0.1279 |

| LTC-MCoVaR | 0.0250 | 0.0750 | 0.0750 | 0.1250 |

| LTC-VCoVaR | 0.0681 | 0.0576 | 0.0419 | 0.1099 |

| XMR-BTC | 0.1078 | 0.0784 | 0.0490 | 0.1667 |

| XMR-ETH | 0.0825 | 0.0825 | 0.0412 | 0.1340 |

| XMR-LTC | 0.0874 | 0.0777 | 0.0485 | 0.1359 |

| XMR-XRP | 0.0948 | 0.0690 | 0.0431 | 0.1466 |

| XMR-SCoVaR | 0.0968 | 0.0860 | 0.0430 | 0.1290 |

| XMR-MCoVaR | 0.0732 | 0.0732 | 0.0732 | 0.1220 |

| XMR-VCoVaR | 0.0737 | 0.0474 | 0.0474 | 0.1105 |

| XRP-BTC | 0.1667 | 0.0980 | 0.0882 | 0.2941 |

| XRP-ETH | 0.1134 | 0.0825 | 0.0825 | 0.1959 |

| XRP-LTC | 0.1165 | 0.0680 | 0.0583 | 0.1845 |

| XRP-XMR | 0.1250 | 0.0795 | 0.0795 | 0.2386 |

| XRP-SCoVaR | 0.0769 | 0.0769 | 0.0769 | 0.1429 |

| XRP-MCoVaR | 0.0732 | 0.0244 | 0.0244 | 0.0732 |

| XRP-VCoVaR | 0.1561 | 0.1040 | 0.0636 | 0.1676 |

NOTE: The copula with the closest rate to for each row is marked bold. BTC-LTC denotes the CoVaR of BTC with LTC under condition.

The resulting VaR violation rates for the CC are with 0.0572 for BTC, 0.0544 for ETH, 0.0578 for LTC, 0.0494 for XMR, and 0.0651 for XRP all close to . Further, the rates for the systems are similarly accurate: 0.0511 for Sys:BTC, 0.0522 for Sys:ETH, 0.0483 for Sys:LTC, 0.0522 for Sys:XMR, and 0.0511 for Sys:XRP. Table 4 shows the rates for the conditional measures while using the time-invariant Gaussian, , Clayton, and Gumbel copulae. Especially for the Clayton model, the CoVaR, SCoVaR, MCoVaR, and VCoVaR forecasts are close to , although the -copula is also a valid choice in most cases. Furthermore, the performance of the copulae relative to each other is as in the in-sample scenario.

7 Conclusion

Quantifying systemic risk in the financial system is a key focus for regulators and risk management practitioners. Especially the rapidly-growing and highly volatile market of CC has attracted the attention of regulating authorities and researchers due to its potential impact on the status of the global financial system. An important methodological contribution is the systemic risk measure CoVaR, introduced by Adrian and Brunnermeier (2016). Cao (2014) proposed an extension called Multi-CoVaR, while Bernardi et al. (2019) introduced a measure named System-CoVaR. Complementing these extensions, a new measure, the Vulnerability-CoVaR is proposed. The VCoVaR offers the improved ability to capture domino effects and is advantageous in a system where there exists at least one other CC which is facing an extreme risk scenario. Due to evidence of spillover effects, tail-dependence, and herding behaviour, such domino effects are an existing threat and source of systemic risk in the CC market.

The simulation-based analysis of dependence consistency displays the property of the VCoVaR to be a monotonically decreasing function of the dependence parameter for selected AC. The empirical analysis on the CC market showed that LTC displays the largest impact on BTC out of the selected currencies, and LTC further affects XRP relatively strong. Generally, each CC is significantly affected if an event of joint distress of the remaining currencies occurs, which can be considered symptomatic for systemic risk events in the CC market. Interestingly, a situation of at least on CC being in distress appears less critical than a specification of one concrete CC in the conditional event. This observation reflects exactly the nature of the conditional event of the VCoVaR. Regarding the estimation quality, significant differences between the considered copulae are detected. However, for the and Clayton copulae, the conditional measures are reliably estimated, as the in-sample and out-of-sample violation rates are approximately in line with the selected probability level.

Future work on the topic of CoVaR extensions could extend the analysis of dependence consistency to broader families of copulae and higher dimensional scenarios. Especially in the case of the newly proposed VCoVaR, theoretical analysis and simulations apart from the considered Archimedean copula models could be conducted. In addition, considered CoVaR extensions could be applied to different asset markets with varied sample sizes, to validate the estimation quality using more observations. It could also be analysed whether the VCoVaR could be reasonably extended to a difference-based measure comparable to the Delta-CoVaR of Adrian and Brunnermeier (2016).

ACKNOWLEDGEMENTS

The authors would like to thank Arsen Palestini for his fruitful answer regarding the System-CoVaR and Jianlin Zhang for writing an excellent Master’s thesis, which inspired this work. The authors report there are no competing interests to declare.

References

- Acharya et al. (2017) Acharya, V. V., Pedersen, L. H., Philippon, T., and Richardson, M. Measuring systemic risk. The Review of Financial Studies, 2017, 30, 2–47.

- Adrian and Brunnermeier (2016) Adrian, T. and Brunnermeier, M. K. CoVaR. The American Economic Review, 2016, 106, 1705–1741.

- Akaike (1974) Akaike, H. A new look at the statistical model identification. IEEE Transactions on Automatic Control, 1974, 19, 716–723.

- Ballis and Drakos (2020) Ballis, A. and Drakos, K. Testing for herding in the cryptocurrency market. Finance Research Letters, 2020, 33, 101210.

- Basel Committee on Banking Supervision (2013) Basel Committee on Banking Supervision, Global Systemically Important Banks: Updated Assessment Methodology and the Higher Loss Absorbency Requirement. Technical report, Bank for International Settlements, Basel, 2013.

- Basel Committee on Banking Supervision (2019) —, Designing a prudential treatment for crypto-assets. Discussion paper, Bank for International Settlements, Basel, 2019.

- Benoit et al. (2017) Benoit, S., Colliard, J.-E., Hurlin, C., and Pérignon, C. Where the risks lie: A survey on systemic risk. Review of Finance, 2017, 21, 109–152.

- Bernardi et al. (2019) Bernardi, M., Cerqueti, R., and Palestini, A. Allocation of risk capital in a cost cooperative game induced by a modified expected shortfall. Journal of the Operational Research Society, 2019.

- Bernardi et al. (2018) Bernardi, M., Durante, F., Jaworski, P., Petrella, L., and Salvadori, G. Conditional risk based on multivariate hazard scenarios. Stochastic Environmental Research and Risk Assessment, 2018, 32, 203–211.

- Bernardi et al. (2017) Bernardi, M., Maruotti, A., and Petrella, L. Multiple risk measures for multivariate dynamic heavy–tailed models. Journal of Empirical Finance, 2017, 43, 1–32.

- Bisias et al. (2012) Bisias, D., Flood, M., Lo, A. W., and Valavanis, S. A survey of systemic risk analytics. Annual Review of Financial Economics, 2012, 4, 255–296.

- Bonaccolto et al. (2021) Bonaccolto, G., Borri, N., and Consiglio, A. Breakup and default risks in the great lockdown. Journal of Banking & Finance, 2021, 106308.

- Borri (2019) Borri, N. Conditional tail-risk in cryptocurrency markets. Journal of Empirical Finance, 2019, 50, 1–19.

- Bouri et al. (2019) Bouri, E., Gupta, R., and Roubaud, D. Herding behaviour in cryptocurrencies. Finance Research Letters, 2019, 29, 216–221.

- Brownlees and Engle (2017) Brownlees, C. and Engle, R. F. SRISK: A conditional capital shortfall measure of systemic risk. The Review of Financial Studies, 2017, 30, 48–79.

- Cao (2014) Cao, Z., Multi-CoVaR and Shapley value: A systemic risk measure. Working paper, Banque de France DSF-SMF, 2014.

- Chang et al. (2000) Chang, E. C., Cheng, J. W., and Khorana, A. An examination of herd behavior in equity markets: An international perspective. Journal of Banking & Finance, 2000, 24, 1651–1679.

- Chiang and Zheng (2010) Chiang, T. C. and Zheng, D. An empirical analysis of herd behavior in global stock markets. Journal of Banking & Finance, 2010, 34, 1911–1921.

- Di Bernardino et al. (2015) Di Bernardino, E., Fernández-Ponce, J. M., Palacios-Rodríguez, F., and Rodríguez-Griñolo, M. R. On multivariate extensions of the conditional Value-at-Risk measure. Insurance: Mathematics and Economics, 2015, 61, 1–16.

- Diebold and Yilmaz (2015) Diebold, F. X. and Yilmaz, K. Trans-Atlantic equity volatility connectedness: US and European financial institutions, 2004–2014. Journal of Financial Econometrics, 2015, 14, 81–127.

- Eling and Toplek (2009) Eling, M. and Toplek, D. Modeling and management of nonlinear dependencies-copulas in dynamic financial analysis. Journal of Risk and Insurance, 2009, 76, 651–681.

- Engle (2002) Engle, R. F. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. Journal of Business & Economic Statistics, 2002, 20, 339–350.

- Engle and Ng (1993) Engle, R. F. and Ng, V. K. Measuring and testing the impact of news on volatility. The Journal of Finance, 1993, 48, 1749–1778.

- Fernández and Steel (1998) Fernández, C. and Steel, M. F. On bayesian modeling of fat tails and skewness. Journal of the American Statistical Association, 1998, 93, 359–371.

- Fisher and Gallagher (2012) Fisher, T. J. and Gallagher, C. M. New weighted portmanteau statistics for time series goodness of fit testing. Journal of the American Statistical Association, 2012, 107, 777–787.

- Georges et al. (2001) Georges, P., Lamy, A.-G., Nicolas, E., Quibel, G., and Roncalli, T., Multivariate survival modelling: A unified approach with copulas. Working Paper, DOI: 10.2139/ssrn.1032559 2001.

- Ghalanos (2019) Ghalanos, A. 2019, rmgarch: Multivariate GARCH models, R package version 1.3-7, URL: https://cran.r-project.org/package=rmgarch, accessed: 23/12/20.

- Ghalanos (2020) — 2020, rugarch: Univariate GARCH models, R package version 1.4-4, URL: https://cran.r-project.org/package=rugarch, accessed: 13/12/21.

- Girardi and Ergün (2013) Girardi, G. and Ergün, A. T. Systemic risk measurement: Multivariate GARCH estimation of CoVaR. Journal of Banking & Finance, 2013, 37, 3169–3180.

- Glosten et al. (1993) Glosten, L. R., Jagannathan, R., and Runkle, D. E. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance, 1993, 48, 1779–1801.

- Härdle et al. (2016) Härdle, W. K., Wang, W., and Yu, L. TENET: Tail-Event driven NETwork risk. Journal of Econometrics, 2016, 192, 499–513.

- Hwang and Salmon (2004) Hwang, S. and Salmon, M. Market stress and herding. Journal of Empirical Finance, 2004, 11, 585–616.

- Ji et al. (2019) Ji, Q., Bouri, E., Lau, C. K. M., and Roubaud, D. Dynamic connectedness and integration in cryptocurrency markets. International Review of Financial Analysis, 2019, 63, 257–272.

- Jin (2010) Jin, X., Large portfolio risk management with dynamic copulas. Technical report, McGill University, 2010.

- Joe (2014) Joe, H., Dependence Modeling with Copulas, 2014, Boca Raton, FL: CRC press.

- Kallinterakis and Wang (2019) Kallinterakis, V. and Wang, Y. Do investors herd in cryptocurrencies–and why? Research in International Business and Finance, 2019, 50, 240–245.

- Karimalis and Nomikos (2018) Karimalis, E. N. and Nomikos, N. K. Measuring systemic risk in the European banking sector: A copula CoVaR approach. The European Journal of Finance, 2018, 24, 944–975.

- Katsiampa et al. (2019) Katsiampa, P., Corbet, S., and Lucey, B. Volatility spillover effects in leading cryptocurrencies: A BEKK-MGARCH analysis. Finance Research Letters, 2019, 29, 68–74.

- Koenker and Bassett Jr (1978) Koenker, R. and Bassett Jr, G. Regression quantiles. Econometrica, 1978, 46, 33–50.

- Kojadinovic and Yan (2010) Kojadinovic, I. and Yan, J. Modeling multivariate distributions with continuous margins using the copula R package. Journal of Statistical Software, 2010, 34, 1–20.

- Koutmos (2018) Koutmos, D. Return and volatility spillovers among cryptocurrencies. Economics Letters, 2018, 173, 122–127.

- Kuester et al. (2006) Kuester, K., Mittnik, S., and Paolella, M. S. Value-at-risk prediction: A comparison of alternative strategies. Journal of Financial Econometrics, 2006, 4, 53–89.

- Kupiec (1995) Kupiec, P. Techniques for verifying the accuracy of risk measurement models. The Journal of Derivatives, 1995, 3, 73–84.

- Kwiatkowski et al. (1992) Kwiatkowski, D., Phillips, P. C., Schmidt, P., and Shin, Y. Testing the null hypothesis of stationarity against the alternative of a unit root. Journal of Econometrics, 1992, 54, 159–178.

- Kyriazis (2019) Kyriazis, N. A. A survey on empirical findings about spillovers in cryptocurrency markets. Journal of Risk and Financial Management, 2019, 12, 170.

- Kyriazis (2020) —Herding behaviour in digital currency markets: An integrated survey and empirical estimation. Heliyon, 2020, 6, e04752.

- Li and Mak (1994) Li, W. K. and Mak, T. K. On the squared residual autocorrelations in non-linear time series with conditional heteroskedasticity. Journal of Time Series Analysis, 1994, 15, 627–636.

- Li et al. (2020) Li, Z., Wang, Y., and Huang, Z. Risk Connectedness Heterogeneity in the Cryptocurrency Markets. Frontiers in Physics, 2020, 8, 243.

- Ljung and Box (1978) Ljung, G. M. and Box, G. E. On a measure of lack of fit in time series models. Biometrika, 1978, 65, 297–303.

- Luu Duc Huynh (2019) Luu Duc Huynh, T. Spillover risks on cryptocurrency markets: A look from VAR-SVAR Granger causality and student’s copulas. Journal of Risk and Financial Management, 2019, 12, 52.

- Lux and Papapantoleon (2017) Lux, T. and Papapantoleon, A. Improved Fréchet–Hoeffding bounds on -copulas and applications in model-free finance. The Annals of Applied Probability, 2017, 27, 3633–3671.

- Mainik and Schaanning (2014) Mainik, G. and Schaanning, E. On dependence consistency of CoVaR and some other systemic risk measures. Statistics & Risk Modeling, 2014, 31, 49–77.

- Manner and Reznikova (2012) Manner, H. and Reznikova, O. A survey on time-varying copulas: Specification, simulations, and application. Econometric Reviews, 2012, 31, 654–687.

- McLeod and Li (1983) McLeod, A. I. and Li, W. K. Diagnostic checking ARMA time series models using squared-residual autocorrelations. Journal of Time Series Analysis, 1983, 4, 269–273.

- Nelsen (2006) Nelsen, R. B., An Introduction to Copulas, 2006, New York: Springer Science & Business Media.

- Oehlert (1992) Oehlert, G. W. A note on the delta method. The American Statistician, 1992, 46, 27–29.

- Okhrin et al. (2013) Okhrin, O., Okhrin, Y., and Schmid, W. On the structure and estimation of hierarchical Archimedean copulas. Journal of Econometrics, 2013, 173, 189–204.

- Okhrin and Ristig (2014) Okhrin, O. and Ristig, A. Hierarchical Archimedean Copulae: The HAC Package. Journal of Statistical Software, 2014, 58, 1–20.

- Patton (2006) Patton, A. J. Modelling asymmetric exchange rate dependence. International Economic Review, 2006, 47, 527–556.

- Petukhina et al. (2021) Petukhina, A., Trimborn, S., Härdle, W. K., and Elendner, H. Investing with cryptocurrencies–evaluating their potential for portfolio allocation strategies. Quantitative Finance, 2021, 1–29.

- Phillip et al. (2018) Phillip, A., Chan, J. S., and Peiris, S. A new look at cryptocurrencies. Economics Letters, 2018, 163, 6–9.

- Phillips and Perron (1988) Phillips, P. C. and Perron, P. Testing for a unit root in time series regression. Biometrika, 1988, 75, 335–346.

- Reboredo and Ugolini (2015) Reboredo, J. C. and Ugolini, A. Systemic risk in European sovereign debt markets: A CoVaR-copula approach. Journal of International Money and Finance, 2015, 51, 214–244.

- Said and Dickey (1984) Said, S. E. and Dickey, D. A. Testing for unit roots in autoregressive-moving average models of unknown order. Biometrika, 1984, 71, 599–607.

- Sklar (1959) Sklar, A. Fonctions de Répartition à n Dimension et Leurs Marges. Publications de l’Institut de Statistique de l’Université de Paris, 1959, 8, 299–231.

- Smales (2020) Smales, L. A. One Cryptocurrency to explain them all? Understanding the importance of Bitcoin in Cryptocurrency returns. Economic Papers. Special Section: Economics of Blockchain Technology, 2020, 39, 118–132.

- Stavroyiannis and Babalos (2017) Stavroyiannis, S. and Babalos, V. Herding, faith-based investments and the global financial crisis: Empirical evidence from static and dynamic models. Journal of Behavioral Finance, 2017, 18, 478–489.

- Szczygielski et al. (2020) Szczygielski, J. J., Karathanasopoulos, A., and Zaremba, A. One shape fits all? A comprehensive examination of cryptocurrency return distributions. Applied Economics Letters, 2020, 27, 1567–1573.

- Tiwari et al. (2020) Tiwari, A. K., Adewuyi, A. O., Albulescu, C. T., and Wohar, M. E. Empirical evidence of extreme dependence and contagion risk between main cryptocurrencies. The North American Journal of Economics and Finance, 2020, 51, 101083.

- Tsay (2010) Tsay, R. S., Analysis of Financial Time Series, 2010, New Jersey: John Wiley & Sons.

- Vidal-Tomás (2021) Vidal-Tomás, D. An investigation of cryptocurrency data: The market that never sleeps. Quantitative Finance, 2021, 1–18.

- Vidal-Tomás et al. (2019) Vidal-Tomás, D., Ibáñez, A. M., and Farinós, J. E. Herding in the cryptocurrency market: CSSD and CSAD approaches. Finance Research Letters, 2019, 30, 181–186.

- Xu et al. (2021) Xu, Q., Zhang, Y., and Zhang, Z. Tail-risk spillovers in cryptocurrency markets. Finance Research Letters, 2021, 38, 101453.

- Zhang et al. (2018) Zhang, W., Wang, P., Li, X., and Shen, D. Some stylized facts of the cryptocurrency market. Applied Economics, 2018, 50, 5950–5965.

- Zhou (2010) Zhou, C. Are banks too big to fail? Measuring systemic importance of financial institutions. International Journal of Central Banking, 2010, 6, 205–250.

Appendix A: Proofs

Proof of Lemma 3.1.

Proof of Lemma 3.2.

Proof of Lemma 4.1.

Proof of Lemma 4.2.

The CoVaR of (9) becomes: as the copula equals the upper Fréchet-Hoeffding bound. Solving leads to: , based on . Similarly for the MCoVaR, (11) transforms in:

which is solved as: . For the VCoVaR, (13) becomes:

| (A.4) |

which applies the upper Fréchet-Hoeffding bound to survival copulae, see Lux and Papapantoleon (2017). Notice that implies . This follows directly as (A.4) would reduce in this case to:

which is simplified to: . As is imposed, it must hold: . In this scenario, (A.4) can be transformed to:

which yields: . ∎

Appendix B: Supplements to the Empirical Study

B.1 Data Description

Tables B.1, B.2 provides descriptive statistics and tests of the log-returns of the empirical study for the CCs and system variables. For example, ’Sys:BTC’ denotes the system for BTC, and is the equally weighted sum of the log-returns of ETH, LTC, XMR, and XRP. ADF refers to the test of Said and Dickey (1984), PP to Phillips and Perron (1988), and KPSS to Kwiatkowski et al. (1992). An asterisk (*) indicates rejection of the null hypothesis at level .

| BTC | ETH | LTC | XMR | XRP | |

| Min | -0.4706 | -0.5656 | -0.4588 | -0.4922 | -0.6365 |

| Mean | 0.0024 | 0.0036 | 0.0019 | 0.0027 | 0.0021 |

| Median | 0.0024 | 0.0013 | -0.0005 | 0.0018 | -0.0015 |

| Max | 0.2241 | 0.3006 | 0.5568 | 0.5963 | 1.0087 |

| Sd | 0.0399 | 0.0615 | 0.0567 | 0.0620 | 0.0705 |

| Kurtosis | 11.2569 | 6.7074 | 12.4750 | 11.2825 | 30.2736 |

| Skewness | -0.7495 | -0.3117 | 0.7160 | 0.5130 | 1.9136 |

| -value: Jarque-Bera | 0.0000* | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| -value: Ljung-Box (8 lags) | 0.0950 | 0.0046* | 0.0004* | 0.0000* | 0.0001* |

| Statistics: ADF | -15.7728* | -15.7839* | -16.0902* | -14.7867* | -13.2823* |

| Statistics: PP | -49.6547* | -49.9640* | -48.7192* | -51.2537* | -49.6844* |

| Statistics: KPSS | 0.1178 | 0.2188 | 0.1194 | 0.3638 | 0.1115 |

| Sys:BTC | Sys:ETH | Sys:LTC | Sys:XMR | Sys:XRP | |

| Min | -1.9056 | -1.8106 | -1.9174 | -1.8918 | -1.9793 |

| Mean | 0.0103 | 0.0092 | 0.0109 | 0.0100 | 0.0106 |

| Median | 0.0122 | 0.0090 | 0.0133 | 0.0111 | 0.0141 |

| Max | 1.3151 | 1.0483 | 0.9200 | 1.2294 | 0.9068 |

| Sd | 0.1950 | 0.1816 | 0.1812 | 0.1818 | 0.1807 |

| Kurtosis | 8.5834 | 8.8517 | 8.8186 | 9.2215 | 9.7159 |

| Skewness | -0.6068 | -0.6277 | -0.7920 | -0.5603 | -0.9170 |

| -value: Jarque-Bera | 0.0000* | 0.0000* | 0.0000* | 0.0000* | 0.0000* |

| -value: Ljung-Box (8 lags) | 0.0000* | 0.0000* | 0.0000* | 0.0001* | 0.0000* |

| Statistics: ADF | -14.8125* | -14.8316* | -14.6531* | -15.0416* | -15.6975* |

| Statistics: PP | -50.5398* | -50.8404* | -51.1797* | -50.3953* | -50.6902* |

| Statistics: KPSS | 0.2609 | 0.2261 | 0.2738 | 0.1905 | 0.2673 |

Table B.3 shows estimates of Kendall’s between the log-returns. BTC and LTC display the strongest dependency between the five CCs, while between the systems is by design relatively high.

| BTC | ETH | LTC | XMR | XRP | Sys:BTC | Sys:ETH | Sys:LTC | Sys:XMR | Sys:XRP | |

| BTC | 1.0000 | 0.4218 | 0.5558 | 0.4278 | 0.3805 | 0.5070 | 0.5978 | 0.5570 | 0.5892 | 0.6049 |

| ETH | 1.0000 | 0.4558 | 0.4206 | 0.4166 | 0.6428 | 0.5013 | 0.6469 | 0.6617 | 0.6560 | |

| LTC | 1.0000 | 0.4228 | 0.4597 | 0.6262 | 0.6641 | 0.5467 | 0.6698 | 0.6543 | ||

| XMR | 1.0000 | 0.3737 | 0.6241 | 0.6416 | 0.6391 | 0.4794 | 0.6460 | |||

| XRP | 1.0000 | 0.6120 | 0.6170 | 0.6061 | 0.6273 | 0.4655 | ||||

| Sys:BTC | 1.0000 | 0.8298 | 0.8858 | 0.8283 | 0.8286 | |||||

| Sys:ETH | 1.0000 | 0.8073 | 0.7718 | 0.7788 | ||||||

| Sys:LTC | 1.0000 | 0.7997 | 0.8157 | |||||||

| Sys:XMR | 1.0000 | 0.7704 | ||||||||

| Sys:XRP | 1.0000 |

B.2 Univariate Model Selection

B.2.1 Procedure

We propose to use the following procedure to select the univariate models, while we perform the ML estimation in the R-package rugarch (Ghalanos 2020).

-

Step 1:

Calculate all possible ARMA() models with . Of those models, consider the ones non-rejecting the Ljung and Box (1978) (LB) hypothesis of having no serial correlation in the residuals.

- Step 2:

-

Step 3:

If the hypothesis of having no ARCH effects of the model of Step 2 is non-rejected, return the model of Step 2. If is rejected, calculate all possible ARMA()-GARCH(P,Q) models with and . Of those models, consider the ones non-rejecting the LB test and the weighted version of the test of Li and Mak (1994) proposed in Fisher and Gallagher (2012) (WLM) for correct ARCH model specification, applied to the standardized residuals.

-

Step 4:

From the models left after Step 3, select the one with the lowest AIC. Test the model for asymmetries/leverage effect using the Sign Bias tests of Engle and Ng (1993).

-

Step 5:

If the hypotheses of having no asymmetries are non-rejected, return the model of Step 4. If an is rejected, calculate all ARMA()-GJR-GARCH(P,Q) models with and . Of those models, consider the ones non-rejecting the LB, the WLM and the Sign Bias tests on the standardized residuals.

-

Step 6:

From the models of Step 5, return the one with the lowest AIC.

Following Tsay (2010), the degrees of freedom of the chi-square distribution of the test statistic of the LB test is reduced by to account for the parametrization of the ARMA model. The same holds for the test of McLeod and Li (1983) of Step 2 in the selection procedure, which tests the null hypothesis of having no ARCH effects by applying the LB statistic to the squared residuals (Tsay 2010). Common use in practice is to pursue the same procedure for the squared standardized residuals of an ARMA-GARCH model, see, e.g., Reboredo and Ugolini (2015). However, Li and Mak (1994) proposed an improved test statistic to test the null hypothesis of having no ARCH effects in GARCH-type models. In the given application, the modification of Fisher and Gallagher (2012) is used while pursuing a correction of the respective degrees of freedom following the implementation of the rugarch package. The Sign Bias tests of Engle and Ng (1993) regress the squared standardized residuals on the lagged estimated residuals as follows:

where is the indicator function, to examine the hypotheses with and for the Joint effect . The test of is referred to as Sign Bias, the one of as Negative Sign Bias, and the one of as Positive Sign Bias (Ghalanos 2020). In case of rejection of a hypothesis, there are significant asymmetries in the data, and the model is adjusted.

Please note that this procedure results in finding the best fitting model (in the sense of AIC) while maintaining parsimony and fulfilling the conditions on the standardized residuals. All models were estimated twice - with estimated from the data and with - to capture possible improvements. We remark that this procedure is statistically thoroughly debatable, as a test is regarded as fulfilled if its hypothesis is not rejected. However, such approaches are heavily pursued in practical time series testing, which is the reason we specified this kind of selection procedure. The resulting models of this procedure have not been used in the case of the systems, which are necessary for the SCoVaR. Since each system is the sum of four CC, the dynamics become extremely complex and the found models yielded large VaR violations. More research has to be done to analyze the dynamics in such systems and we stick to a standard GARCH(1,1) specification for these cases.

B.2.2 Results

The results of the univariate model selection are given in Tables B.4 and B.5. Standard errors are given in parentheses, and an asterisk (*) denotes significance at level . The AIC of a model with log-likelihood and number of parameters is given as: (Akaike 1974). LB is the test of Ljung and Box (1978), while LB2 performs the test on the squared standardized residuals. WLM is the weighted version of the test in Li and Mak (1994) proposed by Fisher and Gallagher (2012). The Sign Bias (SB) tests relate to Engle and Ng (1993).

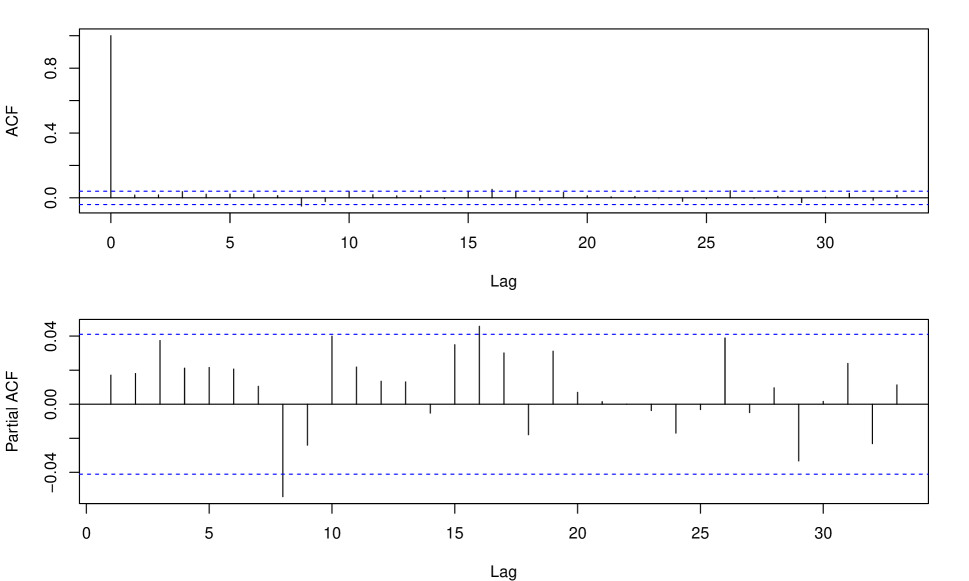

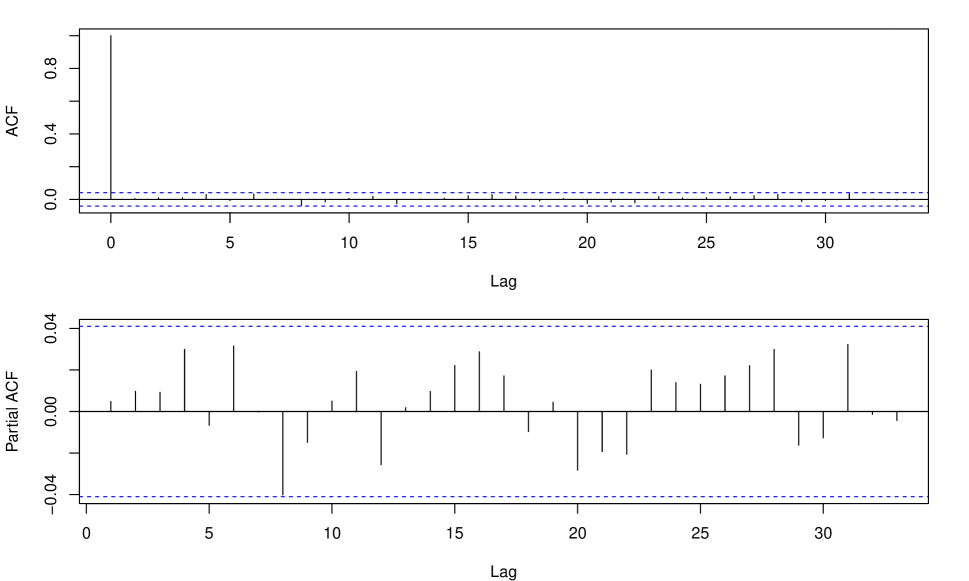

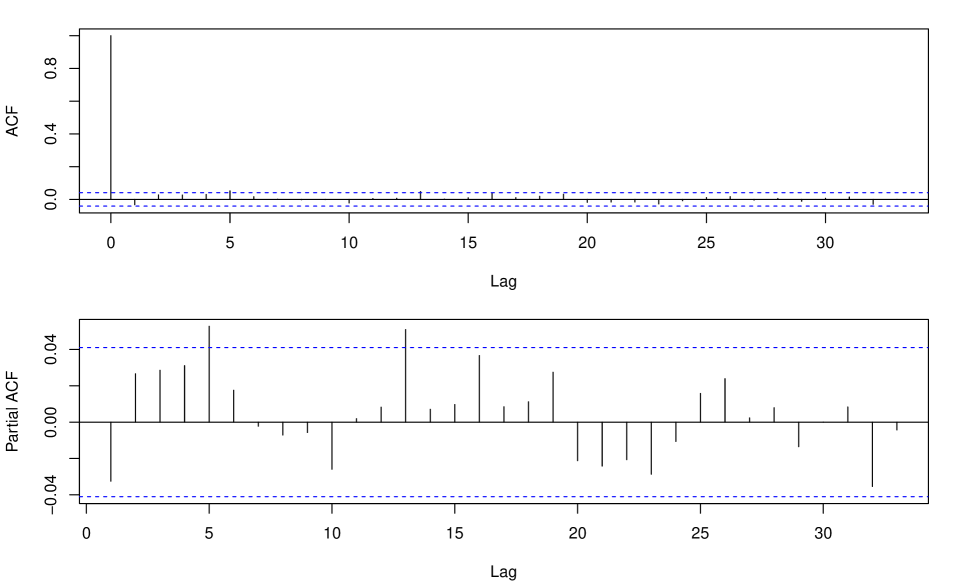

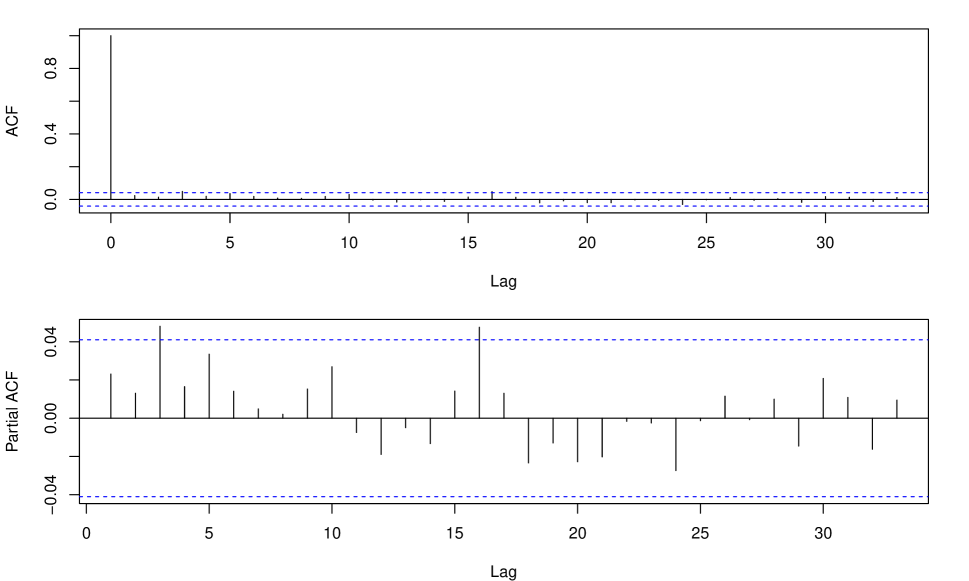

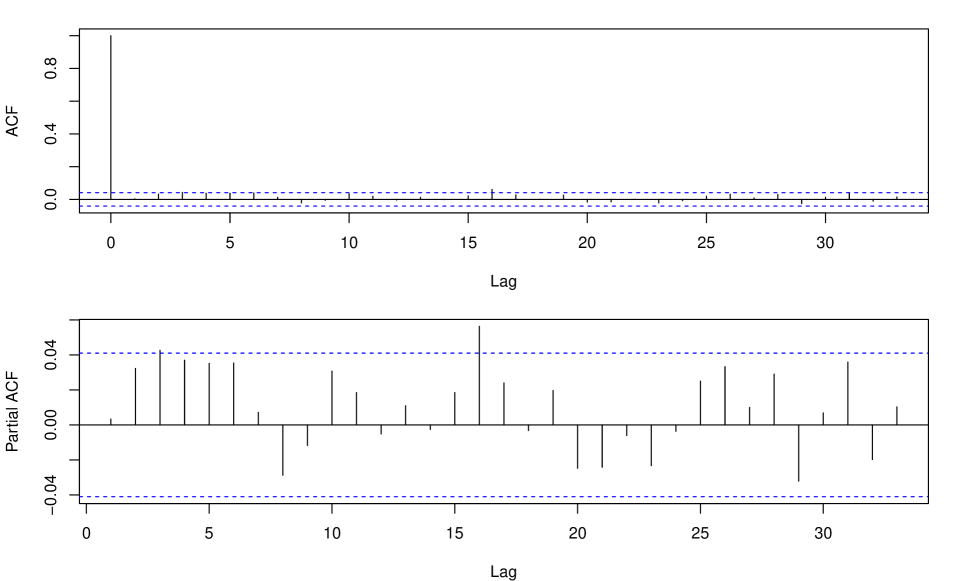

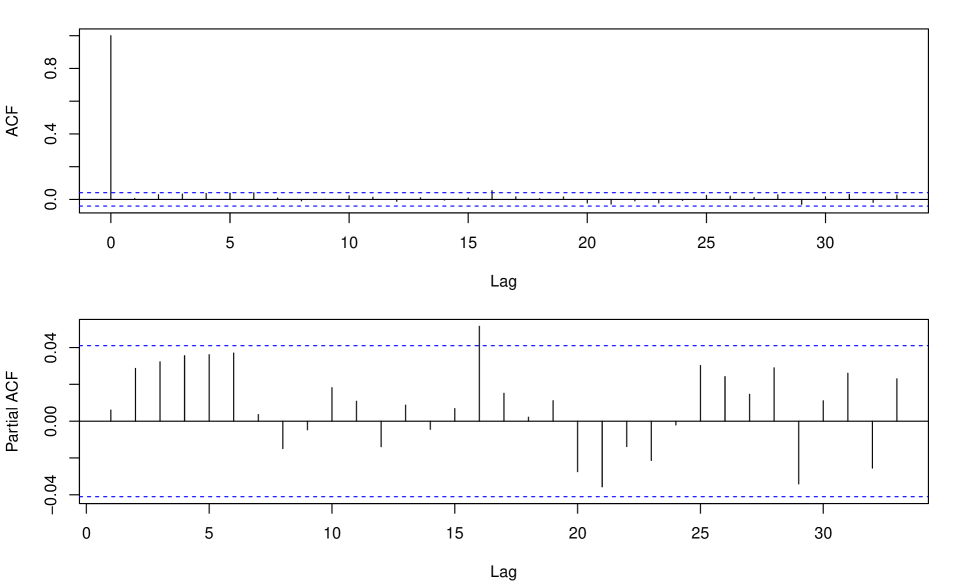

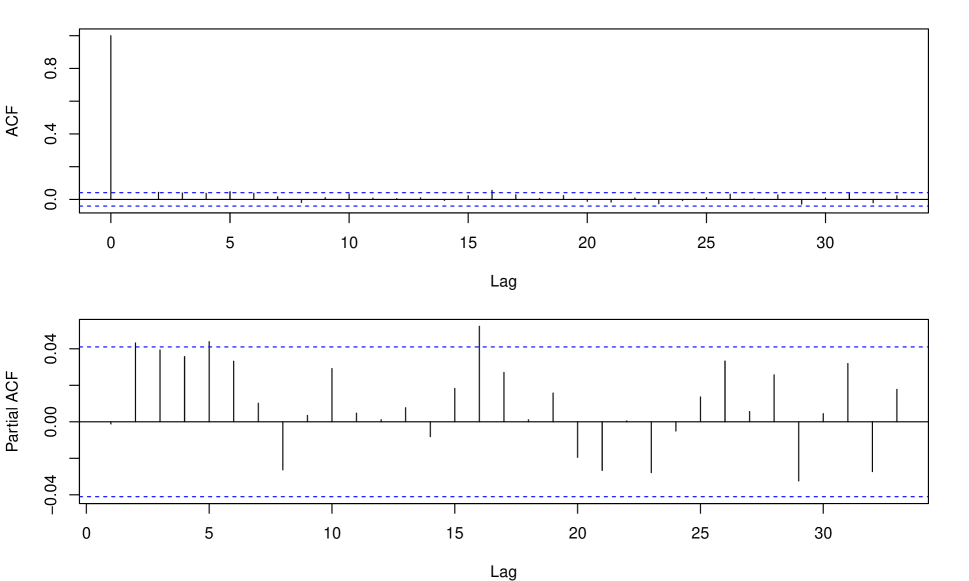

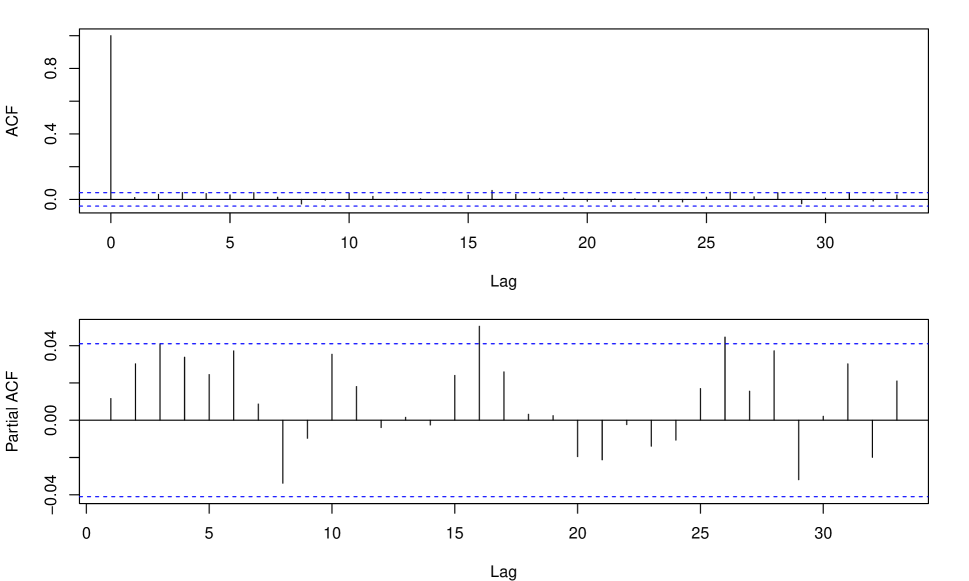

All time series exhibit relevant ARCH effects, and the pure ARMA() specification was in all cases not sufficient to pass the considered tests. Moreover, a symmetric GARCH(P,Q) specification seems to be adequate in most cases. An exception is BTC, with significant asymmetric effects causing the necessity of considering GJR-GARCH(P,Q) models for the variance equation. However, in the final model, the -estimates were not significant. Regarding , the estimates of and are significant in all cases, confirming the relevance of a non-normal distribution. Tables B.4 and B.5 further show the AIC and relevant tests of the standardized residuals of the selected models. For comparison, the LB test on the squared standardized residuals is included, which is in line with the WLM test in most cases. In the following, the plots of the autocorrelation functions (ACF) and partial autocorrelation functions (PACF) of the standardized residuals of the selected models are displayed.

| BTC | ETH | LTC | XMR | XRP | |

| Selected Model | ARMA(2,2)- GJR-ARCH(5) | ARCH(3) | GARCH(1,1) | GARCH(1,1) | GARCH(1,1) |

| 0.0024* (0.0012) | 0.0028* (0.0011) | 0.0019 (0.0010) | |||

| -0.0043 (0.0036) | |||||

| 0.9846* (0.0035) | |||||

| 0.0162* (0.0003) | |||||

| -0.9759* (0.0000) | |||||

| 0.0005* (0.0001) | 0.0020* (0.0003) | 0.0000 (0.0000) | 0.0002* (0.0001) | 0.0002* (0.0000) | |

| 0.1524* (0.0610) | 0.3246* (0.0720) | 0.0890* (0.0109) | 0.1669* (0.0302) | 0.2295* (0.0360) | |

| 0.0771 (0.0452) | 0.2498* (0.0605) | ||||

| 0.1236* (0.0501) | 0.2063* (0.0590) | ||||

| 0.3485* (0.0835) | |||||

| 0.2230* (0.0724) | |||||

| 0.1687 (0.0935) | |||||

| 0.0711 (0.0674) | |||||

| 0.0442 (0.0747) | |||||

| -0.0400 (0.1031) | |||||

| -0.0935 (0.0815) | |||||

| 0.9100* (0.0115) | 0.8045* (0.0291) | 0.7695* (0.0342) | |||

| 0.979* (0.0232) | 1.0426* (0.0268) | 1.0426* (0.0226) | 1.0141* (0.0294) | 1.0694* (0.0227) | |

| 3.0091* (0.1624) | 3.0941* (0.2385) | 3.4214* (0.1823) | 3.6145* (0.2881) | 2.9867* (0.1567) | |

| AIC | -9092.8599 | -6975.8293 | -7839.1305 | -7031.3708 | -7519.3082 |

| -val.: LB | 0.0524 | 0.0635 | 0.3947 | 0.0656 | 0.1635 |

| -val.: LB2 | 0.0202* | 0.1608 | 0.9881 | 0.3693 | 0.9070 |

| -val.: WLM | 0.5244 | 0.2693 | 0.9923 | 0.4216 | 0.9117 |

| -val.: SB | 0.5536 | 0.2434 | 0.7885 | 0.7513 | 0.0916 |

| -val.: Neg. SB | 0.4161 | 0.4363 | 0.5272 | 0.1465 | 0.9266 |

| -val.: Pos. SB | 0.1552 | 0.8325 | 0.4973 | 0.6267 | 0.5489 |

| -val.: Joint SB | 0.4202 | 0.5247 | 0.8075 | 0.4924 | 0.1243 |

| Sys:BTC | Sys:ETH | Sys:LTC | Sys:XMR | Sys:XRP | |

| Selected Model | GARCH(1,1) | GARCH(1,1) | GARCH(1,1) | GARCH(1,1) | GARCH(1,1) |

| 0.0052 (0.0034) | 0.0052 (0.0030) | 0.0071* (0.0032) | 0.0055 (0.0028) | 0.0088* (0.0033) | |

| 0.0018* (0.0005) | 0.0010* (0.0003) | 0.0018* (0.0005) | 0.0008* (0.0003) | 0.0015* (0.0004) | |

| 0.1649* (0.0322) | 0.1452* (0.0266) | 0.1683* (0.0337) | 0.1521* (0.0247) | 0.1367* (0.0264) | |

| 0.8223* (0.0299) | 0.8538* (0.0257) | 0.8152* (0.0318) | 0.8469* (0.0248) | 0.8435* (0.0260) | |

| 0.9446* (0.0267) | 0.9538* (0.0265) | 0.9404* (0.0260) | 0.9517* (0.0255) | 0.9363* (0.0265) | |

| 3.5653* (0.2926) | 3.3996* (0.2448) | 3.4711* (0.2838) | 3.5796* (0.2523) | 3.6289* (0.3025) | |

| AIC | -1667.4989 | -2109.0873 | -1972.6166 | -2114.0524 | -1955.2041 |

| -val.: LB | 0.0197* | 0.0625 | 0.0085* | 0.0290* | 0.0184* |