Modified Method of Moments

for Generalized Laplace Distribution

Abstract.

In this note, we consider the performance of the classic method of moments for parameter estimation of symmetric variance-gamma (generalized Laplace) distributions. We do this through both theoretical analysis (multivariate delta method) and a comprehensive simulation study with comparison to maximum likelihood estimation, finding performance is often unsatisfactory. In addition, we modify the method of moments by taking absolute moments to improve efficiency; in particular, our simulation studies demonstrate that our modified estimators have significantly improved performance for parameter values typically encountered in financial modelling, and is also competitive with maximum likelihood estimation.

Keywords: Variance-gamma distribution; method of moments; parameter estimation

1. Introduction

1.1. Generalized asymmetric Laplace (variance-gamma) distributions

In recent decades, a family of generalized asymmetric Laplace (GAL), or variance-gamma (VG) distributions has gathered the attention of researchers. A random variable with distribution from this family has characteristic function (Fouier transform)

| (1) |

Here, are real-valued parameters, with restrictions . The probability density function (PDF) is known and involves the modified Bessel function of the second kind; see equation (3) for an expression in the case . This family was introduced (for the case ) into the financial literature in a seminal work of [16] under the name variance-gamma and later independently in [13] under the name generalized asymmetric Laplace; see a more detailed exposition of a multivariate version in [14]. The class of asymmetric Laplace distributions was studied in the book [12], which also mentions GAL; see also [6] for an up to date review. This random variable has moments of all orders, and finite moment generating function (MGF) for in a neighborhood of zero. Its tails are heavier than Gaussian. It can be represented as a mean-variance Gaussian mixture:

| (2) |

where the density of the distribution is , . In addition, the GAL distribution is infinitely divisible: For each we can represent (on a certain probability space), where are independent and identically distributed. Moreover, each has a distribution which belongs to the same family, with changed parameters. Thus we can create a Lévy process with increments distributed as GAL. This is called Laplace motion, [19]. From (2), we can derive that this process can be represented as a Brownian motion (with non-trivial drift and diffusion) subordinated by a gamma process : . These properties make this family valuable for financial modeling, as in [20]; see applications to option pricing in [15] and fitting financial data in [21].

1.2. Estimation methods

Parameter estimation, however, remains difficult for the variance-gamma distribution. A direct maximum likelihood estimation (MLE) is computationally difficult because of the presence of the modified Bessel function of the second kind in the density formula for GAL; see various methods in the thesis [25] and a similar approach to autoregressive models in [17]. Representation as in (2) opens the door for expectation-maximization algorithms (EM). The thesis [25] contains several estimation methods which are modifications of MLE.

1.3. Method of moments estimation

In some literature, perhaps the simplest method was used: method of moments estimation (MME). For example, we compute the first 4 moments of the variance-gamma distribution. We solve the resulting system of equations explicitly. This gives us an expression of parameters via moments. Finally, we substitute empirical moments in place of exact ones. This gives us parameter estimators. See [24] for MME and generalizations for VG distributions. In addition, [21] obtains MME for skewness parameter approaching zero, and removing terms of order and higher from expressions of moments.

It is straightforward to show that these estimators are consistent (converge to the true values as the sample size tends to infinity) and asymptotically normal: as , where is the limiting covariance matrix. However, these estimators are not efficient: The variances in this limiting matrix are larger than the variances for the MLE.

In several articles, the MME is mentioned for estimation of these distributions and related time series models. This gives an impression that MME is acceptable for parameter estimation for these families. However, this question has typically been addressed with applications to financial modelling in mind with quite specialized parameter values considered. To the best of our knowledge, no rigorous simulation or theoretical study has been conducted to study actual applicability and to quantify errors for this method across the full range of parameter values that may appear in applications. This note fills this gap in the symmetric case.

1.4. Our contributions

In this article, we focus on the symmetric variance-gamma (generalized Laplace) distribution, where in (2). Through theoretical results and a simulation study, with comparison to the classic MLE, we test the performance of MME, finding performance is often unsatisfactory.

Next, we modify MME to improve efficiency. Specifically, the location parameter is estimated using the empirical mean. Then, we take the first absolute moment and the standard deviation . We find their expression using parameters. Their ratio depends only on the shape , not on scale or location . Through our simulation study, we demonstrate that this method improves on the original MME (in terms of lower bias and mean square error) across a broad range of parameter values of and . Of particular note is that performance is significantly improved for parameter values encountered in financial modelling, the most common application of the variance-gamma distribution.

We also compare this modified MME to the classic MLE. As expected, for most parameter constellations MLE outperforms our modified MME (in terms of smaller bias and mean squared error), although our modified MME is still quite competitive, and much more so than classic MME. We also remark that MLE is difficult to implement in practice; see [4] for an investigation of the computational problems associated with implementing MLE for parameter estimation for the variance-gamma distribution.

1.5. Organization of this article

Section 2 is devoted to the classic MME. We take the symmetric VG distribution, and state and prove asymptotic results and use them together with simulations to assess the performance of this MME. Section 3 studies the modification of this MME with absolute moments for symmetric VG distributions. It is here that we make the main positive contribution of this note. We perform the simulations both in case and in the more realistic setting when is unknown. Section 4 contains conclusions and some suggestions for subsequent research. Proofs are postponed until Appendix A.

2. Classic Method of Moments Estimation

First, we define the family of distributions which we deal with. As discussed in the Introduction, we deal with a subset of the GAL family: symmetric variance-gamma (SVG) or generalized Laplace. We show the classic MME performs poorly for these distributions. The SVG distribution corresponds to setting in (1), and we have the following formula for the PDF:

| (3) |

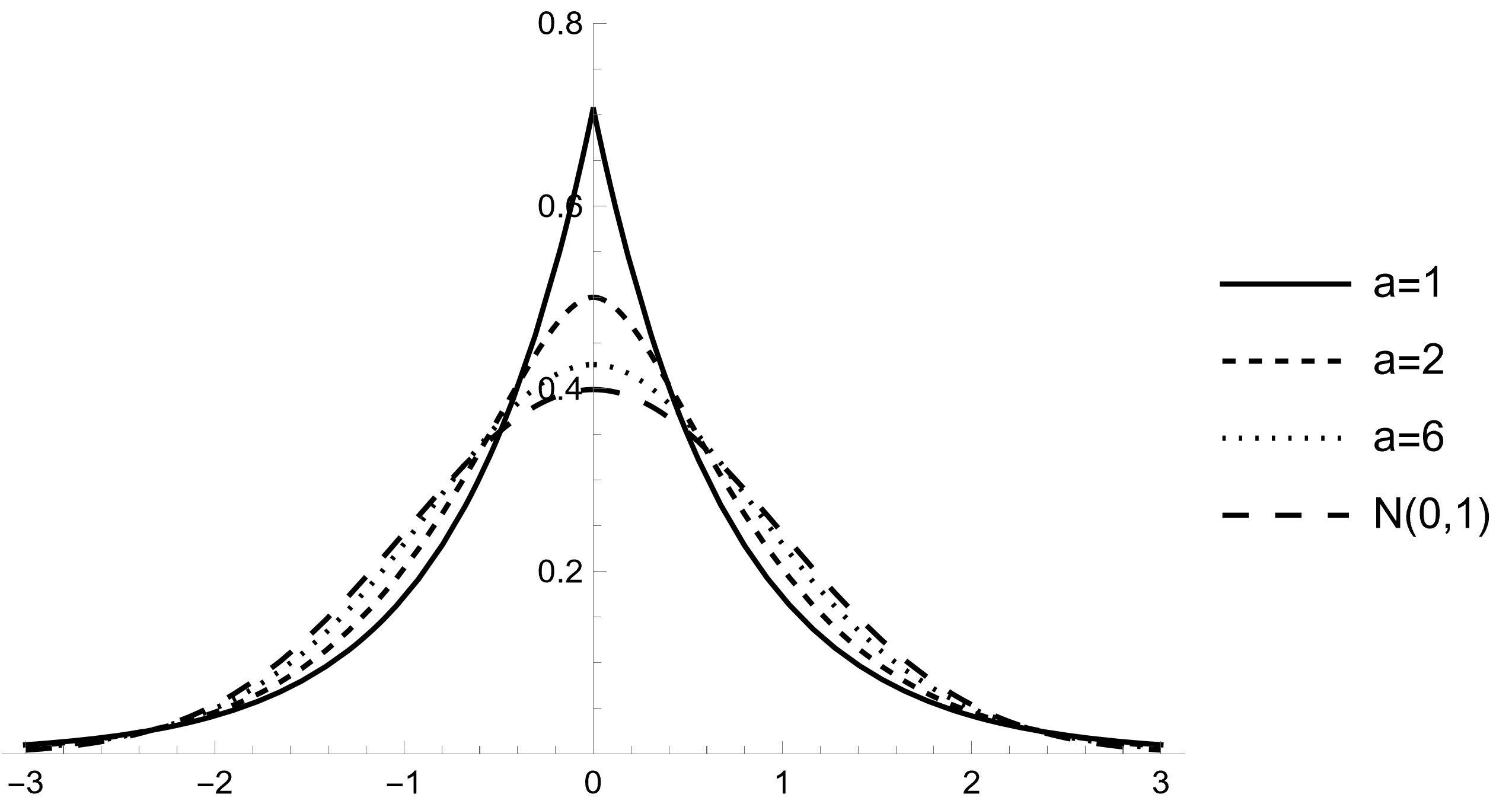

where , , is a modified Bessel function of the second kind [18]; note that this function is sometimes also referred to as the modified Bessel function of the third kind. A plot of the PDF for several parameter values is given in Figure 1. The parameterisation (3) is very similar to those given by [2, 8, 12], whilst the parametrisation of [5] (similar to that of [15]) is obtained via , and . When , the PDF (3) reduces to that of the classical Laplace distribution (see [12]). The parameter is the location parameter. Since the distribution is symmetric around , this is the mean and the median. In addition, this is the (only) mode: The symmetric variance-gamma distribution is unimodal. The parameter is the shape parameter. As increases, the distribution becomes more rounded around its peak value . For example, it is differentiable at for . For , the density behaves as as : continuous, but not differentiable. Next, the density has a logarithmic singularity at if and a power singularity if . The parameter is the scale parameter, and as decreases the tails decay more quickly. A recent article [9] has precise statements and proofs of these asymptotic results.

Remark 1.

As , the symmetric variance-gamma distribution converges weakly to the normal distribution if we scale the parameter as . This easily follows from the convergence of characteristic function given in (1) to the characteristic function of the normal distribution .

The SVG distribution has a fundamental representation in terms of gamma and normal random variables (see [12, Proposition 4.1.2]). Fix parameters . Then a SVG random variable can be written as

| (4) |

where and are independent.

Of course, all centered odd moments are zero: for . With the representation (4), moments of the SVG can be calculated using standard formulas for the moments of the gamma and normal distributions (see [12, Proposition 4.1.6]). In particular, the variance and fourth central moment are

| (5) |

With the formulas in (5), we can develop a classic method of moments. We shall show it is consistent and asymptotically normal, but with large asymptotic variance. Assume are i.i.d. from this variance-gamma distribution (4). Define the empirical second and fourth moments:

| (6) |

Theorem 1.

The MME estimators are given by

| (7) |

They are consistent: almost surely as .

Remark 2.

In (6), we have used the naive moment estimators rather than the unbiased ones; for example, multiplication of by a factor of yields an unbiased estimator of variance. We note, however, that our use of the naive estimators will have only a negligible effect for the purposes of this article, as, by the Slutsky theorem, this slight changes preserves consistency and asymptotic normality, and does not change limiting covariance matrix of the estimators. Also, for our simulation studies, we take a sample size of , for which there is little difference in performance between the naive and unbiased estimators.

Remark 3.

The moment estimators of Theorem 1 do not satisfy support constraints on the parameters, because, for given data, we do not necessarily have . This condition is of course met (with high probability; see Lemma 2 below) for large sample sizes, because the estimators are consistent and . The fact that method of moments estimators do not always satisfy support constraints is a well-known deficiency of the method; we also remark that our simulation results suggest that classical MME is not suitable for small sample sizes (when there is a possibility of the support conditions being violated).

Lemma 2.

There exists a constant , dependent upon and , such that

The theoretical result of Lemma 2 is complemented with a simulation study that gives estimates on the probability of the support condition being met (in the case of unknown ); see Table 3 below.

Remark 4.

For the normal distribution, we have . In light of the Remark 1, we can expect that with high probability, we cannot apply the MME for large . We will see later in simulations that, in general, the MME works better for smaller .

As we shall see, the limiting variance of each estimator is rather large. To illustrate this, let us consider a special case, where, without loss of generality, we have . Then we can modify the estimators (6) for and :

| (8) |

Remark 5.

Below, we always add primes to empirical moments if we do NOT subtract the empirical mean . However, for empirical centered moments, where we do subtract , we do not add primes.

We plug (8) into formulas (7) for and and get consistent estimators for and . Below we state an asymptotic normality result. We note that in our result we are able to give an explicit formula for the limiting covariance matrix; we should, however, point out that the asymptotic covariance matrix of the MLE is complicated and, to our best knowledge, an explicit formula is not available in the literature.

Theorem 3.

Assuming , the modified estimators from (8) are asymptotically normal:

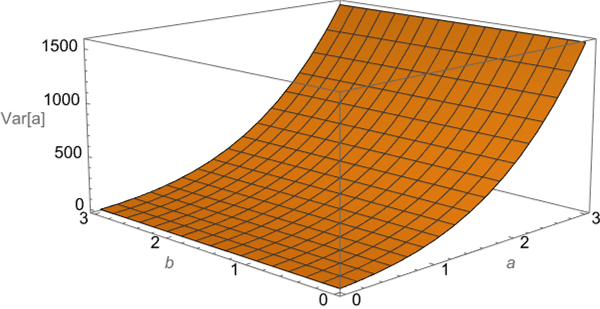

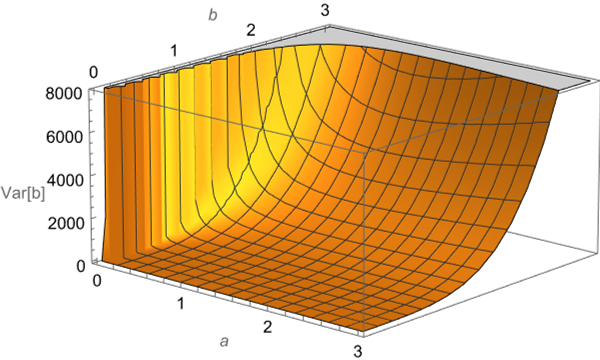

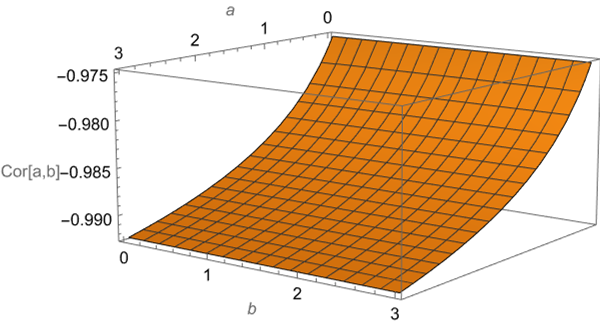

A plot of the entries in the covariance matrix are given in Figures 2 and 3. It can be seen that the variance of the estimator get large as increases, whilst the variance of the estimator becomes large as increases. This means estimators and may often be of poor quality, particularly for moderate sample sizes or for larger values of and .

Example 1.

Take . Then

For example, if , then the standard deviation of the estimator is . This implies that the estimator is of low quality. Note also that the limiting correlation is , which is very strong.

We now state an asymptotic normality result for the more realistic case of unknown .

Theorem 4.

Remark 6.

The limiting covariance matrix is block diagonal. Therefore, asymptotically, the estimators for and the empirical mean are independent.

In addition, we performed simulations to assess the quality of the MME (7): Fix and repeat times the following procedure. We implemented the procedure in Mathematica.

-

(1)

Repeat times the following procedure:

-

•

Generate a symmetric variance-gamma sample of variables with .

-

•

Compute estimates from (7).

-

•

Denote them to be for the th iteration.

-

•

-

(2)

Find the average over all estimates and .

-

(3)

Find mean squared errors and .

The results are reported in Table 1. We chose a wide range of parameter values, under which the SVG distribution exhibits quite different behaviour. Indeed, as mentioned above, () corresponds to a power law (logarithmic) singularity in the PDF at , whilst corresponds to the classical Laplace distribution, and for the distribution becomes increasingly rounded about the peak. Similarly, we consider various different orders of magnitude for the scale parameter . Later, we repeat the simulations in the more realistic setting, where the true value of the location parameter is unknown.

As a means of comparison, we repeated the simulations using classic MLE. In order to calculate the MLE, we used the Nelder-Mead algorithm, as implmented in the R function optim. For the evaluation of the log-likelihood function, we used the dvg function delivered by the R VarianceGamma package. In order to avoid the singularity of the density and negative values for the parameters, we set or equal to when the Nelder-Mead algorithm wants to evaluate the log-likelihood function at negative parameter values, and similarly we set the variables and equal to as soon as they are smaller than . The results are reported in Table 2.

From Table 1, we infer that for small values of and the performance of the estimators in terms of bias and MSE is quite reasonable. In fact, in our finite sample simulation, when , the MSE of the moment estimator is smaller than the MSE for the corresponding MLE estimator for all values of except . This good performance for small , is consistent with results in the literature in which MME has been used to fit the variance-gamma distribution to financial data, like log returns of assets prices over many () trading days; see, for example [21] in which values of the order and were considered. Indeed, when fitting the VG distribution to log returns of financial assets, very small values of and values of are typically encountered. However, as the values of and increase, we see that the performance of the classic MME degrades. We see that the MSE of the moment estimator when is now significantly larger than for the MLE. We found that this gets worse as increases beyond . We therefore conclude, that whilst performance of the MME in terms of bias and MSE is quite reasonable for some of the specialised values of and that have been tested on some financial data sets, for other values of and performance deteriorates, meaning that the performance of the method is quite sensitive to the true values of model parameters. We do, however, note that as becomes larger, the SVG PDF approaches that of the normal distribution (see Remark 1 and Figure 1), and so for practical purposes the differences in performance between classic MME and MLE for may not be as great as suggested by our simulations.

3. Modified Method of Moments

3.1. Main idea

Define the absolute centered moment . The following formula for was stated and proved in [9, Proposition 2.2]:

| (9) |

Knowing and , we can solve for :

Taking logarithms, we get:

Lemma 5.

The function is a one-to-one strictly decreasing smooth mapping from onto , with for .

3.2. Centered case

First, assume that we know the mean (and median) is zero. Then we no longer have to subtract the empirical mean from each observation. This makes proofs of consistency and asymptotic normality for this case easier, and they serve as stepping stone for proofs in the general case.

Centrality seems like an artificial restriction. However, this special case also arises in practice. For example, consider linear regressions with residuals with heavier than Gaussian tails. For said residuals, one could fit symmetric variance-gamma distributions. However, by construction residuals have zero mean, since a regression has an intercept, which is an additive constant.

In the next subsection, we consider the general case. Meanwhile, here we used simplified estimators for the first absolute moment and the second moment (which is equal to the variance).

We can estimate from (9) as

| (10) |

The estmate of is given in (8). Lemma 5 allows us to estimate as follows: We can define the inverse function

to . It is continuous and smooth. Thus we can define the estimators for and :

| (11) |

Theorem 6.

The estimators in (11) are consistent and asymptotically normal.

Remark 7.

The covariance matrix for the asymptotic normal distribution in Theorem 6 is not explicit, and so is not reported.

As for any MME, the feasibility question arises. We have a result similar to Lemma 2 above.

Lemma 7.

There exists a constant , dependent upon and , such that the modified MME can be, in fact, applied with probability at least :

Remark 8.

The MLE for the (centered) symmetric Laplace distribution , , is just our modified MME: It uses only , since this is a one-parameter family of distributions. Classic MME uses only classic moments . Modified MME uses . The classic MME for this symmetric Laplace family will use . The resulting estimate is consistent and asymptotically normal, but not efficient. This observation is a motivation for using the modified MME for generalized symmetric Laplace (symmetric variance-gamma) distributions.

Example 2.

We now compute the asymptotic variance for the estimators (11) in the case , to compare it with the classic MME. First, in this case and , therefore and . Using Python, we compute and therefore . Next, the gradient of the function (the first component of ) is equal to . At and this is equal to . Thus the gradient of the function is equal to . The Jacobi matrix of the function at and has first row equal to . The second row can be computed similarly:

From (29), we have

By the delta method, the limiting covariance matrix is

Both limiting variances are smaller than those in Example 1. To be fair, the limiting correlation is still , which is very strong. This is perhaps to be expected since .

3.3. General case

Now, we drop the assumption that . We have the obvious estimator for the location parameter . We subtract this from each observation to modify the estimator from (10) of the absolute first moment:

| (12) |

For empirical variance, we use from (6):

We create estimators from just like in (11).

Theorem 8.

The estimators are consistent and asymptotically normal. The limiting covariance matrix is , where is the limiting covariance matrix from Theorem 6.

We have the following analogue of Lemma 7 for the case where is unknown. Simulations were used to estimate the probability that , with the results reported in Table 3. We see similar behaviour for the probabilities for both the classic and modified MME estimates, although the probability of the classic moment estimators existing is greater than for the modified MME. Note that these simulations have been performed on small sample sizes; for a sample size of (for the parameter values we considered) the estimators exist with very high probability.

Lemma 9.

There exists a constant (possibly different from the one in Lemma 7), dependent upon and , such that the modified MME can be, in fact, applied with probability at least :

Remark 9.

Similarly to Remark 4, we can note that for any normal distribution, and . Thus . In light of Remark 1, we can expect that the modified MME (similarly to the classic MME) is impossible to apply with higher probability for larger . Simulations below show that, indeed, the modified MME works better for smaller .

Remark 10.

As in Theorem 4, the covariance matrix is block diagonal, and therefore, asymptotically, the estimators for and the empirical mean are independent.

| 0.25 | 0.01 | 0.723 | 0.954 | 0.999 | 0.817 | 0.976 | 1 |

|---|---|---|---|---|---|---|---|

| 0.25 | 0.1 | 0.717 | 0.954 | 1 | 0.812 | 0.975 | 1 |

| 0.25 | 1 | 0.725 | 0.952 | 1 | 0.825 | 0.975 | 1 |

| 0.25 | 5 | 0.72 | 0.951 | 1 | 0.817 | 0.973 | 1 |

| 0.5 | 0.01 | 0.559 | 0.84 | 0.99 | 0.701 | 0.922 | 0.998 |

| 0.5 | 0.1 | 0.568 | 0.847 | 0.989 | 0.718 | 0.926 | 0.998 |

| 0.5 | 1 | 0.568 | 0.848 | 0.99 | 0.708 | 0.924 | 0.998 |

| 0.5 | 5 | 0.557 | 0.849 | 0.988 | 0.704 | 0.923 | 0.999 |

| 1 | 0.01 | 0.412 | 0.687 | 0.927 | 0.572 | 0.801 | 0.97 |

| 1 | 0.1 | 0.421 | 0.682 | 0.915 | 0.583 | 0.79 | 0.964 |

| 1 | 1 | 0.42 | 0.68 | 0.925 | 0.577 | 0.797 | 0.967 |

| 1 | 5 | 0.417 | 0.689 | 0.92 | 0.575 | 0.796 | 0.963 |

| 2 | 0.01 | 0.318 | 0.52 | 0.77 | 0.465 | 0.639 | 0.84 |

| 2 | 0.1 | 0.317 | 0.522 | 0.773 | 0.467 | 0.64 | 0.841 |

| 2 | 1 | 0.317 | 0.518 | 0.772 | 0.474 | 0.637 | 0.838 |

| 2 | 5 | 0.314 | 0.53 | 0.775 | 0.465 | 0.646 | 0.842 |

| 3 | 0.01 | 0.284 | 0.454 | 0.678 | 0.438 | 0.573 | 0.748 |

| 3 | 0.1 | 0.274 | 0.45 | 0.68 | 0.433 | 0.566 | 0.747 |

| 3 | 1 | 0.277 | 0.452 | 0.669 | 0.431 | 0.567 | 0.737 |

| 3 | 5 | 0.278 | 0.449 | 0.67 | 0.432 | 0.565 | 0.746 |

3.4. Simulations

Simulation results for the modified estimators are given in Table 4. We find that, for all values of and considered, the MSEs of the modified MMEs and are reduced, often substantially, compared to the classic MME. In fact, performance is competitive even when compared to the MLE. We do, however, note that as increases, it occasionally happens that the function becomes very flat in the region close to , which leads to a high sensitivity of the numerical procedure used by Mathematica with respect to small changes in the sample. This means that on rare occasions the modified MME fails completely, and gives very poor estimates. We did not exclude these rare very poor estimates from our results.

Overall, we find that the modified MME outperforms, often substantially, classic MME in terms of smaller bias and MSE, and is quite competitive even against MLE. This suggests our modified MME could be an excellent alternative to classic MME for fitting the VG distribution to financial data (for which these parameter values are typically encountered). For other parameter values, performance is often better than for classic MME, but on rare occasions the modified MME fails completely when . Therefore, as with classic MME, caution must be applied when implementing the modified MME.

We also performed simulations for which the true location parameter is unknown. The results are reported in Table 5 (classical MME) and Table 6 (our modified MME). The results can be seen to be very similar to simulation results for known . We remark that the MSE for classic MME for seem to be large in general. Therefore one needs a large number of Monte Carlo repetitions in order to determine the values more precisely and our estimates have to be treated with caution. We again stress that caution is also needed when applying modified MME for , as the numerical procedure may fail. In addition, we report the estimated values of the unknown parameter in Table 7. We see that the performance of this estimator is rather good, and given this good performance it is perhaps to be expected that our simulation results for the estimators and via classic and our modified MME are similar for the cases of known and unknown .

4. Conclusion and Further Research

We tested the classic MME for a symmetric variance-gamma (generalized symmetric Laplace) distribution. Using simulations and the delta method, we showed that caution must be used in implementing this method in practice as performance is often not acceptable. This runs contrary to some remarks in the existing literature, some of which was cited in the Introduction, that may give the impression that MME works across the full range of parameter values for the variance-gamma distribution (and time series models based on it).

However, we also produced positive results. We modified MME for symmetric variance-gamma by switching to the first two absolute moments (mean absolute deviation) instead of regular ones. Our simulation results showed that our modified estimator is more efficient than for the classic MME across a broad range of parameter values, in particular those encountered in financial modelling. However, like classic MME, caution must be used in implementing this modified MME as when performance degrades. Our study suggests using absolute centered moments for other symmetric distributions offers a possibility for improved performance.

A natural question is how to extend this modified MME to the asymmetric variance-gamma (generalized asymmetric Laplace) . It is, however, not so easy to solve the system of equations for these cases, at least not nearly as easily as for symmetric variance-gamma. Indeed, for the asymmetric Laplace distribution (2) with , formulas for the absolute raw moments take a complicated form involving the hypergeometric function (see [10, Theorem 2.1]) and, to the best knowledge of the authors, explicit formulas are not available in the literature for the absolute centered raw moments .

Appendix A Proofs

Proof of Theorem 1. Just solve for and this system of two equations (5):

| (13) |

Next, plug in instead of , and instead of . By the Strong Law of Large Numbers, a.s. and a.s. as . Next, in (13) is a continuous function. Thus we get almost surely .

Proof of Lemma 2. We consider the (open) feasibility set

| (14) |

Therefore, there exists an -neighborhood of . It suffices to show the estimate

But this follows from the estimate (where has the SVG distribution):

| (15) |

and Markov’s inequality (with the defined in (15)):

Proof of Theorem 3. State the Central Limit Theorem for (8):

since are i.i.d. random vectors with finite covariance matrix. Now, let us find the limiting covariance matrix. We have that

| (16) | ||||

Using the representation (4) and standard formulas for moments of gamma and normal random variables, or appealing to [12, Proposition 4.1.6], we have the following formulas for the moments of orders 6 and 8:

| (17) |

Plug these moments (17), together with and from (5), into the matrix from (16):

Finally, let us compute the Jacobian of the function from (13):

| (18) |

Plugging and from (5) into (18), we get:

Applying the bivariate method to , as in [3, Section 5.5], we get the CLT for with limiting covariance matrix .

Proof of Theorem 4. Assume without loss of generality that . There are two facts:

| (19) |

| (20) |

Assuming we proved (19) and (20), let us complete the proof of Theorem 4. Similarly to the proof of Theorem 3, we can get

| (21) |

where the limiting covariance matrix is given by

Its 12 and 13 elements are odd moments. By symmetry of , these are equal to zero. Therefore, the matrix is block diagonal. Its block is

| (22) |

Next, apply the Slutsky theorem to (26). Together with (19) and (20), we conclude that the statement of (21) holds even if we replace with and with . Next, apply the delta method as before to ; or, rather, to the entire with the mapping . The Jacobi matrix is also block-diagonal:

| (23) |

Combining (22) and (23), we conclude that the limiting covariance matrix is block-diagonal as well: . This concludes the proof of Theorem 4.

It remains only to show (19) and (20). First, (19) follows from direct computation: , and the CLT: as . Combining these observations, we get that the left-hand side of (19) behaves asymptotically as . Similarly, (20) follows from expanding , we have:

| (24) |

where we define the empirical average of the th moment:

| (25) |

Applying the CLT to (25) for , and using the symmetry of around , we get:

| (26) |

By the Strong Law of Large Numbers applied to (25), we have:

| (27) |

Combining (24), (26), (27) and applying the Slutsky theorem, we prove (20).

Proof of Lemma 5. Step 1. Let us show that for all . Consider the digamma function . We have that . Applying the two-sided inequality (see [11]) we get the upper estimate:

| (28) |

The derivative of is thus is increasing. Next, as . Thus for all . Combining this observation with (28), we complete the proof that .

Step 2. Let us show that : It follows from convergence

and as .

Step 3. Finally, let us show . Indeed, as , we have

So , thus .

Proof of Theorem 6. We use the same techniques as in the proof of Theorem 3. Namely, we use continuity and smoothness of the mapping

which maps into and similarly into . By the Central Limit Theorem,

| (29) |

where and . Applying the method, we complete the proof.

Proof of Lemma 7. This is very similar to the proof of Lemma 2. The following set is open:

| (30) |

Therefore, there exists an -neighborhood of . It suffices to show the estimate

But this follows from the estimate (where has the SVG distribution):

| (31) |

and the Markov inequality (with the defined in (31)):

Proof of Theorem 8. This is very similar to the proof of Theorem 4. Without loss of generality we assume . There are two facts:

| (32) |

and (19), shown in the proof of Theorem 4. Assuming we proved (32) and (19), let us complete the proof of Theorem 8. Similarly to the proof of Theorem 3, we can get

| (33) |

where the limiting covariance matrix is given by

By symmetry of the distribution of and the fact that , we get: . Therefore, the matrix is block diagonal. Its block is the same as the limiting covariance matrix in (29):

| (34) |

Next, apply the Slutsky theorem to (33). Together with (32) and (19), we conclude that the statement of (33) holds even if we replace with and with . Next, apply the delta method as before to ; or, rather, to the entire with the mapping . The Jacobi matrix is also block-diagonal:

| (35) |

Combining (34) and (35), we conclude that the limiting covariance matrix is block-diagonal as well: . This concludes the proof of Theorem 8.

It remains only to show (32). The first statement follows from [1, Theorem 2.2]. We again apply the simple observation that the SVG distribution is symmetric: its mean and median coincide. In addition, the value of the density function at the mean is strictly positive.

Proof of Lemma 9. Without loss of generality, assume . Consider the -norm

The vector has . For the SVG sample , define the vector . By the Minkowski inequality,

| (36) |

Applying (36) to and , we get:

| (37) |

Recall the notation (30) from the proof of Lemma 7. From (37), there exist and such that if and is in the -neighbourhood of , then , and therefore the modified MME is applicable. We already have an estimate of the type (from the proof of Lemma 7):

| (38) |

We can get another estimate

| (39) |

From (38) and (39) together, we can get the required estimate.

Acknowledgements

We would like to thank the two reviewers and the AE for their constructive comments and suggestions that have lead to a much improved article. AF is funded in part by ARC Consolidator grant from ULB and FNRS Grant CDR/OL J.0197.20.

References

- [1] Gutti Jogesh Babu, C. Radhakrishna Rao (1992). Expansions for Statistics Involving the Mean Absolute Deviations. Annals of the Institute of Statistical Mathematics 44 (2), 387–403.

- [2] Bo M. Bibby, Michael Sørensen (2003). Hyperbolic Processes in Finance. In: Rachev, S. (Ed.), Handbook of Heavy Tailed Distributions in Finance. Elsevier Science, Amsterdam, 211–248.

- [3] George Casella, Roger L. Berger (2001). Statistical Inference, Brooks/Cole, Cengage Learning. Second edition.

- [4] Gian P. Cervellera, Marco P. Tucci (2017). A Note on the Estimation of a Gamma-Variance Process: Learning from a Failure. Computational Economics , 363–385.

- [5] Richard Finlay, Eugene Seneta (2008). Stationary-Increment Variance-Gamma and Models: Simulation and Parameter Estimation. International Statistical Review , 167–186.

- [6] Adrian Fischer, Robert E. Gaunt, Andrey Sarantsev (2023). The Variance-Gamma Distribution: A Review. arXiv:2303.05615.

- [7] Robert E. Gaunt (2013). Rates of Convergence of Variance-Gamma Approximations via Stein’s Method. DPhil Thesis, University of Oxford.

- [8] Robert E. Gaunt (2014). Variance-Gamma approximation via Stein’s method. Electronic Journal of Probability (38), 1–33.

- [9] Robert E. Gaunt (2020). Wasserstein and Kolmogorov Error Bounds for Variance-Gamma Approximation via Stein’s Method I. Journal of Theoretical Probability 33 (1), 465–505.

- [10] Robert E. Gaunt (2023). On the moments of the variance-gamma distribution. Stat. Probabil. Lett. Art. 109884.

- [11] Bai-Ni Guo, Feng Qi (2011). An Extension of an Inequality for Ratios of Gamma Functions. Journal of Approximation Theory 163 1208–1216.

- [12] Samuel Kotz, Tomasz Kozubowski, Krzysztof Podgórski (2001). The Laplace Distribution and Generalizations. Birkhäuser.

- [13] Tomasz J. Kozubowski, Krzysztof Podgórski (2000). A Multivariate and Asymmetric Generalization of Laplace Distribution. Computational Statistics 15, 531–540.

- [14] Tomasz J. Kozubowski, Krzysztof Podgórski, Igor Rychlik (2013). Multivariate Generalized Laplace Distribution and Related Random Fields. Journal of Multivariate Analysis 113, 59–72.

- [15] Dilip B. Madan, Peter P. Carr, Eric C. Chang (1998). The Variance Gamma Process and Option Pricing. European Finance Review 2, 79–105.

- [16] Dilip B. Madan, Eugene Seneta (1990). The Variance Gamma Model for Share Market Returns. The Journal of Business 63, 511–524.

- [17] Thanakorn Nitithumbundit, Jennifer S. K. Chan (2020). ECM Algorithm for Auto-Regressive Multivariate Skewed Variance Gamma Model with Unbounded Density. Methodology and Computing in Applied Probability 22, 1169–1191.

- [18] Frank W. J. Olver, Daniel W. Lozier, Ronald F. Boisvert, Charles W. Clark. (2010). NIST Handbook of Mathematical Functions. Cambridge University Press.

- [19] Krzysztof Podgórski, Jörg Wegener (2011). Estimation for Stochastic Models Driven by Laplace Motion. Communications in Statistics – Theory and Methods 40, 3281–3302.

- [20] Wim Schoutens (2003). Lévy Processes in Finance. Wiley.

- [21] Eugene Seneta (2004). Fitting the Variance-Gamma Model to Financial Data. Journal of Applied Probability 41A, 177-–187.

- [22] Elias M. Stein, Rami Shakarchi (2003). Complex Analysis. Princeton University Press.

- [23] Lishamol Tomy, Kanichukattu Korakutty Jose (2009). Generalized Normal-Laplace AR Process. Statistics & Probability Letters 79, 1615–1620.

- [24] Annelies Tjetjep, Eugene Seneta (2006). Skewed Normal Variance-Mean Models for Asset Pricing and the Method of Moments International Statistical Review 74, 109–126.

- [25] Fan Wu (2008). Applications of The Normal Laplace and Generalized Normal Laplace Distributions. Ph.D. Thesis. University of Victoria.