chapter [0em] \thecontentslabel \contentspage \titlecontentssection[1.72em]\thecontentslabel. \titlerule*[1.2pc].\contentspage

Option Volume Imbalance as a predictor for equity market returns

Abstract

We investigate the use of the normalized imbalance between option volumes corresponding to positive and negative market views, as a predictor for directional price movements in the spot market. Via a nonlinear analysis, and using a decomposition of aggregated volumes into five distinct market participant classes, we find strong signs of predictability of excess market overnight returns. The strongest signals come from Market-Maker volumes. Among other findings, we demonstrate that most of the predictability stems from high-implied-volatility option contracts, and that the informational content of put option volumes is greater than that of call options.

Keywords: Options; Implied Volatility; Informational Role of Option Volume; Market Prediction; Market Microstructure; Signal Analysis; Quantitative Trading Strategies; Options Applications

1 Introduction

Since the opening of the CBOE in 1973, derivative markets have been a prominent presence in the financial system, and have grown rapidly ever since. According to BIS estimates [Bank for International Settlements, 2021], the total global nominal amount outstanding for derivatives for the second half of 2020 amounts to USD 582 tn of which 7 tn are equity-linked Options111By comparison the global total GDP was estimated by the World Bank to be USD 88 tn [World Bank, 2021].. The latter is accounted for by multiple option exchanges across the world, including CBOE, the CME group, Nasdaq, and Eurex. Equity options are appealing to traders due to the higher leverage they offer, as well as the absence of restrictions such as the uptick rule. The limited downside risk of a long put position as opposed to a short futures position in the stock, and the hedging opportunities, are also attractive to investors.

Naturally, derivative markets are strongly intertwined with the spot markets. It has been argued that, due to informed trading, option markets lead the spot market (e.g [Black, 1975]). In particular, an interesting line of research is concerned with the information content of signed option volumes. A trader who (either from private information or by using predictive models) expects a spot-price rise can take a long call position or a short put position, while a trader who takes a short call position or a long put position may expect a price fall instead. Therefore, aggregating the signed volumes into these two categories of positive and negative signals yields a metric of the discrepancy in trader anticipation. Our main question is whether this discrepancy can act as a predictor for the direction of future price movements in the spot market.

To this end, we consider a decomposition of the trade flow into positive and negative “signals” (defined below), and use their normalized difference as a predictor for future stock returns. We refer to this metric as the Option Volume Imbalance (OVI). We employ two data sets, from the NOM and PHLX option exchanges, which dis-aggregate the daily option volume into 10-minute buckets, distinguishing between five different market participants and between call and put options. Although our analysis simply makes use of the aggregate volumes rather than, say, order book data, it still yields significant results.

Similar research usually uses either customer data or generally non-market maker data, without distinguishing between classes of market participants. In this paper, a special emphasis is placed into the decomposition between different classes of traders (or market participant classes), and especially that of Market Makers. While this may create an instance of double counting orders for both sides of a trade, it provides an insight on how the same transactions can be used from different angles, to provide trading signals of varying performances. Furthermore, this shows that on a purely speculative level, only certain classes can produce a positive signal under this analysis. If for example Customers are at least partially successful in their speculative ability, this should translate into a financial signal that produces positive returns. On the other hand, Market Makers who profit in other ways (e.g spreads) would not be expected to provide a positive signal, but rather a negative one, reflecting the speculative ability of all those who trade with them.

Furthermore, we empirically assess how the predictive power of OVI varies based on different values of the options’ Greeks, and other characteristics. We compare the two different exchanges, and provide a qualitative description of certain intraday patterns we observe. Lastly, we investigate the cross-sectional effects of this metric, by modeling the interactions across the various assets using a directed network.

Throughout the paper, we use the cumulative Profit and Loss (P&L) and Sharpe Ratio as measures of predictability in future returns. However, as we consider multiple types of OVI (e.g different market participants), we also wish to consider their total predictive power. This motivates us to formulate a novel regression approach which directly maximizes the cumulative P&L, which we refer to as P&L regression. Unlike other research of this type, which usually tests the relationship between covariates and future returns by considering or values, our approach is not limited to linear relationships and can deal effectively with correlated features. We summarize our main contributions as follows.

As a secondary theme, we also consider a short high-level overview of the two markets, showing how most of the activity comes from Market Makers and Customers. We also provide an approximation of how option volume flows between the different market participants.

Paper outline

The remainder of the paper is organized as follows. In Section 2 we give an overview of related literature, and define the Option Volume Imbalance metric (OVI). In Section 3, we describe the data sets used in our analysis. In Section 4, we discuss the evaluation methods used subsequently. In Section 5, using volumes from different market participants, we show the predictive power of the OVI for the future returns in the spot market. In Section 6, we see the effects of various option features, such as the Greeks, on the predictive power of the OVI metric. In Section 7, we extend our analysis by comparing the two data sets (from different exchanges), we consider results for longer time horizons as well as some intraday variants of the OVI-based strategies. In Section 7.4, we check for cross-impact effects, using a network model. Lastly, we summarize our conclusions and detail future research directions in Section 8. Additional numerical results are deferred to the Supplementary Material.

2 Motivation and the Option Volume Imbalance

2.1 Related literature

Traditionally, derivative markets have been used for hedging purposes, and have been shown to play a role in reducing the risk of portfolios. However, the high leverage offered by options has led to the suggestion that they play an additional role as an avenue for informed trading ([Black, 1975] and [Grossman, 1977]). A theoretical model was provided by [Easley et al., 1998], showing that under certain reasonable conditions, informed traders choose to capitalize on their private information by trading in both the stock and the options market. Under this model, informed trading is more prevalent when the liquidity and leverage of the option markets are sufficiently high. Furthermore, under [Biais and Hillion, 2015]’s model, the introduction of options reduces the informational efficiency of the market, making it harder for market makers to distinguish the information content of trades, as the option market becomes a more attractive avenue for informed traders.

The early empirical investigation [Manaster and Rendleman, 1982], focused on the opportunity signals appearing whenever implied option prices from the Black-Scholes (BS) model differed significantly from observed prices, speculated that there was information in the option prices not reflected in the stock markets. This was extended by [Bhattacharya, 1987] to intraday prices, with a pseudo-American BS model for the implied options, supporting and extending the results of [Manaster and Rendleman, 1982]. They used a number of different holding periods for equities, with most intraday strategies resulting in losses due to transactions costs, even though they do report profits in the overnight holding case.

Under the sequential information arrival model of [Copeland, 1976], volumes can be used as a proxy for the rate of information arrival. Based on that, [Anthony, 1988] showed that call volumes lead stock volumes, which indicates the presence of informed traders in the options market. Challenging these results, [Stephan and Whaley, 1990] showed empirically that the stock market leads the option market by at least 15 minutes, rather than vice versa. It was observed by [Easley et al., 1998] that, while price changes in the stock market lead the option volumes, as articulated by [Stephan and Whaley, 1990], the results are quite different if one aggregates volumes into positive (call buys and put sells) and negative (call sells and put buys) flows. They rejected the hypothesis that these aggregated volumes hold no information about the spot market. This led to research based on option flow volume or option imbalance, i.e. features proportional to the difference between volumes corresponding to positive and negative flow.

One of the most important studies focusing on the decomposition to positive and negative flows, was [Xiaoyan et al., 2008], who showed that the signed option volume, (which they referred to as demand for volatility) was correlated with the realized volatility, and that market makers responded to imbalances by raising the spreads, in order to shield themselves from informed traders. According to the findings of [Schlag and Stoll, 2005], signed option volumes have some predictive power of short-term returns, which however reverse at longer timescales, in contrast to the predictive power they found in futures. Later on, [Pan and Poteshman, 2006] used put/call ratios from the opening of new buyer-initiated options, and showed their predictive power for future stock returns. They concluded that the source of predictability was primarily informed trading, by differentiating between publicly and non-publicly available data. Furthermore, they showed that deep out-of-the-money options had the highest predictive power, as well as data that came from customers who traded using full-service brokerage houses; in contrast, firm proprietary trades had no predictive power.

Another option volume flow metric was defined by [Hu, 2014], who used delta-adjusted volumes and showed its significant predictive power for stock returns. The sign of the resulting coefficients did not reverse for longer horizons, as also observed earlier by [Pan and Poteshman, 2006]. Furthermore, they found that the predictability of future returns is stronger for assets with a higher ratio of informed traders, low analyst coverage, large bid-ask spreads, small market capitalization, and low institutional ownership.

Another promising metric proposed was the Option to Stock volume ratio (O/S), first constructed by [Roll et al., 2010], who concluded that the cross-sectional and time-series variation of this metric reflected the presence of informed trading. The predictive power of this metric for future returns was empirically verified by [Johnson and So, 2012], and was shown to be stronger when short-sale constraints were higher. [Ge et al., 2016] compared the different signed option volumes by using the O/S ratio and concluded that there was no significant difference in predictive power between long and short positions, thereby speculating that the source of predictability was the embedded leverage common to the two positions, while the short-sale costs played no significant role. Later, [Lin and Lu, 2015] decomposed the O/S metric into eight distinct ratios, differentiating between open and close, buy and sell, and calls and puts. Noticing how the informational content in both long and short positions was similar, they concluded that the most important channel of predictability was the embedded leverage in the options market.

A more recent study was [Chan et al., 2015], regarding the interplay between returns and net volume (buyer-initiated minus seller-initiated) across stock, call and put markets. They found that it was the stock net volume that led the spot and option quote-price revisions, while the net option volumes had no effect. However, both net flows seemed to be negatively auto-correlated, perhaps indicating the effect of inventory control.

The hypothesis that informed trading is the source of predictability deriving from the option market is strengthened by studies focusing on eventful dates. For example, [Amin and Lee, 1997] found that around announcement days, both the profitability and the effective bid-ask spread of options increased. [Lin et al., 2013] provided conclusive evidence that, prior to any type of corporate analyst events, both the skew and spread of implied volatility become significant predictors, especially in liquid markets. It has been conjectured that this is due to analyst tipping (analysts give traders tips on upcoming information). For example, [Cao et al., 2005] investigated the effect of option volumes prior to takeover and merger announcements. They found that the lagged call option imbalance (the difference between buyer and seller initiated volumes) is not a significant predictor for next day returns, but that this was not the case for pre-announcement periods. They also showed that short-term out-of-the-money options experienced the largest increase in trading volume during these periods.

Lastly, [Goncalves-Pinto et al., 2020], contrary to previous research, argued that the main driving force behind the predictive power of option prices stems from price pressure and not from informed trading, as the predictive power was not lowered when considering option contracts with zero volumes for a specific day.

2.2 Option Volume Imbalance

Denote by the number of assets whose options were traded on financial day , and denote the number of different option contracts corresponding to the asset. Given day and asset , let and denote the number of trades and volume for option contract by investors of market participant class . ”Number of trades” refers to the total number of transactions (regardless of their size), while volume refers to the total number of option contracts traded. Also let denote the average of opening and closing price of option contract for day .

As [Easley et al., 1998] observed, while the option volumes do not reliably predict movements in the stock market, this changes when one considers the volumes of positive and negative signals separately. Positive signals include call buys and put sells, while negative signals include call sells and put buys. If a trader (with or without private information) predicts a positive movement in the price of the underlying, they can opt to enter into either or both of a long call position and a short put position. Conversely, if predicting a downward movement, they can take either or both of a long put position and a short call position222This excludes customers who trade in the options market to hedge an existing stock position, and customers who trade option straddles and other more complicated strategies. The latter poses no issue as the two types of volumes cancel each other out, while, unfortunately, we are unable to identify customers purchasing options for hedging purposes.. Thus, we define

to be the volumes corresponding to speculation for upwards and downwards movement respectively. We similarly define

to be the number of trades corresponding to speculation for upwards and downwards movement respectively. Note that will be used to encode different filters we apply to the transaction data before running different experiments (deliberately left general).

Therefore, using the volume of Call-Buy/Sell and Put-Sell/Buy transactions as positive and negative directional signals respectively, and normalizing by the total volume, we define the Option Volume Imbalance (OVI) for asset and market participant class (for day ) as

| (1) |

where X denotes a generic flow variable 333Note that for this definition we define , i.e when the total volume is equal to , the OVI is also equal to .. We will mostly be using the volume-based OVI, which is defined by setting , i.e and . The normalization ensures that OVI lies in the interval , so that the OVI of different assets can still be directly compared, independent of the asset’s liquidity or market cap.

Note that each transaction is double-counted, from the perspective of both parties. For example, if a Customer buys a call option from a Market Maker, with the intention of creating a long position, it is counted both as a Customer-Buy and a Market Maker-Sell transaction. More details regarding the data set are given in Section 3.

One potential shortcoming of volume-based OVI, is that more weight could be given to option contracts with lower prices (e.g deep OTM options) as they are sometimes transacted in larger volumes. To ameliorate this concern, we can define alternative OVI features by using the total number of trades (which we refer to as trade-based OVI) by setting = , i.e and . We also define the nominal volume-based OVI, by weighting the volume by the option price, i.e set and . Nominal-volume based OVI explicitly gives more weight to higher cost trades, thus preventing low-cost options from having a disproportionate influence 444Note that the choice of sign in (1) is arbitrary; depending on the market participant, the OVI can be either positively or negatively correlated with future spot returns. The choice of signs, was made in accordance to the intuition of positive and negative news, as characterizations of Call-Buys,Put-Sells and Call-Sells,Put-Buys respectively..

Our OVI-based approach is similar in spirit to, but slightly different from the put-to-call volume ratio, that was used by [Pan and Poteshman, 2006]; those authors restricted their analysis to Open-Buy transactions (see appendix for definition) and showed how the put-to-call ratio is a negative predictor for the price movement of the underlying. Since our data set splits transactions based on Market Participant, we do not need to restrict to Open-Buy transactions. Instead, by using (1), all of the available types of transaction are used to construct a metric, for each Market Participant Class.

Importantly, unlike other similar studies in this area, we do not make a linearity assumption between OVI and future returns. In contrast, our analysis uses the sign of the OVI as a directional predictor for subsequent price movements, by making a hypothetical transaction in the corresponding direction. If a significant profit (or loss) is made from this transaction, then we conclude that the OVI contains significant information about the future spot market returns.

3 NASDAQ data sets

Data sets Description

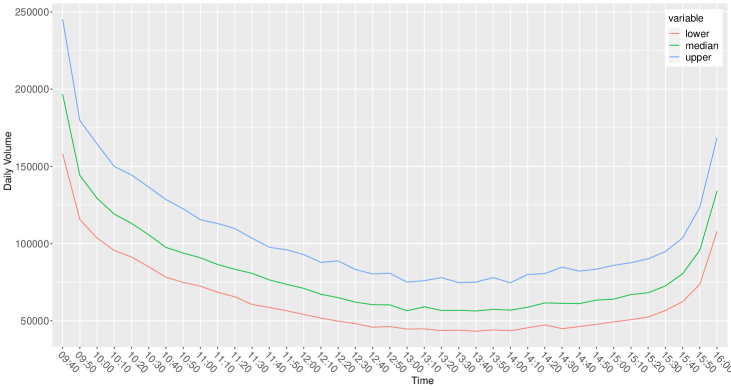

We consider two data sets, from the Nasdaq Option Market (NOTO) and Nasdaq PHLX (PHOTO) exchanges. The data sets provide information about the aggregate option volumes for the period 02 Jan 2015–31 Dec 2019. For each day in this range, we are given a time series of intraday updates from the exchange, disseminated at 10-minute intervals, detailing the total cumulative volume of options transacted up to that intraday time point. As the market opens at 9:30 ET, the first report is disseminated at 9:40 ET, and the last report at 16:00 ET (a total of 39 intraday time points). We are also given a daily summary report containing the total daily option volume for each contract. In the daily report, we are also given its low, high, opening and closing price, its open interest, and total electronic volume, as well as the total volume for the specific exchange. Aggregate volumes are further broken down into five different market participant classes (hereafter MPCs) which are: Firm (Proprietary Trades), Brokers, Market Makers, Customers, and Professional Customers. Definitions for these are given in Appendix A.

Furthermore, for each MPC other than Market Makers, volumes are further decomposed into four parts based on the type of transaction and intention of the agent: Opening Buy, Opening Sell, Closing Buy and Closing Sell (definitions are given in Appendix A) . In Table 1, we give a summary of the main notation used throughout the paper, some of which is defined later on.

| : | Number of days covered by the data set. | |

| : | Number of assets, whose option contracts were traded on day . | |

| : | Number of option contracts traded for asset on day . | |

| : | Number of option contracts corresponding to asset traded on day . | |

| : | Opening price of underlying asset , on day . | |

| : | Closing price of underlying asset , on day . | |

| : | Average of opening and closing price of option contract for underlying asset , on day . | |

| : | OVI of MPC for asset on day . | |

| : | Raw return of asset on day (overnight returns, unless otherwise specified). | |

| : | Excess Market Return, of asset on day (overnight returns, unless otherwise specified). | |

| : | Signal observed on day for asset ’s price movement. | |

| : | Profit and Loss for portfolio at day | |

| SR | : | Sharpe Ratio performance metric of the portfolio for the time span of days |

| PPD | : | Profit Per Dollar performance metric of the portfolio for the time span of days |

| : | Option volume (total number of contracts traded) of option contract of the asset on day , by investors of MPC | |

| : | Option trades (total number of transactions) of option contract of the asset on day , by investors of MPC | |

| : | activation function for P&L regression | |

| : | Objective function for P&L regression. | |

| : | Smooth proxy for the absolute value (used for P%L regression). | |

| : | Window Length for sliding window. |

3.1 Descriptive Analysis of the Market.

In the rest of this Section, we show some preliminary analysis for the two data sets, including an analysis of the interaction between different MPCs. The purpose of this section is twofold; first the analysis in itself is novel and some interesting observations are noted. Second, these observations will help us interpret the results of the subsequent sections.

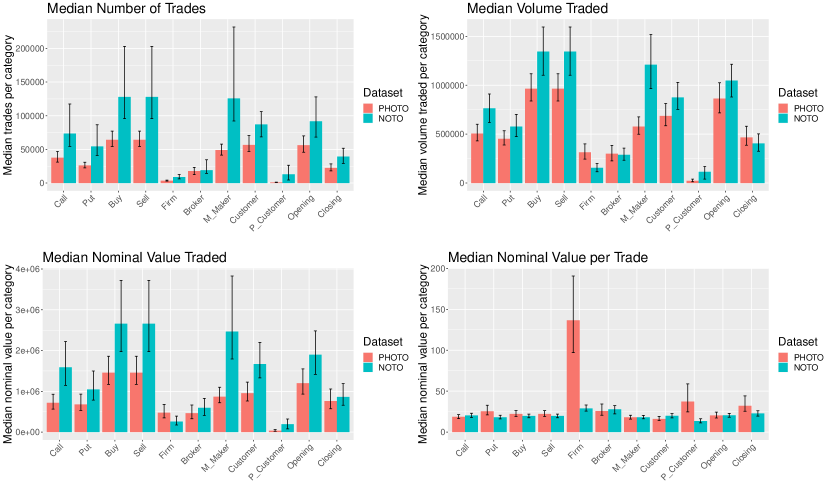

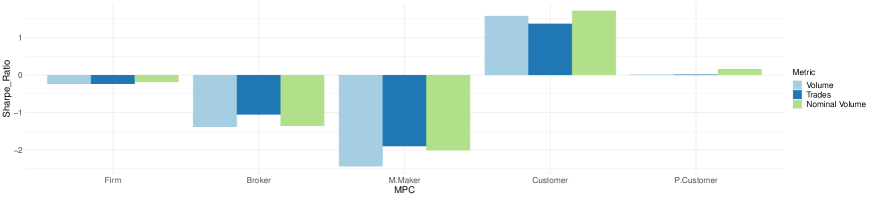

In Figure 1, we show summary statistics (on a daily basis) for the trades in the two data sets, disaggregated by trade type and MPC as defined in appendix A. Although NOTO has a higher average trade count across MPCs, the aggregates of the two data sets are qualitatively similar. In particular, for both data sets call options have a higher median volume than put options and the most prevalent MPCs are Market Makers and Customers. Firms and Professional Customers have a very small median volume. However, when it comes to nominal value per trade for the PHOTO data set, Firms have by far the highest ratio compared with other MPCs. Overall, we expect the OVI of Market Makers and Customers to be the most informative, as the OVI of the other MPCs is constructed from fewer transactions and thus more likely to be noisy (this is confirmed in Section 5, where we observe higher performance for Market Maker and Customers OVI).

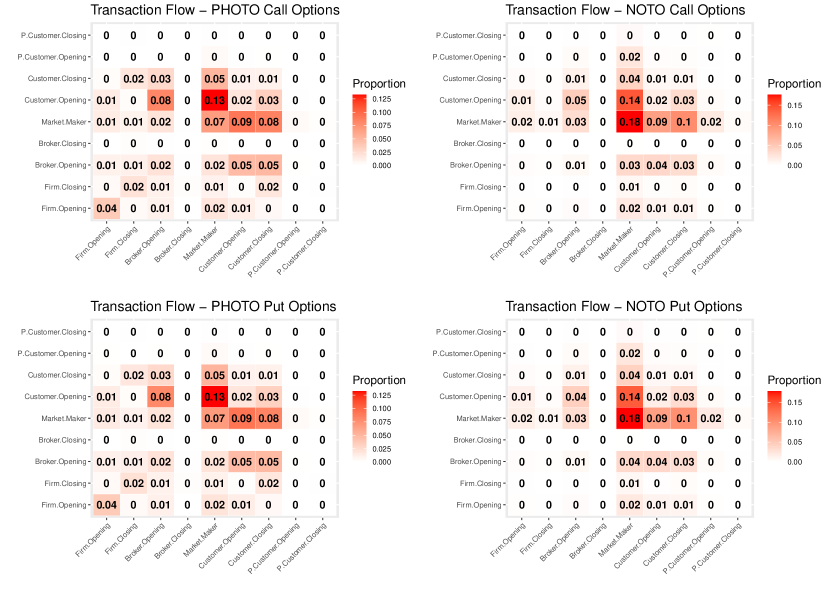

To complement the overview of Figure 1, we also show the flow between different MPCs, i.e how much they trade with each other. Denote by , the average trade flow from MPC (as a seller) to MPC (as a buyer), which represents the median percentage of trades that correspond to these MPCs. The full transaction details are not available, thus we can approximate it by inspecting the 10-minute intraday aggregate volume reports, and then interpreting and matching the flow between different MPCs. For details see Appendix B. The heatmap of the median flow for the two data sets is shown in Figure 2, differentiating between call and put options. Once again, the two data sets display many similarities in their flow structure. Firstly, in both cases the call and put flow structures are very similar. Second, whenever a flow from MPC to () is relatively high, the reverse flow () also tends to be relatively high. In addition, a very large proportion of the flow includes either an (Ordinary) Customer and/or a Market Maker in the transaction. In both cases, the flow between Brokers and Customers is much higher than between Brokers and Market Makers, but in the case of PHOTO the difference is much higher.

The proportion of trades involving the Firms MPC is much higher for PHOTO in comparison to NOTO. The opposite is true for Market Makers, where higher proportion for NOTO, and sharing a significant proportion of the flow with Professional Customers Opening.

In both data sets, Firms and Professional Customers trade mostly with Market Makers, while for Brokers their flow with Customers is larger than for Market Makers.

Correlation of Volume and OVI

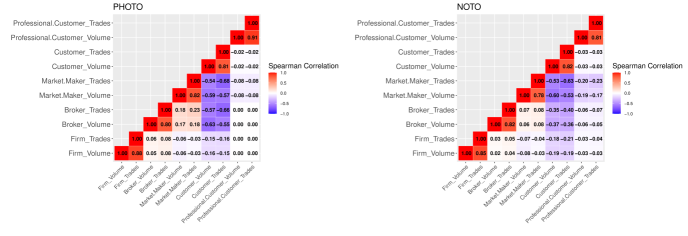

The correlation between PHOTO and NOTO option volume ( and ) ranges between 0.00 to 0.93, for different assets. The correlation between the total volume for different MPCs ( for different ) are also naturally quite high, ranging between . More interestingly, in Figure 3 we plot the median (across days) correlations between the OVI features built using the data from the five MPCs 555Note that the correlation map is very similar across days, with each entry having a standard deviation of 0.05 or less, aross days. Also note that for this analysis the Spearman correlation was chosen for its simplicity and ability to identify nonlinear relationships (the Pearson correlations were, however, very similar).. Unsurprisingly (as trades are double-counted), there is a strong correlation between the volume- and trade-based OVI when they correspond to the same MPC. More importantly, for both data sets (Ordinary) Customers have a high negative correlation, of around 0.6, with Market Makers and Brokers, and a low negative correlation, of around with Firms. We also observe a weak correlation, of around , between Market Makers and Brokers for the PHOTO data set, as well as a weak correlation, of around between Market Makers and Professional Customers for the NOTO data set. The rest of the correlations are below 0.1 in magnitude. Therefore, we should keep in mind the strong multicollinearity present in the OVI features (which later on brings up the need for a regularization term in the P&L regression Section 4.1).

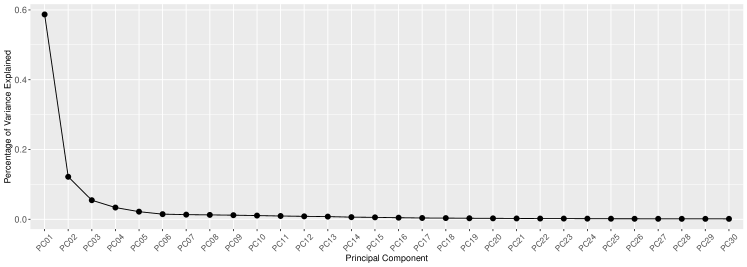

Principal Component Analysis

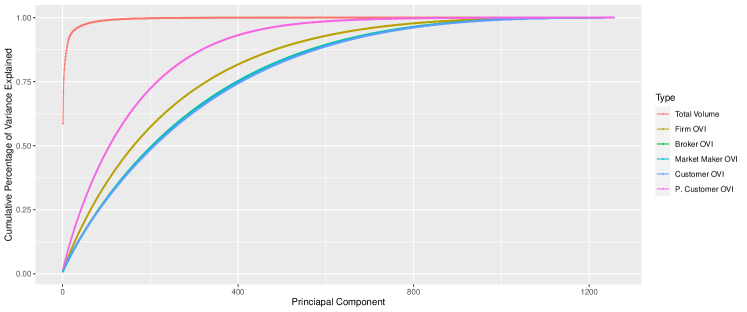

We carry out PCA to investigate the intrinsic dimensionality of the option volumes and OVI observed for the PHOTO data set. In Figure 4, we plot the cumulative percentage of variance explained for volumes and each type of OVI. For volumes, the first principal component explains 59% of variance, with the 12 first components explaining more than 90%. In Figure 5, we show a scree plot for the first few principal components corresponding to PHOTO option volumes. For all OVIs, more than 100 principal components are required to explain 50% of the variance. MPCs with lower daily volumes require fewer principal components, with Professional Customers requiring just 107 components, while Customers require 211 components. Thus, using option volumes to construct OVI significantly increases the intrinsic dimensionality of the data set. This could potentially be an indication that OVI is a better metric in determining asset-specific returns, when compared to option volumes (which have a very low intrinsic dimensionality).

Overall, we see that PHOTO and NOTO are similar in terms of the trade breakdown, while the breakdowns between call and put options are almost identical. We see that the major MPCs are Customers and Market Makers, while all the OVIs are highly interconnected. On the other hand, the higher intrinsic dimensionality observed from the OVI is further motivation for its use instead of the option volumes themselves.

4 Evaluation methods

In the subsequent sections, we investigate how the different OVI features can be used as predictors for the daily returns of the corresponding underlying assets. Underlying assets include mostly stocks, but also a selection of 11 ETFs. We obtain stock and ETF return data for NYSE from the Center for Research in Security Prices (CRSP) database.

Profit and Loss (P&L) and related performance measures

Let and denote the opening and closing price for asset at day . We define the following return types 666Note that all returns considered are adjusted for splits and dividends for asset :

Whenever considering returns for any of the above types, unless specified otherwise, we use the overnight CL_tmOP returns. In this case we drop the superscripts and simply write . Also denote the market-excess returns for asset at day 777Using Risk-Adjusted return using the Fama and French 3-factor model ([Fama and French, 1993]) does not significantly change the results.

where denotes the future return of the S&P-500 index. The S&P-500 index is a widely-used proxy for market returns, due to its wide range of large-cap firms and quarterly updates. Considering market excess returns, allows us to consider a market neutral study, by considering price movements relative to the market price movement. We will refer to market excess returns as EMR, and to raw returns as RR.

Generally, we are interested in predicting directional movement of future prices. We denote by the observed signal, on day , for the future price of asset . Note that as defined here is deliberately left general and could be either some observed variable or the output of a predictive model. However, in the context of this paper, this will be either a single OVI metric or a linear combination of several OVI metrics (as seen later in this section). Then, the sign of this signal is used to select the direction in which to make a hypothetical transaction in the underlying, with and corresponding to buy and sell respectively. We also specify the size of the trade (the ’bet size’), denoted by in one of various ways described below; this quantity may be used to express one’s degree of confidence in the predictive power of the signal. A sequence of such trades constitutes a strategy. To assess the performance obtained using a series of signals, we consider the (excess-returns-adjusted) Profit and Loss (P&L) metric defined by

| (2) |

The P&L is the difference in profit or loss that would have been earned, had we invested units of currency (in our case dollars) in comparison to making an equivalent transaction in the benchmark SPY ETF (which is tracking the S&P-500 index). Note that the idea of P&L described here may not derive from a strategy that is executable in practice (for example, there may be liquidity or timing constraints); nor, given the existence of transaction costs (which we do not take into account here), does it show the realistic return obtained from the strategy. Instead, this metric is a measure of predictability across a number of stocks based on the predictor .

The P&L is defined above for each day , and this gives a vector of daily P&L’s which measures the outcome of the hypothetical strategy over the whole time horizon. A measure of the long-term performance of a strategy is the annualized Sharpe Ratio (hereafter SR) [Sharpe, 1994], defined as

| (3) |

Lastly, we define the P&L per dollar traded (PPD) as

| (4) |

where is the total bet size for day .

When assessing whether a hypothetical strategy is significantly profitable, we use a test with the null hypothesis . We make use of this test throughout the paper, by conducting a test in the same fashion as [Bailey and Lopez de Prado, 2014], which takes into account the non-normality of returns. In particular, we use the test statistic

where the denominator term is based on the estimate provided by [Bao, 2008], for the variance of the Sharpe Ratio.

Whenever comparing the SRs of two different strategies, we need to test the hypothesis of the form of . For that purpose we use the hypothesis test of [Ledoit and Wolf, 2008]. To adjust for the non-normality of returns, they use a studentized bootstrap test on the residuals of a VAR model (ia a circular block approach) to adjust for the non-normality of returns.

Quantile rank portfolios

The P&L (17) only uses the sign of the observed signal (for example, the OVI), and does not take into account its magnitude. Naturally, a larger magnitude for the signal should entail a higher confidence in the prediction. To that end, for each MPC and each day, we split underlying assets into 5 groups, in two different ways.

For each financial day, we divide the underlying assets into five quantile buckets on the basis of the magnitude (strength) of the corresponding option-market signal, . We denote by QB1 the group of assets with the 20% of weakest signals, and so on up to QB5, which corresponds to the 20% strongest signals. Our first split of the equities is simply into the five quantile buckets QB1–QB5, and we refer to this as Quantile-Ranked buckets. For the second and main split, all groups contain equities corresponding to different percentages of the strongest signals, with the first corresponding to all 100% of signals and the fifth to just the strongest 20% signals. In particular we define Q1 = QB1QB2QB3QB4QB5, Q2 = QB1QB2QB3QB4, and so on; we refer to it as a quantile ranked group.

We assess performance of the P&Ls of strategies based on OVI-based signals using a number of different bet weighting schemes, where the bet size (ie., capital) allocated to each equity (equation (17)) depends either on the liquidity of the asset in the option market for that financial day (as measured by traded volume) or on the magnitude of its signal (OVI).

Bet-size weighting schemes

We now discuss the bet-size term of (2), by discussing a number of different betting schemes. Naturally, we can naively allocate equal capital to all the equities traded (we refer to this as the Uniform Weighting Scheme). However, we could take into account our confidence in the used signals, by basing the bet scheme either on the magnitude of the signal or the liquidity of the option contract (as for more liquid assets, the OVI is calculated using more transaction data). In each case, we first define a “raw” bet size for each equity on the basis of an appropriate measure of the market, and set

In this way we ensure comparability of schemes by betting a total of dollar, distributed across all the underlying assets for which trading is indicated, each day. This way, the cumulative P&L (17) has the interpretation of being the cumulative percentage return.

-

•

Uniform Weighting Scheme. Here . In this case we do not differentiate between the different underlying assets, allocating equal capital to each asset with .

-

•

Imbalance Weighting Scheme. Here . Using this betting scheme is equivalent to using the signal instead of just its sign as in (17). As higher-magnitude signals (for example, higher OVI magnitude) indicate a higher confidence level, this weighting scheme allows us to incorporate our prediction confidence in the bet size. Splitting equities into quantile rank portfolios is an alternative way to differentiate based on the magnitude of the signals, but using this scheme allows us to use the whole portfolio, without splitting into groups.

-

•

(Nominal) Volume Weighting Scheme. Here the bet size is set to , or for the nominal volume case (depending on the MPC ). The (nominal) volume is used as a proxy for option liquidity in order to de-emphasize illiquid cases. The log transformation is applied to soften the significant differences in volumes between different contracts.

-

•

Relative Volume Weighting Scheme. Here the bet size is set to (depending on the MPC ), where is the open interest for option contract (of asset ). One issue with the volume weighting scheme, is that equities with lower volumes in the option market, will tend to get a lower weight, even when their liquidity is relatively high. The relative volume weighting scheme, takes this shortcoming into account, by normalizing volumes by the open interest of each contract.

Unless specified otherwise, we will be using a Uniform Weighting Scheme.

4.1 P&L Regression.

In our analysis, we consider several variants of OVI, based on different option transaction types (Buys, Sells or both), data sets (PHOTO, NOTO or both) and MPCs. We are also interested in analyzing the joint predictive power of such OVI features, in explaining future returns. Usually a linear method is employed (OLS or LASSO Regression), and the corresponding or -values are used to compare the explanatory power of different covariates (e.g [Pan and Poteshman, 2006]).

However, a linear model is only suitable for finding linear relationships. Furthermore, the objective function of OLS regression is based on the euclidean distance between observed and fitted values. Such an objective function can be unsuitable for directional predictions (as predicting the direction is an inherently nonlinear problem). A predictor that is successful in capturing the signs of future returns, may be deemed uninformative with respect to the euclidean distance. In the case of linear models, while a predictor’s sign may match the observations perfectly, we may still observe a small corresponding value. Finally, some of the options corresponding to an asset may not be traded at all on a given day, meaning that the OVI can be zero for a large number of days. Linear methods are also unable to deal with feature sparsity, as they are unable to ignore zero-valued features. Indeed, while OLS regression is able to show that all of the OVIs are significant predictors for future returns, the corresponding values are quite low (check section 1 in the Supplementary Material) and it is hard to distinguish between the explanatory power of the different OVIs.

For these reasons, we suggest a novel method for regressing the future returns against different variables (in our case, different variants of OVI), where we directly set an objective function equal to the cumulative P&L (17), thus searching a combination of covariates which maximizes the net profit. Equivalently, we can minimize the negative P&L. Inspired by the popular LASSO regression [Tibshirani, 1996], we also impose an penalty term on the objective function. This allows us to a distinguish between significant and non-significant covariates, by penalizing large coefficient values for the latter. Similar previous research has optimized the Sharpe Ratio by including it in the objective function for portfolio optimization problems such as [Zhang et al., 2020] and [Cao et al., 2020], but in this case we are looking to combine multiple features for the forecasting of future returns for different assets.

Suppose that we have a total of variants of OVI. Denote by the type of feature/OVI, for asset at day (e.g for some MPC and some restrictions ). In this case, we define a signal which is a linear combination of the different OVI

| (5) |

for some vector . The goal is to choose , in a way which maximizes the profit of a strategy based on the signal in (5). In particular, we look for a vector , which maximizes the total P&L (denoted as PL) defined as

| (6) |

Thus, we look for an objective function which incorporates the total P&L. In order to use gradient methods, we require a smooth objective function. The sign function used in (6) is not smooth, therefore we wish to substitute it with a differentiable activation function , such as

| (7) |

This is equivalent to the tanh function for , and for large it converges pointwise to the sign function. We can get rid of the sign function by choosing a bet size, similar to the uniform scheme

| (8) |

Therefore, Equation 6 can be rewritten as

| (9) |

This brings another differentiability issue with the absolute value function, which is used twice, one for the bet sizes (8), and for the regularization term, which is non-differentiable at . There exist many methods to circumvent this, but we shall make use of one of the simpler ones, which is to replace these functions with a smooth approximation, in the same spirit as how we used the modified sigmoid. We use the function , defined as

| (10) |

for some small value of . In summary, the objective function to be minimized, takes the form

| (11) |

To minimize (11), we employ the ADAM algorithm [Kingma and Ba, 2014]888Using the ADAM optimizer, requires choosing two parameters, the so-called moment parameters. For this paper, we use the recommended values given in the original paper ( and ).. The derivative of the objective function is given by

where

| (12) |

Equivalently, written in vector form, this amounts to

Lastly, once the algorithm converges and a vector is obtained, we rescale the coefficients, so that the non-intercept coefficients have a total absolute value of one, i.e

Since only affects the P&L only through the signal (see (5)), rescaling all of the coefficients, does not affect the objective function if we are using the sign function. Note however, that due to using the proxy function, there is in fact a small difference that is caused by the rescaling.

As already mentioned, this method has various advantages over the standard linear regression, as it is for example, better able to uncover monotonic relationships than standard linear regression. The disadvantage is that unlike OLS, the minimization of Equation 11 does not have a closed-form solution nor is it convex, and we are also burdened with the choice of . On the other hand, the magnitude of the fitted coefficient has a direct interpretation as the weighting factor that contributes in making the buy/sell/neutral decision.

Throughout the rest of the paper, signals will either be equal to a particular type of OVI or take the form (5). In the first case the strategy does not require any parameters, and so remains the same throughout the whole evaluation period. In the second case, the model could be trained on more recent data, via a sliding-window approach.

In particular, we set a window size of 500 trading days (about 2 years), a testing window size of days999Note that choosing different and , does not significantly alter results.. A window at day , contains the range of days . For each window, we regress the future returns against the OVI features, using the P&L regression described above, to obtain coefficients . After obtaining the fitted coefficients , we calculate the P&L in (9) using the days in the testing set for the window at day d

i.e . This is an out-of-sample metric, with the direct interpretation of being the hypothetical profit one would make in 100 days of trading by following such a strategy (in the absence of trading costs).

5 Main Empirical Results

In this section, we assess the predictive power of OVI against the future returns across different MPCs, across differet return types (overnight,intraday and close to close) for the PHOTO data set, and by using different betting schemes.

Comparison across market participant classes

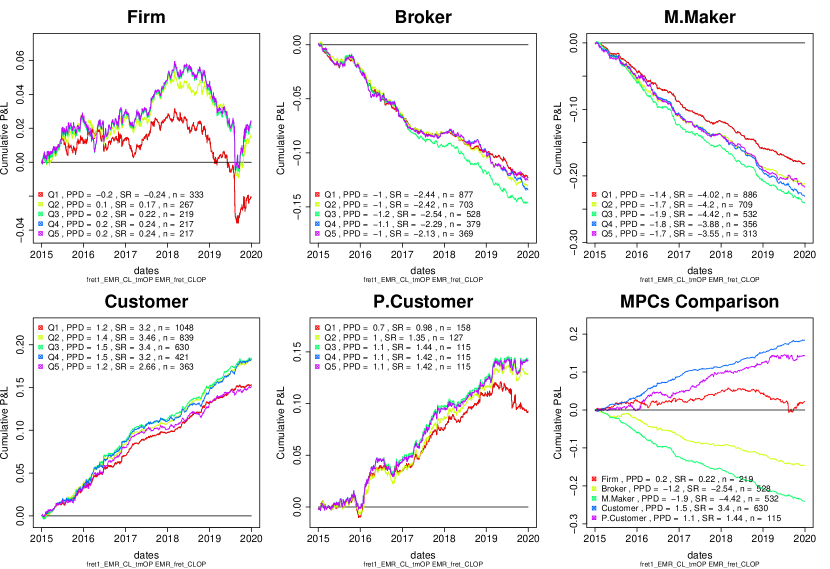

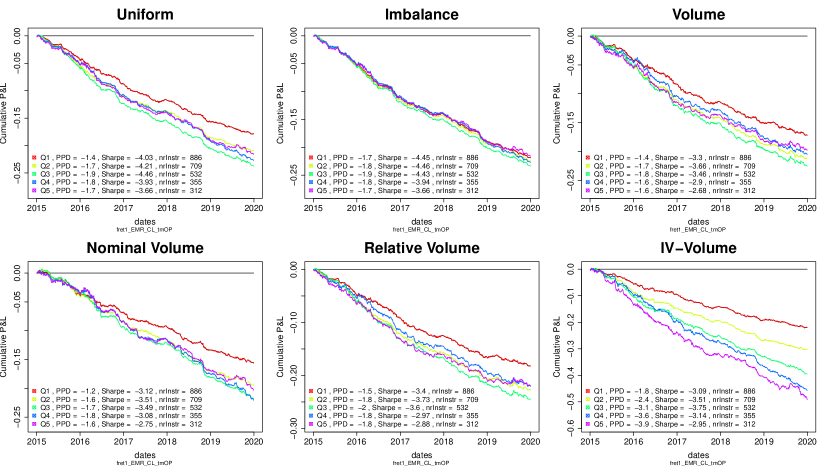

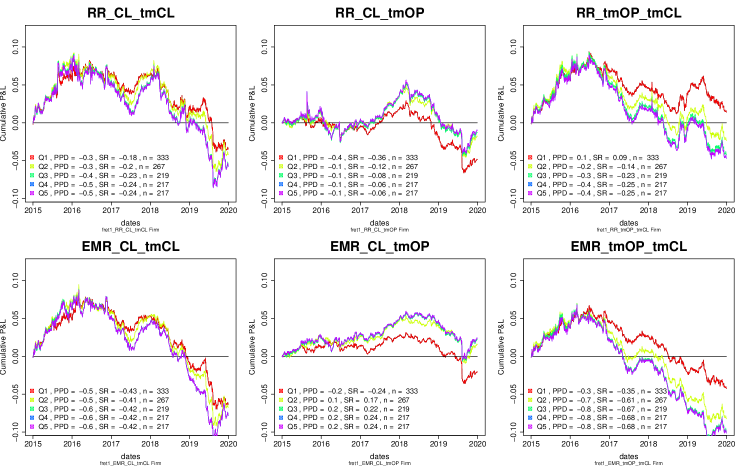

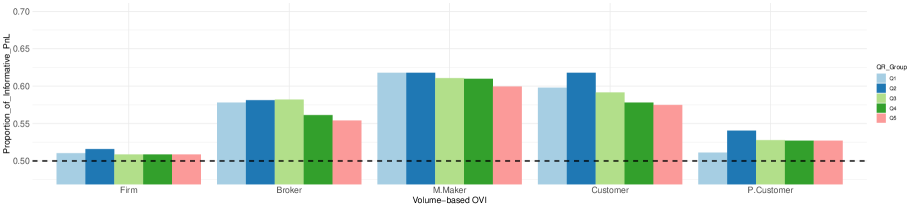

We consider the OVI for each of the 5 MPCs seperately by using their sign as the signal for future returns ( = for each ). We then evaluate their corresponding P&L using Equation 17, for their excess market overnight returns (EMR CL_tmOP), and for different quantile ranked groups (Q1-Q5) built as described in Section 4. In particular, we plot the time series for the cumulative P&L incurred over the period 2015-2019 in Figure 6.

The highest performance is observed for Market Makers, where the cumulative returns are between 17% and 25% and annualized SRs lie between 3.5 and 4.4 depending on the quantile rank portfolio used. The second best performance is observed for Customers, whose cumulative P&L display a clear upwards trend, and SRs with magnitudes in the range 2.7–3.5. Strong positive signals are also observed for Brokers, with SRs between 2.1 and2.5. Lastly, Professional Customers display a downwards trend with SRs of magnitude 1–1.4. For Firms, while the total P&L is slightly positive, there does not appear to be a clear upwards trend, with SRs very close to 0. Note that there seems to be a trend shift happening after 2018 for Firms, from a somewhat upward trend to a downward trend (a trend shift can also be noticed for other MPCs).

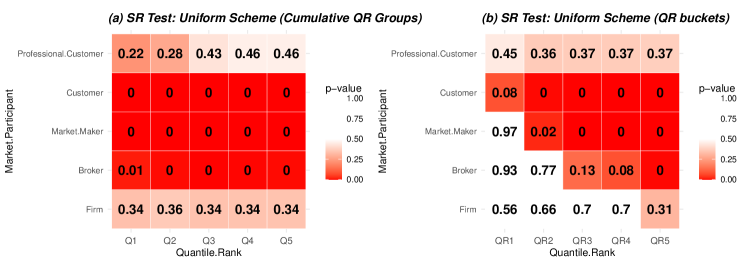

In Figure 7(a), we report the -values obtained when running a significance test for the SRs corresponding to excess market CL_tmOP returns. The tests for Brokers, Market Makers, and Customers are rejected with a -value of 0 (up to 2 decimal places) across all quantile ranks. Firm and Professional Customers have -values close to 0.5 across all ranks. Thus, in the span of five years, we observe a clear signal from three out of five of the MPCs, with the Market Maker achieving a return of about 30% in a period of 5 years. The two participants without a clear signal are also the MPCs with the lowest mean volume per day (see Figure 1), which partly accounts for the reduced performance. The clearest signals come from Market Makers, followed by Customers, which have on average the highest volume per day. These observations clearly mark the OVI as holding predictive power for future returns. Note that this verifies the findings of the earlier study [Xiaoyan et al., 2008], who report that the informational context of Customer volumes is higher than Firm volumes.

Quantile rank portfolios

For all MPCs except Firms, the best performing portfolio is Q3 both in terms of PPD and in terms of SR. The worst performing portfolio in terms of PPD is Q1, which in most cases has a noticeably worse performance than other QR groups. In terms of SR, the worst performing portfolio is either Q1 (all assets) or Q5 (top 20% of strongest signals) depending on the MPC. Therefore, the strategies of taking into account all the non-zero OVIs, or only considering a very small subset of the strongest signals, are both outclassed by following a portfolio consisting of the top 60% or 80% of the highest-magnitude OVIs.

The same analysis is carried out for quantile ranked buckets. In Figure 7(b), it becomes apparent that across MPCs, lower QR Buckets highly outperform the higher buckets, with QB1 being almost uninformative. For both Market Makers and Customers, QB2-QB5 appear to be the most significant. Overall, this confirms that not only is the sign of the OVI informative on future returns, but that the predictability observed is stronger for higher magnitudes of the OVI, which justifies using the OVIs as signals.

Comparison across Return Modes

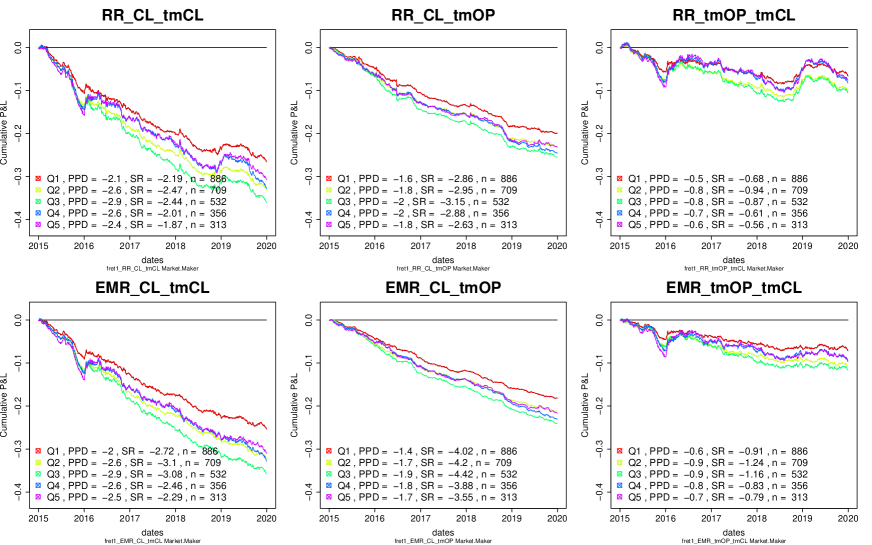

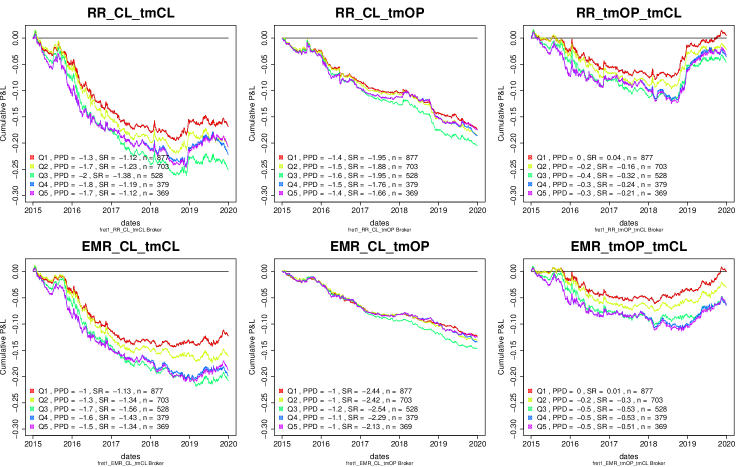

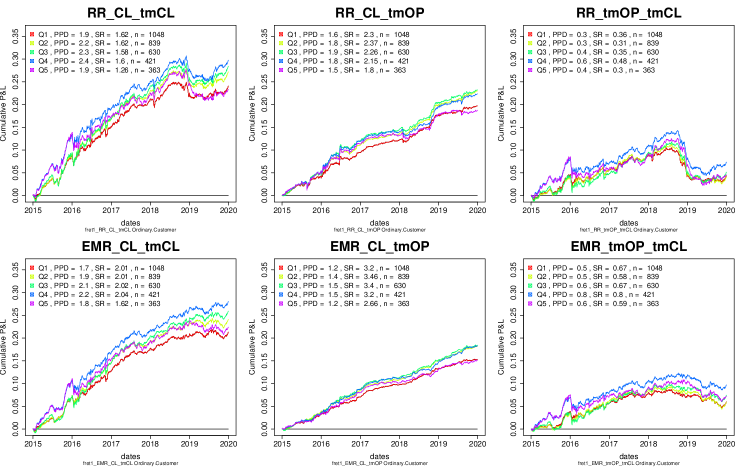

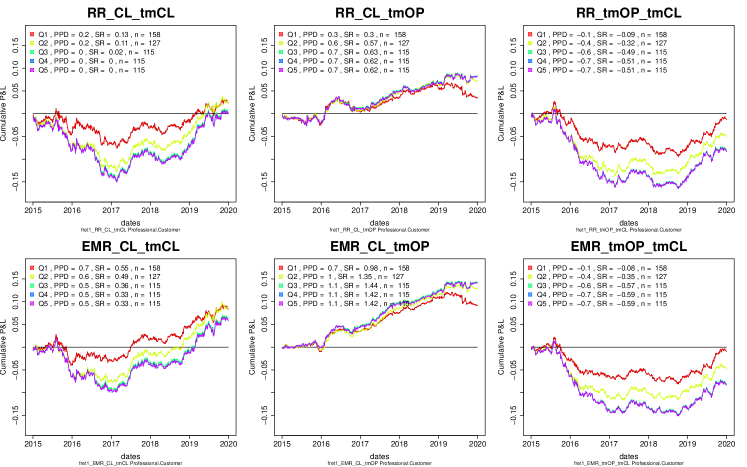

In Figure 8, the cumulative P&L corresponding to each type of return is shown, when using the Market Maker OVI.

The highest predictability is clearly observed for the the overnight (CL_tmOP) returns, followed by the close-to-close (CL_tmCL), and then by the open-to-close (tmOP_tmCL) returns. Close-to-close return is a combination of the other two types of returns, with most of its predictability stemming from the overnight returns rather than the next-day returns. Using market excess returns, results in higher returns as shown by higher SRs, but raw returns also give significant results across MPCs and quantile rank groups.

Comparison across OVI types

Throughout this section we have been using the Volume-based OVI. In Figure 11, we compare the different types of OVI (for Q3 quantiles, Uniform Weighting Scheme) across MPCs. Trade-based OVI has the lowest performance for Brokers (significantly lower than both volume and nominal volume based OVI), Market Makers (significantly lower than volume based OVI) and Customers (significantly lower than nominal volume based OVI), and therefore seems as a less suitable feature, than the others. This is expected as it is naturally the least informative of the three types of features, compared to volume and nominal volume. Volume-based OVI scores the highest (in magnitude) SR for Market Makers and Brokers, and the difference with the other two types for Market Makers is significant when running a pairwise SR Difference test.

5.1 Alternative Weighting Schemes

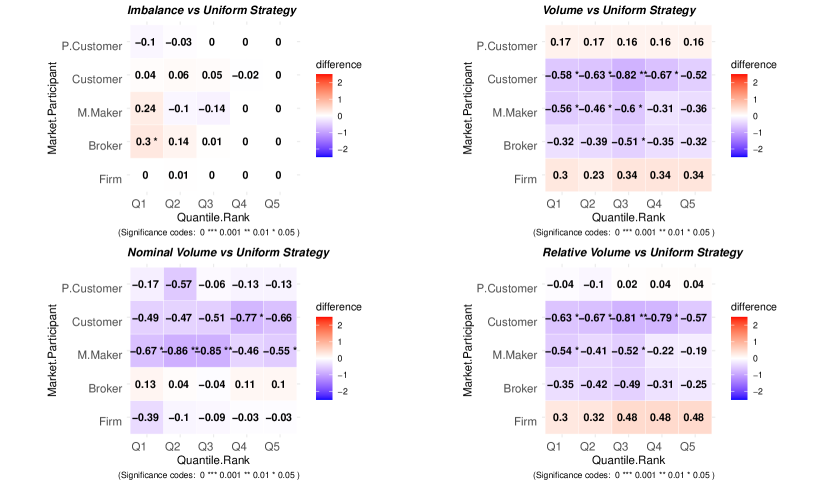

In this subsection, we compare the Uniform Weighting Scheme with the alternative schemes defined in the previous section. We use the Market Maker OVI, and record the P&L corresponding to excess market overnight returns Equation 17. In Figure 9, we carry out a SR difference test to compare the performance of different weighting schemes for the overnight returns with the uniform scheme. In Figure 10 we plot the cumulative P&L for excess market overnight returns obtained by following a strategy for each of the different weighting schemes, for the Market Maker OVI.

Imbalance Weighting Scheme

In most cases across MPCs and quantile rank groups, when performing pairwise SR difference tests between the Uniform and Imbalance Weighting Schemes, the hypothesis is not rejected, and if we correct for multiple testing, none of the hypothesis’ is rejected. However, as seen in Figure 9, the SRs corresponding to the Imbalance Scheme are slightly higher than those for the Uniform Weighting Scheme, for all quantile rank groups for Brokers and Customers, as well as Q2, Q4 and Q5 for Market Makers. Therefore, this suggests that the Imbalance Weighting Scheme is a better way to incorporate the information embedded in the OVI, than a simple uniform scheme.

Furthermore, as seen in the cumulative plot Figure 10(e), we can clearly see that the quantile rank groups are more indistinguishable (both in terms of SR and PPD) in comparison with the Uniform Scheme, especially for Q1-Q3. In addition, the QR group is the worst performing, despite being one of the highest performing groups for the other weighting schemes.

Volume-Weighting Scheme

In Figure 9, it can be seen that in most cases, both the Volume and Nominal Volume Weighting Schemes are outperformed by the Uniform Weighting Scheme both in terms of SR as well as PPD. The Relative Volume Scheme, is also outperformed by the Uniform Scheme in terms of SR, but slightly outclasses it in terms of PPD. In addition it outclasses the other two schemes in terms of both SR and PPD, for most of the QR Groups. The lower SRs are a result of higher variability introduced when incorporating volume into the betting scheme. However, none of the volume betting schemes seems to be suitable in replacing the uniform betting scheme. Note, that defining a weighting scheme based on the raw option volume (without the log transform), the sqrt-transformed volume, or the liquidity of the underlying, also fails to outperform the uniform scheme, even though the raw-Volume Weighting Scheme does outperform it in terms of PPD (but has a very high variability).

5.2 Multi-factor analysis and stability analysis across time

In predicting future overnight returns, using the signal given by the sign of the Market Maker OVI, has reulted in the highest performance. The Market Maker signal can be written as

| (13) |

In this subsection we evaluate the joint predictive power of the OVI corresponding to the five different market participants (K=5) using the P&L regression method described in Section 4, to predict the future EMR CL_tmOP return, by using a signal of the form

| (14) |

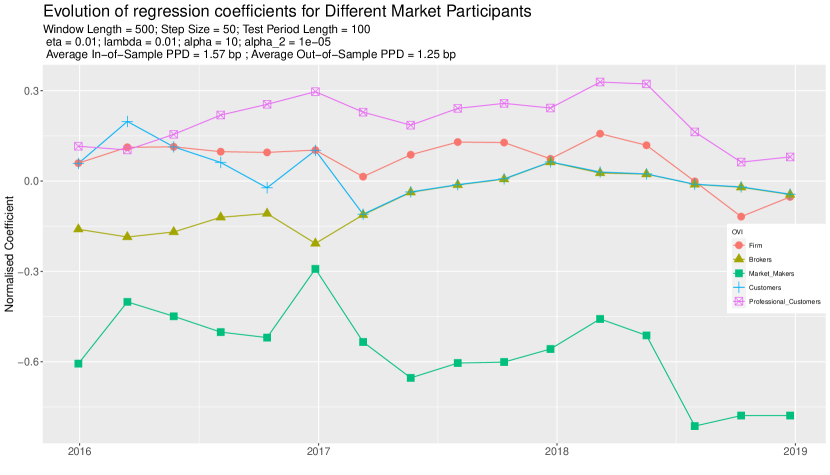

We regress in a sliding window manner and record the evolution of the normalized coefficients during 2016-2019, as shown in Figure 12. Note that at each time point, the coefficient of Market Maker OVI dominates, by having a magnitude of 0.3-0.75. Generally, the Market Maker OVI seems to have a higher weight for the later years, which is partly due to the coefficients of Broker and Customer OVI shrinking in magnitude. Firms show mostly negative coefficients, with low magnitude for the entire 5-year period. Interestingly, the OVI for Professional Customers has a consistently negative coefficient throughout the 5-year period, with a relatively high magnitude. Since the volumes of Professional Customers are quite low (i.e the OVI is equal to zero in most cases), the high coefficient does not disrupt the model (which would have not been possible if we used a linear regression model). On the other hand, as seen in the correlation map in Figure 3, the OVI for Professional Customers is not correlated with the other features, which potentially shows that additional information is brought when it is used in conjunction with Market Makers’ OVI.

Since such a method results in a coefficient vector dominated by the Market Maker’s OVI, it is worth comparing the performance of and , when using the bet sizes Equation 8. The two strategies give similar mean in-sample PPDs with 1.50bps and 1.57bps respectively. However, using results in a slightly higher out-of-sample mean PPD of 1.33bps compared to 1.25bps for , indicating some overfitting in the second case.

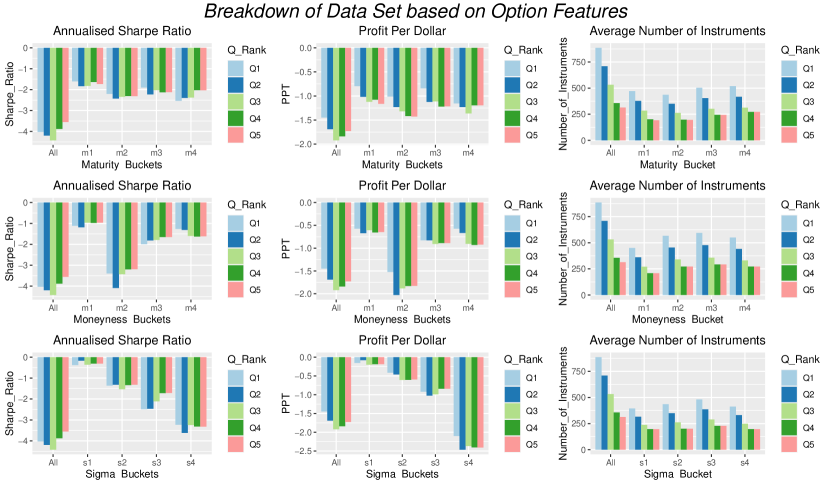

6 Influence of options features on OVI predictability

In the previous section, we showed how the OVI can be used as a predictor for next day returns. In this section, we investigate which options carry most of the predictability, by segmenting options according to the value of certain option features, namely a subset of the “Greeks”: moneyness, maturity, and implied volatility; we calculate all of these features in a standard Black–Scholes model without dividends. One might naturally expect option moneyness, being a measure of the relative sizes of the spot and strike prices, to influence OVI predictability. Indeed, [Pan and Poteshman, 2006] and [Ge et al., 2016] both find that the highest predictability over comparatively long timescales stems from volumes of OTM options, which is attributed to the relatively high leverage that they offer speculative traders targeting (or hedging) large price moves over these timescales. Here, however, we consider next-day returns, and we expect ATM options returns to be more informative, as they offer a more geared return from small price moves than OTM options. On the other hand, ITM options’ intrinic value, results in a higher price, hindering the high leverage advantage offered by the option market, and resulting in relatively low volumes.

Note that there is not a one-to-one map between moneyness and other Greeks; while the Greeks are related in various ways, different Greeks can serve to segment the universe of options in different ways. For example, is highly correlated with the absolute value of moneyness, while depends monotonically on moneyness. As we see below, this enables us to consider a range of perspectives.

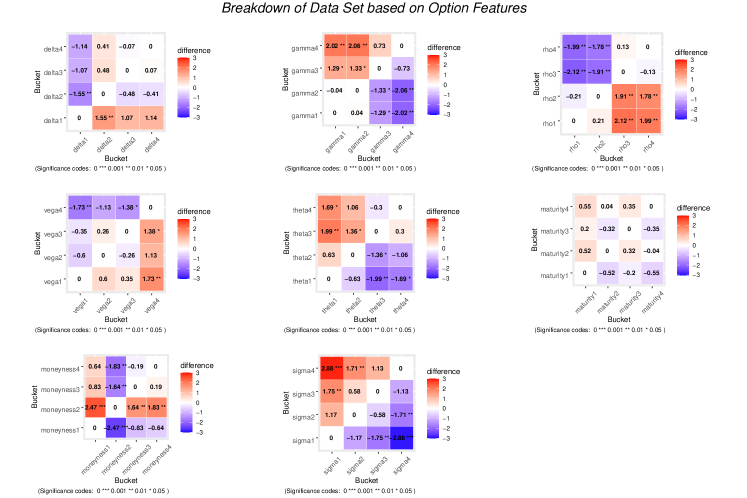

For each day, we divide the option contracts into four disjoint buckets, based on the quantiles of the feature in question. The first bucket contains options corresponding to the lowest 25% of values for that feature, and so on up to the bucket, which contains options corresponding to the highest 25%. The OVI pipeline described in the previous sections is then applied to each bucket separately, and the performance of the resulting buckets is compared. For each feature, we run the pairwise SR difference test between the four buckets (at the 5% level). We only follow this process for Brokers, Market Makers and Customers, as they are the MPCs whose OVI was concluded to be a significant predictor of future returns.

Below we show some interesting results based on the , as well as the implied volatility of options, calculated (for simplicity and ease of computation) using the Black–Scholes (BS) model101010Note that since equity options are mostly American, the Black–Scholes Model may systematically undervalue them. However, as these differences are typically of the order of 1–2%, we accept the inaccuracy and avoid large-scale computations. for European Options without dividends [Black and Scholes, 1973]. We also provide a short discussion on moneyness and maturity, to interpret the results.

Under the BS model, a call option has a price equal to

| (15) |

and a put option has a price equal to

| (16) |

where

Here refers to the current price of the underlying asset (in our case, we use the average of close and open), refers to the risk free interest rate, to the time until maturity, to the strike price, the unobserved volatility of the underlying and the cumulative distribution function of a normal distribution. Lastly, / denote the average of the opening and closing prices. The implied volatility , is the value of that solves (15) / (16) (with / being the average of the opening and closing prices), and can be obtained using a simple iterative method. Importantly, note that all these quantities describe an option from the buyer-perspective (e.g all call options will have a positive ).

In Figure 13 and Figure 14 we plot, for Market Makers, the results for the option Maturity , standardised Moneyness defined as

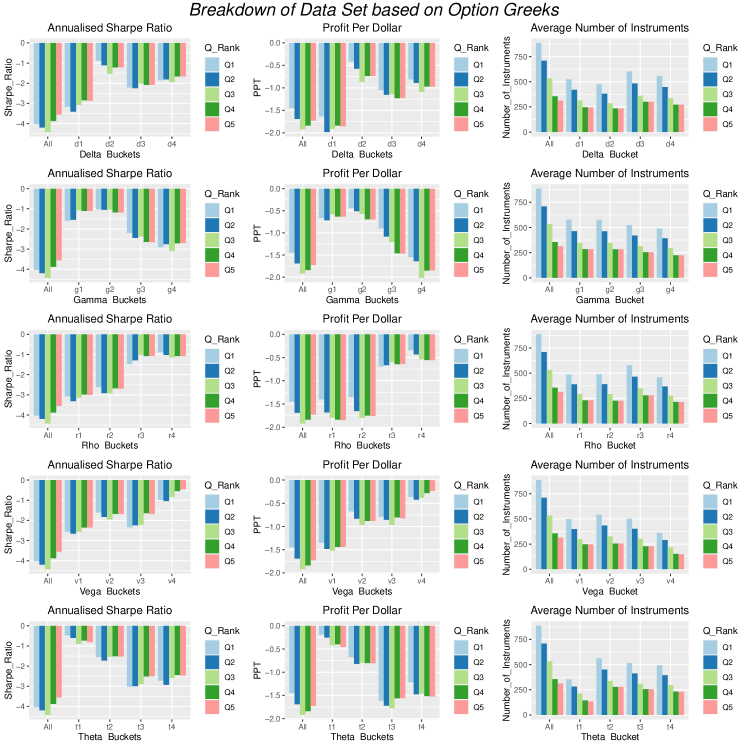

and implied volatility , as well as the five main Greeks (Delta, ; Gamma, ; Theta, ; Rho, ; and Vega, ).

Moneyness, Gamma and Theta

Consistently with our expectation noted above, ATM options show the highest predictability. For example, across MPCs, higher Gamma options/higher Gamma buckets (corresponding to ATM options) tend to perform better. For Market Makers, the Gamma bucket significantly outperforms the others, clearly indicating how higher is linked to higher predictability. Likewise, higher (also closer to being ATM) have the highest performance, with the and buckets significantly outperforming the first two ones. Results are not as clear with moneyness buckets, with no consistent pattern followed by the buckets, except that the bucket is outperformed by the rest, hinting that deep OTM options have the lowest informational content111111Replicating this analysis with five buckets still fails to produce any significant results. This is mainly because the five buckets do not exaclty correspond to deep OTM, OTM, ATM, ITM and deep ITM, as the moneyness distribution is skewed towards OTM options..

(Non) Effect of Maturity ()

One could expect maturity to play an important role in the predictability, and as is often done in other works, one might be tempted to filter options with very high maturities. In particular, similar to the moneyness case, one could expect that higher periods to maturity would result in a poor informational content. However, no consistent pattern can be observed across MPCs for the different maturity buckets, indicating that maturity has no effect on predictability. Thus, there is no need to filter option contracts with high or low maturity as is done in other works, when calculating the OVI.

Difference between call and put options

By definition, call options have a positive , while put options have a negative . In addition, as the future value of assets rises with interest rates, call options also have a positive , while put options have negative .

We can clearly observe that put options play a more important role in predicting future returns compared to call options. Across all MPCs, the first bucket for Delta (consisting mostly of ITM put options) outperforms the other buckets (consisting mostly of call and OTM put options). For Market Makers and Customers, the bucket significantly outperforms the other buckets. In addition, the first two buckets for (corresponding to the Put Options) are the best performing, with the difference being statistically significant for all MPCs.

Implied Volatility () and Vega ()

For all of Brokers, Market Makers, and Customers, higher implied volatility results in higher predictability. In particular, the bucket is the best performing bucket across all MPCs, and significantly outperforms all other buckets except the bucket for Brokers. The bucket also outperforms the complete data set, in terms of PPD for Brokers and Market Makers, as well as in terms of the SR for Brokers. The bucket is also consistently the second best performing, significantly outperforming the first two buckets for Market Makers, as well as the bucket for Brokers. Overall, these results clearly indicate that most of the predictability stems from high implied volatility contracts.

Given that this feature has the most significant and consistent effect on the predictability of OVI, we consider an additional betting weighting scheme. Similarly to the volume weighted betting scheme, we consider a strategy based on the product’s volume, multiplied by the implied volatility of the asset. We set the IV-Volume Weighting Scheme as

where is the implied volatility corresponding to option contract of asset on day . As can be seen from Figure 10, this scheme results in a higher PPD than all the other schemes, even though its SR is lower than most schemes with the exception of the volume scheme. Therefore, similarly to the Relative Volume Weighting Scheme, this is a more profitable yet less consistent scheme than the Uniform Scheme.

For Vega, no consistent pattern can be observed across MPCs. Thus, while implied volatility plays a big role in determining the informational content of an option’s volume, the sensitivity of options to implied volatility does not.

7 Extensions

In this section, we build on the results of Section 5, by performing further tests for more general scenarios. These include checking the price persistence for longer holding periods, comparing the PHOTO and NOTO data sets, and a short intraday and cross-sectional analysis.

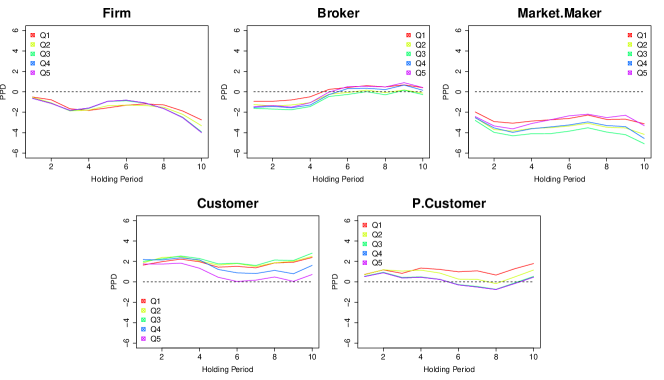

7.1 Short-term versus long-term price persistence

Previously, we observed that for Market Makers, Customers and Brokers, a strategy based on the OVI with a holding period of one day, results in either significant profits or losses. In a similar fashion to [Pan and Poteshman, 2006], we test how the results change for different holding periods. For each strategy, we record the cumulative returns obtained when using a longer holding period. Therefore, for a holding period of days we calculate the P&L as

| (17) |

and plot the cumulative returns in Figure 16, for holding periods of up to 10 days.

For Market Makers, aside from a significant SR displayed during the first day, the SR corresponding to the (non-cumulative) returns of the second day after execution are also statistically significant (with a p-value of 0.00). The cumulative returns do not revert over the following days, clearly demonstrating a persistent return.

For the rest of the MPCs, only the first day (non-cumulative) returns are significant. There is a long lasting effect shown for Customers’ Q4 and Q5, where cumulative returns do not significantly decrease after the first day, not displaying any mean reversion. For Brokers, this is not the case, as the cumulative returns revert signs from around the fifth day onward. The other two MPCs do not produce significant results for the first day.

Overall, as the returns for Market Maker OVI do not revert, the predictive power does not seem to stem from price pressure, but is potentially due to a degree of informed trading, confirming the observations of [Pan and Poteshman, 2006].

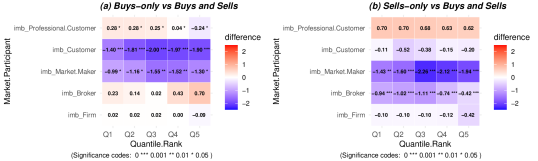

7.2 Difference between Buys and Sells

Recalling the definition of OVI (1), the terms and are defined as using the volumes from both the buying and selling activities of a MPC. In order to gain a better understanding of which type of transaction is the major source of predictive power, we calculate the OVI restricted to only the “buy” transactions (resp. sells) denoted as (resp. ). We compare both of these with the standard volume-based OVI feature (), by using the SR difference test. As can be seen from Figure 17, performs significantly worse than across QR Groups, with its OVI being almost uninformative. also has a lower SR than , but the difference is not statistically significant. This implies that for Customers most of the predictability comes from the selling activity. The opposite is true for Brokers, where performs significantly worse than , but has a slightly higher performance than . When it comes to Market Makers, both differences are significant across all quantile rank groups. Recall that the differences in volume for buying and selling activity was small for all of the MPCs (see Figure 2), therefore the above results could indicate that Customers utilize their speculative ability (or possibly inside information) mostly by writing option contracts.

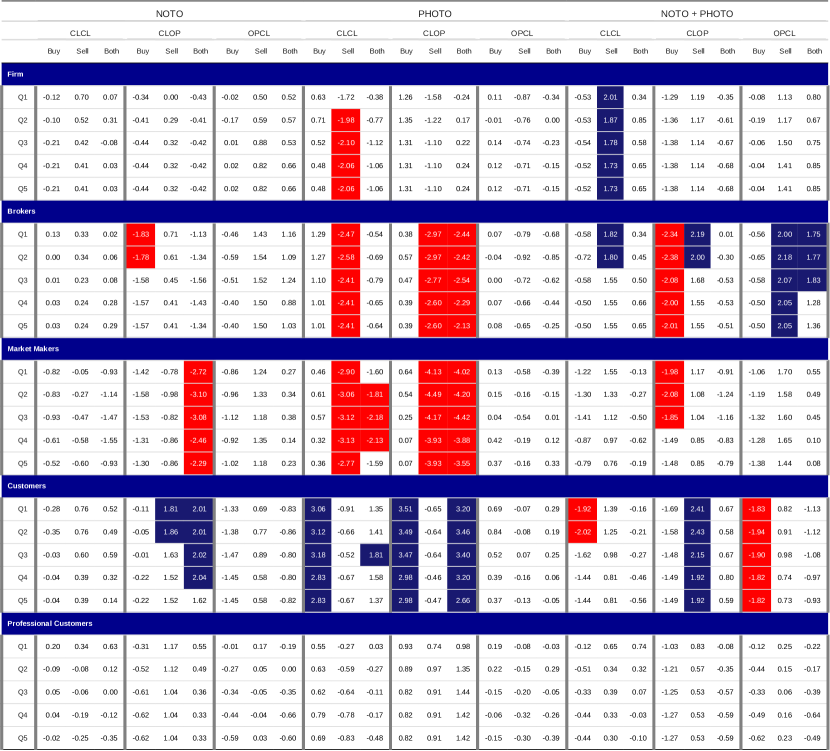

7.3 Additional features from the NOTO data set

We have so far considered only the PHOTO data set corresponding to the PHLX option exchange. We now consider the NOTO data set, which corresponds to the NASDAQ exchange. In Figure 18, we show a complete overview of the SR corresponding to the three types of returns for the five MPCs, across quantile rank groups, using either buys, sells or both for the calculation of the OVI feature. Furthermore, we show these values when using NOTO, PHOTO or the union of the two data sets. About half of the values in the table have p-values less than 0.05 for the SR significance. In addition, the colored cells denote the cells which have a significant SR when Bonferonni corrected across all tests, i.e using a p-value of .

Similarly to the PHOTO data set, the highest performance corresponds to the CL_tmOP future returns for Customers and Market Makers, while Brokers also have a significantly good performance. Another similarity is that the middle quantile rank groups (Q2-Q4) tend to outperform Q1 and Q5. In the cases of statistical significance, CL_tmOP and CL_tmCL future returns have identical signs, with the CL_tmOP returns consistently scoring higher SRs. For the NOTO data set, tmOP_tmCL returns display higher SRs than for PHOTO, with some of them being significant (when ignoring the Bonferonni correction) such as Broker sells or Customers buys. Note that in both of these cases, the sign of SR is in the opposite direction of what is displayed by the CL_tmOP returns, showing a price reversal effect between the overnight and tmOP_tmCL returns, which is not as strongly present in the PHOTO data set. In fact, one can further notice that no result corresponding to CL_tmCL returns is significant for the NOTO data set. This seems to indicate a sharper price reversal present in the NOTO data set. Coupled with the the highest SRs scored by the PHOTO data set, this could be indicating that a higher proportion of traders in the PHLX exchange are informed when compared to the NOM exchange, where most of the predictability stems from short term price pressure.

Due to the higher median daily volume displayed for NOTO (as seen in Figure 1), the combined OVI’s SR takes the same sign as the SR of the corresponding NOTO value in almost all cases. When a combined OVI is significant, we observe a weak result when using PHOTO’s OVIs and a strong result using NOTO’s OVIs (that is weaker than the result of using the combined OVI). An interesting example is when using the selling transactions for Firms corresponding to the CL_tmCL returns, where there is a significantly positive SR for the PHOTO data set, but a significantly negative SR when using the combined data set.

Most of the predictability comes either from the buying or selling transactions, and in almost no cases do they both appear to result in a significant SR. The one exception is the NOTO OVI of Market Makers for CL_tmOP returns, where both and are negative, resulting in a statistically significant performance for . Therefore, using only Buys or Sells outperforms the OVI obtained by using the complete data set in almost all cases.

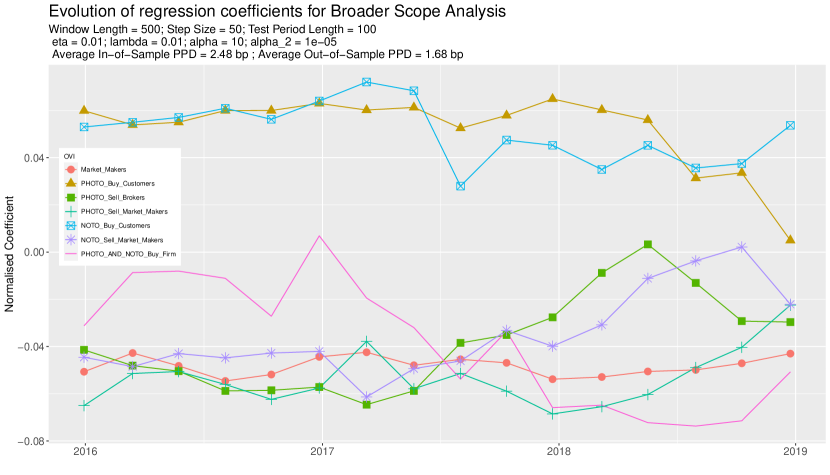

Taking into account the plethora of different OVI features, we consider another model, in order to test whether these 45 features can be used to build a better signal (for overnight returns)

| (18) |

where is the OVI corresponding to the stock for the day, for MPC , data set and type of transaction of the data set (Buys, Sells or Both). In Figure 19, we plot the evolution of some of the coefficients (specifically the ones with the highest median magnitude across time). Note that M3 raises the overall PPD compared to M1-M2, with 2.48bp in-sample and 1.68 out-of-sample mean PPD, which signifies that the predictive power can be increased by considering the NOTO data set and decomposing the data set into Buys and Sells.

Looking at the significant coefficients, we draw the following conclusions

-

•

gives a consistently negative coefficient (similar to M2), and the same holds true for and .

-

•

starts with a significantly positive coefficient, which falls close to zero right after 2018, which is similar to the case of for M2.

-

•

yields consistently positive coefficients, similar to for M2.

-

•

is also consistently negative, but its coefficient shrinks for latter years similar to .

-

•

has a fluctuating coefficient for the early years, but a positive one for the latter years, reflecting the pattern observed earlier in Figure 6.

7.4 Cross-Impact analysis

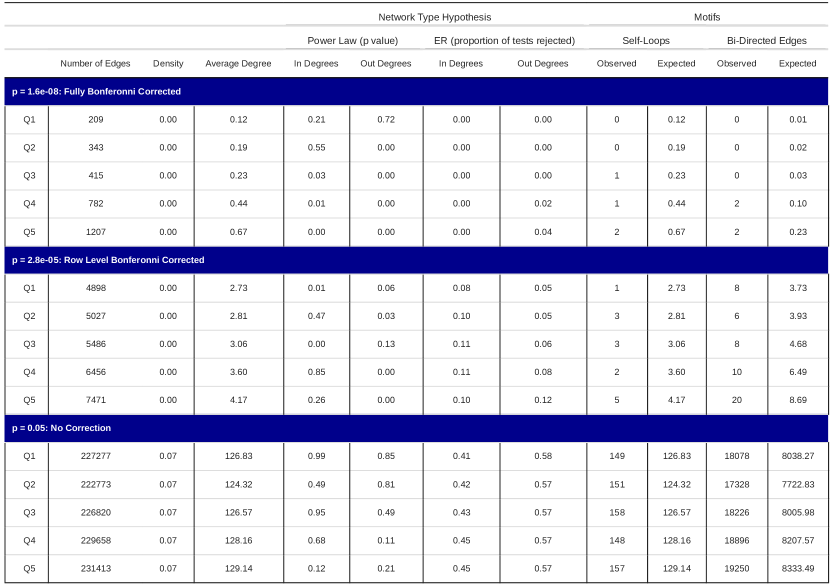

We perform a cross-sectional analysis, where the OVIs of all the assets are tested for predictive power against the future returns of all the underlying equities. With stocks in the universe, there are relationships to be tested. These interactions can be represented as an unweighted directed network, where the existence of an out-edge from vertex to vertex indicates that the OVI of asset can be used as a predictor for the equity returns of asset .

Our approach is similar to the one employing Bonferonni networks ([Tumminello et al., 2011]). Such a network was constructed by [Curme et al., 2014], to investigate the intraday return correlations across stocks. Instead of correlations, we employ the cumulative P&L obtained by following a simple strategy of using the Market Maker OVI of asset as a predictor for the overnight (CL_tmOP) returns of another asset . An edge is added to the network if the SR differs significantly from 0, according to the [Bailey and Lopez de Prado, 2014] hypothesis test.

In particular, let denote the adjacency matrix of the network. For each potential edge , we iterate across days and trade equity , for days where asset ’s OVI belongs to the Q3 portfolio (top 60% of the highest OVI’s in magnitude). In that case, we buy asset , if the OVI of asset is positive, and sell if it is negative. Let , if the asset is in the quantile group for day and 0 otherwise. Then, the daily return for following this simple strategy is equal to . We perform the SR significance test on , and set , if the obtained p-value is less than a predetermined value (and otherwise). By varying , we obtain five different networks for each threshold.

To account for multiple testing, we use the conservative method of a Bonferonni-corrected test by choosing a uniform significance level for all individual tests, giving a bound for the Family-wise error rate (FWER) (see for example Appendix A of [Curme et al., 2014]). We use three different types of p-values corresponding to 0.05, (applying the correction to the row-level), and (applying a full Bonferonni correction). Depending on the p-value and quantile group, we build a different network, resulting in 15 different networks.

For this analysis, we only use assets listed in CRSP for the whole duration from 01 January 2015-31 December 2019, leaving a reduced universe of 1792 NYSE assets. In Figure 20, we summarize the information regarding each of these networks. Obviously, as the p-value grows, the network also grows, with the networks corresponding to a p-value of 0.05 having a density of 7%. For higher QR groups, the network is larger, with Q5 resulting in the largest networks. The fully Bonferonni-corrected networks have a total number of edges between 209 and 1207, which clearly rejects any hypothesis of no cross-impact effects.

Furthermore, out of the 1207 edges of the Q5 network, only two are self-loops (i.e using an asset’s own OVI feature, to predict its future returns). This is higher than what would be expected under an Erdős-Rényi network with the same density (which is 0.67 here). Bi-directed edges (i.e OVI of two different assets, being good predictors of each other’s future returns) are also quite rare, with only two such edges, which is, again, much higher than the expected value of 0.23.

Lastly, we test whether this network is structurally similar to any of the main types of networks usually observed in practice. The degrees of many real-world networks follow a power-law distribution; to this end, we employ the test of [Clauset et al., 2009], to test the null hypothesis that in/out-degrees follow a power-law. As shown in Figure 20, the network degrees do not appear to follow such a power-law distribution. In particular, five of the networks reject the null hypothesis that in-degrees follow a power-law distribution, while six of the networks reject the equivalent hypothesis for out-degrees.

Let , and , denote the in- and out-degrees of node , respectively. Furthermore, let

denote the empirical edge density corresponding to node . Another question is whether the differences between network degrees are statistically significant. In particular, assume that a node’s in- and out-degrees follow a binomial distribution, i.e

Then, we can form the following hypotheses

If the network is a simple Erdős-Rényi network, then both hypotheses should hold in conjunction. To test whether node and node degrees are similar, we use the conservative two-sample binomial t-test, with test statistic

Under the null hypothesis, we have . To account for multiple testing, we once again use a Bonferonni correction by setting the p-value equal to .

Note that such a test is very conservative, both due to the Bonferonni correction, but also the choice of a t-test for the pairwise difference tests. Indeed, for both in- and out-degrees, smaller networks (fully Bonferonni corrected) do not result in any rejections of the null hypothesis. This is different for the larger networks, as we see a 5-12% rejection rate for the row-level Bonferonni corrected networks, and a 41-58% rejection rate for the uncorrected networks. Thus, the networks at hand seem to neither follow a power-law nor form an Erdos-Renyi network, as there are significant differences between node degrees.

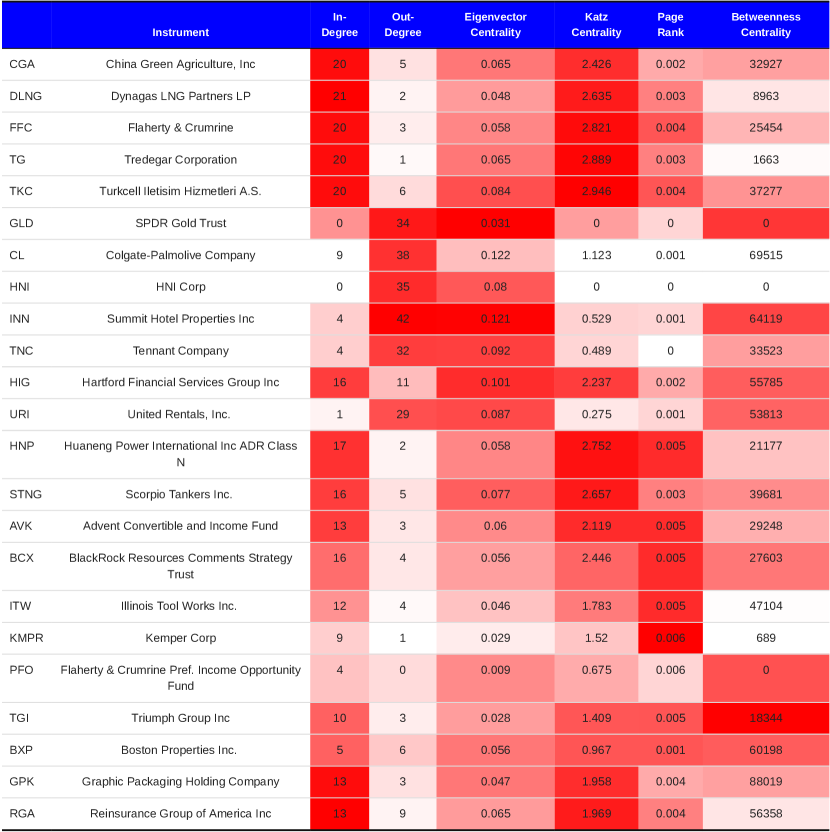

In Section 2 of the Supplementary Material, we provide additional results based on the Q3 row-level Bonferonni corrected network. We show differences in the average degrees of different sectors, and list some of the instruments with the highest centralities, demonstrating a more central role within the network.

8 Conclusion and future research directions

In this paper, we have defined the OVI feature and showed how it can act as a predictor for future equity returns. Focusing on the PHLX exchange, we compared OVI across MPCs, and found that the Market Maker’ OVI consistently provides the highest predictability, yielding annualized Sharpe Ratios of up to 4.5, for a simple betting scheme (without taking into account transaction costs). In terms of PnL, the tail portfolios corresponding to the strongest signals, can attain up to 4 bpts per day, depending on the sizing scheme employed. We have shown that some level of predictability is also present for Customer and Broker OVIs, while no predictability was concluded for Firm Proprietary trades and Professional Customers. We demonstrated how to improve performance, by taking into account the OVI’s magnitude. In particular, when using quantile rank groups, we found that the - quantile rank groups are typically the best performing.

We showed that most of the predictability is present in either Buys or Sells depending on the MPC and the data set used. Decomposing into opening or closing transactions did not significantly affect the observed predictability. However, decomposing transactions based on certain option features significantly affects predictability. In particular, the OVI from high implied volatility contracts is significantly more informative than option contracts with low implied volatility. Other option characteristics that seem to consistently induce higher performance include negative values for Rho, and negative values for Delta (i.e put options). We have also shown that cross-impact effects are present, and in fact, significantly outnumber the cases of direct impact, when applying a conservative Bonferonni Correction. Results obtained for the NOM exchanged (NOTO data set) are consistent with those obtained on the PHLX exchange (PHOTO data set), albeit weaker, with Market Makers still showing a significant annualized SR of around 2.5–3.

Another contribution of this paper was the introduction a new approach to tackling future returns regression, namely the P&L regression, which was motivated by the needs of this particular research, but may also be of independent interest for other financial studies. This approach, while slightly more intricate than a simple OLS method, is problem-tailored for directional predictions, bypasses the requirement for linear effects, and is able to work under sparse data. We have, for the most part, avoided the usage of linear methods, and focused on the usage of metrics like the SR, providing a general framework for analyzing return prediction tasks.

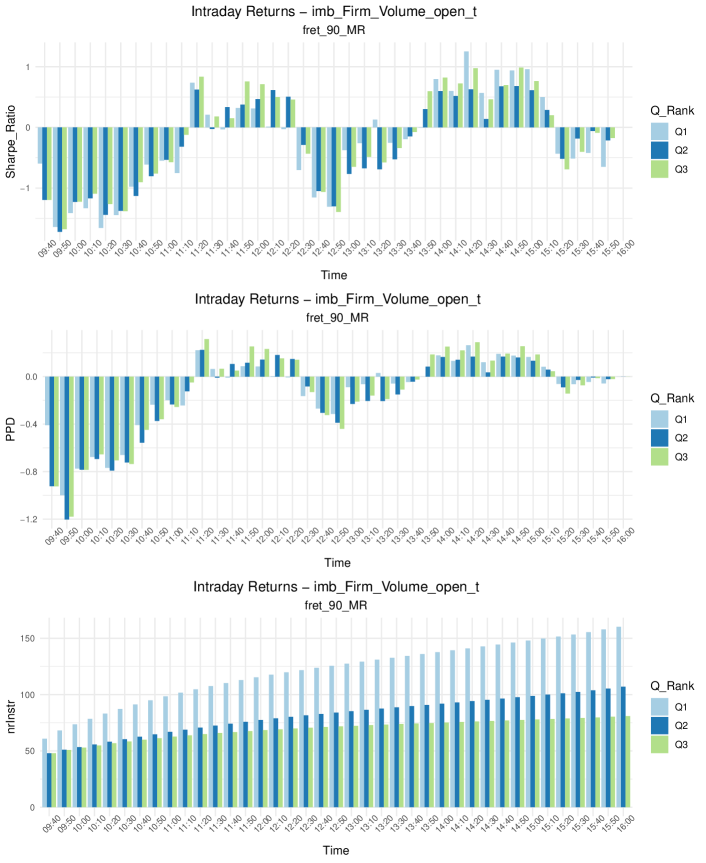

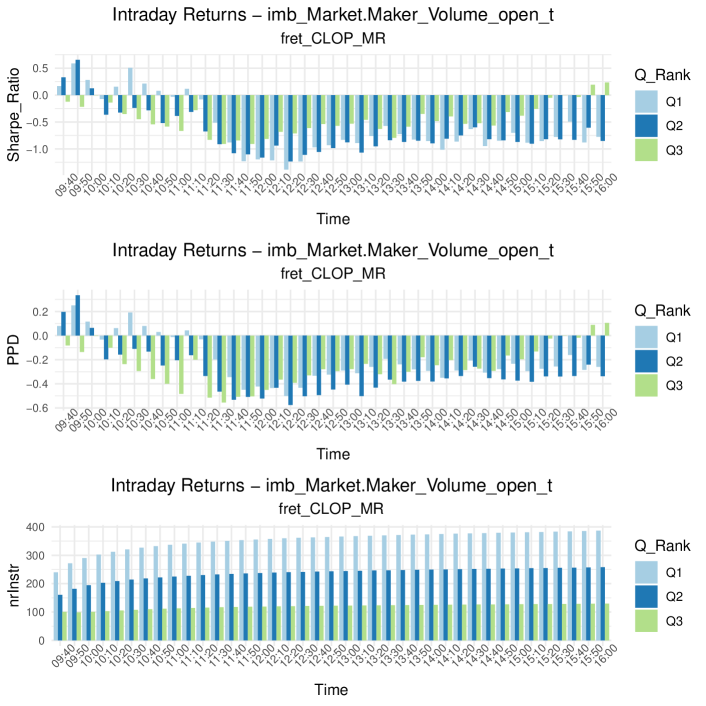

This research could lead to further studies that examine option volumes from different data sets, and at different time horizons. This research could also be extended to an intraday analysis (given that data comes in batches of 10-minute bucket increments), which we consider in Section 3 of the Supplementary Material. This led to promising observations, which we have not been able to quantitatively approach, due to our limited access to intraday data. Another interesting angle would include a study of the interplay between option and stock volumes, and ultimately the prediction of future volumes (for both the option and stock markets), which would be of potential interest for market making and optimal execution.

Acknowledgments

This work was supported by the UK Engineering and Physical Sciences Research Council (EPSRC) grants EP/R513295/1 and EP/V520202/1. We would also like to thank Rama Cont and Stefan Zohren for their valuable and productive feedback.

References

- [Amin and Lee, 1997] Amin, K. I. and Lee, C. M. C. (1997). Option trading, price discovery, and earnings news dissemination*. Contemporary Accounting Research, 14(2):153–192.