High-dimensional model-assisted inference for treatment effects with multi-valued treatments

Wenfu Xu111Wenfu Xu is Assistant Professor, College of Economics and Management, China Jiliang University, Hangzhou 310018, China (E-mail:wf.xu@cjlu.edu.cn), and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854, USA (E-mail:ztan@stat.rutgers.edu). This work was completed when Wenfu Xu was visiting Rutgers University. and Zhiqiang Tan111Wenfu Xu is Assistant Professor, College of Economics and Management, China Jiliang University, Hangzhou 310018, China (E-mail:wf.xu@cjlu.edu.cn), and Zhiqiang Tan is Professor, Department of Statistics, Rutgers University, Piscataway, NJ 08854, USA (E-mail:ztan@stat.rutgers.edu). This work was completed when Wenfu Xu was visiting Rutgers University.

Abstract

Consider estimation of average treatment effects with multi-valued treatments using augmented inverse probability weighted (IPW) estimators, depending on outcome regression and propensity score models in high-dimensional settings. These regression models are often fitted by regularized likelihood-based estimation, while ignoring how the fitted functions are used in the subsequent inference about the treatment parameters. Such separate estimation can be associated with known difficulties in existing methods. We develop regularized calibrated estimation for fitting propensity score and outcome regression models, where sparsity-including penalties are employed to facilitate variable selection but the loss functions are carefully chosen such that valid confidence intervals can be obtained under possible model misspecification. Unlike in the case of binary treatments, the usual augmented IPW estimator is generalized by allowing different copies of coefficient estimators in outcome regression to ensure just-identification. For propensity score estimation, the new loss function and estimating functions are directly tied to achieving covariate balance between weighted treatment groups. We develop practical numerical algorithms for computing the regularized calibrated estimators with group Lasso by innovatively exploiting Fisher scoring, and provide rigorous high-dimensional analysis for the resulting augmented IPW estimators under suitable sparsity conditions, while tackling technical issues absent or overlooked in previous analyses. We present simulation studies and an empirical application to estimate the effects of maternal smoking on birth weights. The proposed methods are implemented in the R package mRCAL.

Key words and phrases:

Multi-valued treatment; Average treatment effect; Calibrated estimation; Doubly robust estimation; Group Lasso; Propensity score; Regularized M-estimation.

1 Introduction

Estimation of average treatment effects (ATEs) has been extensively studied in the potential-outcome framework for causal inference (Neyman 1923; Rubin 1974). As a distinctive feature of the problem, doubly robust (DR) methods are available to achieve consistent estimation if either an outcome regression (OR) model is correctly specified for the outcome given treatment and covariates or a propensity score (PS) model is correctly specified for the treatment given covariates (e.g., Tan 2007). All such methods can be viewed to involve two stages of estimation. First, OR and PS models are built and fitted as regression models. Then the fitted functions are substituted into a DR point estimator, notably the augmented inverse probability weighted (IPW) estimator (Robins et al. 1994). Conventionally, the two stages are treated separately: regression models in the first stage are built and fitted by maximum likelihood or variants, while ignoring how the fitted functions are used in the second stage. Such separate estimation can be associated with known difficulties in the existing methods. For example, augmented IPW estimation may perform poorly if the PS model appears to be nearly correct and fitted by maximum likelihood (Kang and Schafer 2007). There is another difficulty more recently recognized in the high-dimensional settings (Tan 2020b). If the OR and PS models are fitted by regularized maximum likelihood, then DR point estimation can be achieved by the augmented IPW estimator, but valid confidence intervals are obtained under suitable sparsity conditions only when both the OR and PS models are correctly specified (or with negligible specification biases) (Chernozhukov et al. 2018).

In this article, we develop new methods and theory for fitting OR and PS models while using augmented IPW estimation to draw inferences about ATEs with multi-valued treatments in high-dimensional settings, where the number of regressors is close to or greater than the sample size . Estimation of average treatment effects on the treated (ATTs) are also handled in a unified manner. Compared with existing methods, the aforementioned two stages of estimation are integrated in our approach, called regularized calibrated estimation. We employ regularized estimation for fitting the OR and PS models, where sparsity-inducing penalties such as the Lasso or group Lasso penalty are used to facilitate variable selection (Tibshirani 1996; Yuan and Lin 2006). However, we carefully choose the loss functions (or equivalently estimating functions determined from the gradients), depending on augmented IPW estimation in the second stage, such that valid confidence intervals can be obtained for the treatment parameters under suitable sparsity conditions in high-dimensional settings, while accommodating possible model misspecification. In fact, our methods not only lead to DR point estimation but also provide DR confidence intervals for ATEs and ATTs, which are valid if either a multi-class logistic PS model or a linear OR model is correctly specified. Our methods also provide model-assisted confidence intervals for the treatment parameters, which are valid if a multi-class logistic PS model is correctly specified, but a generalized linear OR model may be misspecified. Another advantage of our approach is that the new loss function and estimating functions for PS estimation are directly tied to evaluation of covariate balance after inverse probability weighting with a multi-valued treatment. By analysis of Bregman divergences, minimization of the expected loss function can be shown to control relative errors of propensity scores more effectively than maximum likelihood with possible model misspecification. See Remark 1 and Appendix A.

Our work builds on the recent success of using regularized calibrated estimation for treatment effect estimation with binary treatments and instruments (Tan 2020ab; Sun and Tan 2021), but needs to tackle various analytical and computational complications due to multi-valued treatments. In the case of binary treatments, there are two sets of calibration equations associated with the augmented IPW estimator. One set is just-identifying for the regression coefficients in the PS model, and the other is just-identifying for those in the OR model. These calibration equations can be directly converted into two corresponding loss functions for regularized estimation (Tan 2020b). For a multi-valued treatment, calibration equations derived from the usual augmented IPW estimator are no longer just-identifying for the coefficients in the PS model and separately in the OR model. This complication is related to the fact that a multi-class logistic PS model involves free coefficients, but an OR model involves only coefficients within a fixed treatment group, where is the number of treatment groups. To make progress, we exploit a natural relationship between the two types of expectations in ATEs and ATTs:

| (1) |

where denotes the potential outcome for treatment . Then we define a new augmented IPW estimator for , by decomposing the usual augmented IPW estimator for in terms of augmented IPW estimators of as in (1), while allowing different copies of the coefficient vector in the same OR model for given and for . We show that this approach leads to calibration equations which are just-identifying for the PS coefficient vectors and separately for the copies of the OR coefficient vector and can be converted into convex loss functions for regularized estimation. In particular, the new loss function for PS estimation properly extends the calibration loss in Tan (2020a) to multi-class logistic regression (see Remark 4).

We develop practical numerical algorithms for computing the regularized calibrated estimators with group Lasso penalties (Yuan and Lin 2006). Our algorithms use quadratic approximation (Friedman et al. 2010) and the majorization-minimiation (MM) technique (Wu and Lange 2010), but innovatively exploit Fisher scoring (McCullagh and Nelder 1989) to construct closed-form updates based on the block coordinate descent (Simon et al. 2013). Furthermore, we provide rigorous high-dimensional analysis of the group-Lasso regularized calibrated estimators and the resulting augmented IPW estimators for the treatment parameters with possible model misspecification. Our analysis establishes that doubly robust or model-assisted Wald confidence intervals can be obtained for the treatment parameters as described earlier under the sparsity condition, , where and denote the non-sparsity sizes in PS and OR estimation. Compared with previous high-dimensional analyses, we carefully tackle several technical issues, including the interdependency between the gradient vectors of the loss functions in both PS and OR estimation and the data-dependency of an estimated weight in OR estimation (see Remarks 7–9). These two issues are absent in previous analysis of multi-task linear regression with group Lasso, where tasks are independent of each other (Lounici et al. 2011). The interdependency of gradient vectors appears to be overlooked in analysis of regularized likelihood estimation with group Lasso for multi-class logistic regression in Farrell (2015).

A theoretical limitation of the proposed method is that the confidence intervals are not doubly robust for the treatment parameters unless a linear OR model is used. This limitation can be traced to the fact that PS estimation and evaluation of covariate balance are designed to be applicable in our method without access to any outcome data, which is a desirable property for the PS methodology to avoid bias from outcome modeling (Rubin 2001). Doubly robust confidence intervals can be developed, by adapting the approach of Ghosh and Tan (2021), but PS and OR estimation would then be coupled to each other. See Tan (2020b, Section 3.5) for related discussion.

Related work. There is a vast and growing literature on estimation of average treatment effects. We discuss directly related work to ours, in addition to the earlier discussion.

Theory and methods for ATE estimation have been extensively studied in low-dimensional settings with binary or multi-valued treatments. The case of a multi-valued treatment is often treated as a direct extension from the case of a binary treatment (e.g., Cattaneo 2010; Tan 2010). For DR estimation, it is common to fit a generalized linear OR model and a multi-class logistic PS model by maximum likelihood or quasi-likelihood, from which the fitted values can be combined, sometimes with additional adjustment, for augmented IPW estimation. For PS estimation with a multi-valued treatment, Imai and Ratkovic (2014, Section 4.1) briefly discussed a set of covariate balancing equations, which appear related to our calibration equations (20) or equivalently (26) later. However, there exist important differences: the balancing equations are based on contrasts of IPW averages of covariates between successive treatment groups (0 vs 1, 1 vs 2, etc.), instead of contrasts of probability ratio weighted and simple averages between one treatment group and the remaining ones. In general, the set of balance equations cannot be converted into a loss function (much less a convex loss) and need to be solved as nonlinear equations or combined with score equations from maximum likelihood using the generalized method of moments. Adaption of such equations seems difficult numerically and theoretically in high-dimensional settings.

As an alternative to maximum likelihood estimation, calibrated estimation and related methods have also been studied in low-dimensional settings for fitting PS models in causal inference with binary treatments or fitting response probability models in survey sampling and missing-data problems, where the non-missingness probability represents a propensity score (e.g., Folsom 1991; Tan 2010; Graham et al. 2012; Hainmueller 2012; Imai and Ratkovic 2014; Kim and Haziza 2014; Vermeulen and Vansteelandt 2015). In the binary case, calibrated estimation requires that the IPW averages of covariates in the treated subsample are equal to the simple averages in the overall sample. These equations can also be seen to match the probability ratio weighted averages of covariates in the treated subsample with the simple averages in the untreated subsample (Tan 2020a, Section 7.4), thereby aligned with calibration equations (26) in our multi-valued extension.

For DR estimation of ATEs with binary treatments, Kim and Haziza (2014) and Vermeulen and Vansteelandt (2015) proposed estimating equations which are equivalent to the calibration equations in Tan (2020b). In low-dimensional settings, one of the benefits is to enable computationally simpler variance estimation for augmented IPW estimators, compared with likelihood-based estimation in fitting PS and OR models. In contrast, calibration equations are exploited by Tan (2020b) to develop regularized calibrated estimation for fitting PS and OR models such that doubly robust or model-assisted confidence intervals can be obtained for ATEs in high-dimensional settings. Regularized calibrated estimation has also been proposed by Sun and Tan (2021) for estimating local average treatment effects (LATEs) with instrumental variables, and extended by Ghosh and Tan (2021) to general semiparametric estimation based on DR estimating functions. The calibration equations in the latter work are assumed to be just-identifying for two sets of nuisance parameters to be estimated. But this assumption is not satisfied in ATE estimation with a multi-valued treatment, which is a major challenge addressed in the current work.

In high-dimensional settings, DR estimating functions have also been used to derive valid confidence intervals under suitable sparsity conditions in Belloni et al. (2014) with binary treatments and Farrell (2015) with multi-valued treatments for ATEs, and in Chernozhukov et al. (2018) for more general treatment parameters. As mentioned earlier, regularized likelihood-based estimation is employed in these methods, and the confidence intervals are only shown to be valid for the treatment parameters when all working models for the nuisance parameters are correctly specified (or with negligible biases). To alleviate this limitation, there has been considerable research in high-dimensional causal inference. Examples related to regularized calibrated estimation include Avagyan and Vansteelandt (2017), Smucler et al. (2019), Bradic et al. (2019), and Ning et al. (2020) among others. However, these methods mainly deal with ATE estimation with binary treatments, and would not be applicable to the case of multi-valued treatments.

2 Setup and existing methods

Suppose that are independent and identically distributed observations of , where is an observed outcome, is an observed treatment, and is a vector of covariates. The treatment is assumed to take possible values, denoted as , where denotes the null treatment. Let be the potential outcome that would be observed under treatment (Neyman 1923; Rubin 1974). We make the consistency assumption that if . The average treatment effect (ATE) for treatment versus is defined as , where for . The average treatment effect in the th treated group (ATT) is defined as for . We mainly discuss estimation of and ATEs until Section 5 on ATT estimation.

A fundamental difficulty in estimating ATEs is that for each subject , only one potential outcome is observed, if , and the others are missing. Nevertheless, the means can be identified from observed data under two assumptions:

-

•

Unconfoundedness: and are conditionally independent given for (Rubin 1976), where , equal to 1 if or 0 otherwise;

-

•

Overlap: almost surely for , where is called the propensity score (Rosenbaum and Rubin 1983).

Under the foregoing assumptions, ATE estimation from sample data customarily involves two stages. First, regression models are built and fitted for the outcome regression (OR) function or the propensity score (PS) . In the second stage, the fitted functions are substituted into various estimators for and ATEs. To facilitate discussion in Section 3, we describe regression models with pre-specified regression terms and regularized likelihood estimation commonly used in these models. We also introduce augmented IPW estimation for , which is used in the proposed method and existing ones.

Consider an outcome regression model

| (2) |

where is an inverse link function, is a vector of known functions of covariates (for example, main effects or interactions) with , and is a vector of unknown coefficients for . For concreteness, model (2) is specified to allow separate coefficient vectors associated with different treatments . For a generalized linear model with a canonical link (McCullagh and Nelder 1989), the average negative log-(quasi)-likelihood function in is , where . Throughout, denotes the sample average, for example, . In high-dimensional settings (i.e., large relative to ), a regularized maximum likelihood (RML) estimator, , for can be defined by separately minimizing the likelihood loss with a Lasso penalty (Tibshirani 1996):

| (3) |

where denotes the norm, is excluding the intercept , and is a tuning parameter. Alternatively, a group Lasso penalty (Yuan and Lin 2006; Farrell 2015) can be used to define regularized estimators jointly as a minimizer to

| (4) |

where denotes the norm, consists of coefficients associated with the covariate term , and is a tuning parameter.

Next, consider a multi-class logistic model for the propensity score:

| (5) |

where is a vector of known functions of covariates with , is a vector of unknown coefficients for , and is a matrix. The average negative log-likelihood function is . In high-dimensional settings (i.e., large relative to ), a regularized likelihood estimator can be defined by minimizing the likelihood loss with a group Lasso penalty (Simon et al. 2013; Farrell 2015):

| (6) |

where the intercepts are not penalized, consists of coefficients associated with the covariate term , and is a tuning parameter. For non-penalized estimation (), two constraints are commonly used to ensure identification. One is a one-to-zero constraint, for example, . The other is the sum-to-zero constraint . For penalized estimation, there is a slight difference between use of the two constraints. If the one-to-zero constraint is used, then can be reduced to a matrix and to a vector . If the sum-to-zero constraint is used, then only the intercepts need to be explicitly constrained, , because minimization of (6) with automatically implies that holds for . See the Supplement Section II.1 for a corrected proof of the sum-to-zero relationship originally discussed in Simon et al. (2013).

Various estimators of can be employed, using fitted values from OR model (2) or PS model (5) or both (Tan 2007, 2010a). In particular, there are doubly robust (DR) estimators depending on both OR and PS models in the augmented IPW form (Robins et al. 1994)

| (7) |

where and for some estimators and , and

In high-dimensional settings, Farrell (2015) studied the estimator , using the group Lasso penalized estimators and described above, where and . Two types of results are obtained, each under suitable sparsity conditions. First, is shown to be pointwise doubly robust, i.e., remain consistent if either model (2) or model (5) is correctly specified. Second, is shown to admit an asymptotic expansion which leads to valid Wald confidence intervals for if both models (2) and (5) are correctly specified. See Remark 9 for further discussion.

3 Proposed method

We develop regularized calibrated estimation (RCAL) to tackle ATE estimation with multi-valued treatments in high-dimensional settings, where a large number of regression terms are allowed in OR and PS models. Our approach exploits an interesting generalization of the augmented IPW estimator in (7), and derives a novel set of regularized calibrated estimators when fitting OR model (2) and PS model (5), such that valid Wald confidence intervals can be obtained without requiring both models (2) and (5) are correctly specified.

3.1 Regularized calibrated estimation

For technical convenience, consider the OR model (2) and PS model (5) with the same regressor vectors used (hence ). Otherwise, models (2) and (5) can be enlarged by taking the union of the regressors. Then the OR model can be stated as

| (8) |

where is the same vector of regressors as in model (5), including main effects and interactions of the covariate vector . This choice seems inconsequential, because different subsets of with nonzero coefficients are allowed in models (5) and (8).

As mentioned in Section 2, ATE estimation can be viewed as two-stage semi-parametric estimation, where OR and PS models are fitted to obtain , and then the augmented IPW estimator is used to estimate . Our approach involves two main elements in the first-stage estimation. First, we employ regularized estimation with sparsity-inducing penalties such as the Lasso or group Lasso penalty (Tibshirani 1996; Yuan and Lin 2006), to deal with the large number of regressors under sparsity assumptions. Second, we carefully choose the loss functions for regularized estimation, such that the resulting estimator for admits an asymptotic expansion about in the usual order , and hence valid Wald confidence intervals can be obtained for and ATEs, while allowing for model misspecification. Moreover, the new loss function for PS estimation can be directly tied to evaluation of covariate balance. Unless otherwise stated, we discuss estimation of for a fixed treatment and denote as a generic treatment.

Calibration equations. We derive calibration equations for and in the augmented IPW estimator with possible model misspecification, by similar reasoning as in Tan (2020b) and Ghosh and Tan (2020). Suppose that converges in probability to a limit (or target) value and converges in probability to a limit (or target) value as , such that

- •

- •

For convenience, we fix in in the following discussion. Then a Taylor expansion of yields

| (9) |

where , , and the remainder is taken to be under suitable conditions. For calibrated estimation, a basic idea is that if the derivatives with respect to and , , in (9) have means 0, referred to as calibration equation:

| (10) | |||

| (11) |

then it can be shown that the second and third terms on the right-hand side of (9) reduces to and hence admits the asymptotic expansion

| (12) |

under certain sparsity conditions. The expansion (12) appears similar to the expansion

| (13) |

which is satisfied for the regularized likelihood estimators under suitable conditions if both models (5) and (8) are correctly specified (Farrell 2015). However, an important difference between (12) and (13) is that the expansion (12) is expected to hold even when models (5) and (8) may be misspecified, provided that the estimators and , , are constructed with the limit values satisfying calibration equations (10)–(11). If model (5) or (8) is correctly specified, then or respectively and has mean equal to by the double robustness of augmented IPW estimation. In either case, the expansion (12) implies that the estimator admits as the influence function, and hence valid Wald confidence intervals for can be obtained in the usual manner.

Sequential calibration estimation. While the preceding discussion outlines basic reasoning for our approach, there are nontrivial complications which we need to address. For simplicity, assume that OR model (8) is linear with . Then calibration equations (10) and (11), with , can be directly shown to yield

| (14) | |||

| (15) |

There are free coefficients in , but only equations in (14), whereas there are free coefficients in , but equations in (15). For multi-valued treatments (), equations (14)–(15) are under-identifying in , , but over-identifying in . In addition, solving nonlinear equations such as sample versions of (14)–(15), even if theoretically just-identifying, may suffer the issue of no solution or multiple solutions (Small et al. 2000).

To tackle the foregoing issues, we introduce , , as separate versions of and generalize the augmented IPW estimator in (7) as

| (16) |

where , , and

| (17) | ||||

| (18) |

Because different estimators , , are allowed, in (16) depends on for all , not just as in (7). If , , are all defined to be the same as , then (16) reduces to (7). Interestingly, is directly an unbiased estimator of , and can be identified as an augmented IPW estimator of the expectation for . Hence (16) corresponds to a natural decomposition of the mean in ATEs into the means of potential outcomes involved in ATTs, as stated in equation (1). See Section 5 for further discussion.

Next, we apply similar reasoning as (9)–(11) to the estimator . With , a Taylor expansion of yields

| (19) |

where and is the limit value of , . Setting the expectations of the derivative terms above to 0 leads to the calibration equations:

| (20) | |||

| (21) |

For symmetry, is replaced by for including to remove the constraint . Remarkably, equations (20) are just-identifying in , and, given , equations (21) are just-identifying in . In fact, (20) can be shown to be the stationary condition for minimizing the expected loss , where

| (22) |

is a convex loss in , different from the likelihood loss . Moreover, (21) can be shown to be the stationary condition for minimizing the expected loss , where

| (23) |

is a weighted least squares loss for regression of on in treatment group , with the weight depending on . Different for is associated with different weights. The losses and are called the calibration (CAL) loss in and respectively, and is also called the weighted least squares or likelihood (WL) loss.

For a nonlinear OR model (8), calibration equations obtained from the derivative terms with respect to in (19) are the same as (21), whereas those from the derivative terms with respect to are of a more complicated form than (20):

| (24) |

where denotes the derivative of . Compared with (20) for a linear OR model, equations (24) involve both and , , and hence the sample versions of (21) and (24) cannot be solved sequentially or inverted to define loss functions sequentially as above. To circumvent this complication, we employ sequential calibration as follows: retain the loss function in and then invert the calibration equation (21) to obtain the loss function in :

| (25) |

where . The loss (25) is a weighted version of the likelihood loss in Section 2. The weighted least squares loss (23) is recovered in the special case of a linear OR model, and . This approach has two main advantages. First, as discussed below, the loss functions can be used sequentially for regularized estimation in a computationally convenient manner. Second, the calibration loss can be desirable for PS estimation, independently of outcome regression, in terms of both the informative form of calibration equations (20) and a strong relationship between minimization of the expected calibration loss and reduction of relative errors in propensity scores, which are discussed in Remark 1 and Appendix A.

Remark 1 (PS calibration equations).

Although derived for achieving desirable asymptotic expansions, the calibration equations for PS estimation are directly related to covariate balance after inverse probability weighting. In fact, the calibration equations (20) can be rewritten as

| (26) |

which indicates that the weighted mean of in the th treated group is matched with the simple mean of in the th treated group. The weight used in (26) is the probability ratio related to ATT estimation. Summing the two sides of (26) over yields , that is, calibration equations (14) derived from the usual augmented IPW estimator . Equation (14) indicates that the weighted mean of in the th treated group is matched with the mean of in the population, with the weight being the inverse probability , typically found in ATE estimation. However, equations (26) over all choices are just-identifying in whereas equations (14) are not, unless in the case of binary treatments where the equations are equivalent (Tan 2020a, Section 7.4).

Lasso regularized estimation. In high-dimensional settings, we combine the calibration losses in (22) and (23) or (25) with Lasso-type penalties to define regularized calibrated estimators and , , which are then substituted into the estimator (16) for . To exploit group sparsity in coefficients associated with different covariate terms, we incorporate group Lasso penalties with the calibration losses. First, define the estimator as a minimizer of

| (27) |

where is the transpose of the row vector in associated with , and is a tuning parameter. Similarly to discussed earlier, either a one-to-zero constraint or the sum-to-zero constraint can be used for identification. For simplicity, we fix the one-to-zero constraint and use the notation as a matrix and as a vector, whenever needed from the context.

Instead of the generic constraint , our choice is aligned with the fact that the calibration loss in (22) depends on the treatment for which is estimated, whereas the likelihood loss is invariant regardless of which treatment is considered for estimation of (see Remark 2). By the constraint , the loss function becomes separable in , which then leads to both a simple quadratic approximation (31) to for numerical implementation and a simple compatibility condition in Assumption 1(iii) for theoretical analysis. We defer to Supplement Section II the material about use of the sum-to-zero constraint and comparison with the one-to-zero constraint.

Next, we form a combined loss , and define the estimator as a minimizer of

| (28) |

where is a matrix, is the transpose of the row vector in associated with , and is a tuning parameter. See Appendix B for implications from the Karush–Kuhn–Tucker conditions for minimization of (27) and (28).

Wald confidence intervals. From regularized calibrated estimation, the resulting estimator (16) for is , where and , . In Section 4.2, we show that if PS model (5) is correctly specified but OR model (8) may be misspecified, then admits an asymptotic expansion similar to (12) under suitable sparsity conditions:

| (29) |

where , , , and and are the limit values of , , and respectively. Then an asymptotic confidence interval for can be obtained as , where is the quantile of and, with defined in (17),

| (30) |

For a linear OR model, the asymptotic expansion (29) can be established, with possible misspecification of both models (8) and (5). In this case, the confidence intervals for are doubly robust, being also valid when model (8) is correctly specified, but model (5) may be misspecified.

For a nonlinear OR model, our approach does not in theory lead to doubly robust confidence intervals for , because calibration equations (21) and (24) are not fully taken into account as discussed above. Alternatively, doubly robust confidence intervals can be investigated, while exploiting the calibration equations (21) and (24) based on proposed here. Such methods tend to involve more complex theory and implementation, for example, sample splitting and cross fitting in Smucler et al. (2019) and iterations of regularized calibrated estimation in Ghosh and Tan (2020). Hence our approach is expected to remain useful in applications.

Remark 2 (Separate PS estimation).

A subtle feature of our method is that for fitting the PS model (5), the loss and the estimator depend on the treatment for which the mean is estimated. Such dependency on is suppressed in the notation for simplicity, but needs to be noticed throughout. Hence when estimating different means for , separate estimators of are required in our method, whereas a single estimator of is used in existing methods as described in Section 2. This scheme of separate estimation of propensity scores is inherent to our method, and may be advantageous in allowing treatment-specific approximations in the presence of model misspecification. See Tan (2020b), Section 3.5, for related discussion.

Remark 3 (Separate OR estimation).

There are also important differences between our method and existing methods in handling outcome regression. Farrell (2015) employed the penalized objective function (4), by combining individual loss functions in separate treatment groups and adding a group Lasso penalty, which encourages a small subset of important regressors, with nonzero , for outcome regression over different treatment groups. In contrast, our penalized objection function (28) combines individual loss functions in the fixed treatment group but depending on separate versions of through different weights in outcome regression. A group Lasso penalty is then introduced to encourage a small subset of important regressors, with nonzero , for outcome regression with different weights. Hence for estimating the mean , our method exploits separate versions of weighted outcome regression within treatment group , instead of combining outcome regression across all treatment groups as in Farrell (2015).

Remark 4 (Binary treatments).

We discuss how the proposed method generalizes that in Tan (2020ab) with binary treatments. Take and fix . First, the calibration loss in (22) becomes . By minimization of the penalized loss (27) with the constraint , the estimator is defined such that or equivalently , where is excluding the intercept for . The loss function in only,

is precisely the calibration loss for fitting PS models with binary treatments in Tan (2020ab). Hence the same fitted propensity score can be obtained from Tan (2020ab) with the same tuning parameter . Second, the loss in (25) can be easily shown to coincide with the weighted likelihood loss for fitting OR models in Tan (2020b), where is the only version of and . The group Lasso penalty in (28) also reduces to the Lasso penalty. Hence the same fitted function can be obtained from Tan (2020b) using the same tuning parameter . Finally, the generalized estimator in (16) can be directly shown to coincide with the original version in (7) with binary treatments. Therefore, our estimator for recovers that in Tan (2020b), using the same fitted PS and OR functions.

3.2 Computation

We propose Fisher scoring block coordinate descent algorithms for computing the estimators and , that is, minimizing the objective functions (27) for a fixed and (28) for a fixed . Compared with existing algorithms for group-penalized multi-response and multinomial regression (Simon et al. 2013), our algorithms for both and are derived by innovatively incorporating Fisher scoring before forming a majorizing quadratic approximation to the loss function used and solving a multi-response group-Lasso least-square problem in each iteration. Previously, Fisher scoring is used in the iterative reweighted least squares algorithm for fitting generalized linear models with noncanonical links, such as probit regression (McCullagh and Nelder 1989).

Algorithm for computing . We fix and use the notation and as mentioned below (27). A second-order Taylor expansion of at the current estimate, denoted as , gives the quadratic approximation

| (31) |

where with for , and . Incidentally, if the sum-to-zero constraint is used on , then a quadratic approximation to can also be obtained in the form (31), but with a non-diagonal matrix. See Supplement Section II.3 for a discussion about computation of with the sum-to-zero constraint, where a diagonal matrix dominating is used.

The quadratic function cannot be directly related to a weighted least-square loss as in Simon et al. (2013): the quadratic term in depends on only the observations in the th treated group, but the linear term depends on all the observations from the treatment groups. By Fisher scoring, we replace by its model expectation, which equals 1, and obtain the quadratic approximation

where both the quadratic and linear terms depend on all observations in the sample. Then can be viewed as a weighted least-square loss for multi-response linear regression.

To facilitate block coordinate descent with closed-form updates, we employ the majorization-minimization (MM) technique (Wu and Lange 2010), similarly as in related algorithms (Simon et al. 2013). For the diagonal matrix , we use the simple majorization , where and is the identity matrix. By the quadratic lower bound principle (Bohning and Lindsay 1988), a majorizing function of is

Combining with the group Lasso penalty as in (27) leads to

| (32) |

Minimization of (32) corresponds to a group-penalized least-square estimation for multi-response linear regression with the same design matrix for each response. Then the block coordinate update has the closed form

| (33) |

where is the partial residual.

A complication from Fisher scoring, i.e., replacement of by is that the quadratic function , even though a majoring function of , may not be a majorizing function of . Hence minimization of (32) may not guarantee a decrease in the objective function (27), as otherwise would be achieved by the MM technique. To restore the descent property, we incorporate a backtracking line search similarly as in Tan (2020a).

From the preceding discussion, we obtain the algorithm for computing .

Algorithm 1. Fisher scoring block descent algorithm for minimizing (27).

-

1.

Set an initial value .

- 2.

Algorithm for computing . A second-order Taylor expansion of the loss function in (28), , at the current estimate, denoted as , gives the quadratic approximation

where with and .

In contrast with discussed earlier, the quadratic function can be recast as a weighted least-squares loss in multi-response linear regression, because both the quadratic and linear terms here depend on only the observations from th treated group. Nevertheless, Fisher scoring can be exploited to address another complication. For fast implementation of block coordinate descent, it is desirable to find a constant such that the weight matrices , , are dominated by , where is the identity matrix. Although these weight matrices are diagonal, the th entry on the diagonal of the th weight matrix is a product of and , which may be inflated for small . Taking the maximum of the diagonal entries of the weight matrices would lead to unnecessarily large and slow convergence.

By Fisher scoring, we replace by its model expectation, which equals 1, and obtain the quadratic approximation

The weight matrices can be dominated as for , where , which does not suffer the inflation due to large probability ratios. By the quadratic lower bound principle (Bohning and Lindsay 1988), a majorizing function of is

Combining with the group Lasso penalty as in (28) yields

| (34) |

Minimization of (34) corresponds to a group penalized multi-response linear regression with the same design matrix for each response. Then the block coordinate update has the closed form

| (35) |

where is the partial residual.

Similarly as in Algorithm 1 for computing , we incorporate a backtracking line search to maintain the descent of the objective function (28), which may be violated due to the use of Fisher scoring. Hence our algorithm for computing is as follows.

Algorithm 2. Fisher scoring block descent algorithm for minimizing (28).

-

1.

Set an initial value .

- 2.

4 Theoretical properties

We study statistical properties of the regularized calibrated estimators and the augmented IPW estimator , for a fixed treatment in high-dimensional settings. In particular, we establish the asymptotic expansion (29) and consistency of the estimated variance , which lead to valid Wald confidence intervals for as described in Section 3.1. For , confidence intervals for the ATE, , can be obtained by standard arguments from the asymptotic expansions of and the corresponding estimator for , which requires a separate set of regularized calibrated estimators as explained in Remarks 2–3.

4.1 Estimation of regression coefficients

We develop theoretical analysis of the regularized calibrated estimators with multi-class logistic PS model (5) and OR model (8) in high-dimensional settings. Compared with existing high-dimensional theory (Buhlmann and van de Geer 2011), our analysis needs to deal with several technical complications including the interdependency of multiple responses on each subject in the loss functions and , the dependency of the estimator on , and possible misspecification of both models (5) and (8).

First, we study the regularized calibrated estimator . The tuning parameter in the penalized objective function (27) is specified as , with a constant , and

where comes from Assumption 1 below, and is a tail probability for the error bound, to be discussed below.

With possible misspecification of model (5), the limit (or target) value of , denoted as , can be identified as a minimizer of the expected calibration loss , subject to the constraint , where is defined in (22). The one-to-zero constraint on corresponds to our definition of with the same constraint. If model (5) is correctly specified, then coincides with the true value such that for subject to . Otherwise, may differ from for . For two matrices and , the group norm of is defined as , where or is the transpose of the th row vector in or . The Bregman divergence associated with the convex loss is

The symmetrized Bregman divergence is easily shown to be

The following assumptions are required in our analysis of convergence of to .

Assumption 1.

Suppose that the following conditions are satisfied:

-

(i)

almost surely for a constant ;

-

(ii)

almost surely for a constant ;

-

(iii)

The theoretical compatibility condition below holds with the subset and some constants and ;

-

(iv)

(a) for a constant , and (b) for a constant .

The theoretical compatibility condition in Assumption 1 (iii) is defined as follows: for any matrix satisfying

| (36) |

it holds that

| (37) |

where for , is the transpose of the th row vector in , and with dependency on suppressed. As seen from the Taylor expansion (31), the right-hand side of (37) can be expressed as , where , is the Hessian matrix of at , and denotes the Kronecker product. Hence Assumption 1(iii) amounts to a compatibility condition on the matrix , similarly as in Buhlmann and van de Geer (2011) and Tan (2020ab). See Remark 8 for further discussion.

Remark 5 (On Assumption 1).

Assumption 1(i) may often be satisfied in practice, although relaxation can be made to allow sub-Gaussian regressors with increasing technical complexity. Assumption 1(ii), which is also used in Farrell (2015), is used among others to bound the gradient of the loss at . The compatibility condition in Assumption 1(iii) is discussed in Remark 8, together with related conditions. Assumption 1(iv) requires that is sufficiently small, and is used to obtain the empirical compatibility condition (Lemma S6) and perform localized analysis with a non-quadratic loss function (Lemma S7).

The following result establishes the convergence of to in the norm at rate and in the associated Bregman divergence at the rate . While the rate is familiar in high-dimensional analysis, our analysis appears to, for the first time, allow a theoretical compatibility condition and account for the interdependency between the gradient vectors in , , of a loss function for group-Lasso penalized estimation in multi-class logistic regression (5). See Remark 9 for a comparison with Farrell (2015).

Theorem 1.

Next, we study the regularized calibrated (or weighted likelihood) estimator . The tuning parameter in the objective function (28) is specified as with a constant and

where are from Assumptions 1(i)-(ii), is from Assumption 2(i), and is a tail probability for the error bound.

With possible misspecification of model (8) as well as model (5), the limit (or target) value of , denoted as , can be identified as a minimizer of the expected loss , where . If model (8) is correctly specified, then for each coincides with such that . Otherwise, , , may differ from . For two matrices and , the group norm is defined as , where or is the transpose of th row vector in or . The Bregman divergence associated with the convex loss is

The symmetrized Bregman divergence is easily shown to be

The following assumptions are adapted from Tan (2020b). The theoretical compatibility condition is the same as in Assumption 1(iii), except with the sparsity subset and possibly different constants . Assumption 2(iv) is not needed here, but will be used in later results.

Assumption 2.

Suppose that the following conditions are satisfied:

-

(i)

are uniformly sub-gaussian random variables with parameter given for ;

- (ii)

-

(iii)

almost surely for a constant , where denotes the derivative of ;

-

(iv)

almost surely for a constant ;

-

(v)

For any , holds for a constant ;

-

(vi)

(a) for a constant , (b) for a constant , and (c) for a constant , where are as in Theorem 2.

The following result establishes the convergence of to in the norm at rate and in the associated Bregman divergence at the rate . Compared with related results (Farrell 2015), our analysis needs to handle the interdependency between the gradient vectors of the weighted likelihood loss, corresponding to outcome regression with different weights in the same treatment group . In addition, our error bound for depends on the sparsity subsets of and , due to the construction of depending on . See Remarks 7–9 for further discussion.

Theorem 2.

Remark 6 (Linear outcome model).

If linear OR model (8) is used, the symmetrized Bregman divergence becomes the weighted (in-sample) prediction error

In this case, Assumptions 2(iii)–(v) hold with and and Assumptions 2(vi)(b) and 2(vi)(c) hold with . Therefore, under Assumptions 2(i), (ii) and (vi)(a), we have from Theorem 2 that

| (40) |

where , only depending on , are the same as in Theorem 2.

Remark 7 (Data-dependent weights).

A key step in our proof is to upper-bound the product

| (41) |

which involves the estimated weight . If we replace with , then it is standard to use the following bound,

| (42) | |||

where . To handle the dependency on , we derive an upper bound on the difference between (41) and (42) and a quadratic inequality in terms of , which is then inverted to obtain the desired bound (39).

To compare our results with related ones, we first summarize those in Lounici et al. (2011) and Buhlmann and van de Geer (2011). Consider fixed-design multi-task linear regression:

| (43) |

where is the th response, is the th fixed covariate vector, and is the associated coefficient vector in task , and is independently over and , with the fixed sample size in each task. Similarly to in Section 2, the group-Lasso penalized estimators are defined as a minimizer to , where is the transpose of the th row vector in the matrix , and denotes the sample average over task . For example, . The empirical compatibility condition assumed in Buhlmann and van de Geer (2011), which is weaker than the restricted eigenvalue condition in Lounici et al. (2011), is as follows: for any matrix satisfying , it holds that

| (44) |

where is the sparsity subset for . Then the following error bound is obtained with high probability (Buhlmann and van de Geer 2011, Theorem 8.4) :

| (45) |

where and with . We compare our results with related ones in the following remarks.

Remark 8 (Comparison with multi-task linear regression).

The results in Lounici et al. (2011) and Buhlmann and van de Geer (2011) can be transferred to an error bound on the group-RML estimator in a linear OR model with regressor vector , by taking the treatment group as task and conditioning on such that all treatment groups are of the same size . For the empirical compatibility condition, (44) can be rewritten in a similar form to (37) as

| (46) |

where plays the role of in (37). In this way, the compatibility condition in Buhlmann and van de Geer (2011) and those in Assumptions 1(iii) and 2(ii) are comparable, while treating . Then the error bound (45) can be stated as

| (47) |

where . Hence is of order and is of order , which are smaller than the error bounds on in Theorem 2 by a factor of and respectively. However, this comparison needs to be interpreted with caution, even after ignoring differences caused by the weight . Our analysis involves a random design and a possibly misspecified OR model, whereas the error bound (47) is derived in a fixed design (with fixed treatments and covariates) and a correctly specified linear model (with encoding true coefficients). With possible model misspecification, a random design enables that the gradient of a loss function remains mean-zero unconditionally when evaluated at the target parameter value, but such a mean-zero property is lost in a fixed design. On the other hand, the error bounds are improved in fixed-design multi-task linear regression (43), partly because the sup- norm of the gradient of the loss function at can be more tightly controlled using the independence between different treatmeant subsamples, which is further discussed in Appendix C.

Remark 9 (Comparison with Farrell 2015).

We compare our results with those about the group-RML estimators in Farrell (2015). For a correctly specified linear OR model, Farrell provided finite-sample analysis of the estimator , using an empirical restricted eigenvalue condition as in Lounici et al. (2011), related to the empirical compatibility condition in Remark 8. Such an empirical condition is further assumed to be satisfied in asymptotic analysis, instead of being derived with high probability from a theoretical condition as in our analysis. In addition, Farrell used Lemma 9.1 in Lounici et al. (2011) to control the gradient norm of the least-square loss by the independence between , , from different treatment groups. But the derivatives of our weighted least-square loss , , are interdependent for each , being induced by different weights in the same treatment group . See Appendix C for further discussion about control of gradient norms. For a correctly specified multi-class logistic PS model, Farrell’s finite-sample analysis of the estimator also used an empirical restricted eigenvalue condition, which is further assumed to hold in asymptotic analysis. More importantly, Farrell in his Lemma B.1 also applied Lemma 9.1 in Lounici et al. (2011) to control the sup- norm of the gradient at the true value . But this application appears to be flawed, because the derivatives , , are interdependent for each , violating the independence assumption in Lounici et al.’s Lemma 9.1. In contrast, our analysis appropriately tackles a similar interdependency within the gradient of the calibration loss evaluated at . See Supplement Lemma S1, where the approach can also be applied to appropriately analyze .

4.2 Estimation of treatment means

With the preceding results on , we turn to theoretical analysis of the augmented IPW estimator for the treatment mean . The convergence results in Section 4.1 are obtained with possible misspecification of both PS model (5) and OR model (8). However, statistical properties of are model-dependent in various ways. On one hand, is expected be pointwise doubly robust similarly as the limit version , i.e., remains consistent for if either model (5) or (8) is correctly specified. On the other hand, to obtain valid Wald confidence intervals, the deviation of from can be shown to be of order as stated in the asymptotic expansion (29), depending on whether linear or nonlinear OR model (8) is used.

First, we assume that linear OR model (8) is used together with PS model (5), and develop theoretical analysis which leads to doubly robust Wald confidence intervals for .

Theorem 3.

Theorem 3 shows that is doubly robust for provided , that is, . In addition, Theorem 3 gives the asymptotic expansion (29) provided , that is . To obtain valid confidence intervals for via the Slutsky theorem, the following result gives the consistency of the variance estimator to , where is defined in (30) and with defined in (17).

For notational simplicity, denote and such that . Similarity, denote and such that .

Theorem 4.

Inequality (49) shows that is a consistent estimator of , that is, , provided , which means . Combining Theorems 3 and 4, we have the following doubly robust Wald confidence intervals for . For simplicity, the group Lasso tuning parameters are denoted as for and for .

Proposition 1.

Suppose that Assumption 1 and Assumption 2(i), 2(ii), and 2(iv)(a) hold, and . Then for and with sufficiently large constants and , asymptotic expansion (29) is valid. Moreover, if either PS model (5) or linear OR model (8) is correctly specified, the following results hold:

-

(i)

, where ;

-

(ii)

a consistent estimator of is

-

(iii)

an asymptotic confidence interval for is , where is the quantile of .

That is, a doubly robust confidence interval for is obtained.

Second, we assume that a generalized linear OR model (8) is used together with PS model (5), and develop theoretical analysis which leads to valid Wald confidence intervals for if model (5) is correctly specified. Compared with the upper bound of for linear OR model (8) in Theorem 3, the upper bound for generalized linear OR model (8) depends on additional terms , which is defined as, for any ,

with and . By the definition of , it holds that for whether or not model (5) is correctly specified. But is in general either zero or positive respectively if outcome model (2) is correctly specified or misspecified, except in the case of linear outcome model where is automatically zero because is constant.

Theorem 5.

Theorem 5 shows that is doubly robust for provided , that is, . In addition, the error bounds imply that admits the asymptotic expansion (29) provided , that is when PS model is correctly specified but OR model may be misspecified, because the term involving vanishes when PS model (5) is correctly specified. Unfortunately, asymptotic expansion may fail when PS model is misspecified. The following result gives the consistency of the variance estimator to with a generalized linear OR model (2) together with PS model (5).

Theorem 6.

5 ATT estimation

Our method and theory can be extended for estimating ATTs using the same set of regularized calibrated estimators as in ATE estimation. From Section 2, the ATT for treatment vs in the th treated group is . The mean can be directly estimated as , i.e., the sample average of within the th treated group. In the following, we mainly discuss estimation of the mean for .

By the relation , our estimator for is

where are defined as in , and is defined in (18) such that is an augmented IPW estimator for . Hence our estimators for and satisfy the natural decomposition:

in accordance with our earlier discussion about the estimator in (16). In this sense, our approach handles estimation of ATEs and ATTs in a unified manner.

Statistical properties of can be deduced similarly as in Section 4.2. In particular, if PS model (5) is correctly specified but OR model (8) may be specified, then can be shown to admit the asymptotic expansion under suitable sparsity condition,

| (52) |

where are the limit values of as before. Then an asymptotic confidence interval for can be obtained as , where

| (53) |

For a linear OR model, the asymptotic expansion (52) can be established, with possible misspecification of both models (5) and (8). In this case, the confidence intervals for are doubly robust, being valid when either model (5) or linear model (8) is correctly specified.

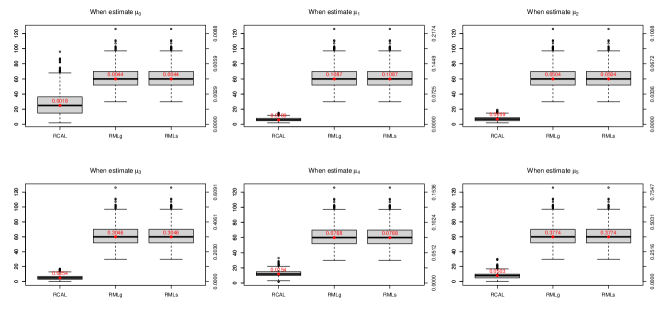

6 Simulation study

We conduct a simulation study to evaluate the performance of compared with and for ATE estimation, where the fitted value is based on the separate Lasso estimator and is based on the group Lasso estimator as described in Section 2. In addition, we also compare the performance of with and for ATT estimation and include the corresponding results in the Supplementary Material, where and for , similarly as in Section 5.

The algorithms for computing the RCAL estimators and are described in Section 3.2, combining Fisher scoring, the MM technique and the block coordinate descent. The constraint is used in when estimating . We compute the RML estimators , , and similarly as in the R package glmnet (Friedman et al. 2010; Simon et al. 2013), except that the one-to-zero constraint is used in . For completeness, we also conduct simulations using the sum-to-zero constraint in and . The results are presented in the Supplementary Material, and similar conclusions are obtained as below. All the methods are implemented in the R package mRCAL, including RCAL and RMLs and RMLg.

For computing or , the group-Lasso tuning parameter is determined using 5-fold cross validation based on the corresponding loss function as follows. For , let be a random subsample of size form . For a loss function , either in (6) or in (22), denote by the loss function obtained when the sample average is computed over only the subsample . The 5-fold cross-validation criterion is defined as , where is a minimizer of the penalized loss over the subsample of size , i.e., the complement to . Then is selected by minimizing over the discrete set , where for , the value is computed as with when the likelihood loss (6) is used, or with when the calibration loss (22) is used.

For selection of the tuning parameter in , , or , 5-fold cross validation is conducted similarity as above using respectively the loss function in (3), in (4), or in (28). In the last case, is determined separately and then fixed during cross validation for computing .

In our simulation, the number of treatments is 4, and sample size is 1000. Let be multivariate normal with means 0 and covariance for . In addition, let for , where , and . Consider the following the data-generating configurations.

-

(C1)

Generate given from a categorical distribution with , and , and, independently, given is generated from a Normal distribution with variance 1 and mean , , and .

-

(C2)

Generate given as in (C1). But given is generated from a Normal distribution with variance 1 and mean , , and .

-

(C3)

Generate given as in (C1). But given is generated with , and .

Consider multi-class logistic propensity score model (5) and linear outcome model (8), both with for . Then the two models can be classified as follows, depending on the data configuration above:

-

(C1)

PS and OR models both correctly specified;

-

(C2)

PS model correctly specified, but OR model misspecified;

-

(C3)

PS model misspecified, but OR model correctly specified.

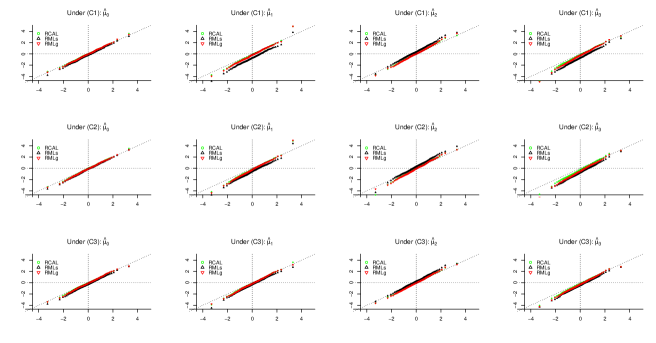

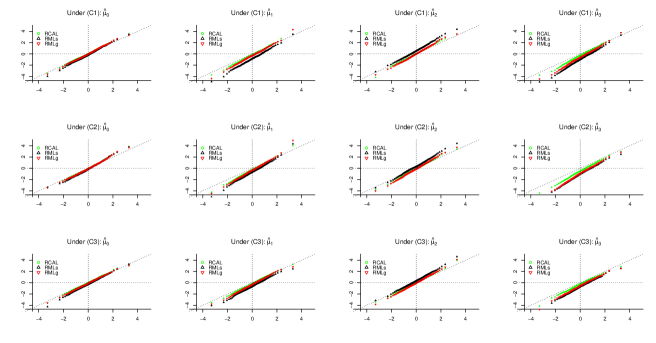

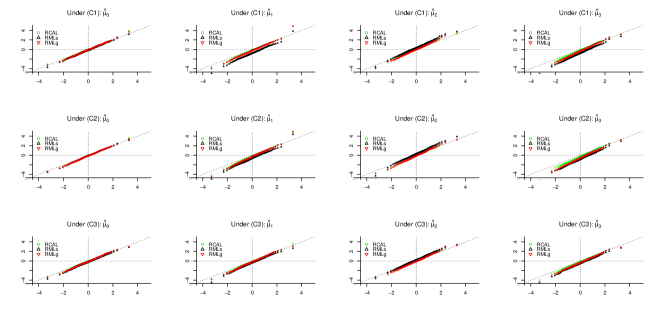

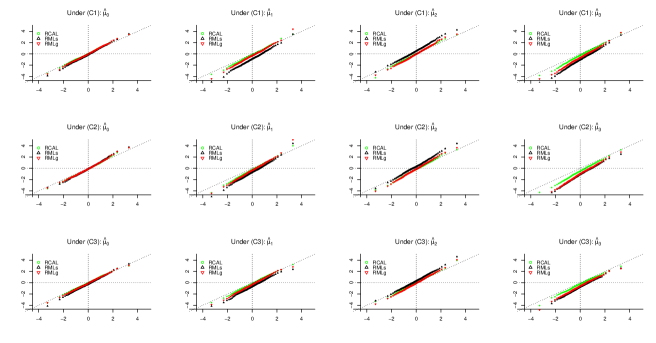

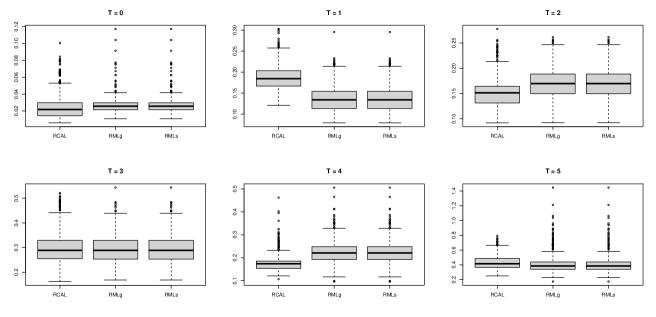

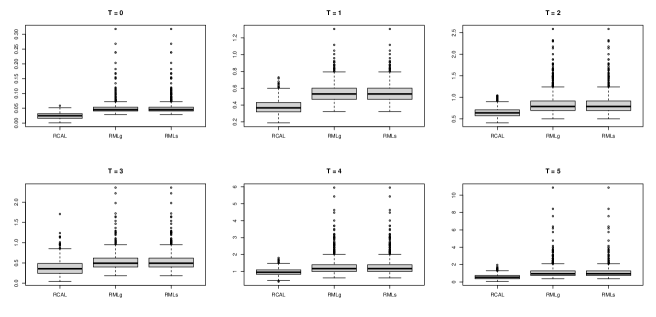

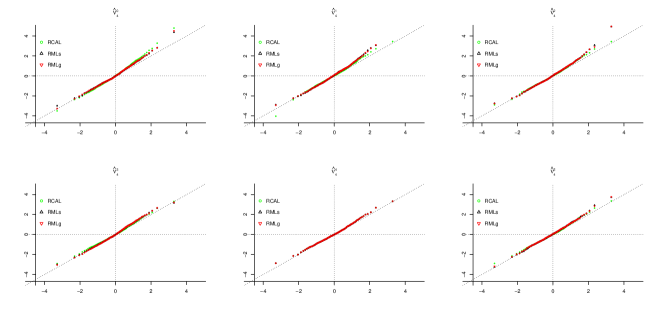

Partly because the regressor is a monotone nonlinear transformation of for , the misspecified OR model in (C2) or PS model in (C1) appears to be nearly correct by standard model diagnosis. See the Supplement Material for boxplots of and scatterplots of against within different treatment groups for .

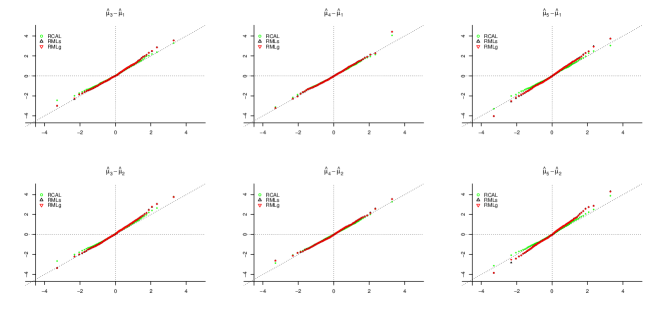

| (C1) cor PS, cor OR | (C2) cor PS, mis OR | (C3) mis PS, cor OR | (C1) cor PS, cor OR | (C2) cor PS, mis OR | (C3) mis PS, cor OR | |||||||||||||

| RCAL | RMLs | RMLg | RCAL | RMLs | RMLg | RCAL | RMLs | RMLg | RCAL | RMLs | RMLg | RCAL | RMLs | RMLg | RCAL | RMLs | RMLg | |

| n = 1000, p = 50 | ||||||||||||||||||

| Bias | -0.001 | -0.021 | -0.005 | -0.006 | -0.021 | -0.011 | -0.004 | -0.027 | -0.008 | -0.015 | -0.067 | -0.020 | -0.019 | -0.058 | -0.025 | -0.012 | -0.033 | -0.016 |

| 0.093 | 0.098 | 0.095 | 0.100 | 0.109 | 0.102 | 0.093 | 0.096 | 0.094 | 0.095 | 0.101 | 0.098 | 0.101 | 0.107 | 0.104 | 0.095 | 0.102 | 0.100 | |

| 0.090 | 0.091 | 0.088 | 0.092 | 0.098 | 0.093 | 0.088 | 0.088 | 0.086 | 0.088 | 0.092 | 0.087 | 0.089 | 0.096 | 0.090 | 0.087 | 0.095 | 0.090 | |

| Cov90 | 0.885 | 0.865 | 0.875 | 0.869 | 0.864 | 0.869 | 0.868 | 0.860 | 0.850 | 0.869 | 0.793 | 0.861 | 0.853 | 0.810 | 0.838 | 0.854 | 0.854 | 0.845 |

| Cov95 | 0.937 | 0.924 | 0.939 | 0.931 | 0.922 | 0.925 | 0.930 | 0.916 | 0.920 | 0.922 | 0.877 | 0.918 | 0.907 | 0.881 | 0.904 | 0.914 | 0.911 | 0.907 |

| Bias | 0.001 | 0.034 | 0.000 | -0.006 | 0.025 | -0.010 | -0.003 | 0.021 | -0.005 | -0.016 | -0.065 | -0.026 | -0.025 | -0.072 | -0.045 | -0.017 | -0.044 | -0.026 |

| 0.100 | 0.106 | 0.103 | 0.107 | 0.114 | 0.110 | 0.098 | 0.105 | 0.102 | 0.100 | 0.105 | 0.103 | 0.105 | 0.111 | 0.109 | 0.096 | 0.100 | 0.098 | |

| 0.088 | 0.092 | 0.089 | 0.090 | 0.097 | 0.092 | 0.088 | 0.093 | 0.089 | 0.088 | 0.090 | 0.086 | 0.089 | 0.096 | 0.089 | 0.087 | 0.089 | 0.086 | |

| Cov90 | 0.852 | 0.823 | 0.839 | 0.834 | 0.822 | 0.838 | 0.852 | 0.844 | 0.837 | 0.860 | 0.769 | 0.821 | 0.826 | 0.760 | 0.792 | 0.860 | 0.822 | 0.847 |

| Cov95 | 0.910 | 0.895 | 0.902 | 0.913 | 0.890 | 0.900 | 0.916 | 0.904 | 0.915 | 0.917 | 0.841 | 0.886 | 0.902 | 0.836 | 0.861 | 0.917 | 0.897 | 0.902 |

| n = 1000, p = 300 | ||||||||||||||||||

| Bias | 0.005 | -0.015 | 0.000 | -0.002 | -0.013 | -0.006 | 0.000 | -0.024 | -0.009 | -0.014 | -0.073 | -0.027 | -0.023 | -0.058 | -0.032 | -0.013 | -0.056 | -0.027 |

| 0.096 | 0.102 | 0.099 | 0.101 | 0.110 | 0.107 | 0.091 | 0.097 | 0.092 | 0.094 | 0.105 | 0.099 | 0.099 | 0.107 | 0.105 | 0.092 | 0.099 | 0.096 | |

| 0.087 | 0.087 | 0.087 | 0.089 | 0.091 | 0.092 | 0.086 | 0.086 | 0.085 | 0.083 | 0.085 | 0.082 | 0.083 | 0.085 | 0.083 | 0.083 | 0.086 | 0.083 | |

| Cov90 | 0.869 | 0.847 | 0.866 | 0.855 | 0.823 | 0.854 | 0.884 | 0.850 | 0.871 | 0.845 | 0.716 | 0.809 | 0.825 | 0.742 | 0.796 | 0.859 | 0.791 | 0.829 |

| Cov95 | 0.928 | 0.910 | 0.925 | 0.912 | 0.881 | 0.911 | 0.938 | 0.899 | 0.933 | 0.912 | 0.804 | 0.888 | 0.882 | 0.826 | 0.868 | 0.925 | 0.871 | 0.893 |

| Bias | 0.003 | 0.045 | -0.002 | -0.007 | 0.028 | -0.011 | 0.000 | 0.029 | -0.005 | -0.025 | -0.084 | -0.052 | -0.044 | -0.091 | -0.080 | -0.023 | -0.064 | -0.047 |

| 0.095 | 0.103 | 0.102 | 0.099 | 0.107 | 0.107 | 0.095 | 0.101 | 0.100 | 0.097 | 0.107 | 0.102 | 0.102 | 0.108 | 0.108 | 0.089 | 0.098 | 0.094 | |

| 0.083 | 0.085 | 0.082 | 0.084 | 0.086 | 0.084 | 0.084 | 0.086 | 0.083 | 0.084 | 0.083 | 0.081 | 0.084 | 0.084 | 0.083 | 0.084 | 0.083 | 0.082 | |

| Cov90 | 0.842 | 0.787 | 0.820 | 0.828 | 0.795 | 0.792 | 0.852 | 0.822 | 0.829 | 0.819 | 0.675 | 0.757 | 0.782 | 0.650 | 0.675 | 0.866 | 0.739 | 0.789 |

| Cov95 | 0.914 | 0.854 | 0.891 | 0.895 | 0.864 | 0.873 | 0.916 | 0.889 | 0.901 | 0.900 | 0.764 | 0.831 | 0.856 | 0.740 | 0.757 | 0.930 | 0.823 | 0.865 |

Note: RCAL denotes , RMLs denotes and RMLg denotes . Bias and Var are the Monte Carlo bias and variance of the point estimates. EVar is the mean of the variance estimates, and hence also measures the -average of lengths of confidence intervals. Cov90 or Cov95 is the coverage proportion of the 90% or 95% confidence intervals.

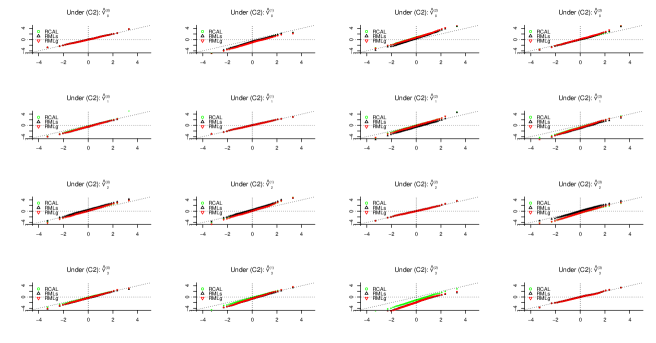

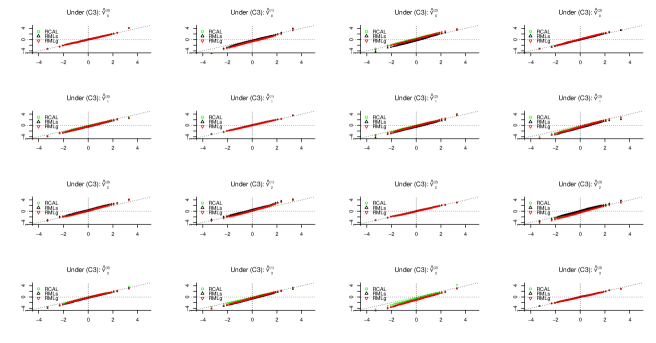

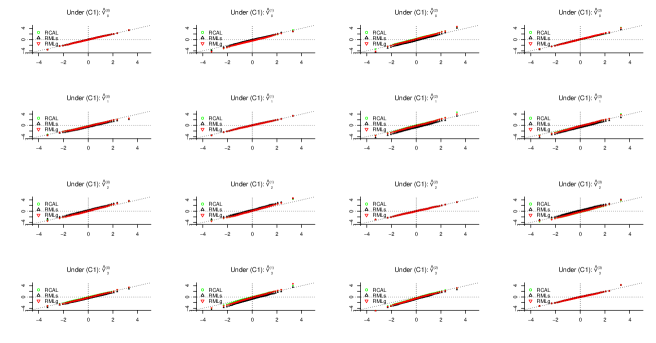

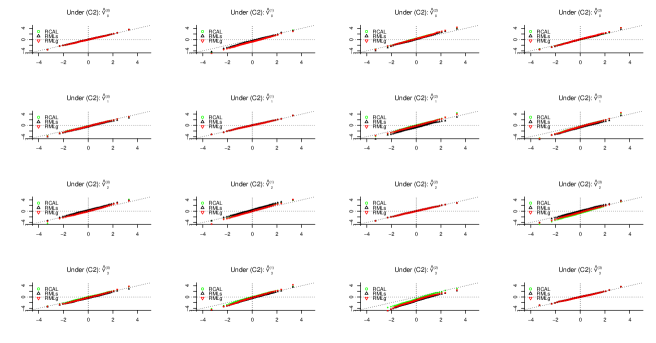

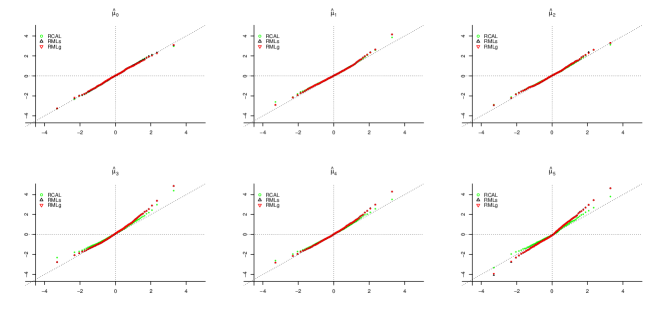

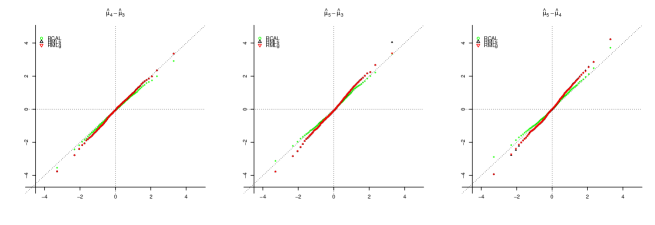

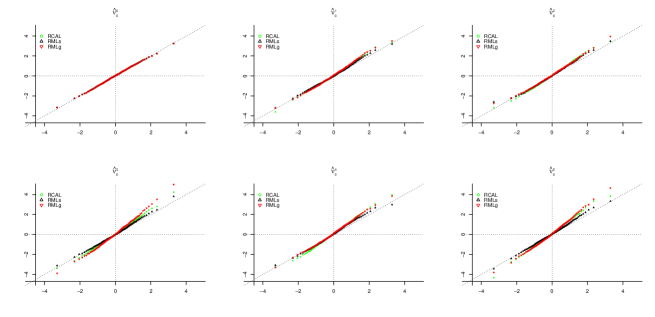

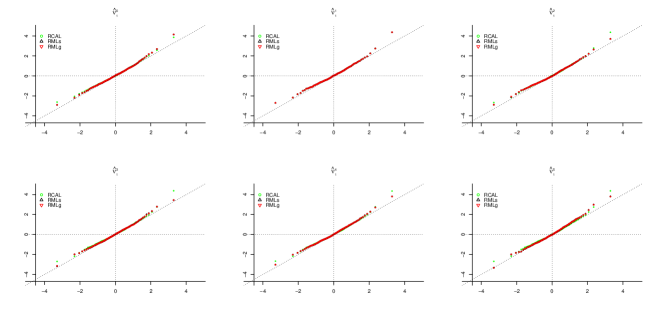

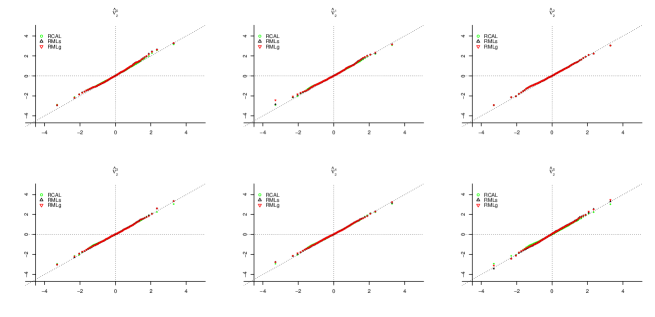

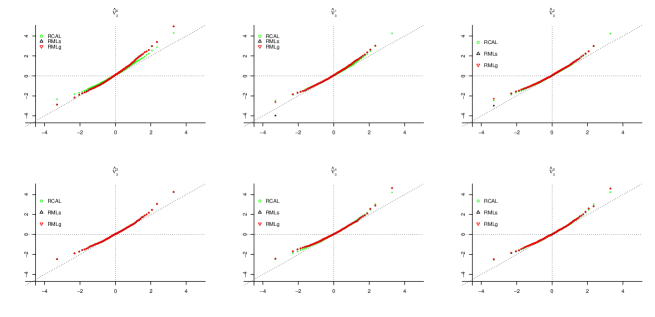

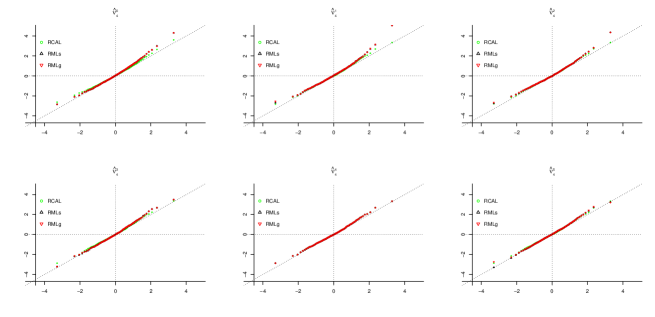

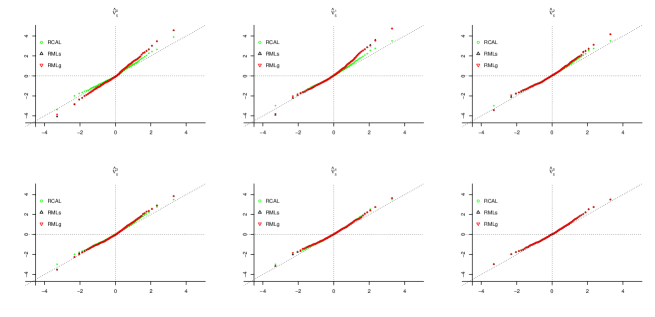

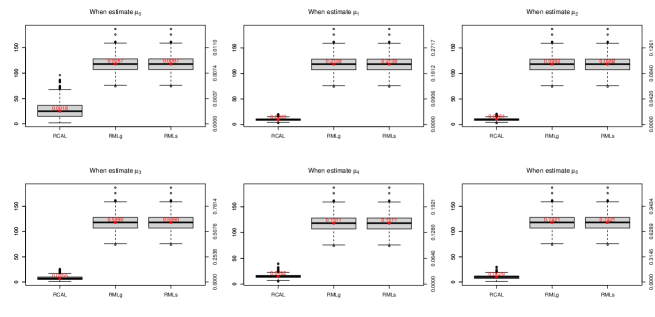

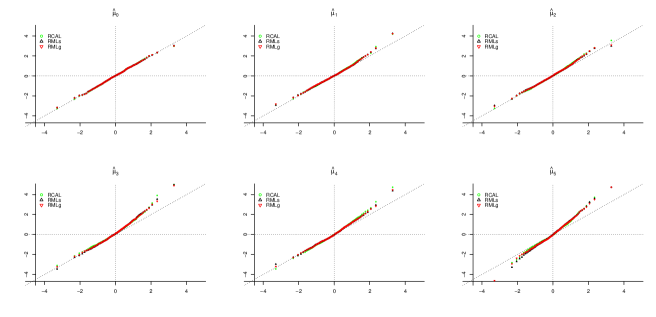

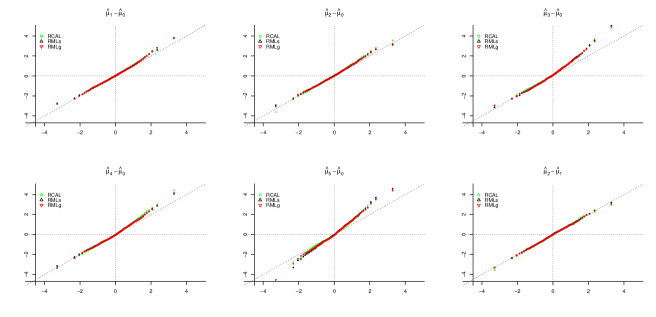

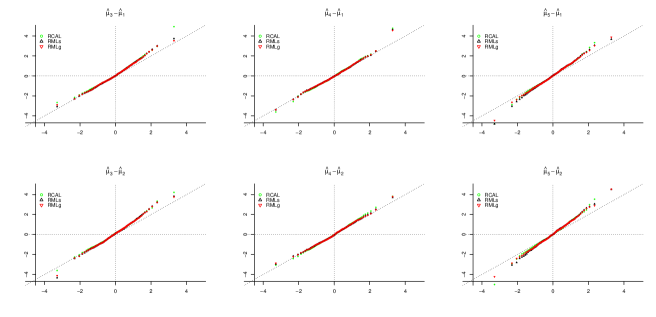

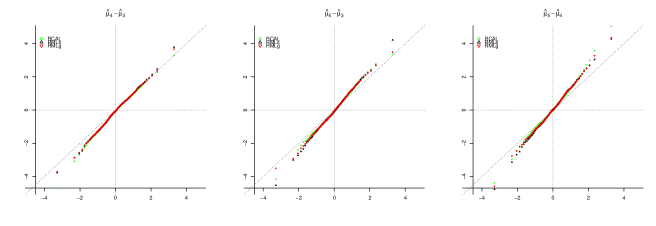

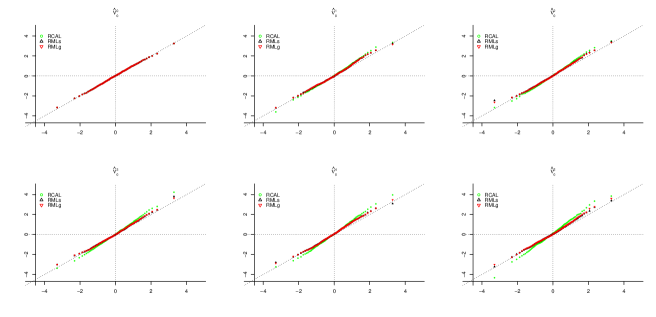

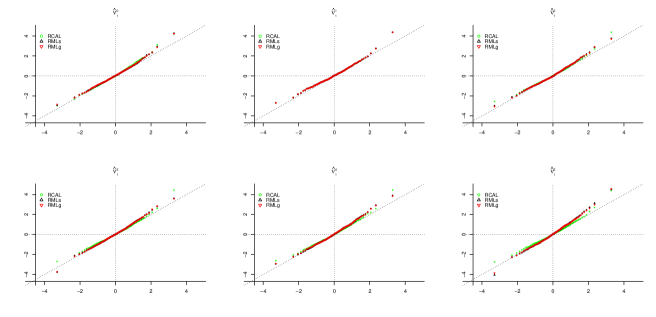

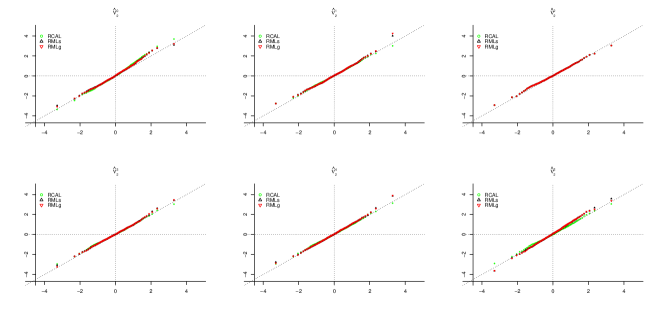

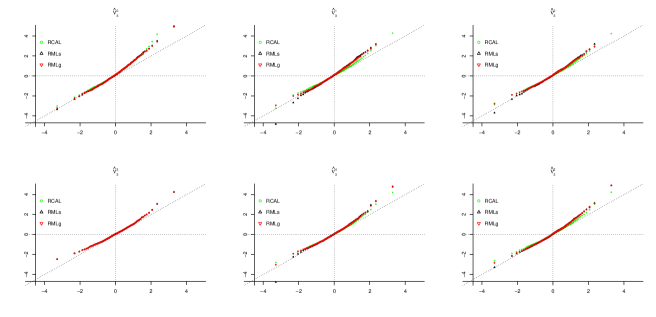

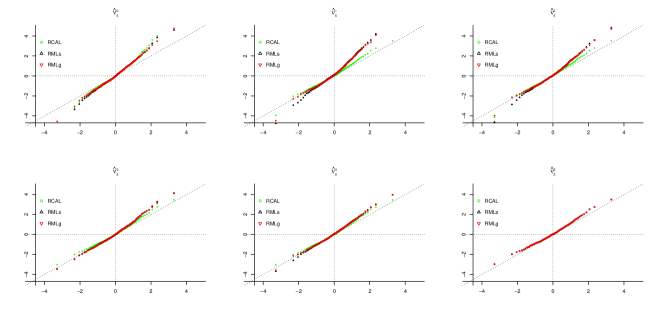

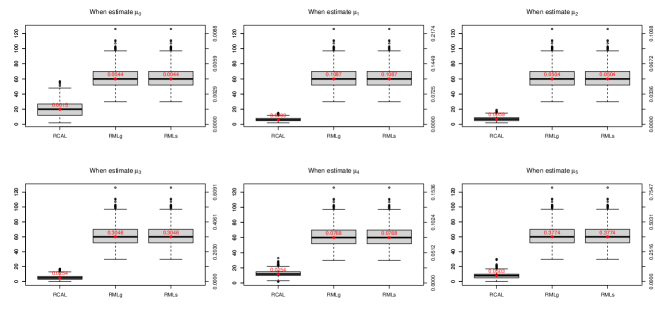

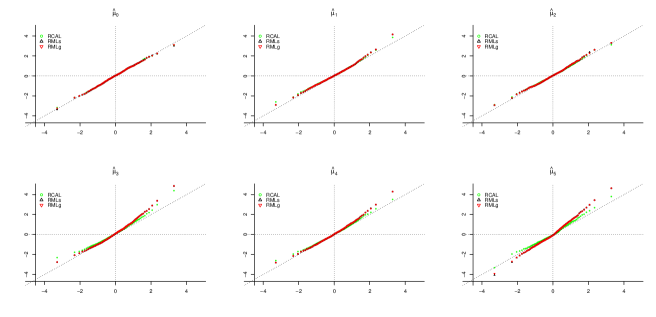

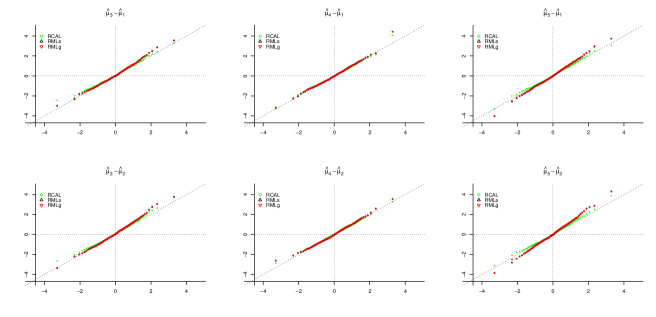

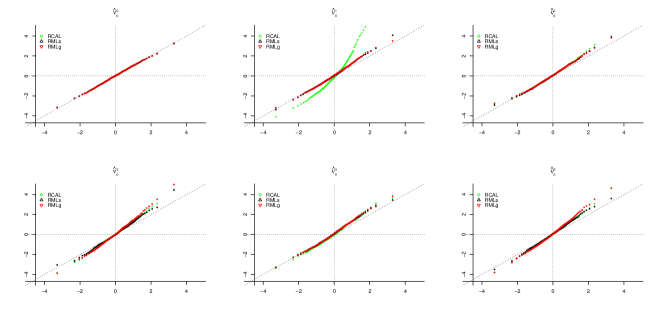

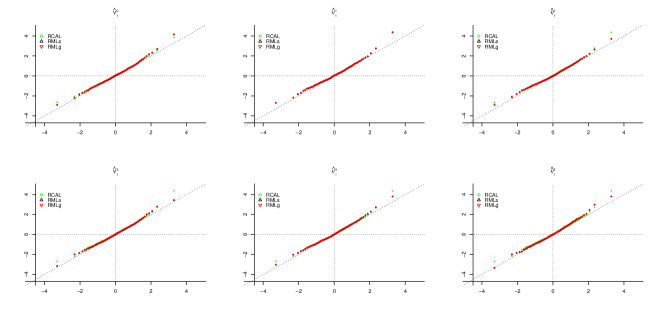

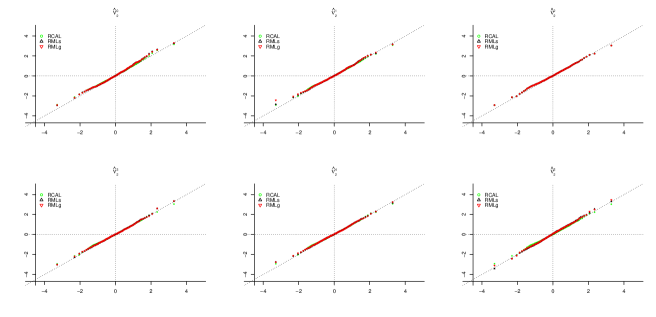

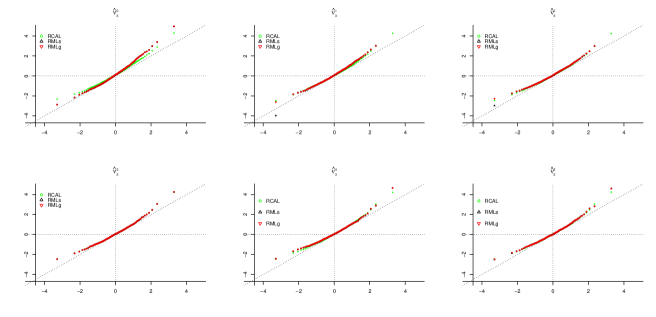

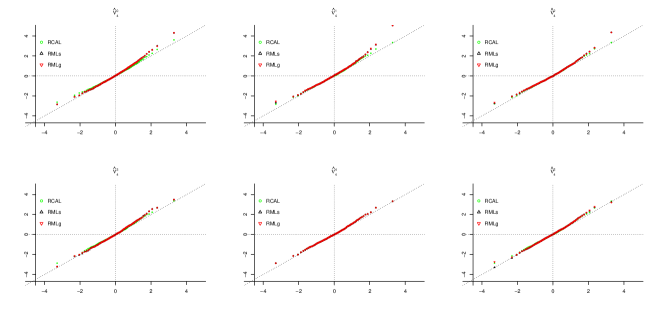

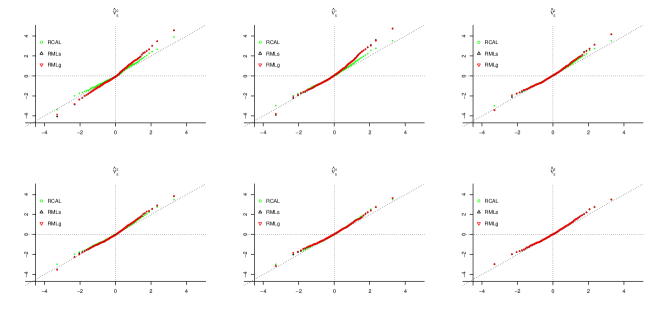

Table 1 summarizes estimates of for , based on 1000 repeated simulations. Three interesting findings can be obtained. First, in terms of bias, RCAL overall has the smallest absolute bias, followed by RMLg and RMLs. For example, the biases of RMLs, RMLg and RCAL are -0.064, -0.047, and -0.023 for estimation of under (C3) with . Second, in terms of variance, the three methods perform similarly to each other. Third, in terms of coverage, RCAL achieves coverage proportions overall the closet to the nominal levels. For example, the 90% coverage proportions of RMLs, RMLg and RCAL are 0.739, 0.789 and 0.866 for estimation of under (C3) with . These properties can also seen from QQ plots of the -statistics in the Supplement.

7 Empirical application

We provide an application to study the effects of maternal smoking during pregnancy on birth weights for singleton births in Pennsylvania between 1989 and 1991, based on a dataset from the US National Center of Health Statistics. The original dataset was also used in Almond et al. (2005) and Cattaneo (2010) among others. To assess multi-valued treatment effects, the treatment is taken to be the number of cigarettes smoked per day collapsed into 6 levels , labeled respectively as , as in Cattaneo (2010). The outcome is defined as the log of the birth weight, hence different from that in Almond et al. (2005) and Cattaneo (2010). After dropping about 18% observations with missing data and converting categorical covariates into dummy variables, the total sample size is 411609 and the number of covariates in is 33. The sample sizes of the six treatment groups are 339659, 13798, 29746, 4923, 19517, 3966. See Supplement Section IV for more information about data preprocessing.

To control for possible confounding beyond main effects of the covariates, we consider a multi-class logistic propensity score model and linear outcome model, where the regressor vector includes all main effects and two-way interactions of except those with the fractions of nonzero values less than 0.8% of the sample size . The dimension of is , excluding the constant. All variables in are standardized with sample means 0 and variances 1.

Given the large sample size relative to the regressor size , we investigate two separate analyses. The first, full-sample analysis, is to apply the existing and proposed methods to the full sample as in a typical application. The second, sub-sample analysis, is to repeatedly draw 1000 sub-samples, each of about 1/25 size of the full sample, and apply different methods to the sub-samples. The sample sizes from treatment groups 0 to 5 are fixed at 13587, 552, 1190, 197, 781 and 159 in each sub-sample. The sub-sample analysis is mainly designed to compare different methods in more challenging settings where sample sizes are comparable to regressor sizes. For space limitation, we present estimation results for the treatment means in this section, and defer those for the ATEs and ATTs to Supplement Section IV.

Full-sample analysis. We apply regularized calibrated estimation (RCAL) and regularized maximum likelihood estimation with separate Lasso (RMLs) or group Lasso (RMLg), similarly as in the simulation study. Each separate or group Lasso tuning parameter is selected by minimizing a 5-fold cross validation error over a discrete set , where is the value leading to a zero solution. For comparison, we also apply the non-regularized calibrated (CAL) and maximum likelihood (ML) estimation using PS and OR models with main effects only. The estimates of the treatment means are summarized in Table 2.

The following findings can be obtained from Table 2. First, the adjusted point estimates of are decreasing as the treatment level increases, i.e., the number of smoked cigarettes increases. There is a slight increase from to in the unadjusted estimates. Second, the point estimates and confidence intervals from RCAL, RMLs, and RMLg are overall similar to each other. Third, compared with those from non-regularized estimation with main effects only, regularized estimation incorporating interactions in PS and OR models leads to comparable or smaller standard errors. For example, the width of the 95% confidence interval for from CAL and RCAL are 0.0224 and 0.0185. This difference not only agrees with the theoretical property that augmented IPW estimation has a smaller asymptotic variance when using a larger (correct) PS model with a fixed number of regressors, but also demonstrates the effectiveness of Lasso regularization in suppressing variation that would otherwise be inflated with a large number of regressors.

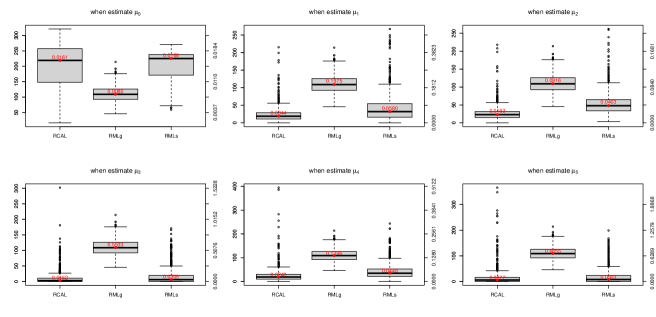

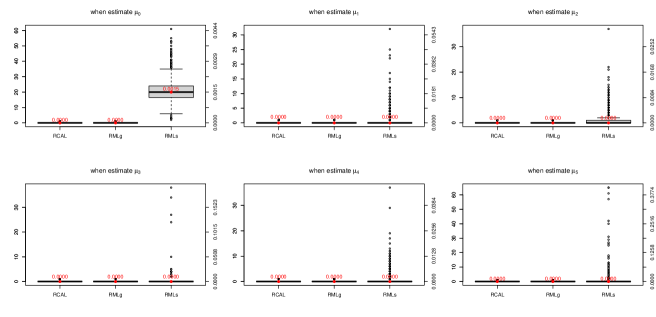

Sub-sample analysis. To further compare different methods, we apply RCAL, RMLs, RMLg estimation to 1000 sub-samples as described earlier. We conduct 5-fold cross validation in each subsample, similarly as in the full-sample analysis, but take as the tuning parameter for PS and OR models in RCAL when estimating and take for PS and OR models in RCAL when estimating , where gives the minimal cross validation error, and gives the most regularized model such that the cross validation error is within one standard error of the minimum (Hastie et al. 2009). Selecting when estimating leads to large ratios of the number of nonzero estimated coefficients over the corresponding treatment group size, which would be incompatible with the sparsity assumptions for our theory. Selecting for treatment 0 does not suffer this issue because the sample size for treatment 0 is much larger. See Supplement Figures S37 and S49. For similar reasons, we also take for OR model in RMLs for treatment 0 and take for OR model in RMLs for the other treatments, and take as the group Lasso tuning parameter for OR model in RMLg. Because RMLs or RMLg treats PS estimation independently of which is estimated, we take for PS model in RMLs and RMLg. Results from always selecting or in all methods can be found in the Supplement.

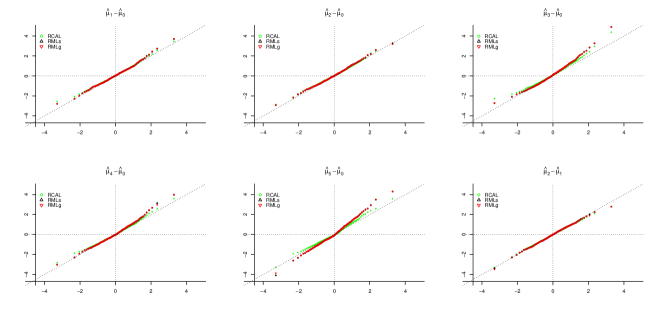

Table 3 summarizes the estimates of from 1000 subsamples similarly as in the simulation study. Coverage proportions are calculated by treating the mean of the 1000 estimates as the true value for each method. We see that RCAL, RMLs and RMLg perform similarly to each other in terms of the repeated-sampling means and variances. However, the estimated variances from RCAL are close to the repeated-sampling variances, whereas those from RMLs and RMLg show underestimation especially for and . Consistently with this observation, the coverage proportions from RCAL are comparable to or more aligned with the nominal probabilities than from RMLs and RMLg. For example, from RCAL, RMLs, RMLg, the 90% coverage proportions are 0.900, 0.847 and 0.849 for and are 0.887, 0.810 and 0.812 for . These differences in coverage can also be seen from the QQ plots of standardized estimates in the Supplement.

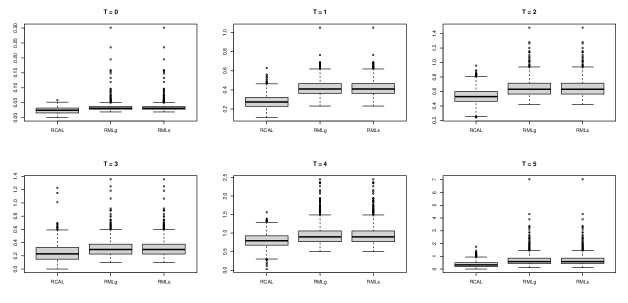

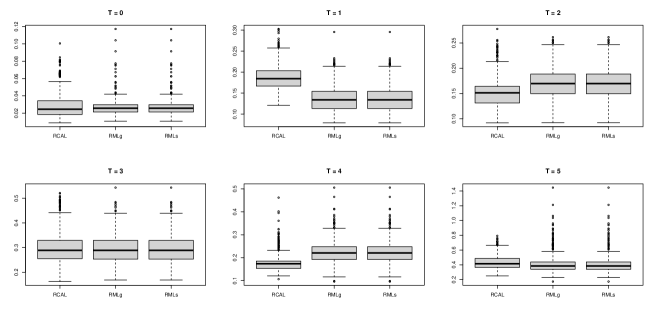

Finally, to compare PS estimation from different methods, we calculate the maximum absolute standardized calibration differences (MASCD) and the relative variances (RV) of the inverse probability weights similarly as in Tan (2020a) by the following formulas:

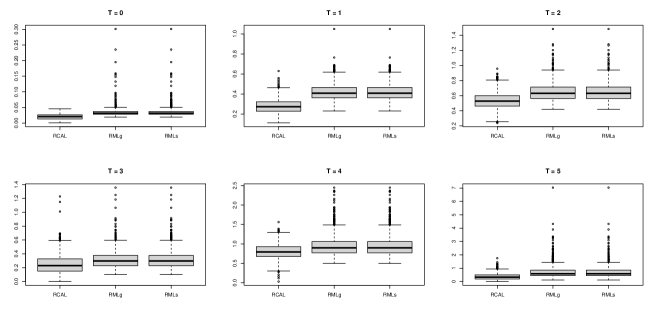

where denotes the sample variance, and and denote the sample mean and variance over treatment respectively. From Supplement Figures S24 and S25, we see that RCAL, RMLs and RMLg are overall comparable to each other in terms of MASCD, but RCAL is associated with a much smaller number of nonzero estimated coefficients. From Figure 1, we find that RCAL is associated with similar or smaller RVs compared with RMLs and RMLg, while more outliers are produced by RMLs and RMLg. These differences indicate that RCAL achieves greater sparsity in estimated coefficients and greater efficiency in weighting than RMLs and RMLg.

| Est | SE | 95CI | Est | SE | 95CI | Est | SE | 95CI | |

| Unadj | 8.1272 | 0.0003 | (8.1266, 8.1279) | 8.0576 | 0.0019 | (8.0538, 8.0614) | 8.0398 | 0.0013 | (8.0372, 8.0424) |

| CAL | 8.1247 | 0.0004 | (8.1240, 8.1254) | 8.0763 | 0.0020 | (8.0723, 8.0803) | 8.0570 | 0.0017 | (8.0537, 8.0602) |

| ML | 8.1252 | 0.0006 | (8.1240, 8.1263) | 8.0768 | 0.0019 | (8.0730, 8.0806) | 8.0573 | 0.0015 | (8.0542, 8.0603) |

| RCAL | 8.1243 | 0.0004 | (8.1236, 8.1250) | 8.0744 | 0.0022 | (8.0702, 8.0786) | 8.0545 | 0.0016 | (8.0513, 8.0577 |

| RMLs | 8.1244 | 0.0004 | (8.1236, 8.1251) | 8.0751 | 0.0020 | (8.0712, 8.0790) | 8.0551 | 0.0017 | (8.0518, 8.0585) |

| RMLg | 8.1244 | 0.0004 | (8.1237, 8.1251) | 8.0750 | 0.0020 | (8.0710, 8.0790) | 8.0541 | 0.0016 | (8.0509, 8.0572) |

| Unadj | 8.0474 | 0.0030 | (8.0416, 8.0533) | 8.0365 | 0.0016 | (8.0334, 8.0396) | 8.0318 | 0.0034 | (8.0251, 8.0384) |

| CAL | 8.0517 | 0.0049 | (8.0421, 8.0612) | 8.0460 | 0.0023 | (8.0415, 8.0505) | 8.0442 | 0.0057 | (8.0330, 8.0554) |

| ML | 8.0536 | 0.0045 | (8.0449, 8.0623) | 8.0460 | 0.0021 | (8.0418, 8.0502) | 8.0413 | 0.0057 | (8.0301, 8.0525) |

| RCAL | 8.0494 | 0.0042 | (8.0411, 8.0576) | 8.0439 | 0.0021 | (8.0399, 8.0480) | 8.0417 | 0.0047 | (8.0324, 8.0509) |

| RMLs | 8.0495 | 0.0036 | (8.0424, 8.0565) | 8.0446 | 0.0020 | (8.0408, 8.0484) | 8.0416 | 0.0044 | (8.0330, 8.0501) |

| RMLg | 8.0484 | 0.0037 | (8.0412, 8.0556) | 8.0448 | 0.0020 | (8.0408, 8.0488) | 8.0410 | 0.0044 | (8.0323, 8.0497) |

Note: Est, SE, or 95CI denotes point estimate, standard error, or 95% confidence interval respectively. Unadj denotes the unadjusted estimate, . RCAL, RMLs, or RMLg denotes , , or respectively. CAL or ML denotes non-regularized estimation with main effects only in PS and OR models.

| Mean | Cov90 | Cov95 | Mean | Cov90 | Cov95 | Mean | Cov90 | Cov95 | |||||||

| RCAL | 8.125 | 0.002 | 0.002 | 0.883 | 0.942 | 8.069 | 0.009 | 0.010 | 0.913 | 0.950 | 8.052 | 0.007 | 0.007 | 0.911 | 0.953 |

| RMLs | 8.125 | 0.002 | 0.002 | 0.888 | 0.946 | 8.073 | 0.009 | 0.009 | 0.896 | 0.939 | 8.052 | 0.007 | 0.007 | 0.906 | 0.944 |

| RMLg | 8.125 | 0.002 | 0.002 | 0.897 | 0.954 | 8.073 | 0.009 | 0.009 | 0.895 | 0.939 | 8.052 | 0.007 | 0.007 | 0.903 | 0.942 |

| RCAL | 8.050 | 0.018 | 0.017 | 0.900 | 0.947 | 8.044 | 0.009 | 0.009 | 0.903 | 0.949 | 8.038 | 0.018 | 0.018 | 0.887 | 0.940 |

| RMLs | 8.049 | 0.017 | 0.014 | 0.847 | 0.912 | 8.041 | 0.009 | 0.009 | 0.881 | 0.929 | 8.039 | 0.018 | 0.014 | 0.810 | 0.886 |

| RMLg | 8.049 | 0.017 | 0.014 | 0.849 | 0.912 | 8.041 | 0.009 | 0.009 | 0.882 | 0.928 | 8.039 | 0.018 | 0.015 | 0.812 | 0.889 |

Note: Mean, Var, EVar, Cov90, and Cov95 are calculated over the 1000 repeated subsamples, with the mean treated as the true value. RCAL denotes . RMLs denotes . RMLg denotes .

8 Appendices

8.1 Appendix A: On multi-class calibration loss

We establish an interesting relationship between the multi-class likelihood and calibration loss functions and , which extends a similar result with binary treatments in Tan (2020a). To allow for misspecification of model (5), we write and , where for a function ,

| (54) | ||||

| (55) |

Both and are convex in . For two functions and , consider the Bregman divergences associated with and ,

where is identified as the vector with , is identified as , and is similarly defined. For two probability vectors and , the Kullback-Liebler divergence is . In addition, for , let , which is strictly convex in , with a minimum of 0 at .

Proposition 3.

(i) For any functions and and the corresponding functions and , where and is similarly defined from . Then

(ii) For any fixed , it holds that

| (56) | |||

| (57) |

where and with the associated function .

While the preceding result closely resembles Proposition 1 in Tan (2020a), the extension is nontrivial. For the relations (56)–(57), the Kullback-Liebler divergence is defined between two multi-class probability vectors and , but the divergence involves only the scalar probabilities and associated with class .

From (56)–(57), the calibration and likelihood divergences can be shown to yield different bounds on the mean squared relative error (MSRE) in propensity sores:

where for two probabilities . As demonstrated in Tan (2020a), Proposition 2 (i), this measure of relative errors in directly governs the mean squared error of an IPW estimator for .

Corollary 1.

(i) If almost surely for some constant , then

| (58) |

The factor in general connot be imcorved up to a constant, independent of .

(ii) If almost surely for some constant , then

| (59) |

The factor in general connot be imcorved up to a divisor of order .

The two bounds (58)–(59) are seemingly the same as those in Tan (2020a), Proposition 2, although the multi-class calibration and likelihood losses are involved. The calibration divergence achieves strong control of the relative errors in propensity scores through the additional term . By Lemma 1 in Tan (2020a), for any probabilities and satisfying with . In contrast, the likelihood divergence mainly controls the absolute errors in propensity scores through Pinsker’s inequality: for any probability vectors and . See Tan (2020a), Section 3.2, for further discussion which relates the minimum calibration and likelihood divergences to the mean squared errors of at the corresponding target values .

8.2 Appendix B: Karush–Kuhn–Tucker conditions

We discuss implications of the Karush–Kuhn–Tucker (KKT) conditions for regularized calibrated estimation in Section 3.1.

First, by the KKT conditions for minimization of in (27) with the one-to-zero constraint, the fitted propensity scores , , satisfy

where equality holds in the second line for any such that the vector is nonzero. By summing the two sides of the first line over of the preceding equation and using inequality on the second line above, the fitted propensity score for treatment satisfies

| (60) | |||

| (61) |

By (60), the inverse probability weights, with , sum to the sample size . By (61), the weighted average of each covariate function in the th treated group may differ from the overall sample average of by no more than . See the Supplement Section II.2 for a discussion on KKT conditions with the sum-to-zero constraint.

Second, by the KKT conditions for minimization of (28), the fitted outcome regression functions , , satisfy

| (62) | |||

| (63) |

where equality holds in (63) for any such that the vector is nonzero. Equation (62) implies that by simple calculation, the estimator can be recast as