A Markov-Modulated Inventory System with Repeated Calls and Blocked Demands

Abstract

In this article, we consider a continuous review inventory system with failures of demand fulfillment (service) modeled as a Markov-modulated retrial queueing system. The inventory system features a single product that experiences Markovian inter-demand and service intervals with random service interruptions and instantaneous replenishments. A recently developed criterion for the ergodicity of a class of discrete-time level-dependent-quasi-birth-and-death (LDQBD) processes with convergent transition matrix rows is applied to the jump chain of the process in order to elicit a closed-form traffic-intensity formula. An analytic solution for the steady-state average minimum cost is provided.

Keywords: Retrial queue; inventory; drift; random environment; LDQBD; service failure.

1 Introduction

The classical inventory model, which was first investigated in Arrow and Harris [1], and its later variants were developed to address the practical concerns of inventory management, and in doing so, posed interesting theoretical questions about model stability and optimal control. In particular, as Fisher and Hornstein [7] assert, models were extensively studied for use in retail applications due to the assumption of fixed ordering costs. The intuitive operation of models, together with their practical relevance, have given them prominence in the inventory literature.

In the classical inventory model, single demands for a type of item arrive to the system, and they are fulfilled as long as the inventory contains at least one item. However, if there arises an order that depletes the inventory to a level at or below a critical threshold value , then an order for just enough items to restore the level of the inventory to its maximum capacity of is made. A time delay between replenishment orders and deliveries may be specified whenever the threshold level is attained, or none at all, as is the case in what is termed an instantaneous replenishment model. Observations of the product level needed to trigger successive replenishment of the inventory may take place continuously or otherwise over time. The first models provided for continuous monitoring of inventory levels, such as in the model of this paper, hence the designation continuous review. This form of monitoring is the one that most often characterizes Markovian queueing inventory models.

The further imposition of a queueing model framework to inventory systems allows the modeler to leverage analytical techniques developed for the performance analysis of queues in steady-state operation. In a Markovian queueing system, incoming demands are often represented as a Poisson input stream and their subsequent processing as the in-service durations that are associated with one or more servers. In the event of blocked demands due to failures or busy periods of a server, the retrial queueing models of Artalejo and Krishnamoorthy [2], and Ushakumari [21] may be employed. In retrial models, blocked demands are redirected into a holding area called a retrial orbit, upon which each demand persistently reattempts fulfillment at i.i.d. time intervals. Demands are thus retained in the system without backlogging, i.e., without a promise of fulfillment, such as happens when items are back-ordered. Consequently, fulfillment will occur only when items are available and the ordering system is functioning, as usually occurs in online ordering scenarios.

In addition to imperfect service, another feature intended to free queueing systems from restrictive simplifying assumptions is the specification of a fluctuating random environment, which was first studied by Yechiali and Naor [22] and expanded upon by Neuts [13]. This is an independently evolving exogenous stochastic process that modifies the distributional parameters of the various time durations at evolutionary epochs. Such queueing systems, which are alternatively referred to as Markov modulated queueing systems, also appear in the context of queueing inventory systems, such as in the publications of Karlin [9] and Iglehart and Karlin [8]. Subsequently, the first to study an inventory system with a compound-Poisson demand process modulated by a finite-state Markovian random environment was Feldman [6]. Other inventory models that utilize a random environment include, but are not limited to Song and Zipkin [20], Ozekici and Parlar [17], and Perry and Posner [18].

A notable outcome of the study of Markov-modulated queueing systems is that their underlying Markov chains were found to be quasi-birth-and-death (QBD) processes, which are discrete- or continuous-time Markov chains whose transition matrix entries in block form are arranged according to a distinctive tri-diagonal pattern, as described by the seminal work of Neuts [15, 14], who also gives an analytic criterion for their positive recurrence. However, this criterion is limited to QBDs whose transition matrices possess infinitely repeating block rows, save for a finite number of boundary rows. Such QBDs are termed homogeneous or level-independent QBDs. These are in turn subsumed within a general class of QBDs whose rows do not repeat, and which are accordingly termed level-dependent QBDs, or LDQBDs. Markovian inventory models with underlying LDQBDs may be found in Artalejo et al. [2], Ushakumari [21], Krishnamoorthy, Nair, and Narayanan [11], and Ko [10]. Analytical criteria for the ergodicity and non-ergodicity of LDQBDs were eventually discovered by Cordeiro, Kharoufeh, and Oxley [5] for irreducible processes whose transition matrices exhibit element-wise row convergence to a single limiting block row, which we shall henceforth term row-convergent LDQBDs. Such behavior characterizes a plethora of useful queueing models, to include the inventory model that is considered in this paper.

To the best of the authors’ knowledge, the ergodicity criteria of Cordeiro et al. [5] has not yet been utilized to develop criteria for the stability of queueing inventory models whose underlying Markov chains may be classified as LDQBDs. Therefore, in this paper, we seek to address this concern by formulating a general traffic intensity formula application using the matrix analytic approach of Cordeiro et al. [5]. In addition, a means to evaluate the performance characteristics of such models in steady-state is likewise developed.

The remainder of this paper is organized as follows. Section 2 introduces the LDQBD and the drift criterion for the ergodicity of row-convergent LDQBDs. After a description of the instantaneous replenishment inventory system in Section 3, Section 4 establishes that its underlying LDQBD is row-convergent, upon which an analytic traffic intensity formula for the system is derived using the method of Cordeiro et al. [5]. With a means to determine positive recurrent inventory systems in hand, Section 5 develops steady-state average performance measures for positive-recurrent systems. Lastly, in Section 6, a comparison of average cost solutions of stable systems over systems of varying traffic intensity is presented.

2 Level-Dependent Quasi-Birth-and-Death Processes

A continuous-time level-dependent quasi-birth-and-death (LDQBD) process is a bivariate continuous-time Markov chain (CTMC) with state space

where is the set of non-negative integers and is some positive integer value. The -coordinate of is denoted as the level of the process while the -coordinate is the phase. The infinitesimal generator of consists of block entries that are arrayed in the distinctive tridiagonal form given by

| (1) |

where 0 denotes the zero matrix and the nonzero entries vary according to the level for each . If the block entries are invariant over all levels, that is, for all levels , save for a finite number of initial levels beginning with level 0, then the process is termed a level-independent, or homogeneous QBD. The closed-form ergodicity criterion for an irreducible continuous-time homogeneous QBD, which was derived by Neuts [15], is that the process is positive-recurrent if and only if

| (2) |

where is a column vector of the appropriate dimension (in this case ) whose scalar entries consist entirely of ones and is a -dimensional row vector that solves the linear system and . In either case, the process is referred to as skip-free, in deference to the characteristic that no transition of the process may exceed one level in either the positive or negative direction.

Next, we consider the discrete-time Markov chain (DTMC)

with state space that is embedded at transitions of the CTMC ; the transition times are enumerated according to . This is known as the jump process of . Its transition probability matrix exhibits the same tridiagonal block structure

| (3) |

The elements of for and for each and are the probabilities

For the purpose of determining system stability, it is necessary to restrict our attention to the class of irreducible discrete-time LDQBD processes for which the following element-wise limits

| (4) |

and, in addition,

| (5) |

In other words, the rows of transition probability matrix of , which is subject to Eqns. (4) and (5), approach a limiting row as the level increases. We henceforth term such discrete-time QBDs as row-convergent LDQBDs. As described in Cordeiro et al. [5], the discrete-time row-convergent LDQBD is positive-recurrent if and only if

| (6) |

where we define the average drift of process to be the scalar quantity

| (7) |

and is the unique -dimensional vector that solves the linear system

| (8) |

3 Model Description

The system that we consider here (refer to Figure 1) is a continuous-review inventory system that consists of a single-product storage facility and a single server that processes incoming demands. Letting , we define to be the fixed inventory storage capacity and to be the threshold level at which a replenishment of the inventory is triggered. If the level of product in the inventory drops to the threshold level of , an instantaneous replenishment of items occurs. Such a replenishment policy maintains the inventory level in the range , which enforces the requirement that only one replenishment takes place at any instant of time.

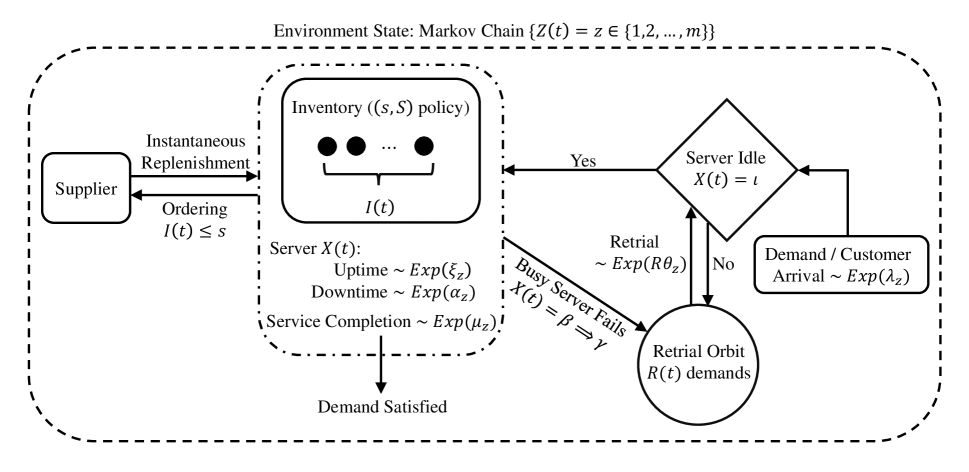

In order to consider the mathematical performance measures of the system in equilibrium, we will model this inventory system as a standard retrial queueing system with a Poisson arrival stream of demands that possesses an average interarrival duration of and a single server that processes incoming demands according to exponential service durations that are of average length . In lieu of a standard FIFO queue, there is, instead, a retrial orbit with unrestricted capacity for unsatisfied demands that proceed here from a busy or failed server. While in orbit, each of these demands will re-attempt service independently of all other demands in orbit at intervals distributed exponentially with average length . This results in a combined output stream with an inter-retrial duration that is distributed exponentially, with an average duration of , where is the current number in orbit.

Before any incoming demand is satisfied, it must be processed by the system server. The server is assumed at all times to be in one of three states, namely idle and operational, busy and operational, or failed. A server that is failed will not satisfy a demand for the product. The server remains operational for an exponential duration with an average length , after which it is considered to be in a failed state. Repair of the server commences immediately for an exponential duration of the average length , after which the server is returned to a fully operational and idle state.

At the time , it is assumed that the server is idle and operational, the inventory is at its maximum level , and there are no demands in the system. Thereafter, single demands arrive to the server according to the specified Poisson process. If the server is idle, processing of the incoming demand commences, and the server assumes a busy state. If the server does not fail, then the inventory is decremented by one unit at the end of the service duration and the demand then leaves the system. Subsequently, if the inventory decrements to items, then an instantaneous replenishment to the full capacity of the inventory takes place.

On the other hand, if a demand encounters a busy or a failed server, it will proceed directly to the retrial orbit. Likewise, if the server fails while in a busy state, the demand being processed will immediately proceed to the retrial orbit. In either case, the number in inventory will not be decremented. A demand in orbit may obtain service only when the combined retrial duration with rate ends when the server is idle. Afterward, the orbit size is decremented to and a busy period of the server commences.

We seek to emulate the effect of external influences, such as fluctuations in economic conditions, by the inclusion of a random environment that varies the exponential distributions of inter-demand arrival times, its subsequent processing (service) times, service up- and down-times, and times between retrials of service. Accordingly, the random environment process will be defined here as a finite-state irreducible CTMC with state space , and infinitesimal generator . In the standard way, we denote the total rate out of state as

If at a time instant , then the exponential parameters of each process appear as follows:

| Process | Arrival | Service | Uptime | Downtime | Retrial | Environment |

|---|---|---|---|---|---|---|

| Rate |

For convenience, the parameters are expressed as entries of the respective -vectors , , , , , and .

We next define the random variables that reflect the state of the system at time . Let

Due to the fact that all of the time durations of the process are exponentially distributed, the Markov property holds. Consequently, we may define the system as the Markov chain

with the state space

For convenience, we define the finite phase state partition of as the set

If the elements of this set are enumerated in lexicographic order as

we may then rewrite the state space as

Moreover, the process possesses an infinitesimal generator matrix , where both and belong to . The rows and columns of the matrix are arranged according in the lexicographic order of ascending orbit size (level) and the order given in at each level . The matrix consequently appears as in Eqn. (1).

Elements of the generator matrix of will next be specified. For the purpose of simplification, we define for each the scalar values

The resulting entries of for and at each level are depicted in Table 1.

| Initial | Terminal | Description | |||

| 2 | Successful retrial | ||||

| 1 | Environment (idle) | ||||

| Arrival while idle | |||||

| Server fails while idle | |||||

| Diagonal entry (idle) | |||||

| Environment (busy) | |||||

| Demand, | |||||

| Demand, restocked | |||||

| Diagonal entry (busy) | |||||

| Environment (failed) | |||||

| Server repaired | |||||

| Diagonal entry (failed) | |||||

| 0 | Server fails when busy | ||||

| Arrival while busy | |||||

| Arrival while failed |

We next formulate in terms of higher-level block entries. As in Neuts [16], let denote the diagonal matrix whose nonzero entries are the corresponding entries of the -vector . The nonzero -dimensional square block entries , , and of defined in Eqn. (1) appear as

where the -dimensional square matrices , , , and are given by

and, for each , the -dimensional square matrices , , and are defined as

| (9) |

The ‘0’ terms in each of the preceding matrices and those that follow are square matrices (or scalars) whose dimensions are given by the context in which they appear.

As a result of the preceding construction, the following result may be stated:

Theorem 1.

Proof.

It remains to show that is a row-convergent discrete-time LDQBD. That its transition probability matrix is of the form given by Eqn. (3) is a fundamental property of jump processes of continuous-time LDQBDs. Accordingly, we begin by constructing the block matrices for each as defined in Eqn. (3), followed by the determination of the element-wise limit

if it exists. For convenience, we will define the - (row) vectors , , and , whose entries consist of terms , , and , for each . Further, define for each the -dimensional composite block matrix

We divide each of the rows of by the corresponding diagonal (nonzero) entries of to obtain the -dimensional square matrix of the jump process:

where the -dimensional square matrix and

is the matrix with scalar diagonal entries set equal to 0.

The subsequent computation of the limiting matrix will be accomplished in an element-wise fashion. Its expression will require the limiting matrix

for which the terms

| (10) |

are evaluated in an element-wise manner. Using the shorthand

for two square matrices and , we obtain the limiting matrix

with block elements given by

is thus a row-convergent LDQBD, which completes the proof of the Theorem. ∎

4 System Stability

An analytic traffic intensity formula will now be derived for the inventory model of this discussion. It is a well-known fact (see Sennott, Humblet, and Tweedie [19]) that the ergodicity or non-ergodicity of an irreducible continuous-time LDQBD is equivalent to that of its embedded, or jump, chain . Moreover, as it was shown in Theorem 1 that is a row-convergent discrete-time LDQBD, the ergodicity condition Eqn. (6) may be used to obtain an analogous drift condition for its stability, which appears as the following result.

Theorem 2.

The continuous-time LDQBD process is positive recurrent if and only if

| (11) |

where the -dimensional row vector solves the system of equations given by

and is the -dimensional column vector of ones. All multiplicative and additive binary relationships in Eqn. (11) are performed element-wise, save for the operation ‘’, which denotes the vector dot product.

Proof.

Let be the jump process of . The criterion given in Eqn. (11) for the positive recurrence of will be derived from the limiting average drift of that was defined in Eqn. (7). In order to compute , the row-vector solution

of the system expressed by Eqn. (8) is required. Note that the vector is written in partitioned form according to the states . For example, the notation denotes the -dimensional partition of for which is held constant and the -dimensional partition for which both and are fixed.

When expanded, the system of equations expressed by Eqn. (8) becomes

| (12) |

We will proceed by induction on the inventory difference term . Consider an inventory system in which . The linear system in Eqn. (12) may be written in vector-matrix form as

| (13) |

with the partitioned vector solution.

For convenience, we will now write Eqn. (13) as the transpose system

which, when expanded, becomes

| (14) |

where each occurrence of the symbol 0 represents the array of zeroes. The solution of Eqn. (14), re-expressed as a column vector with -entry partitions, is most expediently obtained if one first solves the system in terms of the block matrix entries of the corresponding coefficient matrix, from whence we will obtain a vector solution with block matrix entries. This solution may then be easily converted to the requisite scalar vector solution of Eqn. (14).

Variable substitutions will now be made in Eqn. (14) in order to accommodate the expression of systems of matrix terms. First, we replace each occurrence of the -dimensional vector variables with the matrix terms , for each and for each . Consequently, one may perform the conversion from the vector with diagonal matrix entries to the corresponding -entry row vector via the relationship

| (15) |

Next, we replace the entries of the last row of the coefficient matrix with the identity matrix . For the moment, the on the right-hand side will be replaced with the indeterminate quantity until an appropriate value can be determined.

We may then rewrite the system in Eqn. (14) as

| (16) |

We denote the solution of the system in Eqn. (16) as the (row) vector of matrix entries. Once it has been established that the individual entries of , for and , of this system are diagonal matrices, then we may, in a manner analogous to that of Eqn. (15), say that the vector-multiplicative operation

| (17) |

yields a -dimensional row vector with scalar entries.

In order to solve Eqn. (16) using conventional methods for linear systems with scalar unknowns, it would be necessary for all elements of the coefficient matrix to be diagonal matrices. However, the generator matrix of the random environment is not diagonal. In addition, since row sums of are not multiples of , it is not ‘stochastic’ in the block-matrix sense, which, in effect, causes the system to become inconsistent for any value of . To overcome this difficulty, we will first solve for what will be termed a -homogeneous solution of Eqn. (16) by setting , which then results in the matrix becoming ‘stochastic’ in the block-matrix sense. We thus solve

| (18) |

where we allow to be an indeterminate quantity. Using a symbolic linear equation solver, we thus obtain

where

Next, the non--homogeneous system in Eqn. (16) will be solved. In order to do this, we first define the matrix

where is the stationary probability vector of the random environment that was defined in the statement of the Theorem.

Proposition 1.

Proof.

(Proposition 1) That is a solution to Eqn. (16) may be verified by evaluating the system in Eqn. (16) with the given value of and subsequently applying the identity

Uniqueness is a consequence of the fact that is a ‘stationary vector’ of the system in Eqn. (16).

Finally, we will state without formal demonstration that, regardless of whether one evaluates the system in Eqn. (16) as a block-matrix system with the column vector solution of -dimensional matrix entries or as a scalar system with the scalar-entry row vector solution , equivalent results are produced (up to a block-matrix interpretation). This is a consequence of the fact that is expressed entirely in terms of diagonal matrices. ∎

We may use Proposition 1 to construct a vector solution with scalar entries to the system in Eqn. (14), which is detailed in the following result:

Proposition 2.

Proof.

(Proposition 2) It is first necessary to apply Eqn. (15) in order to convert into a (column) -vector term, which is then normalized into a probability vector through division by the following scalar:

Substituting the resulting expression, defined as in the statement of Proposition 2, into the linear system in Eqn. (14) shows that is indeed a solution to this system. ∎

Now that a limiting stationary vector is in hand, we proceed to compute the corresponding limiting drift expression. First, we observe that is composed of repeating blocks of -dimensional vectors , where

which yields

By Eqn. (7), we compute

| (20) |

For the induction step, we assume that the drift expression Eqn. (20) holds for . The stationary probability vector for this model may then be obtained as

For an model, the matrix gains an additional repeated block matrix row, from which we deduce the new stationary probability vector to be

We now repeat the previous computation of drift as

| (21) |

By then setting , we obtain the expression in Eqn. (11) for the positive recurrence of , and the Theorem is proven. ∎

By reformulating the average drift in Eqn. (21) as a traffic intensity, the performance measure of average server occupancy of in steady state is obtained. This is accomplished by setting and rearranging terms, which leads to the following Corollary to Theorem 2.

Corollary 1.

The traffic intensity of the process may be written as

| (22) |

Subsequently, the continuous-time LDQBD process is positive recurrent if and only if .

5 Steady-State Distribution and Performance Measures

If , then by Theorem 1, is positive recurrent. In this case, the joint steady-state probabilities are defined as

exist. Since is a finite set, we may enumerate the elements of this set as , where we define the th element of as and . The steady-state probabilities may then be expressed more concisely as

whereupon we may define the -dimensional row vectors

of steady-state probabilities of grouped according to orbit size . Assuming the positive recurrence of , one may infer the presence of the matrix-geometric relationship between terms of , which is given in Bright and Taylor [3] for as

| (23) |

where the rate matrices are the minimal non-negative solutions to the system of equations

| (24) |

and the level 0 steady state probability is the minimal vector solution to

| (25) |

Since it is unlikely that Eqn. (24) and Eqn. (25) have closed-form solutions; however, it is more expedient to produce estimated measures of performance. To this end, one may apply one of several established algorithms that were developed for the purpose of estimating the steady-state distribution of an LDQBD, such as that of Bright and Taylor [3]. The method, via Algorithm 1, produces estimated stationary probabilities of a truncated system , say, at some level (orbit size) that is sufficiently large. The term ‘sufficiently large’ is used in the context of the fact that

In other words, the estimates become progressively more accurate as the system is truncated at larger levels . Because Algorithm 1 produces successive estimates of by means of the matrix geometric recurrence relation Eqn. (23), there is a need to efficiently compute the rate matrices , a task for which Algorithm 2 is utilized.

With the steady-state distribution of the system in hand, the asymptotic performance measures of the queueing inventory system may be obtained, beginning with the marginal steady-state probabilities of the server status:

| Idle Probability: | ||||

| Busy Probability: | ||||

| Failure Probability: |

Likewise, the steady-state probability of the number of demands in orbit is the marginal probability

The long-run expected number of demands in orbit () and the system (L) may then be expressed in the usual way as

Temporal measures of queueing performance require the long-run average exponential input rate over environment states, which for the stationary probability vector of , is given by

We may then apply Little’s Law to obtain the long-run expected wait times of demands in orbit ( and in the system ():

| (26) |

The next result provides for the independence of all performance measures defined thus far on the state of the inventory.

Proposition 3.

The performance measures , , , and are independent of the inventory threshold values and .

Proof.

As may be ascertained from the nonzero blocks , , of the infinitesimal generator matrix whose entries are listed in Table 1, the evolution of the inventory state does not affect any of the exponential rates that appear in the third column of the Table, either through the appearance of or of any rate term that pertains to restocking delay or some other duration related to the number in inventory. Thus, the marginal distributions of orbit size, as well as the probabilities of server state, along with any performance measures derived from these probabilities, do not depend on the value of , and hence of or . ∎

The system performance-measures of inventory level, depletion, and replenishment require the steady-state distribution of the number of products in the inventory, which is given by the marginal long-run probabilities of there being in inventory

From this distribution, we may obtain the long-run expected inventory level as

| (27) |

The computation of is greatly simplified by the fact that its value is dependent solely upon the quantities and , as stated and proved in the following Lemma.

Lemma 1.

The steady-state probability distribution of the amount in inventory for the positive recurrent process is given by

Consequently, the expected inventory content may be computed as

| (28) |

Proof.

See the Appendix. ∎

For the long-run expected time to deplete (or replenish) the inventory from the maximum level , we observe that the inventory decrements by one just before a demand exits the system. Thus, depletion from the maximum level of items occurs whenever customers are successfully processed, which is, on average, average system sojourn times . Thus,

To obtain the long-run ordering rate , we use the fact that there is one order per depletion time so that

On the other hand, the long-run supply rate is given by the number of items ordered per depletion time . Thus,

6 Optimization Study

In this section, the minimal long-run average costs for the operation of three stable inventory systems of the type described in Section 3 are considered. The objective here is to compare and contrast the optimal inventory threshold parameters and that correspond to the minimum operational cost of systems in steady state over increasing traffic intensity . In what follows, the construction of the inventory systems of interest, along with the formulation of the steady state cost function from queueing parameters and associated steady state performance measures, is described. A method is then given to determine a unique minimal-cost pair (up to a choice of ) for any inventory system of the type described in this paper.

6.1 System Definitions

The construction of stable inventory systems of varying traffic intensity may be accomplished through appropriate choices of the exponential parameters , , , and that produce increasing values of within the interval . In addition, it is ensured that several states in each system exhibit values of the single-environment traffic intensity function (derived from Eqn. (22) with ), given by

that are greater than 1, despite having an overall traffic intensity of . The resulting exponential parameters for each system, together with for each , appear in Tables 2, 3, and 4, respectively.

| Environment () | ||||||

|---|---|---|---|---|---|---|

| 1 | 1.0 | 13.0 | 0.05 | 7.0 | 1.00 | 0.0810 |

| 2 | 8.0 | 1.2 | 3.80 | 0.8 | 0.10 | 9.9600 |

| 3 | 0.3 | 17.0 | 0.02 | 15.0 | 4.00 | 0.0188 |

| 4 | 2.0 | 12.0 | 0.30 | 12.0 | 2.00 | 0.1911 |

| 5 | 0.5 | 18.7 | 1.00 | 5.0 | 5.00 | 0.0812 |

| 6 | 1.0 | 15.0 | 1.20 | 2.8 | 0.10 | 0.1623 |

| 7 | 5.0 | 6.0 | 4.00 | 0.5 | 0.05 | 4.9000 |

| Environment () | ||||||

|---|---|---|---|---|---|---|

| 1 | 6.0 | 7.0 | 5.0 | 2.0 | 1.0 | 2.1667 |

| 2 | 0.1 | 4.2 | 0.8 | 0.1 | 1.7 | 0.3400 |

| 3 | 1.0 | 8.0 | 1.0 | 15.0 | 2.0 | 0.2296 |

| 4 | 0.8 | 10.0 | 0.3 | 12.0 | 2.0 | 0.1087 |

| 5 | 2.0 | 4.5 | 1.0 | 5.0 | 5.0 | 0.6182 |

| 6 | 0.5 | 2.0 | 0.7 | 13.0 | 1.0 | 0.4544 |

| 7 | 9.0 | 0.3 | 0.2 | 0.5 | 0.5 | 25.6000 |

| Environment () | ||||||

|---|---|---|---|---|---|---|

| 1 | 2.0 | 7.0 | 0.50 | 2.0 | 0.05 | 0.4000 |

| 2 | 1.2 | 9.9 | 2.01 | 0.2 | 1.50 | 1.2821 |

| 3 | 1.7 | 8.5 | 0.05 | 4.1 | 4.20 | 0.2071 |

| 4 | 1.2 | 2.7 | 0.30 | 6.8 | 0.40 | 0.5176 |

| 5 | 4.6 | 13.1 | 1.90 | 2.1 | 0.10 | 0.7108 |

| 6 | 10.2 | 1.1 | 2.70 | 1.5 | 0.90 | 8.2263 |

| 7 | 0.3 | 3.9 | 0.10 | 3.2 | 0.50 | 0.1023 |

Lastly, we define a common random environment with the infinitesimal generator given by

The Bright and Taylor algorithm is then applied to each of the systems, which are truncated to a maximum orbit size of . A representative set of steady-state performance measures for each of the three resulting systems is provided in Table 5 for set inventory threshold values of and . Within this set of values, it can be verified that the average long-run inventory size in Table 5, which is computed directly from the first moment of inventory size Eqn. (27) for each system, agrees with the value of calculated using formula Eqn. (28) of Lemma 1.

| Probability | Performance Measure | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Traffic | Idle | Busy | Failed | |||||||

| Low | 0.6061 | 0.2052 | 0.1887 | 1.5971 | 1.8023 | 0.6745 | 0.7612 | 23 | 19.0299 | 0.1692 |

| Medium | 0.2577 | 0.5516 | 0.1907 | 8.8412 | 9.3928 | 3.0707 | 3.2623 | 23 | 81.5578 | 0.4071 |

| High | 0.2891 | 0.4492 | 0.2618 | 13.3542 | 13.8034 | 4.6129 | 4.7681 | 23 | 119.2021 | 0.7305 |

6.2 Results

The steady-state average cost function will now be defined and then analyzed for the presence of minimal values. The elements of the cost function are defined similarly to those of Ko [10], as defined here:

-

•

: inventory holding cost per item per unit of time,

-

•

: blocking cost per item sent to the retrial orbit per unit of time,

-

•

: reordering cost per order from the supplier,

-

•

: purchase, or procurement, cost per item.

Using these elements, together with the average system parameters defined in Section 5, we define the steady-state mean total cost per unit time as

and the pairs of inventory thresholds are, for some fixed , taken from the feasible region

The steady-state average cost optimization problem may now be stated as

| (29) |

where the cost coefficients are assigned the fixed values

By Proposition 3, it may be inferred that the performance measures and are independent of and , and are therefore constant in . This permits an analytical solution to optimization problem Eqn. (29), which appears in the following theorem.

Theorem 3.

Proof.

Let be an arbitrary feasible point satisfying . Then for any value of , the value of can be reduced by decreasing both and by the same amount, since all terms in the objective function are held constant except the first term, which is reduced. Therefore, cannot be locally optimal, which means that is optimal. This reduces the optimization problem to the single variable minimization of

where must hold. Then applying first and second-order optimality conditions, we have

for all . Solving for yields and . Since must be integer and for all , is convex (which ensures uniqueness in this case), and the result is obtained by taking the two integer values that bracket and choosing the one with a smaller function value, but ensuring that the floor function does not drop below (to enforce ). ∎

By applying Theorem 3 to the systems constructed in Section 6.1 for , we arrive at the results for an optimal steady-state average cost that appears in Table 6. The values of the optimal average cost demonstrate the expected monotone increasing behavior with traffic intensity, primarily due to the penalty cost for demands held in orbit. Observe that the minimum cost for the low- and medium-traffic systems are not corner points of , in spite of the constant value of the lower inventory threshold. It is anticipated that a similar formulation for an analogous model with replenishment delay and accompanying penalties for such delays will result in interior-point solutions for those models.

| Traffic Setting | ||

|---|---|---|

| Low | 42.57 | |

| Medium | 44.35 | |

| High | 49.49 |

7 Conclusion

Due to the novel approach enabled by the results contained in Cordeiro et al. [5], it is now possible to derive a closed-form traffic intensity condition for a complex inventory system with exponential rate parameters modulated by a random environment. Particularly notable is the compact matrix-vector form of the traffic intensity formula, whose complexity of expression is unaffected by the number of defined environments and the magnitude of inventory thresholds, thus enabling the construction and subsequent numerical investigation of stable systems.

Such follow-on numerical studies must first proceed with the computation of optimal steady-state average costs for systems with replenishment delay. While simplifying the assumption of instantaneous replenishment is sufficient to demonstrate the efficacy of the method of Cordeiro et al. [5] in deriving a closed-form traffic intensity and to the provision of a basic framework for a cost-optimization study, it prevents the analysis of performance measures that pertain to delays in stock replenishment. It is anticipated that extending the current inventory model to incorporate such a feature would facilitate a more comprehensive numerical investigation into its optimal-cost characteristics.

Beyond such incremental directions in the study of inventory systems similar to the one of this paper, the method described herein to derive a closed-form traffic intensity may potentially be used for other queueing inventory models whose underlying Markov chains are row-convergent LDQBDs. Some relevant examples are multi-server queueing models, multiple product inventory models, and perishable systems with Markovian product degradation, among what is anticipated to be many others.

Competing Interests: The authors have no competing interests to report.

References

- [1] K. J. Arrow, T. Harris, and J. Marschak. Optimal Inventory Policy. Econometrica, 19(3):250–272, Jul 1951.

- [2] J. Artalejo, A. Krishnamoorthy, and M. Lopez-Herrero. Numerical analysis of inventory systems with repeated attempts. Annals of Operations Research, 141(1):67–83, 2006.

- [3] L. Bright and P. Taylor. Calculating the equilibrium distribution in level dependent quasi-birth-and-death processes. Communications in Statistics: Stochastic Models, 11(3):497–525, 1995.

- [4] E. Çınlar. Introduction to Stochastic Processes. Prentice-Hall, Englewood Cliffs, NJ, 1975.

- [5] J. Cordeiro, J. Kharoufeh, and M. Oxley. On the ergodicity of a class of level-dependent quasi-birth-and-death processes. Advances in Applied Probability, 51(4):1109–1128, 2019.

- [6] R. M. Feldman. Continuous review inventory system in a random environment. Journal of Applied Probability, 15(3):654–659, 1978.

- [7] J. D. M. Fisher and A. Hornstein. inventory policies in general equilibrium. Review of Economic Studies, 67(1):117–145, 2000.

- [8] D. Iglehart and S. Karlin. Optimal policy for dynamic inventory process with nonstationary stochastic demands. In K. Arrow, S. Karlin, and H. Scarf, editors, Studies in Applied Probability and Management Science, pages 127–147. Stanford University Press, Redwood City, California, USA, 1962.

- [9] S. Karlin. Dynamic inventory policy with varying stochastic demands. Management Science, 6(3):231–258, Apr 1960.

- [10] S.-S. Ko. A nonhomogeneous quasi-birth-death process approach for an policy for a perishable inventory system with retrial demands. Journal of Industrial & Management Optimization, 16(3):1415–1433, May 2020.

- [11] A. Krishnamoorthy, S. Nair, and V. C. Narayanan. An inventory model with server interruptions and retrials. Operational Research, 12(2):151–171, Sep 2012.

- [12] V. G. Kulkarni. Modeling and Analysis of Stochastic Systems. Chapman & Hall/CRC Texts in Statistical Science. Taylor & Francis, Boca Raton, FL, 1st edition, 1996.

- [13] M. F. Neuts. A queue subject to extraneous phase changes. Advances in Applied Probability, 3:78–119, 1971.

- [14] M. F. Neuts. Further results on the queue with randomly varying rates. OPSEARCH, 15(4):158–168, 1978.

- [15] M. F. Neuts. The queue with randomly varying arrival and service rates. OPSEARCH, 15(4):139–157, 1978.

- [16] M. F. Neuts. Matrix-Geometric Solutions in Stochastic Models: An Algorithmic Approach. Dover Books on Advanced Mathematics. Dover Publications, New York, NY, 1981.

- [17] S. Özekici and M. Parlar. Inventory models with unreliable suppliers in a random environment. Annals of Operations Research, 91:123–236, 1999.

- [18] D. Perry and M. Posner. Production-inventory models with an unreliable facility operating in a two-state random environment. Probability in the Engineering and Informational Sciences, 16(3):325–338, 2002.

- [19] L. I. Sennott, P. A. Humblet, and R. L. Tweedie. Mean Drifts and the Non-Ergodicity of Markov Chains. Operations Research, 31(4):783–789, 1983.

- [20] J. S. Song and P. Zipkin. Inventory control in a fluctuating demand environment. Operations Research, 41(2):351–370, 1993.

- [21] P. V. Ushakumari. On inventory system with random lead time and repeated demands. Journal of Applied Mathematics & Stochastic Analysis, Volume 2006. Article ID 81508:1–22, 2006.

- [22] U. Yechiali and P. Naor. Queuing problems with heterogeneous arrivals and service. Operations Research, 19(3):722–734, 1971.

8 Appendix

Proof of Lemma 1

Proof.

We first define the continuous-time stochastic process on the state-space of inventory states . We will first need to establish that is a semi-Markov process (SMP) with transition epochs taken from the service completion times of , with . To do this, we will define the variables

The process is considered an SMP if (1) it is a piecewise-constant, left-continuous process, and (2) the sequence of bivariate random variables is a Markov renewal sequence (MRS). It can easily be seen that (1) is inherited from . Using the well-known fact that end-of-service epochs in a Markovian queueing system are stopping times, as defined in Çinlar [4], (2) may be shown by means of a routine validation of each of the axioms that define an MRS (see Kulkarni [12]). We may thus conclude that is an SMP with kernel , where

Furthermore, possesses the embedded DTMC with the associated transition probability matrix .

With established as an SMP, we may now utilize Kulkarni [12, Theorem 9.27] to compute the steady-state distribution for . This result requires that exhibits the properties of irreducibility, aperiodicity, and positive recurrence. Since irreducibility and periodicity are inherited from the parent process , it remains to show that is positive recurrent. Let be the time of first jump of to state , namely

which is also the time of the first entry of into the set of states for which . Also, define the conditional distributions of time for to reach state from and the expectations associated with these distributions as

These may likewise be interpreted as the conditional probabilities of the time of the first jump of into beginning in , and their expected values. In order to conclude that is a positive recurrent SMP, it must be shown that and for every .

Consider any state and suppose that is in state at time . In this case, is presumed to be in some state

where . After the return time has elapsed, for the SMP . However, it is possible that is in a different state

and thus , which is the time of first return of to . However, if we consider the quantities

then, since has been assumed to be positive recurrent, it must then be true that and . In other words, returns to state with probability 1, which simultaneously implies that must likewise return to with probability 1. Hence . Moreover, since for any given initial state for , the properties of expected values yield the inequality

Therefore, since was arbitrarily chosen, must be positive recurrent.

It now remains to compute the steady-state probability distribution of the SMP , from which we may obtain the quantity . For each , let

be the steady-state probability of being in state for the irreducible, aperiodic, and positive recurrent SMP , which is then given by the expression

where is a positive row vector solution to the system , if it exists, and is the expected sojourn time of in state . To compute , we first construct the matrix of the embedded DTMC , which becomes

It is possible to visually determine that ; that is, for each .

In order to determine the quantities , we observe that the i.i.d. successive durations of time between service completions for each coincide with the sojourn times of in each of its states . Moreover, since Proposition 3 informs us that the length of these sojourn times is independent of any given inventory size , we may conclude that

Also, because of the positive recurrence of , we have

Therefore, the steady-state probability of inventory size may be calculated as

Substituting each of these terms into Eqn. (27) gives

whereupon application of the identity

yields Eqn. (28). ∎