Geometric insights into robust portfolio construction

Abstract

We investigate and extend the results of Golts and Jones [19] that an alpha-weight angle resulting from unconstrained quadratic portfolio optimisations has an upper bound dependent on the condition number of the covariance matrix. This implies that better conditioned covariance matrices produce weights from unconstrained mean-variance optimisations that are better aligned with each assets expected return. We provide further clarity on the mathematical insights that relate the inequality between the -weight angle and the condition number and extend the result to include portfolio optimisations with gearing constraints. We provide an extended family of robust optimisations that include the gearing constraints, and discuss their interpretation.

keywords:

mean-variance optimization , Kantorovich inequality , gearing constraintsMSC: 91G10 90C20 62P05

1 Introduction

Using a geometric construction that relates the angle between the vector of expected returns and portfolio weights determined under an unconstrained mean-variance optimisation, Golts and Jones [19] were able to quantify the distortions induced by the optimisation process. They were able to link this angle directly to the condition number of the covariance matrix by showing that this angle has an upper bound dependent on the condition number. Therefore, when a covariance matrix is ill-conditioned, or close to degenerate, the alpha-weight angle should be very large; whereas well-conditioned matrices ensure the angle remains within tight bounds.

In general portfolio construction a key question remains to what extent one should drag the optimal bets towards the direction of expected asset returns. In the unconstrained case this is clear because in the mean-variance setting the resulting portfolios will be multipliers, or geared realisations, of the optimal risky portfolio, that is, the result of solving a Sharpe ratio maximisation (F).

Here we investigate the mathematical relationship between this angle, the alpha-weight angle, and the condition of the covariance matrix in more generality. Golts and Jones [19] argued the case for dragging optimal weights towards the direction of alpha for a family of unconstrained quadratic optimisations. Here we extend this family of portfolio choice problems to include a gearing constraint and to consider whether their geometric insights are more generally applicable for practical investment management decision making. The gearing constraint defines exactly how much of the portfolio should be invested (whether it be fully invested, partially invested or geared) and is a fundamental portfolio construction constraint in much of the unit-trust, exchange traded fund and the related collective investment scheme industry. This constraint is to be differentiate from a leverage constraint, which relates the size of portfolio bets relative to a level of borrowing.

Reducing the angle between the weights and expected return vector is not equivalent to the implementation of a return maximisation, or return maximisation constraint. The case of pure return maximisation would result in a portfolio that weighs toward the asset with the greatest expected return, and not the direction of the expected return vector in general. In practice the -weight angle should never be zero as there is always a residual correlation between the assets. In mean variance optimisations there is always a conundrum due to correlation specification error – and the degree of shrinkage should best reflect this. The test of how much one should intervene can only be determined by out-of-period portfolio performance simulation, which is out the scope of this paper.

Concretely, we aim to promote the important benefits related to improving the conditioning of the covariance matrix in the out-of-sample performance of an asset portfolio if the estimated covariance matrix is used for decision making. However, here we specifically promote these benefits in the sense of reducing the angle between the direction of the optimal portfolio in the control space relative to that of the expected asset returns. We feel that this better explains where and how improved conditioning may be beneficial. This is explicitly demonstrated when mean-variance optimisation is strictly followed in an investment process. We hope that this provides insights into how to better manage the combined impact of return expectations and covariance estimation when making asset allocation decisions that require the explicit inversion of the covariance matrix and are governed by the gearing requirement (explicit or implicit).

This will also provide the added advantage of an intuitive geometric interpretation that can be robust. The key insight is that it is not merely covariance matrix inversion, hence error maximisation more generally, that is problematic, but rather that the inversion of a poorly conditioned covariance matrix pushes the direction of an optimal portfolio erroneously away from the direction of expected returns. This implies that when improving the conditioning of a covariance matrix this should be done in a way that pulls the optimal portfolio towards the direction of expected returns – irrespective of whether or not one may be in the presence of constraints. One should first find a shrunk covariance matrix that achieves this, and then ensure that constraints are satisfied.

1.1 Estimation uncertainty

Quadratic or mean–variance analysis was introduced by Harry Markowitz in his seminal 1952 paper [36] to establish what is today known as Modern Portfolio Theory. Within this framework a rational investor selects a portfolio based on the trade-off between estimated expected return and risk. Despite the elegance of this, the practical implementation has a variety of short-comings, with optimised portfolios perceived to to “behave badly” out of sample. Michaud [39] argues that mean variance optimisation often leads to non-intuitive results with unstable weights, further characterising it as being an“error maximiser”.

Additionally, even if means and variances could accurately represent asset class distributions, the theory assumes both future expected returns, and the covariance matrix of asset returns are known, or even that they can be known. The presence of estimation error in input parameters unfortunately makes the use of Modern Portfolio Theory in its classical Markowitz formulation impractical. The short-comings and non-robust nature of mean-variance optimisation has been extensively discussed in the literature, with highlights including the work by Best and Grauer [6], Frankfurter et al. [16], Jobson and Korkie [29, 30], Zimmermann and Nierdermayer [44], Broadie [8], Michaud [39], and Chopra and Ziemba [12].

A broad variety of different forms and approaches to robust optimisation are documented in an extensive literature. As a small subset, Costa and Paiva [14], Halldorsson and Tutuncu [21], Goldfarb and Iyengar [18], and Ceria and Stubbs [11] have proposed various, and unique, specifications of the uncertainty set of the input parameters. Performance and risk metrics of robust portfolios have been shown to be distinct from [36] optimal portfolios. Tutuncu and Koenig [42] showed that robust portfolios tend to investment in fewer assets and display less turnover over time. Increase in the size of the uncertainty sets, when using robust portfolio optimisation procedures, means they tend to under-perform in the more likely scenarios, but crucially display more reasonable tail behaviour.

In order to ameliorate the effect of estimation errors in the estimates of expected returns, attempts have been made to create better and more stable mean-variance optimal portfolios by utilising expected return estimators that have a better behaviour when used in the context of the mean-variance framework. One of the more common techniques is the utilisation of James-Stein estimators (see Jobson and Korkie [30]) to shrink the expected returns towards the average expected return based on the volatility of the asset and the distance of its expected return from the average. Jorion [31] developed a similar technique that shrinks the expected return estimate towards the minimum variance portfolio. The area of robust statistics (see [10]) has recently been employed to create stable expected return estimates as well. Chopra and Ziemba [12] show that errors in the sample mean estimate have a larger impact on the out-of-sample performance than errors in the sample covariance estimate.

In a similar way to estimating robust expected return inputs, one can also build a more robust process through focusing on the estimation of the covariance matrix, which is inverted in the mean variance optimisation process. Papers investigating different covariance matrix estimation techniques include Disatnik and Benninga [15], Clarke et al. [13], Jagannathan and Ma [28] and Bengtsson and Holst [5].This paper makes use of the methodology employed by Ledoit and Wolf [34], who argue that a shrunk covariance matrix should be used instead of the sample covariance matrix as it contains significant estimation error.The shrunk matrix represents a weighted average of the sample covariance matrix, and another structured matrix.

Black and Litterman [7] combine investor’s views with expected returns to generate more robust portfolios. They use reverse optimisation, using portfolio weights and the covariance matrix as inputs and providing the expected returns as output, avoiding the problem of estimation error in expected returns.

The Bayesian approach has been widely recommended for dealing with the estimation errors in the sample estimates, which involves eliminating the dependence of the optimisation process on the true parameters by replacing them with a prior distribution of the fund manager’s view. Brown [9] and Kan and Zhou [32] both investigate the Bayesian approach.

Other attempts to make improvements on the Markowitz mean-variance optimisation issues also includes the portfolio re-sampling methodology of Michaud [38] and Lai et al. [33]. Michaud introduces a statistical re-sampling technique that indirectly considers estimation error by averaging the individual optimal portfolios that result from optimising with respect to many randomly generated expected-return and risk estimates. However, portfolio re-sampling is an ad-hoc methodology that has pitfalls (see Scherer [41]). Lai et al. [33] propose a solution to a stochastic optimisation problem by extending Markowitz’s mean-variance portfolio optimisation theory to the case where the means and covariances of the asset returns for the next investment period are unknown.

Golts and Jones [19] provided a novel geometric perspective on robust portfolio contstruction using insights that arise when one separates the direction and magnitude of the portfolio position vector. They make no assumptions about the distribution of the returns and suggest making the covariance matrix better-conditioned by constraining the angle between the vector of optimised weights and expected returns – the “alpha” angle. The motivation for implementing a minimisation of the -angle is based on showing that this angle is bound by the condition number of the estimated covariance matrix. Here we demonstrate this relationship geometrically and mathematically using an extension of the Kantorovich inequality [25, 23] provided by Bauer and Householder [4]; this elegant machinery will be shown as useful in determining why this relationship exists. Inspiration for this idea can be seen in [2] where much of the geometric interpretation around matrices is described.

1.2 The efficient frontier and -weight angle

Consider a portfolio with assets, expected return vector , covariance matrix , and a fixed portfolio mean . To find this portfolio on the efficient frontier with asset weights , we perform a portfolio variance minimization111Here we use . [36, 37]:

| (1) |

Here we can use the Lagrange method and solve the Kuhn-Tucker conditions to find the optimal portfolio allocation as follows:

| (2) |

This is a classical Markowitz-type optimisation. It can be shown that all optimisation solutions where there are no gearing, or long-only constraints, are of similar form (see Table 1 below). The solutions all show that the results are calculated using the inverse of the covariance matrix contracted in the direction of the expected returns.

Various criticisms with regards to Markowitz portfolios noted that mean-variance optimised portfolios can have weights () that are quite different from the original “alphas” (). To quantify this difference one can look at the angle () between the vector of expected returns, , and the vector of optimised weights, where .

The mathematical formula for the angle is as follows:

| (3) |

The smaller this angle, the more aligned optimal portfolio weights are to expected alpha’s222Here as then . which would indicate a more reasonable and intuitive optimisation result. A poor optimisation result would be indicated by an almost perpendicular angle close to 90 degrees 333Here as then ..

Golts and Jones [19] describe the mathematical relationship between this angle and the condition of the covariance matrix; showing how a well conditioned covariance matrix can ensure a smaller alpha-weight angle (because is closer to one), and hence a more reasonable optimisation result. They show how this angle is bounded above zero by the condition number of the covariance matrix:

| (4) |

Here the condition number is the ratio of the largest eigenvalue, , to the smallest eigenvalue, . It is important to note that although has a lower bound, the actual angle has an upper bound.

Despite the intuitive nature of the result, the mathematical reasoning behind how this relationship came to be in the Golts and Jones [19] paper was not fully described and was only applied to portfolio optimisations that were unconstrained (see Table 1). To clarify, this paper refers to unconstrained optimisations as those described in Table 1, despite the fact that optimisation I and II each have a risk and return constraint respectively, and as the paper will show, some constraints are implicit in the problem. The optimisations described in Table 2, where gearing constraints are explicitly put in place, are referred to as the constrained optimisations.

| No Gearing Constraint Portfolio Choice | ||

|---|---|---|

| # | Optimisation | Constraints |

| I | ||

| II | ||

| III | ||

| IV | ||

1.3 Unconstrained -weight angle

We first motivate the original unconstrained result in Equation (4) [19] using the Kantorovich inequality [25, 24, 22] – this is a special case of the Cauchy-Schwarz inequality.

Theorem 1.

Kantorovich Inequality [25]

Let be a symmetric positive definite matrix with eigenvalues . Then for all ,

| (5) |

From Equation (2) we have that:

| (6) |

This is substituted into the -weight angle (3)

| (7) |

A symmetric matrix is equivalent to its own transpose:

| (8) |

The inverse covariance matrix can be factored in terms of a symmetric matrix so that , and then Equation (8) becomes:

| (9) |

Then let so that , and , and substitute these into Equation (9) to find:

| (10) |

The right hand side of Equation (10) is the square root of the left hand side of the Kantorovich inequality (5) thereby implying that

| (11) |

where has eigenvalues .

Following Golts and Jones [19] and noting that the condition number of the covariance matrix: , we can then show that an upper bound to the -weight angle exists and we recover Equation (4):

| (12) |

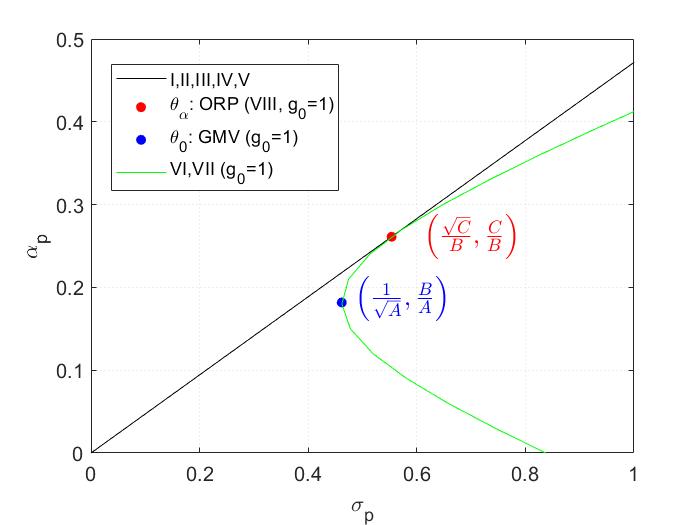

This shows that an improved condition number of the covariance matrix can improve the robustness of the optimisation procedure when constraints, such as that with gearing, a full investment constraint, or a long-only portfolio constraint are ignored. The idea is that as the conditioning of the covariance deteriorates the -angle necessarily increases. With improved conditioning, when there are no constraints, then the optimal portfolio weights can more easily align with the directions of the asset expected returns (See Figure 1).

Many funds have gearing restrictions and may not be outright short an instrument i.e. . A portfolio optimisation enforcing a long only constraint often has the problem that it cannot ensure that closed form solutions can be found. It is similarly problematic to include margin and diversity constraints (see G). A margin constraint is required when investing in futures, or where some sort of deposit proportional to the investment made is required [17, 20]: i.e. , for the margin account required for -th asset. When the level of margining is the same for all the assets this can be written as a leverage constraint of the form: .

However, it is possible to get closed form solutions for a gearing constrained optimisation; using the constraint for some gearing parameter . A fully invested portfolio with constraint is then a special case. These can be implemented as: a return maximisation with a linear and quadratic constraint (C), a portfolio variance minimisation with two linear constraints (D), a mean-variance optimisation with a linear constraint (E), or a Sharpe ratio maximisation with a linear gearing constraint (F).

2 The constrained -weight angle

2.1 Upper bound on the -weight angle

To prove that the lower bound on the -weight angle exists, we make use of the result derived by Bauer and Householder [4] who extended the Kantorovich inequality described in Theorem 1. The proof for this is investigated by Huang and Zhou [26].

Theorem 2.

Here is unbound above and bound by below: and hence we have that . This condition is weaker than that of Theorem 1:

| (14) |

because for .

2.2 Constrained -angle

Following from Equation (7) we can find an expression for the angle : . We can substitute from Equation (31) (or equivalently use from Equation (36)) into the -weight angle Equation (3) for the new angle :

| (15) |

Now, as performed in equations (8) to (10) we let , , and . Using these substitutions we find the desired result from Theorem 2 in Equation (16):

| (16) |

We can argue that for some angle , where and is smaller than the angle :

and then conclude that the -weight angle is still bound below by the condition number of the covariance matrix: . This then extends the geometric interpretation to include linear portfolio constraints, because the -angle is bounded above. Here with more generality, and thus as a weakened condition, to again imply that poor conditioning will limit our ability to align the portfolio weights with the expected returns.

There is now a tension between the linear constraint, the alignment of the optimal control with the direction of the expected returns, and the impact of the conditioning that would push the optimal portfolio out of alignment. This more complex tension is visualised in Figure (2) and we now need to include the role of the global minimum variance (GMV) portfolio .

3 The linear gearing constraint

Consider the optimisations in Table 1 but now include the gearing restriction:

| (17) |

Here gearing is used broadly in the sense of the ratio of exposure of the investment fund relative to the underlying equity444Theoretical the resulting efficient frontier is a linearly scaled version of a risk-return optimisation with a fully invested portfolio constraint; the generalisation is of practical importance for fund managers – see Figure 3. We differentiate this from the concept of leverage, which we use as a measure of the amount we have borrowed to gain exposure. Practically we will consider leverage to be measured by . This is important in order to differentiate the type of constraint we will impose in the fund management problems we consider and the limitations of this. The gearing constraint will not in general limit the extent to which bets are long/short within the fund.

Concretely, we consider four unconstrained optimisations, those in Table 1, and the four gearing constrained optimisations as shown in Table 2. We follow the work of Ingersoll [27] and Merton [37] who investigate and derive the results of optimal mean variance portfolios in detail. In our case, we will only need to investigate two portfolio choice problems in detail. First, that of minimising the portfolio variance and targeting the return with a gearing constraint. Second, by finding a mean-variance optimal portfolio with a risk aversion parameter with the same gearing constraint. Using these solutions we show that their -angles are bounded above (because the cosine is bound below) by some function of the condition number. We then extend the argument made by Golts and Jones [19] that the dragging optimal bets towards the direction of alpha is limited by poor conditioning, albeit in a weakened form.

Optimisation V and VIII in Table 2, respectively the return maximisation with a linear and quadratic constraint, and a Sharpe ratio maximisation with a linear leverage constraint, both trivially have optimal portfolios that are multiplies of the risky portfolio (C and F). This means that Theorem 1 is valid for optimisations I,II,III,VI,V and VIII. We only need to generalise and weaken the condition number lower bound for optimisation VI and VII.

3.1 Constrained minimum variance portfolio

We want to find an investment portfolio with minimum variance and a targeted return with the additional gearing constraint, hence we want to solve for:

| (18) |

This is optimisation VI in Table 2. This problem can be reduced to a Lagrangian with two Lagrange multipliers :

| (19) |

Solving for in terms of the Lagrange multipliers from Equation (19) by solving the Kuhn-Tucker equations to find:

| (20) |

Then with some algebra and using the convenient substitutions: , , and . Here A is the variance of the global minimum variance portfolio, B that of the optimal risky portfolio, is the Sharpe ratio, and D is positive by the Cauchy-Schwarz inequality because we have assumed that is non-singular and all assets do not have the same means. We can eliminate the two Lagrange multipliers (see D) to find the optimal portfolio control:

| (21) |

We can define two new portfolios and :

| (22) |

The optimal portfolio control can then be written in the form of a two fund separation theorem (see B) where the portfolios are weighted by a combination of gearing and expected portfolio return weighted portfolios, we might niavely anticipate that fixing the level of returns may fix the gearing if the solution is unique – this is not the case. In the return maximisation (optimisation VI) when we set the portfolio variance we will set the gearing (C) because the constraint is quadratic. That is no longer the case with risk minimisation.

To more intuitively understand the portfolio, we can also split the optimal portfolio into the global minimum variance portfolios and optimal risk portfolios . Arranging terms in equation (21):

| (23) |

This is convenient because we know that , , and that . The combination is a cash neutral portfolio whose weights sum to zero, and the individual portfolios are fully invested. We can factor out the geared global minimum risk portfolio to find

| (24) |

We see that the resulting portfolio is a combination of a leveraged global minimum risk portfolio and a geared cash neutral portfolio. With some weight this can be written as: . This is the form we will use more generally as in optimisation VI in Table 2.

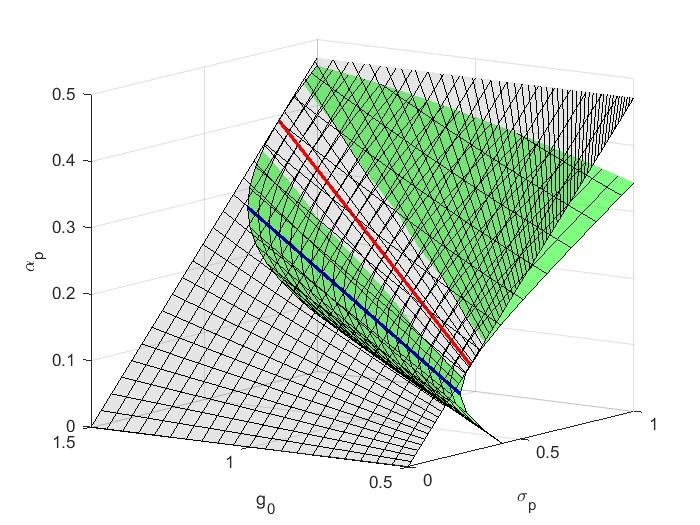

If we set the level of returns we notice that this has no effect on the overall gearing of the portfolio as long as it is part of the set of feasible solutions. It will just change our exposure to the cash neutral portfolio. This will then generate an efficient frontier surface in the space (see Figure 3b).

This does not imply that the the leverage is fixed as this changes with the portfolio return target changes, even for a set level of gearing, because our long/short bets in the cash neutral portfolio will then change. However, there is a minimum return associated with the set of global minimum variance portfolios generated by the different levels of gearing.

The equation of the minimum-variance set can be found using and Equation (20) to find:

| (25) |

Or equivalently from Equation (22) (which is equivalent to substituting for and from 96 and 97):

| (26) |

This is the equation of a parabola. In the mean-standard deviation space the curve is a hyperbola. We can find the set of global minimum variance portfolios with gearing.

First, find the expected return at the inflection point where the minimum variance portfolio is found:

| (27) |

Then find the target return in terms of the gearing, asset returns and asset covariance:

| (28) |

We can substitute this into Equation (23) to find that the second term is zero and that the first term factors cancel to then verify that this in fact just the geared global minimum variance portfolio as expected:

| (29) |

Equation (28) can also be used to eliminate the return target from Equation (26) to find the variance at the point of global minimum variance with gearing: .

We would like to now consider how the lower bound in Theorem 1 is weakened. Rewrite equation (21) as:

| (30) |

Equation (30) can be put into the form of where represents any vector of the same dimension as :

| (31) |

where is the same dimension as . By Theorem 2 we then know the angle between this portfolio and the alpha portfolio has a lower bound dependent on the condition number of the estimated covariance matrix. It is still advantageous to tilt the gearing constrained optimal portfolio towards alpha by improving the conditioning of the covariance matrix while maintaining the constraint.

With the choice of equation (28) we trivially have that . This would fix the angle between and the optimal portfolio. This means that the constraint will fix the tilt of the optimal portfolio relative to the when selecting for the global minimum variance portfolio on the efficient frontier. This means that we cannot naively tilt the optimal portfolio towards alpha if we have any form of gearing because this would break the constraint. We can however tilt the risky optimal portfolio towards alpha.

3.2 Constrained mean-variance optimal portfolio

We now consider the relationship between the gearing constrained minimum risk portfolio from Equation (18) and the gearing constrained mean-variance optimal portfolio:

| (32) |

This is optimisation VII in Table 2. The optimal control can be found by solving the Kuhn-Tucker equations to find the mean-variance optimal portfolios (see Appendix 21):

using and we find

| (33) |

The global minimum variance portfolio is . The sum of its weights are unity: ; this can be trivially seen by multiplying both sides of the equation for by the transpose of . The optimal portfolio can be written as the weighted sum of the GMV portfolio and the risky alpha portfolio :

| (34) |

Here with we have: .

We find that , which is a combination of the global minimum risk portfolio and an optimal risky cash neutral long/short portfolio: . We can factor out the global minimum variance portfolio in Equation (33) and with a bit of matrix algebra we see that the portfolio is made of a geared global minimum variance portfolio, whose weights sum to one, and a risky portfolio which is dependent on the return expectations and risk aversion [35] but can have gearing:

| (35) |

By considering the -th and -th components on the inner bracket in the matrix product in the second term, it can be seen to be driven by the pairs of relative alpha: where . The first term on the left in the bracket is the geared global minimum variance portfolio where, the weights of the GMV portfolio sum to one, but is now multiplied by the gearing parameter . The second term is a portfolio whose weights sum to zero555., but it is leveraged by risk aversion and then projected onto the global minimum risk portfolio. The risky portfolio is independent of the gearing parameter .

We can contrast Equation (34) with Equation (24); and then set to find that for the risk minimisation. We see that with we have recovered the Global Minimum Variance (GMV) portfolio ; as in Equation (35) when we let the risk aversion become sufficiently large. Both portfolio optimisations have the same minimum variance portfolio, as expected following from a two fund separation, and the minimum variance portfolio are combined with a risky portfolio. This is contrasted with the unconstrained optimisations given in Table (1) which are all leveraged versions of the optimal risky portfolio .

Finally, we have that from Equation (34) that the optimal portfolio is not generally aligned with and hence we cannot explain the lower bound deviation from alignment with being due to the condition number. However, we can show that there is a weakened condition number lower bound. Equation (33) can be written in the form of

| (36) |

where is the same dimension as . By Theorem 2, as for the risk minimisation with a gearing constraint in Equation (24), we again know that the angle between this portfolio and the alpha portfolio has a lower bound dependent on the condition number of the estimated covariance matrix. It is still advantageous to tilt the gearing constrained optimal risky portfolio within the overall optimal portfolio towards alpha by improving the conditioning of the covariance matrix, while maintaining the constraint. However, in this instance the gearing can saturate any information advantage as the gearing can drag the portfolio away from the direction of alpha towards the global minimum variance portfolio, even if in the risky portfolio, the angle can be reduced by improving the conditioning.

3.3 Comparing Efficient Frontiers

The efficient frontiers for the different optimisations are shown in Figure 3. Optimisations I, II, III and VI from Table 1 are shown in Figure 3(a). These are implicitly geared versions of the fully invested optimal risky portfolio and hence generate a straight line in the space that can be identified as the Capital Market Line (CML) associated with a 0% risk-free rate. The fully invested version of optimisations VI and VII from Table 2 are shown along with the GMV portfolio. Figure 3(b) depicts a stylised version of optimisations V, VI, VII and VIII from Table 2. Optimisations V and VIII generate the Capital Market surface (the grey plane) which intersects the solutions to optimisations VI and VII (the green curved surface) along the line representing the family of geared optimal risky portfolios (the red line). The family of geared global minimum risk portfolios is also shown (the blue line). The figures were plotted using the expected mean and covariance computed from 10 years (2006-2016) of monthly sampled Johannesburg Stock Exchange equity sector index data. The figures are indicative and aim to recover the well known general geometry of the fully invested portfolio optimisation Pareto surfaces. Figure 3(a) is the slice at from the surface shown in Figure 3.

| Gearing Constrained Portfolio Choice | ||

|---|---|---|

| # | Optimisation | Constraints |

| V | ||

| VI | ||

| . | ||

| VII | ||

| VIII | ||

3.4 Geometric interpretation

The key geometric insight of [19] is to consider the expected portfolio return:

| (37) |

and to split this into a direction and magnitude, to then ameliorate the impact of poor covariance conditioning by constraining the angle . Here the investment “direction” is given by the unit vector associated with the optimal portfolio weight in the portfolio weight space – which will be some simplex. This is visualised in Figure 1 for the optimisations I, II, III, IV, V and VIII. The gearing constrained optimisations are visualised in Figure (2). The investment “magnitude” is given by the .

Equation (37) can be re-written using either of the portfolio solutions: (24) or (34). Both are of the form: for some weight :

| (38) |

This has two angles, the first between alpha and the global minimum variance portfolio, some angle , and the second between the optimal risk portfolio and alpha, . From Equation (38) the -angle can be decomposed into these two angles:

| (39) |

If we improved the conditioning of the covariance we would be able to reduce the lower bound on the second angle , the angle between the optimal risky portfolio and alpha. This would in turn reduce the overall angle between the optimal portfolio and the direction of alpha. However, improving the conditioning of the covariance matrix does not mean the will lead to the overall portfolio being closer to alpha. It may well drag the optimal portfolio away from the expected alpha because it could move the minimum variance portfolio away from the expected returns more. This suggests that one should really be minimising i.e. minimise the angle between the optimal risky portfolio and alpha, rather than the alpha angle itself.

However, from the first order conditions, :

| (40) |

We know that from Equation (39) that minimising with respect to the angle is equivalent to minimising with respect to because we can integrate Equation 40 to find for some well behaved function and .

It is sufficient to minimise the overall -angle even in the presence of the gearing constraint. So if we minimise the -angle we would have minimised , the angle between the optimal risky portfolio and the direction of the expected returns, .

3.5 Long-term equilibrium

In the method of Black and Litterman [7] a long-term equilibrium view is introduced in order to create a tension between the noisy short-term views, (views that are pushing the portfolio away from some longer term market equilibrium), and long-term views , which are views that encode some sort of equilibrium portfolio :

| (41) |

In practice many fund managers have at least two sets of expected returns. First, explicit views associated with their asset views, and second a set of implicit views associated with the funding liabilities of a particular fund, or the some sort of long term objective of the fund. Here we will encode these in the equilibrium view in the spirit of [7]. If we are expected to hold a particular long-term portfolio we can invert equation 41 to solve for the implied long-term equilibrium views . This is unconstrained, in general the inversion should include the funds long-term constraints, for example a gearing constraint.

From equation 24 and 34 we have an optimal portfolio of the form for some weight . The second term is a cash neutral portfolio where we have already seen that this can be re-written in terms of the pair-wise differences of alpha: suggesting that we could modify the view to include following [35] and replace with and then factoring out a tactical component that is a function of both and , and a strategic component that is only a function of long-term views . The combination of this strategic component and the global minimum risk portfolio can then be treated as the benchmark portfolio of some tactical fund. The tactical fund would be taking pair-wise bets of relative short-term and long-term views as tracking error constrained with respect to this benchmark.

This is convenient because we can invert optimise the factored strategic component to find the implied equilibrium expected return views and then use those in the tactical component. This would allow one to naturally include the additional tension between the long-term and the short-term within the -angle framework. We do not pursue this any further here.

4 Robust portfolio optimisations

Following the method of Golts and Jones [19] there are two key issues. First, the improvement of the condition number of the covariance. Second, that of constraining the -weighted angle to ameliorate the error maximisation effect under the inversion of the covariance matrix. Here we want to ameliorate the impact of poor conditioning without compromising the gearing constraint666Theorems 1 and 2 show that aligning with the direction of returns ameliorates estimation error effects under a risk-return optimisation for unconstrained and linearly constrained optimisations, respectively..

4.1 Constraining the -angle

Golts and Jones [19] argue that the mean-variance optimisations can be made robust by constraining the -angle. They considered an uncertainty region as a ball centred on with radius:

| (42) |

This is some 1- neighbourhood. The expected portfolio return in this neighbourhood is: , and the expected return of the optimal risky portfolio in the same neighbourhood is: . In the unconstrained cases given in Table 1 the robust expected returns of the optimal risky portfolios

| (43) |

are equivalent to the robust expected returns of the those of the optimal portfolio [19]:

| (44) |

Here . This is not in general the case in the presence of the gearing constraint, in particular for optimisations VI and VII in Table 2, because and hence .

Our objective is to minimise the angle between the optimal risky portfolio and the expected return in the case of the gearing constraint in order to ameliorate the impact of poor conditioning of the covariance, however, this is equivalent to minimising the overall angle between the optimal portfolio and the expected returns (see equation 39). This implies that from expected portfolio return Equation (37) we can minimise this over the -weight angle :

| (45) |

The optimizations now include the expected returns but with a regularisation term.

In practice this can be achieved by minimising the angle between the optimal risky portfolio and the expected returns by shrinking the covariance matrix because the difference in the direction of the optimal risky portfolio and alpha is entirely due to the covariance : . Hence we try find some new covariance that will approximate the required -angle minimisation.

The reformulated portfolio optimizations are then as in Table (3). What is important to realise is that the less one trusts the expected asset returns the larger we make the regularisation hyper-parameter . This ensures that the less certain we are about the asset returns, the closer to the expect returns the risky portfolio will be, and in turn the closer our portfolio will be – this ensure that we do not excessively leverage the errors in the expected asset returns. The key difference in the presence of the constraint is that we will mix in the equally weighted portfolio so that the overall optimal portfolio is not always aligned with the optimal risky portfolio.

| -angle Robust Portfolio Choice | |||

|---|---|---|---|

| # | Optimisation | Constraints | |

| I, V | |||

| II | |||

| III | |||

| IV,VIII | |||

| VI | |||

| VII | |||

4.2 Shrinking with the -angle

Estimating covariance matrices of stock returns has always been a problematic area. The sample covariance unfortunately creates a well documented problem, where if the number of stocks under consideration are large, particularly relative to the number of observations, the sample covariance matrix contains a lot of error [29]. The most extreme coefficients in the matrix tend to take on extreme values not because they are correct, but because they contain an extreme amount of error. This also implies that the condition number of covariance matrices tend to be large, and very sensitive to the input data. Covariance shrinkage can ameliorate this, as shown by Ledoit and Wolf [34].

Following Golts and Jones [19] one can consider a shrunk covariance for a portfolio with assets that can achieve a minimisation of the -angle. This is because the optimal risky portfolio . The optimal risky portfolio will align with the expected returns when the covariance matrix is diagonal. This suggest that we can define a new regularised covariance matrix (see H):

| (46) |

Here is the identity matrix, the original (mis)-estimated covariance matrix, and can be understood as some quantity for some targeted optimal angle between the optimal risky portfolio and the expected returns. If we substitute the new covariance into the solution for the Sharpe ratio optimisation (see equation 107) we then have that:

| (47) |

We can eliminated the direct dependency on the optimal portfolio returns and risk using equations (107) and (108) and set the optimal risky portfolio to be fully invested () for and :

| (48) |

When the hyper-parameter tends to zero we recover the Sharpe ratio maximisation solution of the optimal portfolio for optimization IV (Table 1) as equivalently in Equation (107) for optimization VIII. This construction is valid for optimisations I, II, III, VI, V and VIII as these are all scalar multiples of the Sharpe ratio maximisation optimal risky portfolio: . When or the direction of the optimal risky portfolio aligns with the direction of the expected returns and the optimal risky portfolio is just the unit vector in the direction of the returns: . Any of the unconstrained optimal portfolio solutions in Table 1 can be modified in this way using an appropriate chosen covariance that would shrink the covariance towards the identity matrix so that the portfolio can be shifted between the original solution and a regularised one.

More generally the idea is to find the regularised optimal risky portfolio by finding a regularised covariance given a prudent choice of from Equation (46) with . We then compute a new global minimum variance portfolio ; using this and the optimal risky portfolio we can find the regularised gearing constrained optimal portfolio solutions.

The new efficient frontier is then generated exploiting the two fund separation theorems using the solutions given in Table 2. This ensures that we have retained consistency with the constraints, while minimising the -angle as in Equation (45). In practice we can simply implement this using: for .

Optimisations VI and VII are combinations of the GMV portfolio and the optimal risky portfolio. Although the shrinkage construction from Equation (46) is still valid, the overall portfolio is built up of the combination of two portfolios: one with direction , and the other with the direction of .

Again, when one is less certain about the asset returns then the regularisation parameter is chosen to be larger. The choice of any hyper-parameter such as the regularisation parameter requires some sort of cross-validation. Hence in practice it should be expected that one would need to engage in simulation work to best decided on the value of k in a way that was not overly prone to backtest over-fitting [3].

In the presence of the gearing constraint, the greater , the more exposed we are to the portfolio factored from the GMV portfolio. This is because when increase to some appropriately chosen we will shrink the covariance towards the identity matrix . This will shrink the GMV portfolio towards the equally weighted portfolio given by a unit vector :

| (49) |

Here , where . The risky portfolio becomes the weighted average of the expected returns which is just the unit vector in the direction of alpha:

| (50) |

Here and for the average alpha . The combination of the GMV portfolio, , and the optimal risky portfolio, , is controlled by the amount of gearing , as seen in equations (24) and (34). The combination remains cash neutral: .

For the gearing constrained mean-variance optimisation given by Equation (34) and using covariance shrinkage towards the identity matrix will have and to find from Equation (35):

| (51) |

The average expected return is: and this can be used to find:

| (52) |

We can confirm this by checking that the last term correctly sums to zero when multiplied by . From the unit vector in the direction of alpha777: where and using this we can write Equation (52) as:

| (53) |

This is geometrically intuitive because we see that when the alpha direction aligns with the equally weighted portfolio then our best case optimal portfolio is just the geared GMV and independent of alpha because of the constraint.

For the case of the risk minimisation the alpha standard deviation will be required: . From Equation (24) again with , , and . We can identify with the alpha variance: . For optimization VII:

| (54) |

Here the weight is: . Putting this all together we find that the maximally shrunk optimal risk minimisation with gearing constraint is:

| (55) |

This can then be written as:

| (56) |

From the definition of the average expected returns:

| (57) |

When the alpha aligns with the equally weighted portfolio we find the best case portfolio is once again the geared equally weighted portfolio: . When the alpha is orthogonal to the equally weight portfolio we again find some combination.

In the unconstrained optimisation, for any of the solutions in Table 1, the risky portfolio is shrunk towards the asset views 888The asset views can be written as a conditional expectation with regards to forecasts i.e. , for forecasts , historic asset (or equilibrium) returns , and forecast ability as an information co-efficient, IC [1, 40]. We do not pursue this any further here. this is not longer the case in the presence of gearing. There will be a combination of an equally weighted portfolio and . However, the gearing contributions can be conveniently factored out and treated separately relative to the unconstrained solution.

5 Conclusions

The lower bound of the -weight angle was introduced by Golts and Jones [19]. Here we show how this result arises as a result of the Kantorovich inequality 1. Despite being framed in the mean-variance setting the -angle approach to covariance shrinkage makes no distributional assumptions about the data generating processes. Golts and Jones [19] only considered unconstrained optimisation problems when demonstrating the relationship between the alpha-weight angle and the condition of the covariance matrix; as in optimisations I, II, III and IV in Table 1). Here we show this result can be weakened and generalised when gearing constraints are added; as in the optimisations V, VI, VII and VIII in Table 2 using the extension of Bauer and Householder given by Theorem 2.

When looking at the results of various forms of mean variance optimisation problems, we note that results of the unconstrained optimisations: I,II, III and IV in Table 1, can simply be thought of as portfolios combined with a risk-less portfolio and hence generate Pareto surfaces equivalent to the Capital Market Line with a risk fee rate set to 0%. Interestingly, these optimisations (I, II, III and IV) all have implicit gearing, as imposed by the choice of , and , despite that there is no outright, or explicit gearing constraint.

We see that optimisation V is equivalent to I because the choice off gearing, , is essentially equivalent to a choice of portfolio risk, . Optimisations I,II,III,IV as well as gearing constrained optimisations V and VIII, all have the same investment directions; in the direction of the optimal risky portfolio (i.e. they are all geared versions of the optimal risky portfolio). The optimal risky portfolio is always fully invested, and gearing can subsequently be applied, which will make the portfolio move up the Capital Market Line and be the tangent portfolio for the efficient frontier where that level of gearing is a constraint.

It is the fact that these solutions are in the direction of the optimal risk portfolio that makes the the Kantorovich inequality (Theorem 1) appropriate for proving the upper bound of the -weight angle (using the lower bound of the cosine of this angle). From a geometric perspective there is no tension between the gearing and the direction in these cases, and there is only a tension between the poor conditioning of the covariance matrix and the direction of . This insight lead to the idea of directly minimising the -angle by shrinking the covariance because for these optimisations this direction is generated by the covariance matrix: i.e. by the vector . This is not equivalent to including a return maximisation constraint.

However, When adding an explicit gearing restriction to certain problems, such as solutions VI and VII, we can see gearing can actually mimic poor conditioning and that the portfolios have investment directions different from those optimisations without a gearing constraint. From the two fund separation theorems the resulting optimal portfolio is a weighted average of the global minimum variance portfolio and the optimal risky portfolio. We see that naively applying gearing to any optimisation other than optimisation IV (the Sharpe optimal portfolio that generates the optimal risky portfolio) and VIII (the return maximisation) will drag the portfolios out of alignment with towards the global minimum variance portfolio.

Using fund separation theorems the global minimum variance portfolio can be factored from the optimal portfolio (24). Geometrically there is now a tension between the gearing, the alpha direction, and the impact of poor conditioning. However, the global minimum variance portfolio is shown to be purely a function of the covariance matrix, and is a fully invested portfolio that sums to one; it’s gearing can be managed separately from the minimisation of the -angle. This key insight allows us to retain the idea of minimising the -angle.

The gearing constrained optimal portfolio has a weakened lower bound that is now given by Theorem 2 Bauer and Householder [4], and not Theorem 1 because of the impact of the constraint. With improved conditioning of the covariance matrix we see we are still able to reduce the lower bound on the the angle between the optimal risky portfolio and , which would in turn reduce the overall angle between the optimal portfolio and the direction of . In fact, we note for the constrained optimisation from equation (24) that a minimisation over the total -angle is equivalent to minimising the angle between the optimal risky portfolio and the direction of expected returns (equation (39)). This extends the unconstrained result and motivates why the combination of an -angle minimisation is equally useful both in the unconstrained and constrained cases. To minimise the overall angle between the optimal portfolio and the expected returns, equation (44), we can minimise the angle between the optimal risky portfolio and the expected returns, equation (43).

Lastly, we again look at the spherical uncertainty region model for , and used it to motivate a simple robust optimisation framework. This motivates the use of covariance matrix shrinkage that explicitly reduces the angle between optimal risky Sharpe ratio portfolio, the optimal risky portfolio, and the direction of expected returns; this is given in equation (46).

By regularising the covariance matrix using equation (46) we constrain the direction of the optimal risk portfolio and achieve an overall -angle minimisation regularisation. This is consistent with reducing the impact of the estimation uncertainty as expressed by the lower bound in equation (16) from Theorem 2.

It is interesting to note that practically, if one is extremely uncertain about the covariance between the assets and uncertain about the returns, but one has a gearing constraint then one should be holding Equation (57) where the broad direction of expected returns is still of value. If one has a sense for the relative variances of asset then instead of the covariance matrix in equation (46), one could use the diagonal covariance matrix with zero off-diagonals.

Acknowledgements

We thank Dave Bradfield for thoughtful discussions and for inspiring us to work on the geometric perspective.

References

- Allen et al. [2019] Allen, D., Lizieri, C., Satchell, S., 2019. ”in defense of portfolio optimization: What if we can forecast?”. Financial Analysts Journal 75:3, 20–38. doi:DOI:10.1080/0015198X.2019.1600958.

- Axelsson [1996] Axelsson, O., 1996. Iterative Solution Methods. Cambridge Univ. Press.

- Bailey et al. [2015] Bailey, D., Borwein, J., de Prado, M.L., Zhu, Q.J., 2015. The probability of backtest overfitting. Journal of Computational Finance (Risk Journals) URL: https://ssrn.com/abstract=2326253, doi:10.2139/ssrn.2326253.

- Bauer and Householder [1960] Bauer, F., Householder, A., 1960. Some inequalities involving the euclidean condition of a matrix. Numer. Math. 2, 308–311. doi:10.1007/BF01386231.

- Bengtsson and Holst [2002] Bengtsson, Holst, 2002. On portfolio selection: Improved covariance matrix estimation for swedish asset returns. Unpublished Manuscript, Department of Economics, Lund University .

- Best and Grauer [1991] Best, M.J., Grauer, R.R., 1991. On the sensitivity of mean-variance efficient portfolios to changes in asset means: Some analytical and computational results. The Review of Financial Studies 4, 315–342.

- Black and Litterman [1992] Black, F., Litterman, R., 1992. Global portfolio optimization. Financial Analysts Journal 48, 28–43.

- Broadie [1993] Broadie, M., 1993. Computing efficient frontiers using estimated parameters. Annals of Operations Research 45, 21–58.

- Brown [1976] Brown, S., 1976. Optimal portfolio choice under uncertainty: A bayesian approach. Phd Dissertation, Univeristy of Chicagol .

- [10] Cavadini, H., Sbuelz, A., Trojani, F., . A simplified way of incorporating model risk, estimation risk, and robustness in mean variance portfolio management. Technical Report, University of Southern Switzerland .

- Ceria and Stubbs [2003] Ceria, S., Stubbs, R.A., 2003. Incorporating estimation errors into portfolio selection: robust portfolio construction. URL: www.axiomainc.com.

- Chopra and Ziemba [1993] Chopra, V., Ziemba, W., 1993. The effect of errors in means, variances, and covariances on optimal portfolio choice. Journal of Portfolio Management Winter, 19, 2, 6–11.

- Clarke et al. [2006] Clarke, R.G., de Silva, H., Thorley, S., 2006. Minimum-variance portfolios in the u.s. equity market. Journal of Portfolio Management 33, 10–24. doi:10.3905/jpm.2006.661366.

- Costa and Paiva [2002] Costa, O.L.V., Paiva, A.C., 2002. Robust portfolio selection using linear-matrix inequalities. Journal of Economic Dynamics and Control 26, 889–909.

- Disatnik and Benninga [2007] Disatnik, Benninga, 2007. Shrinking the covariance matrix. Journal of Portfolio Management 33, 55–63.

- Frankfurter et al. [1971] Frankfurter, G., Phillips, H., Seagle, J., 1971. Portfolio selection: The effect of uncertain means, variances and covariances. Journal of Financial and Quantitative Analysis , 1251–1262.

- Galluccio et al. [1998] Galluccio, S., Bouchaud, J.P., Potters, M., 1998. Rational decisions, random matrices and spin glasses. Physica A: Statistical Mechanics and its Applications 259, 449–456. URL: https://www.sciencedirect.com/science/article/pii/S037843719800332X, doi:10.1016/S0378-4371(98)00332-X.

- Goldfarb and Iyengar [2003] Goldfarb, D., Iyengar, G., 2003. Robust portfolio selection problems. Mathematics of operations research 28, 1–38.

- Golts and Jones [2009] Golts, M., Jones, G.C., 2009. A sharper angle on optimization. URL: http://ssrn.com/abstract=1483412.

- Gábor and Kondor [1999] Gábor, A., Kondor, I., 1999. Portfolios with nonlinear constraints and spin glasses. Physica A: Statistical Mechanics and its Applications 274, 222–228. URL: https://www.sciencedirect.com/science/article/pii/S0378437199003878, doi:10.1016/S0378-4371(99)00387-8.

- Halldorsson and Tutuncu [2003] Halldorsson, B.V., Tutuncu, R.H., 2003. An interior-point method for a class of saddle-point problems. Journal of Optimization Theory and Applications 116, 559 to 590.

- Horn and Johnson [1985a] Horn, Johnson, 1985a. Matrix Analysis. Cambridge University Press, London.

- Horn and Johnson [1985b] Horn, R.A., Johnson, C.R., 1985b. Matrix analysis. Cambridge University Press, London .

- Householder [1965] Householder, A., 1965. The kantorovich and some related inequalities. SIAM Review 7, 463–473. URL: RetrievedJune23,2021,fromhttp://www.jstor.org/stable/2027767, doi:10.1137/1007104.

- Householder [1964] Householder, A.S., 1964. The theory of matrices in numerical analysis. Blaisdell, New York .

- Huang and Zhou [2005] Huang, J., Zhou, J., 2005. A direct proof and a generalization for a kantorovich type inequality. Linear Algebra and its Applications 394, 185–192.

- Ingersoll [1987] Ingersoll, J.E., 1987. Theory of Financial Decision Making. Rowman and Littlefield Publishers, Lanham.

- Jagannathan and Ma [2003] Jagannathan, Ma, 2003. Risk reduction in large portfolios: Why imposing the wrong constraints helps. The Journal of Finance 58, 1651–1683.

- Jobson and Korkie [1980] Jobson, J., Korkie, B., 1980. Estimation for markowitz efficient portfolios. Journal of the American Statistical Association , 544–554.

- Jobson and Korkie [1981] Jobson, J., Korkie, B., 1981. Performance hypothesis testing with the sharpe and treynor measures. Journal of Finance 36, 889–908.

- Jorion [1985] Jorion, P., 1985. International portfolio diversification with estimation risk. Journal of Business 58, 259–278.

- Kan and Zhou [2007] Kan, R., Zhou, G., 2007. Optimal portfolio choice with parameter uncertainty. Journal of Financial and Quantitative Analysis 42, 621–656.

- Lai et al. [2011] Lai, T.L., Xing, H., Chen, Z., 2011. Mean-variance portfolio optimization when means and covariances are unknown. The Annals of Applied Statistics 5, 798–823. URL: http://www.jstor.org/stable/23024906.

- Ledoit and Wolf [2003] Ledoit, Wolf, 2003. Honey, i shrunk the sample covariance matrix. Journal of Portfolio Management 30, 110–119. doi:10.3905/jpm.2004.110.

- Lee [2000] Lee, W., 2000. Theory and methodology of tactical asset allocation. volume 65. John Wiley & Sons.

- Markowitz [1952] Markowitz, H., 1952. Portfolio selection. The Journal of Finance , 77–91.

- Merton [1972] Merton, R.C., 1972. An analytic derivation of the efficient portfolio frontier. Journal of financial and quantitative analysis 7(4), 1851–1872.

- [38] Michaud, R., . Efficient asset management: A practical guide to stock portfolio optimization and asset allocation. Harvard Business School Press, Boston, MA .

- Michaud [1989] Michaud, R.O., 1989. The markowitz optimization enigma is optimized optimal. Financial Analysts Journal 45, 31–42.

- Michaud et al. [2020] Michaud, R.O., Esch, D.N., Michaud, R.O., 2020. ”in defense of portfolio optimization: What if we can forecast?”: A comment. Financial Analysts Journal 76:2, 104–105. doi:DOI:10.1080/0015198X.2019.1701323.

- Scherer [2002] Scherer, B., 2002. Portfolio resampling: Review and critique. Financial Analysts Journal 58, 98–109. doi:10.2469/faj.v58.n6.2489.

- Tutuncu and Koenig [2004] Tutuncu, R.H., Koenig, M., 2004. Robust asset allocation. Annals of Operations Research 132, 157–187.

- Tuy and Hoai-Phuong [2007] Tuy, H., Hoai-Phuong, N., 2007. A robust algorithm for quadratic optimization under quadratic constraints. Journal of Global Optimization 37, 557–569. doi:10.1007/s10898-006-9063-7.

- Zimmermann and Nierdermayer [2007] Zimmermann, H., Nierdermayer, D., 2007. Robust portfolio optimization. URL: http://daniel.niedermayer.ch/uploads/File/papers/RobOptPresentation_niederma_basel.pdf.

Appendix A Minimax degeneracy

The alpha-weight angle can be estimated from the spectral properties of the covariance matrix :

| (58) |

where is an orthogonal matrix and are the eigenvalues of in decreasing order. The rows of , denoted by are the eigenvectors of .

When the mean variance optimisation problem is unconstrained, then the direction of the optimised weights vector in a mean variance optimisation procedure can be given by ; from Equation (11) the quantity is bounded from below:

| (59) |

We refer to the lower bound as the minimax degeneracy number of the matrix . This presents the best case angle that can be achieved when attempting to align the direction of the optimal risky portfolio with that of the direction of expected returns. Equality is achieved in equation (59) when:

| (60) |

This is visualised in Figure 5. This best case angle of alignment can be seen to be problematic as the portfolio is largely invested along the lowest volatility principal component .

Similarly, when the mean variance optimisation problem is constrained, in particular when we get solutions VI and VII in Table 2 where the direction of the optimal portfolio weight vector is given by so that from Equation (16):

| (61) |

Here is and smaller than the angle and

| (62) |

By setting we can calculate that the best case angle for alignment with the expected returns from equality with the lower bound, which is achieved when:

| (63) |

Again this is problematic. However, a key nuance is that optimal portfolio lower bound in gearing constrained optimisations, optimisations VI and VII, is given by Equation (63) from Theorem 2, but the key lower bound for the optimal risky portfolio remains that given in Equation (60) and governed by Theorem 1.

Appendix B Two-fund Separation

The two fund separation theorem derived by Markowitz [36] states that: i.) the optimal portfolio exists, ii.) it is unique for any given return expectation level , and iii.) it can be separated into two distinct portfolios and from which all optimal portfolios can be generated:

| (64) |

This is can proved by first considering two new optimal portfolios and . Then let be another optimal portfolio such that for a real number .

Now , because they are distinct portfolios. So, there exists an unique solution to the equation:

| (65) |

Consider another portfolio with weights which has invested in portfolio’s and , it will satisfy:

| (66) |

so that .Therefore, ; and the optimal portfolio is unique and exists. Further details relating to fund separation theorems can be seen in Ingersoll [27].

All investors who choose portfolios by examining only mean and variance can be satisfied by holding different combinations of only a few (in this case 2) portfolios regardless of their preferences. All of the original assets, therefore, can be purchased by just two portfolios, and the investors can then just buy them in various ratios.

Appendix C Maximum return portfolio

To find an investment portfolio with maximum return at a given level of portfolio variance with a gearing constraint we want to solve:

| (67) |

which can be reduced to the following Lagrangian with two Lagrange multipliers but with a quadratic constraint and a linear constraint:

| (68) |

It should be expected here that picking a gearing necessarily fixes the variance of the portfolio. However there are multiple portfolios with the different portfolio variances, but the same leverage. We would like the minimum variance portfolio at a particular gearing . This is then a multi-objective function optimisation. Hence we rather find the targeted variance first, and then set that variance to provide a portfolio with the required leverage.

Here we want to ensure that there is an upper bound on portfolio risk: and we know that a choice of will set the portfolio gearing. Hence we rather solve the well known reduced problem with a single Lagrange multiplier and then fix the leverage:

| (69) |

From the first order conditions

| (70) | |||||

| (71) |

From the second order conditions:

| (72) |

Multiplying equations (70) by and by to find:

| (73) | |||||

| (74) |

We factor the optimal portfolio out of Equation (74):

| (75) |

We now make use of the following substitutions

| (76) | ||||

| (77) | ||||

| (78) | ||||

| (79) |

Here is positive, by the Cauchy-Schwarz inequality, since we have assumed that is non-singular and all assets do not have the same mean: . If all means were the same, then , and this problem has no solution.

Multiply (74) from the left by to find:

| (80) |

To find we now substitute the portfolio expected returns and risk into (73) to find and then substitute into (80) to find:

| (81) |

Which gives the solution to optimisation I in Table 1 when substituted into Equation (75):

| (82) |

To set the gearing we multiply (82) from the left by to find that

| (83) |

The solution to optimisation V in Table 1 in terms of gearing is:

| (84) |

This is just a gearing optimal risky portfolio. For this reason optimisations I and V are treated as equivalent as they have the same investment directions. The ratio is just the ratio of the variance of optimal risky portfolio to the variance of global minimum variance portfolio.

Appendix D Minimum risk portfolio

We want to find an investment portfolio with minimum variance and a targeted return with the additional gearing constraint, hence we want to solve for:

| (85) |

which can be reduced to the following Lagrangian with two Lagrange multipliers :

| (86) |

From the Kuhn-Tucker conditions

| (87) | ||||

| (88) |

Solving for in terms of from 87

| (89) |

We now solve for by multiplying (89) first by and then by and then substituting these into Equation 88:

| (90) | |||

| (91) |

We again make use of the following substitutions from equations (76),(77),(78) and (79). Using these we simplify equations 90 and 91 to:

| (92) | |||

| (93) |

From 93 above, we can see that

| (94) |

And by substituting 94 above into 92

| (95) |

Solving for :

| (96) |

Substituting 96 into 94 we then solve for :

| (97) |

Finally, from 96 and 97 as substituted into 89 we find

| (98) |

We can then put this into the form , where is the same dimension as :

This can be reduced further to find the global minimum risk portfolio associated with a particular value of the gearing parameter , this allows us to define a second efficient frontier, as a function of , by eliminating by enforcing that (see Section 3.1). We are effectively putting a lower bound on the portfolio returns by associating this with the unleveraged global minimum variance portfolio.

Appendix E Mean-variance portfolio

The gearing constrained mean-variance optimal portfolio choice problem is given by the optimisation:

| (99) |

It has a Lagrangian with a single Lagrange multiplier:

| (100) |

Solving the first order optimality conditions (the Kuhn-Tucker equations) we find:

| (101) | ||||

| (102) |

Using Equation (101) to solve for the optimal control and then substituting this into Equation (102) to eliminate the Lagrange multiplier, to then find the optimal portfolio:

Appendix F Optimal risky portfolio

To find an investment portfolio that maximises the Sharpe ratio but with a gearing constraint and setting the risk free rate to zero; we want to solve:

| (103) |

This can be reduced to a Lagrangian with a single Lagrange multiplier:

| (104) |

From the first order conditions

| (105) | ||||

| (106) |

We can multiply Equation (105) by and using Equation (106) we find that the Lagrange multiplier: and hence that for .

Using this and multiplying Equation (105) from the left by we can show that:

| (107) |

This is convenient because we can now multiply this from the left by the transposed unit vector and use Equation (106), to find that:

| (108) |

Substituting this into Equation (107) this gives the optimal leveraged risk adjusted portfolio:

| (109) |

We note that optimisation I, II, III and IV are all special cases of general leverage Sharpe ratio optimisation in problem VIII – they are all geared optimal risky portfolios.

Appendix G Portfolio diversity constraint

The problem of finding a portfolio constrained to a given number of effective bets [17, 20] requires a quadratic constraint, and this constraint can been seen to act as a regularisation condition. Such an investment portfolio with minimum variance, gearing constrained, but with a quadratic constraints is the following problem:

This is a special case of the problem of Quadratic Optimisation with Quadratic Constraint (QOQC) [43]. Here the Lagrangian has two Lagrange multipliers :

| (110) |

The first order conditions are:

| (111) | ||||

| (112) |

By multiplying Equation 111 by and using the constraints 112 we find that: .

The second order constraint gives a convexity condition:

| (113) |

Solving for in terms of from equations 111 and 112 where for the identity matrix we find:

| (114) |

This is no longer of the form for some vector but we can make the substitution (c.f. Equation 46):

| (115) |

to get the solution into a regularised form . The regularised covariance matrix is still positive semi-definite and hence it can still be factorised into two symmetric matrices; Theorem 2 then remains valid with regards to the condition number of new covariance matrix . So the -angle is still bound below by the condition number. Hence improving the conditioning by aligning the resulting optimal portfolio with the expected returns makes sense.

Appendix H -angle minimising covariance

Following [19] one can consider a shrunk covariance for a portfolio with assets. For example, we can consider the Sharpe ratio maximization solution, optimization IV in Table 1), but with a new covariance that satisfies:

| (116) |

where . Here is the original estimated covariance matrix, is the identity matrix, and , and are as before. From equation (44) into equation (116):

| (117) |

The first term is the Sharpe ratio optimal portfolio where the direction of the expected returns aligns with that of the optimal portfolio, the second term is that from the robust return optimisation and is as a function of the same .

The thinking behind this choice is as follows: if tends to zero, from equation(117), we recover the usual Sharpe optimal portfolio using equations (107) and (108) with :

| (118) |

If the estimated covariance tends to towards the identity matrix we again recover the standard solution for the Sharpe optimal portfolio but where the portfolio is now the unit vector in the direction of the expected returns, this is because the first and last terms will then cancel:

| (119) |

Here the direction of the risky portfolio aligns with that of the expected returns. Using that equation (117) becomes:

| (120) |

As tends towards the current -angle : and , we again recover the identity matrix and the optimal portfolio aligns with the direction of the expected returns:

| (121) |