Random Coordinate Langevin Monte Carlo

Abstract

Langevin Monte Carlo (LMC) is a popular Markov chain Monte Carlo sampling method. One drawback is that it requires the computation of the full gradient at each iteration, an expensive operation if the dimension of the problem is high. We propose a new sampling method: Random Coordinate LMC (RC-LMC). At each iteration, a single coordinate is randomly selected to be updated by a multiple of the partial derivative along this direction plus noise, and all other coordinates remain untouched. We investigate the total complexity of RC-LMC and compare it with the classical LMC for log-concave probability distributions. When the gradient of the log-density is Lipschitz, RC-LMC is less expensive than the classical LMC if the log-density is highly skewed for high dimensional problems, and when both the gradient and the Hessian of the log-density are Lipschitz, RC-LMC is always cheaper than the classical LMC, by a factor proportional to the square root of the problem dimension. In the latter case, our estimate of complexity is sharp with respect to the dimension.

1 Introduction

Monte Carlo sampling plays an important role in machine learning (Andrieu et al.,, 2003) and Bayesian statistics. In applications, the need for sampling is found in atmospheric science (Fabian,, 1981), epidemiology (Li et al.,, 2020), petroleum engineering (Nagarajan et al.,, 2007), in the form of data assimilation (Reich,, 2011), volume computation (Vempala,, 2010) and bandit optimization (Russo et al.,, 2018).

In many of these applications, the dimension of the problem is extremely high. For example, for weather prediction, one measures the current state temperature and moisture level, to infer the flow in the air, before running the Navier–Stokes equations into the near future (Evensen,, 2009). In a global numerical weather prediction model, the degrees of freedom in the air flow can be as high as . Another example is from epidemiology: When a disease is spreading, one measures the everyday new infection cases to infer the transmission rate in different regions. On a county-level modeling, one treats different counties in the US separately, and the parameter to be inferred has a dimension of at least (Li et al.,, 2020).

In this work, we focus on Monte Carlo sampling of log-concave probability distributions on , meaning the probability density can be written as where a is a convex function. The goal is to generate (approximately) i.i.d. samples according to the target probability distribution with density . Several sampling frameworks have been proposed in the literature, including importance sampling and sequential Monte Carlo (Geweke,, 1989; Neal,, 2001; Del Moral et al.,, 2006); ensemble methods (Reich,, 2011; Iglesias et al.,, 2013); Markov chain Monte Carlo (MCMC) (Roberts and Rosenthal,, 2004), including Metropolis-Hasting based MCMC (MH-MCMC) (Metropolis et al.,, 1953; Hastings,, 1970; Roberts and Tweedie,, 1996); Gibbs samplers (Geman and Geman,, 1984; Casella and George,, 1992); and Hamiltonian Monte Carlo (Neal,, 1993; Duane et al.,, 1987). Langevin Monte Carlo (LMC) (Rossky et al.,, 1978; Parisi,, 1981; Roberts and Tweedie,, 1996) is a popular MCMC method that has received intense attention in recent years due to progress in the non-asymptotic analysis of its convergence properties (Durmus and Moulines,, 2017; Dalalyan,, 2017; Dalalyan and Karagulyan,, 2019; Durmus et al.,, 2019).

Denoting by the location of the sample at -th iteration, LMC obtains the next location as follows:

| (1) |

where is the time stepsize, and is drawn i.i.d. from , where denotes identity matrix of size . LMC can be viewed as the Euler-Maruyama discretization of the following stochastic differential equation (SDE):

| (2) |

where is a -dimensional Brownian motion with independent components. It is well known that under mild conditions, the SDE converges exponentially fast to the target distribution (see e.g., (Markowich and Villani,, 1999)). Since (1) approximates the SDE (2) with an discretization error, the probability distribution of produced by LMC (1) converges exponentially to the target distribution up to a discretization error (Dalalyan and Karagulyan,, 2019).

A significant drawback of LMC is that its dependence on the problem dimension is rather poor. In each iteration, the full gradient needs to be evaluated. However, in most practical problems, since the analytical expression of the gradient is not available, each partial derivative component in the gradient needs to be computed separately, either through finite differencing or automatic differentiation, so that the total number of such evaluations can be as many as times the number of required iterations. In the weather prediction and epidemiology problems discussed above, stands for the map from the parameter space of measured quantities via the underlying partial differential equations (PDEs), and each dimensional partial derivative calls for one forward and one adjoint PDE solve. Thus, PDE solves are required in general at each iteration. Another example comes from the study of directed graphs with multiple nodes. Denote the nodes by and directed edges by , and suppose there is a scalar variable associated with each node. When the function has the form , the partial derivative of with respect to is given by

Note that the number of terms in the summations equals the number of edges that touch node , the expected value of which is about times the total number of edges in the graph. Meanwhile, evaluation of the full gradient would require evaluation of both partial derivatives of each for all edges in the graph. Hence, the cost difference between these two operations is a factor of order .

In this paper, we study how to modify the updating strategies of LMC to reduce the numerical cost, with the focus on reducing dependence on . In particular, we will develop and analyze a method called Random Coordinate Langevin Monte Carlo (RC-LMC). This idea is inspired by the random coordinate descent (RCD) algorithm from optimization (Nesterov,, 2012; Wright,, 2015). RCD is a version of Gradient Descent (GD) in which one coordinate (or a block of coordinates) is selected at random for updating along its negative gradient direction. In optimization, RCD can be significantly cheaper than GD, especially when the objective function is skewed and the dimensionality of the problem is high. In RC-LMC, we use the same basic strategy: At iteration , a single coordinate of is randomly selected for updating, while all others are left unchanged.

Although each iteration of RC-LMC is cheaper than conventional LMC, more iterations are required to achieve the target accuracy, and delicate analysis is required to obtain bounds on the total cost. Analagous to optimization, the savings of RC-LMC by comparison with LMC depends strongly on the structure of the dimensional Lipschitz constants. Under the assumption that there is a factor-of- difference in per-iteration costs, we conclude the following:

-

1.

(Theorem 4.2) When the gradient of is Lipschitz but the Hessian is not, RC-LMC costs for an -accurate solution, and it is cheaper than the classical LMC if is skewed and the dimension of the problem is high. The optimal numerical cost in this setting is achieved when the probability of choosing the -th direction is proportional to the -th directional Lipschitz constant.

-

2.

(Theorem 4.3) When both the gradient and the Hessian of are Lipschitz, RC-LMC requires iterations to achieve accuracy. On the other hand, the currently available result indicates that the classical LMC costs . Thus, RC-LMC saves a factor of at least .

-

3.

(Proposition 4.1) The complexity bound for RC-LMC is sharp when both the gradient and the Hessian of are Lipschitz.

The notation omits the possible log terms. We make three additional remarks. (a) Throughout the paper we assume that one element of the gradient is available at an expected cost of approximately of the cost of the full gradient evaluation. Although this property is intuitive, and often holds in many situations (such as the graph-based example presented above), it does not hold for all problems (Wright,, 2015). (b) Besides replacing gradient evaluation by coordinate algorithms, one might also improve the dimension dependence of LMC by utilizing a more rapidly convergent method for the underlying SDEs than (2). One such possibility is to use underdamped Langevin dynamics, see e.g., (Rossky et al.,, 1978; Dalalyan and Riou-Durand,, 2018; Cheng et al.,, 2018; Eberle et al.,, 2019; Shen and Lee,, 2019; Cao et al.,, 2019), which can also be combined with coordinate sampling. For the clarity of presentation, we will focus only on LMC in this work and leave the extension to underdampped samplers to a future work. (c) It is also possible to reduce the cost of full gradient evaluation using stochastic gradient (Welling and Teh,, 2011), but it requires a specific form of the objective function that is not considered in this work.

The paper is organized as follows. We present the RC-LMC algorithm in Section 2. Notations and assumptions on are listed in Section 3, where we also recall theoretical results for the classical LMC method. We present our main results regarding the numerical cost in Section 4 and numerical experiments in Section 5. Proofs of the main results are deferred to the Appendix.

2 Random Coordinate Langevin Monte Carlo

We introduce the Random Coordinate Langevin Monte Carlo (RC-LMC) method in this section. At each iteration, one coordinate is chosen at random and updated, while the other components of are unchanged. Specifically, denoting by the index of the random coordinate chosen at -th iteration, we obtain according to a single-coordinate version of (1) and set for .

The coordinate index can be chosen uniformly from ; but we will consider more general possibilities. Let be the probability of component being chosen, we denote the distribution from which is drawn by , where

| (3) |

The stepsize may depend on the choice of coordinate; we denote the stepsizes by and assume that they do not change across iterations. In this paper, we choose to be inversely dependent on probabilities , as follows:

| (4) |

where is a parameter that can be viewed as the expected stepsize. In Section 4.2-4.3, we will find the optimal form of under different scenarios. The initial iterate is drawn from a distribution , which can be any distribution that is easy to draw from (the normal distribution, for example). We present the complete method in Algorithm 1.

When we compare (5) with the classical LMC (1), we see that in the updating formula, the gradient is replaced by a partial derivative in a random direction :

where is the unit vector for -th direction. Define the elapsed time at -th iteration as

| (6) |

then for , the updating formula (5) can be viewed as the Euler approximation to the following SDE:

| (7) |

We note that the SDE preserves the invariant measure, that is, for any . We discuss further the convergence property of the SDE (7) in Section 4.1.

3 Notations, assumptions and classical results

We unify notations and assumptions in this section, and summarize and discuss the classical results on LMC. Throughout the paper, to quantify the distance between two probability distributions, we use the Wasserstein distance defined by

where is the set of distribution of whose marginal distributions, for and respectively, are and . The distributions in are called the couplings of and . Due to the use of power in the definition, this is sometimes called the Wasserstein- distance.

We assume that is strongly convex, so that is strongly log-concave. We obtain results under two different assumptions: First, Lipschitz continuity of the gradient of (Assumption 3.1) and second, Lipschitz continuity of the Hessian of (Assumption 3.2 together with Assumption 3.1).

Assumption 3.1.

The function is twice differentiable, is -strongly convex for some and its gradient is -Lipschitz. That is, for all , we have

| (8) |

and

| (9) |

It is an elementary consequence of (8) that

| (10) |

Since each coordinate direction plays a distinct role in RC-LMC, we distinguish the Lipschitz constants in each such direction. When Assumption 3.1 holds, partial derivatives in all coordinate directions are also Lipschitz. Denoting them as for each , we have

| (11) |

for any and any . We further denote and define condition numbers as follows:

| (12) |

As shown in (Wright,, 2015), we have

| (13) |

These assumptions together imply that the spectrum of the Hessian is bounded above and below for all , specifically, and for all .

Both upper and lower bounds of in term of in (13) are tight. If is a diagonal matrix, then , both being the biggest eigenvalue of . Thus, in this case. This is the case in which all coordinates are independent of each other, for example . On the other hand, if where satisfies for all , then and . This is a situation in which is highly skewed, that is, .

The next assumption concerns higher regularity for .

Assumption 3.2.

The function is three times differentiable and is H-Lipschitz, that is

| (14) |

When this assumption holds, we further define to satisfy

| (15) |

for any , all , and all , where is , the diagonal entry of the Hessian matrix .

We summarize existing results for the classical LMC in the following theorem.

This theorem yields stopping criteria for the number of iterations to achieve a user-defined accuracy of . When the gradient of is Lipschitz, to achieve -accuracy, we can require both terms on the right hand side of (16) to be smaller than , which occurs when

| (18) |

leading to a cost of evaluations of gradient components (when we assume that each full gradient can be obtained at the cost of individual components of the gradient). When both the gradient and the Hessian are Lipschitz, to achieve -accuracy, we require all three terms on the right hand side of (17) to be smaller than . Assuming and all other constants are , we thus obtain

| (19) |

which yields a cost of evaluations of gradient components. Here denotes for some absolute constant and .

4 Main results

We discuss the main results from two perspectives. In Section 4.1 we examine the convergence of the underlying SDE (7), laying the foundation for the convergence in the discrete setting. We then build upon this result and show the convergence of the RC-LMC algorithm in Section 4.2 and 4.3 under two different assumptions. We show in Section 4.4 that when both Assumption 3.1 and 3.2 are satisfied, our bound is tight with respect to and .

4.1 Convergence of the SDE (7)

To study the convergence of (7), we first let and denote the probability filtration by . Then is a Markov chain and the following theorem shows its geometric ergodicity.

Theorem 4.1.

Denote by the probability density function of . If satisfies Assumption 3.1 and , then is the density of the stationary distribution of the Markov chain . Furthermore, if the second moment of is finite and is drawn from , then there are constants and , independent of , such that for any we have

| (20) |

See proof in Appendix A. This theorem states that the solution to the SDE converges to the target distribution. Since the discrepancy between and decays exponentially in time on the continuous level, the discrete version (as computed in the algorithm) can be expected to converge as well. We will establish this fact in subsequent subsections.

4.2 Convergence of RC-LMC. Case 1: Lipschitz gradient

Theorem 4.2.

We make a few comments here: (1) the requirement on is rather weak. When both and are moderate (both constants), the requirement is essentially . (2) The estimate (21) consists of two terms. The first is an exponentially decaying term and the second comes from the variance of random coordinate selection. If we assume all Lipschitz constants are of , this remainder term is roughly . (3) The theorem suggests a stopping criterion: to have , we roughly need , and , assuming . In terms of and dependence, this puts at the same order as (18), as required by the classical LMC.

Theorem 4.2 holds for all choices of satisfying (3). From the explicit formula (21) we can choose to minimize the right-hand side of the bound. Nesterov, (2012) proposed distributions that depend on the dimensional Lipschitz constants , from (11). For , we can let , specifically,

| (22) |

Note that when , for all : the uniform distribution among all coordinates. When , the directions that with larger Lipschitz constants have higher probability to be chosen. Since , one uses smaller stepsizes for stiffer directions. (On the other hand, when , the directions with larger Lipschitz constants are less likely to be chosen, and the stepsizes are larger in stiffer directions, a situation that is not favorable and should be avoided.) The following corollary discusses various choices of and the corresponding computational cost.

Corollary 4.1.

See proof in Appendix B. We note that the initial error enters through a term and is essentially negligible. To compare RC-LMC with the classical LMC, we compare (23) with (18), adjusting (18) by a factor of to account for the higher cost per iteration. RC-LMC has more favorable computational cost if . Since , this is guaranteed if , which in turn is true when and , that is, for highly skewed in high dimensional space.

Our proof of Theorem 4.2 follows from a coupling approach similar to that used by Dalalyan and Karagulyan, (2019) for LMC. We emphasize that for the coordinate algorithm, we need to overcome the additional difficulty that the process of each coordinate is not contracting on the SDE (7) level. This is a different situation from the classical LMC (Dalalyan and Karagulyan,, 2019) whose corresponding SDE (2) already provides the contraction property and thus only the discretization error needs to be considered. Despite this, the algorithm RC-LMC still enjoys the contraction property that ensures that the distance between two different trajectories following the algorithm contract. However, this contraction property is not component-wise, so we need to choose Young’s constant wisely and take summation of every coordinate. The summation will also produce some extra terms, which we need to bound. Dalalyan and Karagulyan, (2019) obtains an estimate for the cost of the classical LMC of . Compared with this estimate, our estimate for the cost of RC-LMC is always cheaper (since ). The improved estimate of the cost of LMC (18) was obtained by Durmus et al., (2019) using a quite different approach based on optimal transportation. It is not clear whether their technique can be adapted to the coordinate setting to obtain an improved estimate.

4.3 Convergence of RC-LMC. Case 2: Lipschitz Hessian

We now assume that Assumption 3.1 and 3.2 hold, that is, both the gradient and the Hessian of are Lipschitz continuous. In this setting, we obtain the following improved convergence estimate. The proof can be found in Appendix C.

Theorem 4.3.

We see again two terms in the bound, an exponentially decaying term and a variance term. Assuming all Lipschitz constants are , the variance term is of . By comparing with Theorem 4.2, we see that error can be achieved with the looser stepsize requirement .

By choosing to optimize the bound in Theorem 4.3, we obtain the following corollary.

Corollary 4.2.

Under the same conditions as in Theorem 4.3, the optimal choice of is to set:

For this choice, the number of iterations required to guarantee satisfies

| (25) |

If , and are all constants of , then the total cost is regardless of the choice of .

This is a significant improvement compared to the cost of the classical LMC (which requires (Dalalyan and Riou-Durand,, 2018)), regardless of the structure of . Indeed, the cost is reduced by a factor of , which can be significant for high dimensional problems.

4.4 Tightness of the complexity bound

When both the gradient and the Hessian are Lipschitz, we claim that estimate obtained in Corollary 4.2 is tight. An example is presented in the following proposition.

Proposition 4.1.

Let for all , and set the initial distribution and the target distribution to be:

| (26) |

where satisfies for all . Let be the probability distribution of generated by Algorithm 1, and denote . Then we have

| (27) |

In particular, to have , one needs at least .

See proof in Appendix D.

5 Numerical results

We provide some numerical results in this section. Since it is extremely challenging to estimate the Wasserstein distance between two distributions in high dimensions, we demonstrate instead the convergence of estimated expectation for a given observable. Denoting by the list of samples, with each of them computed through Algorithm 1 independently with iterations, we define the error as follows:

| (28) |

where is a test function and is the expectation of under the target distribution . As and , we have , and can be regarded as approximately sampled from . Thus, according to the central limit theorem, we have .

In this example, we set the target and initial distributions to be Gaussian and with

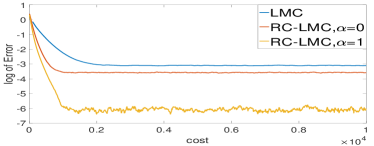

where , , is the identity matrix and is a random matrix with each entry i.i.d. drawn from . We run the simulation with , and we compute with . This measures the spectral norm of the covariance matrix of the first entries. As shown in Figure 1, RC-LMC with converges faster than RC-LMC with , and both converge faster than the classical LMC.

References

- Andrieu et al., (2003) Andrieu, C., Freitas, N., Doucet, A., and Jordan, M. (2003). An introduction to MCMC for Machine Learning. Machine Learning, 50:5–43.

- Cao et al., (2019) Cao, Y., Lu, J., and Wang, L. (2019). On explicit -convergence rate estimate for underdamped langevin dynamics. arXiv preprint arXiv:1908.04746.

- Casella and George, (1992) Casella, G. and George, E. I. (1992). Explaining the gibbs sampler. The American Statistician, 46(3):167–174.

- Cheng et al., (2018) Cheng, X., Chatterji, N., Bartlett, P., and Jordan, M. (2018). Underdamped Langevin MCMC: A non-asymptotic analysis. In Proceedings of the 31st Conference On Learning Theory, volume 75, pages 300–323.

- Dalalyan, (2017) Dalalyan, A. (2017). Theoretical guarantees for approximate sampling from smooth and log-concave densities. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(3):651–676.

- Dalalyan and Karagulyan, (2019) Dalalyan, A. and Karagulyan, A. (2019). User-friendly guarantees for the Langevin Monte Carlo with inaccurate gradient. Stochastic Processes and their Applications, 129(12):5278 – 5311.

- Dalalyan and Riou-Durand, (2018) Dalalyan, A. S. and Riou-Durand, L. (2018). On sampling from a log-concave density using kinetic langevin diffusions. arXiv, abs/1807.09382.

- Del Moral et al., (2006) Del Moral, P., Doucet, A., and Jasra, A. (2006). Sequential monte carlo samplers. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 68(3):411–436.

- Duane et al., (1987) Duane, S., Kennedy, A., Pendleton, B. J., and Roweth, D. (1987). Hybrid monte carlo. Physics Letters B, 195(2):216 – 222.

- Durmus et al., (2019) Durmus, A., Majewski, S., and Miasojedow, B. (2019). Analysis of langevin monte carlo via convex optimization. Journal of Machine Learning Research, 20:73:1–73:46.

- Durmus and Moulines, (2017) Durmus, A. and Moulines, É. (2017). Non-asymptotic convergence analysis for the Unadjusted Langevin Algorithm. Ann. Appl. Probab., 27(3):1551–1587.

- Eberle et al., (2019) Eberle, A., Guillin, A., and Zimmer, R. (2019). Couplings and quantitative contraction rates for Langevin dynamics. Annals of Probability, 47(4):1982–2010.

- Evensen, (2009) Evensen, G. (2009). Data Assimilation: The Ensemble Kalman Filter. Springer-Verlag Berlin Heidelberg.

- Fabian, (1981) Fabian, P. (1981). Atmospheric sampling. Advances in Space Research, 1(11):17 – 27.

- Geman and Geman, (1984) Geman, S. and Geman, D. (1984). Stochastic relaxation, gibbs distributions, and the bayesian restoration of images. IEEE Trans. Pattern Anal. Mach. Intell., 6:721–741.

- Geweke, (1989) Geweke, J. (1989). Bayesian inference in econometric models using Monte Carlo integration. Econometrica, 57(6):1317–1339.

- Hastings, (1970) Hastings, W. (1970). Monte Carlo sampling methods using Markov chains and their applications. Biometrika, 57(1):97–109.

- Iglesias et al., (2013) Iglesias, M., Law, K., and Stuart, A. (2013). Ensemble Kalman methods for inverse problems. Inverse Problems, 29(4):045001.

- Li et al., (2020) Li, R., Pei, S., Chen, B., Song, Y., Zhang, T., Yang, W., and Shaman, J. (2020). Substantial undocumented infection facilitates the rapid dissemination of novel coronavirus (sars-cov-2). Science, 368(6490):489–493.

- Markowich and Villani, (1999) Markowich, P. and Villani, C. (1999). On the trend to equilibrium for the Fokker-Planck equation: An interplay between physics and functional analysis. In Physics and Functional Analysis, Matematica Contemporanea (SBM) 19, pages 1–29.

- Mattingly et al., (2002) Mattingly, J., Stuart, A., and Higham, D. (2002). Ergodicity for sdes and approximations: locally lipschitz vector fields and degenerate noise. Stochastic Processes and their Applications, 101(2):185 – 232.

- Metropolis et al., (1953) Metropolis, N., Rosenbluth, A., Rosenbluth, M., Teller, A., and Teller, E. (1953). Equation of state calculations by fast computing machines. The Journal of Chemical Physics, 21(6):1087–1092.

- Nagarajan et al., (2007) Nagarajan, N., Honarpour, M., and Sampath, K. (2007). Reservoir-fluid sampling and characterization — key to efficient reservoir management. Journal of Petroleum Technology, 59.

- Neal, (1993) Neal, R. M. (1993). Probabilistic inference using Markov Chain Monte Carlo methods. Technical Report CRG-TR-93-1. Dept. of Computer Science, University of Toronto.

- Neal, (2001) Neal, R. M. (2001). Annealed importance sampling. Statistics and Computing, 11:125–139.

- Nesterov, (2012) Nesterov, Y. (2012). Efficiency of coordinate descent methods on huge-scale optimization problems. SIAM Journal on Optimization, 22(2):341–362.

- Parisi, (1981) Parisi, G. (1981). Correlation functions and computer simulations. Nuclear Physics B, 180(3):378–384.

- Reich, (2011) Reich, S. (2011). A dynamical systems framework for intermittent data assimilation. BIT Numerical Mathematics, 51(1):235–249.

- Roberts and Rosenthal, (2004) Roberts, G. and Rosenthal, J. (2004). General state space Markov chains and MCMC algorithms. Probability Surveys, 1.

- Roberts and Tweedie, (1996) Roberts, G. and Tweedie, R. (1996). Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 2(4):341–363.

- Rossky et al., (1978) Rossky, P. J., Doll, J. D., and Friedman, H. L. (1978). Brownian dynamics as smart monte carlo simulation. The Journal of Chemical Physics, 69(10):4628–4633.

- Russo et al., (2018) Russo, D., Roy, B., Kazerouni, A., Osband, I., and Wen, Z. (2018). A tutorial on Thompson sampling. Foundations and Trends in Machine Learning, 11(1):1–96.

- Shen and Lee, (2019) Shen, R. and Lee, Y. T. (2019). The randomized midpoint method for log-concave sampling. In Advances in Neural Information Processing Systems, pages 2100–2111.

- Vempala, (2010) Vempala, S. (2010). Recent progress and open problems in algorithmic convex geometry. In IARCS Annual Conference on Foundations of Software Technology and Theoretical Computer Science, volume 8, pages 42–64.

- Welling and Teh, (2011) Welling, M. and Teh, Y. W. (2011). Bayesian learning via stochastic gradient langevin dynamics. In Proceedings of the 28th international conference on machine learning (ICML-11), pages 681–688.

- Wright, (2015) Wright, S. J. (2015). Coordinate descent algorithms. Mathematical Programming, Series B, 151(1):3–34.

Appendix A Proof of Theorem 4.1

We recall the SDE (7):

| (29) |

where is randomly selected from . Moreover, recall that is a Markovian process. We denote its transition kernel by , meaning that

Moreover, we denote the -step transition kernel. The following proposition establishes the exponential convergence of the Markov chain.

Proposition A.1.

Under conditions of Theorem 4.1, there are constants , such that for any

| (30) |

where is the minimal point of and is the transition kernel for .

Proof of Theorem 4.1.

First, suppose the distribution of is induced by . Then for , the distribution of between is preserved. Meanwhile, we have

and the marginal distribution of is also preserved. Therefore , proving that is the density of the stationary distribution.

Second, to prove (20), let that has finite second moment, we multiply on both sides of (30) and integrate, to obtain

where is a constant.

By using (29) with Itô’s formula, we have

where and are constants that depend only on and . From Grönwall’s inequality, we obtain

Then, if , we have for any that

which implies . Therefore, if has finite second moment, then all have finite second moments for . Letting , multiplying on both sides of (30) and integrating, we obtain

where is a constant. Since this bound holds for all , we set and to obtain (20). ∎

A.1 Proof of Proposition A.1

Before we prove the Proposition, we first recall a result from (Mattingly et al.,, 2002) for the convergence of Markov chain using Lyapunov condition together with minorization condition.

Theorem A.1.

[(Mattingly et al.,, 2002, Theorem 2.5)] Let denote the Markov chain on with transition kernel and filtration . Let satisfy the following two conditions:

-

Lyapunov condition:

There is a function , with , and real numbers , and such that

-

Minorization condition:

For from the Lyqpunov condition, define the set as follows:

(31) for some . Then there exists an and a probability measure supported on (that is, ), such that

Under these conditions, the Markov chain has a unique invariant measure . Furthermore, there are constants and such that, for any , we have

| (32) |

To use this result to prove Proposition A.1, we will consider the -step chain of and verify the two conditions, as in the following two lemmas for the Lyapunov function and the minorization over a small set, respectively.

Lemma A.1.

Lemma A.2.

Proposition A.1 follows easily from these results.

Proof of Proposition A.1.

It suffices to show -step chain satisfies the conditions in Theorem A.1 with , and , and is induced by . We apply (34) from Lemma A.1 iteratively, times, to obtain

which implies that satisfies Lyapunov condition in Theorem A.1 with . Moreover, Lemma A.2 directly implies that the -step transition kernel satisfies the minorization condition. Therefore, by Theorem A.1, we have

which concludes the proof of the proposition when we substitute . ∎

Proof of Lemma A.1.

We assume without loss of generality that (so that ) and drop the filtration in the formula for simplicity of notation. Then

| (36) |

Since

we have

| (37) | ||||

To deal with second term and third term in (37), we first note that, under condition :

| (38) |

This means

| (39) | ||||

We further bound the second term of (39):

| (40) | ||||

where we used Young’s inequality in (I), the Lipschitz condition in (II), Lemma A.3 below (specifically, inequality (43)) in (III), and the Lipschitz condition again in (IV). This, when substituted into (39), gives

To bound the third term in (37), again for the case , we use (38) again for:

| (41) | ||||

where we used Young’s inequality in (I), Lemma A.3 below (specifically, inequality (42)) in (II), and Lipschitz continuity in (III), together with by (33).

Finally, we have

Proof of Lemma A.2.

To prove (35), we construct a new Markov process . Defining , we obtain from by running the following process:

Then for and , let

and set . Denote the transition kernel by (corresponding to one round of a cyclic version of the coordinate algorithm). We then have the following properties:

-

•

For any and , we have

-

•

possesses a positive jointly continuous density.

According to (Mattingly et al.,, 2002, Lemma 2.3), since has a positive jointly continuous density, there exists an and a probability measure with , such that

which implies

This proves (35) by setting . ∎

In the proof of Lemma A.1, we used several estimates in inequalities (40) and (41). We prove these estimates in the following lemma.

Lemma A.3.

Proof.

To obtain (42), we have

| (44) | ||||

To bound the second term, we use (38) again:

| (45) | ||||

where we use Young’s inequality and

by Doob’s maximal inequality. By substituting (45) into (44), we obtain

Using , we move the first term on the right to the left to obtain

leading to (42). Then we obtain (43) by plugging this in (45) and using the fact that by (33). ∎

Appendix B Proof of Theorem 4.2

The proof of this theorem requires us to design a reference solution to explicitly bound . Let be a random vector drawn from target distribution induced by , so that . We then require to solve the following SDE: for , with defined in (6):

| (46) |

If we use the same Brownian motion as in (5), we have

| (47) |

where is the unit vector in direction. Since the -th marginal distribution of is preserved in each time step according to (46), the whole distribution of is preserved to be for all . Therefore, by the definition , we have

where

| (48) |

This means bounding amounts to evaluating . Under Assumption 3.1, we have the following result.

Proposition B.1.

Proof of Theorem 4.2.

The proof for Corollary 4.1 is also obvious.

Proof of Corollary 4.1.

B.1 Proof of Proposition B.1

We prove the Proposition by means of the following lemma.

Lemma B.1.

Under the conditions of Proposition B.1, for and , we have

| (52) | ||||

Proof.

In the -th time step, we have

so that

| (53) | ||||

We now analyze the first term on the right hand side under condition . By definition of , we have

| (54) | ||||

where we have defined

| (55) |

By Young’s inequality, we have

| (56) |

where is a parameter to be specified later.

For the first term on the right hand side of (56), we have

| (57) |

Note that the second term will essentially become the second line in (52), and the third term will become the third line in (52) (upon the proper choice of ). For very small , this term is negligible.

For the second term on the right-hand side of (56), we recall the definition (55) and obtain

| (58) |

where (II) comes from -Lipschitz condition (11), (I) and (III) come from the use of Young’s inequality and Jensen’s inequality when we move the from outside to inside of the integral, and (IV) and (V) hold true because for all . In (VI) we use using (Dalalyan and Karagulyan,, 2019, Lemma 3).

By substituting (57) and (58) into the right hand side of (56), we obtain

| (59) |

By substituting (59) into (53), we have

| (60) |

where we have used .

Now, we need to choose a value of appropriate to establish (52). By comparing the two formulas, we see the need to set

since . It follows that . By substituting into (60), we obtain

| (61) |

We conclude the lemma by using the following Cauchy-Schwartz inequality to control the third term on the right hand side of this expression:

Proposition B.1 is obtained by simply summing all components in the lemma.

Proof of Proposion B.1.

Noting

we bound the right hand side by (52) and get

| (62) | ||||

The second and third terms on the right-hand side can be bounded in terms of :

-

•

By convexity, we have

(63) -

•

As the gradient is -Lipschitz, we have

(64)

By substituting (63) and (64) into (62) and using , we obtain

| (65) |

If we take sufficiently small, the coefficient in front of is strictly smaller than , ensuring the decay of the error. Indeed, by setting , we have

which leads to the iteration formula (49). ∎

Appendix C Proof of Theorem 4.3

Theorem 4.3 is based on the following proposition.

Proposition C.1.

We prove this result in Appendix C.1. The proof of the theorem is now immediate.

Proof of Theorem 4.3.

The proof of Corollary 4.2 is also immediate.

Proof of Corollary 4.2.

Use (24), to ensure , we set two terms on the right hand side of (24) to be smaller than , which implies that

| (67) |

To find optimal choice of , we need to minimize

under constraint and . Introducing a Lagrange multiplier , define the Lagrangian function as follows:

By setting for all , and substituting into the constraint to find the appropriate value of , we find that the optimal satisfies

C.1 Proof of Proposition C.1

The strategy of the proof for this proposition is almost identical to that of the previous section. The reference solution is defined as in (46). We will use the following lemma:

Lemma C.1.

Under the conditions of Proposition C.1, for and , we have

| (68) |

Proof.

In the -th time step, we have

meaning that

| (69) | ||||

To bound the first term in (53) we use the definition of . Under the condition , we have, with the same derivation as in (54):

| (70) | ||||

where we denoted .

However, different from (58), since has higher regularity, we can find a tighter bound for the integral. Denote

| (71) |

and

| (72) |

Then (70) can be written as

| (73) |

which implies, according to Young’s inequality, that, for any :

| (74) | ||||

Both terms on the right-hand side of (74) are small. We now control the first term. Plug in the definition (73), we have:

| (75) |

Noting that

because

according to the property of Itô’s integral, we can discard the cross terms with in (75) to obtain

| (76) |

For the last term of (C.1), we have the following control:

where we use Hölder’s inequality in and for all in . In , we use the following property of Itô’s integral:

By substituting into (C.1), we obtain

| (77) |

To bound the second term on the right-hand side of (74), we first note that is three times continuously differentiable, and (15) implies . Take on both sides of (46), under condition , we first have

| (78) |

According to Itô’s formula, we obtain

| (79) |

Substituting (78) into (79), we have

| (80) | ||||

By substituting into (71), we obtain

| (81) |

In the derivation, (II) comes from plugging in (80), and (I) and (III) come from the use of Jensen’s inequality, (V) comes from the use of Lipschitz continuity in the first and the second derivative ((11) and (15) in particular), and the fact that for all . Note also by (Dalalyan and Karagulyan,, 2019, Lemma 3).

Proof of Proposition C.1.

Appendix D Proof of Proposition 4.1

Proof of Proposition 4.1.

For this special target distribution , the objective function is . With and , we have: for all and

Therefore for all , we have

| (87) |

where we use in the last equation. By summing (87) over , we obtain

Using it iteratively, and considering , we have:

where we use in the last inequality.