Finite element approximation of Lyapunov equations related to parabolic stochastic PDEs

Abstract.

A numerical analysis for the fully discrete approximation of an operator Lyapunov equation related to linear SPDEs (stochastic partial differential equations) driven by multiplicative noise is considered. The discretization of the Lyapunov equation in space is given by finite elements and in time by a semiimplicit Euler scheme. The main result is the derivation of the rate of convergence in operator norm. Moreover, it is shown that the solution of the equation provides a representation of a quadratic and path dependent functional of the SPDE solution. This fact yields a deterministic numerical method to compute such functionals. As a secondary result, weak error rates are established for a fully discrete finite element approximation of the SPDE with respect to this functional. This is obtained as a consequence of the approximation analysis of the Lyapunov equation. It is the first weak convergence analysis for fully discrete finite element approximations of SPDEs driven by multiplicative noise that obtains double the strong rate of convergence, especially for path dependent functionals and smooth spatial noise. Numerical experiments illustrate the results empirically and it is demonstrated that the deterministic method has advantages over Monte Carlo sampling in a stability context.

Key words and phrases:

Lyapunov equations, finite element method, stochastic partial differential equations, stochastic heat equation, weak convergence, parabolic Anderson model, numerical approximation, multiplicative noise1991 Mathematics Subject Classification:

65M60, 60H15, 65J10, 65C30, 60H35, 49J201. Introduction

Lyapunov and Riccati equations have been studied for linear quadratic control and filtering of stochastic partial differential equations (SPDEs for short) since the late 1970s (see references below). Riccati equations are operator equations containing a nonlinear quadratic term. Their solutions provide optimal feedback controls for stochastic control problems and the covariance operators of the filtering distribution in optimal filtering with the Kalman–Bucy filter (see, e.g., [18] for a Hilbert-space-valued setting with bounded generators and trace-class noise). Removing the quadratic term, linear operator equations called Lyapunov equations are obtained. They are crucial for stability analysis and connected to quadratic functionals of SPDEs driven by multiplicative noise.

In this work we establish a complete error analysis for numerical discretizations of Lyapunov equations by the semiimplicit Euler method in time and a finite element method in space. We connect these approximations to approximations of path dependent quadratic functionals of SPDEs. This connection allows us to show weak convergence rates of the SPDE approximation which are twice the strong rates. Our analysis can be used as a stepping stone for approximation results on Riccati equations in future work.

The two main equations that we connect are the linear parabolic SPDE

| (1) |

with initial condition in a Hilbert space and the operator valued Lyapunov equation, written in variational form,

| (2) |

with , where refers to a class of Hilbert–Schmidt operators. We show in Section 3 that these are connected via

| (3) |

with respect to the quadratic functional

| (4) |

Here denotes the bilinear form corresponding to the operator that generates an analytic semigroup and is a cylindrical Wiener process. This includes the classical case of a -Wiener process with trace-class covariance. For the complete details on the setting, the reader is referred to Section 2.

We study Lyapunov equations in a new generality suitable for numerical analysis with an emphasis on regularity. It was surprising to us that the literature does not cover the setting of cylindrical noise (cf. [15, 19, 20, 21, 23, 26, 27, 34]). We therefore develop the solution theory for the Lyapunov equation and prove existence and uniqueness by the Banach fixed point theorem and the Gronwall lemma.

To show (3), we use tools from numerical analysis. We approximate both equations (2) and (1) on a finite-dimensional subspace such as a finite element space and show that (3) holds in the semidiscrete setting. Convergence establishes equality in the limit and gives as a byproduct convergence to the Lyapunov equation and weak convergence of the SPDE approximation.

For the fully discrete approximation of the Lyapunov equation (2), we discretize the above semidiscrete approximation by a semiimplicit Euler method in time. Results on numerical methods for Lyapunov and Riccati equations for stochastic problems are rare. The results of this paper are most closely related to those of [31], which only considers one-dimensional noise in an abstract approximation framework for Riccati equations. Connected to our problem are also [30], in which a time-independent Lyapunov equation related to an approximation of (1) is employed as part of a bigger problem, and [6], which assumes convergence of an approximation of a Riccati equation to derive strong convergence of a finite element approximation of a controlled version of (1). To the best of our knowledge, this work is the first to provide rigorous a priori convergence rates for a fully discrete numerical approximation of the Lyapunov equation (2) in the infinite-dimensional noise setting and the first to connect such approximations to weak convergence for the related SPDE (1).

Weak convergence of numerical approximations of SPDEs with additive noise is a well understood topic, see, e.g., for implicit Euler in time [36] and for finite element and spectral Galerkin methods in space [3, 8, 14]. For multiplicative noise the literature is still restricted to special cases. Weak rates of convergence have been obtained for discretization in time with implicit [9, 16] and exponential [24] Euler schemes and in space with a spectral Galerkin method [12]. For the finite element method, proofs are restricted to the spatially semidiscrete setting with (essentially) linear multiplicative space-time white noise [3]. The fully discrete setting and more regular noise are still open. One reason for this is the appearance of an extra term [3] which is not present in the spectral Galerkin method [12].

Based on the convergence analysis of the fully discrete approximation of the Lyapunov equation and the connection (3), we are able to extend the existing weak convergence analysis for finite element approximations. In the fully discrete setting of (2) and (1), we establish (3) up to a small error and are thus the first to show convergence for path dependent quadratic functionals with multiplicative white or colored noise in the finite element setting. The rate is twice that of strong convergence and coincides with that for additive noise.

Our numerical schemes for (1) and (2) and their convergence open up for two methods to approximate (4): either deterministically for all initial conditions with (2) or combining (1) with a Monte Carlo method. Depending on the application one or the other method might be more suitable. If the problem at hand is the computation of (4) with respect to all initial conditions in parallel, our Lyapunov method is preferable. This method also has an advantage

-

(i)

if the operator is non-local, since then multiplication with a dense matrix needs to be repeated for each time step and each sample in a Monte Carlo simulation. In a Lyapunov method, a similar dense matrix operation only needs to be repeated once for each time step.

-

(ii)

under multiplicative noise of large magnitude, since this causes stability problems [1]. More precisely, the zero solution can be asymptotically stable in the almost sure sense but asymptotically mean square unstable, simultaneously. In this setting, the Monte Carlo method fails to approximate while our deterministic Lyapunov method faces no problem. We demonstrate this phenomenon in an example in Section 6.

The manuscript is organized as follows. In Section 2 the abstract setting and notation of the paper are introduced along with assumptions on the family of approximation spaces . Existence and uniqueness of a mild solution to (2) and its spatial and temporal regularity are established in Section 3. Furthermore, (3) is shown via an analogous equality in the semidiscrete setting, i.e., (1) and (2) are solved on . Section 4 and Section 5 are devoted to convergence analyses of fully discrete semiimplicit approximation schemes for (2) and (1), respectively. In Section 6, numerical experiments conclude the manuscript that illustrate the theoretical results and compare the deterministic approach via (2) with a Monte Carlo simulation of (1) with respect to the stability issues named in (ii) above. For completeness we include proofs based on standard arguments in the appendix.

2. Notation and abstract setting

We start by introducing the necessary notation. For separable Hilbert spaces and with corresponding norms, we denote by the Banach space of all bounded linear operators equipped with the operator norm, where we abbreviate . The space is the closed subspace of all self-adjoint operators and is the restriction to all operators that are additionally non-negative definite. By we denote the space of Hilbert–Schmidt operators . This is a Hilbert space with norm and inner product given by

where is an orthonormal basis of . The definition is independent of the choice of basis. For an interval , we denote by and the spaces of continuous and strongly continuous functions from to , respectively.

The beta function is given by . By a change of variable the following very useful identity is obtained: For all , ,

| (5) |

We next introduce the setting that we consider throughout the article. Here and are fixed separable Hilbert spaces and by and we denote the inner product of and its induced norm, respectively.

Assumption 2.1.

Equations (1) and (4) satisfy the following conditions:

-

(i)

The linear operator is densely defined, self-adjoint and positive definite with compact inverse.

-

(ii)

The process is an adapted cylindrical -Wiener process on a filtered probability space .

-

(iii)

For a fixed regularity parameter , the linear operator satisfies .

-

(iv)

The linear operators and satisfy and .

Fractional powers of , such as in the assumption above, are well-defined and enable us to define the spaces , which are used to measure spatial regularity. More specifically, for

and for the space is the closure of under the -norm and , the dual space of with respect to . In that way we obtain a family of separable Hilbert spaces with the property that whenever , where the embedding is dense and continuous. Moreover, by [7, Lemma 2.1], for every , can be uniquely extended to an operator in . We make no notational distinction between and its extension and define the corresponding bilinear form for by

| (6) |

The operator is the generator of an analytic semigroup of bounded linear operators on that extends to , . As for , we do not differentiate between the semigroup and its extension. The analyticity of the semigroup implies the existence of constants such that for all

| (7) |

and for all

| (8) |

These regularity estimates play an essential role in our proofs. We refer to [29, Appendix B] for a detailed introduction to this setting.

Assumption 2.1(ii) on includes white noise in (by letting ) as well as -valued trace-class -Wiener processes (by letting , cf. [32, Theorem 7.13]). We introduce the notation and set for . Note that for predictable stochastic processes the stochastic integral is well-defined.

We are now in place to introduce the setting for the SPDE (1). By [4, Theorem 2.9] (1) admits an up to modification unique mild solution, i.e., a predictable process that satisfies for all , -a.s.

| (9) |

and

| (10) |

where we denote if there exists a generic constant such that and the size of the constant is of minor relevance.

Next, we introduce spatial approximation spaces. Let be a family of finite-dimensional subspaces of , where denotes the refinement parameter. We equip with the same inner product as so that for an operator ,

Here is the generalized orthogonal projector (see, e.g., [29, Section 3.2]) which coincides with the standard orthogonal projector when restricted to . Let be the unique operator defined for by

This implies that is self-adjoint and positive definite on . Therefore, generates an analytic semigroup on and fractional powers of are defined in the same way as for . For brevity we write for and for , , . By [29, (3.12)] and [29, Lemma B.9(ii)] there exist constants so that for all

| (11) |

and for all that

| (12) |

Here and below we use the notation for a constant depending on the choice of discretization but not the specific value of . The optimal value may differ from line to line.

To guarantee that has appropriate approximation properties and includes finite element approximations, we make the following assumptions.

Assumption 2.2.

There exist constants such that

-

(i)

for , : ,

-

(ii)

for , : ,

-

(iii)

for , : and

-

(iv)

for , : .

Example 2.3.

Assumption 2.2 holds in the following finite element setting. Let for some bounded, convex polygonal domain , and denote the Laplace operator with zero Dirichlet boundary conditions. Let be a regular family of triangulations of and let be the space of all continuous functions that are piecewise polynomials of some fixed degree on . Then (i) and (ii) hold true, see, e.g., [35, Chapters 1-3]. If we assume in addition to this that the family is quasi-uniform, then we also have (iii) and (iv), see, e.g., [35, (3.28)] and [13].

A consequence of (iv) and the definition of (see [3, page 1341]) is the existence of constants such that for all

| (13) |

Using also (i) and (iii) one can show (cf. the proof of [28, Theorem 4.4]) the existence of constants such that for all

| (14) |

Let denote the error operator . As another consequence of (i) we obtain that there exist constants such that for all , and with ,

| (15) |

This is proven analogously to [2, Lemma 5.1], replacing the use of [29, Lemma 3.12] with [29, Lemma 3.8], using also (14) and the fact that is self-adjoint for all . In the next sections, we frequently use this bound with .

We next introduce the setting for the full discretization in space and time. Recall that and set for . For , let be the uniform discretization of given by and . Let us denote by the implicit Euler approximation of the semigroup at time , i.e., . The discrete family of powers of acts as a fully discrete approximation of the semigroup . We again write, for brevity, for .

Let us now collect three properties of the discrete approximation of the semigroup and the error operator . There exist constants such that for all and

| (16) |

for all , and

| (17) |

and for all and

| (18) |

For a proof of (16), see, e.g., [35, Lemma 7.3]. We show (17) in Proposition B.1 and the well-known result (18) can be shown in a similar way, see, e.g., [29, Lemma B.9].

We use the abbreviations , and .

3. Theory of the Lyapunov equation and the SPDE

The goal of this section is threefold. We start with existence, uniqueness and regularity of the solution to the Lyapunov equation (2) in Section 3.1. Second, we present in Section 3.2 an error analysis for semidiscrete space approximations of the Lyapunov equation (2) and the SPDE (1). This is used in Section 3.3 to show (3). As an immediate consequence we obtain weak convergence rates for the semidiscrete SPDE approximation to (1)

3.1. Existence, uniqueness and regularity

While the variational form (2) of the Lyapunov equation is natural for numerics, it is more natural to work in the semigroup framework for the regularity analysis. The mild form of the Lyapunov equation reads: Find such that for all and

| (19) |

We note that the mapping is not necessarily Bochner integrable due to the semigroup being only strongly measurable, which requires to be inside the integral.

With some abuse of notation, we write for the operator in that for all and satisfies

It satisfies .

Let be the space of all operator-valued functions satisfying

for as fixed in Assumption 2.1(iii) and

On this space we introduce the family of equivalent norms given by

The space is a Banach space since the norm is the sum of two proper Banach norms.

An operator-valued function is called a mild solution to (2) if it satisfies (19) for all and . Existence, uniqueness and regularity of a mild solution to (19) are stated in Theorem 3.1 below and the equivalence of solutions to (2) and (19) in Theorem 3.2. Surprisingly, the results seem to be new in our context. Since the proofs are based on standard techniques such as the Banach fixed point theorem and the Gronwall lemma, we omit them here but include them for completeness in Appendix A.1 and A.2.

Theorem 3.1.

There exists a unique mild solution to (19) that satisfies . Moreover, the solution satisfies the following regularity estimates:

-

(i)

For all with , and there exists a constant such that for all

-

(ii)

For all , with , there exists a constant such that for all

3.2. Semidiscrete approximations in space

Let us consider semidiscrete approximations of the Lyapunov equation (2) and the SPDE (1) in this subsection. For this purpose we use the approximation spaces introduced in Section 2 with related operators. Let be the space endowed with the norm

The semidiscrete Lyapunov equation reads in variational form: Given , find such that for all

| (20) | ||||

The mild formulation related to (20) is given for all and by

| (21) | ||||

Existence and uniqueness of a solution to both equations follow from Theorem 3.1 and Theorem 3.2 applied to . In the next proposition, we show that the regularity bounds in Section 3.1 are uniform in and convergence of the approximation (21).

Proposition 3.3.

Let be the family of unique mild solutions to (21).

-

(i)

For all with , there exists a constant such that for all

-

(ii)

For all , with , there exists a constant such that for all and

-

(iii)

For all , with , there exists a constant such that for ,

Proof.

Uniformity in follows from the uniformity in (11) and (12). More precisely, every constant in the proof of Theorem 3.1 can be replaced by a corresponding constant in the semidiscrete setting. The only place where some extra care is needed is the estimate corresponding to (52). For this we observe that for arbitrary

and similarly that . Therefore, we obtain and for any by (13)

| (22) | ||||

This implies the uniform bound corresponding to (52).

Having shown the first two claims of the proof, we are ready to prove (iii). First we rewrite using (19) and (21) to obtain for

which yields

We treat the three error terms separately. Using (7), (11) and (15) the term can be bounded by

and similarly the second term satisfies

Adding, subtracting and applying the triangle inequality, we split into

By Assumption 2.2, its consequences and (22), we bound the three terms by

where we set

| (23) |

Collecting all estimates we obtain

| (24) | ||||

where we bound all terms in by the strongest singularity from . Choosing and ensures that the exponent is bigger than , so that Gronwall’s lemma (see, e.g., [25]) yields

| (25) |

The general claim follows by a bootstrap argument using (25) in (24) and (5), which completes the proof. ∎

Having analyzed the convergence of the semidiscrete Lyapunov equation, let us continue with the semidiscrete SPDE. Let be the family of mild solutions on the finite-dimensional spaces satisfying

| (26) |

and for all , , -a.s.

| (27) |

Existence follows from [4, Theorem 2.9(ii)], where uniformity of (26) in is deduced from (11). The proof of strong convergence is standard, cf., e.g., [29, Theorem 3.10]. Therefore we state the following proposition without proof.

3.3. Connection between the Lyapunov equation and the SPDE

We are now in place to prove (3) in Theorem 3.6 below. As a first step we show the equality in the semidiscrete setting of Section 3.2. We therefore define for , and

used in the following lemma.

Lemma 3.5.

Let be the family of unique mild solutions to (21). For all , ,

Proof.

Fix and let satisfy for that

In a first step, we observe that by (21) and the definition of

The main part of the proof is based on applying the Itô formula to deduce that

| (28) | ||||

Once this has been established, taking expectations on both sides completes the proof since the stochastic integral vanishes.

We now prove (28). In the following application of the Itô formula, we use explicit expressions for the derivatives , , . From (20), for the time derivative satisfies

| (29) |

where denotes an arbitrary orthonormal basis. By direct calculations the space derivatives and are for given by

| (30) |

Since , the semidiscrete solution is a strong solution, meaning that -a.s.

Therefore we can apply the Itô formula [11, Theorem 2.4] to the function to obtain

Inserting the expressions from (29) and (30) proves (28) by cancellations. ∎

We are finally in place to show (3) even in the time dependent setting. Therefore we set with a slight abuse of notation

The proof of the following theorem is based on the convergence of the semidiscrete approximations in Section 3.2 and the equality in .

Theorem 3.6.

Proof.

By the triangle inequality we have that

We prove that the right hand side converges to zero as goes to . Proposition 3.3 with guarantees that

The second term vanishes by Lemma 3.5 since . The strong convergence in Proposition 3.4 and the uniform moment bounds (10) and (26) imply in particular convergence of the quadratic functional and thus

i.e., the convergence of the last term. ∎

Using the polarization identity one can extend the result to bilinear forms. More specifically, let be the mild solution to (9) with initial condition , then for all and

Given the connection between the Lyapunov equation and , Theorem 3.6 implies weak convergence with twice the strong rate of the semidiscrete scheme (27) in a non-standard way. This extends the weak convergence result (in the multiplicative noise setting) of [3] to smooth noise with , albeit for a different class of test functions.

Corollary 3.7.

4. Fully discrete approximation of the Lyapunov equation

This section is devoted to the stability and convergence analysis of a fully discrete scheme for the Lyapunov equation (2). It is based on the -valued implicit Euler approximation of the semigroup , introduced in Section 2. Inspired by the mild solution (19), we define the fully discrete approximation of , , by the discrete variation of constants formula

| (31) |

with . As recursion it reads

| (32) |

or equivalently

| (33) |

Note that for all .

Before proving convergence, let us first show regularity of the fully discrete approximation, which is the analog result to Theorem 3.1 and Proposition 3.3.

Theorem 4.1.

For all and with , there exists a constant such that for , and

Proof.

We fix . By multiplying (31) with from the left and from the right we obtain

For the term containing , we have by (22) that

For the other terms we use the fact that by (16), with and

This then yields

For the first sum we have , so taking and using the discrete Gronwall lemma (cf. [17]) proves the claim for this special case and implies for , , in the above estimate that

The proof is completed by observing that

and that, by Assumption 2.2(iii) and the bound ,

We are now in place to prove convergence of the fully discrete approximation of (19) with the same convergence rate in space as in the semidiscrete setting in Proposition 3.3 and rate in time.

Theorem 4.2.

For all , and with , there exists a constant satisfying for , and

Proof.

With Proposition 3.3, the triangle inequality, (13) and (14) it suffices to prove that under the conditions of this theorem, there exists such that for , and

We introduce the right-continuous interpolation of given by

for which we by (13) and (16) have for the existence of a constant such that for all

| (34) |

We also introduce the corresponding error operator and extend the fully discrete solution to continuous time by , for . From (11), (12) and (17) we obtain the existence of a constant such that for all

| (35) |

Using this notation it follows from (31) that for all and

Since and are self-adjoint at all times, this equality and (21) along with

yield

For the first term we obtain with (17), (16) and (11) that

Similarly we use (34), (16) and (35) for the next term to see that

Using (34), (11), (22), (23), (35) and (5) yields

For the last term we add and subtract a piecewise constant approximation of , for . With (22) we obtain

Proposition 3.3(ii) yields the existence of a constant so that for all and the first of the two terms in the sum is bounded by

For , however, we use (23) and Assumption 2.2(iii) to bound it by

Noting also that by (16), for and and that for , we find that

where the last inequality follows by and the fact that the coupling yields .

Collecting the estimates, the sum of all four terms is bounded by

The choice implies with the discrete Gronwall lemma that

which shows the claim for this special case. Similarly to Proposition 3.3, the proof is completed by a bootstrap argument. ∎

As a consequence, we obtain convergence of the approximation of the quadratic functional (4) by the Lyapunov equation of up to rate in time and double this rate in space.

Corollary 4.3.

For all and , there exists a constant satisfying for , and

where .

5. Fully discrete SPDE approximation

In Section 3 we have shown the connection (3) between the Lyapunov equation and the SPDE by the analogous equality of the space approximations of the equations. In this section we prove that a similar relation holds in the fully discrete setting up to a sufficiently fast converging error. This connection implies weak convergence of a fully discrete approximation of the SPDE (1).

The fully discrete approximation of (1) is obtained by a semiimplicit Euler–Maruyama scheme. Let be the family of discrete stochastic processes satisfying and for all -a.s

| (36) |

where denotes the increment of the Wiener process. Using the fact that the recursion can be rewritten as

| (37) |

which leads to the discrete variation of constants formula

| (38) |

An induction shows that for all , , and by a classical Gronwall argument one obtains for all and the existence of a constant such that

| (39) |

We omit the details and refer to [2, Proposition 3.16] for a proof of a similar stability result. Apart from this, we use the following lemma in our weak convergence proof.

Lemma 5.1.

Let . For all , there exists a constant such that for all and

Proof.

We are now in place to state the fully discrete version of (3), which implies weak convergence stated in Corollary 5.3 below. We set

| (40) |

for .

Theorem 5.2.

Proof.

By a telescoping sum argument and the fact that we obtain

so that

| (41) | ||||

The second equality follows from the identity

obtained by (36), the Itô isometry and the independence of and , along with (32) and that .

For the first term , since , by the triangle inequality, (16), (14), Assumption 2.2(iii) and (39) we obtain for

In the case that , we use the fact that to obtain the split

The term is for handled by Lemma 5.1 with

which is by (14), Theorem 4.1 and (16) bounded by

where , , denotes the constant in Theorem 4.1. For we note that (18) implies

The term is treated similarly to , using for the bound in Lemma 5.1 and (5). We obtain that is bounded by a constant times in the case that , and a constant times for . Similarly, is bounded by a constant times and for and , respectively.

For the term , with , we obtain from (14), (18), Theorem 4.1, (16) and (39) that

For one obtains the same bound without the term since (39) is not used. Collecting the estimates, we bound (41) for by

We note that yields . Moreover, the identity (5) implies

These facts, along with the bounds , and , yield

This shows the claim for . The case is treated similarly. ∎

We now obtain our weak convergence result as a direct consequence of Theorem 5.2 and Corollary 4.3. We write for .

Corollary 5.3.

We conclude this section by relating our approach to prove weak convergence to the most common in the literature. That approach is based a joint use of the Itô formula and the solution to a Kolmogorov equation, see references in the introduction. For additive noise the solution to the Kolmogorov equation is regular enough to show weak convergence rates. For multiplicative noise the solution is less regular and a straight forward generalization of the methodology for additive noise to multiplicative noise leads to suboptimal rates for with finite element approximations, see [3]. This has been solved in [9, 24] but restricts to spectral methods. In our setting the Kolmogorov equation is solved by the quadratic form of the solution of the Lyapunov equation with , see Theorem 3.2. By Theorem 3.1 it has the same regularity as for additive noise. Therefore, a weak convergence proof with desired convergence rates could be carried out by adapting the method of [16]. Our approach is advantageous since it has no regularity assumption on the initial condition as in [5] and can treat path-dependent functionals, where we are only aware of [5, 10] for SPDEs.

6. Numerical implementation and simulation

The goal of this section is to show how the numerical approximations of Sections 4 and 5 are implemented in practice. We demonstrate our theoretical results by numerical simulations in the specific setting of Example 2.3. Solving the Lyapunov equation is then compared to the Monte Carlo method, both by an empirical stability analysis as well as a theoretical computational complexity discussion.

6.1. Implementation and convergence analysis

6.1.1. Implementation of the fully discrete Lyapunov approximation

First, we describe how the fully discrete approximation from (33) of the solution to the Lyapunov equation (2) is implemented numerically. Let denote the dimension of and let be a basis of . By and we denote the matrices with entries given by , , , and , , respectively. For , let be the matrix containing the coefficients in the expansion of the approximation given by (33). Here is given by for all . By we denote the matrix with entries given by

where the adjoint of is taken with respect to .

The matrix version of (33) is now given by

| (42) |

with initial value . With this in place, one approximates , , by . Here, denotes the transpose of the vector of coefficients in the expansion .

6.1.2. Empirical convergence analysis

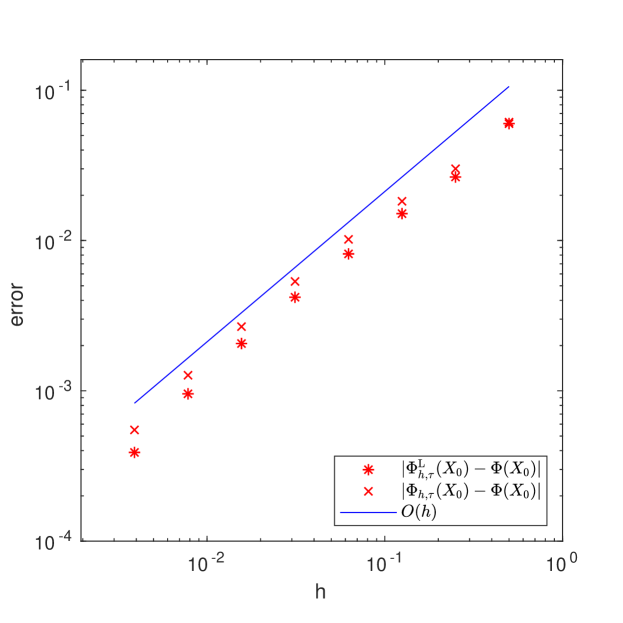

Next, we illustrate, by numerical simulations, our theoretical results (specifically Corollary 4.3 and Corollary 5.3). The same setting as in Example 2.3 is considered, where we recall that . We choose , so that the equation is driven by space-time white noise, and assume that is a linear Nemytskij operator (i.e., that for all and almost every ). Then for all in and for no positive when . We further specify , , , and rescale and by factors and , respectively. We choose an initial value for and compute and for and . The latter quantity is computed in a deterministic way by tensorizing the matrix equation system corresponding to (37) and applying the expectation on both sides. We refer to [33] for computational details on this tensor product approach. This approach was employed for a reference solution instead of a Monte Carlo method due to the stability problems of the latter, see Section 6.2.1. The errors and are shown in Figure 1.

Here we have replaced with the reference solution computed with and . All matrices and vectors are computed exactly, which is possible by our choice of , except for the initial value, which is interpolated onto the finite element space. Since for all , we expect from Corollary 4.3 and Corollary 5.3 a convergence rate of essentially . The results of Figure 1 are consistent with this expectation.

6.2. Comparison to the Monte Carlo method

The most straightforward way of utilizing a finite element method for the approximation of in (4), with fixed, is by a Monte Carlo method, i.e., by computing

| (43) |

Here is the number of iid samples of computed by the recursion (37). The Monte Carlo method has a low memory requirement, is easy to parallelize and can be improved by multilevel methods (see, e.g., [22] as well as the comment at the end of the next section). There are, however, certain situations in which the Lyapunov method of computing is preferable for the approximation of , which we now outline.

6.2.1. Empirical stability analysis

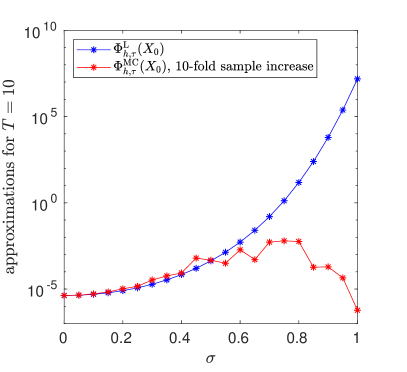

The zero solution to an SPDE with multiplicative noise such as (1) (or a discretization thereof) can be simultaneously asymptotically stable in a -a.s. sense and unstable in a mean square sense. In a Monte Carlo type method, this results in the number of samples needed for a satisfactory approximation in practice being prohibitively large. We discuss this challenge to such methods in detail, in the setting that and .

Consider the rescaled semidiscrete stochastic heat equation

| (44) |

Here, while all other parameters are as in Section 6.1.2. Following [1], the zero solution to (44) is said to be asymptotically stable -a.s. if, for any and , there exist

-

(i)

such that if , then for all and

-

(ii)

such that for any initial value satisfying -a.s., -a.s.

It is said to be asymptotically mean square stable if for every , there exist

-

(i)

such that if then for all and

-

(ii)

such that if then .

In [1], the authors consider a discretized stochastic heat equation, similar to (44) but with finite differences instead of finite elements. They prove that as increases, the zero solution becomes simultaneously asymptotically stable -a.s. and asymptotically mean square unstable. While their results do not directly translate to our setting, we also expect that for large and , becomes very big while most sample paths of are very small, possibly zero within machine accuracy. If the time discretization of shares this property as assumed in [1], approximates , and therefore also , poorly.

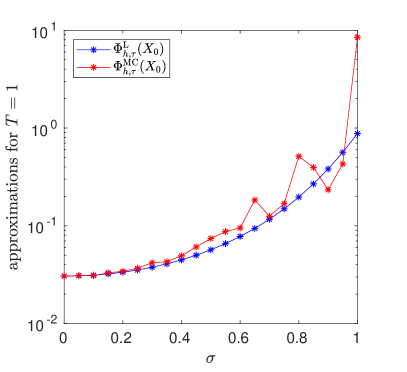

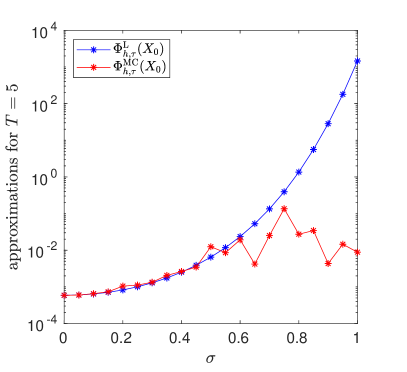

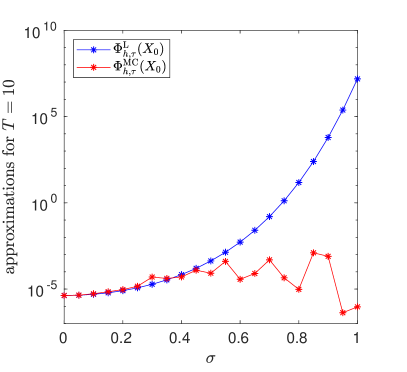

To investigate this in practice, we choose and as in Section 6.1.2 and compute approximations of for various values of and . The results from the Lyapunov method and the Monte Carlo method are compared. We choose and for both methods, with samples in the Monte Carlo method. In Figure 2(a) we see the results of the two methods for and . They seem to agree reasonably well for small values of , while the variance of increases as increases. For moderately larger values of , we already see the consequences of the mean square instability and the -a.s. stability of the zero solution to (44). In Figure 2(b), with , the difference between the two approximations is of several orders of magnitude. This behavior is even more pronounced for in Figure 2(c). Even if we increase the number of samples to (see Figure 2(d)), the results do not improve for . In other words, even for moderately large values of and , the Monte Carlo method fails to give reliable results. As noted in [1], replacing this simple Monte Carlo estimator with a multilevel Monte Carlo method does not solve this issue. Indeed, if empirical variances are used to estimate the number of samples needed at each level this method can suffer even more from this stability problem.

6.2.2. Computational complexity comparison

Even under parameter choices for which the stability problems outlined in the previous section do not occur, there may be other reasons for why one would prefer to approximate by means of the Lyapunov method rather than by Monte Carlo. First, the computation of can be expensive if is a non-local operator. Then the matrix is typically dense. This matrix is applied for the computation of the term containing in (43) a total of times. By the law of large numbers, should be chosen to be proportional to the inverse of the square root of the weak error in Corollary 5.3 in order for the Monte Carlo error not to asymptotically dominate the full mean squared error. Therefore, the computational cost can become prohibitively large.

Second, the Lyapunov method yields a way of approximating for all simultaneously. The Monte Carlo method can be adapted to this setting by iterating (37) to obtain

and then computing

However, forming the matrix corresponding to the sum of operators requires, again, the multiplication and addition of dense matrices, leading to great costs in terms of both computational power and memory. In fact, in the setting of the simulations of Section 6.1.2, it can be seen that the computational cost of is . This can be compared to for , the cost of the iterated Monte Carlo method if one chooses so that the additional Monte Carlo error does not dominate.

In conclusion, we have demonstrated that there may be several situations in which the Lyapunov method of computing is preferable for the approximation of compared to a Monte Carlo method. It should, however, be noted that it may be fruitful to combine these methods. For example, the Lyapunov method, computed at a coarse grid, may be used to indicate the presence of mean square instability combined with -a.s. stability in a system such as (44), suggesting that remedies such as the ones discussed in [1] should be taken.

References

- [1] M. Ableidinger, E. Buckwar, and A. Thalhammer. An importance sampling technique in Monte Carlo methods for SDEs with a.s. stable and mean-square unstable equilibrium. J. Comput. Appl. Math., 316:3–14, 2017.

- [2] A. Andersson, R. Kruse, and S. Larsson. Duality in refined Sobolev-Malliavin spaces and weak approximation of SPDE. J. SPDE Anal. Comp., 4(1):113–149, 2016.

- [3] A. Andersson and S. Larsson. Weak convergence for a spatial approximation of the nonlinear stochastic heat equation. Math. Comp., 85(299):1335–1358, 2016.

- [4] A. Andersson, A. Jentzen, and R. Kurniawan. Existence, uniqueness, and regularity for stochastic evolution equations with irregular initial values. J. Math. Anal. Appl., 495(1):124558, 2021.

- [5] A. Andersson, M. Kovács, and S. Larsson. Weak error analysis for semilinear stochastic Volterra equations with additive noise. J. Math. Anal. Appl., 437(2):1283–1304, 2016.

- [6] P. Benner, T. Stillfjord, and C. Trautwein. A linear implicit Euler method for the finite element discretization of a controlled stochastic heat equation. IMA J. Numer. Anal., 2021.

- [7] D. Bolin, K. Kirchner, and M. Kovács. Numerical solution of fractional elliptic stochastic PDEs with spatial white noise. IMA J. Numer. Anal., 40(2):1051–1073, April 2020.

- [8] C.-E. Bréhier and M. Kopec. Approximation of the invariant law of SPDEs: error analysis using a Poisson equation for a full-discretization scheme. IMA J. Numer. Anal., 37(3):1375–1410, 2017.

- [9] C.-E. Bréhier and A. Debussche. Kolmogorov equations and weak order analysis for SPDEs with nonlinear diffusion coefficient. J. Math. Pures Appl. (9), 119:193–254, 2018.

- [10] C.-E. Bréhier, M. Hairer, and A. M. Stuart. Weak error estimates for trajectories of SPDEs under spectral Galerkin discretization. J. Comput. Math., 36(2):159–182, 2018.

- [11] Z. Brzeźniak, J. M. A. M. van Neerven, M. C. Veraar, and L. Weis. Itô’s formula in UMD Banach spaces and regularity of solutions of the Zakai equation. J. Differ. Equ., 245(1):30–58, 2008.

- [12] D. Conus, A. Jentzen, and R. Kurniawan. Weak convergence rates of spectral Galerkin approximations for SPDEs with nonlinear diffusion coefficients. Ann. Appl. Probab., 29(2):653–716, 2019.

- [13] M. Crouzeix and V. Thomée. The stability in and of the -projection onto finite element function spaces. Math. Comp., 48(178):521–532, 1987.

- [14] J. Cui and J. Hong. Strong and weak convergence rates of a spatial approximation for stochastic partial differential equation with one-sided Lipschitz coefficient. SIAM J. Numer. Anal., 57(4):1815–1841, 2019.

- [15] G. Da Prato. Direct solution of a Riccati equation arising in stochastic control theory. Appl. Math. Optim., 11(3):191–208, 1984.

- [16] A. Debussche. Weak approximation of stochastic partial differential equations: the nonlinear case. Math. Comp., 80(273):89–117, 2011.

- [17] C. M. Elliott and S. Larsson. Error estimates with smooth and nonsmooth data for a finite element method for the Cahn–Hilliard equation. Math. Comp., 58(198):603–630, S33–S36, 1992.

- [18] P. L. Falb. Infinite-dimensional filtering: The Kalman-Bucy filter in Hilbert space. Inf. Control., 11:102–137, 1967.

- [19] F. Flandoli. Riccati equation arising in a stochastic optimal control problem with boundary control. Boll. Un. Mat. Ital. C (6), 1(1):377–393, 1982.

- [20] F. Flandoli. Direct solution of a Riccati equation arising in a stochastic control problem with control and observation on the boundary. Appl. Math. Optim., 14(2):107–129, 1986.

- [21] F. Flandoli. Boundary control of a stochastic parabolic equation with nonsmooth final cost. In Analysis and optimization of systems (Antibes, 1990), volume 144 of Lecture Notes in Control and Inform. Sci., pages 694–703. Springer, Berlin, 1990.

- [22] M. B. Giles. Multilevel Monte Carlo methods. Acta Numer., 24:259–328, 2015.

- [23] G. Guatteri and G. Tessitore. On the backward stochastic Riccati equation in infinite dimensions. SIAM J. Control Optim., 44(1):159–194, 2005.

- [24] M. Hefter, A. Jentzen, and R. Kurniawan. Weak convergence rates for numerical approximations of stochastic partial differential equations with nonlinear diffusion coefficients in UMD Banach spaces. ArXiv Preprint, arXiv:1612.03209, 2016.

- [25] D. Henry. Geometric Theory of Semilinear Parabolic Equations, volume 840 of Lecture Notes in Mathematics. Springer, Berlin, 1981.

- [26] Y. Hu and S. Tang. Stochastic LQ control and associated Riccati equation of PDEs driven by state- and control-dependent white noise. SIAM J. Control. Optim., 60(1):435–457, 2022.

- [27] A. Ichikawa. Dynamic programming approach to stochastic evolution equations. SIAM J. Control Optim., 17(1):152–174, 1979.

- [28] M. Kovács, S. Larsson, and F. Lindgren. Weak convergence of finite element approximations of linear stochastic evolution equations with additive noise. BIT Numer. Math., 52(1):85–108, 2012.

- [29] R. Kruse. Strong and Weak Approximation of Stochastic Evolution Equations, volume 2093 of Lecture Notes in Mathematics. Springer, Cham, 2014.

- [30] C. Kuehn and P. Kürschner. Combined error estimates for local fluctuations of SPDEs. Adv. Comput. Math., 46(1):25, 2020. Id/No 11.

- [31] T. Levajković, H. Mena, and A. Tuffaha. A numerical approximation framework for the stochastic linear quadratic regulator on Hilbert spaces. Appl. Math. Optim., 75(3):499–523, 2017.

- [32] S. Peszat and J. Zabczyk. Stochastic Partial Differential Equations with Lévy Noise, volume 113 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 2007.

- [33] A. Petersson. Computational aspects of Lévy-driven SPDE approximations, December 2017. Licentiate Thesis, Chalmers University of Technology, Gothenburg, Sweden.

- [34] G. Tessitore. Some remarks on the Riccati equation arising in an optimal control problem with state- and control-dependent noise. SIAM J. Control Optim., 30(3):717–744, 1992.

- [35] V. Thomée. Galerkin Finite Element Methods for Parabolic Problems, volume 25 of Springer Series in Computational Mathematics. Springer, Berlin, second edition, 2006.

- [36] X. Wang and S. Gan. Weak convergence analysis of the linear implicit Euler method for semilinear stochastic partial differential equations with additive noise. J. Math. Anal. Appl., 398(1):151–169, 2013.

Appendix A Proofs for Section 3.1

A.1. Proof of Theorem 3.1

As a first step we prove a result that is needed to ensure that the integrals in the proof of Theorem 3.1 are well-defined. The setting and notation is the same as in Sections 2 and 3 of the main text.

Lemma A.1.

For all , and the mappings

and

are strongly continuous.

Proof.

We prove the strong continuity of the second mapping in detail. The proof of the first is done in the same way.

The second mapping is a composition of the mappings , and . The first and third are strongly continuous as mappings and , respectively. This property can be extended to in both cases by considering an approximating sequence in and , respectively. Using (7), the strong continuity of and uniform continuity of we obtain for and that

with the constant notation introduced in Section 2. Since and is strongly continuous and since is uniformly continuous, the right hand side converges to zero as tends to . This completes the proof. ∎

The rest of the proof of Theorem 3.1 is based on a global fixed point argument in . Equation (19) is written in the form of a fixed point equation

with , acting on by

Existence of a unique solution in follows by the Banach fixed point theorem by proving that is well-defined and that for some the fixed point map is a contraction, i.e., that there exists such that for all

| (45) |

The proof is organized as follows: We start by proving that and continue by showing that , and with are strongly and uniformly continuous on and , respectively. From this we conclude that , , are well-defined and derive bounds to show the contraction property (45) of and the claimed regularity estimates.

To prove that we observe, using (7), that for all and

| (46) |

Setting and , respectively, shows the desired bound

| (47) |

For we use (7) to obtain that for all , , and

| (48) |

Together with the strong continuity of the mapping shown in Lemma A.1, this bound implies that when with , and in particular that the Bochner integral in is well-defined. It also shows that can be extended to a mapping . Next, for

| (49) | ||||

Using (48) we have for

| (50) |

Setting and , respectively, shows that

| (51) |

We now turn our attention to . For all , , , , and , we have by using (7) that

| (52) | ||||

Combining this with Lemma A.1 implies that for with , and in particular that the Bochner integral in is well-defined. Similarly to , it also implies that can be extended to . Using (52) we obtain, similarly to (49), the bound

| (53) |

For the case , we conclude from (5) that

| (54) |

Setting again and , respectively, yields

| (55) |

Next we show continuity of , and on and . For this purpose we prove Hölder continuity in operator norms on and strong continuity at zero separately. The Hölder continuity also implies (ii) once existence and uniqueness have been established. For all , and with , we bound using (7), (8) and the semigroup property of

| (56) | ||||

This shows in particular strong continuity and uniform continuity . To prove it remains to prove strong continuity and for this we have by the strong continuity (8) of for

Let us continue with . We observe that for , and with that

Similarly to (49), this yields by using the semigroup property of and (8) that

Since for , and for , , we have

Using (5) we therefore obtain

| (57) |

This implies the desired continuity on . For the continuity at zero, we use (7) to see that

and as a consequence . We conclude that . The proof of is similar and therefore omitted. In conclusion we have shown that the fixed point map is well-defined.

It remains to prove the contraction property (45). For the same arguments as in the proof of [4, Theorem 2.9] imply that for all

Combining this with (53) implies the existence of and such that

We have therefore shown that is a contraction with respect to the -norm for sufficiently large . The Banach fixed point theorem guarantees the existence and uniqueness of a fixed point to the mapping . This is the unique mild solution to (19). To prove that we consider , which is a Banach subspace of since is a closed subspace of , along with the restriction of the fixed point map to . It is a contraction with the same -norm as . One easily checks that is self-adjoint for self-adjoint and thus is well-defined. Therefore, a second application of the Banach fixed point theorem yields a unique such that . Since and is unique, and thus . Moreover, Theorem 3.6 in the end of this section shows that and we stress that none of the proofs of Theorem 3.2, Propositions 3.3–3.4, Lemma 3.5 leading to Theorem 3.6 relies on the positivity of . The bounds (46), (50) and (54) imply (i). The bounds (56), (57) imply the Hölder regularity stated in (ii).

A.2. Proof of Theorem 3.2

We write and let be a mild solution, i.e., satisfies (19). Since for all , ,

we obtain for and

Therefore, for

and subtracting on both sides and dividing by gives

The semigroup is strongly differentiable, hence weakly differentiable with derivative for . In the limit as , we obtain, by the Lebesgue differentiation theorem, the weak form (2). This completes the first direction of the proof.

Assume next that the operator-valued function satisfies for , the variational equation (2). Using (6) we bound

with , . Since we conclude that

By the Riesz representation theorem, there exists satisfying

for and Using now the specific test functions and in the variational formulation (2) yields

By the product rule,

and therefore, integration from to yields

Since this identity holds for all , the mild form of the Lyapunov equation (19) is satisfied for all . Due to the density of , we can approximate any by a sequence in and obtain convergence of the above identity, i.e., it can be extended to elements in .

Appendix B Rational approximation of semigroups

For completeness we include here a result on the error resulting from a rational approximation of a semigroup. This is (17) in the main part of the paper. To the best of our knowledge, it is not available in the literature, but the proof is similar to those of [35, Theorems 7.1-7.2].

Proposition B.1.

Let be a densely defined, linear, self-adjoint and positive definite operator with a compact inverse on a separable Hilbert space , let be the analytic semigroup generated by , let the function be given by and let . With and , there exists for all a constant , not depending on , such that for all

Proof.

First we introduce the notation so that . The bound of the theorem can then be written as

and since diagonalizes with respect to the eigenbasis of , the claim of the theorem is equivalent to the existence of a constant such that

for all , where denotes the spectrum of .

We next consider the case . Due to the definition of , there exist constants and such that, for , and . Using these bounds we get for

In the last step, we have used the fact that the mapping is bounded on .

Next, we assume that and note that then

By inspecting the derivatives of the mappings and we see that as long as , they map into and respectively on . Pick such that . Then

for and the proof is finished. ∎