Adaptive Pricing in Insurance: Generalized Linear Models and Gaussian Process Regression Approaches

Abstract

We study the application of dynamic pricing to insurance. We view this as an online revenue management problem where the insurance company looks to set prices to optimize the long-run revenue from selling a new insurance product. We develop two pricing models: an adaptive Generalized Linear Model (GLM) and an adaptive Gaussian Process (GP) regression model. Both balance between exploration, where we choose prices in order to learn the distribution of demands & claims for the insurance product, and exploitation, where we myopically choose the best price from the information gathered so far. The performance of the pricing policies is measured in terms of regret: the expected revenue loss caused by not using the optimal price. As is commonplace in insurance, we model demand and claims by GLMs. In our adaptive GLM design, we use the maximum quasi-likelihood estimation (MQLE) to estimate the unknown parameters. We show that, if prices are chosen with suitably decreasing variability, the MQLE parameters eventually exist and converge to the correct values, which in turn implies that the sequence of chosen prices will also converge to the optimal price. In the adaptive GP regression model, we sample demand and claims from Gaussian Processes and then choose selling prices by the upper confidence bound rule. We also analyze these GLM and GP pricing algorithms with delayed claims. Although similar results exist in other domains, this is among the first works to consider dynamic pricing problems in the field of insurance. We also believe this is the first work to consider Gaussian Process regression in the context of insurance pricing. These initial findings suggest that online machine learning algorithms could be a fruitful area of future investigation and application in insurance.

JEL classification: C44, C61, G22

keywords:

Learning-pricing; Regret; Generalized Linear Models; Gaussian Processes Regression; Delayed claimsurl]https://sites.google.com/site/neilwaltonswebsite/

1 Introduction

We study the application of dynamic pricing from the perspective of an insurance company. Here the insurance company looks to set prices to optimize the long-run revenue from selling insurance products which also experience a distribution of claims. This can be cast as a revenue management problem, see Philips [1] and Talluri and Ryzin [2] for an overview of this field. If the distribution of demand and claims was known to the insurance company, then this could be formulated as a relatively straight-forward optimization problem. However, in the real world, demand for a new product at each price is not deterministic and known. Thus, we assume that the insurance company only observes the realised demand and does not know the underlying distribution of demand and claims for the insurance product. This is particular relevant for the release of new insurance products.

Given demand and claims are not known, the retailer faces a learning & pricing problem. This is sometimes known as a exploration-exploitation trade-off. At the beginning of each selling period, we set a price close to the estimated best price and then study the changes of demand and claims when varying prices. This is the exploration process, which enables us to find the relationship between price and demand & claims distributions. Further by setting the price close to the estimated best price, we are able to exploit what we have learned. This is the exploitation process. Choosing prices that are far from the best estimated price encourages exploration but can be inefficient in exploiting available information. On the other hand, choosing pricing close to the best estimate price may not discover enough about the underlying distribution of claims to converge to the optimal price. Therefore, the insurance company must create a policy for pricing the insurance product that reveals sufficient information about the underlying demand and claims distributions so as to optimize the long-run revenue of the insurance company. The policy that we consider provides a mechanism for efficiently exploring different prices offering, and then exploiting that knowledge to achieve the revenue maximization objective.

We consider this pricing problem as a multi-armed bandit problem, which has been widely used to address the trade-off between exploration and exploitation in sequential decision making. We investigate two regression models for the learning & pricing problem: the Generalized Linear Models (GLM) and the Gaussian Process (GP). GLMs are a classical statistical technique, introduced by Nelder and Wedderburn [3], and was first applied in insurance rating by McCullagh and Nedler [4]. However, for sequential decision making, prices derived from maximum likelihood estimates may not be consistent due to insufficient exploration [5]. To solve this problem, the strong consistency of least squares estimates is required, which is established by Lai and Robbins [6, 7] and further generalized by Lai and Wei [8]. This analysis is a crucial step in the field of online estimation and optimization. Lai [9] gives a comprehensive survey of several related developments and discussions. Its application to revenue management is given by den Boer and Zwart [10], in which bounds on cumulative regrets are analyzed as a measure of performance. Here, regret is defined to be the difference between the expected revenue and the optimal revenue. We develop these models for the setting of insurance where there are both demand and claims. We, then, consider a second approach to this problem based on a Bayesian optimization. It was proposed by Mockus [11, 12] for optimizing an unknown function using a Gaussian Process. A Gaussian Process is a generalization of the Gaussian probability distribution, where random variables are modelled by stochastic processes. Over the last two decades, GPs have been widely used in machine learning. We investigate the upper-confidence bound (UCB) approach taken by Srinivas et al. [13, 14]. By maximizing the UCB aquisition function, we can determine the price at each time period. For more details on Gaussian Process regression and Bayesian optimization in general, we refer to Rasmussen and Williams [15] and Brochu [16].

In a summary, the contributions of this work are as follows:

-

1.

We address the dynamic pricing problem with unknown demand & claims by adaptive Generalized Linear Models and Gaussian Process regression approaches. To the best of our knowledge this paper is the first to consider online learning in the context of insurance pricing.

-

2.

In the GLM setting, based on den Boer and Zwart [10], we extend the pricing algorithm to insurance pricing by subtracting heavy-tail distributed claims.

-

3.

In the GP setting, we follow Srinivas et al. [13] for Bayesian optimization. GP with an alternative UCB function and additive kernel is applied to select the optimal price.

-

4.

We use cumulative regret to measure the performance of our algorithms, named GLM pricing algorithm and GP pricing algorithm. These have the following bounds:

-

I

The GLM pricing algorithm can achieve regret ,

-

II

The GP pricing algorithm has regret .

Here, is the length of the selling horizon and is maximum information that the algorithm could learn about the demand and total claims functions.

-

I

-

5.

By our analysis, we show that these two mechanisms are simple, implementable and have good performance.

Dynamic pricing and online learning have been successfully applied in a variety of industries such as airline ticketing, hotel bookings, car rentals, and fashion. However, to the best of our knowledge, online learning has not been applied to insurance pricing in any literature. Thus, motivated by the powerful machine learning techniques and the growing applicability insurance industry, this paper is among the first to investigate these methods to address problems in insurance pricing. As insurance increasingly sold online and with insurance products continually changing, we believe that these methods will be important for actuaries now and in the future [17].

1.1 Related Literature

In this section, we provide a brief review of insurance pricing and dynamic pricing. We also highlight related work on applying online learning to two statistical models: Generalized Linear Models and Gaussian Processes. Finally, we discuss the previous work on revenue management with uncertainty.

Insurance Pricing and Dynamic Pricing

Many researchers such as Bühlmann [18], McClenahan [19], Jong and Heller [20] point out that mathematical and statistical methods are needed to support actuaries to make pricing decisions. The linear models have been applied extensively in actuarial work. For example, early literature uses linear models in motor insurance, see Baxter [21] and Coutts [22]. In 1960, Bailey and Simon [23] introduce the minimum bias technique in classification ratemaking, which is an important milestone in non-life insurance pricing development [24]. In the 1980s, British actuaries introduced GLMs to insurance pricing and this has now become a standard approach in many countries [25]. A good overview of the use of GLMs in different situations in actuarial work is available in Haberman and Renshaw [26]; for further research applying GLMs in insurance pricing see [20, 25, 27, 28]. In the last few years, the non-life insurance market has changed due to the increase of online services. Machine learning techniques have become more popular in applications in the insurance sector. These enhance and supplement the standard GLMs analysis. We refer to Wüthrich and Buser [29] for an overview and insight into GLMs and machine learning methods in non-life insurance pricing.

Dynamic pricing is the study of how demand responds to prices in a changing environment. In recent decades, interest in dynamic pricing has grown rapidly. Early profit optimization problems assume sellers have complete knowledge of the market, which means demand functions are known or can be found from previous selling experience. Evans [30, 31] is one of the first to propose a dynamic pricing model by adding time derivatives of prices to a static model. Greenleaf [32] numerically shows the significant effects of reference prices and develops an optimal dynamic pricing strategy in a monopoly setting. Kopalle et al. [33] analytically generalize these results to a duopoly and an oligopoly settings. Following this, Fibich et al. [34] then calculate explicitly the optimal pricing strategy in various nonsmooth optimization problems. All of these works assume the demand function of consumers is deterministic and known. Surveys by Aviv and Vulcano [35] and den Boer [36] provide an excellent overview of this area.

Adaptive Generalized Linear Models

Nelder and Wedderburn [3] first introduce Generalized Linear Models (GLM), which is an extension to classical linear regression. As discussed above, it has become a well-established and standardised statistical technique to price the insurance products [25, 37]. In the GLM framework, maximum likelihood estimation is a commonly used technique to find the parameters of a given Generalized Linear Models. Wedderburn [38] proposes a method named quasi-likelihood estimation, an extension of likelihood estimations but only the first two moments of the observations are needed. McCullagh and Nedler [4] then apply GLMs with quasi-likelihood estimation to insurance ratemaking. They fit a GLM to different types of data, including average claim costs for a motor insurance portfolio and claims frequency for marine insurance.

To price products, often a certainty equivalence rule is used. Here the optimal price is chosen for the estimated parameters. Thus when optimizing we treat estimates as if they were the true (unknown) parameters of the model. Anderson and Taylor [39] apply a certainty equivalence rule to solve a multiperiod control problem. However, strong consistency may not hold when applying a certainty equivalence rule to maximum quasi-likelihood estimates [7, 9]. To deal with this problem, conditions are proposed to ensure the strong consistency for parameters estimators [5, 40]. Lai and Robbins [6] introduce further conditions for an adaptive design, and Lai and Wei [8] generalize these conditions to multiple regression models with errors given by a martingale difference sequence. Chen et al. [41] extend the results of [8, 40] to GLMs under both fixed and adaptive designs.

Multi-armed Bandits and Bayesian Optimization

A multi-arm bandit problem refers to a broad class of sequential decision making problems. At each time step, one must choose an arm amoungst a set of arms, each of which has unknown rewards. There is a trade-off between exploration, i.e. estimating the distribution of rewards for all arms in the past, and exploitation, i.e. choosing the arm with higher expected reward. Bubeck and Cesa-Bianchi [42] present a comprehensive review of work on multi-armed bandit problems. In multi-armed bandits problem, the upper confidence bound (UCB) rule is commonly used to select arms at each time period. The UCB algorithm constructs a confidence interval for the mean of each arm, and then chooses the arm that maximizes revenue under this estimation. The UCB strategy is introduced by Auer et al. [43] to address a specific bandit model, and is used for asymptotic analysis of regret as first discussed in Lai and Robbins [44]. Regret bounds for multi-armed bandits problems have attracted a great deal of interest in different cases, such as linear models [45, 46], Generalized Linear Models [47], Lipschitz functions [48, 49], Gaussian Process [13] and Thompson Sampling [50, 51, 52]. In the insurance context, each price is an “arm” and its revenue is the “reward”.

Bayesian optimization [53] provides an efficient approach to address global optimization of an unknown potentially random or noisy function. It is applicable and efficient when objective functions are unknown or are expensive to evaluate. There are two significant stages in Bayesian optimization. The first stage is to learn the objective function from available samples. Bayesian optimization typically works by assuming the unknown function is sampled from a Gaussian Process (GP) [54]. The second stage is to optimize a acquisition function to determine the next sampling points for the evaluation of the objective function. High acquisition function values occur either because there is large uncertainty in the objective function (exploration) or a high prediction given by the model (exploitation). Srinivas et al. [13] consider a GP-based Bayesian optimization. In this work, the authors propose a Gaussian Process upper confidence bound (GP) algorithm, where they sample the reward function from a GP and apply a UCB algorithm to bound the regret. They achieve sublinear regret in terms of the maximum information gain, the maximum amount of informarion the algorithm could learn about the reward function. For a comprehensive review of the Bayesian optimization and its applications, we refer to Brochu et al. [16]. To the best of our knowledge this is the first paper to consider Bayesian optimization in the context of insurance.

Revenue Management with Unknown Demand

Finally we discuss developments on revenue management with uncertainties. Gallego and van Ryzin [55] introduce a single-product dynamical pricing to revenue management. Subsequent works have adapted this model to allow for unknown demand. One popular case is to consider a parametric setting, where demand can be modeled with fixed but not known parameters. Aviv and Pazgal [56] are among the first to consider model uncertainty. They derive a closed form model with a single unknown parameter and assume that the arrival of consumers follows a Poisson distribution. Harrison et al. [57] improve the learning and profit performance by a new method named the myopic Bayesian policy. Broder and Rusmevichientong [58] present a maximum-likelihood based model for the analysis of regret in dynamic pricing problems with a general parametric model. They show that in a general case, upper bound of the -period regret is . den Boer and Zwart [10] propose a controlled variance pricing policy, in which they create taboo intervals around the average of previously chosen prices to ensure sufficient price dispersion. This policy is the first to consider the parametric model with unknown demand by maximizing the quasi-likelihood estimation. They obtain an asymptotic upper bound on -period regret as , where is extremely small. This work forms the base of our insurance pricing model.

The pricing problem can also be addressed in a nonparametric way. Kleinberg and Leighton [59] provide an analysis of an online auction and introduce regret to measure of the performance of a pricing strategy. Cope [60] applies a nonparametric Bayesian approach using Dirichlet distributions as priors to achieve a revenue-maximizing goal in an e-commerce market. Rusmevichientong et al. [61] develop a nonparametric approach to a multiproduct pricing problem based on a real automobile data set. Besbes and Zeevi [62, 63] use blind pricing policies to balance exploration-exploitation trade-offs and achieves asymptotically optimal.

Bandit Online Learning Problem

Traditionally, delays can be considered as a fixed constant. Under this setting, Dudik et al. [64] provide an efficient algorithm for stochastic contextual bandits and show that regret is additive. Chapelle and Li [65] present the influence of delayed feedback for contextual bandits in news article recommendation. Cesa–Bianchi et al. [66] study networks of nonstochastic bandits. Pike-Burke et al. [67] discuss the case with delayed, aggregated anonymous feedback and the expected delay is known. They assume only the sum of regret is available while individual regret is unknown. In general, delays may be a stochastic process. Agarwal and Duchi [68] analyze stochastic gradient-based optimization algorithms when delays are i.i.d randomly distributed. Desautels et al. [69] study parallel experiments with a bounded delay between an experiment and observation in a Gaussian Process bandit problems. Vernade et al. [70] consider infinite stochastic delays where some feedback can not be observed after a threshold. For a systematic study of online learning with delayed feedback and the effects of delay on regret, we refer to Joulani et al. [71]. In their work, they show that delays additively increases regret in stochastic problems without requiring knowledge on distributions of delays.

1.2 Organization

The sections of the paper are structured as follows. In Section 2, we describe the optimization pricing problem in the insurance setting and define our pricing models. We study GLM and GP models, as well as assumptions and estimation methods associated with each of these models. In Section 3, we propose GLM and GP pricing algorithms and explain how they work, respectively. The main result of this paper is presented in Section 4. We consider bounds on cumulative regret, which help to measure the performance of each pricing policy. In Section 5, we extend both models with unknown delayed claims. Section 6 illustrates an experimental set-up and numerical results . Finally, a conclusion and discussion of future work are provided in Section 7. Auxiliary results and proofs are gathered in the Appendix.

2 Models and Assumptions

In this section, we introduce two regression models and important assumptions. We give a brief overview of the insurance pricing problem in Section 2.1. In Section 2.2, we discuss an adaptive Generalized Linear Model (GLM), which is an parametric model, and explain how to estimate unknown parameters by quasi-likelihood estimation. This model is built on ideas of den Boer and Zwart [10], and Lai and Wei [8]. In Section 2.3, we introduce an adaptive Gaussian Process (GP) model with an UCB rule.

2.1 Overview

We consider an insurance company which sells a single product over a selling horizon . The selling price is determined at the beginning of each time period . We define the set of acceptable prices by , where are the minimum and maximum selling prices.

We assume that dynamic pricing is only associated with past prices. Given a determined selling price at time period , the insurance company observes demand , which is independent realisations of the random demand function for the selling price . Similarly, we denote the total claims as during the time period and observe the total claims . (Often we will suppress the sub-script from i.i.d. random variables and .)

In insurance, the premium is the expected income that the insurance company earns and claims are the amount that the insurance company loses. If the selling price is known, the revenue collected in a single time period is . The expected revenue at time is given by

| (2.1) |

Both demand and total claims respond to changes in prices at each time period simultaneously. Once the price is specified, we assume the demand and total claims are independent of each other. The insurance company aims to find an optimal pricing policy that generates maximum revenue, based on previous selling prices and observations . We use cumulative regret to measure the performance of pricing policies. The regret is the expected revenue loss caused by not using the optimal price. More formally, we define the cumulative regret over time horizon as

| (2.2) |

Here, is the revenue generated by the optimal price :

| (2.3) |

The objective of the seller is to maximize the sum of revenue, that is, to minimize the cumulative regret.

2.2 Generalized Linear Pricing Model

We first consider the dynamic optimization pricing problem in a GLM setting. Here the expected revenue can not be calculated directly because it depends on unknown parameters that must be inferred. We apply the maximum quasi-likelihood estimation (MQLE) to estimate the unknown parameters in the model. We are concerned about the strong consistency for MQLE of regression parameters in the Generalized Linear Models (GLMs).

Our model is based on the work of den Boer and Zwart [10]. However, we consider a single insurance product with demand and heavy-tailed claims claims. Here, we use the log of claims to describe large insurance claims.

2.2.1 Model and Assumptions

We assume that the insurance company knows the functional forms of the first two moments of demand and claims. The model for demand distribution at time is given by

Similarly, we assume the log of total claims is with expectation and variance, given by

Here, parameters and are all unknown. Notice here that we take the logarithm of total claims which is slightly non-standard when compared with results in revenue management. In the context of insurance this can be used to model heavy-tailed claims distributions, such as the log-normal distribution.

We consider functions are known link functions of price and unknown parameters. The variance functions are the variance of the expected demand & claims. The variances of the randomly distributed demand & claims are functions of the variance functions with constants . Functions and are twice continuously differentiable with first and second derivatives denoted by and , respectively. The link function is called a canonical link function when , otherwise it is called a general link function.

Denote and , the expected revenue in (2.1) can be written as

Moreover, the cumulative regret in (5.1) after time periods becomes

Here, the optimal price is defined in (2.3).

Finally, we define the design matrix to be the sum of the transpose matrices achieved from price vectors for . For , the design matrix is given by

We denote the largest eigenvalue of the design matrix as and denote the smallest eigenvalue as .

2.2.2 Estimation of unknown parameters

The optimal policy cannot be calculated directly because regret depends on unknown parameters . To simplify the notations, we define parameter matrix as . And we use to denote the true values of regression parameter . The maximum quasi-likelihood estimators, denoted by , are solutions to

| (2.4) |

Let the filtration be generated by for each . Write . The error terms form a martingale difference sequence w.r.t. , that is, is -measurable and . We also assume that for some almost surely,

-

1.

-

2.

2.3 Gaussian Process Pricing Model

Now, we construct a Bayesian model by sampling the expected demand and expected total claims from Gaussian Processes (GP). Our pricing model is an extension of Srinivas et al.’s [13] with an alternative UCB rule to the field of insurance where demands and claims are considered.

First, we offer a brief introduction of Gaussian Process regression and more complete details can be found in Rasmussen and Williams [15]. A Gaussian Process is a collection of random variables, any finite number of which have a joint Gaussian distribution. It is completely specified by its mean function and covariance function (or kernel) given by

Then, we can generate a Gaussian Process as

Without loss of generality, we assume that mean is a constant and covariance function is strictly bounded.

For a noisy sample , given a collection of input points . We define as the -th sample and , here is independent and identically distributed Gaussian noise with variance . As Gaussian Process can describe a distribution over functions, we use as the prior distribution over . The posterior over is also a GP distribution with mean and covariance function given by

| (2.5) | ||||

where and covariance matrix is the positive definite matrix whose entries are for .

The kernel determines how observations influence the prediction of nearby or similarity inputs. There are two commonly used kernels: the squared exponential kernel and the Matérn kernel , given by

Here, is the length-scale and is the smoothness parameter. Moreover, is the Gamma function and is the modified Bessel function of the second kind of order . Note that the Matérn kernel reduces to the exponential kernel when the smoothness parameter and reduces to the squared exponential kernel when .

We define the function of expected demand at price as , and similarly define the expected claims as . Functions are independently sampled from GPs with known means and kernels . That is, and . The posteriors over and are GPs and also follow GP posterior update in (2.5).

The expected revenue function given a determined price at time is

Here, the noise term is a combination of demand noise and claims noise.

We can see that is sampled from a GP as well, with an additive kernel. This is because the sum of GPs is also a GP, and the kernel has the form of a direct sum. Then, we have with known and . The cumulative regret over time horizon becomes

Our model is an extension of Srinivas et al.’s [13] work to the field of insurance. Srinivas et al. [13] study a only one function . In our case, we consider an additive form, that is the revenue function contains two components: and and is sampled with an additive kernel. Here, the samplings of and are independent of each other.

3 Pricing Policy

In this section, we propose two algorithms called “GLM Pricing Algorithm” and “GP Pricing Algorithm” in Section 3.1 and Section 3.2, respectively.

A popular pricing policy is certainty equivalent pricing, proposed by Anderson and Taylor in a simple linear regression model [39] and further developed by the authors in a more general multiple regression model [72]. We denote the certainty equivalent price by . It is efficient provided current parameter estimates are correct. Given MQLE , is the price that maximizes the expected revenue, given by

| (3.1) |

Certainty equivalent pricing is popular, essentially because it separates the statistical problem from the problem of optimizing revenue and reward. However, it is possible that parameter estimates converge to incorrect values due to convergence being too quick. Specifically, Lai and Robbin [7, Section 2] prove that inconsistency may occur for a linear demand function with constant variance under an iterative least squared policy. den Boer and Zwart [10] further relax the assumptions on the values of prices and propose a variant certainty equivalent pricing: controlled variance pricing policy. By creating taboo intervals around mean prices that have been chosen, they choose the next price outside these intervals to obtain more information. Keskin and Zeevi [73] also point out that the certainty equivalent pricing has poor performance of due to the existence of “uninformative” price and therefore introduce a constrained iterative least squared policy.

3.1 Adaptive GLM Pricing

Based on the work of den Boer and Zwart [10], we propose a dynamic pricing policy with an additional constraint on the smallest eigenvalue of the design matrix with the aim to control the convergence of the pricing policy. If we ensure a lower bound on , we can say that there is sufficient price dispersion guaranteeing the strong convergence of the MQLE. However, there is no simple explicit relation between and . We introduce the inverse of the trace of the inverse design matrix . For any positive definite matrix , we have .

Let be associated unit eigenvectors, which are an orthonormal basis of . For , the optimal price can be written as a linear combination of these unit eigenvectors, that is .

Let be a class of positive differentiable monotone increasing functions such that and is convex. Choose a function , and let for all , then we have

A proper choice of function guarantees sufficient price dispersion, and therefore, guarantees the convergence of parameter estimates to the true parameters, as well as the asymptotical convergence of our price sequence to the optimal price. Specifically, we present the optimal regret bounds when for some .

Now, we show how the pricing algorithm works. First, we choose three linearly independent initial price vectors to estimate the unknown parameters by (2.4). If the MQLE does not exist or the constraint on the price dispersion is not met, we repeat previous prices until we can find solutions of to the MQLE and satisfy the sufficient price dispersion requirement as shown in (1) in Algorithm 1. Condition will eventually be met because is always finite. If the MQLE exist and the constraint on the price dispersion is also satisfied, we set the next price to be the certainty equivalent price , and check whether the condition in (2) in Algorithm 1 holds or not. If it does not hold, we then choose . Here,

| (3.2) |

and is the first component of . Constant must satisfy . These pricing steps are given in Algorithm 1.

-

1.

If does not exist or , then set , here is the smallest integer satisfies .

-

2.

If exists and , then we set and consider

If it does not hold, we instead set and is defined in (3.2). Here we can choose , such that the above requirement is satisfied.

The following proposition guarantees that when prices are chosen, the price dispersion condition (3.3) is satisfied.

Proposition 3.1.

If exists and , we set the next price to be , then

| (3.3) |

3.2 Adaptive GP Pricing Model

In the GP setting, we determine our pricing policy by the upper confidence bound (UCB) rule. We start by reviewing Srinivas et al.’s work [13], where the posterior GP is used to construct a UCB function. At each time step , they set the next sampling point to be the one that maximizes the UCB function, given by

Here, the posterior mean is obtained after observations and is the current estimate of . The posterior standard deviation is the uncertainty associated with this estimate. Term is the explicit exploitation on what we have known and is the exploration on what we haven’t known. Parameter is used to balance the trade-off between exploitation and exploration .

In our work, we update the UCB function with additive mean and kernels, defined by

Here,

| (3.4) | ||||

Now, we present the implementation of GP algorithm for pricing. At time , the algorithm generates a price that maximizes the UCB function, which is the optimal price . Each price is determined by the history and the policy followed by the UCB rule. In the continuous price set, the optimal price exists and is unique. Then, we set the optimal price to be the next sampling price . Given the price , we sample and individually. Since the revenue is determined by two parts: premium and total claims and chosen price can be considered as a constant, the sampled revenue is a linear combination of sampled functions and . Therefore, we can obtain the sampled revenue function. Next, we perform the GP posterior update (2.5) to obtain posterior distributions for demand and total claims and update the posterior distribution of and given , respectively. Finally, we obtain the mean and standard variance defined in (3.4) and then updated the UCB function to determine the next selling price. The pseudocode for pricing a new released insurance product via GP pricing algorithm is shown in Algorithm 2.

-

1.

and by performing the GP posterior update (2.5) ;

and by performing the GP posterior update (2.5) ; 3. Obtain , ;

4 Bounds on the Regret

In this section, we show theoretical analysis obtained by proposed approaches. Our main results on cumulative regret are stated in Theorem 4.1 in Section 4.1 and Theorem 4.2 in Section 4.2, as well as proofs .

4.1 Adaptive GLM Pricing

We show the strong consistency and convergence of the maximum quasi-likelihood estimators in Generalized Linear Models (GLMs). Lai and Wei [8] study the least-squares estimate in linear stochastic regression models. Chen et al. [41] extend the results of Lai and Wei [8] to GLMs with canonical link functions. Regret bounds depend on the lower bound on the smallest eigenvalue of the design matrix and the expected value of difference between the chosen prices and optimal prices.

We will first show that studying the bound on the regret is equivalent to studying the bound on .

Proposition 4.1.

Assume there is an open, bounded neighbourhood around true , such that, for all , we can find a unique optimal price that maximizes the revenue function . Given , and , we can derive

| (4.1) |

Further, if we assume there exists such that for all , then

| (4.2) |

We focus on a simple case, where link functions are canonical, that is, . This gives

Under the Assumptions A1 and A2, we show the MQLE eventually exists and this estimator is also strongly consistent.

Proposition 4.2.

Theorem 4.1 provides an upper bound on the regret in terms of the function .

Theorem 4.1.

Suppose there exists , if MQLE is strongly consistent and following conditions are satisfied:

-

1.

a.s. for all and ,

-

2.

a.s. for all and some ,

then the regret after time periods is

Proof.

By (4.1) in Proposition 4.1, the regret over selling horizon can be derived in terms of , that is

We can expand the expectation above as following and we will explain it step by step afterwards.

here is some non-random constant . In the first inequality, we use , that is

In the second inequality, by Assumption 2 in Theorem 4.1, we bound the terms to obtain the first term

By (4.2) from Proposition 4.1, we have

This gives the second term

Finally, by Proposition 4.2 we can bound the regret by

∎

When , we find an optimal pricing strategy that achieves . The regret bound that we obtained corresponds to the results in Kleinberg and Leighton [59, Theorem 1.2] but with different algorithms.

4.2 Adaptive GP Pricing Model

We now establish cumulative regret for the Gaussian Process (GP) Bayesian optimization, which is bounded by the maximum information gain . Suppose the subset is finite. Let denote the observations and let denote the function values at these points, that is . We introduce the Shannon Mutual Information and denote it as . For a Gaussian Process, , where is the entropy. In the multivariate Gaussian case, , so that , where . After rounds, the maximum information gain between and is

| (4.3) |

The bounds on information gains depend on the kernels used. For example, under a linear regression, under a squared exponential kernel, and under a Matérn kernel with . We refer to Srinivas at al. [13] for more details. In our model, we denote the maximum information gain as , which describes the maximum amount of information that the algorithm could learn about the demand and total claims function.

Assume that both demand and total claims functions satisfy the following Assumption 4.1. It allows us to derive the bound on the cumulative regret w.r.t. the maximum information gain in Theorem 4.2.

Assumption 4.1.

Let be sampled from a GP with kernel and function is almost surely continuously differentiable. Consider partial derivatives of this sample path for satisfy the following high probability bound. For some constants ,

Theorem 4.2.

Pick and choose

With high probability and for any ,

Here is short for .

The proof follows Srinivas et al. [13]. We extend their model to the case of demands and claims. We present related lemmas and results from Srinivas et al. [13] in Appendix D.

Proof.

For any price , we consider demand and claims functions are sampled from GPs. The cumulative regret over time horizon is given by

The price set is bounded, and expected demand and claims functions are independently multivariate Gaussian distributed with bounded variances. Without loss of generality, we assume that . By the UCB rule, we can obtain the bound on regret (see Lemma 7.6 in Appendix D), given by

| (4.4) | ||||

Here, . By the convexity of logarithm function, we know for . Since and , we let and . Then we have

By Jensen’s inequality and is nondecreasing, we have

| (4.5) | ||||

here and . The last inequality is obtained by the definition of information gain (see Lemma 7.2 in Appendix D) and maximum information gain (4.3).

5 Delayed Case

In previous sections, we assume that the insurance premium and total claims are paid at the beginning of each insurance period. This gives the basic outline of how these methods can be applied in an insurance setting. However, in the real world, claims are triggered when the insured events happen, thus are not paid out when an insurance product is purchase. An immediate pricing decision during the delay may give a wrong optimal price and increase the regret. As a consequence, we involve delayed claims here and consider our pricing problem as a delayed bandit problem, based on the idea of Joulani [74].

5.1 Delayed Models

We assume that demands are generated and observed immediately when a price is chosen, while claims might be delayed. It might lead to delayed revenue. Suppose a price is chosen at time and denote the corresponding delayed time is . We assume that is an i.i.d. sequence and is independent of prices and claims. It is possible that when there is no delay. Assume there is a maximum waiting time , that the delayed claims can only be observed by time or if . Without loss of generality, we assume that all information (demands and claims) can be received by the end of time horizon .

When delay occurs, the insurance company observes revenue at time . Therefore, the next selling price is chosen based on history , which is the past information of prices and demands and delayed claims . If for all , we have .

If a price is chosen at time , we denote the claims observed at time by . The insurance company collects the set of start times for delayed claims: by the end of time . Here, the delayed time set can be for instance when or for all . The corresponding observed revenue at time is . It is worth noticing that there is less information to decide due to the delay of claims.

We denote the time that the insurance company observes the -th claim as and the corresponding revenue as , here . Let . The insurance company determines the next selling price after observing . For , we denote the number of claims observed by the end of time as . Since the company determines the next selling price by the latest observed claim, we have .

Let . Here, is the number of claims that can be observed if there is no delay. is the actual number of claims that observed by time . Therefore, is the number of delays that have not been updated when the algorithm chooses at time until the corresponding revenue can be observed. Then we have and (for a proof we refer to Lemma 7.8 in Appendix E). Hence, the regret is

We can see that the regret with delayed claims has two parts: the non-delayed regret and an additional regret caused by delayed claims. We need to bound each of these two terms to get the overall regret bound.

5.2 Adaptive GLM Pricing with Unknown Delays

In GLMs regression model without delays, we find the unknown parameters by maximizing the quasi-likelihood estimation. In the delayed case, we use a similar method. We denote the new least squares estimator of delayed claims by . Specifically is the modified MQLE given by

The following result extends Theorem 4.1 to delayed claims.

Theorem 5.1.

Suppose there exists , if MQLE is strongly consistent and following conditions are satisfied:

-

1.

a.s. for all and ,

-

2.

a.s. for all and some .

The regret bound is

Proof.

Proof is similar to Theorem 4.1. We consider the cumulative regret over selling horizon in terms of . This is

Here, the expected value of is given by

In the first inequality, we use , that is

We extend the first term in the above inequality, that is,

Here by the algorithm, we can obtain

for some . Since is an increasing concave function, by mean value theorem we have for any . It implies and

Together with Assumption 2 in Theorem 5.1 and for any (for a proof we refer to Lemma 7.9 in Appendix E), we obtain the bound on the first term in the second inequality,

for some . By Proposition 4.2, the bound on the second term is given by

Finally, the regret bound is obtained. ∎

5.3 Adaptive GP Pricing with Unknown Delays

Currently, there do not exist theoretical bound for GP with delays. In this section, we present the implementation of an alternative GP pricing algorithm for insurance in a delayed-claim setting. For example, at each time , we set a price by GP Algorithm 2 and collect the set of start times for delayed claims: . For each time , the premium can be observed at time given as , while claims are received at time . We denote the delayed claims by . After receiving the delayed claims, we update the GP for each claim and its premium. This then determines the next selling price. The pseudocode for pricing a new released insurance product with delays via GP algorithm is shown in Algorithm 3.

6 Explicit Formulas and Numerical Examples

In this section, we present the simulation result of the GLMs and GP pricing algorithms and both with delayed claims in numerical examples.

6.1 Adaptive GLM Pricing Without Delays

Assume demand follows logistics distribution and total claims follow lognormal distribution under canonical link functions. For example, let the demand and claims model be

Set three initial price vectors to be , and , with the lowest and highest price and . We now go about estimating the parameters of the above optimization.

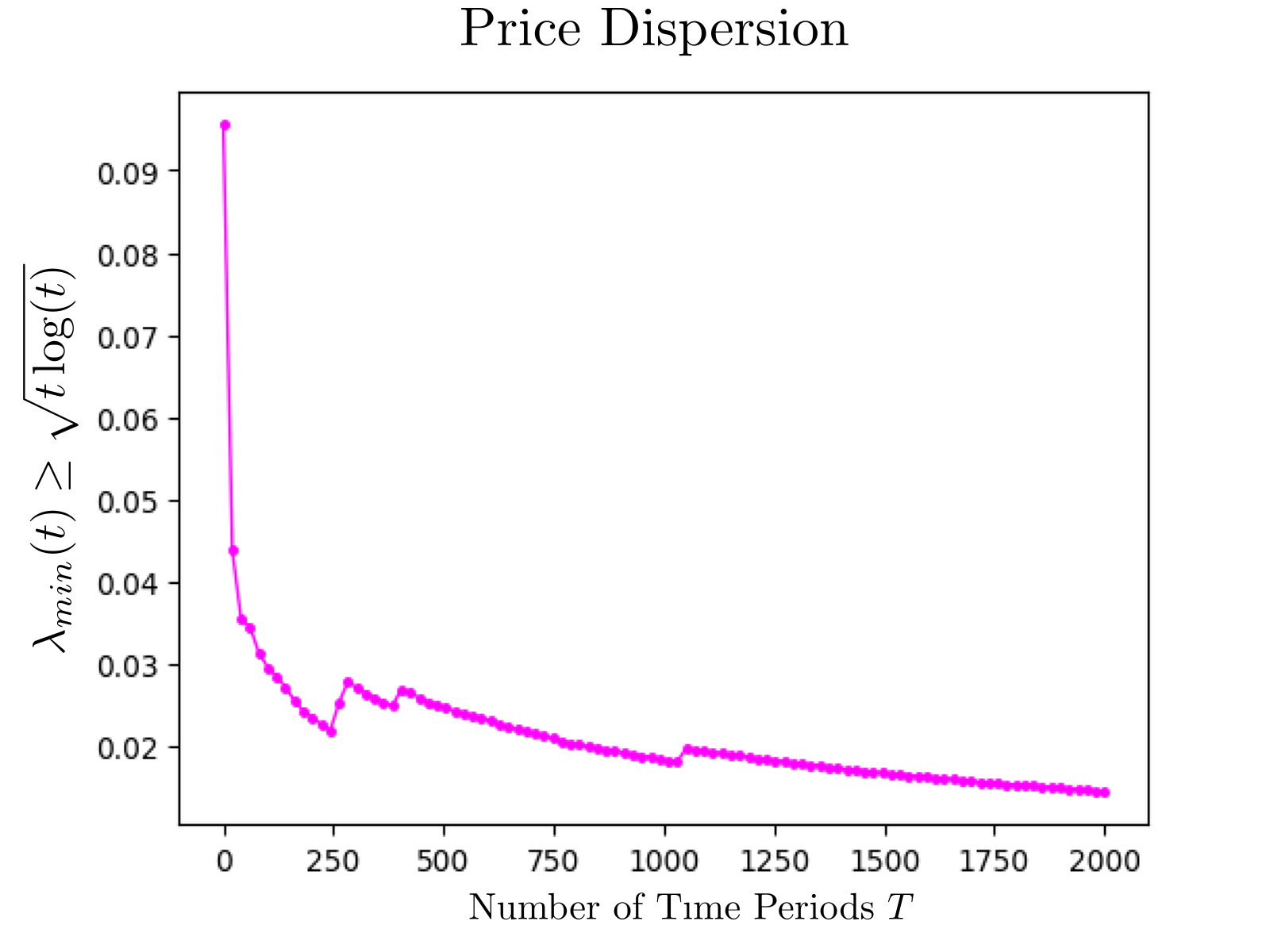

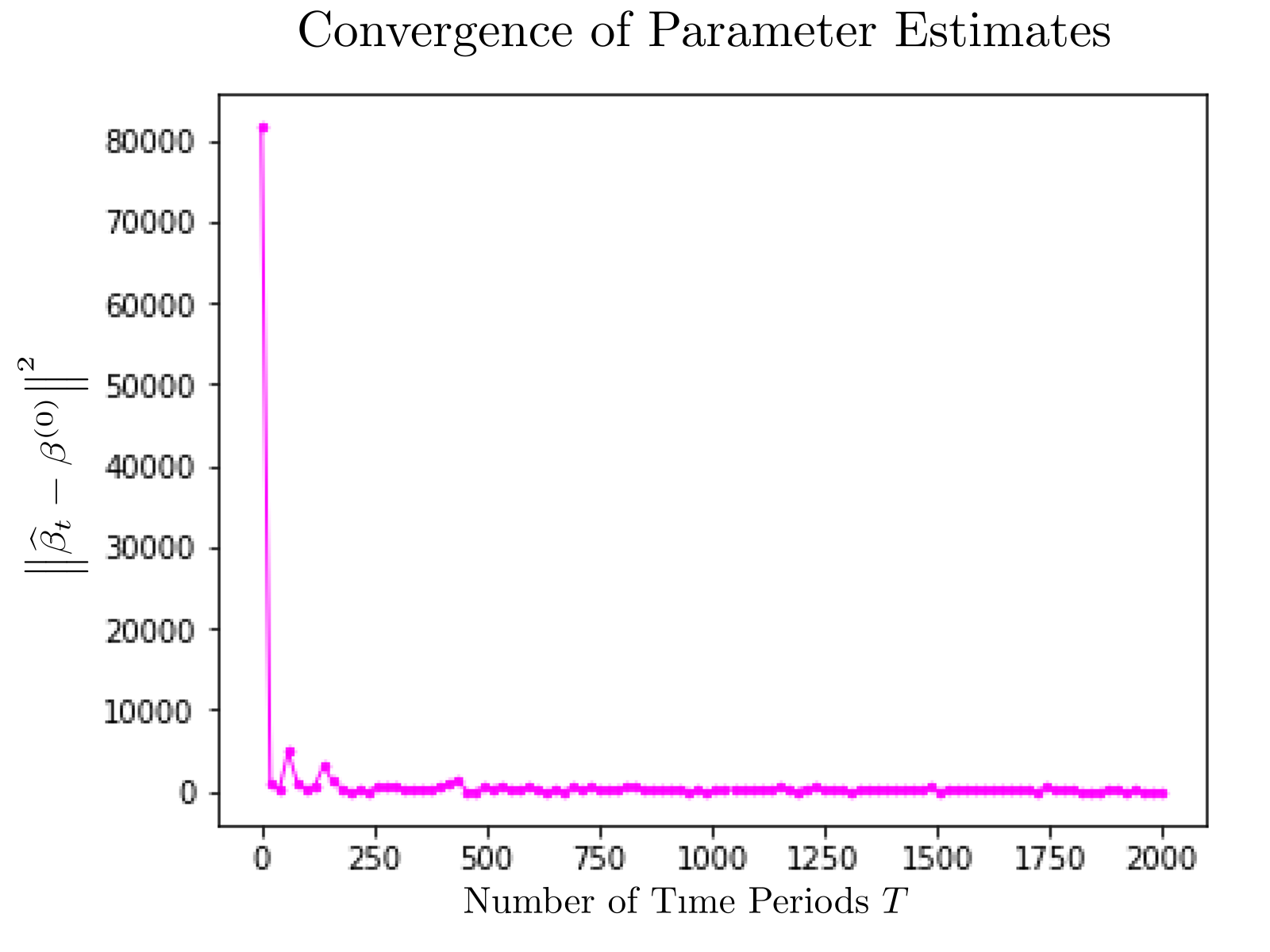

We plot price dispersion and convergence of parameter estimates. According to Figure 1(a), the price dispersion converges to 0.01. Thus, we set , which can guarantee sufficient price dispersion. Figure 1(b) presents , the squared norm of the difference between the parameter estimates and the true parameters. As , , that is, the parameter estimates converge to the true parameters. It implies the strong consistency of parameter estimates.

6.2 Adaptive GP Pricing Without Delays

The most interesting kernels for machine learning are Matérn kernels with and , given by

We sample random functions from GPs with Matérn kernels with and length scale , respectively. Set sample noise to be . The GP algorithm runs for iterations with . This indicates that our choice of the parameter depends on .

6.3 Delay cases

In order to find the effects of delays, we consider same settings as those in non-delayed cases. Delays are non-negative integers and unknown, and we generate delays randomly.

6.4 Compare GLM and GP Algorithms Without and With Delays

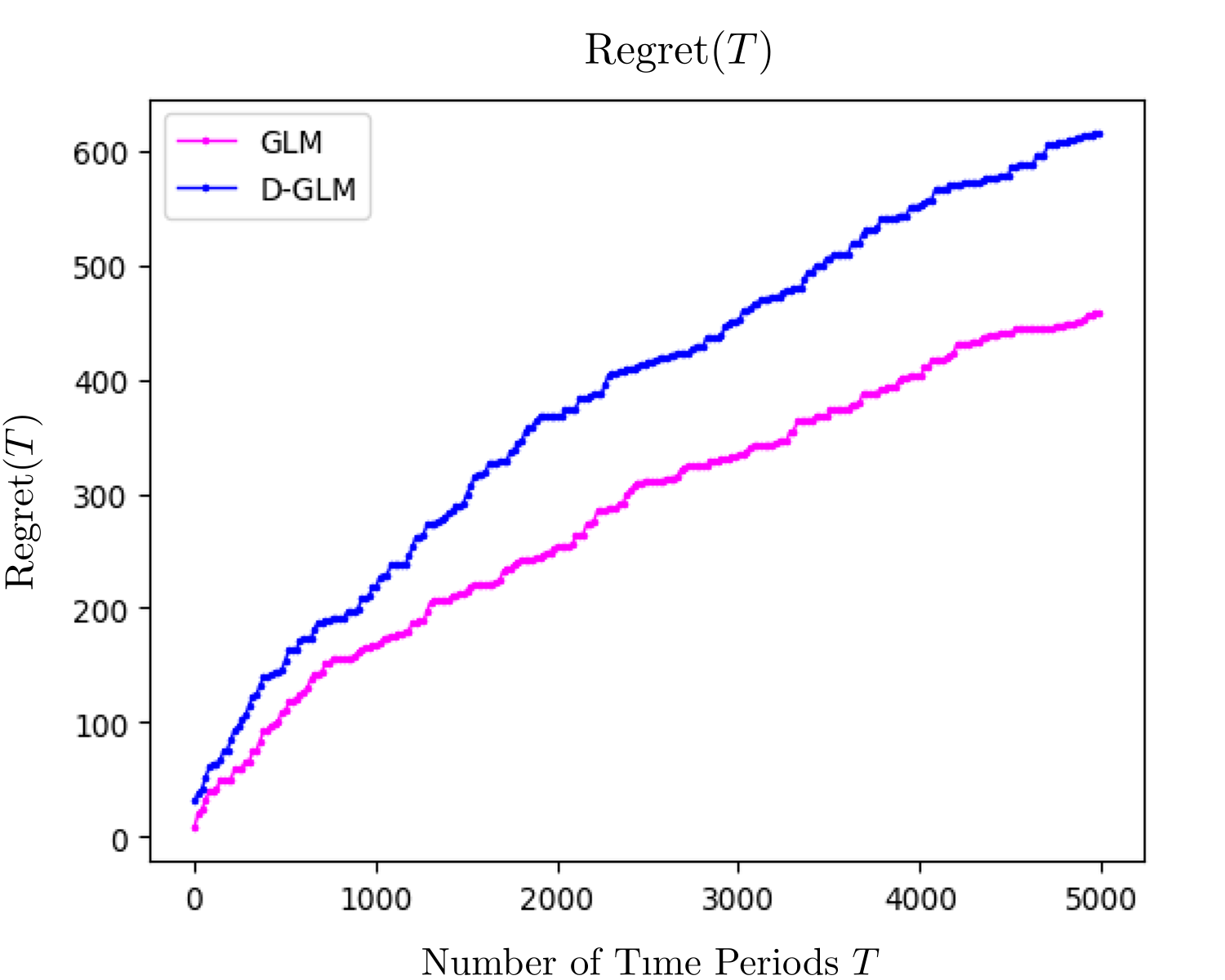

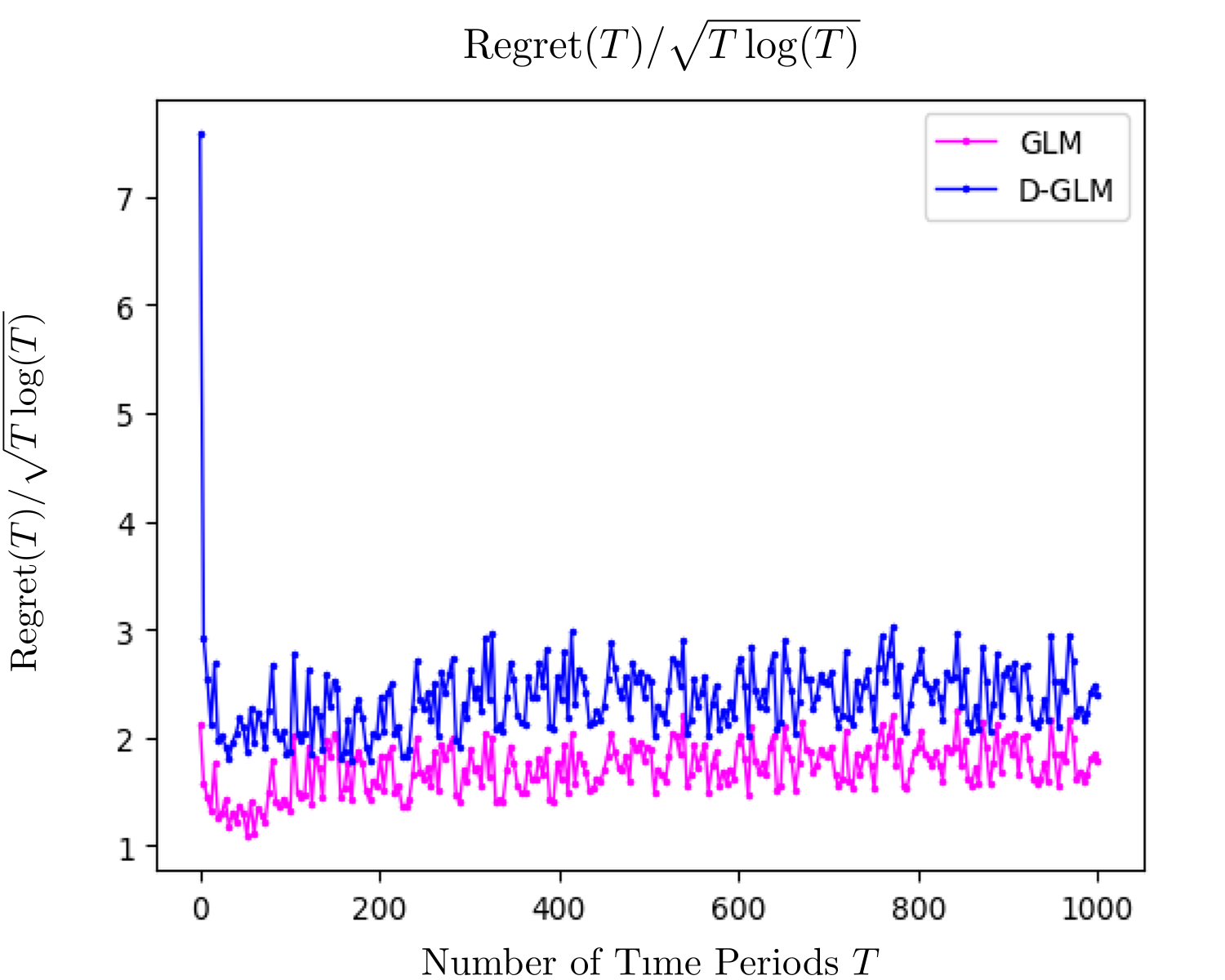

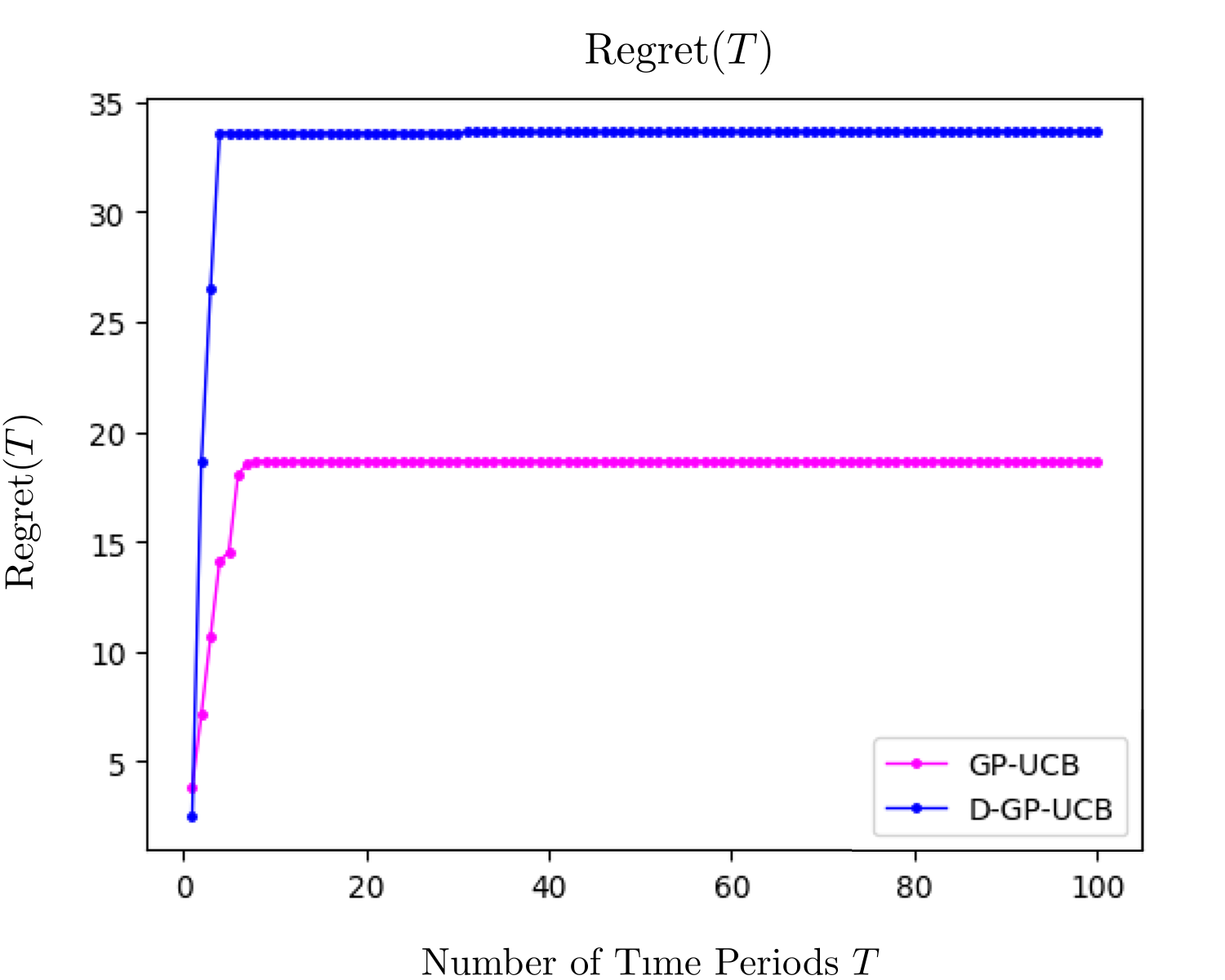

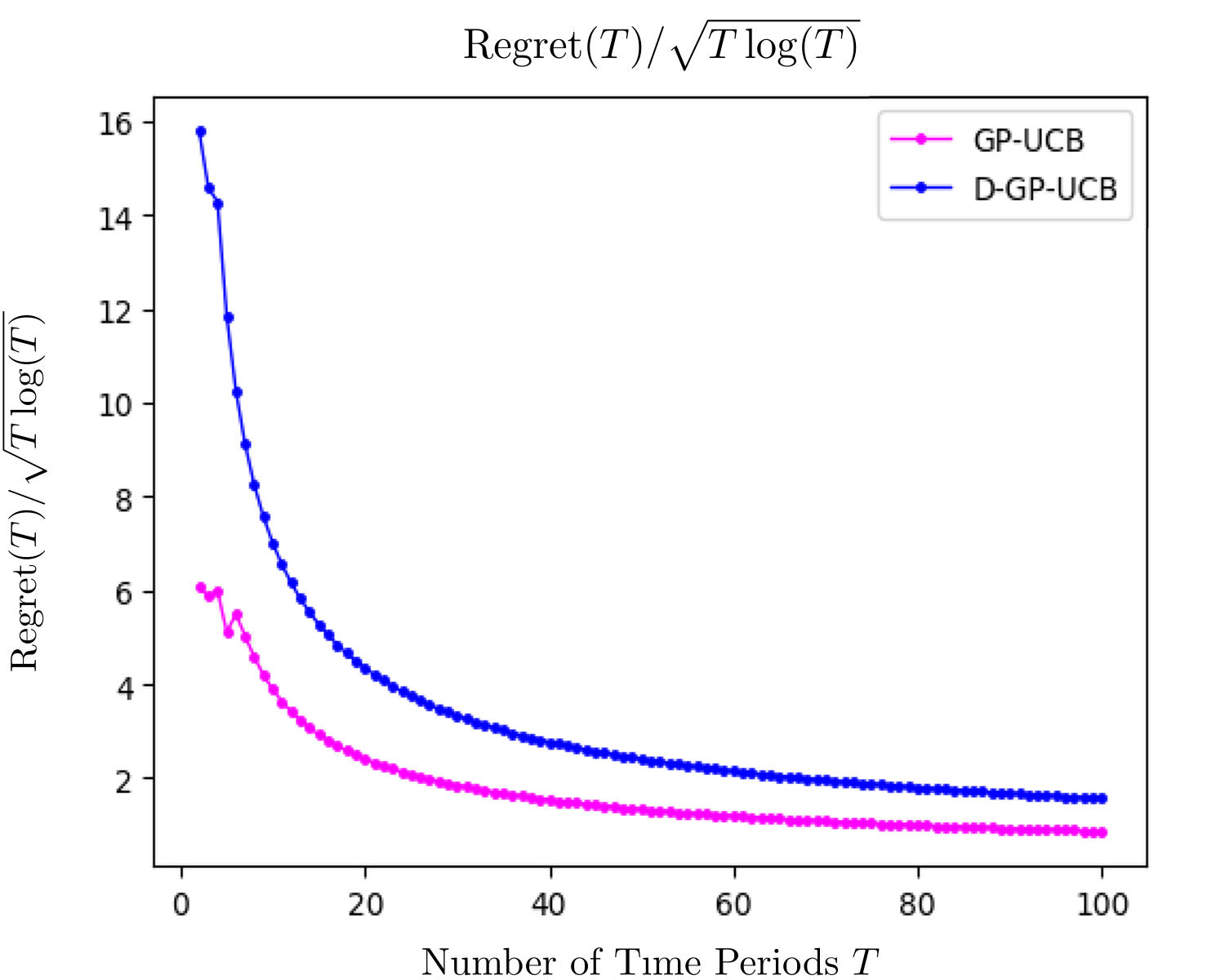

We present the numerical results in Figure 2 and Figure 3. The cumulative regret incurred by the GLM pricing algorithm is plotted in 2(a). The regret in delayed setting is always larger than that in non-delayed setting, which suggests that the insurance company suffers from an extra loss. As we mentioned above, in the delayed case, there is less information to decide selling prices due to the delay of claims. Figure 2 illustrates the regret converges at the rate of . The convergence rate of regret with delayed claims is asymptotic of the rate without delayed claims.

The results obtained by GP pricing algorithm in Figure 3 is similar to GLM pricing algorithm. 3(a) shows that regret in delayed setting is larger than the regret in non-delayed setting and 3(b) shows that convergence rate of regret with delayed and without delayed claims are asymptotic.

By comparing Figure 2(a) and Figure 3(a), we can see that the cumulative regret obtained by GP pricing algorithm converges faster and gives smaller regret. Figure 2(b) and Figure 3(b) illustrate the same results that both algorithms achieve same convergence rate, that is, . Overall, the GP pricing algorithm outperforms GLM pricing algorithm.

7 Conclusion and Discussion

We considered dynamic learning and pricing problems in an insurance context. Our work is among the first to apply online learning to insurance. We found both GLM and GP pricing models have good performance. Applying prior work to an insurance setting with both demand and claims, we demonstrate this theoretically with precise bounds on regret. In numerical results, we found GP pricing has better convergence; however, GLMs have a long history of suitable implementation in insurance. Thus it is important to also consider this setting. More broadly, our findings suggest that the new Gaussian Process regression is potentially applicable in insurance. However it is currently under studied.

Since an insurance company cannot immediately observe claims, in Section 5, we extended the GLM pricing model algorithm to have delayed claims. We prove that the asymptotic regret bound with delayed claims is the same as that achieved in the non-delayed case. The same result for the GP algorithm remains open, but numerical results suggest the same regret bound is achieved.

There are several ideas for future investigation. Thus far we focus on the long-run revenue. In the insurance market, claims may cause loss and even bankruptcy to the insurance company. One idea is to incorporate ruin probability, which is a measure for the risk used for decision taking.

Another possible idea is to implement reinforcement learning (RL) with these online revenue management problems. Bandit problems, as considered in this paper, are simple reinforcement learning routines. However, more complex future market interactions might be considered. This problem may be modeled as a Markov Decision Process (MDP). RL iteratively interacts with a simulation of the insurance model and then use the feedback from the environment to select actions that maximize the insurer’s objective. Although MDPs have been applied for many years in insurance, extending the online learning framework considered here to incorporate forward planning is an area that is yet to be studied.

Acknowledgements

This work was supported by China Scholarship Council (CSC) Grant.

Appendix

A Proof of Proposition 3.1

Recall from Algorithm 1, if exists and , we first set the next price to be . If the condition (3.3) does not hold, that is

| (7.1) |

we then choose the next price to be . We will show there exists , such that

| (7.2) |

is satisfied. By the Sherman-Morrison formula in Bartlett [75], we have

Then, we can derive

| (7.3) | ||||

The last inequality is obtained because is convex and . Now we want to prove that

| (7.4) |

Here, we discuss a general case. Let and let be the eigenvalues of , and be associated eigenvectors. Since is a symmetric positive definite matrix and are an orthonormal basis of , we can define the optimal price as a linear combination of these unit eigenvectors. Let the next price be , here is the first component of . We know that and for all . Then we have

It demonstrates that

| (7.5) |

We choose such that

| (7.6) | ||||

and

| (7.7) | ||||

We write . Since , and , we have

| (7.8) | ||||

Moreover,

| (7.9) | ||||

Since and then . Together with (7.6), we can obtain the second inequality that

Since is a symmetric positive definite matrix, we have . Given (7.1) and by the Sherman-Morrison formula, then we have

| (7.10) |

| (7.11) | ||||

Together with (7.8) and (7.11), we have

Choose and given the LHS of the above inequality, we let

Here by (7.7). Then we obtain

Due to the convexity of , there exists , such that , and

It shows that condition (7.2) holds.

B Proof of Proposition 4.1

The price vector can be written as a function in terms of given by . Since and at the optimal price , by the Taylor series expansion, we can derive

for all . Let , we have

By the definition of implicit function theorem in Duistermaat and Kolk [76], there is an open and bounded neighbourhood such that the function is continuously differentiable with bounded derivatives. Thus, for all and some non-random constant , we have

Assume there exits for all , then

This shows the upper bounds on the regret depend on the upper bounds on .

C Proof of Proposition 4.2

To prove Proposition 4.2, we need the following lemma.

Lemma 7.1.

Let be a smooth continuously differentiable injection from with . Define and . Then, implies , which gives .

Proof.

Since is a homeomorphism, we can directly derive the result based on Theorem 3.1 & Corollary 3.2 in Dugundji [77]. For any set and a homeomorphism , if is an interior boundary point of , then is an interior boundary point of . This is because by the Brouwer domain invariance theorem, for any space , the property “open in ” is a positional invariant of rel .∎

It simply tells us that for all , there is an such that . Similarly, we define a closed and bounded neighbourhood of as and .

Now, we shall start our proof of Proposition 4.2, that is to find the value of .

Proof of Proposition 4.2.

Since is not effected by , without loss of generality we assume that . A Taylor expansion of yields

for some is on the line segment between and . Thus

Under the Assumptions A1 and A2, the strong consistency for in Lai and Wei [8] holds. We define

here . Since , a.s. Write and let . If , then for all , we have

In particular, if , we have

Let with , we have = . By Lemma 7.1, we know is well defined on . Since

we obtain that exists and . Given as and is nonsingular for all large , we have,

Define . Assume and for , we let and

Apply the Sherman-Morrison formula, we obtain the recursive form of . For , we have

Let

Here, and are -measurable. Summing it, we have for ,

Here, is an extended stochastic Liapounov function if it is -measurable (Lai [9]). By the strong laws for martingale, for any , we have

The local martingale convergence theorem and the strong law of large numbers (Chow [78]) show . When , by Kronecker’s lemma and Freeman theorem [79], we have

It implies when , we have

Assume Assumption A1 and A2 hold, by Theorem 2 in Lai and Wei [8] we obtain that is strongly consistent with

Assume that holds, we have

∎

D Proof of Theorem 4.2

In this section, we present lemmas used for the proof of Theorem 4.2. This proof is based on the work of Srinivas et al. [13]. We first present the following results from [13].

Lemma 7.2.

[13, Lemma 5.3] If , the information gain in GP can be expressed as

Here, is the variance of Gaussian noise and is the posterior variance after observations.

Proof.

The Shannon Mutual Information is defined as

| (7.12) |

It quantifies the reduction in uncertainty (measured in terms of differential Shannon entropy) about from revealing . By the definition of , we have that for a Gaussian Process,

| (7.13) | ||||

We can expand as

By expanding the entropy terms, we have

| (7.14) | ||||

Substituting (7.13) and (7.14) into (7.12), we can obtain the result. ∎

The following lemma is used to obtain the finite bound on . The proof is quite involved and we refer the reader to Theorem 8 in Srinivas et al. [13].

Lemma 7.3.

We also need to establish the following lemmas before we prove Theorem 4.2. Lemma 7.4 provides a confidence bound on a finite decision set , where all decisions are chosen. Lemma 7.5 shows a confidence bound on a set of discretizations where is a general compact set.

Denote a sequence of such that .

Lemma 7.4.

Pick and set . Then with probability greater than , for any and , we have

| (7.15) |

Here, .

Proof.

Conditioned on , are deterministic and the marginals follow for any fixed and . By the following tail bound, we know for if . Let and , then

With probability greater than , we have

Given , with probability greater than , we have

Let and choose . By the union bound on all , we obtain the results. ∎

By the Assumption 4.1 and the union bound we have . Therefore, there exits , for , such that

Then with probability greater than , for all , we have

| (7.16) |

Now, consider a sequence of discretisation of cardinality that satisfies

| (7.17) |

where is a constant which is the length of price set and is the closest price to in . Let and apply (7.16). With probability greater than ,

Together with (7.17), we can derive

Choosing yields

We can now derive the bounds on regret.

Lemma 7.5.

Pick and set

Then with probability greater than , for any and , we have

| (7.18) |

Proof.

Lemma 7.6.

with probability greater than , for all , the regret is bounded by

Proof.

Lemma 7.7.

For the combination of additive kernels , we have

Proof.

For , let be the Gram matrix on for and be the Gram matrix for . We can show that

It gives that

∎

E Proof of Theorem 5.1

To prove Theorem 5.1, we need following lemmas.

Lemma 7.8.

.

Proof.

By the definition of , we have

The third equality is obtained because is a permutation of . The forth equality is derived by the definition of . ∎

Lemma 7.9.

Given a maximum waiting time and for all , we have for all .

Proof.

By the definition of , we have

In the first inequality, we use . This is because at the beginning of time , there are at least and at most claims can be observed. In the second inequality, we assume that the -th claim incurs when a price is chosen at time and then observed at time . The number of claims that observed by time is . Then the first claim that observed in time is , which is also the -th claim. It implies

Since for all , we obtain . ∎

References

References

- [1] R. L. Phillips, Pricing and revenue optimization, Stanford Business Books, Stanford, Calif., 2005.

-

[2]

K. Talluri, G. van Ryzin, The theory and

practice of revenue management, Springer, Boston, MA, 2005.

URL https://doi.org/10.1007/b139000 -

[3]

J. A. Nelder, R. W. M. Wedderburn,

Generalized linear models,

Journal of the Royal Statistical Society 135 (3) (1972) 370–384.

doi:10.2307/2344614.

URL http://www.jstor.org/stable/2344614 -

[4]

P. McCullagh, J. A. Nelder,

Generalized

Linear Models, 2nd Edition, Chapman and Hall, London, 1989.

URL http://www.utstat.toronto.edu/~brunner/oldclass/2201s11/readings/glmbook.pdf - [5] T. L. Lai, H. Robbins, Adaptive design and stochastic approximation, The Annals of Statistics 7 (6) (1979) 1196–1221. doi:10.1214/aos/1176344840.

-

[6]

T. Lai, H. Robbins, Consistency and

asymptotic efficiency of slope estimates in stochastic approximation

schemes, Z. Wahrscheinlichkeitstheorie verw. Gebiete 56 (3) (1981) 329–360.

URL https://doi.org/10.1007/BF00536178 -

[7]

T. Lai, H. Robbins,

Iterated least squares

in multiperiod control, Advances in Applied Mathematics 3 (1) (1982) 50–73.

URL https://doi.org/10.1016/S0196-8858(82)80005-5 - [8] T. L. Lai, C. Z. Wei, Least squares estimates in stochastic regression models with applications to identification and control of dynamic systems, The Annals of Statistics 10 (1) (1982) 154–166. doi:10.1214/aos/1176345697.

- [9] T. Lai, Stochastic approximation: invited paper, The Annals of Statistics 31 (2) (2003) 391–406. doi:10.1214/aos/1051027873.

-

[10]

A. Den Boer, B. Zwart,

Simultaneously learning and

optimizing using controlled variance pricing, Management Science 60 (3)

(2013) 770–783.

URL https://doi.org/10.1287/mnsc.2013.1788 - [11] J. Močkus, Bayesian Approach to Global Optimization, Mathematics and its Applications, Springer, Netherlands, 1989. doi:10.1007/978-94-009-0909-0.

- [12] J. Močkus, Bayesian approach to global optimization and application to multiobjective and constrained problems, Journal of Global Optimization 4 (4) (1994) 347–365. doi:10.1007/BF01099263.

-

[13]

N. Srinivas, A. Krause, S. M. Kakade, M. Seeger,

Gaussian process optimization in the

bandit setting: No regret and experimental design, CoRRdoi:10.1109/TIT.2011.2182033.

URL http://arxiv.org/abs/0912.3995 -

[14]

N. Srinivas, A. Krause, S. M. Kakade, M. Seeger,

Information-theoretic

regret bounds for gaussian process optimization in the bandit setting, IEEE

Transactions on Information Theory 58 (5) (2012) 389–434.

doi:10.1109/TIT.2011.2182033.

URL https://ieeexplore.ieee.org/stamp/stamp.jsp?arnumber=6138914 - [15] C. E. Rasmussen, C. K. I. Williams, Gaussian processes for machine learning, Adaptive computation and machine learning, MIT Press, Cambridge, Mass, 2006.

-

[16]

E. Brochu, V. M. Cora, N. de Freitas, A

tutorial on bayesian optimization of expensive cost functions, with

application to active user modeling and hierarchical reinforcement learning,

CoRR abs/1012.2599.

URL http://arxiv.org/abs/1012.2599 -

[17]

SwissRe,

Life

insurance in the digital age: fundamental transformation ahead, Swiss Re

Sigma Report.

URL http://www.biztositasiszemle.hu/files/201512/sigma6_2015_en.pdf - [18] H. Bühlmann, Mathematical Methods in Risk Theory, Grundlehren der mathematischen Wissenschaften, Springer-Verlag Berlin Heidelberg, 2005. doi:10.1007/978-3-540-30711-2.

- [19] C. McClenahan, Ratemaking, 4th Edition, Casualty Actuarial Society, 1984, Ch. 3, pp. 75–148.

-

[20]

P. de Jong, G. Z. Heller,

Generalized Linear

Models for Insurance Data, Cambridge University Press, Cambridge, 2008.

URL https://feb.kuleuven.be/public/u0017833/boek.pdf - [21] L. A. Baxter, S. M. Coutts, G. A. F. Ross, Applications of linear models in motor insurance, in: 21st International Congress of Actuaries, Vol. 2, Elsevier, 1980, pp. 11–29.

-

[22]

S. M. Coutts, Motor insurance

rating, an actuarial approach, Journal of the Institute of Actuaries 111 (1)

(1984) 87–148.

URL https://www.jstor.org/stable/41140673 - [23] R. A. Bailey, L. J. Simon, Two studies in automobile insurance ratemaking, ASTIN Bulletin: The Journal of the International Actuarial Association 1 (4) (1960) 192–217. doi:10.1017/S0515036100009569.

- [24] M. David, Auto insurance premium calculation using generalized linear models, Procedia Economics and Finance 20 (2015) 147–156. doi:10.1016/S2212-5671(15)00059-3.

-

[25]

E. Ohlsson, J. B.,

Non-Life

Insurance Pricing with Generalized Linear Models, Springer, Berlin,

Heidelberg, 2010.

URL https://link.springer.com/book/10.1007/978-3-642-10791-7 - [26] S. Haberman, A. E. Renshaw, Generalized linear models and actuarial science, Journal of the Royal Statistical Society 45 (4) (1996) 407–436. doi:10.2307/2988543.

- [27] R. Kaas, M. Goovaerts, J. Dhaene, M. Denuit, Modern actuarial risk theory : using R, 2nd Edition, Springer, Berlin, 2009. doi:10.1007/978-3-540-70998-5.

- [28] E. W. Frees, Regression modeling with actuarial and financial applications, International series on actuarial science, Cambridge University Press, Cambridge, 2010.

-

[29]

M. V. Wüthrich, C. Buser, Data

analytics for non-life insurance pricing, Swiss Finance Institute Research

Paper No. 16-68.

URL https://ssrn.com/abstract=2870308 -

[30]

G. C. Evans, The dynamics of

monopoly, The American Mathematical Monthly 31 (2) (1924) 77–83.

doi:10.2307/2300113.

URL http://www.jstor.org/stable/2300113 -

[31]

G. C. Evans, Mathematical

introduction to economics, McGraw-Hill, New York, 1930.

URL http://hdl.handle.net/2027/uc1.b3427705 -

[32]

E. A. Greenleaf,

The impact

of reference price effects on the profitability of price promotions,

Marketing Science 14 (1) (1995) 82–104.

doi:10.1287/mksc.14.1.82.

URL https://pubsonline.informs.org/doi/pdf/10.1287/mksc.14.1.82 -

[33]

P. Kopalle, A. Rao, J. Assuncao,

Asymmetric reference price effects

and dynamic pricing policies, Marketing Science 15 (1) (1996) 60–85.

URL http://www.jstor.org/stable/184184 -

[34]

G. Fibich, A. Gavious, Explicit

solutions of optimization models and differential games with nonsmooth

(asymmetric) reference-price effects, Operations Research 51 (5) (2003)

721–734.

URL http://www.jstor.org/stable/4132433 - [35] Y. Aviv, G. Vulcano, Dynamic list pricing, in: The Oxford handbook of pricing management, Oxford University Press, UK, 2012, Ch. 23, pp. 522–58. doi:10.1093/oxfordhb/9780199543175.013.0023.

- [36] A. Den Boer, Dynamic pricing and learning: Historical origins, current research, and new directions, Surveys in operations research and management science 20 (1) (2015) 1–18. doi:10.1016/j.sorms.2015.03.001.

-

[37]

M. V. Wüthrich, Non-life

insurance: Mathematics & statistics (2017).

URL http://dx.doi.org/10.2139/ssrn.2319328 - [38] R. W. M. Wedderburn, Quasi-likelihood functions, generalized linear models, and the gauss-newton method, Biometrika 61 (3) (1974) 439–447. doi:10.2307/2334725.

- [39] T. W. Anderson, J. B. Taylor, Strong consistency of least squares estimates in normal linear regression, The Annals of Statistics 4 (4) (1976) 788–790. doi:10.1214/aos/1176343552.

- [40] T. L. Lai, H. Robbins, C. Z. Wei, Strong consistency of least squares estimates in multiple regression, Proceedings of the National Academy of Sciences of the United States of America 75 (7) (1978) 343–361. doi:10.1016/0047-259X(79)90093-9.

- [41] K. Chen, I. Hu, Z. Ying, Strong consistency of maximum quasi-likelihood estimators in generalized linear models with fixed and adaptive designs, The Annals of Statistics 27 (4) (1999) 1155–1163. doi:10.1214/aos/1017938919.

-

[42]

S. Bubeck, N. Cesa-Bianchi, Regret

analysis of stochastic and nonstochastic multi-armed bandit problems,

Foundations and Trends® in Machine Learning 5 (1) (2012) 1–122.

doi:10.1561/2200000024.

URL http://sbubeck.com/SurveyBCB12.pdf - [43] P. Auer, N. Cesa-Bianchi, P. Fischer, Finite-time analysis of the multiarmed bandit problem, Machine Learning 47 (2-3) (2002) 235–256. doi:10.1023/A:1013689704352.

-

[44]

T. Lai, H. Robbins,

Asymptotically

efficient adaptive allocation rules, Advances in Applied Mathematics 6 (1)

(1985) 4–22.

URL http://dx.doi.org/10.1016/0196-8858(85)90002-8 -

[45]

V. Dani, T. P. Hayes, S. M. Kakade,

Stochastic linear

optimization under bandit feedback, in: 21st Annual Conference on Learning

Theory (COLT), 2008, pp. 355–366.

URL http://colt2008.cs.helsinki.fi/papers/80-Dani.pdf -

[46]

P. Rusmevichientong, J. N. Tsitsiklis,

Linearly

parameterized bandits, Mathematics of Operations Research 35 (2) (2010)

395–411.

URL https://pubsonline.informs.org/doi/pdf/10.1287/moor.1100.0446 -

[47]

S. Filippi, O. Cappe, A. Garivier, C. Szepesvári,

Parametric

bandits: The generalized linear case, in: Advances in Neural Information

Processing Systems 23 (NIPS 2010), 2010, pp. 586–594.

URL https://sites.ualberta.ca/~szepesva/papers/GenLinBandits-NIPS2010.pdf -

[48]

S. Bubeck, R. Munos, G. Stoltz, N. Cesa-Bianchi,

X-armed

bandits, Journal of Machine Learning Research 12 (2011) 1655–1695.

URL http://www.jmlr.org/papers/volume12/bubeck11a/bubeck11a.pdf -

[49]

R. Kleinberg, A. Slivkins, E. Upfal,

Multi-armed bandits in

metric spaces, in: Proceedings of the Fortieth Annual ACM Symposium on

Theory of Computing, ACM, 2008, pp. 681–690.

doi:10.1145/1374376.1374475.

URL http://doi.acm.org/10.1145/1374376.1374475 -

[50]

S. Agrawal, N. Goyal,

Analysis of

thompson sampling for the multi-armed bandit problem, in: 25th Annual

Conference on Learning Theory, Vol. 23, 2012, pp. 39.1–39.26.

URL http://proceedings.mlr.press/v23/agrawal12/agrawal12.pdf -

[51]

S. Agrawal, N. Goyal,

Further optimal regret

bounds for thompson sampling, in: 16th International Conference on

Artificial Intelligence and Statistics (AISTATS), Vol. 31, 2013, pp. 90–107.

URL http://proceedings.mlr.press/v31/agrawal13a.pdf -

[52]

D. Russo, B. Van Roy,

Learning

to optimize via posterior sampling, Mathematics of Operations Research

39 (4) (2013) 1221–1243.

URL https://pubsonline.informs.org/doi/pdf/10.1287/moor.2014.0650 - [53] J. Močkus, V. Tiesis, A. Zilinskas, On bayesian methods for seeking the extremum, in: Towards Global Optimization, 2nd Edition, Vol. 2, Elsevier Science Ltd, North Holland, Amsterdam, 1978, pp. 117–129.

-

[54]

J. Snoek, H. Larochelle, R. P. Adams,

Practical

bayesian optimization of machine learning algorithms, in: F. Pereira,

C. J. C. Burges, L. Bottou, K. Q. Weinberger (Eds.), Advances in Neural

Information Processing Systems 25, Curran Associates, Inc., 2012, pp.

2951–2959.

URL http://papers.nips.cc/paper/4522-practical-bayesian-optimization -

[55]

G. Gallego, G. Van Ryzin,

Optimal

dynamic pricing of inventories with stochastic demand over finite horizons,

Management Science 40 (8) (1994) 999–1020.

URL http://www.jstor.org.manchester.idm.oclc.org/stable/2633090 -

[56]

Y. Aviv, A. Pazgal,

A

partially observed markov decision process for dynamic pricing, Management

Science 51 (9) (2005) 1400–1416.

URL http://www.jstor.org.manchester.idm.oclc.org/stable/20110429 -

[57]

J. Harrison, N. Keskin, A. Zeevi,

Bayesian dynamic pricing

policies: Learning and earning under a binary prior distribution, Management

Science 58 (3) (2012) 570–586.

URL https://doi.org/10.1287/mnsc.1110.1426 -

[58]

J. Broder, P. Rusmevichientong,

Dynamic pricing under a

general parametric choice model, Operations Research 60 (4) (2012) 965–980.

URL http://search.proquest.com/docview/1041256005/ - [59] R. Kleinberg, T. Leighton, The value of knowing a demand curve: bounds on regret for online posted-price auctions, in: Proceedings of the 44th IEEE Symposium on Foundations of Computer Science, IEEE, USA, 2003, pp. 594–605. doi:10.1109/SFCS.2003.1238232.

- [60] E. Cope, Bayesian strategies for dynamic pricing in e-commerce, Naval Research Logistics (NRL) 54 (3) (2007) 265–281. doi:10.1002/nav.20204.

- [61] P. Rusmevichientong, B. Van Roy, P. W. Glynn, A nonparametric approach to multiproduct pricing, Operations Research 54 (1) (2006) 82–98. doi:10.1287/opre.1050.0252.

-

[62]

O. Besbes, A. Zeevi, Dynamic

pricing without knowing the demand function: Risk bounds and near-optimal

algorithms, Operations Research 57 (6) (2009) 1407–1420.

URL http://www.jstor.org/stable/25614853 -

[63]

O. Besbes, A. Zeevi,

Blind

network revenue management, Operations Research 60 (6) (2012) 1537–1550.

URL https://pubsonline.informs.org/doi/pdf/10.1287/opre.1120.1103 -

[64]

M. Dudík, D. J. Hsu, S. Kale, N. Karampatziakis, J. Langford, L. Reyzin,

T. Zhangn, Efficient

optimal learning for contextual bandits, in: Proceedings of the 27th

Conference on Uncertainty in Artificial Intelligence (UAI), 2011, pp. 1–20.

URL http://www.cs.columbia.edu/~djhsu/papers/amo.pdf -

[65]

O. Chapelle, L. Li,

An

empirical evaluation of thompson sampling, in: J. Shawe-Taylor, R. S. Zemel,

P. L. Bartlett, F. Pereira, K. Q. Weinberger (Eds.), Advances in Neural

Information Processing Systems 24, Curran Associates, Inc., 2012, pp.

2249–2257.

URL https://www.microsoft.com/en-us/research/wp-content/uploads/2016/02/thompson.pdf -

[66]

N. Cesa-Bianchi, C. Gentile, Y. Mansour, A. Minora,

Delay and

cooperation in nonstochastic bandits, Journal of Machine Learning Research

20 (17) (2016) 1–38.

URL http://www.jmlr.org/papers/volume20/17-631/17-631.pdf -

[67]

C. Pike-Burke, S. Agrawal, C. Szepesvari, S. Grunewalder,

Bandits

with delayed, aggregated anonymous feedback, in: Proceedings of Machine

Learning (ICML), Vol. 80, 2018, pp. 4105–4113.

URL http://proceedings.mlr.press/v80/pike-burke18a/pike-burke18a.pdf -

[68]

A. Agarwal, J. C. Duchi,

Distributed

delayed stochastic optimization, in: Proceedings of the 24th International

Conference on Neural Information Processing Systems (NIPS), NIPS’11, Curran

Associates Inc., USA, 2011, pp. 2312–2320.

URL https://papers.nips.cc/paper/4247-distributed-delayed-stochastic-optimization -

[69]

T. Desautels, A. Krause, J. W. Burdick,

Parallelizing

exploration-exploitation tradeoffs in gaussian process bandit optimization,

Journal of Machine Learning Research 15 (2014) 4053–4103.

URL http://jmlr.org/papers/volume15/desautels14a/desautels14a.pdf -

[70]

C. Vernade, O. Cappé, V. Perchet,

Stochastic bandit models for delayed

conversions, arXiv preprint abs/1706.09186.

arXiv:1706.09186.

URL http://arxiv.org/abs/1706.09186 -

[71]

P. Joulani, A. György, C. Szepesvári,

Online learning under

delayed feedback, in: Proceedings of the 30th International Conference on

Machine Learning (ICML), Atlanta, Georgia, USA, 2013, pp. 1453–1461.

URL http://proceedings.mlr.press/v28/joulani13.pdf - [72] T. W. Anderson, J. B. Taylor, Strong consistency of least squares estimates in dynamic models, The Annals of Statistics 7 (3) (1979) 484–489. doi:10.1214/aos/1176344670.

-

[73]

N. B. Keskin, A. Zeevi, Dynamic

pricing with an unknown demand model: Asymptotically optimal semi-myopic

policies, Operations Research 62 (5) (2014) 1142–1167.

URL https://doi.org/10.1287/opre.2014.1294 -

[74]

P. Joulani, A. György, C. Szepesvári,

Delay-tolerant

online convex optimization: Unified analysis and adaptive-gradient

algorithms, in: Proceedings of the Thirtieth AAAI Conference on Artificial

Intelligence (AAAI-16), Phoenix, Arizona, USA, 2016, pp. 1744–1750.

URL https://sites.ualberta.ca/~pooria/publications/AAAI16-Extended.pdf - [75] M. S. Bartlett, An inverse matrix adjustment arising in discriminant analysis, Annals of Mathematical Statistics 22 (1) (1951) 107–111. doi:10.1214/aoms/1177729698.

- [76] J. J. Duistermaat, J. A. C. Kolk, Multidimensional Real Analysis I: Differentiation, Cambridge Studies in Advanced Mathematics, Cambridge University Press, Cambridge, Mass, 2004. doi:10.1017/CBO978051161671.

- [77] J. Dugundji, Topology, Series in advanced mathematics, Allyn & Bacon, Boston, 1966.

- [78] Y. S. Chow, Local convergence of martingales and the law of large numbers, The Annals of Mathematical Statistics 36 (2) (1965) 552–558. doi:10.1214/aoms/1177700166.

- [79] D. Freedman, Another note on the borel-cantelli lemma and the strong law, with the poisson approximation as a by-product, Annals of Probability 1 (6) (1973) 910–925. doi:10.1214/aop/1176996800.