Complete Subset Averaging with Many Instruments ††thanks: We are grateful to the Co-editor Victor Chernozhukov and the anonymous referee for helpful comments that improve the paper substantially. We also thank Graham Elliott, Ryo Okui, Marine Carrasco, and the seminar participants at Seoul National University, University of Melbourne, ISNPS 2018, CESG 2018, MEG 2018, BK21plus International Conference on Econometrics for helpful comments. Julius Owusu provided excellent research assistance. Shin gratefully acknowledges financial support received from the Social Sciences and Humanities Research Council of Canada (435-2018-0275) and from Australia Research Council (DP170100987). This work was made possible by the facilities of the Shared Hierarchical Academic Research Computing Network and Compute/Calcul Canada.

Abstract

We propose a two-stage least squares (2SLS) estimator whose first stage is the equal-weighted average over a complete subset with instruments among available, which we call the complete subset averaging (CSA) 2SLS. The approximate mean squared error (MSE) is derived as a function of the subset size by the Nagar (1959) expansion. The subset size is chosen by minimizing the sample counterpart of the approximate MSE. We show that this method achieves the asymptotic optimality among the class of estimators with different subset sizes. To deal with averaging over a growing set of irrelevant instruments, we generalize the approximate MSE to find that the optimal is larger than otherwise. An extensive simulation experiment shows that the CSA-2SLS estimator outperforms the alternative estimators when instruments are correlated. As an empirical illustration, we estimate the logistic demand function in Berry, Levinsohn, and Pakes (1995) and find the CSA-2SLS estimate is better supported by economic theory than the alternative estimates.

Keywords: two-stage least squares, many instruments, endogeneity, model averaging, equal-weight.

1 Introduction

Instrumental variables (IV) estimators are commonly used to estimate the parameters associated with endogenous variables in economic models. The two-stage least squares (2SLS) is the most popular IV estimator for linear regression models with endogenous regressors. While the 2SLS estimator is usually applied to just-identified models where the number of instruments is the same as the number of endogenous variables, there are many applications where more instruments are used than the number of endogenous variables (over-identified). In particular, when the instrument set is a large set of dummy variables or is constructed by interacting the original instruments with exogenous variables, the total number of instruments can be quite large. For example, Angrist and Krueger (1991) use as many as 180 instruments for one endogenous variable in one of their specifications to get a tighter confidence interval for the structural parameter than using a smaller set of instruments.

Although using a large set of instruments can improve efficiency, there is a trade-off in terms of increased bias in the point estimate, e.g. Kunitomo (1980), Morimune (1983), and Bekker (1994). Motivated by the trade-off relationship, Donald and Newey (2001) propose to select the number of instruments by minimizing the approximate mean squared error (MSE) of IV estimators. Kuersteiner and Okui (2010) propose an IV estimator that applies the model averaging approach of Hansen (2007) in the first stage and show that the selected weights attain optimality in the sense of Li (1987). Okui (2011) proposes to average the first stage using shrinkage to obtain the shrinkage IV estimators. When the number of instruments can be much larger than the sample size, Belloni, Chen, Chernozhukov, and Hansen (2012) propose to select instruments using Lasso in the first stage under approximate sparsity and Carrasco (2012) proposes a regularized IV estimator using all the instruments.

In this paper, we propose a 2SLS estimator whose first stage is the equal-weighted average over a complete subset with instruments among the total of instruments. We call this estimator the complete subset averaging (CSA) 2SLS estimator. Our approach differs from the important existing work in the many instruments literature: Unlike Donald and Newey (2001), the CSA-2SLS is based on model averaging in the first-stage rather than model selection and does not require ordering of the instruments; Unlike Kuersteiner and Okui (2010), it does not require weight estimation; Unlike Okui (2011), it does not require to specify the main set of instruments a priori.

The main theoretical contribution of this paper is three-fold. First, we derive the approximate MSE for our CSA-2SLS estimator by the Nagar (1959) expansion. It is technically challenging because the average of non-nested projection matrices is not idempotent. In contrast, the existing literature usually assumes nested models. The derived formula shows the bias-variance trade-off and some interesting features which will be discussed in detail in the following sections. Second, we generalize the approximate MSE formula when irrelevant instruments exist whose number grows as the sample size increases. A penalty term decreasing with the subset size appears in the generalized formula, which suggests that the choice of a larger than otherwise would be desirable in the presence of irrelevant instruments. Third, we prove that the CSA-2SLS estimator with the subset size minimizing the sample approximate MSE is asymptotically optimal in the sense that it attains the lowest possible MSE among the class of the CSA-2SLS estimators with different subset sizes. Our optimality proof is based on Li (1987) and Whittle (1960).

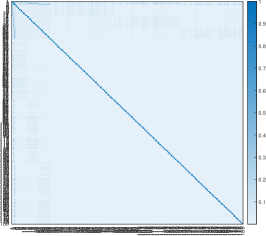

Our approach is motivated by the following observations. First, a set of instruments in economic applications can be correlated with each other, often by construction. In this case, the model averaging approach in the first-stage is more appropriate. We borrow the intuition from the high-dimensional prediction literature. The model selection method, such as Lasso breaks down when predictors are highly correlated. Alternatively, ridge regression works better for highly correlated predictors and Elliott, Gargano, and Timmermann (2013) show the connection between the complete subset averaging and ridge regression. Therefore, we believe that the averaging approach can work better with correlated instruments. Figure 1 shows the correlation structure of instruments in three important studies: 180 instruments (interactions of dummy variables) in Angrist and Krueger (1991), 10 instruments (average characteristics of similar products) in Berry, Levinsohn, and Pakes (1995), and 46 instruments (lagged dependent variables) in Acemoglu, Johnson, Robinson, and Yared (2008). The instruments of the first study do not exhibit high correlation, but those of the other two show high correlation. Therefore, it would be empirically relevant to consider the averaging approach suggested in this paper.

Our second motivation is that, in model averaging, estimating weights can cause finite sample efficiency loss, especially when the weight vector’s dimension is large. In the forecasting literature it is not surprising to see that equal-weighted averaging outperforms other sophisticated optimal weighting schemes, e.g., see Clemen (1989), Stock and Watson (2004), and Smith and Wallis (2009). Bootstrap aggregating (known as bagging; Breiman (1996)) is another example of equal-weight model averaging and is a popular method in the machine learning literature.

It is worth emphasizing the important work by Elliott, Gargano, and Timmermann (2013, 2015) who propose the equal-weight complete subset regressions in the forecasting context. They demonstrate the complete subset regression’s excellent performance relative to competing methods such as ridge regression, Lasso, Elastic Net, bagging, and Bayesian model averaging. We build on their idea of the complete subset regression to provide a formal theoretical justification of the CSA-2SLS estimator with extensive Monte Carlo simulations. Indeed, we find that the CSA-2SLS exhibits potentially huge gains in terms of the bias and the MSE relative to existing methods especially when the instruments are correlated and there is large endogeneity.

There are two limitations to be noted. First, conditionally homoskedastic errors are assumed in the derivation of the approximate MSE, similarly in Donald and Newey (2001), Kuersteiner and Okui (2010), Hansen (2007), Okui (2011), and Carrasco (2012). This is required to obtain the explicit order of the higher-order terms in the expansion of the MSE, which allows one-to-one comparison with the existing literature. Donald, Imbens, and Newey (2009) derive the approximate MSE under heteroskedasticity for the efficient generalized method of moment (GMM) and the generalized empirical likelihood (GEL) estimators at the expense of more complicated expressions. Also, note that the 2SLS is no longer efficient under heteroskedasticity.

Second, we focus on the 2SLS estimator because of its utmost popularity among applied researchers. The limited information maximum likelihood (LIML) estimator has gained considerable attention recently because of its theoretical advantage over the 2SLS having a smaller bias under the many instruments asymptotics (Donald and Newey (2001)). To maintain our focus on the new averaging method, however, we defer any extension to the -class estimators such as LIML and bias-corrected 2SLS to future research.

Finally, we summarize related literature. The model averaging approach becomes prevalent in the econometrics literature. Hansen (2007) shows that the weight choice based on the Mallows criterion achieves optimality. Hansen and Racine (2012) propose the jackknife model averaging, which allows heteroskedasticity. Ando and Li (2014) present a model averaging for high-dimensional regression. Ando and Li (2017) and Zhang, Yu, Zou, and Liang (2016) consider the class of generalized linear models to show the optimality under the Kullback-Leibler loss function. Zhang and Yu (2018) propose a model averaging in the spatial autoregressive models. Kitagawa and Muris (2016) propose the propensity score model averaging estimator for the average treatment effects for treated. Lee and Zhou (2015) propose a model averaging approach over complete subsets in the second stage IV regression.

Our approach is different from the many weak instruments asymptotics in Chao and Swanson (2005), Stock and Yogo (2005), Han and Phillips (2006), Andrews and Stock (2007), and Hansen, Hausman, and Newey (2008), where the concentration parameter can grow slower than the sample size. Alternative estimators under heteroskedasticity and many instruments are proposed by Hausman, Lewis, Menzel, and Newey (2011) and Hausman, Newey, Woutersen, Chao, and Swanson (2012). Kuersteiner (2012) extends the instrument selection criteria of Donald and Newey (2001) to the time series setting and proposes a GMM estimator using lags as instruments. Kang (2018) derives the approximate MSE of IV estimators with locally invalid instruments. Antoine and Lavergne (2014) and Escanciano (2017) propose estimators free from choice variables by adopting the continuum of unconditional moment condition in the first stage.

The remainder of the paper is organized as follows. Section 2 describes the model and proposes the CSA-2SLS estimator. Section 3 derives the approximate MSE formula of the estimator and investigates its properties. We also show the asymptotic optimality result as well as the implementation procedure. Section 4.1 extends the result by allowing an increasing number of irrelevant instruments. Section 4.2 investigates the relationship between our approximate MSE and that of Donald and Newey (2001) when the instruments are orthogonal. Section 5 studies the finite sample properties via Monte Carlo simulations. Section 6 provides an empirical illustration. The online supplement contains proofs and additional simulation results.

2 Model and Estimator

We follow the setup of Donald and Newey (2001) and Kuersteiner and Okui (2010). The model is

| (1) | |||||

| (8) |

where is a scalar outcome variable, is a vector of endogenous variables, is a vector of included exogenous variables, is a vector of exogenous variables (including ), and are unobserved random variables with finite second moments which do not depend on , and is an unknown function of . Let and . The second equation represents a nonparametric reduced form relationship between and the exogenous variables , with by construction. Define the vectors , , and the matrices , , and .

The set of instruments has the form , where ’s are functions of such that is a vector of instruments. The total number of instruments increases as but we suppress the dependency on and write unless we need to express the dependence of on explicitly. Define its matrix version as . To define the complete subset averaging estimator, consider a subset of excluded instruments. Note that the included exogenous variables are always included in the instruments set. To avoid confusion, we will use “instruments” to refer to excluded instruments throughout the paper. The number of subsets with instruments is

A complete subset with size is the collection of all these subsets. Let , which is the number of models given and . For brevity, the dependence of on and will be suppressed unless it is necessary. For any model with instruments, let be an vector of subset instruments including where and be an matrix for . For each , the first stage equation can be rewritten as

| (9) |

or equivalently,

| (10) |

where is the dimensional projection coefficient matrix for model with instruments, is the projection error, and . The projection coefficient matrix is estimated by

| (11) |

and the average fitted value of over complete subset becomes

| (12) |

where and . The complete subset averaging (CSA) 2SLS estimator with a given is now defined as

| (13) |

The matrix is the average of projection matrices. We call this matrix as the complete subset averaging (CSA-) matrix. Note that the CSA- matrix is symmetric but not idempotent in general.

Therefore, we can estimate the model by the CSA-2SLS estimator for a given . We will deliberate on the choice of in the next section and close this section by characterizing the CSA-2SLS estimator and the CSA- matrix in a broader context.

The CSA-2SLS estimator can be interpreted as the minimizer of the average of 2SLS criterion functions. For each subset of instruments , the corresponding moment condition is

| (14) |

The standard 2SLS estimator given the moment condition (14) minimizes

| (15) |

This equation is the GMM criterion with the weight matrix . Conventional model average estimators are based on a weighted average of , the minimizer of (15), over different models. For this type of model averaging estimators, see Hansen (2007) for the OLS estimator, Lee and Zhou (2015) for the 2SLS estimator, and Chen, Jacho-Chávez, and Linton (2016) for the general approach based on moment conditions.

3 Subset Size Choice and Optimality

In this section, we discuss how to choose the subset size . First, we derive the approximate MSE of the CSA-2SLS estimator by the Nagar (1959) expansion. This high-order expansion shows the bias-variance trade-off that helps improve the finite sample performance of the estimator (e.g. Donald and Newey (2001), Kuersteiner and Okui (2010), and Carrasco (2012)). The subset size is chosen to minimize the sample counterpart of the approximate MSE whose formula is provided. We prove the optimality of the chosen subset size in the sense of Li (1987).

3.1 Approximate MSE

In our analysis, the CSA- matrix plays an important role. Since is not idempotent unless , we cannot directly apply the existing technique in Donald and Newey (2001) or Kuersteiner and Okui (2010) to our analysis. We first list regularity conditions. Let denote the Frobenius norm for a matrix .

Assumption 1.

-

(i)

are i.i.d. with finite fourth moment and .

-

(ii)

and .

-

(iii)

Let be the th element of . Then are constant and bounded for all and all and .

-

(iv)

is bounded.

-

(v)

exists and is nonsingular.

-

(vi)

For each and all , is nonsingular with probability approaching one.

-

(vii)

Let denote the th diagonal element of . Then as .

Assumption 2.

Let be given. There exists a sequence such that for all there exists that satisfies

for large enough .

Assumption 1 collects standard moment and identification conditions similar to those of Donald and Newey (2001) and Kuersteiner and Okui (2010).

Assumption 2 controls the speed of the lower bound such that is arbitrarily well-approximated by the size- complete subset projections. This assumption is not particularly stronger than Assumption 2(ii) of Donald and Newey (2001) since they are equivalent when . The approximation error can be small even with when instruments are correlated. For example, consider that and all elements of are the linear transformation of . Then, Assumption 2 holds with and . Below we provide an example where can grow at arbitrarily slow rate when the instruments are equally correlated at the rate of . It is also possible that Assumption 2 holds only if . A leading case is when the instruments are orthogonal. We provide a detailed analysis for orthogonal instruments in Section 4. In sum, Assumption 2 can hold for a fixed , a growing slower than , or a growing as fast as , depending on the correlation structure of the instruments.

We require Assumption 2 only to derive a valid approximate MSE expression, which gives an intuition on how CSA-2SLS can reduce MSE. It also provides a data adaptive method to choose the subset size balancing between the bias and the variance in a finite sample. When the bias is relatively large, can be chosen as we confirm both in the simulation studies in Section 5 and in the empirical application in Section 6. We also provide an alternative method of choosing other than the approximate MSE in Section 3.3 and investigate the approximate MSE under different circumstances in Section 4.

-

Equicorrelated Instruments

We provide a special example to further discuss Assumption 2. Consider the function

for , , and , where ’s have mean zero, the unit variance, and the constant correlation . Since

where , which is the smallest eigenvalue of the covariance matrix of , we set

so that the variance of is fixed at 1. Setting as a decreasing sequence in does not necessarily imply weak instruments. Since , converges to zero at a slower rate than so that -consistency of the CSA-2SLS estimator is still maintained. This sequence of instruments corresponds to “nearly weak” instruments of Hahn and Kuersteiner (2002) and Antoine and Renault (2009). Note that the weak instruments sequence of Staiger and Stock (1997) assumes that the first-stage coefficients are and 2SLS estimators are not -consistent.

The minimized mean squared approximation error of the CSA with instruments111Since the minimization problem is symmetric in , we set and solve the first-order condition to obtain the minimizer and (17). is

(17) Some interesting observations can be made for the expression (17).

First, the approximation error (17) converges to zero so long as for as . Since can grow at an arbitrarily slow rate if , at least for this example, Assumption 2 imposes a very mild condition on . In contrast, if or , then (17) converges to zero if and only if , which would be the least favourable scenario for the CSA-2SLS estimator.

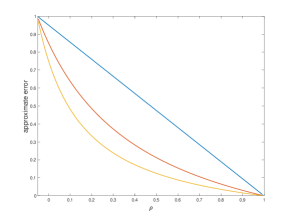

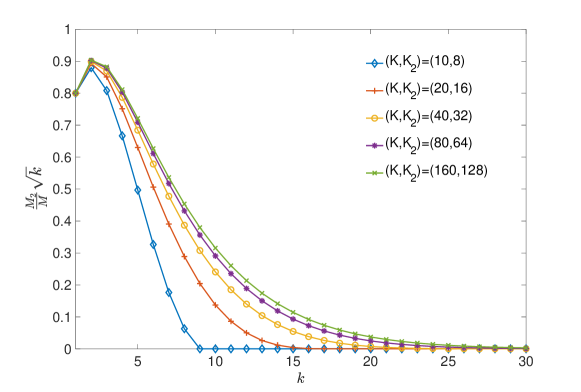

Second, for any given , the approximation error gets smaller as increases and it is equal to zero when . Figure 2 shows the approximation errors when and .

Third, the approximation error is decreasing with uniformly in , which is shown in Figure 2. Evaluating (17) at and , respectively, the difference is .

Figure 2: Approximation error when : (blue), (red), (yellow)

We now provide the approximate MSE formula of CSA-2SLS. Define and .

Theorem 1.

In the expansion, and are terms of smaller order in probability than those in and that the term is the first-order asymptotic variance under homoskedasticity. The first term of (ignoring pre- and post-multiplied ), , corresponds to the bias and is similar to that of Donald and Newey (2001). The second term is different from the usual higher-order variance in similar expansions in the literature. Let . It can be decomposed as

| (22) |

In Donald and Newey (2001), the higher-order variance term, which takes the form of where is the projection matrix consisting of instruments, decreases with . This gives the bias-variance trade-off in their expression. In contrast, is the sum of two components and the monotone decrease with respect to is not always guaranteed.

We further elaborate on the behavior of the higher-order variance term using shrinkage. Since is idempotent, we can write

| (23) |

where . There exist two factors that force to move into opposite directions as varies. First, the norm of decreases as increases since for is the average of the projection matrices on the space spanned by a larger set of instruments. Second, can cause less shrinkage for for a larger , which makes the norm of larger. Note that

| (24) |

and that with less shrinkage lies farther away from the space spanned by . Therefore, if the second factor dominates the first then increases along with .

If there are more than one endogenous variable, then we choose that minimizes a linear combination of the MSE, for a user-specified similarly in Donald and Newey (2001).

3.2 Implementation and Optimality of Approximate MSE

The approximate MSE in (21) gives useful guidance on the data-adaptive choice of . Both terms in converge to zero asymptotically, but there is a trade-off between the higher-order bias and variance terms in finite samples. Similarly, in Donald and Newey (2001) and Kuersteiner and Okui (2010), the approximate MSE sheds light on the choice of only when there exists a non-negligible size of bias for a given sample size with many instruments.

We first introduce notation to construct the sample counterpart of the approximate MSE. Let be a preliminary estimator that is fixed across different values of and . Let be an estimate of . The residual matrix is denoted by and where is a vector. Define , , , , and . The feasible criterion function for is defined as below:

where

Then, we choose as a minimizer of the feasible approximate MSE function, . Given , we can compute the CSA-2SLS estimator defined in (13).

We remark on two practical issues in implementation. First, our theory requires the preliminary estimator be consistent, and it is simply achieved by 2SLS estimation with any valid IVs. However, the performance of the estimator in a finite sample might rely on the choice. Following Donald and Newey (2001) and Kuersteiner and Okui (2010), we propose choosing the set of IVs based on the first stage Mallows criterion, which brings satisfactory performance results in the extensive simulations experiments reported in Section 5. Second, it could be infeasible to estimate when is too large. Note that the number of complete subsets (all the subsets with different ’s) grows exponentially, . To deal with this computational issue, we propose to draw a smaller number of submodels randomly as follows. Let be a class of subsets with elements that are randomly selected from . Then, the CSA projection matrix with randomly drawn submodels is defined as , where is a projection matrix using the set of IVs indexed by . Table 10 in Section C of the Appendix shows simulation results such that randomly drawn submodels work well with a feasible size of .

We finalize this subsection by proving that the CSA-2SLS estimator achieves the asymptotic optimality in the sense that it minimizes the MSE among the class of CSA-2SLS estimators with different complete subset sizes. We collect additional regularity conditions below.

Assumption 3.

-

(i)

, , , , and .

-

(ii)

almost surely in .

-

(iii)

There exist a constant such that where .

Assumptions 3(i) and (ii) are similar to Assumptions 4–5 in Donald and Newey (2001). Assumption 3(i) is a high-level assumption on the consistency of the preliminary estimators. Assumption 3(ii) is a standard assumption in the model selection or model averaging literature (see, e.g. Assumption (A.3) in Li (1987)). This condition excludes the case that is perfectly explained by a finite number of instruments. Assumption 3(iii) is a mild requirement on the convergence rate of that the standard series estimator easily satisfies. For example, consider a series estimator with b-spline bases as in Newey (1997), where where and . By choosing the optimal rate for , we get the rate for the error variance, . Since , we can write for some . Then, Assumption 3(iii) requires . Comparing this rate with above, we can find .

The following result shows that the proposed estimator is optimal among the class of the CSA-2SLS estimators.

3.3 Cross-validation Method

In this subsection we consider an alternative method of choosing the subset size . The approximate MSE provides useful guidance in choosing . More importantly, it gives an intuition on how CSA-2SLS could reduce MSE further by providing the expression for the higher-order bias and variance. However, the theoretical illustration in the previous subsections depends on a few simplifying assumptions: homoskedasticity and the asymptotic approximation of by the complete subset model averaging (Assumption 2). When they are violated, the subset size choice based on the approximate MSE improves the finite sample property of CSA-2SLS less than expected. Therefore, it is worthwhile to propose some alternative methods for the subset size choice.

We propose to choose by the cross-validation (CV) method that minimizes the first-stage mean squared prediction error. We explain it by the leave-one-out cross-validation. This can be immediately extended to any -fold cross-validation, where is the number of subsamples. For , we define the following cross-validation objective function:

where is the jackknife estimator for , which is estimated by (11) without using the -th observation . Then, we choose that minimizes . Lee and Shin (2020) apply a similar cross-validation method in the context of quantile prediction and show that is asymptotically equivalent to the infeasible best subset size. However, the optimality result is not for the second-stage MSE but for the prediction error of the first-stage regression. Therefore, the CV method is robust to the requirement of homoskedasticity and Assumption 2 but it might perform worse than the approximate MSE when those conditions are satisfied.

4 Approximate MSE under Different Circumstances

4.1 Irrelevant Instruments

The higher-order MSE expansion in the previous section assumes an increasing sequence of instruments where the instruments are strong enough for -consistency and the existence of higher-order terms. This implies that the concentration parameter, which measures the strength of the instruments, increases at the rate of . An important feature of the CSA-2SLS is that no instrument is excluded either in finite samples or asymptotically due to equal-weighted averaging. Assume that the econometrician does not know whether irrelevant instruments are included or not. Although irrelevant instruments can be excluded when a pre-screening method is available, it is important to investigate whether the CSA-2SLS estimator and the MSE expansion are still valid if irrelevant instruments happen to be included in the averaging. In contrast, irrelevant instruments can be excluded by zero or negative weights in Kuersteiner and Okui (2010).

In this section, we derive the MSE under a growing set of irrelevant instruments as and increase. This makes the concentration parameter smaller in level for given and than the case where all the instruments are relevant. By comparing the MSEs with and without irrelevant instruments we can analyze the effect of irrelevant instruments on the MSE. Under the many weak instruments asymptotics of Chao and Swanson (2005), the growth rate of the concentration parameter can be slower than . In this case, the 2SLS estimator is not -consistent anymore and it would be difficult to compare the higher-order expansion with the other case. Thus, we leave the analysis with many weak instruments for future research.

For the sake of simplicity, we assume that there is no exogenous variables, , so the model simplifies to

| (26) | |||||

| (27) |

where is a vector of endogenous variables and is a vector of exogenous variables. We set . We divide into the relevant and irrelevant ones, and and make the following definition:

-

Definition 4.1

A vector of instruments is irrelevant if .

Under Definition 4.1, the set of instruments can be divided into two sets, relevant and irrelevant instruments. Let and be the number of relevant and irrelevant instruments, respectively.

We introduce additional definitions. Let be the index set for all subsets with instruments and let and be the index sets for subsets with at least relevant instruments and those with less than , respectively. By construction, . Let and be the cardinality of and , respectively. For brevity, we suppress the dependence on , , , and .

Each element of the index sets and corresponds to a relevant and an irrelevant first stage model (a set of instruments). Since there are endogenous variables, those models in satisfy the order condition for identification and (completely) approximate as increases. In contrast, those irrelevant models in do not approximate as increases.

We make assumptions that will replace Assumption 2.

Assumption 4.

-

(i)

Let be given. There exists a sequence such that for all there exists that satisfies

for large enough .

-

(ii)

For each and some positive constant , .

-

(iii)

as .

Assumption 4(i) is a version of Assumption 2 with relevant instruments. Assumptions 4(ii)-(iii) are restrictions on the proportion of relevant and irrelevant first-stage models. Assumption 4(ii) sets a non-zero lower bound for the proportion of relevant first-stage models but still allows an increasing number of irrelevant instruments. Assumption 4(iii) states that the proportion of irrelevant models decreases to zero at the rate. Since for by construction (e.g. if , , and , one cannot choose a subset of or more irrelevant instruments), Assumption 4(iii) controls the growth rate of the sequence as , , and grow.

To fix ideas, suppose that (one endogenous variable). is the number of subsets with instruments including at least 1 relevant instrument and is the number of subsets with irrelevant instruments. Since by definition and

for and for , we have

Thus, is monotonically increasing in for given and with the minimum at . Thus, Assumption 4(ii) holds if there is a positive constant such that .

We can also find a sufficient condition for Assumption 4(iii) when . By using the bounds for binomial coefficients and Stirling’s formula for a large ,

| (28) |

Thus, Assumption 4(iii) holds if . Since this is a sufficient condition, Assumption 4(iii) can hold even when the proportion of irrelevant instruments is much higher than . Figure 3 shows that as long as grows sufficiently fast as increases when .

Now we can generalize the main theorem allowing for an increasing number of irrelevant instruments.

Theorem 3.

Theorem 29 shows that the approximate MSE formula in the presence of irrelevant instruments is the same as the formula in Theorem 21 except that is multiplied. Since depends on , the optimal that minimizes (29) may differ from the minimizer of (21).

Specifically, by observing that places larger penalties for smaller , we can conclude that the optimal will be (weakly) larger than those without the term . A practical recommendation is to try larger values of than the minimizer of the sample approximate MSE if the presence of irrelevant (or very weak) instruments is suspected.

4.2 Orthogonal Instruments

There are special cases when the CSA-2SLS estimator coincides exactly with the 2SLS estimator using all the instruments. The two estimators are the same if (a) , which is trivial, or (b) the instruments are mutually orthogonal. We elaborate on the second case.

The projection matrix of the orthogonal instruments is equal to the sum of the projection matrices of each of the instruments. Thus, the projection matrix of the 2SLS estimator, , becomes

where for is the projection matrix based on the orthogonal instrument with the subset size 1. Now consider the CSA- matrix with subset size constructed from the orthogonal instruments:

Since the term is cancelled out when we plug-in into Equation (13), the CSA-2SLS estimator becomes identical to the 2SLS estimator for any .

The identity result does not hold in general when instruments are correlated although they can be always orthogonalized without affecting the column space they span. We illustrate this point by a simple example with and . Let be the vector of instruments and be the corresponding vector of orthogonalized instruments. Then,

where denotes a generic projection matrix of the orthogonalized instruments. Therefore, the CSA-2SLS estimator using does not give the same estimate as that using , the 2SLS estimator.

The approximate MSE in (21) is simplified further when instruments are orthogonal. Let . Because of , , and the idempotent property of , we have

| (30) |

Thus, (21) can be written as

| (31) |

where

Note that is the approximate MSE for 2SLS using instruments as shown in Donald and Newey (2001) and is independent of . We show in the following Corollary that the approximate MSE in (21) is asymptotically equivalent to when instruments are orthogonal.

Corollary 1.

Corollary 1 holds because Assumption 1–2 imply and in (31) when instruments are orthogonal. The full proof is given in Appendix A.

Recall that CSA-2SLS does not depend on when instruments are orthogonal. Corollary 1 establishes the logical consistency by showing that the approximate MSE becomes independent of as well when instruments are orthogonal.

5 Simulation

We investigate the finite sample properties of the CSA-2SLS estimator by conducting Monte Carlo simulation studies222The replication R codes for both the Monte Carlo experiments and empirical applications are available at https://github.com/yshin12/ls-csa.. We consider the following simulation design:

| (33) | ||||

| (34) |

where is a scalar, is set to be (0, 0.1), is the parameter of interest, and . The diagonal terms of are ones and off-diagonal terms are ’s. Thus, denotes the correlation between instruments and is set to or . The error terms are i.i.d. over , bivariate normal with variances 1 and covariance . Note that denotes the severity of endogeneity and is set to or . We consider three designs for : flat, decreasing, half-zero signals depending on the element values of the vector . In each design, the signal-noise ratio is controlled by , which is either 0.01 or 0.1. The exact formula of and are provided in the online supplement. The number of observations and the number of instruments are set to and . Note that the flat and decreasing designs of with coincide with those used in Donald and Newey (2001) and Kuersteiner and Okui (2010). The simulation results are based on 400 replications.

In addition to the CSA-2SLS (denoted by CSA hereafter) estimator based on the approximate MSE, we also estimate the model by OLS, 2SLS with full instruments, the optimal 2SLS by Donald and Newey (2001) denoted by DN, and the model average estimator by Kuersteiner and Okui (2010) denoted by KO and compare their performance.333Since we build up the idea of CSA based on 2SLS, we focus on the comparison with similar 2SLS type estimators in various situations. We leave it for future research to develop a CSA estimator in different classes (e.g. LIML or JIVE) and compare the performance with other types of estimators.

Tables 1–4 report the simulation results for designs with . The complete simulation results including are collected in the Appendix. In the tables, we report the mean squared errors (MSE), bias (Bias), median absolute deviation (MAD), median bias (Median Bias), interdecile range (Range), and the coverage probability of the 95% confidence interval (Coverage). The mean and median of are also reported for DN and CSA.

As expected from the theory, the simulation results are quite promising for CSA when the instruments are correlated (). Table 1 reports the results of . It confirms that CSA chooses smaller ’s and shows smaller variances. DN also shows a similar bias level but MSE is much larger. KO performs worse than CSA in terms of both bias and MSE in all designs in the table. However, MSE of KO is still comparable to CSA and is much smaller than that of DN. This indicates that the estimators based on model averaging mitigate the well-known ‘moments problem’ caused by the large outliers with a small number of instruments, e.g. Mariano (1972).444We thank the referee for pointing this out.

Next, we compare some robust statistics such as MAD and Median Bias. CSA shows better performance in both measures than DN except two designs (weak IV signal/decreasing and strong IV signal/flat ), where the losses are much smaller than the gains in other designs. Overall, KO shows smaller MAD but larger Median Bias than CSA. The coverage of CSA is close to the nominal level across different specifications except weak IV signal/half-zero but that of KO is far from the nominal level especially when the instrument signal is weak.555We construct the confidence intervals by assuming the instrument/weight/subset selection in each method is correct. See Section B of the Appendix for details.

Finally, the performance of CSA.CV, which chooses by the 10-fold cross-validation, is slightly worse than CSA in these simulation designs. In Table 2, we observe similar patterns when and . However, the performance of DN, KO, and CSA is quite similar in the lower panel when the signal from the instruments is strong.

Tables 3–4 report the simulation results when the instruments are uncorrelated. As expected from the theory, the performance of CSA is quite similar to 2SLS. We partially confirm the results in Donald and Newey (2001) with the same designs. The coverage of DN is better than other estimators that show quite similar performance but MAD of DN is much larger.666We could duplicate the MAD statistics in Donald and Newey (2001) only by the formula , i.e. re-centered at the true parameter value. However, we use the formula for MAD in this paper. See, for example, Rousseeuw and Croux (1993) for the definition.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.671 | 0.817 | 0.036 | 0.816 | 0.130 | 0.000 | NA | NA |

| TSLS | 0.359 | 0.589 | 0.069 | 0.589 | 0.283 | 0.005 | NA | NA |

| DN | 5.492 | -0.011 | 0.226 | 0.134 | 1.058 | 0.825 | 1.430 | 1.000 |

| KO | 0.232 | 0.460 | 0.088 | 0.468 | 0.366 | 0.172 | NA | NA |

| CSA.AMSE | 0.090 | 0.029 | 0.178 | 0.071 | 0.648 | 0.890 | 1.058 | 1.000 |

| CSA.CV | 0.120 | 0.179 | 0.164 | 0.244 | 0.725 | 0.630 | 3.680 | 3.000 |

| decreasing | ||||||||

| OLS | 0.798 | 0.892 | 0.030 | 0.893 | 0.117 | 0.000 | NA | NA |

| TSLS | 0.744 | 0.856 | 0.071 | 0.858 | 0.263 | 0.000 | NA | NA |

| DN | 13938.210 | -4.575 | 0.373 | 0.596 | 2.900 | 0.635 | 1.840 | 1.000 |

| KO | 0.707 | 0.831 | 0.080 | 0.832 | 0.316 | 0.003 | NA | NA |

| CSA.AMSE | 0.552 | 0.665 | 0.199 | 0.650 | 0.761 | 0.287 | 3.433 | 1.000 |

| CSA.CV | 0.592 | 0.697 | 0.177 | 0.715 | 0.734 | 0.247 | 2.803 | 1.000 |

| half-zero | ||||||||

| OLS | 0.798 | 0.892 | 0.031 | 0.893 | 0.119 | 0.000 | NA | NA |

| TSLS | 0.746 | 0.857 | 0.072 | 0.860 | 0.270 | 0.000 | NA | NA |

| DN | 94.560 | 0.668 | 0.341 | 0.722 | 2.424 | 0.568 | 2.292 | 1.000 |

| KO | 0.726 | 0.843 | 0.078 | 0.848 | 0.303 | 0.003 | NA | NA |

| CSA.AMSE | 0.591 | 0.696 | 0.196 | 0.711 | 0.779 | 0.253 | 4.107 | 1.000 |

| CSA.CV | 0.620 | 0.718 | 0.176 | 0.719 | 0.827 | 0.207 | 2.743 | 1.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.179 | 0.420 | 0.037 | 0.417 | 0.142 | 0.000 | NA | NA |

| TSLS | 0.021 | 0.124 | 0.052 | 0.130 | 0.195 | 0.585 | NA | NA |

| DN | 0.011 | 0.030 | 0.062 | 0.041 | 0.259 | 0.905 | 3.752 | 4.000 |

| KO | 0.013 | 0.075 | 0.055 | 0.082 | 0.213 | 0.772 | NA | NA |

| CSA.AMSE | 0.010 | -0.005 | 0.063 | 0.002 | 0.240 | 0.948 | 1.038 | 1.000 |

| CSA.CV | 0.009 | 0.036 | 0.065 | 0.037 | 0.226 | 0.892 | 6.103 | 6.000 |

| decreasing | ||||||||

| OLS | 0.663 | 0.813 | 0.037 | 0.813 | 0.134 | 0.000 | NA | NA |

| TSLS | 0.345 | 0.577 | 0.071 | 0.579 | 0.278 | 0.010 | NA | NA |

| DN | 4.320 | 0.034 | 0.203 | 0.105 | 0.903 | 0.843 | 1.435 | 1.000 |

| KO | 0.195 | 0.417 | 0.087 | 0.426 | 0.363 | 0.220 | NA | NA |

| CSA.AMSE | 0.087 | 0.034 | 0.179 | 0.072 | 0.652 | 0.890 | 1.050 | 1.000 |

| CSA.CV | 0.125 | 0.187 | 0.163 | 0.256 | 0.723 | 0.605 | 3.962 | 3.000 |

| half-zero | ||||||||

| OLS | 0.666 | 0.814 | 0.037 | 0.813 | 0.138 | 0.000 | NA | NA |

| TSLS | 0.352 | 0.582 | 0.070 | 0.588 | 0.288 | 0.007 | NA | NA |

| DN | 3.987 | 0.028 | 0.250 | 0.179 | 1.195 | 0.785 | 1.567 | 1.000 |

| KO | 0.258 | 0.487 | 0.087 | 0.495 | 0.356 | 0.110 | NA | NA |

| CSA.AMSE | 0.094 | 0.048 | 0.177 | 0.085 | 0.633 | 0.873 | 1.160 | 1.000 |

| CSA.CV | 0.131 | 0.201 | 0.171 | 0.258 | 0.709 | 0.593 | 4.018 | 3.000 |

Note: We report mean squared errors (MSE), mean biases (Bias), median absolute deviations (MAD), median biases (Median Bias), 10-90% ranges of the estimator (Range), coverages for the 95% confidence interval (Coverage), means of and medians of . For estimators DN, KO, and CSA.AMSE, we apply the Mallows criterion for the preliminary estimator. We set the 10-fold cross-validation method for CSA.CV.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.608 | 0.779 | 0.011 | 0.778 | 0.042 | 0.000 | NA | NA |

| TSLS | 0.027 | 0.144 | 0.039 | 0.146 | 0.160 | 0.417 | NA | NA |

| DN | 0.010 | 0.024 | 0.055 | 0.028 | 0.211 | 0.907 | 3.885 | 4.000 |

| KO | 0.011 | 0.059 | 0.047 | 0.061 | 0.181 | 0.835 | NA | NA |

| CSA.AMSE | 0.006 | -0.002 | 0.052 | 0.001 | 0.197 | 0.955 | 1.012 | 1.000 |

| CSA.CV | 0.008 | 0.037 | 0.050 | 0.041 | 0.191 | 0.887 | 7.575 | 7.000 |

| decreasing | ||||||||

| OLS | 0.794 | 0.891 | 0.009 | 0.891 | 0.037 | 0.000 | NA | NA |

| TSLS | 0.468 | 0.678 | 0.060 | 0.672 | 0.236 | 0.000 | NA | NA |

| DN | 3.709 | 0.051 | 0.207 | 0.116 | 0.970 | 0.843 | 1.415 | 1.000 |

| KO | 0.243 | 0.473 | 0.091 | 0.471 | 0.323 | 0.113 | NA | NA |

| CSA.AMSE | 0.074 | 0.045 | 0.162 | 0.076 | 0.603 | 0.892 | 1.157 | 1.000 |

| CSA.CV | 0.143 | 0.229 | 0.176 | 0.297 | 0.688 | 0.540 | 4.468 | 3.000 |

| half-zero | ||||||||

| OLS | 0.794 | 0.891 | 0.009 | 0.891 | 0.037 | 0.000 | NA | NA |

| TSLS | 0.467 | 0.677 | 0.063 | 0.672 | 0.238 | 0.000 | NA | NA |

| DN | 182.108 | 0.541 | 0.246 | 0.135 | 1.297 | 0.810 | 1.387 | 1.000 |

| KO | 0.299 | 0.530 | 0.088 | 0.525 | 0.331 | 0.037 | NA | NA |

| CSA.AMSE | 0.081 | 0.065 | 0.159 | 0.093 | 0.611 | 0.877 | 1.275 | 1.000 |

| CSA.CV | 0.155 | 0.246 | 0.173 | 0.312 | 0.693 | 0.515 | 4.607 | 3.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.115 | 0.335 | 0.011 | 0.330 | 0.043 | 0.000 | NA | NA |

| TSLS | 0.001 | 0.016 | 0.015 | 0.014 | 0.058 | 0.907 | NA | NA |

| DN | 0.001 | 0.006 | 0.016 | 0.007 | 0.062 | 0.935 | 9.617 | 10.000 |

| KO | 0.001 | 0.009 | 0.015 | 0.009 | 0.059 | 0.920 | NA | NA |

| CSA.AMSE | 0.001 | -0.001 | 0.016 | -0.001 | 0.059 | 0.948 | 1.000 | 1.000 |

| CSA.CV | 0.001 | 0.006 | 0.015 | 0.005 | 0.059 | 0.935 | 12.825 | 13.000 |

| decreasing | ||||||||

| OLS | 0.657 | 0.810 | 0.010 | 0.809 | 0.040 | 0.000 | NA | NA |

| TSLS | 0.039 | 0.184 | 0.044 | 0.191 | 0.179 | 0.290 | NA | NA |

| DN | 0.010 | 0.022 | 0.061 | 0.028 | 0.238 | 0.917 | 3.225 | 3.000 |

| KO | 0.011 | 0.063 | 0.054 | 0.068 | 0.216 | 0.850 | NA | NA |

| CSA.AMSE | 0.009 | -0.004 | 0.063 | 0.003 | 0.232 | 0.960 | 1.000 | 1.000 |

| CSA.CV | 0.012 | 0.058 | 0.061 | 0.070 | 0.218 | 0.830 | 8.398 | 8.000 |

| half-zero | ||||||||

| OLS | 0.657 | 0.810 | 0.011 | 0.809 | 0.041 | 0.000 | NA | NA |

| TSLS | 0.038 | 0.184 | 0.045 | 0.191 | 0.176 | 0.285 | NA | NA |

| DN | 0.014 | 0.030 | 0.073 | 0.039 | 0.282 | 0.907 | 3.038 | 3.000 |

| KO | 0.016 | 0.092 | 0.052 | 0.098 | 0.207 | 0.770 | NA | NA |

| CSA.AMSE | 0.010 | -0.003 | 0.064 | 0.003 | 0.244 | 0.960 | 1.010 | 1.000 |

| CSA.CV | 0.014 | 0.076 | 0.056 | 0.089 | 0.214 | 0.782 | 10.252 | 10.000 |

Note: See the Note below Table 1 for details.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.799 | 0.892 | 0.032 | 0.895 | 0.119 | 0.000 | NA | NA |

| TSLS | 0.747 | 0.857 | 0.071 | 0.854 | 0.265 | 0.000 | NA | NA |

| DN.M | 32.443 | 1.214 | 0.260 | 0.881 | 2.010 | 0.540 | 2.312 | 1.000 |

| KO.M | 0.747 | 0.857 | 0.076 | 0.858 | 0.289 | 0.000 | NA | NA |

| CSA.AMSE | 0.737 | 0.850 | 0.076 | 0.849 | 0.282 | 0.000 | 5.145 | 1.000 |

| CSA.CV | 0.736 | 0.850 | 0.077 | 0.846 | 0.299 | 0.000 | 2.895 | 1.000 |

| decreasing | ||||||||

| OLS | 0.798 | 0.892 | 0.030 | 0.893 | 0.116 | 0.000 | NA | NA |

| TSLS | 0.744 | 0.856 | 0.072 | 0.859 | 0.254 | 0.000 | NA | NA |

| DN.M | 16.810 | 0.426 | 0.322 | 0.726 | 2.348 | 0.565 | 2.013 | 1.000 |

| KO.M | 0.718 | 0.839 | 0.077 | 0.842 | 0.308 | 0.003 | NA | NA |

| CSA.AMSE | 0.732 | 0.848 | 0.069 | 0.855 | 0.270 | 0.003 | 3.730 | 1.000 |

| CSA.CV | 0.729 | 0.846 | 0.068 | 0.850 | 0.286 | 0.003 | 2.902 | 1.000 |

| half-zero | ||||||||

| OLS | 0.797 | 0.892 | 0.033 | 0.892 | 0.125 | 0.000 | NA | NA |

| TSLS | 0.743 | 0.855 | 0.074 | 0.855 | 0.281 | 0.000 | NA | NA |

| DN.M | 3.517 | 0.887 | 0.275 | 0.899 | 1.796 | 0.542 | 2.380 | 1.000 |

| KO.M | 0.747 | 0.856 | 0.076 | 0.857 | 0.303 | 0.000 | NA | NA |

| CSA.AMSE | 0.735 | 0.849 | 0.086 | 0.844 | 0.300 | 0.000 | 5.065 | 1.000 |

| CSA.CV | 0.733 | 0.847 | 0.083 | 0.844 | 0.297 | 0.000 | 2.910 | 1.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.665 | 0.814 | 0.033 | 0.812 | 0.137 | 0.000 | NA | NA |

| TSLS | 0.349 | 0.580 | 0.075 | 0.582 | 0.283 | 0.007 | NA | NA |

| DN.M | 44.540 | 0.361 | 0.269 | 0.571 | 2.280 | 0.642 | 2.455 | 1.000 |

| KO.M | 0.344 | 0.573 | 0.075 | 0.577 | 0.312 | 0.020 | NA | NA |

| CSA.AMSE | 0.316 | 0.546 | 0.081 | 0.550 | 0.354 | 0.030 | 3.155 | 1.000 |

| CSA.CV | 0.319 | 0.549 | 0.082 | 0.555 | 0.345 | 0.030 | 5.938 | 6.000 |

| decreasing | ||||||||

| OLS | 0.664 | 0.813 | 0.035 | 0.813 | 0.137 | 0.000 | NA | NA |

| TSLS | 0.347 | 0.579 | 0.071 | 0.576 | 0.269 | 0.005 | NA | NA |

| DN.M | 3.424 | 0.009 | 0.196 | 0.185 | 1.198 | 0.787 | 1.590 | 1.000 |

| KO.M | 0.231 | 0.460 | 0.084 | 0.461 | 0.333 | 0.175 | NA | NA |

| CSA.AMSE | 0.310 | 0.541 | 0.085 | 0.542 | 0.319 | 0.045 | 1.127 | 1.000 |

| CSA.CV | 0.318 | 0.548 | 0.079 | 0.554 | 0.312 | 0.043 | 5.978 | 6.000 |

| half-zero | ||||||||

| OLS | 0.663 | 0.812 | 0.037 | 0.812 | 0.135 | 0.000 | NA | NA |

| TSLS | 0.349 | 0.578 | 0.081 | 0.571 | 0.302 | 0.018 | NA | NA |

| DN.M | 5932.040 | 4.732 | 0.309 | 0.733 | 1.790 | 0.605 | 2.623 | 1.000 |

| KO.M | 0.337 | 0.566 | 0.083 | 0.570 | 0.330 | 0.028 | NA | NA |

| CSA.AMSE | 0.315 | 0.545 | 0.092 | 0.541 | 0.337 | 0.040 | 3.623 | 1.000 |

| CSA.CV | 0.318 | 0.547 | 0.093 | 0.549 | 0.346 | 0.045 | 6.110 | 6.000 |

Note: See the Note below Table 1 for details.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.793 | 0.891 | 0.009 | 0.891 | 0.037 | 0.000 | NA | NA |

| TSLS | 0.462 | 0.673 | 0.062 | 0.678 | 0.235 | 0.003 | NA | NA |

| DN.M | 496.283 | -0.472 | 0.348 | 0.643 | 2.155 | 0.620 | 2.303 | 1.000 |

| KO.M | 0.455 | 0.667 | 0.067 | 0.671 | 0.249 | 0.005 | NA | NA |

| CSA.AMSE | 0.457 | 0.669 | 0.065 | 0.670 | 0.242 | 0.003 | 5.878 | 1.000 |

| CSA.CV | 0.455 | 0.667 | 0.066 | 0.670 | 0.251 | 0.003 | 7.050 | 7.000 |

| decreasing | ||||||||

| OLS | 0.794 | 0.891 | 0.009 | 0.891 | 0.037 | 0.000 | NA | NA |

| TSLS | 0.467 | 0.677 | 0.064 | 0.678 | 0.236 | 0.000 | NA | NA |

| DN.M | 42.391 | 0.203 | 0.245 | 0.210 | 1.461 | 0.780 | 1.528 | 1.000 |

| KO.M | 0.305 | 0.536 | 0.088 | 0.529 | 0.331 | 0.040 | NA | NA |

| CSA.AMSE | 0.460 | 0.671 | 0.065 | 0.673 | 0.246 | 0.000 | 1.292 | 1.000 |

| CSA.CV | 0.462 | 0.673 | 0.067 | 0.674 | 0.248 | 0.000 | 7.032 | 7.000 |

| half-zero | ||||||||

| OLS | 0.794 | 0.891 | 0.010 | 0.891 | 0.037 | 0.000 | NA | NA |

| TSLS | 0.464 | 0.675 | 0.062 | 0.673 | 0.222 | 0.000 | NA | NA |

| DN.M | 5.060 | 0.883 | 0.297 | 0.843 | 1.897 | 0.575 | 2.965 | 1.000 |

| KO.M | 0.456 | 0.667 | 0.069 | 0.667 | 0.257 | 0.003 | NA | NA |

| CSA.AMSE | 0.459 | 0.671 | 0.063 | 0.670 | 0.231 | 0.000 | 8.432 | 1.000 |

| CSA.CV | 0.461 | 0.672 | 0.066 | 0.672 | 0.246 | 0.000 | 7.000 | 7.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.655 | 0.809 | 0.011 | 0.809 | 0.041 | 0.000 | NA | NA |

| TSLS | 0.039 | 0.188 | 0.047 | 0.186 | 0.166 | 0.268 | NA | NA |

| DN.M | 4.709 | -0.107 | 0.143 | 0.218 | 0.972 | 0.762 | 2.185 | 2.000 |

| KO.M | 0.048 | 0.208 | 0.049 | 0.210 | 0.181 | 0.237 | NA | NA |

| CSA.AMSE | 0.038 | 0.183 | 0.048 | 0.180 | 0.167 | 0.315 | 1.000 | 1.000 |

| CSA.CV | 0.039 | 0.187 | 0.048 | 0.184 | 0.167 | 0.282 | 22.767 | 23.000 |

| decreasing | ||||||||

| OLS | 0.656 | 0.810 | 0.011 | 0.809 | 0.040 | 0.000 | NA | NA |

| TSLS | 0.039 | 0.184 | 0.046 | 0.193 | 0.176 | 0.295 | NA | NA |

| DN.M | 0.012 | 0.044 | 0.064 | 0.054 | 0.237 | 0.877 | 4.730 | 5.000 |

| KO.M | 0.013 | 0.075 | 0.056 | 0.084 | 0.207 | 0.807 | NA | NA |

| CSA.AMSE | 0.037 | 0.179 | 0.047 | 0.186 | 0.178 | 0.338 | 1.000 | 1.000 |

| CSA.CV | 0.038 | 0.182 | 0.047 | 0.192 | 0.179 | 0.307 | 22.650 | 23.000 |

| half-zero | ||||||||

| OLS | 0.656 | 0.810 | 0.011 | 0.810 | 0.042 | 0.000 | NA | NA |

| TSLS | 0.038 | 0.184 | 0.050 | 0.184 | 0.179 | 0.295 | NA | NA |

| DN.M | 15609.030 | 7.069 | 0.409 | 0.766 | 2.577 | 0.782 | 1.073 | 1.000 |

| KO.M | 0.026 | 0.145 | 0.049 | 0.148 | 0.190 | 0.522 | NA | NA |

| CSA.AMSE | 0.037 | 0.180 | 0.051 | 0.182 | 0.185 | 0.318 | 1.000 | 1.000 |

| CSA.CV | 0.038 | 0.183 | 0.049 | 0.182 | 0.180 | 0.297 | 22.688 | 23.000 |

Note: See the Note below Table 1 for details.

We finish this section by a remark on the computation. When we compute the CSA-P matrix, we use 100 random draws from complete subsets when the complete subset size is bigger than 100. Table 10 in the Appendix reports simulation results with different sizes of random draws in one design, and it shows that CSA performs satisfactorily with a relatively small number of draws.

6 Empirical Illustration

In this section we illustrate the usefulness of the CSA-2SLS estimator by estimating a logistic demand function for automobiles in Berry, Levinsohn, and Pakes (1995). The model specification is

where is the market share of the product in market with product 0 denoting the outside option, is the endogenous price variable, is a vector of included exogenous variables, and is a vector of instruments. The parameter of interest is from which we can calculate the price elasticity of demand.

| # of Inelastic | # of Inelastic | ||||||

|---|---|---|---|---|---|---|---|

| Demand | Demand | ||||||

| Original Design | Extended Design | ||||||

| OLS | – | -0.0886 | 1502 | – | -0.0991 | 1405 | |

| (0.0114) | (0.0124) | ||||||

| 2SLS | – | -0.1357 | 746 | – | -0.1273 | 874 | |

| (0.0464) | (0.0246) | ||||||

| DN | 10 | -0.1357 | 746 | 47 | -0.1271 | 876 | |

| (0.0464) | (0.0245) | ||||||

| KO | – | -0.1357 | 746 | – | -0.1273 | 874 | |

| (0.0464) | (0.0246) | ||||||

| CSA.AMSE | 9 | -0.1426 | 659 | 1 | -0.2515 | 7 | |

| (0.0491) | (0.0871) | ||||||

| CSA.CV | 5 | -0.1918 | 107 | 2 | -0.2526 | 7 | |

| (0.0634) | (0.0818) | ||||||

Note: The original design uses 5 regressors and 10 instruments and the extended design does 24 regressors and 48 instruments. The sample size is 2,217. The heteroskedasticity and cluster robust standard errors of are provided inside parentheses.

We first estimate the model by using the same set of regressors and instruments used by Berry, Levinsohn, and Pakes (1995). The vector of covariates includes 5 variables: a constant, an air conditioning dummy, horsepower divided by weight, miles per dollar, and vehicle size. The vector of original instruments includes 10 variables and is constructed by the characteristics of other car models. We also consider an extended design by adopting 48 instruments and 24 regressors constructed by Chernozhukov, Hansen, and Spindler (2015). We presume that all instruments are valid and relevant. Based on the previous simulation results, we adopt two methods for choosing for CSA: (a) the approximate MSE (AMSE) method and (b) the cross-validation(CV) method. We use the Mallows criterion for selecting IVs in AMSE and apply the 10-fold cross-validation for CV. For both estimators, we set when calculating the CSA-P matrix.

Table 5 summarizes the estimation results. In addition to two CSA estimates, we also estimate the model using OLS, 2SLS, DN, and KO for comparison. For each design we report the choice of in DN and CSAs, the estimate of , and the heteroskedasticity and cluster robust standard errors of given that we have chosen the correct model for or the optimal weight of KO. Finally, we report the number of products whose price elasticity of demand is inelastic, which is computed by the following formula:

where is an indicator function equal to 1 if holds.

It is interesting to note that the estimation results of CSA contrast sharply with those of other estimation methods in the extended design. Recall that the economic theory predicts elastic demand in this market. Similar to the result in Berry, Levinsohn, and Pakes (1995), the OLS estimate is biased towards zero and makes 1,405 out of 2,217 products (63%) have inelastic own price demand. The 2SLS estimator mitigates the bias but not enough. Still, 874 (41%) products show inelastic own price elasticity. It is interesting to note that DN and KO are not particularly better than 2SLS in this empirical example although they are supposed to correct the bias caused by many instruments. The estimation result of DN comes close to 2SLS by choosing most instruments, 47 out of 48, and that of KO coincides exactly with 2SLS by putting the whole weight to the largest set of instruments. On the contrary, only 7 products (0.3%) have inelastic demand according to both estimation results of CSA. The estimates by CSA is about twice as large as those by other estimators in absolute term. Since the bias caused by many instruments is towards the OLS estimates, this result can be viewed as a correction for the many instrument bias. However, the standard error of CSA is larger than others and there is a potential trade-off between the bias and the variance. Finally, the original design has fewer instruments and the bias correction by CSAs is not as large as in the extended design. However, CSA.CV shows a larger bias correction and its robustness to heteroskedasticity could be a potential reason.

In sum, 2SLS with all the available instruments suffers from many instruments bias in this application. DN and KO do not correct the bias enough to make the estimation results consistent with the prediction by the economic theory. In contrast, the CSA point estimates reduce the bias substantially in the extended design. Therefore, it is worthwhile to estimate a model with CSA and compare it with other existing methods when the model contains many instruments.

Appendices

Appendix A Proofs and Lemmas

Let , , and . In addition, for and defined in Section 4 of the main text, let , , , , and .

A.1 Proof of Theorem 21

The complete subset averaging 2SLS estimator is

By expanding

| (35) | |||||

| (36) |

we can write

| (37) |

where

and

Based on Lemmas 1-2, we specify the convergence rate of each term. By Lemma 2(ii), . By CLT, . By Lemmas 2(iii)-(v),

| (38) |

By Lemma 2(ii), . By Lemma 2(iv), . By WLLN, and thus . By CLT, . By Assumption 1(v) and the continuous mapping theorem, . Let and .

We show that

| (39) |

The leading orders are and by Lemma 2. The proof proceed by showing that as where is the lower order (the slower) between and .

Our expansion is a non-trivial extension of Donald and Newey (2001) and Kuersteiner and Okui (2010) because we need to specify additional terms that are supposed to be small in those papers. This is due to the fact that our matrix not being idempotent. In particular, Lemma 1 of Donald and Newey (2001) cannot be applied because is not . In addition, Lemma A.1 of Kuersteiner and Okui (2010) cannot be applied because is not .

We use the following expansion. Let and . Using

| (40) |

we can write

| (41) |

because , , and . Furthermore, using

| (42) |

and that , by Lemma 2(v), and by Lemma 2(i), (41) can be further expanded as

| (43) |

Thus,

The higher-order terms in the MSE are obtained by taking the conditional expectation on both sides of the above expansion.

First, take (A.1). We derive the conditional expectation of . By Lemma 2,

In the last equation of the above display, the third equality holds by the inequality with and . Thus, we have

| (48) |

Combining the results together, we get

The desired result is established by noting that

| (58) | |||||

| (59) |

where . ∎

A.2 Proof of Theorem 2

In the following proof, let be a generic constant.

Recall that

where . The feasible criterion is obtained by replacing the unknown population quantities , , and with their sample counterparts, which come from the preliminary estimates. Note that these preliminary estimators do not depend on . Then, we can rewrite as

where

Note that if we use the above expression, an additional term will be added to defined in the main text. However, the additional term does not depend on and is irrelevant to get . By Lemma A.9 in Donald and Newey (2001), it suffices to show

| (60) |

We first define

and rewrite the LHS of (60) as

| (61) |

Since and , it holds that

uniformly over all . Thus, consistency of and implies that the first two terms in (61) are uniformly over .

Let . Since by Assumption 3, it remains to show that

| (62) |

By the triangle inequality

| (63) | ||||

| (64) |

We first show the uniform convergence of the RHS of (63). Expanding and applying the triangle inequality, we get

Since , , and uniformly over , it is enough to show that

for the uniform convergence of the RHS of (63). Since the dimension of is fixed, we abuse notation and use for the maximum element of the matrix. Let . Since does not depend on , we can prove the uniform convergence for instead of . Recentering each term and applying the triangle inequality, we have

We show that terms I.1–I.4 converge to zero in probability uniformly over .

We first look at I.1. Given any , it holds almost surely for that

The first inequality holds by the Markov inequality and the second inequality holds by Theorem 2 (7) in Whittle (1960). The third inequality holds by Lemma 4 and from the definition of . The final main convergence result comes from Assumption 3(iii).

We next take our attention to I.2. It holds almost surely for that

The first and the second inequalities hold by the Markov inequality and by Theorem 2 (8) in Whittle (1960), respectively. Third third holds by Lemma 1(ii) and the definition of .

Similarly, we can show the uniform convergence of I.3 as follows:

The third inequality holds by Lemma 1(ii)–(iii) and the definition of .

The uniform convergence of I.4 immediately follow from uniformly over and .

We now show the uniform convergence of (64). For the same arguments above, it is enough to show that

| (65) |

We expand and apply the triangular inequality to get

Note again that , , and uniformly over . Therefore, the uniform convergence in (65) is implied by

| (66) |

Recentering each term and applying the triangle inequality, we have

We first show the uniform convergence of II.1:

The same arguments above apply to the first four inequalities. The final convergence holds from .

We next show the uniform convergence of II.2:

where the first inequality holds from the central limit theorem and the second inequality holds from Assumption 3(ii), .

We next show the uniform convergence of II.3, which holds by the Markov inequality and the Whittle inequality:

We next show the uniform convergence of II.4:

The first equality holds from Assumption 3(iii). The final convergence is implied from Assumption 3(ii) and from .

The uniform convergence of II.5 follows from and uniformly over . ∎

A.3 Proof of Theorem 29

Define

so that

Decompose

| (67) | |||||

and similarly

Now the expansion (35) and (36) can be further expanded as

and

Therefore,

where

and

These expansions simplify to the expansions in the proof of Theorem 21 when and .777If , is not defined. We may define as the null matrix in this case. This happens if (i) all instruments are relevant or (ii) . Since these cases are trivial, we assume in the proof. Also, note that by Assumption 4(ii)-(iii),

The proof proceeds similar to that of Theorem 21. In particular, the current expansion has additional terms, and , that do not appear in the proof of Theorem 21. Characterising the leading (lower-order) terms including and is the main task of the proof. The remainder term also includes additional terms, but will be shown to be higher-order than the leading terms so it will not affect the AMSE formula.

Recall that , , , , and .

We first specify the convergence rate of those terms in and . First, Lemma 1 holds with and because we do not use the instrument strength in the proof at all. Second, Lemma 2 holds with , , and under Assumptions 1 and 4. Thus, , , , and which are the same with those in the proof of Theorem 21 except that is used in place of . Note that the order of convergence of the term may be slower than that of in the proof of Theorem 21 because is the average projection matrix based on the instrument matrix including some irrelevant instruments. Finally, we use Lemmas 1-3 for and .

In the remainder of the proof, we show that the leading orders are , , and , which are under Assumption 4. Similar to the proof of Theorem 21, let so that the higher order terms can be conveniently written as . Note that may have a different convergence rate from the one used in the proof of Theorem 21. We use the same notation for simplicity.

Using Lemma 2 and 3, and Assumption 4,

Thus, the expansion arguments (40)-(41) hold. The next expansion (43) holds if , , and . These hold because , , and .

Now we derive the conditional expectations of (A.1)-(A.1) with and . In particular, it is sufficient to derive those terms including and because the conditional expectation of the other terms can be found in the proof of Theorem 21. Note the expansion

First take (A.1). By Lemma 3, the terms that include are

| (68) | ||||

| (69) | ||||

| (70) | ||||

| (71) |

where (69)-(70) hold by the inequality and

In addition, we note that

| (72) |

Thus, (48) can be written as

| (73) |

Next take (A.1). Since we can verify that , and , only is added to (49). Since

Thus, by symmetry

| (74) | ||||

| (75) |

Finally, consider the remaining terms in (A.1) and (A.1). Since , the terms we consider in (A.1) and (A.1) are identical to those in the proof of Theorem 21.

Combining the results together, we get

Note that the leading order term due to irrelevant instruments, , cancel out and does not appear in the approximate MSE expression.

A.4 Proof of Corollary 1

From (31) and , it is enough to show that (i) and (ii) as . First, note that for any by Lemma 2(i), where . Setting , we have

since and is idempotent. Therefore, (i) is shown. We next turn our attention to (ii). Plugging-in , we have

| (79) |

By taking the trace of both sides,

| (80) |

Under the maintained assumptions, , , and , where is nonsingular. Therefore, (ii) follows by taking on both side of (80). ∎

A.5 Lemmas

Lemma 1.

Under Assumption 1, the followings hold for all .

-

(i)

,

-

(ii)

,

-

(iii)

for all positive integer ,

-

(iv)

,

-

(v)

,

-

(vi)

,

Proof of Lemma 1:

(i)

(ii) Since is positive semidefinite, so are and . From

it follows that .

(iii) Since is symmetric, is positive semidefinite. Thus,

Proof of Lemma 2:

(i) By the matrix version of the Cauchy-Schwarz inequality (Corollary 9.3.9. of Bernstein (2009)) and Jensen’s inequality,

Since , it suffices to show

| (81) |

Using and the fact that and are positive semi-definite,

as by Assumptions 1(i) and 2. By Markov inequality, (81) is shown.

(ii) By the trace inequality, the norm equivalence, the fact that for a positive semi-definite matrix , and ,

| (82) | |||||

| (83) | |||||

| (84) | |||||

| (85) |

Note that by the Markov inequality under Assumptions 1(i) and 1(v).

(iii) To show , it suffices to show it holds for each column vector of , which corresponds to each element of . We use the fact that the expectation and trace are linear operators, , where is any column vector of , and the trace inequality to get

By the Markov inequality, for ,

and similarly

Since and are finite, the desired conclusion follows by taking .

(iv) Since

| (86) | |||||

| (87) |

the statement of the Lemma follows by the Markov inequality.

(v) This is Lemma A.3(vi) of Donald and

Newey (2001).

(vi) By the same argument of the proof of Lemma A.3(iv) of Donald and Newey (2001) and using our Lemma 1,

(vii) This is Lemma A.3(v) of Donald and

Newey (2001).

(viii) The proof proceeds using a similar argument of the proof of Lemma A.3(viii) of Donald and Newey (2001). Let . Note that is not idempotent. For some and , let and . Let and be stacked matrices over . Then by the Cauchy-Schwarz inequality the absolute value of the th element of satisfies

Now by the definition of . In addition, for some constant ,

by Assumption 1(iii) and Lemma 2(iii). Combining these results, the desired conclusion follows.

(ix) This is Lemma A.3(vii) of Donald and Newey (2001).∎

Lemma 3.

Assume . Under Assumption 1, the followings hold for all .

-

(i)

-

(ii)

,

-

(iii)

and ,

-

(iv)

,

-

(v)

.

Proof of Lemma 3:

(i) By the trace inequality (i.e. for any square matrices and such that is symmetric and , )

(ii) By the matrix version of the Cauchy-Schwarz inequality and Jensen’s inequality,

(iii) The proof is the same with that of Lemma 2(iii) by replacing its and with and , respectively.

(iv) By the matrix version of the Cauchy-Schwarz inequality and Jensen’s inequality,

(iv) The proof is the same with that of Lemma 2(viii) by replacing and with and , respectively. ∎

Lemma 4.

Under Assumption 1, for all ,

Proof of Lemma 4:

Since and for are idempotent, they are both positive semi-definite. Thus, and are also positive semi-definite. Since is symmetric (and thus is normal), . From this, we deduce that

| (88) |

By Theorem 1(i) of Furuta (1987) with , , , and , we have

| (89) |

and with and , we have

| (90) |

Since this proves the lemma. ∎

Appendix B Inference with CSA-2SLS

In this section we briefly discuss the inference procedure of the CSA-2SLS estimator. If the bias is the major concern of an estimation problem, then the bias-minimizing CSA-2SLS can be obtained by setting . In other words, we calculate the equal-weighted average of the fitted values of the endogenous variable using only one instrument at a time and use that averaged fitted value as the instrument in the second stage. Since the choice of is not data-dependent, the researcher can proceed the standard inference procedure.

More generally, we could use sample-splitting method to make inference with the optimal . For example, a half of the sample is used to obtain and the other half is used to estimate given . This method is popular in machine-learning literature where various machine-learning methods are used for model selection or averaging before inference. Wager and Athey (2018) use sample-splitting to allow asymptotic inference with causal forests. Chernozhukov, Chetverikov, Demirer, Duflo, Hansen, Newey, and Robins (2018) use cross-fitting to remove bias arising from the machine-learning estimates of nonparametric functions.

Either with a fixed or an optimal by sample-splitting, suppose that the CSA-2SLS point estimate is obtained. The next task is to calculate the standard error, which is robust to heteroskedasticity and clustering. This is important because many empirical studies report heteroskedasticity-and-cluster robust standard errors as a measure of estimation uncertainty.

To present the standard error formula robust to heteroskedasticity and clustering, we first introduce some definitions and notations for clustered data. Let be the number of clusters. The number of observations in each cluster is for . We assume that the clusters are independent but allow for arbitrary dependence within the cluster. Let , , and be the , , and submatrix of corresponding the th cluster, respectively. Define . For i.i.d. sampling, set and . Let be the covariance matrix of under the standard large and fixed asymptotics. Hansen and Lee (2019) provide sufficient conditions for consistency, asymptotic normality, and consistency of variance estimators.

A covariance matrix estimator robust to heteroskedasticity and clustering is given by

| (91) |

The standard error can be obtained by taking the diagonal elements of .

Appendix C Simulation

In this section we provide the details of the simulation designs and the addtional simulation results. Recall the baseline simulation design:

| (92) | ||||

| (93) |

where is a scalar, is set to be (0, 0.1), is the parameter of interest, and . The diagonal terms of are ones and off-diagonal terms are ’s. The error terms are i.i.d. over , bivariate normal with variances 1 and covariance .

We set the parameter value for while controlling the explanatory power of instruments. As instruments are possibly correlated to each other, the theoretical first stage R-squared now becomes

| (94) |

where is the th element of the vector and is the total number of instruments. Thus, we can set the value of given and by solving Equation (94). Specifically, we consider the following three designs:

| Flat Signal: | |||||

| Decreasing Signal: | |||||

| Half-zero Signal: | (97) |

where and are defined as

and

The number of observations and the number of instruments are set to and . The first stage R-squared is set to and . The IV correlation parameter is set to or . The endogeneity parameter is set to or .

We use the Mallows criterion for the preliminary estimates required for DN, KO, and CSA when we use the approximate MSEs. We also consider two different methods in choosing of CSA: (i) the 10-fold cross-validation (CV) method (CSA.CV) and (ii) (CSA.1). We omit to report the results of CSA.1 because the results are similar to the case of the approximate MSE.

The following tables summarize the complete simulation results.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.020 | 0.099 | 0.064 | 0.102 | 0.258 | 0.830 | NA | NA |

| TSLS | 0.063 | 0.098 | 0.147 | 0.098 | 0.563 | 0.930 | NA | NA |

| DN.M | 4.937 | 0.174 | 0.439 | 0.091 | 2.583 | 0.983 | 3.775 | 1.000 |

| KO.M | 0.069 | 0.101 | 0.153 | 0.098 | 0.608 | 0.927 | NA | NA |

| CSA.AMSE | 0.071 | 0.101 | 0.162 | 0.115 | 0.579 | 0.935 | 4.853 | 1.000 |

| CSA.CV | 0.070 | 0.101 | 0.159 | 0.116 | 0.590 | 0.938 | 3.087 | 2.000 |

| decreasing | ||||||||

| OLS | 0.020 | 0.099 | 0.068 | 0.100 | 0.260 | 0.823 | NA | NA |

| TSLS | 0.061 | 0.098 | 0.140 | 0.102 | 0.567 | 0.930 | NA | NA |

| DN.M | 2.882 | 0.054 | 0.403 | 0.081 | 2.045 | 0.980 | 3.938 | 2.000 |

| KO.M | 0.065 | 0.096 | 0.159 | 0.099 | 0.618 | 0.935 | NA | NA |

| CSA.AMSE | 0.066 | 0.100 | 0.163 | 0.101 | 0.585 | 0.935 | 4.240 | 1.000 |

| CSA.CV | 0.066 | 0.099 | 0.168 | 0.100 | 0.604 | 0.943 | 3.035 | 2.000 |

| half-zero | ||||||||

| OLS | 0.020 | 0.100 | 0.065 | 0.101 | 0.262 | 0.828 | NA | NA |

| TSLS | 0.064 | 0.101 | 0.148 | 0.097 | 0.585 | 0.932 | NA | NA |

| DN.M | 7.701 | 0.331 | 0.439 | 0.087 | 2.722 | 0.985 | 4.207 | 1.000 |

| KO.M | 0.071 | 0.104 | 0.145 | 0.096 | 0.610 | 0.927 | NA | NA |

| CSA.AMSE | 0.070 | 0.103 | 0.163 | 0.094 | 0.606 | 0.932 | 5.220 | 1.000 |

| CSA.CV | 0.072 | 0.100 | 0.160 | 0.092 | 0.636 | 0.932 | 3.050 | 1.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.017 | 0.089 | 0.064 | 0.089 | 0.236 | 0.843 | NA | NA |

| TSLS | 0.040 | 0.066 | 0.118 | 0.074 | 0.460 | 0.927 | NA | NA |

| DN.M | 0.796 | 0.059 | 0.264 | 0.066 | 1.469 | 0.973 | 7.143 | 4.000 |

| KO.M | 0.043 | 0.066 | 0.129 | 0.069 | 0.495 | 0.927 | NA | NA |

| CSA.AMSE | 0.043 | 0.061 | 0.129 | 0.075 | 0.472 | 0.950 | 4.327 | 1.000 |

| CSA.CV | 0.042 | 0.062 | 0.134 | 0.065 | 0.472 | 0.935 | 6.152 | 6.000 |

| decreasing | ||||||||

| OLS | 0.018 | 0.090 | 0.061 | 0.091 | 0.248 | 0.833 | NA | NA |

| TSLS | 0.037 | 0.065 | 0.128 | 0.072 | 0.450 | 0.938 | NA | NA |

| DN.M | 0.233 | 0.001 | 0.202 | 0.005 | 0.758 | 0.950 | 6.128 | 5.000 |

| KO.M | 0.041 | 0.056 | 0.135 | 0.051 | 0.491 | 0.925 | NA | NA |

| CSA.AMSE | 0.040 | 0.062 | 0.132 | 0.057 | 0.506 | 0.943 | 2.120 | 1.000 |

| CSA.CV | 0.039 | 0.062 | 0.126 | 0.064 | 0.485 | 0.943 | 6.168 | 6.000 |

| half-zero | ||||||||

| OLS | 0.018 | 0.091 | 0.063 | 0.092 | 0.247 | 0.828 | NA | NA |

| TSLS | 0.041 | 0.070 | 0.126 | 0.070 | 0.467 | 0.930 | NA | NA |

| DN.M | 1.357 | 0.034 | 0.228 | 0.081 | 1.642 | 0.965 | 8.525 | 11.000 |

| KO.M | 0.044 | 0.071 | 0.129 | 0.068 | 0.473 | 0.932 | NA | NA |

| CSA.AMSE | 0.043 | 0.067 | 0.135 | 0.069 | 0.497 | 0.940 | 4.085 | 1.000 |

| CSA.CV | 0.043 | 0.066 | 0.133 | 0.065 | 0.480 | 0.940 | 6.235 | 6.000 |

Note: See the Note below Table 1 for details.

(, , , )

| MSE | Bias | MAD | Median Bias | Range | Coverage | Mean() | Med() | |

|---|---|---|---|---|---|---|---|---|

| (weak IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.018 | 0.090 | 0.063 | 0.090 | 0.245 | 0.835 | NA | NA |

| TSLS | 0.039 | 0.065 | 0.131 | 0.062 | 0.460 | 0.930 | NA | NA |

| DN.M | 0.212 | -0.002 | 0.213 | -0.007 | 0.774 | 0.953 | 5.838 | 4.000 |

| KO.M | 0.044 | 0.055 | 0.140 | 0.059 | 0.509 | 0.920 | NA | NA |

| CSA.AMSE | 0.098 | -0.009 | 0.205 | -0.009 | 0.724 | 0.975 | 2.530 | 1.000 |

| CSA.CV | 0.078 | 0.010 | 0.173 | 0.014 | 0.654 | 0.960 | 3.697 | 3.000 |

| decreasing | ||||||||

| OLS | 0.020 | 0.099 | 0.066 | 0.100 | 0.262 | 0.823 | NA | NA |

| TSLS | 0.061 | 0.097 | 0.146 | 0.101 | 0.578 | 0.932 | NA | NA |

| DN.M | 6.252 | 0.132 | 0.398 | 0.090 | 1.898 | 0.973 | 3.970 | 2.000 |

| KO.M | 0.066 | 0.094 | 0.162 | 0.091 | 0.622 | 0.932 | NA | NA |

| CSA.AMSE | 0.161 | 0.079 | 0.237 | 0.053 | 0.964 | 0.973 | 4.197 | 1.000 |

| CSA.CV | 0.182 | 0.073 | 0.241 | 0.076 | 1.015 | 0.975 | 2.740 | 1.000 |

| half-zero | ||||||||

| OLS | 0.020 | 0.099 | 0.067 | 0.099 | 0.259 | 0.825 | NA | NA |

| TSLS | 0.062 | 0.098 | 0.150 | 0.096 | 0.582 | 0.925 | NA | NA |

| DN.M | 2.085 | 0.069 | 0.398 | 0.074 | 2.021 | 0.978 | 4.003 | 2.000 |

| KO.M | 0.067 | 0.098 | 0.159 | 0.096 | 0.612 | 0.925 | NA | NA |

| CSA.AMSE | 0.152 | 0.074 | 0.229 | 0.053 | 0.939 | 0.970 | 4.580 | 1.000 |

| CSA.CV | 0.180 | 0.073 | 0.231 | 0.082 | 1.051 | 0.970 | 2.748 | 1.000 |

| (strong IV signal) | ||||||||

| flat | ||||||||

| OLS | 0.007 | 0.044 | 0.046 | 0.044 | 0.187 | 0.863 | NA | NA |

| TSLS | 0.008 | 0.011 | 0.061 | 0.011 | 0.222 | 0.943 | NA | NA |