FRACTIONAL RISK PROCESS IN INSURANCE

Arun KUMAR1 Nikolai LEONENKO2 Alois

PICHLER3

Abstract

The Poisson process suitably models the time of successive events and thus has numerous applications in statistics, in economics, it is also fundamental in queueing theory. Economic applications include trading and nowadays particularly high frequency trading. Of outstanding importance are applications in insurance, where arrival times of successive claims are of vital importance.

It turns out, however, that real data do not always support the genuine Poisson process. This has lead to variants and augmentations such as time dependent and varying intensities, for example.

This paper investigates the fractional Poisson process. We introduce the process and elaborate its main characteristics. The exemplary application considered here is the Carmér–Lundberg theory and the Sparre Andersen model. The fractional regime leads to initial economic stress. On the other hand we demonstrate that the average capital required to recover a company after ruin does not change when switching to the fractional Poisson regime. We finally address particular risk measures, which allow simple evaluations in an environment governed by the fractional Poisson process.

1Department of Mathematics, Indian Institute of Technology Ropar, Rupnagar, Punjab 140001, India

2Cardiff School of Mathematics, Cardiff University, Senghennydd Road, Cardiff CF24 4AG, UK

3Chemnitz University of Technology, Faculty of Mathematics, Chemnitz, Germany

Key words: Fractional Poisson process, convex risk measures

Mathematics Subject Classification (1991):

1 Introduction

Companies, which are exposed to random orders or bookings, face the threat of ruin. But what happens if bookings fail to appear and ruin actually happens? The probability of this event cannot be ignored and is of immanent and substantial importance from economic perspective. Recall that some nations have decided to bail-out banks, so a question arising naturally is how much capital is to be expected to bail-out a company after ruin, if liquidation is not an option.

This paper introduces the average capital required to recover a company after ruin. It turns out that this quantity is naturally related to classical, convex risk measures. The corresponding arrival times of random events as bookings, orders, or stock orders on an exchange are often comfortably modelled by a Poisson process — this process is a fundamental building block to model the economy reality of random orders.

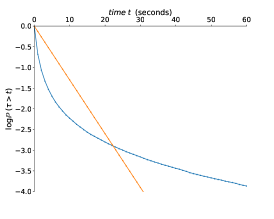

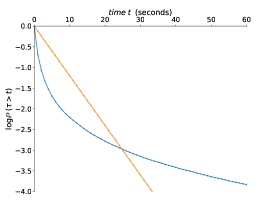

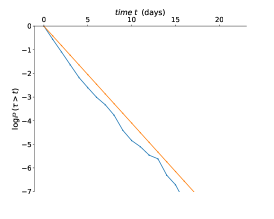

From a technical modelling perspective, the inter-arrival times of the Poisson process are exponentially distributed and independent [17]. However, real data do not always support this property or feature (see, e.g., [13, 16, 36, 39] and references therein). To demonstrate the deviation we display arrival times of two empirical data sets consisting of oil futures high frequency trading (HFT) data and the classical Danish fire insurance data. Oil futures HFT data is considered for the period from July 9, 2007 until August 9, 2007. There is a total of 951,091 observations recorded over market opening hours. The inter-arrival times are recorded in seconds for both up-ticks and down-ticks (cf. Figures 1a and 1b). In addition, the Danish fire insurance data is available for a period of ten years until December 31, 1990, consisting of 2167 observations: the time unit for inter-arrival times in Figure 1c is days. The charts in Figure 1 display the survival function of inter-arrival times of the data on a logarithmic scale and compares them with the exponential distribution. The data are notably not aligned, as is the case for the Poisson process. By inspection it is thus evident that arrival times of the data apparently do not follow a genuine Poisson process.

This paper features the fractional Poisson process. It is a parametrized stochastic counting process which includes the classical Poisson process as a special, perhaps extreme case, but with dependent arrival times. We will see that the fractional Poisson process correctly captures main characteristics of the data displayed in Figure 1.

Arrival times of claim events are of striking economic importance for insurance companies as well and our discussion puts a slight focus on this economic segment. The Cramér–Lundberg model, to give an example, genuinely builds on the Poisson process. We replace the Poisson process by its fractional extension and investigate the new economic characteristics. We observe that the fractional Poisson process exposes companies to higher initial stress. But conversely, we demonstrate that the ruin probability and the average capital required to recover a firm are identical for the classical and the fractional Poisson process. In special cases we can even provide explicit relations.

Outline of the paper.

The following two Sections 2 and 3 are technical, they introduce and discuss the fractional Poisson process by considering Lévy subordinators. Section 4 introduces the risk process based on the fractional Poisson process, while the subsequent Section 5 addresses insurance in a dependent framework. This section contains a discussion of average capital injection to be expected in case of ruin. We finally discuss the risk process for insurance companies and conclude in Section 6.

2 Subordinators and inverse subordinators

This section considers the inverse subordinator first and introduces the Mittag-Leffler distribution. This distribution is essential in defining the fractional Poisson process. Relating the subordinators to -stable distributions enables to simulate trajectories of the fractional Poisson process. Some results here follow Bingham [8], Veillette and Taqqu [40], [41], [32].

2.1 Inverse subordinator

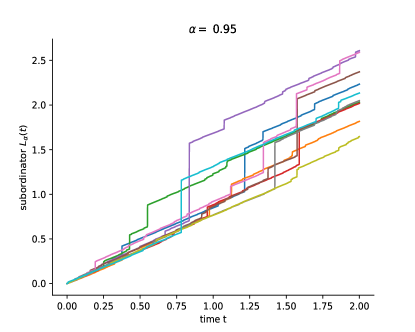

Consider a non-decreasing Lévy process starting from which is continuous from the right with left limits (càdlàg), continuous in probability, with independent and stationary increments. Such process is known as Lévy subordinator with Laplace exponent

| (1) |

where is the drift and the Lévy measure on satisfies

| (2) |

This means that

| (3) |

The inverse subordinator is the first-passage time of , i.e.,

| (4) |

The process is non-decreasing and its sample paths are almost surely (a.s.) continuous if is strictly increasing. Also is, in general, non-Markovian with non-stationary and non-independent increments.

We have

| (5) |

and for any

which implies that all moments are finite, i.e., for any .

Let and the renewal function

| (6) |

and let

Then for , the Laplace transform of is given by

in particular, for

| (7) |

and

| (8) |

thus, characterizes the inverse process , since characterizes

The most important example is considered in the next section, but there are some others.

2.2 Inverse stable subordinator

Let be an -stable subordinator with Laplace exponent , whose density is such that has pdf

| (10) |

Then the inverse stable subordinator

has density

| (11) |

Alternative form for the pdf in term of -function and infinite series are discussed in [15, 18].

Its paths are continuous and nondecreasing. For the inverse stable subordinator is the running supremum process of Brownian motion, and for this process is the local time at zero of a strictly stable Lévy process of index

-

(i)

The Laplace transform of the Mittag-Leffler function is of the form

-

(ii)

The Mittag-Leffler function is a solution of the fractional equation:

where the fractional Caputo-Djrbashian derivative is defined as (see [32])

(13)

Proposition 1

The following hold true for the processes and :

-

(i)

The Laplace transform is

and it holds that

-

(ii)

Both processes and are self-similar, i.e.,

-

(iii)

(14) -

(iv)

(15) where (, resp.) is the Beta function (incomplete Beta function, resp.).

-

(v)

The following asymptotic expansions hold true:

-

(a)

For fixed and large , it is not difficult to show that

(16) Further,

-

(b)

For fixed , it follows

(17)

-

(a)

A finite variance stationary process is said to have long-range-dependence (LRD) property if . Further, for a non-stationary process an equivalent definition is given as follows.

Definition 2 (LRD for non-stationary process)

Let be fixed and . Then the process is said to have LRD property if

| (18) |

where the constant is depending on and .

Remark 3

There is a (complicated) form of all finite-dimensional distributions of in the form of Laplace transforms, see [8].

2.3 Simulation of the stable subordinator

In order to obtain trajectories for the stable subordinator it is necessary to simulate random variables with finite Laplace transform satisfying (10). To this end it is necessary that the -stable random variable is spectrally positive, which means in the standard parametrization (also type 1 parametrization, cf. [38, Definition 1.1.6 and page 6]) of the -stable random variable

| (19) |

with characteristic function (Fourier-transform)

This expression is also obtained by substituting in the Laplace transform

Comparing the latter with (10) reveals that the parameters of the -stable random variable , , in the parametrization (19) are

3 Classical fractional Poisson processes

The first definition of the fractional Poisson process (FPP) is given by Mainardi et al. [27] (see also [28]) as a renewal process with Mittag-Leffler waiting times between the events

| (20) |

where , , are iid random variables with the strictly monotone Mittag-Leffler distribution function

| (21) |

and

Here we denote an indicator as and , , are iid uniformly distributed on random variables. is the pdf of th convolution of the Mittag-Leffler distributions which is known as the generalized Erlang distribution and it is of the form

where the three-parametric Generalized Mittag-Leffler function is defined as (cf. (12) and [14])

| (22) |

where is the rising factorial (sometimes also called Pochhammer function).

Note that and

Meershaert et al. [31] find the stochastic representation for FPP

where is the classical homogeneous Poisson process with parameter which is independent of the inverse stable subordinator

One can compute the following expression for the one-dimensional distribution of FPP:

| (23) | ||||

where is the Mittag-Leffler function (12) evaluated at , and is the th derivative of evaluated at Further, is the Generalized Mittag-Leffler function (22) evaluated at

Finally, Beghin and Orsingher (cf. [5], [6]) show that the marginal distribution of FPP satisfies the system of fractional differential-difference equations

with initial conditions , , , where is the fractional Caputo-Djrbashian derivative (13).

Remark 4 (Expectation and variance)

Finally, Leonenko et al. [26, 25] introduced a fractional non-homogeneous Poisson process (FNPP) with an intecity function as

| (26) |

where is the classical homogeneous Poisson process with parameter , which is independent of the inverse stable subordinator Note that

where is given by (11). Alternatively (cf. [25]),

where is a sequence of non-negative iid random variables such that and , where with The resulting sequence is strictly increasing, since it is obtained from the non-decreasing sequence by omitting all repeating elements.

4 Fractional risk processes

The risk process is of fundamental importance in insurance. Based on the inverse subordinator process (cf. (4)) we extend the classical risk process (also known as surplus process) and consider

| (27) |

Here, is the initial capital relative to the number of claims per time unit (the Poisson parameter ) and the iid variables , with mean model claim sizes. , is an independent of , , fractional Poisson process. The parameter is the safety loading; we demonstrate in Proposition 7 below that the risk process (27) satisfies the net profit condition iff (cf. Mikosch [33, Section 4.1]), which is economically that the company will not necessarily go bankrupt iff .

Remark 5

Note that for so that the model (27) extends the classical ruin process considered in risk theory.

It is essential in (27) to observe that the counting process and the payment process follow the same time scale. These coordinated, or harmonized clocks are essential, as otherwise the model would over-predict too many claims (too many premiums, respectively). As well, different clocks for these two processes violated the profit condition (cf. Proposition 7 below).

The process for the non-homogeneous analogue of (27) is

Remark 6 (Consistency with equivalence principle)

A main motivation for considering the risk process (27) comes from the fact that the stochastic processes

and its non-homogeneous analogon

are martingales with respect to natural filtrations (cf. Proposition 7 below).

It follows from this observation that the time change imposed by does not affect or violate the net or equivalence principle. Further, the part of the risk process corresponding to the premium (i.e., without , or by setting ) is the fair premium of the remaining claims process even under the fractional Poisson process.

Proposition 7

The fractional risk process introduced in (27) is a submartingale (martingale, supermartingale, resp.) for (, , resp.) with respect to the natural filtration.

Proof. Note that the compensated FPP is a martingale with respect to the filtration , cf. [2]. We have

since the compensated FPP is a martingale. Thus

This completes the proof.

Remark 8 (Marginal moments of the risk process)

4.1 A variant of the surplus process

A seemingly simplified version of the surplus process (27) is obtained by replacing the processes or by their expectations (explicitly given in (14)) and to consider

| (29) |

or, more generally,

for the non-homogeneous process. As above, is the initial capital, is the constant premium rate and the sequence of iid random variables is independent of FFP . The net profit condition, as formulated by Mikosch [33], involves the expectation only. For this reason, the adapted surplus process (29) satisfies Mikosch’s net profit condition as well.

For we have that so that the simplified process (29) coincides with the classical surplus process considered in insurance (cf. Remark 5). However, the simplified risk process , in general, is not a martingale unless and , while is martingale for any and by Proposition 7.

Remark 9 (Time shift)

The formula (29) reveals an important property of the fractional Poisson process and the risk process . Indeed, for small times , there are more claims to be expected under the FPP regime, as

The inequality reverses for later times. This means that the premium income rate decays later. The time change imposed by FPP postpones claims to later times — another feature of the fractional Poisson process and a consequence of the martingale property.

However, the premium income is in a real world situation. For this we conclude that the FPP can serve as a stress test for insurance companies within a small, upcoming time horizon.

4.2 Long range dependence of risk process

In this section, we discuss the long range dependency property (LRD property, see Definition 2) of the risk process .

Proposition 10

The covariance structure of risk process is given by

| (30) |

Further, the variance of is

Proof. For , we have .

Further,

Similarly,

Finally,

which completes the proof.

Next, we show that the risk process has the LRD property.

Proposition 11

The process has LRD property for all

4.3 Ruin probabilities

We are interested in the marginal distributions of the stochastic processes

| (31) |

which generalize the classical ruin probability ().

We demonstrate next that the ruin probability for the classical and fractional Poisson process coincide.

Lemma 12

It holds that

is independent of and coincides with the classical ruin probability.

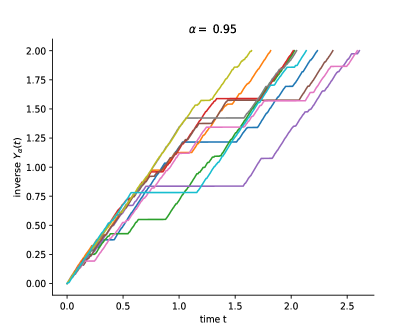

Proof. It holds that (the emphasis being here that does not concentrate measure, ). The inverse process is continuous (cf. the discussion after (11) and Figure 2 for illustration), almost surely strictly increasing without jumps and hence the range of is almost surely. The composition thus attains every value as well, as the non-fractional (classical) process .

Note that if there exists

| (32) |

then ruin probability for non-homogeneous processes can be reduced to the ruin probability for homogeneous one via formulae:

and hence

We thus have the following corollary.

5 Premiums based on the fractional Poisson processes

Risk measures are designed to quantify the risk associated with a random, -valued random variable and they are employed to compute insurance premiums. In what follows we consider risk measures on for an appropriate and use them to express the average capital for a bailout after ruin for the fractional Poisson process and to compare premiums related to the classical and fractional Poisson process.

Definition 14 (Coherent measures of risk, cf. [3])

Let be an appropriate Banach space of random variables. A risk functional is a convex mapping , where

-

(i)

whenever and (positive homogeneity),

-

(ii)

whenever (cash invariance),

-

(iii)

for a.s. (monotonicity), and

-

(iv)

(subadditivity)

for every , .

The most prominent risk functional is the Average Value-at-Risk, as any other, law-invariant risk functional satisfying (i)–(iv) above can be expressed by s (see Kusuoka [19]):

Definition 15 (Average Value-at-Risk)

The Average Value-at-Risk at risk level is the functional

where is the Value-at-Risk (quantile function) at level ().

An equivalent expression for the Average Value-at-Risk, which will be useful later, is the formula

| (33) |

derived in [34].

5.1 Bailout after ruin

The probability of ruin introduced in (31) describes the probability of bankruptcy of an insurance company based on the surplus process. The quantity does not reveal any information of how much capital is required to recover the company after ruin. This can be accomplished by considering the random variable

in an infinite time horizon with corresponding distribution (ruin probability)

| (34) |

In this setting, the average capital required to recover the company from bankruptcy (i.e, conditional on bankruptcy) is

| (35) |

By involving the ruin probability (34) the average capital required to recover from bankruptcy thus is

| (36) |

where the risk level involves , the cdf (34). We shall discuss this quantity in the limiting case corresponding to large companies, for which claims occur instantaneously.

It is well-known that the compensated Poisson process converges to the Wiener process weakly (in distribution, cf. [11]), that is

| (37) |

and thus more generally for the risk process (based on Wald’s formula)

| (38) |

which is a Brownian motion with drift

| (39) |

started at

We shall refer to the process (38) as the limiting case of the risk process.

Lemma 16

Proof. The proof is an immediate consequence of (36) and the fact that

valid for every non-negative random variable, a.s. and applied to here.

Remark 17 (Relation to the fractional Poisson process)

It is an essential consequence of Lemma 12 that the average capital to recover from ruin is independent of in a regime driven by the fractional Poisson process.

Theorem 18 (The limiting case)

The capital requirement defined in (35) is independent of and it holds that

| (40) |

Proof. We infer from Borodin and Salminen [9, Eq. (1.2.4)] that

| (41) |

so that the random variable is exponentially distributed with rate . It follows that and, by Lemma 16, the Average Value-at-Risk is

The result follows by substituting (39) for .

Remark 19 (Units)

Note that is measured in monetary units ($, say). Then the unit of is in the same monetary unit as well, which identifies (40) as a relevant economic quantity.

Remark 20 (Premium loadings, )

The premium loading is in the denominator of (40). As a consequence, the capital injection required in case after ruin is much higher for small premium loadings. Although evident from economic perspective, this is a plea for sufficient premium loadings and it is not possible to recover a company in a competitive market where premium margins are not sufficient.

Corollary 21

The average capital required to recover a firm from ruin is

| (42) |

even if the underlying risk process is driven by the fractional (FPP) or non-homogeneous Poisson process, provided that is unbounded.

Proof. The process (27) with is symmetric and in the limit thus is a time-changed Brownian motion. As in Corollary 13 it is thus sufficient to recall that the range of the process is almost surely.

5.2 The natural relation of the fractional Poisson process to the Entropic Value-at-Risk

The premium of an insurance contract with random payoff based on a risk functional is

| (43) |

This assignment does not take dependencies into account. The fractional Poisson process has an incorporated, natural dependency structure (cf. Section 4, in particular 4.2 above) and so it is natural to choose

| (44) |

as a fair premium in a regime, where dependencies cannot be neglected; by convexity of the risk functional (cf. (i) and (iv) in Definition 14), the premium (43) is more expensive than (44). In a regime base on the fractional Poisson process, the claims up to time are and thus the quantity

is of particular interest.

The Entropic Value-at-Risk has natural features, which combine usefully with the fractional Poisson process.

Definition 23

For an -valued random variable , the entropic Value-at-Risk at risk level is

The Entropic Value-at-Risk derives its name from the constraint , which is the entropy. The convex conjugate (i.e., the dual representation, cf. [1]) of the Entropic Value-at-Risk is given by

| (45) |

The representation (45) bases the Entropic Value-at-Risk on the moment generating function. This function is explicitly available for the fractional Poisson process. This allows evaluating

for specific based on the fractional Poisson process by a minimization exercise with a single variable via (45).

Proposition 24 (Moment generating function)

Assume that the random variables , are iid. Then the moment generating function of the process loss with respect to the fractional Poisson process up to time is given explicitly by

| (46) |

where is the moment generating function of , .

Proof. can be given by employing (3) as

After formally substituting we get

which is the desired assertion.

5.3 The risk process at different levels of

In what follows we compare the fractional Poisson process with the usual compounded Poisson process. To achieve a comparison on a like for like basis the parameters of the processes are adjusted so that both have comparable claim numbers. The fractional Poisson process imposes a covariance structure which accounts for accumulation effects, which are not present for the classical compound Poisson process. Employing the Entropic Value-at-Risk as premium principle we demonstrate that the premium, which is associated with the fractional process, is always higher than the premium associated with the compound Poisson process.

To obtain the comparison on a like for like basis we recall from (24) that the number of claims of the fractional Poisson process grows as , which is much faster than the claim number of a usual compound Poisson process and hence, the fractional Poisson process generates much more claims than the compound Poisson process at the beginning of the observation (cf. also Remark 9). To compare on a like for like basis we adjust the intensity or change the time so that the comparison is fair, that is, we assume that the claims of the classical compounded Poisson process triggered by (denoted ) and the fractional Poisson process are related by

| (47) |

note that equality in (47) corresponds to the situation of Poisson processes at different levels, but with an identical number of average claims up to time (, resp.).

Proposition 25

Proof. It holds that

| (49) |

indeed, the statement is obvious for and and by induction we find that

| (50) | ||||

i.e, Equation (49), where we have employed the induction hypothesis in (50). We conclude that

From the moment generating function we have by (46) that

Now assume that and thus by Jensen’s inequality and we have that whenever . The statement then follows from (45) together with (46).

Remark 26

We mention that the mapping is not monotone in general, so the result in Propositon 25 does not extend to a comparison for all s.

6 Summary and conclusion

This paper introduces the fractional Poisson process and discusses its relevance in companies which are driven by some counting process. Empirical evidence supporting the fractional Poisson process is given by considering high frequency data and the classical Danish fire insurance data. A natural feature of the fractional Poisson process is its dependence structure. We demonstrate that this dependence structure increases risk in a regime governed by the fractional Poisson process in comparison to the classical process.

The fractional Poisson process can serve as a stress test for insurance companies, as the number of claims is higher at its start. It can hence have importance for start ups and for re-insurers, which have a very particular, dependent claim structure in their portfolio.

It is demonstrated that quantities as the average capital to recover after ruin is independent of the risk level of the fractional Poisson process. Further, the Entropic Value-at-Risk is based on the moment generating function of the claims, and for this reason the natural combination of the fractional Poisson process and the Entropic Value-at-Risk is is demonstrated.

7 Acknowledgment

N. Leonenko was supported in particular by Australian Research Council’s Discovery Projects funding scheme (project DP160101366) and by project MTM2015-71839-P of MINECO, Spain (co-funded with FEDER funds).

References

- [1] Ahmadi-Javid, A. and Pichler, A. (2017) An analytical study of norms and Banach spaces induced by the entropic value-at-risk, Mathematics and Financial Economics vol. 11(4), 527–550

- [2] Aletti, G., Leonenko, N. N. and Merzbach, E. (2018) Fractional Poisson processes and martingales, Journal of Statistical Physics, 170, N4, 700–730.

- [3] Artzner, P., Delbaen, F., Eber, J-M and Heath, D. (1999) Coherent Measures of Risk, Mathematical Finance 9, 203–228

- [4] Beghin, L. and Macci, C. (2013) Large deviations for fractional Poisson processes, Stat. & Prob. Letters, 83(4), 1193–1202, doi: 10.1016/j.spl.2013.01.017

- [5] Beghin, L. and Orsingher, E. (2009) Fractional Poisson processes and related planar random motions, Electron. J. Probab. 14, no. 61, 1790–1827.

- [6] Beghin, L. and Orsingher, E. (2010) Poisson-type processes governed by fractional and higher-order recursive differential equations. Electron. J. Probab. 15, no. 22, 684–709.

- [7] Biard, R., Saussereau, B. (2014) Fractional Poisson process: long-range dependence and applications in ruin theory. J. Appl. Probab. 51, no. 3, 727–740.

- [8] Bingham, N. H. (1971) Limit theorems for occupation times of Markov processes, Z. Wahrscheinlichkeitstheorie und Verw. Gebiete 17, 1–22.

- [9] Borodin, A. N. and Salminen, P. (2012) Handbook of Brownian motion-facts and formulae, Birkhäuser, doi:10.1007/978-3-0348-7652-0.

- [10] Cahoy, D. O., Uchaikin, V. V. and Woyczynski, W. A. (2010) Parameter estimation for fractional Poisson processes, J. Statist. Plann. Inference, 140, no. 11, 3106–3120.

- [11] Cont, R. and Tankov, P. (2004) Financial Modeling With Jump Processes, Chapman & Hall/ CRC.

- [12] Daley, D. J. (1999) The Hurst index for a long-range dependent renewal processes, Annals of Probablity, 27, no 4, 2035-2041.

- [13] Grandell, J. (1991) Aspects of Risk Theory, Springer, New York.

- [14] Haubold, H. J., Mathai, A.M. and Saxena, R.K. (2011) Mittag-Leffler functions and their applications. J. Appl. Math. Art. ID 298628, 51 pp.

- [15] Kataria, K. K. and Vellaisamy, P. (2018) On densities of the product, quotient and power of independent subordinators. J. Math. Anal. Appl. 462, 1627–1643.

- [16] Kerss, A. and Leonenko, N. N. and Sikorskii, A. (2014) Fractional Skellam processes with applications to finance. Fract. Calc. & Appl. Analysis. 17, pp. 532–551.

- [17] Khinchin, A. Y. (1969) Mathematical Methods in the Theory of Queueing. Hafner Publishing Co., New York.

- [18] Kumar, A. and Vellaisamy, P. (2015) Inverse tempered stable subordinators. Statist. Probab. Lett. 103, pp. 134–141.

- [19] Kusuoka, S. (2001) On law invariant coherent risk measures. Advances in mathematical economics, Vol. 3 Ch. 4, Springer, 83–95

- [20] Laskin, N. (2003) Fractional Poisson process. Chaotic transport and complexity in classical and quantum dynamics, Commun. Nonlinear Sci. Numer. Simul. 8, no. 3-4, 201–213.

- [21] Leonenko, N. N., Meerschaert, M. M. and Sikorskii, A. (2013) Correlation structure of fractional Pearson diffusions, Computers and Mathematics and Applications, 66, 737–745.

- [22] Leonenko, N. N., Meerschaert, M. M. and Sikorskii, A. (2013) Fractional Pearson diffusions, Journal of Mathematical Analysis and Applications, 403, 532–246.

- [23] Leonenko, N. N., Meerschaert, M. M., Schilling, R. L. and Sikorskii, A. (2014) Correlation structure of time-changed Lévy processes. Commun. Appl. Ind. Math. 6, no. 1, e-483, 22 pp.

- [24] Leonenko, N. N. and Merzbach, E. (2015) Fractional Poisson fields, Methodology and Computing in Applied Probability, 17, no.1, 155–168.

- [25] Leonenko, N. N., Scalas, E. and Trinh, M. (2019) Limit Theorems for the Fractional Non-homogeneous Poisson Process, J. Appl. Prob., In Press.

- [26] Leonenko, N. N., Scalas, E. and Trinh, M. (2017) The fractional non-homogeneous Poisson process, Statistic and Probability Letters, 120, 147–156.

- [27] Mainardi, F., Gorenflo, R. and Scalas, E. (2004) A fractional generalization of the Poisson processes, Vietnam J. Math. 32, Special Issue, 53–64.

- [28] Mainardi, F., Gorenflo, R. and Vivoli, A. (2005) Renewal processes of Mittag-Leffler and Wright type, Fract. Calc. Appl. Anal. 8, no. 1, 7–38.

- [29] Mainardi, F., Gorenflo, R. and Vivoli, A. (2007) Beyond the Poisson renewal process: a tutorial survey. J. Comput. Appl. Math. 205, no. 2, 725–735.

- [30] Malinovskii, V. (1998) Non-Poissonian claims’ arrival and calculation of the ruin, Insurance Math. Econom. 22, 123–222.

- [31] Meerschaert, M. M., Nane, E. and Vellaisamy, P. (2011) The fractional Poisson process and the inverse stable subordinator, Electron. J. Probab. 16, no. 59, 1600–1620.

- [32] Meerschaert, M. M. and Sikorskii, A. (2012) Stochastic Models for Fractional Calculus, De Gruyter, Berlin/Boston.

- [33] Mikosch, T. (2009) Non-life insurance mathematics, an introduction with the Poisson process. Springer.

- [34] Pflug, G. Ch. and Römisch, W. (2007) Modeling, Measuring and Managing Risk, World Scientific, doi: 10.1142/9789812708724

- [35] Podlubny, I. (1999) Fractional differential equations. An introduction to fractional derivatives, fractional differential equations, to methods of their solution and some of their applications, Mathematics in Science and Engineering, 198, Academic Press, Inc., San Diego, CA.

- [36] Raberto, M., Scalas, E. and Mainardi, F. (2002) Waiting times and returns in high-frequency financial data: an empirical study, Physica A, 314, 749–755.

- [37] Repin, O. N. and Saichev, A. I. (2000) Fractional Poisson law, Radiophysics and Quantum Electronics, 43, no. 9, 738–741.

- [38] Samorodnitsky, G. and Taqqu, M. S. (1994) Stable Non-Gaussian Random Processes. Chapman & Hall, New York.

- [39] Scalas, E., Gorenflo, R., Luckock, H., Mainardi, F., Mantelli, M. and Raberto, M. (2004). Anomalous waiting times in high-frequency financial data, Quant. Financ. 4, 695–702.

- [40] Veillette, M. and Taqqu, M. S. (2010) Numerical computation of first passage times of increasing Lévy processes, Methodol. Comput. Appl. Probab. 12, no. 4, 695–729.

- [41] Veillette, M. and Taqqu, M. S. (2010) Using differential equations to obtain joint moments of first-passage times of increasing Lévy processes, Statist. Probab. Lett. 80, no. 7-8, 697–705.

- [42] Wang, X.-T. and Wen, Z.-X. (2003) Poisson fractional processes, Chaos Solitons Fractals, 18, no. 1, 169–177.

- [43] Wang, X.-T., Wen, Z.-X. and Zhang, S.-Y. (2006) Fractional Poisson process. II, Chaos Solitons Fractals, 28, no. 1, 143–147.

- [44] Wang, X.-T., Zhang, S.-Y. and Fan, S. (2007) Nonhomogeneous fractional Poisson processes. Chaos Solitons Fractals, 31, no. 1, 236–241.

- [45] Young, V. R. (2006) Premium Principles in Encyclopedia of Actuarial Science.