Pricing without martingale measure

Abstract

For several decades, the no-arbitrage (NA) condition and the martingale measures have played a major role in the financial asset’s pricing theory. We propose a new approach for estimating the super-replication cost based on convex duality instead of martingale measures duality : Our prices will be expressed using Fenchel conjugate and bi-conjugate. The super-hedging problem leads endogenously to a weak condition of NA called Absence of Immediate Profit (AIP). We propose several characterizations of AIP and study the relation with the classical notions of no-arbitrage. We also give some promising numerical illustrations.

keywords:

Financial market models \sepSuper-hedging prices \sepNo-arbitrage condition \sepConditional support \sepEssential supremum. 2000 MSC: 60G44 \sepG11-G131 Introduction

The problem of giving a fair price to a financial asset is central in the economic and financial theory. A selling price should be an amount which is enough to initiate a hedging strategy for , i.e. a strategy whose value at maturity is always above . It seems also natural to ask for the infimum of such amount. This is the so called super-replication price and it has been introduced in the binomial setup for transaction costs by [7]. Characterizing and computing the super-replication price has become one of the central issue in mathematical finance theory. Until now it was intimately related to the No-Arbitrage (NA) condition. This condition asserts that starting from a zero wealth it is not possible to reach a positive one (non negative almost surely and strictly positive with strictly positive probability measure). Characterizing the NA condition or, more generally, the No Free Lunch condition leads to the Fundamental Theorem of Asset Pricing (FTAP in short). This theorem proves the equivalence between those absence of arbitrage conditions and the existence of equivalent risk-neutral probability measures (also called martingale measures or pricing measures) which are equivalent probability measures under which the (discounted) asset price process is a martingale. This was initially formalised in [13], [14] and [20] while in [10] the FTAP is formulated in a general discrete-time setting under the NA condition. The literature on the subject is huge and we refer to [11] and [17] for a general overview. Under the NA condition, the super-replication price of is equal to the supremum of the (discounted) expectation of computed under the risk-neutral probability measures. This is the so called dual formulation of the super-replication price or superhedging theorem. We refer to [29] and [12] and the references therein.

In this paper, a super-hedging or super-replicating price is the initial value of some super-hedging strategy. We do not postulate any assumption on the financial market and analyze from scratch the set of super-hedging prices and its infimum value, which will be called the infimum super-hedging cost. Under mild assumptions, we show that the one-step set of super-hedging prices can be expressed using Fenchel-Legendre conjugate and the infimum super-replication cost is obtained by the Fenchel-Legendre biconjugate. So, we use here the convex duality instead of the usual financial duality based on martingale measures under the NA condition. To do so, we use the notion of conditional essential supremum. Using measurable selection techniques, we show that the conditional essential supremum of a function of is equal to the usual supremum of the function evaluated on a random set, the conditional support of (see Proposition 2.9). The pricing formula that we obtain (see (2.14)) shows that, if the initial stock price does not belong to the convex hull of the conditional support of the stock value at the end of the period then the super-hedging cost is equal to . To exclude this possibility we postulate the condition of Absence of Immediate Profit (AIP). The AIP is an endogenous condition for pricing and is indeed very weak : If the initial information is trivial, a one period immediate profit is a strategy which starts from 0 and leads to a deterministic strictly positive gain at time 1. We propose several characterization of the AIP condition. In particular we show that AIP is equivalent to the non-negativity of the super-hedging prices of any fixed call option. We also discuss in details the link between AIP and the others no-arbitrage conditions as the no-arbitrage of first and second type and the no-riskless arbitrage of [15] and the No Unbounded Profit with Bounded Risk of [19]. None of the conditions is equivalent to AIP, the closest being the no-riskless arbitrage. Under AIP condition, we show that the one-step infimum super-hedging cost is the concave envelop of the payoff relatively to the convex envelop of the conditional support. Fenchel-Legendre duality have already been used to obtain a dual representation of the super-replication price thanks to deflators (see [24, Exemple 4.2] and [25, Theorem 10 and Corollary 15]). In [25, Theorem 10] the result is shown under the assumption that the set of claims that can be super-replicate from is closed, which holds true under NA. Our approach is different as we do not postulate any assumption on the market and, actually, we do not seek for a dual representation of the (minimal) super-hedging price.

We then consider the multiple-period framework. We show that the global AIP condition and the local ones are equivalent. We study the link between AIP, NA and the absence of weak immediate profit (AWIP) conditions. We show that the AIP condition is the weakest-one and we also provide conditions for the equivalence between the AIP and the AWIP conditions, as well as characterization through absolutely continuous martingale measure.

We then focus on a particular, but still general setup, where we propose a recursive scheme for the computation of the super-hedging prices of a convex option. We obtain the same computation scheme as in [8] and [9] but here it is obtained by only assuming AIP instead of the stronger NA condition. We also give some numerical illustrations. We calibrate historical data of the french index CAC to our model and implement our super-hedging strategy for a call option. Our procedure is somehow model free as it is only based on statistical estimations.

The paper is organized as follows. In Section 2, we study the one-period framework while in Section 3 we study the multi-period one. Section 4 proposes an explicit pricing for a convex payoff and numerical experiments.

In the remaining of this introduction we present our framework and notations. Let be a complete filtered probability space, where is the time horizon. For any -algebra and any , we denote by the set of -measurable and -valued random variables. We consider a non-negative process such that for all . The vector represents the price at time of the risky assets in the financial market in consideration. Trading strategies are given by a process such that for all . The vector represents the investor’s holding in the risky assets between time and time . We assume that trading is self-financing and that the riskless asset’s price is a constant equal to . The value at time of a portfolio starting from initial capital is then given by

where for and is the scalar product of and .

2 The one-period framework

Let and be two complete sub--algebras of such that and which represent respectively the initial and the final information. Let and be two non-negative111For ease of notation, we assume that and for all . random variables. They represents the initial and the final prices of the risky assets.

Finally, we introduce and the associated derivative , where

The objective of the section is to obtain under suitable assumptions on a characterization of , the one-step set of super-hedging (or super-replicating) prices of and of its infimum value. The setting will be applied in Section 3 with the choices , , and .

Definition 2.1.

The set of super-hedging prices of the contingent claim consists in the initial values of super-hedging strategies :

The infimum super-hedging cost of is defined by .

The notions of conditional essential infimum and conditional essential supremum are at the heart of this study and will be defined in Proposition 2.5 below. We will also use the conditional support of which is introduced in Definition 2.2 below. In Section 2.2, we derive the characterization of and from the following steps :

-

1.

Observe that the set of super-hedging prices can be rewritten using a conditional essential supremum (see (2.8)).

-

2.

Show that under mild conditions the conditional essential supremum of a function of is equal to the usual supremum of the function evaluated on the random set (see Proposition 2.9).

-

3.

Recognize that a super-hedging price can be written using a Fenchel-Legendre conjugate (see (2.9)).

-

4.

Take the essential infimum of the set of super-hedging prices and go through the three first steps to recognize the Fenchel-Legendre biconjugate (see (2.11)).

- 5.

With this pricing formula in hand (see (2.14)), the condition of Absence of Immediate Profit (AIP) appears endogenously. In Section 2.3, we develop the concept of AIP and propose several characterization of the AIP condition and compare it with the classical No Arbitrage NA condition.

2.1 Conditional support and conditional essential infimum

This section is the toolbox of the paper. We recall some results and notations that will be used without further references in the rest of the paper. Let . The effective domain of is defined by

and is proper if dom and for all .

Next, if is -normal integrand (see Definition 14.27 in [28]) then is -measurable and is lower semi-continuous (l.s.c. in the sequel, see [28, Definition 1.5]) in and the converse holds true if is complete for some measure, see [28, Corollary 14.34].

Note that, if and is -measurable, then

.

A random set is said -measurable if for all open set of , the subset .

If is a -measurable and closed-valued random set of , then admits a Castaing representation (see Theorem 14.5 in [28]). This means that

for all , where the closure is taken in .

First, we introduce the conditional support of with respect to .

Definition 2.2.

Let be a -stochastic kernel (i.e. for all , is a probability on and is -measurable for all ). We define the random set by :

| (2.1) |

For , is called the support of .

Let , we denote by the set defined in (2.1) when is a regular version of the conditional law of knowing . The random set

is called the conditional support of with respect to .

Remark 2.3.

Lemma 2.4.

is non-empty, closed-valued, -measurable and graph-measurable random set (i.e. ).

Proof. It is clear from (2.1) that, for all , is a non-empty and closed subset of . We show that is -measurable. Let be a fixed open set in and As is a stochastic kernel, is -measurable. By definition of we get that and is -measurable. Now using Theorem 14.8 of [28], (recall that is closed-valued) and is -graph-measurable.

It is possible to incorporate measurability in the definition of the essential supremum (see [17, Section 5.3.1] for the definition and the proof of existence of the classical essential supremum). This has been done by [3] for a single real-valued random variable and by [18] for a family of vector-valued random variables and with respect to a random partial order (see [18, Definition 3.1 and Lemma 3.9]). Proposition 2.5 is given and proved for sake of completeness and for pedagogical purpose. The authors thanks T. Jeulin who suggested this (elegant) proof.

Proposition 2.5.

Let be two -algebras on a probability space. Let be a family of real-valued -measurable random variables. There exists a unique -measurable random variable denoted which satisfies the following properties:

-

1.

For every , a.s.

-

2.

If satisfies a.s. , then a.s.

The conditional essential infimum is defined symmetrically.

Proof.

Considering the homeomorphism we can restrict our-self to taking values in . We denote by a regular version of the conditional law of knowing . Let such that a.s. .

This is equivalent to and a.s. follows from Definition 2.2.

Let

| (2.2) |

Then a.s. and it is easy to see that is -measurable. So taking the classical essential supremum, we get that a.s. and that is -measurable. We conclude that a.s. since for every , (see Remark 2.3).

Remark 2.6.

Let be an absolutely continuous probability measure with respect to . Let and be the expectation under . As for every , a.s. and is -measurable,

| (2.3) |

Inspired by Theorem 2.8 in [3], we may easily show the following tower law property.

Lemma 2.7.

Let be -algebras and let be a family of real-valued -measurable random variables. Then,

Lemma 2.8.

Assume that and consider . Then, we have a.s. that

| (2.4) |

where is the convex envelop of , i.e. the smallest convex set that contains .

Proof. The two first statements follow from the construction of in Proposition 2.5 (see (2.2)). Suppose that on some non-null measure subset of . As is -measurable and closed-valued, by a measurable selection argument, we deduce the existence of such that and on . As a.s. (see Remark 2.3) and a.s., we deduce that on , which contradicts the definition of . The next statement is similarly shown and the last one follows directly.

The following proposition is one of the main ingredient of the paper. It extends the fact that (see (2.2)) and allows to compute a conditional essential supremum as a classical supremum but on a random set.

Proposition 2.9.

Let such that and let be a -measurable function which is l.s.c. in . Then,

| (2.5) |

The proposition has the following easy extension. The proof is postponed to the appendix.

Corollary 2.10.

Let such that for all and is a -measurable and closed-valued random set. Let be a -measurable function which is l.s.c. in . Then,

| (2.6) |

Note that, if is countable, is clearly -measurable. If , then , which is again

-measurable and also closed-valued.

The proof of Proposition 2.9 is based on the two following useful lemmata.

Lemma 2.11.

Let be a -measurable and closed-valued random set such that and let be l.s.c. in . Then,

| (2.7) |

where is a Castaing representation of .

Lemma 2.12.

Let be a -measurable and closed-valued random set such that and let be a -measurable function such that is l.s.c. for all . Then is -measurable.

Proof. Lemma 2.11 implies that where is a Castaing representation of . It implies that for any fixed

As is -measurable and is -measurable, is -measurable and so is .

Proof of Proposition 2.9. As (see Remark 2.3) we have that a.s. and the definition of implies that a.s. since is -measurable by Lemmata 2.4 and 2.12.

Let be a Castaing representation of Lemma 2.11 implies that Fix some rational number and set , where is the closed ball of center and radius . Note that . Indeed if it does not hold true on some such that and by definition 2.2, on , which contradicts . By definition of the essential supremum, we have that a.s. and that is -measurable. This implies for all fixed , where is of full measure, that

As is l.s.c. (recall [28, Definition 1.5, equation 1(2)]), we have that

So on the full measure set , . Taking the supremum over all , we get that

2.2 Fenchel-Legendre conjugate and bi-conjugate to express super-replication prices and cost

We are now in position to perform the points 1 to 4 of the program announced in the beginning of the section.

Proposition 2.13.

| (2.8) |

Suppose that is a -normal integrand. Then, for , we get that

| (2.9) |

where is the Fenchel-Legendre conjugate of i.e.

| (2.10) |

where if and else. Moreover, we have that

| (2.11) |

where is the Fenchel-Legendre biconjugate of i.e.

Notice that the infimum super-hedging cost is not a priori a price, i.e. an element of , as the later may be an open interval.

Remark 2.14.

Fenchel-Legendre duality have already been used many times in financial mathematics. In particular, Pennanen obtains a dual representation of the super-replication price thanks to deflators (see [24, Exemple 4.2] and [25, Theorem 10 and Corollary 15]). The proof of [25, Theorem 10] is also based on the convex biconjugate theorem but the result is shown under the assumption that the set of claims that can be super-replicate from (see (2.15)) is closed, which holds true under the no-arbitrage condition. In [26], the existence and the absence of duality gap in a general stochastic optimization problem is proved through dynamic programming and under a condition (that does no rely on inf-compactness) of linearity on sets constructed with recession functions. This condition in classical mathematical finance problems is equivalent to the no-arbitrage condition (see [26, Exemple 1]). Our approach is different as we do not postulate any assumption on the market and we deduce from the biconjugate representation the condition that should be satisfied by the market. In particular, the goal is not to obtain a dual representation thanks to deflator or martingale measures.

Proof. As if and only if there exists such that , we get by definition of the conditional essential supremum (see Proposition 2.5) that (2.8) holds true. Then (2.9) follows from Proposition 2.9. Lemma 2.4 will be in force. First, it implies that is -measurable and l.s.c. As is non-empty (see Remark 2.3) is convex and l.s.c. as the supremum of affine functions. Hence is also l.s.c. and convex. Moreover, using Lemma 2.12, is -measurable. We obtain that a.s.

The first equality is a direct consequence of (2.8), the second one is trivial. We prove the third one. First, remark that coincides with Moreover, as is -measurable,

and is -measurable (see [28, Theorem 14.8]). Since is a -measurable function and is convex and thus u.s.c. on , we may apply Corollary 2.10 and we obtain that a.s.

We now introduce the notations needed to perform the point 5 of our program. Let is the convex envelop of i.e. the greatest convex function dominated by

The concave envelop is defined symmetrically and denoted by . We also define the (lower) closure of as the greatest l.s.c. function which is dominated by i.e.

. The upper closure is defined symmetrically.

It is easy to see that

It is well-known (see for example [28, Theorem 11.1]) that

Moreover, if is proper, is also proper, convex and l.s.c. and

| (2.12) |

We are now on position to obtain the representation of the infimum super-hedging cost.

Proposition 2.15.

Suppose that is a -normal integrand and that there exists some concave function such that on 222This is equivalent to assume that there exists , such that for all . and on . Then, a.s.

| (2.14) | |||||

where the relative concave envelop of with respect to is given by

Note that [8] and [6] have represented the super-hedging price as

a concave envelop but this was done under the no-arbitrage condition using the dual representation of the super-replication price through martingale measures.

Proof.

We want to use (2.12) in order to compute .

The convex envelop of can be written as follows (see [28, Proposition 2.31]):

Let for some such that and .

Assume that . Then (see [28, Proposition 2.27, Theorem 2.29]),

there exists at least one and and also .

If , by definition .

As is non-empty (see Remark 2.3), is proper if and only if for all and this holds true since

As for all , we get that and one may write that

and using Proposition 2.13 and (2.12)

2.3 The AIP condition

Proposition 2.15 shows that if, , the infimum super-hedging price of a European claim equals . This leads to the natural notion of absence of immediate profit that we present now. It is important to note that this notion is endogenous to the problem of super-replication contrary to the NA condition. Let be the set of all -measurable claims that can be super-replicate from .

| (2.15) |

Then,

Note that so We say that there is an immediate profit when i.e. if it is possible to super-replicate the contingent claim at a negative super-hedging price.

Definition 2.16.

There is an immediate profit (IP) if . On the contrary case if a.s. we say that the Absence of Immediate Profit (AIP) condition holds.

We know propose several characterisations of the AIP condition. We will discuss in Lemma 2.22 and Remark 2.23, the link with the classical no-arbitrage condition and show that AIP is indeed very week.

Proposition 2.17.

AIP holds if and only if one of the following condition holds true.

-

1.

a.s. or a.s.

-

2.

a.s. where is the support function of

-

3.

or

Remark 2.18.

In the case , (2.4) implies that the previous conditions are equivalent to

Example 2.19.

The AIP condition is very easy to check in practice. For , let . To check AIP, compute either or and and compare with . For example, let where is a Brownian motion and and . Then and AIP holds true. We propose in Example 2.25 other situation where AIP is easily verified.

Proof.

The assumptions of Proposition 2.15 are satisfied for

and we get that

a.s. Hence, AIP holds true if and only if a.s. or equivalently a.s. and AIP is equivalent to 1.

Using Proposition 2.13, we get that

Proposition 2.9 implies that for

So, if and only if a.s. and and are equivalent. To achieve the proof, it remains to prove that a.s. is equivalent to a.s. First remark that

So, it remains to prove that for any closed convex set , if and only if . If it is clear that

. Assume that . Then by Hahn-Banach theorem there exists some and some such that

for all and follows.

Corollary 2.20.

The AIP condition holds true if and only if a.s. for some non-negative -normal integrand such that there exists some concave function verifying that .

In particular, the AIP condition holds true if and only if the infimum super-hedging cost of some European call option is non-negative. Note that under AIP the price of some non-zero call option may be zero (see Example 2.28 below).

Proof.

Assume that AIP condition holds true. Then, from Definition 2.16, we get that a.s. As , it is clear that a.s.

Conversely, assume that there exists some IP. Proposition 2.15 implies that

IP and Proposition 2.17 lead to and, since

The converse is proved.

We now compare the AIP condition with the classical No Arbitrage NA one, whose definition is recalled below.

Definition 2.21.

The No Arbitrage NA condition holds true if for , a.s. implies that a.s. or equivalently if

Lemma 2.22.

The AIP condition is strictly weaker than the NA one.

Remark 2.23.

The AIP condition is tailor-made for pricing issues. It allows to give a super-hedging price even in case of arbitrage opportunity (see example 2.28 below).

Note that an IP is a very strong strategy. Assume that is trivial, then an IP corresponds to some such that is determinist and strictly positive. So excluding IP and not NA may be not enough to get existence in the problem of maximization of expected utility.

We compare IP with other notions of arbitrage as introduced by Ingersoll (see [15]) in a one step setting with a finite set of states of the world. Arbitrage opportunity of the first type is the classical arbitrage. An arbitrage opportunity of the second type

is limited liability investments with a current negative commitment. As we assume the existence of a riskless asset, it means that is not determinist but always greater that some strictly positive deterministic number. Finally, a riskless arbitrage

opportunity is a nonpositive investment with a constant, positive profit. This notion is equivalent to our notion of IP (recall that there exits a riskless asset) in the context of a trivial initial filtration. If is not trivial anymore, a riskless arbitrage is an IP but the converse is not true anymore.

An unbounded profit with bounded risk is some such that and Let us show that one can have AIP and some unbounded profit with bounded risk. Fix and choose some random variables and such that and where

Here, AIP holds true (recall Remark 2.18). Observe that

a.s. Now if a.s. then , i.e. a contradiction. So the constant strategy equal to 1 is an unbounded profit with bounded risk.

Proof.

It is clear from Proposition 2.17 and Definition 2.21 that NA implies AIP. Fix and choose some random variables and such that and where

Here, AIP holds true (recall Remark 2.18). Observe that

a.s. Now if a.s. then , i.e. a contradiction. So the constant strategy equal to 1 is an arbitrage opportunity.

We propose now a condition for the equivalence between NA and AIP when .

Lemma 2.24.

Assume that and that . Then AIP and NA are equivalent conditions.

Lemma 2.24 applies if , and .

Proof.

We have already seen that NA implies AIP. Assume that AIP holds true. Using Remark 2.18,

Let such that . On the set , we have that hence . We deduce that . Similarly, we get that and finally .

Example 2.25.

We now provide an other example where AIP holds true and is strictly weaker than NA in the case . First, notice that, if there exists such that is a -super martingale and a -sub martingale, then AIP holds true. Indeed, let for As a.s., and are -measurable, we get that a.s. (see (2.3)) and . So Remark 2.18 implies that AIP holds true.

Let us consider , such that a.s. We define and where is chosen such that a.s. Morever, we suppose that on a non null set that we arbirarily choose. By construction, AIP holds, since and . Suppose that NA holds, then by the FTAP, there exists such that . This implies that

In particular, we have on . This contradicts the hypothesis a.s. We may also show directly that is an arbitrage opportunity. Indeed which is a.s. stricly positive.

We now provide the characterization of the infimum super-hedging cost under the AIP condition.

Corollary 2.26.

Suppose that AIP holds true. Let be a -normal integrand, such that there exists some concave function verifying that on and on . Then, a.s.

If is concave and u.s.c., a.s.

Proof.

The first equalities are a direct consequence of Proposition 2.15. If is concave and u.s.c., the result is trivial.

We finish the one-period study with the computation of the infimum super-hedging cost of a convex derivative when .

In this case, the cost is in fact a super-hedging price and we get the super-hedging strategy explicitly.

Corollary 2.27.

Suppose that AIP holds true and that . Let be a non-negative convex function with and , then a.s.

| (2.17) | |||||

| (2.18) |

where we use the conventions in the case a.s. and if a.s. Moreover, .

Example 2.28.

We compute the price of a call option under AIP in the case . Let for some .

-

•

If then and . As AIP condition holds true, .

-

•

If then and . As is concave and u.s.c., a.s.

- •

We finish with an example of computation of a call price under AIP but when there is some arbitrage opportunity. We choose a simple model that will be studied in Section 4. We assume that a.s. and a.s. for two constants and . From Remark 2.18, AIP is equivalent to and . If (and ) or and (), AIP holds but the NA condition does not hold true. Suppose that and . If , the super-replication price under AIP is and if it is . Suppose that and . If , the super-replication price under AIP is and if it is zero.

Proof. As is convex, the relative concave envelop of with respect to is the affine function that coincides with on the extreme points of the interval and (2.17) and (2.18) follow from Remark 2.18. Then using (LABEL:eqfenchprix), we get that a.s. (recall that ) and this implies by (2.17) that

| (2.19) |

and follows.

3 The multi-period framework

3.1 Multi-period super-hedging prices

For every the set of all claims that can be super-replicated from the zero initial endowment at time is defined by

| (3.20) |

The set of (multi-period) super-hedging prices and the (multi-period) infimum super-hedging cost of some contingent claim at time are given by for all by

| (3.21) | |||||

As in the one-period case, it is clear that the infimum super-hedging cost is not necessarily a price in the sense that when is not closed.

We now define a local version of super-hedging prices. Let , then the set of one-step super-hedging prices of and it associated infimum super-hedging cost are given by

The following lemma makes the link between local and global super-hedging prices under the assumption that the infimum (global) super-replication cost is a price. It also provides a dynamic programming principle.

Lemma 3.1.

Let and . Then

Moreover, assume that . Then

Remark 3.2.

Proof. Let and for all

The set contains at time all the super-hedging prices for some price at time . First we prove that for all

| (3.22) |

It is clear at time . Let . Let . Then there exists for all , such that a.s. So

and and recursively . Conversely, let , then there exists and such that Then as there exists and such that Going forward until , we get that a.s. and follows. This achieve the proof of (3.22).

3.2 Multi-period AIP

We now define the notion of global and local immediate profit at time . The global (resp. local) profits mean that it is possible to super-replicate from a negative cost at time the claim payed at time (resp. time ). We will see that they are equivalent.

Definition 3.3.

Fix . A global immediate profit (IP) at time is a non-null element of . We say that AIP condition holds at time if there is no global IP at :

A local immediate profit (LIP) at time is a non-null element of . We say that (ALIP) condition holds at time if there is no local IP at :

Finally we say that the AIP (resp. ALIP) condition holds true if the AIP (resp. ALIP) condition holds at time for all .

Theorem 3.4 below proposes several characterization of the (AIP) condition.

Theorem 3.4.

AIP holds if and only if one of the the following assertions holds.

-

1.

ALIP holds true.

-

2.

or for all

-

3.

for all

-

4.

a.s. for all

Remark 3.5.

Proof. At time , , thus AIP holds at and . We show by induction that if and if AIP at time holds true then and the following equivalences are true :

As AIP is equivalent to AIP at time for all , this proves the equivalence between AIP, 1., 2. , 3. and 4. Consider , assume that the induction hypothesis holds true at , and that AIP holds at time . As , Lemma 3.1 shows that and . This implies that AIP at time is equivalent to ALIP at time and together with Proposition 2.17 and Definition 2.16 shows that the induction step holds at time and that .

3.3 Absence of weak immediate profit

In this section we study a condition stronger than AIP in the spirit of the No free Lunch condition i.e. by considering the closure of the set . Before, we recall the classical multiperiod no-arbitrage NA condition.

Definition 3.6.

The no-arbitrage NA condition holds if for all

It is easy to see that the NA condition can also be formulated as follows : a.s. implies that a.s. Recall that the set of all super-hedging prices for the zero claim at time is given by (see (3.20) and (3.21)). It follows that (see Definition 3.3)

It is clear that the NA condition implies the AIP one and, by the counter-example of Lemma 2.22, the equivalence does not hold true: The AIP condition is strictly weaker than the NA one. We now introduce a weaker form of IP.

Definition 3.7.

The absence of weak immediate profit (AWIP) condition holds true if for all

where the closure of is taken with respect to the convergence in probability.

We will see in Lemma 3.10 that the AIP condition is not necessarily equivalent to AWIP. Before, in the case we show that AWIP may be equivalent to AIP condition under an extra closeness condition. It also provides a characterization through (absolutely continuous) martingale measures.

Theorem 3.8.

Assume that the case . The following statements are equivalent:

-

1.

AWIP holds.

-

2.

For every , there exists with such that is a -martingale.

-

3.

AIP holds and for every

The proof is based on classical Hahn-Banach Theorem arguments, see for example the textbooks of [11] and [17].

Remark 3.9.

From above, it is clear that AIP and AWIP are equivalent if is closed. Therefore, we deduce by Lemma 3.10 that is not necessarily closed under AIP.

Suppose now that for all . Then, using Lemma 2.24,

AIP is equivalent to NA. Under NA, the set is closed in probability for every and

Theorem 3.8 implies that AWIP, AIP and NA are equivalent conditions.

Proof. First we prove that 1. implies 2. Suppose that AWIP holds and fix some . We may suppose without loss of generality that the process is integrable under . Under AWIP, we then have where the closure is taken in . Therefore, for every nonzero , there exists by the Hahn-Banach theorem a non-zero such that (recall that is a cone) and for every . Since , we deduce that and we way renormalise so that . Let us consider the family

Consider any non-null set . Taking , since , we deduce that has a non-null intersection with . By [17, Lemma 2.1.3], we deduce an at most countable subfamily such that the union is of full measure. Therefore,

is such that and we define such that . As the subset is a linear vector space contained in , we deduce that is a -martingale.

We now prove that 2. implies 3. Suppose that for every , there exists such that is a -martingale with . Let us define for , then and . Consider , i.e. is -measurable and is of the form . Since is -measurable, admits a generalized conditional expectation under knowing and we have by assumption that . The tower law implies that a.s.

Hence a.s., i.e. AIP holds. It remains to show that .

Consider first a one step model, where is a -martingale with and . Suppose that converges in probability to . We need to show that .

On the -measurable set , by [17, Lemma 2.1.2], we may assume w.l.o.g. that is convergent to some hence is also convergent and we can conclude that .

Otherwise, on , we use the normalized sequences for

By [17, Lemma 2.1.2] again, we may assume taking sub-sequences that a.s. , and

Remark that a.s. First consider the subset on which a.s. Since a.s., we get that a.s. Hence a.s. Taking the limit, we get that a.s. and, since , we deduce that a.s. Recall that hence a.s. and . On the subset we may argue similarly and the conclusion follows in the one step model.

We now show the result in multi-step models by recursion. Fix some . We show that implies the same property for instead of . By assumption is a -martingale with for and . Suppose that

If there is nothing to prove. As before on the -measurable set , we may assume w.l.o.g. that converges to . Therefore on

and by the induction hypothesis, also converges to an element of and we conclude that .

On , we use the normalisation procedure as before, and deduce the equality

for some , and such that a.s. We then argue on and respectively.

When , we deduce that

hence a.s. under AIP, see Theorem 3.4.

Since a.s., a.s.

So,

Hence by induction. As admits a generalized conditional expectation knowing , we deduce by the tower law that a.s.

since is a -martingale. Hence a.s. As a.s. so that .

Finally, notice that the AIP condition implies AWIP as soon as the equality holds for every .

Lemma 3.10.

The AIP condition is not necessarily equivalent to AWIP.

Proof. Assume that . Let us consider a positive process which is a -martingale. We suppose that a.s., which holds in particular if a geometric Brownian motion as a.s. Let us define for and . We have and hence AIP holds at time (see Remark 2.18). Moreover, by the martingale property (see Theorem 3.8), AIP and also AWIP hold at any time . Let us suppose that AWIP holds true at . Using Theorem 3.8, there exists with such that is a -martingale where . Therefore, . Since by assumption, we deduce that hence a contradiction.

4 Explicit pricing of a convex payoff under AIP

The aim of this section is to obtain some results in a particular model where , a.s. and a.s. for every with , and are deterministic non-negative numbers. We obtain the same computative scheme (see (4.23)) as in [9] but assuming only AIP and not NA. We also propose some numerical experiments.

4.1 The algorithm

Theorem 4.1.

Suppose that the model is defined by a.s. and a.s. where , and are deterministic non-negative numbers.

-

•

The AIP condition holds true if and only if and for all .

-

•

Suppose that the AIP condition holds. Let be a non-negative convex function with such that . Then the infimum super-hedging cost of the European contingent claim is a price and it is given by

(4.23) where and , with the following conventions. When or , and and when

(4.24)

Moreover, for every , and is non-increasing for all .

In the proof, the strategy associated to the infimum super-hedging price is given and, this result is illustrated through a numerical experiment in Section 4.2.

Proof. The conditions and for all are equivalent to the AIP condition (see Remark 2.18). We denote and . We prove the second statement. Assume that AIP holds true. We establish (i) the recursive formulation given by (4.23), (ii) and (iii) . The case is immediate. As is a convex function with , is clearly a -normal integrand, we can apply Corollary 2.27 (see (2.17) and (2.18)) and we get that a.s.

| (4.25) |

where we use the conventions if either or and if . Moreover, using (2.19), we obtain that

So, using Lemma 3.1, we get that ,

and we may continue the recursion as soon as where satisfies (4.23), is convex with domain equal to , is such that for all and . To see that we distinguish three cases. If either or , and satisfies all the required conditions. If ,

with

using (4.24). The term in the r.h.s. above is larger than by convexity since

As and , for all , we get that is convex function with domain equal to since is so. The function also satisfies (4.23) (see (4.24)). Finally

The last case is when and and . It is clear that (4.25) implies (4.23). Moreover as and ,

and (4.23) implies that for all , is convex with domain equal to since is so. Moreover,

since

Remark 4.2.

The infimum super-hedging cost of the European contingent claim in our model is a price, precisely the same than the price we get in a binomial model a.s., . Moreover, as in Corollary 2.20, one can prove that the AIP condition holds at every instant if and only if the super-hedging prices of some European call option at are non-negative. The advantage of this generalization is to provide a statistical principle to compute the minimal price and the super-hedging strategy, see next section.

4.2 Numerical experiments

4.2.1 Calibration

In this section, we suppose that the discrete dates are given by , where . We assume that

where is a positive Lipschitz-continuous function on . Note that the assumptions on the multipliers and imply that

| (4.26) |

By Theorem 4.1, we deduce that the infimum super-hedging cost of the European Call option is given by defined by (4.23) with terminal condition . We extend the function on in such a way that is constant on each interval , . Such a scheme is proposed by Milstein [23] where a convergence theorem is proved when the terminal condition, i.e. the payoff function is smooth. Precisely, the sequence of functions converges uniformly to , solution to the diffusion equation:

| (4.27) |

In [23], it is supposed that the successive derivatives of the solution of the P.D.E. solution are uniformly bounded. This is not the case for the Call payoff function . On the contrary the successive derivatives of the solution of the P.D.E. explode at the horizon date, see [22]. In [2], it is proven that the uniform convergence still holds when the payoff function is not smooth provided that the successive derivatives of the solution of the P.D.E. do not explode too much.

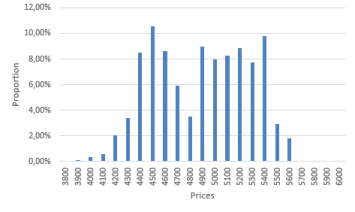

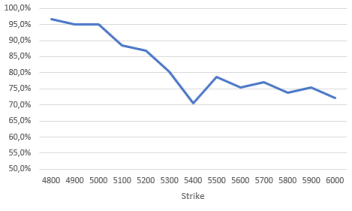

Supposing that is closed to , we can identify the observed prices of the Call option with the theoretical prices limit at any instant , given by (4.27), to deduce an evaluation of the deterministic function and test (4.26) on real data. The data set is composed of historical values of the french index CAC 40 and European call option prices of maturity months from the 23rd of October 2017 to the 19th of January 2018. The observed values of are distributed as in Figure 1.

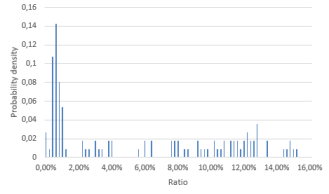

For several strikes, matching the observed prices to the theoretical ones derived from the Black and Scholes formula with time-dependent volatility (see (4.27)), we deduce the associated implied volatility and we compute the proportion of observations satisfying (4.26):

| Strike | 4800 | 4900 | 5000 | 5100 | 5200 | 5300 | 5400 | 5500 | 5600 | 5700 | 5800 | 5900 | 6000 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Ratio | 96,7% | 95,1% | 95,1% | 88,5% | 86,9% | 80,3% | 70,5% | 78,7% | 75,4% | 77,0% | 73,8% | 75,4% | 72,1% |

The results are satisfactory for strikes lower that 5100. Note that when the strike increases less prices’s data are available for the Call option as the strike is too large with respect to the current price , see Figure 1. This could explain the degradation of our results.

4.2.2 Super-hedging prices

We test the infimum super-hedging cost deduced from Theorem 4.1 on some data set composed of historical daily closing values of the french index CAC 40 from the 5th of January 2015 to the 12th of March 2018. The interval we choose corresponds to one week composed of working days so that the discrete dates are , and . We first evaluate , as

| (4.28) |

where is the empirical maximum taken over a one year sliding sample window of weeks. Notice that this estimation is model free and does not depend on the strike as it was the case in the preceding sub-section. So we estimate the volatility on 52 weeks and we implement our hedging strategy on the fifty third one. We then repeat the procedure by sliding the window of one week, We observe the empirical average of the stock price is equal to .

For a payoff function , we implement the strategy associated to the super-hedging cost given by Theorem 4.1. The super-hedging cost is given by and, using (4.25), we compute the super-hedging strategies . We denote by the terminal value of our strategy starting from the minimal price :

We study below the super-hedging error for different strikes.

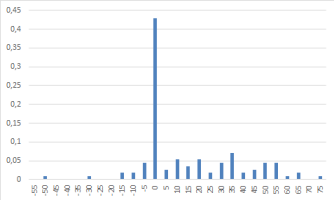

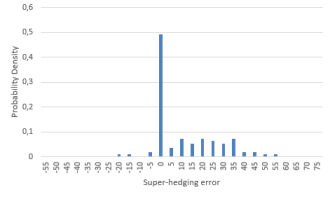

Case where . The distribution of the super-hedging error for is represented in Figure 3:

The empirical average of the error is and its standard deviation is . This result is rather satisfactory in comparison to the large value of the empirical mean of which is equal to . Notice that we observe . This empirically confirms the efficiency of our suggested method. The empirical probability of is equal to but the Value at Risk at 95 % is which confirms that our strategy is conservative.

The empirical average of is and its standard deviation is . This is again satisfactory since the theoretical super-hedging price in incomplete market is often equal to (this is for example the case when and , in particular when the dynamics of is modeled by a (discrete) geometric Brownian motion, see [8]). Note that the loss of -50 is related to so-called black friday week that occures the 24th of June 2016. Large falls of risky assets were observed in European markets mainly explained by the Brexit vote. In particular, the CAC felt from to , with a loss of on Friday.

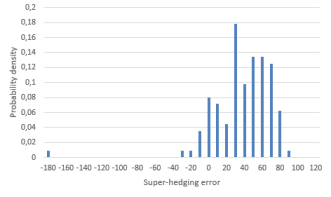

Case where . We know present the “at the money” case. The empirical average of the error is and its standard deviation is . We observe , , the probability and the Value at Risk at 95 % is . The empirical average of is and its standard deviation is .

Asymmetric case. We now propose another estimation probably more natural of the parameters of the model: and are estimated as

where the empirical minimum and maximum are taken over a one year sliding sample window of weeks, as previously.

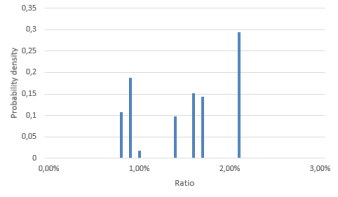

Asymmetric case where .

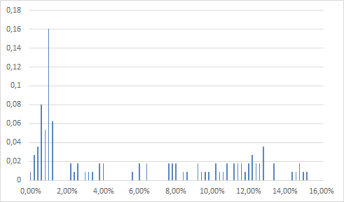

The distribution of the super-hedging error for is represented in Figure 5:

The empirical average of the error is and its standard deviation is . This result is rather satisfactory in comparison to the large value of the empirical mean of which is equal to . The empirical probability of is equal to and the Value at Risk at 95 % is which confirms that our strategy is conservative.

The empirical average of is and its standard deviation is .

Asymmetric case where .

The distribution of the super-hedging error for is represented in Figure 7:

The empirical average of the error is and its standard deviation is . The probability . The Value at Risk at 95 % is

The empirical average of is and its standard deviation is .

We now compare the result of both methods is the table below.

| Mean of | Variance of | Mean of | Variance of | VaR 95 % | ||

|---|---|---|---|---|---|---|

| Symmetric | 5.61% | 5.14 % | 12.76 | 21.65 | 14.29 % | -10.33 |

| Asymmetric | 5.52% | 5.22% | 9.47 | 14.20 | 8.04% | -1.81 |

| Mean of | Variance of | Mean of | Variance of | VaR 95 % | ||

|---|---|---|---|---|---|---|

| Symmetric | 1.51% | 0.47 % | 35.69 | 34.11 | 9.82 % | -11.41 |

| Asymmetric | 1.47% | 0.49% | 33.37 | 32.78 | 12.50% | -9.29 |

The asymmetric method perform better than the symmetric one which is not a surprise.

5 Appendix

Proof of Corollary 2.10. For all , a.s. and as is -measurable, we get that a.s.

Conversely, for all , a.s.

References

- Aliprantis and Border [2006] Aliprantis, C. D. and K. C. Border. Infinite Dimensional Analysis : A Hitchhicker’s Guide, Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, 3rd edition, 2006.

- [2] Baptiste J. and E. Lépinette . Diffusion equations: convergence of the functional scheme derived from the binomial tree with local volatility for non smooth payoff functions. Applied Mathematical Finance, 0,0 (2018), 1-22.

- [3] Barron E. N., Cardaliaguet, P. and R. Jensen . Conditional Essential Suprema with Applications. Appl Math Optim 48, 229-253, 2003.

- [4] Barron E. N., and R. Jensen A stochastic control approach to the pricing of options. Mathematics of operations research, 15,1 49-79, 1990.

- [5] Bensaid B., Lesne J.P., Pagès H. and J. Scheinkman. Derivative asset pricing with transaction costs . Math.Fin. 2, 63-86, 1992.

- [6] Beiglböck, M. and M. Nutz . Martingale Inequalities and Deterministic Counterparts. Electronic Journal of Probability 19, 95, 1-15, 2014.

- [7] Bensaid, B., Lesne J.P., Pagès H. and J. Scheinkman. Derivative asset pricing with transaction costs . Math.Fin. 2, 63-86, 1992.

- [8] Carassus, L., Gobet, E. and E. Temam. A class of financial products and models where super-replication prices are explicit “International Symposium, on Stochastic Processes and Mathematical Finance” at Ritsumeikan University, Kusatsu, Japan, March 2006.

- [9] Carassus L. and T. Vargiolu. Super-replication price: it can be ok. To appear in ESAIM: proceedings and surveys, 2017.

- [10] Dalang E.C., Morton A. and W. Willinger. Equivalent martingale measures and no-arbitrage in stochastic securities market models. Stochastics and Stochastic Reports, 29, 185-201, 1990.

- [11] Delbaen F. and W. Schachermayer. The Mathematics of Arbitrage. Springer Finance, 2006.

- [12] Föllmer H. and D. Kramkov. Optional Decompositions under Constraints, Probability Theory and Related Fields 109, 1-25, 1997.

- [13] Harrison J.M. and D.M. Kreps. Martingale and Arbitrage in Multiperiods Securities Markets, Journal of Economic Theory 20, 381-408, 1979.

- [14] Harrison J.M. and S. Pliska. Martingales and Stochastic Integrals in the Theory of Continuous Trading, Stochastic Processes and their Applications 11, 215-260, 1981.

- [15] Ingersoll, J.E. Jr. Theory of Financial Decision Making. Rowman & Littlefield, 1987.

- [16] Hess, C. Set-valued integration and set-valued probability theory: An overview. E. Pap, editor, Handbook of Measure Theory, Elsevier, 14, 617-673, 2002.

- [17] Kabanov Y. and M. Safarian. Markets with transaction costs. Mathematical Theory. Springer-Verlag, 2009.

- [18] Kabanov Y. and E. Lépinette. Essential supremum with respect to a random partial order. Journal of Mathematical Economics, 49 , 6, 478-487, 2013.

- [19] Karatzas I. and C. Kardaras. The numéraire portfolio in semimartingale financial models. Finance & Stochastics, 11, 447-493, 2007.

- [20] Kreps D. Arbitrage and equilibrium in economies with infinitely many commodities. Journal of Mathematical Economics 8, 15-35, 1981.

- [21] Lépinette E. and I. Molchanov. Conditional cores and conditional convex hulls of random sets. https://arxiv.org/abs/1711.10303, Preprint 2017.

- [22] Lépinette E. and T. Tran. Approximate hedging in a local volatility model with proportional transaction costs. Applied Mathematical Finance, 21, 4, 313-341, 2014.

- [23] Milstein, G.N. The Probability Approach to Numerical Solution of Nonlinear Parabolic Equations. Numerical methods for partial differential equations, 18, 4, 490-522, 2002.

- [24] Pennanen T. Convex duality in stochastic optimization and mathematical Finance. Mathematics of Operations Research, 36(2), 340-362, 2011.

- [25] Pennanen T. Arbitrage and Deflators in illiquid markets. Mathematical Finance, 21 pp. 519-540, 2011.

- [26] Pennanen T. and A-P Perkkio Stochastic programs without duality gaps. Mathematical Programming, 136 pp. 91-110, 2012.

- [27] Rockafellar, R.T. Convex analysis, Princeton University Press, 1972.

- [28] R. T. Rockafellar and R. J.-B. Wets. Variational analysis, volume 317 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences], 2002. Springer-Verlag, Berlin, 1998. ISBN 3-540-62772-3.

- [29] Schal M. Martingale measures and hedging for discrete-time financial markets. Mathematics of Operations Research, 24, 509-528, 1999.