Bayesian Predictive Synthesis with Outcome-Dependent Pools

Abstract

This paper reviews background and examples of Bayesian predictive synthesis (BPS), and develops details in a subset of BPS mixture models. BPS expands on standard Bayesian model uncertainty analysis for model mixing to provide a broader foundation for calibrating and combining predictive densities from multiple models or other sources. One main focus here is BPS as a framework for justifying and understanding generalized “linear opinion pools,” where multiple predictive densities are combined with flexible mixing weights that depend on the forecast outcome itself– i.e., the setting of outcome-dependent model mixing. BPS also defines approaches to incorporating and exploiting dependencies across models defining forecasts, and to formally addressing the problem of model set incompleteness within the subjective Bayesian framework. In addition to an overview of general mixture-based BPS, new methodological developments for dynamic BPS– involving calibration and pooling of sets of predictive distributions in a univariate time series setting– are presented. These developments are exemplified in summaries of an analysis in a univariate financial time series study.

Keywords: Bayesian predictive synthesis, Density forecast combination Forecaster dependence, Forecasting, Forecast calibration, Generalized opinion pools, Model combination, Model set incompleteness, Time series prediction

1 Introduction

The combination of forecast densities, whether they result from a set of models, a group of consulted experts, or other sources, continues to be an active and important research arena that cuts across a range of disciplines. Requiring methodology that goes beyond standard Bayesian model uncertainty and model mixing– with its well-known limitations based on a clearly proscribed theoretical basis– multiple density combination methods have been proposed. In recent years, the literature has been particularly rich in development of density forecast combination methods motivated by applications in economics, policy, and finance (e.g. Amisano and Giacomini, 2007; Hall and Mitchell, 2007; Hoogerheide et al., 2010; Kascha and Ravazzolo, 2010; Geweke and Amisano, 2011, 2012; Billio et al., 2012, 2013; Aastveit et al., 2014; Kapetanios et al., 2015; Pettenuzzo and Ravazzolo, 2016; McAlinn and West, 2019; West, 2020). Other key areas of application are as diverse as meteorology, military intelligence, seismic risk, and environmental risk, among others (e.g. Clemen, 1989; Clemen and Winkler, 1999; Timmermann, 2004; Clemen and Winkler, 2007; Rufo et al., 2012). These and other ensemble, averaging or “synthesis” methods have varying goals, applicability, and degrees of applied success. While empirical results can be be positive and encourage interest in the underlying method, many such forecast combination “rules” lack any sort of generative model or foundational justification. This is a key point of departure and emphasis of Bayesian predictive synthesis (BPS), reviewed, explored and expanded upon here.

The literature on agent opinion synthesis, in which a decision maker solicits the opinions of experts in order to create an informed opinion, provides a framework for model combination. Forecast synthesis fits naturally into the “supra-Bayesian” approach (e.g. Lindley et al., 1979; West, 1988; West and Crosse, 1992; West, 1992). Here, a single Bayesian decision maker regards the new information gained from a set of models- or “agents”- based forecast distributions, and evaluates approaches to formally condition on this information to define resulting predictions. Generalized density combination is approached within this framework.

Importantly and as discussed below, BPS enables the decision maker to address questions of model/agent specific biases and calibration, dependencies across models/agents, as well as to explicitly address the issue of model set incompleteness (Aastveit et al., 2019; McAlinn et al., 2020; McAlinn, 2021; Giannone et al., 2021), also known as the “model space open” or “-open” setting (Bernardo and Smith, 1994; West and Harrison, 1997; Clyde and George, 2004; Clyde and Iversen, 2013). These ideas are also relevant to the generalized Bayes literature and the question of how to combine densities admitting that all models are “wrong but useful” (e.g., de Heide et al., 2019).

Some Notation:

Vectors are denoted using lowercase bold font; for example, represents a vector while is a scalar. Matrices are in upper-case bold font. Index notation represents the sequence . A column vector is denoted or, in context in terms of elements as . The notation indicates the vector or set with the element omitted. The usual notation denotes a normal distribution with mean vector and covariance matrix , with usage and for the p.d.f. The Dirac delta function is the point-mass at as a distribution for . Other specific notation is defined in context.

2 BPS Foundations

2.1 Background and Key Theory

A decision maker is interested in predicting an uncertain quantity . The decision maker has some opinion of , quantified through a subjective prior density . In order to predict , will examine the density forecasts from separate sources , . In general, these sources could be models, analysts, other forecasters, or subject matter experts; here, refer to them as models throughout. How should consolidate this information, and ultimately update ?

The Bayesian paradigm defines the straightforward solution, in theory. updates the prior to a posterior upon learning the information set . Specifying a full prior joint distribution is impractical, however, and the theoretically straightforward approach cannot be easily implemented. This led West (1992) and West and Crosse (1992) to extend the work of Genest and Schervish (1985) to show that, under certain consistency conditions, ’s posterior density has the form

| (1) |

where . Here, is a vector of latent model states, and is a conditional density function that synthesizes these states. The framework allows flexibility in choosing the key synthesis function . One requirement is consistency with ’s prior, i.e.,

| (2) |

where with the expectation taken with respect to ’s implicit prior over .

Operationally and constructively, this result can be noted to require that specify and the conditional density function , inducing the prior . Specifying these two functions allows to incorporate views of the models in terms of past information and expectations on aspects of their calibration, biases, relative expertise, and importantly, dependencies, in predicting . There is a great deal of flexibility in the specification, and a number of approaches to forecast density combination can be represented this way (McAlinn et al., 2018). Some examples are given below.

The Bayesian update of the prior in eqn. (2) to the posterior in eqn. (1) simply substitutes for . This is an example of formal subjective Bayesian updating via (Richard) Jeffrey’s rule rather than by Bayes’ theorem. Implicitly, is ’s prior for the latent model states , while is their “true” distribution later observed. In this update, the conditional density remains unchanged. This method of updating is implicit in all Bayesian analysis and was recognized and formalized in Jeffrey (1990); see further discussion in Diaconis and Zabell (1982). Jeffrey (1990) provides an intuitive example that involves betting on a racehorse that performs better in mud. The probability of the horse winning conditional on rain is known, but the probability of rain is not. ’s prior that the horse wins depends on ’s prior for rain; when a professional forecast for rain becomes available, this simply replaces ’s prior for rain.

The product of the in the key expression in eqn. (1) does not reflect any assumption of independence across models. Rather, it makes clear that the inherent latent factors are conditionally independent given In contrast, the implicit, partially specified prior has over allows for essentially arbitrary dependencies of the as uncertain functions. This is an important conceptual point and a point of departure from traditional pooling methods including Bayesian model averaging (BMA). For example, historical evidence of positive dependence between two models– in terms of them having generated rather similar forecast distributions in the past– can be reflected in the synthesis. Of course, how this is done in any specific context depends on the form of the synthesis function specified.

The interpretation of is a focus of discussion in West (1992) and West and Crosse (1992). The first interpretation is that, if each model were to provide a predictive density degenerate at a point , i.e. , then ’s posterior is given by . A second interpretation is that in order to sample , may first sample a vector from , and then sample .

Much of the review discussion to follow, and ensuing methodological developments of this paper, focus on the theoretical framework of BPS using specific discrete mixture forms for . Among other things, this justifies the approach termed generalized linear pools of Kapetanios et al. (2015), but then extends to address questions of model inter-dependencies and time-varying generalizations relevant to predictive synthesis in time series forecasting. First, however, note a simple example that connects with other variants of BPS– involving other choices of the synthesis functions – and that provides an easily appreciated, entrée example as well as connections to the literature.

2.2 Linear Regression Example

McAlinn and West (2019) explore dynamic BPS examples in which the are extended to time-varying settings and are conditionally normal given relevant defining parameters. A simple, static example involves a synthesis function that is the p.d.f. of

This example, just one potential specification of the conditional synthesis density , easily and intuitively allows for ranges of model biases and miscalibration, viewed through shifts in means and/or variances of implied conditional distributions of individual conditional distributions , and for cross-model dependencies through the regression vector If any model (or all models) are biased, the intercept term allows a correction. If models are correlated (or anti-correlated), appropriate adjustments are made through the weights. Finally, the residual volatility accounts for the relative uncertainty between the outcome and the latent states following corrections for their biases and dependencies.

By observing repeated forecasts over time, Bayesian updating allows for learning about the coefficients, which account for evolving perceptions of model biases and dependencies. This example has been extended to multivariate forecast density synthesis and applied in a detailed macroeconomic study (McAlinn et al., 2020). Related, more extensive developments of dynamic BPS underlie aspects of more recent studies in macroeconomics and allied areas (e.g. McAlinn, 2021; Aastveit et al., 2023).

3 Mixture BPS

3.1 Setting and Background

Empirical methods that simply average a set of predictive densities to form a discrete mixture– or “linear pool”– have a long history (e.g. Clemen, 1989; Genest and Schervish, 1985; Clemen and Winkler, 2007; Hall and Mitchell, 2007, and references therein). Averaging the with respect to defined weights, or mixture probabilities, can arise more formally from standard BMA (Bernardo and Smith, 1994; Clyde and George, 2004; Clyde and Iversen, 2013) and extensions in time-varying settings (e.g. West and Harrison, 1997, chapter 12). Allied approaches choose weights that aim to optimize defined predictive goals (e.g. Geweke and Amisano, 2011; Diebold and Shin, 2019; Diebold et al., 2020; Lavine et al., 2021; Loaiza-Maya et al., 2021, and references therein).

A significant expansion of the scope of linear density pooling was marked by Kapetanios et al. (2015), proposing the use of outcome-dependent weights. This involves the generalized linear pool form

| (3) |

where the weights explicitly depend on the as-yet unobserved outcome being predicted and are defined so that is a p.d.f. The authors presented this as an empirical approach to extending the traditional linear opinion pool using constant weights. The core idea is that, in some regions of the outcome space of , different models may be expected to generate superior forecasts. For example, one model may be generally better at predicting changes in inflation when inflation is high, another superior in times when inflation is low or falling. With more flexible weight functions fitted using semi-parametric Bayesian methods, Kapetanios et al. (2015) give examples of substantial improvements in forecasting accuracy over traditional linear pools. This has been followed by various extensions and demonstrations of empirical success using outcome-dependent density pooling (e.g. Aastveit et al., 2014; Pettenuzzo and Ravazzolo, 2016; Bassetti et al., 2018). While these techniques make intuitive sense as a generalization of constant weight approaches, and have been shown to produce good empirical results in various applications, their use raises questions about foundations and theoretical justifications that would aid in understanding, extensions and identification of limitations. These questions are addressed within the framework of BPS.

3.2 Constant Weight Mixture BPS

Suppose adopts the synthesis function

| (4) |

where the weights are non-negative probabilities that sum to one. Here, is a baseline p.d.f., possibly defined by a further baseline model, that is chosen to represent a “save haven” predictive distribution that will choose to revert to in case models are regarded as suspect, to be down-weighted as a group, based on poor predictive performance. The choice of a rather diffuse baseline p.d.f. is natural and links to other areas of the Bayesian forecasting literature where “diffuse alternatives” are chosen for comparison with predictions from one or more models (e.g. West and Harrison, 1997, section 11.4). The inclusion of this baseline model in the linear pool of eqn. (4) opens the path to addressing the -open, or model set incompleteness, question. Otherwise, eqn. (4) is inspired by the interpretation that, if each model provides an “oracle” prediction , then will linearly average these values and combine with the baseline. Of course, the are latent variables; eqn. (1) recognizes that and results in ’s predictive density

Note that choosing results in classic linear pools of model densities, including many that previously had mainly empirical justification. This also includes formal Bayesian approaches via BMA and its extensions; that is, traditional Bayesian model uncertainty and combination is a special case of BPS.

Evaluation of eqn. (2) provides interesting insight. ’s prior (before observing ) is

where is the -marginal of evaluated at . The prior forecast is a linear pool of and the marginal expectations of each of the model forecast densities.

Simple extensions allow to inject adjustments for expected biases or aspects of mis-calibration in each of the model predictions. The simplest, for example, is to modify the synthesis function to

where specifies expected bias terms . This results in the synthesis function

i.e., has simply adjusted the locations of model forecast distributions to address expected biases.

3.3 Model-Specific Outcome-Dependent Weights

3.3.1 General Framework.

The first generalization to outcome-dependent weights allows the mixture probabilities to depend on the latent forecast location via

| (5) |

where . Of course, eqn. (4) is a special case. Eqn. (1) then yields ’s synthesis

where for each model , , and . In this synthesis, has adjusted each density to a re-calibrated . BPS provides an explicit framework for calibration, and importantly, also delineates the assumptions and conditions required to maintain calibration coherence. Notably, the weights could be functions not only of the , but perhaps also of additional relevant covariates, model scores, or decision-related measures, as in recent developments in Lavine et al. (2021) and Tallman and West (2023).

3.3.2 Example: Gaussian Weights.

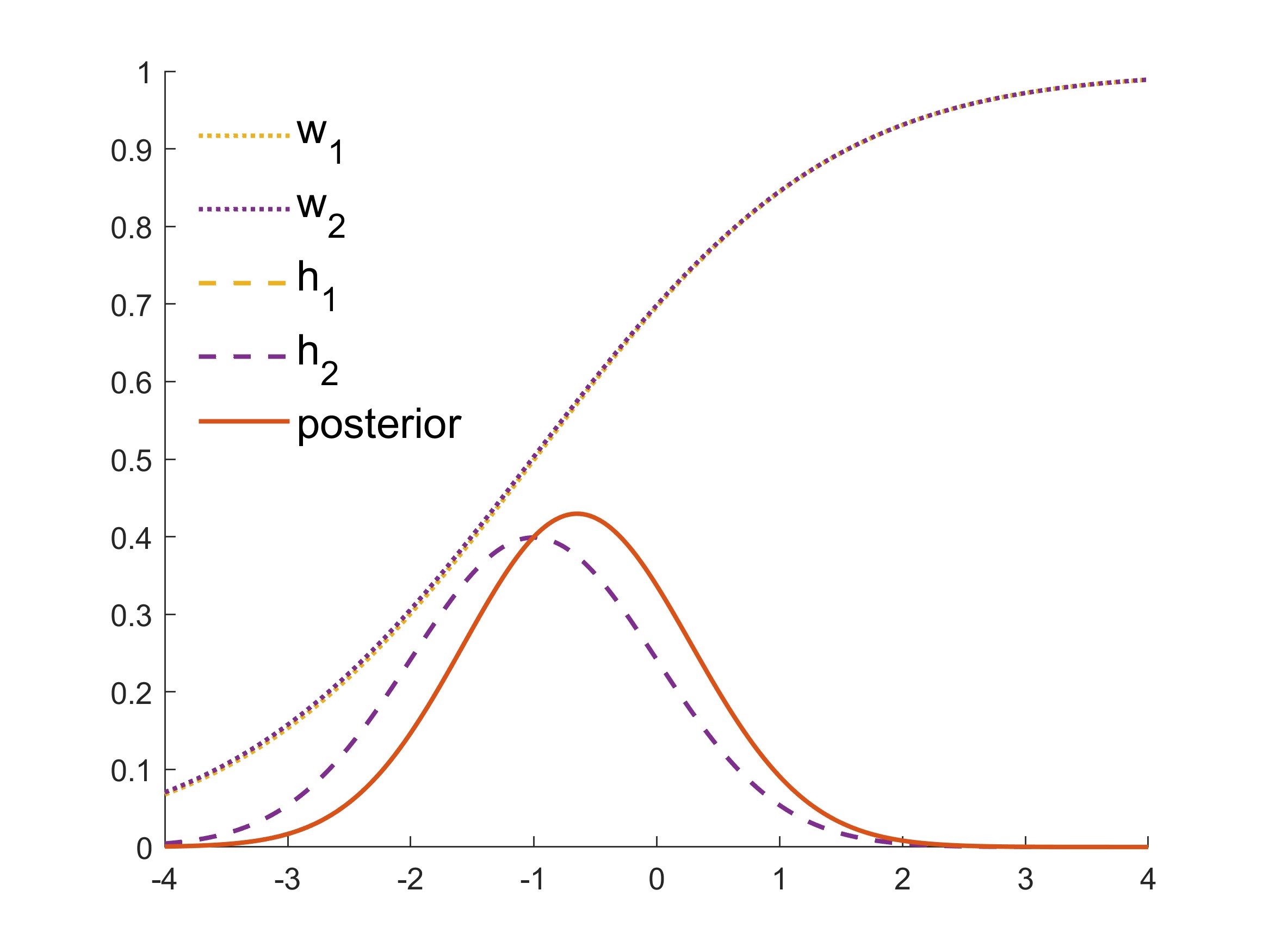

A first example is inspired by Kapetanios et al. (2015). Here different models are regarded as more or less informative in different regions of the outcome variable (e.g., bear markets with negative values vs. bull markets with positive values). Take

for , where the are a set of base synthesis weights that sum to 1, and Write for the vector of base synthesis weights. Here, the overall weight on takes a maximal value of at and decreases as moves away from , with the rate of decrease controlled by . In this way, encodes that is trusted most near .

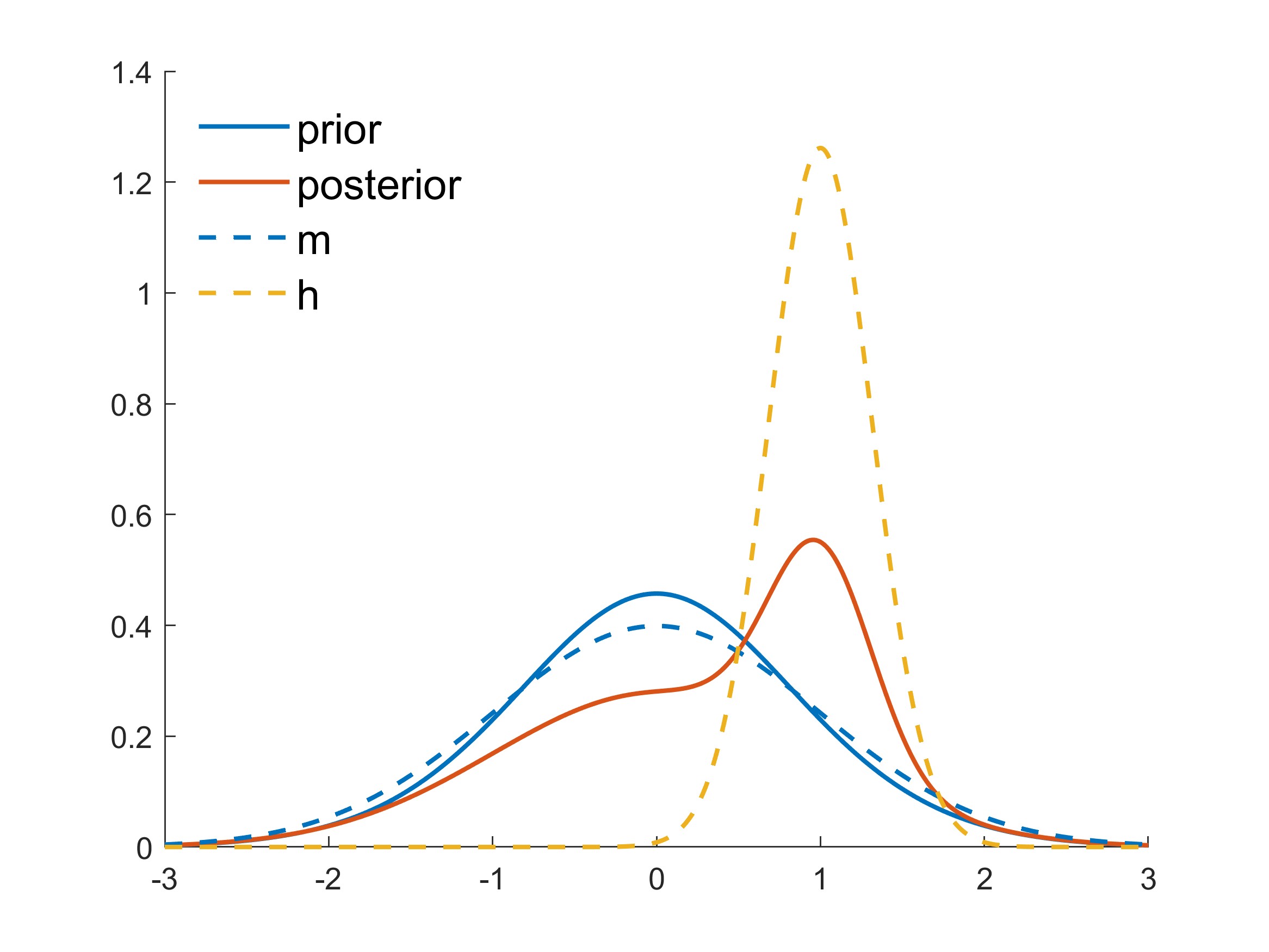

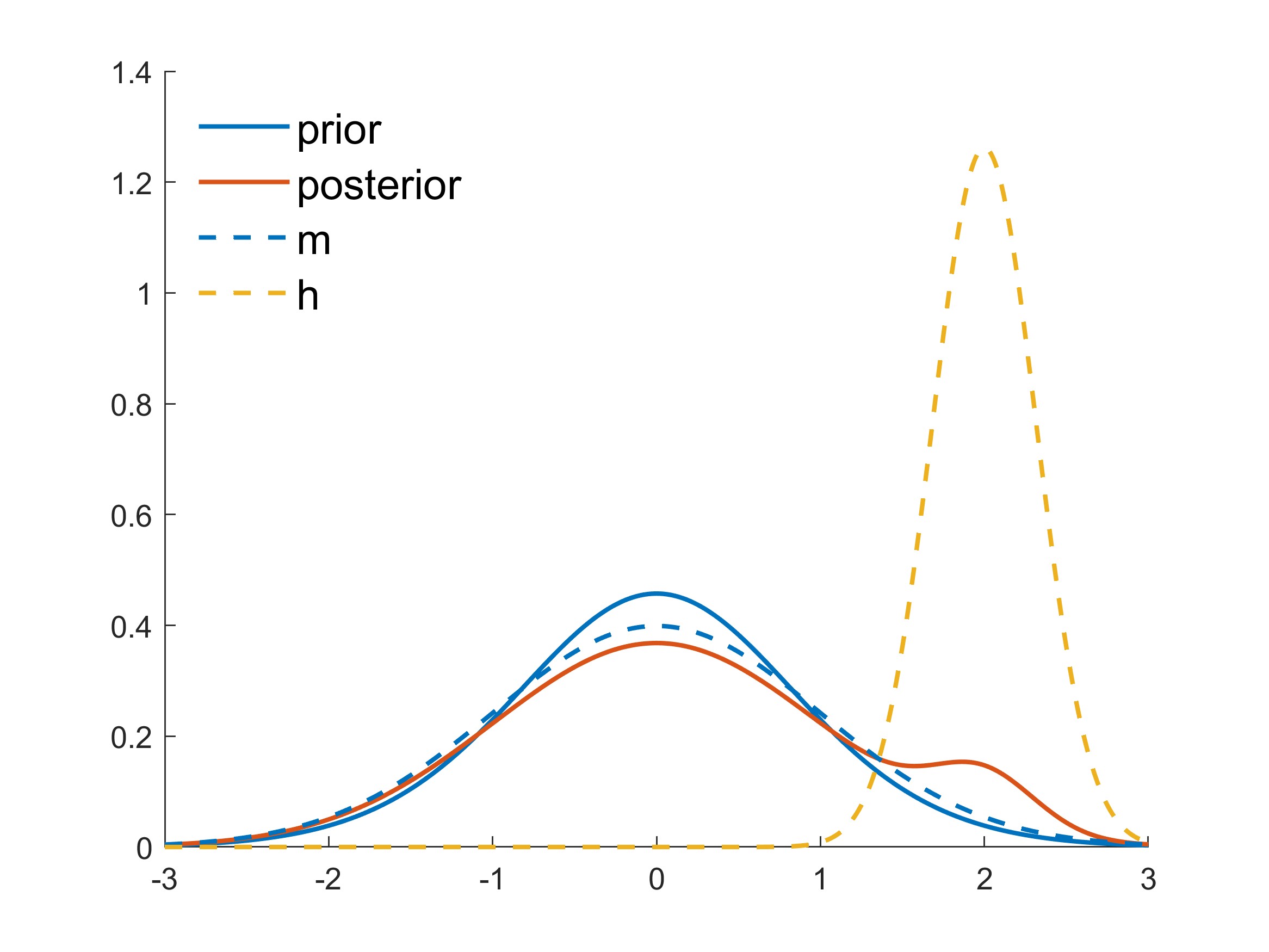

Consider an example with a single model, , and drop the then-superfluous subscript for clarity. Set and so that expects the model to generate forecasts that, relative to baseline, are location-shifted by a factor and scale-adjusted through . Then . Suppose the model now presents for some point forecast and variance . The effect of on is to down-weight the portions of that are further from , resulting in the reweighted model density

where and . So is a compromise between the forecast that expects and the forecast that provides. The weight on in the mixture form is

further emphasizing how lower weight is given to the adjusted model density as moves away from . Figure 1 demonstrates ’s prior-to-posterior update given two different forecasts

3.3.3 Gaussian Well Weights.

In a different applied setting, might be concerned about the reliability of the model forecasts from one model and aim to down-weight that model relative to others and the baseline in regions relatively favored by A synthesis function that reflects this is the Gaussian well form

This example emphasizes emphasizes the flexibility of of choices in the mixture-based BPS framework. Details are not explored here, but weighting with Gaussian wells is further developed in section 3.4.4.

3.4 Cross-Model Weights

3.4.1 General Framework: Model Dependencies.

Generalizations have model weight functions that depend on the full vector rather than just the individual in weighting The general form is

| (6) |

where are non-negative and sum to one for each . Eqns. (4) and (5) are special cases. The resulting predictive synthesis is

where each with

| (7) |

in which is evaluated at , and the are normalizing constants.

Allowing to depend on the full vector of latent states rather than just generalizes and extends the interpretation of outcome-dependent weight pooling. Eqn. (7) defines opportunity to weight predictions given the set of forecasts from other models, as well as in terms of its own specific biases and expected prediction accuracy. This allows adjustments for potential outlier forecasts, and for dependencies– including expected herding behavior, for example– among models. For instance, if three models using similar data provide similar forecasts, equal weights may suffice. If one of the three provides a forecast different from the other two, may wish to give it 50% of the weight; if one model disagrees with 99 others, may choose to ignore it entirely.

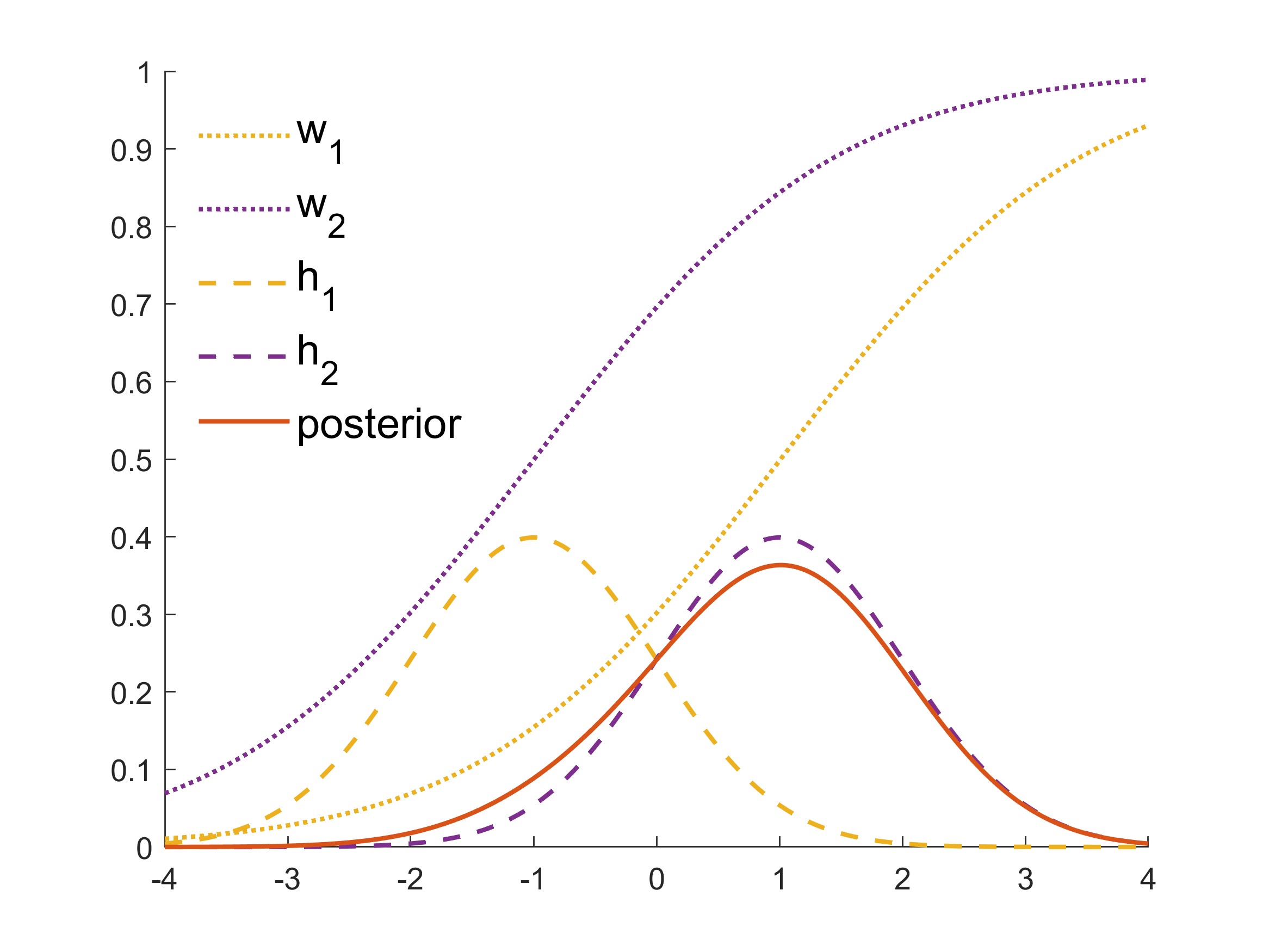

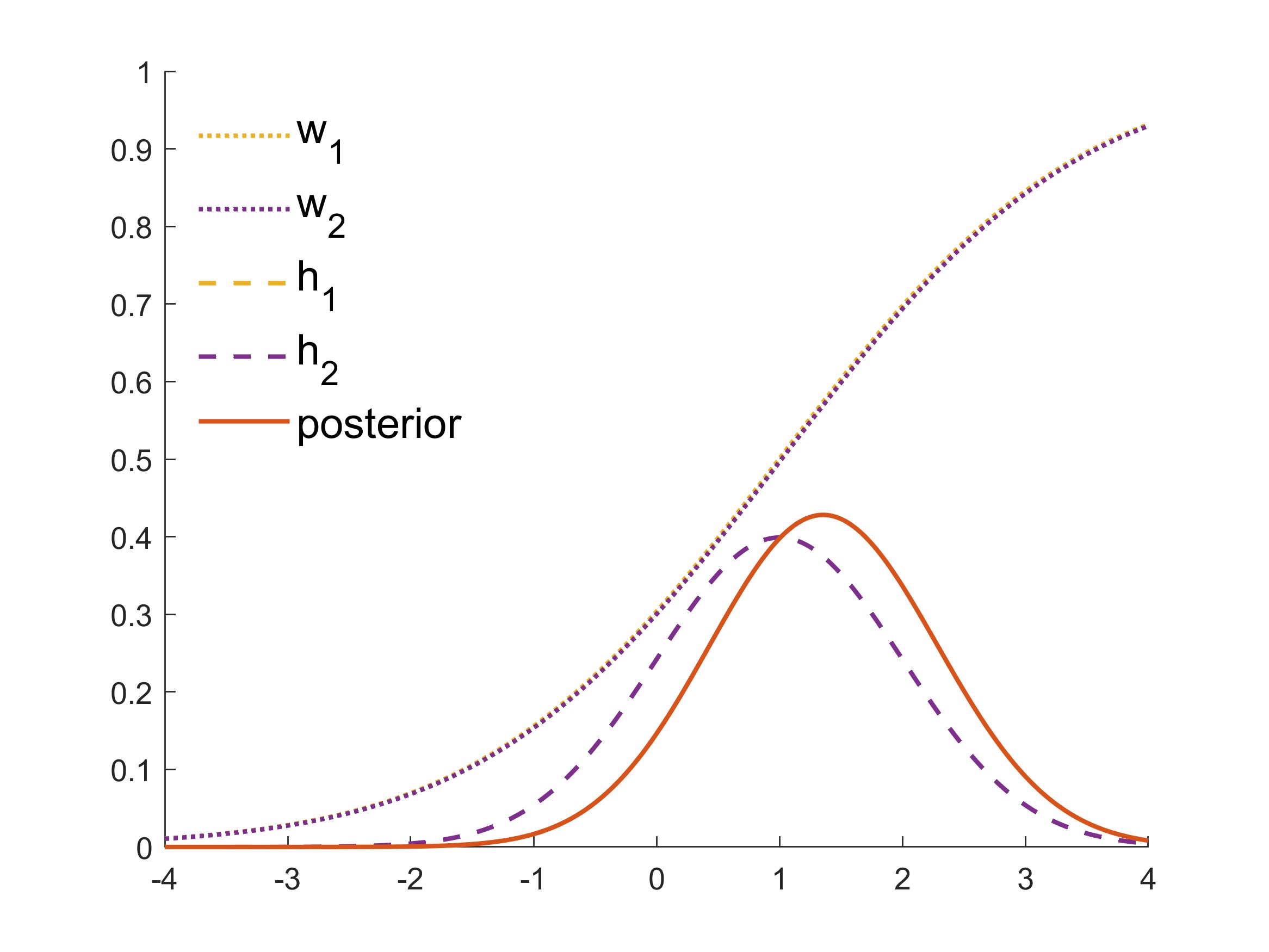

3.4.2 Softmax Weights.

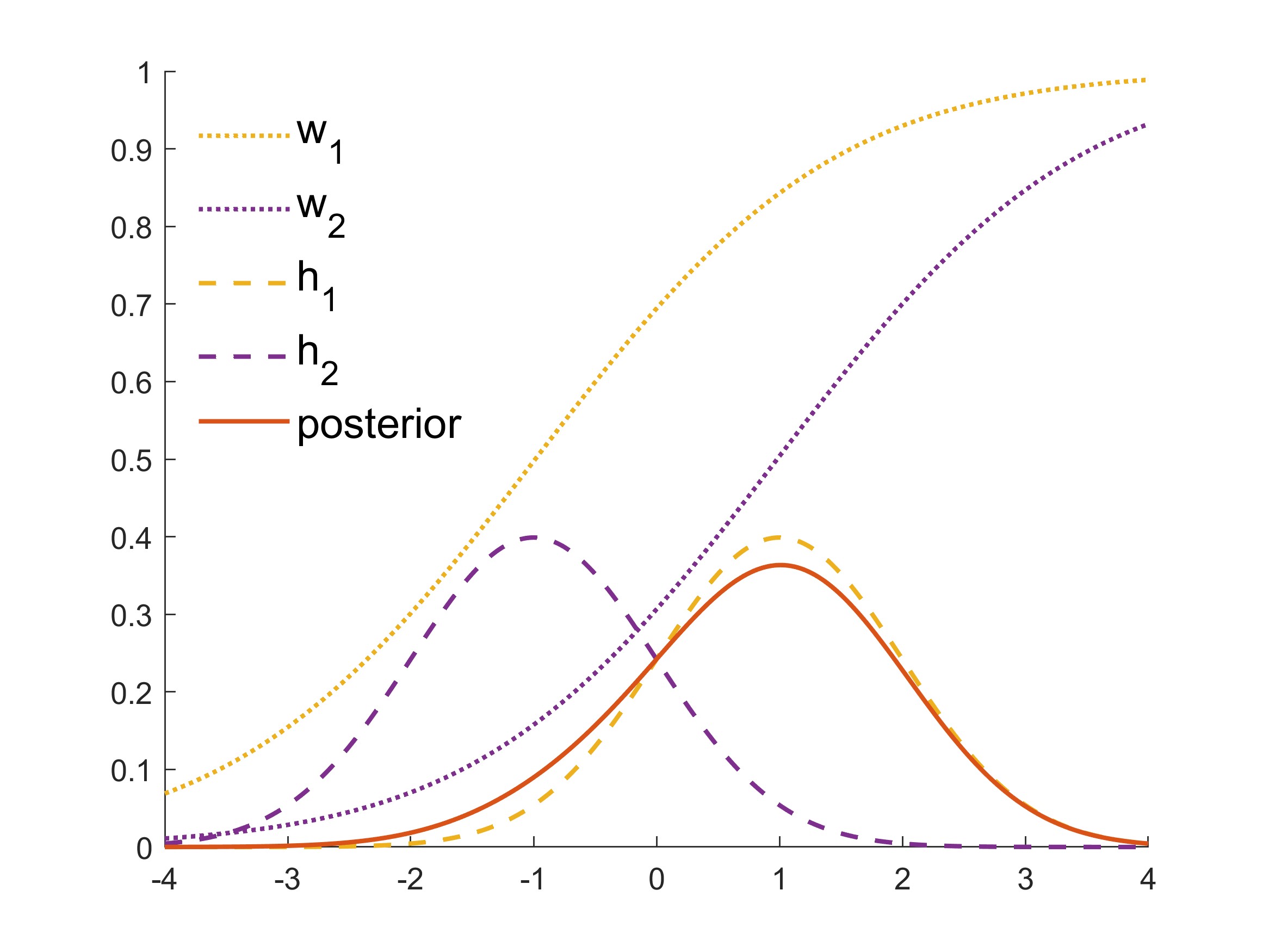

Consider an example with where and , with so that there is no baseline density. If , . If , , and vice versa. In this specification, prefers higher forecasts– higher weight is given to the higher density, regardless of the model that provides it. Figure 2 shows and when for . Note that ignores low forecasts unless both models provide low forecasts.

3.4.3 Weighting for Consensus.

In setting the weight function, the general way to phrase the question is “How much weight should be placed on , given the entire vector ?” Posed another way, “For given , how much weight should be placed on , as a function of ?” Conceptually in terms of values of the latent model states, may wish to ignore a value that disagrees with the others, i.e. it falls outside of a “consensus” of the remaining models. One way to do this is to decrease the weight on around , which is defined through the density .

A key example introduces a multivariate normal for the vector of latent model states, namely with mean and covariance matrix This allows for the representation of expected cross-model dependencies through This example is extended to the time-varying setting in Section 4.2, and explored in the subsequent example in Section 5.

Under this choice of the implied complete conditional is normal with where the regression vector is implied by write for the corresponding conditional variance of . A natural choice for involves the kernel of the implied conditional normal p.d.f., taking

| (8) |

where the deviation of from its point prediction based on the latent states of the other models, and with, as before, defining base synthesis weights. If is specified so that the latent states are positively correlated, lower weight is given to when is large in absolute value, i.e., when is far from its conditional expectation based on the latent states of the other models.

3.4.4 Weighting for Herding.

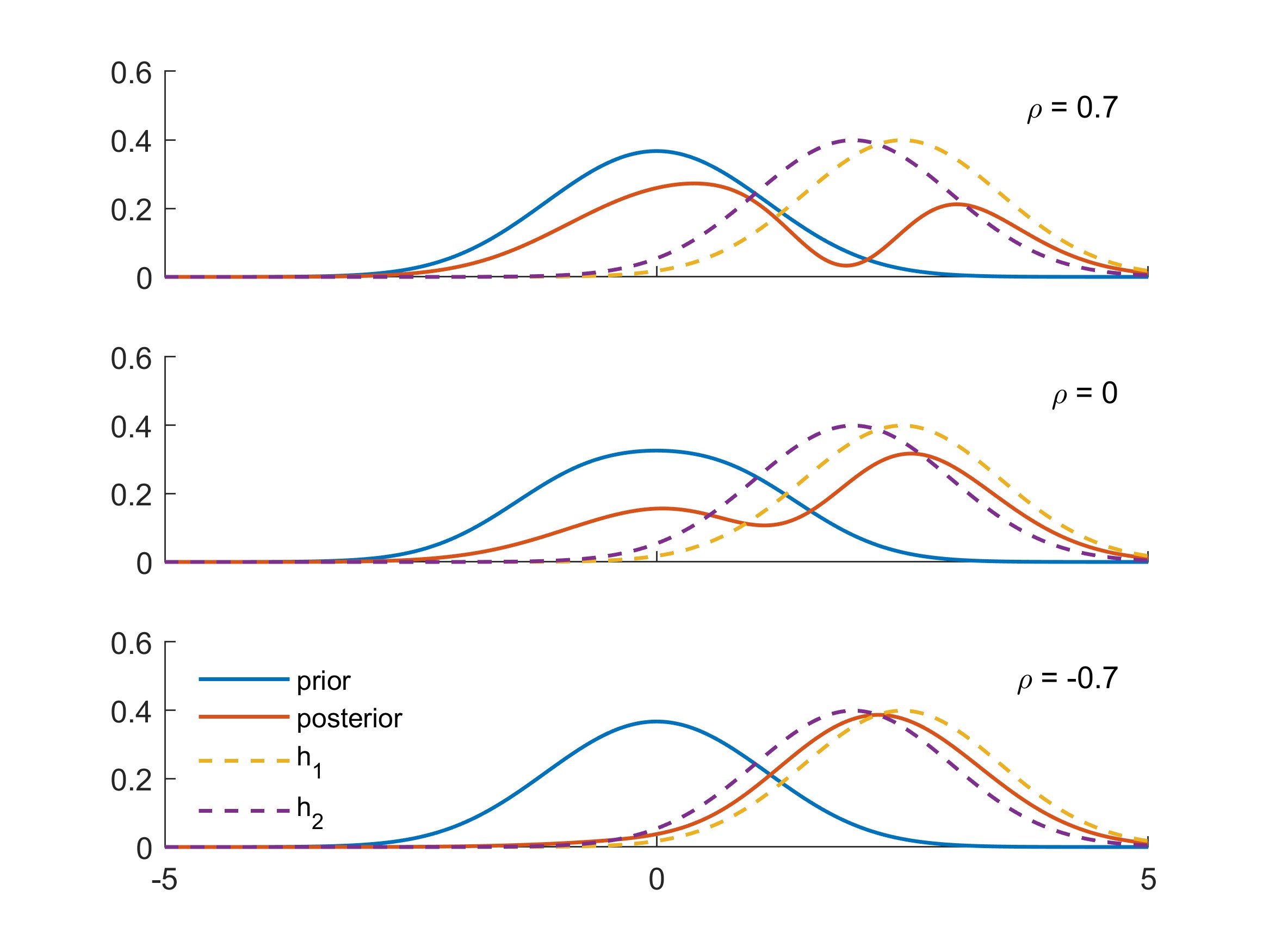

Addressing cross-model dependencies and the herding issue (positive dependencies among model predictions) more directly, may wish to decrease weight on a predictive “consensus”. This can be targeted using a number of synthesis function choices, including the example

| (9) |

with the as in Section 3.4.3, and where denotes the depth of the conditional Gaussian well as in Section 3.3.3. As a result, the weight on will be increased as increases in absolute value, as seeks a diversity of forecasts rather than a consensus. Figure 3 illustrates the results of weighting similar model densities using conditional wells under different assumptions about model dependencies. When models are expected to agree, similar forecasts are weighted lower; hence the analysis naturally discounts positively dependent model forecasts, accounting for herding. In contrast, when they are expected to disagree with negative dependence in the synthesis, similar observed forecast distributions are more highly weighted; this is again natural in reflecting agreement in what is expected to be an antithetical setting.

4 Dynamic Mixture BPS for Time Series

4.1 Time Series Context

Common applications are in time series forecasting, where receives predictive distributions from the same set of models repeatedly over time. Here a parameterized synthesis function may be time-varying. Then sequentially updates information relevant to the synthesis parameters to reflect evolving predictive accuracy of the models, and perceptions of bias and dependence between models, all of which may vary in time.

Adding subscript to denote equally spaced time, focus first on 1-step ahead prediction of a scalar time series. At each time , forecasts based on historical information and new predictive densities supplied by the set of models, each predicting ’s analysis is implicitly conditional on the time filtration consisting of the observed model forecasts and data , though for notational clarity this is not made explicit here.

4.2 A Dynamic Combined Weighting BPS Model

The synthesis function of eqn. (6) is generalized to reflect time dependence throughout: the synthesis weights are now with , and the model is extended to including potentially time-varying model biases . This results in

| (10) |

with implicit latent factors that are now also time-dependent, i.e., define a vector time series of dynamic latent factors.

Structuring uses time-dependent extension of eqn. (8). The time-specific have univariate complete conditionals that imply . Cross-model dependencies and their evolution in time are reflected in the . Coupled with this, evolving model-specific biases are reflected in the specification , where is the known mean of the specified baseline density , and is a vector of bias terms . Thus expects model to have a bias of relative to in forecasting with time-variation accommodated. The bias term acts directly to adjust the mixture locations in the synthesis function, as in the static example at the end of Section 3.2. This translates parameter learning from to , along with the vector of time base synthesis weights .

The analysis to follow assumes that, at time , accrued historical information leads to summarize the time posterior for model parameters as follows: have a normal, inverse-Wishart (NIW) distribution independently of , while the latter has a Dirichlet distribution. Time variation in parameters is defined using standard discount factor methods for Bayesian dynamic modeling. In moving to time , the parameters evolve to and the implied time prior– before observing – is also NIW but with increased uncertainty representing potential changes through the evolution. Standard discount theory for dynamic linear modeling underlies this (West and Harrison, 1997, chapter 16; Prado et al., 2021, chapter 10). In parallel and independently, evolves according to a dynamic Dirichlet model: evolves to and the implied prior– before observing – is also Dirichlet but with a precision parameter that is reduced by a discount factor to represent increased uncertainty.

4.3 Sequential Model Analysis and Computation

4.3.1 Sequential forecasting, filtering and evolution.

Sequential model analysis involves, at each time , the three steps of forecasting, filtering and subsequent evolution to First, at time , forecast or predict ; second, on observing update the prior to posterior over model parameters ; third, evolve this time posterior to the time prior for . The process then repeats over future time periods.

As noted above, the time prior distributions are assumed by as independent NIW and Dirichlet. The BPS model defines implicitly through the mixture over eqn. (10) with respect to the model set input product Whatever the may be, the complexity of analytic form of the BPS weights generally obviates any analytic evaluation of predictive and posterior/filtered quantities of interest. Hence much of the analysis is simulation-based for both prediction and posterior analysis. Then, simulation samples from the time posterior define the basis for constraints to evolve to the constrained NIW and Dirichlet priors at time . The three steps are summarized as follows.

4.3.2 One-step prediction at time

This is trivial via direct Monte Carlo: (i) simulate parameters from the NIW prior for and from its Dirichlet prior; (ii) simulate independent draws of the model latent states ; conditional on these synthetic values, simulate from eqn. (10). Repeat to generate a Monte Carlo random sample from the one-step ahead forecast distribution; summarize as desired.

4.3.3 Prior-to-posterior update at time .

At each time on observing outcome , a structured Gibbs sampling-style Monte Carlo Markov chain (MCMC) sampler defines a simulation approach to evaluation of the posterior for model parameters and the latent model states jointly. Within each overall MCMC iteration, components of this sampler involve exact simulation from relevant conditional posteriors that are analytically tractable, while other components exploit accept/reject sampling. Further details are in Appendix A.

To complete the update step, uses the Monte Carlo posterior sample to define the analytic posterior NIW and Dirichlet distributions required for evolution to the next time point This is done via variational Bayes as in Gruber and West (2016, 2017) in related contexts. Specifically, the parameters of a posterior NIW and Dirichlet for given are computed by minimizing the Küllback-Leibler divergence of the resulting, analytic form from the empirical posterior represented by its Monte Carlo sample. Further details are summarized in Appendix B.

4.3.4 Evolution from to .

In moving to time , the NIW and Dirichlet posteriors are modified with discount factors to define the implied time prior for ; the discount evolution simply increases uncertainty in the distributions in moving ahead one time point, precisely as already discussed above for the time to evolution. See Appendix C.3.

5 Time Series Example

5.1 FX Time Series Setting

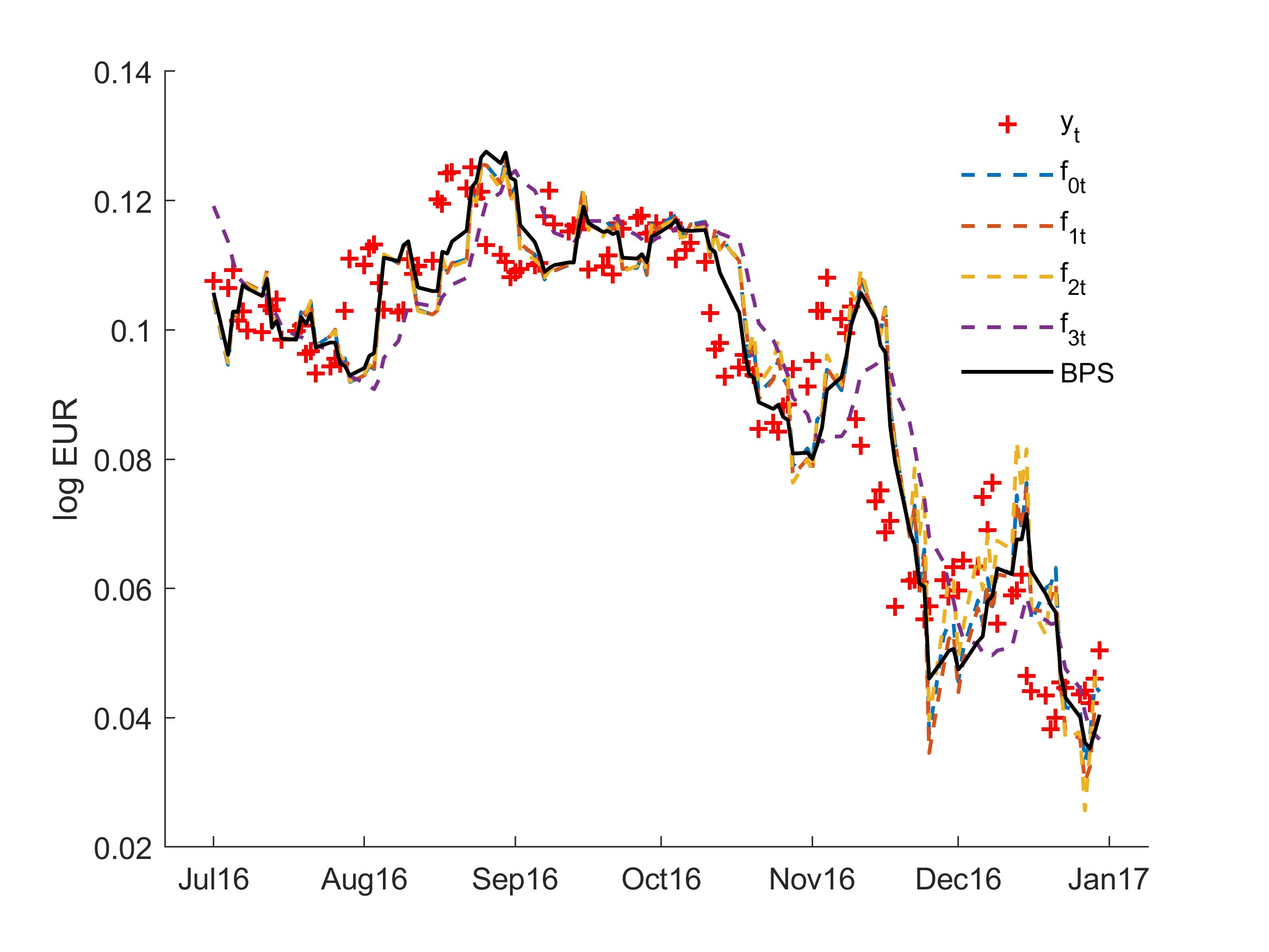

The BPS model and analysis of Section 4 is explored in a study of a daily FX (foreign exchange) currency prices, namely that of the Euro relative to the US$ over a period of six months. Here is the log $price of the Euro each day over the last six months of 2016, 7/1/2016-12/30/2016, for a total of 130 trading days. This time period includes the U.S. presidential election, which caused some quick FX movements in mid-November. The data appear in Figure 4.

In this setting, is interested in predicting 5 days (one working week) ahead. At time , after observing , each model generates 5-step ahead forecast distributions for that are then the inputs to the BPS analysis. That is, synthesizes forecasts of the specific outcome of interest. This is then repeated each day over the time period of interest. With daily FX series, 1-step models are heavily driven by noise and the set of pure time series models here will tend to generate similar 1-day ahead forecasts. Multi-step ahead forecasting allows for more differentiation of model predictive accuracy, and is also much more relevant to financial applications and portfolio decisions (e.g. Zhao et al., 2016; Irie and West, 2019). Technically, the BPS sequential analysis and computational approach are precisely outlined in Section 4.3; the difference is simply that of interpretation: at time , the observation is the outcome that was forecast at time , and reflect ’s time posterior for model biases and dependencies of the 5-day ahead forecasts distributions from the set of models.

This example serves to illustrate and highlight key aspects of BPS including: (i) the ability of BPS to identify and adapt to model-specific biases and their changes over time; (ii) to quantify the nature of cross-model dependencies, again with changes over time; (iii) to highlight and adapt to the issue of model set incompleteness; and (iv) to define improved predictions relative to BMA as well as each of the individual models.

5.2 Model Set and BPS Specification

Mixture BPS explores and synthesizes a set of dynamic linear models (DLMs) and uses another DLM as the default baseline: is a time-varying autoregression of order 1, or TVAR(1); is TVAR(2); is TVAR(5); is a linear growth DLM representing adaptive, locally linear progression over time. These are standard univariate DLMs and widely used in short-term forecasting and other areas (Prado et al., 2021, chapters 4 and 5). Models and have more predictive potential more than one day ahead as they involve more lagged values of as predictors; model extrapolates linearly so has similar potential but only on a few days ahead. FX data often shows 2–3 day momentum effects that these models can pick up. In contrast, is simply a default that in practice will always score as well as more elaborate models in 1-day ahead forecasting over many time periods, reflecting the fact that short-term daily FX forecasting (with purely time series models) is inherently very challenging.

Each day, the analysis of the previous section applies: each model provides predictive distributions for the closing (log) price 5 days ahead, and these are dynamically synthesized using the mixture BPS formulation. Figure 4 shows resulting point forecasts (5-day ahead forecast means) from each of the models and from BPS. Importantly, BPS synthesizes and learns from multi-step ahead forecasts, as opposed to extrapolating a combination based on single-step performance. This contrasts with other forecast pooling approaches– including BMA– that inherently score models based on 1-step ahead forecasts.

5.3 Aspects of BPS Analysis

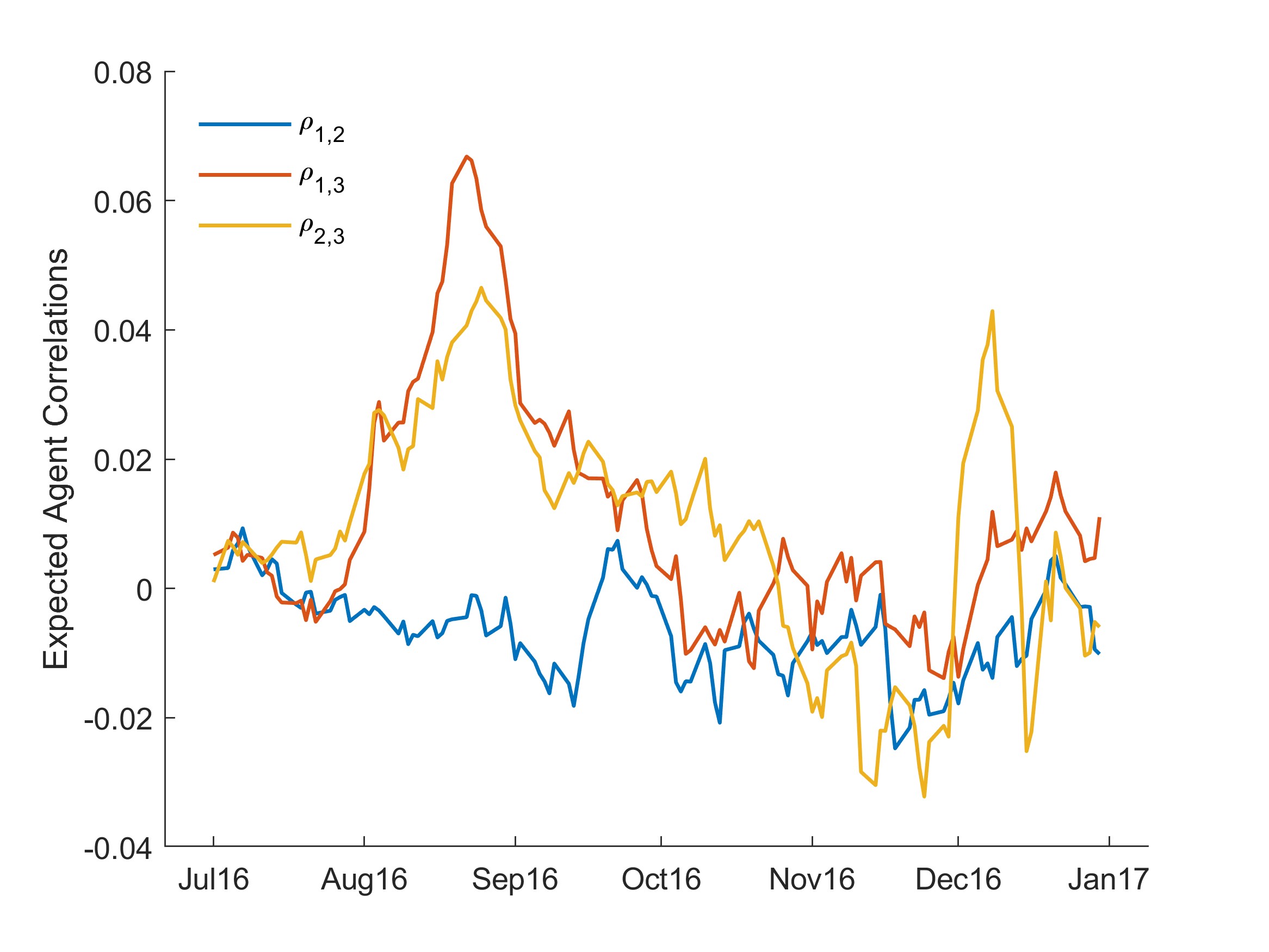

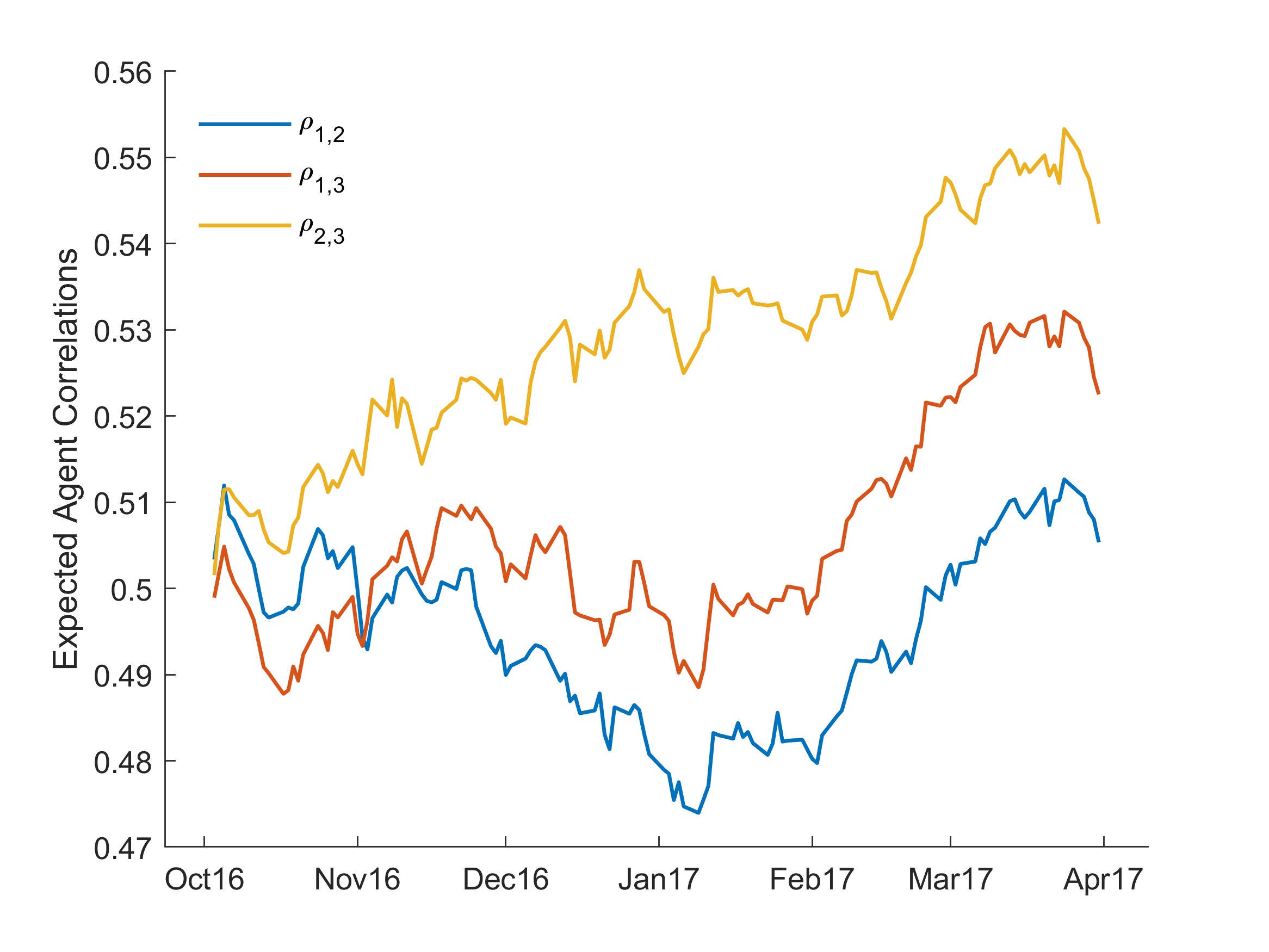

As noted above, some main interests are in learning about bias and dependence among models, and in changes over time in these features that BPS is able to represent. The models in the specific model set are expected to perform fairly similarly for most time periods, with time-varying biases, correlations, and scales. Repeat experience with the set of models over time then also builds up a profile of cross-model dependencies. Figure 5(a) displays point estimates of correlations represented in the BPS covariance matrix ; these are the time filtered posterior means using the Monte Carlo sample of the posterior for on day . There is some notable learning over time, with slightly positive correlations between (the locally linear DLM) and each of the TVAR models. A positive correlation between and TVAR models indicates that the model weights are down-weighted when they disagree. In contrast, BPS learns essentially zero correlation between (TVAR(2)) and (TVAR(5)). As a result, the TVAR models are not down-weighted when they disagree; BPS does not require a “consensus” among TVAR models to assign to them appreciable weights. All correlations break down around the period of the US election, with some recovery of the slight positive dependency of and (the longer history models) later in that year. The pre- and post-election period was a period of increased uncertainty and consequent volatility in the FX markets, and models with different lag structure respond slightly differently over that period as evidenced by the drop on cross-model correlations. Throughout, interpretable cross-model dependencies are inferred and the time trajectories show the adaptability of the BPS analysis in more volatile time periods.

Now consider the the vector of bias parameters . The chosen models are inherently adaptable to changes over time; this is a main feature of DLMs in terms of addressing model biases. However, the models have discount factor parameters that define their degrees of adaptability. The dynamic BPS model overlays this to allow for systematic, possibly time-varying additional biases in location of prediction distributions through . The sequential analysis, illustrated in Figure 5(b), gives insight into how the BPS model sees biases. This shows time trajectories of posterior means of the elements of , with evidence of the need for some bias corrections as well as relationships among inferred biases across models over time. The overall BPS analysis integrates inferences on the biases in defining the synthesized predictions at each time, and then in adapting to new, incoming data.

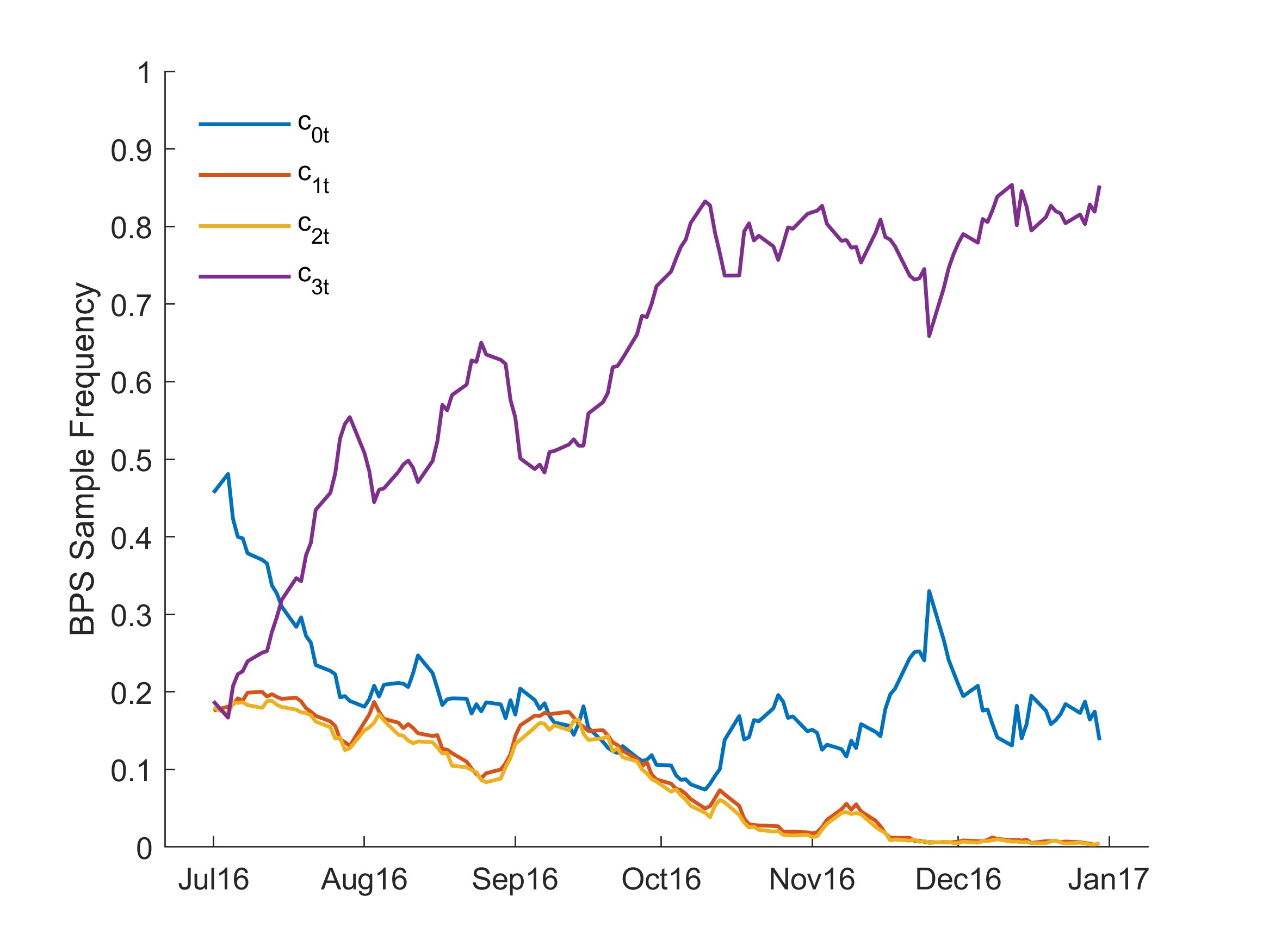

Further evaluation focuses on the BPS baseline weights and resulting sampling frequencies of the models in the MCMC analysis at each day in the sequential analysis over the full time period. The filtered trajectories of the sequentially updated posterior Dirichlet distributions for the is shown in Figure 6(a). Compare these summaries for the baseline weights to the resulting MCMC sampling frequencies of each model in Figure 6(b). The difference between these two figures results wholly from the effect of the BPS outcome-dependent weighting.

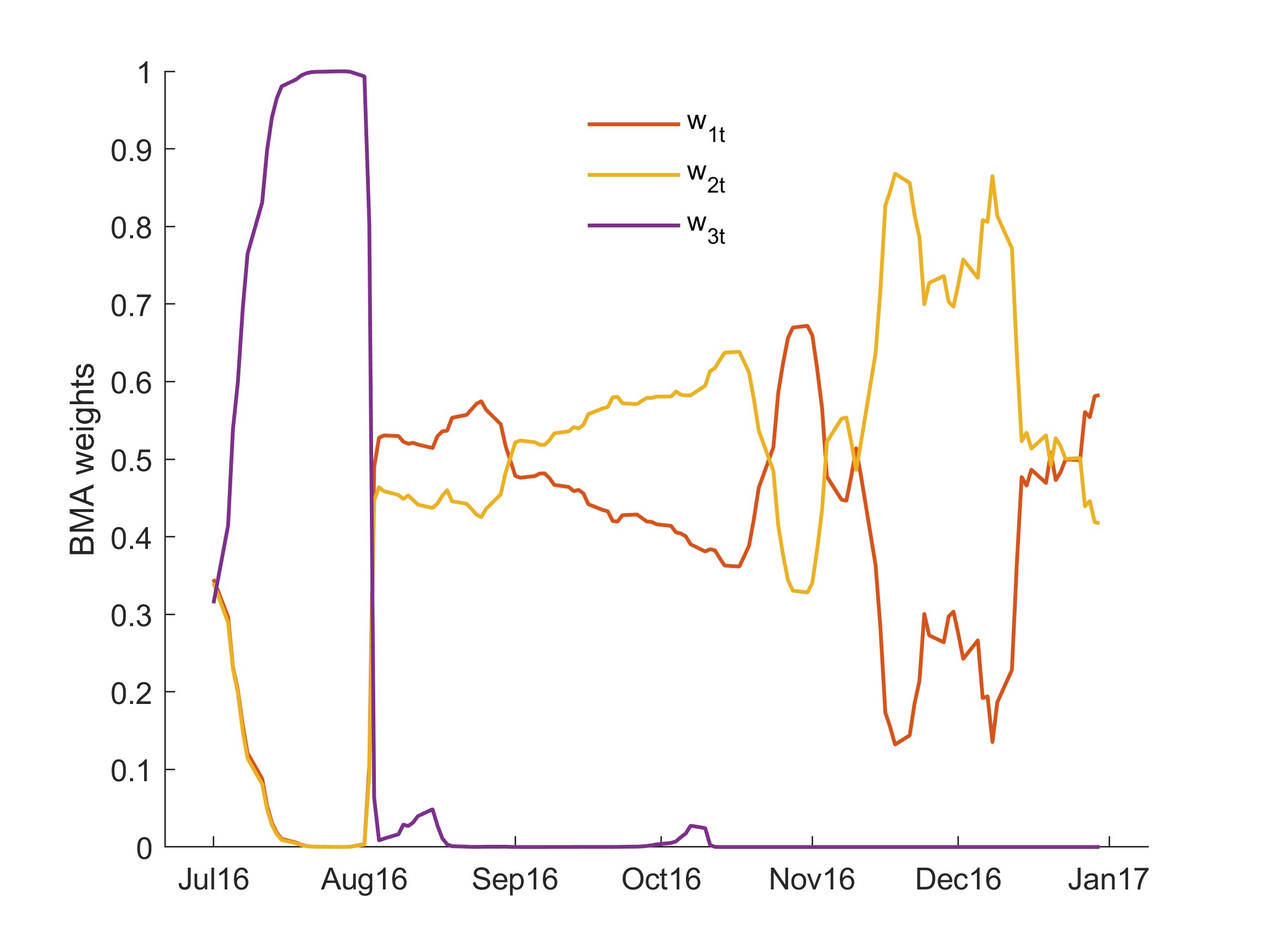

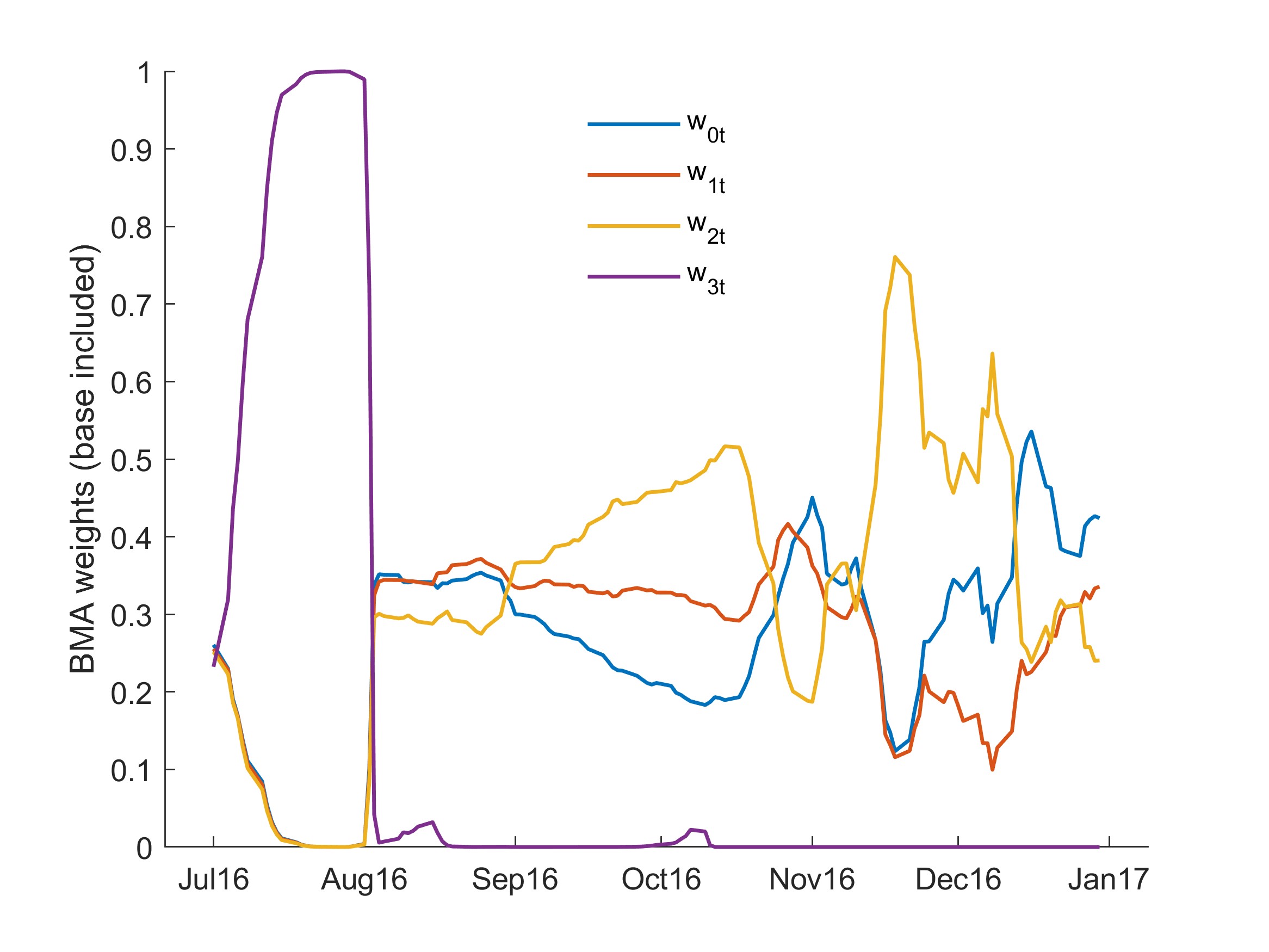

The trajectories of BPS weights contrast with those of BMA model probabilities; the latter are shown in Figure 7(a). As an additional comparison, Figure 7(b) shows BMA analysis extended to included the BPS baseline forecast model as if it were one of the models available to BMA analysis. The theory of BPS explicitly allows and recommends a baseline, but BMA does not and cannot, since it is defined wholly on the initial model set. This is the root cause of the model set completeness issue that bedevils BMA. Here, the extended analysis reflected in Figure 7(b) adds to the BMA simply to advantage BMA in the comparison; since this is an ad-hoc extension of BMA, this is denoted as BMAx.

In this empirical study, BMA effectively settles on an even split of weights between the TVAR models after an initial learning period that showed preference for the locally linear DLM. Under BMA, posterior model probabilities eventually converge on a single model, so with additional data it is expected that the BMA weights will favor one of the TVAR models. Since BMA scores 1-day ahead forecasts, this is likely to be the simpler or In contrast, BPS is open to any one model being favored over time and will not degenerate to any one (wrong) model as samples accrue. This is a theoretical feature of BPS, and an aspect that complements the impact of using a baseline distribution to allow for model set incompleteness. In this example, BPS prefers the DLM that BMA discards, unless its predictions are too far from expectations conditional on predictions from the TVAR models. When the preferred model makes forecasts that are too extreme, BPS falls back to favor the baseline model. Note that although and receive very little weight in the forecast combination itself, these forecasts are still used to balance the up/down-weighting of all models against the baseline

In terms of predictive accuracy, some summaries are given in Table 1. In addition to comparing the individual models, BPS, BMA and BMAx, the summary includes an equally-weighted linear pool of the forecast densities from each of the 3 models (POOL), and an advantaged extension that is an equally-weighted linear pool of the models plus the BPS baseline (POOLx). These are compared on the basis of traditional root mean square error of point forecasts (RMSE) as well as the realized value of the logs of the p.d.f.s of the 5-day forecast distributions (Log Score), each averaged over the last six months of 2016. Evidently, BPS outperforms each of the models as well as the two versions of both BMA and POOL. As with other studies using different BPS model forms (McAlinn and West, 2019) and as already noted above, it is no surprise that BMA is less accurate in multi-step forecasting since it inherently scores 1-step ahead accuracy in the prior-posterior model weight updates.

| Method | RMSE | Log Score |

|---|---|---|

| BPS | 1.00 | 1.000 |

| BMA | 1.09 | 0.956 |

| BMAx | 1.08 | 0.956 |

| POOL | 1.05 | 0.965 |

| POOLx | 1.06 | 0.963 |

| TVAR(1) | 1.09 | 0.946 |

| TVAR(2) | 1.10 | 0.946 |

| TVAR(5) | 1.11 | 0.945 |

| DLM | 1.15 | 0.886 |

5.4 More on Cross-Model Dependence

The nature of cross-model dependencies is impacted by the forms of the realized forecast model distributions and choices underlying the BPS analysis. The outcome-dependent weighting ability of BPS leads to learning on cross-model dependencies that impact on effective pooling weights in the synthesis. Elements of this at the BPS level include the time-varying bias vector , the time-varying cross-model dependence matrix , and the evolving base weights Then, perhaps more importantly in applications is the nature of the underlying model set. A model set that includes a collection of “very similar” models– similar in terms of generating concordant predictive distributions– will yield inferences on model dependencies that indicate the strong herding effect. Models that are more diverse in terms of the predictions they make will, and should, lead to inferences suggestive of weak cross-model dependencies and effective “decoupling,” which can ease interpretation.

In Section 5.3, the model structures are similar but the choice of relatively low discount factors within each model leads to some diversity in model-specific adaptability to incoming data over time. This is coupled with the focus on 5-day ahead forecasting. With this forecasting horizon, shorter-lag TVAR models show increasing differences relative to higher-lag TVAR models that can represent momentum effects in FX prices over a few days. This focus can enhance the ability of BPS to more highly weight longer-lag models in the synthesis pool, while also leading to weaker cross-model dependencies than with less adaptive models and shorter-term forecasting foci.

To highlight these aspects further, note that repeat analysis focused on 1-day ahead forecasting yields time trajectories of estimated correlations that are positive and much higher– in the 0.3-0.5 range. This bears out the reality that these models are very similar in terms of short-term forecasting, but much more distinguished in the BPS analysis based on the longer-term predictive performance. To further investigate this, consider the roles of (i) differing degrees of adaptability to data in the set of models, based on differing discount factors, and (ii) variants of the choice of synthesis function using the same model structures with different discount factors. An example using a synthesis function that responds to both consensus and herding effects– but, critically– with higher values of the within-model discount factors– underlies the point estimates of cross-model dependencies shown in Figure 8. The higher, positive correlations here reflect much stronger herding effects due heavily to the constraints within each model to slower adaptation to incoming data enforced by the use of high discount factors for the model-specific state vectors and volatilities.

6 Closing Comments

This paper provides an overview of the BPS framework for forecast model calibration, comparison and combination, and a detailed development of specific classes of mixture model-based BPS for forecast density pooling. While overviewing the general BPS approach and linking to recent developments of various stylized versions of BPS, a main focus here is the subclass of BPS models that yields linear mixture pooling of predictive distributions from each of a set of models. Discussion details the meanings and implications of outcome-dependent mixture weighting, putting into this foundational BPS setting a number of historical forecast pooling approaches and more recent, important developments in the Bayesian forecasting and econometrics literatures. In addition to allowing a decision maker to incorporate beliefs about specific forecasting models, BPS allows practitioners to understand the assumptions of commonly used methods for forecast combination– including simple pooling with equal (or other) weights on models, traditional Bayesian analysis underlying BMA, and a range of novel and practically relevant extensions that focus on interactions and resulting dependencies across models. In addition to reflecting model dependencies, a critical dimension of BPS pooling is the explicit, theoretically implied need to admit that “all models are wrong,” with the introduction of a baseline forecast density as a global alternative– or safe-haven– to weigh against the forecasts from the chosen set of models. This theoretically required component addresses long-standing questions in the traditional model averaging and combination literature: the issue of model set incompleteness. Then, the paper discusses extensions to time series settings, simply by adapting the core BPS theory to allow time-varying parameters underling the supra-Bayesian view of forecast combination defined by the theory of BPS. The series of examples of theoretically justified forecast density calibration and combination rules emerging from mixture-based BPS, and the detailed example in extension to sequential forecasting in an easily-accessibly FX time series setting, highlight the foundations and methodological opportunities.

Looking ahead, there are several immediate areas of research connections and for potential development. One key point is that, in general, it is not a requirement that the model densities are predictive densities for . These could instead be densities for values related to , and synthesizes this related information using . For example, suppose is tomorrow afternoon’s closing price of the stock for a certain company, and has available density forecasts for that company’s quarterly earnings, which will be announced sometime before tomorrow’s close, and for a relevant stock index. The general BPS framework admits such examples. Then, the overall setting of combining forecasts also links to the broader literatures on other approaches, with other desiderata, for predictive combination (e.g. West, 1984) and on bringing constraints to predictive models– whether deterministic or partial constraints on point forecasts or on full forecast distributions (e.g. Koop et al., 2019, 2020; West, 2023, and references therein). Further, the developments here are open to extension to involve additional, model-specific or external information in structuring choices of the central synthesis functions defining BPS. Some recent developments include ideas to exploit information on historical predictive performance of models (Lavine et al., 2021), and to explicitly integrate intended uses of BPS model predictions in resulting decision settings (Tallman and West, 2023), are noted. The foundational context and theory of BPS has broadened understanding of the scope of subjective Bayesian analysis in the setting of model uncertainty and its roles in prediction, and opened up a number of challenging and interesting directions for future development.

Appendix A Gibbs Sampler

This section details the Monte Carlo sampling of . In what follows, the subscript is omitted in notation, for clarity, with the understanding that sampling takes place at each single point in time after observing .

The Gibbs sampler has some complications due to the discrete nature of the mixture synthesis model (6). This is partly addressed by augmenting with a latent variable that denotes the component of the mixture; then

where the extended notation now makes explicit that depends on all three parameters. Then, the conditional likelihood is

Further, , so that for , , while . This is partially evident from the construction of the directed graph of the model, and the associated conditional independence graph:

The joint density is then

where is the product of model forecast densities.

A.1 Sampling

Analysis samples (with marginalized out), and then . Start with

The first term here is

The integrals here are evaluated via direct Monte Carlo integration based on samples from the The second term has closed form

| (11) | ||||

| (12) |

Normalizing the resulting product of these two terms gives the desired probabilities , and these are used to resample

A.2 Sampling

The full conditional density for breaks down into two cases depending on the value of . When , the likelihood for depends on :

In this case, , and the remainder of the vector is filled in using rejection sampling with acceptance probability . When ,

Rejection sampling is again used, this time with acceptance probability

A.3 Sampling

The full conditional density for is

Split the sampler into cases and . When , rejection sampling is straightforward. , so may be sampled from their prior and accepted with probability

When , is defined as . Then is sampled from its inverse-Wishart prior, , and the remainder of is sampled from its normal prior distribution conditional on and . The sample is accepted with probability .

A.4 Sampling

The full conditional density for also breaks down into two cases. The only relevant terms are and . When ,

If is a Dirichlet density with parameters , this allows for a conjugate update and exact sampling with . When ,

where

Rejection sampling is again used with acceptance probability .

Appendix B Variational Bayes

In the time series context with sequential forecasts, assumed parametric forms of the priors for ) and are adopted at each time step . Since posteriors at the previous time are represented in terms of Monte Carlo samples, the constraint to specific parametric forms for the current time are imposed using variational Bayes (VB). This identifies parameters of the approximating parametric forms that minimize the Küllback-Leibler (KL) divergence of the approximating distribution from that of the posterior samples. The underlying conceptual basis, and resulting methodology, is similar to that of Gruber and West (2016), in which the authors fit a normal-inverse-gamma distribution to posterior samples at each time point by minimizing the KL divergence of the approximating parametric form from the distribution represented by the Monte Carlo sample. This involves a combination of analytic solutions for some of the parameters and a simple numerical optimization for others, as follows.

B.1 Normal Inverse Wishart Approximation

Write the joint NIW distribution such that and . Using this notation, the optimal parameters are given by

-

1.

;

-

2.

;

-

3.

satisfies

where denotes the digamma function ;

-

4.

.

The expectations here are computed from the Monte Carlo sample. Note that and are directly evaluated, a simple Newton-Raphson optimisation generates and then is directly computed. This setting is a complete parallel to that in Gruber and West (2016) with the simple extension of normal, inverse gamma distributions there to NIW distributions here.

B.2 Dirichlet Approximation

For a approximation to the Monte Carlo posterior samples of the -vector on the simplex, the parameters satisfy

where again denotes the digamma function . An analytical solution is not available, but an approximate solution is again trivially implemented using a multivariate Newton-Raphson analysis, solving the above equation within an arbitrary tolerance.

Appendix C Application Details

This section contains additional details for the application in Section 5.

C.1 Model Specification

The example in Section 5 combines predictive densities from 4 pure time series models with time-varying parameters. All models are initialized at year-end 2015 and trained for the first half of 2016 before providing daily 5-step ahead forecasts for the second half of 2016. The models are trained from January 1, 2016 through June 24, 2016 (130 training observations) before producing the first 5-step ahead forecast for July 1, 2016.

A full description of the baseline and model densities requires detailing of initial priors and discount factors on model parameters. The specifications summarized here use the standard notation of West and Harrison (1997) and Prado et al. (2021) for each of these univariate dynamic linear models. The standard notation uses for the model state vector and for the variance of observations around the dynamic linear regression over time Each model has an initial normal prior on and an inverse-gamma (with harmonic mean ) on . These were chosen to reflect relatively vague initial priors for the example analysis. In each model, evolution variances for the coupled random-walk evolutions of and are specified through the use of two discount factors, one for the state vector and one for the residual variance.

The TVAR models differ only in the chosen AR lag. The priors in each have the following features: prior mean of the lag AR parameter is 0.97, that for higher-order AR parameters is 0. The initial prior mean for the intercept in the auto-regression of each model is set so that , the last daily value of the time series before the start of the data analysis time period. The initial variance matrix for the model state vector is diagonal with entries . The initial inverse-gamma prior for is defined by and . The discount factors for both the latent state vector and the residual variance are set to 0.95.

The locally linear DLM has initial prior as follows. The prior mean for the local level (intercept) at is , and that for the gradient from to is zero. The prior variance matrix The inverse-gamma distribution prior for is defined via and . The state and residual variance discount factors are set relatively low at 0.9 to allow faster adaptation to daily variation in FX series.

At each time point, predictive densities are sampled using standard methodology, projecting the model-based forecasts to 5-days ahead in terms of a Monte Carlo sample for each model. Then, a scale- and location- shifted Student distribution is fitted to each of the resulting Monte Carlo samples; this uses the Mathworks fitdist function. These resulting T distributions are taken to define the inputs to the BPS, BMA and POOL analyses.

C.2 Synthesis Function

For clarity, again drop the subscript and denote weight functions as and , with the implicit understanding that they also depend on and ; recall that is defined as the point forecast of the baseline density with offsets given by a bias vector , while represents cross-model dependencies.

The synthesis function is as defined in eqn. (10) with the additional specification

| (13) | |||

| for , with | |||

For , set

where , and and represent the conditional variance and regression vector implied by . This construction accounts for model consensus by discounting far from the conditional expectation.

C.3 BPS Priors and Discount Factors

Consider first the NIW prior specified at for . As the data do not directly inform on , ’s subjective prior at time can be especially important. The reported analysis adopts an inverse-Wishart prior with degrees of freedom and point estimate . is diagonal with elements equal to , the (squared) scale parameter from the baseline density for , reflecting an uninformed prior. The bias vector has conditionally normal distribution . The time conditional normal prior for is likewise centered at zero, so that initially for all . Set , implying a prior variance for the latent states given alone that is double that of the conditional variance given both and . The time Dirichlet prior for the base synthesis weights is taken as the uniform Dirichlet.

The time posteriors for and (having observed ) are denoted and With respective discount factors , , and , the time priors for and are written

and

That is, slightly increases the scalar on the conditional variance from to , while slightly decreases in the degrees of freedom in the IW distribution. In the Dirichlet, scaling the parameters down maintains the same point estimates while increasing uncertainty. The dynamic model discount factors are chosen to indicate the expectation of generally stable patterns of bias and cross-model dependencies over time. The discount factor controlling the time evolution of in section 5 is 0.98, and those related to the time evolution of and the Dirichlet time evolution of are 0.97.

References

- Aastveit et al. (2023) Aastveit, K.A., Cross, J.L., van Dijk, H.K., 2023. Quantifying time-varying forecast uncertainty and risk for the real price of oil. Journal of Business and Economic Statistics 41, 523–537. doi:10.1080/07350015.2022.2039159.

- Aastveit et al. (2014) Aastveit, K.A., Gerdrup, K.R., Jore, A.S., Thorsrud, L.A., 2014. Nowcasting GDP in real time: A density combination approach. Journal of Business & Economic Statistics 32, 48–68. doi:10.1080/07350015.2013.844155.

- Aastveit et al. (2019) Aastveit, K.A., Mitchell, J., Ravazzolo, F., van Dijk, H.K., 2019. The evolution of forecast density combinations in economics. Oxford Research Encyclopedia of Economics and Finance doi:10.1093/acrefore/9780190625979.013.381.

- Amisano and Giacomini (2007) Amisano, G.G., Giacomini, R., 2007. Comparing density forecasts via weighted likelihood ratio tests. Journal of Business & Economic Statistics 25, 177–190. doi:10.1198/073500106000000332.

- Bassetti et al. (2018) Bassetti, F., Casarin, R., Ravazzolo, F., 2018. Bayesian nonparametric calibration and combination of predictive distributions. Journal of the American Statistical Association 113, 675–685. doi:10.1080/01621459.2016.1273117.

- Bernardo and Smith (1994) Bernardo, J.M., Smith, A.F.M., 1994. Bayesian Theory. Wiley, New York.

- Billio et al. (2012) Billio, M., Casarin, R., Ravazzolo, F., van Dijk, H.K., 2012. Combination schemes for turning point predictions. Quarterly Review of Finance and Economics 52, 402–412. doi:10.1016/j.qref.2012.08.002.

- Billio et al. (2013) Billio, M., Casarin, R., Ravazzolo, F., van Dijk, H.K., 2013. Time-varying combinations of predictive densities using nonlinear filtering. Journal of Econometrics 177, 213–232. doi:10.1016/j.jeconom.2013.04.009.

- Clemen (1989) Clemen, R.T., 1989. Combining forecasts: A review and annotated bibliography. International Journal of Forecasting 5, 559–583. doi:10.1016/0169-2070(89)90012-5.

- Clemen and Winkler (1999) Clemen, R.T., Winkler, R.L., 1999. Combining probability distributions from experts in risk analysis. Risk Analysis 19, 187–203. doi:10.1111/j.1539-6924.1999.tb00399.x.

- Clemen and Winkler (2007) Clemen, R.T., Winkler, R.L., 2007. Aggregating probability distributions, in: W. Edwards, R.M., von Winterfeldt, D. (Eds.), Advances in Decision Analysis: From Foundations to Applications. Cambridge University Press. chapter 9, pp. 154–176. doi:10.1017/CBO9780511611308.010.

- Clyde and George (2004) Clyde, M., George, E.I., 2004. Model uncertainty. Statistical Science 19, 81–94. doi:10.1214/088342304000000035.

- Clyde and Iversen (2013) Clyde, M., Iversen, E.S., 2013. Bayesian model averaging in the open framework, in: Damien, P., Dellaportes, P., Polson, N.G., Stephens, D.A. (Eds.), Bayesian Theory and Applications. Clarendon: Oxford University Press, pp. 483–498. doi:10.1093/acprof:oso/9780199695607.003.0024.

- Diaconis and Zabell (1982) Diaconis, P., Zabell, S.L., 1982. Updating subjective probability. Journal of the American Statistical Association 77, 822–830. doi:10.1080/01621459.1982.10477893.

- Diebold and Shin (2019) Diebold, F.X., Shin, M., 2019. Machine learning for regularized survey forecast combination: Partially-egalitarian LASSO and its derivatives. International Journal of Forecasting 35, 1679–1691. doi:10.1016/j.ijforecast.2018.09.006.

- Diebold et al. (2020) Diebold, F.X., Shin, M., Zhang, B., 2020. On the aggregation of probability assessments: Regularized mixtures of predictive densities for Eurozone inflation and real interest rates. doi:10.48550/ARXIV.2012.11649.

- Genest and Schervish (1985) Genest, C., Schervish, M.J., 1985. Modelling expert judgements for Bayesian updating. Annals of Statistics 13, 1198–1212. doi:10.1214/aos/1176349664.

- Geweke and Amisano (2012) Geweke, J., Amisano, G.G., 2012. Prediction with misspecified models. The American Economic Review 102, 482–486. doi:10.1257/aer.102.3.482.

- Geweke and Amisano (2011) Geweke, J.F., Amisano, G.G., 2011. Optimal prediction pools. Journal of Econometrics 164, 130–141. doi:10.1016/j.jeconom.2011.02.017.

- Giannone et al. (2021) Giannone, D., Lenza, M., Primiceri, G.E., 2021. Economic predictions with big data: The illusion of sparsity. Econometrica 89, 2409–2437. doi:10.3982/ECTA17842.

- Gruber and West (2016) Gruber, L.F., West, M., 2016. GPU-accelerated Bayesian learning in simultaneous graphical dynamic linear models. Bayesian Analysis 11, 125–149. doi:10.1214/15-BA946.

- Gruber and West (2017) Gruber, L.F., West, M., 2017. Bayesian forecasting and scalable multivariate volatility analysis using simultaneous graphical dynamic linear models. Econometrics and Statistics , 3–22doi:10.1016/j.ecosta.2017.03.003.

- Hall and Mitchell (2007) Hall, S.G., Mitchell, J., 2007. Combining density forecasts. International Journal of Forecasting 23, 1–13. doi:10.1016/j.ijforecast.2006.08.001.

- de Heide et al. (2019) de Heide, R., Kirichenko, A., Mehta, N., Grünwald, P., 2019. Safe-Bayesian generalized linear regression. doi:10.48550/ARXIV.1910.09227.

- Hoogerheide et al. (2010) Hoogerheide, L., Kleijn, R., Ravazzolo, F., Van Dijk, H.K., Verbeek, M., 2010. Forecast accuracy and economic gains from Bayesian model averaging using time-varying weights. Journal of Forecasting 29, 251–269. doi:10.1002/for.1145.

- Irie and West (2019) Irie, K., West, M., 2019. Bayesian emulation for multi-step optimization in decision problems. Bayesian Analysis 14, 137–160. doi:10.1214/18-BA1105.

- Jeffrey (1990) Jeffrey, R.C., 1990. The Logic of Decision. 2nd ed., University of Chicago Press.

- Kapetanios et al. (2015) Kapetanios, G., Mitchell, J., Price, S., Fawcett, N., 2015. Generalised density forecast combinations. Journal of Econometrics 188, 150–165. doi:10.1016/j.jeconom.2015.02.047.

- Kascha and Ravazzolo (2010) Kascha, C., Ravazzolo, F., 2010. Combining inflation density forecasts. Journal of Forecasting 29, 231–250. doi:10.1002/for.1147.

- Koop et al. (2019) Koop, G., McIntyre, S., Mitchell, J., 2019. Uk regional nowcasting using a mixed frequency vector auto‐regressive model with entropic tilting. Journal of the Royal Statistical Society: Series A (Statistics in Society) 183, 91–119. doi:doi.org/10.1111/rssa.12491.

- Koop et al. (2020) Koop, G., McIntyre, S., Mitchell, J., Poon, A., 2020. Regional output growth in the United Kingdom: More timely and higher frequency estimates from 1970. Journal of Applied Econometrics 35, 176–197. doi:10.1002/jae.2748.

- Lavine et al. (2021) Lavine, I., Lindon, M., West, M., 2021. Adaptive variable selection for sequential prediction in multivariate dynamic models. Bayesian Analysis 16, 1059–1083. doi:10.1214/20-BA1245.

- Lindley et al. (1979) Lindley, D.V., Tversky, A., Brown, R.V., 1979. On the reconciliation of probability assessments. Journal of the Royal Statistical Society Series A (Statistics in Society) 142, 146–180. doi:10.2307/2345078.

- Loaiza-Maya et al. (2021) Loaiza-Maya, R., Martin, G.M., Frazier, D.T., 2021. Focused Bayesian prediction. Journal of Applied Econometrics 36, 517–543. doi:10.1002/jae.2810.

- McAlinn (2021) McAlinn, K., 2021. Mixed-frequency Bayesian predictive synthesis for economic nowcasting. Journal of the Royal Statistical Society (Series C: Applied Statistics) 70, 1143–1163. doi:10.1111/rssc.12500.

- McAlinn et al. (2020) McAlinn, K., Aastveit, K.A., Nakajima, J., West, M., 2020. Multivariate Bayesian predictive synthesis in macroeconomic forecasting. Journal of the American Statistical Association 115, 1092–1110. doi:10.1080/01621459.2019.1660171.

- McAlinn et al. (2018) McAlinn, K., Aastveit, K.A., West, M., 2018. Bayesian predictive synthesis. Discussion of: Using stacking to average Bayesian predictive distributions, by Y. Yao et al. Bayesian Analysis 13, 971–973. doi:10.1214/17-BA1091.

- McAlinn and West (2019) McAlinn, K., West, M., 2019. Dynamic Bayesian predictive synthesis in time series forecasting. Journal of Econometrics 210, 155–169. doi:10.1016/j.jeconom.2018.11.010.

- Pettenuzzo and Ravazzolo (2016) Pettenuzzo, D., Ravazzolo, F., 2016. Optimal portfolio choice under decision-based model combinations. Journal of Applied Econometrics 31, 1312–1332. doi:10.1002/jae.2502.

- Prado et al. (2021) Prado, R., Ferreira, M.A.R., West, M., 2021. Time Series: Modeling, Computation & Inference. 2nd ed., Chapman & Hall/CRC Press. doi:10.1201/9781351259422.

- Rufo et al. (2012) Rufo, M.J., Martín, J., Pérez, C.J., 2012. Log-linear pool to combine prior distributions: A suggestion for a calibration-based approach. Bayesian Analysis 7, 411–438. doi:10.1214/12-BA714.

- Tallman and West (2023) Tallman, E., West, M., 2023. Bayesian predictive decision synthesis. Submitted for publication ArXiv:2206.03815.

- Timmermann (2004) Timmermann, A., 2004. Forecast combinations, in: G. Elliott, C.G., Timmermann, A. (Eds.), Handbook of Economic Forecasting. North Holland. volume 1. chapter 4, pp. 135–196. doi:10.1016/S1574-0706(05)01004-9.

- West (1984) West, M., 1984. Bayesian aggregation. Journal of the Royal Statistical Society Series A (Statistics in Society) 147, 600–607. doi:10.2307/2981847.

- West (1988) West, M., 1988. Modelling expert opinion (with discussion), in: Bernardo, J.M., DeGroot, M.H., Lindley, D.V., Smith, A.F.M. (Eds.), Bayesian Statistics 3, Oxford University Press. pp. 493–508.

- West (1992) West, M., 1992. Modelling agent forecast distributions. Journal of the Royal Statistical Society (Series B: Methodological) 54, 553–567. doi:10.1111/j.2517-6161.1992.tb01896.x.

- West (2020) West, M., 2020. Bayesian forecasting of multivariate time series: Scalability, structure uncertainty and decisions (with discussion). Annals of the Institute of Statistical Mathematics 72, 1–44. doi:10.1007/s10463-019-00741-3.

- West (2023) West, M., 2023. Perspectives on constrained forecasting. Bayesian Analysis doi:10.1214/23-BA1379.

- West and Crosse (1992) West, M., Crosse, J., 1992. Modelling of probabilistic agent opinion. Journal of the Royal Statistical Society (Series B: Methodological) 54, 285–299. doi:10.1111/j.2517-6161.1992.tb01882.x.

- West and Harrison (1997) West, M., Harrison, P.J., 1997. Bayesian Forecasting & Dynamic Models. 2nd ed., Springer.

- Zhao et al. (2016) Zhao, Z.Y., Xie, M., West, M., 2016. Dynamic dependence networks: Financial time series forecasting and portfolio decisions (with discussion). Applied Stochastic Models in Business and Industry 32, 311–339. doi:10.1002/asmb.2161.