NewAppendix References

Revealed Price Preference: Theory and Empirical Analysis

Abstract.

To determine the welfare implications of price changes in demand data, we introduce a revealed preference relation over prices. We show that the absence of cycles in this relation characterizes a consumer who trades off the utility of consumption against the disutility of expenditure. Our model can be applied whenever a consumer’s demand over a strict subset of all available goods is being analyzed; it can also be extended to settings with discrete goods and nonlinear prices. To illustrate its use, we apply our model to a single-agent data set and to a data set with repeated cross-sections. We develop a novel test of linear hypotheses on partially identified parameters to estimate the proportion of the population who are revealed better off due to a price change in the latter application. This new technique can be used for nonparametric counterfactual analysis more broadly.

1. Introduction

A central question in economic analysis is the determination of the welfare effect of price changes. As an example, suppose we observe a consumer’s purchases of two goods, gasoline and food, from two separate trips to a grocery store with an on site gasoline retailer. In the first instance , the prices are of gasoline and food respectively and she buys a bundle . In her second trip , the prices are and she purchases . The most basic welfare question one can ask here is whether the consumer is better off at the prices prevailing at or at (keeping fixed the prices of all other goods she consumes)? In this paper, we introduce a theoretical framework based on revealed preference, along with a nonparametric econometric technique, that would allow us to answer questions of this type.

A typical approach to this problem is to model the consumer as having a quasilinear utility function since, in particular, this allows for simple “sufficient statistics” analysis of welfare gains or losses using a Harberger formula (see Chetty (2009) and most recently Kleven (2021) for an overview of this approach). Of course, the second term () in the quasilinear utility function captures the fact that the goods being analyzed (food and gasoline in our simple example) do not constitute the universe of the consumer’s consumption; expenditure lowers utility because it reduces the consumption of an outside (numeraire) good.

The point of departure of our analysis is the following simple observation. Without having to model the consumer’s preference as quasilinear (or taking any other specific functional form) we can still conclude that she is better off at compared to . This is because whereas . In other words, if the prices prevailing at were instead of , the consumer would be better off since purchasing the same bundle would cost less, leaving the consumer with more money to buy other goods (outside the set of goods analyzed).111Another way of seeing this is the following. Suppose is a supermarket where the prices are and we observe the bundle being bought by a consumer. If at supermarket , the prices are , then we know that the consumer would prefer this supermarket, since the same purchases at would cost less at . More generally, the consumer has a preference over prices that an analyst could at least partially discern from the data: if at observations and , we find that , then

the consumer has revealed that she (strictly) prefers the price to the price .

Welfare comparisons made in this way will only be consistent if the revealed preference relation over prices is free of cycles, a property we call the generalized axiom of price preference (GAPP). This leads inevitably to the following question: precisely what does GAPP mean for consumer behavior?

Augmented Utility Functions: To answer this question, we assume that the analyst collects a data set from a consumer; each observation consists of the prices of goods (representing some but not all the goods she consumes) and the consumer’s demand at those prices. We show that GAPP (on ) is both necessary and sufficient for the existence of a strictly increasing function that rationalizes in the following sense:

The function should be interpreted as an expenditure-augmented utility function, where is the consumer’s utility when she acquires at the cost of . It recognizes that the consumer’s expenditure on the observed goods is endogenous and dependent on prices: she could in principle spend more than what she actually spent (note that she optimizes over ) but the trade-off is the dis-utility of greater expenditure. Note that the quasilinear utility function is a special case of an augmented utility function.

The augmented utility model has a number of features that makes it widely applicable and easy to use. We highlight a few of them.

(1) Being more general than the quasilinear model, it does not have some of its overly strong implications on the structure of consumer demand (see Section 2.3). In particular, it is broad enough to accommodate phenomena emphasized in the behavioral economics literature, such as reference dependence, mental budgeting and inattention to prices. We briefly describe the first of these here, a more detailed discussion can be found in Section 2.4. Kőszegi and Rabin (2006) and Heidhues and Kőszegi (2008) argue that consumption decisions can depend not just on the actual prices but also on the prices the consumer expected to pay. Specifically, the disutility from spending is greater if the expected price was lower than the sticker price and vice versa. A simple way they propose of capturing this phenomenon is the following function

The first two terms capture standard quasilinear preferences whereas the third term captures a general form of reference dependence.222For a related model of reference prices leading to a similar functional form, see Sakovics (2011). In Koszegi and Rabin’s terminology, the consumer gets “gain-loss utility” by comparing the expenditure she incurs on a bundle against the expenditure she expected to incur, where are her reference prices.333A common choice for is where it is typically assumed that or that the consumer feels losses relative to the reference point more severely than commensurate gains.

(2) In this model, a consumer’s utility at prices is given by , which obviously leads to a ranking or preference on prices. Going further, it is possible to develop notions analogous to compensating and equivalent variations, which gives us a quantitative sense of how much one set of prices is ranked above another and could form the basis for interpersonal comparisons (see Section 3.3).

(3) Readers familiar with Afriat’s Theorem (Afriat, 1967) will no doubt have already noticed that we are working in a similar framework. That theorem characterizes a data set that could be rationalized in the following sense: there is such that for all that satisfy . The notion of rationalization in our model is distinct from that in Afriat’s Theorem (even the utility functions have different domains) and there are data sets that could be rationalized in one sense but not the other. We explain these differences in Sections 2.2 and 3.1.

Empirical researchers who apply Afriat’s Theorem must contend with cases where a data set is not exactly rationalizable. They have developed an easily interpretable way of measuring how close a data set is to being rationalized known as the critical cost efficiency index. In Section 3.4 we develop a similarly intuitive index that should facilitate empirical applications of the augmented utility model.

(4) Our notion of revealed preference over prices is not simply applicable to a Euclidean consumption space. It applies even when goods can only be consumed in discrete quantities (as is often the case in empirical IO models) or when they are represented by characteristics. Furthermore, when prices are nonlinear, it is still possible to compare price systems by asking if an agent could replicate the purchases under one system in another price system. Requiring non-cycling comparisons in this case leads to a natural extension of GAPP and the augmented utility model, which we explain in Section 4.

Random Augmented Utility Model (RAUM): In the second part of the paper, we develop the random version of the augmented utility model, in order to study the demand distribution of a population of consumers drawn from repeated cross-sectional data. We first devise a test to check if the data are consistent with the RAUM. We then develop a procedure to estimate the proportion of consumers who are made better or worse off by a given change in prices; welfare analysis of this kind under general preference heterogeneity is a challenging empirical issue, and has attracted considerable recent research (see, for example, Hausman and Newey (2016) and its references).

Unlike the case of data collected from a single individual, it is worth noting that, in this case, both model testing and welfare analysis are statistical since we need to account for sampling error inherent in repeated cross sectional data. Our RAUM test uses existing (though recently developed) econometric methods. On the other hand, to carry out the welfare analysis, we develop new theoretical econometric results; it is worth stressing that this is a stand alone contribution that has applications beyond this paper.

For reasons we shall now explain, testing the RAUM on actual repeated cross-sectional data (such as household survey data) turns out to be a lot more straightforward than testing the random version of the standard budget-constrained utility model where the population is required to be rational in the sense of Afriat’s Theorem (defined earlier). We refer to the latter model as RUM (random utility model) for short. The test for RUM is broadly set out in McFadden and Richter (1991), but two challenges must first be overcome. First, McFadden and Richter (1991) do not account for finite sample issues as they assume that the econometrician observes the population distributions of demand; this hurdle was recently overcome by Kitamura and Stoye (2018) who develop a testing procedure which incorporates sampling error. Second, the test suggested by McFadden and Richter (1991) requires the observation of large samples of consumers who face not only the same prices but also make identical total expenditures. This feature is not true of any real observational data where a consumer’s demand (and thus total expenditure) on a set of observed goods will typically be price dependent. Thus to implement their test, Kitamura and Stoye (2018) need to first estimate demand distributions at a fixed level of (median) expenditure, which requires the use an instrumental variable technique (with all its attendant assumptions) to adjust for the endogeneity of observed total expenditure.

In contrast, the RAUM can be tested directly on household survey data, even when the demand distribution at a given price vector implies heterogenous levels of total expenditure across consumers.444A bit more formally, it is possible for two demand bundles and in the support of the demand distribution when prices are to satisfy . This allows us to estimate the demand distribution by simply using sample frequencies and we can avoid the above-mentioned additional layer of demand estimation needed for testing RUM.

The reason for this remarkable simplification is somewhat ironic: we show that a data set is consistent with the RAUM if, and only if, a converted version of the data set (which results in identical expenditures at each price) of the type envisaged by McFadden and Richter (1991) passes the RUM test suggested by them. In other words, we apply the test suggested by McFadden and Richter (1991), but not for the model they have in mind. This trick also means that we can use, and in a more straightforward way, the econometric techniques in Kitamura and Stoye (2018).

Assuming that a data set is consistent with our model, we can then evaluate the welfare impact of an observed change in prices. Indeed, if we observe the true distribution of demand at each price, it is possible to impose bounds (based on theory) on the proportion of the population who are revealed better off or worse off following an observed change in prices. Of course, when samples are finite, these bounds instead have to be estimated. To do so, we develop new econometric techniques that allow us to form confidence intervals on the proportion of consumers who are better or worse off; these techniques build on the econometric theory in Kitamura and Stoye (2018) but are distinct from it.

We emphasize that these new econometric techniques can be more generally applied to linear hypothesis testing of parameter vectors that are partially identified, even in models that are unrelated to demand theory (see, for example, Lazzati, Quah, and Shirai (2018)). They provide a new method for estimation and inference in nonparametric counterfactual analysis and, since the evaluation of counterfactuals is an important goal of empirical research, they are potentially very useful to practitioners.

Empirical Applications: We use separate data sets to demonstrate how welfare analysis can be done using both the deterministic and random versions of our model. First, we use the deterministic augmented utility model to analyze panel data from the Mexican conditional cash transfer program Progresa. Recently, Attanasio and Pastorino (2020) showed that sellers responded to these transfers by altering the nonlinear prices they charge for staples. We focus our analysis on the untreated households that did not receive cash transfers; we show, via revealed preference over the nonlinear price systems, that these households have tended to benefit from the price changes that occurred during the observation period. This is consistent with the finding in Attanasio and Pastorino (2020) that the change in the wealth distribution induced by Progresa led to larger quantity discounts (which favored the untreated households because they are usually better-off and consumed more).

Finally, we show how the RAUM can be used to estimate the welfare impact of the changes in observed prices in repeated cross-sectional data. Specifically, we take the model to two separate national household expenditure data sets from Canada and the U.K. and show that we can meaningfully estimate bounds on the percentage of households who are better and worse off. Even though these bounds are typically only partially identified, the estimated bounds are almost always narrower than ten percentage points and often substantially narrower than that. This demonstrates how to operationalize our novel econometric methodology to conduct inference for counterfactuals.

2. The Deterministic Model

We consider an econometrician who is studying a consumer’s demand for goods. We assume an idealized environment suitable for partial equilibrium analysis, where the consumer’s demand for these goods at different prices are observed, while the consumer’s wealth and the prices of other goods are held fixed.555Under fairly standard (but strong) assumptions, changes to the external environment can be precisely justified by deflating the prices of the goods (see Section 3.5).

Specifically, the econometrician collects a data set with a finite number of observations; each observation can be represented as , where are the prices of the goods and is the bundle of those goods purchased by the consumer.666We postpone the discussion of discrete consumption spaces and nonlinear pricing to Section 4. We denote the data set by . (We shall slightly abuse notation and use to refer both to the (finite) number of observations and to the set ; similarly, could denote both the number, and the set, of commodities.)

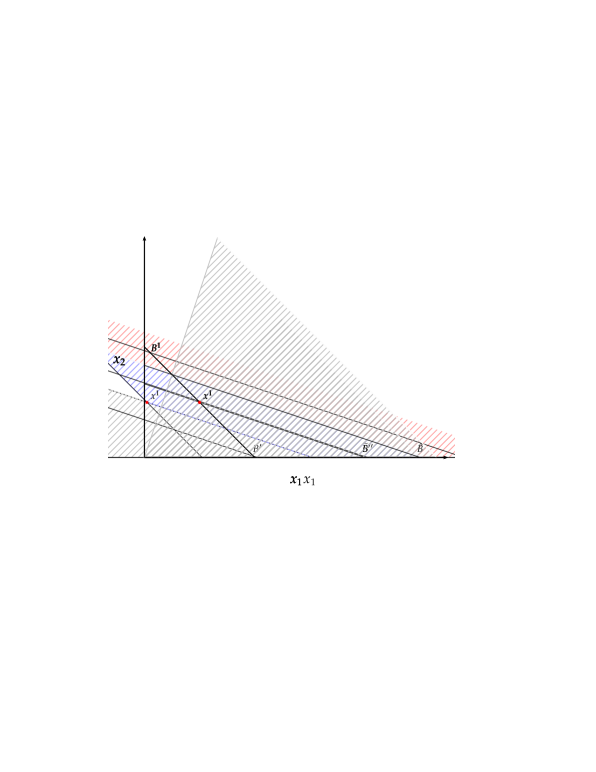

We begin with a basic question: given , can the econometrician sign the welfare impact of a price change from to ? Perhaps the most intuitive welfare comparison that can be made in this setting is as follows: if at prices , the econometrician finds that then he may conclude that the agent is better off at the price vector compared to . This is because, at the price the consumer can, if she wishes, buy the bundle bought at and she would still have money left over to buy other things, so she must be strictly better off at . This ranking is eminently sensible, but can it lead to inconsistencies?

Example 1.

Consider a two observation data set

Since , it seems that the consumer is better off at prices than at ; however, it is also true that , which gives the opposite conclusion.

This example shows that for an econometrician to be able to consistently compare the consumer’s welfare at different prices, some restriction has to be imposed on the data set. To be precise, define the binary relations and on , that is, the set of price vectors observed in , in the following manner:

We say that price is directly (strictly) revealed preferred to if , that is, whenever the bundle is (strictly) cheaper at prices than at prices . We denote the transitive closure of by , that is, for and in , we have if there are , ,…, in such that , ,…, , and ; in this case we say that is revealed preferred to . If anywhere along this sequence, it is possible to replace with then we say that is revealed strictly preferred to and denote that relation by .777Notice that it makes sense to write even if is not in , since the demand at is not needed in the definition revealed preference. Similarly, it is possible to define and the transitive extensions and . This observation is useful later on, in Sections 3.3 and 5.3. . The following restriction, which excludes circularity in the econometrician’s assessment of the consumer’s wellbeing at different prices, is a bare minimum condition to impose on .

Definition 2.1.

The data set satisfies the Generalized Axiom of Price Preference or GAPP if there are no observations such that and .

This in turn leads naturally to the following question: if a consumer’s observed demand behavior obeys GAPP, what could we say about her decision making procedure?

2.1. The Expenditure-Augmented Utility Model

An expenditure-augmented utility function (or simply, an augmented utility function) is a function , where is the consumer’s utility when she spends to purchase the bundle . We require that is strictly increasing in the last argument (in other words, utility is strictly decreasing in expenditure), which captures the tradeoff the consumer faces between consuming and consuming other goods (outside the set ).

At a given price , the consumer chooses a bundle to maximize . We denote the indirect utility at price by

| (1) |

If the consumer’s augmented utility maximization problem has a solution at every price vector , then is also defined at those prices and this induces a reflexive, transitive, and complete preference over prices in .

A data set is rationalized by an augmented utility function if there exists such a function with

| (2) |

It is straightforward to see that GAPP is necessary for a data set to be rationalized by an augmented utility function. First, notice that if , then , and so

Furthermore, if , and in that case . Suppose GAPP were not satisfied and there were two observations such that and . Then there would exist such that

which is impossible.

Our main theoretical result, which we state next, also establishes the sufficiency of GAPP for rationalization. Moreover, the result states that whenever can be rationalized, it can be rationalized by an augmented utility function with a list of properties that make it convenient for analysis.

Theorem 1

Given a data set , the following are equivalent:

-

(1)

is rationalized by an augmented utility function.

-

(2)

satisfies GAPP.

-

(3)

is rationalized by an augmented utility function that is strictly increasing, continuous, and concave. Moreover, is such that has a solution for all .

2.2. Afriat’s Theorem and Proof of Theorem 1

Before presenting the proof of Theorem 1, it is worth providing a short description of the standard theory of revealed preference and, Afriat’s Theorem, its central result. This will be useful not just because we will invoke the result several times but also since it will serve as an important point of contrast for our axiom and results.

The standard theory due to Afriat (1967) is built formally on the same primitives as our model: a finite data set of prices and corresponding consumption bundles. Unlike our model however, it is assumed that the observed goods correspond to the universe of the consumer’s consumption. Formally, a data set is said to be rationalized by a utility function if there exists a locally nonsatiated888This means that at any bundle and open neighborhood of , there is a bundle in the neighborhood with strictly higher utility. utility function such that

| (3) |

In words, this criterion asks whether there is a utility function defined over the observed goods such that the consumer is utility maximizing at every observation over the fixed budget corresponding to the observed expenditure.

Of course, data sets (outside of laboratory data) almost never contain the universe of consumed goods and the consumer’s true budget set is not observed, especially when one takes into account the possibility of borrowing and saving. Given this, when checking if a data set can be rationalized in the sense of (3), we are effectively testing whether the consumer is maximizing a sub-utility function defined specifically on those goods (or equivalently, has weakly separable preferences).

It should be clear that rationalization in the sense of (3) is distinct from rationalization by an augmented utility function. The augmented utility model specifically takes into account the impact of the prices of these goods on the consumption of other goods; it is necessarily a partial equilibrium model, and designed for partial equilibrium welfare analysis of the type carried out in empirical industrial organization or public economics. An example is the study of the welfare impact of a sales tax levied on a subset of goods.

It is possible that a data set can be rationalized in both senses, but that does not hold in general. The precise conditions needed for rationalization by a utility function are given by Afriat’s Theorem, which we now describe.

Revealed preference in Afriat’s setting is captured by two binary relations, and which are defined on the set of chosen bundles observed in , that is, the set , as follows:

We say that the bundle is directly revealed (strictly) preferred to if , that is, whenever the bundle is (strictly) cheaper at prices than the bundle . This terminology is intuitive: if the agent is maximizing some locally nonsatiated utility function , then () must imply that .

We denote the transitive closure of by , that is, for and in , we have if there are , ,…, in such that , , and ; in this case, we say that is revealed preferred to . If anywhere along this sequence, it is possible to replace with then we say that is revealed strictly preferred to and denote that relation by . Clearly, if is rationalizable by some locally nonsatiated utility function , then implies that . This observation in turn implies that a necessary condition for rationalization by a utility function is that the revealed preference relation has no cycles.

Definition 2.2.

A data set satisfies the Generalized Axiom of Revealed Preference or GARP if there are no observations such that and .

The main insight of Afriat’s Theorem is to show that this condition is also sufficient (the formal statement can be found in the online Appendix A.1.1).

Having described Afriat’s Theorem, we are now in a position to prove Theorem 1.

Proof of Theorem 1. We will show that . We have already argued that and by definition.

Choose a number and define the augmented data set . This data set augments since we have introduced an good, which we have priced at 1 across all observations, with the demand for this good equal to .

The crucial observation to make here is that

which means that

Similarly,

and so

Consequently, satisfies GAPP if and only if satisfies GARP. Applying Afriat’s Theorem when satisfies GARP, there is (notice that is defined on and not just ; see Remark 3 in Appendix A.1.1) such that

| (4) |

The function can be chosen to be strictly increasing, continuous, and concave, and the lower envelope of a finite set of affine functions. Clearly, the augmented utility function defined by is strictly increasing in , continuous, concave and rationalizes .

Define by

| (5) |

where is a differentiable function satisfying , , for , and . (For example, .) Like , the function is strictly increasing in , continuous and concave and solves (because for all , and ). Furthermore, for every , is nonempty.999Choose a sequence such that tends to (which we allow to be infinity). It is impossible for because the piecewise linearity of in and the assumption that implies that . So the sequence is bounded, which in turn means that there is a subsequence of that converges to . By the continuity of , we obtain .

We end this section by noting that GARP imposes testable restriction distinct from GAPP. This is immediate from Example 1 and can be seen from Figure 1 which plots not just the observed consumption bundles but also the corresponding budget sets (derived from the observed prices and expenditures).

As we argued, GAPP does not hold in this example but, since the budget sets do not even cross, it is immediate to conclude that GARP does. We defer the description of the exact relation between the two criteria to Section 3.1.

From this point onwards, when we refer to ‘rationalization’ without additional qualifiers, we shall mean rationalization by an augmented utility function, that is, in the sense given by (2) rather than in the sense given by (3).

Up to now, we have motivated our model by showing that it is the utility representation of a basic axiom requiring consistent price comparisons. In the next two subsections, we provide direct motivation for the augmented utility function itself by arguing that it contains, as special cases, several distinct (standard and behavioral) preference-modeling approaches.

2.3. ‘Standard’ consumer theory and the augmented utility function

Perhaps the clearest motivation for our model is to think of it as a generalization of the quasilinear utility model, in which the consumer derives utility from the bundle and maximizes utility net of expenditure, that is, she chooses to maximize

| (6) |

where . There is a familiar textbook way of justifying this objective function by fitting it within the constrained optimization model of standard consumer theory. This is to think of the consumer as having a utility function defined over goods, with the last ‘outside’ good entering additively and linearly into the utility function, so that . Assuming that the consumer has a total wealth of , the utility of purchasing a bundle is then

Ignoring boundary issues, the consumer is effectively maximizing (6).

Even though the quasilinear model is widely used in partial equilibrium analysis, it is well known that the complete absence of income effects makes it unsuitable for certain empirical applications. For this reason, it is also common to remove the linear structure on while retaining the assumption that all outside consumption opportunities can be represented by a single outside good; this is true, for example, in the literature on modeling the demand for differentiated goods.101010For example, in Berry, Levinsohn, and Pakes (1995) and in Nevo (2000), is additively separable between the goods and the outside good; in the former, the utility of consuming units of the outside good is , for some , whereas in the latter it is (in other words, is quasilinear). In Bhattacharya (2015), is allowed to be a general function defined on goods. In models of differentiated goods, the consumption space is typically assumed to be discrete rather than , but the augmented utility model is still applicable in that context (see Section 4). In this case, the utility of purchasing a bundle is ; notice that, provided is fixed, we can think of the consumer as maximizing an augmented utility function: simply let .

Obviously, a consumer’s outside consumption opportunities would in reality involve more than one good, and the prices of those outside goods could change as well. Within the familiar constrained-optimal model of consumer theory, there are known conditions that justify the representation of those consumption opportunities by a representative good (with its corresponding price index). This is explained in detail in Section 3.5.

Finally, it is worth mentioning that the augmented utility function could also capture, as a special case, quasilinear utility maximization subject to certain constraints. One such example is consumption with a subsistence constraint, which we describe in more detail in the empirical application in Section 7.1. Loosely speaking, we can capture constraints on with an augmented utility that assigns very low values at that violate the constraint.

2.4. Behavioral preferences captured by the augmented-utility model

The central feature of the augmented utility model is that consumers experience disutility from expenditure. As we explained in the previous subsection, this disutility could be interpreted in a purely opportunity cost sense – more expenditure on the consumed goods imply less money available for other goods. In this understanding, the augmented utility function is a reduced form of a broader ’true’ utility function defined on all goods.

However, it is also reasonable to think of the augmented utility function in another way: that the consumer has – directly – a preference over bundles of the observed goods and their associated expenditure, which she has developed as a way of guiding her purchasing decisions. Thus it is the basic object of analysis and not the reduced form of something more fundamental. This understanding of choice behavior is exploited in the behavioral economics literature and the following quote from Prelec and Loewenstein (1998) is effectively a description of the augmented utility function:

each time a consumer engages in an episode of consumption, we assume she asks herself: “How much is this pleasure costing me?” The answer to this question is the imputed cost of consumption. This imputed cost is “real” in the sense that it actually detracts from consumption pleasure.

In this understanding, the disutility of expenditure is still related to opportunity cost, but the relationship is more flexible than what is permitted in a classical framework.111111Another paper that spells out remarkably clearly this approach to modelling consumer decisions is friedman2015, though the authors primarily have in mind the quasilinear utility model.

In the Introduction, we described one example of behavioral preferences (reference-dependent preferences) that could be captured by an augmented utility function. In the remainder of this section, we describe how our model relates to two other prominent themes in the behavioral literature.

Inattention to Prices and Expenditure

The public economics literature following Chetty, Looney, and Kroft (2009) has observed that consumers often misperceive prices: in their context, shoppers at grocery stores do not internalize the price effect of taxes. This literature is summarized in a recent survey by Gabaix (2019) who argues that many behavioral biases often take the form of inattention. Our model naturally captures a version of the inattention to prices discussed in Bordalo, Gennaioli, and Shleifer (2013) and Gabaix (2014). Here a consumer faced with a price perceives the expenditure associated with a bundle as , where is increasing in the true expenditure and could potentially depend on . With this misperception, and assuming that the consumer has a quasilinear preference, she then chooses to maximize

| (7) |

A special case of this model is where a consumer has a default price and misperceives the actual price to be where is the ‘attention parameter.’ The perceived expenditure is then . More generally, the model accommodates , where the attention parameter varies across bundles.121212This formulation of perceived expenditure is more general than Gabaix (2014) in that it allows the attention parameter to depend on but is less general in that the parameter does not vary across goods. This is a natural extension since, among other things, it allows a consumer to be more attentive to her actual expenditure if she is purchasing large bundles compared to small ones (so that tends to 1 when is large). Yet another possibility is that the consumer is not completely sensitive to every dollar increase in expenditure but pays more attention only when certain thresholds are crossed; this would correspond to the case where depends only on the expenditure and has the shape of a step function of expenditure.

Clearly, inattention as modeled by (7) is an instance where the agent has an augmented utility function, even though it will typically not be quasilinear (in actual expenditure).

It is also worth mentioning that using an augmented utility function (such as (7)) to capture price inattention is particularly apt because, as Gabaix (2014) notes, the numeraire serves as “the shock absorber that adjusts to the budget constraint.” The alternative is to model the consumer as having both price misperception over a given set of goods and a budget on those goods that must be satisfied, which inevitably leads to the added complication of modelling how the agent adjusts her intended demand when she realizes it violates (because prices are misperceived) the budget constraint at the true prices.131313Gabaix (2014) proposes one way to deal with this issue.

Budgeting and Mental Budgeting

As we discussed in Section 2.3, a common approach to partial equilibrium analysis is to add a numeraire as an additional good and assume that the agent has a (standard) utility function and budget set defined on the goods, with price and income information used to determine the level of the numeraire consumed. Of course such an approach could only work when income information is available and that is not always the case.141414Several widely used data sets, such as supermarket scanner panel data, that contain rich information on purchases, do not have accurate measures of income. Here, income information is typically the category (income ranges) that households self report when applying for loyalty cards (and so the information becomes out of date). Even when this information is available, it is strictly speaking not the right value to use as the global budget if the consumer can save and borrow to a significant degree (as acknowledged, for example, in Hausman and Newey (2016)). More generally, figuring out what really constitutes ‘the budget’ is not always straightforward, even in a classical setting.

Regularities highlighted by behavioral economists add a further wrinkle to the concept of a budget. It has been widely observed that households do not always treat money as fungible and instead create separate accounts for various categories of goods Thaler (1999). This is not only true for consumption decisions (see, for instance, Hastings and Shapiro (2013, 2018)) but also for savings decisions, which is why consumers often save more when they have access to commitment savings options (important theoretical and empirical contributions are Amador, Werning, and Angeletos (2006) and Feldman (2010), Dupas and Robinson (2013) respectively).

Now consider a researcher who is trying to model the demand for a set of goods which form a subset of all the goods consumed by an agent. If mental accounting effects are important, the researcher will have to allow for the fact that he cannot observe how goods are categorized by the agent, nor does he know what really constitutes the mental budget from which the agent is drawing her expenditure (on the observed goods and their perceived alternatives). In this situation, the augmented utility framework provides a natural way to model the demand for those goods: it is consistent with constrained utility maximization incorporating an outside good (see Section 2.3) but does not require the researcher to take a stand on the (unobserved, mental) budget from which the agent is drawing her expenditure.151515Here we are assuming that the data are collected over a period where the mental budget for the observed goods and their alternatives is stable. Changing mental budgets would manifest itself as violations of GAPP (see Example 3).

3. Properties of the augmented utility model

In this section, we explore various aspects of the augmented utility model, beginning with a discussion of the relationship between GAPP and GARP. We then go on to discuss welfare analysis in the augmented utility framework. Since one would not expect data sets to be completely consistent with the augmented utility model, we discuss how departures from GAPP could be measured. Lastly, we discuss how prices could be deflated in this model to account for general changes in the price level.

3.1. Comparing GAPP and GARP

Recall that Example 1 in Section 2 is an example of a data set that obeys GARP but fails GAPP. We now present an example of a data set that satisfies GAPP but fails GARP.

Example 2.

Consider the data set consisting of the following two choices:

These choices, as shown in Figure 2, violate GARP as () and (). However, these choices satisfy GAPP as () but ().

While GAPP and GARP are not in general the same conditions, they coincide in any data set where for all . This is because if and only if since both conditions are equivalent to . Given a data set , we define the iso-expenditure version of as another data set , such that . This new data set has the feature that for all . Notice that the revealed price preference relations , remain unchanged when consumption bundles are scaled. Thus a data set obeys GAPP if and only if its iso-expenditure version obeys GAPP, which in this case is equivalent to GARP.161616There is an analogous ‘GARP-version’ of Proposition 1 and that this observation (or some close variation of it) has been exploited before in the literature (see, for example, Sakai (1977)). Suppose obeys GARP. Then GARP holds even if each observed price vector is arbitrarily scaled. In particular, obeys GARP if and only if , where , obeys GARP (equivalently, GAPP) since for all . The latter perspective is useful because it highlights the possibility of applying Afriat’s Theorem on , in the space of prices (in other words, with the roles of prices and bundles reversed). This immediately gives us a different, ‘dual’ rationalization of in terms of indirect utility, that is, there is a continuous, strictly decreasing, and convex function such that . For an application of this observation, see Brown and Shannon (2000). The next proposition gives a more detailed statement of these observations.

Proposition 1

Let be a data set and let , where . Then the revealed preference relations and on and the revealed preference relations and on are related in the following manner:

-

(1)

if and only if .

-

(2)

if and only if .

As a consequence, obeys GAPP if and only if its iso-expenditure version, , obeys GARP.

Proof. Notice that

The left side of the equivalence says that while the right side says that . This implies (1) since and are the transitive closures of and respectively. Similarly, it follows from

that if and only if , which leads to (2). The claims (1) and (2) together guarantee that there is a sequence of observations in that lead to a GAPP violation if and only if the analogous sequence in lead to a GARP violation.

As an illustration, compare the data sets in Figure 1 and Figure 2 to the iso-expenditure data sets in Figure 3a and Figure 3b. It can be clearly observed that the iso-expenditure data in Figure 3a contains a GARP violation (which implies it does not satisfy GAPP) whereas the data in Figure 3b does not violate GARP (and, hence, satisfies GAPP).

A consequence of Proposition 1 is that the augmented utility model can be tested in two ways: we can either test GAPP directly or we can test GARP on its iso-expenditure version. If we are simply interested in testing GAPP on a single-agent data set , normalization brings no advantage: the test is computationally straightforward in either case and involves the construction of their (respective) revealed preference relations and checking for acyclicity. However, as we shall see in Section 5, iso-expenditure scaling plays an important role in the test we develop (on repeated cross-sectional demand data) for the random utility version of the augmented utility model.

While GARP and GAPP are distinct properties, they are not mutually exclusive and it is possible for a data set to satisfy both. For example, if is collected from a consumer who is maximizing a quasilinear augmented utility function, then it will satisfy both GAPP and GARP.171717When has the form (6), maximizes only if maximizes in . Thus must also obey GARP. A broader class of augmented utility functions that satisfy both GAPP and GARP is given in Section A.1.2. When both properties are satisfied, then an analyst could make use of either property when making predictions of demand at an out-of-sample price; the two properties will then typically lead to different set predictions. We discuss this in greater detail in Section A.1 of the online appendix, which also contains more discussion of the relationship between revealed preferences under GAPP and under GARP.

In light of Proposition 1 and the fact that the revealed price preference relation is not affected by scaling consumption bundles, it is natural to wonder about the relationship between the testable implications of the augmented-utility model and the constrained-optimization model (as in (3)) restricted to homothetic preferences. A data set that can be rationalized in the latter sense181818For the precise characterization, see Varian (1983). will have the feature that it must satisfy GARP for any arbitrary scaling of consumption bundles and thus will satisfy GAPP. By contrast, a data set that satisfies GAPP must only satisfy GARP for the particular scaling that equalizes expenditure across observations. In other words, GAPP is a less stringent property; that it is strictly less stringent is clear from Example 2, which satisfies GAPP but violates GARP and therefore cannot be rationalized in Afriat’s sense (as given by (3)) for any locally nonsatiated preference, let alone a homothetic preference.191919Example A.5 in the online appendix contrasts demand predictions using the augmented utility model and the constrained-optimization model (both with and without imposing homotheticity on the preference).

3.2. Preference over Prices

We know from Theorem 1 that if obeys GAPP then it can be rationalized by an augmented utility function with an indirect utility that is defined at all price vectors in . It is straightforward to check that any indirect utility function as defined by (1) has the following two properties:

-

(a)

it is nonincreasing in , in the sense that if (element by element) then , and

-

(b)

it is quasiconvex in , in the sense that if , then for any .

Any rationalizable data set could potentially be rationalized by many augmented utility functions, with each one leading to a different indirect utility function. We denote this set of indirect utility functions by . We have already observed that if then for any ; in other words, the conclusion that the consumer prefers the prices to is nonparametric in the sense that it is independent of the precise augmented utility function used to rationalize . The next result (proved in Appendix A.2) says that, without further information on the augmented utility function, this is all the information on the consumer’s preference over prices in that we can glean from the data. Thus, in our nonparametric setting, the revealed price preference relation contains the most detailed information for welfare comparisons.

Proposition 2

Suppose is rationalizable by an augmented utility function. Then for any , in :

-

(1)

if and only if for all .

-

(2)

if and only if for all .

3.3. Compensation for a price change

In standard consumer theory, the compensating and equivalent variations are two ways of quantifying the welfare impact of a price change (see Mas-Colell, Whinston, and Green (1995), Chapter 3.I). We now argue that analogues exist for the augmented utility model and that bounds for them can be recovered from the data.

Let be the consumer’s augmented utility function. Suppose that the initial price is and it changes to , leading to a change in consumption from to . Then we can find such that

| (8) |

Note that is unique since is strictly increasing in the last argument. We could think of as the lump sum transferred from the consumer (if it is positive) or to the consumer (if it is negative) after the price change that will make her just indifferent between the situation before and after the change.

Suppose we interpret as arising from an overall utility function (that depends on the observed goods and the level of an outside good), given the consumer’s wealth of , so that . Since solves (8), it will also satisfy

In other words, is the reduction in total wealth that will leave the consumer’s overall utility at the same as it was at . Thus, with this particular interpretation of the augmented utility function, coincides with what is called the compensating variation in standard consumer theory. For this reason, we shall also refer to , defined by (8), as the compensating variation.

Pushing the analogy further, it is possible to use the compensating variation in our model in the same way it is typically used. For example, the price change from to may benefit some consumers while hurting others. The Kaldor criterion would deem this change an overall improvement if the sum of the compensating variations across all consumers is positive since it guarantees that those who benefit from the price change could, in principle, compensate the losers and still be better off.

In a similar way, we can define the equivalent variation as the value that solves

| (9) |

If then also solves

In other words, coincides with the equivalent variation as it is usually defined.

Now suppose a data set obeys GAPP and contains the observation . What can we say about the compensating variation of a price change from to (where the latter may or may not be a price observed in )? There will typically be a range of these values since there is more than one augmented utility function that rationalizes . Nonetheless, it is possible to obtain a tight lower bound for the set of possible compensating variation values. Formally, this is given by

Abusing terminology somewhat, we shall denote this term simply by .

We now describe how to compute this bound.202020We leave the reader to carry out the analogous exercise for the equivalent variation. Let be the set of observations such that if . This set is nonempty since it contains itself. For each , there is such that

| (10) |

We claim that for any that rationalizes , the compensating variation . This is because if , then for any utility function rationalizing . Indeed,

Thus for all . In fact, it is possible to obtain a stronger conclusion:

| (11) |

Since the right side of this equation can be easily computed from the data, we have found a practical way of calculating .

Notice that if is revealed preferred to (equivalently, that there is such that ),212121Recall that makes sense even if is not observed in the data set; see footnote 7. then ; in other words, at , a lump sum tax of will leave the agent no worse off than at and potentially better off. On the other hand, if is not revealed preferred to , that is, for every , we have , then ; in other words, at , a lump sum transfer of to the agent will leave the agent no worse off than at and potentially better off.

We provide a fuller discussion on the compensating variation, including a proof of (11), in Appendix A.5.

3.4. Measuring departures from rationality

Empirical studies that apply Afriat’s Theorem frequently find GARP violations. A common way of measuring the extent of such violations is to compute the critical cost efficiency index Afriat (1973). This refers to the largest such that can be rationalized in the following sense: there is a locally-nonsatiated utility function such that for all in the ‘shrunken’ budget set . Rationality is imperfect if since the consumer behaves as though she ignores bundles that satisfy and, there could be some observation and bundle in this range for which . Importantly, the calculation of the critical cost efficiency index is straightforward and is facilitated by a modified version of GARP.

There is a similar way of measuring the extent to which a data set fails to be rationalized by an augmented utility function. For a given , there is a weaker version of the GAPP test that allows us to determine whether there is an expenditure-augmented utility such that, at each observation ,

If there is, we say that is -rationalized by an augmented utility function. Notice that if can be -rationalized then it can be -rationalized for any , since is strictly decreasing in expenditure. The consumer who is -rational (for ) may have only limited or bounded rationality in the sense that there could be a bundle and an observation such that

In other words, the consumer fails to recognize that bundle is superior to at because she has inflated (by ) the expenditure of purchasing . Any data set can be -rationalized for some and the supremum over these values provides a natural measure of rationality which we shall refer to as the rationality index.

The following proposition establishes a connection of our rationality index with the critical cost efficiency index.

Proposition 3

Let be a data set and let , where , be its iso-expenditure version. Then is the rationality index for if and only if it is the critical cost efficiency index for .

A consequence of this result is that the rationality index inherits the ease of computation of the critical cost efficiency index. In Appendix A.4.2, we provide instructions on this computation including in more general environments with nonlinear prices. The proof of Proposition 3 can be found in Appendix A.4.3.

3.5. Deflating prices

When the data set is collected over an extended period, it is possible that there are changes in the prices of all goods, including goods outside the ones observed. Thus the nominal value of expenditure may no longer be an accurate measure of the opportunity cost of expenditure. A simple way of taking this into account is to deflate the prices of the goods with a general price index. In other words, one could check if obeys GAPP, where is an index of the general price level. If it does, it would mean that there is an augmented utility function that rationalizes the data after deflation; in other words,

This simple way of accounting for general price changes could be precisely justified when the augmented utility function is the reduced form of a larger constrained optimization problem. Indeed, suppose that the consumer is maximizing an overall utility that depends both on the observed bundle and on a bundle of other goods, subject to a global budget of . Formally, the consumer maximizes subject to , where are the prices of goods . Keeping and fixed, is defined as the greatest overall utility the consumer can achieve by choosing optimally, subject to expenditure and conditional on consuming , that is,

| (12) |

At the prices for the observed goods and for the outside goods, the consumer chooses a bundle to maximize subject to . Then will obey GAPP, since maximizes , with as defined by (12).

Now suppose that the prices of the other goods are changing. Consider the simplest case where these prices move up or down proportionately, so they are at observation , for some scalar . Furthermore, assume that the agent’s global budget at also increases by a factor , which means that the consumer’s nominal wealth is keeping pace with price inflation. Then at observation , the consumer maximizes subject to obeying

Dividing this inequality by , we see that the consumer’s choice is identical to the case where the price of the observed goods is , with external prices and total wealth constant at and respectively. Therefore, the data set with deflated prices, obeys GAPP.

In the case where the relative prices of the outside goods change, it is still possible to derive a price index which ensures that GAPP holds after deflating , but this requires stronger assumptions on . We discuss this in detail in Appendix A.3.

4. General consumption spaces and nonlinear pricing

So far we have assumed that the consumption space is and that prices are linear, but in fact neither feature is crucial to our main result. In this section, we assume that the space from which the consumer chooses her consumption is . We define a price system as a map , where is the cost of purchasing . Of course, a special case of a price system is but the more general formulation with allows for quantity discounts, bundle pricing and other pricing features that can be important in certain contexts (such as our empirical application in Section 7.1).

We assume that both the price system and the bundle chosen by the consumer are observed. Formally, a data set is a collection . This data set is rationalized by an augmented utility function if

| (13) |

The notion of revealed preference over prices can be extended to a revealed preference over price systems. We say that is directly revealed preferred (directly revealed strictly preferred) to if ; we denote this by . We denote the transitive closure of by , that is, if there are , in such that , , and ; in this case we say that is revealed preferred to . If anywhere along this sequence, it is possible to replace with then we denote that relation by and say that is strictly revealed preferred to . It is straightforward to check that if, can be rationalized by an augmented utility function, then it obeys the following generalization of GAPP to price systems:

there do not exist observations such that and .

The following theorem asserts that the converse is also true and that, under further conditions, we can guarantee that the data can be rationalized by an augmented utility function with additional properties. The proof of this result (in fact of a more general result allowing for errors) is in Appendix A.4.1.

Theorem 2

A data set can be rationalized by an augmented utility function if and only if satisfies GAPP.

Furthermore, suppose that satisfies GAPP, is closed and that, for all , the price systems have the following properties: (i) is a continuous function; (ii) for any number , is a compact set; and (iii) is strictly increasing in for some .222222This means that if , , , for all , and for all , then . Then, for any closed set containing , there is a continuous augmented utility function that rationalizes , with strictly increasing in .

Remarks: (1) Note that condition (ii) is a weak assumption requiring that there be no arbitrarily large bundles with a bounded price. (2) By definition, an augmented utility function is strictly decreasing in expenditure, but in certain cases it may be natural to require to be strictly increasing in for some set (which can be empty). The theorem says that this is possible, so long as the price systems are also strictly increasing in . (3) Lastly, the theorem guarantees that the domain of the augmented utility function can be larger than . For reasons which will be clear later in this section, this is natural in certain applications. However when we say that rationalizes the data, we mean that (13) holds and, in particular, need not be optimal in .

The literature on mental accounting has emphasized the possibility of actors in the economy manipulating the mental budgets of agents. The following example shows how a nonlinear GAPP test can be used to detect such phenomena.

Example 3.

A store initially prices two goods at and a shopper purchases from the store. The store introduces a scheme where regular customers (such as this shopper) receives a voucher of 12 dollars to be used for the purchase of the store’s products; prices are changed to and the shopper buys .232323If good 1 is cheap to procure, this scheme is advantageous to the store, since in the first instance, the shopper spends 50 dollars while in the second, she spends 58 (net of the voucher). What is the impact of the gift voucher?

Since the value of the voucher is small in terms of total income, the shopper could spread this reward widely across all purchases (including purchases from other stores) and this should result in no (or at least a very small) impact on demand for the store’s products. On the other hand, she may have a mental budget for purchases at that store, and the voucher represents an appreciable increase in that mental budget by 12 dollars.

A revealed preference analysis supports the latter hypothesis. Indeed, if we ignore the voucher, the data are not compatible with the maximization of an augmented utility function since and , which violates GAPP. On the other hand, at observation , we could model the shopper as mentally discounting 12 dollars from her expenditure at the shop. In formal terms, the price system at is a function , so . In this case, we have (where ), but it is no longer the case that since . So the data is now compatible with GAPP, but with a nonlinear pricing system based on the shopper’s mental accounting.242424Notice (in connection with our discussion of mental accounting in Section 2.4) that the total mental budget of the shopper remains unknown, though the researcher observes an event that has altered that budget.

4.1. Discrete consumption spaces

Below are four instances where Theorem 2 could be applied.

(1) Suppose that the consumption space consists of goods of which the first can only be consumed in discrete quantities (as in the model of Polisson and Quah (2013), for example). The consumption space is then , where is the set of natural numbers. Theorem 2 is applicable whether or not prices are linear. Suppose that each good has a price . Since is closed and the price system is strictly increasing in , Theorem 2 guarantees that, if GAPP holds, then there is a continuous augmented utility function that is strictly increasing in and rationalizes .

(2) Another natural choice environment is one where the consumer is deciding on buying a subset of objects from a set with items. Then each subset could be represented as an element of . For , the entry equals 1 if and only if the object is chosen. If only certain subsets are permissible, as in the case of discrete choice, then would be a strict subset of . The price system gives the price of different bundles of goods. Let denote the vector with 1 in the entry and zero everywhere else. Then is the price of purchasing good alone. The price system is nonlinear if for some .

(3) In empirical models of demand for differentiated goods, it is common to model each good as embodying a set of characteristics (see Nevo (2000)). For example, if each good is a type of breakfast cereal, then the characteristics could be the calories, fiber content etc. Suppose that there are characteristics and let be the set of values that characteristic can take. Then, the characteristics space is .252525If characteristic naturally takes on continuous values (such as calories) then we let . Characteristic 2 could be the brand. Suppose there are two brands, then , and so on. There are goods, with good having characteristics . Assuming (as is common in these models) that a consumer purchases only one good, the consumption space is and a price system is just a list of prices for the different goods.

In this context, it is natural to model the consumer with an augmented utility function defined on characteristics and expenditures , even though the products available to her are only those in . Furthermore, among the characteristics, there could be those where higher values are unambiguously better, in which case the researcher could be interested in guaranteeing that utility is strictly increasing in those characteristics. Theorem 2 allows for these considerations. If obeys GAPP then it can be rationalized by a continuous augmented utility function . Additionally, for a set of characteristics , one could guarantee that is strictly increasing in so long as is strictly increasing in , for all .

In models of differentiated goods, it is also common to allow for the introduction of new goods and for changes to a product’s characteristics.262626These changes could be substantive (for example, a change to a breakfast cereal formula) or it could be a change in advertising expenditure that serves as a proxy for a change in a product’s public profile. Obviously, changes to a product’s characteristics could potentially lead to a change in the product’s utility which, unless taken into account by the test, could lead to a spurious rejection of augmented utility-maximization. In formal terms, these changes can be captured by allowing the set of alternatives to depend on ; in Section A.4.4, we explain how it is possible to modify the GAPP test in Theorem 2 to account for changes of this type.

4.2. Characteristics models with continuous consumption spaces

We assume that the space of characteristics is , with each product represented by a vector of characteristics . We allow these goods to be bought in bundles, so the consumption space is the convex cone generated by .272727For a GARP-based test of a model of this type, see Blow, Browning, and Crawford (2008). We assume that the vectors are linearly independent; this guarantees that for each , there is a unique bundle of goods, such that . We denote by . Let be the prices of the goods at observation . To obtain the bundle , the consumer needs to spend .

At observation , the researcher observes and the consumer’s purchases . We assume the researcher knows and so he can work out the consumption in characteristics space, , as well as the price system . Theorem 2 guarantees that if satisfies GAPP then it can be rationalized by a continuous augmented utility function . So long as is strictly increasing in for each , we can also ensure that is increasing in the characteristics .

5. The Random Augmented Utility Model

In this section, we develop the random version of the expenditure-augmented utility model. We first describe our test procedure for this model via a simple example.

5.1. An Illustrative Example

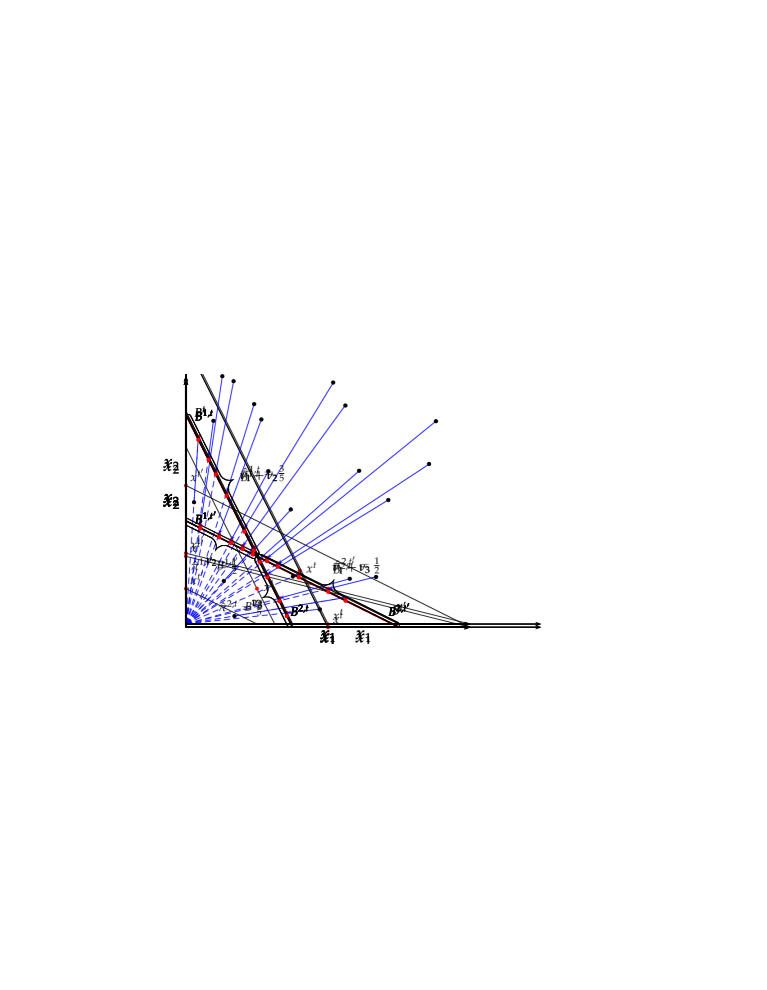

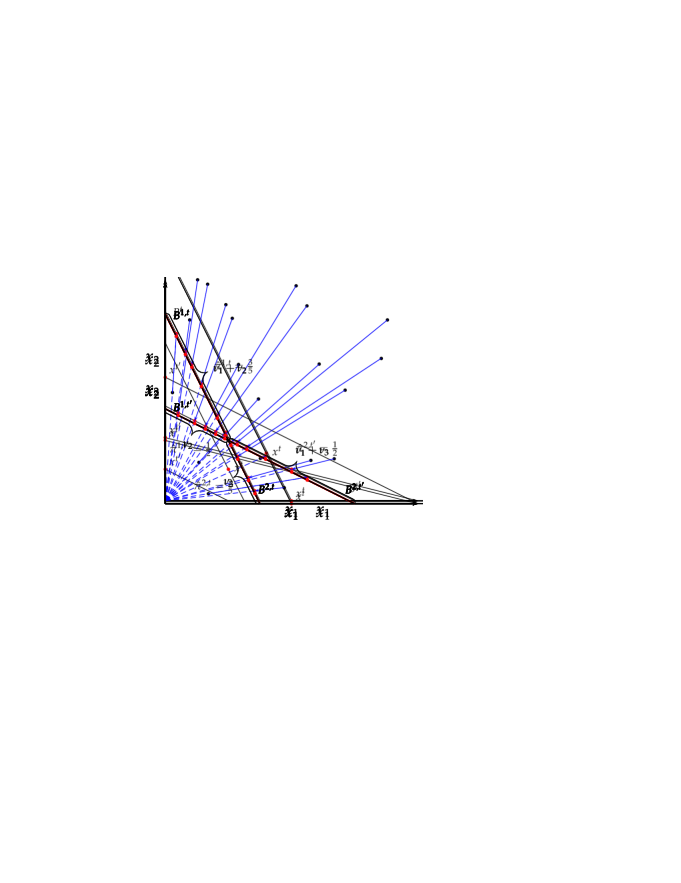

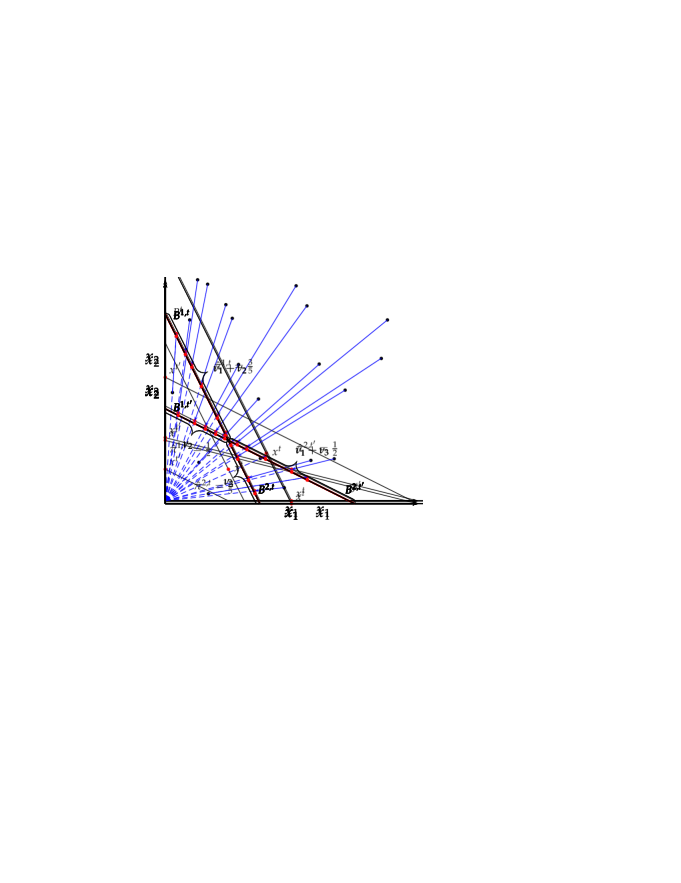

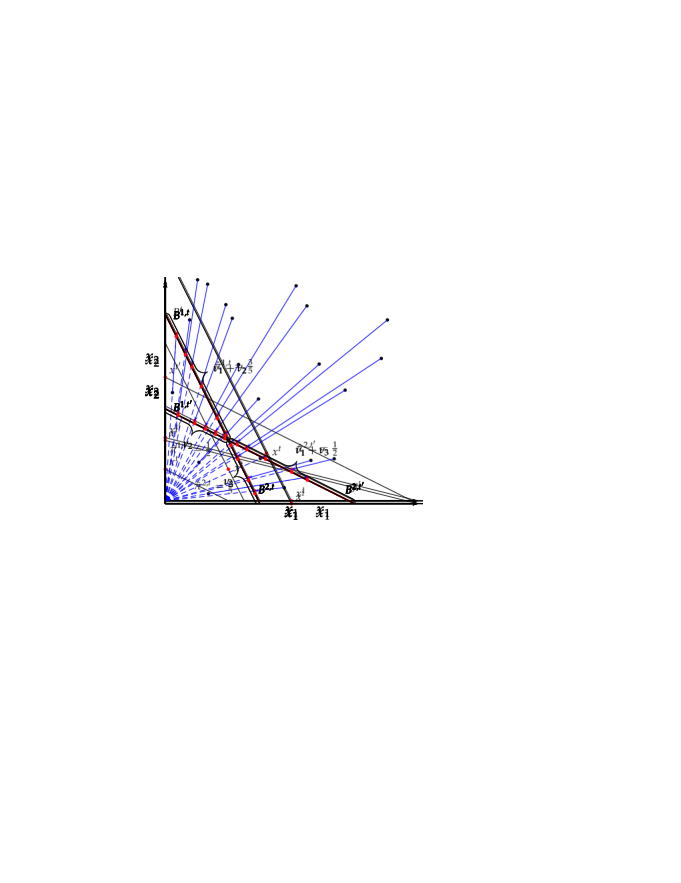

Example 4.

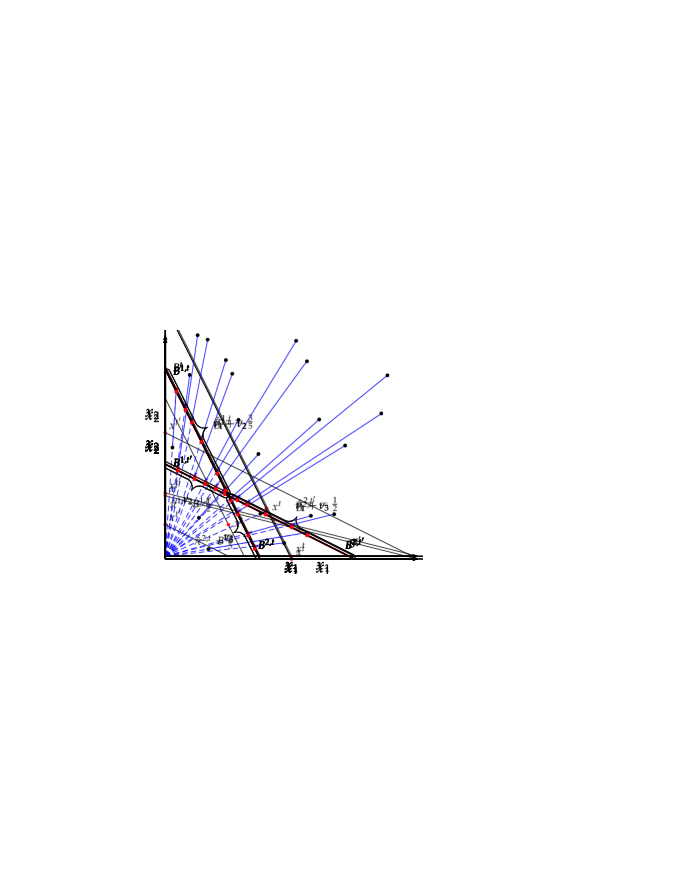

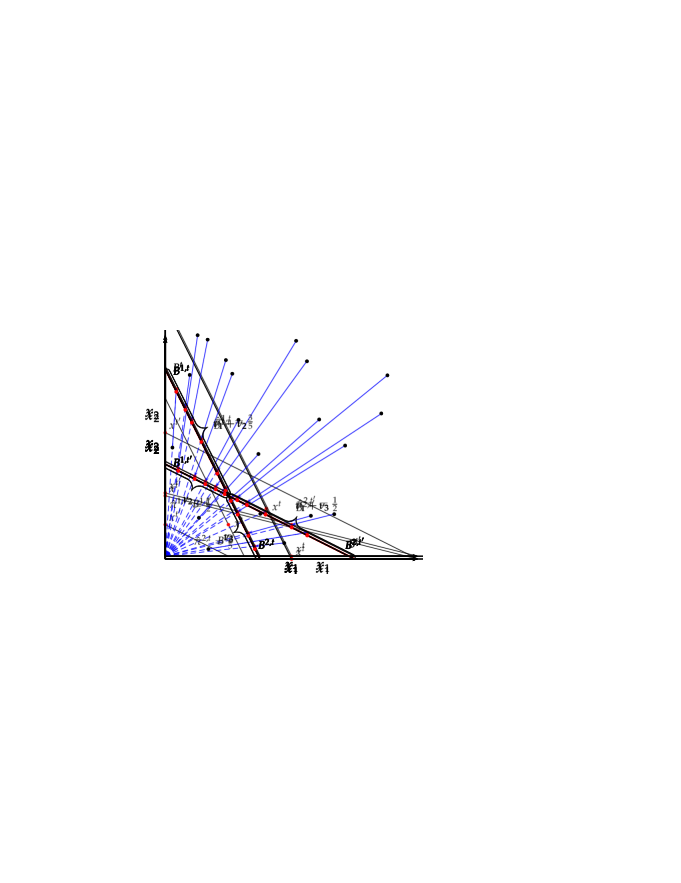

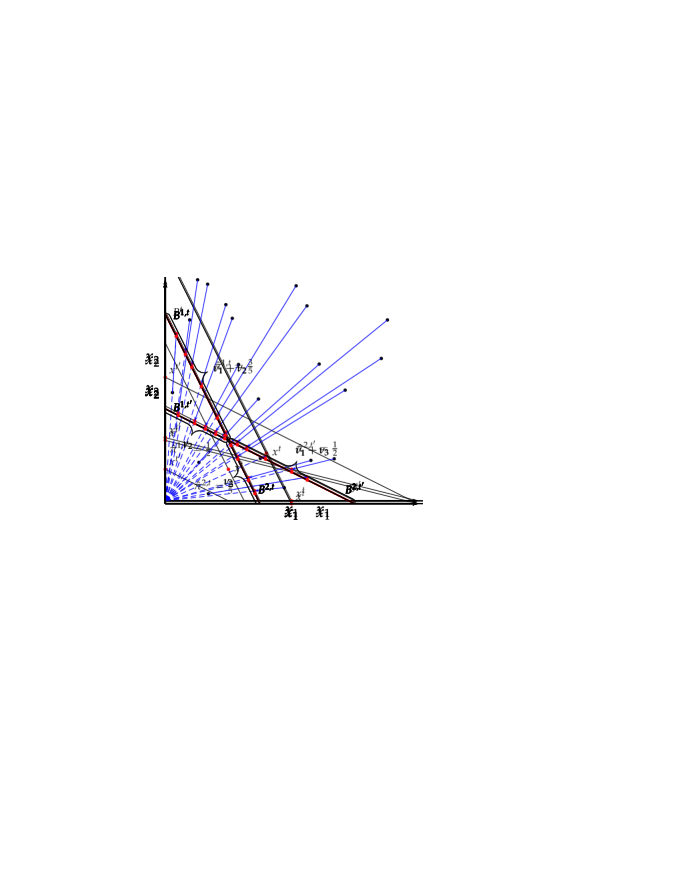

Suppose we have repeated cross-sectional data consisting of the demand of a population of ten consumers at two price vectors. This is illustrated in Figure 4 where the collection of points in the left and right panels indicate the demand bundles at and respectively. The lines in Figure 4 indicate relative prices.

Since we assume this is a cross-sectional data set, the econometrician cannot match consumption bundles across the two panels by consumer identity. The question we wish to address is whether this data set can be rationalized, by which we mean the following.

Can we match the choices at with those at , forming ten distinct pairs, such that each pair can be rationalized by an augmented utility function (or, equivalently, satisfies GAPP)?

This exercise illustrates the problem we address in this section: given the empirical demand distributions in different periods, is there a time-invariant distribution over consumer types that could explain these empirical distributions, subject to the restriction that each type is an augmented utility function maximizer.

An obvious way of answering the above question would be to consider all possible partitions into pairs and test GAPP on each pair.282828Note that when we formally define our test in the next subsection, the choice distribution will be assumed to be atomless. The simple finite matching analogy in this section, while inexact, is meant to provide the intuition our methodology. This approach, however, is not practical when the population at each observation is large and when there are more than two periods. Fortunately, there is a different procedure that works in general, which we now explain.

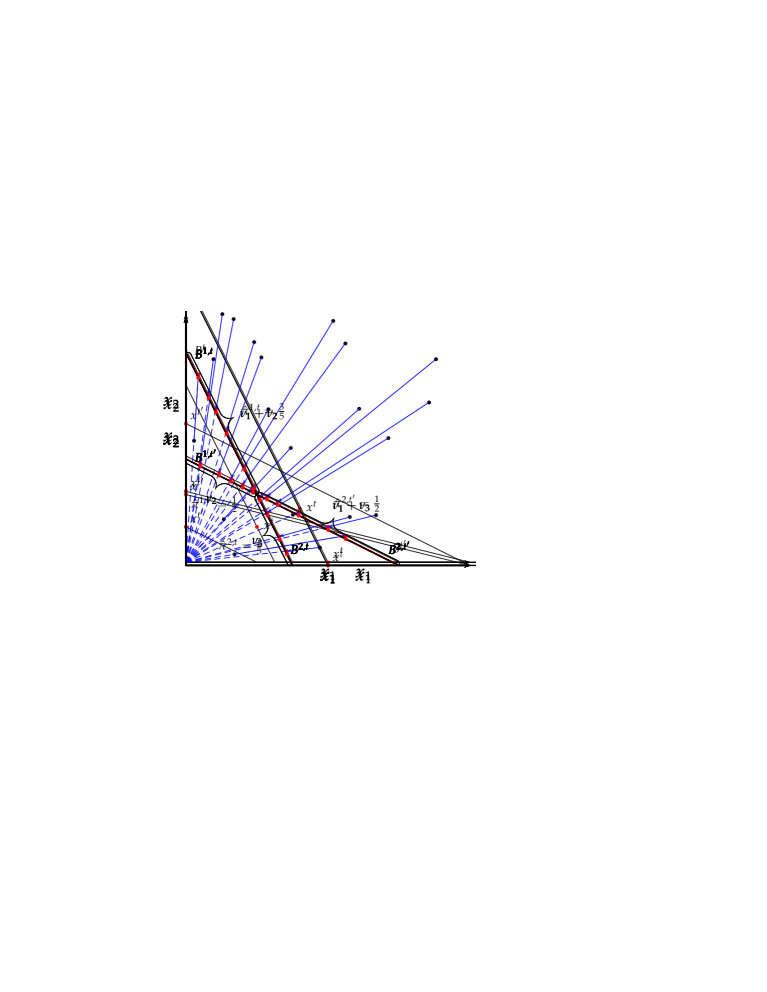

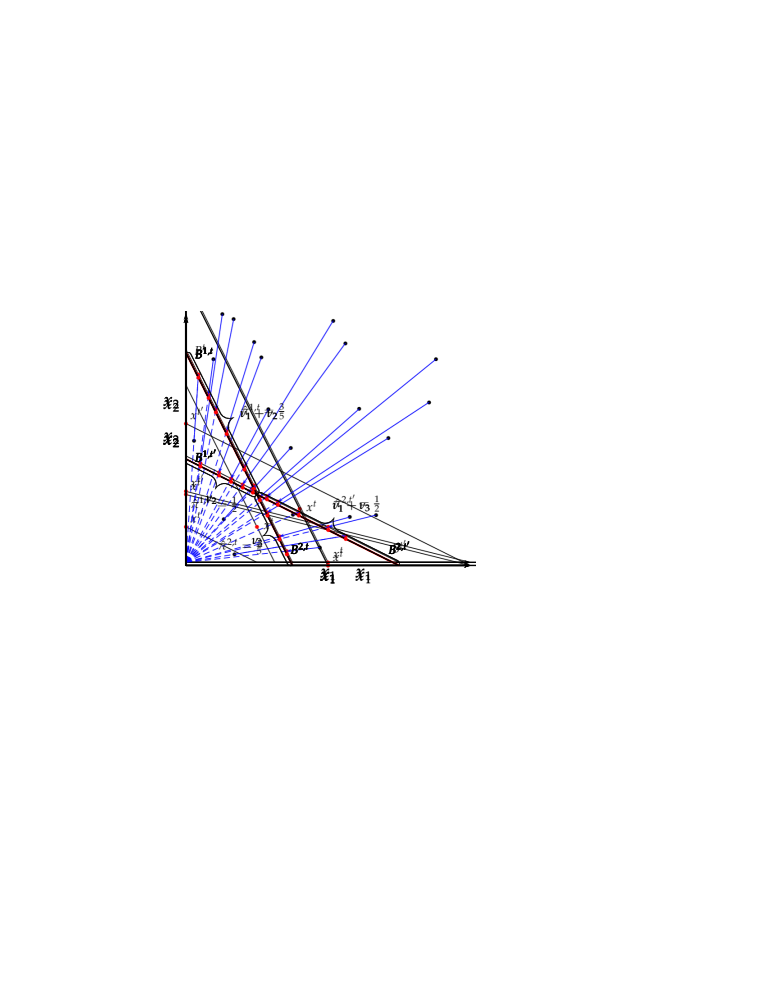

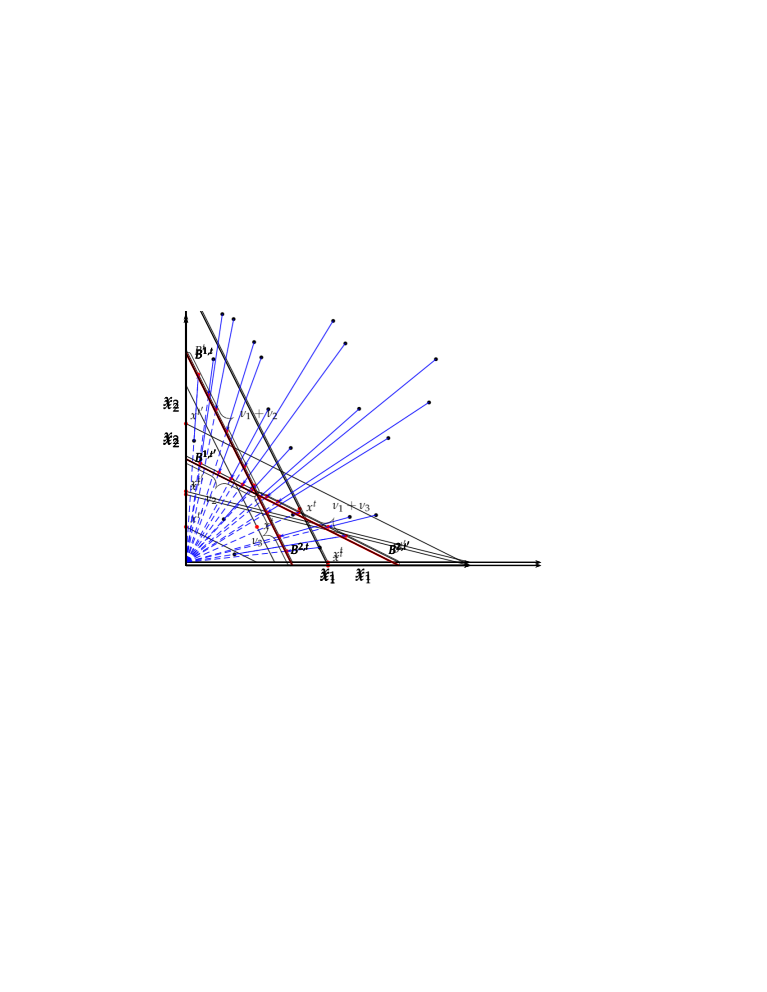

Proposition 3 tells us that a pair created by choosing bundle from observation and from observation obeys GAPP if and only if its iso-expenditure analog, obeys GARP, where and are scaled versions of and that satisfy . This scaling is demonstrated in Figures 5a and 5b. Figure 5c shows the scaled bundles from both observations superimposed onto a single picture. This figure also labels different partitions of the budget lines and we use this notation in what follows.

Now recall that, if satisfies GARP, then it is not possible for to lie on and for to lie on (see Figure 5(c)). Instead must belong to one of the following three types: lies on and lies on ; lies on and lies on ; or lies on and lies on . These cases are graphically depicted in Figure 6a, Figure 6b and Figure 6c respectively.

Denoting the fraction of each of these GAPP-consistent consumer types in the population by , and respectively, together they must generate the observed proportion of choices on the segments and . Figure 7a demonstrates the proportion of choices in terms of the s, while Figure 7b displays the empirical proportion of choices on each segment (after scaling), which we denote by

| (14) |

(For instance, because six of the ten rescaled demand bundles lie on .) Therefore, a necessary condition for rationalizing the data is that there are s that solve

| (15) |

Two observations should be immediate from this process. The first is that there could be data where the system (15) has no solution; this occurs when . The second is that when the values of are given by (14), the solution to (15) is

| (16) |

To confirm that the data in this example can indeed be rationalized, it remains for us to pair up the demand bundles at the two observations. To do this, arbitrarily choose pair of choices that lie on and ; any 5 () pairs that lie on and ; and the remaining 4 () pairs on and . Clearly each pair satisfies GARP and thus the original (un-scaled) pair satisfies GAPP.

5.2. Rationalization by Random Augmented Utility

The starting point of our analysis is a repeated cross-sectional data set, , where each observation consists of the prevailing price and the distribution of demand in the population at that price, represented by a probability measure on . An example of is the data set depicted in Figure 4 where the probability measure corresponds to the empirical distribution of demand bundles. The following definition generalizes the notion of rationalization considered in that example.

Definition 5.1.

The repeated cross-sectional data set is rationalized by the random augmented utility model (RAUM) if there exists a probability space and a random variable such that, almost surely, can be rationalized by an augmented utility function (equivalently, obeys GAPP) and

| (17) |

In this definition, one could interpret as the population of consumers and as the demand of consumer type at observation (when the prevailing price is ); all consumer types in the support of are required to be consistent with the augmented utility model and the observed distribution of demand at each observation , given by , must coincide with that induced by the distribution over consumer types. Alternatively, the model can also be interpreted as one where each individual’s augmented utility changes over time but in such a way that the population distribution is stationary.

In Example 4, the repeated cross-sectional data set has two observations, where the probability distributions are simply uniform distributions on finite support. A RAUM-rationalization involves matching observations in with those in , so that each pair obeys GAPP. In the general case with observations, the function solves a -fold matching problem, where each group (along with the associated prices) satisfies GAPP and agrees with the observations (that is, (17) is satisfied).292929It is straightforward to check that, with two observations, finding a rationalization is equivalent to finding a zero-cost solution to the transportation problem (see Galichon and Henry (2011)) where the cost of a pair of bundles is 0 if it obeys GAPP and 1 otherwise.

We shall now explain the general procedure for deciding if a given repeated cross-sectional data set can be RAUM-rationalized. This procedure mimics our solution to Example 4. For ease of exposition, we impose the following assumption on the data.

Assumption 1.

Let be the budget plane at prices and expenditure 1. For all with ,

This assumption states that the probability of a bundle lying, after re-scaling, at the intersection of two budget planes is zero. The assumption is not required for any of our results but it is convenient because it simplifies the exposition.303030If we allow for mass at budget intersections, then we would have to include them in our definition of patches. This is notationally cumbersome but once included our arguments (and Theorem 3) remain correct. It is always satisfied if is absolutely continuous with respect to the Lebesgue measure and is unlikely to be violated in any application with a continuous consumption space and linear prices.

Let denote the collection of subsets, or patches, of where each subset has as its boundaries the intersection of with other budget sets and/or the boundary planes of the positive orthant. These are the higher-dimensional and multi-period analogs to the line segments in Figure 5c. Formally, for all and , each set in is closed and convex and satisfies the following conditions:

-

(i)

,

-

(ii)

for all that satisfy (where denotes the relative interior of ),

-

(iii)

implies that for some that satisfies .

For the patch , we let

| (18) |

In words, is the probability that a bundle lies in after re-scaling. Note that, even though there may be , for which is nonempty, Assumption 1 guarantees that . We denote by the vector and by the column vector . We refer to as the vector of observed patch probabilities.

Consider a single-agent data set of the form . Given , we can define its iso-expenditure version, which is , where (so for all ). Suppose that does not lie on the intersection of budget planes, that is, there is such that . We make two important observations. First, Proposition 1 tells us that satisfies GAPP if and only if satisfies GARP. Second, if satisfies GAPP then so does if has the property that its re-scaled version satisfies ; this is because the revealed preference relations (over the bundles ) are determined only by where lies on the budget set relative to its intersection with another budget.

It follows from these observations that we may classify all single-agent data sets that obey GAPP according to the patch occupied by the scaled bundle at each . In formal terms, each that obeys GAPP is associated with an iso-expenditure that obeys GARP, which is in turn associated with a vector where

| (19) |

Thus, for the observed prices, we have partitioned the collection of all deterministic data sets obeying GAPP (of which there could be infinitely many) into a finite number of distinct classes or types, based on its associated vector . We denote this set of vectors by . We use to denote the matrix whose columns consist of every , arranged in an arbitrary order; we refer to as the matrix of GARP-consistent types.

In Example 4, all the deterministic data sets that obey GAPP must correspond to one of three types (as depicted in Figure 6) and

| (20) |

(Each column in describes the types in Figure 6: from left to right the columns capture the types in Figures 6a, 6b and 6c respectively.)

Given a repeated cross-sectional data set , we can construct and the matrix of GARP-consistent types . Suppose that this data set can be rationalized by some distribution . Let denote the mass of consumers of type in the population, that is

At a given observation , let ; this is the subset of GARP-consistent types that have their re-scaled demands in the patch at observation . The proportion of the population whose types belong to is

Since is rationalized by , setting in (17), we obtain

| (21) |

where is defined by (18). In other words, the observed probability of choices that land on after scaling must equal to the mass of GARP-consistent types implied by . This condition must hold for all patches , so (21) can be more succinctly written as , where is the column vector . (Recall that is the vector of observed patch probabilities.) In Example 4, is given by (20), is given by (14) and the solution by (16).

To recap, given a data set , we calculate the matrix of GARP-consistent types and the vector of patch probabilities . A necessary condition for to be rationalized by RAUM is that there is that solves . It turns out that this condition is also sufficient: if exists, then we can find a RAUM-rationalization of where the proportion of the population with type is precisely . The details of this final step are in the Appendix A.6. The next result summarizes this discussion.

Theorem 3

Let be a repeated cross-sectional data set obeying Assumption 1. Then can be RAUM-rationalized if and only if there exists a such that .

We end this section by contrasting the RAUM test with that of the classic random utility model (or RUM for short). The typical data environment for the latter is one where each observation consists of a distribution of choices on a given constraint set (which varies across observations). In that environment, McFadden and Richter (1991) and McFadden (2005) observe that the problem of testing RUM can be discretized. KS operationalize this insight in the case where constraint sets are linear budget sets. In that context, requiring choices from the same constraint set simply means that is iso-expenditure, in the sense that if is in the support of then . KS demonstrates that an iso-expenditure data set can be RUM-rationalized if and only if for some (where is the matrix of GARP-consistent types and is the vector of patch probabilities).

Notice that Theorem 3 recovers the result of KS as a corollary. RAUM-rationalization guarantees the existence of a distribution over types that is consistent with the observations (that is, (17) holds), with satisfying GAPP almost surely. With the iso-expenditure condition, GAPP and GARP are equivalent properties, which means (by Afriat’s Theorem) that there is is a strictly increasing utility function with for all ; this is precisely what is needed for a RUM-rationalization. Of course, it is also clear from our proof of Theorem 3 that we are building on KS, since our proof strategy involves (in effect) the following three steps: (i) converting into an iso-expenditure data set (obtained from simply by scaling demands); (ii) noticing that can be RAUM-rationalized if and only if can be RUM-rationalized; and (iii) then relying on the characterization of RUM-rationalization in KS.

Since a population of heterogenous consumers typically do not have identical expenditures, an actual data set would not typically be iso-expenditure. In order to test RUM, KS found it necessary to estimate an iso-expenditure data set from the true data set , which in turn requires an additional econometric procedure with all its attendant assumptions. In contrast, as we have established in Theorem 3, the RAUM has the important empirical feature that it can be directly tested on data sets that are not iso-expenditure.

5.3. Welfare Comparisons

Since the test for rationalizability involves finding a distribution over different types, it is possible to use this distribution for welfare analysis. To be specific, suppose that a government is contemplating a change in sales tax that could lead to prices changing from its current value to . Relevant to the government’s re-election prospects is the proportion of consumers who will be better off as a result of this price change.313131We would like to thank an anonymous referee for suggesting this motivation. Our methods allow us to obtain information on this proportion.

To be specific, suppose the analyst has access to a data set that contains among its observations , i.e., the prevailing prices and the demand distribution. To determine the welfare effect of a price change from to , let denote the row vector with its length equal to the number of rational types (), such that the element is 1 if for the rational type corresponding to column of and 0 otherwise.323232Even though is not among the observed prices, one could still define ; see footnote 7. In words, enumerates the set of rational types for which is revealed preferred to . For a rationalizable data set , Theorem 3 guarantees that

| (22) |

is the lower bound on the proportion of consumers who are revealed better off at prices compared to , while the upper bound is

| (23) |

Since (22) and (23) are both linear programming problems (which have solutions if, and only if, is rationalizable), they are easy to implement and computationally efficient. Suppose that the solutions are and respectively; then for any , is also a solution to and, in this case, the proportion of consumers who are revealed better off at compared to is exactly . In other words, the proportion of consumers who are revealed better off can take any value in the interval .

Proposition 2 tells us that the revealed preference relations are tight, in the sense that if, for some consumer, is not revealed preferred to then there exists an augmented utility function which rationalizes her consumption choices and for which she strictly prefers to . Given this, we know that, amongst all rationalizations of , is also the infimum on the proportion of consumers who are better off at compared to .

The following proposition summarizes these observations.

Proposition 4