Non-stochastic portfolio theory

Abstract

This paper studies a non-stochastic version of Fernholz’s stochastic portfolio theory for a simple model of stock markets with continuous price paths. It establishes non-stochastic versions of the most basic results of stochastic portfolio theory and discusses connections with Stroock–Varadhan martingales.

The version at http://probabilityandfinance.com (Working Paper 51) is updated most often.

1 Introduction

Fernholz’s stochastic portfolio theory [2, 3, 4], as its name suggests, depends on a stochastic model of stock prices. This paper proposes a non-stochastic version of this theory based on the framework of [16] (see the end of this section for a brief discussion of its relation to [13]).

A key finding (see, e.g., [2, Section 4], [3, Chapters 2 and 3], [4, Section 7]) of stochastic portfolio theory is that, under certain simplifying assumptions, there is a long-only portfolio that outperforms the capital-weighted market portfolio. The principal aim of this paper is to give a simple non-stochastic formalization of this phenomenon.

Section 2 defines our model of a stock market and introduces non-stochastic notions of a portfolio’s value and its excess growth component. Section 3 is devoted to a non-stochastic version of the “master equation” of stochastic portfolio theory, and Section 4 to its applications. In particular, the latter covers the entropy-weighted portfolio (as in [2, Theorem 4.1] and [3, Theorem 2.3.4]) and diversity-weighted portfolios ([3, Example 3.4.4], [4, Section 7], going back to at least [1]). Section 5 is devoted to detailed interpretations and discussions of the results of the previous sections. Section 6 discusses connections with Stroock–Varadhan martingales, which make the master equation very intuitive. Finally, Section 7 lists some directions of further research.

Another paper treating stochastic portfolio theory in a pathwise manner is [13], and it considers a wider class of portfolios. However, that paper relies on some assumptions that are not justified by economic considerations:

-

•

it postulates a suitable “refining sequence of partitions”;

-

•

it postulates the existence of a continuous covariation between each pair of price paths w.r. to this refining sequence of partitions (in Föllmer’s [7] sense);

- •

2 Market and portfolios

This paper uses the definitions and notation of [16] and [3] (the latter, however, will always be repeated). The notation is used for the process whose value at time is , both for Itô and Lebesgue–Stieltjes integration. The brackets always signify quadratic variation and are never used in the role of parentheses. The abbreviations “q.a.” and “ucqa” stand for “quasi always” and “uniformly on compacts quasi always”; see [16] for definitions.

We consider a financial market in which idealized securities, referred to as stocks, are traded; their price paths , , are assumed to be continuous functions, and they never pay dividends. We let stand for the set of all continuous real-valued functions on . As in [16, Section 4], we fix a sufficiently rich language for defining sequences of partitions; all notions of non-stochastic Itô calculus used in this paper (such as Itô integral and Doléans exponential and logarithm) are relative to this language.

For convenience, we identify with the total market capitalization of the th stock at time . The total capitalization of the market is defined as the process

and the market weight of the th stock is

We take the total capitalization of the market as our numéraire, which allows us to regard as the traded securities (cf. [16, Section 9]), the first of them being just like our original securities but constrained by . (In fact, the original securities will never be used explicitly in the rest of this paper apart from an informal remark.)

Let be the interior of the standard simplex in ,

A basic portfolio is a continuous bounded function mapping to its closure in ; intuitively, it maps the current market weights to the fractions of the current capital invested in the stocks. (In this paper we will only need these very primitive Markovian portfolios.)

The non-stochastic notions of Doléans exponential and Doléans logarithm used in this paper are defined in [16]. The most useful for us interpretation of Doléans logarithm is that is the cumulative return of a price path , and Doléans exponential restores the price path from its cumulative return. The value process of is the Doléans exponential

| (1) |

where is defined by , is defined by , and is defined by . The value process is defined and continuous quasi always.

The definition (1) involves Doléans logarithm, but stochastic portfolio theory emphasizes regular logarithm (cf. the logarithmic model in [3, Section 1.1]). On the log scale the definition (1) can be rewritten as

| (2) | ||||

| (3) | ||||

| (4) | ||||

| (5) |

The second equality in the chain (2)–(5) follows from the standard equality

| (6) |

and the third equality in (2)–(5) follows from

| (7) |

(showing that the first term in (3) can be represented as (4)) and a slight generalization of

| (8) |

(showing that the second term in (3) can be rewritten as (5)). See [16, Section 7] for (6)–(8).

The part

| (9) | ||||

of (2)–(5) consisting of the last two addends will be called the excess growth term (it corresponds to the cumulative excess growth rate in stochastic portfolio theory). We can use it to summarize (2)–(5) as

| (10) |

The addend is the naive expression for the cumulative log growth in the value of , and is the adjustment required to obtain the true cumulative log growth.

A particularly important special case is that of the market portfolio, . To understand the intuition behind the excess growth term (9) in this case, we can rewrite as

| (11) | ||||

| (12) | ||||

where we have used the fact that the subtrahend in (11), being the quadratic variation of a monotonic function (remember that ), is zero. We can see that is bounded below by the total quadratic variation of the market weights.

3 Master equation

Let be a positive function defined on an open neighbourhood of in . For any function (such as ) defined on we let stand for its th partial derivative,

and stand for its second partial derivative in and ,

The portfolio generated by is defined by

| (13) |

The main part of the expression in the parentheses is ; the rest is simply the normalizing constant making a portfolio (it is a constant in the sense of not depending on ).

Now we can state a non-stochastic version of the “master equation” of stochastic portfolio theory (see, e.g., [3, Theorem 3.1.5]).

Theorem 1.

The value process of the portfolio generated by satisfies

| (14) |

where

| (15) |

Proof.

The middle equality (3) in the chain (2)–(5) gives for the left-hand side of (14):

| (16) | ||||

| (17) |

where the last equality follows from . Next we apply the Itô formula to the function on the right-hand side of (14); the Itô formula still holds in our non-stochastic setting: cf. [16, Section 6]. For the first addend on the right-hand side of (14) it gives us the expression

4 Special cases

A positive function defined on an open neighbourhood of is a measure of diversity if it is symmetric and concave. In this section we will discuss three examples of measures of diversity.

4.1 Fernholz’s arbitrage opportunity

In [3, Section 3.3], Fernholz describes an arbitrage opportunity for his stochastic model of the market. In the non-stochastic setting of this paper his portfolio ceases to be an arbitrage opportunity but it is still interesting and suggests the possibility of beating the market (as discussed in the next section). Now we are interested in the measure of diversity

| (18) |

The components (13) of the corresponding portfolio are

| (19) |

Now Theorem 1 gives the following non-stochastic version of [3, Example 3.3.3].

Corollary 2.

The value process of the portfolio (19) satisfies

| (20) |

Proof.

Plugging (where stands for the indicator function of ) into (15), we indeed obtain

A slightly cruder but simpler version of Corollary 2 is:

Corollary 3.

The value process of the portfolio (19) satisfies

| (21) |

Proof.

It suffices to notice that . ∎

4.2 Entropy-weighted portfolio

The archetypal measure of diversity [3, Examples 3.1.2 and 3.4.3] is the entropy function

Using (13), the components of the corresponding entropy-weighted portfolio can be computed as

| (22) |

Calculating the drift term in Theorem 1, we obtain the following corollary (a non-stochastic version of [3, Theorem 2.3.4]).

Corollary 4.

The value process of the entropy-weighted portfolio satisfies

| (23) |

4.3 Diversity-weighted portfolios with parameter

Fix . Define the measure of diversity with parameter [3, Example 3.4.4] as

The -diversity-weighted portfolio has components

| (24) |

The following corollary is a non-stochastic version of [3, Example 3.4.4].

Corollary 5.

The value process of the diversity-weighted portfolio with parameter satisfies

| (25) |

Proof.

Now (15) gives

Corollary 5 immediately implies:

Corollary 6.

The value process of the diversity-weighted portfolio with parameter satisfies

| (26) |

5 Beating the market

The results of the previous section have striking implications for our idealized financial market. The easiest to discuss is Corollary 3. It can be interpreted, very informally, as the following Fisherian disjunction: either the variation of each stock in the market decays, in that the total quadratic variation of each of the market weights over is finite, or we can beat the market in the sense that (cf. [6], p. 42). Notice that the second alternative of the disjunction also takes care of the “q.a.” in (21).

The portfolio (19) is particularly tame (or admissible, in Fernholz’s [3, Section 3.3] terminology): it is long-only, it never loses more than of its value relative to the market portfolio (by (21)), and it never invests more than 3 times more than the market portfolio in any of the stocks.

A more specific possible interpretation of Corollary 3 is based on the efficient market hypothesis in the form that was so forcefully advocated in the bestseller [11] by Burton G. Malkiel; for him, “the strongest evidence suggesting that markets are generally quite efficient is that professional investors do not beat the market.” Even if there are ways to beat the market, it is often believed that they should involve something unusual rather than merely simple portfolios such as (19), (22), or (24) (widely known since at least 2002). According to this interpretation, Corollary 3 implies that in efficient markets we expect market variation to die down eventually.

If we believe that the variation in our stock market will never die down, we are forced to admit that Corollary 3 “opens the door to superior long-term investment returns through disciplined active investment management” [10, Section 1.3]. This is the interpretation on which typical practical applications of stochastic portfolio theory are based (see, e.g., [1], which, however, is based on the stochastic versions of Corollaries 5 and 6 rather than Corollary 3).

Corollary 3 is a cruder version of Corollary 2 that replaces the first addend on the right-hand side of (20) by its lower bound and the denominator in the second addend by its upper bound. Corollary 2 is more precise in that it decomposes the growth in the portfolio’s value into two components: one related to the growth in the diversity of the market weights and the other related to the accumulation of the variation of the market weights.

It is standard in stochastic portfolio theory to assume both that the market does not become concentrated, or almost concentrated, in a single stock and that there is a minimal level of stock volatility; precise versions of these assumptions are referred to as diversity and non-degeneracy, respectively. We will see that the results of the previous section can be interpreted as saying that we can beat the market unless it loses its diversity or degenerates. Corollary 3 says that, in fact, the condition of non-degeneracy alone is sufficient; this follows from the representation . (But remember that our exposition is in terms of market weights rather than prices , which are usually used in stochastic portfolio theory.)

Corollary 4 relies on both assumptions, diversity and non-degeneracy. If the market maintains its diversity, we expect the first addend on the right-hand side of (23) to stay bounded below, and if, in addition, the market does not degenerate, we expect the second addend to increase steadily. As a result, the entropy-weighted portfolio outperforms the market.

To discuss Corollaries 5 and 6, it is convenient to extend our discussion of given in Section 2 to more general . Let us now rewrite twice the excess growth term (9), , as

Define (using our fixed language) a sequence of partitions that is fine for all processes used in this paper and set, for a given partition ,

with the dependence on suppressed. We can then regard

| (27) |

as the th approximation to ; it can be shown that

Rewriting (27) as

we can see that this expression is the cumulative variance of the logarithmic returns over the time interval w.r. to the “portfolio probability measure” . This makes the expression (10) very intuitive: the excess growth rate of the portfolio over the naive expression is determined by the volatility of the market weights w.r. to .

As already mentioned, the stochastic versions of Corollaries 5 and 6 have been used for active portfolio management [1]. The remarks made above about the relation between Corollaries 2 and 3 are also applicable to Corollaries 5 and 6; the latter replaces the first addend on the right-hand side of (25) by its lower bound. Corollary 5 decomposes the growth in the value of the diversity-weighted portfolio into two components, one related to the growth in the diversity of the market weights and the other related to the accumulation of the diversity-weighted variance of the market weights. Corollary 6 ignores the first component, which does not make it vacuous since is bounded, always being between (corresponding to a market concentrated in one stock) and (corresponding to a market with equal capitalizations of all stocks).

Several explanations have been suggested for the somewhat counterintuitive disjunction stated at the beginning of this section:

-

•

If we include all stocks traded in a real-world market in our model, perhaps making very large, the portfolio (13) and its special cases (19), (22), and (24) (particularly the last two) will not be efficient since they will be forced to invest into smaller and so less liquid stocks; it is known that portfolios generated by measures of diversity invest into smaller stocks more heavily than the market portfolio does [3, Proposition 3.4.2].

-

•

There is another explanation related to this common feature of the portfolios discussed in this paper that outperform the market (increased weights of smaller stocks as compared with the market). Over the last decades, such portfolios have been adversely affected by the tendency of larger companies to pay higher dividends (cf., e.g., [3, Figure 7.4], describing the performance of an index that has been used in investment practice). The role of differential dividend rates in maintaining market diversity is emphasized in [2].

-

•

If we restrict our attention only to largest stocks traded in a real-world market, for a moderately large (such as for S&P 500), the performance of portfolios such as (19), (22), or (24) w.r. to this smaller “market” (which is now, in fact, a large cap market index) will be affected by the phenomenon of “leakage” [3, Example 4.3.5 and Figure 7.5].

6 Fernholz’s master martingale and Stroock–Varadhan martingales

One way to restate Theorem 1 is to say that

| (28) |

is a value process q.a.; in the terminology of [16], it is a continuous martingale. In this section we will see that Fernholz’s master martingale (28) is in fact a very natural object, and not just a product of formal manipulations with the Itô formula, as might have appeared from its derivation in Section 3. Connections with recent papers [8] and [5] will be discussed later in the section.

Let be a function defined on an open neighbourhood of in . The non-stochastic Itô formula [16] implies that

| (29) |

and so the left-hand side of (29) is a continuous martingale, which we will refer to as the Stroock–Varadhan martingale [9, (5.4.2)]; it is a non-stochastic version of the classical martingales used by Stroock and Varadhan in their study of diffusion processes.

Fernholz’s master martingale (28) is the Doléans exponential of the Stroock–Varadhan martingale on the left-hand side of (29) for . Indeed, applying (6) gives the Doléans exponential

of the left-hand side of (29), which is equal, by the identity

to (28). If we regard the Stroock–Varadhan martingale to be an additive process, Fernholz’s master martingale (28) becomes its multiplicative counterpart. “Additive” and “multiplicative” is the terminology used in [8, 5] (more carefully than in this paper), and the relation between the Stroock–Varadhan martingale on the left-hand side of (29) and Fernholz’s master martingale (28) is somewhat analogous to the relation between the additive Bachelier formula [14, Section 11.2] and the multiplicative Black–Scholes formula [14, Section 11.3] in option pricing.

The papers [8] and [5] study additive portfolio generation in depth. In particular, these papers give numerous interesting examples (including (32) below).

We can rewrite (21) in Corollary 3 as

which implies

| (30) |

where is a positive constant, is the stopping time

| (31) |

and .

Qualitatively, (30) means that the market satisfies Fernholz’s arbitrage-type property: we can beat a non-degenerate market (interpreting non-degeneracy as for all ). The Stroock–Varadhan martingale on the left-hand side of (29) also gives a Fernholz-type arbitrage, which is, however, polynomial (and even linear) in , unlike (30). Setting

| (32) |

(cf. (18)), we can rewrite the continuous martingale on the left-hand side of (29) as

therefore, is a nonnegative continuous martingale satisfying and

| (33) |

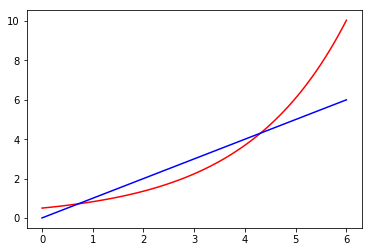

Therefore, this is an alternative method for achieving the same qualitative goal, as . Quantitatively the result might appear weaker; after all, we lose the exponential growth rate in . However, there is a range of (roughly between and ) where the Stroock–Varadhan martingale performs better: see Figure 1.

7 Conclusion

Figure 1 gives two functions such that a final capital of is achievable at time . It would be interesting to characterize the class of such functions . A related question is: what is the best growth rate of as ? This question can be asked in both stochastic and non-stochastic settings. These are some directions of further research for non-stochastic theory:

-

•

A natural direction is to try and strip other results of stochastic portfolio theory of their stochastic assumptions. First of all, it should be possible to extend Theorem 1 to functions that are not smooth (as in [3, Theorem 4.2.1]); the existence of local time in a non-stochastic setting is shown in [12] and, in the case of continuous price paths, can be deduced from the main result of [15].

-

•

Another direction is to extend this paper’s results to general numéraires (this paper uses the value of the market portfolio as our numéraire).

-

•

Finally, it would be very interesting to extend some of the results to càdlàg price paths.

Acknowledgements

The first draft of this paper was prompted by discussions with Martin Schweizer and Dániel Bálint in December 2017. I am grateful to Ioannis Karatzas for information on the existing literature (in particular, he drew my attention to connections between Section 6 of this paper and additive portfolio generation in [8] and [5]) and for his advice on presentation, notation, and terminology. Thanks to Peter Carr, Marcel Nutz, Philip Protter, and Glenn Shafer for useful comments.

References

- [1] E. Robert Fernholz. Diversity-weighted equity indexes. ETF Journal of Indexes, http://www.etf.com/publications/journalofindexes/joi-articles/1074.html, April 1, 1999.

- [2] E. Robert Fernholz. On the diversity of equity markets. Journal of Mathematical Economics, 31:393–417, 1999.

- [3] E. Robert Fernholz. Stochastic Portfolio Theory. Springer, New York, 2002.

- [4] E. Robert Fernholz and Ioannis Karatzas. Stochastic portfolio theory: an overview. In P. G. Ciarlet, editor, Handbook of Numerical Analysis, volume 15, Special Volume: Mathematical Modelling and Numerical Methods in Finance (Alain Bensoussan and Qiang Zhang, guest editors), pages 89–167. North-Holland, Amsterdam, 2009.

- [5] E. Robert Fernholz, Ioannis Karatzas, and Johannes Ruf. Volatility and arbitrage. Technical Report arXiv:1608.06121 [q-fin.PM], arXiv.org e-Print archive, August 2016. Journal version (to appear): Annals of Applied Probability.

- [6] Ronald A. Fisher. Statistical Methods and Scientific Inference. Hafner, New York, third edition, 1973.

- [7] Hans Föllmer. Calcul d’Itô sans probabilités. Séminaire de probabilités de Strasbourg, 15:143–150, 1981.

- [8] Ioannis Karatzas and Johannes Ruf. Trading strategies generated by Lyapunov functions. Finance and Stochastics, 21:753–787, 2017.

- [9] Ioannis Karatzas and Steven E. Shreve. Brownian Motion and Stochastic Calculus. Springer, New York, second edition, 1991.

- [10] Andrew W. Lo and A. Craig MacKinlay. A Non-Random Walk Down Wall Street. Princeton University Press, Princeton, NJ, 1999.

- [11] Burton G. Malkiel. A Random Walk Down Wall Street. Norton, New York, eleventh revised edition, 2016.

- [12] Nicolas Perkowski and David J. Prömel. Local times for typical price paths and pathwise Tanaka formulas. Electronic Journal of Probability, 20(46):1–15, 2015.

- [13] Alexander Schied, Leo Speiser, and Iryna Voloshchenko. Model-free portfolio theory and its functional master formula. Technical Report arXiv:1606.03325 [q-fin.PM], arXiv.org e-Print archive, December 2016.

- [14] Glenn Shafer and Vladimir Vovk. Probability and Finance: It’s Only a Game! Wiley, New York, 2001.

- [15] Vladimir Vovk. Continuous-time trading and the emergence of probability. Technical Report arXiv:0904.4364v4 [math.PR], arXiv.org e-Print archive, May 2015. Journal version: Finance and Stochastics, 16:561–609, 2012.

- [16] Vladimir Vovk and Glenn Shafer. Towards a probability-free theory of continuous martingales. Technical Report arXiv:1703.08715 [q-fin.MF], arXiv.org e-Print archive, March 2017.

- [17] M. Würmli. Lokalzeiten für Martingale. Master’s thesis, Universität Bonn, 1980. Supervised by Hans Föllmer.

Appendix A Connections with the foundations of game-theoretic probability

In this appendix we will see yet another method of achieving the qualitative goal of for a nonnegative supermartingale . The result will be weaker than both functions in Figure 1, but it will shed light on a seemingly paradoxical feature of continuous-time game-theoretic probability.

The method uses the non-stochastic Dubins–Schwarz theorem presented in [15] and is based on the following apparent paradox, which we first discuss informally. As agreed in Section 2, we regard as tradable securities. According to the non-stochastic Dubins–Schwarz theorem and a standard property of Brownian motion, with very high lower probability all securities will eventually hit zero if their volatility is appreciable. When this happens, the normalized value of the market will be 0 rather than 1, which is impossible. Therefore, we expect an event of a low upper game-theoretic probability to happen, i.e., we expect to be able to outperform the market. This is formalized in the following statement:

Proposition 7.

For any constant , there is a nonnegative supermartingale such that and

| (34) |

where is the stopping time (31) and is interpreted as .

Proof.

For each , we will construct a nonnegative continuous martingale satisfying and

| (35) |

where

(In this case we can set to the average of all of stopped at time .) According to [9, (2.6.2)], the probability that a Brownian motion started from 1 (in fact is started from ) does not hit zero over the time period is

In combination with the non-stochastic Dubins–Schwarz result [15, Theorem 3.1] applied to , this gives (35) with

in place of . ∎

The processes in (30) and in (33) are nonnegative supermartingales in the sense of [16] (in fact, nonnegative continuous martingales). On the other hand, the process in (34) is a nonnegative supermartingale in the sense of the more cautious definitions in [15]. This can be regarded as advantage of (34) over (30) and (33). However, a disadvantage of (34) is that quantitatively it is much weaker than both (30) and (33); the right-hand side of (34) is always smaller than the right-hand side of (30), and it is greater than the right-hand side of (33) only for a small range of (approximately for ).