Explicit minimisation of a convex quadratic under a general quadratic constraint: a global, analytic approach

A novel approach is introduced to a very widely occurring problem, providing a complete, explicit resolution of it: minimisation of a convex quadratic under a general quadratic, equality or inequality, constraint. Completeness comes via identification of a set of mutually exclusive and exhaustive special cases. Explicitness, via algebraic expressions for each solution set. Throughout, underlying geometry illuminates and informs algebraic development. In particular, centrally to this new approach, affine equivalence is exploited to re-express the same problem in simpler coordinate systems. Overall, the analysis presented provides insight into the diverse forms taken both by the problem itself and its solution set, showing how each may be intrinsically unstable. Comparisons of this global, analytic approach with the, intrinsically complementary, local, computational approach of (generalised) trust region methods point to potential synergies between them. Points of contact with simultaneous diagonalisation results are noted.

Keywords Constrained optimisation, quadratic programming, simultaneous diagonalisation

2000 MSC: 15A18, 90C20, 90C30

1 Introduction

1.1 Background

This paper introduces a novel approach to a very widely occurring problem: minimisation of a convex quadratic under a general quadratic, equality or inequality, constraint. This may arise by itself, or as a component of a larger problem – notably, as a single iteration in minimising a smooth convex objective function under a smooth constraint. In either case, we treat solving the above problem as of interest in itself.

Statistical instances of this problem – our primary motivation – occur, for example, in minimum distance estimation, Bayesian decision theory, generalised linear models with smooth constraints, canonical variate analysis with fewer samples than variables, various forms of oblique Procrustes analysis, Fisher/Guttmann estimation of optimal scores, spline fitting, estimation of Hardy-Weinberg equilibrium, and size and location constraints in iterative missing value procedures in Procrustes analysis. Associated literature is reviewed, united and extended in Albers et al. [4]. Some of these instances are elaborated in Albers et al. [3, 7].

Within the optimisation and numerical analysis literatures, the above problem has particularly close connections with (generalised) trust region ((G)TR) methods, being a special case of the GTRS problem defined in [23]. At the same time, the global, analytic approach presented here is, intrinsically, complementary to the local, computational one in the GTR literature. Valuable in itself, this new approach points to potential synergies with existing methodology, as we briefly indicate in closing.

In the main, GTR methods adapt a nonlinear optimisation protocol to address the problem on hand. Regularity conditions (constraint qualifications) are introduced, as required, under which the Karush-Kuhn-Tucker conditions are necessary for a local optimum, assuming such exists, additional conditions typically being required to ensure their sufficiency. Algorithms are then designed to seek a point satisfying all of these conditions. The literature on TR and GTR methods can be accessed via the excellent accounts presented in [9] and [23, 21, 25] respectively. See also [24, 15, 11, 29, 28, 26, 27, 19], algorithms to handle the extreme forms of ill-conditioning that can occur being presented, for example, in [12, 13]. Recent work in [1] on non-iterative algorithms extends [16], and notes the possibility of non-unique solutions [[, cf.]]Martinez. Other related recent work includes [18, 8, 14, 20, 30].

In contrast to the GTR approach, the one introduced here exploits a series of nonsingular affine transformations to re-express the same problem in successively simpler forms, each transformation corresponding to a convenient change of coordinate system. Solving the last of these affinely equivalent forms solves at once the initial problem, via back transformation. Throughout, underlying geometry illuminates and informs algebraic development. This approach offers a complete, explicit resolution of the problem presented at the outset. Completeness comes from analysing (literally, splitting) all of its possible instances into precisely identified, mutually exclusive and exhaustive, special cases. Explicitness comes from providing, in each case, closed-form expressions for the solution set and optimised value attained thereon.

Overall, this new approach highlights the diverse nature of different instances of both problem and solution set. And, moreover, the possibility of intrinsic instability – whereby arbitrarily (hence, undetectably) small changes in problem specification lead to radical changes in the form of problem and/or solution set – pinpointing where this occurs. It may then, in practice, be impossible to be sure which of several forms applies.

Concerning this approach, Critchley [10], cited in [21], provided an early account of the strictly convex form, the general case being first addressed in the technical report [2]. Again, Gower and Dijksterhuis [17] addressed the problem in the context of Procrustes analysis and gave a preliminary algorithm, further worked out in Albers and Gower [6].

1.2 Notation and conventions

The following notation and conventions are used. Terms involving arrays of vanishing order are absent. is endowed with the standard Euclidean inner product, inherited by each of its subspaces. Its zero member is denoted by , and the span of its first unit coordinate vectors . denotes the set of all real symmetric matrices, with zero member . Subscripts denoting the order of arrays may be omitted when no confusion is possible. Positive (semi-)definiteness of a matrix is denoted by (respectively, ), the latter terminology here implying that is singular. The Moore-Penrose inverse of is denoted by . Finally, denotes a (block)diagonal matrix with the diagonal entries listed, while denotes strict inclusion.

For brevity, straightforward proofs are omitted.

1.3 The general problem

The general equality-constrained problem is as follows.

Definition 1.1.

For , in , , in and in , , writing , the -variable problem is:

where the objective (loss) function is convex and the feasible set nonempty; when the solution set is nonempty, may be written as . The set of all such is denoted by . Where no confusion is possible, we may omit the subscript . We say that is (a) centred if the target , (b) a (partitioned) least-squares problem if has the form , and (c) a full least-squares problem if . For any least-squares problem, we partition

| (1) |

conformably with , subscripts and connoting its range and null spaces, so that . In this way, terms with subscripts are absent when , so that and .

Remark 1.1.

Denoting the rank of by , and is strictly convex when , while otherwise , with if and only if lies in the -dimensional null space of . Symmetry of and is assumed without loss, while taking nonzero avoids one obvious triviality. avoids another, entailing restrictions on characterised (by negation) in Lemma 1.1 below. The overall sign of the constraint coefficients can be reversed at will, being unchanged under . Additional consistent affine constraints do not require separate treatment: they can be substituted out to arrive at an equivalent instance of in fewer variables.

Lemma 1.1.

Let , where , and . Let have decomposition , , along the range and null spaces of , so that , and let . Then:

| (2) |

Accordingly, does not have a solution if and only if

|

1.4 Overview of paper

The solution to when is well-known. For all other , the infimal value and solution set are given explicitly. The variant of in which the constraint is relaxed to a weak inequality is also completely resolved. The organisation and principal subsidiary results of the paper are as follows.

Sections 2 and 3: Theorem 2.1 describes affine equivalence on the set of problems , Theorem 3.1 showing that every is affinely equivalent to a centred least-squares problem.

Section 4 deals with the inequality constrained case. We say that two minimisation problems with the same loss function are effectively equivalent if they have the same infimal value attained on the same solution set. A simple continuity argument shows that, for every , its weak inequality constraint variant either has a trivial solution or is effectively equivalent to itself, Theorem 4.1 specifying exactly when each occurs.

Section 5 discusses the case, Lemma 5.2 showing that every centred least-squares problem is now affinely equivalent to a simplified form. Theorem 5.1 establishes that there are at most three possibilities for such a form, specifying exactly when each occurs. In two of them, distinguished by whether or not is empty, . In the third, (a) while (b) a reduced form of is effectively equivalent to an induced (centred) full least-squares problem in variables. Remark 5.2 establishes direct points of contact with simultaneous diagonalisation.

Section 6: given the above results, there is no loss in assuming now that is positive definite, in which case, always has a solution (Theorem 6.1), Theorem 6.2 establishing that it is affinely – indeed, linearly – equivalent to a canonical form , governed by the spectral decomposition of .

Section 7: exploiting orthogonal indeterminacy within eigenspaces, Theorem 7.1 establishes that solutions to can be characterised in terms of those of a dimension-reduced canonical form . There is no loss in restricting attention to regular such forms, denoted by (Remark 7.2).

2 Affine equivalence

Recalling that the nonsingular affine transformations on form a group under composition, whose general member we denote by , the same instance of can be re-expressed in different, affinely equivalent, coordinate systems.

Definition 2.1.

For any vector and for any nonsingular , denotes the map , inducing via:

For linear maps (), we abbreviate as .

Remark 2.1.

Note that: (a) the rank and signature of and are maintained in those of and respectively, (b) and are unchanged under translation , and (c) is unchanged under linear maps ().

Theorem 2.1.

For all , and : and , so that , , and , in which case .

In view of Theorem 2.1, we say that and are affinely equivalent, writing . Again, if with orthogonal, we call and Euclideanly equivalent.

Recall that also leaves unchanged. For later use (Section 6), we note here

Lemma 2.1.

commutes with , .

3 Centred least-squares form

We characterise here the set of centred least-squares problems to which a given problem is affinely equivalent. Partitioning conformably with , as in (1), let denote is orthogonal, and is nonsingular, noting that forms a group under multiplication.

Theorem 3.1.

Let and where has spectral decomposition with orthogonal and diagonal, positive definite. Then:

-

(i)

, , is a centred least-squares problem;

-

(ii)

is also such a problem if and only if for some .

4 Inequality contrained variant

We denote by the inequality constrained variant of in which the feasible set required to be nonempty is replaced by , its infimal value and solution set being denoted by and respectively. The reverse inequality is accommodated by changing the overall sign of .

Affine equivalence generalises at once to the inequality constrained case, as does Theorem 3.1. Accordingly, in discussing , there is again no loss in restricting attention to the centred least-squares case, when .

Theorem 4.1.

Let be an inequality constrained, centred least-squares problem.

-

(i)

When :

if , and ;

otherwise, and is effectively equivalent to . -

(ii)

When , putting :

if , and ;

otherwise, and is effectively equivalent to .

Proof.

The proof is similar in both cases.

-

(i)

If , the result is immediate. Else, , continuity of ensuring that, , with .

-

(ii)

If , the result is immediate. Else, while, , with .

∎

5 Solving when is positive semi-definite

In this section, we take positive semi-definite (), so that occurs in the constraint but not in the objective function. Accordingly, any centred least-squares problem takes an associated reduced form, an immediate lemma providing geometric insight.

Denoting orthogonal projection of onto by , we have:

Definition 5.1.

For any centred least-squares problem with , its reduced form is:

| (3) |

Remark 5.1.

Note that is (a) nonempty, since is nonempty, and (b) given by

where .

Lemma 5.1.

Let be a centred least-squares problem with . Then , while , so that , while solves solves (3) and .

Geometrically, the reduced form seeks the infimal (squared) distance from the origin in to the orthogonal projection of the conic onto that subspace, its solution set being the orthogonal projection of onto .

To help solve the reduced form (3), we introduce a simplifying linear transformation, via a decomposition of the null space of according to its intersections with the range and null spaces of .

Definition 5.2.

Let be a centred least-squares problem with . Then, is said to be in simplified form if, for some and for some nonsingular diagonal of order , has the partitioned form:

| (4) |

Accordingly, any term involving is absent if and only if , and any involving if and only if is nonsingular – in particular, if is (positive or negative) definite.

Lemma 5.2.

Let be a centred least-squares problem with . Then, with in simplified form.

Proof.

Let have rank and spectral decomposition , with orthogonal and nonsingular diagonal. Define and implicitly via

and put

| (5) |

Then and so, by Theorem 3.1, is a centred least-squares problem in simplified form. ∎

We note in passing that, while preserving simplified form, a further linear transformation establishes direct points of contact with simultaneous diagonalisation.

Remark 5.2.

If is in simplified form, while in (4) has spectral decomposition:

the further transformation with induces:

| (6) |

so that, using again Theorem 3.1, , , remains in its simplified form. This can be seen as extending Newcomb [22] who showed that any two symmetric matrices, neither of which is indefinite, can be simultaneously diagonalised. For, there is no loss in restricting attention to matrices that, like , are either positive definite or positive semi-definite, which, if true of , entails that and in (6) are absent or zero respectively.

Returning to the mainstream, the following additional terms are used.

Definition 5.3.

For any centred least-squares problem in simplified form, we sub-partition and so that

conform. Accordingly, any term involving or is absent if and only if is nonsingular; and any involving or if and only if .

For given , depends quadratically on , but only linearly on , since

| (7) |

in which with .

If , , , so that is , or according as is indefinite, positive definite or negative definite, while if is definite. If is singular and , , while , so that .

In view of previous results, when , it suffices to solve – or, giving also each , its reduced form (3) – for centred least-squares problems in simplified form.

Definition 5.4.

Let with be a centred least-squares problem in simplified form. Then, is called the projected form of , and we say that admits:

-

(a)

a perfect solution if for some ;

-

(b)

an essentially perfect solution if , but ;

-

(c)

a projected, yet imperfect, reduced form if (i) , so that , and (ii) its reduced form is effectively equivalent to :

in which .

Example 5.1.

Examples of these three possibilities are the problems, with and , of finding the infimum of over all satisfying, respectively, (a) , (b) and (c) , the corresponding sets being , and .

Indeed, there are no other possibilities. Denoting the closure and boundary of by and , we have:

Theorem 5.1.

Let with be a centred least-squares problem in simplified form. There are at most three, mutually exclusive, possibilities:

-

(a)

admits a perfect solution,

-

(b)

admits an essentially perfect solution,

-

(c)

admits a projected, yet imperfect, reduced form,

whose occurrences are characterised thus:

-

(a)

occurs ,

-

(b)

occurs ,

-

(c)

occurs ,

these arising as follows:

-

(i)

If :

being or respectively. Otherwise, , with (c) or (b) occurring according as does, or does not, vanish. When (c) occurs, with each .

-

(ii)

If :

being or respectively, while (b) does not occur. Thus, (c) occurs , when with each .

-

(iii)

If :

or comprising all with in , or , respectively. Otherwise, , with (c) or (b) occurring according as does, or does not, vanish. When (c) occurs, and each are as in (ii).

Proof.

Using Lemma 5.1, the characterisations of the occurrence of (a) and of (b) are immediate. Since

| (8) |

so, too, is the fact that (c) occurs . Recall that

| (9) |

Using the instances of (7) and (9), and identifying the former as an instance of the identity (2), Lemma 1.1 gives:

Similarly, using also (8), we have:

Suppose . If also , , so that and the reduced form (3) of is . Thus, (c) occurs, while each . If, instead, we also have , and

so that . Since while , Theorem 4.1 establishes that (c) again occurs, while each has the form stated. The forms taken by when (a) occurs are immediate. ∎

Corollary 5.1.

Under the hypotheses of Theorem 5.1, and adopting its terminology, it is necessary for (b) to occur that be indefinite.

Proof.

If is not indefinite, is either absent or zero. ∎

Geometrically, a hyperbolic quadratic constraint is necessary for to admit an essentially perfect solution.

As Theorem 5.1 shows – and as the example of (b) given immediately before it illustrates – it is possible that has no solution when , reflecting the fact that, although is closed, its projection may not be. In contrast, a simple compactness argument, used in proving Theorem 6.1 below, shows that always has a solution when .

6 Canonical form

Given the above results, it suffices to solve the centred, full least-squares form , of problem . The affinely constrained case being well-known, there is no essential loss in also requiring . Reversing if necessary the overall sign of , and recalling Lemma 2.1, there is no loss in further assuming that has a positive eigenvalue.

Such a problem always has a solution.

Theorem 6.1.

for any full least-squares problem .

Proof.

For any , is essentially equivalent to minimising over the compact set . ∎

Geometrically, there is always a shortest normal from to the conic .

We introduce next the notion of a canonical form, a full least-squares form of in which the constraint has been simplified according to the spectral decomposition of . In it, denotes the first unit coordinate vector in .

Definition 6.1.

Let be a centred,

full least-squares problem in which has a positive eigenvalue. Let

have rank and distinct nonzero eigenvalues

, so that . For each , let

have multiplicity and let the orthogonal projection

of onto the corresponding eigenspace have length . Let

denote the dimension of the null space of , and

the length of the orthogonal projection of onto this

subspace.

With and , , let

in which

, where

,

and . Then, we call the canonical form of .

The reason for this terminology is made clear by the following result.

Theorem 6.2.

is Euclideanly equivalent to .

Proof.

By the spectral decomposition of , there is an orthogonal matrix with , where is unique up to postmultiplication by .

Let and conform, so that while , and let now be such that the first column of is if and of is if .

Finally, let . Then, using Lemma 1.1, is Euclideanly equivalent to . ∎

Remark 6.1.

Viewed geometrically, the isometry inducing

so translates, rotates and reflects coordinate axes that:

(a) , determining the quadratic part of the constraint,

becomes diagonal,

(b) , determining its linear

part, vanishes when is nonsingular and, otherwise, has at most one

nonzero element – its coordinate on the first dimension of

the null space of – and:

(c) the target

is orthogonal to this subspace, and has at most one

nonzero element associated with each nonzero eigenvalue of – its

coordinate on the first dimension of the corresponding eigenspace.

As is explicit in the proof of Theorem 6.2, the simple structure enjoyed by a canonical form within each eigenspace of is made possible by a well-known orthogonal indeterminacy there. This simple structure invites a natural dimension reduction, further exploiting this same indeterminacy.

7 Dimension-reduced canonical form

Solutions to can be characterised in terms of those of a dimension-reduced canonical form , having just one variable for each distinct eigenvalue of . Variables enter the constraint quadratically. When is singular, an additional scalar variable associated with its null space enters the constraint linearly.

A unified account is provided in which we denote these variables by , whether is nonsingular or not . In the former case, and . In the latter, and .

Definition 7.1.

Adopting the assumptions and

notation of Definition 6.1, let , so that is either positive

definite or nonsingular indefinite , requiring .

If is singular, let

and conform with , while

. Otherwise, put , , and . Then, the dimension-reduced

canonical form of is , , with ,

, , and

. That is, the problem is to:

| (10) |

where the feasible and solution sets and are nonempty, as and are so. We may write as , or . Reflecting the form of the conic, when , we call the constraint in elliptic or hyperbolic according as or . When , we call it parabolic-elliptic or parabolic-hyperbolic in the same two cases.

Remark 7.1.

When each eigenvalue of – equivalently, of – is simple, no such dimension reduction is possible, and coincides with . That is,

Theorem 7.1.

Let , where . Then, solves if and only if

where solves . In particular, .

Clearly, . Moreover, Theorem 7.1 has the immediate

Corollary 7.1.

solving determines more than one solution to and for some , in which case the sign of is indeterminate, while is orthogonally indeterminate.

Example 7.1.

A clear example of Corollary 7.1 is when the problem is to minimise the (squared) distance to the unit sphere in from its centre, the origin . The solution set is, of course, the unit sphere, while is one-dimensional with .

Remark 7.2.

If is singular, but has zero component in its null space – that is, if , but – the linear term in the constraint vanishes so that the optimal , reducing to the corresponding case. It suffices, then, to solve dimension-reduced canonical forms which are regular in the sense defined next.

Definition 7.2.

A dimension-reduced canonical form is called regular if either or and . We denote such forms by .

Since, trivially, , we have at once

Remark 7.3.

For any regular dimension-reduced canonical form :

in which case, substituting out the constraint, can be rephrased as the unrestricted minimisation of a quartic in .

8 Solving

We solve any regular dimension-reduced canonical form via a series of simple, insightful, auxiliary results. The first shows that a Lagrangian approach establishes sufficient conditions for this.

8.1 Sufficient conditions

The Lagrangian for has normal equations

| (11) |

and Hessian .

Definition 8.1.

We refer to has no negative eigenvalues as the admissible region – that is:

| (12) |

– its interior, denoted by , being where . For each ,

so that denotes the set of feasible vectors, if any, obeying the normal equations.

Lemma 8.1.

For any , . Indeed, if ,

In particular, if , uniquely solves .

Proof.

It suffices to note that, by the Cosine Law:

∎

In view of Lemma 8.1, is completely resolved if we can find, in explicit form, a nonempty set for any .

8.2 Feasible solutions to the normal equations

Characterising when feasible solutions to the normal equations exist requires extensions of terminology established in Section 7. Continuing its unified presentation of and , terms involving any of , or, introduced below, or are absent by convention if .

We distinguish between interior and boundary points of . Accordingly, recalling (12), there are either two or three cases to consider according as or . We call these Cases A (), B1 () and Bq (), this last arising when and only when . By convention this last condition – that the constraint (10) be, at least in part, hyperbolic – is implicit whenever any of the terms defined only in Case Bq is mentioned. In particular, this applies to , , and, defined next.

Definition 8.2.

Let be a regular dimension-reduced canonical form and let .

Case A denotes the unique solution to the normal equations, while the function is defined by . That is, for all :

| (13) |

and respectively denote the infimum and supremum of .

Case B1 , has general element , while where .

Case Bq when and only when : , has general element , while where .

Remark 8.1.

The constraint is polynomial in .

Key properties of are summarised in

Proposition 8.1.

For any

if and

, for all ,

so that ;

else, if

either or does not vanish, is continuous and

strictly increasing, being given by

|

Consider now Case A. Regularity of and Proposition 8.1 give at once

Lemma 8.2.

does not depend upon and for every .

Again, using Lemma 8.1, we have at once

Lemma 8.3.

Let . Then,

so that:

In view of Lemma 8.3, we may define as the common value of among all solutions to , when at least one such exists. Putting , Lemmas 8.1 and 8.3 now give

Lemma 8.4.

Combining the above auxiliary results makes explicit and, with it, the following summary of Case A.

Proposition 8.2.

For any , there are three possibilities

(a) If , has a

unique solution and .

(b) If , for every and

.

(c) In all other cases,

has no solutions and .

In view of Proposition 8.2, we refer to as a potential Lagrangian solution set, this potential being realised if and only if it is non-empty. Turning now to the boundary cases, there are two other potential Lagrangian solution sets and , this second definition being made when and only when . The hessian being singular here, the normal equations (11) have either no solution, or a unique solution for all but one member of , which they leave unconstrained. We have

Proposition 8.3.

For any

(1) Case B1 and , in which case:

(2) Case Bq and , in which case:

Proof.

in which case:

being unconstrained. Thus,

(1) now follows from Lemma 8.1. The proof of (2) is entirely similar. ∎

8.3 The minimised objective function and the solution set

We are now ready to solve any regular dimension-reduced canonical form in which, by definition, either or and .

To aid geometric interpretation, recall that, under the assumptions and

notation of Definition 6.1:

(a) denotes the

length of the orthogonal projection of onto the null space of , whose

dimension is ;

(b) for each distinct nonzero eigenvalue

of , has general element

in which

denotes the length of the orthogonal projection of onto the corresponding

eigenspace of , whose dimension is .

Accordingly:

| the linear part of the constraint vanishes | |||

| the origin is feasible | |||

| the origin is the target | and: | ||

| the constraint is, at least in part, elliptic |

We distinguish three mutually exclusive and exhaustive types of regular dimension-reduced canonical form . The first two are trivial.

We call non-Lagrangian if and , (so that, in particular, is undefined). Geometrically, if the feasible set is the origin, the target being a positive distance away. As Theorem 8.1 establishes, in this case, both and are empty. That is, the constraint and normal equations are inconsistent, so that is not amenable to Lagrangian solution.

We call multiply-Lagrangian if . That is, if and . Geometrically, if the target is the origin, through which the conic defining the constraint passes. As Theorem 8.1 establishes, in this case, coincides with each of the nonempty sets , and, when defined, .

Finally, we call singly-Lagrangian if it is neither non-Lagrangian nor multiply-Lagrangian. Algebraically, if either and , or and , or and . As Theorem 8.1 establishes, in this case, exactly one of , and is nonempty, and so provides the solution set required.

Theorem 8.1.

The minimised objective function and solution set for a regular dimension-reduced canonical form are as follows.

-

(a)

If is non-Lagrangian, , while

-

(b)

If is multiply-Lagrangian

-

(c)

Otherwise, if is singly-Lagrangian, is the unique nonempty member of . Specifically, and being as in Proposition 8.1

if , , while is or according as or if , is , or according as , or

When ,attained at , where uniquely solves .

When ,attained at , where .

When ,attained at , where .

Proof.

The result follows from detailed, straightforward application of the auxiliary results of Section 8.2, noting the following:

-

(a)

Here, as and while, by definition, .

-

(b)

Here, and , while .

-

(c)

Here, if , either so that , or so that , consistency of the constraint implying . In either case, . Again, is impossible, so that when, being continuous and strictly increasing, has a unique solution.

∎

Corollary 8.1.

Let be a canonical form whose dimension-reduced form is regular. Then:

-

(1)

has a unique solution whenever does.

-

(2)

does not have a unique solution if, and only if, it is singly-Lagrangian and either:

-

(a)

, when its solutions are unique up to the sign of ; or:

-

(b)

, when its solutions are unique up to the sign of ,

in which cases solutions to are unique up to orthogonal indeterminacy of (a) or (b) respectively.

-

(a)

Proof.

Theorem 8.1 and its Corollary 8.1 complete our primary objective, providing the minimised objective function and solution set of any regular dimension-reduced and so, via Theorem 7.1, of any initial canonical form .

Two worked examples of this overall approach are given in [5].

9 Intrinsic instability

The above analysis of any, equality or inequality constrained, problem rests on several partitions of possibilities. Passage between different members of a partition can involve movement between equality and inequality of the same two reals. Or, again, between weak () and strict () versions of the same inequality. As a result, both the form of the solution set and, indeed, of the problem itself can be intrinsically unstable under arbitrarily small perturbations of problem parameters. Whether or not the solution set varies continuously with across such partition boundaries is implicit in the above analysis. In particular, in its summative Theorems 4.1, 5.1, 7.1 and 8.1, and their key Corollaries 7.1 and 8.1. The discontinuities involved can be dramatic, as the following instances illustrate.

Potential synergetic uses of these analytical insights in connection with efficient numerical optimisation methods are noted in the closing discussion (Section 10).

9.1 Instability of the form of the solution set

We begin with a marked instance of the passage from non-unique to unique solutions. As in Example 7.1, consider minimisation of the distance to a sphere from its centre, whose solution set is, of course, the sphere itself. Changing this to minimising the same distance from any other point, the solution suddenly becomes unique. This instability corresponds to the passage from to in Corollary 8.1.

In the hyperbolic case, there can be extreme directional instability, due to the orthogonality of the eigenspaces of and . For instance, consider minimisation of the distance from the origin to the hyperbola , both of whose eigenvalues, , are simple. When , this comprises the lines which meet at the (repeated) solution , while is multiply-Lagrangian. Otherwise, it comprises two branches with these lines as asymptotes, being singly-Lagrangian. For , these branches meet the –axis at the twin solutions while, for , they meet the –axis at the twin solutions . Thus, no matter how small we take , the twin solutions for are always orthogonal to those for . In terms of Theorem 8.1, the solution set changes from to via as goes from positive to negative via zero.

Geometrically, it is clear that this same extreme directional instability can arise in the elliptic case. Consider, for example, minimising the distance from the origin to the ellipse so that, when , the solution set is the ellipse itself. Then, with , no matter how close we take and to – and so, to each other – the solution set for is while, for , it remains in the directions orthogonal to these.

9.2 Instability of the form of the problem

Intrinsic instability of the form of the problem comes, itself, in a variety of forms, as we illustrate.

As a first instance, consider the variant of Example 5.1(b) with constraint for given . Whereas the perfect solution here has for every , it has which tends to as and to as . Such instability holds generally. Indeed, Theorem 5.1 shows that, if admits an essentially perfect solution, it is intrinsically unstable under small constraint perturbations. And, relatedly, that the occurrence of essentially perfect solutions to is itself intrinsically unstable, depending as it does on the vanishing of the constraint parameter . Replacing by , the same is true of reducibility of when is singular. That is, when is positive semi-definite, there is intrinsic instability at the boundaries between the three possibilities – admits a perfect solution, admits an essentially perfect solution, or admits a projected, yet imperfect, reduced form – their occurrences being characterised in Theorem 5.1.

As a second instance, any positive semi-definite is arbitrarily close to a positive definite matrix , – for example, – analysis of the problem changing from that of Section 5 to that discussed in the sequel.

Similar intrinsic instabilities in problem form occur at the boundaries between members of the following partitions made for positive definite :

-

(i)

the four possible forms of constraint – elliptic, hyperbolic, or the partly parabolic variant of either – as detailed in Definition 7.1;

-

(ii)

in the dimension-reduced canonical form , whether it is regular or not – as detailed in Definition 7.2;

-

(iii)

the three possibilities – non-Lagrangian, multiply Lagrangian and singly Lagrangian – as detailed in Section 8.3.

10 Discussion

The current approach to the problem addressed in this paper, and the more generally applicable approach of generalised trust region (GTR) methods, broadly reviewed at the outset, may be compared as follows. Their intrinsic complementarity is evident and raises two substantial questions for future research.

Being derivative-based, the GTR approach is, intrinsically, local. A local optimum is identified implicitly, and then sought numerically, via simultaneous satisfaction of an appropriate set of conditions. These may include conditions additional to those of the problem itself (notably, those introduced to ensure numerical stability). Instances of the problem not satisfying such conditions require separate resolution. Under certain such additional constraint qualifications, it may be possible to characterise global optimality: see, for example, [23, 21, 25]. Unless a local optimum can be shown to be unique, identifying a global optimum requires repeated use of one or more algorithms. Of course, at most a finite number of local optima may be obtained in this way. The desired trade-off to be struck between the speed, accuracy and numerical stability of the overall computational procedure depends on context and purpose.

In contrast, the approach presented here is, intrinsically, global in three distinct senses: (a) it partitions all possible instances of the problem, and of its solution set, without exception; (b) its simplifying transformations are applied to the whole space; and: (c) its solution sets comprise global optima only. These sets are specified explicitly in closed algebraic form, affording both insight and interpretation. In particular, it is shown that, depending on precisely defined circumstances, there may be 0, 1, 2, or more – indeed, uncountably many – global optima, geometry illuminating when each possibility occurs. Overall, the current global, analytic approach throws a distinctive algebraic and geometric spotlight on the diverse nature of different instances of both problem and solution set; and, on the possibility of intrinsic instability of both, pinpointing precisely when this occurs: specifically, when passage between its different partition members involve distinctions that cannot be drawn in the floating-point world, yet lead to radical changes in the form of either the solution set, or of problem itself.

Two substantial questions arise at once:

-

1.

can the current global, analytic approach be extended to accommodate possible non-convexity of the objective function?

-

2.

can the intrinsic complementarity it shares with the local, computational GTR approach be exploited, releasing potential synergies between them?

Motivations for examining these questions in future work, and first pointers towards possible answers, are briefly offered in closing.

Concerning (1), broadening the applicability of the current approach in this way would bring it closer to that of GTR methods. One natural strategy here would work with affine transformations such that the partitioned least-squares form of is replaced by , for some affine invariants , with .

Concerning (2), generic motivation here comes from seeking to capitalise on the distinctive advantages of both approaches: the former providing, in principle, global solution sets that are complete, exact, insightful and interpretable; the latter providing, in practice, algorithms whose specification and deployment can be varied to deliver a balance of speed, accuracy and numerical stability well-suited to a given context and purpose. Especially strong when the present problem arises as one iteration of a general purpose optimisation procedure, specific motivation here includes the need to handle the possibility of various forms of intrinsic – not just numerical – instability highlighted by the present global analysis and illustrated in Section 9: among these, the possibility of undetectably small changes leading to solutions in orthogonal directions is particularly striking (see Section 9.1). One natural strategy here would be to modify existing computational procedures so that, when numerical checks informed by global analysis indicate its appropriateness, multiple forms of problem or solution set are entertained. This strategy has the potential advantage of identifying several, quite different, locally-promising search directions at each iteration.

Concerning both, it will be of interest to see how far, and by what means, progress can best be made in addressing these challenging, open questions.

References

- [1] S. Adachi, S. Iwata, Y. Nakatsukasa, and A. Takeda. Solving the trust region subproblem by a generalized eigenvalue problem. Mathematical Engeneering Technical Report, University of Tokyo, 2015-14, 2015.

- [2] C. J. Albers, F. Critchley, and J. C. Gower. Explicit minimisation of a convex quadratic under a general quadratic constraint. Technical Report 08/03, Department of Statistics, The Open University, (2008), 2008.

- [3] C. J. Albers, F. Critchley, and J. C. Gower. Applications of quadratic minimisation problems in statistics. Journal of Multivariate Analysis, 102(3):714 – 722, 2011.

- [4] C. J. Albers, F. Critchley, and J. C. Gower. Quadratic minimisation problems in statistics. Journal of Multivariate Analysis, 102(3):698 – 713, 2011.

- [5] C. J. Albers, F. Critchley, and J. C. Gower. Two worked examples for ‘explicit minimisation of a convex quadratic under a general quadratic constraint: a general, analytic approach’. Included as Appendix A in this arXiv preprint, (2017), 2017.

- [6] C. J. Albers and John C. Gower. A general approach to handling missing values in procrustes analysis. Advances in Data Analysis and Classification, 4(4):223–237, 2010.

- [7] C. J. Albers and John C. Gower. Canonical analysis: Ranks, ratios and fits. Journal of Classification, 31(1):2–27, 2014.

- [8] A. Ben-Tal and D. den Hertog. Hidden conic quadratic representation of some nonconvex quadratic optimization problems. Mathematical Programming, 143(1):1–29, 2013.

- [9] A. R. Conn, N. I. M. Gould, and P. L. Toint. Trust Region Methods. Society for Industrial and Applied Mathematics, 2000.

- [10] F. Critchley. On the minimisation of a positive definite quadratic form under a quadratic constraint: analytical solution and statistical applications. Statistics Research Report 165, Department of Statistics, University of Warwick, 1989.

- [11] L. Eldén. A weighted pseudoinverse, generalized singular values, and constrained least squares problems. BIT Numerical Mathematics, 22(4):487–502, 1982.

- [12] L. Eldén. Algorithms for the computation of functionals defined on the solution of a discrete ill-posed problem. BIT Numerical Mathematics, 30(3):466–483, 1990.

- [13] L. Eldén. Solving quadratically constrained least squares problems using a differential-geometric approach. BIT Numerical Mathematics, 42(2):323–335, 2002.

- [14] F. Flores-Bazán and G. Cárcamo. A geometric characterization of strong duality in nonconvex quadratic programming with linear and nonconvex quadratic constraints. Mathematical Programming, 145(1):263–290, 2013.

- [15] W. Gander. Least squares with a quadratic constraint. Numerische Mathematik, 36(3):291–307, 1980.

- [16] W. Gander, G. H. Golub, and U. von Matt. Special issue dedicated to alan j. hoffman a constrained eigenvalue problem. Linear Algebra and its Applications, 114–115:815–839, 1989.

- [17] J. C. Gower and G. B. Dijksterhuis. Procrustes Problems. Number 30 in Oxford Statistical Science Series. Oxford University Press, 2004.

- [18] R. Jiang, D. Li, and B. Wu. SOCP reformulation for the generalized trust region subproblem via a canonical form of two symmetric matrices. arXiv preprints, 1602.07819v1, 2016.

- [19] Rujun Jiang and Duan Li. Simultaneous diagonalization of matrices and its application in quadratic constrained quadratic programming. arXiv preprint arXiv:1507.05703, 2015.

- [20] M. Locatelli. Some results for quadratic problems with one or two quadratic constraints. Operations Research Letters, 43(2):126 – 131, 2015.

- [21] Jorge J. Moré. Generalizations of the trust region problem. Optimization Methods and Software, 2(3-4):189–209, 1993.

- [22] R. W. Newcomb. On the simultaneous diagonalization of two semidefinite matrices. Quarterly Journal of Applied Mathematics, 19:144–146, 1960.

- [23] T. K. Pong and H. Wolkowicz. The generalized trust region problem. Computational Optimization and Applications, 58:273–322, 2014.

- [24] D. C. Sorensen. Newton’s method with a model trust region modification. SIAM Journal on Numerical Analysis, 19(2):409–426, 1982.

- [25] R. Stern and H. Wolkowicz. Indefinite trust region subproblems and nonsymmetric eigenvalue perturbations. SIAM Journal of Optimization, 5:286–313, 1995.

- [26] H. Tuy and N. T. Hoai-Phuong. A robust algorithm for quadratic optimization under quadratic constraints. Journal of Global Optimization, 37(4):557–569, 2007.

- [27] V. V. Jeyakumar and G. Y. Li. Robust solutions of quadratic optimization over single quadratic constraint under interval uncertainty. Journal of Global Optimization, 55(2):209–226, 2012.

- [28] S. Wang and Y. Xia. Strong duality for generalized trust region subproblem: S-lemma with interval bounds. Optimization Letters, 9:1063–1073, 2015.

- [29] Y. Xia, S. Wang, and R.-L. Sheu. S-lemma with equality and its applications. Mathematical Programming, 156(1):513–547, 2015.

- [30] W. Xing, S-C. Fangand R-L. SheuLin, and L. Zhang. Canonical dual solutions to quadratic optimization over one quadratic constraint. Asia-Pacific Journal of Operational Research, 32(01):1540007, 2015.

Appendix A Two worked examples

We provide with two worked examples and a short conclusion. The examples differ only by a single element of , yet involve completely different approaches to their solution. As such, they illustrate one of the intrinsic instabilities noted in Section 9. Namely, that at the boundary between where Section 5 applies, and where Sections 6 to 8 pertain.

Whereas this generic type of instability can of course arise whatever the scale of the problem, to make things explicit, we work here with and with values of for which exact calculations are fairly straightforward. Specifically, we take , , , and

so that , while for all . While reporting exact results, we also indicate where there is – or is not – numerical uncertainty, especially concerning which member of a partition of possibilities the problem on hand belongs to.

Examples A.1 and A.2 concern and respectively. In the first case, one of the computed eigenvalues of will be within machine accuracy of zero; in the second, all will be clearly positive. As , both problem forms will be flagged up. Numerically, is clearly positive definite.

Example A.1.

Here, clearly has rank , and we follow the approach of Section 5.

Analysis begins with a three-stage transformation: first, to centred least-squares form, as in part (i) of Theorem 3.1; second, to simplified form, via (5) of Lemma 5.2; and third, to simultaneous diagonal form, via the further linear transformation of Remark 5.2. Overall, this transformation is where

inducing with and . These two components of are known (and so do not require calculation), as is the diagonal nature of . To within machine accuracy, , and .

Next, we apply Theorem 5.1 to , dropping the subscript where notationally convenient. Identifying terms in Definitions 5.2 and 5.3 for this transformed member of , and noting that the third diagonal element is clearly positive, we have , so that , while . In particular, , so that part (ii) of Theorem 5.1 applies. Moreover, to within machine accuracy, and , so that admits perfect solution , .

Finally, invoking Theorem 2.1, we transform back to conclude that has perfect solution , .

Example A.2.

Here, clearly has full rank, and we follow Sections 6 to 8.

Analysis begins with a two-stage transformation: first, to centred – here, full – least-squares form, using again Theorem 3.1(i); second, to canonical form, via the Euclidean transformation of Theorem 6.2. Overall, apart from a constant, this transformation is where

inducing in which is and is diagonal. To within machine accuracy, , which clearly has distinct, positive, eigenvalues. Accordingly, is, itself, dimension-reduced and regular. Finally, in the notation of Definition 6.1, we compute that and .

We solve the regular dimension-reduced canonical form via the steps described in Section 8. Since, clearly, and , is singly-Lagrangian. Here, , the function as given in Definition 8.2 taking the form:

| (14) |

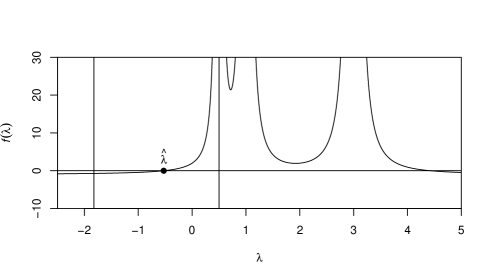

Again, it is numerically clear that and so that, by Proposition 8.1, and . Accordingly (Proposition 8.2), where is the unique root of . Albers et al [4] show how to reduce to a finite interval , , containing . Here, . This is visualised in Figure 1, where the functional form (14) is plotted over an interval containing , its two vertical lines being at and , while there are vertical asymptotes at , . Numerical solution over – for example, by the bisection method – is straightforward, yielding here the approximate value .

Finally, substituting in the relevant part of Theorem 8.1(c), and back transforming , yields the final solution , .