Abstract.

Building on insights of Jovanovic (1982) and subsequent authors, we develop a comprehensive theory of optimal timing of decisions based around continuation value functions and operators that act on them. Optimality results are provided under general settings, with bounded or unbounded reward functions. This approach has several intrinsic advantages that we exploit in developing the theory. One is that continuation value functions are smoother than value functions, allowing for sharper analysis of optimal policies and more efficient computation. Another is that, for a range of problems, the continuation value function exists in a lower dimensional space than the value function, mitigating the curse of dimensionality. In one typical experiment, this reduces the computation time from over a week to less than three minutes.

Keywords: Continuation values, dynamic programming, optimal timing

Optimal Timing of Decisions: A General Theory Based on Continuation

Values111 Financial support from Australian Research

Council Discovery Grant DP120100321 is gratefully acknowledged.

Email addresses: qingyin.ma@anu.edu.au, john.stachurski@anu.edu.au

Qingyin Maa and John Stachurskib

a, bResearch School of Economics, Australian National

University

1. Introduction

A large variety of decision making problems involve choosing when to act in the face of risk and uncertainty. Examples include deciding if or when to accept a job offer, exit or enter a market, default on a loan, bring a new product to market, exploit some new technology or business opportunity, or exercise a real or financial option. See, for example, McCall (1970), Jovanovic (1982), Hopenhayn (1992), Dixit and Pindyck (1994), Ericson and Pakes (1995), Peskir and Shiryaev (2006), Arellano (2008), Perla and Tonetti (2014), and Fajgelbaum et al. (2015).

The most general and robust techniques for solving these kinds of problems revolve around the theory of dynamic programming. The standard machinery centers on the Bellman equation, which identifies current value in terms of a trade off between current rewards and the discounted value of future states. The Bellman equation is traditionally solved by framing the solution as a fixed point of the Bellman operator. Standard references include Bellman (1969) and Stokey et al. (1989). Applications of these methods to optimal timing include Dixit and Pindyck (1994), Albuquerque and Hopenhayn (2004), Crawford and Shum (2005), Ljungqvist and Sargent (2012), and Fajgelbaum et al. (2015).

Interestingly, over the past few decades, economists have initiated development of an alternative method, based around continuation values, that is both essentially parallel to the traditional method described above and yet significantly different in certain asymmetric ways (described in detail below).

Perhaps the earliest technically sophisticated analysis based around operations in continuation value function space is Jovanovic (1982). In an incumbent firm’s exit decision context, Jovanovic proposes an operator that is a contraction mapping on the space of bounded continuous functions, and shows that the unique fixed point of the operator coincides with the value of staying in the industry for the current period and then behave optimally. Intuitively, this value can be understood as the continuation value of the firm, since the firm gives up the choice to terminate the sequential decision process (exit the industry) in the current period.

Other papers in a similar vein include Burdett and Vishwanath (1988), Gomes et al. (2001), Ljungqvist and Sargent (2008), Lise (2013), Dunne et al. (2013), Moscarini and Postel-Vinay (2013), and Menzio and Trachter (2015). All of the results found in these papers are tied to particular applications, and many are applied rather than technical in nature.

It is not difficult to understand why economists often focus on continuation values as a function of the state rather than traditional value functions. One is economic intuition. In a given context it might be more natural or intuitive to frame a decision problem in terms of the continuation values faced by an agent. For example, in a job search context, one of the key questions is how the reservation wage, the wage at which the agent is indifferent between accepting and rejecting an offer, changes with economic environments. Obviously, the continuation value, the value of rejecting the current offer, has closer connection to the reservation wage than the value function, the maximum value of accepting and rejecting the offer.

There are, however, deeper reasons why a focus on continuation values can be highly fruitful. To illustrate, recall that, for a given problem, the value function provides the value of optimally choosing to either act today or wait, given the current environment. The continuation value is the value associated with choosing to wait today and then reoptimize next period, again taking into account the current environment. One key asymmetry arising here is that, if one chooses to wait, then certain aspects of the current environment become irrelevant, and hence need not be considered as arguments to the continuation value function.

To give one example, consider a potential entrant to a market who must consider fixed costs of entry, the evolution of prices, their own productivity and so on. In some settings, certain aspects of the environment will be transitory, while others are persistent. (For example, in Fajgelbaum et al. (2015), prices and beliefs are persistent while fixed costs are transitory.) All relevant state components must be included in the value function, whether persistent or transitory, since all affect the choice of whether to enter or wait today. On the other hand, purely transitory components do not affect continuation values, since, in that scenario, the decision to wait has already been made.

Such asymmetries place the continuation value function in a lower dimensional space than the value function whenever they exist, thereby mitigating the curse of dimensionality. This matters from both an analytical and a computational perspective. On the analytical side, lower dimensionality can simplify challenging problems associated with, say, unbounded reward functions, continuity and differentiability arguments, parametric monotonicity results, etc. On the computational side, reduction of the state space by even one dimension can radically increase computational speed. For example, while solving a well known version of the job search model in section 5.1, the continuation value based approach takes only 171 seconds to compute the optimal policy to a given level of precision, as opposed to more than 7 days for the traditional value function based approach.

One might imagine that this difference in dimensionality between the two approaches could, in some circumstances, work in the other direction, with the value function existing in a strictly lower dimensional space than the continuation value function. In fact this is not possible. As will be clear from the discussion below, for any decision problem in the broad class that we consider, the dimensionality of the value function is always at least as large.

Another asymmetry between value functions and continuation value functions is that the latter are typically smoother. For example, in a job search problem, the value function is usually kinked at the reservation wage. However, the continuation value function can be smooth. More generally, continuation value functions are lent smoothness by stochastic transitions, since integration is a smoothing operation. Like lower dimensionality, increased smoothness helps on both the analytical and the computational side. On the computational side, smoother functions are easier to approximate. On the analytical side, greater smoothness lends itself to sharper results based on derivatives, as elaborated on below.

To summarize the discussion above, economists have pioneered the continuation value function based approach to optimal timing of decisions. This has been driven by researchers correctly surmising that such an approach will yield tighter intuition and sharper analysis than the traditional approach in many modeling problems. However, all of the analysis to date has been in the context of specific, individual applications. This fosters unnecessary replication, inhibits applied researchers seeking off-the-shelf results, and also hides deeper advantages.

In this paper we undertake a systematic study of optimal timing of decisions based around continuation value functions and the operators that act on them. The theory we develop accommodates both bounded rewards and the kinds of unbounded rewards routinely encountered in modeling economic decisions.222 For example, many applications include Markov state processes (possibly with unit roots), driving the state space and various common reward functions (e.g., CRRA, CARA and log returns) unbounded (see, e.g, Low et al. (2010), Bagger et al. (2014), Kellogg (2014)). Moreover, many search-theoretic studies model agent’s learning behavior (see, e.g., Burdett and Vishwanath (1988), Mitchell (2000), Crawford and Shum (2005), Nagypál (2007), Timoshenko (2015)). To have favorable prior-posterior structure (e.g., both follow normal distributions), unbounded state spaces and rewards are usually required. We show that most of these problems can be handled without difficulty. In fact, within the context of optimal timing, the assumptions placed on the primitives in the theory we develop are weaker than those found in existing work framed in terms of the traditional approach to dynamic programming, as discussed below.

We also exploit the asymmetries between traditional and continuation value function based approaches to provide a detailed set of continuity, monotonicity and differentiability results. For example, we use the relative smoothness of the continuation value function to state conditions under which so-called “threshold policies” (i.e., policies where action occurs whenever a reservation threshold is crossed) are continuously differentiable with respect to features of the economic environment, as well as to derive expressions for the derivative.

Since we explicitly treat unbounded problems, our work also contributes to ongoing research on dynamic programming with unbounded rewards. One general approach tackles unbounded rewards via the weighted supremum norm. The underlying idea is to introduce a weighted norm in a certain space of candidate functions, and then establish the contraction property for the relevant operator. This theory was pioneered by Boyd (1990) and has been used in numerous other studies of unbounded dynamic programming. Examples include Becker and Boyd (1997), Alvarez and Stokey (1998), Durán (2000, 2003) and Le Van and Vailakis (2005).

Another line of research treats unboundedness via the local contraction approach, which constructs a local contraction based on a suitable sequence of increasing compact subsets. See, e.g., Rincón-Zapatero and Rodríguez-Palmero (2003), Rincón-Zapatero and Rodríguez-Palmero (2009), Martins-da Rocha and Vailakis (2010) and Matkowski and Nowak (2011). One motivation of this line of work is to deal with dynamic programming problems that are unbounded both above and below.

So far, existing theories of unbounded dynamic programming have been confined to optimal growth problems. Rather less attention, however, has been paid to the study of optimal timing of decisions. Indeed, applied studies of unbounded problems in this field still rely on theorem 9.12 of Stokey et al. (1989) (see, e.g., Poschke (2010), Chatterjee and Rossi-Hansberg (2012)). Since the assumptions of this theorem are not based on model primitives, it is hard to verify in applications. Even if they are applicable to some specialized setups, the contraction mapping structure is unavailable. A recent study of unbounded problem via contraction mapping is Kellogg (2014). However, he focuses on a highly specialized decision problem with linear rewards. Since there is no general unbounded dynamic programming theory in this field, we attempt to fill this gap.

Notably, the local contraction approach exploits the underlying structure of the technological correspondence related to the state process, which, in optimal growth models, provides natural bounds on the growth rate of the state process, thus a suitable selection of a sequence of compact subsets to construct local contractions. However, such structures are missing in most sequential decision settings we study, making the local contraction approach inapplicable.

In response to that, we come back to the idea of weighted supremum norm, which turns out to interact well with the sequential decision structure we explore. To obtain an appropriate weight function, we introduce an innovative idea centered on dominating the future transitions of the reward functions, which renders the classical weighted supremum norm theory of Boyd (1990) as a special case, and leads to simple sufficient conditions that are straightforward to check in applications.

The intuitions of our theory are twofold. First, when the underlying state process is mean-reverting, the effect of initial conditions tends to die out as time iterates forward, making the conditional expectations of the reward functions flatter than the original rewards. Second, in a wide range of applications, a subset of states are conditionally independent of the future states, so the conditional expectation of the payoff functions is actually defined on a space that is lower dimensional than the state space.333 Technically, this also accounts for the lower dimensionality of the continuation value function than the value function, as documented above. Section 4 provides a detailed discussion. In each scenario, finding an appropriate weight function becomes an easier job.

The paper is structured as follows. Section 2 outlines the method and provides the basic optimality results. Section 3 discusses the properties of the continuation value function, such as monotonicity and differentiability. Section 4 explores the connections between the continuation value and the optimal policy. Section 5 provides a list of economic applications and compares the computational efficiency of the continuation value approach and traditional approach. Section 6 provides extensions and section 7 concludes. Proofs are deferred to the appendix.

2. Optimality Results

This section studies the optimality results. Prior to this task, we introduce some mathematical techniques used in this paper.

2.1. Preliminaries

For real numbers and let . If and are functions, then . If is a measurable space, then is the set of -measurable bounded functions from to , with norm . Given a function , the -weighted supremum norm of is

If , we say that is -bounded. The symbol will denote the set of all functions from to that are both -measurable and -bounded. The pair forms a Banach space (see e.g., Boyd (1990), page 331).

A stochastic kernel on is a map such that is -measurable for each and is a probability measure for each . We understand as the probability of a state transition from to in one step. Throughout, we let and . For all , is the probability of a state transition from to in steps. Given a -measurable function , let

where . When is a Borel subset of , a stochastic density kernel (or density kernel) on is a measurable map such that for all . We say that the stochastic kernel has a density representation if there exists a density kernel such that

2.2. Set Up

Let be a time-homogeneous Markov process defined on probability space and taking values in measurable space . Let denote the corresponding stochastic kernel. Let be a filtration contained in such that is adapted to . Let indicate probability conditioned on , while is expectation conditioned on the same event. In proofs we take to be the canonical sequence space, so that and is the product -algebra generated by .444 For the formal construction of on given and see theorem 3.4.1 of Meyn and Tweedie (2012) or section 8.2 of Stokey et al. (1989).

A random variable taking values in is called a (finite) stopping time with respect to the filtration if and for all . Below, has the interpretation of choosing to act at time . Let denote the set of all stopping times on with respect to the filtration .

Let and be measurable functions, referred to below as the exit payoff and flow continuation payoff, respectively. Consider a decision problem where, at each time , an agent observes and chooses between stopping (e.g., accepting a job, exiting a market, exercising an option) and continuing to the next stage. Stopping generates final payoff . Continuing involves a continuation payoff and transition to the next period, where the agent observes and the process repeats. Future payoffs are discounted at rate .

Let be the value function, which is defined at by

| (1) |

A stopping time is called an optimal stopping time if it attains the supremum in (1). A policy is a map from to , with indicating the decision to continue and indicating the decision to stop. A policy is called an optimal policy if defined by is an optimal stopping time.

To guarantee existence of the value function and related properties without insisting that payoff functions are bounded, we adopt the next assumption:

Assumption 2.1.

There exist a -measurable function and constants , such that , and, for all ,

| (2) |

and

| (3) |

Note that by definition, condition (2) reduces to when . The interpretation of assumption 2.1 is that both and are small relative to some function such that does not grow too quickly. Slow growth in is imposed by (3), which can be understood as a geometric drift condition (see, e.g., Meyn and Tweedie (2012), chapter 15).

Remark 2.1.

Remark 2.2.

Example 2.1.

Consider first an example with bounded rewards. Suppose, as in McCall (1970), that a worker can either accept a current wage offer and work permanently at that wage, or reject the offer, receive unemployment compensation and reconsider next period. Let the current wage offer be a function of some idiosyncratic or aggregate state process . The exit payoff is , where is a utility function and is the discount factor. The flow continuation payoff is . If is bounded, then we can set , and assumption 2.1 is satisfied with , and .

Example 2.2.

Consider now Markov state dynamics in a job search framework (see, e.g., Lucas and Prescott (1974), Jovanovic (1987), Bull and Jovanovic (1988), Gomes et al. (2001), Cooper et al. (2007), Ljungqvist and Sargent (2008), Kambourov and Manovskii (2009), Robin (2011), Moscarini and Postel-Vinay (2013), Bagger et al. (2014)). Consider the same setting as example 2.1, with state process

| (4) |

The state space is . We consider a typical unbounded problem and provide its proof in appendix B. Let and the utility of the agent be defined by the CRRA form

| (5) |

Case I: and . If , then we can select an that satisfies , where . In this case, assumption 2.1 holds for and . Indeed, if , then assumption 2.1 holds (with ) for all .

Case II: . If , then assumption 2.1 holds with , , and . Notably, since is not excluded, wages can be nonstationary provided that they do not grow too fast.

Remark 2.3.

Assumption 2.1 is weaker than the assumptions of existing theory. Consider the local contraction method of Rincón-Zapatero and Rodríguez-Palmero (2003). The essence is to find a countable increasing sequence of compact subsets, denoted by , such that . Let be the technological correspondence of the state process giving the set of feasible actions. To construct local contractions, one need or with probability one for all (see, e.g., theorems 3–4 of Rincón-Zapatero and Rodríguez-Palmero (2003), or assumptions D1–D2 of Matkowski and Nowak (2011)). This assumption is often violated when has unbounded supports. In example 2.2, since the AR state process (4) travels intertemporally through with positive probability, the local contraction method breaks down.

Remark 2.4.

The use of -step transitions in assumption 2.1-(2) has certain advantages. For example, if is mean-reverting, as time iterates forward, the initial effect tends to die out, making the conditional expectations and flatter than the original payoffs. As a result, finding an appropriate -function with geometric drift property is much easier. Typically, in Case I of example 2.2, if , without using future transitions (i.e., is imposed),555 Indeed, our assumption in this case reduces to the standard weighted supnorm assumption. See, e.g., section 4 of Boyd (1990), or assumptions 1-4 of Durán (2003). one need further assumptions such as (see appendix B), which puts nontrivial restrictions on the key parameters and . Using -step transitions, however, such restrictions are completely removed.

Example 2.3.

Consider now agent’s learning in a job search framework (see, e.g., McCall (1970), Chalkley (1984), Burdett and Vishwanath (1988), Pries and Rogerson (2005), Nagypál (2007), Ljungqvist and Sargent (2012)). We follow McCall (1970) (section IV) and explore how the reservation wage changes in response to the agent’s expectation of the mean and variance of the (unknown) wage offer distribution. Each period, the agent observes an offer and decides whether to accept it or remain unemployed. The wage process follows

| (6) |

where is the mean of the wage process, which is not observed by the worker, who has prior belief .666 In general, can be a stochastic process, e.g., , . We consider such an extension in a firm entry framework in section 5.3. The worker’s current estimate of the next period wage distribution is . After observing , the belief is updated, with posterior , where

| (7) |

Let the utility of the worker be defined by (5). If he accepts the offer, the search process terminates and a utility is obtained in each future period. Otherwise, the worker gets compensation , updates his belief next period, and reconsiders. The state vector is . For any integrable function , the stochastic kernel satisfies

| (8) |

where and are defined by (7). The exit payoff is , and the flow continuation payoff is . If and , assumption 2.1 holds by letting , , and . If , assumption 2.1 holds with , , and . See appendix B for a detailed proof.

Remark 2.5.

Since in example 2.3, the wage process is independent and has unbounded support , the local contraction method cannot be applied.

Remark 2.6.

From (8) we know that the conditional expectation of the reward functions in example 2.3 is defined on a space of lower dimension than the state space. Although there are 3 states, is a function of only 2 arguments: and . Hence, taking conditional expectation makes it easier to find an appropriate function. Indeed, if the standard weighted supnorm method were applied, one need to find a with geometric drift property that dominates (see, e.g., section 4 of Boyd (1990), or, assumptions 1–4 of Durán (2003)), which is more challenging due to the higher state dimension. This type of problem is pervasive in economics. Sections 4–5 provide a systematic study, along with a list of applications.

2.3. The Continuation Value Operator

The continuation value function associated with the sequential decision problem (1) is defined at by

| (9) |

Under assumption 2.1, the value function is a solution to the Bellman equation, i.e., . To see this, by theorem 1.11 of Peskir and Shiryaev (2006), it suffices to show that

for all . This obviously holds since

with probability one, and by lemma 7.1 (see (Proof.) in appendix A), the right hand side is -integrable for all .

To obtain some fundamental optimality results concerning the continuation value function, define an operator by

| (10) |

We call the Jovanovic operator or the continuation value operator. As shown below, fixed points of are continuation value functions. From them we can derive value functions, optimal policies and so on. To begin with, recall , and defined in assumption 2.1. Let such that , and . Let the weight function be

| (11) |

We have the following optimality result.

Theorem 2.1.

Under assumption 2.1, the following statements are true:

-

1.

is a contraction mapping on of modulus .

-

2.

The unique fixed point of in is .

-

3.

The policy defined by is an optimal policy.

Remark 2.7.

Example 2.4.

Recall the job search problem of example 2.2. Let and be defined as in that example. Define as in (11). The Jovanovic operator is

Since assumption 2.1 holds, theorem 2.1 implies that has a unique fixed point in that coincides with the continuation value function, which, in this case, can be interpreted as the expected value of unemployment.

Example 2.5.

Example 2.6.

Consider an infinite-horizon American option (see, e.g., Shiryaev (1999) or Duffie (2010)). Let the state process be as in (4) so that the state space . Let be the current price of the underlying asset, and be the riskless rate of return (i.e., ). The exit payoff for a call option with a strike price is , while the flow continuation payoff is . The Jovanovic operator for the option satisfies

If , we can let and such that , then assumption 2.1 holds with and . Moreover, if , then assumption 2.1 holds (with ) for all . For as defined by (11), theorem 2.1 implies that admits a unique fixed point in that coincides with , the expected value of retaining the option and exercising at a later stage. The proof is similar to that of example 2.2 and thus omitted.

Example 2.7.

Firm’s RD decisions are often modeled as a sequential search process for better technologies (see, e.g., Jovanovic and Rob (1989), Bental and Peled (1996), Perla and Tonetti (2014)). In each period, an idea with value is observed, and the firm decides whether to put this idea into productive use, or develop it further by investing in RD. The former choice gives a payoff . The latter incurs a fixed cost so as to create a new technology. Let the RD process be governed by the exponential law of motion (with rate ),

| (13) |

While the payoff functions are unbounded, assumption 2.1 is satisfied with , , and . The Jovanovic operator satisfies

With as in (11), is a contraction mapping on with unique fixed point , the expected value of investing in RD. The proof is straightforward and omitted.

Example 2.8.

Consider a firm exit problem (see, e.g., Hopenhayn (1992), Ericson and Pakes (1995), Albuquerque and Hopenhayn (2004), Asplund and Nocke (2006), Poschke (2010), Dinlersoz and Yorukoglu (2012), Coşar et al. (2016)). Each period, a productivity shock is observed by an incumbent firm, where , and the state process is defined by (4). The firm then decides whether to exit the market next period or not (before observing ). A fixed cost is paid each period by the incumbent firm. The firm’s output is , where and is labor demand. Given output and input prices and , the payoff functions are , where . The Jovanovic operator satisfies

For , choose such that , where . Then assumption 2.1 holds with and . Moreover, if , then assumption 2.1 holds (with ) for all . The case is similar. By theorem 2.1, admits a unique fixed point in that corresponds to , the expected value of staying in the industry next period.777 The proof is similar to that of example 2.2. Here we are considering the case and separately. Alternatively, we can treat directly as in examples 2.2 and 2.6. As shown in the proof of example 2.2, the former provides a simpler function when .

Example 2.9.

Consider agent’s learning in a firm exit framework (see, e.g., Jovanovic (1982), Pakes and Ericson (1998), Mitchell (2000), Timoshenko (2015)). Let be firm’s output, a cost function, and be the total cost, where the state process satisfies with denoting the firm type. Beginning each period, the firm observes and decides whether to exit the industry or not. The prior belief is , so the posterior after observing is , where and . Let be the maximal profit, and be the profit of other industries, where is price. Consider, for example, , and satisfies , . Let . Then the Jovanovic operator satisfies

where with and . If and for some constants , let and choose such that . Define such that .888 Implicitly, we are considering . The case is trivial. Then assumption 2.1 holds by letting , and . Hence, admits a unique fixed point in that equals , the value of staying in the industry.999 In fact, the same result holds for more general settings, e.g., for some .

3. Properties of Continuation Values

In this section we explore some further properties of the continuation value function. As one of the most significant results, is shown to be continuously differentiable under certain assumptions.

3.1. Continuity

We first develop a theory for the continuity of the fixed point.

Assumption 3.1.

The stochastic kernel satisfies the Feller property, i.e., maps bounded continuous functions into bounded continuous functions.

Assumption 3.2.

The functions , and are continuous.

Assumption 3.3.

The functions and are continuous.

The next result treats the special case when admits a density representation. The proof is similar to that of proposition 3.1, except that we use lemma 7.2 instead of the generalized Fatou’s lemma of Feinberg et al. (2014) to establish continuity in (43). In this way, notably, the continuity of is not necessary for the continuity of . The proof is omitted.

Corollary 3.1.

Remark 3.1.

By proposition 3.1, if the payoffs and are bounded, assumption 3.1 and the continuity of and are sufficient for the continuity of and . If in addition has a density representation , by corollary 3.1, the continuity of the flow payoff and (for all ) is sufficient for to be continuous.101010 Notice that in these cases, can be chosen as a constant, so assumption 3.3 holds naturally. Based on these, the continuity of and of example 2.1 can be established.

Remark 3.2.

If assumption 2.1 satisfies for and assumption 3.1 holds, then assumptions 3.2–3.3 are equivalent to: , , and are continuous.111111 When , , so for some constant . Since and are continuous, Feinberg et al. (2014) (theorem 1.1) implies that is continuous. The next claim in this remark can be proved similarly. If assumption 2.1 holds for and assumptions 3.1–3.2 are satisfied, then assumption 3.3 holds if and only if and are continuous.

Example 3.1.

Recall the job search model of examples 2.2 and 2.4. By corollary 3.1, and are continuous. Here is the proof. Assumption 2.1 holds, as was shown. has a density representation that is continuous in . Moreover, and are continuous. It remains to verify assumption 3.3.

Example 3.2.

Recall the adaptive search model of examples 2.3 and 2.5. Assumption 2.1 holds for , as already shown. Assumption 3.1 follows from (8) and lemma 7.2. Moreover, and are continuous. In the proof of example 2.3, we have shown that are continuous (see (39)–(41) in appendix B), where is defined by (40) and . Since when , assumptions 3.2–3.3 hold. By proposition 3.1, and are continuous.

Example 3.3.

Example 3.4.

Recall the RD decision problem of example 2.7. Assumption 2.1 holds for . For all bounded continuous function , lemma 7.2 shows that is continuous, so assumption 3.1 holds. Moreover, , and are continuous, and

implies that are continuous. Since when , assumptions 3.2–3.3 hold. By proposition 3.1, and are continuous.

Example 3.5.

Example 3.6.

Recall the firm exit model of example 2.9. Assumption 2.1 holds, as was shown. The flow continuation payoff since . Recall that , and for all integrable , we have

Since by definition is continuous in and is continuous in and , assumption 3.1 holds by lemma 7.2. Further, induction shows that for some constant and all ,

which is continuous in . If is continuous, then, by lemma 7.2 and induction (similarly as in example 3.3), is continuous for all . Moreover, is continuous and

which is continuous in . Hence, assumptions 3.2–3.3 hold. Proposition 3.1 then implies that and are continuous.

3.2. Monotonicity

We now study monotonicity under the following assumptions.

Assumption 3.4.

The flow continuation payoff is increasing (resp. decreasing).

Assumption 3.5.

The function is increasing (resp. decreasing) for all increasing (resp. decreasing) function .

Assumption 3.6.

The exit payoff is increasing (resp. decreasing).

Remark 3.3.

Proposition 3.2.

Proof of proposition 3.2.

Let (resp. ) be the set of increasing (resp. decreasing) functions in . Then (resp. ) is a closed subset of .131313 Let such that , then pointwise. Since is complete, . For all with , . The second term on the right side is nonpositive, . Taking limit supremum on both sides yields . Hence, and is a closed subset. The case is similar. To show that is increasing (resp. decreasing), it suffices to verify that (resp. ).141414 See, e.g., Stokey et al. (1989), corollary 1 of theorem 3.2. The assumptions of the proposition guarantee that this is the case. Since, in addition, is increasing (resp. decreasing) by assumption and , is increasing (resp. decreasing). ∎

Example 3.7.

Remark 3.4.

Example 3.8.

Example 3.9.

Recall the firm exit model of examples 2.9 and 3.6. The flow continuation payoff is increasing in and decreasing in . Since is not a function of , is decreasing in . If the exit payoff is decreasing in , then is decreasing in . If and is increasing in , since is stochastically increasing, is increasing in for all candidate that is increasing in . By proposition 3.2, and are increasing in . Recall that is increasing in . Since is stochastically increasing in , is decreasing in for all candidate that is decreasing in . By proposition 3.2, and are decreasing in .

3.3. Differentiability

Suppose . For , let be the -th dimension and the remaining dimensions of . A typical element takes form of . Let . Given and , let and be its closure.

Given , let and . For a density kernel , let and . Let , , and denote and .

Assumption 3.7.

exists for all and .

Assumption 3.8.

has a density representation , and, for :

-

(1)

exits for all ;

-

(2)

is continuous;

-

(3)

There are finite solutions of to (denoted by ), and, for all , there exist and a compact subset such that implies .

Remark 3.5.

When the state space is unbounded above and below, for example, a sufficient condition for assumption 3.8-(3) is: there are finite solutions of to , and, for all , implies .

Assumption 3.9.

is continuous, and, for and .

The following provides a general result for the differentiability of .

Proposition 3.3.

Proof of proposition 3.3.

3.4. Smoothness

Now we are ready to study smoothness (i.e., continuous differentiability), an essential property for numerical computation and characterizing optimal policies.

Assumption 3.10.

For and , the following conditions hold:

-

(1)

is continuous on ;

-

(2)

is continuous, and, is continuous on .

The next result provides sufficient conditions for smoothness.

Proof of proposition 3.4.

Since assumption 3.10 implies assumptions 3.7 and 3.9, by proposition 3.3, on . Since is continuous by assumption 3.10-(1), to show that is continuously differentiable, it remains to verify: is continuous on . Since for some ,

| (14) |

By assumptions 3.8 and 3.10-(2), the right side of (14) is continuous in , and is continuous. Lemma 7.2 then implies that is continuous, as was to be shown. ∎

Example 3.10.

Recall the job search model of example 2.2 (subsequently studied by examples 2.4, 3.1 and 3.7). For all , let . We can show that the following statements hold:

-

(a)

There are two solutions to ;

-

(b)

;

-

(c)

;

-

(d)

, ;

-

(e)

The four terms on both sides of (c) and (d) are continuous in ;

-

(f)

The integrations (w.r.t. ) of the two terms on the right side of (c) and (d) are continuous in .

Remark 3.5 and (a) imply that assumption 3.8-(3) holds. If , assumption 3.10-(2) holds by conditions (b), (c), (e), (f) and lemma 7.2. If and , based on (36) (appendix B), conditions (b) and (d)–(f), and lemma 7.2, we can show that assumption 3.10-(2) holds. The other assumptions of proposition 3.4 are easy to verify. Hence, is continuously differentiable.

Example 3.11.

Recall the option pricing problem of example 2.6 (subsequently studied by example 3.3 and remark 3.4). Through similar analysis as in example 3.10, we can show that is continuously differentiable.151515 This holds even if the exit payoff has a kink at . Hence, the differentiability of the exit payoff is not necessary for the smoothness of the continuation value.

Example 3.12.

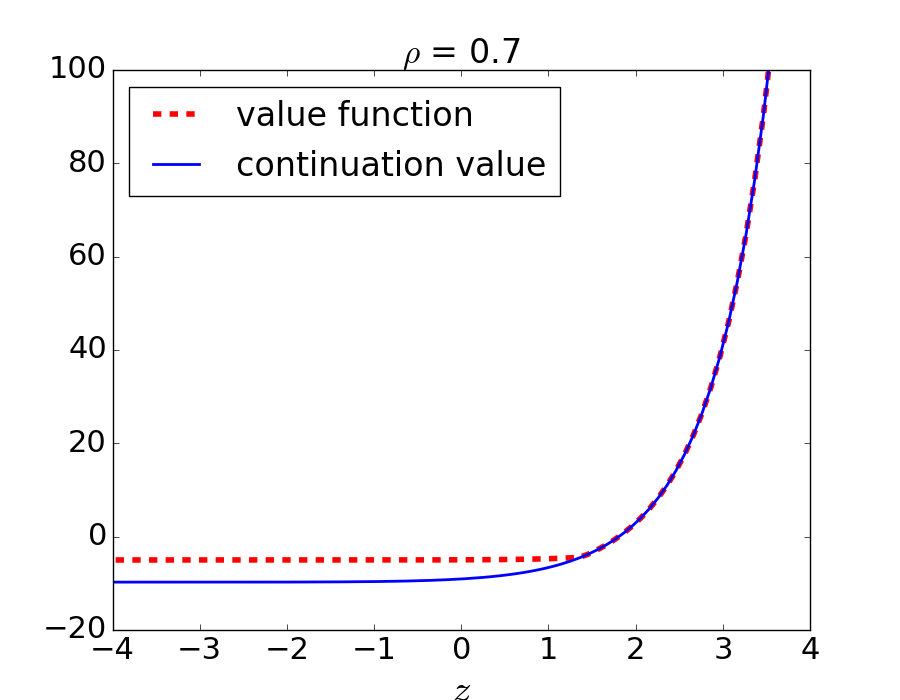

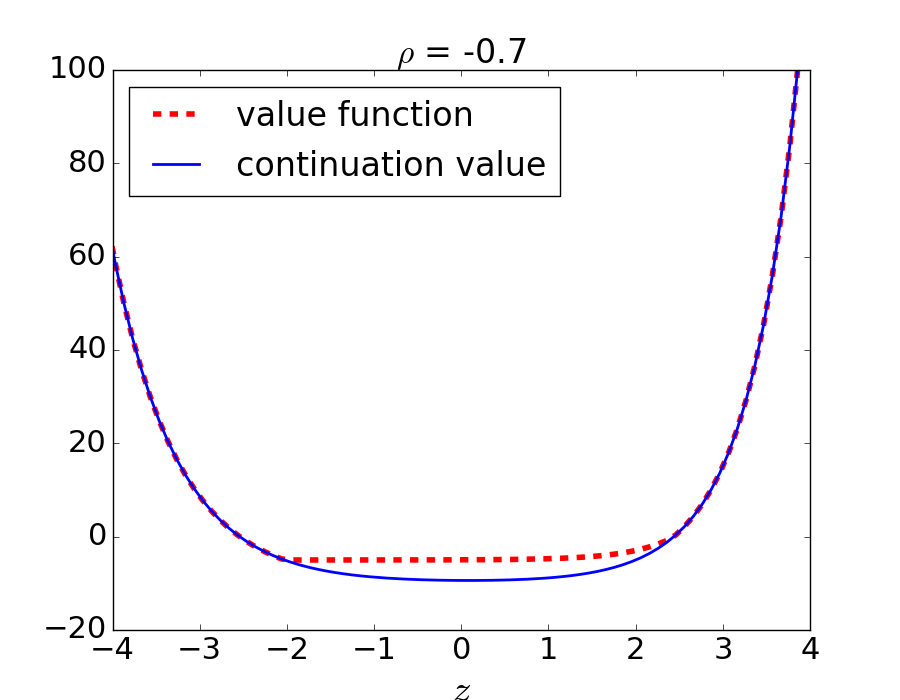

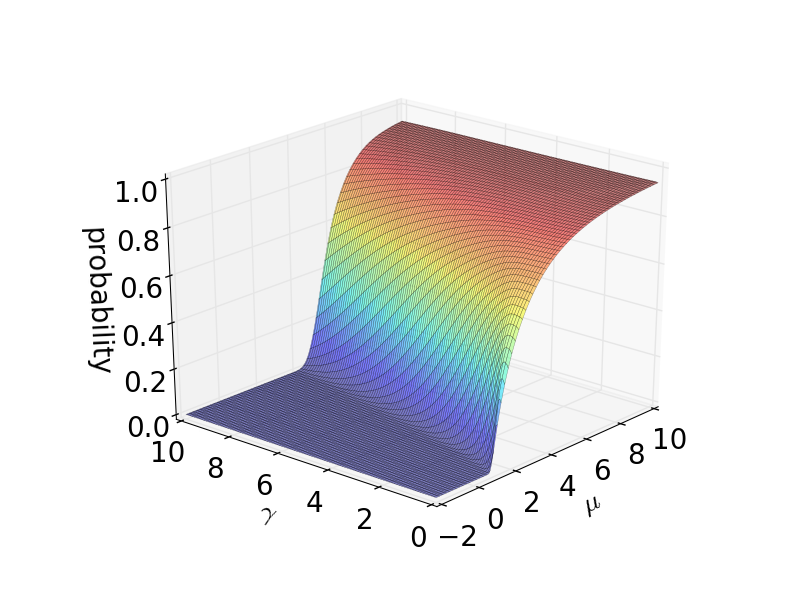

Recall the firm exit model of example 2.8 (subsequently studied by example 3.5 and remark 3.4). Through similar analysis to examples 3.10–3.11, we can show that is continuously differentiable. Figure 1 illustrates. We set , , , , , , , and consider respectively and . While is smooth, is kinked at around when , and has two kinks when .

3.5. Parametric Continuity

Consider the parameter space . Let , , and denote the stochastic kernel, exit and flow continuation payoffs, value and continuation value functions with respect to the parameter , respectively. Similarly, let , , and denote the key elements in assumption 2.1 with respect to . Define , and .

Assumption 3.11.

Assumption 2.1 holds at all , with and .

Under this assumption, let and such that , and . Consider defined by

where denotes the conditional expectation with respect to .

Remark 3.6.

We implicitly assume that does not include . However, by letting and , we can incorporate into . in assumption 3.11 is then replaced by . All the parametric continuity results of this paper remain true after this change.

Assumption 3.12.

satisfies the Feller property, i.e., is continuous for all bounded continuous function .

Assumption 3.13.

are continuous.

The following result is a simple extension of proposition 3.1. We omit its proof.

Example 3.13.

Remark 3.7.

The parametric continuity of all the other examples discussed above can be established in a similar manner.

4. Optimal Policies

In this section, we provide a systematic study of optimal timing of decisions when there are threshold states, and explore the key properties of the optimal policies.

4.1. Conditional Independence in Transitions

For a broad range of problems, the continuation value function exists in a lower dimensional space than the value function. Moreover, the relationship is asymmetric. While each state variable that appears in the continuation value must appear in the value function, the converse is not true. The continuation value function can have strictly fewer arguments than the value function (recall example 2.3).

To verify, suppose that the state space and can be written as , where is a convex subset of , is a convex subset of , and such that . The state process is then , where and are two stochastic processes taking values in and , respectively. In particular, for each , represents the first dimensions and the rest dimensions of the period- state .

Assume that the stochastic processes and are conditionally independent, in the sense that conditional on each , the next period states and are independent. Let and be the current and next period states, respectively. With conditional independence, the stochastic kernel can be represented by the conditional distribution of on , denoted as , i.e., .

Assume further that the flow continuation payoff is defined on , i.e., .161616 Indeed, in many applications, the flow payoff is a constant, as seen in previous examples. Under this setup, has strictly fewer arguments than . While is a function of both and , is a function of only. Hence, the continuation value based method allows us to mitigate one of the primary stumbling blocks for numerical dynamic programming: the so-called curse of dimensionality (see, e.g., Bellman (1969), Rust (1997)).

4.2. The Threshold State Problem

Among problems where conditional independence exists, the optimal policy is usually determined by a reservation rule, in the sense that the decision process terminates whenever a specific state variable hits a threshold level. In such cases, the continuation value based method allows for a sharp analysis of the optimal policy. This type of problem is pervasive in quantitative and theoretical economic modeling, as we now formulate.

For simplicity, we assume that , in which case is a convex subset of and is a convex subset of . For each , represents the first dimension and the rest dimensions of the period- state . If, in addition, is monotone on , we call the threshold state and the environment state (or environment) of period , moreover, we call the threshold state space and the environment space.

Assumption 4.1.

is strictly monotone on . Moreover, for all , there exists such that .

Under assumption 4.1, the reservation rule property holds. When the exit payoff is strictly increasing in , for instance, this property states that if the agent terminates at at a given point of time, then he would have terminated at any higher state at that moment. Specifically, there is a decision threshold such that when attains this threshold level, i.e., , the agent is indifferent between stopping and continuing, i.e., for all .

As shown in theorem 2.1, the optimal policy satisfies . For a sequential decision problem with threshold state, this policy is fully specified by the decision threshold . In particular, under assumption 4.1, we have

| (15) |

Further, based on properties of the continuation value, properties of the decision threshold can be established. The next result provides sufficient conditions for continuity. The proof is similar to proposition 4.4 below and thus omitted.

Proposition 4.1.

The next result discusses monotonicity. The proof is obvious and we omit it.

Proposition 4.2.

A typical element is . For given functions and , define , , and . The next result follows immediately from proposition 3.4 and the implicit function theorem.

Proposition 4.3.

Intuitively, denotes the premium of terminating the decision process. Hence, are the instantaneous rates of change of the terminating premium in response to changes in and , respectively. Holding aggregate premium null, the premium changes due to changes in and cancel out. As a result, the rate of change of with respect to changes in is equivalent to the ratio of the instantaneous rates of change in the premium. The negativity is due to zero terminating premium at the decision threshold.

Let be the decision threshold with respect to . We have the following result for parametric continuity.

Proposition 4.4.

Proof of proposition 4.4.

Define by . Without loss of generality, assume that is strictly increasing in , then is strictly increasing in and continuous. For all fixed and , since is strictly increasing in and , we have

Since is continuous with respect to , there exists such that for all , we have

Since and is strictly increasing in , we have

Hence, is continuous, as was to be shown. ∎

5. Applications

In this section we consider several typical applications in economics, and compare the computational efficiency of continuation value and value function based methods. Numerical experiments show that the partial impact of lower dimensionality of the continuation value can be huge, even when the difference between the arguments of this function and the value function is only a single variable.

5.1. Job Search II

Consider the adaptive search model of Ljungqvist and Sargent (2012) (section 6.6). The model is as example 2.1, apart from the fact that the distribution of the wage process is unknown. The worker knows that there are two possible densities and , and puts prior probability on being chosen. If the current offer is rejected, a new offer is observed at the beginning of next period, and, by the Bayes’ rule, updates via

| (16) |

The state space is , where is a compact interval of . Let . The value function of the unemployed worker satisfies

where . This is a typical threshold state problem, with threshold state and environment . As to be shown, the optimal policy is determined by a reservation wage such that when , the worker is indifferent between accepting and rejecting the offer. Consider the candidate space . The Jovanovic operator is

| (17) |

Proposition 5.1.

Let . The following statements are true:

-

1.

is a contraction on of modulus , with unique fixed point .

-

2.

The value function , reservation wage , and optimal policy for all .

-

3.

, and are continuous.

Since the computation is 2-dimensional via value function iteration (VFI), and is only 1-dimensional via continuation value function iteration (CVI), we expect the computation via CVI to be much faster. We run several groups of tests and compare the time taken by the two methods. All tests are processed in a standard Python environment on a laptop with a 2.5 GHz Intel Core i5 and 8GB RAM.

5.1.1. Group-1 Experiments

This group documents the time taken to compute the fixed point across different parameter values and at different precision levels. Table 1 provides the list of experiments performed and table 2 shows the result.

| Parameter | Test 1 | Test 2 | Test 3 | Test 4 | Test 5 |

|---|---|---|---|---|---|

-

•

Note: Different parameter values in each experiment.

| Test/Method/Precision | |||||||

|---|---|---|---|---|---|---|---|

| Test 1 | VFI | ||||||

| CVI | |||||||

| Test 2 | VFI | ||||||

| CVI | |||||||

| Test 3 | VFI | ||||||

| CVI | |||||||

| Test 4 | VFI | ||||||

| CVI | |||||||

| Test 5 | VFI | ||||||

| CVI | |||||||

-

•

Note: We set , and . The grid points of lie in with points for and for . For each given test and level of precision, we run the simulation times for CVI, 20 times for VFI, and calculate the average time (in seconds).

As shown in table 2, CVI performs much better than VFI. On average, CVI is times faster than VFI. In the best case, CVI is times faster (in test 5, VFI takes seconds to achieve a level of accuracy , while CVI takes only seconds). In the worst case, CVI is times faster (in test 5, CVI takes seconds as opposed to seconds by VFI to attain a precision level ).

5.1.2. Group-2 Experiments

In applications, increasing the number of grid points provides more accurate numerical approximations. This group of tests compares how the two approaches perform under different grid sizes. The setup and result are summarized in table 3 and table 4, respectively.

| Variable | Test 2 | Test 6 | Test 7 | Test 8 | Test 9 | Test 10 |

|---|---|---|---|---|---|---|

-

•

Note: Different grid sizes of the state variables in each experiment.

| Test/Precision/Method | |||||||

|---|---|---|---|---|---|---|---|

| Test 2 | VFI | ||||||

| CVI | |||||||

| Test 6 | VFI | ||||||

| CVI | |||||||

| Test 7 | VFI | ||||||

| CVI | |||||||

| Test 8 | VFI | ||||||

| CVI | |||||||

| Test 9 | VFI | ||||||

| CVI | |||||||

| Test 10 | VFI | ||||||

| CVI | |||||||

-

•

Note: We set , , , and . The grid points of lie in . For each given test and precision level, we run the simulation times for CVI, 20 times for VFI, and calculate the average time (in seconds).

CVI outperforms VFI more obviously as the grid size increases. In table 4 we see that as we increase the number of grid points for , the speed of CVI is not affected. However, the speed of VFI drops significantly. Amongst tests 2, 6 and 7, CVI is times faster than VFI on average. In the best case, CVI is 386 times faster (while it takes VFI seconds to achieve a precision level in test 7, CVI takes only second). As we increase the grid size of from to , CVI is not affected, but the time taken for VFI almost doubles.

As we increase the grid size of both and , there is a slight decrease in the speed of CVI. Nevertheless, the decrease in the speed of VFI is exponential. Among tests 2 and 8–10, CVI is times as fast as VFI on average. In test 10, VFI takes seconds to obtain a level of precision , instead, CVI takes only seconds, which is 386 times faster.

5.1.3. Group-3 Experiments

Since the total number of grid points increases exponentially with the number of states, the speed of computation will drop dramatically with an additional state. To illustrate, consider a parametric class problem with respect to . We set , , and . Let lie in with grid points for each. In this case, VFI is -dimensional and suffers the ”curse of dimensionality”: the computation takes more than 7 days. However, CVI is only -dimensional and the computation finishes within 171 seconds (with precision ).

In figure 2, we see that the reservation wage is increasing in and decreasing in . Intuitively, a higher level of compensation hinders the agent’s incentive of entering into the labor market. Moreover, since is a less attractive distribution than and larger means more weight on and less on , a larger depresses the worker’s assessment of future prospects, and relatively low current offers become more attractive.

5.2. Job Search III

Recall the adaptive search model of example 2.3 (subsequently studied by examples 2.5, 3.2 and 3.8). The value function satisfies

| (18) |

Recall the Jovanovic operator defined by (12). This is a threshold state sequential decision problem, with threshold state and environment . By the intermediate value theorem, assumption 4.1 holds. Hence, the optimal policy is determined by a reservation wage such that when , the worker is indifferent between accepting and rejecting the offer. Since all the assumptions of proposition 3.1 hold (see example 3.2), by proposition 4.1, is continuous. Since is increasing in (see example 3.8), by proposition 4.2, is increasing in .

In simulation, we set , , , and consider different levels of risk aversion: . The grid points of lie in , with points for the grid and points for the grid. We set the threshold function outside the grid to its value at the closest grid. The integration is computed via Monte Carlo with 1000 draws.171717 Changing the number of Monte Carlo samples, the grid range and grid density produce almost the same results. Figure 3 provides the simulation results. There are several key characteristics, as can be seen.

First, in each case, the reservation wage is an increasing function of , which parallels the above analysis. Naturally, a more optimistic agent (higher ) would expect that higher offers can be obtained, and will not accept the offer until the wage is high enough.

Second, the reservation wage is increasing in for given of relatively small values, though it is decreasing in for given of relatively large values. Intuitively, although a pessimistic worker (low ) expects to obtain low wage offers on average, part of the downside risks are chopped off since a compensation is obtained when the offer is turned down. In this case, a higher level of uncertainty (higher ) provides a better chance to ”try the fortune” for a good offer, boosting up the reservation wage. For an optimistic (high ) but risk-averse worker, the insurance out of compensation loses power. Facing a higher level of uncertainty, the worker has an incentive to enter the labor market at an earlier stage so as to avoid downside risks. As a result, the reservation wage goes down.

5.3. Firm Entry

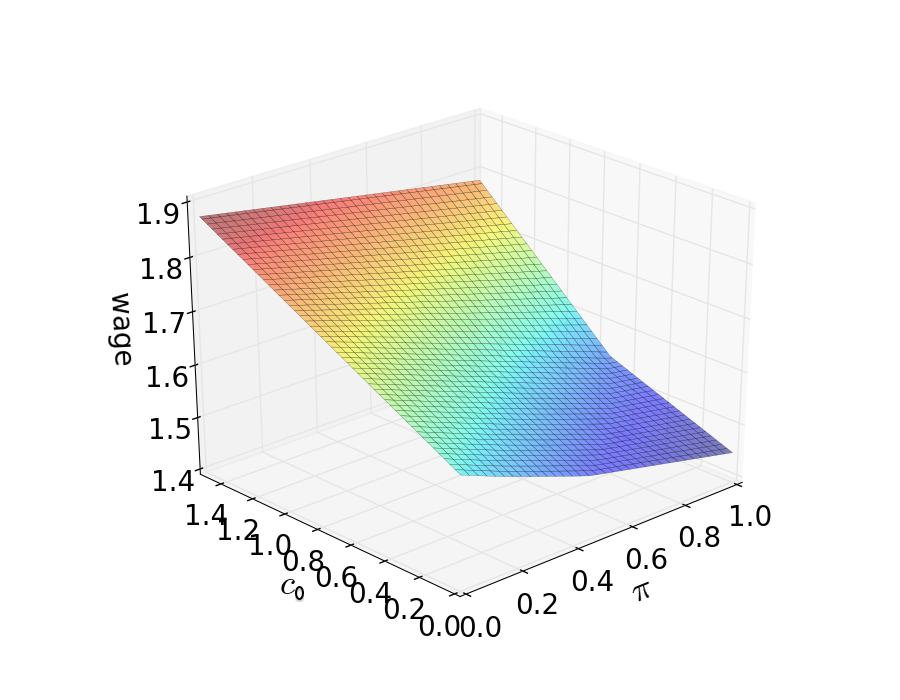

Consider a firm entry problem in the style of Fajgelbaum et al. (2015). Each period, an investment cost is observed, where with finite mean. The firm then decides whether to incur this cost and enter the market to win a stochastic dividend via production, or wait and reconsider next period. The firm aims to find a decision rule that maximizes the net returns.

The dividend follows , , where and are respectively a persistent and a transient component, and , . A public signal is released at the end of each period , where , . The firm has prior belief that is Bayesian updated after observing , so the posterior satisfies , with

| (19) |

The firm has utility , where is the coefficient of absolute risk aversion. The value function satisfies

where with . The exit payoff is . This is a threshold state problem, with threshold state and environment . The Jovanovic operator is

| (20) |

Let , , and . Define according to (11). We use to denote the reservation cost.

Proposition 5.2.

The following statements are true:

-

1.

is a contraction mapping on with unique fixed point .

-

2.

The value function , reservation cost and optimal policy for all .

-

3.

, and are continuous functions.

-

4.

is decreasing in , and, if , then and are increasing in .

Remark 5.1.

Notably, the first three claims of proposition 5.2 have no restriction on the range of values, the autoregression coefficient of .

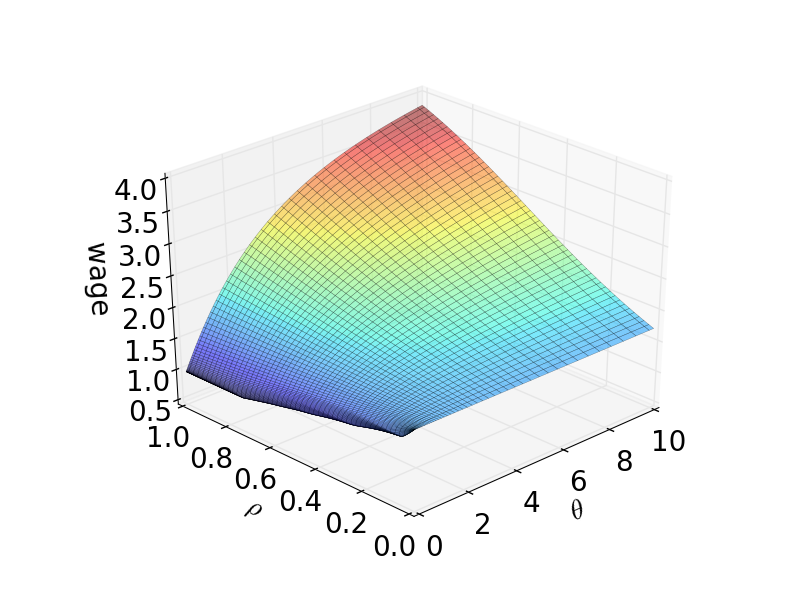

In simulation, we set , , , , and . Consider , , and let the grid points of lie in with points for the grid and points for the grid. The reservation cost function outside of the grid points is set to its value at the closest grid point. The integration in the operator is computed via Monte Carlo with 1000 draws.181818 Changing the number of Monte Carlo samples, the grid range and grid density produces almost the same results. We plot the perceived probability of investment, i.e., .

As shown in figure 4, the perceived probability of investment is increasing in and decreasing in . This parallels propositions 1 and 2 of Fajgelbaum et al. (2015). Intuitively, for given investment cost and variance , a more optimistic firm (higher ) is more likely to invest. Furthermore, higher implies a higher level of uncertainty, thus a higher risk of low returns. As a result, the risk averse firm prefers to delay investment (gather more information to avoid downside risks), and will not enter the market unless the cost of investment is low enough.

5.4. Job Search IV

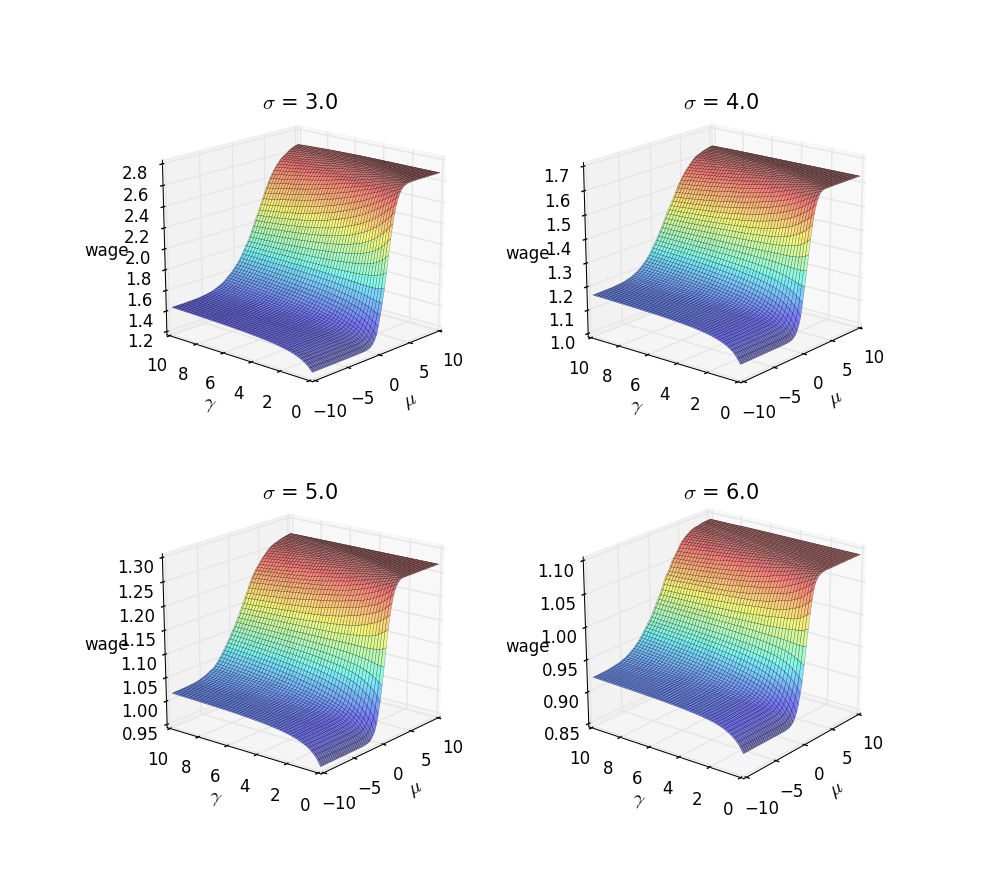

We consider another extension of McCall (1970). The setup is as in example 2.2, except that the state process follows

| (21) | ||||

| (22) |

where , and with finite first moments, and . Moreover, , and are independent, and is independent of and . Similar settings as (21)–(22) appear in many search-theoretic and real options studies (see e.g., Gomes et al. (2001), Low et al. (2010), Chatterjee and Eyigungor (2012), Bagger et al. (2014), Kellogg (2014)).

We set and . In this case, and are persistent and transitory components of income, respectively, and is treated as a shock to the persistent component. can be interpreted as social security, gifts, etc. Recall that the utility of the agent is defined by (5), is the unemployment compensation and . The value function of the agent satisfies

where and is the density kernel of . The Jovanovic operator is

This is another threshold state problem, with threshold state and environment . Let be the reservation wage. Recall the relative risk aversion coefficient in (5) and the weight function defined by (11).

5.4.1. Case I: and

For , choose such that , where . Let and .

Proposition 5.3.

If , then the following statements hold:

-

1.

is a contraction mapping on with unique fixed point .

-

2.

The value function , reservation wage , and optimal policy for all .

-

3.

and are continuously differentiable, and is continuous.

-

4.

is increasing in , and, if , then , and are increasing in .

Remark 5.2.

If , then claims 1–3 of proposition 5.3 remain true for , and claim 4 remains true for .

5.4.2. Case II:

For , choose such that . Let and .

Proposition 5.4.

If , then the following statements hold:

-

1.

is a contraction mapping on with unique fixed point is .

-

2.

The value function , reservation wage , and optimal policy for all .

-

3.

and are continuously differentiable, and is continuous.

-

4.

is increasing in , and, if , then , and are increasing in .

Remark 5.3.

If , then claims 1–3 of proposition 5.4 remain true for , and claim 4 remains true for .

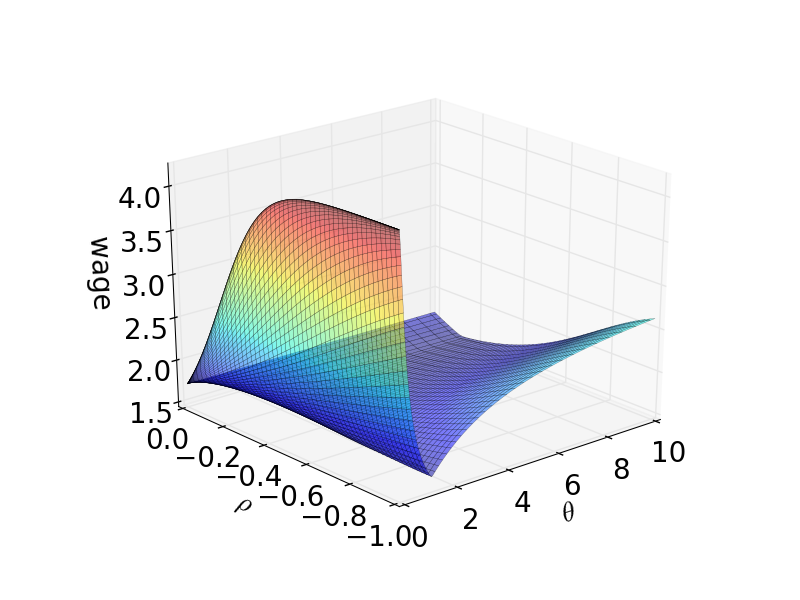

We choose and as in Ljungqvist and Sargent (2012) (section 6.6). Further, , , , and . We consider parametric class problems with respect to , where and are treated separately, with grid points in each case. Moreover, the grid points of lie in with points, and the grid is scaled to be more dense when is smaller. The reservation wage outside the grid points is set to its value at the closest grid, and the integration is computed via Monte Carlo with 1000 draws.

When , the state process is independent and identically distributed, in which case each realized persistent component will be forgotten in future stages. As a result, the continuation value is independent of , yielding a reservation wage that is horizontal to the -axis, as shown in figure 5.

When , the reservation wage is increasing in , which parallels propositions 5.3–5.4. Naturally, a higher puts the agent in a better situation, raising his desired wage level. Moreover, since measures the degree of income persistence, a higher prolongs the recovery from bad states (i.e., ), and hinders the attenuation of good states (i.e., ). As a result, the reservation wage tends to be decreasing in when and increasing in when .

When , the agent always has chance to arrive at a good state in future stages. In this case, a very bad or a very good current state is favorable since a very bad state tends to evolve into a very good one next period, and a very good state tends to show up again in two periods. If the current state is at a medium level (e.g., is close to ), however, the agent cannot take advantage of the countercyclical patterns. Hence, the reservation wage is decreasing in at the beginning and then starts to be increasing in after some point.

6. Extensions

6.1. Repeated Sequential Decisions

In many economic models, the choice to stop is not permanent. For example, when a worker accepts a job offer, the resulting job might only be temporary (see, e.g., Rendon (2006), Ljungqvist and Sargent (2008), Poschke (2010), Chatterjee and Rossi-Hansberg (2012), Lise (2013), Moscarini and Postel-Vinay (2013), Bagger et al. (2014)). Another example is sovereign default (see, e.g., Choi et al. (2003), Albuquerque and Hopenhayn (2004), Arellano (2008), Alfaro and Kanczuk (2009), Arellano and Ramanarayanan (2012), Bai and Zhang (2012), Chatterjee and Eyigungor (2012), Mendoza and Yue (2012), Hatchondo et al. (2016)), where default on international debt leads to a period of exclusion from international financial markets. The exclusion is not permanent, however. With positive probability, the country exits autarky and begins borrowing from international markets again.

To put this type of problem in a general setting, suppose that, at date , an agent is either active or passive. When active, the agent observes and chooses whether to continue or exit. Continuation results in a current payoff and the agent remains active at . Exit results in a current payoff and transition to the passive state. From there the agent has no action available, but will return to the active state at and all subsequent period with probability .

Assumption 6.1.

There exist a -measurable function and constants , such that , and, for all ,

-

(1)

;

-

(2)

Let and be the maximal discounted value starting at in the active and passive state respectively. One can show that, under assumption 6.1, and satisfy191919 A formal proof of this statement is available from the authors upon request.

| (23) |

and

| (24) |

With we can write . Using this notation, we can view and as solutions to the functional equations

| (25) |

Choose such that , and . Consider the weight function defined by

| (26) |

and the product space , where is a metric on defined by

With this metric, inherits the completeness of . Now define the operator on by

Theorem 6.1.

Under assumption 6.1, the following statements hold:

-

1.

is a contraction mapping on with modulus .

-

2.

The unique fixed point of in is .

6.2. Sequential Decision with More Choices

In many economic problems, agents face multiple choices in the sequential decision process (see, e.g., Crawford and Shum (2005), Cooper et al. (2007), Vereshchagina and Hopenhayn (2009), Low et al. (2010), Moscarini and Postel-Vinay (2013)). A standard example is on-the-job search, where an employee can choose from quitting the job market and taking the unemployment compensation, staying in the current job at a flow wage, or searching for a new job (see, e.g., Jovanovic (1987), Bull and Jovanovic (1988), Gomes et al. (2001)). A common characteristic of this type of problem is that different choices lead to different transition probabilities.

To treat this type of problem generally, suppose that in period , the agent observes and makes choices among alternatives. A selection of alternative results in a current payoff along with a stochastic kernel . We assume the following.

Assumption 6.2.

There exist a -measurable function and constants such that , and, for all and ,

-

(1)

,

-

(2)

.

Let be the value function and be the expected value of choosing alternative . Under assumption 6.2, we can show that and satisfy202020 A formal proof of this result is available from the authors upon request.

| (27) |

where

| (28) |

for . (27)–(28) imply that can be written as

| (29) |

for . Define the continuation value function .

Choose such that and . Consider the weight function defined by

| (30) |

One can show that the product space is a complete metric space, where is defined by for all , . The Jovanovic operator on is defined by

| (31) |

The next result is a simple extension of theorem 6.1 and we omit its proof.

Theorem 6.2.

Under assumption 6.2, the following statements hold:

-

1.

is a contraction mapping on of modulus .

-

2.

The unique fixed point of in is .

Example 6.1.

Consider the on-the-job search model of Bull and Jovanovic (1988). Each period, an employee has three choices: quit the job market, stay in the current job, or search for a new job. Let be the value of leisure and be the worker’s productivity at a given firm, with . Let be the current price. The price sequence is Markov with transition probability and stationary distribution . It is assumed that there is no aggregate shock so that is the distribution of prices over firms. The current wage of the worker is . The value function satisfies , where

denotes the expected value of quitting the job,

is the expected value of staying in the current firm, and,

represents the expected value of searching for a new job. Bull and Jovanovic (1988) assumes that there are compact supports and for the state processes and , where and . This assumption can be relaxed based on our theory. Let the state space be . Let and .

Assumption 6.3.

There exist a Borel measurable map , and constants such that , and, for all ,

-

(1)

,

-

(2)

,

-

(3)

and .

7. Conclusion

A comprehensive theory of optimal timing of decisions was developed here. The theory successfully addresses a wide range of unbounded sequential decision problems that are hard to deal with via existing unbounded dynamic programming theory, including both the traditional weighted supremum norm theory and the local contraction theory. Moreover, this theory characterizes the continuation value function directly, and has obvious advantages over the traditional dynamic programming theory based on the value function and Bellman operator. First, since continuation value functions are typically smoother than value functions, this theory allows for shaper analysis of the optimal policies and more efficient computation. Second, when there is conditional independence along the transition path (e.g., the class of threshold state problems), this theory mitigates the curse of dimensionality, a key stumbling block for numerical dynamic programming.

Appendix A

Lemma 7.1.

Under assumption 2.1, there exist such that for all ,

-

(1)

.

-

(2)

.

Proof.

Without loss of generality, we assume . By assumption 2.1, we have , and for all . For all , by the Markov property (see, e.g., Meyn and Tweedie (2012), section 3.4.3),

Induction shows that for all ,

| (32) |

Moreover, for all , apply the Markov property again shows that

Based on (32) we know that

| (33) |

Similarly, for all , we have

| (34) |

Denote as a measurable space and as a measure space.

Lemma 7.2.

Let be a measurable map that is continuous in . If there exists a measurable map that is continuous in with for all , and that is continuous, then the mapping is continuous.

Proof.

Since for all , we know that are nonnegative measurable functions. Let be a sequence of with . By Fatou’s lemma, we have

From the given assumptions we know that . Combine this result with the above inequality, we have

where we have used the fact that for any two given sequences and of with exists, we have: . So

Therefore, the mapping is continuous. ∎

Appendix B : Main Proofs

7.1. Proof of Section 2 Results.

In this section, we prove examples 2.2–2.3. Note that in example 2.2, has a density representation .

Proof of example 2.2.

Case I: and . In this case, the exit payoff is . Since for some constant , induction shows that

| (36) |

for some constant and all . Recall the definition of in example 2.2. Let such that , and . By remark 2.1, it remains to show that satisfies the geometric drift condition (3). Let and , then , and we have212121 To obtain the second inequality of (7.1), note that either or . Assume without loss of generality that the former holds, then and . The latter implies that . Combine this with yields the second inequality of (7.1).

| (37) |

Since , satisfies the geometric drift property, and assumption 2.1 holds.

Remark 7.1.

In fact, if , by (36), we can also let , then

| (38) |

In this way, we have a simpler with geometric drift property.

Remark 7.2.

Case II: . In this case, the exit payoff is . Let , , and . Since , by Jensen’s inequality,

Since , assumption 2.1 holds. This concludes the proof. ∎

Proof of example 2.3.

Case I: and . Recall the definition of . We have

| (39) |

By remark 2.1, it remains to verify the geometric drift condition (3). This follows from (7)–(8). Indeed, one can show that

| (40) |

Case II: . Since , , we have: , and

| (41) |

Similarly as case I, one can show that .

Hence, assumption 2.1 holds in both cases. This concludes the proof. ∎

Proof of theorem 2.1.

To prove claim 1, based on the weighted contraction mapping theorem (see, e.g., Boyd (1990), section 3), it suffices to verify: (a) is monotone, i.e., if and ; (b) and is -measurable for all ; and (c) for all and . Obviously, condition (a) holds. By (10)–(11), we have

for all , so . The measurability of follows immediately from our primitive assumptions. Hence, condition (b) holds. By the Markov property (see, e.g., Meyn and Tweedie (2012), section 3.4.3), we have

Let , then we have

| (42) |

By the assumptions on and , we have and . Assumption 2.1 and (42) then imply that

Hence, for all , and , we have

So condition (c) holds. Claim 1 is verified.

Regarding claim 2, substituting into (9) we get

This implies that is a fixed point of . Moreover, from lemma 7.1 we know that . Hence, must coincide with the unique fixed point of under .

Finally, by theorem 1.11 of Peskir and Shiryaev (2006), we can show that is an optimal stopping time. Claim 3 then follows from the definition of the optimal policy and the fact that . ∎

7.2. Proof of Section 3 Results.

Proof of proposition 3.1.

Let be the set of continuous functions in . Since is continuous by assumption, is a closed subset of (see e.g., Boyd (1990), section 3). To show the continuity of , it suffices to verify that (see, e.g., Stokey et al. (1989), corollary 1 of theorem 3.2). For all , there exists a constant such that . In particular,

are nonnegative and continuous. Let . Based on the generalized Fatou’s lemma of Feinberg et al. (2014) (theorem 1.1), we can show that for all sequence of such that , we have

Since assumptions 3.2–3.3 imply that

we have

where we have used the fact that for given sequences and of with exists, we have: . Hence,

| (43) |

i.e., is continuous. Since is continuous by assumption, . Hence, and is continuous. The continuity of follows from the continuity of and and the fact that . ∎

Recall and defined in the beginning of section 3.3. The next lemma holds.

Lemma 7.3.

Suppose assumption 2.1 holds, and, for and

-

(1)

has a density representation such that exists, .

-

(2)

For all , there exists , such that

Then: for all and .

Proof of lemma 7.3.

For all , let be an arbitrary sequence of such that , and for all . For the given by (2), there exists such that for all . Holding , by the mean value theorem, there exists such that

Since in addition for some , we have: for all ,

-

(a)

,

-

(b)

, and

-

(c)

as ,

where (b) follows from condition (2). By the dominated convergence theorem,

Hence, , as was to be shown. ∎

7.3. Proof of Section 5 Results

Proof of proposition 5.1.

Assumption 2.1 holds due to bounded payoffs. By theorem 2.1, claim 1 holds. Let . Since , , then . By the intermediate value theorem, assumption 4.1 holds. By theorem 2.1 and (15), claim 2 holds. satisfies the Feller property by lemma 7.2. Since payoff functions are continuous, the continuity of and follows from proposition 3.1 (or remark 3.1). The continuity of follows from proposition 4.1. Claim 3 is verified. ∎

Proof of proposition 5.2.

The exit payoff satisfies

| (44) |

Using (19), we can show that

| (45) |

Let denote the mean of . Combine (44)–(45), we have

| (46) |

Notice that (45) is equivalent to

| (47) |

Hence, assumption 2.1 holds with , and . The intermediate value theorem shows that assumption 4.1 holds. By theorem 2.1 and the analysis of section 4, claims 1–2 hold.

For all bounded continuous function , we have

By (19) and lemma 7.2, this function is bounded and continuous in . Hence, assumption 3.1 holds. The exit payoff is continuous. By (19), both sides of (44) are continuous in . By (45)–(46), the conditional expectation of the right side of (44) is continuous in . Lemma 7.2 then implies that is continuous. Now we have shown that assumption 3.2 holds. Assumption 3.3 holds since is continuous and (47) holds. Proposition 3.1 then implies that and are continuous. By proposition 4.1, is continuous. Claim 3 is verified.

Proof of proposition 5.3.

Proof of claim 1. Since

| (48) |

we have

| (49) |

Induction shows that

| (50) |

for some , and all . Define as in the assumption, then

| (51) | ||||

Hence, assumption 2.1 holds. Claim 1 then follows from theorem 2.1.

Proof of claim 2. Assumption 4.1 holds by the intermediate value theorem. Claim 2 then follows from theorem 2.1, assumption 4.1 and (15).

Proof of claim 3. Note that the stochastic kernel has a density representation in the sense that for all and ,

Moreover, it is straightforward (though tedious) to show that is twice differentiable for all , that is continuous, and that

| (52) |

where . If , then as and as . If , then as and as . Hence, assumption 3.8 holds. Based on (48)–(51) and lemma 7.2, we can show that assumption 3.10 holds. By proposition 3.4, is continuously differentiable. Since assumption 4.1 holds and is continuously differentiable, by proposition 4.3, is continuously differentiable. is continuous since .

Proof of claim 4. Assumption 3.4 holds since . Note that

is increasing in , and, when , is stochastically increasing in . Hence, assumption 3.5 holds. By propositions 3.2 and 4.2, and are increasing in . Moreover, is a function of , is a function of , both functions are increasing, and . Hence, is increasing in and . ∎

Proof of proposition 5.4.

Since for all , we have

Hence,

Induction shows that

| (53) |

for some , and all . Hence, we can define as in the assumption. Similarly as in the proof of proposition 5.3, we can show that

| (54) | ||||

Hence, assumption 2.1 holds. Claim 1 then follows from theorem 2.1. The remaining proof is similar to proposition 5.3. ∎

7.4. Proof of Section 6 Results

Proof of theorem 6.1.

Regarding claim 1, similar to the proof of theorem 2.1, we can show that

for all . We next show that . For all , define the functions and . Then there exists such that for all ,

and

This implies that and . Hence, . Next, we show that is indeed a contraction mapping on . For all fixed and in , we have , where

and

For all , we have

where the second inequality is due to the elementary fact . This implies that . Regarding , similar arguments yield . In conclusion, we have

| (55) |

Hence, is a contraction mapping on with modulus , as was to be shown. Claim 1 is verified.

References

- Albuquerque and Hopenhayn (2004) Albuquerque, R. and H. A. Hopenhayn (2004): “Optimal lending contracts and firm dynamics,” The Review of Economic Studies, 71, 285–315.

- Alfaro and Kanczuk (2009) Alfaro, L. and F. Kanczuk (2009): “Optimal reserve management and sovereign debt,” Journal of International Economics, 77, 23–36.

- Alvarez and Stokey (1998) Alvarez, F. and N. L. Stokey (1998): “Dynamic programming with homogeneous functions,” Journal of Economic Theory, 82, 167–189.

- Arellano (2008) Arellano, C. (2008): “Default risk and income fluctuations in emerging economies,” The American Economic Review, 98, 690–712.

- Arellano and Ramanarayanan (2012) Arellano, C. and A. Ramanarayanan (2012): “Default and the maturity structure in sovereign bonds,” Journal of Political Economy, 120, 187–232.

- Asplund and Nocke (2006) Asplund, M. and V. Nocke (2006): “Firm turnover in imperfectly competitive markets,” The Review of Economic Studies, 73, 295–327.

- Bagger et al. (2014) Bagger, J., F. Fontaine, F. Postel-Vinay, and J.-M. Robin (2014): “Tenure, experience, human capital, and wages: A tractable equilibrium search model of wage dynamics,” The American Economic Review, 104, 1551–1596.

- Bai and Zhang (2012) Bai, Y. and J. Zhang (2012): “Financial integration and international risk sharing,” Journal of International Economics, 86, 17–32.

- Becker and Boyd (1997) Becker, R. A. and J. H. Boyd (1997): Capital Theory, Equilibrium Analysis, and Recursive Utility, Wiley-Blackwell.

- Bellman (1969) Bellman, R. (1969): “A new type of approximation leading to reduction of dimensionality in control processes,” Journal of Mathematical Analysis and Applications, 27, 454–459.

- Bental and Peled (1996) Bental, B. and D. Peled (1996): “The accumulation of wealth and the cyclical generation of new technologies: A search theoretic approach,” International Economic Review, 37, 687–718.

- Boyd (1990) Boyd, J. H. (1990): “Recursive utility and the Ramsey problem,” Journal of Economic Theory, 50, 326–345.

- Bull and Jovanovic (1988) Bull, C. and B. Jovanovic (1988): “Mismatch versus derived-demand shift as causes of labour mobility,” The Review of Economic Studies, 55, 169–175.

- Burdett and Vishwanath (1988) Burdett, K. and T. Vishwanath (1988): “Declining reservation wages and learning,” The Review of Economic Studies, 55, 655–665.

- Chalkley (1984) Chalkley, M. (1984): “Adaptive job search and null offers: A model of quantity constrained search,” The Economic Journal, 94, 148–157.

- Chatterjee and Eyigungor (2012) Chatterjee, S. and B. Eyigungor (2012): “Maturity, indebtedness, and default risk,” The American Economic Review, 102, 2674–2699.

- Chatterjee and Rossi-Hansberg (2012) Chatterjee, S. and E. Rossi-Hansberg (2012): “Spinoffs and the Market for Ideas,” International Economic Review, 53, 53–93.

- Choi et al. (2003) Choi, J. J., D. Laibson, B. C. Madrian, and A. Metrick (2003): “Optimal defaults,” The American Economic Review, 93, 180–185.

- Cooper et al. (2007) Cooper, R., J. Haltiwanger, and J. L. Willis (2007): “Search frictions: Matching aggregate and establishment observations,” Journal of Monetary Economics, 54, 56–78.

- Coşar et al. (2016) Coşar, A. K., N. Guner, and J. Tybout (2016): “Firm dynamics, job turnover, and wage distributions in an open economy,” The American Economic Review, 106, 625–663.

- Crawford and Shum (2005) Crawford, G. S. and M. Shum (2005): “Uncertainty and learning in pharmaceutical demand,” Econometrica, 73, 1137–1173.

- Dinlersoz and Yorukoglu (2012) Dinlersoz, E. M. and M. Yorukoglu (2012): “Information and industry dynamics,” The American Economic Review, 102, 884–913.

- Dixit and Pindyck (1994) Dixit, A. K. and R. S. Pindyck (1994): Investment Under Uncertainty, Princeton University Press.

- Duffie (2010) Duffie, D. (2010): Dynamic Asset Pricing Theory, Princeton University Press.

- Dunne et al. (2013) Dunne, T., S. D. Klimek, M. J. Roberts, and D. Y. Xu (2013): “Entry, exit, and the determinants of market structure,” The RAND Journal of Economics, 44, 462–487.