Kaplan, Nordman, and Vardeman

On the instability and degeneracy of deep learning models

Abstract

A probability model exhibits instability if small changes in a data outcome result in large, and often unanticipated, changes in probability. This instability is a property of the probability model, given by a distributional form and a given configuration of parameters. For correlated data structures found in several application areas, there is increasing interest in identifying such sensitivity in model probability structure. We consider the problem of quantifying instability for general probability models defined on sequences of observations, where each sequence of length has a finite number of possible values that can be taken at each point. A sequence of probability models results, indexed by , and an associated parameter sequence, that accommodates data of expanding dimension. Model instability is formally shown to occur when a certain log-probability ratio under such models grows faster than . In this case, a one component change in the data sequence can shift probability by orders of magnitude. Also, as instability becomes more extreme, the resulting probability models are shown to tend to degeneracy, placing all their probability on potentially small portions of the sample space. These results on instability apply to large classes of models commonly used in random graphs, network analysis, and machine learning contexts. Degeneracy, Instability, Classification, Deep Learning, Graphical Models

1 Introduction

We consider the behavior, and the potential impropriety, of sequences of discrete probability models built to incorporate observations of increasing sample size . Interest is in identifying instability in such models, which is roughly characterized by probabilities with extreme sensitivity to small changes in data configuration. The concept of instability was introduced in the field of statistical physics (i.e., point processes) by Ruelle, (1999) and then further extended by Schweinberger, (2011) for a family of exponential models. At issue, models exhibiting instability are typically undesirable as these tend to provide poor representations of data or data-generation. As an example, such models can include near-degenerate distributions that assign essentially all probability mass to only a subset of an overall sample space. The latter issue in connection to degeneracy has been recognized as a concern in that dominant model outcomes may not resemble observed data (cf. Handcock,, 2003). As a compounding issue, model instability often has direct negative impacts for statistical inference and computations based on likelihood functions. Namely, volatilities in probability structure can potentially hamper the numerical evaluations required for maximum likelihood estimation as well as other model-based simulations via Markov Chain Monte Carlo (MCMC). These reasons motivate our general study of instability for a broad class of probability models, described next.

In the model framework, let denote a collection of discrete random variables with a finite sample space, , represented as some -fold Cartesian product. That is, with denotes the set of potential outcomes for each single variable , so that the product space corresponds to values for the variables . For each , let denote a probability model on , under which is the probability of the data outcome . In this, we assume that the model support of is the sample space . This framework produces probability models , indexed by a defining sequence of parameters , to describe data of any given sample size . For simplicity, we will refer to this distributional class as Finite Outcome Everywhere Supported (FOES) models in the following. The dimension and structure of such parameters are generic, without restriction, though natural cases will be seen to include those where for some arbitrary integer-valued function .

Section 2 provides some examples of FOES models encountered in graph/network analysis and machine learning (i.e., deep learning models). These are used as references for later illustrations. Section LABEL:instability-results then establishes several formal results for FOES models with regard to instability. Schweinberger, (2011) originally developed instability results specific to a certain class of discrete exponential models. For similar exponential models with random networks, Handcock, (2003) studied model degeneracy, where a probability model places near complete mass on modes and may thereby narrow the feasible model outcomes. As findings here and from Schweinberger, (2011) suggest, model instability and degeneracy may also be related by viewing degeneracy as an extreme, or limiting form, of instability. Our main results establish a broad characterization of model instability, appropriate across the whole FOES model class, that incorporates results of Schweinberger, (2011) as a special case. We prescribe a general and simple condition for identifying instability in a FOES model sequence, which quantifies whether certain maximal probabilities in a FOES model are too extreme relative to the sample size . When these conditions are met, the probability structure of a FOES model is shown to exhibit extreme sensitivity, with probability assignments possessing extreme peaks and troughs across nearly identical outcomes. As the measure of model instability increases, probabilities from an unstable FOES model additionally increase in volatility and provably slide into degeneracy. Section 4 then emphasizes the implications of such model instability, showing that such impropriety can be expected to numerically hinder maximum likelihood estimation and MCMC-based simulations. As one potential remedy, suggestions are given for constraining model parameterizations to avoid the most problematic regions of the parameter space (see Section 4.2 for further discussion). Proofs of the main results appear in Appendix A.

2 Examples

Many model families lead to FOES models. (For clarity, we use “model family” to refer to generic class or functional form of parametric distributions, while ”model” often refers here to a member of the class for an instantiation or selection of parameters. This distinction is not so important for the examples presented in Sections 2.1-2.3, but becomes more so in Section LABEL:instability-results where model instability depends on both form and a given parameter configuration) For illustration, Sections 2.1-2.3 present three specific examples of FOES model classes, including models with deep architectures.

2.1 Discrete Exponential Family Models

For random variables with sample space , , consider an exponential model family for with probability mass function given by

| (1) |

depending on parameter vector and natural parameter function with fixed positive integers and denoting their dimensions. Above, is a vector of sufficient statistics, while

denotes the normalizing function with parameter space . The natural parameter function has a linear form (i.e., for a given matrix ) in many common model formulations, though may also be nonlinear (e.g., curved exponential families). In the linear case, may be generally assumed in the exponential parameterization with a minor modification to the definition of sufficient statistics .

Such discrete exponential models are special cases of the FOES models, as seen by defining , , based on (1) and a parameter sequence . For example, if observations correspond to independent and identically distributed Bernoulli random variables, each indicating a binary - outcome, the resulting probabilities have exponential form (1) given by

| (2) |

with sufficient statistic and “log odds ratio” parameter . More generally, supposing represent independent trials, each assuming an outcome among possibilities (e.g., a die roll), a multinomial distribution is given by

| (3) |

with sufficient statistic involving a count for each outcome , where denotes the indicator function, and parameters defining log-probability ratios . In addition to such standard models for discrete independent data, exponential models of FOES type commonly arise with dependent spatial data (Besag,, 1974) and network/relational data (Wasserman & Faust,, 1994; Handcock,, 2003). For a random graph or network with, say, nodes , consider random edges where the th edge is associated with a pair of nodes and a binary variable indicating presence/absence of an edge among the node pair , . Here the length of the edge variable sequence increases as a function of node number and corresponding exponential models often incorporate graph topographical features derived from . As an example, consider a graph model of exponential/FOES form prescribed by

| (4) |

involving the numbers of edges, 2-stars and triangles among an outcome given by , and , respectively, along with real parameters . For this network model (4) in particular, as well as for more general models of form (1), Schweinberger, (2011) considered instability in such exponential models with sequences of fixed parameters , , of fixed dimension .

For model sequences of the exponential type (1), such as those in (2)-(4), note that the dimension of the parameter necessarily remains the same for all sample sizes as the form of the natural parameter function in (1) and the number of sufficient statistics do not depend on . Consequently, lies in a parameter space of fixed Euclidean dimension . However, this aspect need not be true for other types of FOES models considered in Sections 2.2 - 2.3, where instead the numbers of parameters and sufficient statistics commonly increase with the sample size .

2.2 Restricted Boltzmann Machines

A restricted Boltzmann machine (RBM) is an undirected graphical model specified for discrete or continuous random variables, with binary variables being most common (cf. Smolensky,, 1986). A RBM architecture has two layers, hidden () and visible (), with conditional independence within each layer. Let denote the random variables for visibles with support and denote the random variables for hiddens with support where . For specified parameters , , and as a real matrix with dimension , the RBM model for has the joint probability mass function

| (5) |

with normalizing function . Let , with , denote a given parameter vector for the RBM, as indexed by the number of visible random variables (which may differ from the actual lengths of these parameter vectors). The probability mass function for the visible variables follows from marginalizing the joint specification to yield

| (6) |

Here the baseline model (5) for hidden/visible variables is a linear exponential one in sufficient statistics using from (5), but the form differs from the previous exponential models in (1) in that the lengths of parameters and statistics increase to incorporate more visible variables. That is, in contrast to (1), the natural parameter function involved in the RBM model (5), as the identity mapping of the parameters , naturally grows in dimension to accommodate visible variables of increasing data size . Additionally, one may further arbitrarily choose the number of hidden variables in the joint RBM model (5) to define a marginal model (6) for the visible variables , and the number of hiddens may also potentially increase with . Because and for all , the RBM specification (6) for visibles

We now present a formal definition for instability of FOES models as well as a simple condition for identifying instability in a FOES model sequence. The basic intuition is that, if the smallest and largest probabilities from a given model are “too different,” then instability may arise, which manifests as extreme sensitivity in other probability behavior: large shifts in probability may be associated with only small differences in the input space for FOES models, and is related to a particular model placing almost all probability on a subset of potential outcomes. We present both non-asymptotic (Theorem 2.2) and asymptotic (Theorem 2.3) results to this effect.

2.4 A Criterion for Instability

To define a measure of instability in FOES models, it is useful to consider the behavior of data models , again supported on a set of outcomes for and for a prescribed configuration of parameters , in connection to the sample size . A relevant quantity to this end is a log-ratio of extremal probabilities (LREP), defined as

| (7) |

based on maximum and minimal model probabilities. In what follows, the main idea is that instability, and other negative model features, can be associated with a FOES model formulation for random variables where the LREP (7) is overly large relative to the sample size . That is, a sequence of FOES probability models results in specifying a distribution of observations for each sample size (dependent on the prescribed values for , ) and instability will generally occur among these models whenever the corresponding LREP (7) grows faster than . This leads to the following definition.

Definition 2.1 (S-unstable FOES model)

A FOES model formulation for , based on parameter specification , , is Schweinberger-unstable or S-unstable if

| (8) |

as the number of variables increases ().

In other words, a model is S-unstable if is an unbounded sequence of sample size ; namely, given any , there exists an integer so that holds for all . A FOES model formulation may be termed S-stable if it fails to be S-unstable, i.e., if is bounded.

This definition of S-unstable is a generalization or reinterpretation of “unstable” used in Schweinberger, (2011) by allowing possibly non-exponential family models (e.g., RBM and DBM models in Sections 2.2-2.3 as well as a potentially increasing number of parameters through the parameter sequence . While this definition differs in form and scope from the original, it does match that in Schweinberger, (2011) for the special case of exponential models (cf. Section 2.1 considered there which translates to , , in our model notation). Note the definition (8) of model instability depends intricately on the prescribed parameter sequence or the particular parameter values indexing the distribution . This also agrees with the notion of unstable distributions from Schweinberger, (2011), as well as other characterizations of distributional stability in networks (cf. Handcock, (2003)), that model instability is crucially tied to the parameter configuration (i.e., where lies in the parameter space) in addition to distributional form. Hence, a given model family or form may may result in an unstable/stable model, depending on the parameters chosen. Section 3 provides several examples of unstable models as well as causes for model instability, where the latter may often be traced to issues in model form (i.e., data functions) and/or type of parameterization. We next describe several potentially undesirable features associated with S-unstable FOES models.

Remark 2.1

Different notions of model stability/instability exist. For example, Handcock, (2003) refers to how small changes in parameters may dramatically change a probability mass function, while Kaiser, (2007) discusses how interpretation of model parameters and conditional expectations may break down in parts of the parameter space. However, these may be intuitively connected in the sense that the same (undesirable) parameter/model configurations may often be associated with varying conceptualizations of instability. While beyond the scope of the current paper, Kaplan et al., (2019) investigates and numerically demonstrates some such connections for a class of RBM models. Section 4.3 also explains one relation between our notion of stable models and parameter interpretation in centered models (Kaiser & Caragea,, 2009, cf.).

Remark 2.2

In the definition (8) of S-instability, we note that the numerical measure of model instability is invariant to independent replications of data. Consequently, the definition of an S-unstable model is unaffected by independent replication and all instability properties may be characterized by those of one observation from the common FOES model. Remark A.2 of the Appendix provides more details.

2.5 Characterizations and Consequences of Instability

As a basic characteristic, S-unstable FOES model sequences have extremely sensitive probability structures. One aspect is that small changes in data configuration can lead to very large changes in probability. Consider, for example, the quantity given by

which represents the biggest log-probability ratio for a one-component change (i.e., the data vector differs in exactly one component value) in data outcomes in a FOES model with parameter . This is the smallest difference possible between two data vectors, making it a good notion of a small distance in the input space and has been similarly used by Schweinberger, (2011, , Sec 2.2). We then have the following result prescribing the behavior of for S-unstable FOES models.

Theorem 2.2

Let , with support , , be a sequence of FOES models.

- (i)

-

(ii)

Suppose the FOES model sequence is S-unstable. Then, for any there exists such that for all , there exist outcomes , differing by one component, such that

Theorem 2.2 aims to describe some model implications when a log-ratio of extreme model probabilities (7) is too large relative to the associated sample size , which underlies the definition of a S-unstable FOES model (8). If so, Theorem 2.2(i) guarantees the FOES model must also exhibit correspondingly large changes in probability for small differences among some data configurations. Hence, as a further consequence in Theorem 2.2(ii), S-unstable models can never have universally bounded changes in probability among single component variations in data configurations. While not all one-component changes in data may produce massive changes in probability, unstable models must have some such data outcomes with this property. Hence, unstable probability structures may exhibit extreme sensitivity through large peaks and troughs over the sample space. Theorem 2.2 supports and generalizes findings in Schweinberger, (2011, Theorem 1) for classes of discrete exponential models (i.e., the result there entails that, if is unbounded as increases, then the nearest-point log-odds ratio is unbounded as well in these models).

Additionally, S-unstable FOES model sequences are also connected to degenerate models, where degeneracy involves assigning essentially all probability to modes within the sample space, which could potentially represent a small subset among the totality of outcomes. For perspective, note that differing sizes of the scaled log-ratio from (7) induce a spectrum of levels of instability/stability and Theorem 2.2 indicates increasing sensitivity of model probabilities as (7) increases. Furthermore, as the instability measure grows and the log-ratio diverges, as in the definition (8) of S-unstable models, then a FOES model sequence will become degenerate. Theorem 2.3 provides a formal statement of such degeneracy due to S-instability. For a given , define a -modal set of outcomes as

| (9) |

In other words, as the sample size grows in S-unstable FOES models, all probability tends to concentrate mass on an -modal set, where can be made arbitrarily small. Intuitively, the occurrence of such degeneracy can be explained by a type of “reverse” pigeonhole principle for unstable FOES models: if all outcomes should receive positive probability but the maximal probability far exceeds the minimal one in the model, then little probability remains for distribution among remaining model outcomes (i.e., if nearly all available pigeons are stuffed into one hole, the remaining pigeonholes must have few occupants). Degeneracy in unstable models can pose dangers in data modeling as well, particularly when a mode set represents a narrow collection of outcomes among those realistically possible for adequately describing data. In which case, model outcomes may fail to look like data of interest.

Connected to degeneracy, S-unstable FOES models may also exhibit additional kinds of extreme and undesirable sensitivity in probabilities if model parameters can further be “dialed” between positive and negative values. That is, some FOES models naturally involve parameter spaces covering a positive-negative spectrum of parameter possibilities, where the signs of parameters provide a standard device for increasing or decreasing probabilities of outcomes in the model formulation. In fact, for many models, the switch of a parameter sign serves to produce reciprocal probabilities, as outlined in the following model assumption about parameter sign reversal (PSR).

Model Condition PSR (Reciprocal Probabilities from Parameter Sign Reversal): Let , with support , , represent a sequence of FOES models. For each and any outcome , suppose it holds that

where and denote the maximum and minimum probabilities under parameters and , respectively.

The above model condition incorporates many standard parameterizations and follows, for instance, whenever holds for outcomes in a FOES model. For instance, this latter condition is fulfilled for all linear exponential families from Section 2.1 (e.g., (2)-(4)) as well as all network models from Sections 2.2-2.3 (e.g., (5)-(6)). When parameters can be tuned in sign with effects prescribed in the model condition PSR, unstable FOES models will exhibit further probability sensitivities, as outlined in the following extension of Theorem 2.3.

Corollary 2.1

Let , with support , , be a sequence of FOES models satisfying model condition PSR. If the models are additionally S-unstable, then

-

(i)

the models defined by are also S-unstable;

- (ii)

For unstable models, Corollary 2.1 shows that shifts in parameters around zero (i.e., from to ) can induce extreme changes in probability among subsets of the sample space, as another manifestation of instability and hyper-sensitivity in probability structure. For one-parameter exponential families, involving a fixed real-valued linear parameter and sufficient statistic in (1), Schweinberger, (2011, Theorem 3) proved a result similar in spirit, though based on a characterization there in terms of maximum and minimal values of the sufficient statistic. For this case in particular, mode sets have specific, and essentially complementary, forms over positive and negative parameters, namely, and for any , and Schweinberger, (2011, Theorem 3) showed each mode set collects all mass, under positive and negative parameters, respectively, with unstable models of this exponential type. However, for all unstable FOES models, Corollary 2.1 generalizes the same principle that unstable models can push all probability to different, and in fact disjoint, parts of the sample space, depending on how parameters fall with respect to zero. This feature can numerically complicate likelihood manipulations, such as maximization or MCMC-based Bayes posterior simulation, as further discussed in Section 4.

Remark 2.3

Under the model condition PSR, Corollary 2.1 can also be extended to cases where parameter components (say) are not all changed in sign (e.g., ) but, more generally, are instead altered to another parameter configuration involving a switch in sign only among some dominating model parameters with remaining parameters being arbitrarily chosen. If a change sign occurs among parameters () which dominate the probability structure of the model, then the results of Corollary 2.1 can still hold with replacing ; as an example of one sufficient condition, if holds in addition to Corollary 2.1 assumptions, where

represents a standardized form of -model probabilities, then the results of Corollary 2.1 apply to in addition to . As a consequence, an unstable model under can then imply that many more unstable models exist over a broader spectrum of possibilities for variations of , which involves some amount of sign change among components of .

3 Illustrations

Model instability can depend intricately on how functions of parameters and data are combined in the formulation of the model probabilities, though some general causes may be identified. As one issue, a broad parameter space (or wide interpretation of this space) may admit some parameters as technically valid that have an undue and often undesirable impact on the model structure for a prescribed data size . In this case, both the size and dimension of model parameters can be problematic and induce instability. In combination to this last point, further causes of instability may also be traced to the magnitude of statistics in the model. Potentially massive, and thereby unstable, statistics were the primary focus of instability studies of Schweinberger, (2011) for certain discrete exponential models having parameters/statistics of fixed dimension. However, as shown in the following, bounded statistics may still lead to instability if the parameter dimension is high. We next provide some examples to illustrate S-instability in FOES models, which also suggest some potential strategies for preventing unstable models (e.g., for many model types in the following, a control of the combined magnitudes of parameters can ensure S-stability, which is also discussed further in Section 4.3).

3.1 Equi-probability Models

As a baseline for comparisons, consider a simplistic model for with uniform probabilities over the sample space, say , , where each random variable has outcomes. In contrast to instability, model probabilities here are completely insensitive to changes in data outcomes across the sample space, and the associated log-ratio of extreme probabilities (7) is

which is as small as possible. In fact, a LREP value of zero can only occur for a FOES model having uniform probabilities, and such equi-probability models are always S-stable.

3.2 One-parameter Exponential Models

A fundamental model considered in the instability work of Schweinberger, (2011) involves a one-parameter exponential model corresponding to (1) with a real-valued parameter, say , and sufficient statistic . For such models, upon scaling by sample size , the log-ratio of extreme probabilities in (7) for assessing instability becomes

| (10) |

where and denote the maximal and minimal values of the single sufficient statistic. In this case, an S-unstable model results, by definition (8), whenever holds or, in other words, if the combined magnitudes of parameter and maximal difference in statistic values are overwhelmingly large relative to the sample size . If we further assume that is a fixed (non-zero) parameter for all , as considered in Schweinberger, (2011), then an S-unstable model results solely if the sufficient statistic admits a value too large relative to number of observations, i.e., if as . The latter aspect reflects the definition of Schweinberger, (2011), for this setting, that a real-valued statistic may be classified as unstable when holds and as stable otherwise (e.g., if ).

For illustration, consider the iid Bernoulli model (2) for with log-odds ratio parameter . Remark 3.2 (Section 2.4) then gives the model instability measure (8) directly as

so that an unstable (or stable) model results for a divergent (or bounded) parameter sequence . In this case, Schweinberger, (2011) has also noted that the statistic is stable (i.e., bounded ) and the Bernoulli model is as well when, in particular, is fixed for .

Alternatively, considering a random graph with edges among nodes, the exponential graph model from (4), when based purely on the number of of 2-stars or solely the number of triangles, , has a measure of instability from (8) as

by using the (one-parameter exponential) LREP formula (10) with statistic maximums for 2-stars or for triangles and with minimums in both cases. Because the variable number as the node number , both counts of 2-stars and triangles are unstable statistics in the sense of Schweinberger, (2011) (i.e., ). Furthermore, both types of graph models are always S-unstable for all possible of parameter sequences that are bounded away from zero (i.e., then holds, including the fixed parameter case from Schweinberger, (2011)).

3.3 Fixed-dimensional Linear Exponential Models

As a generalization of the one-parameter exponential case, we next consider linear exponential families (1) with parameters and sufficient statistics . Here the dimension of model parameters/statistics is fixed, and we next prescribe a condition helpful to avoiding instability in such models. For this, define and as the maximal and minimal values of the th statistic, , based on observations .

Proposition 3.1

Let , , denote linear exponential models (1) with parameters and statistics , for fixed . Then, the models are S-stable if

| (11) |

holds, i.e., if is bounded sequence of sample size .

Remark 3.1

Proposition 3.1 provides a sufficient condition for the stability of linear exponential models with fixed parameter dimension , whereby an S-stable model is guaranteed if the product of magnitudes of each combination of parameter and sufficient statistic value is bounded by the sample size , . This supports the findings of Schweinberger, (2011), who showed degeneracy follows in such models under one type of violation of the condition (11) in Proposition 3.1 (namely, involving non-zero parameters with statistics being bounded while one statistic diverges in maximal size faster than the number of observations). To further illustrate the result in Proposition 3.1, consider the multinomial distribution (3) for having categories and parameters . The variables are iid under this model so that Remark 3.2 (Section 2.4) yields the corresponding -scaled log-ratio of extreme probabilities (7) as

Hence, a multinomial model sequence is unstable (or stable) depending on whether (or not) the maximal parameter difference diverges. Furthermore, using that each of the sufficient (count) statistics from the multinomial model (3) satisfies , we see that (11) of Proposition 3.1 becomes purely a parameter condition, , for ensuring that is bounded and stability follows for the multinomial distribution. Additionally, a stable multinomial sequence (i.e., bounded ) turns out to be nearly equivalent to (11) (e.g., these are the same if the smallest parameter remains bounded).

When the condition (11) of Proposition 3.1 is violated, this aspect suggests a potentially unstable model that may be investigated more closely. For example, consider the exponential graph model from (4) involving counts of edges, 2-stars and triangles with fixed parameters for . If either the 2-star parameter or triangle parameter is non-zero, then holds in (11) by for 2-star and triangle statistics (), so that Proposition 3.1 hints that an unstable model may result when . Relatedly, a result from Schweinberger, (2011, Result 3) states that this model is unstable for all fixed parameters excluding cases or . However, more in line with the instability suggested by Proposition 3.1 , this model is unstable whenever (i.e., excluding ) ; Remark A.1 in the Appendix gives a proof. That is, instability holds even under the case potentially allowed by Schweinberger’s (2011) results. Thus, graph models of the form (4), with 2-stars and triangles are always S-unstable for all possible parameter sequences with bounded away from .

3.4 Latent Variable Models of Increasing Parameter Dimension

We next consider instability of discrete data models based on exponential formulations involving hidden, or latent, variables, such as those probabilistic graphical models described in Sections 2.2-2.3. We will focus on restricted Boltzmann machine (RBM) models (Section 2.2, having one layer of latent variables for simplicity, though the same instability concepts may be extended to other deep learning models (Section 2.3. For visible variables as data, each observation being binary, the RBM-based model (6) for is again of FOES-type, though not an exponential model. However, the distribution of visible variables is induced by an underlying joint exponential model (5) for both visible and latent variables , where denotes a vector of hidden variables (similarly binary). The joint model is of linear exponential form involving sufficient statistics given by and parameters corresponding to the visible variables (i.e., ), the hidden variables (i.e., ), and the cross-product variables (i.e., ). However, unlike some previous exponential models considered in Sections 3.2-3.3 (cf. Proposition 3.1, note that the RBM formulation always associates parameters with bounded statistics (i.e., the components of ) so that model instability cannot arise here due to the magnitude of sufficient statistics exceeding the sample size . Instead, RBM instability may be linked solely to parameter configuration and the fact that the number of parameters necessarily increases with the number of observations , in contrast to previous exponential cases of fixed parameter dimension.

To highlight the instability issues for the RBM model, consider a simple model for visibles with no hidden variables (), for which model statements (5)-(6) coincide. An independence model then results for variables in , which has parameters , and the measure of model instability becomes

Hence, this model sequence for will be S-unstable if the aggregation of absolute parameters grows faster than the number of parameters/visible variables. Consequently, even for the simplest RBM model involving independence, preventing instability requires careful choice of parameters, particularly with regard to how a parameter configuration differs from zero. For more general RBM models, the number of hidden variables can also be chosen arbitrarily (i.e., as some function of ), which can substantially inflate the number of model parameters and further impact model instability through accumulated parameters. To better understand the effects of instability in the RBM structure, Proposition 3.2 next frames the general behavior of extreme probabilities in the joint RBM model (5) for and the implied RBM data model (6) for alone. Specifically, critical measures of instability may be closely connected in both models through tight bounds on their respective LREP values (7). As a result, Proposition 3.2 shows how an unstable distribution for observations may be traced to sources of instability in the original joint distribution for . This also suggests a device for avoiding instability, as provided next.

To state the result, let denote the LREP value (7) from the marginal distribution of visibles in (6) and write the LREP for the joint distribution of from (5) as

written as a function

| (12) |

of outcomes , and parameters , with , and denoting respective parameter components, , . Due to the marginalization steps in defining the distribution (6) of , note that has no immediate analytical expression similar to that of . For clarity, recall also that S-instability (8) in each model type refers to a respective divergence (i.e., , ) upon scaling by the corresponding number of variables in a distribution. In the following, let denote the L1 norm of a generic vector , .

Proposition 3.2

Let denote a RBM-based data model (6) for visible variables derived from as the joint RBM distribution (5) of involving some number of hidden variables and parameters . Then,

- (i)

-

(ii)

The instability measure for the joint model of satisfies

for

and based on a function of hidden variable outcomes and visible-related parameters and .

-

(iii)

Assuming additionally, then the following properties 1.-7. hold:

-

1.

an S-unstable visible model is equivalent to the condition ; further, is stable when , , is bounded.

-

2.

an S-unstable joint model is equivalent to the condition ; further, is stable when , , is bounded.

-

3.

if the visible model is S-unstable, then the joint model is also S-unstable.

-

4.

when , both and are necessarily S-unstable.

-

5.

when , the joint model is necessarily S-unstable.

-

6.

when , the visible model being S-stable or S-unstable is equivalent to the joint model being stable or unstable.

-

7.

an S-stable visible model results if

for some , while an S-stable joint model results if

-

1.

Remark 3.2

The condition in Proposition 3.2(iii) is often mild in practice (i.e., the number of hidden variables is typically not excessively larger than the number of visible observations). This allows instability results for both marginal and joint RBM models to be more readily stated together, as the numbers and of variables in these models become asymptotically equivalent.

With regard to instability and the effects of different parameter types, the relationships between RBM models in Proposition 3.2(iii) follow from the bounds on model instability measures in Proposition 3.2(i)-(ii). Generally speaking, all instability in the marginal RBM model for the data can be attributed to an excessively large model quantity , which predominantly follows when main and interaction parameters related to visible variables are too large in magnitude (e.g., upon accumulation in terms such as , or ). For example, for any bounded sequence of hidden parameters, main visible parameters that are too extreme () will guarantee instability in the visible model (). In fact, the instability measure for marginal/visible model represents a clearly smaller portion of the instability measure in the joint RBM model . This implies that an unstable marginal model (i.e., due to , ) must always translate to an unstable joint model and that further potential causes of instability exist for the joint model, often due to the size .

While the joint RBM model for must always be unstable due to a diverging combination of visible and/or interaction parameters ( or ) (Proposition 3.2(iii.2)), instability for the joint model can also result when the main hidden parameters become too large relative to sample size ( in Proposition 3.2(iii.5)). However, under Proposition 3.2, the main hidden parameters do not necessarily entail a source of instability for the marginal visible model . When the hidden parameters are bounded relative to the sample size (), then all instability in both the joint and marginal RBM models can be directly linked to excessively large visible and/or interaction parameters so that features of stability/instability must be the same across both models (Proposition 3.2(iii.6)). Hence, to prevent instability in the joint model, the combined magnitudes of all parameters must be controlled (cf. Proposition 3.2(iii.7)), while a stable visible data model technically results from constraining only the sizes of visible-related parameters , . Nevertheless, because the joint model often is employed in practice for purposes of simulation and simulation-based inference, it is still reasonable to consider parameter choices for ensuring a stable joint model (and, consequently, a stable visible model as well). Further evidence of this is seen in the following numerical example.

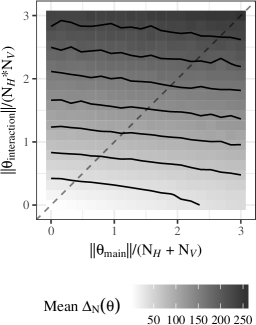

In our numerical experiment, we allow the two types of terms (main effects terms corresponding to visible and hidden parameters and interaction parameters ) to have varying average magnitudes, and for a RBM with visibles and hiddens. These average magnitudes vary on a grid between and with breaks, yielding grid points. At each point in the grid, vectors () are sampled uniformly on a sphere with radius corresponding to the first coordinate in the grid and vectors () are sampled uniformly on a sphere with radius corresponding to the second coordinate in the grid via sums of squared and scaled iid Normal variables. These vectors are then paired to create values of with magnitudes at each point in the grid. The values and are then calculated for each and then summarized for each point in the grid using the sample mean. The results of this numerical study are shown in Figure 1. From these two plots, it is clear that for larger magnitudes of the parameter vectors, there is evidence of S-instability in that the log-ratio of extremal probabilities scaled by and the the biggest log-probability ratio for a one-component change in data outcomes are both increasing away from , further supporting 3.2(iii.2 and iii.5).

In more complicated graphical models involving further or deeper hidden layers, the same issues and causes of instability similarly exist, but are compounded by a greater number of model parameters and depend on the configuration of the particular models in consideration. Consider the following two models – a RBM with visible nodes and one hidden layer with nodes and a deep RBM with visible nodes and layers, with and hidden nodes respectively such that . The length of the parameter vector in the single layer RBM is then equal to , whereas the length of the parameter vector in the two layer RBM is . If , then the deep model will have more parameters, if , then the deep model will have less parameters, and if , then the deep model will the same number of parameters as the single layer RBM. S-unstable joint models will similarly follow if the combined sizes of all parameters are too great relative to the total number of variables, while instability in the data model for visible variables will depend only on the main or interaction parameters directly related to visibles (i.e. all the parameters for the single layer RBM and only the parameters for the visible layer, layer , and the interactions between them for the two layer RBM) and how their accumulated magnitude compares to the observation sample size . This indicates that for the name number of hidden variables , a deeper, rather than a wider, structure can be beneficial when considering instability in the data model for visible variables. However, as the size of a model considered grows, this point becomes moot.

4 Statistical Consequences of Instability

Due to sensitivity in the probability structure of an unstable FOES model, S-instability may often translate to numerical complications, and in fact obstructions, in both simulation and statistical inference based on likelihoods. We describe these aspects in Sections 4.1-4.2 with regard to data simulation, maximum likelihood estimation and Bayes inference.

4.1 Implications for Maximum Likelihood Inference

Volatility in the probability structure of an unstable model can also hamper efforts to maximize likelihood functions in statistical inference. When a FOES model is unstable along a parameter sequence , the same model can further be unstable along parameters in an opposite direction from the origin (model condition PSR and Corollary 2.1). This can translate into potential sensitivity of the likelihood function around zero, and lead to numerical complications in maximizing the objective function. We next provide a discussion of this issue in a way that builds upon and extends related findings by Schweinberger, (2011), who largely focused on the case of one-parameter exponential models.

With many probability models, the modes and anti-modes in the probability structure under one parameter are reversed in role when the parameter sign changes . Because unstable models tend to degeneracy, the opposite signed parameters further push unstable models to assign nearly all probability to extremely opposite data configurations, given by modes/anti-modes. This is made concrete in Theorem 4.1, relating the degeneracy from unstable models to the expected behavior of log-likelihood functions.

Theorem 4.1

Let , , denote an S-unstable FOES model sequence, which additionally satisfies model condition PSR. Let denote, respectively, a mode and anti-mode of the model , , for observations , whereby and .

Then, letting denote convergence in probability and expectation, as ,

under while

under , where

Theorem 4.1 implies log-likelihood functions based on unstable models are both inversely related and degenerate at opposited signed parameters or , so that likelihoods are highest at different extremes in data configuration (e.g., under -probabilities or under -probabilities). If the observed outcome for data is not a mode/anti-mode, then probabilities for the outcome may be small under both parameters and , in which case associated optimization steps may then shift around zero and struggle to converge.

In many model formulations, the zero parameter is a “safe” position among parameters, representing a guaranteed stable model (having uniform probabilities among outcomes), which can also tether a broad parameter search attempted among unstable models. Handcock, (2003) describes similar results for degenerate exponential models, and Theorem 4.1 also supports an important finding of Schweinberger, (2011, Corollary 1) for one-parameter linear exponential models (1). In the latter case, the likelihood score function at is the expected value of the sufficient statistic , and optimization involves solving for an observed outcome . For unstable models in this exponential class, Schweinberger, (2011, Corollary 1) shows that

where again and denote the maximum and minimum values of the statistic , . As described by Schweinberger, (2011), the implication for maximum likelihood estimation is that, unless an observed outcome falls at an extreme (i.e., modes/anti-modes), optimization steps in the parameter space can iterate in relatively small increments around zero and fail to converge. For unstable one-parameter exponential models, the maximum likelihood results of Schweinberger, (2011) turn out to be a special case of Theorem 4.1 and the LREP expansion (10) in this setting; namely, for an unstable model with ,

holds as by Theorem 4.1, while under

Again, when all probability in unstable models may be pushed to opposite extremes in the sample space, due to a combination of degeneracy and parameter sign, numerical complications in likelihood maximization may occur.

4.2 Implications for Bayes Inference

The potential numerical difficulties with maximum likelihood with unstable models, as described in the previous section, can naturally carry over to Bayes inference. Considering that the degeneracy issues related to unstable models can cause likelihoods can be flat (e.g., near zero) for many parameters under a given data outcome and that sign changes in parameters can shift tremendous probability to extreme and opposite outcomes in the sample space (e.g., Corollary 2.1, Theorem 4.1), then numerical complications may arise with Bayes inference in sampling a posterior parameter space based on MCMC. Instability may hinder effective chain mixing, related to the findings of Handcock, (2003) and Schweinberger, (2011) with exponential graph models. For example, a Markov chain may become entrapped within a mode, and fail to adequately mimic the overall occupation frequencies required for a reasonable MCMC distributional approximaton. If modes of the unstable model are not unique, then important outcomes may be missed without multiple chains or impractically enormous numbers of MCMC samples. This mixing problem is due to the unstable stationary distribution (unbounded ratios of probabilities under the joint model), rather than in any particulars of the MCMC algorithm. Hence, in the Bayes setting for sampling a posterior distribution for , a chain may be unable to effectively explore the parameter space due partly to extreme and potentially unbounded probability ratios from parameter sign changes.

For example, if denotes a prior density for and denotes a proposal distribution for use in a Metropolis-Hastings (MH) sampler, then MH acceptance probability becomes

which indicates how parameter sensitivity in the likelihood may complicate sampling of the posterior (i.e., moving from to in the parameter space). Furthermore, the potential for model instability and the size of the parameter space can also become greater with the introduction of latent variables to existing data variables, as involved in some model formulations described in Sections 2.2-2.3. As latent variables are often sampled with parameters in a Bayes MCMC approach, this aspect may further compound numerical problems in chain mixing.

4.3 Fitting Stable Models

The instability results presented in Section LABEL:instability-results also suggest the potential use of regularization and penalization as a solution to avoid instability when fitting FOES models. One example of a rigorous approach to penalization can be found in Kaplan et al., (2019), which employs Bayesian fitting for a single layer RBM using multivariate Gaussian priors with constrained covariance matrices to control the sizes of the parameter values. For example, considering a latent variable model described in Section 3.3, Proposition 3.2(iii) suggests how parameter contributions from sources of “main hidden,” “main visible,” and “interaction” parameters may each be constrained (relative to the visible variable sample size ) to ensure model stability. In a Bayes inference framework, priors can be developed so that parameters are then appropriately bounded (in a stochastic sense) to lie in a parameter subset compatible with stability. For example, for a latent model with numbers , and for hidden, visible and interaction parameters, respectively, Proposition 3.2(iii.7) suggests a potential prior specification where parameters have root second moments bounded by the parameter type: , , and for visible, hidden and interactions parameters with a constant (i.e., so that the condition in Proposition 3.2(iii.7) holds in a stochastic sense). The same general strategy can apply with other models with results from Section 3, and the adequacy of the subsequent fitted model might then be assessed.

As opposed to approaches for fitting (e.g., penalization as above), the findings here on model stability/instability also support alternative strategies to model formulation and re-pameterization using “centered conditional” distributions (cf. Kaiser,, 2007); see Kaiser & Caragea, (2009) and Kaiser et al., (2012) for applications with spatial data and Casleton et al., (2017) for network data. In a joint model , these authors consider associated (full) conditional distributions and re-parameterize by centering/averaging sums in the expression of in order to separate model effects between “mean” and “dependence” parameters. The intent is to improve model interpretation and help detect degeneracy (characterized by the “mean parameters” in the model failing to match averages observed in data generations from the model and attributable to large “dependence parameters”). The works above describe advantages of such centered parameterizations based on empirical studies, but findings here also support these parameterizations as useful for avoiding model instability, where the corresponding “centered” models can be checked for ratios that are bounded over wider possible parameters than “uncentered” counterpart models. For illustration, the appendix provides details on a graph model example.

5 Concluding Remarks

For a large class of models that covers a broad range of applications (including “deep learning”), we have developed a formal definition of instability in model probability structure and elucidated multiple consequences of instability. We have shown for FOES models that instability manifests through a large amount of probability being placed on a subset of the theoretically possible realizations that may be narrower than intended. Such instability is often due to a complex interaction between the model statistics used (i.e., how numerous and large these may become) and the number and magnitudes of parameters in the model formulation. For many FOES models, the possibility exists, at least in principle, to constrain parameters in a way that balances their potential contributions against those of model statistics in order to prevent probability instabilities. While the results on instability here only address model formulations with finite sample spaces, the same underlying principles might be extended to models for continuous data as well by discretizing the model (i.e., binning outcomes into intervals), as data typically have some given level of discretization. Such a generalization could help toward understanding potential model instability in a wider class of data applications. As it sits currently, the FOES model class is quite broad and findings here can help in identifying undesirable probability features in such models.

Appendix A Proofs of instability results

Proof of Theorem 2.2. For part (i), we prove the contrapositive, supposing that holds for some and show . Let and . Note there exists a sequence in of component-wise switches to move from to in the sample space (i.e. differ in exactly component, ) for some integer . Under the FOES model, recall holds so that is well-defined for each outcome . Then, if , it follows that

using and . If , then and the same bound above holds. This establishes part (i). To show part (ii), note the definition of S-instability (i.e., ) combined with part (i) implies that .

Proof of Theorem 2.3. As holds in the FOES model, we may suppose ; otherwise, has one outcome and the model is trivially degenerate for all . Fix and write and . Then, , so . If , then by definition holds so that

From the lower bound on and the upper bound on , it follows that

as by the definition of an S-unstable FOES model (8). Consequently, as as claimed.

Proof of Corollary 2.1. The model condition PSR implies that

| (13) |

so that the log-ratio is the same for both and in (7). Now part (i) of Corollary 2.1 follows from as in (8). To show part (ii), fix and consider a -mode set under from (9). If , then, by definition,

holds, which is equivalent to

by model condition PSR and (13). The latter is in turn equivalent to

| (14) |

so that if and only if (14) holds. Next consider the -mode set under from (9). If , then by definition fulfills (14) and so , showing that . By this and the fact that that Theorem 2.3 and Corollary 2.1(i) entail that as (i.e., is S-unstable), we have

proving Corollary 2.1(ii)

Proof of Proposition 3.1. For any two outcomes , the log-ratio of probabilities from the linear exponential model (1) with parameters/statistics satisfies

consequently, holds in (7) and model stability in Proposition 3.1 follows from (8).

Proof of Proposition 3.2. Writing and with all components , probabilities in the joint RBM model (5) can be written as in terms of the function from (12) and the normalizing constant from (5). Let be such that and under the marginal RBM model from (6). Also, be such that and . Then, Proposition 3.2(i) follows from and the lower/upper bounds on and as

and

To prove Proposition 3.2, we next expand the function from (12) as

By this and the fact that , we then have

| (15) |

where , and . From this, it follows that

which leads to the upper bound . Then, taking (i.e., before maximization) gives and taking , such that , gives ; this yields the lower bound .

We next consider and, by (15), write

Taking and maximizing over both produces the upper bound . Then, using and maximizing over gives , while setting for such that gives . Finally, note that for any , the triangle inequality gives

Proof of Theorem 4.1. Let , where again and . As , convergence of to 1 in probability under is equivalent to convergence to in expectation under (i.e., convergence in expectation implies probabilistic convergence by Markov’s inequality while probabilistic convergence implies convergence in expectation by uniform integrability/boundedness).

For , let denote a modal set as in (9). By Theorem 2.3, holds as and, by definition of (9), follows if and only if . Hence, holds under in Theorem 4.1. The convergence under likewise follows from Corollary 2.1.

Remark A.1

Consider the exponential graph model from (4) involving counts of edges, 2-stars and triangles with fixed parameters for . This model is unstable whenever . To see this, consider an even number of nodes and let denote the data outcome in with all edges being zero, let denote the outcome with all edges being 1, and let denote the edge configuration from dividing the nodes into two equal groups, with no edges within a group and all edges between the groups (so that no triangles exist in ). Then, the -scaled log-ratio (7) for the exponential graph model (4) can, by definition, be bounded below by

a similar expression also holds for an odd node number . Consequently, for all fixed parameters excluding , then follows and the graph model with 2-stars and triangles is S-unstable, as suggested by the breach of Proposition 3.1 for this model when .

Remark A.2

Let denote a possible number of replications and consider data formed by as iid replications of a random vector , where the latter follows a FOES model with probabilities , . This leads to a joint model, say , , for consisting of random variables in total. Then, the LREP for , scaled by associated size, is given by

where denotes the log-ratio of extremal probabilities for defined from (7). That is, due to iid properties, the sample-size corrected LREP for equals the analog, , from the underlying common data model for alone, regardless of the level of independent replication. Hence, the definition of an S-unstable model is unaffected by independent replication. For computational purposes, this aspect also implies that if the original data in a FOES model consist of iid random variables, then the size-scaled log-ratio (7) may be calculated as

based on the extremal probabilities of just one random variable .

Appendix B Details on Centered Graph Example

To illustrate centered model parameterizations and n examination of stability in these, consider the two-star model (4) for the edges in simple graph with nodes and binary edge-variables . Here a common or standard parameterization in (4) leads to a conditional probability of “” for an edge as

based on summing other edge observations in a neighborhood to edge (i.e., edges , marked by pairs of graph vertices , that share a common vertex with edge marked by the vertex pair ). In contrast, a centered conditional would yield

involving a parameter for and as the size of (cf. (Kaiser & Caragea,, 2009)); the corresponding joint model would involve parameters and in (4). The purpose of the centerization is to have represent a model mean parameter (note is the edge proportion/probability under independence ), while a separate parameter (for dependence) modifies the conditional probability of “” up/down from , depending on neighbors or 0. A similar interpretation does not hold in the uncentered model; see (Kaiser & Caragea,, 2009) and (Casleton et al.,, 2017) for a discussion of the centered parameterization in spatial and network modeling, where the intent is to improve parameter interpretation and help detect degeneracy (e.g., intuitively given by large dependence parameters , so that fails to correspond to the mean or the marginal proportion of ’s in data generations from the model). However, from a different perspective using the model measures here, centered parameterizations also lead to models which are more stable over wider regions of the parameter space. To illustrate, in the standard/uncentered parameterization for a graph model (4) with only two-stars , our measure of model instability becomes , which is unbounded as for all non-zero parameters (i.e., all models with are S-unstable). However, in the centered parameterization with only two-stars, corresponding to and , the measure becomes

which is bounded, for any fixed , as increases (i.e., note is a conditional/neighborhood sample proportion while is a marginal proportion). This aspect owes to adjusting parameters by neighborhood sizes in centered conditional distributions, but centering also induces an additional effect of alternating signs in parameters (e.g., ). The latter has been suggested in other contexts with exponential graph models for regulating degeneracy (cf. Snijders et al.,, 2006).

References

- Besag, (1974) Besag, J. (1974) Spatial interaction and the statistical analysis of lattice systems. Journal of the Royal Statistical Society. Series B (Methodological), pages 192–236.

- Casleton et al., (2017) Casleton, E., Nordman, D. J. & Kaiser, M. S. (2017) A local structure model for network analysis. Statistics and Its Interface, 10(2), 355–367.

- Handcock, (2003) Handcock, M. S. (2003) Assessing degeneracy in statistical models of social networks. Technical report, Center for Statistics and the Social Sciences, University of Washington.

- Hinton et al., (2006) Hinton, G. E., Osindero, S. & Teh, Y.-W. (2006) A fast learning algorithm for deep belief nets. Neural computation, 18(7), 1527–1554.

- Kaiser, (2007) Kaiser, M. S. (2007) Statistical Dependence in Markov Random Field Models. Statistics Preprints, Paper 57.

- Kaiser & Caragea, (2009) Kaiser, M. S. & Caragea, P. C. (2009) Exploring dependence with data on spatial lattices. Biometrics, 65(3), 857–865.

- Kaiser et al., (2012) Kaiser, M. S., Caragea, P. C. & Furukawa, K. (2012) Centered parameterizations and dependence limitations in Markov random field models. Journal of Statistical Planning and Inference, 142(7), 1855–1863.

- Kaplan et al., (2019) Kaplan, A., Nordman, D. & Vardeman, S. (2019) Properties and Bayesian fitting of restricted Boltzmann machines. Statistical Analysis and Data Mining: The ASA Data Science Journal, 12(1), 23–38.

- Neal, (1992) Neal, R. M. (1992) Connectionist learning of belief networks. Artificial intelligence, 56(1), 71–113.

- Pearl, (1985) Pearl, J. (1985) Bayesian networks: A model of self-activated memory for evidential reasoning. Technical report, UCLA Computer Science Department.

- Ruelle, (1999) Ruelle, D. (1999) Statistical Mechanics: Rigorous Results. Imperial College Press, London.

- Salakhutdinov & Hinton, (2009) Salakhutdinov, R. & Hinton, G. E. (2009) Deep boltzmann machines. In International Conference on Artificial Intelligence and Statistics, pages 448–455. AI & Statistics.

- Schweinberger, (2011) Schweinberger, M. (2011) Instability, sensitivity, and degeneracy of discrete exponential families. Journal of the American Statistical Association, 106(496), 1361–1370.

- Smolensky, (1986) Smolensky, P. (1986) Information processing in dynamical systems: Foundations of harmony theory. Technical report, DTIC Document.

- Snijders et al., (2006) Snijders, T. A., Pattison, P. E., Robins, G. L. & Handcock, M. S. (2006) New specifications for exponential random graph models. Sociological methodology, 36(1), 99–153.

- Wasserman & Faust, (1994) Wasserman, S. & Faust, K. (1994) Social network analysis: Methods and applications, volume 8. Cambridge University Press, Cambridge.