Risk Aversion in the Small and in the Large under Rank-Dependent Utility

Abstract

Under expected utility the local index of absolute risk aversion has played

a central role in many applications.

Besides, its link with the “global” concepts of the risk and probability premia has reinforced its attractiveness.

This paper shows that, with an appropriate approach, similar developments can be achieved in the framework of Yaari’s dual theory

and, more generally, under rank-dependent utility.

Keywords:

Risk Premium; Probability Premium; Expected Utility; Dual Theory; Rank-Dependent Utility;

Risk Aversion.

AMS 2010 Classification: Primary: 91B06, 91B16, 91B30; Secondary: 60E15, 62P05.

OR/MS Classification: Decision analysis: Risk.

JEL Classification: D81, G10, G20.

1 Introduction

Under expected utility (EU) there exist various equivalent ways to evaluate the degree of risk aversion of a decision maker (DM). These measures were developed independently a little more than 50 years ago by Arrow A65 , A71 and Pratt P64 .111See also the early contribution (written in Italian) by B. de Finetti dF52 . Since then they have played a well-known and important role in the analysis of risky choices under EU.

The notion of risk aversion has also received attention outside EU. For instance, in the dual theory (Yaari Y87 ) or under rank-dependent utility (Quiggin Q82 ), Yaari Y86 , Chew, Karni and Safra CKS87 , Roëll R87 , Chateauneuf, Cohen and Meilijson CCM04 , and Ryan R06 have proposed various measures of risk aversion, but their approach is rather different from the local risk aversion approach of Arrow and Pratt (henceforth AP) in the EU model.222One exception is Yaari Y86 who proposes in a relatively little used paper the dual analog of the local index of absolute risk aversion. However, his analysis focuses on global aversion to mean-preserving spreads via a concavification of the probability weighting function.,333As is well-known, rank-dependent utility encompasses expected utility and the dual theory as special cases and is at the basis of (cumulative) prospect theory (Tversky and Kahneman TK92 ). For measures of risk aversion under prospect theory, see Schmidt and Zank SZ08 .

The purpose of this paper is to show that the analysis “à la AP” can be developed both in the dual theory (DT) and under rank-dependent utility (RDU). This goes by defining the appropriate notion of a “small risk”, which is small in payoff under EU, but small in probability under DT, and small in both under RDU. It reveals that for small risks under RDU the risk premium and the probability premium are simply the sums of the suitably scaled equivalent notions under EU and DT. As a result, AP’s approach turns out to be appropriate to measure the intensity of risk aversion also outside the EU model.

In this paper we refer to three measures of the degree of risk aversion: the risk premium, the probability premium and the local index of absolute risk aversion. Among these concepts, the probability premium was for a long time by far the least popular. However, because of its appealing nature, it starts now being discussed in the literature (Jindapon J10 , Liu and Meyer LM13 , Liu and Neilson LN15 , and Eeckhoudt and Laeven EL15 ). Initially, the probability premium was discussed by Pratt P64 for a binary zero mean and symmetric risk. We will stick here to this approach, even though it was very recently extended (Liu and Neilson LN15 ).

Our analysis shows that the probability (risk) premium under DT, obtained by defining the appropriate counterpart of the AP approach, exactly mimics the risk (probability) premium under EU. Our results also illustrate that the ratio of the second and first derivatives of the probability weighting function of DT plays a central role in dictating locally the respective risk and probability premia, and that the interplay between this ratio and the local index of absolute risk aversion of EU dictates these premia under RDU. We show furthermore that not only the local properties of AP’s approach can be obtained under DT and RDU, but that also the corresponding global properties are valid.

Our developments are made possible by appropriate comparisons between simple pairs of lotteries, just like under EU. In particular, the AP local risk aversion approach under EU defines the risk and probability premia by comparing a certain situation to a corresponding risky one with small payoff. To define the risk and probability premia under DT and RDU, we consider changes in situations that involve small probabilities for DT and joint small payoffs and small probabilities for RDU.

Our paper is organized as follows. In Section 2 we recall the local risk aversion approach of AP and the definitions of the risk and probability premia under the EU model. In Section 3 we develop the appropriate counterparts under the DT model and we provide the corresponding global properties in Section 4. In Sections 5 and 6 we extend our development to the RDU model. We conclude in Section 7. Proofs are relegated to the Appendix.

2 Preliminaries under EU

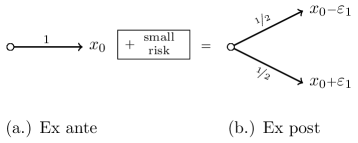

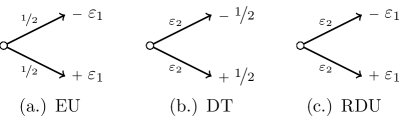

Consider an EU DM endowed with a certain initial wealth who takes a binary symmetric risk that pays off each with probability . His ex ante and ex post situations can be represented by Figure 1. (In all figures throughout this paper, the parameters and values alongside the arrows represent probabilities and those at the end of the arrows represent payoffs.)

This figure plots the initial situation and the situation after the addition of a small risk under EU.

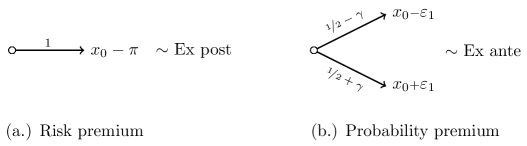

For this individual, the risk premium is defined such that with certainty is equivalent to the ex post situation. The probability premium denoted by is the increase in the probability of obtaining that makes the DM indifferent between the then resulting situation and the initial situation in which occurs with certainty. See the illustrations in Figure 2. (In all figures, the symbol indicates indifference.)

This figure visualizes the construction of the risk and probability premia under EU.

Formally, under EU, for a given initial wealth level and a given lottery payoff (with ) each occurring with probability , the risk premium is obtained as the solution to

| (2.1) |

with the decision maker’s (DM’s) subjective utility function. For ease of exposition is supposed to be twice continuously differentiable with . As is well-known implies .

As in the local risk aversion approach of Pratt P64 and Arrow A65 , A71 , we approximate the solution to (2.1) using Taylor series approximations. Upon invoking a first order Taylor series expansion of around , and a second order Taylor series expansion of around , we obtain the well-known result

| (2.2) |

omitting terms of order and .

Next, under EU, the probability premium is obtained as the solution to

| (2.3) |

Approximating the solution to (2.3) by invoking a second order Taylor series expansion of around yields

| (2.4) |

omitting terms of order . Thus, upon comparing (2.2) and (2.4), one finds that (the Taylor series approximations to) the primal risk and probability premia and are linked through

| (2.5) |

Under AP’s local risk aversion approach, is considered to be small and appearing in (2.2) and (2.4) is referred to as the local index of absolute risk aversion of EU.

3 Risk and Probability Premia under DT

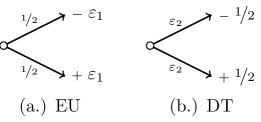

We now turn to DT. Rather than considering a binary symmetric risk with small payoff each occurring with probability as under EU, we now consider a binary symmetric risk with payoff each occurring with small probability . See the illustration in Figure 3.

This figure plots the small binary symmetric risks for EU and DT.

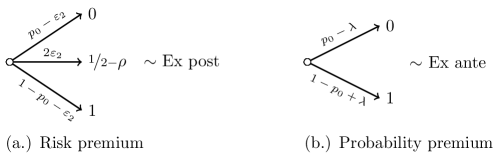

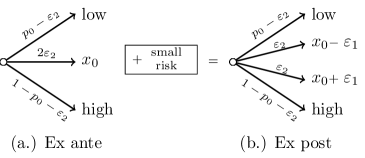

This binary symmetric risk with total probability mass of is added to an initial situation consisting of three states. The initial situation equals (middle) with probability and divides the remaining probability mass between wealth levels 0 (low) and 1 (high), as follows: with probability and with probability (). The binary symmetric risk is attached to the middle state of the initial situation such that, ex post, wealth level 0 occurs with probability and wealth level 1 occurs with probability . Attaching the small risk induces an equally likely change in payoff of in a state with total probability mass of . See Figure 4.

This figure plots the initial situation and the situation after attaching the small risk under DT.

We then define the dual risk premium, now denoted by to distinguish it from that under EU, such that indifference occurs between the ex post situation and a reduction of the wealth level (equal to the dual risk premium) in the middle state of the initial situation with total probability mass of .444One may say that this constitutes a -sure reduction in wealth, as opposed to a sure reduction in wealth as under EU. The dual probability premium answers the question of by how much the probability of the unfavorable payoff should be reduced and shifted towards the favorable payoff to restore equivalence with the initial situation. See the illustrations in Figure 5.

This figure visualizes the construction of the risk and probability premia under DT.

Formally, under DT, we define the risk premium as the solution to

| (3.1) |

with , mapping the unit interval onto itself with and and supposed to be twice continuously differentiable with , the DM’s subjective probability weighting (distortion) function.555Under DT, an -state risk with payoffs and associated probabilities is evaluated according to with by convention. Equivalently, the -state risk may be evaluated by distorting decumulative probabilities rather than cumulative probabilities, as follows: with . Note that , , and that is equivalent to . The condition , referred to as “strong risk aversion”, means that the DM is averse to any mean preserving increase in risk (Chew, Karni and Safra CKS87 and Roëll R87 ). Observe that the terms associated with the low and high wealth level states on the left- and right-hand sides of (3.1) partially cancel. Observe that where the AP local risk aversion approach under EU defines the risk and probability premia by comparing a certain situation to a corresponding risky one with small payoff, (3.1) defines the DT risk premium by comparing a constant situation with small probability to an equal probability risky one.666The same will be true for the dual probability premium and for the risk and probability premia under RDU.

Thus, we obtain the explicit solution

| (3.2) |

Approximating the right-hand side of (3.2), by invoking a second order Taylor series expansion of around , yields

| (3.3) |

omitting terms of order . Upon comparing (2.4) and (3.3) we find that the dual risk premium exactly mimics the primal probability premium. We also find that the risk premium under DT is dictated locally by the ratio of the second and first derivatives of the probability weighting function, .

This dual local index of risk aversion first appeared in Yaari Y86 , in the context of a concavification of the DM’s probability weighting function to which a uniformly larger dual local index is shown to be equivalent, when analyzing globally comparative risk aversion in the sense of aversion to any mean-preserving spread.

Next, under DT, we define the probability premium as the solution to

which reduces to

| (3.4) |

From (3.4), a first order Taylor series expansion of around , and a second order Taylor series expansion of around , yield hence

| (3.5) |

omitting terms of order and . Thus, by comparing (3.3) and (3.5), we find that (the Taylor series approximations to) the dual risk premium and the dual probability premium are linked through

| (3.6) |

and the local index is central to both premia. In particular, and are both increasing with respect to this dual local index of absolute risk aversion and with respect to the “size” of the risk represented by . Observe also the similarity to the (reverse) link between the probability and risk premia under EU displayed in (2.5).

4 Comparative Risk Aversion under DT

A concavification of an initial probability weighting function with into via the transformation , where is a twice continuously differentiable function mapping the unit interval onto itself with , , and , yields

The analysis in the previous section has revealed that if the dual local index of absolute risk aversion increases at a point , then the corresponding risk and probability premia increase, too, for “small risks”, i.e., binary symmetric risks with payoff each occurring with small probability ; see (3.3) and (3.5).

In this section, we show that not just the local properties of the previous section hold, but that also the corresponding global properties are valid. That is, we obtain for the DT an analysis that parallels the one of Pratt P64 , pp. 127-129. Specifically:

Theorem 4.1

The equivalence between (i) and (iv) can already be found in Yaari Y86 .

5 Risk and Probability Premia under RDU

We finally turn to RDU, which encompasses both EU and DT as special cases when the utility function or the probability weighting are the identity function, respectively. Under RDU we consider a binary symmetric risk that is small in both payoff () and probability of occurrence (). See the illustration in Figure 6.

This figure plots the small binary symmetric risks for the three models for decision under risk: EU, DT and RDU.

This small risk is added to an initial situation consisting of three states: a middle state at wealth level with total probability mass of occurrence equal to , and two states, one at a low wealth level and one at a high wealth level (that can be left unspecified as long as they are at least apart from ), subdividing the remaining probability mass as and (), respectively. The small binary symmetric risk is attached to the middle state of the initial situation and induces a payoff of (with ) each with probability , all else equal. See Figure 7.

This figure plots the initial situation and the situation after attaching the small risk under RDU.

The RDU risk premium then achieves indifference between the ex post situation (with the small risk added) and a reduction in wealth (equal to the RDU risk premium) in the middle state of the initial situation with probability of occurrence equal to . The RDU probability premium restores equivalence with the ex ante situation by shifting probability mass from the unfavorable payoff to the favorable payoff. See the illustrations in Figure 8.

This figure visualizes the construction of the risk and probability premia under RDU.

Formally, under RDU, we define the risk premium as the solution to777Under RDU, an -state risk with payoffs and associated probabilities is evaluated according to cf. footnote 5.

| (5.1) |

We approximate the solution to (5.1). First, upon invoking a first order Taylor series expansion of around , and a second order Taylor series expansion of around , we obtain

omitting terms of order and . Next, recalling (3.2) (and effectively taking a second order Taylor series expansion of around ) we obtain

| (5.2) |

omitting terms of order . Thus, we find that (the Taylor series approximations to) the RDU risk premium is simply obtained as the suitably scaled sum of the primal risk premium and the dual risk premium :

| (5.3) |

Observe also from (5.2) the interplay between the local indexes and in dictating locally the RDU risk premium.

Finally, we consider the probability premium under RDU, denoted by and defined as the solution to

| (5.4) |

We approximate the solution to (5.4) by first invoking a second order Taylor series expansion of around to obtain

omitting terms of order . Next, a first order Taylor series expansion of around , and a second order Taylor series expansion of around , yield

| (5.5) |

omitting terms of order and . We thus find that the (Taylor series approximation to the) RDU probability premium, , is connected to the (Taylor series approximation to the) EU and DT probability premia, and , through

| (5.6) |

Observe also from (5.2) and (5.5) that the RDU risk and probability premia are linked through

| (5.7) |

6 Comparative Risk Aversion under RDU

Just like under EU and DT, not only the local properties of the previous section are valid under RDU, but also the corresponding global properties are true. However, due to the simultaneous involvement of both the utility function and the probability weighting function, the proof of the global properties under RDU is more complicated than that of the analogous properties under EU and DT. Our proof is based on the total differential of the RDU evaluation, and the sensitivities of the risk and probability premia with respect to changes in outcomes and probabilities, respectively.

Theorem 6.1

Let , , and be the utility function, the probability weighting function, the risk premium solving (5.1) and the probability premium solving (5.4) for RDU DM . Then the following conditions are equivalent:

-

(i)

and for all and all .

-

(ii)

for all , all , and all .

-

(iii)

for all , all , and all .

-

(iv)

and are concave functions of and for all and all .

-

(v)

and for all and all .

7 Conclusion

We have extended the well-known Arrow-Pratt analysis of the risk and probability premia under expected utility (EU) to the dual theory (DT) and rank-dependent utility (RDU) models for decision under risk. By adopting the appropriate notion of a “small” binary symmetric risk, which is small in payoff under EU, but small in probability under DT and small in both under RDU, we have developed Taylor series approximations to the DT and RDU risk and probability premia. Our analysis has revealed that the development of the dual probability (risk) premium exactly mimics that of the primal risk (probability) premium. Furthermore, for small risks the RDU risk and probability premia appear to simply sum up the respective EU and DT premia, upon suitable scaling. Our analysis has also illustrated the central role of the probability weighting function’s concavity index and its interplay with the well-known utility function’s concavity index in dictating locally the DT and RDU risk and probability premia. Finally, we have also obtained the corresponding global properties under DT and RDU.

In the EU model the local index of absolute risk aversion has been extremely useful for the analysis of risky choices made by individuals or groups. Since a similar approach seems to be appropriate also for alternative models of choice under risk, this paper should open the way for their use in many applications such as portfolio composition, insurance coverage or self-protection activities.

Appendix A Proofs

Proof of Theorem 4.1. Invoking the appropriate notion of a binary symmetric risk that under DT has payoff each occurring with probability (), which is not necessarily small, and upon replacing the equation for the EU risk premium, (2.1), by that for the DT probability premium, (3.4), and the equation for the EU probability premium, (2.3), by the expression for the DT risk premium, (3.2), the proof follows essentially the same arguments as the proof of Theorem 1 in Pratt P64 . To save space we omit the details.

Proof of Theorem 6.1. The equivalence of (i), (iv) and (v) follows trivially from the equivalence of (a), (d) and (e) in Theorem 1 in Pratt P64 and the equivalence of (i), (iv) and (v) in Theorem 4.1 above.

We will first prove that (the equivalent) (i), (iv) and (v) imply (ii) and (iii). Reconsider (5.1). Fix (a feasible) (satisfying ). Note that if we let in (5.1), then . Define

We compute the total differential It is given by

Equating the total differential to zero yields

| (A.1) |

From (i), as in Pratt P64 , Eqn. (20),

Furthermore, from (v),

Taking yields

hence

for . In all inequalities in this paragraph, may be replaced by , with and restricted to .

Next, reconsider (5.4). Fix . If we let in (5.4), then . Define

We compute the total differential It is given by

Equating the total differential to zero yields

| (A.3) |

Invoking the inequalities associated with and above, where may be replaced by (upon restricting the corresponding domains to ), we find from (A.3) that

| (A.4) |

hence (iii).

We have now proved that (ii) and (iii) are implied by (the equivalent) (i), (iv) and (v). We finally show that (ii) implies (i), and (iii) implies (i), or rather that not (i) implies not (ii) and not (iii). This goes by realizing that, by the arbitrariness of , , and with , if (i) does not hold on some interval (of or ), one can always find feasible , , and , such that (A.2) and (A.4), hence (ii) and (iii), hold on some interval but with the inequality signs strict and flipped.

Acknowledgements. We are very grateful to Harris Schlesinger for discussions. This research was funded in part by the Netherlands Organization for Scientific Research (Laeven) under grant NWO VIDI 2009. Research assistance of Andrei Lalu is gratefully acknowledged.

References

- [1] Arrow, K.J. (1965). Aspects of the Theory of Risk-Bearing. Yrjö Jahnsson Foundation, Helsinki.

- [2] Arrow, K.J. (1971). Essays in the Theory of Risk Bearing. North-Holland, Amsterdam.

- [3] Chateauneuf, A., M. Cohen and I. Meilijson (2004). Four notions of mean preserving increase in risk, risk attitudes and applications to the Rank-Dependent Expected Utility model. Journal of Mathematical Economics 40, 547-571.

- [4] Chew, S.H., E. Karni and Z. Safra (1987). Risk aversion in the theory of expected utility with rank dependent probabilities. Journal of Economic Theory 42, 370-381.

- [5] Eeckhoudt, L.R. and R.J.A. Laeven (2015). The probability premium: A graphical representation. Economics Letters 136, 39-41.

- [6] de Finetti, B. (1952). Sulla preferibilita. Giornale degli Economisti e Annali di Economia 11, 685-709.

- [7] Jindapon, P. (2010). Prudence probability premium. Economics Letters 109, 34-37.

- [8] Liu, L. and J. Meyer (2013). Substituting one risk increase for another: A method for measuring risk aversion. Journal of Economic Theory 148, 2706-2718.

- [9] Liu, L. and W.S. Neilson (2015). The probability premium approach to comparative risk aversion, Mimeo, Texas A&M University and University of Tennessee.

- [10] Pratt, J.W. (1964). Risk aversion in the small and in the large. Econometrica 32, 122-136.

- [11] Quiggin, J. (1982). A theory of anticipated utility. Journal of Economic Behaviour and Organization 3, 323-343.

- [12] Roëll, A. (1987). Risk aversion in Quiggin and Yaari’s rank-order model of choice under uncertainty. The Economic Journal 97, 143-159.

- [13] Ryan, M.J. (2006). Risk aversion in RDEU. Journal of Mathematical Economics 42, 675-697.

- [14] Schmidt, U. and H. Zank (2008). Risk aversion in cumulative prospect theory. Management Science 54, 208-216.

- [15] Tversky, A. and D. Kahneman (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty 5, 297-323.

- [16] Yaari, M.E. (1986). Univariate and multivariate comparisons of risk aversion: a new approach. In: Heller, W.P., R.M. Starr and D.A. Starrett (Eds.). Uncertainty, Information, and Communication. Essays in honor of Kenneth J. Arrow, Volume III, pp. 173-188, 1st Ed., Cambridge University Press, Cambridge.

- [17] Yaari, M.E. (1987). The dual theory of choice under risk. Econometrica 55, 95-115.