Random Extensive Form Games and its Application to Bargaining

Abstract

We consider two-player random extensive form games where the payoffs at the leaves are independently drawn uniformly at random from a given feasible set . We study the asymptotic distribution of the subgame perfect equilibrium outcome for binary-trees with increasing depth in various random (or deterministic) assignments of players to nodes. We characterize the assignments under which the asymptotic distribution concentrates around a point. Our analysis provides a natural way to derive from the asymptotic distribution a novel solution concept for two-player bargaining problems with a solid strategic justification.

1 Introduction

A subgame perfect equilibrium is one of the fundamental solution concepts in game theory. Its characterization is very simple: A strategy profile is a subgame perfect equilibrium if it constitutes a Nash equilibrium of every subgame of the original game. In extensive form games with perfect information, subgame perfect equilibrium coincides with backward-induction and can be easily determined.

In this work we study the distribution of the subgame perfect equilibrium outcome in random two-player extensive form games. In these games there are two potential natural degrees of randomness that may be considered. The first is random payoffs where the payoffs at the leaves of the tree are randomly drawn. The second is random assignment of players to nodes, where one of the two decision makers at every node is drawn at random in accordance with a certain distribution. We restrict attention to binary trees with two players and focus on the case where the payoffs are i.i.d. uniform random draws over a given domain . Our analysis combines the two potential sources of randomness and relates properties of the subgame perfect equilibrium outcome to a solution concept in the theory of bargaining.

The existing literature on random games focuses on normal form games and studies properties such as the expected number of Nash equilibrium [7, 8], the distribution of pure Nash equilibria [3, 13, 15, 12, 14, 16] or the maximal number of equilibria [6]. Here we restrict our attention to random extensive form games. We consider binary random games and study the asymptotic properties of the subgame perfect equilibrium outcome when the depth is increasing. The fundamental natural question that arises is under which condition the limit exists and whether in some sense the subgame perfect distribution concentrates around a certain point, i.e., whether the subgame perfect equilibrium outcome is close to a certain point with probability close to 1, for sufficiently deep trees. Such a concentration point, if exists, may serve as a benchmark solution for a bargaining problem with as its feasible set. Indeed this point has quite solid strategic justification: For almost all111By “almost all” we mean in the context of the standard Lebesgue measure (when we refer to games as points in for the correct dimension ). Note that analyzing probability under i.i.d. uniform distribution is equivalent to analyzing the Lebesgue measure. strategic interactions of a quite natural type with outcomes in , the solution of the interaction will be close to this concentration point, i.e., for large enough perfect information games over binary trees (with a particular assignment of players to control the nodes) and with payoffs in . Hence we are interested in characterizing the cases where concentration occurs, and these cases will induce interesting incites into bargaining theory.

Our main theorem introduces the random extensive form bargaining solution that naturally arises from random extensive form games (see Section 4.1). We characterize our solution concept by introducing a sequence of increasing random extensive form games for which concentration around a point holds. This point defines our solution concept and satisfies the three core axioms of a standard solution concept in bargaining: Symmetry, efficiency and scale invariance.

1.1 Application to Bargaining

Starting with Nash [11] in 1950, the bargaining problem has been widely studied from different perspectives. Two complementary trusts of the bargaining theory are the axiomatic approach and implementation theory. The axiomatic approach aims to understand what should be the solution of a bargaining problem by introducing basic properties that it should satisfy. However, this approach provides no strategic reasoning for how this solution arises. The so-called “Nash program” aims to support solutions in a non-cooperative framework. This is exactly where implementation theory comes to play, where the goal is to design a game (i.e., a bargaining mechanism) whose equilibrium is the solution.

Many axioms have been suggested in the context of bargaining. Among the suggested axioms, the standard axioms that are satisfied by most of the classical solutions (e.g., Nash solution [11], Kalai-Smorodinski solution [5], and others) are Pareto efficiency, Symmetry, and Invariance with respect to positive affine transformations. The terminology of Kalai-Smorodinsky [5] (see also [17]), defines a solution to be standard if it satisfies these three axioms. Our focus will be on implementing a standard solution.

Implementation theory in bargaining, and in particular implementation in subgame perfect equilibrium, has been widely studied. Several mechanisms [10, 2, 4, 1, 9] have been suggested for implementing standard bargaining solutions. All these mechanisms are based on the idea that players sequentially offer an allocation that should be approved by the other players.

We take a different approach to the implementation problem, and we pose the question: Can a random extensive form game serve as an implementation to a standard bargaining solution? Theorem 3 constitutes a positive answer to this question. This approach differs from the above [10, 2, 4, 1, 9] in the following aspects.

First, the designed game is not based on offers and approvals. Second, it has minimalistic requirements about the abilities of the designer: It is sufficient that the designer will be able to draw outcomes from the bargaining set uniformly at random (as outcomes of the game) in order to design a game whose equilibrium outcome is (close to) a standard solution. Third, our result, in some sense, answers the following type of questions: How hard is it to implement a standard solution? How structured should the designed game be? Our result can be interpreted as follows, almost all binary choice large enough extensive form games (with a particular random structure of the decision maker over the nodes) implement a standard bargaining solution.

1.2 Outline of the Results

For ease of clarity of the presentation, throughout the paper we focus on a specific simple setting. As shown in Comment 1 of Section 5, our analysis holds in much more general settings.

We let be a compact convex set222Convexity of the set is not essential; see Comment 1 of Section 5.. Let be the uniform distribution over333Our analysis holds for every non-atomic probability distribution with positive density over ; see Comment 1 of Section 5. . The game is played over a complete binary tree of depth . The payoffs at the leaves are random independent draws in accordance with .

We consider two benchmark models of assigning players to control nodes in the tree:

-

1.

The alternating game. Player 1 controls all nodes at depths Player 2 controls all nodes at depths . Such a game (with random payoffs) will be denoted by .

-

2.

The random controlling player game. Each Player controls each node with probability , where the controlling player at each node is drawn independently across the nodes and independently of the payoffs. Such a game (with random controlling players and random payoffs) will be denoted by .

In Section 4 we consider additional assignments of players to nodes, which combines these two models.

For both players , both random games and have no two equal payoffs for player with probability one. Therefore, both and have almost surely unique subgame perfect equilibrium. We denote by and the random variable of the games’ value, which is the payoff profile at the unique subgame perfect equilibrium. We are interested in the asymptotic properties of the values and when . In particular are interested in the phenomena of concentration of the value which holds if there exists a point such that the probability that lies in a given neighborhood of goes to one as the depth of the tree goes to infinity. Formally,

Definition 1.

For a sequence of random games , we say that concentrates around the point if the sequence weakly converges to the Dirac measure on the singleton , i.e., .

We start our analysis with the zero-sum case, namely . The results for random zero-sum games are as follows:

Then we turn to the non-zero sum case where is a convex set with non-empty interior. The results for this case are as follows:

Our next target is to examine whether random extensive form games can serve as an implementation to a bargaining solution. The set can be considered as the feasible set of alternatives. A solution concept assigns a unique point for every such feasible set. Therefore, the first property that should be satisfied for such a random game is

-

1.

Concentration of the value around a point.

Another two natural properties that are common to most solution concepts in bargaining (the standard axioms) are:

-

2.

Pareto efficiency: The unique solution should be Pareto efficient.

-

3.

Symmetry: For every symmetric sets the solution should be symmetric.

By considering the results mentioned so far, we see that none of the suggested random extensive form games enjoys all three properties. The alternating game concentrates around a Pareto efficient point (Theorem 2). However, the concentration point does not satisfy symmetry (Theorem 1); Player 1 who acts last has an advantage. The random controlling player game is symmetric by nature; however it fails to satisfy concentration (Proposition 1).

It turns out that a random extensive form game, which satisfies all the above desirable properties can be obtained by a “hybrid” of the two discussed cases (the alternating and the random). In the hybrid game all nodes at depth for odd are controlled by Player with probability and by Player with the remaining probability . All nodes at depth for even are controlled by Player with probability and by Player with probability . Such a game (with random controlling players and random payoffs) will be denoted by . Note that and . We show in Theorem 3 that for small values of the hybrid game , indeed (approximately) satisfies the above-mentioned desirable property:

-

1.

For every fixed , the value of concentrates around a point.

-

2.

For every fixed , the concentration point of is Pareto efficient.

-

3.

For a symmetric set , given we can set such that the concentration point of will be -close to the diagonal (i.e., -close to the symmetric solution).

2 Zero sum games

We first consider the case of random zero-sum games, where , i.e., Player 1’s payoff is uniformly distributed in . For convenience of notations, along this section we drop the payoff of player 2, which is equal to minus player’s 1 payoff.

2.1 Alternating game

The following theorem states that the value of the alternating zero-sum game converges to the golden ratio minus one.

Theorem 1.

concentrates around point where .

Proof.

We denote . By the backward induction procedure we can deduce a recursive formula for the sequence of measures . The value of a game of depth is a function of the values of the two subgames of depth (which correspond to the two possible actions of the player that controls the root). Note that the two values of the two subgames are two independent draws according to . We denote by and the minimum and the maximum of two independent draws according to , and we have the following recursive formula

because Player 1 will choose the maximal value (among the two), and Player 2 will choose the minimal.

For we denote . For we have

| (1) |

because the maximum of two independent random variables is below iff both of them are below . Note also that

| (2) |

The first equality follows from the inclusion-exclusion principle. The second inequality follows from equation (1). Let , and let be times composition of on itself, i.e.,

It readily follows by induction from equation (2) that

| (3) |

Note that for , is a monotonically increasing polynomial with three fixed points: . In addition, for , and for (see Figure 3).

For every we consider the sequence , which is monotonically decreasing because

Let . The sequence is monotonically decreasing; therefore, is well defined and . Note also that is a fixed point of because

Hence .

Using similar arguments we can show that for the sequence is monotonically increasing and its limit is the fixed point 1. Summarizing, we have

| (4) |

This implies that converges to a limit Dirac measure concentrated in . The fact that the sequence converges to the same limit readily follows from equation (1).

We have proved that the CDF of pointwise converges to the CDF of the Dirac measure, which implies weak convergence. ∎

2.2 Random controlling player game

The following observation demonstrates that unlike alternating random games the value of a random zero-sum game with random structure does not concentrate.

Proposition 1.

For every , is the uniform distribution over .

Proof.

Using similar arguments to those in the proof of Theorem 1, we can write a recursive formula for the sequence of probability measures . We argue that

| (5) |

This follows from the fact that with probability Player 1 controls a certain vertex at depth , and then he chooses the maximal payoff. With probability Player 2 controls this vertex, and then he chooses the minimal payoff. From this recursive formula we deduce that

Namely, the sequence of measures remains constant for every initial probability measure . ∎

3 General Domains

Now we consider the case where is a general compact convex set with non-empty interior.

Definition 2.

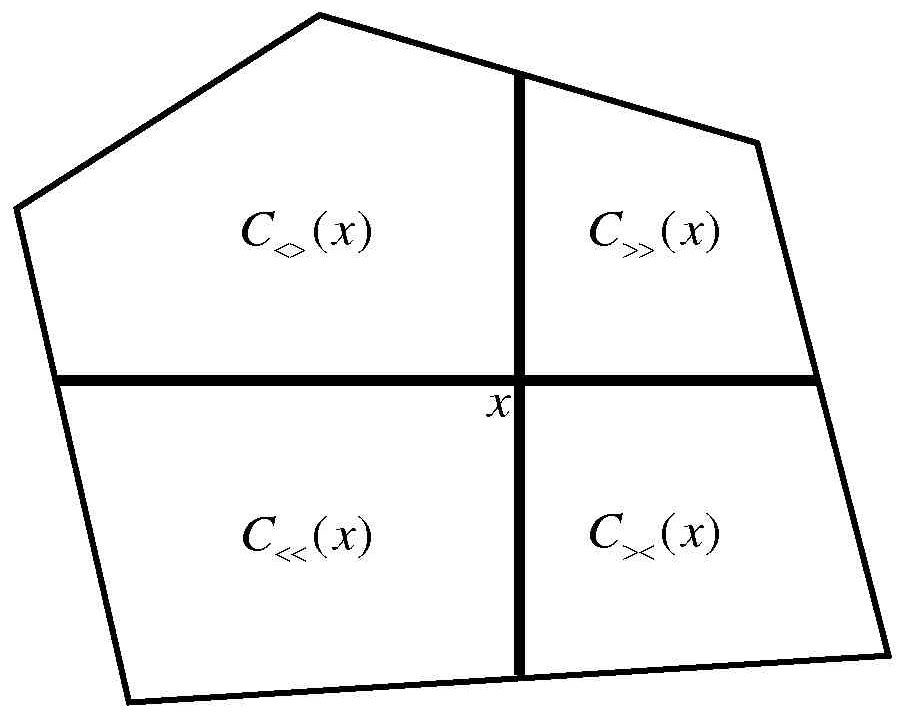

For a point we denote the first quadrant with the origin at point . Similarly we denote , , and the second, third, and fourth quadrants respectively, see Figure 2. More generally we denote where .

3.1 Alternating game

As in the zero-sum case, the value of the alternating game concentrates around a point. Moreover the concentration point is Pareto efficient.

Theorem 2.

The value of the alternating game concentrates around a Pareto efficient point.

Proof.

For we denote , similarly, for we denote . We let be the CDF of the marginal of to Player 1’s payoffs and to Player 2’s payoffs. Let be the number for which and similarly is defined by the number for which .

Lemma 1.

Both and are increasing sequences.

Proof.

In order to show that is increasing with it is sufficient to show that

| (6) |

Since if (6) holds, then , and by the monotonicity of the CDF we have that .

First, note that and hence ; this follows directly by a similar consideration as in equation (1).

Now we consider step . Clearly, is bounded from above by the probability that two i.i.d. draws that are distributed according to lies in (because is essentially obtained by a selection rule among i.i.d. outcomes that are distributed according to ). Therefore we have

| (7) |

A symmetric consideration applied to Player shows that is increasing. ∎

Let , and . We first contend that if then . To see this note that, by definition for some . A similar derivation to those applied in the proof of Theorem 1 yields that

| (8) |

where the last equality follows from the fact that . From this we can deduce that , because for odd steps we can bound .

Similar arguments show that for every ,

| (9) |

We next show that lies on the Pareto efficient boundary. Equations (8) and (9) imply that is nonempty for every and (see Definition 2), and therefore is nonempty.

Assume by way of contradiction that is Pareto dominated. Let be any point such that and has a nonempty interior. In particular . We claim first that for every ,

| (10) |

Because with probability at least the value of the left subtree is in and the value of the right subtree is in ; in such a case Player 1 will choose the outcome from . However, we also have the disjoint event where the left and right realizations are flipped (this event is disjoint because ) where again the chosen outcome is in . Therefore is a lower bound on .

3.2 Random controlling player game

We denote by the set of points within a distance at most from the Pareto efficient boundary. We say that a sequence of measures concentrates on the Pareto efficient boundary if for every .

The following proposition shows that although does not concentrate around a point, the value is (approximately) Pareto efficient with probability close to 1.

Proposition 2.

The value of the random controlling player game concentrates on the Pareto efficient boundary.

Proof.

Similar to the zero-sum case (equation 5), we can deduce the following recursive formula on .

| (12) |

where denotes the maximum over the th coordinate of two independent realizations of .

We let be the set of points with a distance of precisely from the efficient boundary. We will show first that for every it holds that (see Definition 2).

If not, there exists some and for which for infinitely many ’s. As before represents the probability under that the realised outcome for Player would be less than and similarly for Player .

We bound from below the probability using the recursive formula (12). There are three events under which the realization of lies in .

-

1.

Both realizations of lie in . The probability of this event is .

-

2.

Player 1 controls the root—one realization of is in , and the other realization is in . The probability of the first of the two is clearly The probability of the second is since the realizations can be flipped (each can appear in the left subgame or the right subgame). Overall this event holds with probability .

-

3.

Player 2 controls the root—one realization of lies in , and the other realization lies in . The probability of this event is .

These three events are disjoint (note that (2) and (3) are disjoint because the controlling player defers). Therefore, we deduce that for every

We can rewrite Equation (3.2) as follows

| (14) | |||

Since we conclude that increases with . Also if then

Hence since for infinitely many we have that for every there exists such that for every ,

This stands in contradiction to the fact that .

Fix . We show that there exists such that for every ,

Choose to be a finite sequence of points, dense enough such that if satisfies

then , i.e., . By the above we can find large enough such that for every , and every ,

We therefore conclude that for every ,

Since we conclude that

This completes the proof of the proposition. ∎

4 The Hybrid Model

As we did previously, we consider as a warm-up the zero-sum case where . We establish a generalization of Theorem 1 which states that the value of the random hybrid game converges to . This is indeed a generalization of Theorem because if we set then the random game and .

Proposition 3.

concentrates around the point .

The proof uses similar ideas to the proof of Theorem 1.

Proof.

For every , let be the CDF of . For every we have,

| (15) |

and

| (16) |

Using equations (15) and (16) we get,

| (17) | |||

Let

Simple algebraic computations show that the function has four fixed points

Among these fixed points only and are in the segment . We denote , and we note that and . Note also that for (for instance because ) and for (for instance because ). Figure 3 illustrates the function for .

The following theorem studies the asymptotic properties of for the general convex domain .

Theorem 3.

For every the value of the hybrid game concentrates around a Pareto efficient point . Moreover, if the domain is symmetric then ; namely, the concentration point approaches the diagonal when goes to .

Before establishing the proof of the Theorem (Section 4.2) we present more formally the applications of this result to bargaining and implementation.

4.1 Application to Bargaining

Given a bargaining set444Unlike standard bargaining models, in our case a bargaining problem contains a bargaining set only, without a disagreement point. we define the random-extensive-form (REF) solution to be

Note that the REF solution can also be derived from a more natural version of a random extinctive form game , where the REF solution is the limit point of the medians of the marginal distributions (see Proposition 6).

We recall that a solution is called standard if it satisfies Pareto efficiency, Symmetry, and Invariance with respect to positive affine transformations.

Corollary 1.

The REF solution is a standard solution.

Proof.

Pareto efficiency and symmetry follow immediately from Theorem 3. For invariance with respect to positive affine transformations we note that the uniform distribution remains uniform after operating such a transformation. In addition, the subgame perfect equilibria outcomes are invariant to such transformations. ∎

Beyond the fact that the REF solution satisfies several desirable axioms, the main advantage of the REF solution is the fact that this solution has a very clean probabilistic (approximate) implementation. We set small and large . Now we simply randomize the decision makers and the outcomes in the game as it is done in the hybrid game . With high probability the subgame perfect equilibrium outcome of the game is close to the REF solution.

4.2 Proof of Theorem 3

We start with a proof of the first part of Theorem 3 (regarding the concentration around a Pareto efficient point). In fact, we derive a stronger statement which provides also a type of characterization for the concentration point.

We denote by the probability distribution of and for we let be the CDF of the marginal distribution of over the payoffs to Player . We define to be the unique number such that . Similarly, is the number such that .

Proposition 4.

The sequences and have the following properties.

-

(A1)

and are monotonically increasing in .

-

(A2)

is a converging sequence.

-

(A3)

, namely, the limit of the sequence is the concentration point of .

-

(A4)

lies on the Pareto efficient boundary of .

Proof.

By applying identical considerations to those in the proof of Theorem 2, and replacing by we get exactly all these properties. ∎

Now we get to the proof of the second statement in Theorem 3. The proof is based on a connection between the sequences of measures and (see Proposition 6). In order to state this connection we need an additional convergence statement about the random structure games .

We denote by the CDFs of the marginal distribution of over the payoffs to Player . We denote by and the medians of and (respectively).

Proposition 5.

The sequences and are monotonically increasing. Moreover the limit point lies on the Pareto efficient boundary of555Unlike other structures of random games discussed in this paper, in the (symmetric) random structure we do not have a concentration of the limit measure around the point . Nevertheless, the proposition states that the limit point is well defined, and is Pareto efficient. .

Proof.

For we denote . In order to prove that is monotonically increasing it is sufficient to show that .

With probability Player 1 controls the node, and in such a case, the result (at the th iteration) is in iff both i.i.d. realizations (according to ) are in . The probability of such an event is .

With probability Player 2 controls the node, and in such a case, a necessary condition for the result (at the th iteration) to be in is that at least one realization is in . The probability of such an event is .

Summarizing, over the two cases we get .

Similar arguments show that the sequence is monotonically increasing.

Now we turn to the proof of statement (2).

Assume by way of contradiction that lies in the interior of , and then (see Definition 2). By equation (3.2) (which holds for the random controlling player case) we have that for every

Since (and ) we have . Hence,

which contradicts the fact that for every .

Assume by way of contradiction that lies out of the . Then for some finite is out of the set . We denote and . Note that , and , which implies that . This contradicts the fact that the density of remains strictly positive everywhere in for every finite .

Therefore must lie on the Pareto efficient boundary. ∎

The connection between the sequences of measures and is given by following proposition, which states that the concentration point of is close to the limit of medians of from Proposition 5.

Proposition 6.

.

We emphasize that and behave very differently for large (the first one concentrates around a point, whereas the latter does not). Therefore it is somewhat surprising that we succeeded to connect the concentration point of with some object that is derived from the sequence .

Proof of Proposition 6.

Let be a global Lipschitz constant such that for every two points and on the Pareto efficient boundary of holds666Actually we do not have to assume existence of a global Lipschitz constant for the Pareto efficient boundary. Existence of a local Lipschitz constant around the point will suffice for the arguments that we present here in the proof.

| (18) |

We set , and we shall prove that there exists such that for every holds . The way we do it is by considering the sequences and .

By Proposition 5 , so there exists such that

| (19) |

We emphasize that does not depend on (because depends only on a symmetric random structure where is not involved).

We denote by and the medians of and . By Lemma 2 the measures and are strongly continuous with respect to . In particular, it follows that the medians of converge to the medians of . Namely, and . Therefore, there exists such that for every holds

| (20) |

Note that and are continuous with respect to and (respectively). Note also that . Therefore by the definition of and there exists such that for every holds

| (21) |

If we set then inequalities (19), (20), and (21) guarantee that

By properties (1) and (3) in Proposition 4 (at the beginning of the proof) we know that Pareto dominates the point . In addition, by Proposition 5 we know that is Pareto efficient. By the definition of together with the above three properties we get that . ∎

Lemma 2.

For every constant the measure is strongly continuous (in the total variation distance) with respect to around .

Proof.

The random variable can be obtained by the following procedure.

-

1.

We randomize i.i.d. random outcomes according to .

-

2.

For each node we choose Player to control node with probability .

-

3.

For each node we draw a Bernoulli random variable with .

-

4.

For each odd-depth node , if we set Player 1 to control the node (irrespective of who was chosen to control it at step (2)).

-

5.

For each even-depth node , if we set Player 2 to control the node (irrespective of who was chosen to control it at step (2)).

-

6.

We apply backward induction on the resulted game.

Note that . In such a case (of for all ) we have exactly the random variable . Therefore the total variation distance is bounded by , i.e., .

∎

5 Discussion

1. General settings for which all the results hold. By looking on the proofs of the results one can observe that the properties of the domain which were used in the proofs are as follows:

-

1.

is a compact set with a non-empty interior.

-

2.

For every not Pareto efficient point the set has a non-empty interior.

-

3.

The Pareto efficient boundary forms a connected path which has the Lipschitz property. This requirement is needed only for the analysis of the hybrid game.

These are very minimalistic requirements which include in particular the cases where is a simply connected set with a concave Pareto efficient boundary (rather than convex).

Again by looking at the proofs of the results one can observe that the only property on the initial distribution that was used is the fact that is a non-atomic measure with strictly positive density over all . The only change in the results (but not in the proofs) that is caused by changing the uniform distribution by a general distribution is Theorem 1: The concentration point is obviously not the point but the point for which .

2. Games over ternary trees. The paper focuses on the case where the game tree is a complete binary tree. The techniques derived in the paper can be applied also for the case where the game tree is ternary. We overview here the results for this case (without proofs). As we can see part of the results are similar but part are not:

-

•

The value of the alternating game concentrates around a Pareto efficient point. In the case of a zero-sum game the concentration is around , where is the unique solution of in the segment . These results are similar to the case of binary trees.

-

•

The value of the random controlling player game converges to the distribution which assigns a probability of to both points , where is the best point in for Player . This statement holds for both, the zero sum case and the case of a general two-dimensional set . These results defer from the binary case where the limit measure has positive density over the entire Pareto efficient boundary.

-

•

For small enough values of , the value of the hybrid game converges to , where assigns a probability close to to (from the previous bullet) and the remaining probability to . In particular, the hybrid game fails to have the desirable property of concentration around a point. Namely, a different random structure than the hybrid game is required in order to implement a standard solution in ternary games.

References

- [1] Anbarci, N. “Noncooperative foundations of the area monotonic solution,” The Quarterly Journal of Economics (1993) 245-258.

- [2] Binmore, K., Rubinstein, A., and Wolinsky, A. “The Nash bargaining solution in economic modelling,” The RAND Journal of Economics (1986) 176-188.

- [3] Dresher, Melvin. “Probability of a pure equilibrium point in n-person games.” Journal of Combinatorial Theory 8.1 (1970): 134-145.

- [4] Howard, J. V. “A social choice rule and its implementation in perfect equilibrium,” Journal of Economic Theory, 56(1) (1992) 142-159.

- [5] Kalai, E., and Smorodinsky, M. “Other solutions to Nash’s bargaining problem,” Econometrica (1975) 513-518.

- [6] McLennan, A. “The maximal generic number of pure Nash equilibria.” Journal of Economic Theory 72.2 (1997): 408-410.

- [7] McLennan, A. “The expected number of Nash equilibria of a normal form game.” Econometrica (2005): 141-174.

- [8] McLennan, A., and Berg, J. “Asymptotic expected number of Nash equilibria of two-player normal form games.” Games and Economic Behavior 51.2 (2005): 264-295.

- [9] Miyagawa, E. “Subgame-perfect implementation of bargaining solutions,” Games and Economic Behavior, 41(2) (2002): 292-308.

- [10] Moulin, H. “Implementing the Kalai-Smorodinsky bargaining solution,” Journal of Economic Theory, 33(1) (1984): 32-45.

- [11] Nash Jr, J. F. “The bargaining problem,” Econometrica (1950): 155-162.

- [12] Papavassilopoulos, G. P. “On the probability of existence of pure equilibria in matrix games.” Journal of Optimization Theory and Applications 87.2 (1995): 419-439.

- [13] Powers, I. Y. “Limiting distributions of the number of pure strategy Nash equilibria in N-person games.” International Journal of Game Theory 19.3 (1990): 277-286.

- [14] Rinott, Y., and Scarsini, M. “On the number of pure strategy Nash equilibria in random games.” Games and Economic Behavior 33.2 (2000): 274-293.

- [15] Stanford, W. “A note on the probability of k pure Nash equilibria in matrix games.” Games and Economic Behavior 9.2 (1995): 238-246.

- [16] Takahashi, S. “The number of pure Nash equilibria in a random game with nondecreasing best responses.” Games and Economic Behavior 63.1 (2008): 328-340.

- [17] Trockel, W. “Axiomatization of the discrete Raiffa solution,” Economic Theory Bulletin, (2004) 1-9.