A solvable two-dimensional singular stochastic control problem with non convex costs111 The first and the third authors were supported by EPSRC grant EP/K00557X/1; financial support by the German Research Foundation (DFG) via grant Ri–1128–4–2 is gratefully acknowledged by the second author.

Abstract. In this paper we provide a complete theoretical analysis of a two-dimensional degenerate non convex singular stochastic control problem. The optimisation is motivated by a storage-consumption model in an electricity market, and features a stochastic real-valued spot price modelled by Brownian motion. We find analytical expressions for the value function, the optimal control and the boundaries of the action and inaction regions. The optimal policy is characterised in terms of two monotone and discontinuous repelling free boundaries, although part of one boundary is constant and the smooth fit condition holds there.

Keywords: finite-fuel singular stochastic control; optimal stopping; free boundary; Hamilton-Jacobi-Bellman equation; irreversible investment; electricity market.

MSC2010 subsject classification: 91B70, 93E20, 60G40, 49L20.

1 Introduction

Consider the following problem introduced in [4]: a firm purchases electricity over time at a stochastic spot price for the purpose of storage in a battery. The battery must be full at a random terminal time , and any deficit leads to a terminal cost given by the product of a convex function of the undersupply and the terminal spot price . The terminal cost accounts for the use of a quicker but less efficient charging method at the time of demand, while the restriction to purchasing is interpreted as the firm not having necessary approval to sell electricity to the grid.

Taking as a real-valued Markov process carried by a complete probability space , and letting be independent of and exponentially distributed with parameter , it is shown in Appendix A of [4] that this optimal charging problem is equivalent to solving

| (1.1) |

Here is taken to be a strictly convex, twice continuously differentiable, decreasing function and the infimum is taken over a suitable class of nondecreasing controls such that , -a.s. for all . The control is the cumulative amount of energy purchased up to time and represents the inventory level at time of the battery whose inventory level is at time . The finite fuel constraint , , -a.s. for all , reflects the fact that the battery has limited total capacity.

Certain deregulated electricity markets with renewable generation exhibit periods of negative electricity price, due to the requirement to balance real-time supply and demand. Such negative prices are understood to arise from a combination of the priority given to highly variable renewable generation, together with the short-term relative inflexibility of traditional thermal generation units [10], [8]. In order to capture this feature, which is unusual in other areas of mathematical finance, we assume a one-dimensional spot price taking negative values with positive probability. In [4] is an Ornstein-Uhlenbeck (OU) process. In the present paper, with the aim of a full theoretical investigation, we take a more canonical example letting be a Brownian motion and we completely solve problem (1.1).

From the mathematical point of view, (1.1) falls into the class of singular stochastic control (SSC) problems. The associated Hamilton-Jacobi-Bellman (HJB) equation is formulated as a two-dimensional degenerate variational problem with a state-dependent gradient constraint. The problem is degenerate because the control acts in a direction of the state space which is orthogonal to the diffusion. It is worth mentioning that explicit solutions of problems with state-dependent gradient constraints are relatively rare in the literature (a recent contribution is [12]) when compared to problems with constant constraints on the gradient and one or two-dimensional state space (see for example [1] and [18] amongst others).

As also noted in [4], a key peculiarity of our problem is that the total expected cost functional which we want to minimise in (1.1) is non convex with respect to the control variable . In particular, by recalling that is real-valued and simply writing it as the difference of its positive and negative part, it is easy to see that the cost functional in (1.1) can be written as a d.c. functional, i.e. as the difference of two functionals convex with respect to (see [14] or [15] for references on d.c. functions). SSC problems which are convex with respect to are of particular interest since they typically have optimal controls of reflecting type, leading in turn to a certain differential connection to problems of optimal stopping (OS), see for example [7] and [16]. Clearly, however, the d.c. property of the functional in (1.1) means that problem (1.1) does not fall directly into this setting. Indeed the study in [4], where the uncontrolled process is of OU type, reveals how the non-convexity of the cost criterion impacts in a complex way on the structure of the optimal control and on the connection between SSC problems and OS ones. It is shown in [4] that while connections to OS do hold for problem (1.1), they may or may not be of differential type depending on parameter values and the initial inventory level . This suggests that the solutions of two-dimensional degenerate problems of this kind are complex and should be considered case by case.

In particular, the analysis in [4] identifies three regimes, two of which are solved and the third of which is left as an open problem under the OU dynamics. Here we aim at a complete solution of (1.1) and address the third regime of [4] in the Brownian case. Such a complete solution also gives some insight in the open case of [4] since Brownian motion is a special case of OU with null rate of mean reversion. The geometric methodology we employ in this paper (see Figures 2 and 3) is a significant departure from that in [4]. In Section 4.2 below we rely on the characterisation via concavity of excessive functions for Brownian motion introduced in [5], Chapter 3 (later expanded in [2]) to study a parameterised family of OS problems. It is thanks to this characterisation that we succeed in obtaining the necessary monotonicity and regularity results for the optimal boundaries of the action region associated to (1.1) (i.e. the region in which it is profitable to exert control). In contrast to the OU case, the Laplace transforms of the hitting times of Brownian motion are available in closed form and it is this feature which ultimately enables the method of the present paper.

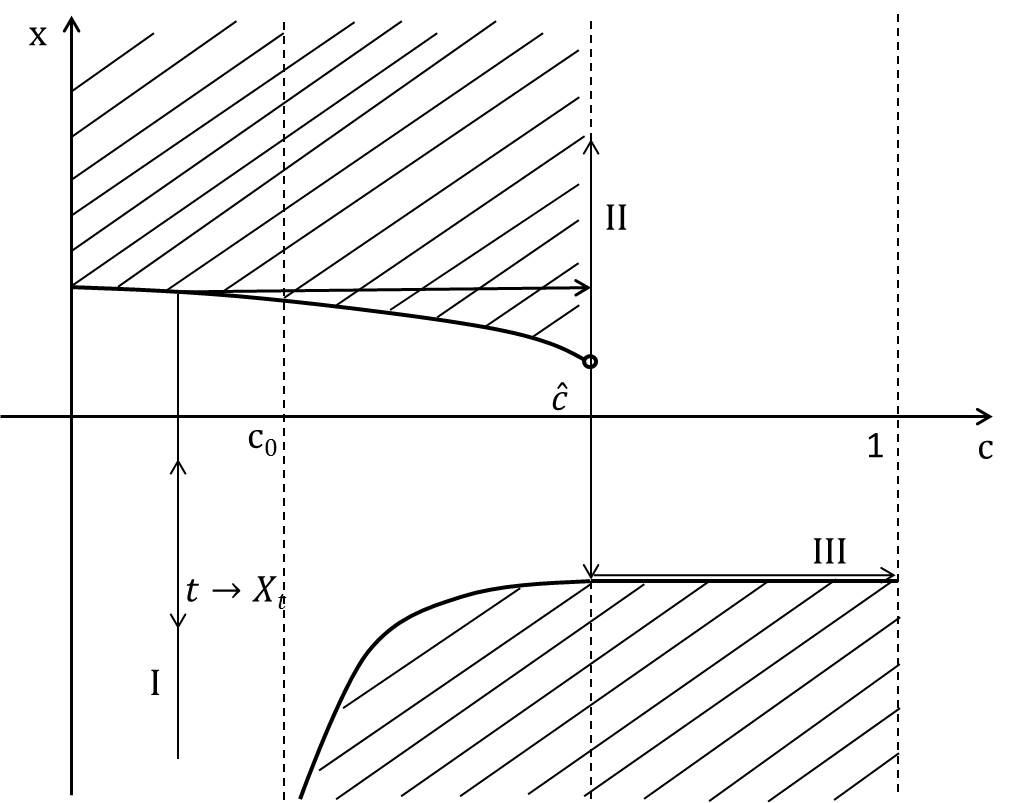

We show that the action region of problem (1.1) is disconnected. It is characterised in terms of two boundaries which we denote below by and which are discontinuous, the former being non-increasing everywhere but at a single jump and the latter being non-decreasing with a vertical asymptote (see Fig. 1). Through a verification argument we are able to show that the optimal control always acts by inducing discontinuities in the state process. The boundaries and are therefore repelling (in the terminology of [3] or [17]). However, in contrast with most known examples of repelling boundaries, if the optimally controlled process hits the upper boundary the controller does not immediately exercise all available control but, rather, causes the inventory level to jump to a critical level (which coincides with the point of discontinuity of the upper boundary ). After this jump the optimally controlled process continues to evolve until hitting the lower boundary where all the remaining control is spent to fill the inventory (the upper boundary is then formally infinite; for details see Sections 4 and 4.3).

The present solution does in part display a differential connection between SSC and OS. In particular, when the initial inventory level is strictly larger than there is a single lower boundary which is constant. Moreover coincides with the value function of an associated optimal stopping problem on and the so-called smooth fit condition holds at (for ) in the sense that is continuous across it. This constant boundary can therefore be considered discontinuously reflecting. That is, it may be viewed as a limiting case of the more canonical strictly decreasing reflecting boundaries. On the other hand, when the initial inventory level is smaller than the critical value the control problem is more challenging due to the presence of two moving boundaries, which we identify in Section 4.2 with the optimal boundaries of a family of auxiliary OS problems. In this case it can easily be verified that is discontinuous across the optimal boundaries so that the smooth fit condition breaks down, and there is no differential connection to OS.

Smooth fit is one of the most studied features of OS and SSC theory and it is per se interesting to understand why it breaks down. It is known for example (see [19]) that diffusions whose scale function is not continuously differentiable may induce a lack of smooth fit in OS problems with arbitrarily regular objective functionals. On the other hand when the scale function is Guo and Tomecek [11] provide necessary and sufficient conditions for the existence of smooth fit in two-dimensional degenerate SSC problems. In particular [11] looks at bounded variation control problems of maximisation for objective functionals which are concave with respect to the control variable and one of their results states that the smooth fit certainly holds if the running profit (i.e. their counterpart of our function ) lies in . It is therefore interesting to observe that in the present paper we indeed have a smooth running cost and the break down of smooth fit is a consequence exclusively of the lack of convexity (in ) of the cost functional. To the best of our knowledge, this phenomenon is a novelty in the literature.

The rest of the paper is organised as follows. In Section 2 we set up the problem and make some standing assumptions. In Section 3 we provide a heuristic study of the action region and of the optimal control, and then we state the main results of the paper (see Theorems 3.1 and 3.3) which provide a full solution to (1.1). Section 4 is devoted to proving all the technical steps needed to obtain the main result and it follows a constructive approach validated at the end by a verification argument. Finally, proofs of some results needed in Section 4 are collected in Appendix A.

2 Setting and assumptions

Let be a complete probability space carrying a one-dimensional standard Brownian motion adapted to its natural filtration augmented by -null sets . We denote by the Brownian motion starting from at time zero,

| (2.1) |

It is well known that is a (null) recurrent process with infinitesimal generator and with fundamental decreasing and increasing solutions of the characteristic equation given by and , respectively.

Letting be constant, we denote by the purely controlled process evolving according to

| (2.2) |

where is a control process belonging to the set

From now on controls belonging to will be called admissible.

Given a positive discount factor and a running cost function , our problem (1.1) is to find

| (2.3) |

with

| (2.4) |

and to determine a minimising control policy if one exists. A priori existence results for the optimal solutions of SSC problems with cost criteria which are not necessarily convex are rare in the literature. Two papers dealing with questions of such existence in abstract form are [6] and [13]. Here we do not provide any abstract existence result for the optimal policy of problem (2.3), but we explicitly construct it in Section 4 below.

Throughout this paper, for and we will make use of the notation to indicate the Stieltjes integral with respect to . Moreover, from now on the following standing assumption on the running cost factor will hold.

Assumption 2.1.

lies in and is decreasing and strictly convex with .

We will observe in Section 3 below that the sign of

| (2.5) |

plays a crucial role. We now define also the function

| (2.6) |

and assume the existence of constants and , both lying in , such that

| (2.7) | |||||

| (2.8) |

It follows from the strict convexity of that the function is strictly increasing and that , are uniquely defined. The assumption that lies in allows us to consider the most general setting but the case where does not exist in is also covered by the method presented in the next sections. The next result easily follows from properties of .

Lemma 2.2.

and is strictly concave, hence it is negative on and positive on ; also, has a positive maximum at and therefore .

3 Preliminary discussion and main results

In order to derive a candidate solution to problem (2.3) we perform a preliminary heuristic analysis, distinguishing three cases according to the signs of and .

(A). When (i.e. when ) consider the costs of the following three strategies exerting respectively: no control, a small amount of control, or a large amount. Firstly if control is never exercised, i.e. , , one obtains from (2.4) an overall cost by an application of Fubini’s theorem. If instead at time zero one increases the inventory by a small amount and then does nothing for the remaining time, i.e. for in (2.4), the total cost is . Writing we find that so that exercising a small amount of control reduces future expected costs relative to a complete inaction strategy only if , i.e. , since . It is then natural to expect that for each there should exist such that it is optimal to exercise control only when .

We next want to understand whether a small control increment is more favourable than a large one and for this we consider a strategy where at time zero one exercises all available control, i.e. for . The latter produces a total expected cost equal to , so that for and recalling that is increasing one has

| (3.1) |

Since the last expression is negative whenever , so it is reasonable to expect that large control increments are more profitable than small ones. This suggests that the threshold introduced above should not be of the reflecting type (see for instance [18]) but rather of repelling type as observed in [3] and [17] among others. Using this heuristic a corresponding free boundary problem is formulated and solved in Section 4.1.

(B1). When (that is, when ) we again compare inaction to small and large control increments. Observe that now is favourable (with respect to complete inaction) if and only if , i.e. , since now . Hence we expect that for fixed one should act when the process exceeds a positive upper threshold . Then compare a small control increment with a large one, in particular consider a policy that immediately exercises an amount of control and then acts optimally for problem (2.3) with initial conditions . The expected cost associated to is and one has

| (3.2) |

where we have used that . If we fix and , then for sufficiently small the right-hand side of (3.2) becomes negative, which suggests that a reflection strategy at the upper boundary would be less favourable than the strategy described by .

(B2). Finally, when and we compare the ‘large’ increment to inaction. Note that to obtain

| (3.3) |

The first integral on the right-hand side of (3.3) is negative but its absolute value can be made arbitrarily small by taking close to . The second integral is positive and independent of . Thus the overall expression becomes negative when approaches from the left. This suggests that when the inventory is a little below the critical value an investment sufficient to increase the inventory to the level is preferable to inaction, after which the optimisation continues as discussed above for . We therefore explore the presence of both upper and lower repelling boundaries when is a little below , and this is done in Section 4.2.1. The candidate solution for smaller values of (when the heuristic suggests only an upper boundary) is constructed in Section 4.2.2.

In each of the previous heuristics it is preferable to exert a large amount of control. This suggests suitable connections to optimal stopping problems (although not necessarily of differential type) and the main novelty in this paper is to exploit these expected connections. In particular we take advantage of the opportunity to solve optimal stopping problems using geometric arguments as in [2]. This allows candidates for the control boundaries, value function and optimal control policy to be constructed and analytical properties to be derived. Further these optimal stopping problems have similar variational inequalities to the control problem, which facilitates verification of the candidate solution.

Before proceeding with the formal analysis we present the solution to problem (2.3), which is our main result. As suggested by the above heuristics the solution is somewhat complex, but a straightforward graphical presentation is given in Figure 1. The formal solution is given in the next three results.

Theorem 3.1.

Recall and as in (2.8) and (2.7), respectively. There exists two functions defined on and taking values in the extended real line fulfilling

-

i)

In , , it is and decreasing, whereas for , ;

-

ii)

In , , it is and non decreasing, whereas for , ;

and such that an optimal control can be constructed as follows: for define the stopping times

| (3.4) |

and

| (3.5) |

with the convention (note that , -a.s. if ); then the admissible purely discontinuous control

| (3.6) |

is optimal for (2.3).

Proposition 3.2.

The optimal boundaries and of Theorem 3.1 are characterised as follows:

-

i)

For one has (and );

-

ii)

For one has and where and are the unique couple solving the following problem:

Find and such that and with (3.7) (3.8) -

iii)

For one has (and ) where is the unique solution in of with

(3.9)

Theorem 3.3.

The boundaries and of Proposition 3.2 fully characterise the optimal control illustrated in Figure 1, which prescribes to do nothing until the uncontrolled process leaves the interval , where is the initial inventory level. Then, if one should immediately exert all the available control after hitting the lower moving boundary . If instead one should initially increase the inventory to after hitting the upper moving boundary and then wait until hits the new value of the lower boundary before exerting all remaining available control.

4 Construction of a candidate value function

The direct solution of (3.10) is challenging in general as it is a free boundary problem with (multiple) non constant boundaries. When necessary, however, for each fixed value of we will identify an associated optimal stopping problem whose solution is simpler since its free boundaries are given by two points. Our candidate solution is then effectively obtained by piecing together partial solutions on different domains. More precisely, recalling the definitions of and from (2.7)-(2.8), we carry out the following steps:

We begin the construction of a candidate value function by establishing the finiteness of the expression (2.3) under our assumptions.

Proposition 4.1.

Let be as in (2.3). Then there exists such that for any .

Proof.

4.1 Step 1: initial value of inventory

We formulate the first heuristic of Section 3 mathematically by writing (3.10) as a free boundary problem, to find the couple of functions , with and , solving

| (4.8) |

Proof.

A general solution to the first equation in (4.8) is given by

with , and to be determined. Since diverges with a superlinear trend as and has sublinear growth by Proposition 4.1, we set . Imposing the fourth and fifth conditions of (4.8) for and recalling the expression for in (2.6) we have

| (4.10) |

This way the function of (4.9) clearly satisfies , is continuous by construction and by some algebra it is not difficult to see that is continuous on with , . Moreover one also has

| (4.11) |

and hence , for , i.e. the smooth fit condition holds, and on as required. It should be noted that fails to be continuous across the boundary although it remains bounded on any compact subset of .

Finally we observe that

| (4.12) |

since and on . ∎

Remark 4.3.

We may observe a double connection to optimal stopping problems here, as follows:

1. We could have applied heuristic (A) from Section 3, approaching this sub-problem as one of optimal stopping. However the free boundary turns out to be constant for and the direct solution of (3.10) is straightforward in this case. Links to OS are, however, more convenient in the following sections.

2. Alternatively we may differentiate the explicit solution (4.9) with respect to . Then holding constant it is straightforward to confirm that solves the free boundary problem associated to the following OS problem:

| (4.13) |

This differential connection to optimal stopping is formally the same as the differential connection previously observed in convex SSC problems (see [16]).

4.2 Step 2: an auxiliary problem of optimal stopping for

We now use heuristics (B1) and (B2) from Section 3 to identify an associated parametric family of optimal stopping problems, which are solved in this section. More precisely we conjecture here (and will verify in Section 4.3) that for and , the value function equals

| (4.14) |

where the optimisation is taken over the set of -stopping times valued in , -a.s. We begin by noting that Itô’s formula may be used to express (4.14) as an OS problem in the form:

| (4.15) |

where

| (4.16) | |||||

| (4.17) |

Note that , for suitable and is continuous for any fixed and . Then from standard theory an optimal stopping time is where

| (4.18) |

are continuation and stopping regions respectively, and is finite valued.

The solution of the parameter-dependent optimal stopping problem (4.16) is somewhat complex and we will apply the geometric approach originally introduced in [5], Chapter 3, for Brownian motion and expanded in [2]. The solutions are illustrated in Figures 2 and 3 in a sense which will be clarified in Proposition 4.4. This allows the analytical characterisation of the optimal stopping boundaries as varies and thus the study of their properties, avoiding the difficulties encountered in the more direct approach of [4]. As in [2], eq. (4.6), we define

| (4.19) |

together with its inverse

| (4.20) |

and the function

| (4.23) |

We can now restate part of Proposition 5.12 and Remark 5.13 of [2] as follows.

Proposition 4.4.

Note that characterising is equivalent to characterising , which is in turn equivalent to finding . The latter and its contact sets will be the object of our study in Sections 4.2.1 and 4.2.2. Fixing , we first establish regularity properties of . We have (from (4.9) and (4.17))

| (4.24) |

Noting that , , we obtain

| (4.25) |

Lemma 4.5.

The function belongs to with for all and .

Proof.

Since is continuous in the function is continuous on by construction and it is easy to verify that for any . Since

| (4.28) |

then for any , letting as , , one has

hence is continuous on . Moreover we also have

| (4.29) | ||||

| (4.30) | ||||

| (4.33) |

so that the remaining claims easily follow. ∎

The sign of (defined in (2.6)) will play an important role in determining the geometry of the obstacle . Recalling that is the unique root of in , in Sections 4.2.1 and 4.2.2 we consider the cases and respectively. The intermediate case is obtained by pasting together the former two in the limits as and and noting that these limits coincide.

4.2.1 Step 3: initial value of inventory

For , so that and , we now apply heuristic (B2). Lemma 4.6 collects some geometric properties of while Proposition 4.7 enables us to establish that in the present case, the minorant of Proposition 4.4 has the form illustrated in Figure 2.

Lemma 4.6.

Let be arbitrary but fixed. The function is strictly decreasing, with and , and is strictly convex on and concave in .

The next proposition uses these properties to uniquely define a straight line tangent to at two points and , which will be used to define the moving boundaries and introduced in Proposition 3.2. The convexity/concavity of then guarantee that the largest non-positive convex minorant of Proposition 4.4 is equal to this line on and equal to otherwise.

Proposition 4.7.

For any there exists a unique couple solving the system

| (4.34) |

with and .

Proof.

Define

| (4.35) | ||||

| (4.36) | ||||

| (4.37) |

so that is the straight line tangent to at , with vertical intercept . The function is decreasing and continuous and it is clear that , since is concave on . To establish the existence of a unique such that , it is therefore sufficient to find with . Such a exists since as : it is clear from (4.37) that if then .

For the minorant is therefore

| (4.38) |

The following propositionis proved in Appendix A.

Proposition 4.8.

The functions and of Proposition 4.7 belong to with increasing and decreasing on and

-

1.

;

-

2.

;

-

3.

for all ;

-

4.

.

4.2.2 Step 4: initial value of inventory .

The geometry indicated in Figure 2 does not hold in general. Indeed in heuristic (B2), a lower repelling boundary is suggested only for values of close to . It turns out that ‘close’ in this sense means greater than or equal to . We now take and show that in this case the geometry of the auxiliary optimal stopping problems is as in Figure 3, so that each of these problems (which are parametrised by ) has just one boundary. The following Lemma has a proof very similar to that of Lemma 4.6 and it is therefore omitted.

Lemma 4.9.

Let be arbitrary but fixed. The function of (4.25) is strictly increasing in and strictly decreasing in . Moreover, is strictly concave in the interval and it is strictly convex in with .

The strict concavity of in suggests that there should exist a unique point solving

| (4.39) |

The straight line given by

is then tangent to at and .

The proof of the next result may be found in Appendix A.

Proposition 4.10.

4.2.3 Step 5: partial candidate value function

In this section we paste together the solutions obtained in sections 4.2.1 and 4.2.2 across , and then apply the transformation of Proposition 4.4 to obtain (recall (4.15)) and thus the partial candidate solution conjectured at the beginning of Section 4.2 for initial inventory levels . We also establish a free boundary problem solved by , which will help to show that solves (3.10) for .

The function of Section 4.2.1 may be extended to a function by setting for . The function may be extended to (thanks to Proposition 4.10) by setting for . With these definitions the expression (4.38), which we now recall, is valid for all :

| (4.43) |

Note that by construction and thanks to the regularity of and of the boundaries (cf. Lemma 4.5 and Proposition 4.10) is well defined across and is continuous on . We next confirm that is continuously differentiable.

Proposition 4.11.

The function lies in .

Proof.

Denoting

the surfaces and are clearly on since . As a consequence is away from the free boundaries and and it remains to verify whether the pasting across the boundaries is as well. At the two boundaries we clearly have (cf. Proposition 4.7)

| (4.44) |

Recall that , then an application of the chain rule to the left hand side of (4.44) gives

| (4.45) |

for . Hence for since from the construction of we know that at the two boundaries. Similar arguments also provide for . ∎

For the rest of the paper we employ exclusively analytical arguments, working in the coordinate system of the original problem (1.1). Using Proposition 4.4 we therefore set

| (4.48) |

and obtain the following expression for :

| (4.49) |

Remark 4.12.

Corollary 4.13.

We have

-

i)

The boundary lies in and is strictly decreasing with for all ;

-

ii)

The boundary lies in and is strictly increasing with for all .

We can now show that the parameter-dependent optimal stopping value function satisfies the following free boundary problem. This will in turn establish some properties of required to verify optimality in Section 4.3.

Proposition 4.14.

The value function of (4.16) belongs to with . Moreover and satisfies

| (4.55) |

Proof.

From Proposition 4.4 we have that implies . Analogously to prove that is locally bounded it suffices to show it for . Since for , , and is linear in elsewhere the claim follows.

By construction and therefore . From (4.49) we see that inside the continuation region may be rewritten as , with suitable and , and therefore the first equation of (4.55) holds. Outside the continuation region one has so that can be computed explicitly by recalling the expression for (see (4.9)) and it may be verified that the subsequent inequality holds (using that since and for ). The last three equalities in (4.55) follow since . ∎

Corollary 4.15.

, with and in particular we have

| (4.56) |

for and .

The next two propositions follow from results collected above and their detailed proofs are given in Appendix A.

Proposition 4.16.

for all .

Proposition 4.17.

Let

| (4.59) |

then and .

In the next definition we extend the boundaries and to the whole of . With this extension they correspond to the boundaries introduced in the statement of Theorem 3.1.

4.3 Step 6: verification theorem and the optimal control

In this section we establish the optimality of the candidate value function and show that the purely discontinuous control defined in (3.6) of Theorem 3.1 is indeed optimal for problem (2.3). Firstly, several results obtained above are summarised in the following proposition.

Proposition 4.19.

Proof.

The functions and solve the variational problem on and respectively (see Proposition 4.2 for the claim regarding and Propositions 4.14, 4.16 and Corollary 4.15 for the claim regarding ). Then Proposition 4.17 guarantees that solves the variational problem on as required. From the definitions of , and (see (4.59), (4.9) and (4.14)) one also obtains the sublinear growth property and . ∎

Proof.

The proof is based on a verification argument and, as usual, it splits into two parts.

(i) Fix and take . Set , take an admissible control , and recall the regularity results for in Proposition 4.17. Then we can use Itô’s formula in the weak version of [9], Chapter 8, Section VIII.4, Theorem 4.1, up to the stopping time , for some , to obtain

where and the expectation of the stochastic integral vanishes since is bounded on .

Now, recalling that any can be decomposed into the sum of its continuous part and its pure jump part, i.e. , one has (see [9], Chapter 8, Section VIII.4, Theorem 4.1 at pp. 301-302)

Since satisfies the Hamilton-Jacobi-Bellman equation (3.10) (cf. Proposition 4.19) and by writing

| (4.60) |

we obtain

| (4.61) | ||||

When taking limits as we have , -a.s. By standard properties of Brownian motion it is easy to prove that the integral terms in the last expression on the right hand side of (4.3) are uniformly bounded in , hence uniformly integrable. Moreover, has sub-linear growth by Proposition 4.19. Then we also take limits as and it follows that

| (4.62) |

due to the fact that . Since the latter holds for all admissible we have .

(ii) If then . Then take and define , with as in (3.6). Applying Itô’s formula again (possibly using localisation arguments as above) up to time (cf. (3.4)) we find

| (4.63) |

where we have used that does not have a continuous part. We also recall, as already observed, that , -a.s. under the control policy of .

From (3.5) one has , -a.s. and therefore we can always write

| (4.64) |

where the last equality follows by recalling that for and hence it holds in the first integral for . To evaluate the last term of (4.3) we study separately the events and . We start by observing that under the control strategy one has and we get

| (4.65) |

by Proposition 4.2 since for any on . On the other hand

| (4.66) |

Then it follows from (4.3), (4.65) and (4.66) that

| (4.67) |

Moreover for any because for any such and thus we finally get from (4.67)

| (4.68) |

Note that under the control strategy we also have and , then from (3.6) we have

| (4.69) |

by using that for all as proved in Section 4 (see also Figure 1).

For the jump part of the control, i.e. for the last term in (4.3), again we argue in a similar way as above and use that on the event there is no jump strictly prior to and the sum in (4.3) is zero, whereas on the event a single jump occurs prior to , precisely at . This gives

| (4.70) |

Combining (4.68), (4.3) and (4.3) it follows from (4.3) that

| (4.71) |

which together with (i) above implies , and of (3.6) is optimal. ∎

Appendix A Some proofs needed in Section 4

Proof.

[Proposition 4.8]

Rewrite (4.34) as

| (A-1) |

with the two functions , , defined by (3.7) and (3.8) of Proposition 3.2. The Jacobian matrix

has determinant

which is strictly negative when , and . To simplify notation we suppress the dependency of and on . Total differentiation of (A-1) with respect to and the Implicit Function Theorem imply that and lie in , with

so that

| (A-2) |

and

| (A-3) |

It is not hard to verify that by using , and . The sign of the right hand side of (A) is opposite to the sign of

| (A-4) |

since , and , . Recalling now (A-1), (3.7) and (3.8), we obtain

and

which plugged into (A-4) give

It is now easy to see that is strictly decreasing on and such that and . Hence implies that and .

To complete the proof we need to show properties -. We observe that due to the monotonicity of , , on their limits exist at all points of this interval.

-

We argue by contradiction and assume that . Then taking limits as in the first equation of (A-1) and recalling that we find

which is clearly impossible since due to the fact that for any .

-

We take limits as in (A) and notice that since (notice also that both functions and are proportional to so that their quotient remains finite).

∎

Proof.

[Proposition 4.10]

Note first that by (4.25) and (4.28), equation (4.39) may be rewritten in the equivalent form

| (A-6) |

where the jointly continuous function is defined in (3.9) of Proposition 3.2. The proof is carried out in three parts and for simplicity we omit the dependency of on .

(i) The function is strictly decreasing on with and so, since the absolute value of the second term of (3.9) is smaller than one, there exists a unique solving (A-6). Moreover since

| (A-7) |

we can use the implicit function theorem to conclude that and

| (A-8) |

(ii) The limit exists by monotonicity and so by continuity we have , i.e.

| (A-9) |

We now take limits as in (3.8) and use part 2 of Proposition 4.8 to conclude that

| (A-10) |

where exists by monotonicity of (cf. Proposition 4.8). Hence from (A-9), (A-10) and uniqueness of the solution to we obtain (4.40).

(iii) Setting and taking limits as in (A-8) we obtain

| (A-11) |

Proof.

[Proposition 4.16]

Recalling (4.15), (4.16), (4.17) and Proposition 4.14 we see that it suffices to show that for any and . The proof is performed in two parts.

(i) Fix and recall that (cf. Section 4.2.2 and (4.18)) for any such the continuation set is of the form . Define , then it is not hard to see by (4.17), Proposition 4.14 and (4.55) that and it is the unique classical solution of

| (A-14) |

Therefore, setting and using the Feynmann-Kac representation formula (possibly up to a standard localisation argument), we get

| (A-15) |

where we have used that -a.s. since -a.s. by the recurrence property of Brownian motion. Recalling that (cf. (2.1)) Dynkin’s formula and standard formulae for the Laplace transform of lead from (A-15) to

| (A-16) |

Since for , we have if and only if

| (A-17) |

From Proposition 4.10 we obtain and hence . Therefore, also recalling that , one has for any

We can now conclude that (A-17) is fulfilled since is increasing for and . Hence in .

(ii) Fix now , take and denote again . As in part (i) above it is not hard to see that

| (A-18) |

Set with as in part (i) above and . Then is continuous and it admits the Feynmann-Kac representation

| (A-19) |

where we have used that -a.s. due to (A-18) and to the fact that -a.s. by the recurrence property of Brownian motion. Since on then on (i.e. ) if and only if for . Thanks to Dynkin’s and Green’s formulae (cf. also [2], eq. (4.3))

| (A-20) |

where we define

| (A-21) | ||||

To simplify notation we set . The right-hand side of (A) is negative for any if and only if therein. To study the sign of we first note that and

| (A-22) |

From (A-22) it is easy to see that , since , , and . Hence is strictly decreasing and there exists a unique point such that . Clearly is a maximum of in . We claim now, and will prove later, that . Then for . Moreover since , there exists a unique point such that . This point is the unique stationary point of in and it is a negative minimum due to the fact that for any . Therefore, recalling also , we conclude that for any . From (A-19) and (A) we thus get for any .

To complete the proof it remains to show that . For that it is convenient to rewrite the first equation of (A-22) in terms of and (cf. (4.48)) so to have

| (A-23) |

From system (4.34) (see also (A-1), (3.7) and (3.8)) we obtain

| (A-24) |

which plugged into (A) give

| (A-25) |

Recalling now that , and noting that the function is nonnegative on , we conclude by (A) that for all as claimed. ∎

Proof.

[Proposition 4.17]

Since and their limits exist and are finite at , one can verify by direct computation in (4.49) (recalling also Lemma 4.5 and that ) that , and are uniformly continuous on open sets of the form for and arbitrary . Therefore has a extension to which we denote again by .

For we have , and since , and in that set (cf. (4.16), (4.17) and (4.9)). For we have

| (A-26) | ||||

| (A-27) | ||||

| (A-28) |

by (4.15) and Proposition 4.4. To find an explicit expression of (A-26) we study for (see of Proposition 4.8). In particular from (4.38), Remark 4.12 and Proposition 4.8 (noting that for ) we find

| (A-29) |

It then follows that by simple calculations, (4.9) and (4.19).

Acknowledgments. The authors thank two anonymous referees for their pertinent and useful comments.

References

- [1] Alvarez, L.H.R. (2001). Singular Stochastic Control, Linear Diffusions, and Optimal Stopping: a Class of Solvable Problems, SIAM J. Control Optim. 39(6), pp. 1697–1710.

- [2] Dayanik, S., Karatzas, I. (2003). On the Optimal Stopping Problem for One-Dimensional Diffusions, Stochastic Process. Appl. , pp. 173–212.

- [3] Davis, M., Zervos, M. (1994). A Problem of Singular Stochastic Control with Discretionary Stopping, Ann. Appl. Probab. , pp. 226–240.

- [4] De Angelis, T., Ferrari, G., and Moriarty, J. (2014). A Non Convex Singular Stochastic Control Problem and its Related Optimal Stopping Boundaries, SIAM J. Control Optim. , pp. 1199–1223.

- [5] Dynkin, E.B., Yushkevich, A.A. (1969). Markov Processes: Theorems and Problems. Plenum Press, New York.

- [6] Dufour, F., Miller, B. (2004). Singular Stochastic Control Problems, SIAM J. Control Optim. , pp. 708–730.

- [7] El Karoui, N., Karatzas, I. (1988). Probabilistic Aspects of Finite-fuel, Reflected Follower Problems, Acta Applicandae Math. , pp. 223–258.

-

[8]

European Power Exchange website. Negative prices Q&A - How they occur, what they mean. Available at:

https://www.epexspot.com/en/company-info/basics_of_the_power_market/negative_prices - [9] Fleming, W.H., Soner, H.M. (2005). Controlled Markov Processes and Viscosity Solutions, 2nd Edition. Springer.

- [10] Genoese, F., Genoese, M., Wietschel, M. (2010). Occurrence of Negative Prices on the German Spot Market for Electricity and their Influence on Balancing Power Markets, published in Energy Market (EEM2010), 7th International Conference on European Energy Markets, pp. 1–6.

- [11] Guo, X., Tomecek, P. (2009). A Class of Singular Control Problems and the Smooth Fit Principle, SIAM J. Control Optim. , pp. 3076–3099.

- [12] Guo, X., Zervos, M. (2015). Optimal Execution with Multiplicative Price Impact, SIAM J. Financial Math. , pp. 281–306.

- [13] Haussmann, U.G., Suo, W. (1995). Singular Optimal Stochastic Controls I: Existence, SIAM J. Control Optim. , pp. 916–936.

- [14] Horst, R., Pardalos, P.M., Thoai, N.V. (editors) (1995). Introduction to Global Optimization, Vol. 3 of Nonconvex Optimization and its Applications, Kluwer Academic Publishers, Dordrecht.

- [15] Horst, R., Pardalos, P.M., Thoai, N.V. (1999). DC Programming: Overview, J. Optim. Theory Appl. 103(1), pp. 1-43.

- [16] Karatzas, I., Shreve, S.E. (1984). Connections between Optimal Stopping and Singular Stochastic Control I. Monotone Follower Problems, SIAM J. Control Optim. , pp. 856–877.

- [17] Karatzas, I., Ocone, D., Wang, H., Zervos, M. (2000). Finite-Fuel Singular Control with Discretionary Stopping, Stoch. Stoch. Rep. , pp. 1–50.

- [18] Merhi, A., Zervos, M. (2007). A Model for Reversible Investment Capacity Expansion, SIAM J. Control Optim. , pp. 839–876.

- [19] Peskir, G. (2007). Principle of Smooth Fit and Diffusions with Angles, Stochastics , pp. 293–302.