Maximum entropy copula with given diagonal section

Abstract.

We consider copulas with a given diagonal section and compute the explicit density of the unique optimal copula which maximizes the entropy. In this sense, this copula is the least informative among the copulas with a given diagonal section. We give an explicit criterion on the diagonal section for the existence of the optimal copula and give a closed formula for its entropy. We also provide examples for some diagonal sections of usual bivariate copulas and illustrate the differences between them and the maximum entropy copula with the same diagonal section.

Key words and phrases:

copula, entropy, diagonal section2010 Mathematics Subject Classification:

62H05,60E051. Introduction

Dependence of random variables can be described by copula distributions. A copula is the cumulative distribution function of a random vector with uniformly distributed on . For an exhaustive overview on copulas, we refer to Nelsen [16]. The diagonal section of a -dimesional copula , defined on as is the cumulative distribution function of . The function is non-decreasing, -Lipschitz, and verifies for all with and . It was shown that if a function satisfies these properties, then there exists a copula with as diagonal section (see Bertino [2] or Fredricks and Nelsen [12] for and Cuculescu and Theodorescu [6] for ).

Copulas with a given diagonal section have been studied in different papers, as the diagonal sections are considered in various fields of application. Beyond the fact that is the cumulative distribution function of the maximum of the marginals, it also characterizes the tail dependence of the copula (see Joe [14] p.33. and references in Nelsen et al. [18], Durante and Jaworski [8], Jaworski [13]) as well as the generator for Archimedean copulas (Sungur and Yang [25]). For , Bertino in [2] introduces the so-called Bertino copula given by for . Fredricks and Nelsen in [12] give the example called diagonal copula defined by for . In Nelsen et al. [17, 18] lower and upper bounds related to the pointwise partial ordering are given for copulas with a given diagonal section. They showed that if is a symmetric copula with diagonal section , then for every , we have:

Durante et al. [10] provide another construction of copulas for a certain class of diagonal sections, called MT-copulas named after Mayor and Torrens and defined as . Bivariate copulas with given sub-diagonal sections are constructed from copulas with given diagonal sections in Quesada-Molina et al. [22]. Durante et al. [9] or [18] introduce the technique of diagonal splicing to create new copulas with a given diagonal section based on other such copulas. According to [8] for and Jaworski [13] for , there exists an absolutely continuous copula with diagonal section if and only if the set has zero Lebesgue measure. de Amo et al. [7] is an extension of [8] for given sub-diagonal sections. Further construction of possibly asymmetric absolutely continuous bidimensional copulas with a given diagonal section is provided in Erdely and González [11].

Our aim is to find the most uninformative copula with a given diagonal section . We choose here to maximize the relative entropy to the uniform distribution on , among the copulas with given diagonal section. This is equivalent to minimizing the Kullback-Leibler divergence with respect to the independent copula. The Kullback-Leibler divergence is finite only for absolutely continuous copulas. The previously introduced bivariate copulas , and are not absolutely continuous, therefore their Kullback-Leibler divergence is infinite. Possible other entropy criteria, such as Rényi, Tsallis, etc. are considered for example in Pougaza and Mohammad-Djafari [21]. We recall that the entropy of a -dimensional absolutely continuous random vector can be decomposed as the sum of the entropy of the marginals and the entropy of the corresponding copula (see Zhao and Lin [26]) :

where is the entropy of the random variable with density , and is a random vector with uniformly distributed on , such that has the same copula as ; namely is distributed as with the cumulative distribution function of . Maximizing the entropy of with given marginals therefore corresponds to maximizing the entropy of its copula. The maximum relative entropy approach for copulas has an extensive litterature. Existence results for an optimal solution on convex closed subsets of copulas for the total variation distance can be derived from Csiszár [5]. A general discussion on abstract entropy maximization is given by Borwein et al. [3]. This theory was applied for copulas and a finite number of expectation constraints in Bedford and Wilson [1]. Some applications for various moment-based constraints include rank correlation (Meeuwissen and Bedford [15], Chu [4], Piantadosi et al. [20]) and marginal moments (Pasha and Mansoury [19]).

We shall apply the theory developed in [3] to compute the density of the maximum entropy copula with a given diagonal section. We show that there exists a copula with diagonal section and finite entropy if and only if satisfies: . Notice that this condition is stronger than the condition of having zero Lebesgue measure which is required for the existence of an absolutely continuous copula with diagonal section . Under this condition, and in the case of , the optimal copula’s density turns out to be of the form, for :

with the notation , see Theorem 2.3. The optimal copula’s density in the general case is given in Theorem 2.4. Notice that is symmetric, that is it is invariant under the permutation of the variables. This provides a new family of absolutely continuous symmetric copulas with given diagonal section enriching previous work on this subject that we discussed, see [2],[8],[9],[10],[11],[12],[18]. We also calculate the maximum entropy copula for diagonal sections that arise from well-known families of bivariate copulas.

The rest of the paper is organised as follows. Section 2 introduces the definitions and notations used later on, and gives the main theorems of the paper. In Section 3 we study the properties of the feasible solution of the problem for a special class of diagonal sections with . In Section 4, we formulate our problem as a linear optimization problem in order to apply the theory established in [3]. Then in Section 5 we give the proof for our main theorem showing that is indeed the optimal solution when . In Section 6 we extend our results for the general case when has zero Lebesgue measure. We give in Section 7 several examples with diagonals of popular bivariate copula families such as the Gaussian, Gumbel or Farlie-Gumbel-Morgenstern copulas among others.

2. Main results

Let be fixed. We recall a function defined on , with , is a -dimensional copula if there exists a random vector such that are uniform on and for , with the convention that for and elements of if and only if for all . We shall say that is the copula of . We refer to [16] for a monograph on copulas. The copula is said absolutely continuous if the random variable has a density, which we shall denote by . In this case, we have that a.e. for . When there is no confusion, we shall write for the density associated to the copula . We denote by the set of -dimensional copulas and by the subset of the -dimensional absolutely continuous copulas.

The diagonal section of a copula is defined by: . Let us note, for , . Notice that if is the copula of , then is the cumulative distribution function of as for . We denote by the set of diagonal sections of -dimensional copulas and by the set of diagonal sections of absolutely continuous copulas. According to [12], a function defined on belongs to if and only if:

-

(i)

is a cumulative function on : , and is non decreasing;

-

(ii)

for and is -Lipschitz: for .

For , we shall consider the set of copulas with diagonal section , and the subset of absolutely continuous copulas with section . According to [8] and [13], the set is non empty if and only if the set has zero Lebesgue measure.

For a non-negative measurable function defined on , we set

Since copulas are cumulative functions of probability measures, we will consider the Kullback-Leibler divergence relative to the uniform distribution as a measure of entropy, see [5]:

with the density associated to when . Notice the Shannon-entropy introduced in [24] of the probability measure defined on with cumulative distribution function is defined as . Thus minimizing the Kullback-Leibler divergence (w.r.t. the uniform distribution) is equivalent to maximizing the Shannon-entropy. It is well known that the copula with density , which corresponds to being independent, minimizes over .

We shall minimize the entropy over the set or equivalently over of copulas with a given diagonal section (in fact for as otherwise is empty). If minimizes on , it means that is the least informative (or the “most random”) copula with given diagonal section .

For , let us denote:

| (1) |

Notice that and it is infinite if . Since is -Lipschitz, the derivative of exists a.e. and since is non-decreasing we have a.e. . This implies that and are well defined. Let us denote:

| (2) |

We have the rough upper bound:

| (3) |

The following Proposition gives an absolutely continuous copula whose diagonal section is . The proof of this Proposition can be found in Section 3 and Section 8 is dedicated to the proof of (6).

Proposition 2.1.

Let with . We define, for :

| (4) |

Then defined a.e. by

| (5) |

is the density of a symmetric copula with diagonal section . Furthermore, we have:

| (6) |

This and (3) readily implies the following Remark.

Remark 2.2.

Let such that . We have if and only if .

We can now state our main result in the simpler case . It gives the necessary and sufficient condition for to be the unique optimal solution of the minimization problem. The proof is given in Section 5.

Theorem 2.3.

Let such that .

-

a)

If then .

-

b)

If then and is the unique copula such that .

To give the answer in the general case where has zero Lebesgue measure, we need some extra notations. Since is continuous, we get that can be written as the union of non-empty open intervals , with and at most countable. Notice that and . For and , we set and for :

| (7) |

It is clear that satisfies (i) and (ii) and it belongs to as . Let be defined by (5) with replaced by . For such that , we define the function by, for :

| (8) |

with . It is easy to check that is a copula density and that is zero outside for . We state our main result in the general case whose proof is given in Section 6.

Theorem 2.4.

3. Proof of Proposition 2.1

We assume that and . We give the proof of Proposition 2.1, which states that , with density given by (5), is indeed a symmetric copula with diagonal section whose entropy is given by (6).

Recall the definition of and from Theorem 2.3. Notice that by construction is non-negative and well defined on . In order to prove that is the density of a copula, we only have to prove that for all , :

or equivalently

We define for :

| (9) |

Elementary computations yield for :

| (10) |

Notice that which implies that . A direct integration gives:

| (11) |

We also have:

| (12) |

where we used for the last step that and . We have:

where we first divided the integral according to which was the maximum; then we used (9) for the second equality, finally (11) and (3) for the forth. This implies that is indeed the density of a copula. We denote by the copula with density . We check that is the diagonal section of . Using (11), we get, for :

4. The minimization problem

Let . As a first step we will show, using [3], that the problem of a maximum entropy copula with a given diagonal section has at most a unique optimal solution. To formulate this problem in the framework of [3], we introduce the continuous linear functional defined by, for , and ,

We also define with and for , with the identity map on . Notice that the conditions , , and a.e. imply that is the density of a copula . If we assume further that the condition holds then the diagonal section of is (thus ).

Since is infinite outside and the density of any copula in belongs to , we get that minimizing over is equivalent to the linear optimization problem given by:

| () |

We say that a function is feasible for if , a.e., and . Notice that any feasible is the density of a copula. We say that is an optimal solution to if is feasible and for all feasible.

Proposition 4.1.

Let . If there exists a feasible , then there exists a unique optimal solution to and it is symmetric.

Proof.

Since implies that is , we can directly apply Corollary 2.3 of [3] which states that if there exists a feasible , then there exists a unique optimal solution to . Since the constraints are symmetric and the functional is also symmetric, we deduce that the unique optimal solution is also symmetric. ∎

The next Proposition gives that the set of zeros of any non-negative solution of contains:

| (13) |

Proposition 4.2.

Let . If is feasible then a.e. on (that is a.e.).

Proof.

Recall that . Since , the condition , that is for all

implies, by the monotone class theorem, that for all measurable subset of , we have:

Since a.e., we deduce that a.e. .

Next, notice that for all , , the symmetrical property of gives:

This implies that a.e. . This gives the result. ∎

We define to be the Lebesgue measure restricted to : . We define, for :

From Proposition 4.2 we can deduce that if is feasible then . Let us also define, for , :

The corresponding optimization problem is given by :

| () |

with . For , we define:

Using Proposition 4.2, we easily get the following Corollary.

Corollary 4.3.

If is a solution of , then is a solution of . If is a solution of , then it is also a solution of .

5. Proof of Theorem 2.3

5.1. Form of the optimal solution

Let be the adjoint of . We will use Theorem 2.9. from [3] on abstract entropy minimization, which we recall here, adapted to the context of .

Theorem 5.1 (Borwein, Lewis and Nussbaum).

Suppose there exists -a.e. which is feasible for . Then there exists a unique optimal solution, , to . Furthermore, we have -a.e. and there exists a sequence of elements of such that:

| (14) |

We first compute . For and , we have:

where we used the definition of the adjoint operator for the first equality, Fubini’s theorem for the second, and the following notation for the third equality:

Thus, we can set for and :

| (15) |

Now we are ready to prove that the optimal solution of is the product of measurable univariate functions.

Lemma 5.2.

Let such that . Suppose that there exists -a.e.which is feasible for . Then there exist non-negative, measurable functions defined on such that

with if and if .

Proof.

According to Theorem 5.1, there exists a sequence of elements of such that the optimal solution, say , satisfies (14). This implies, thanks to (15), that there exist sequences of elements of such that the following convergence holds in :

| (16) |

Arguing as in Proposition 4.1 and since is symmetric, we deduce that is symmetric. Therefore we shall only consider functions supported on the set . The convergence (16) holds in . For simplicity, we introduce the functions defined by for , and . Then we have in :

| (17) |

We first assume that there exist and measurable functions defined on such that -a.e. on :

| (18) |

The symmetric property of seen in Proposition 4.1 implies we can choose for up to adding a constant to . Set and so that -a.e. on :

| (19) |

Recall . From the definition (13) of , we deduce that without loss of generality, we can assume that if and if . Use the symmetry of to conclude.

To complete the proof, we now show that (18) holds for and measurable functions. We introduce the notation . Let us define the probability measure on . We fix , . In order to apply Proposition 2 of [23], we first check that is absolutely continuous with respect to , where and are the marginals of . Notice the following equivalence of measures:

| (20) |

Let be measurable. We have:

By Fubini’s theorem this last equiality is equivalent to:

| (21) |

Since, for , , we have for all . Therefore (21) is equivalent to

This implies that there exists a.e. on such that

Similarly we have for that if and only if

| (22) |

Since, for , , there exists a.e. on such that . Therefore by (20) we deduce that is absolutely continuous with respect to . Then according to Proposition 2 of [23], (17) implies that there exist measurable functions and defined respectively on and , such that -a.e. on :

As -a.e. , this equality holds -a.e. on . Since we have such a representation for every , we can easily verify that there exists a measurable function defined on such that -a.e. on .

∎

5.2. Calculation of the optimal solution

Now we prove that the optimal solution to , if it exists, is indeed .

Proposition 5.3.

Let such that . If there exists an optimal solution to , then it is given by (5).

Proof.

In Lemma 5.2 we have already shown that if an optimal solution exists for , then it is of the form . Here we will prove that the constraints of uniquely determine the functions and up to a multiplicative constant, giving . We set for :

which take values in . From , we have for :

| (23) |

Taking the derivative with respect to gives a.e. on :

| (24) |

This implies that is finite for all and thus . Similarly, using that , we get that for :

Using this and (5.2) we deduce that for :

| (25) |

Since on , we have that and are positive on . Dividing (24) by (25) gives a.e. for :

We integrate both sides to get for :

Taking the exponential yields:

| (26) |

for some positive constant . From (25) and (26), we derive:

| (27) |

This proves that the function is uniquely determined up to a multiplicative constant and so is . With the help of (24) and (27), we can express as, for :

| (28) |

The function is also uniquely determined up to a multiplicative constant. Therefore (24) implies that there is a unique of the form (19) which solves . (Notice however that the functions and are defined up to a multiplicative constant.) Then according to Proposition 2.1 we get that defined by (19) with and defined by (4) solves , implying that is equal to . ∎

5.3. Proof of Theorem 2.3

6. Proof of Theorem 2.4

We first state an elementary Lemma, whose proof if left to the reader. For a function defined on and , we define by, for :

Lemma 6.1.

If is the density of a copula such that and for some fixed , then is also the density of a copula, and its diagonal section, , is given by, for :

According to Remark 2.5, it is enough to consider the case , that is with zero Lebesgue measure. We shall assume that . Since is continuous, we get that can be written as the union of non-empty open intervals , with and non-empty and at most countable. Set . Since is of zero Lebesgue measure, we have . We define also

For , notice that any feasible function of satisfies for all :

where . This implies that a.e. on . We set for . We deduce that if is feasible for , then we have that a.e.:

| (29) |

and:

| (30) |

Thanks to Lemma 6.1, the condition is equivalent to for all . We deduce that the optimal solution of , if it exists, is given by (29), where the functions are the optimal solutions of for . Notice that by construction . Thanks to Theorem 2.3, the optimal solution to exists if and only if we have ; and if it exists it is given by . Therefore, if there exists an optimal solution to , then it is given by (8). To conclude, we have to compute . Recall that for . We have:

where we used the monotone convergence theorem for the first equality, (6) for the second and the fact that is uniformly bounded over and the monotone convergence theorem for the last. Elementary computations yields:

So, we get:

Since is uniformly bounded over , we get that is finite if and only if is finite. To end the proof, recall the definition of to conclude that .

7. Examples for

In this section we compute the density of the maximum entropy copula for various diagonal sections of popular bivariate copula families. In this Section, and will denote elements of . The density for is of the form . We illustrate these densities by displaying their isodensity lines or contour plots, and their diagonal cross-section defined as , .

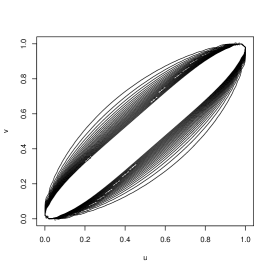

7.1. Maximum entropy copula for a piecewise linear diagonal section

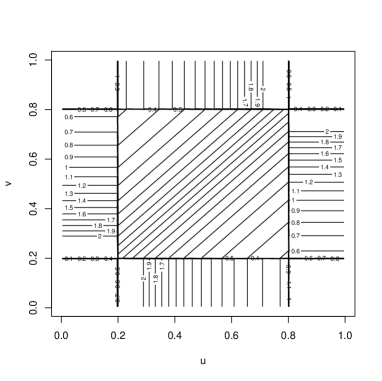

Let . Let us calculate the density of the maximum entropy copula in the case of the following diagonal section:

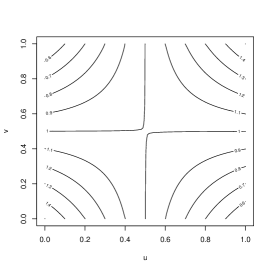

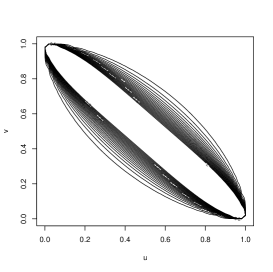

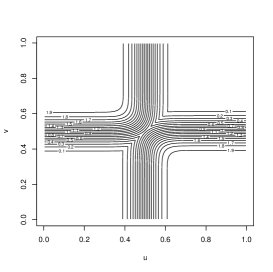

This example was considered for example in [17]. The limiting cases and correspond to the Fréchet-Hoeffding upper and lower bound copulas, respectively. However for , , therefore every copula with this diagonal section gives . (In fact the only copula that has this diagonal section is the Fréchet-Hoeffding upper bound defined by , .) When , is satisfied, therefore we can apply Theorem 2.3 to compute the density of the maximum entropy copula. The graph of can be seen in Figure 1 for . We compute the functions , and :

| (31) |

Figure 2(b) shows the isodensity lines of . In the limiting case of , the diagonal section is given by ,which is the pointwise lower bound for all elements in . Accordingly, it is the diagonal section of the Fréchet-Hoeffding lower bound copula given by for . All copulas having this diagonal section are of the following form:

where and are copula functions. Recall that the independent copula with uniform density on minimizes over . According to (31), the maximum entropy copula with diagonal section is . This corresponds to choosing the maximum entropy copulas on and .

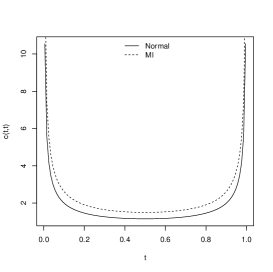

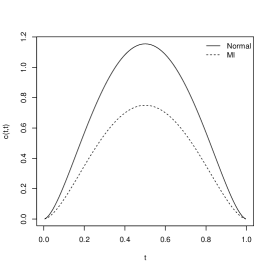

7.2. Maximum entropy copula for

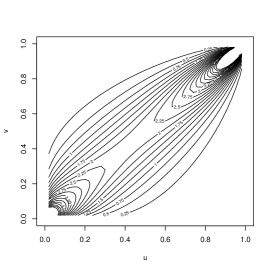

Let . We consider the family of diagonal sections given by . This corresponds to the Gumbel family of copulas and also to the family of Cuadras-Augé copulas. The Gumbel copula with parameter is an Archimedean copula defined as, for :

with generator function . Its diagonal section is given by with . The Cuadras-Augé copula with parameter is defined as, for :

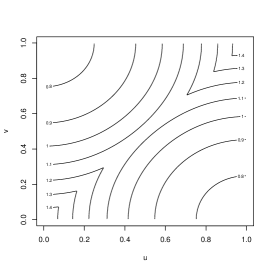

It is a subclass of the two parameter Marshall-Olkin family of copulas given by . The diagonal section of is given by with . While the Gumbel copula is absolutely continuous, the Cuadras-Augé copula is not, although it has full support. Since , we can apply Theorem 2.3. To give the density of the maximum entropy copula, we have to calculate . Elementary computations yield:

The density is therefore given by, for :

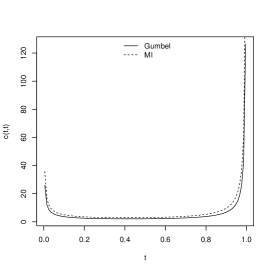

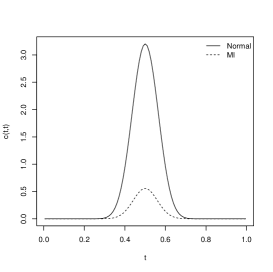

Figure 3 represents the isodensity lines of the Gumbel and the maximum entropy copula with common parameter , which corresponds to for the Gumbel copula. We have also added a graph of the diagonal cross-section of the two densities. In the limiting case of , the above formula gives , which is the density of the independent copula , which is also maximizes the entropy on the entire set of copulas.

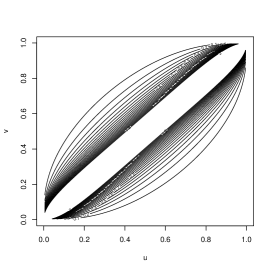

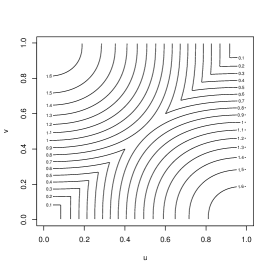

7.3. Maximum entropy copula for the Farlie-Gumbel-Morgenstern diagonal section

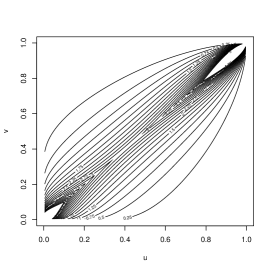

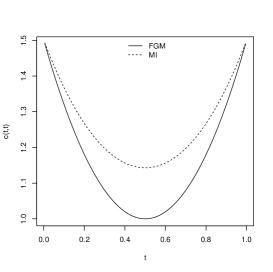

Let . The Farlie-Gumbel-Morgenstern family of copulas (FGM copulas for short) are defined as:

These copulas are absolutely continuous with densities . Its diagonal section is given by:

Since on and it verifies , we can apply Theorem 2.3 to calculate the density of the maximum entropy copula. For , we have:

The density is given by, for and :

Figure 4 illustrates the isodensities of the FGM copula and the maximum entropy copula with the same diagonal section for as well as the diagonal cross-section of their densities.

The case of corresponds once again to the diagonal section , and the formula gives the density of the independent copula , accordingly.

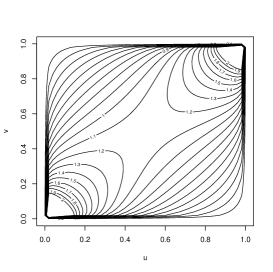

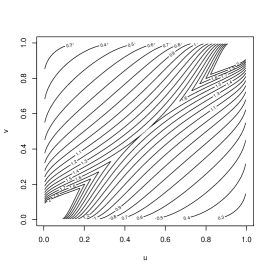

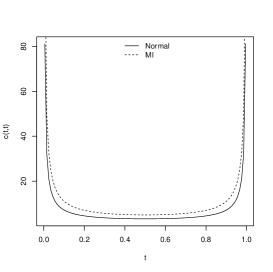

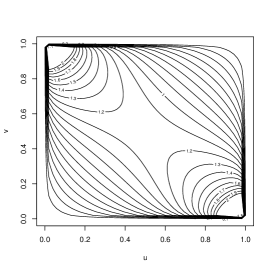

7.4. Maximum entropy copula for the Gaussian diagonal section

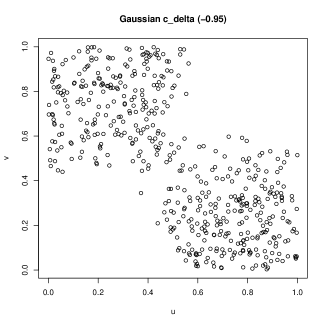

The Gaussian (normal) copula takes the form:

with the joint cumulative distribution function of a two-dimensional normal random variable with standard normal marginals and correlation parameter , and the quantile function of the standard normal distribution. The density of can be written as:

where and stand for respectively the densities of a standard normal distribution and a two-dimensional normal distribution with correlation parameter , respectively. The diagonal section and its derivative are given by:

| (33) |

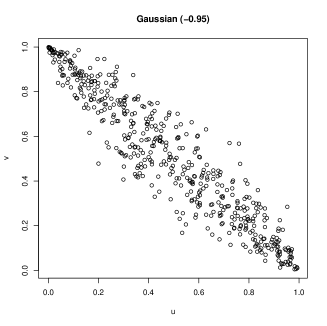

Since verifies on and , we can apply Theorem 2.3 to calculate the density of the maximum entropy copula. We have calculated numerically the density of the maximum entropy copula with diagonal section for and . The comparison between these densities and the densities of the corresponding normal copula can be seen in Figures 5,6 and 7. We observe a very different behaviour of and in the case of . In the limiting case when goes down to , we retrieve the diagonal , which we have studied earlier in Section 7.1.

8. Appendix - Calculation of the entropy of

Let us first introduce some notations. Let . Since for , we deduce by the monotone convergence theorem that:

| (34) |

with:

Using and that is a non-decresing, -Lipschitz function, we get that for :

| (35) |

We set:

| (36) |

From the symmetric property of , we have that

| (37) |

with:

We introduce . For , we have:

Notice that using (10) and (3), we have:

By Fubini’s theorem, we get:

with:

To study , we first give an upper bound for the term :

| (38) | ||||

where we used that for for the first inequality, (3) for the first equality, and (35) for the last inequality. Since , we have, using (36):

where we used (3) for the second inequality, and that is non-decreasing and (38) for the third inequality. On the other hand, we have , if , which gives:

where we used (38) and for for the first inequality, and that is non-decreasing for the last. This proves that . For , we first observe that for we have and thus:

| (39) |

Using the previous inequality we obtain:

where we used for the first inequality, (39) for the second, (10) and (3) in the following equality, and (35) to conclude. For an upper bound, we have after noticing that :

where we used (39) and for the second inequality; (10) and (3) in the second equality; and (35) to conclude. The results on the two bounds show that . Similarly, for , we get:

with and given by, using (11):

Similarly to we can show that .

Adding up and gives

with

Notice that is non-decreasing in and that:

Since , we deduce that and are bounded on from above by and from below by and therefore integrable on . This implies :

As for , we have by integration by parts:

Summing up all the terms and taking the limit give :

References

- [1] T. Bedford and K. Wilson. On the construction of minimum information bivariate copula families. Annals of the Institute of Statistical Mathematics, pages 1–21, 2013.

- [2] S. Bertino. Sulla dissomiglianza tra mutabili cicliche. Metron, 35:53 – 88, 1977.

- [3] J. Borwein, A. Lewis, and R. Nussbaum. Entropy minimization, problems, and doubly stochastic kernels. Journal of Functional Analysis, 123(2):264 – 307, 1994.

- [4] B. Chu. Recovering copulas from limited information and an application to asset allocation. Journal of Banking & Finance, 35(7):1824–1842, 2011.

- [5] I. Csiszár. -divergence geometry of probability distributions and minimization problems. Ann. Probability, 3:146–158, 1975.

- [6] I. Cuculescu and R. Theodorescu. Copulas: diagonals, tracks. Revue roumaine de mathématiques pures et appliquées, 46(6):731–742, 2001.

- [7] E. de Amo, M. D. Carrillo, and J. F. Sánchez. Absolutely continuous copulas with given sub-diagonal section. Fuzzy Sets and Systems, 228(0):105 – 113, 2013. Special issue on 2011 and EUSFLAT/LFA 2011.

- [8] F. Durante and P. Jaworski. Absolutely continuous copulas with given diagonal sections. Communications in Statistics - Theory and Methods, 37(18):2924–2942, 2008.

- [9] F. Durante, A. Kolesárová, R. Mesiar, and C. Sempi. Copulas with given diagonal sections: novel constructions and applications. Internat. J. Uncertain. Fuzziness Knowledge-Based Systems, 15(4):397–410, 2007.

- [10] F. Durante, R. Mesiar, and C. Sempi. On a family of copulas constructed from the diagonal section. Soft Computing, 10:490–494, 2006.

- [11] A. Erdely and J. M. González-Barrios. On the construction of families of absolutely continuous copulas with given restrictions. Comm. Statist. Theory Methods, 35(4-6):649–659, 2006.

- [12] G. Fredricks and R. Nelsen. Copulas Constructed from Diagonal Sections. In V. Beneš and J. Štěpán, editors, Distributions with given Marginals and Moment Problems, pages 129–136. Springer Netherlands, 1997.

- [13] P. Jaworski. On copulas and their diagonals. Information Sciences, 179(17):2863 – 2871, 2009.

- [14] H. Joe. Multivariate models and dependence concepts, volume 73 of Monographs on Statistics and Applied Probability. Chapman & Hall, London, 1997.

- [15] A. Meeuwissen and T. Bedford. Minimally informative distributions with given rank correlation for use in uncertainty analysis. Journal of Statistical Computation and Simulation, 57(1-4):143–174, 1997.

- [16] R. B. Nelsen. An introduction to copulas. Springer Series in Statistics. Springer, New York, second edition, 2006.

- [17] R. B. Nelsen, J. J. Q. Molina, J. A. R. Lallena, and M. Úbeda Flores. Best-possible bounds on sets of bivariate distribution functions. Journal of Multivariate Analysis, 90(2):348 – 358, 2004.

- [18] R. B. Nelsen, J. J. Quesada-Molina, J. A. Rodríguez-Lallena, and M. Úbeda Flores. On the construction of copulas and quasi-copulas with given diagonal sections. Insurance: Mathematics and Economics, 42(2):473 – 483, 2008.

- [19] E. Pasha and S. Mansoury. Determination of maximum entropy multivariate probability distribution under some constraints. Applied Mathematical Sciences, 2(57):2843–2849, 2008.

- [20] J. Piantadosi, P. Howlett, and J. Borwein. Copulas with maximum entropy. Optimization Letters, 6:99–125, 2012.

- [21] D.-B. Pougaza, A. Mohammad-Djafari, and J.-F. Bercher. Link between copula and tomography. Pattern Recognition Letters, 31(14):2258–2264, 2010.

- [22] J. J. Quesada-Molina, S. Saminger-Platz, and C. Sempi. Quasi-copulas with a given sub-diagonal section. Nonlinear Analysis: Theory, Methods & Applications, 69(12):4654 – 4673, 2008.

- [23] L. Rüschendorf and W. Thomsen. Note on the Schrödinger equation and -projections. Statist. Probab. Lett., 17(5):369–375, 1993.

- [24] C. E. Shannon. A mathematical theory of communication. Bell System Technical Journal, 27:379–423, 1948.

- [25] E. A. Sungur and Y. Yang. Diagonal copulas of Archimedean class. Comm. Statist. Theory Methods, 25(7):1659–1676, 1996.

- [26] N. Zhao and W. T. Lin. A copula entropy approach to correlation measurement at the country level. Applied Mathematics and Computation, 218(2):628 – 642, 2011.