On the implicite interest rate in the Yunus equation

1 Introduction : microcredit

Microcredit is a set of contracts taylored to provide very small loans to very poor people to help develop small businesses or activities generating income. The basic idea came from the finding that a large part of humanity has no access to traditional credit because banks require their borrowers to meet a range of criteria, such as being able to read and write, bears some identification documents, or to have already secured a minimum deposit. The first experiments date back to the 70s in Bangladesh as an initiative of Muhammad Yunus, then a professor of economics at Chittagong University. In 1974, he watched helplessly as a terrible famine in the little village Joha near to his University. He then with his students asks the craftsmen and peasants of the village in order to try to understand their needs and lists a demand for small loans for 42 women to whom he finally decides to pay himself a total of about 27 Euros. Then he spends nearly 10 years trying to persuade banks to take on these loans before finally deciding to start his own bank, the Grameen Bank in 1983. This bank and himself receive the Nobel Prize for Peace in 2006. Currently microcredit activity has spread to most countries in the world, it is ensured by close 10 000 Micro Finance Institutes (MFIs) who lend 50 billions euros to almost 500 millions beneficiaries. The main characteristics of microcredit are

-

•

Very small loans over short periods (10 Euros a year) with frequent (weekly) reimbursements.

-

•

Beneficiaries are mostly women.

-

•

Borrowers can’t provide personal wealth to secure the loan.

-

•

Usually loans are with joint liability of a group of borrowers (5 to 30) each borrower receiving her loan individually but all are interdependent in that they must assume all or part of the failure (called the “default”) of any member of the group.

-

•

Interest rates are high, around 20%, some of them up to 30%.

-

•

Possibility of a new loan granted automatically in case of timely refunds (dynamic incentive mechanism).

-

•

repayment rate close to 100%.

2 The Yunus polynomial and equation

Grameen lends 1000 BDT (Bangladesh Taka) to borrowers that pay back 22 BDT111The value of Bangladesh Taka (BDT) is about Euro. each week during 50 weeks. Let’s denote by the annual continuously compound interest rate. The present value of the BDT refunded after one week is this value of those of the next payment is …and so on. So, letting , as the 50 refundings balance the 1000 BDT received, we get following equation for :

| (1) |

that reduces to (the degree 51 polynomial equation) where denotes what we shall call que Yunus polynomial

| (2) |

We observe that has obviously as zero, has two other zeros , and all other zeros are complex conjugate. An approximation of gives which leads to , so nearly .

But some borrowers don’t pay in time, so the -th payment takes place at some random time

Lets assume i.i.d, , the geometric distribution, , close to ; in other words each week the borrower has probability to be able to pay the BDT she should pay, weekly refunding accidents being assumed to be independent. So becomes a random variable, , satisfying the “Yunus equation” :

| (3) |

For the sake of getting a better understanding of the risks faced by the lender under these new asumptions we wish to have informations on the probability law of the random variable . The sequel of this paper is devoted to the results we got so far.

3 Actuarial expected rate

Let us call actuarial expected rate the positive real number such that, replacing by , it satisfies the expectation of the Yunus equation :

where is the moment generating function of . So , the positive non trivial zero of the Yunus polynomial, which leads to

So .

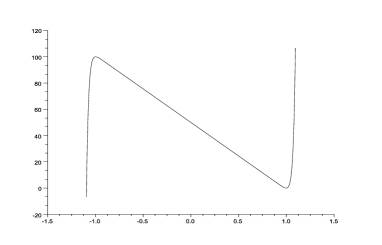

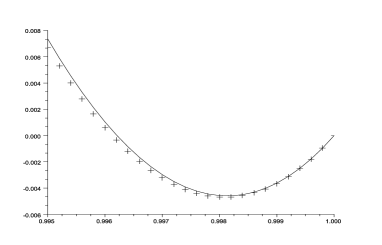

4 Some experimental results

We have the chance to have with us three good students222Léo Augé, Aurore Lebrun, and Anaïs Pozin from Polytech’Nice with skills in Scilab that did some numerical experiments. It turns out that the law for R is impressively similar to a Gaussian , with

![[Uncaptioned image]](/html/1312.2179/assets/x1.png)

On the other hand, obviously , so can’t be Gaussian, and indeed, even if the skewness of if very small, its kurtosis is close to , not .

So the question is (and stays, up to here) : what is the law of ?

5 Where could infinitesimals enter the model ?

Here some remarks related to the idea that “50=N is large”. Observe that, for and the equation is equivalent (dividing both members by 20) to

| (4) |

Now assume is infinitely large and let , so is a blow-up of around . Let , so (4) reduces to . But, as is infinitely large, and denoting by o/ any infinitesimal, we have

Actually, the equation has two solutions : and so we get the approximation for the non-trivial positive solution of . For for instance we have , and .

So, denoting by the solution of different of we have

Proposition 1

Assume that the number of refunds is infinitely large. Then the actuarial expected rate is

| (5) |

References

- [1] M. Yunus avec Alan Jolis. Vers un monde sans pauvreté. JC Lattès, 1997.

- [2] M. Yunus with Alan Jolis. Banker to the Poor : micro-lending and the battle against world poverty. Public Affairs, 1999.

Address of the authors:

Université de Nice Sophia-Antipolis

Laboratoire de Mathématiques Jean Dieudonné

Parc Valrose

06108 Nice cedex 2, France

E-mail: diener@unice.fr, pheak@unice.fr