Universal Algorithm for Online Trading Based on the Method of Calibration

\nameVladimir V. V’yugin \emailvyugin@iitp.ru

\addrInstitute for Information Transmission Problems

Russian Academy of Sciences

Bol’shoi Karetnyi per. 19

Moscow GSP-4, 127994, Russia

\AND\nameVladimir G. Trunov \emailtrunov@iitp.ru

\addrInstitute for Information Transmission Problems

Russian Academy of Sciences

Bol’shoi Karetnyi per. 19

Moscow GSP-4, 127994, Russia

Abstract

We present a universal method for algorithmic trading in Stock Market

which performs asymptotically at least as well as any stationary trading strategy

that computes the investment at each step using a fixed function of the

side information that belongs to a given RKHS

(Reproducing Kernel Hilbert Space). Using a universal kernel,

we extend this result for any continuous stationary strategy.

In this learning process, a trader rationally chooses his gambles

using predictions made by a randomized well-calibrated

algorithm. Our strategy is based on Dawid’s notion of

calibration with more general checking rules and on

some modification of Kakade and Foster’s randomized rounding algorithm

for computing the well-calibrated forecasts. We combine the method of

randomized calibration with Vovk’s method of

defensive forecasting in RKHS.

Unlike in statistical theory, no stochastic assumptions are made about

the stock prices. Our empirical results on historical markets provide strong

evidence that this type of technical trading can “beat the market”

if transaction costs are ignored.

Predicting sequences is the key problem for machine learning, computational

finance and statistics. These predictions can serve as a base

for developing the efficient methods for playing financial games

in Stock Market.

The learning process proceeds as follows: observing a finite-state

sequence given online, a forecaster assigns a subjective estimate to

future states.

A minimal requirement for testing any prediction algorithm is that

it should be calibrated (cf. Dawid 1982).

Dawid gave an informal explanation of calibration for binary outcomes.

Let a sequence of binary outcomes

be observed by a forecaster whose task is to give a probability

of a future event . In a typical example, is interpreted

as a probability that it will rain. Forecaster is said to be

well-calibrated if it rains as often as he leads us to expect. It should rain

about of the days for which , and so on.

A more precise definition is as follows.

Let denote the characteristic function of a

subinterval , i.e., if and ,

otherwise.

An infinite sequence of forecasts is calibrated

for an infinite binary sequence of outcomes

if for characteristic function

of any subinterval of the calibration error tends to zero, i.e.,

as .

The indicator function determines some

“checking rule” that selects indices , where we compute

the deviation between forecasts and outcomes .

If the weather acts adversatively, then, as shown by Oakes (1985)

and Dawid (1985), any deterministic

forecasting algorithm will not always be calibrated.

Foster and Vohra (1998) show that calibration is almost surely

guaranteed with a randomizing forecasting rule, i.e., where the forecasts

are chosen using internal randomization and the forecasts are hidden

from the weather until the weather makes its decision whether to rain or not.

The origin of the calibration algorithms is the Blackwell (1956)

approachability theorem

but, as its drawback, the forecaster has to use linear programming to compute

the forecasts. We modify and generalize a more computationally efficient method from

Kakade and Foster (2004), where “an almost deterministic”

randomized rounding universal forecasting algorithm is presented.

For any sequence of outcomes and for any precision of

rounding ,

an observer can simply randomly round the deterministic forecast up to

to a random forecast in order to calibrate

for this sequence with probability one:

(1)

where is the characteristic function of any subinterval of .

This algorithm can be easily generalized

such that the calibration error tends to zero as .

Kakade and Foster and others considered a finite outcome space

and a probability distribution as the forecast. In this paper,

the outcomes are real numbers from unit interval and the

forecast is a single real number (which can

be an output of a random variable). This setting is closely

related to Vovk (2005a) defensive forecasting approach

(see below).

In this case real valued predictions could

be interpreted as mean values of future outcomes under

some unknown to us probability distributions in . We do not know

precise form of such distributions – we should predict only future means.

The well known applications of the method of calibration belong

to different fields of the game theory and machine learning.

Kakade and Foster proved that empirical

frequencies of play in any normal-form game with finite

strategy sets converges to a set of correlated equilibrium if

each player chooses his gamble as the best response to the well

calibrated forecasts of the gambles of other players. In series

of papers:

Vovk et al. (2005), Vovk (2005a), Vovk (2006), Vovk (2006a),

Vovk (2007), Vovk developed the method of calibration for the

case of more general RKHS and

Banach spaces. Vovk called his method defensive forecasting

(DF). He also applied his method for recovering unknown

functional dependencies presented by arbitrary functions from

RKHS and Banach spaces. Chernov et al. (2010) show

that well-calibrated forecasts can be used to compute

predictions for the Vovk (1997) aggregating algorithm.

In defensive forecasting, continuous loss (gain) functions are considered.

In this paper we present a new application of the method of

calibration. We construct “a universal” strategy for algorithmic trading in

Stock Market which performs asymptotically at least as well as any not “too

complex” trading strategy . Technically, we are

interested in the case where the trading strategy is

assumed to belong to a large reproducing kernel Hilbert space

(to be defined shortly) and the complexity of is measured

by its norm. Using a universal kernel, we extend this result

to any continuous stationary trading strategy. Our universal

trading strategy is represented by a discontinuous function though

it uses a randomization.

First discuss some standard financial terminology.

A trader in Stock Market uses a strategy: going long or going short,

or skip the step.

In finance, a long position in a security, such as a stock or a bond,

or equivalently to be long in a security, means that the holder of the position

owns the security and will profit if the price of the security goes up.

Short selling (also known as shorting or going short) is the practice of

selling securities or other financial instruments, with the intention of

subsequently repurchasing them (“covering”) at a lower price.

In this paper, the problem of universal sequential investment in Stock Market

with side information is studied.

We consider the method of trading called in financial industrial

applications algorithmic trading or

systematic quantitative trading, which

means rule-based automatic trading strategies, usually implemented

with computer based trading systems.

The problem of algorithmic

trading is considered in machine learning framework, where algorithms

adaptive to input data are designed and their performance is evaluated.

There are three common types of analysis for adaptive algorithms: average case

analysis which requires a statistical model of input data; worst-case

analysis which is non-informative because, for any trading algorithm,

we can present a sequence of stock prices moving in the

direction opposite to the trader’s decisions;

competitive analysis which is popular

in the prediction with expert advice framework.

A non-traditional objective (in computational finance) is to

develop algorithmic trading strategies that are in some sense always

guaranteed to perform well. In competitive analysis, the

performance of an algorithm is measured to any trading

algorithm from a broad class. We only ask than an algorithm

performs well relative to the difficulty in classsifying of the input data.

Given a particular performance measure, an adaptive algorithm is

strongly competitive with a class of trading algorithms if it

achieves the maximum possible regret over all input sequences.

Unlike in statistical theory, no stochastic assumptions are

made about the stock prices.

This line of research in finance was pioneered by Cover

(see Cover and Gluss 1986, Cover 1991, Cover and Ordentlich 1996) who designed

universal portfolio selection algorithms that can provably do well (in terms

of their total return) with respect to some adaptive online or offline

benchmark algorithms. Such algorithms are called universal.

We consider the simplest case: algorithmic trading with only stock.

Our results can be generalized for the case of several stocks

and for dynamical portfolio hedging in sense of framework proposed

by Cover and Ordentlich (1996).

We consider a game with players: Stock Market and Trader.

At the beginning of each round Trader is shown an object

which contains a side information. Past prices of the stock

are also given for Trader (they can be considered

as a part of the side information). Using this information, Trader

announces a number of shares of the stock

he wants to purchase by

each. At the end of the round Stock Market announces

the price of the stock, and Trader receives his gain or

suffers loss for round . The total gain or loss

for the first rounds is equal to .

We show that, using the well-calibrated forecasts, it is possible

to construct a universal strategy for algorithmic trading in the stock market

which performs asymptotically at least as well as any stationary trading

strategy presented by a continuous function from the object .

This universal trading strategy is of decision type: we

buy or sell only one share of the stock at each round.

The learning process is the most traditional one. At each step,

Trader makes a randomized prediction of

a future price of the stock and takes “the best response” to this

prediction.

He chooses a strategy to going long:

if , or to going short: , otherwise,

where is the randomized past price of the stock.

Trader uses some randomized

algorithm for computing the well-calibrated forecasts .

Therefore, our universal strategy uses some internal randomization.

Trader M can buy or sell only one share of the stock.

Therefore, in order to compare the performance of the traders we

have to standardize the strategy of Trader D.

We use the norm and

a normalization factor ,

where is a continuous function.

Our main result,

Theorems 4 and 5 (Section 4), and

Theorem 7 (Section 5),

says that this trading strategy performs asymptotically

at least as well as any stationary trading strategy presented by a

continuous function .

With probability one, the gain of this trading strategy

is asymptotically not less than the average gain of any stationary

trading strategy from one share of the stock:

(2)

where is a side information used by the stationary

trading strategy at step .

Evidently, the requirement (2)

for all continuous is equivalent to

the requirement:

for all continuous such that .

To achieve this goal we extend in Theorem 1

(Section 3) Kakade and Foster’s forecasting algorithm

for a case of arbitrary real valued outcomes and to a more general notion of calibration

with changing parameterized checking rules. We combine

it with Vovk et al. (2005) defensive forecasting method in RKHS

(see Vovk 2005a).

In Section 5,

using a universal kernel, we generalize

this result to any continuous stationary trading strategy.

We show in Section 6 that the universality

property fails if we consider discontinuous trading strategies.

On the other hand, we show in Theorem 9 that a universal

trading strategy exists for a class of randomized discontinuous trading

strategies.

In Section 7 results of numerical experiments are

presented. Our empirical results on historical markets provide

strong evidence that this type of algorithmic trading can beat the

market : our universal strategy is always better than

“buy-and-hold” strategy for each stock chosen arbitrarily in

Stock Market. This strategy outperforms also an algorithmic trading

strategy using some standard prediction algorithm (ARMA).

Some parts of this work were presented in Vyugin (2013) and V yugin and Trunov (2013).

2 Preliminaries

By a kernel function on a set we mean any function

which can be represented as a dot product ,

where is a mapping from to some Hilbert feature space.

The reproducing kernels are of special interest.

A Hilbert space of real-valued functions on a compact

metric space is called RKHS (Reproducing Kernel Hilbert Space) on if

the evaluation functional is continuous for each .

Let be a norm in and

.

The embedding constant of is defined

.

We consider RKHS with

.

Let for .

An example of RKHS is the Sobolev space , which

consists of absolutely continuous functions

with , where

For this space, (see Vovk 2005a).

Let be an RKHS on with the dot product

for . By Riesz–Fisher theorem, for each

there exists such that .

The reproducing kernel is defined .

The main properties of the kernel: 1) for all

(symmetry property); 2)

for all , for all , and for all real numbers

, where (positive semidefinite property).

Conversely, a kernel defines RKHS: any symmetric, positive

semidefinite kernel function defines some canonical RKHS

and a mapping such that

. Also, . The mapping

is also called “feature map” (see Cristianini and Shawe-Taylor 2000, Chapter 3).

A function is induced by a kernel if

there exists an element such that

. This definition is independent of a map

. For any continuous kernel , every induced

function is continuous (see Steinwart (2001)).

111

It is Lipschitz continuous (with respect to some

semimetrics induced by the feature map

(Steinwart 2001, Lemma 3).

In what follows we consider continuous kernels.

Therefore, all functions from canonical RKHS are continuous.

Well known examples of kernels on : Gaussian kernel

,

where is the Euclidian norm; ,

where and .

Other examples and details of

the kernel theory see in Scholkopf and Smola (2002).

Some special kernel corresponds to the method of randomization

defined below.

A random variable is called randomization of a real number

if , where is the symbol of

mathematical expectation with respect to the corresponding to

probability distribution.

We use a specific method of randomization of real numbers from

unit interval proposed by Kakade and Foster (2004).

Given positive integer number divide the interval on

subintervals of length

with rational endpoints , where .

Let denotes the set of these points.

Any number can be represented as a linear

combination of two neighboring endpoints of defining

subinterval containing :

(3)

where , ,

, and

.

Define for all other .

Define a random variable

Let be a vector of probabilities of rounding.

For any -dimensional vector ,

we round each coordinate , to

with probability and to

with probability ,

where . Let be the corresponding

random vector.

Let and

. For any ,

let be a vector of

probability distribution in :

.

For , the dot product

is the symmetric positive semidefinite kernel function.

3 Well-calibrated forecasting with side information

A universal trading strategy, which will be defined in Section 4, is

based on the well-calibrated forecasts of stock prices.

In this section we present a randomized algorithm for computing

well-calibrated forecasts using a side information.

A standard way to present any forecasting process is the game-theoretic

protocol. The basic online

prediction protocol has two players Reality and Predictor

(see Fig 1).

Basic prediction protocol.FOR Reality announces a signal .

Predictor announces a forecast .

Reality announces an outcome .

ENDFOR

Figure 1: Basic prediction protocol

At the beginning of each step , Predictor is given some

data relevant to predicting the following outcome .

We call a signal or a side information.

Signals are taken from the object space.

The outcomes are taken from an outcome space and predictions

are taken from a prediction space.

In this paper an outcome is a real number from the unit interval and a

forecast is a single number from this interval (which can be

output of a random variable). We could interpret the forecast

as the mean value of a future outcome under some

unknown to us probability distribution in .

Reality is called oblivious if an infinite sequence

of outcomes and signals

is defined before the game starts and Reality

only reveals their next value at each step . In

this case the outcomes and signals do not depend on past predictions.

In case of non obliviousReality this sequence is not

fixed in advance and any next value can be output

of some measurable function from previous moves of Predictor, ie,

from past predictions .

In what follows we compare two types of forecasting algorithms:

randomized algorithms which we will construct and stationary

forecasting strategies which are continuous functions from

some RKHS using a side information as input.

We consider two type of predictors: and , playing according

to the basic prediction protocol presented at Fig 1.

This protocol is perfect-information

for Predictor C. This means that Predictor C can

use other players moves so far. Past outcomes

and predictions are also known to Reality in

the perfect-information protocol.

Predictor D can use only a signal that is given at

the beginning of any step .

Predictor D uses a stationary prediction strategy ,

where is a function whose input is the signal and

output is the number of shares. We suppose that

is a real number from the unit interval. The number

can encode any information.

For example, it can be past outcomes and signals and even the future

outcome .

Predictor C uses a randomized strategy which we will

define below.

We collect all information used for the internal

randomization in a vector . This vector can contain

any information known before the move of Predictor C at

step : the signal , past outcomes and so on.

For example, in Section 4, the information is one-dimensional

vector that is the past outcome,

in Section 6, is the pair

of the past outcome and the signal.

In general, we suppose that

is a vector of dimension : .

We call it an information vector and assume that some method

for computing information vectors given past outcomes and signals is fixed.

We use the tests of calibration to measure the discrepancy

between predictions and outcomes. These tests use

the checking rules. We consider checking rules of more general type

than that used in the literature on asymptotic calibration.

For any subset , define

the checking rule that is an indicator function:

where is an -dimensional vector.

In Section 3 we set and or

, where .

In Section 6,

and a set is defined in a more complex way.

In the online prediction protocol defined on Fig 1,

given , a sequence of forecasts is called

-calibrated for a sequences of outcomes

and information vectors if

for any subset the following asymptotic inequality

holds:

The sequence of forecasts is called well-calibrated if

(4)

If Reality is non oblivious and acts “adversatively”, then,

as shown by Oakes (1985) and Dawid (1985), any deterministic

forecasting algorithm will not always be calibrated. In case where ,

Reality can define their outcomes by the rule:

Then any sequence of forecasts will not be calibrated

for the sequence of such outcomes .

It is easy to verify that the condition (4) fails for

or for .

Following the method of Foster and Vohra (1998), at each step ,

using the past outcomes ,

we will define a deterministic forecast and randomize

it to a random variable using the method

of randomization defined in Section 2. We also randomize

the information vector to a random vector .

We call this sequential randomization.

This sequential randomization generates for any a probability distribution

on the set of all finite sequences

of forecasts and information vectors.

In case of oblivious Reality this is simply the product distribution

which in their turn generates the overall probability distribution

on the set of all infinite trajectories

.

In case of non oblivious Reality, at any step , a probability

distribution on exists such that the corresponding

method of randomization of

is defined as conditional distribution

on . The overall probability distribution on the set

of all infinite trajectories generating these

can be defined by Ionescu–Tulcea theorem (see Shiryaev (1980)).

The following theorem on calibration with a side information

is the main tool for an analysis

presented in Sections 4 and 6.

We will show that for any subset ,

with -probability 1, the equality (4) is valid,

where and are replaced on their

randomized variants and .

In the prediction protocol defined on

Fig 1, let be a sequence of outcomes and

be the corresponding sequences of signals

given online.

We assume that a sequence of the information vectors

also be defined online.

Let also, be an RKHS on with a kernel

and a finite embedding constant .

Theorem 1

For any , an algorithm for computing

forecasts and a sequential method of randomization

can be constructed such that the following three items hold:

•

For any , , and ,

with probability at least ,

(5)

where are the

corresponding randomizations of and

are the corresponding randomizations

of -dimensional information vectors ;

•

For any and ,

(6)

where are signals.

•

For any , with probability 1,

(7)

Proof.

At first, in Proposition 2 (below),

given , we modify a randomized rounding algorithm of

Kakade and Foster (2004) to construct some -calibrated

forecasting algorithm, and combine it with Vovk (2005a)

defensive forecasting algorithm. After that, we revise it

tending such that (5) will hold.

Proposition 2

Under the assumptions of Theorem 1,

an algorithm for computing forecasts and a method of randomization

can be constructed such that

the inequality (6) holds for all from RKHS

and for all . Also, for any , , and ,

with probability at least ,

Proof. We define a deterministic forecast and after that we randomize it.

The partition and probabilities of rounding

were defined above by (3).

In what follows we round some deterministic forecast to

with probability and to

with probability .

We also round each coordinate , , of the

information vector to

with probability and to

with probability ,

where .

Let ,

where and , ,

,

and be a vector of

probability distribution in . Define the corresponding kernel

.

Let the deterministic forecasts be already defined

(put ). We want to define a deterministic forecast .

The kernel can be represented

as a dot product in some feature space:

.

Consider

(8)

The following lemma presents a general method for computing the

deterministic forecasts.

Define and

for all .

Lemma 3

( Vovk et al. 2005)

A sequence of forecasts can be

computed such that for all .

Proof. By definition the function is

continuous in . The needed forecast is computed as follows.

If for all then

define ; if for all then

define . Otherwise, define to be a root of the equation

(some root exists by the intermediate value theorem).

Evidently, for all . Lemma is proved.

Now we continue the proof of the proposition.

Let forecasts be computed by the method of

Lemma 3. Then for any ,

(9)

(10)

(11)

In (10), is Euclidian norm, and in

(11), is the norm in RKHS .

Insert the term in the sum (14), where is

the characteristic function of an arbitrary set

,

sum by , and exchange the order of

summation. Using Cauchy–Schwarz inequality for vectors

, and

Euclidian norm, we obtain

(15)

for all , where is the cardinality of

the partition.

Let be a random variable taking values

with probabilities (only two of them are nonzero).

Recall that is a random variable taking

values with probabilities .

Let and be its indicator function.

For any , the mathematical expectation of a random variable

is equal to

(16)

where .

By Azuma–Hoeffding inequality (see (28) below), for any and

, with -probability ,

(17)

By definition of the deterministic forecast

for all , where .

Summing (16) over and using the inequality

(3), we obtain

To prove the bound (5) choose a monotonic sequence of

rational numbers

such that as .

We also define an increasing sequence of positive integer numbers

For any , we use for randomization on steps

the partition of on subintervals of length .

We start our sequences from and .

Also, define the numbers such that the inequality

(21)

holds for all and for all .

We define this sequence by mathematical induction on .

Suppose that () is defined such that the inequality

(22)

holds for all , and the inequality

(23)

also holds.

Let us define . Consider all forecasts

defined by the algorithm given above for the discretization

. We do not use first of these

forecasts (more correctly we will use them only in bounds

(24) and (25); denote these forecasts

). We add the forecasts

for to the forecasts defined before this

step of induction (for ). Let be such that the

inequality

(24)

holds. Here the first sum of the right-hand side of the

inequality (24) is bounded by

– by the induction hypothesis (23). The second and

third sums are bounded by and by

, respectively, where is defined

such that (20) holds. This follows from (18)

and by choice of .

for . Here the first sum of the right-hand

inequality (24) is also bounded by

– by the induction

hypothesis (23). The second and the third sums are

bounded by and by

, respectively. This follows

from (18) and from choice of . The

induction hypothesis (22) is valid.

We show now that sequences and satisfying

all the conditions above exist.

Let and , where

is the least integer number such that .

Define and

Easy to verify that all requirements for and

given above are satisfied for all , where is

sufficiently large. We redefine for all .

Then all these requirements hold for these trivially.

for all .

Azuma–Hoeffding inequality says that for any

(28)

for all , where are martingale–differences.

We set and

,

where . Denote .

Combining (27) with (28), we obtain that

for any and , with probability ,

The asymptotic relation (7) follows from (5)

by Borel–Cantelli lemma. The proof is similar to the final part of the proof

of Theorem 5 below.

Theorem 1 is proved.

4 Competing with stationary trading strategies from RKHS

A trading game has two players: Trader and Stock Market.

They correspond to Predictor and Reality in the simple

prediction game defined in Section 3.

We suppose that the prices of a stock are bounded and

rescaled such that for all . We set also .

These prices are analogs of outcomes of the prediction game.

We present the process of algorithmic trading in Stock Market in the form of

a trading game regulated by the perfect-information protocol

presented on Fig 2.

Basic trading protocol.FOR Stock Market announces a signal .

Trader bets by buying or selling a number of shares of

the stock by each.

Stock Market reveals a price of the stock.

Trader receives his total gain (or suffers loss)

at the end of step :

.

We set .

ENDFOR

Figure 2: Basic trading protocol

At the beginning of each step Trader is given an object

which was called a side information at step .

Without loss of generality suppose that .

We call any sequence , , of random variables

a randomized trading strategy.

In case Trader playing for a rise, in case

Trader playing for a fall, Trader passes the step

if .

We suppose that Trader buys shares (if ) or sells

shares (if ) at the beginning of any round and

sells or buys them at the end this round correspondingly.

Thus, Trader receives the gain or suffers the loss in the amount

of money units.

We suppose also that Trader can borrow money for buying shares

and can incur debt.

A stationary trading strategy is a function from to .

We suppose that some RKHS on

with a kernel and with a finite embedding constant

be given.

Any stationary trading strategy uses at step a side information

that is a real number .

Our universal trading strategy will be randomized.

The universal trading strategy, which we define

below, uses the past price of the stock as one-dimensional

information vector in sense of Theorem 1, where .

This information is used for the internal randomization.

We define a universal trading strategy as a sequence of random variables

and show that

this trading strategy performs almost surely at least as well as any

stationary trading strategy using arbitrary side

information .

To be more concise, define on Fig 3 the perfect-information

protocol of the game with two traders:

Trader M uses the randomized strategy ,

Trader D uses an arbitrary stationary trading strategy .

Trading protocol with two traders.FOR Stock Market announces a signal .

Trader M bets by buying or selling the random number of shares of

the stock by each.

Trader D bets by buying or selling a number of shares of

the stock by each.

Stock Market reveals a price of the stock.

Trader M receives his total gain (or suffers loss)

at the end of step :

.

We set .

Trader D receives his total gain (or suffers loss)

at the end of step :

.

We set .

ENDFOR

Figure 3: Trading protocol with two traders

This protocol is more general than two basic trading protocols

(Fig 2) together, since Stock Market

can use information on the decisions of both traders and

before revealing a future price .

Past prices, signals and predictions are also known to Trader M in

the perfect-information protocol. Trader D can use only

side information. For example, at any step ,

past prices and predictions can be encoded in the signal

and used by Trader D.

At first, for simplicity, we consider a case of going long,

since the proof of optimality (Theorem 4) is much more clear

in this case than that in general case (Theorem 5).

Also, a series of numerical experiments presented in Section 7,

are performed for the case where both traders going long.

The case of going short is considered similarly.

At each step

we will compute a forecast of a future price and randomize it to

. We also randomize the past price of the stock

to . Details of this computation and randomization

are given in Section 3. Our universal strategy is a randomized

decision rule – it takes only two values:

Assume that prices and signals

be given online according to the protocol presented on Fig 3.

Denote .

Since Trader M can buy or sell only one share of the stock,

we have to standardize the strategy of Trader D.

We will use the norm

and

the normalization factor

where is a nonnegative continuous function.

Informally, Theorem 4 says that if the forecasts

are well-calibrated for the sequence of prices , , then

Trader M, using the strategy , performs

at least as well as any trader who going long using

a stationary trading strategy .

Theorem 4

An algorithm for computing forecasts and a sequential

method of randomization can be constructed such that for any

nonnegative stationary trading strategy

(29)

holds almost surely with respect to a probability distribution

generated by the corresponding sequential randomization.

Moreover, for any this trading strategy

can be tuned such that

for any and , with probability at least , for

all nonnegative ,

(30)

Proof. We use the randomized trading strategy

based on the well-calibrated forecasts defined in Section 3,

where and .

Recall

that at any step we compute the deterministic forecast

defined in Section 3 and its randomization to

using parameters and ,

where . Let also, be a

randomization of the past price . The following upper

bound directly follows from the method of discretization:

(31)

Let be an arbitrary nonnegative trading strategy

from RKHS .

Clearly, the bound (31) holds if we replace

on .

Let be the randomized trading strategy

defined above. We use abbreviations:

(32)

(33)

(34)

All sums below are for . By definition

for all .

Let and be given.

Then, with probability , for any ,

the following chain of equalities and inequalities is valid:

(35)

(36)

(37)

(38)

(39)

(40)

(41)

In transition from (35) to (36) the inequality

(5) of Theorem 1 and the bound

(31) were used,

and so, the terms (32) and (33)

were subtracted. The transition from (36) to (37)

is valid since for all .

In transition from (38) to (39)

the bound (31)

was applied twice to intermediate terms, and so,

the term (31)

was subtracted twice. In transition from (39)

to (40) the inequality (6) of Theorem 1

was used, and so, the term (34) was subtracted.

In transition from (40) to (41) we have used

the inequality (6) of Theorem 1.

Therefore, we have (30).

The inequality (29) follows from (30)

by Borel–Cantelli lemma (see the final part of the proof

of Theorem 5 below). Theorem 4 is proved.

Now, we consider the general case of going long and going short.

The corresponding universal trading strategy is defined:

Trader is also can going long and short.

Let and

be given online according to the protocol presented on Fig 3.

Informally, Theorem 5 says that if the forecasts

are well-calibrated for the sequence of prices , , then

Trader M, using the strategy , performs

at least as well as any trader who going long or short using

a stationary trading strategy .

Theorem 5

An algorithm for computing forecasts and a sequential method of

randomization can be constructed such that for any

stationary trading strategy ,

(42)

holds almost surely with respect to a probability distribution

generated by the corresponding sequential randomization.

Moreover, for any this trading strategy

can be tuned such that for any and ,

with probability at least , for all ,

(43)

Proof. We use abbreviations (32)–(34)

from the proof of Theorem 4. Define

and

By definition .

The proof of Theorem 5 is based on transformations

similar to (35)–(41).

Let and be given.

Then, with probability , for any ,

(44)

(45)

(46)

(47)

The proof of these transitions is similar

to the proof of transitions in (35)–(41) of

Theorem 4.

To prove (42) we turn to Azuma–Hoeffding

inequality (28).

Denote .

Then . Rewrite (43) in the form:

(48)

where is a positive constant.

By (30), for any and ,

the inequality (48) fails with probability .

Since given the series

converges, by Borel–Cantelli lemma, for any

the inequality (48) can be violated

not more than for a finite number of different . Hence, the event

(42) holds almost surely.

This completes the proof of Theorem 5.

Theorem 5 can be rewritten for

the strategy and for the class of

stationary strategies with bounded norm

, where is an arbitrary positive integer

number.

We present the following evident corollary for .

Corollary 6

Given a positive integer number , for any

stationary trading strategy such that

,

holds almost surely.

For any , this trading strategy

can be tuned such that for any and ,

with probability at least , for

all nonnegative such that ,

5 Universal consistency

Using a universal kernel and the corresponding canonical universal RKHS,

we can extend our asymptotic results for all continuous

stationary trading strategies.

An RKHS on is universal if is a compact metric space

and every continuous function on can be arbitrarily well approximated

in the metric by a function from :

for any there exists such that

We use . The Sobolev space defined in

Section 2 is the universal RKHS

(see Steinwart 2001, Vovk 2005a).

We call a randomized trading strategy universally consistent

if for any continuous function with probability one

(49)

This definition is similar to Vovk (2005a) definition of

a universally consistent prediction strategy.

The existence of the universal RKHS on implies the following

Theorem 7

An algorithm for computing forecasts and a sequential method of

randomization can be constructed which performs at least as well as any

continuous trading strategy :

(50)

holds almost surely with respect to a probability distribution

generated by the corresponding sequential randomization.

This result directly follows from the possibility to approximate

arbitrarily close any continuous function on by a function

from the universal RKHS :

for any continuous function and for any

take a such that

. Then

The property of universal consistency is

asymptotic and does not tell

us anything about finite data sequences: we cannot obtain the

convergence bounds like (30) and (43)

which holds for stationary strategies from RKHS.

6 Competing with discontinuous trading strategies

The trading strategy defined in Section 4

performs at least as well as any stationary trading strategy

(up to some regret) even if the future price of the stock is known to

as a side information contained in .

Theorems 4 and 5 are also valid in

this case.

This impressive efficiency of the trading strategy can be explained

by the restrictive power of continuous functions.

A weak point of Trader D is that a set of his strategies is limited by .

A continuous stationary trading strategy cannot respond sufficiently

quickly to information about changes of the value of a future price .

the optimal trading strategy ,

is a discontinuous function, though it is applied to the random variables.

A positive argument in favor of the requirement of continuity of is that

it is natural to compete only with computable trading strategies,

and continuity is often regarded as a necessary condition for computability

(Brouwer’s “continuity principle”).

If is allowed to be discontinuous, we cannot prove (29)

and (42) in general case. We demonstrate the weakness

of discontinuous in Theorem 8 below.

Let an arbitrary randomizing trading strategy be given

that is a sequence of random variables , .

We suppose that they are independent like random variables that form

the universal trading strategy defined in Section 4.

A stationary trading strategy is called decision rule

if its range is finite. Decision rule is binary if it takes only two

values.

Consider the protocol of trading game presented on Fig 3

with two players and with signals that are probabilities:

for .

Define a sequence of stock prices: and for

By definition for all .

Define the binary decision rule :

where .

Theorem 8

Let an arbitrary randomizing trading strategy such that

for all .

Then, with probability one,

(52)

where .

Inequality (52) means that trading strategy outperforms

twice.

Proof. We bound the conditional mathematical expectation of the random

variable :

Theorem 8 is valid in a more general setting where

random variable , are be dependent. In this

case we have to use signals that

are random variables representing conditional probabilities:

.

The proof of Theorem 8 is almost the same

but we have to consider conditional mathematical expectation

in (53) and in what follows.

222

In general case the law of large numbers (57)

is a corollary of Azuma–Hoeffding inequality be

applied for martingale-differences (see Cesa-Bianchi and Lugosi (2006)).

The discontinuous trading strategy defined in Theorem 8

is unstable under small changes of the signal .

In the next theorem, we show that if we randomly round the

signal then our universal trading strategy

(and ), performs at least as well as .

Consider the protocol of trading game with two players

and a side information (see Fig 3).

We specify the information vector using by our universal strategy

to be ,

where is the past price of the stock

and is the signal at step . The universal trading strategy

uses the sequential method of randomization defined in

Section 2 to perform a randomized forecast and

a randomized information vector

.

The strategy of Trader M is the same as before:

except that it uses a slightly different randomization.

Theorem 9

An algorithm for computing forecasts and a sequential

method of randomization

can be constructed such that for any decision rule

(58)

holds almost surely with respect to a probability distribution

generated by the corresponding sequential randomization.

Moreover, for any this trading strategy

can be tuned such that for any and ,

with probability at least , for

all nonnegative decision rule ,

(59)

where is the cardinality of the range of .

Proof. For simplicity, we give the proof for the case of nonnegative

decision rule and the randomized strategy .

The case of arbitrary decision rule and strategy

is considered similarly.

We apply Theorem 1 to zero kernel

with and to the information vector

, .

Recall that and .

At any step we compute the deterministic forecast defined

in Theorem 1 (Section 3) and its randomization

to

using parameters

and , where .

The following upper bound is valid:

(60)

where .

Let be an arbitrary nonnegative decision rule.

Let be the randomized trading strategy

defined in Section 4.

We use abbreviations:

(61)

(62)

All sums below are for . By definition

for all .

Let be all values of .

Define

where . Let be the characteristic

function of the set .

Let and be given. Then, with probability ,

the following chain of equalities and inequalities is valid:

(63)

(64)

(65)

(66)

(67)

In change from (63) to (64) and in change

from (66) to (67) we have used

the inequality (60). In change

from (66) to (67) we have used also

Theorem 1, where , and, with probability ,

The inequality (58) follows from (59).

Theorem 9 is proved.

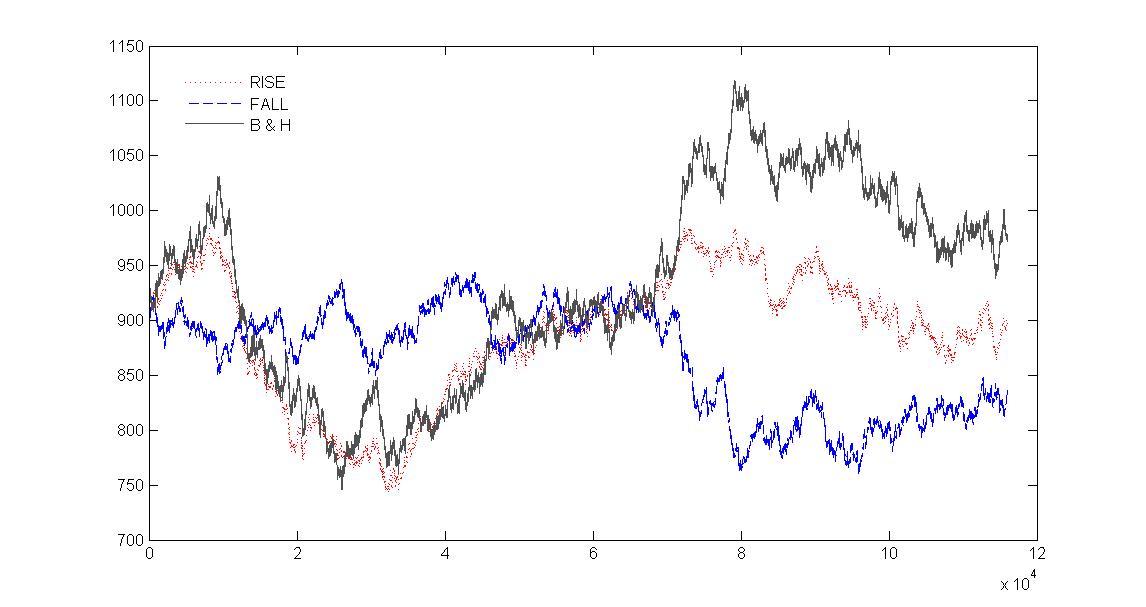

Figure 4: Evolution of capitals of three trading strategies

for the period 26.03.10–25.03.11:

Buy and Hold – solid line, UN going long – dotted line,

UN going short – dashed line.

One run of trading is performed with a simulated stock TEST

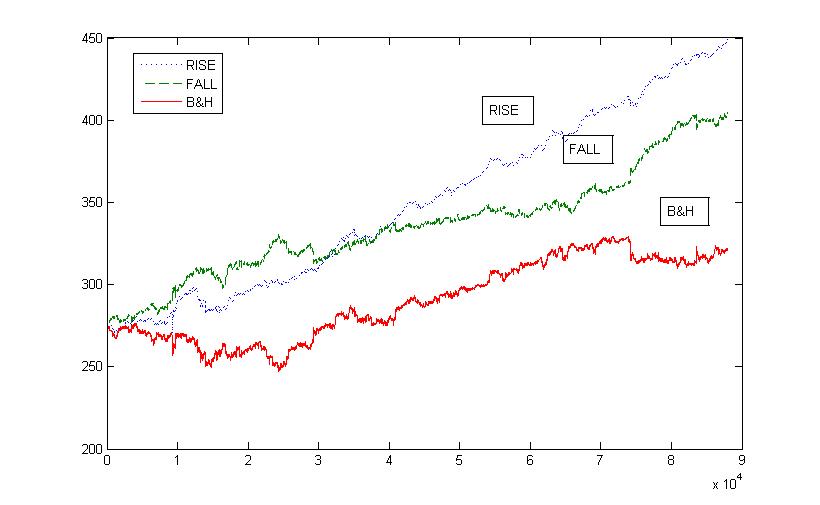

(see Table 1)Figure 5: Evolution of capitals of three trading strategies

for the period 26.03.10–25.03.11:

Buy and Hold – solid line, UN going long – dotted line,

UN going short – dashed line.

One run of trading is performed with the stock KOCO

(see also Table 1)

7 Numerical experiments

Computer technology.

In the numerical experiments, we have used historical data in the

form of per minute time series of prices of arbitrarily chosen stocks.

Two types of kernel functions

were used as the smooth approximations of the

combined kernel

from

the sum (8): (i) ,

(ii) ,

where are positive constants.

In any short-term trading algorithm, the time characteristics are crucial.

The greatest time cost is associated with the calculation

of sums (8) and finding the roots of this equation.

The performed experiments show that the computation time for one point of

the forecast increases linearly with increasing length of

history.

To provide one point of time, predicting within 1 - 3 seconds

of CPU time, the length of the series was limited

up to 5000 points. For series of length greater than 5000 points,

“a chain” method of forecasting was used.

Two processes working on overlapping intervals of time series

are performed at the same time (see Fig 6).

Let be the chain length,

and be the value of time shift, where

. In any process, the first

time-points are used only for scaling prices

and preliminary learning of the forecasting algorithm.

The trading is not performed

at first time-points of the series.

When a regular process terminates we switch to the time-point

of the next process.

The results of parallel computing are accumulated into a single overall

forecasting series. We take and .

Figure 6: Scheme of parallel computations

The prices of a stock are scaled such that for all .

The scaling is performed for time series of each process separately. The first

time points of any process are used for computing

a scaling constant. Prices are scaled as follows:

where and are real prices of the stock.

We set .

The forecasting algorithm is performed for the scaled prices ,

where .

We implement this computer technology for two forecasting algorithms:

the universal strategy constructed in Section 3 (UN–model)

and Autoregressive Moving Average algorithm

(ARMA–model) (see Peng and Aston 2011).

333

See also the State Space Models Toolbox for

MATLAB:

http://sourceforge.net/projects/ssmodels/.

Table 1: Universal trading

Buy&

UN

UN

ARMA

ARMA

Ticker

Hold

going long

going short

going long

going short

Profit %

Profit %

Profit %

Profit %

Profit %

TEST

6.85

-1.39

-8.19

9.88

3.08

AT-T

7.71

137.40

129.70

30.73

23.02

CTGR

15.04

1594.34

1579.34

1167.22

1152.53

KOCO

16.55

62.66

46.15

2.90

-13.61

GOOG

10.25

114.85

104.62

12.85

2.62

InBM

24.28

85.38

61.09

29.31

5.02

INTL

4.29

111.70

107.50

25.86

21.66

MSD

10.71

58.32

47.60

18.66

7.95

US1.AMT

22.01

22.74

0.77

28.46

6.49

US1.IP

2.40

19.83

17.47

9.36

7.00

US2.BRCM

25.30

53.62

28.28

20.06

-5.27

US2.FSLR

40.15

143.92

103.61

-9.86

-50.16

SIBN

-6.54

732.87

739.33

357.74

364.20

GAZP

22.75

101.20

78.45

31.75

9.00

LKOH

19.39

261.84

242.45

87.08

67.68

MTSI

-1.61

669.16

670.68

326.12

327.64

ROSN

9.69

188.89

179.12

34.40

24.63

SBER

14.21

108.97

94.90

37.53

23.46

Results of numerical experiments.

In the numerical experiments, we have used historical data in

form of per minute time series of prices of arbitrarily chosen

17 stocks (11 US stocks, and 6 Russian stocks) and of one simulated stock

TEST. Data has been downloaded from FINAM site: www.finam.ru.

Number of trading points in each game is N=88000–116000 min.

(From March 26 2010 to March 25 2011).

The artificial stock TEST is simulated as , ,

where is the Gaussian random variable with mean 0 and a

variance equal to the variance of the scaled GAZP stock.

We implement the trading strategy defined in Section 4.

Two series of numerical experiments were performed.

In the first series, we use the trading strategy studied in

Theorem 5. At each step, starting from initial capital

,

where is the price of a stock at the first

time point, this strategy performs going long or for going short with

shares of the stock. We take in our experiments.

In case of going long, the capital changes at any step as

if

and otherwise.

In case of dealing for a fall

if and

otherwise, where .

Results of numerical experiments

are shown in Table 1. In the first column,

stocks ticker symbols are shown. The second column contains the

profit of Buy-and-Hold trading strategy. By this strategy, we buy a

holding of shares using capital and sell them for

at the end of the trading period.

Table 2: Defensive trading

Buy&

UN

UN

ARMA

ARMA

UN

ARMA

UN

ARMA

Ticker

hold

Profit

Profit

Profit

Profit

%

%

-0.01%

%

-0.01%

In

In

D

D

TEST

6.85

3.58

-80.93

3.58

-80.90

0.232

0.163

1.453

1.890

AT-T

7.71

69.01

-79.19

29.86

-79.19

0.218

0.205

1.611

1.576

CTGR

15.04

1030.12

658.13

937.46

540.18

0.238

0.253

1.654

1.479

KOCO

16.55

36.47

-78.62

15.69

-78.55

0.216

0.198

1.604

1.502

GOOG

10.25

46.54

-80.57

3.53

-82.68

0.231

0.211

1.462

1.474

InBM

24.28

54.79

-78.53

34.66

-78.10

0.219

0.187

1.514

1.517

INTL

4.29

43.06

-76.60

5.63

-76.28

0.220

0.179

1.630

1.585

MCD

10.71

34.22

-78.56

19.21

-78.41

0.222

0.190

1.571

1.876

AMT

22.01

16.47

-77.01

24.04

-77.09

0.212

0.183

1.654

1.758

IP

2.40

4.45

-82.78

-14.79

-81.06

0.213

0.181

1.657

1.760

BRCM

25.30

11.40

-80.47

23.98

-76.10

0.216

0.172

1.585

1.876

FLSR

40.15

21.02

-80.04

-27.50

-80.03

0.227

0.196

1.499

1.506

SIBN

-6.54

600.62

249.87

287.48

-58.55

0.169

0.179

2.460

2.292

GAZP

22.75

51.29

-82.04

4.34

-82.16

0.224

0.210

1.539

1.526

LKOH

19.39

149.03

-79.91

46.44

-80.62

0.230

0.244

1.527

1.501

MTSI

-1.61

482.83

79.23

275.13

-69.36

0.188

0.195

2.174

1.959

ROSN

9.69

101.15

-83.14

-0.53

-83.54

0.228

0.240

1.549

1.499

SBER

14.21

51.56

-82.52

-14.47

-82.73

0.225

0.196

1.559

1.674

In the 3th and 4th columns, results of one run of trading based on

the universal randomized

forecasting strategy (UN) are shown. In the 3th column,

a relative return, percentagewise, to the initial capital

is shown for going long,

in the 4th column, the same relative return

is shown for going short,

In the 5th and 6th columns, the same results are shown for

trading using ARMA forecasts.

It was found that for , i.e.,

we never incur debt in our experiments (with an exception of TEST stock).

Results presented in Table 2 show that trading based on UN model of

forecasting performs at least as well as the trading based on ARMA forecasting model and

essentially outperforms it for some stocks.

The second series of experiments is closer to a real short-term trading.

The trading strategy has a defence guarantee. Starting with the same initial

capital , where is the initial price of a stock

and , we perform going long using “a defensive” trading strategy.

At any step , our working capital is

. Using this capital,

we buy shares of the stock at the

beginning of any step , if , and stop trading otherwise:

. We update the cumulative

capital at the end of each step: .

Thereby, we can set aside the extra income.

Results of second series of numerical experiments are shown in

Table 2. In the first column, stocks ticker symbols

are shown. The second column contains the relative return of

Buy-and-Hold trading strategy.

In the next pair of columns marked “UN”, relative returns

of one run of randomized trading, percentagewise,

for the initial capital are presented

for the case with no transaction costs and for the case where

transaction cost at the rate is subtracted.

We compute the forecast of a future stock price

by the method of calibration and defensive forecasting (UN)

presented in Theorem 1.

The next two columns marked by “ARMA” are similar,

with the exception that the ARMA forecasting model is used for

computing forecasts. The frequencies of market entry steps

, where ,

are given in the next two columns marked “In” (for UN and ARMA).

We sell all shares of a stock at step in case

.

The average time spent in the market is shown in the rest two columns

marked “D” (for UN and ARMA).

8 Acknowledgement

This research was partially supported by Russian foundation

for fundamental research: Grant 13-01-12447 and 13-01-0052.

9 Conclusion

Asymptotic calibration is an area of intensive research where several

algorithms for computing well-calibrated forecasts have been

developed. Several applications of well-calibrated forecasting

have been proposed (convergence to correlated equilibrium,

recovering unknown functional dependencies, predictions with expert

advice). We present a new application of the calibration

method.

We show that the universal trading strategy can be

constructed using the well-calibrated forecasts. We prove that this

strategy performs at least as well as any stationary trading strategy

presented by a rule from any RKHS with regret .

Using the universal kernel, we prove that this strategy performs at

least as good as any stationary continuous trading strategy.

The obvious drawback of a universal

strategy is that it uses the high frequency trading,

which prevents it from practical applications in the presence of

transaction costs.

To construct the universal trading strategy, we

generalize Kakade and Foster’s algorithm and combine it with

Vovk’s DF–model for arbitrary RKHS. Using Vovk (2006) theory of

defensive forecasting in Banach

spaces, these results can be generalized to these spaces.

Unlike in statistical theory, no stochastic assumptions are made about

the stock prices.

Numerical experiments show a positive return for all chosen

stocks, and for some of them we receive a positive return even when

transaction costs are subtracted. Results of this type can be

useful for technical analysis in finance.

References

Blackwell (1956)

D. Blackwell. An analog of the minimax theorem for vector payoffs.

Pacific Journal of Mathematics, 6, 1956, 1–8

Chernov et al. (2010)

A. Chernov, Y. Kalnishkan, F. Zhdanov, V. Vovk.

Supermartingales in Prediction with Expert Advice.

Lecture Notes in Computer Science, 5254, 2008, 199–213

Cesa-Bianchi and Lugosi (2006)

N. Cesa-Bianchi, G. Lugosi.

Prediction, Learning and Games. Cambridge University Press, 2006

Cover and Gluss (1986)

T. Cover, D. Gluss. Empirical Bayes stock market portfolios.

Advances in Applied Mathematics, 1986, 7, 170 -181.

Cover and Ordentlich (1996)

T. Cover, E. Ordentlich. Universal portfolio with side information.

IEEE Transaction on Information Theory, 42. 1996, 348–363

Cristianini and Shawe-Taylor (2000)

N. Cristianini, J. Shawe-Taylor. An Introduction to Support Vector

Machines and other kernel-based learning methods.

Cambridge University Press, Cambridge, 2000.

Dawid (1982)

A.P. Dawid. The well-calibrated Bayesian [with discussion].

J. Am. Statist. Assoc. 77, 1982, 605–613

Dawid (1985)

A.P. Dawid.

Calibration-based empirical probability [with discussion].

Ann. Statist., 13, 1985, 1251–1285

Foster and Vohra (1998)

D.P. Foster, R. Vohra. Asymptotic calibration. Biometrika, 85, 1998, 379–390

Peng and Aston (2011)

Jyh-Ying Peng J.A.D. Aston.

The State Space Models Toolbox for MATLAB.

Journal of Statistical Software, 41, Issue 6, 2011

Kakade and Foster (2004)

S.M. Kakade, D.P. Foster.

Deterministic calibration and Nash equilibrium.

Journal of Computer and System Sciences, 74(1), 2008, 115–130.

Oakes (1985)

D. Oakes. Self-Calibrating Priors Do not Exist

[with discussion]. J. Am. Statist. Assoc. 80, 1985, 339–342

Scholkopf and Smola (2002)

B. Scholkopf, A. Smola. Learning with Kernels. MIT

Press, Cambridge, MA, 2002

Steinwart (2001)

I. Steinwart. On the influence of the kernel on the consistency of support

vector machines. Journal of Machine Learning Research, 2, 67 93, 2001

Vovk (1997)

V. Vovk. A game of prediction with expert advice.

Journal of Computer and System Sciences, 56, Issue 2, 1998, 153–173

Vovk et al. (2005)

V. Vovk, A. Takemura, G. Shafer.

Defensive forecasting. Proceedings of the 10th International Workshop

on Artificial Intelligence and Statistics (ed. by R. G. Cowell and

Z. Ghahramani) – Cambridge UK: Society for Artificial Intelligence

and Statistics, 2005, 365–372

Vovk (2005a)

V. Vovk. On-line regression competitive with reproducing

kernel Hilbert spaces (extended abstract). TAMS

Lecture Notes in Computer

Science – Berlin: Springer, 3959, 2006, 452–463

Vovk (2006)

V. Vovk. Competing with wild prediction rules.

Machine Learning, 69, Issue 2-3, 2007, 193–212

Vovk (2006a)

V. Vovk. Predictions as statements and decisions.

Theoretical Computer Science, 405, Issue 3, 2008, 285–296

Vovk (2007)

V. Vovk. Defensive Forecasting for Optimal Prediction with Expert Advice.

arXiv:0708.1503v1 2007

V yugin and Trunov (2013)

V. V yugin, V. Trunov. Universal algorithmic trading.

Journal of Investment Strategies Volume 2/Number 1, Winter 2012/13, 63 88.

Vyugin (2013)

V. Vyugin. Universal Algorithm for Trading in Stock Market Based

on the Method of Calibration. Lecture Notes in Artificial Intelligence

(LNAI). 8139, 2013, 53–67