The AEP algorithm for the fast computation of the distribution of the sum of dependent random variables

Abstract

We propose a new algorithm to compute numerically the distribution function of the sum of dependent, non-negative random variables with given joint distribution.

doi:

10.3150/10-BEJ284keywords:

, and

1 Motivations and preliminaries

In probability theory, the exact calculation of the distribution function of the sum of dependent random variables is a rather onerous task. Even assuming the knowledge of the joint distribution of the vector , one often has to rely on tools like Monte Carlo and quasi-Monte Carlo methods. All of these techniques warrant considerable expertise and, more importantly, need to be tailored to the specific problem under consideration. In this paper, we introduce a numerical procedure, called the AEP algorithm (from the names of the authors), which accurately calculates

| (1) |

at a fixed real threshold and only uses the joint distribution without the need for any specific adaptation.

Problems like the computation of (1) arise especially in insurance or finance when one has to calculate an overall capital charge in order to offset the risk position deriving from a portfolio of random losses with known joint distribution . The minimum capital requirement associated to is typically calculated as the value-at-risk (i.e., quantile) for the distribution of at some high level of probability. Therefore, the calculation of a VaR-based capital requirement is equivalent to the computation of the distribution of (see (1)). For an internationally active bank, this latter task is required, for example, under the terms of the New Basel Capital Accord (Basel II); see (BASEL2d, ).

An area of application in quantitative risk management where our algorithm may be particularly useful is stress-testing. In this context, one often has information on the marginal distributions of the underlying risks, but wants to stress-test the interdependence between these risks; a concept that enters here is that of the copula. Especially in the context of the current (credit) crisis, flexibility of the copula used when linking marginal distributions to a joint distribution has no doubt gained importance; see, for instance, (pE09b, ).

Although the examples treated in this paper are mainly illustrative, the dimension (5), the marginal assumptions and the dependence structure (Clayton and Gumbel copula) used are typical for risk management applications in insurance and finance. For more information on this type of question, see, for instance, (SCOR08, ; ADO07, ; BDI08, ).

In the following, we will denote (row) vectors in boldface, for example, , . represents the th vector of the canonical basis of and . Given a vector and a real number , denotes the hypercube defined as

| (2) |

For notational purposes, we set . On some probability space , let the random variables have joint -variate distribution ; induces the probability measure on via

We denote by all the vectors in , that is, , , and so on, , where . By , we denote the number of ’s in the vector , for example, . The -measure of a hypercube , , can also be expressed as

| (3) |

The case is analogous. If necessary, (3) can also be expressed in terms of the survival function . Moreover, denotes the -dimensional simplex defined as

| (4) |

Again, . Finally, we denote by the Lebesgue measure on . For instance, the Lebesgue measure of the simplex is given by

| (5) |

2 Description of the AEP algorithm for

Throughout the paper, we assume the random variables to be non-negative, that is, . The extension to random variables bounded from below is straightforward and will be illustrated below. We assume that we know the joint distribution of the vector and define . Our aim is then to numerically calculate

for a fixed positive threshold .

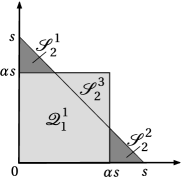

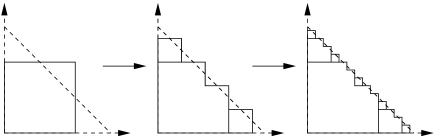

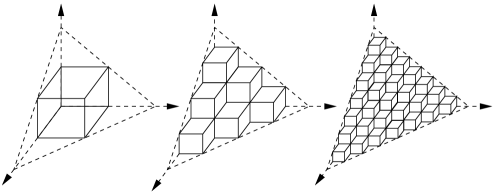

Due to (3), it is very easy to compute the -measure of hypercubes in . The idea behind the AEP algorithm is then to approximate the simplex by hypercubes. Before proceeding to the general case, we first illustrate our method for dimension .

As illustrated in Figure 1, the -measure of the simplex can be proxied by the -measure of the hypercube with . The error committed by using this approximation can be expressed in terms of the measure of the three simplexes

Formally, we have

| (6) |

Since , the sets and are pairwise disjoint. Also, note that . The -measure of can thus be written as

With the notation and , we translate the equation above into

| (7) |

Using (3), a first approximation of is given by the value

Using (7), the error committed by considering instead of can be expressed in terms of the -measure of the three simplexes defined above, that is,

| (8) |

At this point, we can apply to each of the ’s a decomposition analogous to the one given in (7) for , in order to obtain a better approximation of their measures and hence of the measure of . The only difference between the first and the following step is that we have to keep track of whether the measure of a simplex has to be added to or subtracted from the next approximation, , of . The value , associated to each simplex , indicates whether the corresponding measure is to be added () or subtracted (). The next approximation, , will be defined such that the difference is the sum of the -measures of a total of nine simplexes produced by the decompositions of the three ’s. The nine simplexes are then passed as input to the third iteration and so on.

Before formally defining the algorithm in arbitrary dimension , it is important to make the following points.

-

•

We will prove that the set decomposition (6) holds analogously in arbitrary dimension for every choice of . Unfortunately, the simplexes generated at the th iteration of the algorithm are, in general, not disjoint for . This will imply a more complicated formula for the general -measure decomposition.

- •

3 Description of the AEP algorithm for arbitrary

Recall that in Section 1, we denoted by all of the vectors in , where . Also, let . At the beginning of the th iteration (), the algorithm receives as input simplexes which we denote by for . To each simplex, we associate the value , which indicates whether the measure of the simplex has to be added () or subtracted () in order to compute an approximation of .

Each simplex is then decomposed via one hypercube and simplexes . In Appendix Appendix: Proof of (9), we prove the rather technical result that the -measure of each simplex can be calculated as

| (9) |

where the sequences and are defined by their initial values and

for all and . At this point, we note that by changing the value , one can apply the algorithm to the case in which the random vector also assumes negative values, but is still bounded from below by .

We define the sequence as the sum of the -measures of the , multiplied by the corresponding ,

| (11) |

where and the are defined by and

| (12) |

We will show that, under weak assumptions on , the sequence converges to . Moreover, from (3), can be calculated in a straightforward way. The simplexes generated by (9) are then passed to the th iteration in order to approximate their -measures with the measures of the hypercubes .

As a first step to show that tends to , we calculate the error by using instead of .

Theorem 3.1

With the notation introduced above, we have that

| (13) |

Proof.

We are now ready to give a sufficient condition for the convergence of the sequence to . The idea of the proof is that if the total Lebesgue measure of the new simplexes generated by the simplex , is smaller than the Lebesgue measure of itself, then, by assuming continuity of , the error (13) will go to zero. Let us define to be the sum of the Lebesgue measure of the simplexes passed to iteration . We define the volume factor to be the ratio between the sum of the Lebesgue measure of the simplexes in two subsequent iterations, that is, . Recalling the formula (5) for the -measure of a simplex, we have that

Observing that the simplexes , , are generated by the simplex , we use the above equation to conclude that

A sufficient condition for the convergence of the AEP algorithm can then be expressed in terms of the volume factor . We first assume to be absolutely continuous with a bounded density.

Theorem 3.2

Assume that has a bounded density . If the volume factor satisfies then

| (14) |

Proof.

Since has a density bounded by a constant , using (13), we have that

We conclude by noting that since and by assumption, goes to zero exponentially in . ∎

In order for (14) to hold, it is sufficient that is bounded on for large enough. Define the curve as

| (15) |

The following theorem states that the -distance from the curve to each point in is bounded by a factor , where . When , we have and that this distance goes to zero as . For Theorem 3.2 to hold when , it is then sufficient to require that has a bounded density only in a neighborhood of . We will discuss this assumption further in Section 8.

Theorem 3.3

If , then its -distance from the curve is bounded by , with .

Proof.

We denote by (resp., ) for the components of the vectors (resp., ). We prove by induction on that

| (16) |

For , the statement is true since there is only one simplex with and . Now, assume the statement holds for . By (3), we have that, for all and ,

where the last equality is the induction assumption. Due to (16), every simplex generated by the AEP algorithm has its diagonal face lying on the curve . As a consequence, the -distance from of each point in is strictly smaller than the distance of the vector , which is . For a fixed and , we have that for all . Hence,

| (17) |

where, for every , equality holds since we have for or . ∎

4 Choice of

As already remarked, the AEP algorithm depends on the choice of the parameter . It is important to note that, in general, an optimal choice of would depend on the measure . In the proof of Theorem 3.2, we have shown that

where is a positive constant. Since we want to keep our algorithm independent of the choice of the distribution , we suggest using the which minimizes , that is,

For dimensions , some values of and the corresponding optimal volume factors are given in Table 1.

=8cm 1 1

We will show that using has several desirable consequences. First, when and the dimension is odd, in the measure decomposition (9), a number of simplexes have the corresponding coefficient equal to zero and can therefore be neglected, increasing the computational efficiency of the algorithm. For example, in the decomposition of a three-dimensional simplex, the algorithm generates only new simplexes at every iteration with , instead of the generated with any other feasible value of . Hence, for , the number of new simplexes generated at each step is given by the function

| (18) |

see Section 5 for further details on this.

Since we have that (proof of Theorem 3.3)

| (19) |

the choice of will be convenient. Note that, when , we have that and goes to zero as . In order to guarantee the convergence of the sequence , it is then sufficient to require that the distribution has a bounded density only in a neighborhood of . Moreover, it is straightforward to see that also minimizes .

As illustrated in Table 1, Theorem 3.2 states the convergence of the sequence when . Various elements affect the speed at which converges. First, in order to seriously affect the convergence rate of , it is, in general, always possible to put probability mass in a smooth way in a neighborhood of the curve . For the distributions of financial and actuarial interest used in Section 6, the algorithm performs very well; slow convergence is typically restricted to more pathological cases, such as those illustrated in Section 8. We also have to consider that, for the same distribution , it is, in general, required to compute the distribution of at different thresholds . Problems such as those described in Section 8 may then occur only at a few points .

A more relevant issue is the fact that the memory required by the algorithm to run the th iteration increases exponentially in . At each iteration of the algorithm, every simplex produces one hypercube and a number of new simplexes to be passed to the following iteration; see (18). The computational effort in the th step thus increases as . While the dimensions are manageable, as reported in Section 6, the numerical complexity for increases considerably and quickly exhausts the memory of a standard computer.

Finally, choosing also allows the accuracy of the AEP algorithm to be increased and, under slightly stronger assumptions on , will lead to convergence of AEP in higher dimensions; see Section 5.

5 An improvement of the numerical accuracy of the algorithm via extrapolation

In this section, we introduce a method to increase the accuracy of the AEP algorithm. This method is based on the choice , as discussed in Section 4. To this end, we will make the stronger assumption that the joint distribution has a twice continuously differentiable density , with bounded derivatives. This will allow us to approximate the density by its linear Taylor expansion, providing a good estimate of the approximation error of AEP after a number of iterations.

We first need two simple integration results. Denoting by a simplex in dimension , for all , we have

Analogously, for all , we have

We now compute the -measures of a hypercube and a simplex in the basic case in which the distribution has a linear density, that is, for . For all , we obtain

Thus, for a linear density , the ratio can be made independent of the parameters and of the ’s, by choosing , for which we have

| (22) |

With similar computations, we obtain the same result for . The following theorem shows that (22) analogously holds for any sufficiently smooth density, in the limit as the number of iterations of the AEP algorithm goes to infinity.

Theorem 5.1

Assume that has a twice continuously differentiable density with all partial derivatives of first and second-order bounded by some constant . We then have that

| (23) |

for some positive constant depending only on the dimension and the distribution .

Proof.

For a given , we can use a Taylor expansion to find some coefficients and , , depending on , such that

| (24) |

where is a ball in centered at such that . Note that in equation (24), we used multi-index notation to indicate that the sum in the last equation extends over multi-indices . Using the assumption on the partial derivatives of , the remainder term satisfies the inequality

| (25) |

for all with . Using (24) and recalling the expressions (5) and (5) for a linear density and a positive , we obtain

Choosing , the previous expression simplifies to

where the last inequality follows from (25). Using the facts that

and

we finally obtain

| (26) |

where is a positive constant depending only on the dimension and the distribution . Note that in (26), we write in absolute value in order to consider the completely analogous case in which is negative. Thus, the theorem easily follows from (26). ∎

Equation (23) gives a local estimator of the mass of the simplex in terms of the volume of the corresponding hypercube , which is straightforward to compute:

| (27) |

In the case where the density is sufficiently smooth, it is then possible, after a number of iterations of AEP, to estimate the right-hand side of (13) by using the approximation (27). This procedure defines the estimator as

| (28) |

In what follows, the use of as an approximation of will be referred to as the extrapolation technique. The following theorem shows that converges to faster, and in higher dimensions, than .

Theorem 5.2

Under the assumptions of Theorem 5.1, we have, for , that

Proof.

| na |

We should point out that, due to Theorem 3.3, Theorem 5.2 also remains valid in the case where satisfies the extra smoothness conditions on its first and second derivatives only in a neighborhood of . Moreover, under the assumptions of Theorem 5.1, it is possible to calculate an upper bound for the error as a function of the number of evaluations performed by AEP. Indeed, (5) can be rewritten as

| (31) |

We now denote by the total number of evaluations of the joint distribution performed by AEP after the th iteration. Then, (as well as the computational time used) is proportional to the number of simplexes passed to the th iteration. For all , we have that

Here, is a positive constant depending only on the dimension . Combining (31) and (5) gives

| (33) |

Then, (33) provides an upper bound on the AEP approximation error as a function of the number of evaluations performed. The polynomial rate of convergence of this bound depends only on the dimensionality . In Table 2, we calculate this bound for dimensions . These numbers can be useful in order to compare the efficiency of AEP with that of other algorithms, such as Monte Carlo methods (see Section 7 and Table 5).

6 Applications

In this section, we test the AEP algorithm on some risk vectors of financial and actuarial interest. For illustrative reasons, we will provide the joint distribution function in terms of the marginal distributions and a copula . For the theory of copulas, we refer the reader to (rN06, ).

In Table 6, we consider a two-dimensional portfolio () with Pareto marginals, that is,

with tail parameters and . We couple these Pareto marginals via a Clayton copula with

The parameter is set to 1.2. For the portfolio described above, we compute the approximation (see (11)) at some given thresholds and for different numbers of iterations of the algorithm. The thresholds are chosen in order to have estimates in the center as well as in the (heavy) tail of the distribution. For each , we provide the computational time needed to obtain the estimate on an Apple MacBook (2.4 GHz Intel Core 2 Duo, 2 GB RAM). Of course, computational times may vary depending on the hardware used for computations. We also provide the estimates obtained by using the estimator , as defined in (28).

For all iterations and thresholds , in Table 6, we provide the differences or . This has been done in order to show the speed of convergence of the algorithm and the increase in accuracy due to extrapolation. The choice of as the reference value in Table 6 represents the maximum number of iterations allowed by the memory (2 GB RAM) of our laptop. However, for a two-dimensional vector, we see that all iterations after the seventh leave the first eight decimal digits of the probability estimate unaltered for all the thresholds. Thus, the estimate (0.01 seconds) could already be considered reasonably accurate. We also note that, on average, extrapolation allows the accuracy of the estimates to be increased by two decimal digits without increasing computational time.

In Tables 6 () to 6 () we perform the same analysis for different Clayton–Pareto models in which we progressively increase the number of random variables used. In Tables 6–6, the numbers for , for and for again represent the maximum number of iterations allowed by the memory (2 GB RAM) of our laptop.

AEP shows good convergence results for all dimensions and thresholds under study. In higher dimensions , the extrapolation technique still seems to provide some relevant extra accuracy. Memory constraints made estimates for prohibitive. For dimensions , Figure 4 shows that the average computational time needed by AEP to provide a single estimate increases exponentially in the number of iterations . These average computational times have been computed based on several portfolios of Pareto marginals coupled by a Clayton copula.

=Values for and (starred columns) for the sum of two Pareto distributions with parameters and , coupled by a Clayton copula with parameter ; for all , we give the difference from the reference value (reference value, 49.25 s) (0.01 s) (0.01 s) (0.06 s) (0.06 s) (1.61 s) (1.61 s) This is the same as Table 6, but for the sum of three Pareto distributions with parameters , and , coupled by a Clayton copula with parameter (reference value, 118.50 s) (0.02 s) (0.02 s) (0.41 s) (0.41 s) (6.65 s) (6.65 s) This is the same as Table 6, but for the sum of four Pareto distributions with parameters , , and , coupled by a Clayton copula with parameter (reference value, 107.70 s) (0.03 s) (0.03 s) (0.47 s) (0.47 s) (7.15 s) (7.15 s)

Note that Tables 6–6 provide information about the convergence of the algorithm to a certain value, but do not say anything about the correctness of the limit. Indeed, we do not have analytical methods to compute when the vector has a general dependence structure (copula) .

In practice, it is possible to test the accuracy of AEP in particular cases when the are independent or comonotonic. Some test cases are analyzed in Tables 6 () to 3 (), where we still assume that we have Pareto marginals, but coupled by a Gumbel copula , in which the parameter is allowed to vary. Formally, for , , we have

In the tables mentioned above, the multivariate model varies from independence () to comonotonicity (). In these two extreme (with respect to the dependence parameter ) cases, we compare the analytical values for with their AEP estimates. Tables 6–6 show that the extrapolated estimator provides accurate estimates within a very reasonable computational time. A comparison with alternative methods is discussed in Section 7.

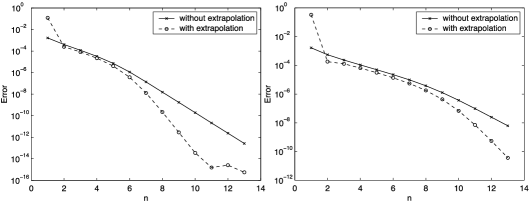

The possibility of computing the value independently from AEP also allows us to test more specifically the effect of extrapolation. For this, we consider two- and three-dimensional vectors of independent Pareto marginals. Figure 5 shows the increase of accuracy due to extrapolation. Therefore, under a smooth model for (see Theorem 5.1), the extrapolated estimator is to be preferred over .

=This is the same as Table 6, but for the sum of five Pareto distributions with parameters , , , and , coupled by a Clayton copula with parameter (reference value, 92.91 s) (0.01 s) (0.01 s) (0.20 s) (0.20 s) (4.37 s) (4.37 s) Values for for the sum of two Pareto distributions with parameters , coupled by a Gumbel copula with parameter ; the values in the first and last columns are calculated analytically; the computational time for each estimate in this table is 0.53 seconds with (exact) (exact) This is the same as Table 6, but for the sum of three Pareto distributions with parameters , coupled by a Gumbel copula with parameter ; the computational time for each estimate in this table is 6.65 seconds with (exact) (exact)

Of course, the AEP algorithm can be used to find estimates for the quantile function, that is, for the inverse of the distribution of the sum . Such quantiles are especially useful in finance and insurance, where they are generally referred to as value-at-risk (VaR) or return periods. In Table 4, we calculate, by numerical inversion, VaR at different quantile levels for two different three-dimensional portfolios of risks. In order to calculate VaR values, we use root-finding algorithms like the bisection method.

We finally note that the choices of copula families (Clayton, Gumbel) and marginal distributions used in this section are purely illustrative and do not in any way affect the functioning of the AEP algorithm. The same performances were reached for vectors showing negative dependence, as in the case of Pareto marginals coupled by a Frank copula with negative parameter.

| (exact) | (exact) | ||||||

|---|---|---|---|---|---|---|---|

The accuracy of AEP is not sufficient to estimate high level quantiles in dimensions as done in Table 4 for some three-dimensional portfolios. The algorithm can, however, be used to compute a numerical range for the quantiles of the sum of four and five random variables. The error resulting from AEP in these higher dimensions turns out to be extremely small if compared to the error due to statistical inference. As a comparison to statistical methods, we estimate the VaR of the sum of the five Pareto marginals described in Table 6 via extreme value theory (EVT) methodology in its “peaks over threshold” (POT) form; see (MNFE05, ), Section 7.2. We set the quantile level , a value not uncommon in several risk management applications in insurance and finance. The POT method is widely used for calculating quantiles in the presence of heavy-tailed risks and is known to perform very well in the case of exact Pareto models, such as the one studied here. In order to focus on the statistical error produced by the POT method, we use, as data, a sample of realizations from the portfolio described in Table 6. It is well known that the statistical reliability of the POT approach is very sensitive to the choice of the threshold beyond which a GPD distribution is fitted. In Figure 6, we plot the VaR estimates obtained by choosing different thresholds . The picture on the left is obtained by generating data, while the one on the right uses simulations. It is remarkable that, even in an ideal data world, the statistical range of variation of the VaR estimates obtained via POT is broader than the numerical VaR range calculated via AEP. Moreover, the POT range of values depends on the specific sample used for estimation, while the AEP range is deterministic. In the next section, we will compare AEP with more competitive numerical techniques such as Monte Carlo, quasi-Monte Carlo and quadrature methods.

7 A comparison with Monte Carlo, quasi-Monte Carlo and quadrature methods

For the estimation of , the main competitors of the AEP algorithm are probably Monte Carlo and quasi-Monte Carlo methods. Given points in , it is possible to approximate by the average of the density function evaluated at those points, that is,

| (34) |

If the ’s are chosen to be (pseudo-)randomly distributed, this is the Monte Carlo (MC) method. If the ’s are chosen as elements of a low-discrepancy sequence, this is the quasi-Monte Carlo (QMC) method. A low-discrepancy sequence is a totally deterministic sequence of vectors that generates representative samples from a uniform distribution on a given set. With respect to Monte Carlo methods, the advantage of using quasi-random sequences is that points cannot cluster coincidentally on some region of the set. However, randomization of a low-discrepancy sequence often improves performance; see (EL00, ).

In recent years, various methods and algorithms have been developed in order to reduce the variance of MC and QMC estimators and to obtain probabilities of (rare) events with reasonable precision and effort. For details on the theory of rare event simulation within MC methods, we refer the reader to (AG07, ; pG04, ; McL05, ; McL08, ). For an introduction to quasi-Monte Carlo methods and recent improvements, we refer to, for instance, (hN92, ) and (EL00, ). A comprehensive overview of both methods is given in (SW00, ).

Using central limit theorem arguments, it is possible to show that traditional MC, using (pseudo-)random numbers, has a convergence rate of , independently of the number of dimensions . QMC can be much faster than MC with errors approaching in optimal cases (see (wM98, )), but the worst theoretic rate of convergence decreases with the dimension as ; see (hN92, ). In applications to finance and insurance, it is more common to get results closer to the best rate of convergence if the density is smooth, that is, has a Lipschitz-continuous second derivative. In this case, it is possible to show that the convergence rate is at least ; see (CMO97, ). In Table 5, we compare convergence rates of MC and QMC methods with respect to the AEP rates (depending on ), as provided in Section 5. We thus expect a well-designed QMC algorithm to perform better, asymptotically, than AEP under a smooth probability model and for dimensions . Because of the computational issues for AEP in higher dimensions, we restrict our attention to in Table 5.

| 2 | 3 | 4 | 5 | |

|---|---|---|---|---|

| AEP (upper bound) | ||||

| MC | ||||

| QMC (best) | ||||

| QMC (worst) |

Don McLeish kindly adapted an algorithm using a randomized Korobov low-discrepancy sequence to the portfolio leading to Table 6. The parameters for the sequence are those recommended in (HL07, ). The standard errors (s.e.’s) are obtained by independently randomizing ten (part (a) of the table) and fifty (part (b) of the table) sequences with 1 million terms each, corresponding to (a) and (b). The average CPU times are, of course, on a different machine (IBM Thinkpad 2.5 GHz Intel Core 2 Dual, 4 GB RAM). In Table 6b, we provide the comparison between QMC and AEP extrapolated estimates. The results seem to be coherent with Table 5 above. For the same precision, AEP is much faster than QMC in the two-dimensional example and slightly slower for . Recall that, in higher dimensions, programming a randomized Korobov rule is much more demanding than using AEP.

| AEP estimate (, 4.87 s) | QMC estimate (107, 6.6 s) | QMC s.e. | |

|---|---|---|---|

| 0.315835041363413 | 0.3158345 | ||

| 0.983690398912470 | 0.98369106 | ||

| 0.999748719228038 | 0.99974872 | ||

| 0.999996018907752 | 0.999996 |

| AEP estimate (, 107.70 s) | QMC estimate (507, 95 s) | QMC s.e. | |

|---|---|---|---|

| 0.833826902853978 | 0.83380176 | ||

| 0.983565803484355 | 0.98362452 | ||

| 0.997972831330699 | 0.997997715 | ||

| 0.999745113409911 | 0.999748680 |

What is important to stress here is that in MC and randomized QMC methods similar to the one applied in Table 6b, the final estimates contain a source of randomness. Contrary to this, the AEP algorithm is deterministic, being solely based on geometric properties of a certain domain. Moreover, the accuracy of MC and QMC methods is generally lost for problems in which the density is not smooth or cannot be given in closed form, and comes at the price of an adaptation of the sampling algorithm to the specific example under study. Recall that the AEP algorithm does not require the density of the distribution in analytic form, nor does it have to assume overall smoothness. Finally, the precision of MC methods depends on the threshold at which is evaluated: estimates in the (far) tail of the distribution will be less accurate.

The re-tailoring, from example to example, of the rule to be iterated is also common to other numerical techniques for the estimation of such as quadrature methods; see (DR84, ) and (PTSV07, ) for a review. However, in the computation of multi-dimensional integrals, as in (34), numerical quadrature rules are typically less efficient than MC and QMC.

When the random variables are exchangeable and heavy-tailed, some asymptotic approximations of for large can be found in BFG06 ; LGH05 and references therein. It is important to remark that the behavior of AEP is not affected by the threshold at which is computed, nor by the tail properties of the marginal distributions . This is particularly interesting as, under heavy-tailedness, the relative error of MC and QMC methods increases in the tail of the distribution function of .

We are, of course, aware that a well-designed quadrature rule or a specific quasi-random sequence might perform better than AEP in a specific example, with respect to both accuracy and computational effort. However, AEP provides very accurate estimates of the distribution of sums up to five dimensions in a reasonable time without the need to adapt to the probabilistic model under study. AEP can handle, in a uniform way, any joint distribution , possibly in the form of its copula and marginal distributions. Because of its ease of use and the very weak assumptions upon which it is based, AEP offers a competitive tool for the computation of the distribution function of a sum of up to five random variables. A Web-based, user-friendly version has been programmed and will eventually be made available.

8 Final remarks

In this paper, we have introduced the AEP algorithm in order to compute numerically the distribution function of the sum of random variables with given joint distribution . The algorithm is mainly based on two assumptions: the random variables are bounded from below and the distribution has a bounded density in a neighborhood of the curve defined in (15). Under this last assumption, the sum has to be continuous at the threshold where the distribution is calculated, that is, . When, instead, , the algorithm may fail to converge. As an example, take two random variables and with . Then, , but the sequence alternates between and . Similar examples for arbitrary dimension can easily be constructed.

If has at least a bounded density near , then the convergence of the sequence to the value is guaranteed. As already remarked, the speed of convergence may vary, depending on the probability mass of a neighborhood of . Tools to increase the efficiency of the algorithm are therefore much needed in these latter cases.

The AEP algorithm has been shown to converge when if the joint distribution of the vector has a bounded density . Under some extra smoothness assumptions on , convergence holds when . All of these conditions can be weakened to hold only in a neighborhood of the curve and are satisfied by most examples which are relevant in practice.

We were not able to prove convergence of AEP in arbitrary dimensions, although we conjecture this to hold. The main problem in higher dimensions is the non-monotonicity of and . This results from the fact that the ’s, as defined in (12), may be positive as well as negative. From a geometric point of view, the main problem is the fact that the simplexes , , passed to the th iteration of the algorithm, are generally not disjoint for . As illustrated in Table 1, the sum of the Lebesgue measures of the ’s is increasing in the number of iterations when , while their union always lies in some neighborhood of the curve . A general convergence theorem may need a volume decomposition different from (9) and using only a family of disjoint simplexes, or else an extension of the extrapolation technique.

We also remark that the statement of a general convergence theorem will not entail any practical improvement of AEP, since memory constraints limit the use of the algorithm to dimension . However, in these manageable dimensions, we expect the AEP convergence rates to be better than their upper bounds given in Table 2.

Apart from the study of convergence of AEP in higher dimensions, in future research, we will also address an extension of the algorithm to more general aggregating functions and the study of an adaptive (i.e., depending on ) and more efficient (in terms of new simplexes produced at each iteration) decomposition of the simplexes.

Appendix: Proof of (9)

Recall that, in Section 1, we denoted by all of the vectors in , with , , , and , where . Also, recall that denotes the number of ’s in the vector , for instance, , .

Theorem .1

For any , and , we have that

where, for all ,

Note that (.1) is equivalent to (9) under the notation introduced in Section 3. In order to prove the above theorem, we need some lemmas. In the following, denotes the Kronecker delta, that is,

Lemma .2

Fix with . Then, for any with and , we have that

Proof.

Proof of First, assume . By definition (4), for a vector , we have that

from which it follows that

that is, . Now, assume that . For a vector , we have that

| (36) |

Again, , therefore . Subtracting from both sides of the last inequality, we obtain

| (37) |

Equations (36) and (37) show that . The case is analogous.\noqed

Proof of If , there is nothing to show. Suppose, then, that . For any fixed , (37) holds with , . By adding in the sum on the left-hand side and to the right-hand side of (37), we find that

| (38) |

Since is still positive for all , (38) shows that . By similar reasoning, we also have that . The case is analogous; the case is trivial. \noqed∎

Lemma .3

For any , and , we have that

Proof.

Proof of First, assume that . If , then , and , while, by definition (2), there exists a such that . For this , it is then possible to write

| (39) |

which yields \noqed

Lemma .4

For any , and , we have that

Proof.

Proof of If , then the lemma is straightforward. So, choose and assume . If , then for all . Since , it follows that . Since for all , we can write

| (40) |

As , we conclude that and, hence, by assumption, .

Proof of Let . Due to , it follows that (40) holds, implying that , that is, . The case is analogous, while the case is trivial. \noqed∎

We are now ready to prove the main result in this appendix. {pf*}Proof of Theorem .1 The case is trivial. Suppose, then, that . From the general property of two sets that , and , it follows that

| (41) |

Using the notation , Lemma .3 implies, for the second summand in (41), that

| (42) |

Fixing with , iteratively using Lemma .2 yields

Substituting this last expression into (42) implies that

Using Lemma .4 for the third summand in (41), we can also write that

| (44) | |||

Note that if , then the quantity in (Appendix: Proof of (9)) is zero. We can hence assume that . Observing that and defining , and , we can write

Note that the right-hand side of the previous equation is empty if , that is, . At this point, equation (Appendix: Proof of (9)) yields

Substituting () into the previous equation, we can equivalently write

| (45) | |||

In keeping with what was noted above, this last equation is null in the aforementioned case in which . Recalling (Appendix: Proof of (9)) and noting that

we obtain

Finally, recalling the definitions in (.1), we substitute equations (Appendix: Proof of (9)) and (Appendix: Proof of (9)) into (41) to obtain

Acknowledgements

The authors are grateful to Don McLeish for providing relevant comments on the paper and the example illustrated in Table 5. Giovanni Puccetti would like to thank RiskLab and the Forschungsinstitut für Mathematik (FIM) of the Department of Mathematics, ETH Zürich, for its financial support and kind hospitality. Philipp Arbenz would like to thank SCOR for financial support toward the final stages of writing this paper. The final version of the paper was written while Paul Embrechts was visiting the Institute for Mathematical Sciences at the National University of Singapore. Finally, the authors would like to thank two anonymous referees and an Associate Editor for several valuable comments which significantly improved the paper.

References

- (1) Aas, K., Dimakos, X.K. &Øksendal, A. (2007). Risk capital aggregation. Risk Management 9 82–107.

- (2) Asmussen, S. &Glynn, P.W. (2007). Stochastic Simulation: Algorithms and Analysis 57. New York: Springer. MR2331321

- (3) Barbe, P., Fougères, A.-L. &Genest, C. (2006). On the tail behavior of sums of dependent risks. Astin Bull. 36 361–373. MR2312671

- (4) Basel Committee on Banking Supervision (2006). International Convergence of Capital Measurement and Capital Standards. Basel: Bank for International Settlements.

- (5) Bürgi, R., Dacorogna, M. &Iles, R. (2008). Risk aggregation, dependence structure and diversification benefit. In Stress-Testing for Financial Institutions. Applications, Regulations and Techniques (D. Rösch &H. Scheule, eds.). London: Risk Books.

- (6) Caflisch, R.E., Morokoff, W. &Owen, A. (1997). Valuation of mortgage-backed securities using Brownian bridges to reduce effective dimension. J. Comput. Finance 1 27–46.

- (7) Davis, P.J. &Rabinowitz, P. (1984). Methods of Numerical Integration, 2nd ed. Orlando, FL: Academic Press. MR0760629

- (8) Embrechts, P. (2009). Copulas: A personal view. J. Risk Insurance 76 639–650.

- (9) Gill, H.S. &Lemieux, C. (2007). Searching for extensible Korobov rules. J. Complexity 23 603–613. MR2372017

- (10) Glasserman, P. (2004). Monte Carlo Methods in Financial Engineering. New York: Springer. MR1999614

- (11) Laeven, R.J., Goovaerts, M.J. &Hoedemakers, T. (2005). Some asymptotic results for sums of dependent random variables, with actuarial applications. Insurance Math. Econom. 37 154–172. MR2172096

- (12) L’Ecuyer, P. &Lemieux, C. (2000). Variance reduction via lattice rules. Management Science 46 1214–1235.

- (13) McLeish, D.L. (2005). Monte Carlo Simulation and Finance. Hoboken, NJ: Wiley. MR2263887

- (14) McLeish, D.L. (2008). Bounded relative error importance sampling and rare event simulation. Astin Bull. 40 377–398.

- (15) McNeil, A.J., Frey, R. &Embrechts, P. (2005). Quantitative Risk Management: Concepts, Techniques and Tools. Princeton, NJ: Princeton Univ. Press. MR2175089

- (16) Morokoff, W.J. (1998). Generating quasi-random paths for stochastic processes. SIAM Rev. 40 765–788. MR1659693

- (17) Nelsen, R.B. (2006). An Introduction to Copulas, 2nd ed. New York: Springer. MR2197664

- (18) Niederreiter, H. (1992). Random Number Generation and Quasi-Monte Carlo Methods. CBMS-NSF Regional Conference Series in Applied Mathematics 63. Philadelphia: SIAM. MR1172997

- (19) Press, W.H., Teukolsky, S.A., Vetterling, W.T. &Flannery, B.P. (2007). Numerical Recipes: The Art of Scientific Computing, 3rd ed. Cambridge: Cambridge Univ. Press. MR0833288

- (20) SCOR (2008). From Principle Based Risk Management to Solvency Requirements. Switzerland: Swiss Solvency Test Documentation, SCOR.

- (21) Weinzierl, S. (2000). Introduction to Monte Carlo methods. Available at arXiv:hep-ph/ 0006269.