Nonparametric methods for volatility density estimation

Abstract

Stochastic volatility modelling of financial processes has become increasingly popular. The proposed models usually contain a stationary volatility process. We will motivate and review several nonparametric methods for estimation of the density of the volatility process. Both models based on discretely sampled continuous time processes and discrete time models will be discussed.

The key insight for the analysis is a transformation of the volatility density estimation problem to a

deconvolution model for which standard methods exist.

Three type of nonparametric density estimators are reviewed: the Fourier-type deconvolution kernel density estimator,

a wavelet deconvolution density estimator and a penalized projection estimator.

The performance of these estimators will be compared.

Key words: stochastic volatility models, deconvolution, density

estimation, kernel estimator, wavelets, minimum contrast estimation, mixing

AMS subject classification: 62G07, 62G08, 62M07, 62P20, 91G70

1 Introduction

We discuss a number of nonparametric methods that come into play when one wants to estimate the density of the volatility process, given observations of the price process of some asset. The models that we treat are mainly formulated in continuous time, although we pay some separate attention to discrete time models. The observations of the continuous time models will always be in discrete time however and may occur at low frequency (fixed lag between observation instants), or high frequency (vanishing time lag). In this review, for simplicity we focus on the univariate marginal distribution of the volatility process, although similar results can be obtained for multivariate marginal distributions.

Although the underlying models differ in the sense that they are formulated either in continuous or in discrete time, in all cases the observations are given by a discrete time process. Moreover, as we shall see, the observation scheme can always (approximately) be cast as of ‘signal plus noise’ type

where is to be interpreted as the ‘signal’. If for fixed the random variables and are independent, the distribution of the is a convolution of the distributions of and . The density of the ‘signal’ is the object of interest, while the density of the ‘noise’ is supposed to be known to the observer. The statistical problem is to recover the density of the signal by deconvolution. Classically for such models it was often also assumed that the processes and are i.i.d. Under these conditions Fan [12] gave lower bounds for the estimation of the unknown density at a fixed point and showed that kernel-type estimators achieve the optimal rate. An alternative estimation method was proposed in the paper Pensky and Vidakovic [23], using wavelet methods instead of kernel estimators and where global -errors were considered instead of pointwise errors.

However, for the stochastic volatility models that we consider, the i.i.d. assumption on the is violated. Instead, the may be modelled as stationary random variables, that are allowed to exhibit some form of weak dependence, controlled by appropriate mixing properties, strongly mixing or -mixing. These mixing conditions are justified by the fact that they are satisfied for many popular GARCH-type and stochastic volatility models (see e.g. Carrasco and Chen [6]), as well as for continuous time models, where is solves a stochastic differential equation, see e.g. Genon-Catalot et al. [17]. The estimators that we discuss are based on kernel methods, wavelets and penalized contrast estimation, also referred to as penalized projection estimation. We will review the performance of these deconvolution estimators under weaker than i.i.d. assumptions and show that this essentially depends on the smoothness and mixing conditions of the underlying process and the frequency of the observations. For a survey of other nonparametric statistical problems for financial data we refer to Franke et al. [14]

The paper is organized as follows. In Section 2 we introduce the continuous time model. In Section 3 we consider a kernel type estimator of the invariant volatility density and apply it to a set of real data. Section 4 is devoted to a wavelet density estimator and in Section 5 a minimum contrast estimator is discussed. Some related results for discrete time models are reviewed in Section 6 and Section 7 contains some concluding remarks.

2 The continuous time model

Let denote the log price process of some stock in a financial market. It is often assumed that can be modelled as the solution of a stochastic differential equation or, more general, as an Itô diffusion process. So we assume that we can write

| (1) |

or, in integral form,

| (2) |

where is a standard Brownian motion and the processes and are assumed to satisfy certain regularity conditions (see Karatzas and Shreve [22]) to have the integrals in (2) well-defined. In a financial context, the process is called the volatility process. One often takes the process independent of the Brownian motion .

Adopting this common assumption throughout the paper, unless explicitly stated otherwise, we also assume that is a strictly stationary positive process satisfying a mixing condition, for example an ergodic diffusion on . We will assume that the one-dimensional marginal distribution of has an invariant density with respect to the Lebesgue measure on . This is typically the case in virtually all stochastic volatility models that are proposed in the literature, where the evolution of is modelled by a stochastic differential equation, mostly in terms of , or (cf. e.g. Wiggins [31], Heston [20]). Often is a function of a process satisfying a stochastic differential equation of the type

| (3) |

with a Brownian motion. Under regularity conditions, the invariant density of is up to a multiplicative constant equal to

| (4) |

where is an arbitrary element of the state space, see e.g. Gihman and Skorohod [19] or Skorokhod [25]. From formula (4) one sees that the invariant distribution of the volatility process (take for instance equal to or ) may take on many different forms, as is the case for the various models that have been proposed in the literature. In absence of parametric assumptions on the coefficients and , we will investigate nonparametric procedures to estimate the corresponding densities, even refraining from an underlying model like (3), partly aimed at recovering possible ‘stylized facts’ exhibited by the observations.

For instance, one could think of volatility clustering. This may be cast by saying that for different time instants that are close, the corresponding values of are close again. This can partly be explained by assumed continuity of the process , but it might also result from specific areas around the diagonal where the multivariate density of assumes high values if and are relatively close. It is therefore conceivable that the density of has high concentrations around points and , with , a kind of bimodality of the joint distribution, with the interpretation that clustering occurs around a low value or around a high value . This in turn may be reflected by bimodality of the univariate marginal distribution of .

A situation in which this naturally occurs is the following. Consider a regime switching volatility process. Assume that for we have two stationary processes having stationary densities . We assume these two processes to be independent, and also independent of a two-state stationary homogeneous Markov chain with states . The stationary distribution of is given by . The process is defined by

Then is stationary too and it has a stationary density given by

Suppose that the volatility process is defined by and that the are both Ornstein-Uhlenbeck processes given by

with , independent Brownian motions, and . Suppose that the start in their stationary distributions. Then the stationary density is a bimodal mixture of normal densities with and as the locations of the local maxima. Nonparametric procedures are able to detect such a property and are consequently by all means sensible tools to get some first insights into the shape of the invariant density.

A first object of study is the marginal univariate distribution of the stationary volatility process . The standing assumption in all what follows is that this distribution admits a density w.r.t. Lebesgue measure. We will also consider the invariant density of the integrated squared volatility process over an interval of length . By stationarity of this is the density of . We will consider density estimators and assess their quality by giving results on their mean squared or integrated mean squared error. For kernel estimators, we rely on Van Es et al. [10], where this problem has been studied for the marginal univariate density of . In Van Es and Spreij [9] one can find results for multivariate density estimators. Results on wavelet estimators will be taken from Van Zanten and Zareba [32]. Penalized contrast estimators have been treated in Comte and Genon-Catalot [7].

The observations of log-asset price process are assumed to take place at the time instants . In case one deals with low frequency observations, is fixed. For high frequency observations, the time gap satisfies as . To obtain consistency for the estimators that we will study in the latter case, we will make the additional assumption .

To explain the origin of the estimators that we consider in this paper, we often work with the simplified model, which is obtained from (1) by taking . We then suppose to have discrete-time data from a continuous-time stochastic volatility model of the form

Under this additional assumption, we will see that we (approximately) deal with stationary observations that can be represented as , where for each the random variables and are independent.

3 Kernel deconvolution

In this section we consider kernel deconvolution density estimators. We construct them, give expressions for bias and variance and give an application to real data.

3.1 Construction of the estimator

To motivate the construction of the estimator, we first consider (1) without the drift term, so we assume to have the simplified model

| (5) |

It is assumed that we observe the process at the discrete time instants , , , satisfying , . For we work, as in Genon-Catalot et al. [15, 16], with the normalized increments

For small , we have the rough approximation

| (6) | ||||

where for we define

By the independence and stationarity of Brownian increments, the sequence is an i.i.d. sequence of standard normal random variables. Moreover, the sequence is independent of the process by assumption.

Writing , , and taking the logarithm of the square of we get

where the terms in the sum are independent. Assuming that the approximation is sufficiently accurate we can use this approximate convolution structure to estimate the unknown density of from the transformed observed . The characteristic functions involved are denoted by , and , where is the density of the ‘noise’ . One obviously has and one easily sees that the density is given by

and its characteristic function by

The idea of getting a deconvolution estimator of is simple. Using a kernel function , a bandwidth , and the , the density of the is estimated by

Denoting the characteristic function of , one estimates by and by . Following a well-known approach in statistical deconvolution theory (see e.g. Section 6.2.4 of Wand and Jones [30]), Fourier inversion then yields the density estimator of . By elementary calculations one obtains from this procedure

| (7) |

where is the kernel function, depending on the bandwidth ,

| (8) |

One easily verifies that the estimator , is real-valued.

To justify the approximation in (6), we quantify a stochastic continuity property of . In addition to this we make the mixing condition explicit. We impose

Condition 3.1.

The process satisfies the following conditions.

-

1.

It is -Hölder continuous of order one half, for .

-

2.

It is strongly mixing with coefficient satisfying, for some ,

(9)

The kernel function is assumed to satisfy the following conditions (an example of such a kernel is given in (12) below, see also Wand [29]), which includes in particular the behavior of at the boundary of its domain.

Condition 3.2.

Let be a real symmetric function with real valued symmetric characteristic function with support [-1,1]. Assume further

-

1.

, , ,

-

2.

for some , .

The first part of Condition 3.1 is motivated by the situation where solves a SDE like (1). It is easily verified that for such processes it holds that , provided that and , where is the invariant probability measure. Indeed we have .

The main result we present for this estimator concerns its mean squared error at a fixed point . Although the motivation of the estimator was based on the simplified model (5), the result below applies to the original model (1). For its proof and additional technical details, see Van Es et al. [10].

Theorem 3.3.

Assume that is bounded. Let the process satisfy Condition 3.1, and let the kernel function satisfy Condition 3.2. Moreover, let the density of be twice continuously differentiable with a bounded second derivative. Also assume that the density of is bounded in a neighbourhood of zero. Suppose that for given and choose , where . Then the bias of the estimator (7) satisfies

| (10) |

whereas, the variance of the estimator satisfies the order bounds

| (11) |

Remark 3.4.

The choices , with and , with render a variance that is of order for the first term of (11) and for the second term. Since by assumption we have so the second term dominates the first term. The order of the variance is thus . Of course, the order of the bias is logarithmic, hence the bias dominates the variance and the mean squared error of is of order .

Remark 3.5.

It can then be shown that for the characteristic function one has the behavior

This means that is supersmooth in the terminology of Fan [12] which explains the slow logarithmic rate at which the bias vanishes. Sharper results on the variance can be obtained when is strongly mixing, see Van Es et al. [11] for further details. The orders of the bias and of the MSE remain unchanged though.

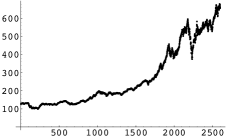

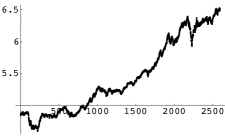

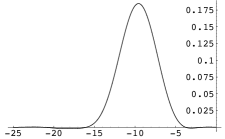

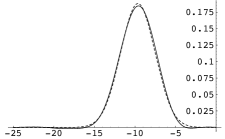

3.2 An application to the Amsterdam AEX index

In this section we present an example using real data of the Amsterdam AEX stock exchange. We have estimated the volatility density from 2600 daily closing values of the Amsterdam stock exchange index AEX from 12/03/1990 until 14/03/2000. These data are represented in Figure 1. We have centered the daily log returns, i.e we have subtracted the mean (which equaled 0.000636), see Figure 2. The deconvolution estimator is given as the left hand picture in Figure 3. Observe that the estimator strongly indicates that the underlying density is unimodal. Based on computations of the mean and variance of the estimate, with , we have also fitted a normal density by hand and compared it to the kernel deconvolution estimator. The result is given as the right hand picture in Figure 3. The resemblance is remarkable.

The kernel used to compute the estimates is a kernel from Wand [29], with and ,

| (12) |

It has characteristic function

| (13) |

The bandwidths are chosen by hand. The estimates have been computed by fast Fourier transforms using the Mathematica 4.2 package.

This is actually the same example as in our paper Van Es et al. [11] on volatility density estimation for discrete time models. The estimator (7) presented here is, as a function of the sampled data, exactly the same as the one for the discrete time models. The difference lies in the choice of underlying model. In the present paper the model is a discretely sampled continuous time process, while in Van Es et al. [11] it is a discrete time process. For the latter type of models the discretization step in the beginning of this section is not necessary since these models satisfy an exact convolution structure.

4 Wavelet deconvolution

As an alternative to kernel methods, in this section we consider estimators based on wavelets. Starting point is again the simplified model (5). Contrary to the previous section, we are now interested in estimating the accumulated squared volatility over an interval of length . We assume having observations of at times to our disposal, but now with fixed (low frequency observations). Let, as before, and let . Denote by the -algebra generated by the process . By the assumed independence of the processes and , we have for the characteristic function of given

Consider also the model , with and independent for each and a standard Gaussian random variable. Then

It follows that and are identically distributed. From this observation we conclude that the transformed increments are then distributed as , where

and is an i.i.d. sequence of standard Gaussian random variables, independent of . The sequence is stationary and we assume that its marginal density exists, i.e. is the density of . The density of the is again denoted by . Of course, estimating is equivalent to estimating the density of the aggregated squared volatility .

In the present section the main focus is on the quality of the estimator in terms of the mean integrated squared error, as opposed to establishing results for the (pointwise) mean squared error as in Section 3. At the end of this section we compare the results presented here to those of Section 3.

First we recall the construction of the wavelet estimator proposed in Pensky and Vidakovic [23]. For the necessary background on wavelet theory, see for instance Blatter [1], Jawerth and Sweldens [21], and the references therein. For the construction of deconvolution estimators we need to use band-limited wavelets. As in Pensky and Vidakovic [23] we use a Meyer-type wavelet (see also Walter [27], Walter and Zayed [28]). We consider an orthogonal scaling function and wavelet and , respectively, associated with an orthogonal multiresolution analysis of . We denote in this section the Fourier transform of a function by , i.e.

and suppose that for a symmetric probability measure with support contained in it holds that

Observe that the assumptions imply that and are indeed band-limited. For the supports of their Fourier transforms we have and . By choosing smooth enough we ensure that and are at least twice continuously differentiable.

For any integer , the unknown density can now be written as

| (14) |

where , and the coefficients are given by

The idea behind the linear wavelet estimator is simple. We first approximate by the orthogonal projection given by the first term on the right-hand side of (14). For large enough the second term will be small, and can be controlled by using the approximation properties of the specific family of wavelets that is being used. The projection of is estimated by replacing the coefficients by consistent estimators and truncating the sum. Using the fact that the density of an observation is the convolution of and it is easily verified that

where is the function with Fourier transform

| (15) |

We estimate the coefficient by its empirical counterpart

Under the mixing assumptions that we will impose on the sequence , it will be stationary and ergodic. Hence, by the ergodic theorem, is a consistent estimator for . The wavelet estimator is now defined by

| (16) |

where the detail level and the truncation point will be chosen appropriately later.

The main results in the present section are upper bounds for the mean integrated square error of the wavelet estimator , which is defined as usual by

We will specify how to choose the detail level and the truncation point in (16) optimally in different cases, depending on the smoothness of and . The smoothness properties of are described in terms of belonging to certain Sobolev balls and by imposing a weak condition on its decay rate. The Sobolev space is defined for by

| (17) |

Roughly speaking, means that the first derivatives of belong to . The Sobolev ball of radius is defined by

The additional assumption on the decay rate is reflected by belonging to

We now have the following result, see Van Zanten and Zareba [32], for the wavelet density estimator of defined by (16).

Theorem 4.1.

Suppose that the volatility process is strongly mixing with mixing coefficients satisfying

| (18) |

for some . Then with the choices

the mean square error of the wavelet estimator satisfies

for . If (18) is satisfied for all , the same bound is true if the choice for is replaced by .

Let us point out the relation with the results of Section 3 and with those in Van Es et al. [11], see also Section 6.1. In that paper kernel-type deconvolution estimators for discrete time stochastic volatility models were considered. When applied to the present model the results say that under the same mixing condition and assuming that has two bounded and continuous derivatives, the (pointwise) mean squared error of the kernel estimator is of order . The analogue of having two bounded derivatives in our setting is that for some . Indeed, the theorem yields the same bound for the MISE in this case. The same bound is valid for the MSE when estimating the marginal density for continuous time models, see Theorem 3.3 and its consequences in Remark 3.4. Theorem 4.1 is more general, because the smoothness level is not fixed at , but allows for different smoothness levels of order as well. Moreover, the wavelet estimator is adaptive in the sense that it does not depend on the unknown smoothness level, if the condition on the mixing coefficients holds for all .

5 Penalized projection estimators

The results of the preceding sections assume that the true (integrated) volatility density has a finite degree of regularity, either in Hölder or in Sobolev sense. Under this assumption the nonparametric estimators have logarithmic convergence rates, cf. Remark 3.4 and Theorem 4.1. Although admittedly slow, the minimax results of Fan [12] show that these rates are in fact optimal in this setting. In the paper Pensky and Vidakovic [23] it was shown however that if in a deconvolution setting the density of the unobserved variables has the same degree of smoothness as the noise density, the rates can be significantly improved, cf. also the lower bounds obtained in Butucea [4] and Butucea and Tsybakov [5]. This observation forms the starting point of the paper Comte and Genon-Catalot [7], in which a nonparametric volatility density estimator is developed that achieves better rates than logarithmic if the true density is super smooth.

In the latter paper it is assumed that there are observations of a process satisfying the simple equation (5), with a -valued process independent of the Brownian motion . It is assumed that we deal with high frequency observations, and . We impose the following condition on .

Condition 5.1.

The process is a time-homogenous, continuous Markov process, strictly stationary and ergodic. It is either -mixing with coefficient satisfying

or is -mixing. Moreover, it satisfies the Lipschitz condition

for some .

In addition to this a technical assumption is necessary on the density of we are interested in and on the density of , which is assumed to exist. Contrary to the notation of the previous section, we write instead of , since now is not fixed.

Condition 5.2.

The invariant density is bounded and has a second moment and .

As a first step in the construction of the final estimator a preliminary estimator is constructed for fixed. Note that Condition 5.2 implies that , hence we can consider its orthogonal projection on the subspace of , defined as the space of functions whose Fourier transform is supported on the compact interval . An orthonormal basis for the latter space is formed by the Shannon basis functions , , with the sinc kernel. For integers to be specified below, the space is approximated by the finite-dimensional spaces . The function is estimated by , where the contrast function is defined for by

Here, as before, is the characteristic function of , with standard normal and is the Fourier transform of . It is easily seen that

Straightforward computations show that, with the inner product, , and hence . So in fact, is an estimator of the element of which is closest to . Since approximates for large and is close to for small , the latter element should be close to .

Under Conditions 5.1 and 5.2, a bound for the mean integrated square error, or quadratic risk MISE can be derived, depending on the approximation error , the bandwidth and the truncation point , see Comte and Genon-Catalot [7], Theorem 1. The result implies that if belongs to the Sobolev space as defined in (17), then the choices and yield a MISE of the order , provided that for some . Not surprisingly, this is completely analogous to the result obtained in Theorem 4.1 for the wavelet-based estimator in the fixed setting. In particular the procedure is adaptive, in that the estimator does not depend on the unknown regularity parameter .

To obtain faster than logarithmic rates and adaptation in the case that is supersmooth, a data-driven choice of the bandwidth is proposed. Define

where the penalty term is given by

for a calibration constant and

For the quadratic risk of the estimator , the following result holds (Comte and Genon-Catalot [7]).

It can be seen that this bound is worse than the corresponding bound for the estimator by a factor of the order . This is at worst a logarithmic factor which, as usual in this kind of setting, has to be paid for achieving adaptation. The examples in Section 6 of Comte and Genon-Catalot [7] show that indeed, the estimator can achieve algebraic convergence rates in case the true density is supersmooth.

6 Estimation for discrete time models

Although the main focus of the present paper is on estimation procedures for continuous time models, in the present section we also highlight some analogous results for discrete time models. These deal with both density and regression function estimation.

6.1 Discrete time models

The discrete analogue of (5) is

| (19) |

Here we denote by the detrended or demeaned log-return process. Stochastic volatility models are often described in this form. The sequence is typically an i.i.d. noise (e.g. Gaussian) and at each time the random variables and are independent. See the survey papers by Ghysels et al. [18] or Shephard [24]. Also in this section we assume that the process is strictly stationary and that the marginal distribution of has a density with respect to the Lebesgue measure on . We present some results for a nonparametric estimator of the density of , as well as results for a nonparametric estimator of a nonlinear regression function, in case is given by a nonlinear autoregression. The standing assumption in all what follows is that for each the random variables and are independent, the noise sequence is standard Gaussian and is a strictly stationary, positive process satisfying a certain mixing condition.

In principle one can distinguish two classes of models. The way in which the bivariate process , in particular its dependence structure, is further modelled offers different possibilities. In the first class of models one assumes that the process is predictable with respect to the filtration generated by the process , and obtains that is independent of for each fixed time . We furthermore have that (assuming that the unconditional variances are finite) is equal to the conditional variance of given . This class of models has become quite popular in the econometrics literature. It is well known that this class also contains the (parametric) family of GARCH-models, introduced by Bollerslev [2].

In the second class of models one assumes that the whole process is independent of the noise process , and one commonly refers to the resulting model as a stochastic volatility model. In this case, the natural underlying filtration is generated by the two processes and in the following way. For each the -algebra is generated by , and , . This choice of the filtration enforces to be predictable. As in the first model the process becomes a martingale difference sequence and we have again (assuming that the unconditional variances are finite) that is the conditional variance of given . An example of such a model is given in De Vries [26], where is generated as an AR(1) process with -stable noise ().

As in the previous sections we refrain from parametric modelling and review some completely nonparametric approaches. We will mainly focus on results for the second class, as it is the discrete time analogue of the stochastic volatility models of the previous sections. At the heart of all what follows is again the convolution structure that is obtained from (19) by squaring and taking logarithms,

6.2 Density estimation

The main result of this section gives a bias expansion and a variance bound of a kernel density type estimator of the density of , which chosen to be, analogously to (7),

| (20) |

where is the kernel function of (8).

The next theorem is derived from Van Es et al. [11], where a multivariate density estimator is considered. It establishes the expansion of the bias and an order bound on the variance of our estimator under a strong mixing condition. Under broad conditions this mixing condition is satisfied if the process Markov, since then convergence of the mixing coefficients to zero takes place at an exponential rate, see Theorems 4.2 and Theorem 4.3 of Bradley [3] for precise statements. Similar behaviour occurs for ARMA processes with absolutely continuous distributions of the noise terms (Bradley [3], Example 6.1).

Theorem 6.1.

Assume that the process is strongly mixing with coefficient satisfying

for some . Let the kernel function satisfy Condition 3.2 and let the density of be bounded and twice continuously differentiable with bounded second order partial derivatives. Assume furthermore that and are independent processes. Then we have for the estimator of defined as in (20) and

| (21) |

and

| (22) |

Remark 6.2.

Comparing the above results to the ones in Theorem 3.3, we observe that in the continuous time case, the variance has an additional term.

6.3 Regression function estimation

In this section we assume the basic model (19), but in addition we assume that the process satisfies a nonlinear autoregression and we consider nonparametric estimation of the regression function as proposed in Franke et al. [13]. In that paper a discrete time model was proposed as a discretization of the continuous time model given by (1). In fact, Franke et al. include a mean parameter , but since they assume it to be known, without loss of generality we can still assume (19). Assume that the volatility process is strictly positive and consider . It is assumed that its evolution is governed by

| (23) |

where the are i.i.d. Gaussian random variables with zero mean. The regression function is assumed to satisfy the stability condition

| (24) |

Under this condition the process is exponentially ergodic and strongly mixing, see Doukhan [8] and these properties carry over to the process as well. Moreover, the process admits an invariant density .

Denoting , we have

It is common to assume that the processes and are independent, the second class of models described in Section 6.1, but dependence between and for fixed can be allowed for (first model class) without changing in what follows, see Franke et al. [13].

The purpose of the present section is to estimate the function in (23). To that end we use the estimator as defined in (20). Since this estimator resembles an ordinary kernel density estimator, the important difference being that the kernel function now depends on the bandwidth , the idea is to mimic the classical Nadaraya-Watson regression estimator similarly, in order to obtain an estimator of . Doing so, one obtains the estimator

| (25) |

It follows that

where

In Franke et al. [13] bias expansions for and are given that fully correspond to those in Theorem 6.1. They are again of order , under similar assumptions. It is also shown that the variances of and tend to zero. The main result concerning the asymptotic behavior then follows from combining the asymptotics for and .

Theorem 6.3.

Following the proofs in Franke et al. [13], one can conclude that e.g. the variance of is of order , which tends to zero for , with . For the variance of a similar bound holds. Comparing these order bounds to the ones in Theorem 6.1, we see that the latter ones are sharper. This is partly due to the fact that Franke et al. [13], don’t impose conditions on the boundary behavior of the function (the second of Condition 3.2), whereas their other assumptions are the same as in Theorem 6.1.

7 Concluding remarks

In recent years, many different parametric stochastic volatility models have been proposed in the literature. To investigate which of these models are best supported by observed asset price data, nonparametric methods can be useful. In this paper we reviewed a number of such methods that have recently been proposed. The overview shows that ideas from deconvolution theory can be instrumental in dealing with this statistical problem and that both for high and for low frequency data, methods are now available for nonparametric estimation of the (integrated) volatility density at optimal convergence rates.

On a critical note, the methods available so far all assume that the volatility process is independent of the Brownian motion driving the asset price dynamics. This is a limitation, since in several interesting models non-zero correlations are assumed between the Brownian motions driving the volatility dynamics and the asset price dynamics.

References

- [1] Blatter, C. (1998). Wavelets, a primer. A. K. Peters Ltd.

- [2] Bollerslev, T. (1986), Generalized autoregressive conditional heteroscedasticity, J. Econometrics 31, 307–321.

- [3] Bradley, R.C. (1986), Basic properties of strong mixing conditions, in Dependence in Probability and Statistics, E. Eberlein and M.S. Taqqu Eds., Birkhaüser.

- [4] Butucea, C. (2004). Deconvolution of supersmooth densities with smooth noise. Can. J. Statist. 32, 181–192.

- [5] Butucea, C. and Tsybakov, A.B. (2008). Sharp optimality in density deconvolution with dominating bias. I. Theory Probab. Appl. 52(1), 24–39.

- [6] Carrasco, M. and Chen, X. (2002). Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory 18, 17–39.

- [7] Comte, F. and Genon-Catalot, V. (2006), Penalized projection estimator for volatility density, Scand. J. Statist. 33(4), 875–893.

- [8] Doukhan, P. (1994). Mixing: properties and examples. Springer.

- [9] Van Es, A.J. and Spreij, P.J.C. (2009), Multivariate Nonparametric Volatility Density Estimation, preprint Mathematics ArXiv 0910.4337.

- [10] Van Es, A.J., Spreij, P.J.C. and Van Zanten, J.H. (2003). Nonparametric volatility density estimation. Bernoulli 9(3), 451–465.

- [11] Van Es, A.J., Spreij, P.J.C. and Van Zanten J.H. (2005), Nonparametric volatility density estimation for discrete time models, J. Nonparametr. Stat. 17, 237–251.

- [12] Fan, J. (1991). On the optimal rates of convergence of nonparametric deconvolution problems. Ann. Statist. 19, 1257–1272.

- [13] Franke, J., Härdle, W. and Kreiss, J.P. (2003), Nonparametric estimation in a stochastic volatility model, In: Recent Advances and Trends in Nonparametric Statistics, M.G. Akritas and D.N. Politis Eds, Elsevier.

- [14] Franke, J., Kreiss, J.P. and Mammen E. (2009), Nonparametric modelling in financial time series, In: Handbook of Financial Time Series, T. Mikosch, J.P. Kreiss, R.A. Davis and T.G. Andersen Eds, Springer.

- [15] Genon-Catalot, V., Jeantheau, T. and Larédo, C. (1998), Limit theorems for discretely observed stochastic volatility models, Bernoulli 4, 283–303.

- [16] Genon-Catalot, V., Jeantheau, T. and Larédo, C. (1999), Parameter estimation for discretely observed stochastic volatility models, Bernoulli 5, 855-872.

- [17] Genon-Catalot, V., Jeantheau, T. and Larédo, C. (2000). Stochastic volatility models as hidden Markov models and statistical applications. Bernoulli 6(6),1051–1079.

- [18] Ghysels, E., Harvey, A. and Renault, E. (1996), Stochastic Volatility, in Maddala, G.S. and Rao, C.R. (eds), Handbook of Statistics, Vol. 14, Statistical Methods in Finance, North-Holland, Amsterdam, 119–191.

- [19] Gihman, I.I. and Skorohod A.V. (1972), Stochastic Differential Equations, Springer.

- [20] Heston, S.L. (1993), A closed-form solution for options with stochastic volatility with applications to Bond and Currency options, The Review of Finacial Studies 6 (2), 327–343.

- [21] Jawerth, B. and Sweldens, W. (1994). An overview of wavelet based multiresolution analyses. SIAM Rev. 36, 377–412.

- [22] Karatzas, I. and S.E. Shreve (1991), Brownian Motion and Stochastic Calculus, Springer Verlag, New York.

- [23] Pensky, M. and Vidakovic, B. (1999). Adaptive wavelet estimator for nonparametric density deconvolution. Ann. Statist. 27, 2033–2053.

- [24] Shephard, N. (1996), Statistical aspects of ARCH and stochastic volatility, in D.R. Cox, D.V Hinkley and O.E. Barndorff-Nielsen (eds.), Time Series Models in Econometrics, Finance and Other Fields, Chapman & Hall, London, 1–67.

- [25] Skorokhod, A.V. (1989), Asymptotic Methods in the Theory of Stochastic Differential Equations, AMS.

- [26] De Vries, C.G. (1991), On the relation between GARCH and stable processes, J. Econometrics 48, 313–324.

- [27] Walter, G.G. (1994). Wavelets and Other Orthogonal Systems with Applications. CRC Press.

- [28] Walter, G.G. and Zayed, A.I. (1996). Characterization of analytic functions in terms of their wavelet coefficients. Complex Variables 29, 265–276.

- [29] Wand, M.P. (1998), Finite sample performance of deconvolving kernel density estimators, Statist. Probab. Lett. 37, 131–139.

- [30] Wand, M.P. and Jones, M.C. (1995), Kernel Smoothing, Chapman and Hall, London.

- [31] Wiggins, J. B. (1987), Option valuation under stochastic volatility, Journal of Financial Economics 19, 351–372.

- [32] Van Zanten, H. and Zareba, P. (2008), A note on wavelet density deconvolution for weakly dependent data, Stat. Inference Stoch. Process. 11, 207–219.