A CLOSED-FORM APPROXIMATION OF LIKELIHOOD FUNCTIONS FOR

DISCRETELY SAMPLED DIFFUSIONS:

THE EXPONENT EXPANSION

Abstract

In this paper we discuss a closed-form approximation of the likelihood functions of an arbitrary diffusion process. The approximation is based on an exponential ansatz of the transition probability for a finite time step , and a series expansion of the deviation of its logarithm from that of a Gaussian distribution. Through this procedure, dubbed exponent expansion, the transition probability is obtained as a power series in . This becomes asymptotically exact if an increasing number of terms is included, and provides remarkably accurate results even when truncated to the first few (say 3) terms. The coefficients of such expansion can be determined straightforwardly through a recursion, and involve simple one-dimensional integrals.

We present several examples of financial interest, and we compare our results with the state-of-the-art approximation of discretely sampled diffusions [Aït-Sahalia, Journal of Finance 54, 1361 (1999)]. We find that the exponent expansion provides a similar accuracy in most of the cases, but a better behavior in the low-volatility regime. Furthermore the implementation of the present approach turns out to be simpler.

Within the functional integration framework the exponent expansion allows one to obtain remarkably good approximations of the pricing kernels of financial derivatives. This is illustrated with the application to simple path-dependent interest rate derivatives. Finally we discuss how these results can also be used to increase the efficiency of numerical (both deterministic and stochastic) approaches to derivative pricing.

1 INTRODUCTION

Continuous-time diffusion processes is the basis of much of the modeling work performed every day in Finance and Economics, from portfolio optimization and econometric applications, to contingent claim pricing. Indeed, since Bachelier’s 1900 doctoral thesis on the dynamics of stock prices [1], many economic variables subject to unpredictable fluctuations, have been modeled by stochastic differential equations of the form

| (1) |

Here is the drift, describing a deterministic trend, and is the volatility function, describing the level of randomness introduced by the Wiener process (i.e., white noise), . The main reason for the popularity of this class of models is probably that in continuous time one can perform analytic calculations using the instruments of stochastic calculus, and the powerful framework of partial differential equations.

In particular, for the few cases for which the process (1) is exactly solvable, one can derive closed-form solutions for the associated transition probability. The latter contains all the statistical properties of the financial quantity modeled by the diffusion, and can be exploited in a variety of ways, including the derivation of no-arbitrage prices for financial derivatives in complete markets. The milestone results derived by Black, Scholes and Merton [2, 3], Cox, Ingersoll and Ross [4], or Vasicek [6], are among the most significant examples of the amount of progress in Economics that has been done using integrable continuous-time diffusion processes.

Nonetheless, an accurate description of the market observables requires in general more sophisticated models than those for which an analytic solution is available. These are usually tackled by means of numerical schemes ultimately relying on a discretization of the diffusion, obtained by replacing the infinitesimal time with a finite time step, . These approaches typically involve either solving numerically a Kolmogorov partial differential equation, or a Monte Carlo sampling of the diffusive paths. The approximate results obtained in this way become exact only approaching the limit , and this can be done with some computational effort. In addition, a drawback of these numerical methods, more specific to econometric applications, is that they do not produce closed-form expressions for the transition probability. These are crucial for maximum-likelihood estimations of the parameters, say , of model diffusions. In fact, economic data are generally available on discrete sets of observations, usually well spaced in time, say weekly or monthly. As a result, only if the transition probability, , associated with each time interval of the series (), is known in closed form, the maximum likelihood function,

| (2) |

can be analytically maximized over . If this is not the case, one has to repeat the numerical calculation of the transition probability for every value of needed for the determination of the maximum, e.g. by means of an optimization algorithm. This can be clearly very time consuming.

Motivated by this difficulty, Aït-Sahalia recently proposed a method to approximate the transition probability for one dimensional diffusions [7] by means of a Hermite polynomial expansion. This was applied to a variety of test cases, and the accuracy of the method was clearly demonstrated.

In this paper, we utilize the exponent expansion – a technique introduced in chemical physics by Makri and Miller [8] – to derive a closed-form short-time approximation of the transition probability of the diffusion process (1). The aim is to obtain an analytic approximation which is as accurate as possible for a time step as large as possible. On one hand, this allows one to derive approximations of financial quantities that are very accurate even for sizable values of the time step, and to derive closed-form expression for the maximum likelihood function (2). On the other, it allows a reduction of the computational burden of numerical schemes as the limit can be achieved with larger time steps, i.e., with less calculations. Our approach is similar in spirit to the one of Ref. [7], reviewed in Section 2.1, but it overcomes some of its shortcomings, and it is of simpler implementation. In particular, the coefficients of the exponent expansion can be expressed in terms of one dimensional integrals that can be easily calculated numerically. In addition, we show how we can apply our approach to any sufficiently regular volatility function, even when the latter does not have an analytic expression but it is specified numerically through an interpolation procedure, as it is the typically the case for local volatility models.

The possibility to use Makri and Miller’s technique to derive approximations of the transition probability was originally hinted by Bennati et al. in Ref. [9, 10]. Here we explore this route, giving derivations for a generic diffusion process with state-dependent drift and volatility, and we study the reliability of the exponent expansion by applying it to several test problems of financial interest.

Through the exponent expansion, the transition probability is obtained as a power series in which becomes asymptotically exact if an increasing number of terms is included, and provides remarkably accurate results even when truncated to the first few (say, ) terms. Two derivations are offered, the first by means of Kolmogorov’s forward equation [11] (Sec. 2.2), and the second introducing a slightly different formalism (Sec. 2.2.1). The latter, once the problem is formulated in terms of Feynman’s path integrals [12, 13], allows the generalization of the exponent expansion to the calculation of the pricing kernel of financial derivatives whose underlying follows the considered diffusion. This allows in turn the derivation of simple approximations for the price of such contingent claims (Sec. 3). In Sections 2.3 and 3.3, we illustrate the exponent expansion through the application to the Vasicek, the Cox-Ingersoll-Ross, and the Constant Elasticity of Variance models, and in Section 4 we discuss its application to Monte Carlo and deterministic numerical methods within the path integral framework [14, 15, 16, 17, 18, 10]. Finally, we draw our conclusions, and we discuss future developments in Section 6.

2 TRANSITION PROBABILITIES OF DIFFUSION PROCESSES

Let us consider the problem of estimating the transition probability, , associated with one-dimensional continuous-time diffusion processes of the form (1). This represents the likelihood that the random walker following the process (1) ends up in the position at time , given that it was in at time , and satisfies the Kolmogorov forward (or Fokker-Planck) equation [11]:

| (3) |

In this Section we will consider two short-time approximations of the transition probability above that can be derived in closed form. We will start by reviewing the Hermite polynomial expansion, recently introduced by Aït-Sahalia [7], and then describe the exponent expansion.

2.1 Review of the Hermite polynomials expansion

The first step of Aït-Sahalia’s derivation is to transform the original process in an auxiliary one, say , with constant volatility . Following Ref. [7], this can be achieved in general through the following integral transformations

| (4) |

where the choice of the sign is just a matter of convenience depending on the specific problem considered. The latter relation defines a one to one mapping between the and processes as the condition ensures that the function defined by (4) is monotonic, and therefore invertible. 111For a discussion of the regularity conditions on the drift and volatility functions see e.g., Ref. [7]. A straightforward application of Ito’s Lemma [11] allows one to write the diffusion process followed by as

| (5) |

with

| (6) |

where is the inverse of the transformation (4).

Using Hermite polynomials, it is possible to show [7], that a short time approximation of the transition probability can be expressed up to order as

| (7) |

where is a standard normal distribution. Here the coefficients can be derived by solving the recursive equation

| (8) |

for , with , and

| (9) |

Finally, the transition probability for the process can be determined through the Jacobian of the transformation (4) giving

| (10) |

The expansion above turns out to provide very accurate results in a variety of test cases for which the exact expression of the transition probability is available. Some of these examples will be considered in detail in the following when we will compare the results obtained with the approximation Eqs. (7)-(10), with those given by the exponent expansion described in this paper, and introduced in the following Section.

2.2 The Exponent Expansion

In this Section, we derive the exponent expansion for the transition probability for the process (1), . In order to make the derivation easier, it is convenient to transform the original process in the constant volatility one Eq. (5) by means of the transformation (4).

For the transition probability for is dominated by the diffusive Gaussian component and therefore reads:

| (11) |

Guided by this observation, in order to find an expression for the transition probability associated with Eq. (5) which is accurate for a time as long as possible, we make the following ansatz:

| (12) |

Such transition probability must satisfy the Kolmogorov forward equation [11]:

| (13) |

Note that since the auxiliary process has a constant volatility, the latter equation is mathematically much simpler than the one for the process (3). Equation (13) implies in turn that the function satisfies the relation:

| (14) |

Expanding in powers of ,

| (15) |

substituting it in Eq. (14), and equating equal powers of leads in a straightforward way to a decoupled equation for the order zero in giving

| (16) |

and to the following set of recursive differential equations:

| (17) | |||||

In particular, for Eqs. (17) read:

| (18) | |||||

| (19) | |||||

| (20) | |||||

The differential equations above (17) are all first order, linear and inhomogeneous of the form

| (21) |

where is a function that is completely determined by the first relations. It can be readily verified by substitution and integration by parts that the solution of (21) reads

| (22) |

This, for , after some manipulations, gives:

| (23) | |||||

| (24) | |||||

| (25) | |||||

where , and, for reasons that will be clearer in the next Section, we have also introduced the ‘effective potential’ as the following quantity with dimension :

| (26) |

Note that, from Eq. (9), . The first order correction can be rewritten as

| (27) |

leading to the interpretation of this term as a time-average of the effective potential over the straight line, constant velocity () trajectory between and . Similarly, the leading term in (i.e., the one proportional to the lowest power of the volatility) is proportional to the variance of the effective potential over the same trajectory. Note that the corrections are well defined in the limit . In particular, for it is not difficult to show that

| (28) | |||||

| (29) | |||||

| (30) |

Finally, the transition probability of the original diffusion (1) is recovered by means of the Jacobian transformation (10).

The form of the trial transition probability represents the main difference of the present approach to the one described in Section 2.1 Ref. [7], which is otherwise very similar in spirit. In fact, the latter expands in powers of the exponential rather then just the exponent, as we do here, instead. As it will be shown explicitly in the following, the present choice gives rise to a distinct approximation scheme for providing generally a similar level of accuracy but remarkably simpler mathematical expressions. In particular, all the calculations related to the test cases presented in the following Sections have been easily obtained by hand, i.e., without the aid of symbolic calculation computer programs. This is because, by keeping the exponential form of the ansatz, one formulates a guess which is closer to the exact one. The latter, can be expected to have an exponential form in order to satisfy the Chapman-Kolmogorov property of Markov processes [11]. In addition, the exponential choice of the ansatz automatically enforces the positive definiteness of the transition density which is not granted in the approach of Ref. [7]. In fact, as it will be shown explicitly in Sec. 2.3, in the limit of very small volatility (), when the effect of the noise disappears, and the transition density converges to a Dirac’s distribution, the expansion of Ref. [7] breaks down as the transition probability becomes negative. On the contrary, the exponent expansion remains well defined and accurate also in this limit. Indeed, the first terms of the expansion in can be also derived through a small volatility expansion of the transition density, as it will be discussed in Sec. 3.1.

Similarly to the approximation developed in Ref. [7], the exponent expansion has in general a finite convergence radius which is a decreasing function of the volatility. As it will be shown in the following, for the values of volatilities and relevant for financial applications the exponent expansion turns out to be very accurate even when truncated to the first few terms.

2.2.1 Alternative derivation

The term in the exponent expansion is somewhat different from the higher order terms. In fact, it is defined by Eq. (16) which is decoupled from the recursive system (17). Indeed, it is possible to obtain the same result for the exponent expansion by expressing the transition density as

| (31) |

and looking for an approximate expansion of the form (12) for . It is easy to show by direct substitution in the forward Kolmogorov equation (13) that is the solution of

| (32) |

where is the “Hamiltonian” differential operator

| (33) |

and is the effective potential of Eq. (26). As a result one can equivalently derive the exponent expansion by substituting in Eq. (32) the following trial function

| (34) |

which does not contain the term . This observation will be used in Section 3 to generalize the exponent expansion to the pricing kernel of financial derivatives.

2.2.2 Exponent Expansion Coefficients in terms of the the Original Diffusion

The derivations of the exponent expansion, and of the Hermite polynomial approximation of Section 2.1, both rely on the introduction of the auxiliary process (5), and the integral transformation (4). As a result, the expressions obtained are easy to handle if the the volatility of the original process is such that both the function (4) and its inverse admit a closed-form expression. In fact, in this case the effective potential (26) – or the function (9) – has a closed-form expression, and the determination of the coefficients of the expansion can be determined either analytically or through numerical quadrature. This is the case for the examples considered in the following. However, these are very special cases. In fact, very few volatility functions have a reciprocal for which a primitive exist. On the contrary, in many practical applications, e.g. in local volatility models [5], the volatility is specified numerically through a fit to an volatility function. For all these cases the application of the exponent expansion or the approach of Section 2.1 becomes cumbersome and computationally demanding, because it requires the numerical inversion of the integral equation (4).

However, at a more careful analysis, it turns out that it is possible to circumvent this difficulty, and to eliminate any dependence on the function in the expressions for the exponent expansion. This makes its application straightforward for any diffusion process, irrespective of the analytic tractability of the specified volatility function. The first step to do this, is to note that, according to the Jacobian transformation (10), and in Eq. (12) need to be calculated for , and , respectively. As a result, one can express the exponent expansion as

| (35) |

with the notation

| (36) |

and taking, without any loss of generality . Now, using Eq. (16), by means of the change of variables one can express the zeroth order term as

where, using Eq. (6),

| (37) |

As anticipated, the expression for does not contain any reference to the function so that it can be calculated even if there is no closed-form expression for available, or if the latter is not analytically invertible. Similarly, using Eqs. (23)-(25) one can easily find

| (38) | |||||

| (39) | |||||

| (40) | |||||

where , and the effective potential now reads

| (41) |

As a result, the exponent expansion can be easily applied for any specification of the volatility function . Indeed, given any drift and volatility function one can immediately calculate – possibly numerically – their derivatives and the function . From these quantities, one then easily calculates the effective potential (41), and the coefficients of the exponent expansion (38)-(40).

2.3 Examples

The application of the exponent expansion to a generic diffusion process of the form (1) is rather straightforward and reduces to the calculation of one dimensional integrals. In this Section, we illustrate this procedure for a few test cases, namely for the Vasicek [6], the Cox-Ingersoll-Ross [4], and the Constant Elasticity of Variance [19] diffusion processes. We will compare the results of the exponent expansion with the exact results available in literature, and with the approach of Ref.[7].

2.3.1 Vasicek diffusion

We first consider the Ornstein-Uhlenbeck diffusion proposed by Vasicek [6] as a model for the short-term interest rate:

| (42) |

where , , and are positive constants representing the mean-reversion level, the velocity to mean reversion, and the volatility, respectively. This model is integrable and the corresponding probability density function is Gaussian:

| (43) |

with

| (44) |

The exponent expansion of the Vasicek model can be easily derived using Eqs. (16), and (23-25) with the effective potential, Eq. (26),

| (45) |

and gives,

| (46) | |||||

up to the third order in (). Here

| (47) | |||||

| (48) | |||||

| (49) | |||||

| (50) | |||||

with . It is interesting to note that the approximate transition probability obtained with the present approach reproduces exactly the expansion of the exact transition density Eq. (43) at the same order.

On the other hand, the first two coefficients of the Hermite polynomials expansion (7) as quoted in Ref. [7] read:

| (51) | |||||

| (52) | |||||

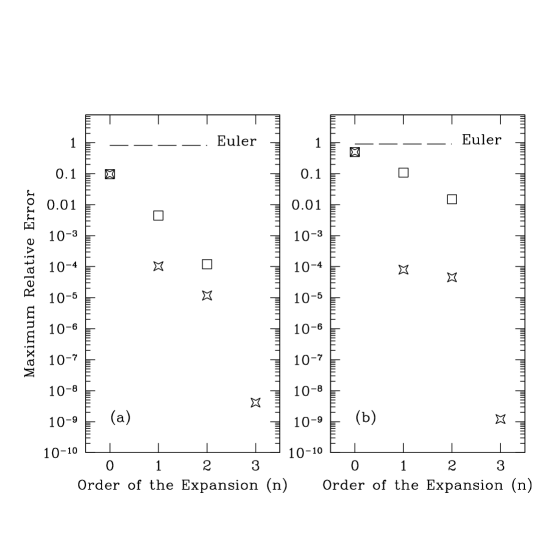

The fast convergence of the approximation scheme is illustrated in Figs. 12. Here the percentage error of the exponent expansion with respect to the exact result (43) is plotted for various , and compared with the approach of Ref. [7]. The parameter choice, also taken from Ref. [7] corresponds to a sensible parameterization for interest rate markets. We adopt one year as unit of time, and we express the various parameters in this unit. The Euler approximation

| (53) |

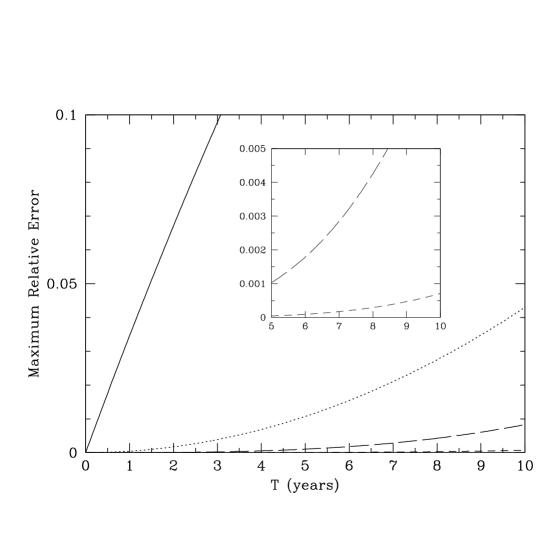

is also reported for comparison. The inclusion of each successive order allows one to increase dramatically the accuracy of the approximation so that the third order expansion has basically a negligible error even for a sizable time step of order 6 months. Remarkably, for the considered example, the third order expansion allows one to estimate the 10 years transition probability with a relative error of less than 10 basis points (Fig. 2). As illustrated in Fig. 1-(a), in the present case the approach of Ref. [7] provides a slightly poorer level of accuracy for . In addition, it generally produces more complicated mathematical expressions. Furthermore, as shown in Fig. 1-(b), in the regime of small volatility the exponent expansion still provides accurate results while the performance of the approach of Ref. [7] degrades. In fact, as anticipated, in the limit of small volatility () the first order correction of the latter approach produces a negative transition probability signaling a break down of the scheme.

2.3.2 Cox, Ingersoll and Ross diffusion

The Vasicek model is probably too easy of a test case as the associated transition probability is Gaussian. In fact, since the exponent expansion has a leading term which is Gaussian, the higher powers in just have to renormalize its average and variance in order to reproduce the exact result. It is interesting therefore to test the accuracy of the exponent expansion for a diffusion process that, while still integrable, generates a non-normal transition density. This is the case for the Feller’s square root process [20]

| (54) |

which is the basis of Cox-Ingersoll-Ross model for the instantaneous interest rate [4]. The exact transition probability is given by [4]

| (55) |

where , , , and is the modified Bessel function of the first kind of order [21].

As explained in Sec.2.2, since the volatility is not uniform, it is convenient to introduce the auxiliary process defined by Eq. (4), as . The process follows Eq. (5), with and

| (56) |

and . In this case the effective potential reads:

| (57) |

and the first four terms of the exponent expansion in Eq. (15) are:

| (58) | |||||

| (59) | |||||

| (60) | |||||

| (61) | |||||

where , , and

| (62) |

and , , . Finally, going back to the original process with Eq. (10), the transition probability reads:

| (63) |

The coefficients of the expansion in Hermite polynomials Eq. (7) as quoted in Ref. [7] read instead:

| (64) | |||||

| (65) | |||||

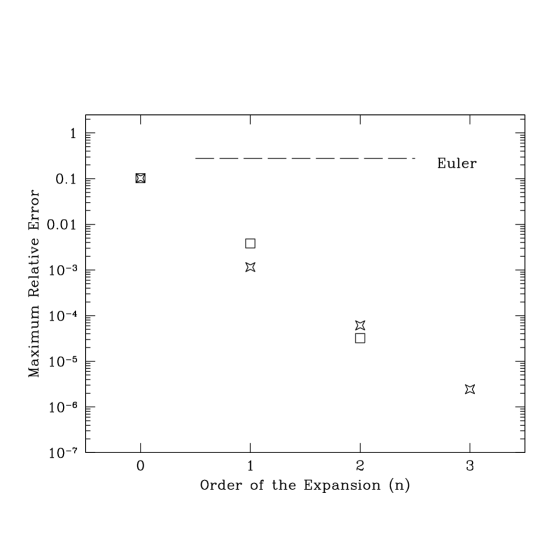

The accuracy of the exponent expansion in this case is illustrated in Figs. 3 and 4. Similarly to the case of the Vasicek diffusion, the exponent expansion is characterized by a remarkably fast convergence by including successive terms of the approximation so that provides already a virtually exact representation of the transition density, for . In this case, the approach of Ref. [7] performs slightly worse of the exponent expansion for , and slightly better for . However, also in this case the former breaks down for small values of the volatility, generating unphysical transition densities.

2.3.3 Constant Elasticity of Variance diffusion

As a last example we consider the Constant Elasticity of Variance model:

| (66) |

Here we consider for brevity only the case . The transformation to a process with constant (unit) variance is and gives, according to Eq. (6)

| (67) |

with , , and . In this case the effective potential reads

| (68) |

and the first three terms of the expansion are:

| (69) | |||||

| (70) | |||||

| (71) |

with

| (72) | |||||

Similarly to the examples considered previously, also for the Constant Elasticity of Variance model we find a very fast convergence of the exponent expansion for , and a performance generally similar to the one of the approach of Ref. [7], for values of the volatility large enough.

3 PRICING KERNELS OF CONTINGENT CLAIMS

3.1 Path integral formulation

The exponent expansion can be generalized to obtain an approximation of the pricing kernels of ‘standard’ derivatives. This can be done by formulating the pricing problem within Feynman’s path integral framework [9, 10]. Here we indicate as ‘standard’ any contingent claim written on the underlying, , whose value at time , , can be expressed as an expectation value of a functional of a certain type, namely

| (73) |

where

| (74) |

and is a payout function. Above is the time to expiry, and the expectation value is performed with respect to the probability measure defined by the diffusion for that we assume of the form (1). European Vanilla options, zero coupon bonds, caplets, and floorets clearly belong to this family of contingent claims. In addition, other path-dependent derivatives, like barrier or Asian options can be expressed in this form (see e.g., Refs. [23, 24]).

Similarly to the case of the transition probability, it is in general convenient to introduce an auxiliary diffusion with constant volatility of the form (5) by means of the integral transformations (4). Then, the expectation value in (73) can be transformed in an integral over the distribution generated by such auxiliary diffusion by means of the usual Jacobian transformation (10). As a result, the value of the option can be in general written as:

| (75) |

where is the domain of the auxiliary process as defined by the relative stochastic differential equation (5), and is the pricing kernel. The latter can be expressed in terms of a path integral as it follows[9, 10]

| (76) |

with

| (77) |

where is given by Eq. (16) and the functional is the effective Euclidean Lagrangian

| (78) |

() with the effective potential, , defined as:

| (79) |

Finally, the measure is defined by discretizing each path connecting and . This can be done by dividing the time interval into intervals so that ( with ), and by integrating the internal variables over the domain . The path integral is then obtained as the limit for of this procedure, namely

| (80) |

It is well known form the physical sciences that the path integral satisfies the partial differential equation Eq. (32) [12, 13]. Note that this is consistent with the fact that, by definition, for the pricing kernel coincides with the transition density of the underlying diffusion process for . In particular, as observed in Sec. 2.2.1, one can use Eq. (32) to derive the exponent expansion for using the trial form (34). As a result, the same expressions Eqs.(23-25) derived for the transition density hold true also for the pricing kernel, provided that the effective potential (79) replaces the one in Eq. (26).

3.2 Correspondence with Quantum Mechanics

It is interesting to note that the path integral formulation of the pricing kernel (77) is mathematically equivalent to the quantum mechanical description of the thermodynamic properties of an ideal gas of particles moving in the potential ( is the reduced Planck’s constant giving the correct energy dimensions). The complete correspondence is obtained by identifying and where is the mass of the particle, is the temperature, and is the Boltzmann constant. With this prescription, becomes the so-called single particle density matrix, and the results of Makri and Miller [8] can be readily recovered. In addition, it is straightforward to show using Eqs. (30) that the exponent expansion of its diagonal elements, , are consistent with the so called Wigner expansion for the high-temperature limit. Finally, performing the analytic continuation known as Wick rotation allows one to obtain the single-particle quantum propagator. In this case (32) becomes the celebrated Schrödinger equation.

This correspondence provides an alternative justification of the choice of the exponential ansatz in Eq. (12). Indeed, this is the form in which can be expressed in general the quantum mechanical propagator or the single particle density matrix [12, 13]. Furthermore, it has been shown for the quantum problem [22] that the exponent expansion up to third order in and first order in can be derived starting from the short time semiclassical propagator obtained through a saddle point analysis of the limit [25]. Indeed, it can be shown that the second order correction , Eq. (24), is the so-called van-Vleck determinant of the saddle point expansion. This explains why the accuracy of the present scheme is preserved in the corresponding regime of low volatility, as it was anticipated in Sec.2.2, and illustrated in Sec.2.3.

3.3 An example: Zero Coupon Bond

In this Section we illustrate the prescriptions outlined above by applying the exponent expansion to the calculation of a zero coupon bond within the Vasicek and Cox-Ingersoll-Ross models. The zero coupon bond is a financial instrument that provides at time a payout of one unit of a certain notional. Its value at time can be expressed therefore as

| (81) |

which is of the standard form given by Eqs. (73) and (74), with , and .

As a result, the exponent expansion for the kernel Eq. (76) can be easily derived giving for the Vasicek model

| (82) | |||||

| (83) | |||||

| (84) |

where are the expressions obtained for the transition probability Eqs. (47)-(50) of Sec. 2.3.1. For the Cox-Ingersoll-Ross model instead we get:

| (85) | |||||

| (86) |

with given by Eqs. (58)-(60), and related to the previous quantities as in Eq. (61) with

| (87) |

as in Eq. (62), and . The exponent expansion for the pricing kernel can be compared with the exact results that can be shown to read for the Vasicek model (42)

| (88) | |||||

with given by Eq. (44), and

| (89) |

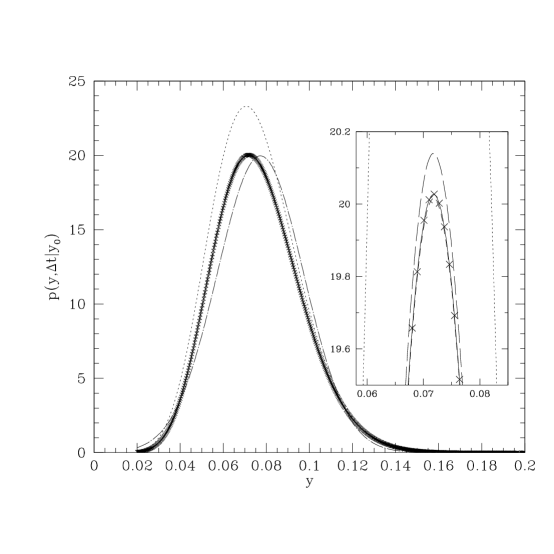

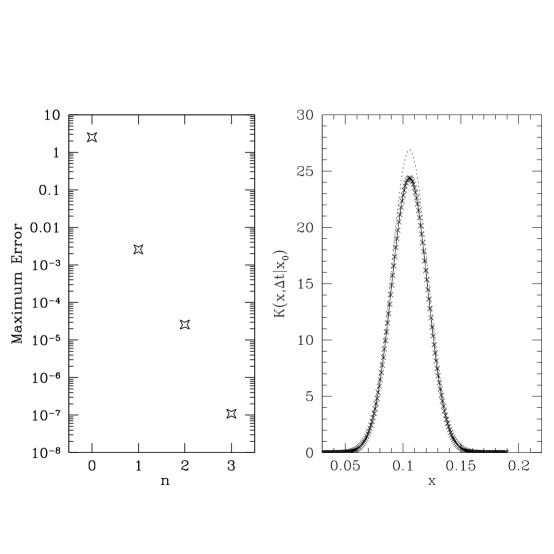

with , for the Cox-Ingersoll-Ross one. As illustrated in Fig.5, similarly to the case of the transition probability, the exponent expansion provides a remarkably good, and fast converging approximation of the exact pricing kernel for financially sensible parameterizations, and for a sizable value of the time step .

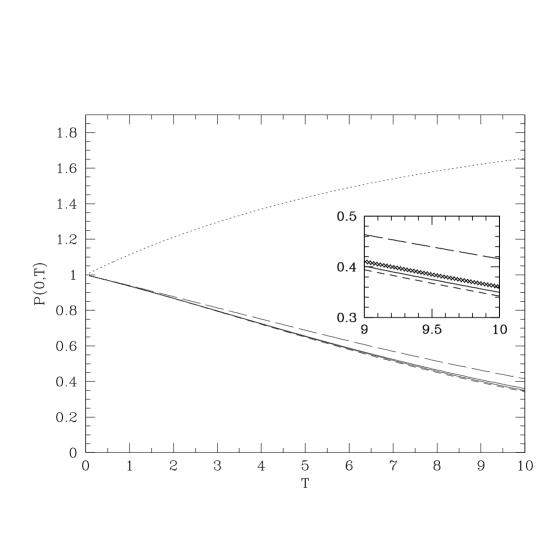

Finally, the zero coupon bond can be obtained by numerical integration of the pricing kernel according to Eq. (75). The corresponding results are shown in Fig. 6 confirming once more the quality of the approximation. In a similar fashion, one can obtain systematic approximations for caplets, floorets, and other simple interest rate derivatives whose value depends only on the value of the instantaneous short rate at time . It is also possible to generalize this approach to path dependent contingent claims, like Asian options.

4 EXTENDING THE TIME STEP: PATH INTEGRAL MONTE CARLO METHODS

For an extended time interval , the calculation of the transition density or, more in general, of the pricing kernel (76) can be performed by discretizing the path integral (77), and taking the limit of large number of time slices () according to the standard Trotter product formula:

| (90) | |||||

with , , and the effective potential given by Eq. (79). It is worth remarking that, for the case of the transition density, by interpreting the latter equation as the Chapman-Kolmogorov property of Markov processes [11] one obtains the following approximation of the short-time propagator

| (91) |

However, in contrast to the exponent expansion, the latter expression is not strictly correct up to order , and only in the limit the difference becomes negligible.

In general, to obtain an accurate result for the pricing kernel for an extended time period one has to increase the number of time slices, or Trotter number , until convergence is achieved. By replacing the Trotter formula with the improved short-time kernel obtained through the exponent expansion (12) one achieves a faster convergence with the Trotter number, thus significantly reducing the computational burden. In this case the finite-time expression of the pricing kernel reads

| (92) | |||||

with given by Eq. (15).

Equation (92) allows one to obtain the transition density or the pricing kernel for a standard derivative through the calculation of a multidimensional integral over the variables . The latter integration is ideally suited for Monte Carlo methods either in real, or in Fourier space [26], the specific choice depending on the particular problem at hand. In addition, importance-sampling schemes, e.g., by means of the Metropolis algorithm [27], can be easily applied in order to reduce the computation time. However, in order not to introduce a systematic bias in the result a particular attention has to be paid in order to sample accurately the configuration space.

The most straightforward way to perform a Monte Carlo quadrature of Eq. (92), is to realize that a simple Markov chain

| (93) |

with , sampled from a standard normal distribution, generates an ensemble of walkers distributed according to

| (94) |

As a result, the pricing kernel (92) can be obtained as the average over the random paths generated according to Eq. (93) of the following estimator:

| (95) |

A remarkable property of the path integral approach is that for any final point can be evaluated with a single Monte Carlo simulation by appropriately reweighting the accumulated estimator. In fact the distribution of walkers is independent of the final point so that can be calculated by averaging . In addition, the latter quantity can be efficiently obtained by means of the following reweighting procedure

| (96) |

with

| (97) |

Expectation values of the form (75) on a time horizon can be calculated by integrating over the final variable giving:

| (98) | |||||

This can be simulated by extending the Markov chain (93) up to step , and accumulating the estimator

| (99) |

Remarkably, within the path integral approach, the sensitivities of such expectation values with respect to the model parameters (the so-called Greeks) can be computed in the same Monte Carlo simulation, thus avoiding any numerical differentiation. Indeed, indicating with a generic parameter, under quite general conditions [28], one has

| (100) |

As a result the sensitivity can be calculated by means of the estimator:

| (101) |

Higher order sensitivities can be obtained in a similar fashion.

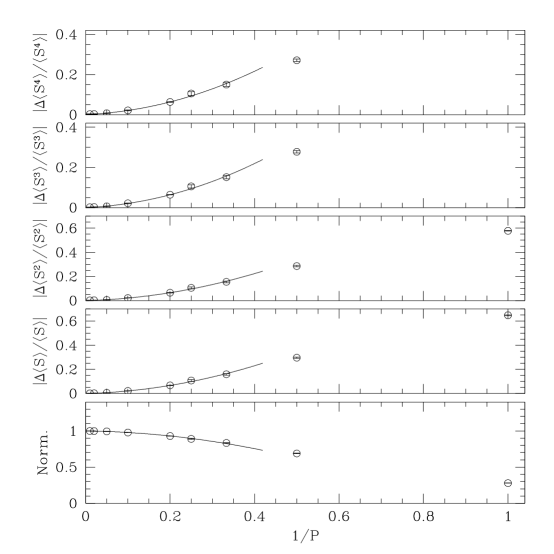

The convergence with the Trotter number of the path integral Monte Carlo estimates is illustrated in Fig. 7 for the calculation of the first five moments of the transition probability of the Cox-Ingersoll-Ross model (54). The finite estimates converge very rapidly with . In particular, for the case considered, already provides estimates in agreement with the exact result within statistical uncertainties. In general, as also shown in the figure, a convenient indicator of the convergence is the zeroth-moment or normalization of the distribution. The calculation of this quantity allows in general to assess the level of convergence without performing a complete scaling with , thus saving computational time.

5 EXTENDING THE TIME STEP: GREEN’S FUNCTION BACKWARD INDUCTION

The Green’s function backward induction is a deterministic approach alternative to partial differential equation methods, introduced in financial context by Rosa-Clot and Taddei [10]. This is based on the path integral representation of standard contingent claims (73), that we rewrite here for convenience as

| (102) |

Here is the payout functional dependent on the realization of the path of the underlying up to expiry , and is the general process following the diffusion (1). As partial differential methods, the Green’s function backward induction is efficient for low-dimensional problems but allows one to include naturally early exercise features in the contingent claim, i.e., to treat expectation values of the form

| (103) |

where is the stopping time of the process [11].

For standard contingent claims, Eqs. (73) and (74), the functional can be discretized in the form,

| (104) |

and the conditional expectation value (102) is given by

| (105) |

where the function, , is

| (106) |

and is the transition probability associated with the process (1). This is the Green’s function of the partial differential equation associated with the calculation of the expectation value (102), hence the name of the method.

Let us now consider a single integration

| (107) |

If we approximate this integral by using a numerical quadrature rule, we obtain the following algebraic relation

| (108) |

where the matrices, , are defined by

| (109) |

the quantities, , and , are the weights and the grid points, respectively, associated with the integration rule, and . In conclusion, the expression (105) can be written as

| (110) |

where , and . Therefore, we have reduced the evaluation of the expectation value of a functional to the product of matrices with dimension . By starting the calculation from the right (backward induction), we need to memorize just linear arrays, while the matrix elements, , can be computed step by step. In practice, one can follow the following algorithm:

-

i.

Set (), and .

-

ii.

Set ().

-

iii.

If then set (), , and go to ii.

Here the arrays, , and , are two working vectors.

The inclusion of early exercise features is completely straightforward and simply involves the following steps:

-

i.

Set (), and .

-

ii.

Set , and

().

-

iii.

If then set (), , and go to ii.

The only difference is in the point ii, where we have now a test operation, and the function is the exercise value of the option.

The exponent expansion can significatively speed up the Green’s function backward induction presented above. In fact, as illustrated in the previous Sections, it allows one obtain reliable approximations of for a time step much larger than those that can be safely used with a simple Euler discretization. As a result, one can reduce the discretization bias to acceptable levels with a much smaller number of intermediate time steps . The application of this procedure to local volatility models is currently in progress and will be presented elsewhere [29].

6 CONCLUSIONS

Closed-form approximations of non-liner diffusions are of primary importance in a variety of fields of quantitative Finance. In Econometrics, they are crucial for an efficient maximum likelihood estimation of the parameters of continuous time processes. In derivative pricing, they allow one to develop effective approximation schemes or to improve the efficiency of numerical approaches.

In this paper we have presented an effective method to produce a family of closed-form approximations of the transition probability of a general diffusion process. Such approximation, dubbed exponent expansion, is based on an exponential ansatz of the transition probability for a finite time interval , and a series expansion of the deviation of its logarithm from that of a Gaussian distribution. Through this procedure the transition probability is obtained as a power series in which becomes asymptotically exact if an increasing number of terms is included, and provides remarkably accurate results even when truncated to the first few (say 3) terms. This approach can be easily implemented, and involves the calculation of simple one dimensional integrals. In addition, it applies to a very wide class of volatility functions, even to those that do not have a simple analytic expression but they are specified through a numerical interpolation.

We have shown that the exponent expansion produces very accurate results for integrable diffusions of financial interest, like the Vasicek and the Cox-Ingersoll-Ross models. In particular, we have compared our results with those obtained with the state-of-the-art approximation of discretely sampled diffusions [7], that shares a similar rationale. We find that the exponent expansion provides a similar accuracy in most of the cases but it is more stable in the low-volatility regimes. Furthermore the implementation of the exponent expansion turns out to be simpler.

By introducing a path integral framework we have generalized the exponent expansion to the calculation of the pricing kernels of financial derivatives, and we have shown how to obtain accurate approximations for the price of simple contingent claims. We have also shown how the exponent expansion can be naturally used to increase the efficiency of both deterministic and stochastic numerical simulations. A systematic study of the efficiency of this approach for the pricing of exotic derivatives, and the calibration of local and stochastic volatility models will be the object of future investigations.

Acknowledgments It is a pleasure to thank Gabriele Cipriani for sparking my interest in the path integral approach to option pricing, and for continuous stimulating discussions. I would also like to thank Marco Rosa-Clot for kindly sharing with me a series of unpublished results.

References

- [1] L. Bachelier, Theorie de la Spéculation, Annales de l’Ecole Normale Supérieure (1900).

- [2] F. Black and M. Scholes, The Pricing of Options and Corporate Liabilities, Journal of Political Economy 81 (1973) 637-45.

- [3] R. C Merton, Theory of Rational Option Pricing, Bell Journal of Economics 4 (1973) 141-183.

- [4] J.C. Cox, J.E. Ingersoll, and S.A. Ross, A Theory of the Term Structure of Interest Rates, Econometrica 53 (1985) 385-408.

- [5] B. Dupire, Pricing with a Smile, Risk 7 18-20 (1994).

- [6] O. Vasicek, An equilibrium Characterization of the Term Structure, Journal of Financial Economics 5 (1977) 177-188.

- [7] Y. Aït Sahalia, Transition Densities for Interest Rate and Other Nonlinear Diffusions, Journal of Finance 54 (1999) 1361-1395.

- [8] N. Makri and W.H. Miller, Exponential Power Series Expansion for the Quantum Time Evolution Operator, Journal of Chemical Physics 90 (1989) 904-911.

- [9] M. Bennati, M. Rosa-Clot, and S. Taddei, A Path Integral Approach to Derivative Security Pricing I: General Method and Analytical Results, International Journal of Theoretical and Applied Finance 2 (1999) 381-407.

- [10] M. Rosa-Clot, and S. Taddei, A Path Integral Approach to Derivative Security Pricing II: Numerical Results, International Journal of Theoretical and Applied Finance 5 (2002) 123-146.

- [11] S. E. Shreve, Stochastic Calculus for Finance (Springer-Verlag, New York, 2004).

- [12] R. P. Feynman, Space-Time Approach to Non-Relativistic Quantum Mechanics, Review of Modern Physics 20 (1948) 367-387.

- [13] R. P. Feynman and A. R. Hibbs, Quantum Mechanics (McGraw-Hill, New York, 1965).

- [14] G. Montagna, O. Nicrosini, and N. Moreni, A Path Integral Way to Option Pricing, Physica A 310 (2002) 450-466.

- [15] G. Bormetti, G. Montagna, N. Moreni, and N. Nicrosini, Pricing Exotic Options in a Path Integral Approach, Quantitative Finance 6 (2006) 55-66.

- [16] B.E. Baaquie, C. Corianò, and M. Srikant, Hamiltonian and Potentials in Derivative Pricing Models: Exact Results and Lattice Simulations, Physica A 334 (2004) 531-557.

- [17] A. Matacz, Path Dependent Option Pricing: the Path Integral Partial Averaging Method, e.print arXiv:cond-mat/0005319 (2000).

- [18] J. W. Dash, Quantitative Finance and Risk Management: a Physicist’s approach (World Scientific, Singapore, 2004).

- [19] J. C. Cox and S. A. Ross, The Valuation of Options for Alternative Stochastic Processes, Journal of Financial Economics 3 (1976) 145-166.

- [20] W. Feller, The Parabolic Differential Equations and the Associated Semi-Groups of Transformations, Annals of Mathematics 55 (1952) 468-519.

- [21] M. Abramovitz, I. A. Stegun, Handbook of Mathematical Functions (National Bureau of Standards, Applied Mathematics Series, 1965).

- [22] N. Makri and W.H. Miller, Correct Short Time Propagator for Feynman Path Integration by Power Series Expansion in , Chemical Physics Letters 151 (1989) 1-8.

- [23] B. E. Baaquie, Quantum Finance (Cambridge University Press, 2004).

- [24] V. Linetsky, The Path Integral Approach to Financial Modeling and Options Pricing, Computational Economics 11 (1998) 129-163.

- [25] L.S. Schulman, Techniques and applications of path integration (Wiley, New York, 1981).

- [26] R.D. Coalson, On the Connection between Fourier Coefficient and Discretized Cartesian Path Integration, Journal of Chemical Physics 85 (1986) 926-936.

- [27] N. Metropolis, A.W. Rosenbluth, M.N. Rosenbluth, H. Teller, and E. Teller, Equation of State Calculations by Fast Computing Machines, Journal of Chemical Physics 21 (1953) 1087-1092.

- [28] P. Glasserman, Monte Carlo Methods in Financial Engineering (Springer-Verlag, New York, 2004).

- [29] L. Capriotti, in preparation.