Power Law in Firms Bankruptcy

Abstract

We consider the scaling behaviors for fluctuations of the number of Korean firms bankrupted in the period from August 1 2002 to October 28 2003. We observe a power law for the distribution of the number of the bankrupted firms. The Pareto exponent is close to unity. We also consider the daily increments of the number of firms bankrupted. The probability distribution of the daily increments for the firms bankrupted follows the Gaussian distribution in central part and has a fat tail. The tail parts of the probability distribution of the daily increments for the firms bankrupted follow a power law.

keywords:

Econophysics , Zipf law , Bankruptcy , Stock market , Self-organized criticality ,PACS:

05.45.Tp , 89.65.-s , 89.75.-k ,Zipf law is appeared in many natural and social systems such as the distribution of city sizes, the size of earthquakes, moon craters, solar flares, the intensity of wars, the frequency of use in any human language, the sales of books, the number of species in biological taxa[1, 2, 3, 4, 5, 6, 7, 8]. In Zipf law or Pareto law, the distribution or histogram follows a power law, where is a Pareto exponent.

Zipf law has also been reported in economic systems such as the income distribution of companies, the sales of books and almost every other bounded commodity, the distribution of bank assets, and the distribution of firm’s debt when the company is bankrupted[9, 10, 11, 12, 13, 14, 15, 16]. Fujiwara has reported the Zipf law in firms bankrupted in Japan. He found a power law, with for the cumulative distribution of firm’s debt[9]. Okuyama and Takayasu reported Zipf law with a Pareto exponent for the income distribution of Japanese companies[10]. Aoyama et al. analyzed the distribution of income and income tax of individuals in Japan. They observed the power law with the Pareto exponent [11]. Ishkawa reported the income distribution in Japan. He observed Pareto law with the Pareto index for the income distribution of companies[12].

We observe the power law for the distribution of the number of firms bankrupted. The Pareto exponent is close to unity. We also observe the power law for daily increments of the firms bankrupted.

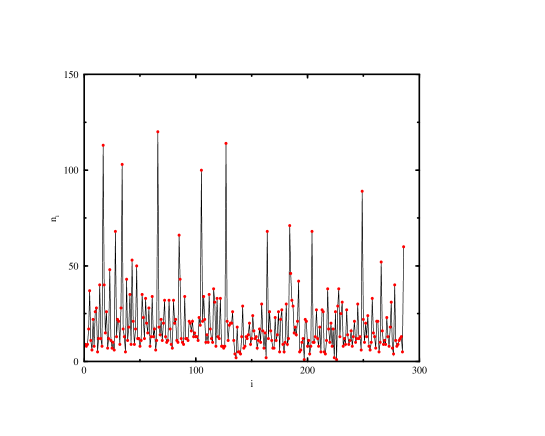

We consider the firms bankrupted in Korea in the period from August 1 2002 to October 28 2003[17]. The total number of the recorded date are 286 days. We deleted the weekends and holidays from the time series. We count the number of daily bankrupted firms. Let be the number of the firms bankrupted at date . Fig. 1 presents the number of the firms bankrupted as a function of the date . The time series of the firms bankrupted show many big peaks. We can observe that the number of the bankruptcies is increased before the big crash. The average number of the firms bankrupted is and the standard deviation is .

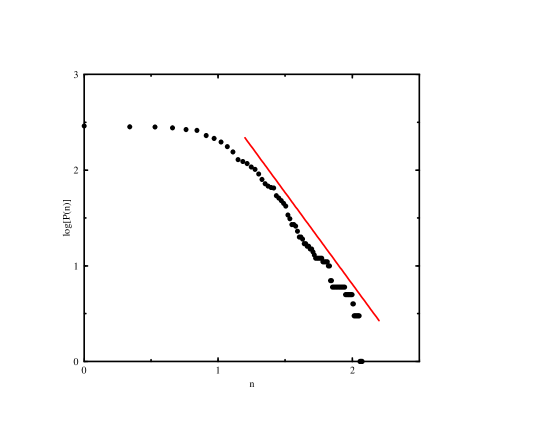

Consider the probability distribution for the number of the firms bankrupted. We expect the power law at the large ,

| (1) |

When the probability distribution follows the power law, the cumulative probability distribution also shows the power law as

| (2) |

where is a Pareto index.

Fig. 2 presents a log-log plot of the cumulative probability distribution for the number of the firms bankrupted. We observe the obvious power law and obtain the Pareto index by a least-square fit. The number of the firms bankrupted shows the Zipf law. This Pareto index is compared to the Pareto index for the distribution of firm’s debt when the firm was bankrupted in Japan[9].

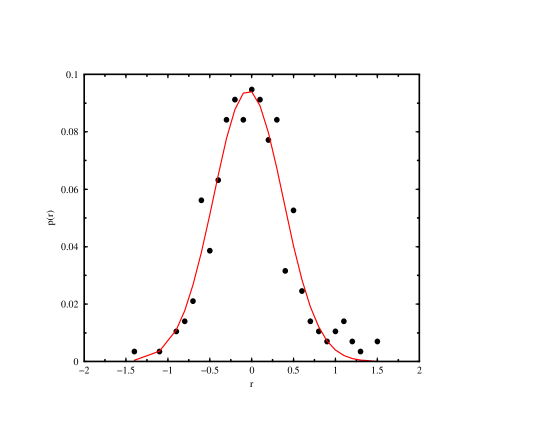

We also consider increments of the number of firms bankrupted defined by

| (3) |

The increments is similar to the return in the analysis of the financial time series such as stock index[1]. Fig. 3 presents the probability distribution for the increments of the number of the firms bankrupted. The probability distribution is well fitted by a Gaussian function in the central parts and deviates from the Gaussian at the tail parts. However, our observations are limited results due to the small number of the data sets.

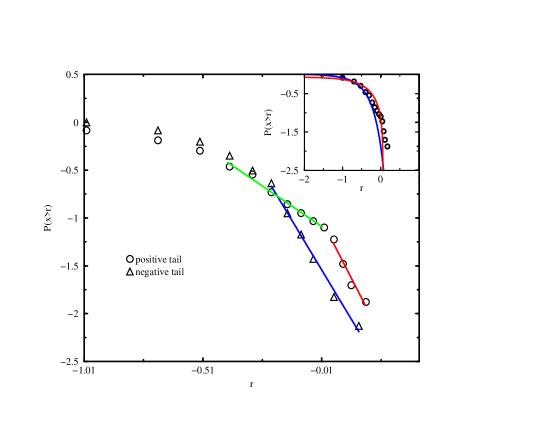

Fig. 4 presents the log-log plot of the cumulative probability distribution as a function of increment . We observe the power law, for the positive and negative tails. For the positive tail we observe two scaling regions with the slopes and . In the inset of Fig. 4 we observe that the cumulative probability distribution deviates from the Gaussian fit at large increments. For the negative tail we observe a single scaling region with the slope . The scaling exponents are compared to the scaling behaviors for the increment of the daily volume in Tokyo stock exchange. Kaijoji and Nuki reported the exponent (positive tail) and (negative tail) for increments of volume in Tokyo stock exchange[18].

Let’s consider the independence of the successive values . We change the variable as . If the pdf of is , the pdf of the variable is given by by the transformation of the probability distribution. If successive values of are uncorrelated, i.e. , the pdf of is simply obtained by a convolution. We obtain the pdf of the varialbe as . In the inset of Fig. 4 we present the pdf, with . At the small values of the data are well fitted by the exponential distribution function. However, in the large value of the data deviate from the exponential distribution. We conclude that there are long range correlations at the parts of the power-law tail. Long range correlations are an origin of the power-law in the probability distribution of firms bankrupted.

Fujiwara propsed a model for the dynamics of balance and sheets of a bank and firms[9]. He observed a power law for the probability distribution of debts bankrupted. However, his model is not involved to the network relations between firms. Aleksiejuk et al. propsed a model of collective bank bankruptcies[20]. In their model banks are located on a lattice. Banks with surpluses tend to invest their money, whereas banks with shortfalls borrow money from the nearest neighbor bank. Above three dimension the distribution of avalanches for bank bankrupted follows the power law, with where is the size of avalanche.

The bankruptcies are a complicated phenomena in economics. Failure of a firm is caused by the internal and external factors of the firms. The effects of a bankruptcy of a firm propagate through the network of creditor-debtor. The creditors are perturbed by the firm bankrupted. The bankruptcy induces some chain reactions to the market and economic systems. If the effects of the bankruptcy are weak, the market absorbs the perturbations and recovers from the damages. However, if the effects are strong, secondary bankruptcies are induced. The chain reactions of the bankruptcy are created. The number of firms bankrupted in the chain reactions is similar to the number of toppled sites in avalanche of the sand pile[19]. The herding dynamics is a reason for the scaling behavior in the bankruptcies.

We consider the scaling properties of the distribution of fluctuations in the number of firms bankrupted in Korea. We observe the power law distribution of the number of firms bankrupted. The Pareto exponent is close to unity. This Pareto exponent is similar ot Fujiwara’s result for the distribution of debt of bankrupted firms. We also observe the power law for increments of the number of firms bankrupted. The distribution of increments has the different scaling exponents for positive and negative tail.

The bankruptcy of a firm influences to many firms through creditor-debtor network. Such avalanche propagates through the creditor-debtor network. The group dynamics of the firms induces the self-organized criticality in the bankruptcy.

Acknowledgments

The present research has been conducted by the Research Grant of Kwangwoon University in 2006.

References

- [1] D. Sornette, ”Critical Phenomena in Natural Science”, Springer, Heidelberg, 2003.

- [2] G. K. Zipf, ”Human Behavior and the Principle of Least Effort”, Addison-Wesley, Reading, 1949.

- [3] B. Gutenberg and R. F. Richter, Bulletin of the Seismological Society of America 34 (1944) 185.

- [4] T. Gehrels, ”Hazards due to Comets and Asteroids”, University of Arizona, Tucson, 1994.

- [5] E. T. Lu and R. J. Hamilton, Astrophysical Journal 390 (1991) 89.

- [6] D. C. Roberts and D. L. Turcotte, Fractals 6 (1998) 351.

- [7] R. A. K. Cox, J. M. Felton and K. C. Chung, Journal of Cultural Economics 19 (1995) 333.

- [8] J. W. Willis and G. U. Yule, Nature 109 (1922) 177.

- [9] Y. Fujiwara, Physica A 337 (2004) 219.

- [10] K. Okuyama, M. Takayasu, and H. Takayasu, Physica A 269 (1999) 125.

- [11] H. Aoyama, W. Souma, Y. Nagahara, M. P. Okazaki, H. Takayasu, and M. Takayasu, Fractal 8 (2000) 293.

- [12] A. Ishikawa, Physica A 349 (2005) 597.

- [13] D. O. Pushkin and H. Aref, Physica A 336 (2004) 571.

- [14] K. E. Lee and J. W. Lee, J. Korean Phys. Soc. 44 (2004) 668.

- [15] J. W. Lee, K. E. Lee, and P. A. Rikvold, J. Korean Phys. Soc. 48 S123(2006).

- [16] J. W. Lee, K. E. Lee, and P. A. Rikvold, Physica A 364 (2006) 355.

- [17] http,//www.rating.co.kr.

- [18] T. Kaizoji and M. Nuki, Fractals 12 (2004) 49.

- [19] P. Bak, ”How Nature Works, the science of self-organized criticality”, Springer, New York, 1996.

- [20] A. Aleksiejuk, J. A. Holyst, and G. Kossinets, cond-mat/0111586.