Fluctuations in time intervals of financial data from the view point of the Gini index

Abstract

We propose an approach to explain fluctuations in time intervals of financial markets data from the view point of the Gini index. We show the explicit form of the Gini index for a Weibull distribution which is a good candidate to describe the first passage time of foreign exchange rate. The analytical expression of the Gini index gives a very close value with that of empirical data analysis.

keywords:

Stochastic process; Gini index; time interval distribution; Weibull distribution; The Sony bank USD/JPY rate;PACS:

89.65.Gh1 Introduction

Almost years, financial data have attracted a lot of attentions of physicists as informative materials to investigate the macroscopic behavior of the markets from the microscopic statistical properties [1, 2, 3]. Some of these studies are restricted to the stochastic variables of the price changes (returns) and most of them is specified by a key word, that is to say, fat tails of the distributions [1]. However, the distribution of time intervals also might have important information about the markets and it is worth while for us to investigate these properties extensively [4, 5, 6, 7, 8].

In our previous studies [9, 10, 11], we showed that a Weibull distribution is a good candidate to describe the time intervals of the first passage process of foreign exchange rate. However, from the shape of the Weibull distribution, intuitively, it is not easy to understand fluctuations in time intervals. To overcome this point, in this paper, we introduce a Gini index, which is often used in economics to measure an inequality of income distribution. We here introduce the Gini index as a measure of an inequality of the time interval lengths. We first derive the Lorentz curve and the explicit form of the corresponding Gini index for a Weibull distribution analytically. We show the analytical expression of the Gini index is in a good agreement with empirical data analysis. Then, our analysis makes it possible to explain fluctuations in time intervals from the view point of the Gini index.

The paper is organized as follows. In the next section, we introduce a Gini index and derive the analytical expression of the Gini index for the Weibull distribution. We also evaluate the Gini index for empirical data and find a good agreement with empirical data analysis. The last section is conclusion and discussions.

2 Gini index for a Weibull distribution

In our previous studies [9, 10, 11], we showed that the distribution of the time interval between price changes of the Sony bank USD/JPY rate is approximated by a Weibull distribution. The Sony bank rate is that the Sony bank [12] offers to their individual customers on their online foreign exchange trading service via the internet. The Sony bank rate is a kind of first passage processes [13, 14] with above and below 0.1yen for the market rate, and once the market rate exceeds a threshold, the process stops and restarts at the updated Sony bank rate. Thus, the mean first passage time of the Sony bank rate is 20 minutes [9], which is longer than the mean time intervals of the market rate ( 7 seconds).

In this section, we investigate the Lorentz curve and the corresponding Gini index for a Weibull distribution. The Weibull distribution is described by

| (1) |

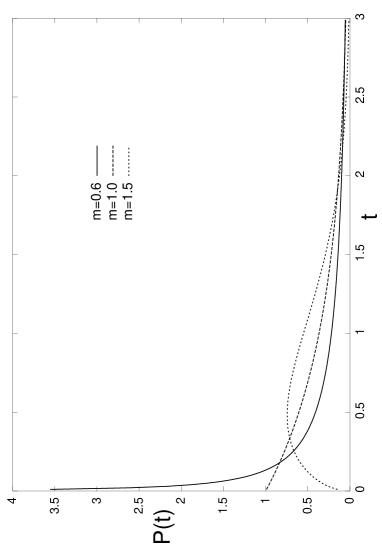

where and are the scale parameter, the shape parameter, respectively. When , a Weibull distribution is identical to an exponential distribution.

In FIG. 1, we plot the Weibull distribution for several values of with .

The Gini index is a measure of an inequality in a distribution. It is often used in economics to measure an inequality of income or wealth in each country or community. However, we here introduce a Gini index as a measure of an inequality in the length of time interval between data. Namely, we try to recognize the meaning of parameter through the Gini index. The Gini index takes between when all intervals are equal lengths (perfect equality) and when all intervals but one are zero lengths (perfect inequality).

2.1 Analytical expression of the Gini index

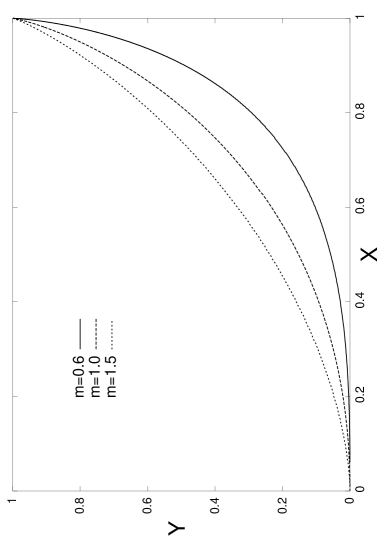

The Gini index is derived analytically if the corresponding “wealth distribution” is given. In this subsection, we show explicit form of the Gini index for a Weibull distribution as the “wealth distribution”. The Gini index is derived from the Lorentz curve. The Lorentz curve for a Weibull distribution is described by the following relation between and Thus, we have the Lorentz curve for a Weibull distribution as follows.

| (2) |

where is the incomplete Gamma function given by . In FIG. 2 (upper panel), we plot the Lorentz curve for several values of .

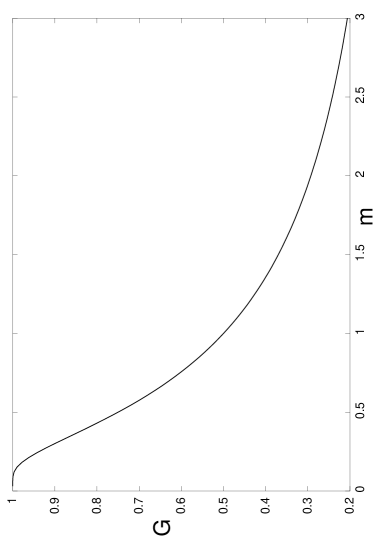

We next calculate the Gini index that is given as twice an area between the perfect equality line and the Lorentz curve. Carrying out some simple algebra, we have the Gini index as follows.

| (3) |

It should be noticed that the Gini index for a Weibull distribution is independent of the scale parameter . In FIG. 2 (lower panel), we plot the Gini index as a function of . We find that the Gini index monotonically decreases as increases. This means that for small , long intervals are merely generated from the Weibull distribution, whereas, short intervals are generated with high probability. As a result, the inequality of the interval length becomes quite large and the Gini index has a value close to . For large , on the other hand, similar interval lengths are generated from the Weibull distribution. As a result, the inequality is small and the Gini index is close to zero. Therefore, now the shape of the Weibull distribution was explained from the view point of the inequality of interval length, namely, the Gini index. As a special case, substituting into (3) we can check the Gini index is for exponential distribution, which is caused by the Poisson arrival process of price changes.

Since the empirical value of is about for our data set, which is around 31,000 data from September 2002 to May 2004, the analytical expression of the Gini index gives , which means more variations than the Poisson arrival process of price changes. Therefore, the Sony bank rate has mainly short intervals and few long intervals.

2.2 Gini index for empirical data

For comparison, we next derive the Gini index for empirical data, that is, the Gini index for discrete probabilistic variables [15]. Given a sample of intervals with the length in non-decreasing order . Discrete probabilistic variables and , which are ingredients of the Lorenz curve, are given by and for . A parameter denotes the mean length and and are set to zero. Thus, the Gini index for the discrete empirical data can be obtained as follows.

| (4) |

From (4) the empirical result of the Gini index for the Sony bank rate is , which is very close to the Gini index for the estimated Weibull distribution from (3). We find that the Weibull distribution is a plausible candidate for the time interval distribution of the Sony bank rate in terms of the Gini index. The detail calculations of the Gini index will be reported in our forthcoming paper [16].

3 Conclusion and dicussions

In this paper, we proposed an approach to explain fluctuations in time intervals of financial markets data from the view point of the Gini index. We showed the explicit form of the Gini index for a Weibull distribution which is a good candidate to describe the first passage time of foreign exchange rate. The analytical expression gave the very close value to the empirical data analysis. More precisely, we previously found that the tails of the time interval distribution changes its shape from Weibull-law to power-law [10]. However, even if without the correction of the power-law tail, the Gini index for a Weibull distribution is in a good agreement with the empirical result. It is reasonably expected that the tails of the distribution does not have a significant effect on the Gini index. Finally, our approach can be applicable to other stochastic processes to explain fluctuations in intervals.

Acknowledgement

One of the authors (N.S.) would like to appreciate Shigeru Ishi, President of the Sony bank, for kindly providing the Sony bank data and useful discussions.

References

- [1] R.N. Mantegna and H.E. Stanley, An Introduction to Econophysics: Correlations and Complexity in Finance, Cambridge University Press (2000).

- [2] J.-P. Bouchaud and M. Potters, Theory of Financial Risk and Derivative Pricing, Cambridge University Press (2000).

- [3] J. Voit, The Statistical Mechanics of Financial Markets, Springer (2001).

- [4] R. F. Engle and J. R. Russel, Econometrica 66 (1998), 1127.

- [5] M. Raberto, E. Scalas and F. Mainardi, Physica A 314, 749 (2002).

- [6] E. Scalas, R. Gorenflo, H. Luckock, F. Mainardi, M. Mantelli and M. Raberto, Quantitative Finance 4, 695 (2004).

- [7] E. Scalas, Physica A. 362 (2006), 225.

- [8] T. Kaizoji and M. Kaizoji, Physica A. 336 (2004), 563.

- [9] N. Sazuka, Eur. Phys. J. B. 50 (2006), 129.

- [10] N. Sazuka, http://arxiv.org/abs/physics/0606005 to appear in PhysicaA.

- [11] J. Inoue and N. Sazuka, http://arxiv.org/abs/physics/0606040.

- [12] http://moneykit.net

- [13] S. Redner, A Guide to First-Passage Processes, Cambridge University Press (2001).

- [14] N.G. van Kappen, Stochastic Processes in Physics and Chemistry, North Holland, Amsterdam (1992).

- [15] Kuan Xu, http://economics.dal.ca/RePEc/dal/wparch/howgini.pdf.

- [16] N. Sazuka and J. Inoue, in preparation.