Statistical equilibrium in simple exchange games I

Abstract

Simple stochastic exchange games are based on random allocation of finite resources. These games are Markov chains that can be studied either analytically or by Monte Carlo simulations. In particular, the equilibrium distribution can be derived either by direct diagonalization of the transition matrix, or using the detailed balance equation, or by Monte Carlo estimates. In this paper, these methods are introduced and applied to the Bennati-Dragulescu-Yakovenko (BDY) game. The exact analysis shows that the statistical-mechanical analogies used in the previous literature have to be revised.

pacs:

89.65.GhEconomics; econophysics, financial markets, business and management and 02.50.CwProbability theory1 Introduction

Agent-based models used for simulating the allocation of finite resources in economics include agents that can interact. These interactions can be direct and can include both two-body and many-body terms, but they can also be indirect, through some coupling and feedback mechanism with an external field .

Each agent is characterized by a certain quantity , which represents either size, or wealth or another relevant quantity. The interactions determine a variation of as a function of time. In the models, the evolution of the system can be described both in continuous time and in discrete time. In this framework, it is worth mentioning the so-called Interacting Particle Systems paradigm that includes, as special cases, percolation, the Ising model, the voter model, and the contact model liggett85 .

In general, these models are Markov chains or continuous-time Markov processes. Therefore, there is a full set of mathematical tools to analyze them and compute the equilibrium distribution. In this paper, however, the focus is on conservative models, where the total number of agents, , and the total size or wealth, , are conserved by the dynamics.

John Angle has introduced the so-called One Parameter Inequality Process (OPIP) that can be defined as follows. Let us suppose that there are players in a room, each of them with an initial amount of money, . Two individuals are randomly selected to play against each other. They flip a coin and the winner gets a fixed fraction, , of the loser’s money. Then the game is iterated. If and are the selected players at step , their amount of money at step is given by:

and

where is a Bernoullian random variable assuming the value with probability or the value with probability . Angle has studied the equilibrium distribution for the OPIP by means of Monte Carlo simulations and analytical approximations angle86 ; angle96 ; angle02 .

The Bennati-Dragulescu-Yakovenko (BDY) model described in bennati88 ; bennati93 and rediscovered in dragulescu00 is very similar to the OPIP, but there is an important difference. After the coin toss, the winner receives a fixed amount of money, . Indebtedness is impossible: Players reaching cannot lose money any more. If they are selected to play and they lose, they stay with no money, if they win, they get the fixed amount of money from the loser. On the contrary, in the OPIP, very poor agents always lose only a fraction of their money, and they never reach the situation . In the OPIP, the variables are intrinsically continuous, whereas in the BDY model they can be considered discrete.

To summarize, the BDY game can be described as follows. Let us consider a system of individuals (agents) who share coins, . At each discrete time step two agents are chosen, and they toss a coin. At the end of the bet, the winner has one more coin and the loser has one coin less ( is assumed, without loss of generality). Agents’ choice is random (i.e. each distinct couple has the same probability to be extracted) and each bet is fair. If the loser has no coins, then the move is forbidden and a new couple of players is extracted. An equivalent formulation of the game, avoiding forbidden moves, is the following. An agent is chosen randomly among all those having at least one coin, and this agent is declared to be the loser; the winner is chosen randomly among all agents.

This paper will be devoted to an analysis of the BDY game. In section II, the basic random variables for the description of the game will be introduced. Section III will be devoted to the methods of solution and it is the core section of this paper. Finally, in section IV a critical discussion of the results will be presented. The reader will find further mathematical details in an appendix.

2 Random Variables

In the BDY game, as well as in similar exchange games, one has to allocate coins among agents. In the following, a random variable will be denoted by a capital letter: , whereas will refer to a specific value or realization.

The most complete description of the game states is in terms of coin configurations: . Each random variable is associated to the coin, and its range is the set of agents; for instance, denotes that the coin belongs to the agent. The total number of configurations for coins distributed among agents is . This can be called the coin description.

The second (and most important in the present case) description is in terms of coin occupation numbers, where the random variable denotes the number of coins (the wealth) of the agent. If the set of configurations, , is known, then , that is the value of conditioned on is the number, , of all equal to . Then, one can define as the set of occupation numbers; they satisfy the constraint . This can be called the agent description. It tells us the number of coins (wealth) of each agent. The total number of distinct agent descriptions for agents sharing coins is

The less complete description is in terms of coin occupancy numbers or partitions: , where , that is the number (not the names or labels) of agents with coins. This is the frequency distribution of agents, commonly referred to as wealth distribution; it is an event, not to be confused with a probability distribution. The constraints for are . For the BDY game, the number of agents without money, , is very important. Its complement is , the number of agents with at least one coin.

3 Methods of solution

3.1 An irreducible Markov chain

The dynamic mechanism of the BDY game is the hopping of a coin from one agent (the loser) to another (the winner). The natural description is in terms of agents, Let us suppose that at given time, , the agents are described by the state . At the next step, the possible values of are: corresponding to the a loss of the agent and a win of the one. The transition probability between these states is:

| (1) |

where the first term, , describes the random choice of the loser among the agents with at least one coin (, and the second term, , is the probability that the agent is the winner. As also an agent with zero coins can be a winner, there are no absorbing states. Note that in eq. (1) the assumption is made that coins necessarily change agent; if one admits that coins can come back to the loser, the second term simplifies to , the dynamics slightly changes, but the equilibrium distribution is not affected. Considering both the intuitive meaning of the game and the formal transition probability (1), the sequence is a discrete-space and discrete-time Markov process, i.e. a finite Markov chain; every state can be reached from any other state, the set of states is irreducible, and no periodicity is present. Hence, there exists an invariant probability distribution, and this distribution coincides with the equilibrium one. This means that independently from the initial state Moreover, holds for all the possible occupation numbers.

3.2 Direct enumeration and Monte Carlo sampling

The direct enumeration method can be used to study the game when and are not too large. To illustrate the method, let us consider the case . The total number of agent descriptions is : ; ; ; ; ; ; ; ; ; . The transition matrix between these states can be directly computed by using the rules of the game. For instance, the state can only go into the two states and with equal probability . The state can go into the four states , , , and and each final state can be reached with probability . These considerations lead to the definition of the following transition matrix:

The vector, , giving the equilibrium probability distribution can be computed diagonalizing , as its transpose, , satisfies: . In particular, in this case, one gets: and A Monte Carlo simulation of the game can help in the case of larger systems. The simulation can sample both the transition matrix and the equilibrium distribution. Both methods, direct enumeration and Monte Carlo sampling, are limited by the size of the state space. However, for the BDY game a general exact solution can be derived.

3.3 Exact solution

As the size of the state space is a rapidly growing function of and , the invariant distribution can be investigated via the detailed balance equation costantini .

Let us consider two consecutive states: , and with the conditions and . The direct flux is given by

the inverse flux is

The two fluxes are equal if

that is if , where is a constant.

Hence the probability function:

| (2) |

is invariant, and it coincides with the equilibrium one.

Two remarks are useful. First of all, in eq. (2) does not depend on the agent labels but is a function of the partition to which the description belongs. This implies that all the sequences and are equiprobable, if and belong to the same , that is if is any permutation of Therefore, the random variables are exchangeable costantini , and they are also equidistributed, once equilibrium has been reached and eq. (2) holds. All belonging to the same being equiprobable, one gets for the partition probability distribution:

| (3) |

Secondly, only those agent descriptions sharing the same number of agents without coins have the same probability. Indeed, the probability of a given occupation vector depends on and, thus, it is not uniform. The reader is invited to verify this property in the particular case described in the previous subsection.

The hypothesis of equal a priori probabilities for all the agent descriptions seems at the basis of Bennati’s and Dragulescu and Yakovenko’s analysis of the game, whose conclusions are not fully correct if one considers eq. (2). This hypothesis on occupation numbers can already be found in a paper by Boltzmann published in 1868 and leading to the so-called Bose-Einstein statistics boltzmann68 ; bach90 ; costantini97 . Indeed, if were uniform in eq. (3), one would get the most probable value of by maximizing the multinomial prefactor subject to the constraints for . In the limit of large systems, the result is . At the end of the next subsection, the limit will be considered for the BDY game, where the exponential wealth distribution is recovered as an approximation to the exact solution.

The normalization constant is computed in the Appendix, based on the method described in a paper by Hill hill77 . It turns out that:

| (4) |

3.4 The average wealth distribution

The number of the agent descriptions, , and of the partitions, , is very large for and large. Moreover, both and are multidimensional distributions. In order to search for a quantity that can compared with experimental observations, one can notice that agents are exchangeable and any probability distribution is symmetric with respect to the exchange of their labels. Empirical data are given in terms of the actual wealth distribution . At any step, is just the actual wealth distribution. If equilibrium is reached, represents the multivariate sampling distribution, and the vector denotes the set of first moments of . It is useful to define the marginal average

| (5) |

continuously fluctuates around . As a consequence of the ergodic thorem for Markov chains, one has that and this convergence is in probability. Hence, if the empirical or simulated sequence, , is available, the comparison is possible between the time average and the ensemble average predicted from the knowledge of . , the average wealth distribution, will coincide with the most probable value of (say ) for large systems. As already noticed, if were uniform, then one could find the most probable value of , , by using Lagrange multipliers, and the functional form of would be exponential in the Stirling approximation.

In the BDY game, this is not the case. However, as a consequence of eq. (2), is uniform for all vectors with the same . The exact value of can be derived analyzing all the agent descriptions with the same . Conditioned on , one gets:

| (6) |

and the equilibrium probability of is

| (7) |

Finally, using eqs. (4), (6) and (7), one gets

| (8) |

The proof of the above results can be found in the Appendix. Notice that the thermodynamic limit ( of eq. (6) is . Then, the average fraction of agents with at least one coin follows a geometric distribution that becomes exponential in the continuous limit. In this limit, the average wealth distribution, , (or the most probable wealth distribution ) is a mixture of exponential distributions with mixing measure given by eq. (7).

Considering eq. (7), one observes that

with for , and for Therefore, in the case of minimum density, , one has that is bell-shaped with flat maximum at and as , . In the large density limit , the curve is left-skewed, the maximum is very close to , as . Furthermore, if , i.e. , the maximum value is just . In the case of large density, the mixing probability distribution is concentrated on a small number of values of and, thus, if the behaviour is not very different from the single geometric distribution that becomes the exponential . This remark explains why large scale simulations of the BDY game with appear compatible with an exponential wealth distribution.

3.5 Comparison with Monte Carlo simulations

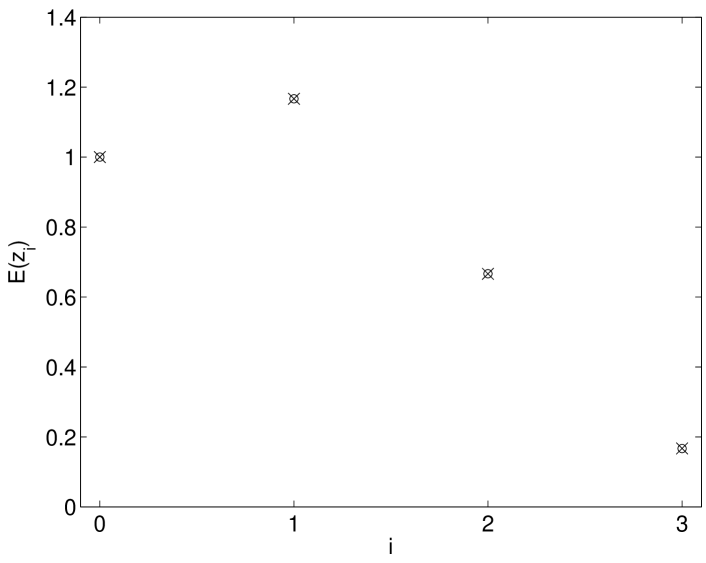

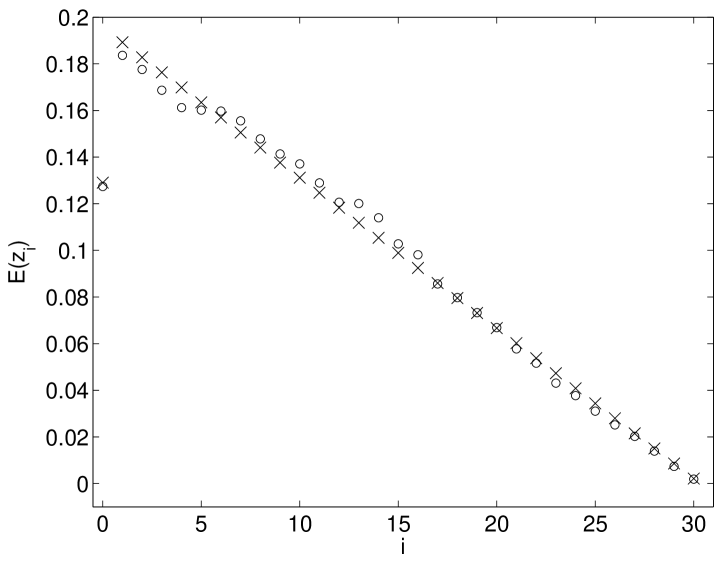

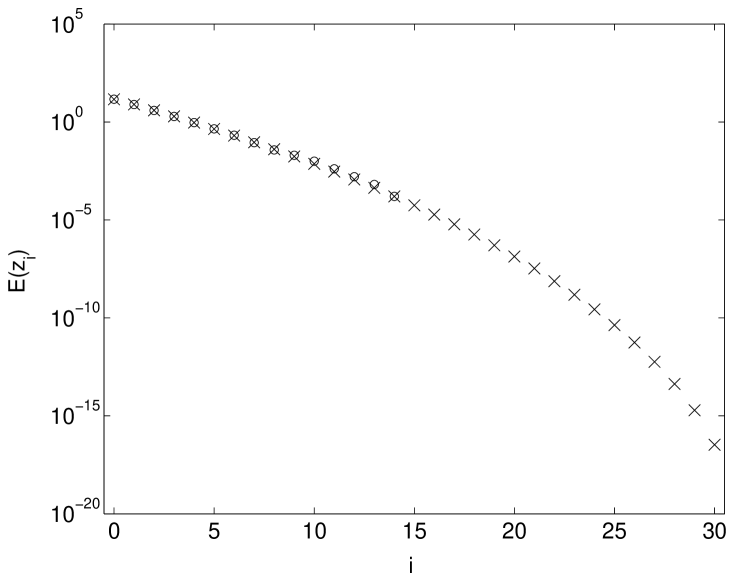

In this section, the results of Monte Carlo simulations are compared with the exact equilibrium wealth distribution. The simulations have been performed on a standard desktop computer equipped with a 1GHz processor. In the initial state all the agents are given the same amount of coins. After an equilibration run of 1000 MC steps, the values of have been sampled and averaged over MC steps. In the cases reported in Figs. 1-3, the execution time is a few seconds.

It is interesting to remark that for small values of the distribution is strongly dependent on : it is uniform for linear for , parabolic for for ,. Except for the very peculiar case , the distribution is decreasing for , but in some cases . The latter feature deserves further investigations. Fig.1 shows the case and , whereas Fig.2 has again 3 agents, but 30 coins. Fig.3 is the logarithmic graph for and to illustrate the approach to an exponential-type distribution for large values of the number of agents, .

4 Discussion and conclusions

Recently, parsimonious exchange games like the one studied in this paper have been challenged by a group of leading non-orthodox economists lux05 ; gallegati06 . These games have been introduced in order to explain the allocation of wealth in the presence of finite resources. In lux05 ; gallegati06 , they are considered unrealistic because they do not take into account the free will of agents to participate in an exchange, and they include only strictly conserved resources, without production. Incidentally, in games such as the OPIP or the BDY models, inequality is obtained by pure chance. Rich agents have no specific individual merit. Based on their beliefs, some scholars could also dislike this feature.

Replies to the objections in lux05 ; gallegati06 have already appeared in two papers by Angle angle06a and by McCauley mac06 . In particular, Angle presents various arguments in favour of parsimonious exchange games, including their ability to reproduce empirical facts angle06b .

The present authors would also like to stress that, also thanks to simple exchange models, a new concept of equilibrium could find its way into Economics: namely Statistical equilibrium. Many stochastic models in Economics are Markov chains or Markov processes (see refs. silver02 ; foellmer05 ; bottazzi04 for recent examples) and the concepts developed in this paper apply to those cases. These ideas will be the subject of future papers on the role of statistical equilibrium in Economics. The reader can consult ref. foley94 for an early discussion and refs. mac06 ; mac04 for a criticism on the relevance of thermodynamic equilibrium in Economics.

One of the main results of this paper is eq. (8), giving the so-called wealth distribution. As the agent descriptions are not equiprobable, previous statistical mechanical arguments have to be revised. In general, the wealth distribution is not exponential and it becomes exponential only in the appropriate limit of large density and large number of agents. It is interesting to study the rate of approach to equilibrium in the BDY model, but this will the subject of a future paper of this series. The next paper of the series, will be devoted to a set of simple exchange models for the redistribution of wealth that can be regarded as toy taxation mechanisms.

APPENDIX

The normalization constant

The total number of possible agent descriptions, , is

and they can be classified in terms of the number of agents with at least one coin: , . Therefore, the number of agent descriptions with fixed agents with at least one coin is given by all occupation numbers which allocate coins to agents, that is

while are the different ways to choose the agents among the available. Then

is the number of agent descriptions with agents with at least one coin. Indeed, one has:

and this formula expresses the decomposition of all possible states in terms of their “support” . The decomposition can be re-written as:

Turning to eq.(2), the sum on all states can be divided into a sum over and a sum over , that is:

which gives the desired normalization constant.

Derivation of equation (6)

The average number of agents whose occupation number is equal to is

the last equality holding as the are equidistributed. , is the marginal equilibrium probability of the wealth of the agent, and it is the same for all ’s. It is necessary to study the marginal distribution of an agent associated to the agent description probability (2) and to the partition probability (3), both holding at equilibrium. In order to derive formula (6), one needs

the marginal wealth distribution of an agent conditioned to . One knows from (2) that all agent descriptions with the same are equiprobable, and their number is

Then is equal to the number of such that agents share coins divided by The calculation can be divided into three parts. First, let us consider ; one has:

then, let us consider with , and ; as there are agents left with at least one coin, one has:

| (9) |

finally, for , one gets: for , as in this case all coins are concentrated on a single agent. Eventually, by determining , one obtains eq. (6) as required.

ACKNOWLEDGEMENTS

E.S. acknowledges useful discussion with Giulio Bottazzi, Mauro Gallegati, Eric Guerci, David Mas, Marco Raberto, and Alessandra Tedeschi during a Thematic Institute sponsored by the Exystence EU network held in Ancona in 2005. He is grateful to J. Angle and J. McCauley for pointing him to refs. angle06a and mac06 , respectively. This work has been partially supported by MIUR project ”Dinamica di altissima frequenza nei mercati finanziari”.

References

- (1) T.M. Liggett, Interacting Particle Systems, (Springer, Berlin, 1985).

- (2) J. Angle, The Surplus Theory of Social Stratification and the Size Distribution of Personal Wealth, Social Forces 65, 293–326, (1986).

- (3) J. Angle, How the Gamma Law of Income Distribution Appears Invariant under Aggregation, Journal of Mathematical Sociology 21, 325–358, (1996).

- (4) J. Angle, The statistical signature of pervasive competition on wages and salaries, Journal of Mathematical Sociology 26, 217–270, (2002).

- (5) E. Bennati, Un metodo di simulazione statistica per l’analisi della distribuzione del reddito, Rivista Internazionale di Scienze Economiche e Commerciali 35, 735–756, (1988).

- (6) E. Bennati, Il metodo di Montecarlo nell’analisi economica, Rassegna di Lavori dell’ISCO, Anno X, n. 4, 31–79, (1993).

- (7) A. Dragulescu and V. M. Yakovenko, Statistical mechanics of money, Eur. Phys. J. B 17, 723–729 (2000).

- (8) D. Costantini and U. Garibaldi, The Ehrenfest Fleas: from Model to Theory, Synthese 139, 107-142, (2004).

- (9) L. Boltzmann, Studien über das Gleichgewicht der lebendingen Kraft zwischen bewegten materielle Punkten (1868) in Wissenschaftliche Abhandlungen, vol. I, F. Hasenhörl (ed.), Leipzig, Barth, pp. 49-96 (1909).

- (10) A. Bach, Boltzmann’s Probability Distribution of 1877, Archive for History of Exact Sciences 41, 1–40, (1990).

- (11) D. Costantini and U. Garibaldi, A Probabilistic Foundation of Elementary Particle Statistics. Part I Stud. Hist. Phil. Mod. Phys. 28, 483–506, (1997).

- (12) B.M.Hill, The Rank-Frequency Form of Zipf’s Law, Jour. Am. Stat. Ass. 69 (348), 1017-1026, (1977).

- (13) T. Lux, Emergent statistical wealth distributions in simple monetary exchange models: A critical review, in Econophysics of Wealth Distribution, A. Chatterjee, S. Yarlagadda, B.K. Chakrabarti eds., (Springer, Berlin, 2005).

- (14) M. Gallegati, S. Keen, T. Lux, P. Ormerod, Worrying Trends in Econophysics, working paper, 2006.

- (15) J. Angle, A Comment on Gallegati et al.’s “Worrying Trends in Econophysics”, working paper, 2006.

- (16) J. McCauley, Response to “Worrying Trends in Econophysics” working paper, 2006.

- (17) J. Angle, The Inequality Process as a wealth maximizing process Physica A, 367, 388–414 (2006).

- (18) J. Silver, E. Slud, and K. Takamoto, Statistical Equilibrium Wealth Distributions in an Exchange Economy with Stochastic Preferences Journal of Economic Theory 106, 417–435 (2002).

- (19) H. Föllmer, U. Horst, and A. Kirman, Equilibria in financial markets with heterogeneous agents: A probabilistic perspective, Journal of Mathematical Economics 41, 123–155 (2005).

- (20) G. Bottazzi, G. Dosi, G. Fagiolo, and A. Secchi, Sectoral and Geographical Specificities in the Spatial Structure of Economic Activities Scuola Superiore S.Anna, LEM Working Paper 2004/21, (2004).

- (21) D.K. Foley, A statistical equilibrium theory of markets, Journal of Economic Theory 62, 321–345 (1994).

- (22) J. McCauley, Dynamics of Markets: Econophysics and Finance, (Cambridge University Press, Cambridge UK, 2004).