The Asymptotic Dependence of Elliptic Random Variables ††thanks: Presented at FENS 2006

Krystyna Jaworska

Institute of Mathematics and Cryptology, Military University of Technology

ul. Kaliskiego 2, 00-908 Warszawa, Poland

Abstract

In this paper, we try to answer the question, whether for bivariate elliptic random variable

the marginal random variables and are asymptotically dependent.

We show, that for some special form of the characteristic generator of the answer is positive.

keywords:

dependence of extreme events, risk management,

\PACS

89.65.Gh

MSC 2000: 91B28, 91B30, 62H05

1 Motivation

In order to give an answer to the question, ”What is the origin of the interest of the asymptotic dependence

of elliptic random variables?” one has to go back several dozen years.

Already in the years 1950’s and 1960’s researchers discovered the non-normal behaviour of financial market

data. In the early 1990’s an understanding of the methodology underlying financial or insurance extremes

became very important. Traditional statistics mostly concerns the laws governing averages. But when we look

at the largest ( respectively the smallest) elements in a sample, the assumption of normality seems not to

be reasonable in the number of applications, particularly in finance and insurance. And heavy-tailed

distributions have a chance to be more appropriate.

Why? Let , be insurance claims due to flood disasters and wind storms .

Last year events taught us that very often the extreme values of are accompanied by extreme values of .

In mathematical language it means, that and are asymptotically dependent. Traditional models based

on multidimensional normal probability law give rise to quite opposite conclusion. Therefore in modelling

of extreme events more and more often the researchers use the wider class of distributions, which includes

the normal distribution as a special case.

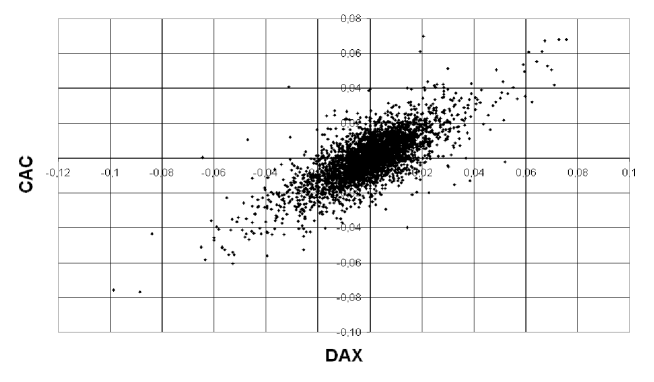

Let us now consider a simple example from finance market. On the figure below you see daily log-returns

of stock indices DAX and CAC ( horizontal axis -DAX, vertical axis -CAC). The data cover the period

from 1990 to 2004 (about 4000 data). The scatter plot assumes a shape of ”elliptic cloud”. And the level sets of

the probability density, of the random vector , are ellipses. This empirical observation suggests,

that the family of elliptic distributions should be taken under consideration.

Figure 1: Log-returns of DAX and CAC.

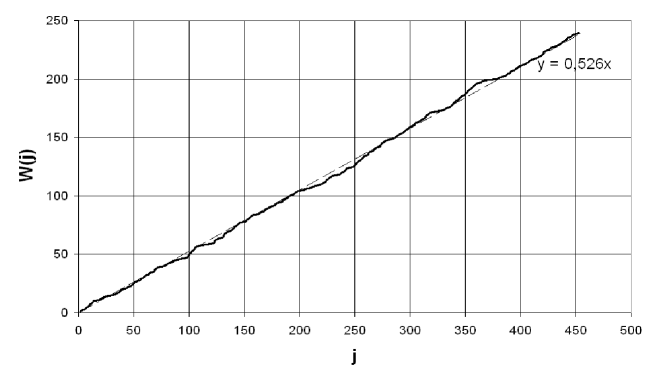

Furthermore we can ask how often we observe the situation, when the daily log-returns of the both indices take

the extreme values.

Let be the quantity of observations such that

,

where is the j-th order statistics of the random variable , .

Figure 2: Graph of .

The graph of the function shows us, that and are asymptotically dependent. So the joint

random variable couldn’t be normally distributed.

2 Preliminaries

To begin with, we recall the basic definitions.

Let be an univariate distribution function and its generalized inverse

Definition 2.1.

Let be a random vector with marginal distribution functions and .

The coefficient of upper tail dependence of is defined to be

provided, that the limit exists.

If , then we say that and are asymptotically independent.

Otherwise ( that is or doesn’t exists ) we say that, they are asymptotically dependent.

For a pair of random variables upper tail dependence is a measure of joint extremes. That is

they measure the probability that one component is at an extreme of size given that the other is at the same

extreme, relative to the marginal distributions.

Lemma 2.1.

If two continuously distributed random variables , are independent, then they are asymptotically

independent.

Proof.

Note that the bivariate normal distribution has the same property.

The tail behaviour can be also described in a ”symmetric way”.

Definition 2.2.

The bivariate random variable is said to be regularly varying with index , if for all

and for every angle

where

is a certain measure on the interval .

Definition 2.3.

If is a bivariate random variable and, for some

, some 2x2 nonnegative definite symmetric

matrix and some function , the characteristic function is of

the form

then we say that has an elliptical distribution with parameters

and , and we write .

The function is referred to as the characteristic generator of .

Remark 2.1.

The following widespread used distributions prove to be

elliptic:

1. the normal distribution

2. some -stable with characteristic generator of the form

3. T-Student distribution.

3 Result

Theorem 3.1.

Let

be a characteristic function of a bivariate elliptically distributed random variable .

1. is a positive definite symmetric matrix,

2. is such that:

, ,

,

,

then the marginal random variables and are asymptotically dependent .

4 Concluding remarks

1. For all , if is elliptic and - stable, then and are

asymptotically dependent.

2. The result is also valid for the characteristic generator of the form

, where

.

5 Proof of the Theorem

Lemma 5.1.

Let us have the same assumptions as in theorem 3.1.

Then the asymptotics of the probability density of bivariate random variable

formulates as follows

, .

Proof.

Let us denote

We calculate the asymptotics of the integral above, for .

and symmetric .

after the change of the variables .

Next we substitute and obtain

We change the variables a second time ,

and let us express in the form

.

Then

Now we compute the first term of asymptotics of the integral

We assumed that the function and its derivatives tend quickly to , as .

Therefore with the help of localization rule and Erdelyi Lemma cf.[4] we obtain

The expression above isn’t trivial, when is not a natural even number.

Hence the first term of the asymptotics of the integral is given by a formula:

Thus

Lemma 5.2.

Under the assumptions of theorem 3.1 the bivariate random variable is regularly varying with the index

.

Proof.

Lemma 5.2 implies the thesis of Theorem 3.1 cf.[5].

References

[1]

P. Billingsley,

Probability and Measure,

John Wiley & Sons, Inc. 1979.

[2]

J.-P. Bouchaud, M. Potters,

Theory of Financial Risks: from Statistical Physics to Risk Management,

Cambridge University Press 2000.

[3]Extremes and Integrated Risk Management, Ed. by Paul Embrechts, Risk Books, 2000.

[4]

M.W.Fiedoruk,

Metod pierewala, Izd. Nauka, 1977.

[5]

H.Hult, F.Lindskog,

Multivariate Extremes, Aggregation and Dependence in Elliptical Distributions,

Adv.Appl.Prob.34.587-608(2002).

[6]

J.L.Jensen,

Saddlepoint Approximations, Oxford University Press, 1995.

[7]

R.N.Mantegna, H.E.Stanley,

An Introduction to Econophysics. Correlations and Complexity in Finance,

Cambridge University Press 2000.